Embed Size (px)

Citation preview

CHAPTER 6

Western Energy Equipmentand Technology Trade With

the U.S.S.R.

CONTENTS

Page

EAST-WEST TRADE IN ENERGYTECHNOLOGY ANDEQUIPMENT . . . . . . . . . . . . . . . . . . . . 171

NUCLEAR . . . . . . . . . . . . . . . . . . . . .. ..174Western Exports. . .................174Foreign Availability of Nuclear

Equipment and Technology. . .......176Summary and Conclusions. . ..........177

COAL . . . . . . . . . . . . . . . . . . . . . .......177

PageForeign Availability of Coal

Technology and Equipment. . . . . . . . .180Summary and Conclusions. . . . . . . . . . . .180

ELECTRIC POWER, . . . . . . . . . . . . . . .181Western Exports. . .................181Foreign Availability of Electric Power

Equipment and Technology. . .......183Summary and Conclusions. . ..........183

OIL AND GAS. . . . . . . . . . . . . . . . . . . . . 184Western Exports. . .................177 Western Exports. . .................184

.

Page

Foreign Availability of Oil and GasIndustry Equipment andTechnology . . . . . . . . . . . . . . . . . . . . . . 191

Technology Transfer and “ForeignAvailability” . . . . . . . . .............200

Summary and Conclusions. . ..........204

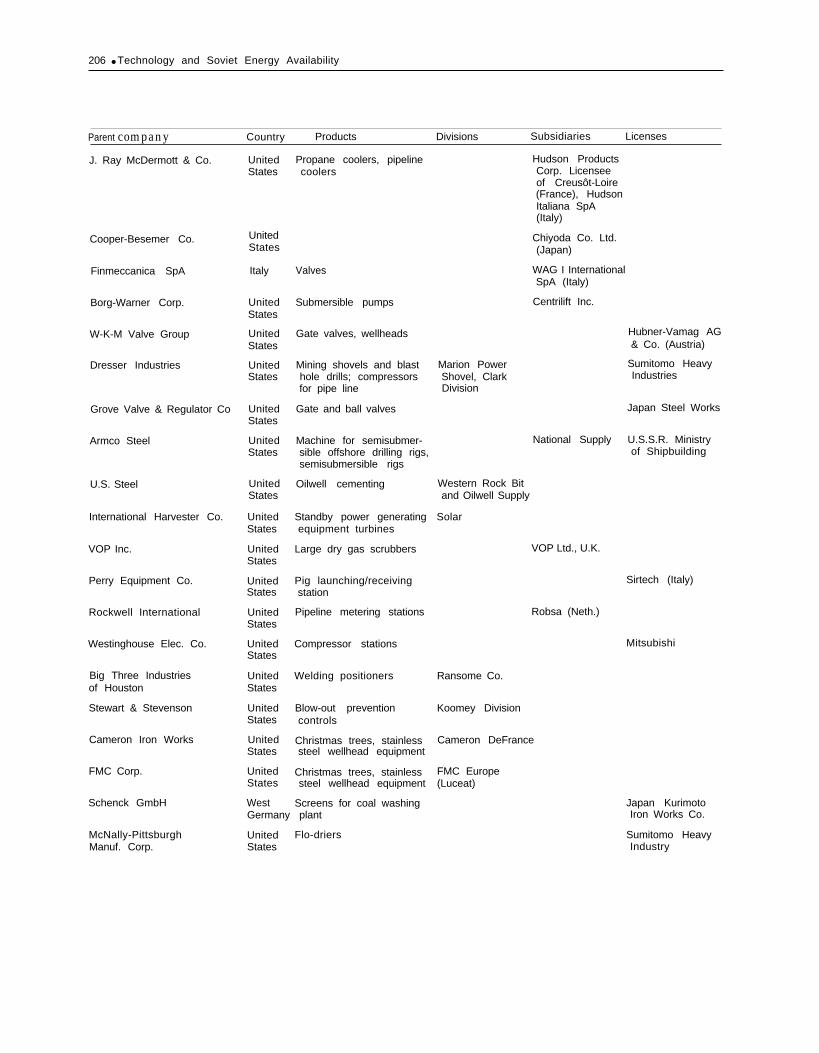

APPENDIX A. Energy CorporationAffiliations. . . . . . . . . . . . . . . . . . . . . ..205

APPENDIX B. Trade by Company. .. .209

APPENDIX C. Suppliers of EssentialEquipment. . . . . . . . . . . . . . . . . . . . . ..219

LIST OF TABLES

Table No. Page

40.

41.

42.

43.

44.

45.

46.

47.

48.

UN SITC Energy-RelatedEquipment Codes. . ..............170Industrial West Exports to theU. S. S. R., Selected Countries. .. ....172Soviet Energy-Related ImportsFrom Selected Western Countries. .. 172Energy-Related Exports to theU.S.S.R. by Selected Countries. .. ..174Soviet Imports From SelectedWestern Nations. ... , . ...........179U.S. Oil and Gas Equipment TradeWith U.S.S.R. Relative Percentageof Each Technology Area. . . . . . . . . .186Comparison of U.S. and FrenchSeismic Equipment. . . . . . . . .......192Manufacture of Siesmic Equipmentby Country. . . . . . . . . . . . . . . . . . . . . 193Non-U.S. Offshore EngineeringFirms , . . . . . . . . . . . . . . . . . . . . ., .. .199

B-1. Trade by Company–Oiland Gas. . . . . . . . . . . . . . . . . . . . . . .209

B-2. Trade by Company–Coal. . .......217C-1. Suppliers of Nuclear Grade

c-2

c-3

Pip& and Tubes Outsidethe United States. . .............219Suppliers of Welding EquipmentOutside the United States. . ......219Suppliers of Steam GeneratorsOutside the United States. . ......220

c-4.

c-5.

C-6.

c-7.

C-8.

c-9.

Page

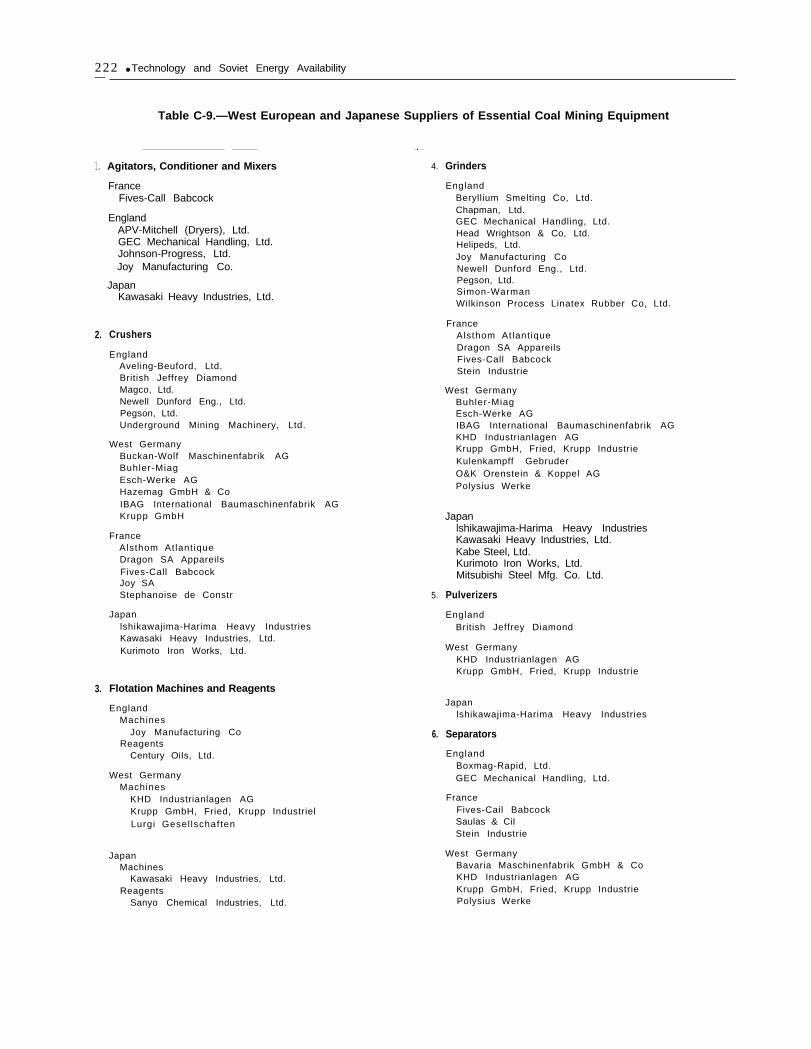

Suppliers of Pumps Outside theUnited States. . ................220Suppliers of Valves Outside theUnited States. . ................220Suppliers of ContainmentStructures Outside theUnited States. . ................221Suppliers of Control SystemsOutside the United States. . ......221Essential Equipment for CoalMining . . . . . . . . . . . . . . . . . . . . .. ..221West European and JapaneseSuppliers of Essential CoalMining Equipment. . ............222

C-10. West European and JapaneseProducers of ElectricTransmission Equipment. . ......225

LIST OF FIGURES

Figure No. Page

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

Soviet Imports of Western Energy “Equipment and Technology, by -

Industry . . . . . . . . . . . . . . . . . . . . . . . 173U.S. Energy-Related Exports tothe U. S. S. R., by Industry. ... , .. ...174Western Energy Trade WithU.S.S.R.–Welding Equipment. .. ..175Coal-Related Equipment Exportsto the U. S: S. R.. . ................178Electric Power Equipment Exportsto the U. S. S. R.. . . . . . . . . . . . . . .. ..182U.S.S.R. Imports of Oil and GasEquipment ., . . . . . . . . . . . . . . . . . . . 185U.S. Oil and Gas Equipment TradeWith U.S.S.R. by TechnologyArea. . . . . . . . . . . . . . . . . . . . . . . . . . .187Western Energy Trade WithU.S.S.R. Automated DataProcessing Equipment. . ..........188Western Energy Trade WithU.S.S.R. Pumps for Liquids. . ......189Relative Importance to SovietEnergy Industries of Computer-Related Technologies in Which theU.S.S.R. Lags the United States. .. .203

.

CHAPTER 6

Western Energy Equipment andTechnology Trade With the U.S.S.R.

—.—-

The previous four chapters have discussedthe impact of Western energy technologyand equipment on Soviet energy productionin qualitative terms. This chapter examinesthe nature and extent of Soviet energy-related purchases from the West. Usingavailable trade data, it seeks t. ascertain the

magnitude and sources of this trade, toanalyze identifiable patterns and trends, andto illuminate the role of the United States inproviding material assistance to Sovietenergy industries. In the latter context, thechapter addresses the issue of “foreign avail-ability," i.e., the extent to which the UnitedStates is the sole or preferred supplier ofenergy equipment and technologies that theSoviet Union has purchased in the last 5years or is likely to seek during the presentdecade.

The methodology employed in this chap-ter is as follows: OTA used the surveys ofthe Soviet oil, gas, coal, nuclear, and elec-tricity transmission industries which appearin chapters 2 through 5, together with in-formation on common Western practice, tocompile a broad list of important energytechnologies, items of equipment, and serv-ices.1 This list was refined by using tradestatistics to identify those areas in which theU.S.S.R. has made purchases from the Westin the past 5 years. Major items were thensubjected to a foreign availability analysis inwhich OTA attempted to ascertain whichWest European and Japanese firms manu-facture similar equipment or possess exper-tise comparable to those companies that ac-tually supplied the U.S.S.R.—

1No attempt has been made here to distinguish between“technology” and “products” or “equipment”. For a discus-sion of this subject, see OTA, Technology and East-WestTrade (Washington, D. C.: U.S. Government Printing Office,1979), ch. VI.

