Embed Size (px)

Citation preview

NBER WORKING PAPER SERIES

WHAT IS THE IMPACT OF SUCCESSFUL CYBERATTACKS ON TARGET FIRMS?

Shinichi KamiyaJun-Koo KangJungmin Kim

Andreas MilidonisRené M. Stulz

Working Paper 24409http://www.nber.org/papers/w24409

NATIONAL BUREAU OF ECONOMIC RESEARCH1050 Massachusetts Avenue

Cambridge, MA 02138March 2018, Revised July 2018

We thank Claudia Biancotti, Andrei Gonçalves, Jan Jindra, Christos Makridis, and seminar participants at Hong Kong Polytechnic University, Kent State University, Korea University, and the SEC for their useful comments. All errors are our own. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research.

At least one co-author has disclosed a financial relationship of potential relevance for this research. Further information is available online at http://www.nber.org/papers/w24409.ack

NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications.

© 2018 by Shinichi Kamiya, Jun-Koo Kang, Jungmin Kim, Andreas Milidonis, and René M. Stulz. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source.

What is the Impact of Successful Cyberattacks on Target Firms?Shinichi Kamiya, Jun-Koo Kang, Jungmin Kim, Andreas Milidonis, and René M. Stulz NBER Working Paper No. 24409March 2018, Revised July 2018JEL No. G14,G32,G34,G35

ABSTRACT

We examine which firms are targets of cyberattacks and how they are affected. We find that cyberattacks cause firms to reassess the risks that they are exposed to and their consequences, so that they have real effects on firm policies even when targets are not financially constrained. Cyberattacks are more likely to occur at more visible firms, firms with more intangible assets, and firms with less board attention to risk management. Attacks where personal financial information is appropriated are associated with a negative stock-market reaction, a decrease in sales growth for large firms and retail firms, an increase in leverage, a deterioration in financial health, and a decrease in investment in the short run. Firms further respond to cyberattacks by reducing CEO bonuses and risk-taking incentives and by strengthening their risk management.

Shinichi KamiyaNanyang Technological University Nanyang Business School50 Nanyang [email protected]

Jun-Koo KangNanyang Technological University Nanyang Business School50 Nanyang [email protected]

Jungmin KimHong Kong Polytechnic UniversitySchool of Accounting and Finance Hong [email protected]

Andreas MilidonisUniversity of CyprusSchool of Economics and ManagementDepartment of Accounting and FinanceP.O. Box 20537, NicosiaCY-1678 [email protected]

René M. StulzThe Ohio State UniversityFisher College of Business806A Fisher HallColumbus, OH 43210-1144and [email protected]

1

I. Introduction

Cyber risk has become an important source of risk for corporations.1 For example, in 2017, risk

practitioners estimated that the most important operational risk is cyber risk and data security.2 A survey of

CEOs across the world by PWC found that more than half of the CEOs expect cybersecurity and data

breaches to threaten stakeholder trust in their industries over the next five years.3 Despite the widespread

recognition of emerging threats posed by cyber risk and its importance as a new type of risk, there is little

evidence on how successful cyberattacks affect corporations. In particular, we know little about which types

of firms are more likely to experience successful cyberattacks, and how such attacks affect target firm

shareholder wealth, growth, and financial strength. We also know little about how firms change managerial

risk-taking incentives and their risk management after attacks. In this study, we investigate these important

but unexplored issues by analyzing a comprehensive sample of disclosed cyberattacks involving data

breaches on public corporations from 2005 to 2017.

Although there is no systematic evidence on the impact of cyberattacks on firms, the case of Target

Corporation, the Minnesota-based second largest discount store retailer, provides a useful illustration of

what the impact of such an attack can be. From November 27 to December 15, 2013, Target experienced a

massive cyberattack that resulted in the loss of almost 70 million customers’ personal information such as

phone numbers and credit card information.4 On December 19, 2013, Target publicly acknowledged the

breach and unveiled measures that cost $100 million for upgrading its IT system and adapting new

technology to increase the security of credit card transactions. Despite its strong public commitment to take

1 Although there is no consensus about an exact definition of cyber risk, the U.S. Department of Homeland Security describes it as “capabilities to disrupt, destroy, or threaten the delivery of essential services, or exploit vulnerabilities to steal information and money by sophisticated cyber actors and nation-states” (“Cybersecurity Overview,” Homeland Security, https://www.dhs.gov/cybersecurity-overview).” The Institute of Risk Management views cyber risk as “any risk of financial loss, disruption or damage to the reputation of an organization from some sort of failure of its information technology systems (“Cyber Risk,” The Institute of Risk Management, https://www.theirm.org/knowledge-and-resources/thought-leadership/cyber-risk/”). 2 “Top 10 Operational Risks for 2017,” Risk.net (January 23, 2017). 3 See “Risk in Review 2017 Study,” PWC (April 2017), p. 20. 4 “Timeline of Target's Cyberattack and Aftermath: How Cyber Theft Snowballed for the Giant Retailer,” International Business Times (May 5, 2014), http://www.ibtimes.com/timeline-targets-data-breach-aftermath-how-cybertheft-snowballed-giant-retailer-1580056.

2

measures to reduce the risk of being attacked, the stock price of Target dropped by almost 2.2% on the

announcement day, which represents an estimated market value loss of $890 million. Target’s EBIT

decreased by $1.59 billion (-28.6%) from $5.52 billion during the four quarters prior to the breach to $3.94

billion during the four quarters after the breach. In addition, Target reported data breach-related expenses

of $292 million including the settlement of class action lawsuits and investigations by state prosecutors in

its 2016 10-K. This example shows that a cyberattack can have a large negative impact on the target firm.

This example is by no means extreme. For instance, two months after the announcement of the 2017

cyberattack on Equifax, a consumer credit reporting agency, its stock price was lower by almost a quarter

than before the attack.

We provide a simple model to examine the economic implications of successful cyberattacks. We

define a successful cyberattack as one that breaches the firm’s defenses. In the following, we use

cyberattack to denote a successful cyberattack for simplicity.5 We distinguish between cyberattacks that

change the assessment of the loss distribution of cyberattacks versus those that have no such impact. With

the loss distribution unchanged, we show that a firm’s loss from a cyberattack should not affect its future

actions if it is not financially constrained except for actions that restore it to its financial position before the

attack. If the loss distribution or more generally the firm’s assessment of its risk exposures changes, the

firm will adjust its policies to its new understanding of the loss distribution. The change in the assessment

of the loss distribution may be rational – the result of the firm having more information – or can be due to

behavioral reactions to adverse outcomes that were believed to have an extremely low probability. As the

loss distribution becomes less favorable, the firm increases its expenditures to decrease the probability of

an attack, invests more in risk management, and decreases its willingness to take other risks. We test these

predictions by examining the costs of cyberattacks (i.e., adverse effects on firm value) and post-attack

changes in firm policies.

To provide systematic evidence on how successful cyberattacks affect firm value, financial strength,

5 Throughout the paper, we use the words “cyberattacks” and “attacks” interchangeably.

3

growth, and policies, we use data breach events caused by cyberattacks reported to the Privacy Rights

Clearinghouse (PRC) over the period 2005 to 2017. Studying security breaches that result in the loss of

personal information obtained from the PRC has an important advantage compared to using other types of

data breaches because firms must disclose such breaches to affected persons in a timely manner under the

State Security Breach Notification Laws. Although it is possible that an attacked firm in our sample

withheld the information about the discovery of the incident and delayed its announcement to the public,

the disclosure requirements mandated by the data breach notification laws help alleviate potential sample

underreporting biases that may occur in other studies using data breaches without such reporting

requirements.6

Moreover, there are two additional advantages in our sample. First, our sample includes a homogenous

sample of attacks as it only includes attacks initiated by outside parties. Specifically, throughout our

analyses, we include as cyberattack events only successful malicious external actions, such as hacking and

malware (hereafter “cyberattacks”) and exclude other incidents associated with internal errors or failure to

follow information handling policies (e.g., internal fraud, unintended disclosure, the loss of portable device,

the loss of stationary device, and physical loss) as these events are not the result of attacks on computers

and computer networks by outsiders. Second, while previous studies use only data breaches that occurred

at the parent firm level, we include cyberattacks on subsidiaries (e.g., attack on Kmart that is a subsidiary

of Sears) as well as those on parent firms. This comprehensive attack sample allows us to examine the

consequences of adverse cyber security events in a systematic manner.

We first examine which firms are more likely to be affected by cyberattacks. A priori, it is unclear

which types of firms are more likely to become the targets of cyberattacks. To the extent that hackers target

firms in which the benefits of hacking exceed its costs, they are more likely to breach firms’ security in

which they can take advantage of valuable information such as visible firms (e.g., large firms and firms

6 For example, using the data breaches covered in the AuditAnalytics cyber-attacks and VCDB VERIS databases, Amir, Levi, and Livne (2018) examine the extent to which firms withhold information on cyberattacks. Their sample includes data breaches that do not involve the loss of personal information (and thus are not subject to the Security Breach Notification Law) as well as “Confidentiality” events that potentially involve the loss of personal information.

