Embed Size (px)

Citation preview

1

Open innovation: Shifting the paradigm

to reap more benefits from R&D?

Prof. dr. Wim Vanhaverbeke Hasselt University

ESADE Business School National University of Singapore

IASP - Bangkok - November 27, 2012

What is Open Innovation?

“Open innovation is the use of purposive inflows and outflows of knowledge to accelerate internal innovation, and expand the markets for external use of innovation, respectively.”

Chesbrough, Vanhaverbeke, West Open Innovation: Researching a New Paradigm

(OUP, 2006)

A Closed Innovation System

Research Investigations

Development New Products /Services

The Market

Science &

Technology Base

R D Source: Henry Chesbrough

What changed? New Division of Innovation Labor n Increasingly mobile trained workers n More capable universities n Knowledge distributed more widely throughout

the world n Diminished US hegemony in many leading

technology fields n Erosion of oligopoly market positions n Deregulation (EU-liberalization) n Enormous increase in Venture Capital

Source: Henry Chesbrough

Current Market

Internal Technology

Base

R D

Inbound OI: Filling the gaps with external technology

Technology Insourcing

New Market

External Technology

Base External research projects

Venture investing

Technology in-licensing Technology acquisition

Source: H. Chesbrough, Sloan Management Review, Spring 2003

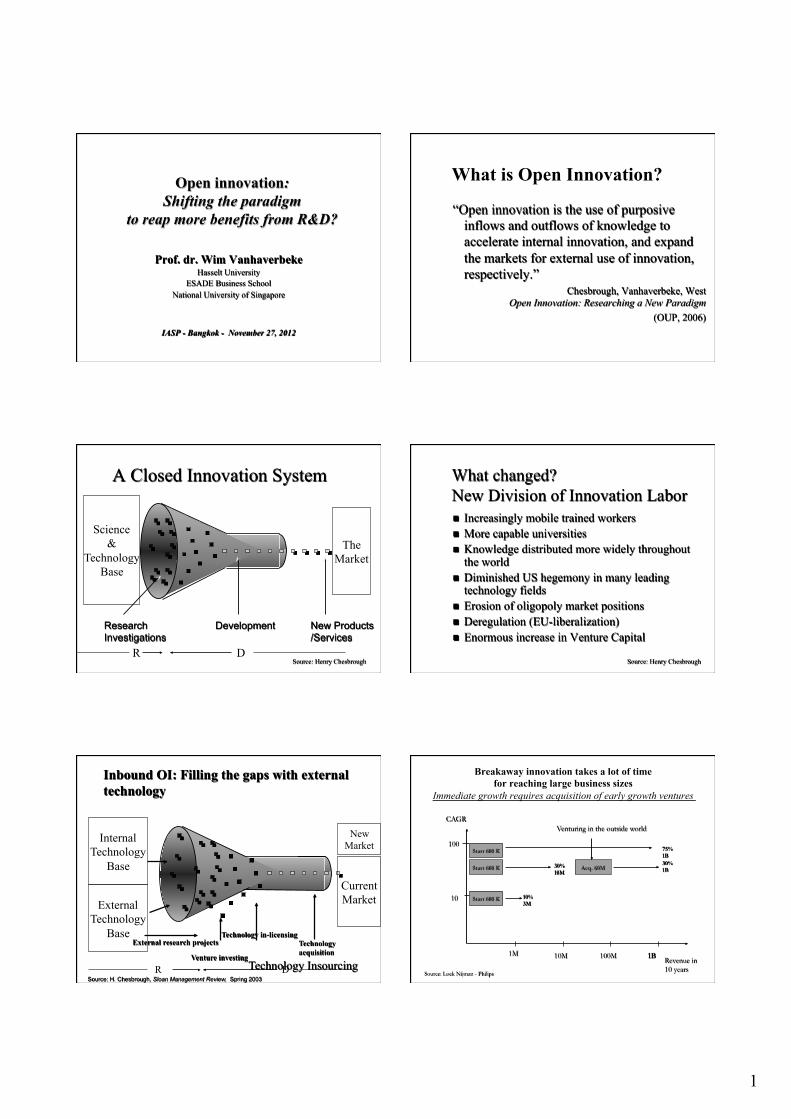

Breakaway innovation takes a lot of time for reaching large business sizes

Immediate growth requires acquisition of early growth ventures

Source: Loek Nijman - Philips

CAGR

Revenue in 10 years

100

10M 100M 1B

10

1M

Start 600 K

Start 600 K

Start 600 K

10% 3M

30% 10M

75% 1B

Acq. 60M 30% 1B

Venturing in the outside world

2

Current Market

Internal Technology

Base

R D

Outbound OI: Profiting from others’ use of your technology

Technology Insourcing

New Market

Technology Spin-offs

External Technology

Base

Other Firm’s Market

Licensing

Source: H. Chesbrough, Sloan Management Review, Spring 2003

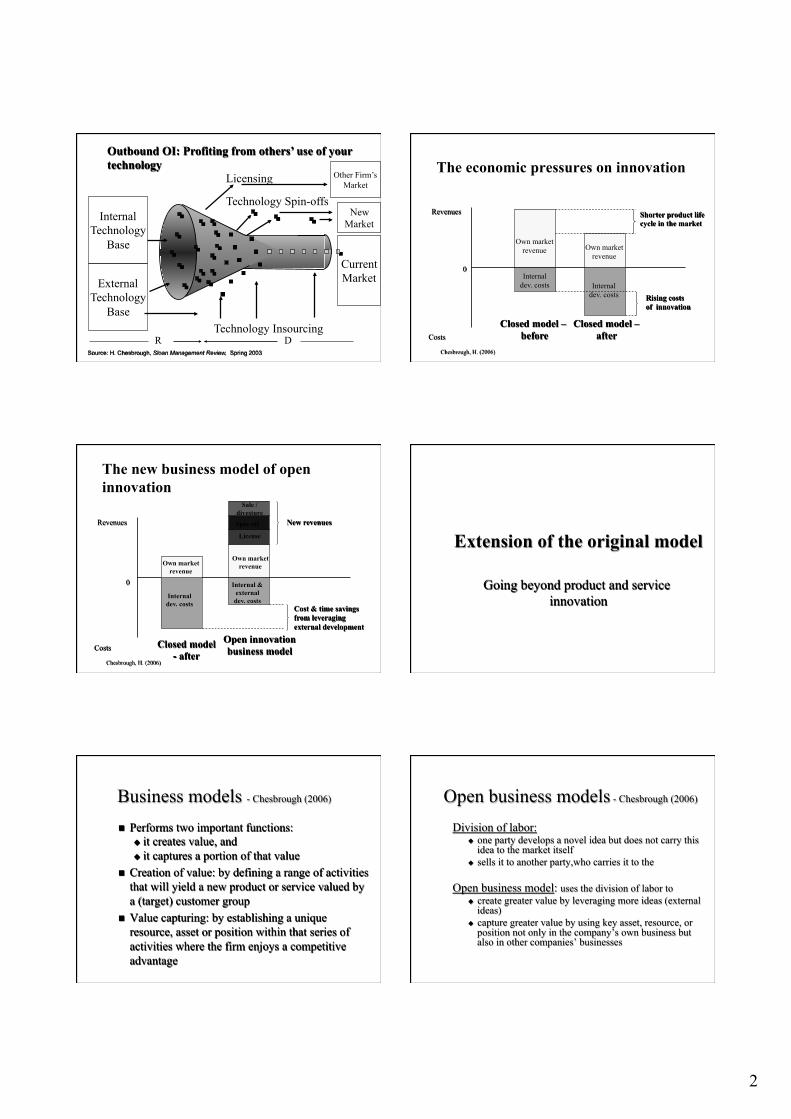

The economic pressures on innovation

Costs

Revenues

Own market revenue Own market

revenue

Internal dev. costs Internal

dev. costs

Closed model – before

Closed model – after

Shorter product life cycle in the market

Rising costs of innovation

Chesbrough, H. (2006)

0

The new business model of open innovation

Costs

Revenues

Own market revenue

Own market revenue

Internal dev. costs

Internal & external dev. costs

Closed model - after

Open innovation business model

New revenues

Cost & time savings from leveraging external development

License

Spin-off