Foreign availability is a highly subjectiveconcept. As chapter 13 discusses in detail,there is no universal agreement on theparameters that define the degree of equiva-lency necessary to constitute foreign avail-ability, on how the parameters should beweighted, or indeed on how equivalencyitself can and should be measured. Given thelimitations of this study, no attempt wasmade to conduct an exhaustive worldwidesearch for all alternative sources for eachitem; in most cases identification of two orthree suppliers was deemed sufficient.

Nor did OTA construct a rigorous frame-work for defining and measuring foreignavailability. Information on energy tech-nologies and equipment was collected fromindustry sources in a number of countriesand evaluated by independent technicians.These evaluations were supplemented by in-terviews with representatives from energy-related companies in the United States andwith members of the intelligence commu-nity. The criteria of comparability werequality, price, and technical capabilities (i.e.,speed, capacity, precision). OTA did not in-vestigate the potential manufacturing ca-pacity of alternative suppliers or evaluatethe willingness of firms to sell to theU.S.S.R. The latter are both issues thatwould have to be taken into account in an ex-haustive foreign availability analysis.

Although the results of the analysis car-ried out here are limited, they can be used toindicate those areas in which the UnitedStates enjoys a significant technologicaledge over other Western nations in an ener-gy-related process, system, or piece of equip-ment important to the oil, gas, coal, nuclear,or electric power industries of the U.S.S.R.

169

170 • Technology and Soviet Energy Availability

A variety of statistical systems were ex-amined in the course of this study, no one ofwhich provided an ideal data base. OTA hasdealt elsewhere with the problems associatedwith measuring and reporting trade,2 but abrief review of the data sources employedhere can provide a sense of the limitations ofthe analysis that follows and of the strengthof the generalizations that may legitimatelybe drawn from it.

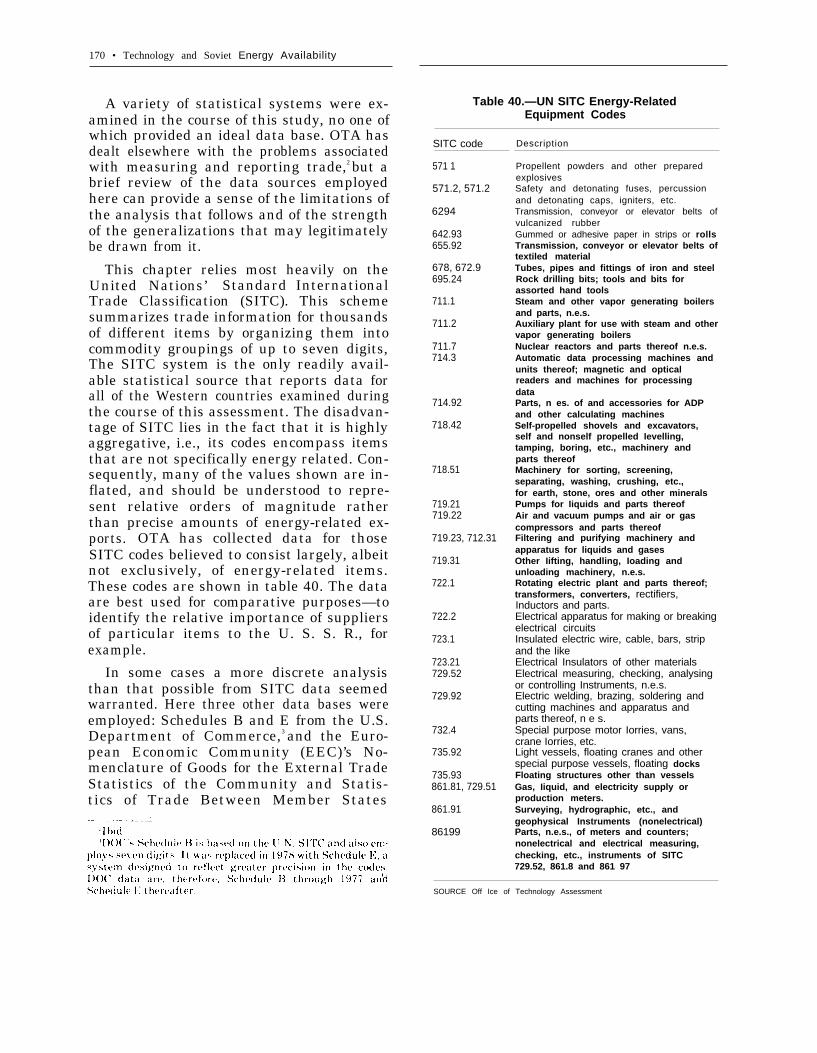

This chapter relies most heavily on theUnited Nations’ Standard InternationalTrade Classification (SITC). This schemesummarizes trade information for thousandsof different items by organizing them intocommodity groupings of up to seven digits,The SITC system is the only readily avail-able statistical source that reports data forall of the Western countries examined duringthe course of this assessment. The disadvan-tage of SITC lies in the fact that it is highlyaggregative, i.e., its codes encompass itemsthat are not specifically energy related. Con-sequently, many of the values shown are in-flated, and should be understood to repre-sent relative orders of magnitude ratherthan precise amounts of energy-related ex-ports. OTA has collected data for thoseSITC codes believed to consist largely, albeitnot exclusively, of energy-related items.These codes are shown in table 40. The dataare best used for comparative purposes—toidentify the relative importance of suppliersof particular items to the U. S. S. R., forexample.

In some cases a more discrete analysisthan that possible from SITC data seemedwarranted. Here three other data bases wereemployed: Schedules B and E from the U.S.Department of Commerce,3 and the Euro-pean Economic Community (EEC)’s No-menclature of Goods for the External TradeStatistics of the Community and Statis-tics of Trade Between Member States

Table 40.—UN SITC Energy-RelatedEquipment Codes

SITC code

571 1

571.2, 571.2

6294

642.93655.92

678, 672.9695.24

711.1

711.2

711.7714.3

714.92

718.42

718.51

719.21719.22

719.23, 712.31

719.31

722.1

722.2

723.1

723.21729.52

729.92

732.4

735.92

735.93861.81, 729.51

861.91

86199

Description

Propellent powders and other preparedexplosivesSafety and detonating fuses, percussionand detonating caps, igniters, etc.Transmission, conveyor or elevator belts ofvulcanized rubberGummed or adhesive paper in strips or rollsTransmission, conveyor or elevator belts oftextiled materialTubes, pipes and fittings of iron and steelRock drilling bits; tools and bits forassorted hand toolsSteam and other vapor generating boilersand parts, n.e.s.Auxiliary plant for use with steam and othervapor generating boilersNuclear reactors and parts thereof n.e.s.Automatic data processing machines andunits thereof; magnetic and opticalreaders and machines for processingdataParts, n es. of and accessories for ADPand other calculating machinesSelf-propelled shovels and excavators,self and nonself propelled Ievelling,tamping, boring, etc., machinery andparts thereofMachinery for sorting, screening,separating, washing, crushing, etc.,for earth, stone, ores and other mineralsPumps for Iiquids and parts thereofAir and vacuum pumps and air or gascompressors and parts thereofFiltering and purifying machinery andapparatus for liquids and gasesOther Iifting, handling, Ioading andunloading machinery, n.e.s.Rotating electric plant and parts thereof;transformers, converters, rectifiers,Inductors and parts.Electrical apparatus for making or breakingelectrical circuitsInsulated electric wire, cable, bars, stripand the IikeElectrical Insulators of other materialsElectrical measuring, checking, analysingor controlling Instruments, n.e.s.Electric welding, brazing, soldering andcutting machines and apparatus andparts thereof, n e s.Special purpose motor Iorries, vans,crane Iorries, etc.Light vessels, floating cranes and otherspecial purpose vessels, floating docksFloating structures other than vesselsGas, Iiquid, and electricity supply orproduction meters.Surveying, hydrographic, etc., andgeophysical Instruments (nonelectrical)Parts, n.e.s., of meters and counters;nonelectrical and electrical measuring,checking, etc., instruments of SITC729.52, 861.8 and 861 97

SOURCE Off Ice of Technology Assessment

Ch. 6— Western Energy Equipment and Technology Trade With the U.S.S.R. ● 171

(NIMEXE). The former were useful in pro-viding a clearer sense of the role of energy-related items in U.S. exports; the latter ful-filled the same role for West European coun-tries. Cross-checking Western export withSoviet import data proved impossible. Thisphenomenon is not unique to the energy sec-tor; it reflects different classification sys-tems and data reporting criteria.

It must be noted that U.S. export statis-tics do not include the value of Western tech-nology and equipment sales that originatefrom U.S. subsidiaries or licensees abroad;nor will the category of U.S. exports to theU.S.S.R. include items that are first destinedfor third countries. Corporations that exportenergy technology and equipment are oftenmultinationals or at least have internationalcorporate affiliations in other countries.Some sense of the international nature ofthis industry can be gleaned from appendixA, which shows a partial list of energy cor-

poration affiliations worldwide. The com-plexity of these relationships makes it ex-tremely difficult, if not impossible, to alwaysattribute technology sales to the true coun-try of origin. The data collected here, there-fore, very likely understate the contributionof American technology to the U.S.S.R.