4

included in the Fortune 500 list) and firms in which customers’ personal information is important in doing

business (e.g., financial and retail firms). However, it is also possible that hackers target the firms whose

defenses are easier to breach, such as small firms or risky firms, because visible firms and firms for which

customers’ personal information is important may have more effective risk management and IT security

systems. Our likelihood analysis shows that firms are more likely to experience cyberattacks when they are

larger, are included in the list of Fortune 500 companies, are financially less constrained, are more highly

valued, and have more intangible assets. We also find that cyberattacks are more likely to occur in firms

operating in industries that are less competitive (i.e., industries with higher Herfindahl index and those in

which firms sell more unique products, measured as the ratio of selling expense to sales). Firm-level

corporate governance characteristics, such as CEO-chair duality, the proportion of outside directors on the

board, and board size, do not predict the likelihood of cyberattacks. Lastly, firms that pay more attention to

risk management at the top, which we measure using the information reported in BoardEx about the

existence of a risk management committee on the board, are less likely to be attacked.

Second, we analyze market reactions to the announcement of cyberattacks. A cyberattack is expected

to be costly for a firm as it is likely to distract management and lead to expenses on systems, to litigation

costs, and possibly to fines. Consequently, we expect a negative abnormal return for firms that announce a

cyberattack. Consistent with this expectation, we find a significant mean cumulative abnormal return (CAR)

of −0.84% during the three-day window around cyber-attack announcements. With a mean market value of

about $58.93 billion for our sample of attacked firms, this translates into an average value loss of $495

million per attack. When we divide the sample into the attacks that result in financial information loss (i.e.,

loss of social security numbers and/or loss of bank account and credit card information) and those that result

in no financial information loss (loss of other personally identifiable non-financial information such as

information on driver license, medical records, and e-mails), the abnormal returns are only significantly

negative for the former sample. For firms experiencing cyberattacks that result in loss of personal financial

information, their mean CAR (-1, 1) is −1.09%. We also find weak evidence that cyberattacks have a much

worse impact when the incident is a recurring event within one year. The impact is especially negative when

5

attacked firms are older and when they do not have evidence of board attention to risk management

(measured by whether the board or a board committee explicitly has the role of monitoring firm risks and

risk management) as the abnormal return is lower by 4 percentage points for such firms. However, we find

no consistent evidence that the stock-price reaction is worse for financially constrained firms.

Third, we investigate whether attacked firms experience a decrease in sales growth by conducting a

difference-in-differences analysis using a propensity-score-matched sample. Given the fact that only attacks

with loss of financial information have a significant adverse impact on target firms, we highlight results

that use only the attacks with loss of financial information. From our simple model, sales growth would fall

if customers learn about the risk. Consistent with this prediction, we find that sales growth significantly

declines for the three years after the attack. We further find that the impact of cyberattacks on sales growth

exhibits substantial cross-sectional variation: large firms experience a significant decrease in sales growth

while small firms do not. We also find a significant large negative impact of cyberattacks on sales growth

for firms operating in the retail industry. Though we do not find an adverse impact of cyberattacks on

operating performance (ROA and cash flow / total assets) in general, they do have an adverse impact for

large firms and firms operating in durable goods industries.

We next examine whether attacked firms’ financial strength falls using a difference-in-differences

analysis. We find that, after the attack, attacked firms experience a decrease in credit ratings, an increase in

the probability of bankruptcy, an increase in cash flow volatility, and a decrease in shareholder net worth.

Fourth, we examine how firms adjust their investment and financial policies in response to cyberattacks.

If a cyberattack changes the perception of the board and management about the likelihood and cost of

cyberattacks, or more generally changes their perception of the firm’s risk exposures and its ability to

manage risk, we would expect post-attack changes in investment and financial policies. There is weak

evidence that compared to non-attacked control firms, attacked firms reduce capital expenditures and

experience a greater financing deficit after the attack. Since attacks involve out-of-pocket costs and result

in a greater financing deficit, attacked firms have to respond by securing funds to pay for these costs. We

find that attacked firms use debt rather than equity to address their funding requirements, and that they use

6

long-term debt rather than short-term debt, so that the maturity of their debt lengthens. A potential

explanation for the increase in debt maturity is that firms that are potentially vulnerable to attacks in the

short-term want to avoid frequent debt rollovers, as rolling over debt shortly after an attack might be

difficult. We find no evidence that firms’ responses depend on whether they are financially constrained

before the attack. This result is perhaps not surprising in light of the fact that almost no attacked firm is

financially constrained.

Fifth, we assess how a firm’s risk management changes as a result of an attack. We find that victims

of a cyberattack are more likely to increase board oversight of firm risk. This result is again consistent with

the hypothesis that the board and management reassess the risks the firm is exposed to after an attack and

the costs of these risks. For example, management could conclude that exposures to risks have become

more costly if customers have become more concerned about the risks the firm is exposed to, including the

risk of cyberattacks. In this case, management might want to decrease the firm’s risk exposures to affect

customers’ willingness to do businesses with it.

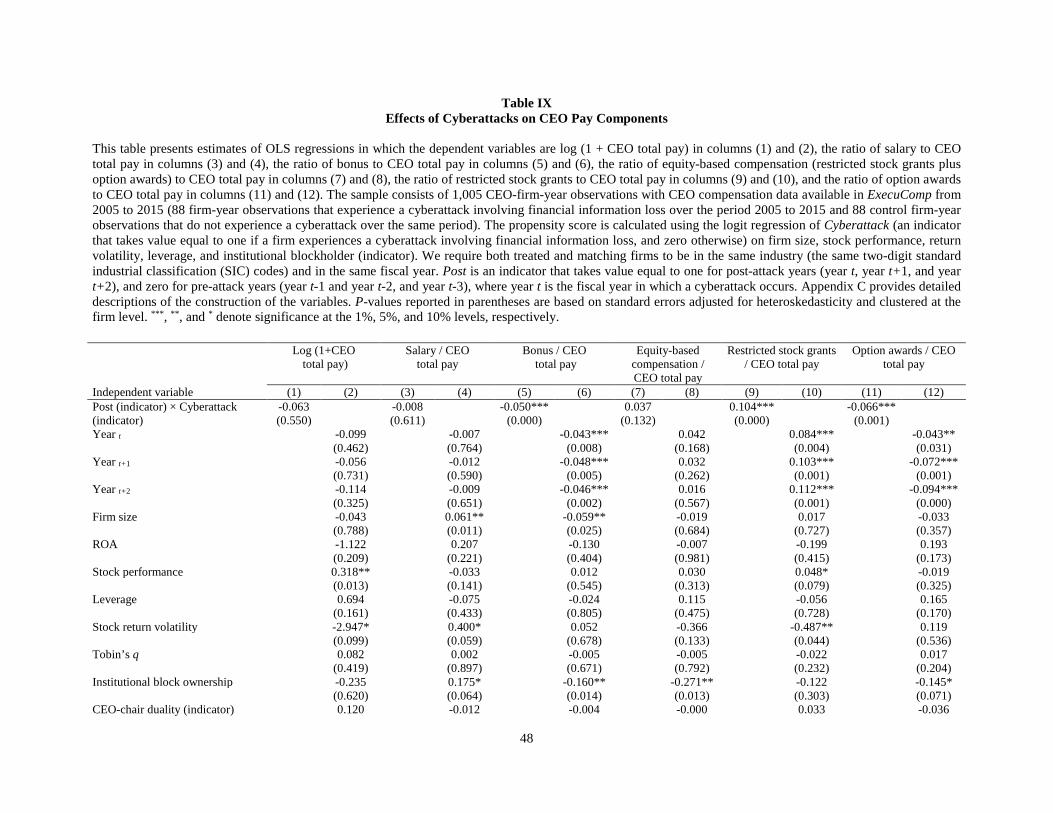

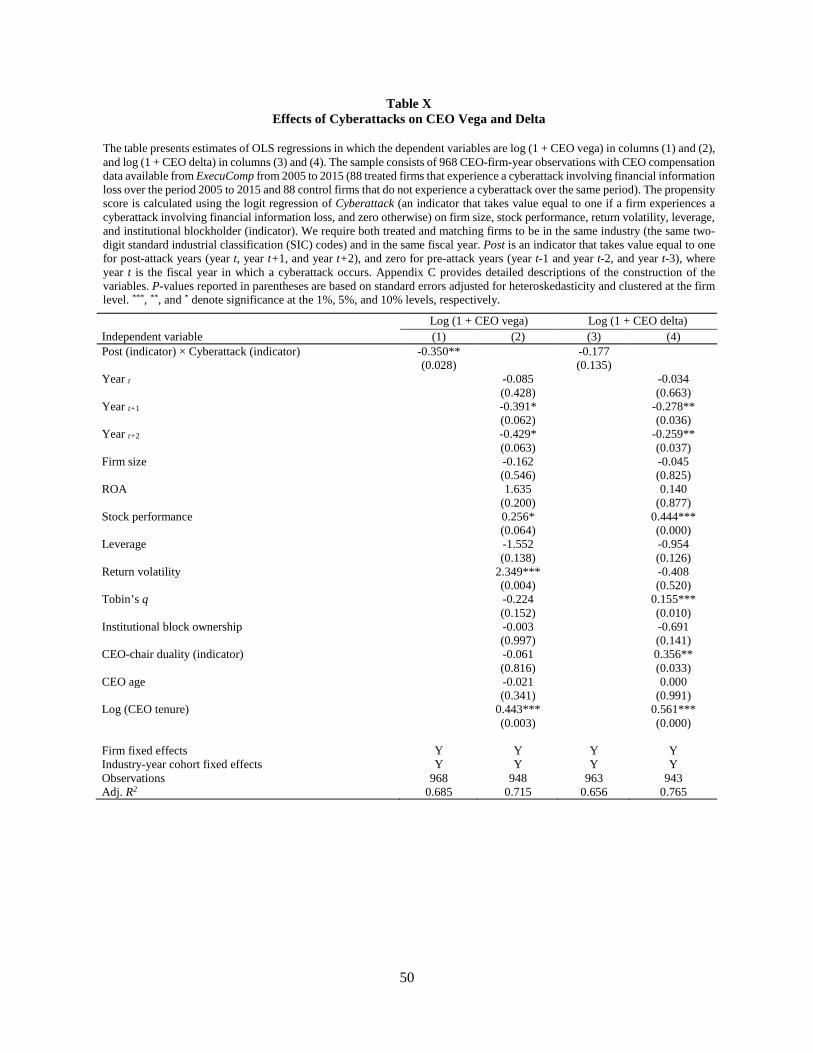

Sixth, if a cyberattack changes the board’s assessment of firm risk, we would expect the CEO’s risk-

