Embed Size (px)

Citation preview

Journal of Agricultural and Resource Economics, 19(2): 425-445Copyright 1994 Western Agricultural Economics Association

What Do We Know About Decision Making UnderRisk and Where Do We Go from Here?

David E. Buschena and David Zilberman

This article reviews two major approaches used in the past for risk analysis-the expected utility approach and the use of safety rules-and endeavors toreconcile their applicability and use in light of the recent nonexpected utilityrisk literature and work using the mean-Gini coefficient for risk analysis. Thisleads to the identification of several "reduced form" hypotheses that hold undera variety of theoretical structures and to a discussion of some empirical evidenceregarding these hypotheses. The major lesson of recent research of individualbehavior under risk is that it is not always consistent with the expected utilityapproach; in short, there is no generic model for evaluating behavior underrisk.

Key words: expected utility, multiattribute utility, safety rules.

Introduction

Promoting an understanding of the effects that considerations of risk have on the choicesof economic agents, as well as the development of effective tools to address decisionmaking under risk, have been major objectives of economic research over the last 60years. While these issues have been given much effort and have been the foci of majorresearch literature, researchers still are confused and unsure about modeling risk. Aseconomists, we have made much progress-both in our understanding and measurementof human reactions to risk and in the development of mechanisms and policies to addressit. Although much of this progress has hinged on the expected utility (EU) hypothesis,recent developments have shown its limitations and call for more understanding andreassessment of our methodologies. This reassessment is of particular significance toagricultural and natural resource economists who recognize the importance of accuratemodeling of risk effects on decision making and have a comparative advantage in un-derstanding, modeling, and testing hypothesized behavior. As we prepare for these efforts,it is worthwhile to take stock and identify what we have learned and accomplished aboutbehavior under risk, how we can apply this knowledge effectively, and how it can be usedto develop better understanding of risky choices.

This article is an attempt at this overview and assessment. Two major approaches usedin the past for risk analysis are reviewed-the EU approach and the use of safety rules-and we endeavor to reconcile their applicability and use in light of the recent non-EUrisk literature and the literature on the use of the mean-Gini coefficient for risk analysis.This leads to the identification of several "reduced form" hypotheses that hold under avariety of theoretical structures and to a discussion of some empirical evidence in view

The authors are assistant professor, Department of Agricultural Economics and Economics, Montana StateUniversity, and professor, Department of Agricultural and Resource Economics, University of California atBerkeley, respectively.

Support is acknowledged from the Montana Agricultural Experiment Station, Montana State University,Bozeman, under Project No. 101088 (Journal Series No. J-2994). For reprint identification purposes only, thisis Giannini Foundation Paper No. 1103, University of California at Berkeley. Some of the research leading tothis paper was supported by the Environmental Protection Agency.

425

Journal of Agricultural and Resource Economics

of these hypotheses. We conclude that, in spite of the conceptual confusion, we haveidentified several "down-to-earth" relationships that allow for prediction and give modelselection guidelines for choices under risky conditions.'

Behavioral Models of Choice Under Risk

Before the development of the von Neumann-Morgenstern EU models, economists andmanagement scientists developed simple tools to incorporate considerations of risk ineconomic decision models. The rigorous justification for this framework is not alwaysclear; these tools are ad hoc in their nature. Still, they reflect formal presentations ofbehavioral rules that their developers deemed to be reasonable for choice under risk. Theyare also practical in their computational and data requirements. Simon's notions of"bounded rationality" for decision makers may explain the introduction and appeal ofthis set of "behavioral" approaches.

Keynes introduces such a behavior rule in his analysis of investment under risk. Hesuggests that the discount rate is adjusted for the risk level and degree of risk aversionwhen analyzing risky choices. The greater the level of risk aversion, the greater is the "riskpremium." Although Keynes does not present a formal model to elaborate this practicalnotion, this idea has had substantial impact on the development of models of capitalformation. This approach has become a standard tool in macroeconomics and in finance.For example, Feder and Just apply this approach to evaluate riskiness of investment indifferent countries by comparing the interest rates charged for loans in these countries.

Another set of behavioral approaches for risk modeling is represented by the safety-rule models. Safety rules are based on the idea that decision makers are concerned withavoiding unfavorable outcomes such as bankruptcy or starvation. The nature of thisconcern can be viewed by considering utility functions, u(ir, d), that include a continuousvariable for wealth increases (7r) plus a discrete element (d). In these safety-rule models,7r represents profit (or income), d* is some critical level of profit, a is some criticalprobability level associated with d*, and P(x) denotes the probability of occurrence forevent x. For example, d could reflect financial criteria where solvency occurs if r >- d*,and insolvency occurs if ir < d*. While safety rules have not been used in many studiesof behavior under risk, they are important models for the evaluation of behavior underpotential crisis outcomes. There are three primary forms for safety rules: (a) Roy's safety-first rule-minimize P(ir < d*); (b) Telser's safety-fixed rule-maximize E(ir) subject toP(ir < d*) < a; and (c) Katoka's safety rule-maximize d* subject to P(-r < d*) < a.

Both Telser's and Katoka's models are parallel to the use of classical statistics. Telser'smodel uses the notion of a significance level (a) for controlling the likelihood of a type Ierror in much the same way that this likelihood is controlled by using the standardhypothesis-testing procedure of classical statistics. Katoka's model is a mini-max model;it chooses the distribution that has the highest value in the event of a crisis outcome,where the likelihood of this outcome is fixed. The prevalence of use of the hypothesis-testing procedure can serve as witness to the appeal of safety rules for decision makingunder risk.

The significance levels (a) used by decision makers whose decisions follow either theTelser or the Katoka models serve as measures of their aversion to risk. Note that, withboth models, when returns are normally distributed,2 these decision criteria are in essenceequivalent to maximizing a linear combination of mean and variance of profits (or income),but distributions outside of the normal also may satisfy this model. The standard deviationcoefficient is negative and increases in absolute value as the decision maker becomes morerisk averse; this coefficient is zero if the standard deviation is low enough. While safetyrules are ad hoc decision rules, they (or some variant of them) may be followed by largenumbers of the population, justifying them as "positive" models (Bitros and Kelljian;Moscardi and de Janvry; Collins, Musser, and Mason; Patrick et al.)

426 December 1994

Review of Risk Models 427

Expected Utility: General Discussion

The EU approach has been the mainstay of the analysis of behavior under risk for thelast 40 years. Two major lines of research establish the prominence of this approach, oneproviding normative justification of EU and another extending EU for positive analysis.Von Neumann and Morgenstern are the major contributors to a large body of work thatprovides normative justification for the use of EU by rational decision makers. Here, wediscuss the EU model in general, its extensions, and problems with its implementation.A more detailed discussion of these concepts is given in following sections. The EU modelviews decision making under risk as a choice between alternatives, usually consisting ofa vector of outcomes, x (representing income or wealth levels), with a correspondingprobability vector, p. The dimensions of x and p are n for this discrete case.3 Decisionmakers are assumed to have a preference ordering defined over the probability distri-butions for which a number of axioms hold (Jensen; Fishburn 1983).4 Risky alternativescan be evaluated under these assumptions using the EU preference function, u(xi), onoutcomes giving the summary measure, 2 u(xi)pi, which is linear in probabilities but notnecessarily linear in outcomes. The utility function u(xi) usually is assumed to be concave,implying risk aversion.

Uses of Expected Utility

Several studies have contributed to the emergence of the EU approach as a major tool ofpositive analysis, i.e., an approach to explain actual behavior of farmers. Friedman andSavage demonstrate its usefulness for explaining diversifying behavior and seeminglyparadoxical phenomena (e.g., when people both hold insurance and gamble) through ageneral functional form of the u(xi) representation; they also introduce basic notions suchas certainty equivalents and risk premiums. Tobin relies on Friedman and Savage's workto develop a major literature on portfolio analysis, while Arrow (1958, 1974) establishesbasic notions and concepts associated with the emergence of insurance contracts (e.g.,moral hazard). Furthermore, Arrow (1958, 1974) and Pratt (1964) introduce basic conceptsfor risk attitude measurement (measures of absolute and relative risk aversion). Rothschildand Stiglitz (and others) develop theoretical foundations to quantify and measure risk.Sandmo presents an analytical framework for analyzing producers' choices under risk anduses it to explain decreases in production and supply associated with the existence of riskyprices.

Criticisms of the Expected Utility Approach

In spite of the major achievements toward providing an understanding of choices underrisk that have been made with the EU approach, experiments have revealed notablelimitations in this approach. Situations have been identified where choices are contraryto the predictions of the EU model. Expansion of the range of applications for riskydecisions has identified important elements that often are not commonly considered inrisk analysis using the EU model. The EU approach provides only a partial explanationof choices under risk; the stage is set for new, more general, and realistic approaches toaugment the EU model.

The first problem with the EU approach as a descriptive model is that it representsrational choices, i.e., not taking into account the impacts of anxieties and worry associatedwith random outcomes or choices, or the effort and expertise needed for optimal selection.The EU literature refers to individuals who have concave utility functions as risk averse,whereas on the surface this phrase seems to suggest the person experiences disutility fromrisk. Von Neumann and Morgenstern recognize that these "psychological" factors of fearof risk may be present, but abstract from these factors to give an objective model ofbehavior (Harsanyi). Technically, however, the term only implies a decreasing marginal

Buschena and Zilberman

Journal of Agricultural and Resource Economics

utility of income. 5 The EU model also assumes that agents can and will completelyoptimize their choices, regardless of the importance and difficulty of the decision.

When risk exists, the correct choice criteria of individuals who do not suffer from fearsor anxieties, or from limits or costs of decisions, should be to maximize EU. Thus, theEU model seems to be a useful normative model since it determines choices under riskignoring the effects of "irrational" factors such as fear and anxiety and the cost of makingthe decision. However, it may not always be a good model for assessing actual behavioralpatterns when anxiety or decision costs may affect choices under risk. Development ofmore realistic models that incorporate these factors will require interdisciplinary effortsand inputs, especially those of psychologists.

A second problem with the EU approach as it is commonly used is its failure to includeelements other than income in the utility function. In particular, there is a lack of con-sideration of discrete variables that (a) have a strong impact on the quality of life, (b)may be affected by the randomness of income, and (c) consequently have a strong impacton risky decision making. For example, a farmer's utility from a certain income level maybe quite different in situations depending on whether he/she is solvent or not; the potentialfor bankruptcy has a substantial impact on choices, but it is not regularly incorporatedinto standard EU models.