Sale / divesture

Chesbrough, H. (2006)

0

Extension of the original model

Going beyond product and service innovation

Business models - Chesbrough (2006)

n Performs two important functions: u it creates value, and u it captures a portion of that value

n Creation of value: by defining a range of activities that will yield a new product or service valued by a (target) customer group

n Value capturing: by establishing a unique resource, asset or position within that series of activities where the firm enjoys a competitive advantage

Open business models - Chesbrough (2006)

Division of labor: u one party develops a novel idea but does not carry this

idea to the market itself u sells it to another party,who carries it to the

Open business model: uses the division of labor to u create greater value by leveraging more ideas (external

ideas) u capture greater value by using key asset, resource, or

position not only in the company’s own business but also in other companies’ businesses

3

Broadening the scope n OI when it is not related to your NPD:

u You are a service company with no technical expertise

u SME with insufficient technological expertise u Government agency:

t Nasa: new technologies may help you a lot in your mission as space agency

n Insourcing knowledge of others in an indirect way through an open business model (OBM)

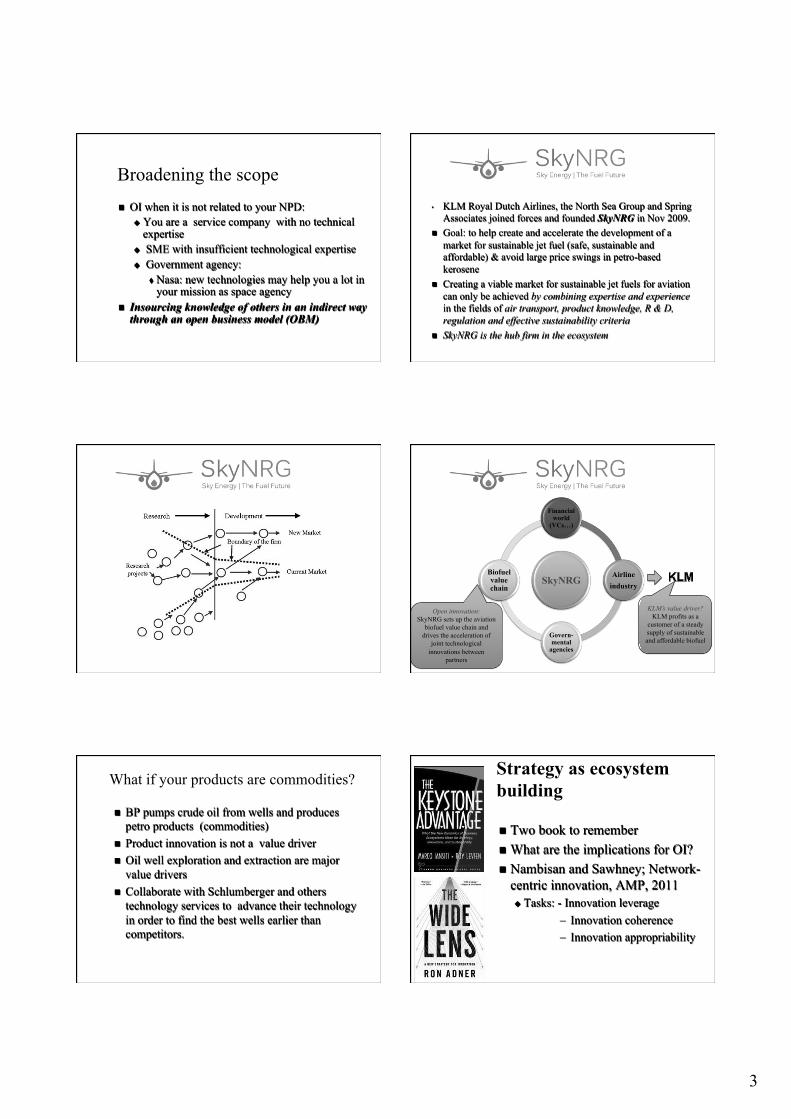

• KLM Royal Dutch Airlines, the North Sea Group and Spring Associates joined forces and founded SkyNRG in Nov 2009.

n Goal: to help create and accelerate the development of a market for sustainable jet fuel (safe, sustainable and affordable) & avoid large price swings in petro-based kerosene

n Creating a viable market for sustainable jet fuels for aviation can only be achieved by combining expertise and experience in the fields of air transport, product knowledge, R & D, regulation and effective sustainability criteria

n SkyNRG is the hub firm in the ecosystem

SkyNRG

Financial world

(VCs…)

Airline industry

Govern-mental

agencies

Biofuel value chain

KLM’s value driver? KLM profits as a

customer of a steady supply of sustainable and affordable biofuel

Open innovation: SkyNRG sets up the aviation

biofuel value chain and drives the acceleration of

joint technological innovations between

partners

What if your products are commodities?

n BP pumps crude oil from wells and produces petro products (commodities)

n Product innovation is not a value driver n Oil well exploration and extraction are major

value drivers n Collaborate with Schlumberger and others

technology services to advance their technology in order to find the best wells earlier than competitors.

