Embed Size (px)

Citation preview

www.corporate-env-strategy.comCorporate Environmentalism

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002) 4091066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

What is Driving CorporateEnvironmentalism: Opportunity or

Threat?

Madhu Khanna* and Wilma Rose Q. Anton

Environmental management systems (EMSs) can differ considerably in the mix of practicesand the number of practices adopted by firms. This paper explores the various incentivesmotivating adoption of different types of practices by a sample of Standard & Poor’s 500firms and provides an explanation for why firms adopt practices selectively. Observable firmcharacteristics, proxies for the incentives faced by firms, are used to determine the types offirms more likely to adopt certain types of practices. We find that practices, such as havingan internal environmental policy, corporate environmental standards and environmentalauditing are motivated more strongly by regulatory pressures, while practices such as totalquality environmental management and environmental reporting are motivated more stronglyby the potential for gaining competitive advantage and improving relations with stakeholders.� 2002 Elsevier Science Inc. All rights reserved.

Madhu Khanna is an Associate Professor at theDepartment of Agricultural and Consumer Eco-nomics, University of Illinois at Urbana-Cham-paign.

Wilma Rose Q. Anton is an Assistant Professorat the Department of Economics, University ofCentral Florida in Orlando.

*Corresponding Author: 440 Mumford Hall, 1301 W.Gregory Dr., Urbana, IL 61801, USA.Tel.: q1-217-333-5176;fax: q1-217-333-5502;E-mail: [email protected].

There is now an increasing shift in thecorporate approach to environmental con-cerns from reactive compliance with environ-mental regulations to voluntary proactive ef-forts to improve environmental performanceand go beyond-compliance. A growing num-ber of firms are participating in voluntarytrade association programs that emphasizecodes of environmental management, seek-ing international certification by adopting theISO 14001 system for environmental man-agement, and developing their own environ-mental management systems (EMSs). EMSsrepresent an organizational change withinfirms and a self-motivated effort at internal-izing environmental externalities by adoptingmanagement practices that integrate envi-ronment and production decisions, which

Corporate Environmentalism

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002)4101066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

Table 1 Description of Environmental Management Practices

Variable Description of the Variable

Type I PracticesStaff Firm has an environmental staff of more than 50Directors Firm has more than 3 environmental directorsPolicy Firm has a formal written policy and codes of conduct on environmental issuesCorp. Stds. Firm applies uniform standards to environmental practices worldwideAudits Firm conducts audits to assess compliance with environmental regulationsReserves Firm sets aside funds to cover the costs of penalties for environmental violation

or remediation activitiesInsurance Firm purchases insurance to meet unexpected environmental liabilities

Type II PracticesTQEM Firm applies total quality management philosophy to environmental managementPayments Firm provides incentive compensation to employees whose efforts lead to

achievement of specific environmental goalsSuppliers Firm evaluates its environmental risks when selecting its suppliersPartners Firm evaluates its environmental risks when selecting its partnersClients Firm evaluates its environmental risks when selecting its clientsReport Firm regularly releases reports about its environmental performance and activities

Each of these variables takes a value of 1 if adopted and 0 otherwise

identify opportunities for pollution reductionand enable the firm to make continuousimprovements in production methods andenvironmental performance. EMSs consist ofa suite of environmental management prac-tices (EMPs) such as formally articulatingenvironmental goals and plans; implementingthose plans by assigning responsibility andproviding resources, training and incentivesto employees; and establishing organization-al structures to gather information and trackprogress towards meeting environmental tar-gets as well as to improve relations withstakeholders and clients.

Firms have considerable flexibility in the de-sign of their EMS. The mix and the numberof EMPs adopted can vary markedly acrossfirms. This paper seeks to explain the ob-served selectivity in the EMPs that constitutethe EMSs adopted by a sample of Standardand Poor’s (S&P) 500 firms for 1994 and1995. In particular, we examine how the fac-tors motivating adoption of different EMPsdiffer and whether the impact of regulatoryand market based pressures on the adoptiondecision varies across EMPs. A broad rangeof observable firm characteristics are usedas proxies for market pressures from con-

sumers, investors and a competitive market,and for regulatory pressures from existingand anticipated mandatory regulations. Thedifferential influence of these characteristicson incentives to adopt different types ofEMPs is used to draw inferences about theextent to which market-opportunities andyorregulatory threat are driving the design of theEMS as reflected in the combination of man-agement practices chosen by firms. This pa-per extends existing studies that have eithersought to explain motivations for participa-tion in voluntary programs (see survey1) oradoption of a single EMP2 or a set of EMPs(without distinguishing among different typesof practices).3