The Expected Utility Theory

Standard EU theory has progressed along two paths: (a) the normative axiomatic approachfor behavior under risk based on game theory, and (b) the positive approach using summarymeasures based on some general properties of utility functions. This section reviews thestatus of the EU approach along these two paths.

Normative Approach

The initial normative approach to behavior under risk was set forth by early probabilitytheorists using simple expected value maximization. Let xi be the outcome and p(x,)denote the probability of outcome xi, where i = 1, ... , n. Then consider:

n

(1) E(x, p) = xp(xi).i--

Both Cramer and Bernoulli recognize that utility is not necessarily linear in wealth, leadingto the use of v(-), a cardinal utility measure on wealth in the maximization of the followingsummation:

n

(2) EU(x, p) = v(wi)p(Wi),i=-

or, alternatively,n

EU(x, p) v(wo + x,)p(x).

For the model in equation (2), wi is the final wealth under state i, w0 is the initial wealth,and xi is the new income under state i. The assumption of the existence of a cardinalutility function, v(.), is now considered too strong for the evaluation of decisions underrisk.

Von Neumann and Morgenstern develop a preference representation on risky choicesdefined by outcomes and probabilities and show that, if certain conditions are met, thesepreferences are consistent with maximization of EU as presented in equation (2), butwhere v(-) is replaced by a representation u(-). This cardinal representation u(-) is de-

428 December 1994

Review of Risk Models 429

veloped from ordinal choices and is unique only up to an affine transformation. A re-finement of the von Neumann and Morgenstern arguments is presented in the appendix.These conditions require that the preferences on risky alternatives are continuous, welldefined on the feasible set of outcomes, and independent. Independence means that choicesdepend only on differences between alternatives, regardless of their common features.These assumptions imply that the same preferences can be presented by utility functionsthat are unique up to an affine transformation.

Refinements of Expected Utility for Applications

To make EU operational for empirical work evaluating specific choices, the frameworkhas to be well defined, and some basic measures of preference have to be established.Savage argues that EU is a useful tool with either objective or subjective probabilities.Friedman and Savage argue that the second derivative of the utility function determineswhether an individual is risk averse or risk loving. A decision maker is described as riskaverse for a particular income level x if u"(x) < 0, risk neutral around x if u"(x) = 0, andrisk preferring around x if u"(x) > 0, where u"(x) is the second derivative of u(.) withrespect to outcomes.

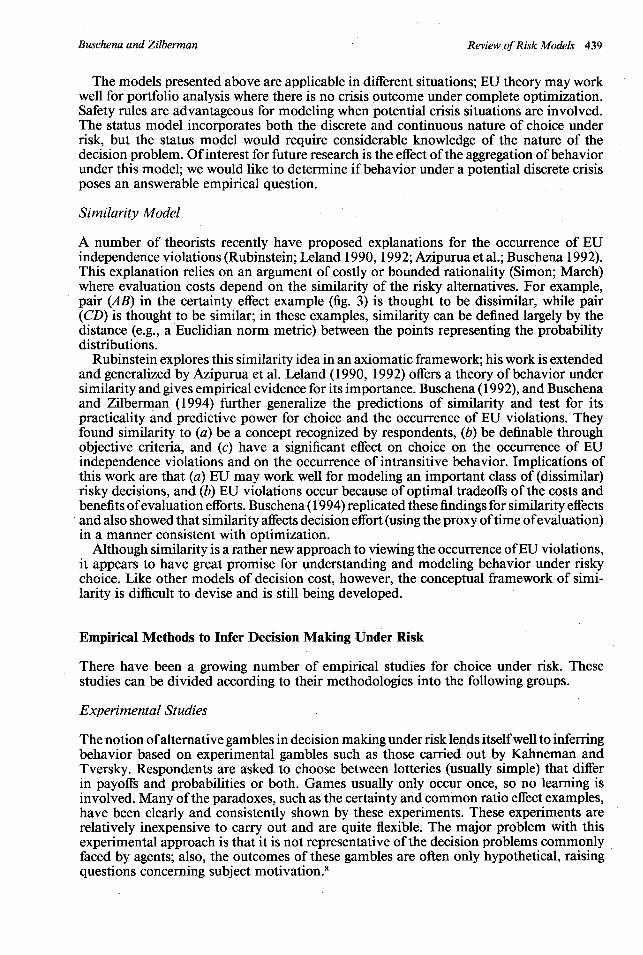

Certainty Equivalent and Risk Premium

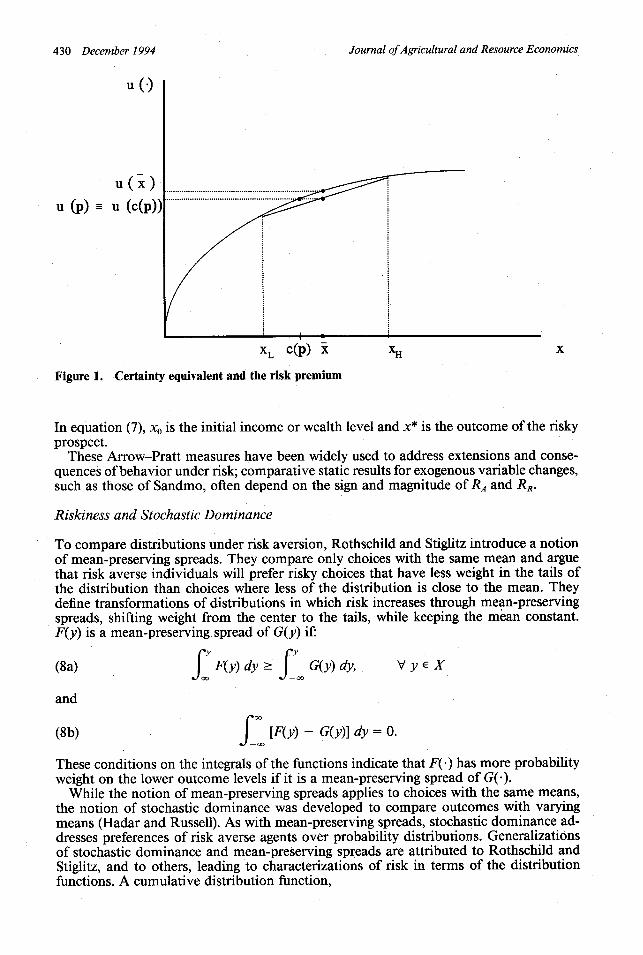

Under risk aversion, additional risk leads to utility losses. Two notions-certainty equiv-alent (CE) and risk premium-are useful in quantifying these losses. The certainty equiv-alent c(p) of a lottery with probability vector p over x is such that the agent is indifferentunder the EU framework between the lottery p or receiving the certainty equivalentoutcome c(p), given by the identity:

n

(3) u[c(p)] = u(x,)p(x).i=1

Let the expected value of a risky alternative from equation (1) be given as E(x, p) = ,giving the utility u(x). A risk premium 7r(p) is given as the difference between the expectedutility of the average u(x) and the certainty equivalent of a gamble:

(4) u() - c(p) = ir(p).This relationship is shown in figure 1 for a concave utility representation u(.). The agent

faces risky outcomes XL and XH, here each occurring with probabilities 1/2; i.e., (PL, Pn)= (1/2, 1/2). The agent is indifferent between the lottery and receiving the certaintyequivalent of the lottery, c(p), for sure; this relationship is shown by the equality of u(c(p))and u(p), the utility of the lottery.

Risk Aversion Measures

To develop simple indicators to allow comparisons of interpersonal preferences aboutrisk, Arrow (1974) and Pratt (1964) develop measures of risk aversion. These measuresare invariant to affine transformations of x, allowing unit-free discussion of risk attitudes.The measure of absolute risk aversion (RA) is given by:

(5) -u"(x)/u'(x).

A relative risk aversion measure (RR), which also can be thought of as an elasticity of riskaversion measure, is given by:

(6) -[u"(x)/u'(x)]x.

There is also a partial risk aversion measure (Rp):

Buschena and Zilberman

(7) - [u"(xo)/u'(xo~lx*.

Journal of Agricultural and Resource Economics

u ()

u(x)u (p) u (c(p))

U (P) = u (C(p))

...................................................................................... o..........

XL c(p) x XH X

Figure 1. Certainty equivalent and the risk premium

In equation (7), xO is the initial income or wealth level and x* is the outcome of the riskyprospect.

These Arrow-Pratt measures have been widely used to address extensions and conse-quences of behavior under risk; comparative static results for exogenous variable changes,such as those of Sandmo, often depend on the sign and magnitude of RA and RR.

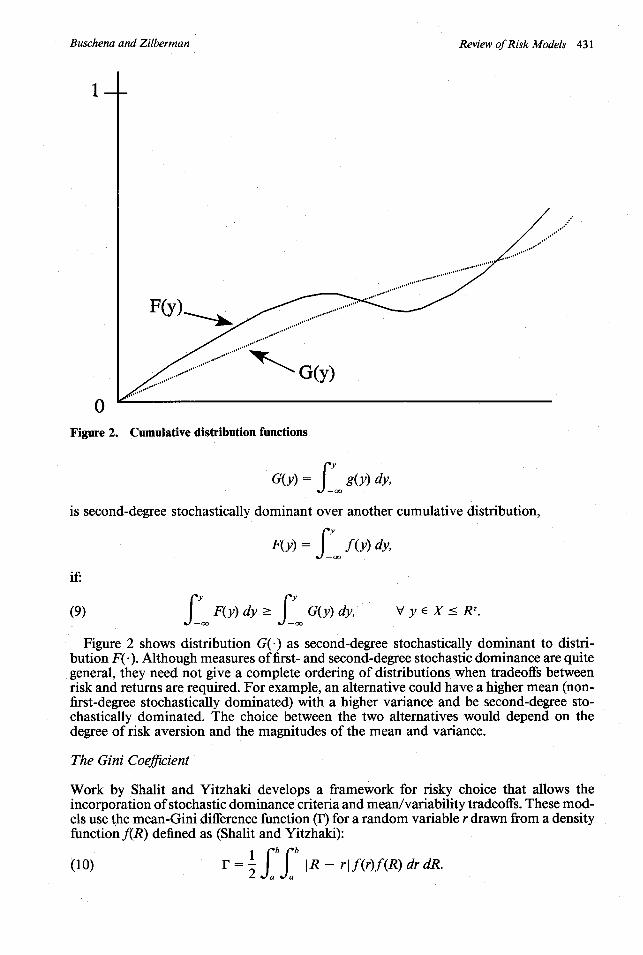

Riskiness and Stochastic Dominance

To compare distributions under risk aversion, Rothschild and Stiglitz introduce a notionof mean-preserving spreads. They compare only choices with the same mean and arguethat risk averse individuals will prefer risky choices that have less weight in the tails ofthe distribution than choices where less of the distribution is close to the mean. Theydefine transformations of distributions in which risk increases through mean-preservingspreads, shifting weight from the center to the tails, while keeping the mean constant.F(y) is a mean-preserving spread of G(y) if:

(8a) JF(y)dy f G(y) dy, V y E X

and

(8b) [F(y) - G(y)] dy = 0.-oo00

These conditions on the integrals of the functions indicate that F(.) has more probabilityweight on the lower outcome levels if it is a mean-preserving spread of G(.).