taking incentives to be adjusted. An increase in assessed firm-level risk caused by cyberattacks can have

two opposing impacts that boards would be expected to take into account when they adjust CEOs’ pre-

attack compensation structure. On the one hand, when a cyberattack significantly increases firm-specific

risk, to minimize its effect on her undiversified (with respect to firm risk) wealth, a risk-averse CEO may

forgo risky, positive NPV projects that shareholders prefer to invest in. Thus, to provide the CEO with

strong risk-taking incentives, a board may attempt to adjust the CEO’s compensation structure, for example,

by increasing compensation convexity (e.g., using more stock options in CEO compensation). On the other

hand, a cyberattack may lead a board to reconsider the risk-taking incentives of the CEO and decrease these

incentives because the attack may have led to a reduction in the board’s risk appetite, either because it was

surprised by the consequences of the cyberattack or simply due to behavioral reasons. This will prompt

boards to lower compensation convexity by reducing the use of stock options or replacing stock options

with restricted stocks, a form of equity-based compensation that does not share the convexity of stock

7

options. We should also see the bonus component of compensation being reduced if the board believes that

management performed poorly either by not taking steps to prevent an attack or in responding to the attack.

We find that attacked firms do not reduce the overall level of CEO equity incentives (i.e., the ratio of

equity-based compensation to CEO total pay) after a cyberattack. However, attacked firms significantly

increase restricted stock grants and reduce option awards, suggesting that they replace stock options with

restricted stock and hence reduce the risk-taking incentives of CEOs. Attacked firms also respond to

cyberattacks by significantly reducing the proportion of CEO bonus to total pay.

Our study contributes to the literature at least in three important ways. First, we provide systematic

evidence on potential losses in shareholder value and changes in corporate policies caused by cyberattacks.

Although previous studies also examine the valuation effect of cyberattack announcements, most of these

studies use breach events including both cyberattacks and incidents associated with internal errors or failure

to follow information handling policies,7 and do not examine the post-attack changes in corporate policies

that we focus on.8 By utilizing the most recent and comprehensive cyber risk incidents reported in the PRC

database and focusing only on successful cyberattacks, we are able to reevaluate the overall effects of cyber

risk on firm value and assess the impact of attacks on various corporate policies. Further, we show that only

7 Most studies in the information security literature that examine the impact of cyberattacks on the market value of U.S. firms focus on the events that occur in the late 1990s and the early 2000s, and their empirical evidence is inconclusive (Campbell et al. (2003), Garg, Curtis, and Halper (2003a, 2003b), Hovav and D’arcy (2003), Cavusoglu, Mishra, and Raghunathan (2004), Hovav and D’arcy (2004), Ko and Dorantes (2006)). There are only a limited number of finance studies that examine the valuation impact of cyberattacks including Cummins, Lewis, and Wei (2006), Gatzlaff and McCullough (2010), Hilary, Segal, and Zhang (2016), Johnson, Kang, and Lawson (2017), Amir, Levi, and Livne (2018), Bianchi and Tosun (2018), Lending, Minnick, and Schorno (2018), and Akey, Lewellen, and Liskovich (2018). Unlike our analyses that focus only on malicious external actions such as hacking and malware, their main analyses include data breaches caused by insiders’ mishandling of sensitive information and by theft of laptops and physical devices. 8 Several previous papers examine post-breach changes in firm outcomes that are different from those in our study. For example, using all types of breaches including insiders’ mishandling of sensitive information, Hilary, Segal, and Zhang (2016) find that attacked firms do not experience any significant changes in operational performance, executive departure likelihood, shareholder clientele, and the amount of disclosure after the breaches. Makridis and Dean (2018) find some evidence on the negative association between breaches and firm productivity using data from the PRC and Department of Health and Human Services from 2005 to 2016. Akey, Lewellen, and Liskovich (2018) and Lending, Minnick, and Schorno (2018) further find that firms significantly increase their investment in corporate social responsibility (CSR) in the years following a breach, and Nordlund (2017) documents that directors in a breached firm experience an increase in the likelihood of turnover.

8

the attacks that involve theft of financial information decrease shareholder wealth and that as a result of the

attacks, firms become more financially fragile.

Second, though cyber risk has become one of the most important operational risks of firms, the risk

management literature has not paid much attention to this risk thus far. We find that firms’ attention to risk

management, as evidenced by the existence of a risk committee on the board, is associated with a lower

incidence of cyberattacks. We also find that firms whose boards pay attention to risk management prior to

cyberattacks experience a less negative valuation impact when cyberattacks do happen. Our evidence also

suggests that one important effect of cyberattacks on target firms is that they result in a reassessment of

target firms’ risk exposures. We would expect firms realizing that their risk exposures are greater than

previously known to pay more attention to risk management, as operational risk management can decrease

the probability of operational risk events and reduce their severity, and we find that this is the case.

Third, our study contributes to the compensation literature by showing that boards adjust the mix of

the CEO’s equity-based pay in responding to uncertainty-increasing exogenous events that occur at the

firm-level. Although many studies have examined the relation between equity incentives and risk-taking

incentives (e.g., Guay (1999), Coles, Daniel, and Naveen (2006)), there is little evidence showing how

firms dynamically adjust CEOs’ optimal compensation package to manage their risk-taking incentives in

response to changes in a firm’s risk environment. The only exception is Gormley, Matsa, and Milbourn

(2013) who examine how an increase in a firm’s left-tail risk (i.e., a jump in risk that is created when a

chemical to which a firm’s workers have already been exposed is newly identified as a carcinogen) affects

the board’s compensation policy and how the changes in compensation policy affect the CEO’s risk-taking

behavior. Our study is different from theirs in that we focus on cyber risk as an unexpected shock to a firm’s

assessed risk exposures. Our analysis indicates that firms respond to cyberattacks by replacing stock options

with restricted stocks, and hence they decrease management’s incentives to take risks. These actions are

consistent with firms learning from such attacks that they have greater risk exposures than they expected.

The rest of this paper is organized as follows. In Section II, we examine the theoretical predictions of

the impact of cyberattacks on firms. In Section III, we describe our sample construction and present the

9

distribution of sample events and firm characteristics. In Section IV, we examine the likelihood of firms

being attacked using various firm and industry characteristics. In Section V, we analyze the shareholder

wealth impact of cyberattacks and, in Section VI, we examine the impacts of cyberattacks on operating

performance, financial health, and financial, investment, and risk management policies. We also investigate

how boards adjust CEO compensation structure in responding to cyber risk incidents. We conclude in

Section VII.

II. Risk management and cyberattacks

Cyber risk is one form of operational risk. Firms try to assess operational risk using loss distributions

(e.g., Crouhy, Galai, and Marks (2014)). These distributions are the result of the convolution of a frequency

distribution and a loss severity distribution. Firms can affect their exposure to an operational risk by taking

risk mitigating actions (e.g., upgrading IT security systems and hiring Chief Information Officers who are

responsible for cyber risk management), but these mitigating actions have a cost. As a result, we expect

firms to invest more in risk mitigating actions if adverse outcomes (e.g., loss of sales, recovery costs of IT

systems, and litigation costs)) are costlier to them. Our model is designed to capture these effects.

We consider the problem of a single firm deciding how much to invest in risk management (i.e., the

risk mitigating action). The firm has valuable databases that could be hacked and it can invest in risk

management to decrease the probability of being hacked, 𝑝𝑝 ∈ [0,1]. If hacked, the firm loses 𝐶𝐶𝐶𝐶 > 0,

which, for simplicity, is a fixed and known amount. Consequently, the expected cost of being hacked is

equal to 𝑝𝑝 × 𝐶𝐶𝐶𝐶.

The cost of maintaining a risk management program to keep the probability of being hacked at 𝑝𝑝 is

equal to 𝑄𝑄(𝑝𝑝), which is a decreasing (𝑄𝑄′ < 0) and convex (𝑄𝑄" > 0) function of 𝑝𝑝 with lim𝑝𝑝→0

𝑄𝑄(𝑝𝑝) = ∞.

Intuitively, it is costlier to maintain a lower probability of being hacked and the marginal cost of improving

risk management becomes prohibitively expensive as the probability of being hacked gets closer to zero,

so that it is effectively impossible to fully eliminate the risk of being hacked.