Strategy as ecosystem building

n Two book to remember n What are the implications for OI? n Nambisan and Sawhney; Network-

centric innovation, AMP, 2011 u Tasks: - Innovation leverage

– Innovation coherence – Innovation appropriability

4

Some shortcomings of OI

n Only large, technology user firms in the picture u What about small, high-tech technology suppliers

n Only technology driven focus (upstream partners)? u What about downstream partners? (Experience lab?)

n Only firm level analysis: No eco-system or network perspective u How to build an OI perspective at the network level?

n Absence of the geographical dimension u How to organize open innovation close by and at large

distance?

Broadening the scope of OI

22

Global Local

Network

Firm

Individual Individual networks

Cross company teams

Local cooperation

Campus

Upstream partners

downstream partners

RIS NIS

National

Global economic trends

Virtual Networks e.g. LinkedIn

Cross company teams

Alliances

Your vision , your focus of a science park

n On which steps in the VC the campus is targeting at? n What are the benefits you want / can offer to the residents? n What is the optimal composition of campus residents? n Management: How to go from a closed to a open campus?

Benefits the HTC offers to its residents

24

Save on capital investments The Facilities

Outsourcing capabilities

Technology solutions

Value Network

The Services

The Experts

The Others

5

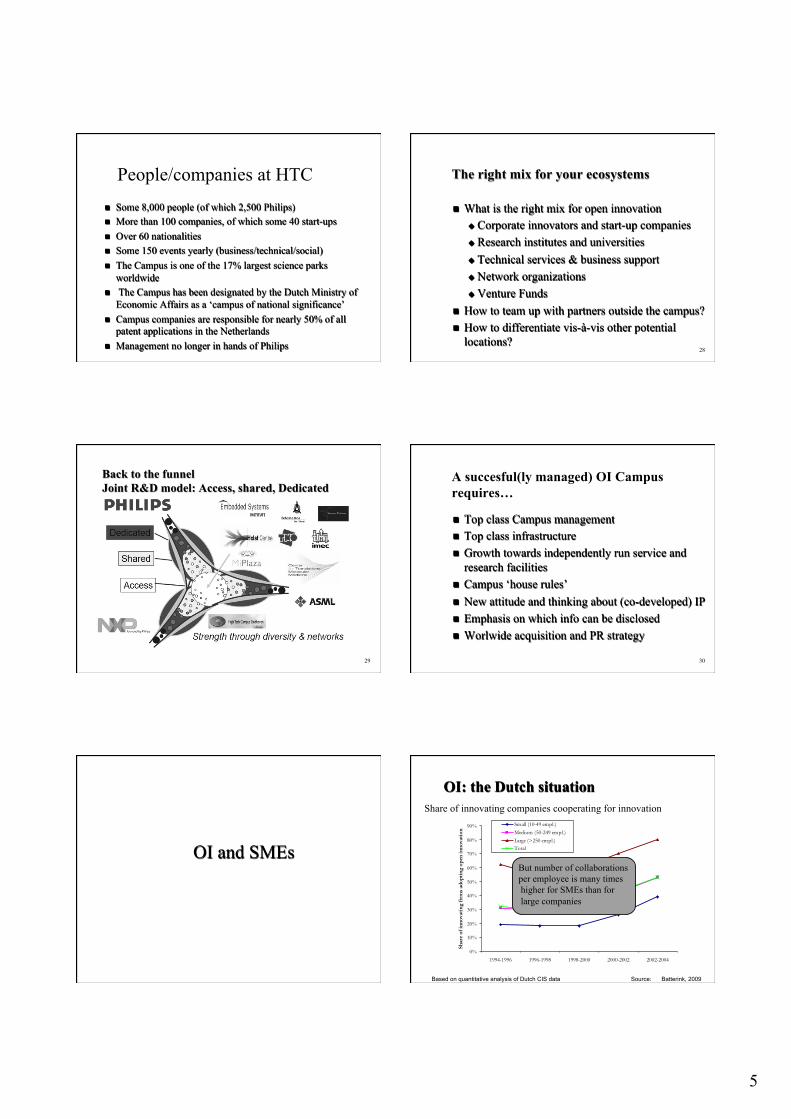

People/companies at HTC n Some 8,000 people (of which 2,500 Philips) n More than 100 companies, of which some 40 start-ups n Over 60 nationalities n Some 150 events yearly (business/technical/social) n The Campus is one of the 17% largest science parks

worldwide n The Campus has been designated by the Dutch Ministry of

Economic Affairs as a ‘campus of national significance’ n Campus companies are responsible for nearly 50% of all

patent applications in the Netherlands n Management no longer in hands of Philips

The right mix for your ecosystems

n What is the right mix for open innovation u Corporate innovators and start-up companies u Research institutes and universities u Technical services & business support u Network organizations u Venture Funds

n How to team up with partners outside the campus? n How to differentiate vis-à-vis other potential

locations? 28

Back to the funnel Joint R&D model: Access, shared, Dedicated

29

A succesful(ly managed) OI Campus requires…

n Top class Campus management n Top class infrastructure n Growth towards independently run service and

research facilities n Campus ‘house rules’ n New attitude and thinking about (co-developed) IP n Emphasis on which info can be disclosed n Worlwide acquisition and PR strategy

30

OI and SMEs

OI: the Dutch situation Share of innovating companies cooperating for innovation

Based on quantitative analysis of Dutch CIS data Source: Batterink, 2009

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1994-1996 1996-1998 1998-2000 2000-2002 2002-2004