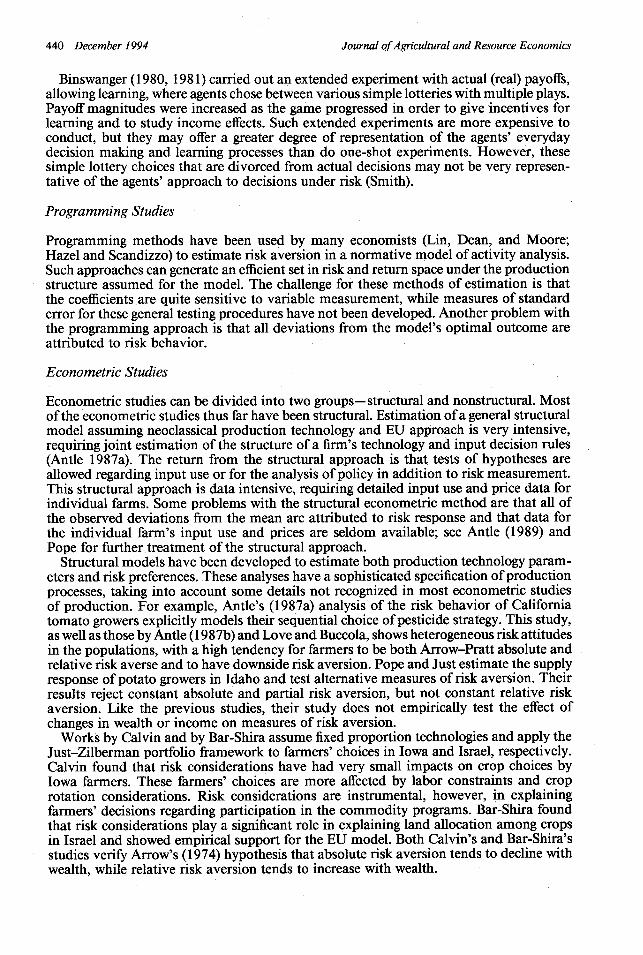

While the notion of mean-preserving spreads applies to choices with the same means,the notion of stochastic dominance was developed to compare outcomes with varyingmeans (Hadar and Russell). As with mean-preserving spreads, stochastic dominance ad-dresses preferences of risk averse agents over probability distributions. Generalizationsof stochastic dominance and mean-preserving spreads are attributed to Rothschild andStiglitz, and to others, leading to characterizations of risk in terms of the distributionfunctions. A cumulative distribution function,

430 December 1994

I I

i

Review of Risk Models 431

1

nU

Figure 2. Cumulative distribution functions

G(y)= g(y) dy,

is second-degree stochastically dominant over another cumulative distribution,

F(y) = f(y) dy,

if:

(9) F(y) dy J G(y) dy, V y E X Rt .

Figure 2 shows distribution G(.) as second-degree stochastically dominant to distri-bution F(-). Although measures of first- and second-degree stochastic dominance are quitegeneral, they need not give a complete ordering of distributions when tradeoffs betweenrisk and returns are required. For example, an alternative could have a higher mean (non-first-degree stochastically dominated) with a higher variance and be second-degree sto-chastically dominated. The choice between the two alternatives would depend on thedegree of risk aversion and the magnitudes of the mean and variance.

The Gini Coefficient

Work by Shalit and Yitzhaki develops a framework for risky choice that allows theincorporation of stochastic dominance criteria and mean/variability tradeoffs. These mod-els use the mean-Gini difference function (r) for a random variable r drawn from a densityfunctionf(R) defined as (Shalit and Yitzhaki):

b(10) r b(10) r -= I R - rlf(r)f(R) dr dR.

2 a a

Buschena and Zilberman

Journal of Agricultural and Resource Economics

In (10) the bounds a and b are defined so that F(a) = 0 and F(b) = 1, where F(.) is thecumulative distribution function for risky prospect R that corresponds with f() on r.

Thus, the mean-Gini is a measure of the absolute expected spread of a realized randomevent r from a risky prospect R. This mean-Gini approach in general allows for comparisonamong a large set of risky choices since notions of stochastic dominance can be includedin the model (Shalit and Yitzhaki). In addition, specific portions of this distribution canbe stressed (e.g., portions giving low outcomes), allowing the mean-Gini approach toapproximate behavior under safety-rule models.

Expected Utility: Systematic Violations

The existence of systematic behavior (paradoxes) violating the EU model's independenceaxiom has cast doubt on its viability as a basis for prediction. The following is a detailedcriticism of the underlying axioms leading to the EU approach and a presentation of twonew models that augment it.

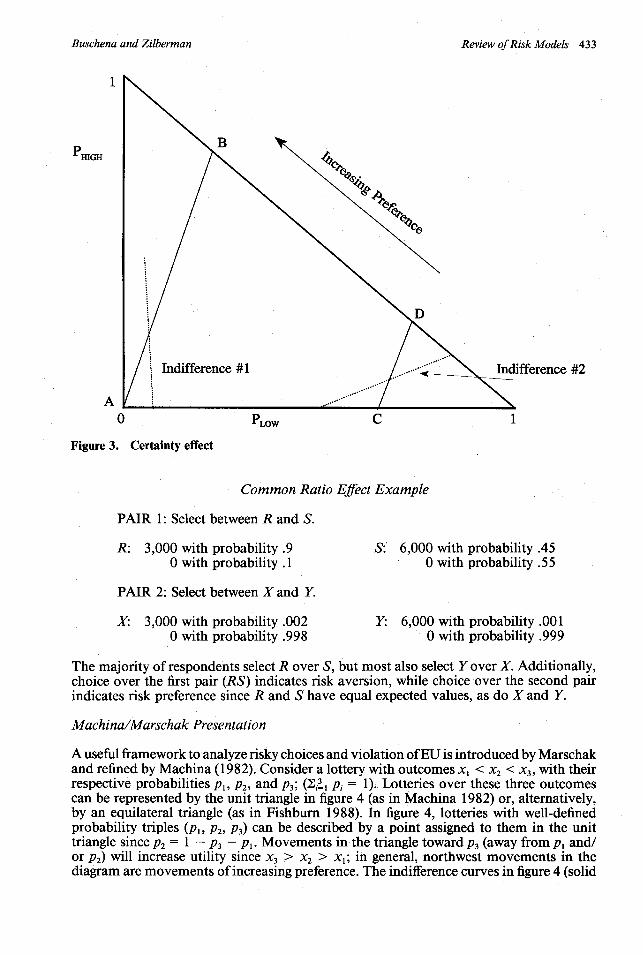

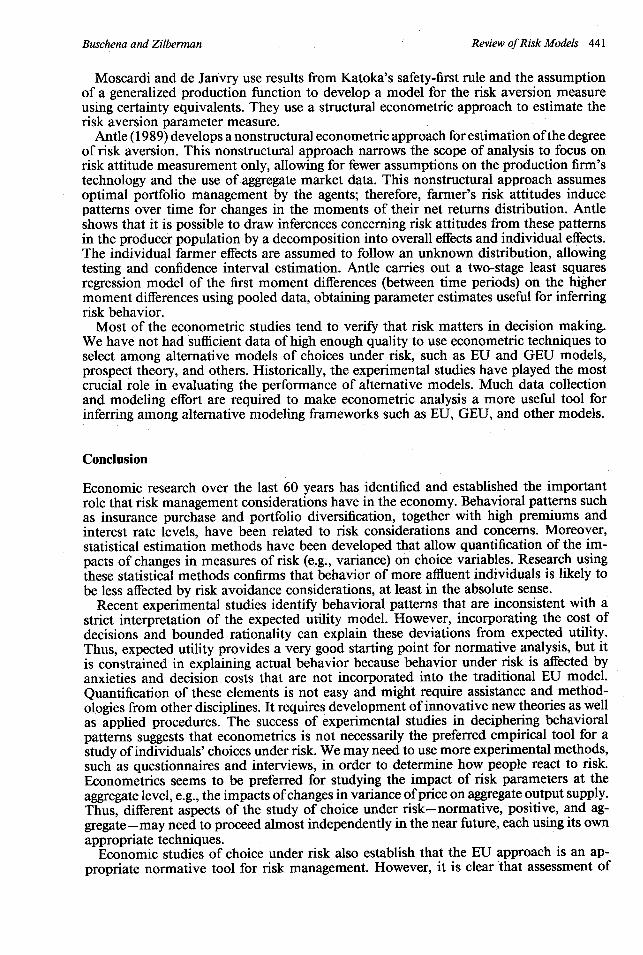

Choices made over the risky alternatives, illustrated in the Machina/Marschak trianglein figure 3, show a violation pattern of the EU model known as the "certainty effect" inan experiment from Kahneman and Tversky.6 Points in this two-dimensional simplexrepresent values for the discrete probability vector (PL, PM, P) over the rank-orderedoutcomes (xL, xM, xH) = (0, 3,000, 4,000). Most of Kahneman and Tversky's respondents(80%) selected the certain alternative, A, giving 3,000 with certainty over the more riskyalternative, B, that has a higher probability for both the lower (0) and the higher (4,000)outcomes. However, 65% of their respondents selected the riskier alternative, D, over Cfor the second-choice pair. Critically, over half of their respondents selected first A (overB) and then D (over C), directly violating EU as further discussed below.

Figure 3 also shows the approximate slope that linear preference representations, "in-difference #1" and "indifference #2," must take to be consistent with the majority of therespondents' choices reported by Kahneman and Tversky; the key point here is that thesecurves cannot be parallel since the two lines connecting points (AB) and (CD) must beparallel. These lines are parallel because the distribution (pl, q') defining the risky choicepair (CD) is a linear combination of the pair of probability distributions [pO, qO] = [(0,1.0, 0), (.2, 0, .8)] defining alternatives (AB) with a common distribution r = (0), where(0) indicates the degenerate probability distribution for a lottery that gives a 100% chanceof 0:

(11) pl = .25-.p + .75.(0);q1 =.25-.q + .75-(0).