Motivations for SelectiveEnvironmental ManagementEMSs are a cluster of EMPs that indicatemultifaceted efforts that are proactive andanticipative in orientation. We focus here ona set of thirteen practices that are definedand listed in Table 1. We group these practic-es into two categories, Types I and II. Thefirst category includes management practic-es such as designating personnel specializedin addressing environmental issues, havingan environmental policy, setting corporation-

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002) 4111066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

Corporate Environmentalism

wide internal standards, environmental audit-ing, setting aside funds to cover risks offuture environmental liability costs and buy-ing insurance to cover liability or remediationcosts of environmental incidents. Type IIEMPs include training and rewarding workersto find opportunities to prevent pollution,applying the philosophy of Total Quality Man-agement (TQM) to making continuous effortsat improving performance across the firm’sactivities and improving environmental per-formance, evaluating the environmental per-formance of potential suppliers, partners andclients while making strategic business de-cisions and publishing environmental reportsthat benchmark a firm’s commitment andperformance. Firms may adopt EMPs selec-tively both within a category and acrosscategories.

We hypothesize that Type I EMPs are morelikely to have been adopted in response toregulatory pressures and requirements. Inter-nal environmental policies and standards arelikely to be influenced by expectations forenvironmental performance set by mandatoryregulations. In a survey of Fortune 500 com-panies in 1990, legal and regulatory require-ments were most frequently chosen as themost important determinant of the size of theenvironmental, health and safety staff.4 Envi-ronmental audits were originally undertakenby firms to determine if they were complyingwith regulations on their pollutants.5. Auditsare also required to enable firms to meet theirlegal obligation to report their toxic releasesto the Toxics Release Inventory (TRI) and toreport any prospective environmental liabili-ties to the Securities and Exchange Commis-sion. Additionally, environmental regulationsbased on the Comprehensive EnvironmentalResponse, Compensation, and Liability Act(CERCLA and commonly known as Super-fund) and the Resource Conservation andRecovery Act (RCRA) are making firms moreaware of penalties and liabilities that couldbe imposed on them for environmental con-tamination. This has led to efforts to improve

environmental safety and to set aside fundsto cover risks of environmental accidents.

«environmentalregulations«are making firmsmore aware of penalties and

liabilities that could beimposed«

w1xWhile auditing and preparedness for environ-mental crisis provides an internal disciplinefor the firm, their usefulness in improving thequality of management can be enhanced byfollow up actions such as those embodied inType II practices like as Total Quality Environ-mental Management (TQEM) and using en-vironmental data to train employees to pre-vent pollution. TQEM involves continuousefforts at improving performance and reduc-ing production waste and defects. Addition-ally, firms can provide incentives to employ-ees to improve environmental performanceby linking it to their compensation. Evaluatingenvironmental risks when choosing partners,suppliers and clients are other ways to iden-tify opportunities to reduce waste, preventpollution and increase efficiency. A growingnumber of firms are publishing environmentalreports as a means of communicating afirm’s level of environmental performance toconcerned stakeholders.6 Thus, Type II prac-tices represent efforts to improve a firm’scompetitiveness by establishing a positivereputation and image on environmental pro-tection, gain stakeholder goodwill, lowercosts through continuous improvements inwaste reduction and to move the firm beyondcompliance. In reality, the adoption of bothType I and Type II practices is not likely tobe driven purely by either regulatory require-ments or by a desire to capitalize on oppor-tunities to improve competitiveness but by acombination of both types of incentives.However, our purpose here is to examinewhether certain factors are stronger in influ-encing the adoption of a given type of prac-

Corporate Environmentalism

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002)4121066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