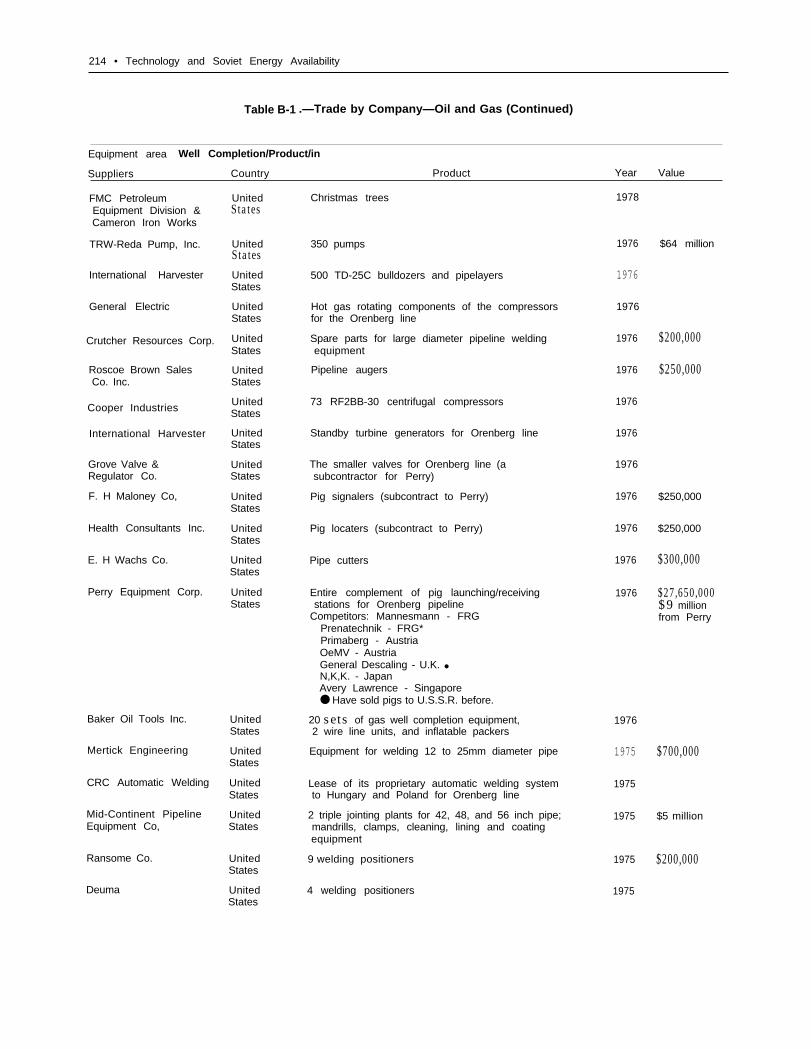

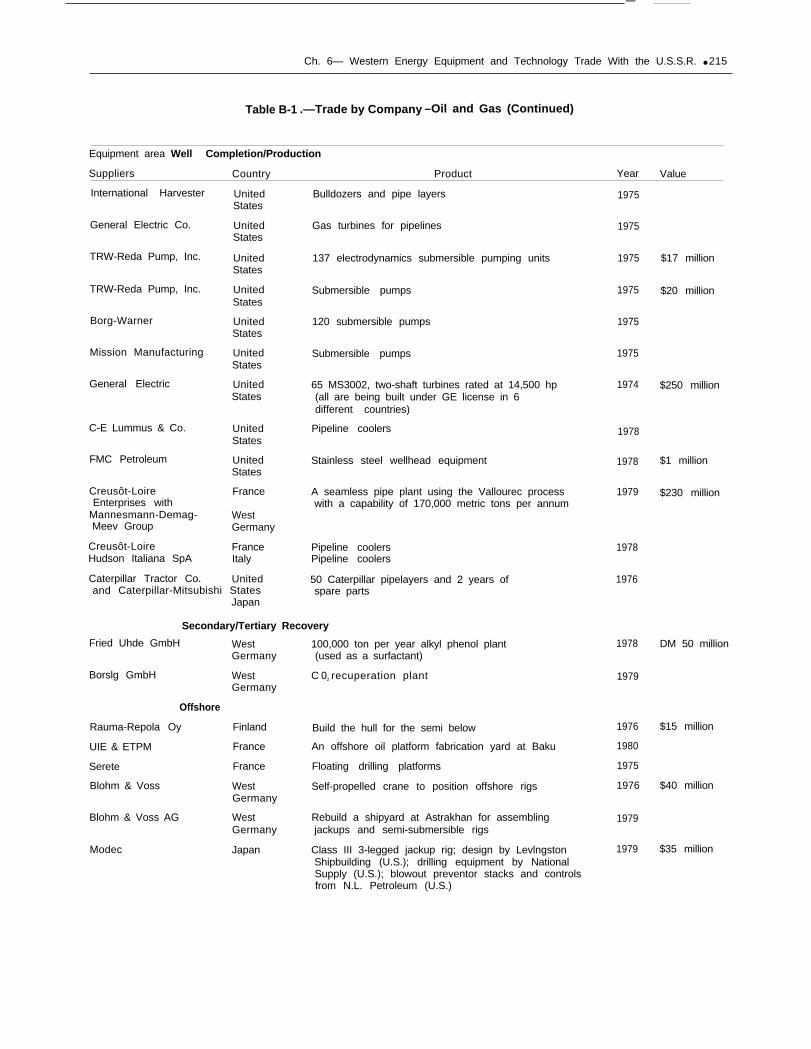

Finally, export statistics are ill-suited toidentifying such technology transfers as thesale of licenses or turnkey plants. For thisreason, OTA supplemented its statisticaldata bases with a comprehensive search ofSoviet Business and Trade, a biweeklypublication that reports major trade dealsbetween the U.S.S.R. and the West.4 TablesB-1 and B-2 in appendix B summarize ener-gy-related transactions reported in this pub-lication between 1975 and 1980.

EAST-WEST TRADE IN ENERGY TECHNOLOGYAND EQUIPMENT

Although Soviet trade with the West hasgrown markedly in the past decade, it has re-mained a relatively small part of world tradeas a whole. Except for sales of agriculturalcommodities (i.e., grain), the United Stateshas captured relatively small market sharesof this trade compared to other nations inthe Industrial West (IW, defined here asCanada, France, Italy, Japan, Netherlands,Norway, Sweden, Switzerland, the UnitedKingdom, the United States, and West Ger-many). 5 Table 41, which shows total Sovietimports from the IW, demonstrates thatwhen agricultural commodities are excluded,in 1979 the United States lagged behindWest Germany, Japan, and France in in-dustrial exports to the U.S.S.R.

Table 42 shows the value of Soviet im-ports of items in the energy-related SITCcodes listed in table 40. From these data,

5 See OTA, op cit., ch. 111.

OTA estimates that energy-related itemsconstituted about 25 percent of total Sovietimports from the IW in 1975, and about 22percent in 1979. When total imports are ad-justed to omit agricultural commodities, therelative importance of energy-related tradeincreases slightly. In 1979, about 28 percentof Soviet nonagricultural imports from theWest consisted of energy equipment andtechnology.

It is clear from table 42 that the vastpreponderance of the U.S.S.R.’s energy-related imports are destined for its oil andgas industries, a fact that is demonstratedgraphically in figure 11. The oil and gas sec-tor in 1979 took up 77 percent of such im-ports. Assuming that a similar proportion ofmultiarea items—i.e., those that could beemployed in more than one energy in-dustry—were destined for the oil and gas in-dustries, approximately 81 percent of allSoviet purchases of energy equipment and

172 • Technology and Soviet Energy Availability

Table 41 .—industrial West Exports to the U. S. S. R., Selected Countriesa 1975-1979 (million U.S. dollars)

Total Industrial United West UnitedYear West a States Japan France Germany Italy Kingdom Other— . —

1979 . . . . . . . . . . . . . . . . $15,255 $3,604 $2,461.0 $2,007 $3,619 $1,220 $694 $1650.4Industrial. . . . . . . . . 12,151 1,319 2,461 1,791 3551 1,191 655 1,183,1Agricultural . . . . . . 3,104 2,285 0.2 216 68 29 39 467,3

1978 . . . . . . . . . . . . . . . . 12,419 2,249 2,502 1,455 3,141 1,133 665 1,274Industrial. . . . . . . . . 10,485 804 2,501 1,408 3,128 1,084 615 945Agricultural . . . . . . 1,934 1,445 1 47 13 49 50 329

1977 . . . . . . . . . . . . . . . . 10,788 1,624 1,934 1,496 2,789 1,228 607 1,110,1Industrial. . . . . . . . . 9,411 747 1,934 1,369 2,765 1,218 602 776Agricultural . . . . . . 1,377 877 0 127 24 10 5 334

1976 . . . . . . . . . . . . . . . . 11,051 2,306 2,252 1,118 2,685 981 432 1,277Industrial, . . . . . . . . 9,005 946 2,252 977 2,659 974 427 770Agricultural . . . . . . 2,047 1,360 0 141 26 8 5 507

1975 . . . . . . . . . . . . . . . . 10,092 1,834 1,625 1,147 2,824 1,020 464 1,178Industrial. . . . . . . . . 8,469 720 1,625 1,059 2,816 996 459 794Agricultural . . . . . . $1,623 $1,114 $ 0 $ 88 $ 8 $ 24 $ 5 $384

a l ndus t r ia l i zed W e s t e r n n a t i o n s In c l u d e C a n a d a F r a n c e I t a l y J a p a n t h e N e t h e r l a n d s N o r w a y S w e d e n S w i t z e r l a n d t h e U n i t e d K i n g d o m t h e U n i t e d S t a l e s a n d W e s t

Germany

SOURCE: OECD, Stastitics of Foreign Trade Series B Paris (Annual).

Table 42.—Soviet Energy-Related Imports From Selected Western Countriesa

(million U.S. dollars)

Electric MultiareaYear Oil/qas Coal Nuclear power commodities Total

1979 . . . . . . . . . . . . . . . . . . . . $2,652.5 $255.9 $84.1 $279,3 $155.1 $3,427

1978 ..., . . . . . . . . . . . . . . . . 2,321,0 237.0 70.4 3319 134.8 3,095

1977 . . . . . . . . . . . . . . . . . . . . 1,991.7 174.4 98.8 252.6 103.4 2,621

1976 ......, . . . . . . . . . . . . . 2,250,0 202.8 70.2 157.0 86,5 2,767

1975 ......, . . . . . . . . . . . . . $1,989.5 $212.5 $90.5 $117,6 $90.3 $2,500

a l nc ludes Canada France I ta ly Japan, the Netherlands Norway Sweden, Switzer land the United Kingdom the United States and West Germany

NOTE Data here IS for the SITC codes Iisted in table 40

SOURCE Un i t ed Na t i ons S ITC da ta

technology were used to find, produce, anddeliver oil and gas. The share of the nuclearpower sector was less than 3 percent; that ofcoal 7 percent; electric power, 8 percent; andother multiarea items, 1 percent.

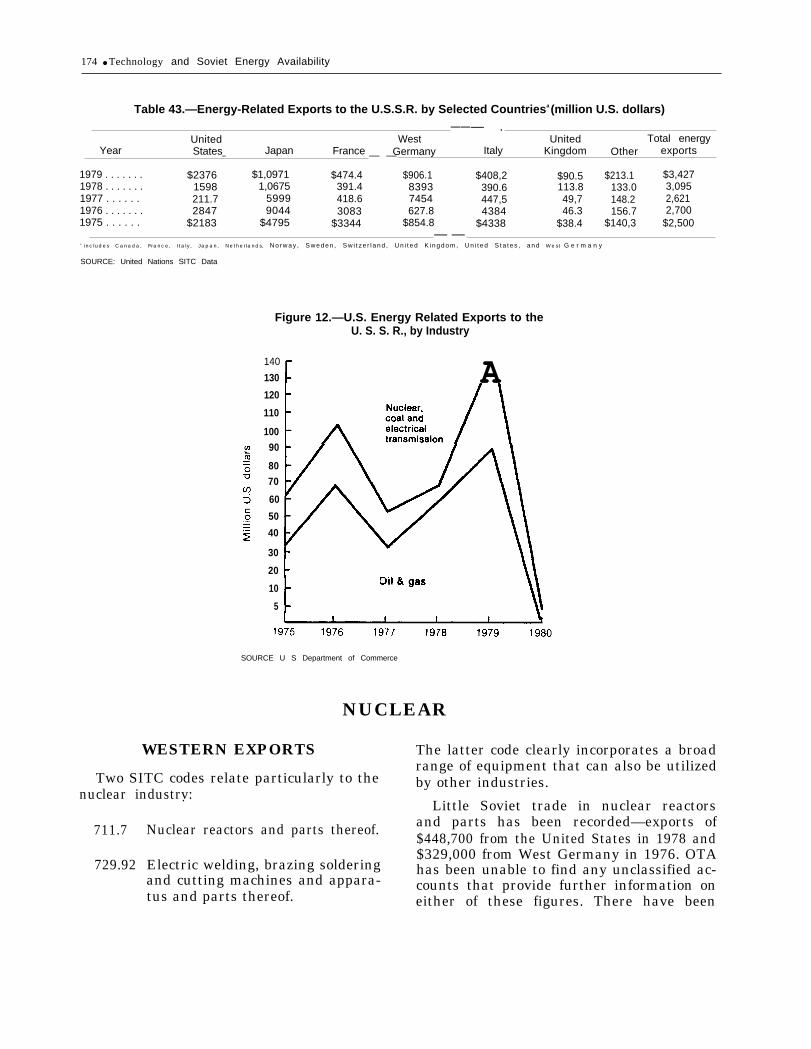

The role of the United States in thisenergy-related trade has been small, both interms of its share in U.S.-Soviet trade as awhole, and in comparison to the relative

shares of energy-related equipment and tech-nology in the Soviet trade of America’sallies. As table 43 displays, the value of U.S.exports to the U.S.S.R. in energy-relatedSITC codes for 1979 was $237.6 million. Thisconstituted some 6.6 percent of America’stotal and about 18 percent of its industrialexports to the Soviet Union in that year.Table 43 also shows that in 1979, the valueof U.S. energy-related exports to the

Ch. 6— Western Energy Equipment and Technology Trade With the US.S.R. ● 173

Figure 11 .—SovietEquipment and

Imports of Western EnergyTechnology, by Industry

U.S.S.R. was lower than those of Japan,West Germany, France, and Italy. Japanwas by far the largest energy equipment sup-plier to the U. S. S. R., its exports totallingabout one-third of all Soviet purchases inthis area. West Germany was a close second.France and Italy both recorded exportsabout double those of the United States. In1979, the United States accounted for under7 percent of energy-related exports to theU.S.S.R. of the Western countries examined.

on which this analysis is based seriously in-flates the export figures by including itemsnot destined for the Soviet energy sector,this percentage may actually be evensmaller. U.S. trade statistics as of this writ-ing are available only through October 1980,but these suggest that U.S. energy-relatedexports plummeted in 1980, the result of thepost-Afghanistan technology embargo.