The independence axiom (I) states that the choice between the sets of risky pairs (AB)and (NO), described through their respective probability distributions (pO, q0) and (pl,q'), should not depend on their common probability distribution [r = (0)], or on the factor[a = .25 for pair (CD) versus a = 1.0 for pair (AB)] defining the alternatives' shares oftheir non-common distributions (p0, q0). Therefore, the individuals who select A (overthe riskier alternative B, which has higher expected value) in the first pair and D (overthe less risky alternative C) in the second pair show an independence violation of EU.

This EU violation reflects the importance of receiving the certain outcome (A) oversomething that is risky (B). The importance of this form of "safety" is shown moregenerally in Buschena (1992) and in Buschena and Zilberman (1994).

Another well-known pattern of choice inconsistent with EU (and also from Kahnemanand Tversky) is known as the "common ratio example." This pattern is of particularinterest since the risky alternatives in each pair have equal means and unequal variances.Respondents are asked to select between the following two pairs of risky alternatives wherethe choice between the second pair (XY) is EU-comparable with the choice over the firstpair (RS) by the same argument showing EU-comparability between the certainty effectexample pairs above.

432 December 1994

Review of Risk Models 433

1

HIGH

A

ifference #2

0 PLOW C 1

Figure 3. Certainty effect

Common Ratio Effect Example

PAIR 1: Select between R and S.

R: 3,000 with probability .9 S:' 6,000 with probability .450 with probability .1 0 with probability .55

PAIR 2: Select between X and Y.

X: 3,000 with probability .002 Y: 6,000 with probability .0010 with probability .998 0 with probability .999

The majority of respondents select R over S, but most also select Y over X. Additionally,choice over the first pair (RS) indicates risk aversion, while choice over the second pairindicates risk preference since R and S have equal expected values, as do X and Y.

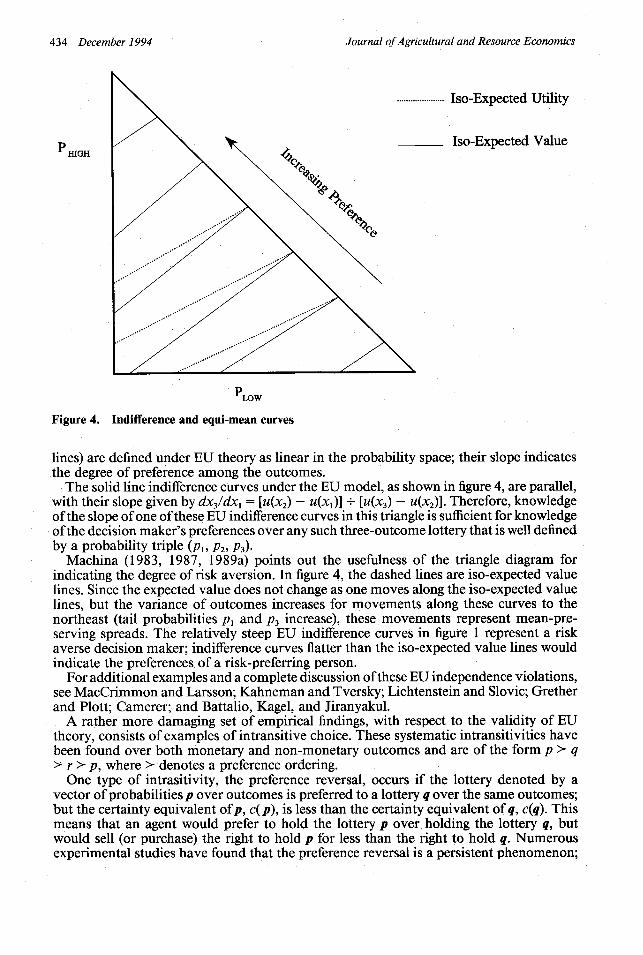

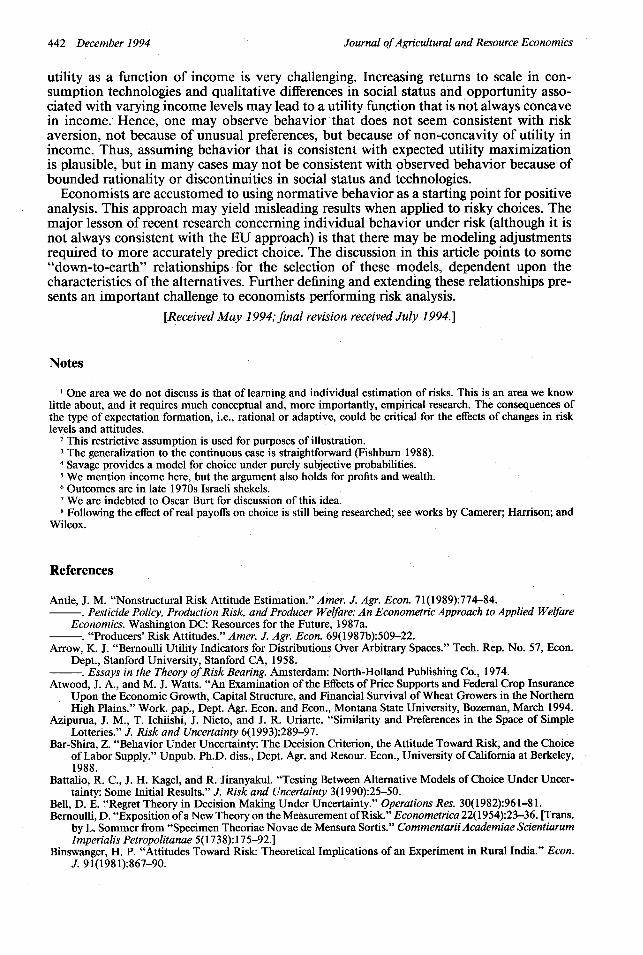

Machina/Marschak Presentation

A useful framework to analyze risky choices and violation of EU is introduced by Marschakand refined by Machina (1982). Consider a lottery with outcomes x < x 2 < x 3, with theirrespective probabilities p1, P2, and P3; (Z131 Pi = 1). Lotteries over these three outcomescan be represented by the unit triangle in figure 4 (as in Machina 1982) or, alternatively,by an equilateral triangle (as in Fishburn 1988). In figure 4, lotteries with well-definedprobability triples (pI, P2, P3) can be described by a point assigned to them in the unittriangle since P2 = 1 - p3 - p. Movements in the triangle toward P3 (away from p, and/or P2) will increase utility since x3 > x 2 > X1; in general, northwest movements in thediagram are movements of increasing preference. The indifference curves in figure 4 (solid

Buschena and Zilberman

Journal of Agricultural and Resource Economics

......... Iso-Expected Utility

Iso-Expected Value

LOW

Figure 4. Indifference and equi-mean curves

lines) are defined under EU theory as linear in the probability space; their slope indicatesthe degree of preference among the outcomes.

The solid line indifference curves under the EU model, as shown in figure 4, are parallel,with their slope given by dx3/dxl = [u(x) - u(xl)] + [u(x3) - u(x2 )]. Therefore, knowledgeof the slope of one of these EU indifference curves in this triangle is sufficient for knowledgeof the decision maker's preferences over any such three-outcome lottery that is well definedby a probability triple (PI, , P3).

Machina (1983, 1987, 1989a) points out the usefulness of the triangle diagram forindicating the degree of risk aversion. In figure 4, the dashed lines are iso-expected valuelines. Since the expected value does not change as one moves along the iso-expected valuelines, but the variance of outcomes increases for movements along these curves to thenortheast (tail probabilities pI and p3 increase), these movements represent mean-pre-serving spreads. The relatively steep EU indifference curves in figure 1 represent a riskaverse decision maker; indifference curves flatter than the iso-expected value lines wouldindicate the preferences of a risk-preferring person.

For additional examples and a complete discussion of these EU independence violations,see MacCrimmon and Larsson; Kahneman and Tversky; Lichtenstein and Slovic; Gretherand Plott; Camerer; and Battalio, Kagel, and Jiranyakul.

A rather more damaging set of empirical findings, with respect to the validity of EUtheory, consists of examples of intransitive choice. These systematic intransitivities havebeen found over both monetary and non-monetary outcomes and are of the form p > q> r > p, where > denotes a preference ordering.

One type of intrasitivity, the preference reversal, occurs if the lottery denoted by avector of probabilities p over outcomes is preferred to a lottery q over the same outcomes;but the certainty equivalent ofp, c(p), is less than the certainty equivalent of q, c(q). Thismeans that an agent would prefer to hold the lottery p over holding the lottery q, butwould sell (or purchase) the right to hold p for less than the right to hold q. Numerousexperimental studies have found that the preference reversal is a persistent phenomenon;

HIGH

434 December 1994

Review of Risk Models 435

see Fishburn (1988) for a discussion of this paradox and more general types of intransi-tivities.

The existence of intransitive behavior suggests that a clever broker could profit byoffering to purchase for an infinite number of times the preferred risky alternative p andto sell the less preferred alternative q at a higher price, then trading this least preferred qfor the more preferred p. This line of argument is characterized by the person being a"money pump"; the decision maker, not realizing that he/she is being bilked, continuespaying to exchange for the lottery currently held. Machina (1989b) evaluates this argumentusing game-theoretic concepts to show that even naive agents in this dynamic settingwould recall their previous payments, effectively limiting the amount involved in tradeson the intransitivities. Also, recent work with real payoffs (Chu and Chu) shows thatpreference reversals are eliminated when these irrational decisions are made explicitlycostly to agents.

Expected Utility: Generalizations

Generalizations of the EU framework have been developed in order to account for thesystematic paradoxes revealed through experimental studies. Models addressing the CEand the CRE seek to generalize EU theory by introducing some form of a decision weightas a function of the probabilities, giving a measure of utility marginal in the decisionweights:

n

(12) V(p, x) = u(xi)f,[p(x)].i=1

In equation (12), f[p(x)] is a decision weight on the vector p over the values of theoutcome vector x. Therefore, these models still use a marginal utility measure, but on atransformed probability axis, f[p(x)]. This method effectively changes the structure ofpreferences to fit the experimental results.