Shar

e of

inno

vati

ng fi

rms

adop

ting

ope

n in

nova

tion

Small (10-49 empl.)Medium (50-249 empl.)Large (>250 empl.)Total

But number of collaborations per employee is many times higher for SMEs than for large companies

6

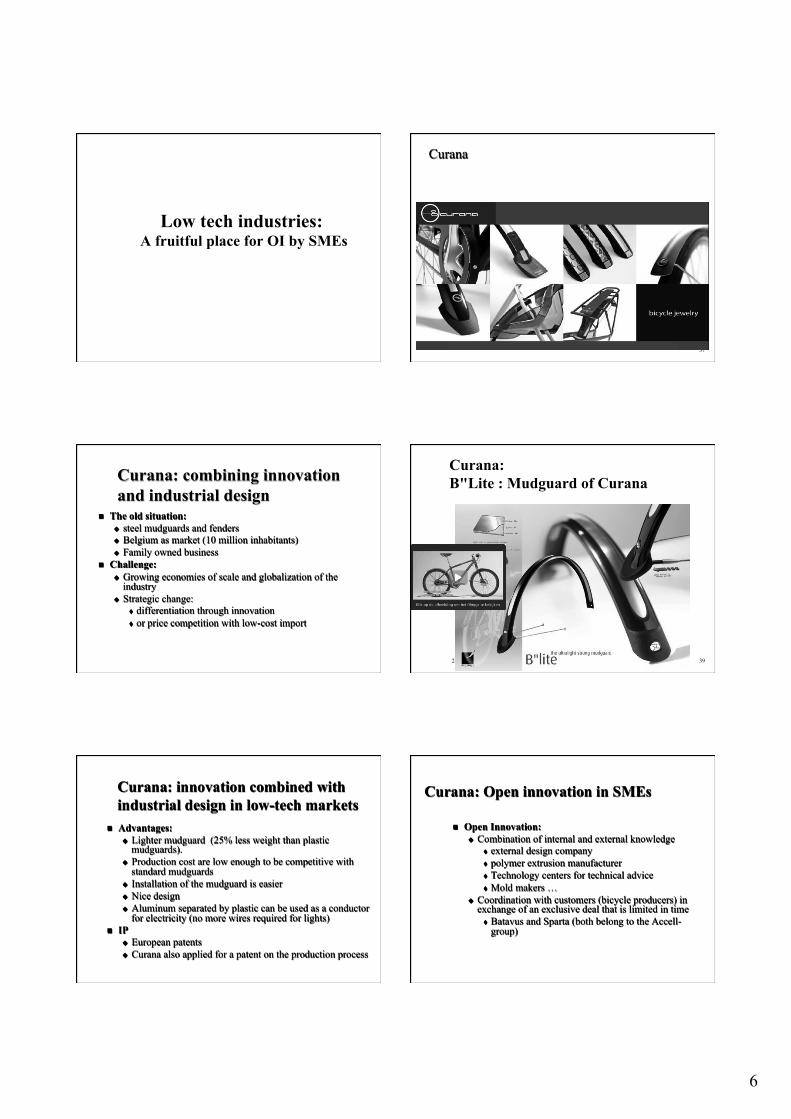

Low tech industries: A fruitful place for OI by SMEs

37

Curana

Curana: combining innovation and industrial design

n The old situation: u steel mudguards and fenders u Belgium as market (10 million inhabitants) u Family owned business

n Challenge: u Growing economies of scale and globalization of the

industry u Strategic change:

t differentiation through innovation t or price competition with low-cost import

Curana: B"Lite : Mudguard of Curana

24/11/12 Wim Vanhaverbeke 39

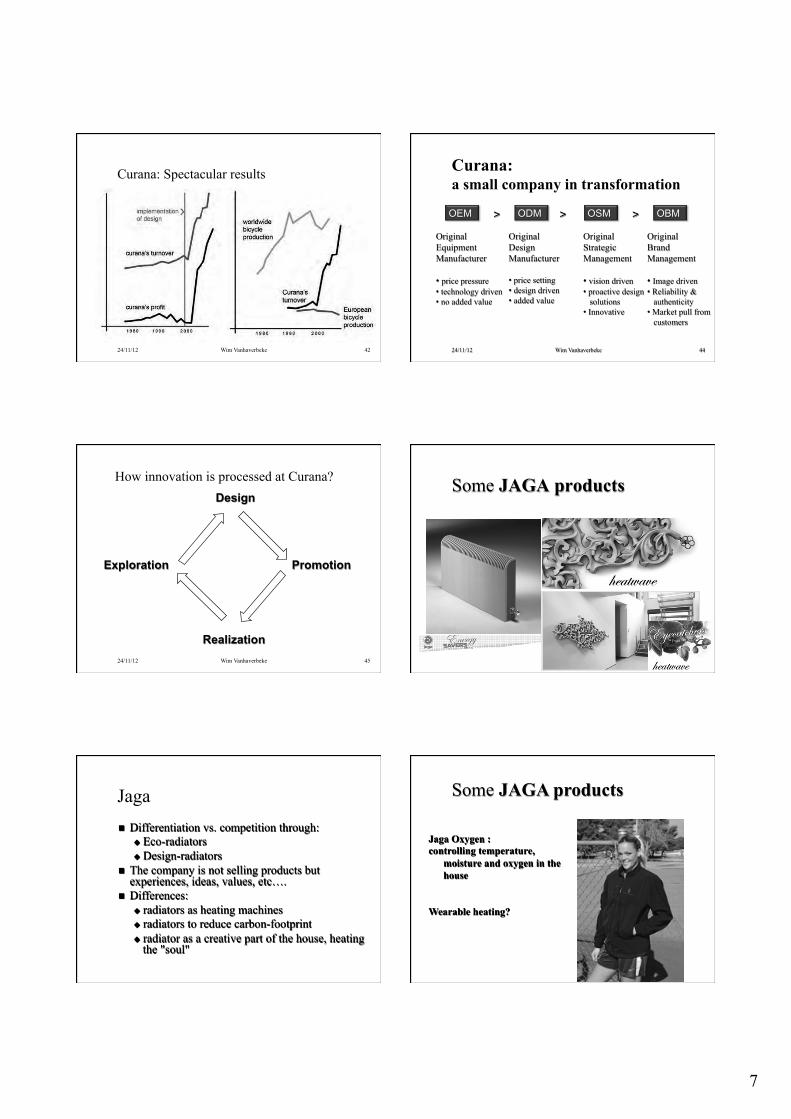

Curana: innovation combined with industrial design in low-tech markets

n Advantages: u Lighter mudguard (25% less weight than plastic

mudguards). u Production cost are low enough to be competitive with

standard mudguards u Installation of the mudguard is easier u Nice design u Aluminum separated by plastic can be used as a conductor

for electricity (no more wires required for lights) n IP

u European patents u Curana also applied for a patent on the production process

Curana: Open innovation in SMEs

n Open Innovation: u Combination of internal and external knowledge

t external design company t polymer extrusion manufacturer t Technology centers for technical advice t Mold makers …

u Coordination with customers (bicycle producers) in exchange of an exclusive deal that is limited in time t Batavus and Sparta (both belong to the Accell-

group)

