Embed Size (px)

Citation preview

WHAT IS DEFECT ?

Price of Non-Conformance

WHAT DO YOU THINK ABOUT?

1. Missing the key input product

2. Getting the wrong information from buyer

3. Passing the incomplete and inaccurate information to vendors (factories)

4. Lack of communication during the product development in Pre-Production and production dept.

5. Delay in reply during the materialization of enquiries to orders.

6. Non-availability of product specification

7. Not checking the product as per agreed specifications.

8. Not sharing the customer specification to vendors (factories)

9. Communicating the wrong production status of product

10. Do not forecast any delay during production and accordingly do not update the buyer.

11. No need to optimize the resources

12. Fire everyone from QC deptt. to avoid inspection.

QUALITY COSTS

The term “Quality Costs” is associated solely with defective product

a) the costs of making defective products

b) the costs of finding defective products

c) the costs of repairing defective products

d) the costs of avoiding defects

Cost of Quality is generally known as the sum of costs incurred to

prevent non-conformances and the costs incurred when non-

conformance in products and system occurs.

CATEOGIRES OF COST OF QUALITY

COST OF QUALITY

Cost of Non-ConformanceCost of Poor Quality

Cost of Conformance

External FailureCosts

Internal FailureCosts

AppraisalCosts

Prevention Costs

COST OF CONFORMANCE

The cost of doing things right the first time.

The cost of Prevention and Appraisal.

The cost incurred in efforts to maintain and improve quality.

COST OF CONFORMANCE

The cost incurred in order to maintain or improve quality.

1. PREVENTION COSTS

2. APPRAISAL COSTS

PREVENTION COSTS

Costs of all activities associated with reducing / preventing failures

or improving quality.

There are the costs of any action taken to investigate, prevent or

reduce the risk of non-conformity or defect.

EXAMPLES OF PREVENTION COSTS

Quality Training

Vendor Assurance / Rating

Quality Improvement Programs

Planning and Writing of Procedures and Instructions.

Collection, Analysis and Reporting of Quality Data

Design Review/New-Product Review

Design Qualification Tests

Quality Planning

Marketing Surveys/Research

Contract Review

Process Validation

Preventive Maintenance

SPC/Process Control

QA functions and salaries

Improvement Projects

APPRAISAL COSTS

Costs of all activities associated with measuring, evaluating or

auditing the conformance of product to quality requirements.

Costs of all activities incurred to discover the condition of the

product, mainly during the “first time though”.

These are the costs of evaluating the achievement of quality

requirements including the cost of verification and control

performed at any stage of the quality loop.

EXAMPLES OF APPRAISAL COSTS In-coming Inspection

In-process Inspection

Final Testing and Inspection

Production Trials

Field Performance Tests

Calibration

Laboratory Expenses

Third Party Product Cost

Review of Test and Inspection Data

Certification Cost

Product and Service Quality Audits

Qualification of Supplier product

QC Function Salaries and Expenditure

COST OF NON-CONFORMANCE

The costs of internal and external failures.

The cost resulting from products or services not conforming to

customer/user requirements.

The cost incurved as a result of things not being done right the first

time.

COST OF NON-CONFORMANCE

The costs incurred due to non-conformance in product or service prior and after shipment

1. INTERNAL FAILURE COSTS

2. EXTERNAL FAILURE COSTS

INTERNAL FAILURE COSTS

These are costs which would disappear if no defects existed in the

product prior to shipment to the customer.

The costs resulting from failing to conform to specified

requirement prior to delivery of product or the furnishing of a

customer to the customers.

These are the costs arising within the organization due to non-

conformity or defects at any style of the Quality loop.

EXAMPLES OF INTERNAL FAILURE COSTS

Rework

Scrape/Rejects

Downtime

Sub-contractors Faults

Replacement of Purchase Materials

Defect/Failure Analysis

Re-inspection and Re-testing

Down grading

Accidents

In proper Invoicing

Disposition Costs

Yield Losses

Excessive Inventory Costs

Overtime Costs Due to Poor Planning

Product/Service Design Failure

Corrective Actions and Redesign

EXTERNAL FAILURE COSTS

These costs resulting from failing to conform to specified

requirements after the delivery.

These costs also would disappear if there were no defects.

These are the costs arising after delivery to the customer due to

non-conformities.

EXAMPLES OF EXTERNAL FAILURE COSTS

Complaints

Warranty Claims

Bad Debt

Returned Material

Concessions / Quality rebate

Loss of sale

Product liability

Penalties

Loss of Customer/user good will (Administration Costs)

Field repairs/reworks

Overdue Accounts receivable

Equipment failure at customer end

MODEL FOR OPTIMUM QUALITY COSTS:

CO

ST P

ER G

OO

D U

NIT

OF

PRO

DU

CT

QUALITY OF CONFORMANCE, %0 100

COSTS OF APPRAISALPLUS PREVENTION

FAILURECOSTS

TOTAL QUALITYCOSTS

TOoo

TOoo

(a) TRADITIONAL PROCESSES

MODEL FOR OPTIMUM QUALITY COSTS:

CO

ST P

ER G

OO

D U

NIT

OF

PRO

DU

CT

QUALITY OF CONFORMANCE, %0 100

COSTS OF APPRAISALPLUS PREVENTION

FAILURECOSTS

TOTAL QUALITYCOSTS

(b) EMERGING PROCESSES

OPTIMUM SEGMENT OF QUALITY COST MODEL

Zone of Improvement Zone of Indifference Zone of High Appraisal

Projects Costs

Failure Costs > 70% Failure Cost ~ 50% Failure Costs < 40%

Prevention < 10% Prevention ~ 10% Appraisal > 50%

Find Break Through If no Profitable Study Cost Per Defect

Projects; Pursue Projects can be Found, Detected, Verify Validity of

Shift Emphasis to Control Standards; Reduce

Inspection; Try Audit of

Decisions

TOTAL QUALITY COSTS

OPTIMUM

100% Defective Quality of Conformance 100% Good

QUALITY COSTS DATA SOURCES

1. Established accounts

2. Analysis of ingredients of established accounts

3. Basic accounting documents

4. Estimates

a) Temporary records

b) Work sampling

c) Allocation

d) Standard cost data

e) Opinion of knowledgeable persons

QUANTIFICATION OF COST OFQUALITY (COQ)

Step 1: Source of COC and CONC Data

Production Records

QC Records

Operation Records

Accounting Records

Step 2: Develop and Formulate Accounting Basis

Step 3: Executive Costing of COQ Items

Whole Account

This method requires gathering existing financial data from company accounts. If accounts are set up to capture costs, such as training and rework, information from the accounts can be used to measure COQ.

Unit Pricing

This method is effective when a defect or problem is recurring. To use defect pricing, simply multiply the cost of one defective unit by number of defective units.

QUANTIFICATION OF COST OFQUALITY (COQ)

Whole Person

This method is used when people are employed is recurring. To use purpose of working on or handling defects.

Labour / Resource Claiming

This method involves calculating actual expenditure on a specific activity, such as the amount of time spent by an employee performing a task or the amount of financial outlay for a one-time expense. This information might come from time sheet, vouchers or any other method for determining exactly how much was spent.

INTREPRETATION AND PRESENTATION TO MANAGEMENT

Quality Costs as a percent of Sales

= Total Quality Costs x 100

Net Sales

Quality Costs Compared to Profit

= Total Quality Costs x 100

Net Profit

Quality Costs compared to the magnitude of current problems in

terms of

a) number of employees

b) number of inventory items.

c) space

INTREPRETATION AND PRESENTATION TO MANAGEMENT

Quality Costs as a percent of Manufacturing Costs

= Total Quality Costs x 100

Total manufacturing Costs

EXERCISE NO. 2

SAMPLE COST OF QUALITY SHEET

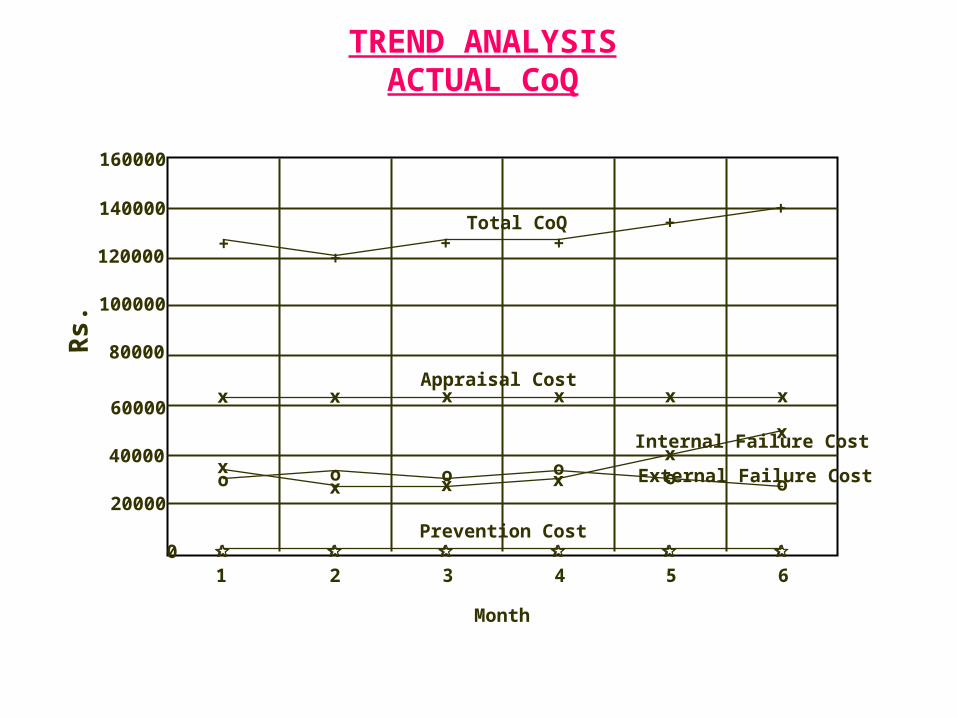

TREND ANALYSISACTUAL CoQ

160000

140000

120000

100000

80000

60000

40000

20000

0

++

x

x

o

x

o

x

+ ++

+

x x x x

1 2 3 4 5 6

oxox o

x

o

x

Prevention Cost

Appraisal Cost

Total CoQ

Internal Failure Cost

External Failure Cost

Month

Rs.

TREND ANALYSISCoQ as %age of Sales

0

++

x

x

o

x

o

x

++

+ +

x x x x

1 2 3 4 5 6

oxox

ox

o

x

Prevention Cost

Appraisal Cost

Total CoQ

Internal Failure Cost

External Failure Cost

Months

%ag

e of

Sal

es

1

2

3

4

5

6

7

8

9