10

To determine the optimal investment in risk management related to hacking, management trades off

the expected cost of being hacked with the cost of risk management. Optimally, the firm invests in risk

management up to the point where the probability of being hacked is such that 𝑄𝑄′ = −𝐶𝐶𝐶𝐶 . For

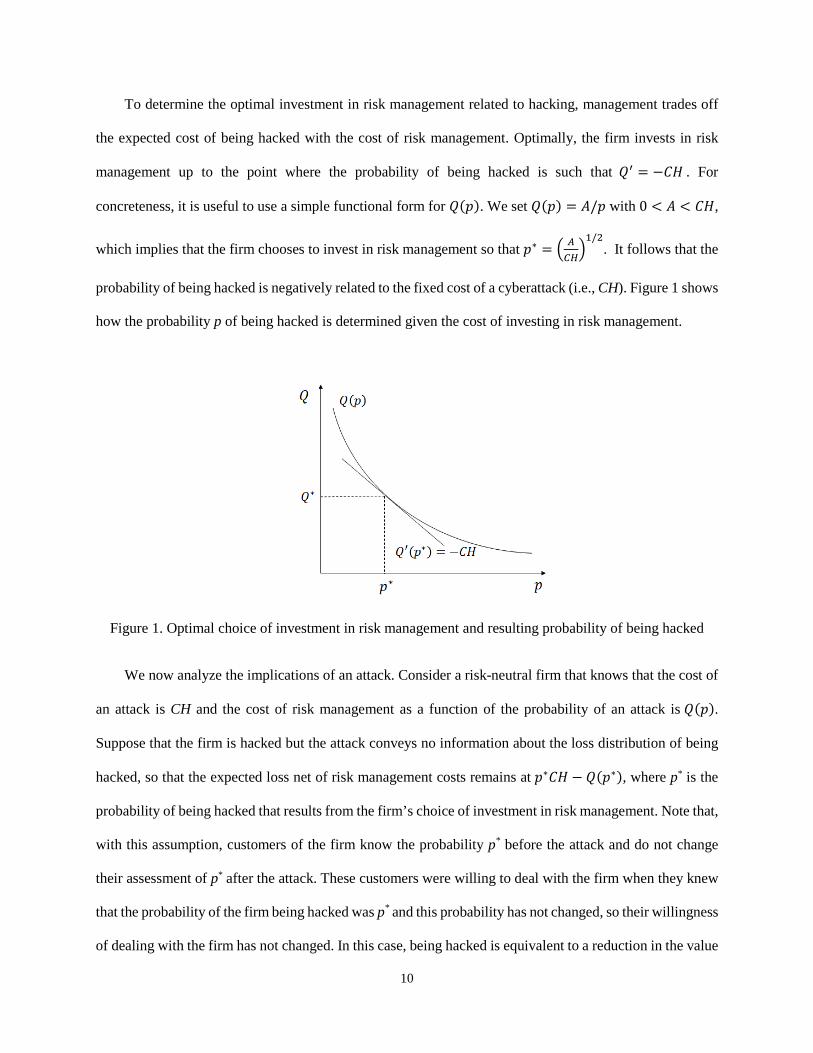

concreteness, it is useful to use a simple functional form for 𝑄𝑄(𝑝𝑝). We set 𝑄𝑄(𝑝𝑝) = 𝐴𝐴/𝑝𝑝 with 0 < 𝐴𝐴 < 𝐶𝐶𝐶𝐶,

which implies that the firm chooses to invest in risk management so that 𝑝𝑝∗ = � 𝐴𝐴𝐶𝐶𝐶𝐶�1/2

. It follows that the

probability of being hacked is negatively related to the fixed cost of a cyberattack (i.e., CH). Figure 1 shows

how the probability p of being hacked is determined given the cost of investing in risk management.

Figure 1. Optimal choice of investment in risk management and resulting probability of being hacked

We now analyze the implications of an attack. Consider a risk-neutral firm that knows that the cost of

an attack is CH and the cost of risk management as a function of the probability of an attack is 𝑄𝑄(𝑝𝑝).

Suppose that the firm is hacked but the attack conveys no information about the loss distribution of being

hacked, so that the expected loss net of risk management costs remains at 𝑝𝑝∗𝐶𝐶𝐶𝐶 − 𝑄𝑄(𝑝𝑝∗), where p* is the

probability of being hacked that results from the firm’s choice of investment in risk management. Note that,

with this assumption, customers of the firm know the probability p* before the attack and do not change

their assessment of p* after the attack. These customers were willing to deal with the firm when they knew

that the probability of the firm being hacked was p* and this probability has not changed, so their willingness

of dealing with the firm has not changed. In this case, being hacked is equivalent to a reduction in the value

11

of the firm as it will have out-of-pocket costs as a result of the cyberattack. As long as these costs do not

make the firm financially constrained, the cyberattack has no implications beyond the sunk cost resulting

from the attack. If the firm had good growth opportunities before the attack, it still has these opportunities

and thus should take advantage of them. If the attack worsens financial constraints or makes the firm

financially constrained, it will not be able to put itself back in the situation it was in before the attack. As a

result, it will have to change its policies to reflect its financially constrained state. Such a firm might, for

instance, have to cut investment to make cash available to deal with the consequences of the attack.

Alternatively, firms or their customers learn from the cyberattack. First, customers could infer that the

probability of an attack was higher than they thought. This could be because they thought risk management

would be more effective. In this case, customers’ demand for the firm’s products will fall. Customers could

also infer that the firm is generally willing to take risks that could be costly for them or is managing its risks

more poorly than anticipated. This could reduce demand further. Second, management could infer that the

probability of an attack is higher than they thought or that the costs of an attack are higher than they thought.

Such an outcome could arise, for instance, because the attack reveals defensive weaknesses that the firm is

not aware of or that the firm is too optimistic in its assessment that defensive weaknesses would not be

discovered by outsiders. In this case, the attack would lead the firm to make further investments to decrease

the risk of an attack, to invest more in risk management, and to become less willing to take risks generally.

The firm would have a similar response if the attack leads it to develop a worse assessment of its risk

exposures and its ability to manage risk in general. Financially constrained firms might not be able to make

some investments and might have to cut back on capital expenditures, for instance, to release resources to

cope with the aftermath of the attack.

The analysis so far assumes that customers and managers are fully and equally informed and rational.

It is well-known in the behavioral literature that individuals can ignore or underestimate risks (Kahneman

and Tversky (1972)). Recent work in finance further shows the possibility for some low risk events to be

neglected (e.g., Gennaioli, Shleifer, and Vishny (2015)). When such risks manifest themselves, a

reassessment of the distribution of risks takes place. As a result, when an attack occurs, it leads customers

12

and/or managers to reassess the importance of these risks. It is then possible for customers and/or managers

to overreact to an attack in the sense that they might conclude that the probability of an attack is much

higher than it actually is due to the availability heuristic (Tversky and Kahneman (1973)).

Consider a firm with value that is a concave function of future profits, so that greater volatility in

profits keeping the mean constant decreases the value of the firm. For such a firm, there is value to risk

management that decreases the volatility of profits and there exists an optimal level of volatility of profits

given the cost of risk management (see, for instance, Smith and Stulz (1985) and Froot, Scharfstein, and

Stein (1993)). If a particular risk is discovered to be higher than anticipated, this firm will choose to reduce

risk generally to bring its level of risk back to the optimal level. Hence, a firm that discovers that the risk

of hacking is higher than expected is likely to make risk management investments to reduce risk along other

dimensions.

These theoretical arguments lead to the following hypotheses:

Hypothesis 1 (no learning case). In this case, the attack has no impact on future activities of the firm

if the firm is not financially constrained except for activities that raise funds to offset the loss resulting

directly from the attack. The attack itself results in a loss of value of the firm’s securities. The impact of the

attack is higher if the firm is financially constrained as, in that case, the attack also changes the firm’s

investment and financial policies and has a larger impact on the firm’s securities.

Hypothesis 2 (learning case). In this case, if customers learn that the probability of an attack is higher

than they expected, sales growth falls, but in response managers will increase investment in risk

management, which will reduce the decrease in sales growth. If managers learn that the cost of an attack is

higher than anticipated or that the probability of an attack is higher than anticipated for a given investment

in risk management, the firm will invest more to reduce the risk of an attack, reduce its risk-taking, and

invest more in risk management.

13

III. Sample

To construct our sample of cyberattacks, we first start with all data breach incidents (6,328 incidents)

covered in the PRC database over the period of 2005 to 2017.9 We use the PRC database since firms are

required to disclose data breaches to affected persons in a timely manner under the State Security Breach

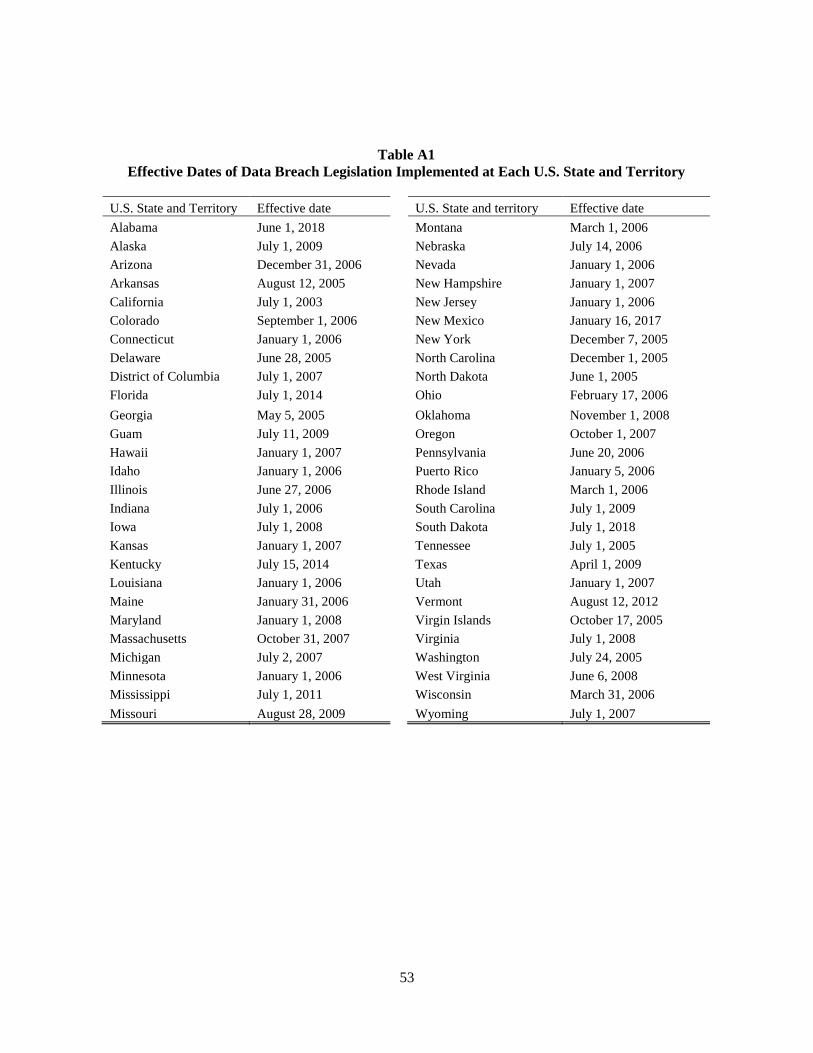

Notification Laws. In Appendix A, we discuss these State Security Breach Notification Laws and other

regulations that govern firms’ disclosure requirements for data breaches, such as the Securities and