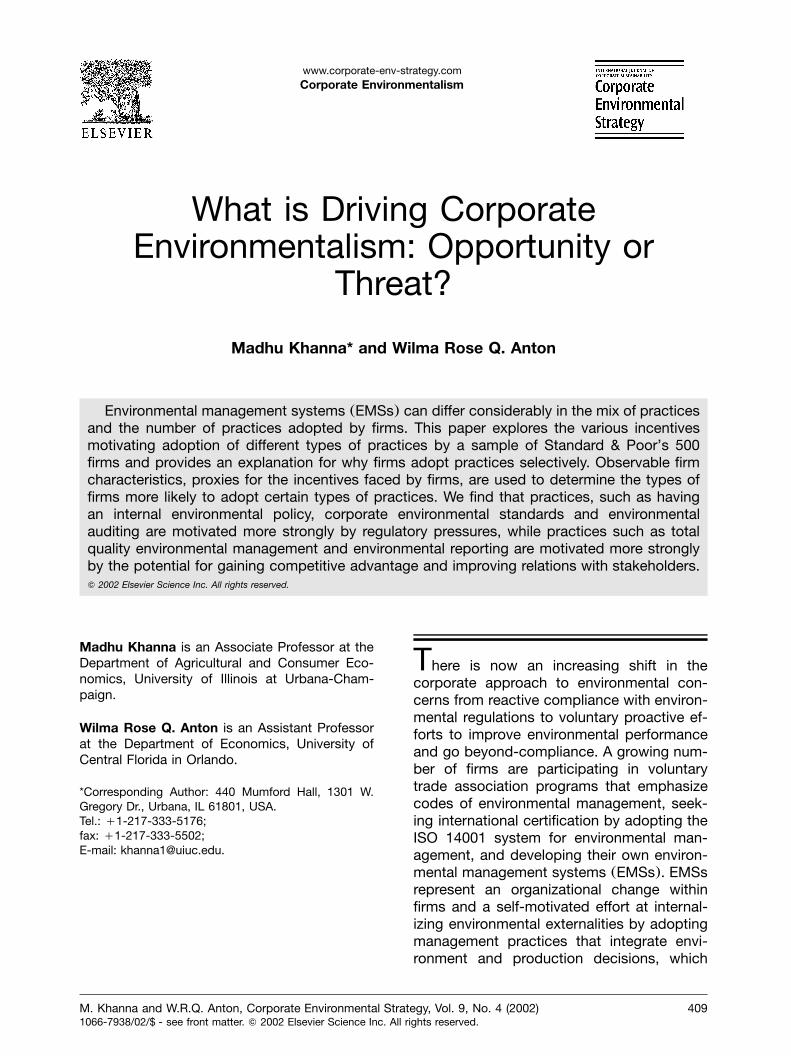

Fig. 1 Rate of Adoption of EMPs.

tices than other factors. We therefore test thefollowing hypotheses:

Hypothesis 1: A threat of environmental lia-bilities and high costs of compliance withexisting and anticipated mandatory regula-tions are likely to induce greater adoption ofType I practices instead of Type II practices.

Hypothesis 2: The opportunity for improvingcompetitiveness and gaining an environmen-tally friendly reputation with consumers, in-vestors and the public is likely to inducegreater adoption of Type II practices as com-pared to Type I practices.

DataData on management practices adopted areobtained from a 1994–1995 survey of S&P500 firms conducted by the Investor Re-search Responsibility Center (IRRC) andcompiled in the Corporate EnvironmentalProfile Directories. Of the S&P 500 firmssurveyed by the IRRC, only firms that re-sponded to the survey and reported to theTRI and for which financial data are availableare included in this study. This results in asample of 176 firms for 1995 and 159 firmsfor 1994, with 156 firms having observationsfor both years. The explanatory variables thatwe use in this study include environmentalperformance and financial characteristicsthat are measured with a five-year lag (1989and 1990). Environmental performance dataare obtained from the TRI database that

contains facility-level information on on-sitereleases and off-site transfers of chemical-specific toxic pollutants. Financial informa-tion, on the other hand, is obtained from thepublicly available S&P 500 and Super Com-pustat databases.

The survey inquires about the adoption de-cision of firms for 13 EMPs listed in Table 1.There is variability in the extent to whicheach of these practices is adopted by firmsin our sample. This is shown in Fig. 1 using1995 data. We find that certain managementpractices are adopted more frequently thanothers; about 90 percent had a formal envi-ronmental policy and 70 percent appliedTQM principles, while less than 40 percentimposed uniform environmental standardsacross the corporation and regularly releasedenvironmental reports in 1995.