7

Curana: Spectacular results

24/11/12 Wim Vanhaverbeke 42

Curana: a small company in transformation

24/11/12 Wim Vanhaverbeke 44

Original Design Manufacturer

• price setting • design driven • added value

OEM ODM OSM OBM

Original Equipment Manufacturer

• price pressure • technology driven • no added value

Original Strategic Management

• vision driven • proactive design solutions • Innovative

Original Brand Management

• Image driven • Reliability & authenticity • Market pull from customers

> > >

How innovation is processed at Curana?

24/11/12 Wim Vanhaverbeke 45

Exploration

Design

Realization

Promotion

Some JAGA products

50

Jaga n Differentiation vs. competition through:

u Eco-radiators u Design-radiators

n The company is not selling products but experiences, ideas, values, etc….

n Differences: u radiators as heating machines u radiators to reduce carbon-footprint u radiator as a creative part of the house, heating

the "soul"

Jaga Oxygen : controlling temperature,

moisture and oxygen in the house

Wearable heating?

Some JAGA products

8

Jaga Experience Lab : JEL - Product: test-facility

- Experience: test and develop your own products

- Jaga invites professors & engineers worldwide

- Low cost form of publicity: new projects as Federation Tower / Telefonica

Open innovation # 1 Experience Strategy

Open innovation #2 Jaga Product days 2007 n Total number of projects: 119 n Total number of products by 1 or more designers/engineers: 70 n Total number of products created by non professionals: 49 n Total number of solo projects*: 95

u created by a designer/engineer: 47 u made by non professionals: 48

n Number of Jaga Product days ideas taken into production within 6 months: 6 *= Created by only one person

24/11/12 Wim Vanhaverbeke 55

Jaga products days

Example: Play radiator

24/11/12 Wim Vanhaverbeke 57

Example: The play radiator

9

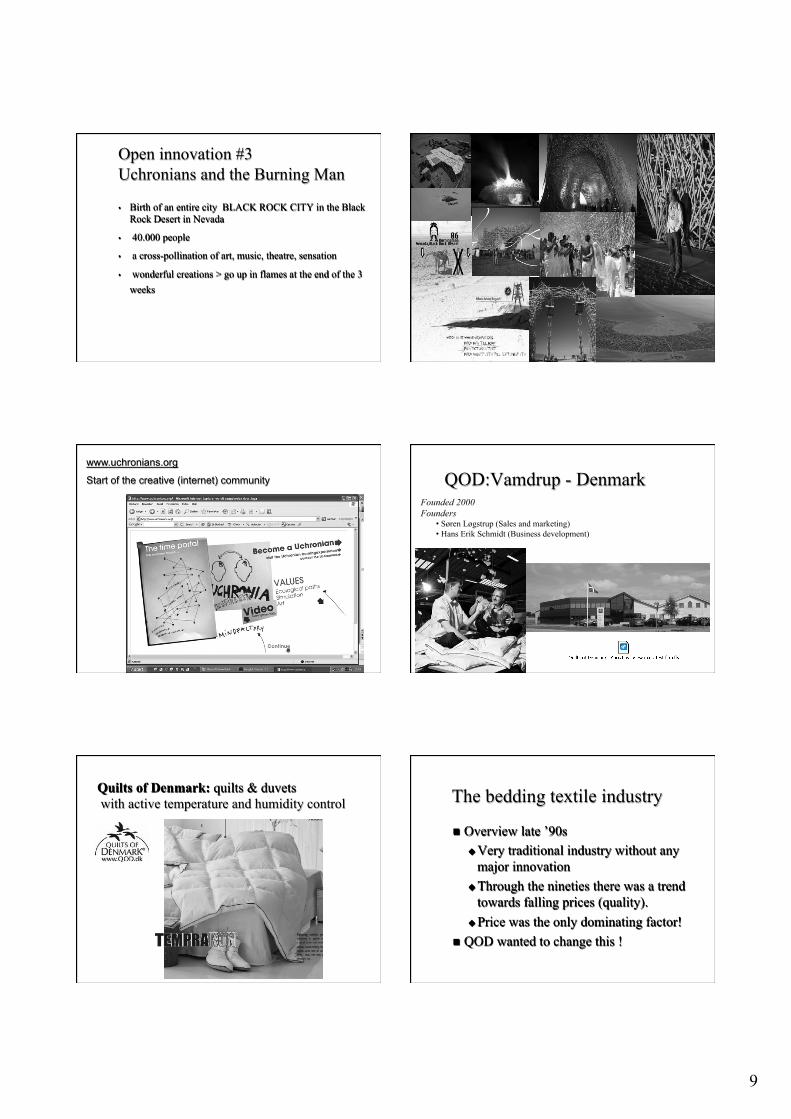

• Birth of an entire city BLACK ROCK CITY in the Black Rock Desert in Nevada

• 40.000 people

• a cross-pollination of art, music, theatre, sensation

• wonderful creations > go up in flames at the end of the 3 weeks

Open innovation #3 Uchronians and the Burning Man

www.uchronians.org

Start of the creative (internet) community QOD:Vamdrup - Denmark Founded 2000 Founders

• Søren Løgstrup (Sales and marketing) • Hans Erik Schmidt (Business development)

Quilts of Denmark: quilts & duvets with active temperature and humidity control The bedding textile industry

n Overview late ’90s u Very traditional industry without any

major innovation u Through the nineties there was a trend

towards falling prices (quality). u Price was the only dominating factor!

n QOD wanted to change this !