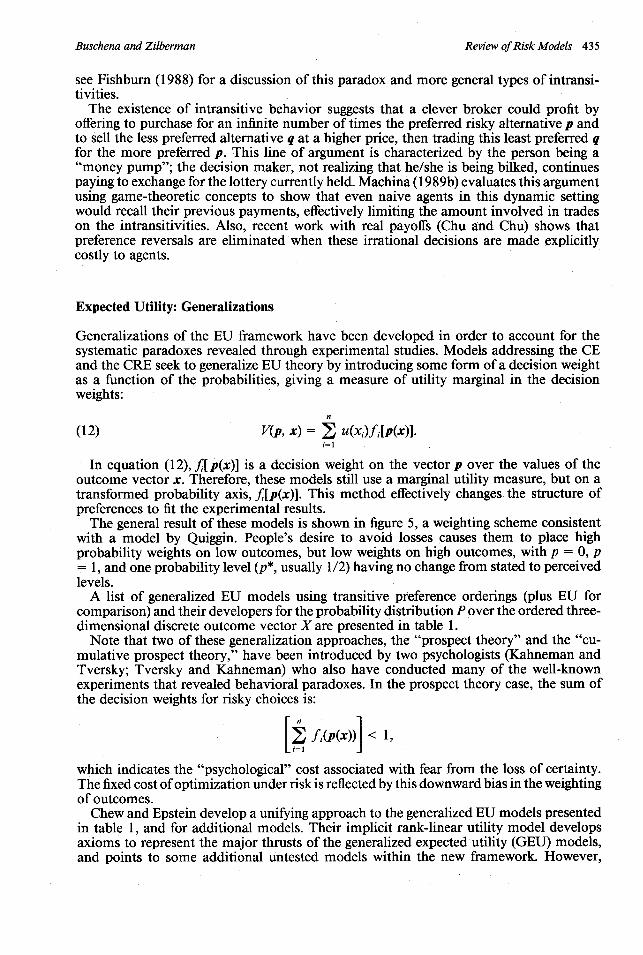

The general result of these models is shown in figure 5, a weighting scheme consistentwith a model by Quiggin. People's desire to avoid losses causes them to place highprobability weights on low outcomes, but low weights on high outcomes, with p = 0, p= 1, and one probability level (p*, usually 1/2) having no change from stated to perceivedlevels.

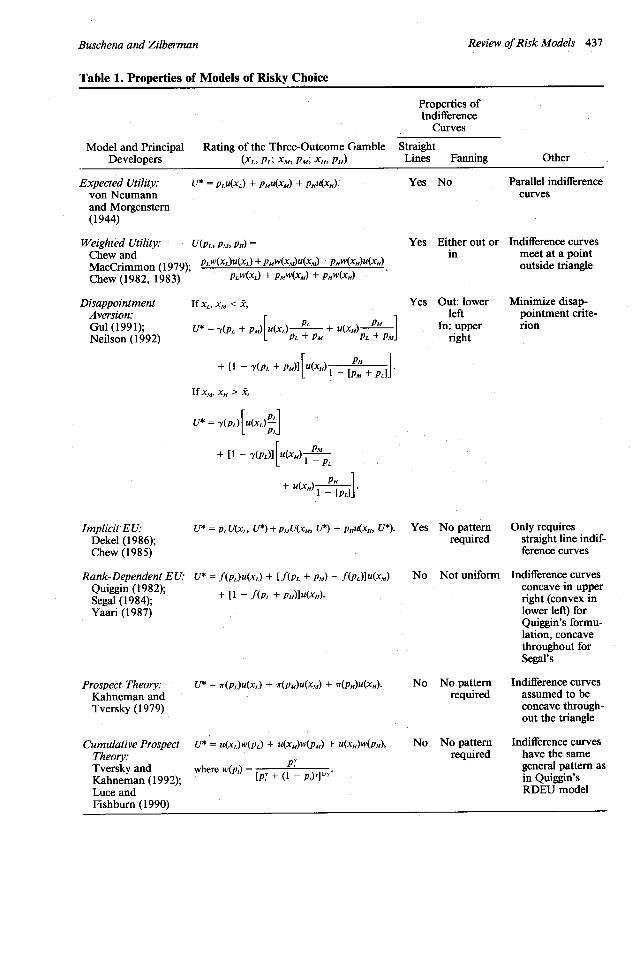

A list of generalized EU models using transitive preference orderings (plus EU forcomparison) and their developers for the probability distribution P over the ordered three-dimensional discrete outcome vector X are presented in table 1.

Note that two of these generalization approaches, the "prospect theory" and the "cu-mulative prospect theory," have been introduced by two psychologists (Kahneman andTversky; Tversky and Kahneman) who also have conducted many of the well-knownexperiments that revealed behavioral paradoxes. In the prospect theory case, the sum ofthe decision weights for risky choices is:

which indicates the "psychological" cost associated with fear from the loss of certainty.which indicates the "psychological" cost associated with fear from the loss of certainty.The fixed cost of optimization under risk is reflected by this downward bias in the weightingof outcomes.

Chew and Epstein develop a unifying approach to the generalized EU models presentedin table 1, and for additional models. Their implicit rank-linear utility model developsaxioms to represent the major thrusts of the generalized expected utility (GEU) models,and points to some additional untested models within the new framework. However,

Buschena and Zilberman

Journal of Agricultural and Resource Economics

Posterior Prob.(Perceived)

Prior Prob.(Actual)

p* 1

Figure 5. Weighting function under Quiggin's RDEU model

Camerer reports the results of empirical tests that show violations of all of these GEUmodels. Buschena (1992) shows violations of the GEU models and also of prospect theory.

Expected Utility Model: Multicomponent Extensions

Regret/Rejoice Theory

The EU theory uses the term "risk aversion" to describe the shape of the utility function:concavity indicating risk aversion or convexity for risk-preferring behavior. However, thecurvature of the utility function over income or goods alone might not reflect all of the"costs" of risk. People may have constant marginal utility of income for certain outcomes[u'(x) = c], described by the EU theory as risk neutral, but still prefer a certain to a riskyoutcome.

Planning for, and even worrying about, the actual outcome under a risky situation mayentail costs that are nontrivial. This notion of costs of risk goes beyond independenceviolations, the EU preference reversal paradox, and other behavior violating EU. In thesecases, normative models of behavior under risk should allow for some notion of the cost(or disutility) experienced from being involved in the risky situation itself.

One idea capturing some of the notions of disutility from partaking in a gamble is amodel developed by Loomes and Sudgen (1982, 1987), and by Bell, identified as theregret/rejoice model. In this model, the agent chooses an action and then experiencesregret (rejoice) if the outcome of his or her chosen action is dominated by (dominates)an alternative action's outcome. This model can account for the intransitivities experi-enced in the preference reversal paradox in addition to the behavior under the commonconsequence and common ratio effects.

The regret/rejoice preference ordering gives a relationship between action Xg and xh,such that Xg preferred to Xh implies that Y(xg, x^) > 0 for a real valued function Y(-, -).Thus, the preference ordering is not only on the realized outcomes but, rather, it is onboth the probabilities of the realized and the alternative outcomes.

436 December 1994

Review of Risk Models 437

Table 1. Properties of Models of Risky Choice

Properties ofIndifference

Curves

Model and Principal Rating of the Three-Outcome Gamble StraightDevelopers (XL, PL; XM PM; XH, PH) Lines Fanning Other

Expected Utility:von Neumannand Morgenstern(1944)

U* = PLU(XL) + PMU(XM) + PHU(XH). Yes No Parallel indifferencecurves

Weighted Utility: U(PL, PM, PH)Chew andMacCrimmon (1979)- PLW(XL)U(XL) + PMW(XM)U(XM) + PHW(XH)U(XH)

Chew (1982, 1983) PLW(XL) + PMW(XM) + PHW(XH)

Yes Either out or Indifference curvesin meet at a point

outside triangle

DisappointmentAversion:Gul (1991);Neilson (1992)

Implicit EU:Dekel (1986);Chew (1985)

Rank-Dependent EU:Quiggin (1982);Segal (1984);Yaari (1987)

Prospect Theory:Kahneman andTversky (1979)

If XL, XM < X,

U* = Y(PL + PM) U(XL) + u(XM) PPL + PM PL+ PM]

L 1 - [PM + PL+ [1 - 'y(PL+PM)] [U(X)i - [PM+PL]H

If X, XH > X,

U* =' Y(PL) U(XL)LL PL

+ [1 - 'Y(PL)] [U(XM) p

+ u) 1 - P.]+" r(XH)I

U* = PLU(XL, U*) + PMU(XM, U*) + PHU(XH, U*).

U* = f(PL)(XL) + [f(PL + PM) - f(PL)]U(XM )

+ [1 - f(PL + PM)]U(XH).

U* = rr(pL)U(XL) + 7(PM)U(XM) + rr(PH)U(XH).

Yes Out: lowerleft

In: upperright

Yes No patternrequired

No Not uniform

No No patternrequired

Minimize disap-pointment crite-rion

Only requiresstraight line indif-ference curves

Indifference curvesconcave in upperright (convex inlower left) forQuiggin's formu-lation, concavethroughout forSegal's

Indifference curvesassumed to beconcave through-out the triangle

Cumulative Prospect U* = u(xL)w(p,) + U(XM)W(pM) + U(X,)W(pH),Theory:Tversky and where w(p,) = P' -Kahneman (1992); [p + 1 - Pi)']"Luce andFishburn (1990)

No No patternrequired

Indifference curveshave the samegeneral pattern asin Quiggin'sRDEU model

Buschena and Zilberman

Journal of Agricultural and Resource Economics

Status Model

Recently, there has been a renewed interest in decision making under risk where factorsin addition to income enter into the utility function. One approach to modeling suchbehavior has been to consider multiattribute utility functions; for example, preferencesover outcome distributions may depend on consumption as well as income. Pratt (1988)and Finkelshtain and Chalfant (1989, 1990) examine multiattribute utility models andhave obtained behavioral results using an approach parallel to that of Sandmo in theunivariate case. These models use a smooth von Neumann-Morgenstern utility functionin their analysis.

For some choices under risk, a discrete "crisis" outcome, such as bankruptcy or star-vation, may affect the utility from income. The possibility of such a crisis occurringpresents real threats to the life and livelihood of decision makers. These crisis outcomesmay become a critical issue for entire communities, particularly in the not unexpectedinstances where agents' realized outcomes are not independent of those of others in thecommunity. Concern with these potential crisis outcomes may well overwhelm decisionsregarding the marginal conditions (regarding other variables) that usually are consideredin models of economic behavior.