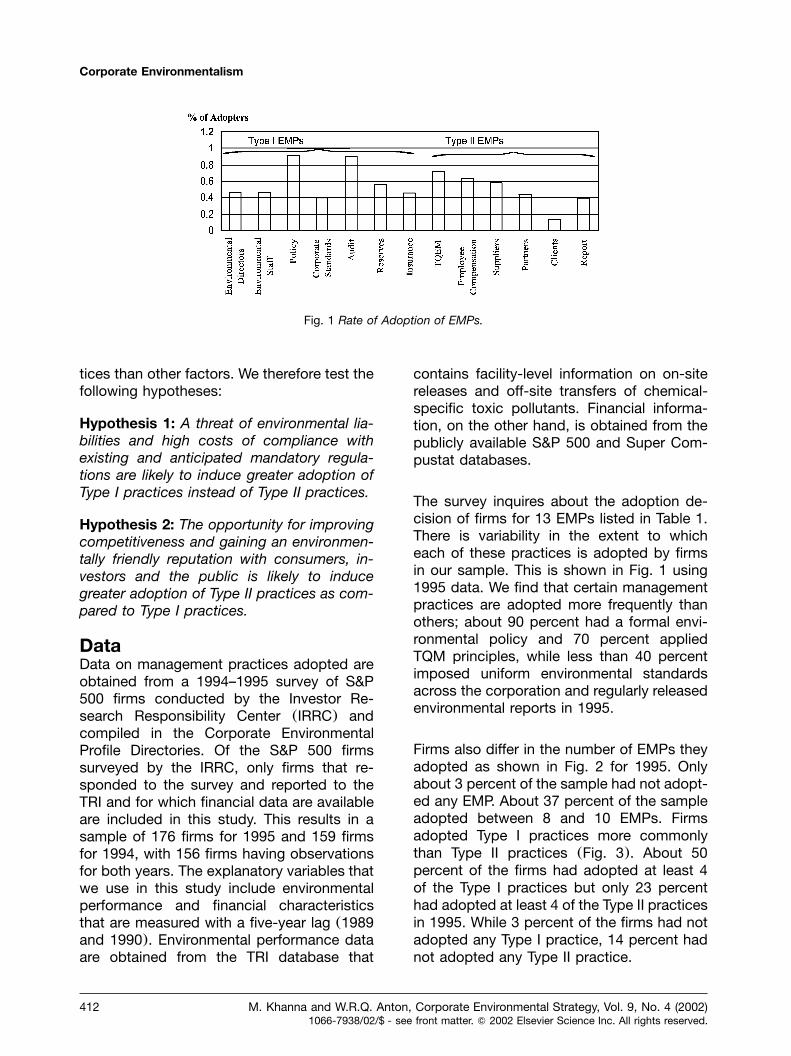

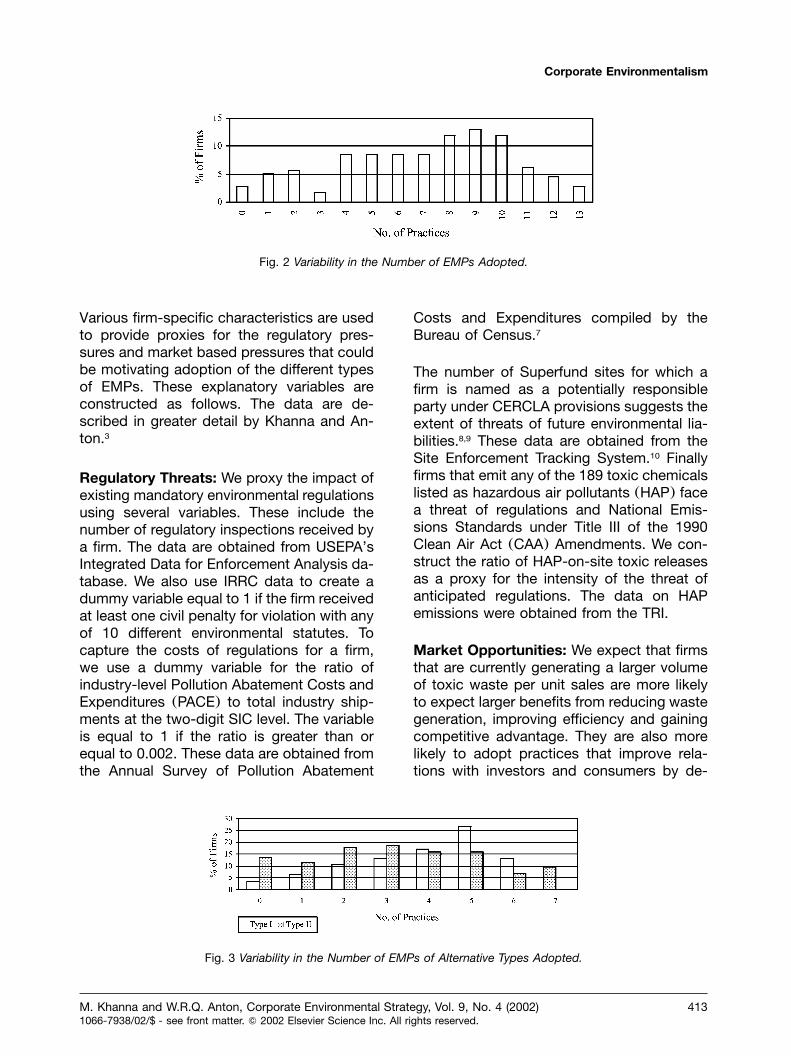

Firms also differ in the number of EMPs theyadopted as shown in Fig. 2 for 1995. Onlyabout 3 percent of the sample had not adopt-ed any EMP. About 37 percent of the sampleadopted between 8 and 10 EMPs. Firmsadopted Type I practices more commonlythan Type II practices (Fig. 3). About 50percent of the firms had adopted at least 4of the Type I practices but only 23 percenthad adopted at least 4 of the Type II practicesin 1995. While 3 percent of the firms had notadopted any Type I practice, 14 percent hadnot adopted any Type II practice.