The composition of the Soviet Union’spurchases from the United States reflectsthe same pattern as its energy-related im-ports from the West as a whole, i.e., they arelargely composed of items destined for theoil and gas industries. This pattern is shownin figure 12. But although U.S. sales havenot been high in dollar amounts, or particu-larly impressive as a percentage of totalSoviet energy-related imports, it has beencontended that their importance to theU.S.S.R. is greatly magnified by the factthat they have been composed of criticalitems, some of which are unavailable else-where in the world. The remainder of thischapter will investigate this assertion, exam-ining sector by sector the composition and

n

1975 1976 1977 1978 1979

Year

SOURCE Table 42

magnitude of Soviet imports in each of thefive energy industries under consideration,and identifying the sources of these imports.Where U.S. firms have been active traders,an attempt has been made to ascertainwhether or not comparable items areavailable elsewhere in the West.

174 ● Technology and Soviet Energy Availability

Table 43.—Energy-Related Exports to the U.S.S.R. by Selected Countriesa (million U.S. dollars)——— .

United West United Total energyYear States Japan France Germany Italy Kingdom Other exports— — —

1979 . . . . . . . $2376 $1,0971 $474.4 $906.1 $408,2 $90.5 $213.1 $3,4271978 . . . . . . . 1598 1,0675 391.4 8393 390.6 113.8 133.0 3,0951977 . . . . . . 211.7 5999 418.6 7454 447,5 49,7 148.2 2,6211976 . . . . . . . 2847 9044 3083 627.8 4384 46.3 156.7 2,7001975 . . . . . . $2183 $4795 $3344 $854.8 $4338 $38.4 $140,3 $2,500

— —a i nc ludes Canada, F rance, I ta ly , Japan, Nether lands , N o r w a y , S w e d e n , S w i t z e r l a n d , U n i t e d K i n g d o m , U n i t e d S t a t e s , a n d W e s t G e r m a n y

SOURCE: United Nations SITC Data

Figure 12.—U.S. Energy Related Exports to theU. S. S. R., by Industry

140

130

120

110

10090

8070

60

50

40

30

20

10

5

A

SOURCE U S Department of Commerce

NUCLEAR

WESTERN EXPORTS The latter code clearly incorporates a broad

Two SITC codes relate particularly to therange of equipment that can also be utilizedby other industries.

nuclear industrv:.Little Soviet trade in nuclear reactors

711.7

729.92

Nuclear reactors and parts thereof. and parts has been recorded—exports of$448,700 from the United States in 1978 and

Electric welding, brazing soldering$329,000 from West Germany in 1976. OTAhas been unable to find any unclassified ac-

and cutting machines and appara-tus and parts thereof.

counts that provide further information oneither of these figures. There have been

Ch. 6— Western Energy Equipment and Technology Trade With the U.S.S.R. ● 175

report that the U.S.S.R. may be consideringthe purchase of reactors from Italy, but asyet no such deal has been completed. (Itmust be noted that the U.S.S.R. has also ex-ported nuclear reactors to the West.) How-ever, the limitations of using and difficultiesin interpreting trade statistics may be il-lustrated by the fact that a $47 million con-tract purportedly signed with the Italianfirm Breda Termomeccanica in 1976 for thedesign and building of reactor manufactur-ing facilities at Atommash and Izhora does

Figure 13.— Western Energy Trade With

not appear in this SITC code.6 It is possiblethat this deal was not consummated or thatit is reflected elsewhere in the trade data,

SITC code 729.92 covers electric welding,brazing, soldering, and cutting machines andapparatus and parts. IW trade in this areaamounted to over $90 million in 1975 andover $84 million in 1979, but as figure 13 in-dicates, U.S. shares have been falling since

6 Soviet Business and Trade,

U.S.S.R.—Welding Equipment

I United Kingdom

l \ \ \

Nov. 24, 1976, p. 4.

(SITC 729.92)

\

West Germany

1975 1976 1977 1978 1979

Year

SOURCE United Nations SITC Data

176 ● Technology and Soviet Energy Availability

1975. In 1979, less than 10 percent of thewelding equipment supplied to the U.S.S.R.by the IW came from the United States,while West Germany and Italy together sup-plied nearly half.

In addition to the items contained in thesetwo codes, several purchases that may havebeen destined for the nuclear industry havebeen noted in Soviet Business and Trade.These include a hydraulic press purchasedfrom Japan;7 pumps from a United Kingdomfirm, 8 and various valves, shutters, andplugs from West Germany and Canada.9

Velan Engineering Co. of Canada is a majorsupplier of valves for the Soviet oil, gas,chemical, and nuclear industries.

F O R E I G N A V A I L A B I L I T Y O FN U C L E A R E Q U I P M E N T A N D

T E C H N O L O G Y

Aside from complete reactors, chapter 4has identified some areas in which, shouldthey decide to step up their nuclear-relatedpurchases, the Soviets might usefully turnto the West to supplement their own manu-facturing capabilities. These areas includenuclear grade tubing and pipes, welding andbrazing equipment, steam generators,pumps and casings (to circulate coolantthrough the reactor), nuclear valves, andcomputers, software, and automatic control.It must be stressed that at present theU.S.S.R. imports very little, if any, suchequipment. Indeed, analysis of the tradedata has confirmed chapter 4’s generaliza-tion that the Soviet nuclear power industryhas been virtually self-sufficient. Assumingfor purposes of argument that the U.S.S.R.might reverse its policy, OTA sought todetermine in which, if any, of these areas the

————— ——“i${)/itJt Bu,sinc,s,s art[i Tru~ie, No\T. 24, 1976. T h i s , t o g e t h e r

with Italian large boring and milling machines, Germanmachine tools, and U.S. welding and X-ray equipment, wasdestined for Atommash. See also Nucleonics Week, Nov. 8,1979, p. 12.

‘1 la~’w.ard ‘1’a?rlor & (’o., 1,td. .Sf)[ ‘ict };u.sin~).s.s IIn(i ‘/’ra(ie,

1+’et). 17, 1975.“.%)fict l~u.iillf~s,s IIHfi ‘1’r[~tlf, P’eh. 1 l’, 1 975; Apr . 2H, 1975:

and I)ec. 6, 1978.

United States might be considered a sole orpreferred supplier to the U.S.S.R.

OTA’s “foreign availability analysis” forthe nuclear industry was based on informa-tion from industrial trade journals and inter-views with representatives of U.S. firms(Westinghouse, Rollmet, Ransome), OakRidge National Laboratories, the NuclearRegulatory Commission, and the U.S. De-partment of Energy. The results of thisanalysis are reported in tables C-1 throughC-7 of appendix C. It can be seen from thesetables that firms in a variety of countriescould potentially supply the U.S.S.R. withthe kind of nuclear equipment and tech-nology it is most likely to seek.

There is one area in which the UnitedStates could be a strongly preferred sup-plier. The United States is the acknowledgedworld leader in many areas of computer tech-nology. Computers are normally used at nu-clear power stations for rather mundanetasks—data acquisition and simple processcontrol—and the U.S.S.R. presently reliesheavily on domestically produced computersat its nuclear stations. If greater power sta-tion automation is planned, however, moresophisticated systems might be necessary.

The United States is also a world leader indeveloping and mass-producing exotic, high-strength materials (zircalloy, and high nickelcontent stainless steel). These are useful inthe nuclear industry, particularly for ad-vanced breeder reactors. Such technologyhas been fairly widely diffused. Indeed, themeans by which nuclear technology is spreadthroughout the world may be illustrated byseveral examples: The U.S.-based Westing-house Electric Co. exports nuclear grade tub-ing to Mitsubishi in Japan, Framatone inFrance, and ENSA in Spain, and each ofthese companies constructs nuclear reactorsunder a Westinghouse license. Toshiba andHitachi of Japan are General Electric licens-ees.10 The reactor in the state-owned plant at

10 Mans Lonnroth and William Walker, T’he Viahilit J’ oft h e (’ivil N u c l e a r IndustrJr, ” Internat ional Consultati~e(;roup on Nuclear Flnergy (The Rockefeller l’oundation,1979),

Ch. 6— Western Energy Equipment and Technology Trade With the U.S.S.R • 177

Krsko, Yugoslavia, was purchased from nuclear plants. Should it reverse its policyWestinghouse. and begin seeking Western imports in this

area, it would find numerous potential sup-S U M M A R Y A N D C O N C L U S I O N S pliers in several nations.

The U.S.S.R. is presently self-sufficient inthe design, manufacture, and operation of its

COAL

WESTERN EXPORTS

The U.N. SITC codes that contain equip-ment applicable to coal mining are asfollows: ‘ ‘

571.1

571.2

629.4

655.92

695.24

718.42

718.51

Figure

Propellent powers and other pre-pared explosives.

Safety and detonating fuses, per-cussion, and detonating caps,igniters, etc.

Transmission, conveyor and ele-vator belts of vulcanized rub-ber.

Transmission, conveyor and ele-vator belts of textile materials.

Rock drilling bits: tools and bitsfor assorted hand tools.

Self-propelled shovels and exca-vators, self and non-self-pro-pelled leveling, tamping, bor-ing, etc., machinery and partsthereof.

Machinery for sorting, screen-ing, separating, washing, crush-ing, etc., for earth, stone, ores,and other minerals.

14 summarizes trade in each ofthese categories for the period 1975-79. Itshows that the U.S.S.R. has purchased nofuses or explosives from any IW nation(SITC 571.1 and 571.2) since 1977. During1975 and 1976, U.S. exports in these cate-gories were very small ($5,000 to $28,000).Japan and West Germany led the sale of

transmission, conveyor, and elevator belts ofvulcanized rubber (SITC 629.4) to theU.S.S.R. in 1975-79; Soviet purchases fromthe United States were a weak third orfourth (behind Italy). These sales totaledabout $48.7 million for all countries duringthe entire period. Sales in the category655.92 were negligible.

In sales of rock drilling bits and tools, andbits for assorted hand tools (SITC 695.24) tothe U. S. S. R., the United States lagged WestGermany, Japan, France, Italy, and theUnited Kingdom. Indeed, the U.S. marketshare here has fallen precipitously since 1975when sales of $1.3 million were recorded—in1979 only $13,000 of such goods were pur-chased from the United States. Because thisequipment might equally well be destined forthe oil and gas sector, it is discussed in moredetail below.

The Soviet Union buys considerableamounts of self-propelled shovels and ex-cavators, leveling, tamping, and boring ma-chinery (SITC 718.42). However, the finerbreakdowns available from U.S. Scheduled Band E and NIMEXE data reveal that mostof the purchases here are for items probablydestined for the oil and gas industries. Coal-relevant subcategories from Schedule B andSchedule E include draglines, dragline buck-ets, coal cutting machines, continuous min-ing machines, longwall mining machines,and excavating machines (including attach-ments). No exports from the United Statesto the U.S.S.R. whatsoever have been re-ported in any of these subcategories.