Of particular interest is to develop a model that combines the treatment of discreteproblems by safety rules with the axiomized treatment of decisions under risk by the EUand generalized EU models. The status model (Buschena and Zilberman 1991) incor-porates this critical discrete factor into a normative model. Consider an indicator variableD, having the value 1 if an adverse event occurs and 0 if the event does not occur. Supposethat the probability of the adverse situation occurring depends on income x, i.e., P(D =1) = f(x). Also, let the utility representation (which is obtained through a well-definedpreference ordering in the sense of von Neumann and Morgenstern), vi(x) = v(x/D = i),depend on the value of D (i = 1, 0) in addition to the level of income. For example, v,(x)may represent the utility function of a farmer who retains ownership of his/her land whileVo(x) represents the utility function of a farmer who gives up land ownership and mustrent the land. The function f(x) denotes the likelihood that the farmer will need to sellthe land (or declare bankruptcy) when his/her income equals y.

Then, the agents' maximization problem becomes:

(13a) EU(D, x)= f v,(y)[f(y)]g(y) dy + Vo(y)[l - f(y)]g(y) dy

(13b) = v,(y)f,(y) dy + f vo(y)fo(y) dy,

where g(x) is the density function for x,fi(x) = [f(x)]g(x), andf0 (x) = [1 - f(x)]g(x). Theindependence axiom for a representation over income alone, u(x), could hold for a constantlevel of D, but, if both levels of D could occur, the independence axiom in general wouldnot hold.

The status model has the following as special cases: (a) safety-rule models, where Vo(x)is extremely negative, and f(x) = 1 if x < t for some level of income t; and (b) the EUmodel, where vl(x) = Vo(x), g(x) are objective probabilities.

Due to its discrete nature over D, the reduced form EU(D, x) required for estimationwill differ according to the situation at hand. Familiarity with details of the decisionmaker's situation will be needed for utilization of the status model.

Atwood and Watts argue that risky choices are dynamic in nature; they use simulationto show that even when decision makers are risk neutral, they make dynamic decisionssubject to bankruptcy constraints and therefore may exhibit risk aversion. Their observedbehavior can be interpreted as risk averse in a static context. Thus, risk averse behaviormay not reflect inherent preferences, but rather may reflect financial constraints in adynamic setting.7

438 December 1994

Review of Risk Models 439

The models presented above are applicable in different situations; EU theory may workwell for portfolio analysis where there is no crisis outcome under complete optimization.Safety rules are advantageous for modeling when potential crisis situations are involved.The status model incorporates both the discrete and continuous nature of choice underrisk, but the status model would require considerable knowledge of the nature of thedecision problem. Of interest for future research is the effect of the aggregation of behaviorunder this model; we would like to determine if behavior under a potential discrete crisisposes an answerable empirical question.

Similarity Model

A number of theorists recently have proposed explanations for the occurrence of EUindependence violations (Rubinstein; Leland 1990, 1992; Azipurua et al.; Buschena 1992).This explanation relies on an argument of costly or bounded rationality (Simon; March)where evaluation costs depend on the similarity of the risky alternatives. For example,pair (AB) in the certainty effect example (fig. 3) is thought to be dissimilar, while pair(CD) is thought to be similar; in these examples, similarity can be defined largely by thedistance (e.g., a Euclidian norm metric) between the points representing the probabilitydistributions.

Rubinstein explores this similarity idea in an axiomatic framework; his work is extendedand generalized by Azipurua et al. Leland (1990, 1992) offers a theory of behavior undersimilarity and gives empirical evidence for its importance. Buschena (1992), and Buschenaand Zilberman (1994) further generalize the predictions of similarity and test for itspracticality and predictive power for choice and the occurrence of EU violations. Theyfound similarity to (a) be a concept recognized by respondents, (b) be definable throughobjective criteria, and (c) have a significant effect on choice on the occurrence of EUindependence violations and on the occurrence of intransitive behavior. Implications ofthis work are that (a) EU may work well for modeling an important class of (dissimilar)risky decisions, and (b) EU violations occur because of optimal tradeoffs of the costs andbenefits of evaluation efforts. Buschena (1994) replicated these findings for similarity effectsand also showed that similarity affects decision effort (using the proxy of time of evaluation)in a manner consistent with optimization.

Although similarity is a rather new approach to viewing the occurrence of EU violations,it appears to have great promise for understanding and modeling behavior under riskychoice. Like other models of decision cost, however, the conceptual framework of simi-larity is difficult to devise and is still being developed.

Empirical Methods to Infer Decision Making Under Risk

There have been a growing number of empirical studies for choice under risk. Thesestudies can be divided according to their methodologies into the following groups.

Experimental Studies

The notion of alternative gambles in decision making under risk lends itself well to inferringbehavior based on experimental gambles such as those carried out by Kahneman andTversky. Respondents are asked to choose between lotteries (usually simple) that differin payoffs and probabilities or both. Games usually only occur once, so no learning isinvolved. Many of the paradoxes, such as the certainty and common ratio effect examples,have been clearly and consistently shown by these experiments. These experiments arerelatively inexpensive to carry out and are quite flexible. The major problem with thisexperimental approach is that it is not representative of the decision problems commonlyfaced by agents; also, the outcomes of these gambles are often only hypothetical, raisingquestions concerning subject motivation.8

Buschena and Zilberman

Journal of Agricultural and Resource Economics

Binswanger (1980, 1981) carried out an extended experiment with actual (real) payoffs,allowing learning, where agents chose between various simple lotteries with multiple plays.Payoff magnitudes were increased as the game progressed in order to give incentives forlearning and to study income effects. Such extended experiments are more expensive toconduct, but they may offer a greater degree of representation of the agents' everydaydecision making and learning processes than do one-shot experiments. However, thesesimple lottery choices that are divorced from actual decisions may not be very represen-tative of the agents' approach to decisions under risk (Smith).

Programming Studies

Programming methods have been used by many economists (Lin, Dean, and Moore;Hazel and Scandizzo) to estimate risk aversion in a normative model of activity analysis.Such approaches can generate an efficient set in risk and return space under the productionstructure assumed for the model. The challenge for these methods of estimation is thatthe coefficients are quite sensitive to variable measurement, while measures of standarderror for these general testing procedures have not been developed. Another problem withthe programming approach is that all deviations from the model's optimal outcome areattributed to risk behavior.

Econometric Studies

Econometric studies can be divided into two groups--structural and nonstructural. Mostof the econometric studies thus far have been structural. Estimation of a general structuralmodel assuming neoclassical production technology and EU approach is very intensive,requiring joint estimation of the structure of a firm's technology and input decision rules(Antle 1987a). The return from the structural approach is that tests of hypotheses areallowed regarding input use or for the analysis of policy in addition to risk measurement.This structural approach is data intensive, requiring detailed input use and price data forindividual farms. Some problems with the structural econometric method are that all ofthe observed deviations from the mean are attributed to risk response and that data forthe individual farm's input use and prices are seldom available; see Antle (1989) andPope for further treatment of the structural approach.

Structural models have been developed to estimate both production technology param-eters and risk preferences. These analyses have a sophisticated specification of productionprocesses, taking into account some details not recognized in most econometric studiesof production. For example, Antle's (1987a) analysis of the risk behavior of Californiatomato growers explicitly models their sequential choice of pesticide strategy. This study,as well as those by Antle (1987b) and Love and Buccola, shows heterogeneous risk attitudesin the populations, with a high tendency for farmers to be both Arrow-Pratt absolute andrelative risk averse and to have downside risk aversion. Pope and Just estimate the supplyresponse of potato growers in Idaho and test alternative measures of risk aversion. Theirresults reject constant absolute and partial risk aversion, but not constant relative riskaversion. Like the previous studies, their study does not empirically test the effect ofchanges in wealth or income on measures of risk aversion.

Works by Calvin and by Bar-Shira assume fixed proportion technologies and apply theJust-Zilberman portfolio framework to farmers' choices in Iowa and Israel, respectively.Calvin found that risk considerations have had very small impacts on crop choices byIowa farmers. These farmers' choices are more affected by labor constraints and croprotation considerations. Risk considerations are instrumental, however, in explainingfarmers' decisions regarding participation in the commodity programs. Bar-Shira foundthat risk considerations play a significant role in explaining land allocation among cropsin Israel and showed empirical support for the EU model. Both Calvin's and Bar-Shira'sstudies verify Arrow's (1974) hypothesis that absolute risk aversion tends to decline withwealth, while relative risk aversion tends to increase with wealth.

440 December 1994

Review of Risk Models 441

Moscardi and de Janvry use results from Katoka's safety-first rule and the assumptionof a generalized production function to develop a model for the risk aversion measureusing certainty equivalents. They use a structural econometric approach to estimate therisk aversion parameter measure.

Antle (1989) develops a nonstructural econometric approach for estimation of the degreeof risk aversion. This nonstructural approach narrows the scope of analysis to focus onrisk attitude measurement only, allowing for fewer assumptions on the production firm'stechnology and the use of aggregate market data. This nonstructural approach assumesoptimal portfolio management by the agents; therefore, farmer's risk attitudes inducepatterns over time for changes in the moments of their net returns distribution. Antleshows that it is possible to draw inferences concerning risk attitudes from these patternsin the producer population by a decomposition into overall effects and individual effects.The individual farmer effects are assumed to follow an unknown distribution, allowingtesting and confidence interval estimation. Antle carries out a two-stage least squaresregression model of the first moment differences (between time periods) on the highermoment differences using pooled data, obtaining parameter estimates useful for inferringrisk behavior.

Most of the econometric studies tend to verify that risk matters in decision making.We have not had sufficient data of high enough quality to use econometric techniques toselect among alternative models of choices under risk, such as EU and GEU models,prospect theory, and others. Historically, the experimental studies have played the mostcrucial role in evaluating the performance of alternative models. Much data collectionand modeling effort are required to make econometric analysis a more useful tool forinferring among alternative modeling frameworks such as EU, GEU, and other models.

Conclusion

Economic research over the last 60 years has identified and established the importantrole that risk management considerations have in the economy. Behavioral patterns suchas insurance purchase and portfolio diversification, together with high premiums andinterest rate levels, have been related to risk considerations and concerns. Moreover,statistical estimation methods have been developed that allow quantification of the im-pacts of changes in measures of risk (e.g., variance) on choice variables. Research usingthese statistical methods confirms that behavior of more affluent individuals is likely tobe less affected by risk avoidance considerations, at least in the absolute sense.