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002) 4131066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

Corporate Environmentalism

Fig. 2 Variability in the Number of EMPs Adopted.

Fig. 3 Variability in the Number of EMPs of Alternative Types Adopted.

Various firm-specific characteristics are usedto provide proxies for the regulatory pres-sures and market based pressures that couldbe motivating adoption of the different typesof EMPs. These explanatory variables areconstructed as follows. The data are de-scribed in greater detail by Khanna and An-ton.3

Regulatory Threats: We proxy the impact ofexisting mandatory environmental regulationsusing several variables. These include thenumber of regulatory inspections received bya firm. The data are obtained from USEPA’sIntegrated Data for Enforcement Analysis da-tabase. We also use IRRC data to create adummy variable equal to 1 if the firm receivedat least one civil penalty for violation with anyof 10 different environmental statutes. Tocapture the costs of regulations for a firm,we use a dummy variable for the ratio ofindustry-level Pollution Abatement Costs andExpenditures (PACE) to total industry ship-ments at the two-digit SIC level. The variableis equal to 1 if the ratio is greater than orequal to 0.002. These data are obtained fromthe Annual Survey of Pollution Abatement

Costs and Expenditures compiled by theBureau of Census.7

The number of Superfund sites for which afirm is named as a potentially responsibleparty under CERCLA provisions suggests theextent of threats of future environmental lia-bilities.8,9 These data are obtained from theSite Enforcement Tracking System.10 Finallyfirms that emit any of the 189 toxic chemicalslisted as hazardous air pollutants (HAP) facea threat of regulations and National Emis-sions Standards under Title III of the 1990Clean Air Act (CAA) Amendments. We con-struct the ratio of HAP-on-site toxic releasesas a proxy for the intensity of the threat ofanticipated regulations. The data on HAPemissions were obtained from the TRI.

Market Opportunities: We expect that firmsthat are currently generating a larger volumeof toxic waste per unit sales are more likelyto expect larger benefits from reducing wastegeneration, improving efficiency and gainingcompetitive advantage. They are also morelikely to adopt practices that improve rela-tions with investors and consumers by de-

Corporate Environmentalism

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002)4141066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

veloping an environmentally friendly image.We distinguish between two types of toxicwastes, those released on-site and thosetransferred off-site for end-of-pipe abatement

The number of Superfundsites«suggests the extent of wa

firm’sx threats of futureenvironmental liabilities.

and disposal since they are likely to generatedifferent reactions from firms and the public.Unlike on-site releases, off-site disposal oftoxic waste is regulated under RCRA andfirms face a cost for shipping wastes off-siteand for disposal at the end-of-the-pipe. Off-site transfers of toxic wastes were obtainedat the parent company level by aggregatingthe data on wastes of all toxic pollutantsbeing sent for treatment, incineration, energyrecovery and disposal by each facility. On-site toxic emissions data were obtained byaggregating all releases to air, land, waterand underground injections of all TRI chemi-cals by each facility of a parent company.

w2xWe also expect that firms with a low salesper unit asset ratio, which could be indicativeof idle capacity and poorer financial health,are more likely to seek to improve competi-tive advantage by improving efficiency andstakeholder relations. Such firms are alsolikely to be more dependent on capital mar-kets and thereby more concerned about neg-ative investor and market reactions.

Other Firm-Specific Characteristics: Wecontrol for other firm characteristics thatcould influence adoption of both types ofEMPs equally strongly. These include themultinational status of the firm, the type ofgood (final or intermediate) that it produces,the age of its assets and its innovativeness.We proxy the multinational status of a firmby the proportion of its facilities located out-side the U.S. We expect that firms that pro-duce final goods are closer to consumers.

We use the 4-digit secondary SIC code ofthe firm to classify them into final goods andintermediate goods. The variable is equal to1 if a firm is primarily selling final products(e.g. pharmaceutical preparations, cosmet-ics, food products) and providing services(e.g. retail stores, restaurants, banks) directlyto consumers. The age of a firm’s assets ismeasured by dividing the total assets of afirm by its gross assets. Age of assets takesa value between 0 and 1, with higher valuesindicating newer plant and equipment, morecurrent assets and smaller accumulated de-preciation. Innovativeness of the firm is prox-ied by its research and development expen-ditures per unit sales.