Exchange Commission (SEC) Cybersecurity Disclosure Guidance that requires publicly traded firms to

disclose “materially important” cyber incidents in a Form 8-K filing and the Privacy Rule of the Health

Insurance Portability and Accountability Act of 1996 (HIPAA) that requires firms to notify breaches of

unsecured protected health information to the Secretary of the U.S. Department of Health and Human

Services. We delete incidents on governments, educational institutions, and non-profit organizations,

resulting in a sample of 4,769 incidents on privately held and publicly listed firms. We then include only

incidents in which a firm lost personal information by hacking or malware-electronic entry by an outside

party (1,580 incidents). Next, we manually match organization names reported in the PRC database with

firm names listed in Compustat and the Center for Research in Securities Prices (CRSP). When attacked

firms are unlisted subsidiaries of listed firms, we consider cyberattacks as having occurred in their listed

parent firms. If we cannot match organization names recorded in the PRC database with firm names in

Compustat and CRSP, we search Capital IQ corporate profiles and other sources including company

9 We obtain the data from the PRC’s website, http://www.privacyrights.org/data-breach, which are downloaded on July 10, 2015 for the 2005-2014 sample period and on April 14, 2018 for the later sample period. Established to protect individuals’ privacy, PRC, a nonprofit consumer and advocacy organization, located in San Diego, California, collects information about breach events from government agencies and verifiable news sources, and publishes the chronology of reported breach events involving loss of personally identifiable information that can be used to identify an individual in context (e.g., social security numbers, bank account information, emails, driver license numbers, and medical information) in the U.S. starting from 2005. The PRC classifies the attacks with the loss of personally identifiable information into breaches that result in financial information loss (e.g., loss of social security numbers and financial information such as credit card information) and others that result in no financial information loss (i.e., loss of driver license numbers and medical information). However, the PRC does not provide such a classification in recent years. Thus, we obtain the information after 2014 by manually searching event descriptions in the PRC database and news articles from Factiva. Although the PRC database also includes certain cyberattack incidents that do not involve the loss of personal information, we exclude these incidents from our sample to minimize the self-selection bias because they are not subject to cyberattack notification laws and firms may not have an obligation to disclose them. See also https://www.privacyrights.org/data-breach-FAQ for a detailed description of the data provided by PRC.

14

websites and Factiva to ensure the accuracy of their names for proper matching. We restrict the sample to

attacked firms with financial and stock return data available in Compustat and CRSP, respectively. We

require the sample firms to be listed on the New York Stock Exchange, the American Stock Exchange, or

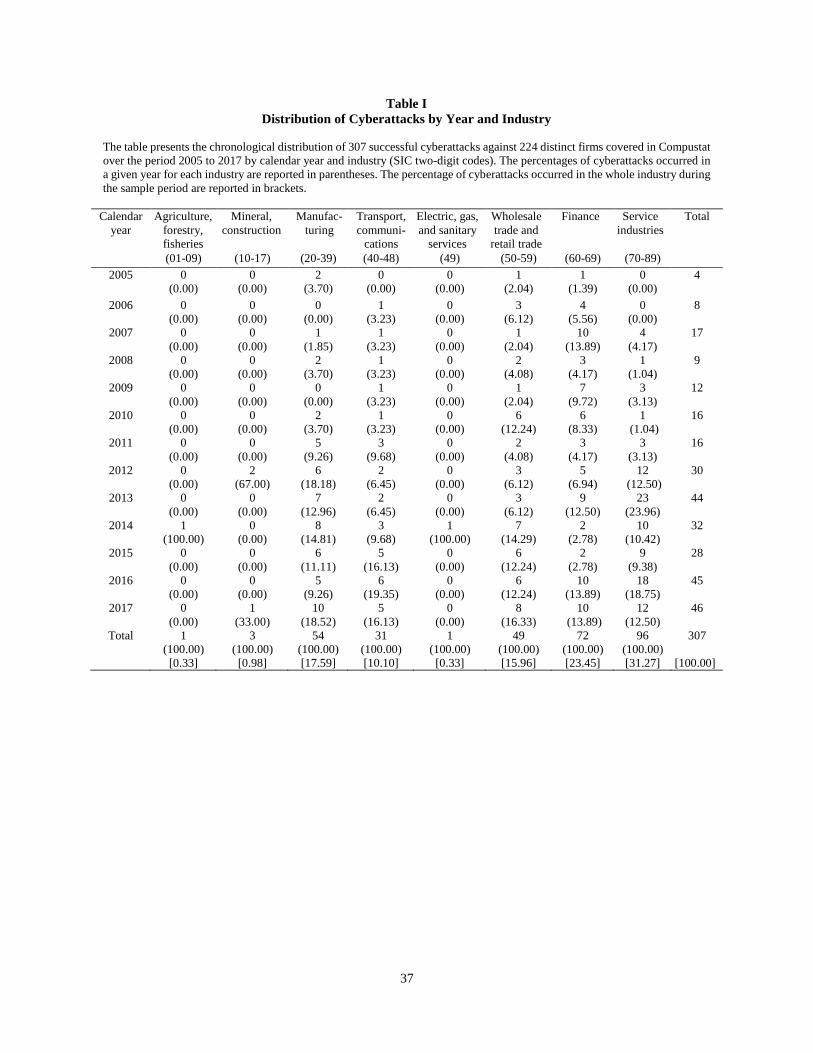

Nasdaq. These procedures yield a final sample of 307 cyberattacks for 224 unique firms, of which 163 are

attacks on parents firms and 144 are attacks on subsidiaries.10 Of 224 attacked firms, 51 firms (22.8%)

experience multiple cyberattacks during our sample period. In our sample, 73.9% of the reported

cyberattacks involve financial information loss and the remaining 26.1% involve no financial information

loss.

Table I presents a chronological distribution of the 307 cyberattacks by industry (SIC two-digit codes)

and year. We find a generally increasing trend in the number of cyberattacks occurring over time: only four

attacks occurred in 2005, in contrast to 46 in 2017. We also find that industries in which cyberattacks occur

most frequently are service industries (31.27%), followed by finance (23.45%), manufacturing (17.59%)

and wholesale trade and retail trade industries (15.96%), which suggests that firms that deal with a large

number of customers are more likely to experience a cyberattack.

IV. Likelihood of Experiencing Cyberattacks

To examine firm and industry characteristics that drive cyberattack incidents, we first compare the

characteristics of firms that were successfully attacked, which we call targets, with those of firms that were

10 As discussed in Appendix A, the PRC database does not cover all cyberattack incidents of publicly listed firms in the U.S. due to the following two reasons. First, although most states have legislated state cyberattack notification laws by 2009, which require firms operating in the state to notify affected residents about cyberattack incidents, three states (i.e., Alabama, New Mexico, and South Dakota) had no such laws for the whole sample period. Second, even for incidents that are subject to state cyberattack notification laws, many states do not have legislations that require the state government to collect data on cyberattack incidents and disclose the relevant information. Thus, it is possible that our sample underestimates the true extent of cyberattacks that affect publicly listed firms in the U.S. To check the representativeness of our sample, we independently search Factiva to locate news articles reporting cyberattack incidents in 2012 alone and compare the incidents reported by news media with those collected by the PRC database in 2012. We use the following keywords to locate the articles on cyberattack events in Factiva: “hacking,” “hacked,” “malware,” “spyware,” “cyber attack,” and cyberattack.” We restrict news sources to major wires including Dow Jones Newswires, Major News and Business Sources, Press Release Wires, Reuters Newswires, and The Wall Street Journal-All sources. We find that 18 incidents are covered in news media, of which 17 are included in the PRC database. The remaining one does not involve any loss of personal information and thus is not covered in the PRC database. Thus, it appears that the PRC database covers most of major cyberattack incidents.