In 1979, the U.S.S.R. bought $81.8 millionworth of machinery for sorting, screening,

178 • Technology and Soviet Energy Availability

Figure 14.—Coal-Related Equipment Exports to U.S.S.R. (million U.S. dollars)

130-

1 2 5 -

1 2 0 -

1 1 5 -

1 1 0 -

1 0 5 -

1 0 0 -

9 5 -

8 0 -

6 5 -

8 0 -

7 5 -

7 0 -

6 5 -

6 0 -

5 5 -

5 0 -

4 5 -

4 0 -

3 5 -

3 0 -

2 5 -

2 0 -

1 5 -

l o -

5 -

0 -

126.0—

Othel119.6—Otho—

UK—

Italy

—

v Oe

—

Japaf

—

ram

—

us

—

Othe! N Ge—

UK 110.7

106.4

99.7

—N GGI

Oth#

7s—

Ma!)—UK

—Fran<—

Jbpa

—

v Ge

—

—

‘m-m Otue—

UK

T&—us

Franc4

w 501

Italy

82.4

UK—

w G@

France

usus

—

64.963.5

Othe,

—%anc{—Italy

—

N GOI

—

us

OttwrItalyT

France

Swttz

W Ger

us

51.0

Otilel—

JaPM

us

w GIN

1976

N Ger

aaan

21.4

& ,8.IOther

w Ger

‘$-

Othel

JapanOlhef France

France ~apa,,

w tam

us

12.4Japan

France

— —19?7 1 9 7 8 19781975 1976 1977 19?8 1079 1975 1976 1977 1978 1979

SITC 695.24

1977 1976 19791975 1975

SITC 571.1, 571.2628.4, 655,92

SITC 718.42 SITC 718.42

SOURCE United N a t i o n s , S I T C d a t a

Ch. 6—Western Energy Equipment and Technology Trade With the U.S.S.R. ● 179

separating, washing, and crushing (SITC718.51) from West Germany. Imports fromthe United States in the same category cameto less than $2.4 million, mostly for crush-ing, pulverizing, and grinding machines andparts. West Germany has carried most ofthis market since 1976.

In sum, it would appear that Soviet pur-chases from the West for its coal industryhave been relatively modest and that be-tween 1975 and 1979 little of these camefrom American firms. Soviet import statis-tics corroborate this broad conclusion. Al-though the Soviet method of reporting com-modity trade differs from that employed inthe West—in commodity groupings, valu-ation, coverage, and the method used foridentifying trade partners—data from theU.S.S.R. reflect the same patterns as West-ern export statistics.

Table 44 shows official Soviet import dataon items that may have an impact on coal-related activities, These data indicate that inrecent years, Soviet purchases from WestGermany and Japan have been much largerthan those from the United States. For ex-ample, in 1978, the figures show imports of$115.4 million of sorting machinery fromWest Germany, but only $6 million from theUnited States. West Germany ($30.4 million)also led the United States ($4.2 million) in ex-ports of mechanical shovels and excavators.Although the only Soviet imports of ships,derricks, and cranes reported in 1977 and1978 come from the United States, the dollaramounts ($891 ,000 and $5.7 million) arerelatively small. The U.S.S.R. purchased$58.6 million and $92.4 million worth ofthese goods from Japan in 1976 and 1975,respectively.

A search of Soviet Business and Trade fortransactions that might not have appearedin the SITC codes indicates that the mostimportant category of U.S. exports likelydestined for the Soviet coal industry wastransportation. Approximately 100 trucks(ranging in size from 100 to 200 tons) pur-chased from the Unit Rig & Equipment Co.of Tulsa, Okla., for about $70 million were

Table 44.—Soviet Imports From SelectedWestern Nationsa

-——.1978 1977 1976 1975 —

U.S.S.R. imports of machinery for sorting

United States . . 6 ,096 26 ,287 32 ,900 24 ,110

West Germany 115,423 30,780 7,573 4,555

1978 1977 1976 1975

U.S.S.R. Imports of mechancial shovels and excavators

United States . . 4,169 9 1 7 9 , 6 9 2 1 0 , 9 2 3

West Germany . 30 ,444 11 ,799 9 ,262 28 ,516

France . . . . . . . . 2,790 1,157 13,299 5,522

1978 1977 1976 1975

U.S.S.R. imports of ships, derricks and cranes

United States . . 5,677 891 266 10 ,424

Italy . . . . . . . . . . . — — 3,693 16,068

United Kingdom 110 037 2,758 3,700

Japan . . . . . . . . . — — 58 ,646 92 ,403

aOTA collected Soviet data for France, Italy, Japan, the United K Ingdom, Uni tedStates West Germany and West Berlin. Only those areas that showed trade in a

given category are presented here

SOURCE CIA based on Soviet trade data

for use in coal-related activit ies.12 O t h e rAmerican deals have included $14 millionworth of slurry pumps from Ingersoll-Randb e t w e e n 1 9 7 4 a n d 1 9 7 6 ;13 a n d f r o n t - e n dloaders contracted for $1 million from theClark Equipment Co. in 1978, and for $2.9million from Dart Division of Paccar, inc. in1979. 14

Between 1974 and 1980 Japanese firms in-volved in the South Yakutian DevelopmentCorp. were responsible for sales totaling ap-proximately $450 mil l ion,15 most of whichconsisted of shovels and other surface min-ing equipment. In addit ion, in 1976 and1975, respectively, the U.S.S.R. reportedlycontracted for $500,000 worth of equipmentfor excavation in underground mines from

180 ● Technology and Soviet Energy Availability

the United Kingdom, and a similar amountin front tunneling machines and loaders fromWest Germany.16

F O R E I G N A V A I L A B I L I T Y O FC O A L T E C H N O L O G Y A N D

E Q U I P M E N T

As chapter 3 has indicated, the U.S.S.R.is well able to design, test, and manufactureits own coal mining equipment. Soviet equip-ment is heavier and somewhat less sophisti-cated than U.S. equipment, but it is ade-quate. A common Soviet practice has been tobuy items applicable to a specific phase ofcoal mining and reproduce them. Soviet-made continuous miners, for example, arecopies of West German, English, and Frenchmodels. Drill bits that were formerly pur-chased from Western Europe are now do-mestically produced. Equipment for Siberiansurface mining was originally purchasedfrom Marion in Japan.

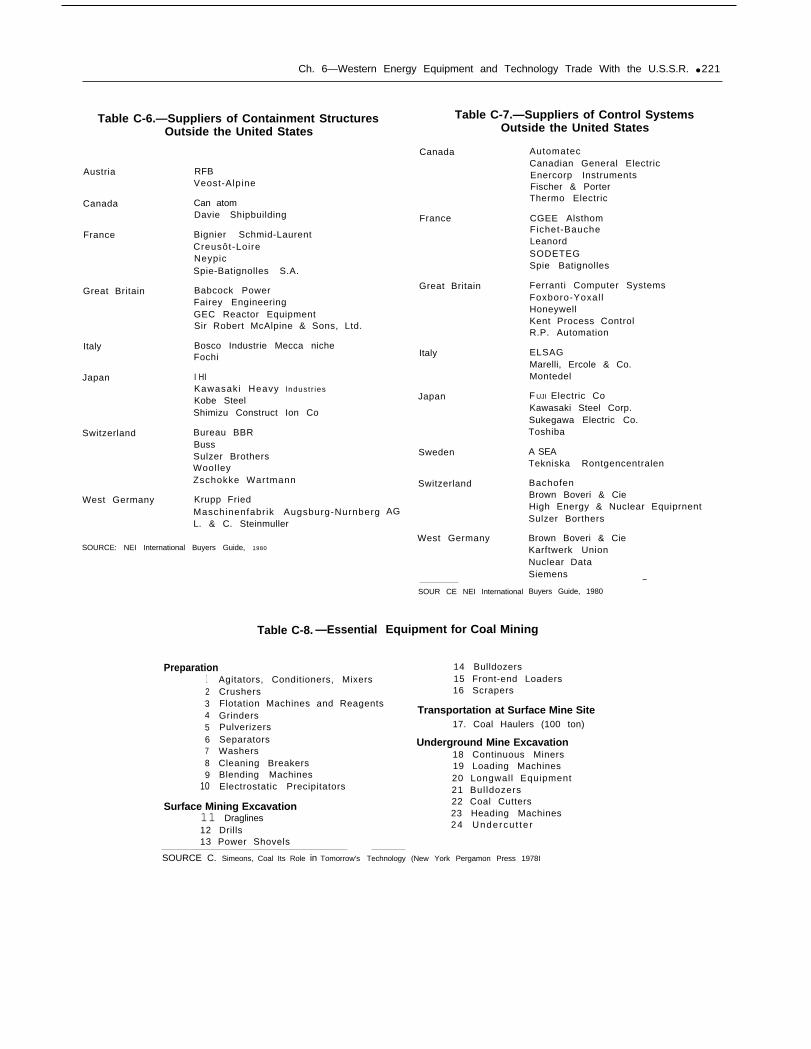

In short, like the nuclear industry, theSoviet coal mining industry has been essen-tially self-sufficient. In an attempt to ascer-tain whether a reversal of past Soviet prac-tice with respect to coal-industry equipmentimports would focus on items in which theUnited States is a sole or preferred supplier,OTA assembled a list of essential equipmentfor coal mining operations, and attempted tolocate suppliers of this equipment in West-ern Europe and Japan. The results may befound in tables C-8 and C-9 of appendix C.Outside of the few deals discussed above,there is no evidence that any of the com-panies listed here have actually supplied orintend to supply equipment to the U.S.S.R.Nevertheless, it is clear from table C-9 thatthere exist many European and Japanesesuppliers of coal mining equipment.

Comparison of the items available fromthese companies and those produced in theUnited States reveals substantial differ-ences between underground and surface min-ing capabilities. The majority of Soviet un-——

16 Soviet Business and Trade, Nov., 22, 1978; June 6, 1979.

derground mining utilizes longwall tech-niques not widely employed in the UnitedStates. Longwall mining was invented in the1950’s in West Germany; in fact, the UnitedStates is heavily dependent on Britain andWest Germany for longwall research and de-velopment, and it also imports substantialamounts of European longwall equipment.(The U.S.S.R. has attempted to export itsown longwall systems to the United States.)Much of the underground coal mining equip-ment manufactured in large quantities in theUnited States is therefore of little or no useto the U.S.S.R. Undercutter are availableonly from the United States, but these arenot necessary for longwall mining opera-tions. There are also differences in geologicformations that render much U.S. equip-ment inapplicable in the U.S.S.R.; e.g., thenarrow seams in many Soviet mines do noteasily lend themselves to mechanization.

A different situation pertains with respectto surface mining, which, as chapter 3 haspointed out, will become increasingly crucialto Soviet coal production as the decade pro-gresses. The United States is a world leaderin surface mining equipment and technol-ogy, and produces items that could be ofgreat use to the U.S.S.R. One example is thedragline. This is the only piece of surfacemining equipment in continuous operation,and coal output is heavily affected by itsspeed in removing overburden. U.S. drag-lines and excavators have the largest capac-ities currently available. Increased excava-tion capacity would allow Soviet surfacemining to become more productive, and big-ger draglines would facilitate deeper surfacemining. U.S. firms also produce trucks,power shovels, and excavators with capac-ities much larger than any available fromWestern Europe or Japan. These items,though not vital to the ability to mine coal,could help to increase output.