10

Changing the industry?

n Founders formulated two guidelines for the QOD business:

1. ”to promote a healthy sleep for a better tomorrow”

2. A dream team : only best people in the industry

Provider of healthy sleep n Vision:

u We are not a textile company. u We are providers of healthy sleep!

n Sleep is a major problem u We sleep less than we did 50 years ago u More than 70 million Americans do not sleep well (309 mill

inhabitants or 23% ) u The lack of sleep is costing the American society billions of

dollars annually. u It is estimated that 56.000 car accidents in the United States

happen because the driver falls asleep behind the wheel. u Danish teenagers sleep too little and have difficulties attending

early lectures.

How to improve sleep? n In order to become a provider of healthy sleep, QOD

needed to know which factors are important for a good night’s sleep:

n They started a cooperation with external experts: u Sleep scientists (Glostrup hospital) u Danish Asthma & Allergy Association u Physiotherapists

n Temperature (variation) rapidly emerged as one of the major determinants of a good / bad sleep

How to find the required technology? n Lot’s of trials with different technologies n H-E Schmidt reads an article in a scientific journal

about phase change technologies developed by Nasa n Contacts Nasa & Outlast

Phase change materials How to develop the required technology?

n Outlast was mainly interested in building material applications

n Gradually shifted attention towards textiles when it saw the economic opportunities while collaborating with QOD

n Outlast invented the microcapsules with PCMs n QOD optimized the technology (getting the right mix)

to have a better sleep u combining the insights of different fields

11

How to deal with IP?

n Outlast licenses the technology to QOD u Worldwide and exclusive license for quilts & pillows u Sublicenses to other manufacturers in countries where QOD

is not active / interested u Outlasts licenses to other firms for other applications

t Shoes, jackets, underwear, etc… n Sublicenses lead to easy price erosion, insufficient

control, brand damage u Outlast deal: grow and internationalize fast – too many

sublicenses

More recent developments

n Both companies co-developed a new, stronger Temprakon. Launched autumn 2010 u QOD is now a world-wide producer minimizing the number

of sublicenses

n Need to educate the retail shops and final customer u Training of sales people in retailing shops in return for a

marketing budget. u Working on new concepts to reach the customer

• Airborn, Temprakon shops • Internet sales ? • How to experience the quilt’s effect before buying it?

Temprakon-Airborn concept More recent developments

n Both companies co-developed a new, stronger Temprakon. Launched autumn 2010 u QOD is now a world-wide producer minimizing the number

of sublicenses

n Need to educate the retail shops and final customer u Training of sales people in retailing shops in return for a

marketing budget. u Working on new concepts to reach the customer

• Airborn, Temprakon shops • Internet sales ? • How to experience the quilt’s effect before buying it?

Whats next: The launch of the new TempraKON?

n QOD developed with Outlast a new Temprakon u Better performance and moisture control

n How to launch it? Two basic options 1. Launch the new generation TempraKON within the whole

range of QODs products. u QOD can re-negotiate sublicenses and price settings with partners in

several countries u push previous licensees out of the market in countries where QOD wants

to sell its products directly to retailers.

2. Keep the old TempraKON and add on a second layer of premium products u Advantages? Size of premium market? Price sensitivity?

Open innovation in services: Example: Pet insurance! § Combining resources, knowledge and

databases of insurance company, pet food manufacturer

§ Collaboration between different partners § Bonding of clients in commodity like

markets § Cross industry innovation, § Relational capital / open innovation § Sustainable competitive advantage

§ Similar example: Yacht insurance

12

OI in Services: KLM jet service § Value creation: improve time productivity of C-level

managers through jet service (vs. regular flights) § 3 - 4 clients instead of 1 – 2 per day

§ Set up the OI-value chain: § Internal innovation lab § European network of taxi’s § European network of low-cost, small airports § New technological applications increasing on flight

productivity

§ Value capture: how to maximize profitability? § Licensing in consecutive steps (KLM-Air France; Skyteam

world; all competitors (One World; Star alliance)

§ Move ahead: Include some of Netjets’ BM: time sharing!

How to manage OI?

An example: How to cooperate with high-tech

start-ups?

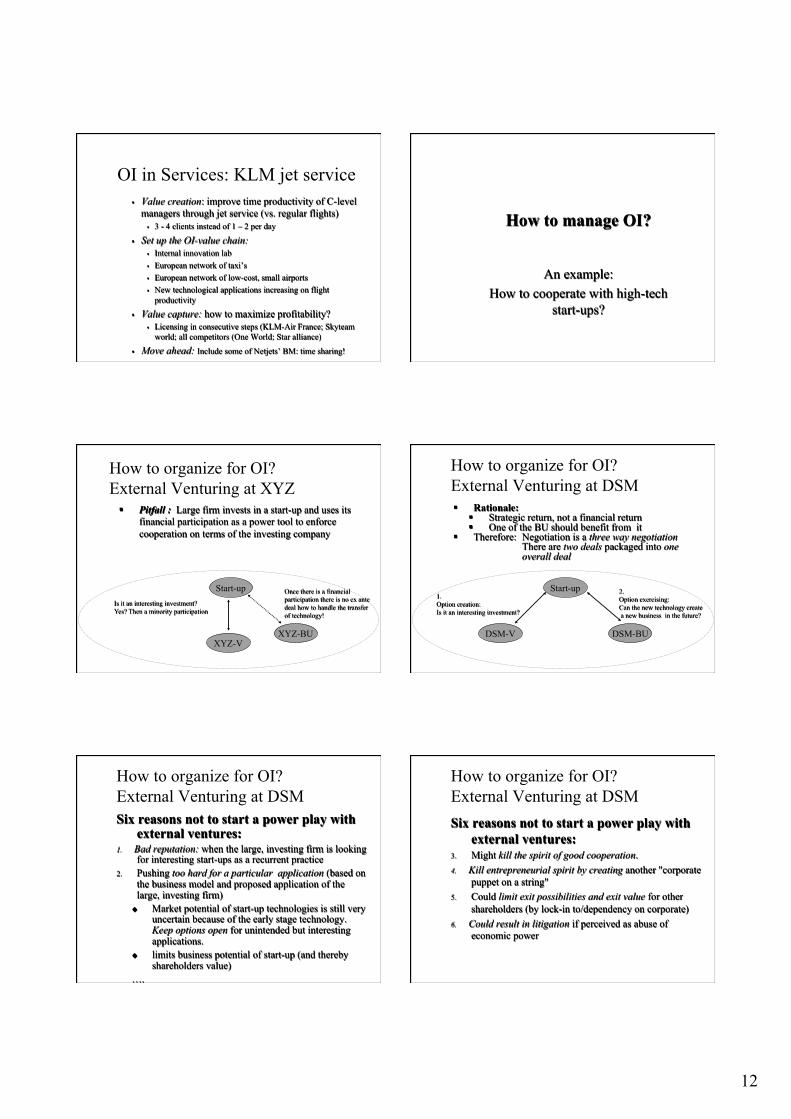

How to organize for OI? External Venturing at XYZ § Pitfall : Large firm invests in a start-up and uses its