15

not attacked successfully, which we call non-targets. Note that a non-target can have been attacked, but the

attack was not successful. No data is available on unsuccessful attacks. As we focus only on cyberattack

incidents that involve the loss of personal information subject to cyberattack notification laws, the sample

used in this analysis represents the population of successful attacks where targets follow existing disclosure

requirements. When a firm experiences multiple cyberattacks in a given fiscal year, we treat all these

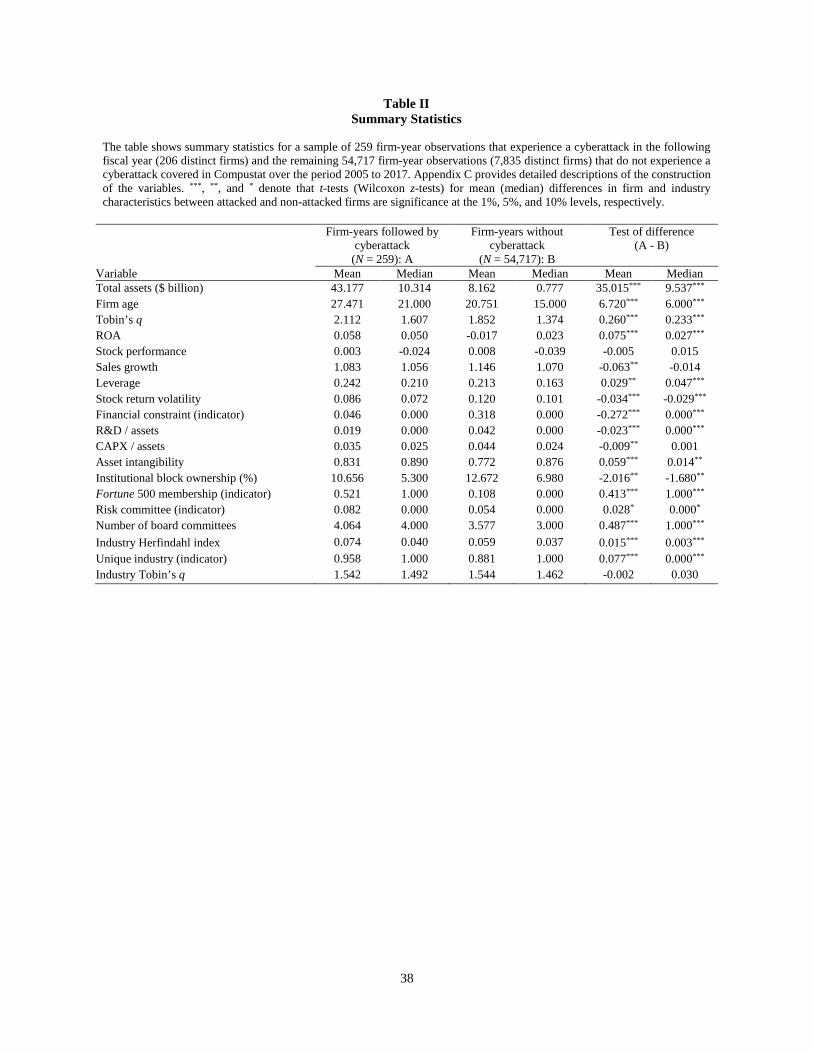

multiple attacks as a single attack in that year, so the sample size reduces to 259 from 307. Table II presents

summary statistics for 259 firm-year observations with cyberattack incidents and 54,717 firm-year

observations without cyberattack incidents covered in Compustat. It follows that the unconditional

probability of a cyberattack in a given year for a firm in our sample is extremely low, as it is 0.47%. We

winsorize all continuous variables at the 1st and 99th percentiles to mitigate the impact of outliers on our

analysis.

Focusing on firm-level characteristics, we find that compared to firms experiencing no cyberattack,

those experiencing cyberattacks are larger and older, and have a larger presence among Fortune 500

companies. These findings indicate that targets in our sample are more visible firms than non-target firms.

Targets are also more profitable (higher ROA) and less risky (lower stock return volatility), have higher

future growth opportunities (higher Tobin’s q), higher leverage, and higher asset intangibility, and invest

less in capital expenditures and R&D activities. Importantly, few targets are financially constrained. We

report results using the index of Whited and Wu (2006), but results are similar with other indices. Using

BoardEx board committee-level data, we also find that the proportion of firms having a risk committee on

the board is higher for targets than for non-targets.11 We consider a board having a risk committee if the

name of its committee includes “risk” (e.g., Enterprise Risk Management Committee, Risk Management

Committee, Audit and Risk Committee, and Governance, Nominating, and Risk Oversight Committee).

Turning to industry-specific characteristics, we find that cyberattacks are more prevalent among firms

11 When we exclude firms in finance industries (SIC 6000-6999) from the sample, we find the difference in the proportion of firms having a risk committee on the board between targets and non-targets (0.024 compared to 0.022) is insignificant. Thus, the difference in the existence of a risk committee between these two groups of firms reported in Table II is largely driven by firms in finance industries.

16

operating in industries in which product market competition is less intense (measured by Herfindahl index

and product uniqueness).

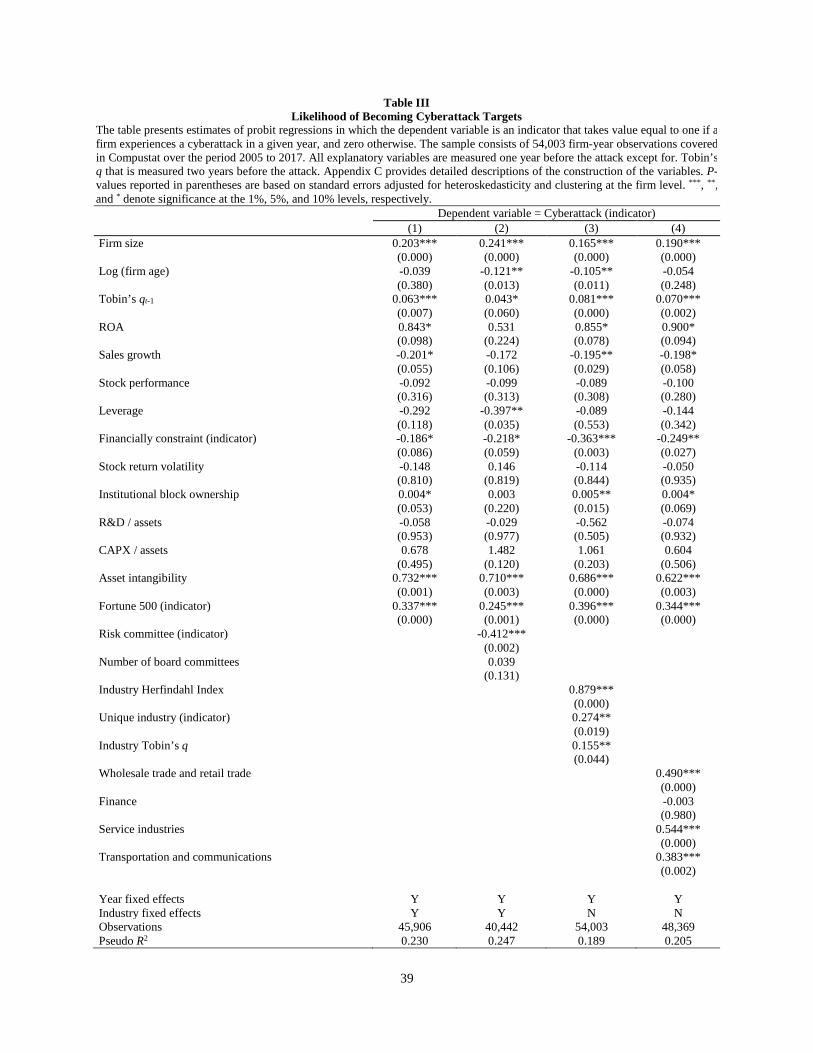

We turn next to a more direct examination of the likelihood of firms being targets. We use the data

panel from Table II as the sample. Table III reports results of estimates of probit regressions in which the

dependent variable is an indicator that takes value equal to one if a firm experiences a cyberattack in a given

year, and zero otherwise.12 We include several firm- and industry-level characteristics reported in Table II

as the explanatory variables that are measured one year before the attack. The only exception is Tobin’s q

that is measured two years before the attack since we find that it is highly correlated with past stock

performance. Using the lagged value of Tobin’s q helps address the correlation issue since Tobin’s q is

directly affected by returns. In Regression (1), we include only firm-level characteristics as determinants.

We also control for year and industry fixed effects (measured by two-digit SIC codes). We find that firms

with higher visibility (measured by firm size, Fortune 500 membership, and institutional block ownership),

higher valuations as measured by Tobin’s q, higher ROA, higher asset tangibility, and fewer financial

constraints are more likely to be targets of a cyberattack. In Regression (2), we add to Regression (1) an

indicator for whether the firm has a risk committee (Risk committee), measured using the board committee

information on BoardEx as discussed above. We control for the number of board committees in the

regression. We see that firms with a risk committee are less likely to be targets. The sample is smaller as

we require firms to have data available through BoardEx. With this smaller sample, we also find that

younger and less leveraged firms are more likely to be targets. Though we do not report the results, we also

estimate the regressions by adding corporate governance characteristics such as CEO-chair duality, the

proportion of outside directors on the board, and board size to examine whether the quality of corporate

governance can predict the likelihood of cyberattack incidents. We find that none of these variables is

12 We do not use hazard models in estimating the regressions in Table III due to the possibility of doubly censored data (i.e., the existence of multiple events for the same firm) in the analysis. Our sample may also not satisfy the assumption of non-informative censoring, the assumption that the mechanisms giving rise to censoring of the sample should not be related to the probability of an event occurring (Lagakos (1979)). For example, in our study, firms that are censored are unlikely to have the same probability of experiencing a subsequent event as firms that experience no cyberattacks.

17

significant. This result is in contrast to that of Chernobai, Jorion, and Yu (2011) who show that good

corporate governance plays an important role in reducing operational risk at U.S. financial institutions,

suggesting that either their results are specific to the financial industry or are specific to operational risks

in general but not to cyber risks.