S U M M A R Y A N D C O N C L U S I O N S

Both Soviet and Western trade data showthat the U.S.S.R. has purchased relativelylittle coal mining equipment and technology

Ch. 6— Western Energy Equipment and Technology Trade With the U.S.S.R • 181

from the West, perhaps less than 10 percentof its total equipment needs. With the possi-ble exception of transport vehicles, Amer-ican market shares in this trade are smallerthan those of other Western countries, espe-cially West Germany and Japan. The onlycoal mining technology that OTA could es-tablish as unique to the United States isundercutter, but these are not used inthe U.S.S.R. American underground miningtechnology is unlikely to be particularly at-tractive to the Soviet Union.

ELECTRIC

WESTERN EXPORTSFigure 15 shows export statistics for the

following SITC codes containing equipmentused for the generation and transmission ofelectric power:

711.1 Steam generating boilers.711.2 Auxiliary plant for use with steam

and other vapor generatingboilers.

722.1 Rotating electric plant and partsthereof; transformers, conver-ters, rectifiers, inductors andparts.

722.2 Electrical apparatus for makingor breaking electric circuits.

723.1 Insulated electric wire, cable,bars, strip and the like.

723.21 Electrical insulators and othermaterials.

1979 statistics for SITC 722.1 indicatethat Japanese, French, and West Germanfirms supplied the U.S.S.R. with $15.2 mil-lion, $11.9 million, and $11.1 million worth oftransformers, converters, rectifiers, induc-tors, and parts thereof, respectively. Pur-chases from the United States in this cate-gory amounted to only $1.35 million. Muchthe same situation has prevailed since 1977.Similar patterns hold for electrical appara-tus used in making or breaking electrical cir-cuits (SITC 722.2). From 1975 to 1979,Soviet imports from the United States ($3

While no surface mining technologiesseem to be unique to the United States, U.S.firms do produce the largest capacity trucks,draglines, and excavators in the world.Chapter 3 has maintained that the future ofSoviet coal production rests on expandingits surface mining operations. Should theU.S.S.R. depart from past practice and beginto import large quantities of Western sur-face mining equipment, the United Stateswould—all other things being equal—be thepreferred supplier.

POWER

million) have been dwarfed by imports fromFrance ($59.2 million), Japan ($51.7 million),West German ($11.3 million), and Italy($13.6 million). The Soviet Union does notpurchase many electrical insulators (SITC723.21). Most of its 1979 purchases camefrom the United States, but these amountedto only $666,000. Even this was an anomaly.Between 1975 and 1979, no Soviet purchasesfrom any country exceeded $48,000.

A similar aberration can be seen in thedata for SITC 711.1, steam generatingboilers. The $19 million recorded in thiscategory for U.S. exports in 1979, althoughnot a large amount in absolute terms, repre-sented a departure from Soviet practice overthe past 5 years in two ways. The UnitedSta tes had not be fore been the l a rges tWestern supplier of this equipment, and theamount was significantly greater than anyrecorded previously for a single country in asingle year. OTA has been unable to discoverany details of the transaction or transactionsthat accounted for these expor ts . S ITC711 .2 conta ins aux i l i a ry p lant for suchboilers. Except for large U.S. sales in 1976and 1977 ($9.4 and $22.7 million), for whichOTA has been unable to obtain more infor-mation, Soviet purchases in this categoryhave come almost exclusively from France inamounts ranging between about $.2 and $5million per year.

182 ● Technology and Soviet Energy Availability

Figure 15.—Electric Power Equipment Exports to the U.S.S.R. (million U.S. dollars)

180 -

175-

170-

165-

mo-

155-

150-

145-

140 “

135-

130-

125-

120 -

115-

110-

105-

100-

9 5 -

90“

85-

so-

75-

70 -

65”

6 o -

5 5 -

5 0 -

45-

40-

35-

3 0 -

25-

20-

M

t o - -

5 -

0 -1975 1976 1977 1978 1979 1975 1976 1977 1978 1979

SITC 711.1 SITC 711.2 SITC 722.1

SOURCE United Nat Ions, SITC data

am

—Ux

—

Japan

W. Ger.

4 1 &

1975

106.9—Other

U.K.—U.S.

—

Japan

—

Italy

—

33.7

Other W. Ger.

U.K.U.S.

Italy

W. Ger

France

France

—

Japan

1976 1977

SITC 722.2

72.’—

Other

U.S.

U.K.—

Italy

.

W. Ger.

.

France

Japan

1978

148.6

Other—

U.S.—

U.K.

—

W. Ger,

.

Italy,

—

Japan

France

1979

59.4

48.2

other

W. Ger.

Italy

France

Japan

—1975 1976 1977 1978 1979

SITC 723.1,723.21

Ch. 6—Western Energy Equipment and Technology Trade With the U.S.S.R. * 183

It was not possible to determine the pro-portion of the equipment in these codes thatwas actually destined for the Soviet electricpower industry. Soviet Business and Tradenoted only one relevant deal over the past 5years, a Soviet purchase of cable for theSiberian power grid from Siemans AG ofIndia and West Germany. 1 7

F O R E I G N A V A I L A B I L I T Y O FE L E C T R I C P O W E R E Q U I P M E N T

A N D T E C H N O L O G Y

The U.S.S.R. does not purchase very largeamounts of electric generation or transmis-sion equipment from the West. As in the coaland nuclear sectors, however, Soviet policycould change. OTA, therefore, attempted todetermine whether competing firms inEurope and Japan could supply the U.S.S.R.with electrical transmission technology.

American industry representatives havemaintained that technology for the produc-tion of most of the necessary equipment forelectricity generation and transmission iswidespread and available in the open liter-ature. Interviews with General Electric(GE), Westinghouse, the Electric Power Re-search Institute (EPRI), and the BonnevillePower Administration produced a consensusview that European-produced equipmenttypically costs less than American equip-ment, and that the quality and capacity ofthe equipment produced by West Europeanand Japanese companies compare favorablywith U.S. items. A representative from GEclaimed that the West Europeans were at———.—

‘‘L5’{)({Pt B(t.sttte.vs an(i 7’ra(le, Sept. 29, 1976.

least on par with, and possibly ahead of, theUnited States in high voltage transmission,and a representative from the BonnevillePower Administration told OTA that WestGermany, Sweden, and Japan equal theUnited States in producing high capacityunderground cable technology and equip-ment,

West European and Japanese firms thatproduce electric generation and transmissionequipment are listed in tables C-3 and C-10of appendix C. Licensing agreements be-tween Mitsubishi and Siemens exist formany of the items used in transmission,Moreover, the U.S.S.R. itself produces sometransmission components for export. TheSoviet trading organization, Energomash,has sales agents in Australia, Austria, Ar-gentina, Belgium, Brazil, Canada, West Ger-many, and the United States. Among theproducts it markets are coupling capacitorsfor high voltage transmission lines, three-phase power transformers, and circuitbreakers for use in substations.

S U M M A R Y A N D C O N C L U S I O N S

While the Soviets buy some electricalequipment from the West, these purchasesare relatively modest and no corroboratingevidence is available to link them to electrictransmission. The sole exception is pur-chases of cable (from Siemens of West Ger-many). International sales representativesfor General Electric and Westinghouse, andelectric transmission experts who havevisited the U.S.S.R. agree that the Sovietsdesign and produce virtually all their owntransmission equipment.

184 ● Technology and Soviet Energy Availability

OIL AND GAS

WESTERN EXPORTS

Figure 16 shows United Nations data forthe most important oil and gas related SITCcodes:

Exploration714.3

714.92

861.91

861.99

Drilling695.24

732.4

Automatic data processing(ADP) machines and unitsthereof; magnetic and opticalreaders and machines for proc-essing data.

Parts and accessories for ADPand other calculating ma-chines.

Surveying, hydrographic, etc.,and geophysical instruments(nonelectric).

Parts of meters and counters;nonelectric and electricalmeasuring, checking, etc., in-struments.

Rock drilling bits; tools andbits for assorted hand tools.

Special purpose motor lorries,vans, crane lorries, etc. (in-cludes rigs).

~>roductionlcom ple tiOn/t7-anSpOrta tion

678,679.2

642.93

719.21

719.22

719.23,712.31

719.31

Tube-s, pipes, and-fittings ofiron and steel.

Gummed or adhesive paper instrips or rolls (for pipe insula-tion).

Pumps for liquids and partsthereof.

Air and vacuum pumps and airor gas compressors and partsthereof.

Filtering and purifyingmachinery and apparatus forliquids and gases.

Ships, derricks, cranes andmobile lifting cranes andparts; other lifting, handling,and loading and unloadingmachinery.

Offshore735.92 Light vessels, floating cranes

and other special purposevessels, floating docks.

735.93 Floating structures other thanvessels.

Multiarea729.52 Electrical measuring, checking,

analyzing, or controlling in-struments.

861.81, Gas, liquid, and electricity729.51 supply or production meters.

The codes presented here are clearly un-suitable for any precise analysis of Soviet oiland gas industry imports. They includemany items that may have been destined forother energy sectors or for another part ofthe Soviet economy altogether, and they failto reflect known important transactions—the U.S. sale by Dresser Industries of a drillbit plant, for instance. For this reason, OTAhas supplemented the SITC data with De-partment of Commerce Schedules B and Estatistics—which provide detailed informa-tion about U.S. exports–the EEC NIMEXEsystem, and information about specifictransactions gleaned from Soviet Businessand Trade. These sources have allowed arather more detailed, albeit sometimes quali-tative, discussion of the nature, extent, andsource of Western exports in the Soviet oiland gas industry.

The Department of Commerce data shownin table 45 indicate that U.S. oil and gasequipment trade with the U.S.S.R. nearlytripled between 1975 and 1979, from about$31 million to about $90 million. This growthhas been largely due to increases in the valueof computers and parts, drill rigs and parts,and pumps. The data also show that whilethe share of Soviet purchases of explorationequipment has declined slightly, that of drill-ing-related equipment has grown enormous-ly, largely at the expense of well completionand production items. This may partly re-flect a shift in Soviet emphasis away from

Ch. 6—Western Energy Equipment and Technology Trade With the U.S.S.R. ● 185

Figure 16.— U.S.S.R. Imports of Oil and Gas Equipment (million U.S. dollars)

1900-

1850-

1600-

1750-

1700-

1650-

1600-

1550.

1500-

1450-

1400-

1350-

1300-

1250-

12043-

1150-

1100-

1050-

1000-

950-

9oo -

850-

8oo-

750-

700-

650-

600-

550-

500-

450-

4oo-

350-

3oo -

Offshore!.’,6

,IWl%

197519761977 19781979 1975 19761977 1978 1979

SITC 735.92, 735.93 SITC 729.52,661.81/728.51

Oil and gas completion

250

200I

150i

Exploration Drilling

011 and gas pipelines

“u;

production‘(excluding pipe)

0250

F1Otttn

Lm

“

u

?80R-

%

,“.

Italy

—

Japan,

W . G e r .

—

,4:(

~—

Q

,*”.

—

w,

—

W. Ger.

—

—

*),..

=II.—

,,,,,

—

,,*,

—

! 0“

.,..

.

1975 1976 1977 19781979 1975 1976197719761979 1975 1976197719781979 1975197619771978 1979

SITC 714.3, 714.92. SITC 732.4 SITC 64293, 71921, 71922, SITC 678/6729861.91. 861.99 71923171237, 719.31

SOURCE United Nations SITC data

186 ● Technology and Soviet Energy Availability

Table 45.—U.S. Oil and Gas Equipment Trade With U.S.S.R. Relative Percentage ofEach Technology Area (thousand U.S. dollars)

1975 1976 1977 1978 1979

Total 30,818.0 68,418.8 33,882.8 59,652.7 89,741.0

ExplorationGeophysical . . . . . . . . . . . . . . . . . . . . . . . . 2,282.0

Computers & pts . . . . . . . . . . . . . . . . . . . 8,282.0

Total exploration . . . . . . . . . . . + . . . . . . . . . . 10,569.8

Percent of total . . . . . . . . . . . . . . . . . . . . . . . 3 4 %

Pipe . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —

Bits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 219,9

Rigs and pts . . . . . . . . . . . . . . . . . . . . . . . 1,477.0

Total drilling . . . . . . . . . . . . . . . . . . . . . . . . . 1,696.9

Percent of total . . . . . . . . . . . . . . . . . . . . . . 5%

Well completion/production . . . . . . . . . . . . . . . . . . . . . . . . .