Empirical MethodWe use the count of EMPs of each typeadopted as an index of the extent to whicha firm is adopting Type I and Type II practices.Since the difference between adopting 3 and4 EMPs is not the same as that betweenadopting 2 and 3 EMPs, we use the OrderedProbit (OP) method (instead of ordinary leastsquares) to examine the factors influencingthe extent to which firms adopt practices ofeach of the two types. The OP method con-siders the number of practices adopted asbeing an ordinal index of the scope of theEMS. Higher sums of EMPs adopted corre-spond to a higher range of the scope of theEMS. The ordinal index is specified as alinear function of explanatory variables, aparameter vector and a stochastic error termthat captures any unobserved explanatoryvariables or measurement errors. Estimationof the parameters reported in Table 2 isundertaken by maximum likelihood methods.

ResultsWe use two alternative specifications to ex-amine the impact of various incentives moti-vating the scope of adoption of Type I and IIpractices. The specification in Model II differsfrom that in Model I in that it also includes aproxy for the threat of anticipated HAP reg-ulations as an explanatory variable. Resultsof the estimation (Table 2) show that regu-

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002) 4151066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

Corporate Environmentalism

Table 2 The Determinants of the Type of EMPs Adopted

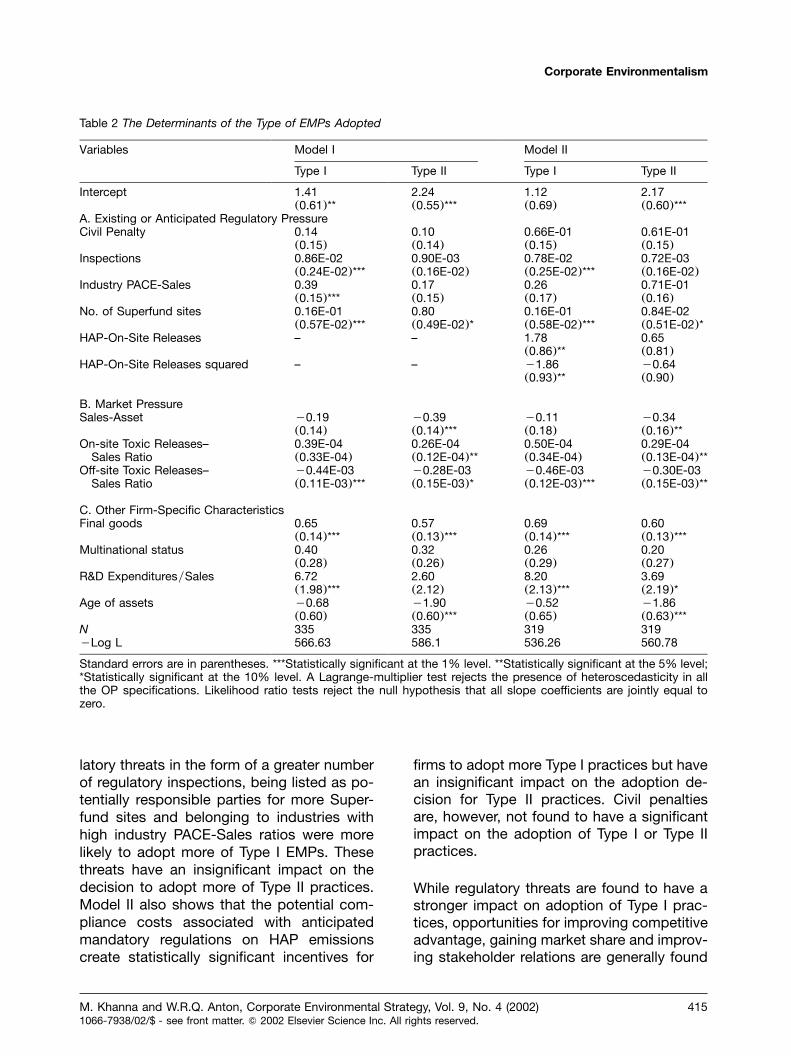

Variables Model I Model II

Type I Type II Type I Type II

Intercept 1.41 2.24 1.12 2.17(0.61)** (0.55)*** (0.69) (0.60)***

A. Existing or Anticipated Regulatory PressureCivil Penalty 0.14 0.10 0.66E-01 0.61E-01

(0.15) (0.14) (0.15) (0.15)Inspections 0.86E-02 0.90E-03 0.78E-02 0.72E-03

(0.24E-02)*** (0.16E-02) (0.25E-02)*** (0.16E-02)Industry PACE-Sales 0.39 0.17 0.26 0.71E-01