In Regression (3), we add industry variables that capture industry competition (Industry Herfindahl

index and an indicator for unique industry) and future growth opportunities (industry Tobin’s q). We find

that cyberattacks are more likely in industries that face less intense product market competition (i.e.,

industries with a higher Herfindahl index and more unique products) and industries with higher growth

opportunities.

In Regression (4), we replace industry characteristics in Regression (3) with five industry indicators

defined using the first two-digit SIC codes and omit the manufacturing industry as a reference group to

examine whether cyberattacks are more likely in certain industries controlling for firm characteristics.13

We find that among the major industries, cyberattacks are more likely in service industries, wholesale trade

and retail trade industries, and transportation and communications industries. The coefficient on finance

industries, however, is not significant. Hence, controlling for firm characteristics, it is not just the fact that

a firm deals with large numbers of customers that makes an attack more likely.

Overall, the results in this section suggest that cyberattacks are more likely to occur in firms that are

more visible, with greater valuations, more intangible assets, without a board risk committee, and in less

competitive industries. Firms that are successfully targeted seem to rely more on customer personal

information in doing business.

13 In this regression, we exclude firms operating in three industries (agriculture, forestry, and fisheries industries, mineral and construction industries, and electric, gas, and sanitary services industries) in which the frequency of cyberattacks is too low (only one or three) during our sample period.

18

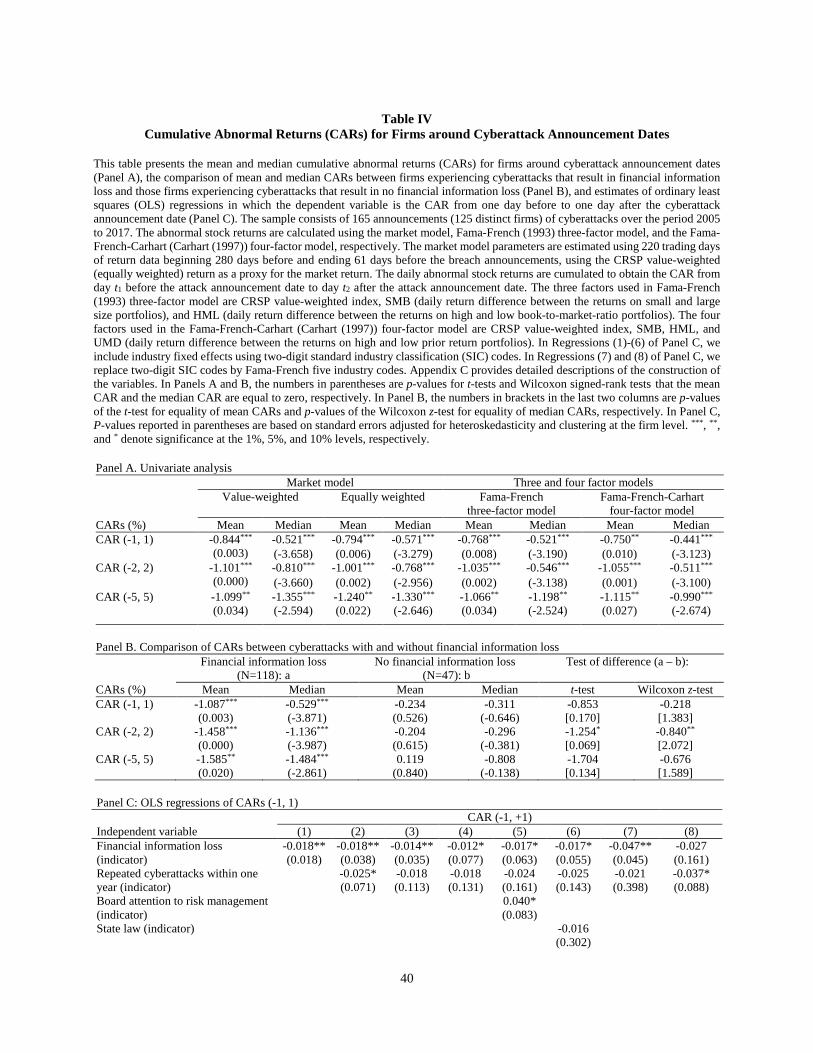

V. Impact of Cyberattacks on Shareholder Wealth

In this section, we investigate the shareholder wealth impact of cyberattacks using an event study. To

identify cyberattack announcement dates, we search news articles reported in Factiva for the 188 attacks

we identify. We also search Factiva for major confounding corporate events (e.g., announcements of

mergers and acquisitions, earnings, and security issuance) within one trading day before and after the

announcement and exclude observations associated with such news. Of 188 incidents, we are able to find

165 uncontaminated events in which news articles report cyberattacks and data on stock returns are not

missing in CRSP. We use the date when a news article reporting the cyberattack appears in Factiva for the

first time as the initial public announcement date. The abnormal stock returns are calculated using the

market model, the Fama-French (1993) three-factor model, and the Fama-French-Carhart (Carhart (1997))

four-factor model, respectively. The market model parameters are estimated using 220 trading days of

return data beginning 280 days before and ending 61 days before the breach announcement, using either

the value-weighted or the equally weighted CRSP index return as a proxy for the market return. The three

factors used in the Fama-French (1993) three-factor model are the CRSP value-weighted index, SMB (daily

return difference between the returns on small and large size portfolios), and HML (daily return difference

between the returns on high and low book-to-market-ratio portfolios). The four factors used in the Fama-

French-Carhart (Carhart (1997)) four-factor model are the CRSP value-weighted index, SMB, HML, and

UMD (daily return difference between the returns on high and low prior return portfolios). Daily abnormal

stock returns are cumulated to obtain the cumulative abnormal return (CAR) from day t1 before the breach

announcement date to day t2 after the breach announcement date.

Panel A of Table IV reports the mean and median CARs for various event windows. The mean CAR

(−1, 1), CAR (−2, 2), and CAR (−5, 5) computed using the market model and the CRSP value-weighted

index return are −0.84%, −1.10%, and −1.10%, respectively, all of which are significant. The corresponding

median CARs are −0.52%, −0.81%, and −1.36%, all of which are also significant. The results using the

CRSP equally weighted index return and those using the Fama-French (1993) three-factor model and the

Fama-French-Carhart (Carhart (1997)) four-factor model are similar.

19

In Panel B of Table IV, we examine whether the stock-price reaction differs when personal financial

information is stolen. We see that there is a highly significant difference in the stock-price reaction between

cyberattacks involving financial information loss and the other cyberattacks. The average CAR (−1, 1) is

−1.09% when there is financial information loss and an insignificant −0.23% when there is none. Similarly,

the corresponding average CARs (−2, 2) for cyberattacks with and without financial information loss are

−1.46% and −0.20%, respectively. The difference is significant at the 10% level. Tests for the significance

of median CARs using a non-parametric Wilcoxon signed-rank test show a similar pattern.

In untabulated tests, to examine whether the market reaction to cyberattacks worsens over time, we

also divide our sample into two sub-periods, the early sub-period from 2005 to June 2011 and the late sub-

period from July 2011 to 2017, and examine whether abnormal returns differ between these two sub-

periods. We find that the mean (median) CAR (-1, +1) for the early sub-period is -1.365 (-0.808) and the

corresponding CAR (-1, +1) for the late sub-period is -0.649 (-0.458), both of which are significant. The

difference in mean (median) CARs (-1, +1) between the two sub-periods is insignificant.

In Panel C, we investigate the determinants of the shareholder wealth impact of cyberattacks using

ordinary least squares (OLS) regressions in which the dependent variable is CAR (−1, 1). All regressions

use year and industry fixed effects (two-digit SIC codes) except for Regressions (3) and (4). We use as

explanatory variables firm size, log (firm age), ROA, leverage, sales growth, Tobin’s q, and institutional

block ownership. We also include an indicator that takes value equal to one if a firm’s Whited and Wu’s

(2006) index (WW index) is above the top tercile in a given year, and zero otherwise, an indicator that takes

the value one if a cyberattack involves financial information loss, and zero otherwise (Financial information

loss), and an indicator that takes value equal to one if a firm experiences another cyberattack incident within

one year of the previous cyberattack, and zero otherwise (Repeated cyberattacks within one year).

In Regression (1), we include only Financial information loss in addition to year and industry fixed

effects.14 We find that the coefficient on Financial information loss is negative and significant at the 1%

14 Although the PRC provides the information about the number of records breached, we do not use such information in our analyses. First, about a half of our sample observations used in our event study analysis have missing values on

20

level. The coefficient of −0.018 suggests that cyberattacks that involve the loss of financial information

lead to a 1.8 percentage points lower CAR (−1, 1) than those without such information loss. With a mean

market value of about $58.93 billion for our sample firms, the coefficient estimate of −0.018 suggests that,

all else equal, cyberattacks that result in financial information loss result in an average value loss of more

than $1.06 billion for the attacked firms than those that do not result in financial information loss.

In Regression (2), we add Repeated cyberattacks within one year and firm characteristics as additional

explanatory variables. The coefficient on Repeated cyberattacks within one year is −0.025 and significant

at the 10% level. The coefficient on Financial information loss is unchanged. It follows that repeated attacks

within one year involving financial information loss yield a stock-price reaction worse by 4.3 percentage

points than a first-time attack involving no information loss. Thus, firms experiencing repeated cyberattacks

have a more significant negative valuation effect than those experiencing a single cyberattack. We also find

that the market reaction is more negative when target firms are older and have higher leverage. The

coefficient on the indicator variable for financially constrained firms is insignificant.