Pumps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11,657.4

Pump parts . . . . . . . . . . . . . . . . . . . . . . . . . 5,928.8

Gas compressors . . . . . . . . . . . . . . . . . . . 765.3

Oil and gas sep. . . . . . . . . . . . . . . . . . . . . . 199.8

Total comp/prod . . . . . . . . . . . . . . . . . . . . . . 18,551.3

Percent of total . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60%

983.1

16,215.0

17,198.1

25%

2,821.0

—

6,513.0

9,334.0

13.6%

22,220.1

8,235.6

10,445.6

685.4

41,886.7

61%

480.7

3,643.4

4,124.1

12.2%

1.9

147.2

8,272.0

8,421.1

24.8%

3,674.3

11,743,9

5,432.3

487.1

21,337.6

63%

862.5

17,578.3

18,440.8

31%

404.7

—

33,247.9

33,652.6

56.4%

1,241.9

242.9

5,937.8

136.7

7,559.3

12.7%

SOURCE Department of Commerce

the use of U.S. electric submersible pumps infavor of gaslift techniques that are availablefrom non-U.S. sources (see below).

According to these data, the UnitedStates captured only 3.3 percent of the 1979estimated Western sales in the oil and gassector reported in table 42 above. It must benoted, however, that the Department ofCommerce statistics underrepresent the fullvalue of the U.S. equipment and technologypurchased by the U.S.S.R. For instance,neither SITC nor DOC trade statistics showany U.S. contributions in the area of offshoreequipment. Yet, a recent survey of Sovietoffshore rigs revealed drilling equipment of

2,022,6

22,311.0

24,333.6

27%

579.2

—

37,235.3

37,814.5

42%

9,979.7

17,613.2

—

—

27,592,9

30,7%

U.S. origin.” This apparent contradictionmay be attributed to the fact that althoughthe U.S.S.R. has purchased its rigs fromother nations, these suppliers themselveshave imported U.S. drilling equipment for in-stallation on the rigs. The U.S. sale will ap-pear as an export to the third country.19

Similarly, although U.S. statistics show nosales in the area of refining, U.S. firms areknown to have supplied engineering andtechnical services to West European andJapanese companies engaged in the con-——

18 1980-81 Directory of Marine Drilling Rigs, pp. 19-172.“American technology reexported from third countries is

still subject to U.S. export control laws.

Ch. 6— Western Energy Equipment and Technology Trade With the U.S.S.R. • 187

struction of petroleum refineries in theU . S . S . R . 20 These t rans fers o f know-how–like the sale of the Dresser drill bit plant–are not recorded in Schedule B/E data andare thus not reflected in table 45 or figure 17.

These data problems limit the precision ofany conclusions that can be drawn fromWestern export statistics. Nonetheless,some generalizations about Western exportsto the U.S.S.R. in a number of oil and gas in-dustry sectors are possible.

ExplorationMost of the exploration equipment ex-

ported to the U.S.S.R. has consisted of com-puters and geophysical equipment. Figure18, for instance, illustrates Soviet purchasesof automated data processing equipmentfrom selected Western countries. This figureshows that the primary exporters of this ex-ploration-related computer equipment werethe United States, France, and West Ger-many. Through 1978, the United Statestended to supply the majority of the hard--—

20 Soviet Business and Trade, Jan. 1, 1979

Figure 17.— U.S. Oil and Gas Equipment Trade WithU.S.S.R. by Technology Area

100r

1 1 1 I I I1975 1976 1977 1978 1979 1980

ware and the French to specialize in soft-ware.21 The post-1978 decline in such exportsmay be due to tighter multilateral exportcontrols on computers, or to improvementsin the Soviet hardware base.

The Control Data Corp. (CDC) has been byfar the leading exporter of American com-puters capable of processing the large quan-tities of data associated with seismic survey-ing. In recent years, CDC has sold threeCyber 172s and a Cyber 73 to various Sovietministries engaged in seismic exploration.IBM has also sold two S/370-148 computersfor geophysical applications. AnotherAmerican firm, Geosource, Inc. of Houston,had by 1979 sold 13 Command II field proc-essing systems that are used to preprocessseismic data in the field.22 This sale alone,valued at $6 million, accounted for nearly 30percent of total U.S. sales of computers andcomputer parts in 1979. The French firmsFerney-Voltaire and CIE Generale Geo-physique (CGG) have provided the majorityof the specialized software used with theCDC computers. 23

The United States and France are also theU.S.S.R.’s leading Western suppliers ofgeophysical equipment. NIMEXE and DOCd a t a s h o w t h a t b e t w e e n 1 9 7 5 a n d 1 9 7 9French sales in this area have increased,while those from the United States havebeen erratic, ranging from as high as $2.2million to as low as $480,000. CGG was amajor supplier of geophysical equipment, in1976 alone selling to the U.S.S.R. $14 millionworth of digital seismographic recorders,magnetometers, gravity meters, and hydro-phones. The equipment was used to equiptwo geophysical ships that were built for theSoviet Union by Mitsubishi of Japan.24

Geosource is the largest American sup-plier of geophysical equipment, and it soldapproximately $30 million worth of equip-ment to the U .S .S .R . be tween 1975 and

SOURCE Table 45

2 1Soviet Business andi Trade, Apr. 11, 1979.22 Ibid,23 Ibid., and Mar. 18, 1979.24 Soviet Business and Trade, Sept. 29, 1976.

188 . Technology and Soviet Energy Availability

70

60

50

40

30

20

10

0

Figure 18.— Western Energy Trade With U.S.S.R. Automated Data Processing Equipment

;

Switzerland ,

I l l

Sweden ~ .

The Nethariands

Canada

I

L

1975 1976

SOURCE United Nations SITC Data

1979.25 Geosource has supplied the U.S.S.R.with a wide array of geophysical prospectingequipment, including 13 photodot auto-mated digital display systems that are usedin conjunction with the Command I I system.

DrillingThe major Soviet imports in this area have

been drill pipe and casing. Soviet imports ofdrill pipe and casing have come predom-inantly from Japan, West Germany, France,and Italy. Within these countries, importantsuppliers have been Mannesmann (WestGermany); Vallourec (France); and Finsider(Italy). The U.S.S.R. has also sporadicallypurchased packers, mud additives, power

1977 1978 1979

Year

tongs, and heavy drilling equipment fromthe West. The Soviets have purchased anumber of packers from both Technip inF r a n c e a n d L y n e s International in theUnited States. 26

U.S. exports of drill pipe and casing to theU.S.S.R. totaled less than $1 million over thelast 3 years. These relatively low levels are atleast partially due to a rapid increase in U.S.drilling activity, which caused U.S. demandfor drill pipe and casing to exceed domesticsupply. The American shortfall has largelybeen made up with pipe and casing importedfrom Japan. The majority of U.S. drilling-related exports to the U.S.S.R. are drillingrigs and parts for drilling rigs. While the

25 Soviet Business and Trade, Feb. 14, 1979.

Ch.. 6— Western Energy Equipment and Technology Trade With the U.S.S.R. ● 189

United States has not been a major supplierof complete rigs–-approximately 12 U.S. rigshave been sold to the Soviet Union over thelast 10 years–the Soviets are purchasingU.S. drilling rig parts in significant dollarvalues.

U.S. firms account for most of the non-Communist world’s production of drill bits,and U.S. bits are of significantly higherquality than Soviet counterparts. The So-viets, however, have purchased fewer than100 U.S. drill bits over the last 5 years. In-stead they have opted to purchase the de-sign and equipment for a drill bit plant fromDresser Industries. Nor have drill bit im-ports from Western Europe been large. TheNIMEXE system classifies drill bits intoboth bits made of base metal and metal car-bide. EEC exports of both types have beeninconsequential.

Well Completion/ProductionFigure 19 shows a steady growth in Soviet

imports of pumps for liquids. The leading ex-porters of these items have been France,West Germany, and the United States.While it is not clear that West German andFrench pumps are used in the production ofoil and gas, Schedule B/E data show thatalmost all of the U.S. trade is in oil well andoilfield pumps. This is confirmed by articlesin Soviet Business and Trade that indicatethat U.S. companies such as TRW-Reda,Centrilift, and Oil Dynamics have been ma-jor exporters of electric submersible pumpsfor Soviet oilfields.

Finally, Western trade activity in pipehandlers and gas lift equipment was not as-certainable from the trade data due to prob-lems of aggregation. It was apparent from

Figure 19.— Western Energy Trade With U.S.S.R. Pumps for Liquids

140

120

100

80

60

40

20

0

.

. United States

.

France

}-

West Germany

1975 1976 1977 1978 1979

Year

SOURCE United Nat Ions SITC D a t a

190 • Technology and Soviet Energy Availability

articles in Soviet Business and Trade,however, that these items have been ex-ported to the Soviets by the United States,Japan, and France: gas lift equipment pre-dominantly by the French, and pipelayersprimarily by the United States and Japan.Technip of France has sold gas lift equip-ment for over 2,000 wells. Pipelayers havebeen sold to the U.S.S.R. by Caterpillar andInternational Harvester in the United Statesand Komatsu in Japan.

The Soviet Union has made sporadic pur-chases of enhanced recovery equipment andtechnology. Among the transactions thathave appeared in Soviet Business and Tradehave been the sale of two carbon dioxide(co 2) plants by Borsig of West Germany,two surfactant plants by Pressindustria ofItaly, a surfactant plant as well as chemicalsfrom Sanyo Chemical Industries of Japan,and an alpha-olefin plant from Davy Inter-national in Great Britain.27

Transportation

The most important commodities in thissector have been large diameter pipe and gaspipeline compressor stations. SITC codes678 and 672.9 contain a number of subcate-gories and cover a wide variety of tubes andpipes. Figure 16 shows that in each category,Japan, West Germany, and France are themajor Soviet suppliers, and the UnitedStates is by far the smallest. In the categoryof tubes, pipes, and fittings of iron and steel,for instance, 1979 Japanese exports wereworth approximately $0.75 billion and WestGermany’s over $0.5 billion, while U.S. salesamounted to a little over $1 million. Some ofthis pipe may have been used in the nuclearindustry, but it is probably safe to assumethat a large portion of it went to the oil andgas sector. The principal companies supply-ing the pipe are Sumitomo (Japan), Mannes-mann (West Germany), Vallourec (France),and Finsider (Italy). The United States does

“Soviet Business and Trade, Aug. 15, 1979.

not produce the 56-inch diameter pipe thatthe Soviets use to construct gas pipelines.28

Compressor stations for gas pipelines areanother active commodity. The largest ex-porters of compressor stations to theU.S.S.R. have been Italy, West Germany,and the United States, with Nuovo Pignoneof Italy and GE of the United States themajor suppliers.29

Refining

The U.S.S.R. has purchased refineries andrefinery equipment from Japan, Italy, andFrance, the tendency being to import entirerefineries rather than component parts. Theprimary contribution of the United States inthis area has been through Fluor Corp.,which provided design and engineering serv-ices to Italian and Japanese constructionfirms. 30

Offshore

Trade in this area has consisted primarilyof sales of offshore drilling rigs and auxiliaryvessels and equipment, and the principalsuppliers have been Japan and the Nether-lands. 31 Rauma-Repola Oy of Finland wasrecently granted a contract to build threedynamically positioned drill ships for theSoviet Union, to be delivered in 1981 and1982. The United States has supplied aux-iliary equipment for rigs sold to the Soviets,but Soviet purchases in this area have beenboth moderate and sporadic.32

Conclusions

Examination of trade data reveals thatthe U.S.S.R. has been very selective in thekinds of Western equipment and technologyit has purchased to supplement its domestic

28 Interview with J. 13rougher, Bureau of East-W’est Af-fairs, Department of Commerce.

“’.SO[ !iet Business and Trade, Nov. 10, 1976.‘(’Sot’iet Business and Trade, Jan. 31, 1979.“So[’iet Z?usines.s and Trade, July 15, 1980; May 21, 1980.“1980-81 Directory of Marine Drilling Rigs, pp. 19-172.