Recent experimental studies identify behavioral patterns that are inconsistent with astrict interpretation of the expected utility model. However, incorporating the cost ofdecisions and bounded rationality can explain these deviations from expected utility.Thus, expected utility provides a very good starting point for normative analysis, but itis constrained in explaining actual behavior because behavior under risk is affected byanxieties and decision costs that are not incorporated into the traditional EU model.Quantification of these elements is not easy and might require assistance and method-ologies from other disciplines. It requires development of innovative new theories as wellas applied procedures. The success of experimental studies in deciphering behavioralpatterns suggests that econometrics is not necessarily the preferred empirical tool for astudy of individuals' choices under risk. We may need to use more experimental methods,such as questionnaires and interviews, in order to determine how people react to risk.Econometrics seems to be preferred for studying the impact of risk parameters at theaggregate level, e.g., the impacts of changes in variance of price on aggregate output supply.Thus, different aspects of the study of choice under risk-normative, positive, and ag-gregate-may need to proceed almost independently in the near future, each using its ownappropriate techniques.

Economic studies of choice under risk also establish that the EU approach is an ap-propriate normative tool for risk management. However, it is clear that assessment of

Buschena and Zilberman

Journal of Agricultural and Resource Economics

utility as a function of income is very challenging. Increasing returns to scale in con-sumption technologies and qualitative differences in social status and opportunity asso-ciated with varying income levels may lead to a utility function that is not always concavein income. Hence, one may observe behavior that does not seem consistent with riskaversion, not because of unusual preferences, but because of non-concavity of utility inincome. Thus, assuming behavior that is consistent with expected utility maximizationis plausible, but in many cases may not be consistent with observed behavior because ofbounded rationality or discontinuities in social status and technologies.

Economists are accustomed to using normative behavior as a starting point for positiveanalysis. This approach may yield misleading results when applied to risky choices. Themajor lesson of recent research concerning individual behavior under risk (although it isnot always consistent with the EU approach) is that there may be modeling adjustmentsrequired to more accurately predict choice. The discussion in this article points to some"down-to-earth" relationships for the selection of these models, dependent upon thecharacteristics of the alternatives. Further defining and extending these relationships pre-sents an important challenge to economists performing risk analysis.

[Received May 1994; final revision received July 1994.]

Notes

One area we do not discuss is that of learning and individual estimation of risks. This is an area we knowlittle about, and it requires much conceptual and, more importantly, empirical research. The consequences ofthe type of expectation formation, i.e., rational or adaptive, could be critical for the effects of changes in risklevels and attitudes.

2 This restrictive assumption is used for purposes of illustration.3 The generalization to the continuous case is straightforward (Fishburn 1988).4 Savage provides a model for choice under purely subjective probabilities.5 We mention income here, but the argument also holds for profits and wealth.6 Outcomes are in late 1970s Israeli shekels.7 We are indebted to Oscar Burt for discussion of this idea.8 Following the effect of real payoffs on choice is still being researched; see works by Camerer; Harrison; and

Wilcox.

References

Antle, J. M. "Nonstructural Risk Attitude Estimation." Amer. J. Agr. Econ. 71(1989):774-84.. Pesticide Policy, Production Risk, and Producer Welfare: An Econometric Approach to Applied Welfare

Economics. Washington DC: Resources for the Future, 1987a.."Producers' Risk Attitudes." Amer. J. Agr. Econ. 69(1987b):509-22.

Arrow, K. J. "Bernoulli Utility Indicators for Distributions Over Arbitrary Spaces." Tech. Rep. No. 57, Econ.Dept., Stanford University, Stanford CA, 1958.

- . Essays in the Theory of Risk Bearing. Amsterdam: North-Holland Publishing Co., 1974.Atwood, J. A., and M. J. Watts. "An Examination of the Effects of Price Supports and Federal Crop Insurance

Upon the Economic Growth, Capital Structure, and Financial Survival of Wheat Growers in the NorthernHigh Plains." Work. pap., Dept. Agr. Econ. and Econ., Montana State University, Bozeman, March 1994.

Azipurua, J. M., T. Ichiishi, J. Nieto, and J. R. Uriarte. "Similarity and Preferences in the Space of SimpleLotteries." J. Risk and Uncertainty 6(1993):289-97.

Bar-Shira, Z. "Behavior Under Uncertainty: The Decision Criterion, the Attitude Toward Risk, and the Choiceof Labor Supply." Unpub. Ph.D. diss., Dept. Agr. and Resour. Econ., University of California at Berkeley,1988.

Battalio, R. C., J. H. Kagel, and R. Jiranyakul. "Testing Between Alternative Models of Choice Under Uncer-tainty: Some Initial Results." J. Risk and Uncertainty 3(1990):25-50.

Bell, D. E. "Regret Theory in Decision Making Under Uncertainty." Operations Res. 30(1982):961-81.Bernoulli, D. "Exposition of a New Theory on the Measurement of Risk." Econometrica 22(1954):23-36. [Trans.

by L. Sommer from "Specimen Theoriae Novae de Mensura Sortis." Commentarii Academiae ScientiarumImperialis Petropolitanae 5(1738): 175-92.]

Binswanger, H. P. "Attitudes Toward Risk: Theoretical Implications of an Experiment in Rural India." Econ.J. 91(1981):867-90.

442 December 1994

Review of Risk Models 443

. "Risk Aversion, Collateral Requirements, and the Markets for Credit and Insurance in Rural Areas."Studies in Employment and Rural Development No. 79, International Bank for Reconstruction and De-velopment. Washington DC: The World Bank, 1980.

Bitros, G. C., and H. H. Kelljian. "A Stochastic Control Approach to Factor Demand." Internat. Econ. Rev.17(1976):701-17.

Buschena, D. E. "The Effects of Alternative Similarity on Choice Under Risk: Toward a Plausible Explanationof Independence Violations of the Expected Utility Model." Unpub. Ph.D. diss., Dept. Agr. and Resour.Econ., University of California at Berkeley, 1992.- . "The Effects of Similarity on Choice and Decision Effort." Work. pap., Dept. Agr. Econ. and Econ.,Montana State University, Bozeman, 1994.

Buschena, D. E., and D. Zilberman. "The Effects of Alternative Similarity on Risky Choice: Implications forViolations of Expected Utility." Work. pap., Dept. Agr. Econ. and Econ., Montana State University, Boze-man, 1994.

. "Risk Attitudes Over Income Under Discrete Status Levels." Paper presented at the annual meeting ofthe American Agricultural Economics Association, Manhattan KS, August 1991.

Calvin, L. S. "Distributional Consequences of Agricultural Commodity Policy." Unpubl Ph.D. diss., Dept. Agr.and Resour. Econ., University of California at Berkeley, 1988.

Camerer, C. "An Experimental Test of Several Generalized Utility Theories." J. Risk and Uncertainty 2(89):61-104.

Chew, S. H. "From Strong Substitution to Very Weak Substitution: Mixture-Utility Theory and Semi-WeightedUtility Theory." Work. pap., Dept. Polit. Econ., Johns Hopkins University, Baltimore MD, 1985.

. "A Generalization of the Quasilinear Mean with Applications to the Measurement of Income Inequalityand Decision Theory Resolving the Allais Paradox." Econometrica 51(1983):1065-92.

-- . "A Mixture Set Axiomatization of Weighted Utility Theory." Work. pap., College of Business andPublic Administration, University of Arizona, Tucson, 1982.

Chew, S. H., and L. G. Epstein. "A Unifying Approach to Axiomatic Non-Expected Utility Theories." J. Econ.Theory 49(1989):207-40.

Chew, S. H., and K. MacCrimmon. "Alpha-Nu Choice Theory: A Generalization of Expected Utility Theory."Unpub. manu., Faculty of Commerce and Business Administration, University of British Columbia, Van-couver, 1979.

Chu, Y. P., and R. L. Chu. "The Subsidence of Preference Reversals in Simplified and Marketlike ExperimentalSettings: A Note." Amer. Econ. Rev. 80(1990):902-11.

Collins, A., W. N. Musser, and R. Mason. "Prospect Theory and Risk Preferences of Oregon Seed Producers."Amer. J. Agr. Econ. 73(1991):429-35.

Cramer, G. Correspondence to N. Bernoulli, 1728. Reported in D. Bernoulli, "Exposition of a New Theory onthe Measurement of Risk." Econometrica 22(1954):23-36. [Trans. by L. Sommer from "Specimen TheoriaeNovae de Mensura Sortis." Commentarii Academiae Scientiarum Imperialis Petropolitanae 5(1738):175-92.]

Dekel, E. "An Axiomatic Characterization of Preferences Under Uncertainty: Weakening the IndependenceAxiom." J. Econ. Theory 40(1986):304-18.

Feder, G., and R. Just. "A Study of Debt Serving Capacity Applying Logit Analysis." J. Development Econ.4(1977):25-38.

Finkelshtain, I., and J. Chalfant. "Portfolio Choices in the Presence of Other Risks." Work. Pap. No. 505, Dept.Agr. and Resour. Econ., University of California at Berkeley, 1989.

. "Production Decisions in the Presence of Multivariate Risk." Unpub. pap., Dept. Agr. and Resour.Econ., University of California at Berkeley, 1990.

Fishbur, P. C. Nonlinear Preference and Utility Theory. London: Johns Hopkins University Press, Ltd., 1988.. "Transitive Measurable Utility." J. Econ. Theory 31(1983):293-317.

Friedman, M., and L. J. Savage. "The Utility Analysis of Choices Involving Risk." J. Polit. Econ. 56(1948):279-304.

Grether, D. M., and C. R. Plott. "Economic Theory of Choice and the Preference Reversal Phenomenon." Amer.Econ. Rev. 69(1979):623-38.

Gul, F. "A Theory of Disappointment Aversion." Econometrica 59(1991):667-86.Hadar, J., and W. R. Russell. "Rules for Ordering Uncertain Prospects." Econ. Rev. 59(1969):25-34.Harrison, W. G. "Flat Payoff Functions and the Experimentalists: Reply to the Critics." Work. pap., Econ.

Dept., University of South Carolina, Columbia, 1992.Harsanyi, J. "Von Neumann-Morgenstern Utilities, Risk Taking, and Welfare." In Essays on Ethics, Social

Behavior, and Scientific Explanation, pp. 545-58. Dordrecht, Holland: Reidel, 1976.Hazel, P. B. R., and P. L. Scandizzo. "Market Intervention Policies When Production Is Risky." Amer. J. Agr.

Econ. 57(1975):641-49.Jensen, N. E. "An Introduction to Bernoullian Utility Theory: I. Utility Functions." Swedish J. Econ. 69(1967):

163-83.Kahneman, D., and A. Tversky. "Prospect Theory: An Analysis of Decision Under Risk." Econometrica 47(1979):

263-91.Katoka, S. "A Stochastic Programming Model." Econometrica 31(1963):181-96.Keynes, J. M. The General Theory ofEmployment, Interest, and Money. New York: Harcourt, Brace, and World,

1936.