financial participation as a power tool to enforce cooperation on terms of the investing company

Start-up

XYZ-BU XYZ-V

Is it an interesting investment? Yes? Then a minority participation

Once there is a financial participation there is no ex ante deal how to handle the transfer of technology!

How to organize for OI? External Venturing at DSM § Rationale:

§ Strategic return, not a financial return § One of the BU should benefit from it

§ Therefore: Negotiation is a three way negotiation There are two deals packaged into one

overall deal

Start-up

DSM-BU DSM-V

1. Option creation: Is it an interesting investment?

2. Option exercising: Can the new technology create a new business in the future?

How to organize for OI? External Venturing at DSM Six reasons not to start a power play with

external ventures: 1. Bad reputation: when the large, investing firm is looking

for interesting start-ups as a recurrent practice 2. Pushing too hard for a particular application (based on

the business model and proposed application of the large, investing firm)

u Market potential of start-up technologies is still very uncertain because of the early stage technology. Keep options open for unintended but interesting applications.

u limits business potential of start-up (and thereby shareholders value)

….

How to organize for OI? External Venturing at DSM Six reasons not to start a power play with

external ventures: 3. Might kill the spirit of good cooperation. 4. Kill entrepreneurial spirit by creating another "corporate

puppet on a string" 5. Could limit exit possibilities and exit value for other

shareholders (by lock-in to/dependency on corporate) 6. Could result in litigation if perceived as abuse of

economic power

13

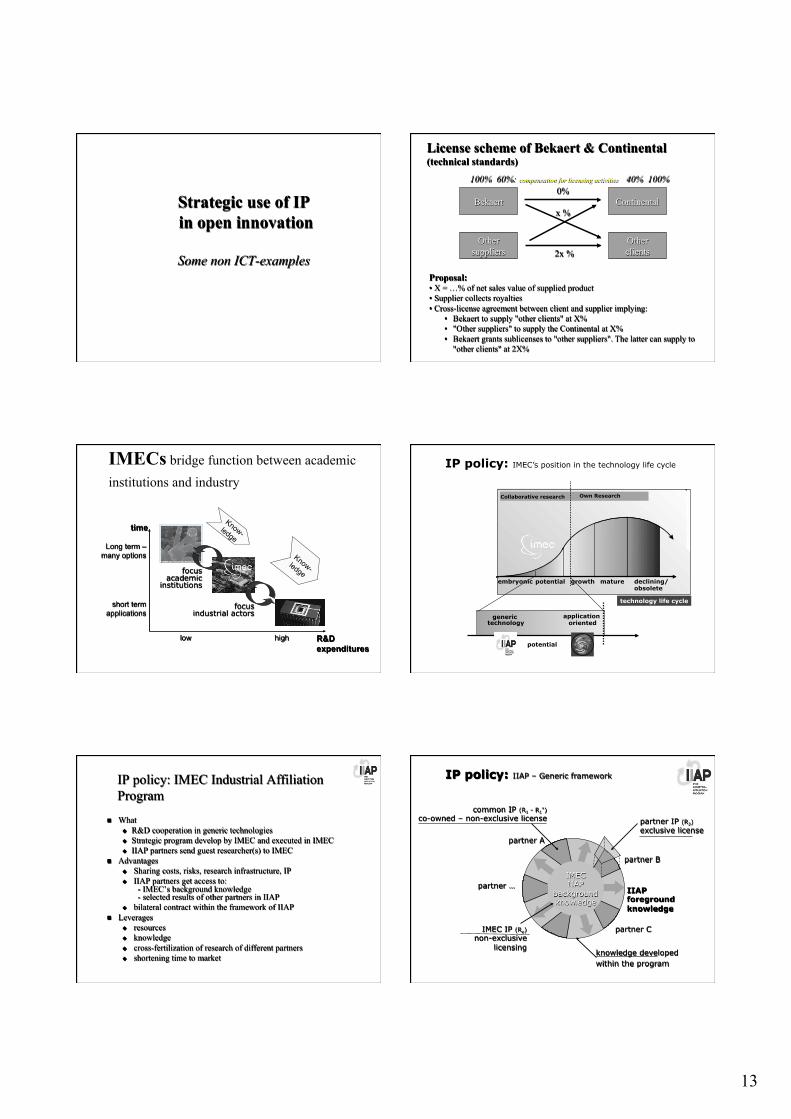

Strategic use of IP in open innovation

Some non ICT-examples

License scheme of Bekaert & Continental (technical standards)

Bekaert Continental

Other clients

Other suppliers

Proposal: • X = …% of net sales value of supplied product • Supplier collects royalties • Cross-license agreement between client and supplier implying:

• Bekaert to supply "other clients" at X% • "Other suppliers" to supply the Continental at X% • Bekaert grants sublicenses to "other suppliers". The latter can supply to

"other clients" at 2X%

0%

x %

2x %

100% 100% 60%: compensation for licensing activities 40%

time

Long term – many options

short term applications

low high R&D expenditures

Know- ledge

Know- ledge focus

academic institutions

focus industrial actors

IMECs bridge function between academic institutions and industry

embryonic potential growth mature declining/ obsolete

Collaborative research Own Research

technology life cycle

potential

generic technology

application oriented

IP policy: IMEC’s position in the technology life cycle

IP policy: IMEC Industrial Affiliation Program

n What u R&D cooperation in generic technologies u Strategic program develop by IMEC and executed in IMEC u IIAP partners send guest researcher(s) to IMEC

n Advantages u Sharing costs, risks, research infrastructure, IP u IIAP partners get access to:

- IMEC’s background knowledge - selected results of other partners in IIAP

u bilateral contract within the framework of IIAP n Leverages

u resources u knowledge u cross-fertilization of research of different partners u shortening time to market

IIAP foreground knowledge

partner B

partner C

partner …

partner A

IMEC IIAP

background knowledge

knowledge developed within the program

common IP (R1 - R1*)

co-owned – non-exclusive license partner IP (R2) exclusive license

IMEC IP (Ro) non-exclusive

licensing

IP policy: IIAP – Generic framework

14

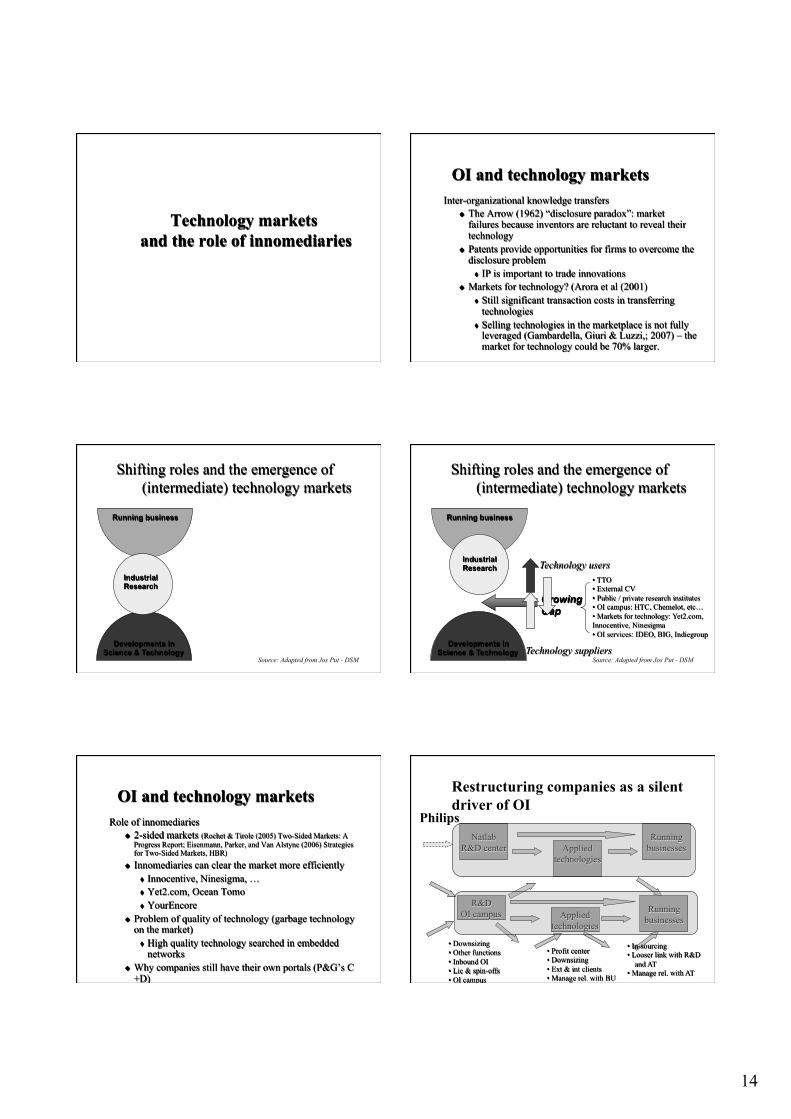

Technology markets and the role of innomediaries

OI and technology markets Inter-organizational knowledge transfers

u The Arrow (1962) “disclosure paradox”: market failures because inventors are reluctant to reveal their technology

u Patents provide opportunities for firms to overcome the disclosure problem t IP is important to trade innovations

u Markets for technology? (Arora et al (2001) t Still significant transaction costs in transferring

technologies t Selling technologies in the marketplace is not fully

leveraged (Gambardella, Giuri & Luzzi,; 2007) – the market for technology could be 70% larger.

Shifting roles and the emergence of (intermediate) technology markets

Running business

Developments in Science & Technology

Source: Adapted from Jos Put - DSM

Industrial Research

Shifting roles and the emergence of (intermediate) technology markets

Running business

Industrial Research

Developments in Science & Technology

Source: Adapted from Jos Put - DSM

• TTO • External CV • Public / private research institutes • OI campus: HTC, Chemelot, etc… • Markets for technology: Yet2.com, Innocentive, Ninesigma • OI services: IDEO, BIG, Indiegroup

Technology suppliers

Technology users

GrowingGap

OI and technology markets Role of innomediaries

u 2-sided markets (Rochet & Tirole (2005) Two-Sided Markets: A Progress Report; Eisenmann, Parker, and Van Alstyne (2006) Strategies for Two-Sided Markets, HBR)

u Innomediaries can clear the market more efficiently t Innocentive, Ninesigma, … t Yet2.com, Ocean Tomo t YourEncore

u Problem of quality of technology (garbage technology on the market) t High quality technology searched in embedded

networks u Why companies still have their own portals (P&G’s C

+D)

Restructuring companies as a silent driver of OI

Philips Natlab

R&D center Applied technologies

Running businesses

R&D OI campus Applied

technologies

Running businesses

• Downsizing • Other functions • Inbound OI • Lic & spin-offs • OI campus

• Profit center • Downsizing • Ext & int clients • Manage rel. with BU

• In-sourcing • Looser link with R&D and AT • Manage rel. with AT

15

OI Research: The next wave

Edited by: Henry Chesbrough, Wim Vanhaverbeke Joel West

2003

2006

2006 2008 2011

2013 2011

Exnovate as a network of excellence for OI-practitioners and scholars? n www.exnovate.org n An international network of excellence on Open and

Collaborative Innovation n Projects

u PhD course OI in ESADE (4th time – 7-9 Janaury Barcelona)

u CE and OI Masterclass (9 times already; 10th time at ESADE Barcelona June 2013)

u Study on open innovation metrics u Using best practices to improve OI in SMEs u Dispatching surveys about OI u …

http://www.exnovate.org/