Ch. 6— Western Energy Equipment and Technology Trade With the U.S.S.R, . 191

oil and gas equipment. Indeed, the relativelymodest imports of may items lead one tosuspect that the U.S.S.R. has been sup-plementing domestic equipment stocks attimes of peak demand and/or purchasing thebest available product for particularly dif-ficult application. It is equally probable thatsome items have been procured for labor-atory examination and duplication, or toserve as guides to correct specific prob-lems. 33 The most prominent exception hereis Soviet imports of Japanese and WestEuropean large diameter pipe, which havebeen consistently large and which seem to berequired because of insufficient domesticproduction capacity.

Interestingly, the U.S.S.R. has not pur-chased many items basic to the petroleum in-dustry. These include magnetometers, gravi-meters, mud-pumps, drilling mud, casingcement, engines, pipe insulation, separationequipment, and offshore floating productionplatforms. These omissions or gaps in tradewith Western countries can be interpreted ina number of ways: that the U.S.S.R. and itsCMEA partners have an adequate industrialbase to supply their needs, even if the resultis inefficient by Western standards; that in-sufficient hard currency has forced priority-setting among Western imports; or that theU.S.S.R. has made a policy decision to be asindependent as possible of supplies from theWestern countries in certain critical seg-ments of the oil and gas industries. It ismost likely that a combination of such fac-tors is at work.

Be that as it may, the following gener-alizations seem warranted by the data:

• In value terms, by far the largest Sovietpurchases from the West have been inthe area of iron or steel seamless pipesand tubes (including the large diameterpipe used in Soviet oil and gas lines).Purchases in this area from the United

33 There is substantial evidence of duplication. 1 n an inter-

view with OTA, a Vice President of TRW-Reda Pump, Inc.,asserted that when one of his technicians toured a Sovietpump plant in 1979, he saw 20-year-old Reda models beingproduced.

States have been negligible. By far thelargest suppliers have been Japan andWest Germany.The U.S.S.R. has also purchased sub-stantial amounts of various pumps andgas compression equipment. Here, theUnited States has had larger marketshares. The U.S.S.R. has made only afew large purchases in the area of lightvessels, floating docks, etc., which in-cludes offshore drilling rigs. None of thevessels themselves have come from theUnited States. In 1979, Japan andSweden were the only large exporters inthis category.The U.S.S.R. has purchased very fewdrill bits from the West, apparently pre-ferring to acquire its own additionalmanufacturing capacity in the form ofan entire plant.

FOREIGN AVAILABILITY OF OILAND GAS INDUSTRY EQUIPMENT

AND TECHNOLOGY34

Much oil and gas technology originated inthe United States, but that technology haslost its American identity over the yearsthrough licensed production, wholly ownedsubsidiaries overseas, and employment ofU.S. commodities and expertise worldwide.Other sophisticated technology was devel-oped elsewhere. For example, Schlumbergerof France first developed electric well log-

34 This section is based on trade journals, industry cata-logues. Sov ie t Bus iness and Trade, T h e C o m p o s i t e C a t a l o g u e

of Oil Field Equipmcnt and Services (Houston, Tex.: GulfPublishing Co., 1980), and inter~.iews with representati~res ofthe following firms: Gulf Oil Exploration & Production CO.,(ieosource, Inc. , Dresser Industr ies , BW”T M’orld T r a d e ,Cameron Iron Works, Inc., Hughes Tool Co., TRW-Redapump, Inc., Brown & Root, Inc., and Williams Bros. Engi-neering Co. Representatives of these firms provided candid,forthright observations of their past deal ings with theU. S. S. R., insight gained during country visits and an ap-praisal of their foreign competitors. These visits, coupledwith the other reported U.S.S.R./Western trade deals, pro-vided a basis on which to judge the availability of Western oiland gas technology. While these sources could not providecomplete identification of all possible suppliers, OTA believesthat it was acquainted with the most significant suppliersand the strongest competitors to U.S. firms.

192 • Technology and Soviet Energy Availability

ging equipment that is recognized today asthe world’s standard. Likewise, the steel in-dustries in Western Europe and Japan gen-erally produce products that are as good as,if not better than, those available from theUnited States–and at lower prices. Tech-nological leads are perishable with time.Licensed manufacturers frequently improveupon designs or manufacturing processesbased on local conditions and equipment.Wherever the original development workand design may have been done, ideas soonbecome general knowledge. The followingsections discuss the foreign availability ofenergy technology that would be useful tothe U.S.S.R. in the various phases of oil andgas production and delivery.

Exploration

As noted above, the American firm Geo-source has been very active in Soviet trade.Sercel of France has been a strong com-

petitor to Geosource for sales of field datacollection and preprocessing centers. Table46 compares basic parameters of Geosource,Texas Instruments (another U.S. firm), andSercel products used in seismic work. Thetable shows that the equipment, althoughnot identical, is similar.

Table 47 identifies the major items ofseismic surveying equipment and suppliersaround the world. Most items are producedby firms in Western Europe and Japan, andmany are available in the Eastern Bloc,although the quality of the latter is ques-tionable and Western equipment tends to bemore advanced. The United States may leadtechnically in one or two items, but thegeneral consensus is that products fromSercel, for example, are capable of perform-ing similar functions. On the other hand,only the United States is able to supply thefull range of equipment.

Table 46.—Comparison of U.S. and French Seismic Equipment

Geosource MDS-10 Texas Instruments DFSV Sercel 338 B

Data Sample Packing Data Auxiliary Samplechannels Interval (MS) density channels channels rates

24 ½ 1,600 SEG-B 24 Channels @ 1, 2, 4 msData 24 1 800 or 1,600a To 24 4 1, 2 or 4 ms

24 2 800 or 1,600a 28 2 1, 2 or 4 ms24 4 800

Channels 48 1 1,600 48 4 1b, 2 or 4 ms 48 Channels @ 2, 4 ms48 2 800 or 1,600a 60 2 2 or 4 ms48 4 800 or 1,600a 96 4 2 or 4 ms96 2 1,600 120 4 2 or 4 ms96 4 800 or 1,600a 240 4 4 ms

Solid state stacking available at Packing density 800 or 1,600 bpiall sample rates except (1) 1,600 bpi only.

Packing density 1,600 1,600maximumBPI

Number of bits 14 bits plus sign bit 14 bits plus sign bit4 bit gain word 3 bit gain word

Frequency 2 to 1,000 Hz 3 to 256 Hzresponse

Distortion 0.1 0/0 maximum @ 0.050/00.53V RMS input

Tape speed Unknown 10 to 120 ipsrange

—

96 Channels @ 4 ms

1,6006,250 for 338lR(IBM recorder)

14 bits plus sign bit

Unknown

Less than 0.1 0/0 @.05V input

20 to 92 ips

a800 BPI NRZI optionalb 1 ms at extra cost to 56 channels

SOURCE Office of Technology Assessment

Ch. 6— Western Energy Equipment and Technology Trade With the U.S.S.R, ● 193

Table 47.—Manufacture of Seismic Equipment by Country

Vibrator

Vibrator control

Shooter explosive

Recorder field

Tape transport

Camera CRT

Cables

Connector

Geophone

Airgun (marine)

Marine streamer

Marine positioning

Seismic computer

Array transformprocessor

Plotter

,

xxx

x

xxxxxxxx

x

xx

NOTE No Inferences as to quality or comparability can be made from

SOURCE Off Ice of Technology Assessment

Seismic survey data must ultimately beprocessed by large mainframe, third genera-tion computers with floating point and arrayprocessors. The United States has approvedthe sale of six large computers, with some-what restricted array processors, for use inthe major hydrocarbon producing regions inthe U.S.S.R. Two French firms, Ferney -Voltaire and CGG, are known to have sup-plied sophisticated geophysical software( c o m p u t e r p r o g r a m s ) used on the U .S .machines to analyze seismic survey results.An IBM sale included American software.

In sum, the equipment to perform seismicsurveys and record seismic data are gener-ally available worldwide. U.S. firms areunique, however, in being able to providesystems displaying the full range of equip-ment and know-how. U.S. firms also lead inthe accuracy of some equipment; and theUnited States has a substantial lead in com-puters that process the seismic data. Soviet

this table which merely shows the existence of commercial manufacturers

capabilities in this area are generally 5 to 15years behind the West and purchases of suchequipment would certainly enhance theU.S.S.R.’s seismic work. The degree towhich this would necessarily lead to increas-ed oil production in the present decade isunclear, however.

Drilling

The U.S.S.R. has purchased 15 portabledrilling rigs from Tamrock Oy of Finland.Canadian sales of $12 million to $32 millioneach year between 1975 and 1979 were prob-ably also portable rigs, which are known tobe produced by the Canadian firm Foremost.Mobile equipment capable of drilling to20,000 ft is also available from Romania,although it may not perform to advertisedspecifications.

The U.S.S.R. has imported drill pipe al-most entirely from firms in Western Europe

194 ● Technology and Soviet Energy Availability

and Japan. Prominent suppliers have beenVallourec and Creusôt-Loire of France; Man-nesmann of West Germany; Italsider andEFIM of Italy; and Mitsubishi, Mitsui,Sumitomo, Japan Steel Works, and NipponKokan of Japan. Japanese pipe is generallyconsidered to be equal to, if not better than,U.S. pipe and is available at a significantlylower price. It is manufactured by the latestmethods including inertial welding of thetool joints on the ends of the pipe, and U.S.drillers are buying Japanese pipe to supple-ment U.S. production capacity.

The United States is the predominant pro-ducer of drill bits in the West, with theAmerican firms Hughes, Dresser, Smith,and Reed supplying the vast majority of bitsused outside the Communist world. Thesefirms produce the greatest diversity of high-quality bit types for varying undergroundrock strata. A few diamond bits and core bitsare produced by Diament-Boart of Belgiumand Tsukimoto Seiki in France, but thesecannot substitute directly for rock drill bits.While Tsukimoto produces both diamondand metal bits, its total annual production isvery small, approximately 5,000 bits. Euro-pean bits have a more limited operatingcapability than their U.S. counterparts andtheir quality does not match U.S. standards.Creusôt-Loire, SMF Division of France, hasrecently been purchased by Hughes Tool Co.and the drill bit plant is being modernized toU.S. standards.

The Soviet Union is itself a prodigous pro-ducer of drill bits, and it has not purchasedWestern bits in large quantities. A greatdeal of publicity has accompanied the sale byDresser Industries of a tungsen carbide jour-nal bearing drill bit plant to the U. S. S. R., thecapabilities of which are discussed in chapter2. The export license for this plant wasrecently revoked, but all the technologyrelating to production machinery, manufac-turing processes and metallurgical specifica-tions has already been transferred. Therevocation mainly prohibits Dresser fromproviding onsite training of Soviet tech-nicians once the manufacturing plant is com-