(0.15)*** (0.15) (0.17) (0.16)No. of Superfund sites 0.16E-01 0.80 0.16E-01 0.84E-02

(0.57E-02)*** (0.49E-02)* (0.58E-02)*** (0.51E-02)*HAP-On-Site Releases – – 1.78 0.65

(0.86)** (0.81)HAP-On-Site Releases squared – – y1.86 y0.64

(0.93)** (0.90)

B. Market PressureSales-Asset y0.19 y0.39 y0.11 y0.34

(0.14) (0.14)*** (0.18) (0.16)**On-site Toxic Releases– 0.39E-04 0.26E-04 0.50E-04 0.29E-04

Sales Ratio (0.33E-04) (0.12E-04)** (0.34E-04) (0.13E-04)**Off-site Toxic Releases– y0.44E-03 y0.28E-03 y0.46E-03 y0.30E-03

Sales Ratio (0.11E-03)*** (0.15E-03)* (0.12E-03)*** (0.15E-03)**

C. Other Firm-Specific CharacteristicsFinal goods 0.65 0.57 0.69 0.60

(0.14)*** (0.13)*** (0.14)*** (0.13)***Multinational status 0.40 0.32 0.26 0.20

(0.28) (0.26) (0.29) (0.27)R&D ExpendituresySales 6.72 2.60 8.20 3.69

(1.98)*** (2.12) (2.13)*** (2.19)*Age of assets y0.68 y1.90 y0.52 y1.86

(0.60) (0.60)*** (0.65) (0.63)***N 335 335 319 319yLog L 566.63 586.1 536.26 560.78

Standard errors are in parentheses. ***Statistically significant at the 1% level. **Statistically significant at the 5% level;*Statistically significant at the 10% level. A Lagrange-multiplier test rejects the presence of heteroscedasticity in allthe OP specifications. Likelihood ratio tests reject the null hypothesis that all slope coefficients are jointly equal tozero.

latory threats in the form of a greater numberof regulatory inspections, being listed as po-tentially responsible parties for more Super-fund sites and belonging to industries withhigh industry PACE-Sales ratios were morelikely to adopt more of Type I EMPs. Thesethreats have an insignificant impact on thedecision to adopt more of Type II practices.Model II also shows that the potential com-pliance costs associated with anticipatedmandatory regulations on HAP emissionscreate statistically significant incentives for

firms to adopt more Type I practices but havean insignificant impact on the adoption de-cision for Type II practices. Civil penaltiesare, however, not found to have a significantimpact on the adoption of Type I or Type IIpractices.

While regulatory threats are found to have astronger impact on adoption of Type I prac-tices, opportunities for improving competitiveadvantage, gaining market share and improv-ing stakeholder relations are generally found

Corporate Environmentalism

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002)4161066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

to have a stronger impact on the adoption ofType II practices. Firms with low sales-assetratios (or high capital-output ratios) andthose with high on-site releases per unit salesare more likely to adopt Type II practices.The incentives provided by these variablesfor adopting Type I practices are insignificant.

We find that firms with low off-site transfersin the past were more likely to adopt a largernumber of both Type I and II practices al-though the impact on Type I practices wasstronger and more statistically significant.This could indicate that firms that were facinghigh costs of off-site transfers and had al-ready reduced their generation through othermethods were now seeking more innovative

«regulatory threats areencouraging environmentally

friendly organizational changeswithin the firm that enhance

compliance and reduce the threatof potential liabilities«

and cost-effective ways to deal with them.Similarly, firms that were final good producerswere more likely to adopt more of both TypeI and II practices. Such firms may perceivethat consumers will value the entire range ofefforts undertaken by them that improve theircompliance records as well as their efficiencyand reduce waste generation.

w3xOur analysis also shows that firms with olderequipment were more likely to adopt moreType II EMPs. This suggests that firms withlower replacement costs were more likely toimplement management strategies thatproactively target pollution prevention andimprovement in the efficiency of the produc-tion system. The level of innovativeness of afirm is also a significant driving force behindthe adoption of more Type I and Type IIEMPs, although the effect on the former ismore statistically significant. This could indi-

cate that innovative firms with higher re-search and development expenditures perunit output were directing their innovativeactivity more towards lowering the burdendue to regulations. Our analysis thus pro-vides support for the two hypotheses dis-cussed above. Adoption of Type I practicesis motivated more strongly by regulatorythreats, while adoption of Type II practicesappears to be motivated more strongly by adesire to capitalize on opportunities to gainmarket share, lower costs of production andgain investor and public confidence.