Buschena and Zilberman

Journal of Agricultural and Resource Economics

Leland, J. W. "Generalized Similarity Judgments." Work. pap., Dept. Social and Decision Sciences, Carnegie-Mellon University, Pittsburgh PA, 1992.

. "A Theory of Approximate Expected Utility Maximization." Work. pap., Dept. Social and DecisionSciences, Carnegie-Mellon University, Pittsburgh PA, 1990.

Lichtenstein, S., and P. Slovic. "Response-Induced Reversals of Preferences in Gambling: An Extended Rep-lication in Las Vegas." J. Experimental Psych. 101(1973):16-20.

Lin, W., G. W. Dean, and C. V. Moore. "An Empirical Test of Utility versus Profit Maximization in AgriculturalProduction." Amer. J. Agr. Econ. 56(1974):497-508.

Loomes, G., and R. Sudgen. "Regret Theory: An Alternative Theory of Rational Choice Under Uncertainty."Econ. J. 92(1982):805-24.

. "Some Implications of a More General Form of Regret Theory." J. Econ. Theory 41(1987):270-87.Love, H. A., and S. T. Buccola. "Joint Risk Preference Technology Estimation with a Primal System." Amer.

J. Agr. Econ. 73(1991):765-74.Luce, R. D., and P. C. Fishburn. "Rank- and Sign-Dependent Linear Utility Models for Finite First-Order

Gambles." J. Risk and Uncertainty 3(1990):29-59.MacCrimmon, K. R., and S. Larsson. "Utility Theory: Axioms versus 'Pardoxes.'" In Expected Utility Hy-

pothesis and the Allais Paradox, eds., M. Allais and 0. Hagan, pp. 333-409. Dordrecht, Holland: Reidel,1979.

Machina, M. J. "Choice Under Uncertainty: Problems Solved and Unsolved." J. Econ. Perspectives 1(1987):121-54.

- . "Comparative Statics and Non-Expected Utility Preferences." J. Econ. Theory 47(1989a):393-405.- . "Dynamic Consistency and Non-Expected Utility Models of Choice Under Uncertainty." J. Econ. Lit.27(1989b): 1622-68.

. "The Economic Theory of Individual Behavior Toward Risk: Theory, Evidence, and New Directions."Tech. Rep. No. 433, Center for Research on Organizational Efficiency, Stanford University, Palo Alto CA,1983.

- ." 'Expected Utility': Analysis Without the Independence Axiom." Econometrica 50(1982):227-323.March, J. G. "Bounded Rationality, Ambiguity, and the Engineering of Choice." Bell J. Econ. 9(1978):587-

608.Marschak, J. "Rational Behavior, Uncertain Prospects, and Measurable Utility." Econometrica 18(1950): 111-

41. Errata 18(1950):312.Moscardi, E., and A. de Janvry. "Attitudes Toward Risk Among Peasants: An Econometric Approach." Amer.

J. Agr. Econ. 59(1977):710-16.Neilson, W. S. "A Mixed Fan Hypothesis and Its Implications for Behavior Towards Risk." J. Econ. Behavior

and Organization 19(1992): 197-212.Patrick, G. F., P. N. Wilson, P. J. Barry, W. G. Boggess, and D. T. Young. "Risk Perceptions and Management

Responses: Producer-Generated Hypotheses for Risk Modeling." S. J. Agr. Econ. 17(1985):231-38.Pope, R. D. "Empirical Estimation and Use of Risk Preferences: An Appraisal of Estimation Methods That

Use Actual Economic Decisions." Amer. J. Agr. Econ. 64(1982):376-83.Pope, R. D., and R. E. Just. "On Testing the Structure of Risk Preferences in Agricultural Supply Analysis."

Amer. J. Agr. Econ. 73(1991):743-48.Pratt, J. W. "Aversion to One Risk in the Presence of Others." J. Risk and Uncertainty 1(1988):395-413.

. "Risk Aversion in the Small and in the Large." Econometrica 32(1964):122-36.Quiggin, J. "A Theory of Anticipated Utility." J. Econ. Behavior and Organization 3(1982):323-43.Rothschild, M., and J. E. Stiglitz. "Increasing Risk: A Definition." J. Econ. Theory 2(1970):225-43.Roy, A. D. "Safety First and the Holding of Assets." Econometrica 20(1952):431-49.Rubinstein, A. "Similarity and Decision Making Under Risk: Is There a Utility Theory Resolution to the Allais

Paradox?" J. Econ. Theory 46(1988): 145-53.Sandmo, A. "On the Theory of the Competitive Firm Under Price Uncertainty." Amer. Econ. Rev. 61(1971):

65-73.Savage, L. J. The Foundations of Statistics. New York: Wiley, 1954.Segal, U. "Nonlinear Decision Weights with the Independence Axiom." Work. Pap. No. 353, Econ. Dept.,

University of California, Los Angeles, 1984.Shalit, H., and S. Yitzhaki. "Mean-Gini, Portfolio Theory, and the Pricing of Risky Assets." J. Finance 39(1984):

1449-68.Simon, H. Administrative Behavior, 2nd ed. New York: Free Press, 1957.Smith, V. L. "Review of Rational Choice: The Contrast Between Economics and Psychology." J. Polit. Econ.

99(1991):877-97.Telser, L. G. "Safety First and Hedging." Rev. Econ. Stud. 23(1955-56):1-16.Tobin, J. "Liquidity Preference as Behavior Risk." Rev. Econ. Stud. 25(1958):65-86.Tversky, A., and D. Kahneman. "Cumulative Prospect Theory: An Analysis of Decision Making Under Un-

certainty." Work. pap., Dept. Psychology, Stanford University, Stanford CA, 1992.von Neumann, J., and 0. Morgenstern. Theory of Games and Economic Behavior. Princeton NJ: Princeton

University Press, 1944.Wilcox, N. "Lottery Pricing: Incentives, Complexity, and Decision Time." Econ. J. 103(1993):311-24.Yaari, M. E. "The Dual Theory of Choice Under Risk." Econometrica 55(1987):95-115.

444 December 1994

Review of Risk Models 445

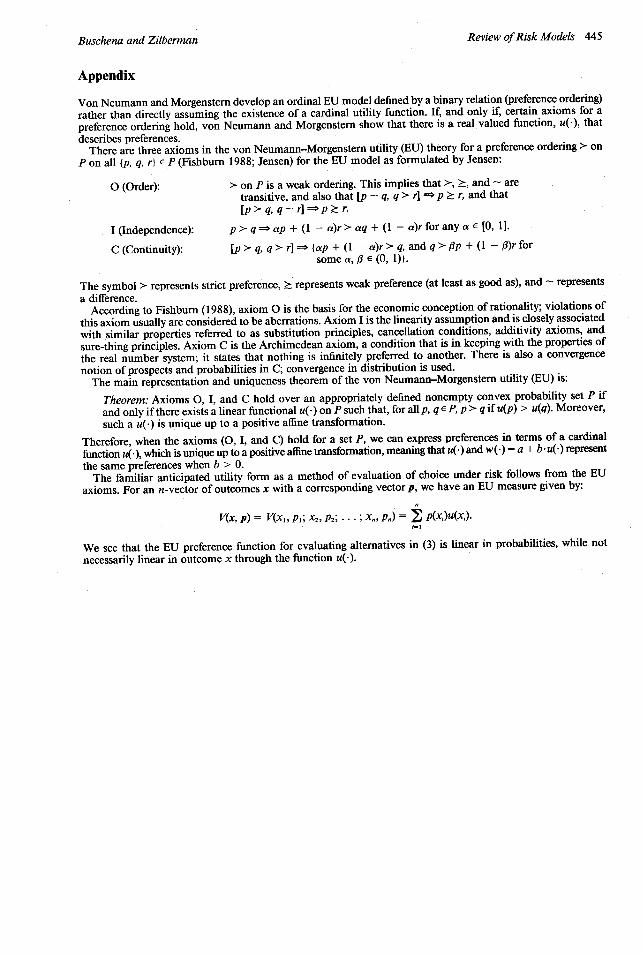

Appendix

Von Neumann and Morgenstern develop an ordinal EU model defined by a binary relation (preference ordering)rather than directly assuming the existence of a cardinal utility function. If, and only if, certain axioms for apreference ordering hold, von Neumann and Morgenstern show that there is a real valued function, u(-), that

describes preferences.There are three axioms in the von Neumann-Morgenstern utility (EU) theory for a preference ordering > on

P on all {p, q, r} E P (Fishburn 1988; Jensen) for the EU model as formulated by Jensen:

O (Order): > on P is a weak ordering. This implies that >, >, and - aretransitive, and also that [p - q, q > r] = p e r, and that[p > q, q - r] p > r.

I (Independence): p > q =o ap + (1 - a)r > aq + (1 - a)r for any a E [0, 1].

C (Continuity): [p > , q > r] = {ap + (1 - a)r > q, and q > Up + (1 -f)r forsome a, e E (0, 1)}.

The symbol > represents strict preference, > represents weak preference (at least as good as), and - representsa difference.

According to Fishbum (1988), axiom O is the basis for the economic conception of rationality; violations of

this axiom usually are considered to be aberrations. Axiom I is the linearity assumption and is closely associatedwith similar properties referred to as substitution principles, cancellation conditions, additivity axioms, and

sure-thing principles. Axiom C is the Archimedean axiom, a condition that is in keeping with the properties of

the real number system; it states that nothing is infinitely preferred to another. There is also a convergencenotion of prospects and probabilities in C; convergence in distribution is used.

The main representation and uniqueness theorem of the von Neumann-Morgenstern utility (EU) is:

Theorem: Axioms 0, I, and C hold over an appropriately defined nonempty convex probability set P if

and only if there exists a linear functional u(-) on P such that, for all p, q E P, p > q if u(p) > u(q). Moreover,such a u(.) is unique up to a positive affine transformation.

Therefore, when the axioms (0, I, and C) hold for a set P, we can express preferences in terms of a cardinal

function u(.), which is unique up to a positive affine transformation, meaning that u(-) and w(-) = a + b u(-) representthe same preferences when b > 0.

The familiar anticipated utility form as a method of evaluation of choice under risk follows from the EU

axioms. For an n-vector of outcomes x with a corresponding vector , we have an EU measure given by:

V(x, p) = V(x, p,; X2, P2; ... ; x, P,) = p(xi)u(x,).

We see that the EU preference function for evaluating alternatives in (3) is linear in probabilities, while notnecessarily linear in outcome x through the function u(.).

Buschena and Zilberman