ConclusionsMany firms are adopting EMSs and makinginternally motivated efforts at solving environ-mental problems. However, firms have flexi-bility to create their own self-regulatorymechanisms and not all EMSs are the same.EMSs can vary considerably across firmsboth in the number of practices adopted andthe types of practices adopted. This paperseeks to explain the observed variations inthe types of EMPs adopted by firms and todetermine the types of firms more likely toadopt certain types of practices.

The results of our analysis show that highcosts of compliance, threats of liabilities,inspections and anticipated regulations pro-vide statistically significant incentives for theadoption of more Type I EMPs but have aninsignificant impact on the likelihood ofadopting Type II EMPs. On the other hand,firms with a lower sales-asset ratio and ahigh on-site toxic release per unit sales ratiowere more likely to adopt more of the TypeII practices, possibly with the expectationthat this would reduce wastes generation,increase efficiency, and improve marketshare and competitiveness. Some factorssuch as high costs of off-site transfers, closercontact with consumers and greater innova-tiveness provided incentives for adoption ofboth Type I and II EMPs.

Our analysis shows that the design and com-ponents of EMSs are reflective of the differ-

M. Khanna and W.R.Q. Anton, Corporate Environmental Strategy, Vol. 9, No. 4 (2002) 4171066-7938/02/$ - see front matter. � 2002 Elsevier Science Inc. All rights reserved.

Corporate Environmentalism

ential incentives firms face. Regulatorythreats and market opportunities create in-centives to adopt very different types ofEMPs, since these practices differ in thefunction they serve and in the benefits theyare expected to provide the firm. These find-ings have implications for the design of pol-icies targeted towards encouraging greateradoption of EMPs. They show that whileregulatory threats are encouraging environ-mentally friendly organizational changes with-in the firm that enhance compliance andreduce the threat of potential liabilities, theyare not likely to provide strong incentives toadopt practices that improve relations withthe public and that enhance production effi-ciency. Disclosure of environmental informa-tion to the public as well as competitivepressures are relatively more effective in in-ducing firms to adopt practices that canenable them to meet strategic business goalsby making continuous progress in improvingproduct quality and process efficiencythrough waste reduction. Both regulatorythreats and market opportunities play a com-plementary role by inducing adoption of dif-ferent types of EMPs and together they caninduce the adoption of more comprehensiveEMSs.

AcknowledgementsThe authors would like to acknowledge re-search funding provided by U.S. Environmen-tal Protection Agency (USEPA) National Cen-ter for Environmental Research, Science toAchieve Results (STAR) Program, Grant�R827919-01. Any opinions, findings, con-clusions, or recommendations expressed inthis publication are those of the authors anddo not necessarily reflect the view of theUSEPA.

Endnotes

1. M. Khanna, Non-Mandatory Approaches toEnvironmental Protection, Journal ofEconomic Surveys 15 (3) (2001) 291–324.

2. I. Henriques, P. Sadorsky, The Determinantsof an Environmentally Responsive Firm: AnEmpirical Approach, Journal ofEnvironmental Economics and Management30 (3) (1996) 381–395.

3. M. Khanna, W. Anton, CorporateEnvironmental Management: Regulatory andMarket-based Incentives, Land Economics(forthcoming, November 2002).

4. M. Flaherty, A. Rappaport, MultinationalCorporations and the Environment: A Surveyof Global Practices, The Center forEnvironmental Management, Tufts University,1991.

5. F. Cairncross, Green Inc.: A Guide toBusiness and the Environment, Island Press,Washington DC, 1995.

6. L.B. Larsen, Strategic Implication ofEnvironmental Reporting, CorporateEnvironmental Strategy 7 (2000) 276–287.

7. U.S. Bureau of the Census, CurrentIndustrial Reports: Pollution AbatementCosts and Expenditures: MA200(89)-1. U.S.Government Printing Office, Washington DC,1989–90.

8. M. Khanna, L. Damon, EPA’s Voluntary 33y50 Program: Impact on Toxic Releases andEconomic Performance of Firms, Journal ofEnvironmental Economics and Management37 (1) (1999) 1–25.

9. J. Videras, A. Alberini, The Appeal ofVoluntary Environmental Programs: WhichFirms Participate and Why?, ContemporaryEconomic Policy 18 (4) (2000) 449–461.

10. USEPA, Site Enforcement Tracking System(National) (for microcomputers), Office ofScience and Technology (Producer),National Technical Information Service,Virginia, 1996.