In Regression (3), we add industry characteristics and find that the stock price reaction is not affected

by the degree of competition in an industry or by the uniqueness of industry products. However, firms in

industries with better growth opportunities are more adversely affected by a cyberattack.

In Regression (4), as in Regression (4) of Table III, we replace industry characteristics used in

Regression (3) with five industry indicators identified according to the first two-digit SIC codes and omit

the manufacturing industries. We do not find that the impact of attacks is worse for any particular industry.

In Regression (5), we examine whether board oversight of firm risk affects the impact of cyberattacks

on announcement returns. To capture board oversight of firm risk, we search a firm’s 10-K and Def14A

SEC filings.15 Specifically, we define Board attention to risk management as an indicator that takes value

the number of records breached. Second, the units of the number of records breached are not standardized and vary by incidents. 15 In Table III, we use BoardEx to define Risk committee for a large sample of firm-year observations covered in Compustat. Since BoardEx provides only the names of board committees, we identify the existence of a risk committee on the board by checking whether the name of a board committee includes “risk.” However, we find that some board committees whose names do not include “risk” still play an important role in firms’ risk oversight. For example, eBay

21

equal to one if a specific board committee (e.g., Enterprise-Wide Risk Management Committee, Risk

Committee, Audit and Risk committee, and Audit Committee that is responsible for risk oversight) or the

board as a whole explicitly monitors firm-wide risks and risk management, and zero otherwise. We find

that firms without board oversight of risk management experience a worse stock-price reaction by four

percentage points than those with board oversight of risk management.

In Regression (6), we examine whether the market reaction to a cyberattack announcement is affected

by the existence of a data breach notification law, which would affect managers’ incentives to disclose the

incidents. For example, managers of targets that are not subject to the state-level mandatory disclosure

requirements are likely to have greater incentives to withhold the bad news, which may cause more negative

announcement returns than those for incidents without information withholdings. To test this conjecture,

we add State law, an indicator that takes value equal to one if a firm is headquartered in a state in which a

data breach notification law is effective in a given year, and zero otherwise, and find that its coefficient is

negative and insignificant. However, it should be noted that, as discussed in Appendix A, a firm is required

to disclose a breach based upon the residency of the affected person, not based upon the location of the

breach. Given that a firm’s affected persons (for instance, customers) do not necessarily reside in its

headquarters state, this result should be interpreted with caution.

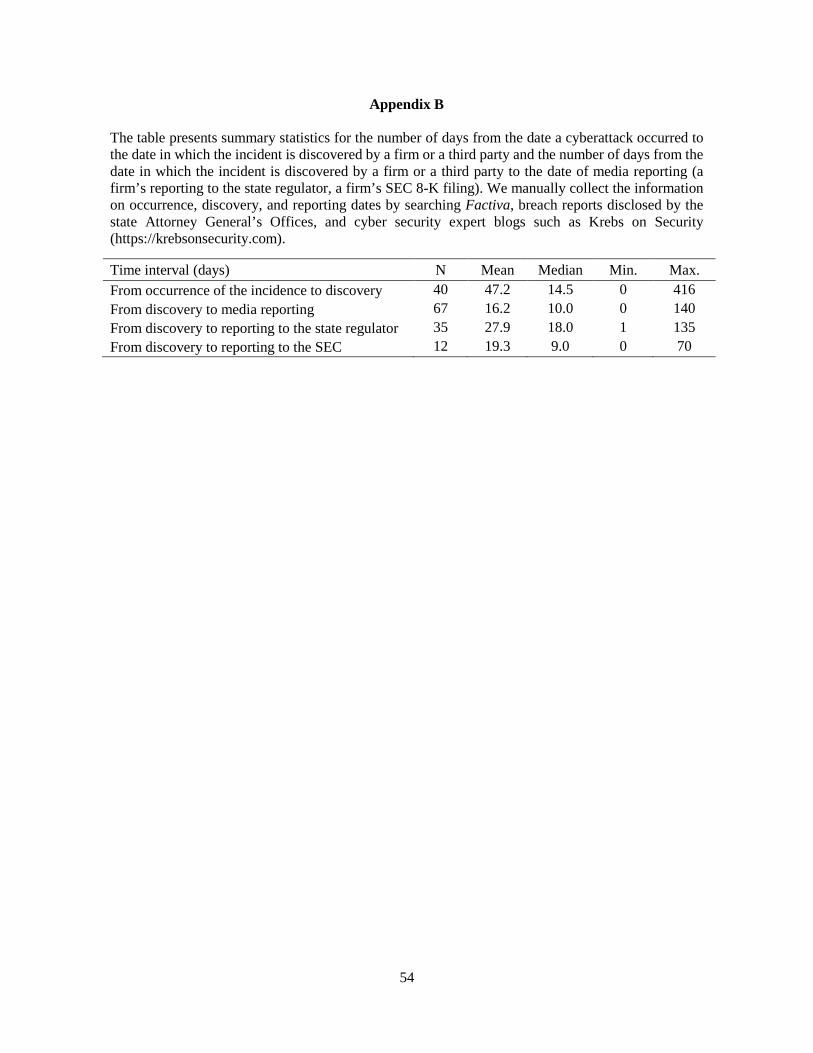

Next, we directly examine whether a firm’s delay of discovery and reporting about its cyberattack

affects its announcement return. To address this issue, we manually collect the information about the breach

date and the date in which the data breach was discovered by the target or a third party by searching Factiva,

breach reports disclosed by the state Attorney General’s Offices, and cyber security expert blogs such as

Krebs on Security.16 Using these dates, together with the announcement date obtained from Factiva, we

states in its 2016 proxy statement that “While the board is ultimately responsible for risk oversight at eBay, the board has delegated to the Audit Committee the primary responsibility for the oversight of risks facing our businesses.” Thus, using BoardEx data and focusing on board committee names alone does not allow us to accurately capture firms’ risk oversight at the board level in the case of firms such as eBay. To overcome this limitation of using BoardEx in identifying board oversight of firm risk, we manually collect the data on firm’s risk oversight by carefully reading 10-K and Def14A SEC filings for the relatively small sample used in Table IV. 16 https://krebsonsecurity.com

22

then construct two variables: 1) Delay of discovery, which is measured by the number of days from the

occurrence of the breach to the discovery of the breach by the firm and 2) Delay of reporting, which is

measured as the number of days from a firm’s discovery of the breach to the first media reporting. We use

Delay of discovery to capture the extent to which the firm finds it difficult to discover a security breach

caused by a cyberattack and Delay of reporting to capture the firm’s reporting delay of its incident.

Appendix B presents summary statistics for these two variables. Because of limited information available

in public sources and the difficulty to judge the exact timing of each event, the sample used in Appendix B

is very small. We find that the average (median) number of days from the occurrence to discovery is 47.2

(14.5) for a sample of 40 firms with the information available. We also find that the average number of

days from the discovery to the first media reporting is 16.2 for a sample of 67 firms with the information

available. The Appendix also reports that the average number of days from a firm’s discovery of the breach

to its reporting to the state regulator (a firm’s SEC 8-K filing) is 27.9 (19.3) days for a sample of 35 (12)

firms with the information available.

We estimate regressions where we use information about the delay in discovery and the delay in

reporting as key independent variables of interest. These regressions have to be treated with caution as the

sample size falls drastically. In Regression (7), we examine how a firm’s difficulty to discover the breach

affects its announcement return by adding the natural logarithm of Delay of discovery. Given that the sample

size used in the regression is very small, we replace two-digit SIC codes used to control for industry fixed

effects with Fama-French five industry codes. We find the market reaction is more negative for cyberattacks

in which target firms spent more time to uncover the breaches, suggesting that the firms’ difficulty in

detecting the attacks sends a bad signal to the market about the weakness of their internal controls and cyber

defenses. Excluding year fixed effects from the regression does not change the result. In Regression (8), we

examine how a firm’s delay in reporting an attack affects its abnormal return by including the natural

23

logarithm of Delay of reporting. We find that the coefficient on this variable is negative. However, it is not

significant, possibly due to the small sample size used in the regression.17

VI. Impact of Cyberattacks on Firm Performance, Risk, and Corporate Policies

A. Difference-in-differences Tests

To examine how cyberattacks affect firm performance, risk, and corporate policies, we perform

difference-in-differences tests using firm-year observations three years before and three years after the

attack. Since our difference-in-differences tests require three years of financial and stock return data after

the attacks, we do not include cyberattack events that occurred after 2014 in these analyses. We consider

only cyberattacks that result in financial information loss as our treatment sample since the analysis in

Section V shows that the negative impact of cyberattacks on firm value is concentrated in such events. For

firms that experience multiple cyberattacks during our sample period, we include only the first attack event.

For each treatment firm, we then identify a control firm that does not experience cyberattacks using

propensity-score matching. The propensity score is calculated using the logit regression of Cyberattack (an

indicator that takes value equal to one if a firm experiences a cyberattack in a given year, and zero

otherwise) on firm size, stock performance, stock return volatility, leverage, and the existence of an

institutional blockholder (indicator). We require both treated and matched firms to be in the same industry

(measured by two-digit SIC codes) as cyberattacks are concentrated among certain industries as shown in

the previous section. We also require treated and matched firms to be in the same fiscal year, so the control

firm has an “artificial” cyberattack year even if it does not experience a cyberattack (Chan, Chen, and Chen

(2013)). This approach allows us to perform difference-in-differences tests for the changes in performance,

risk, and corporate policies surrounding the cyberattack. We then match, without replacement, a target with

17 For a subsample of 67 firms for which discovery dates are available, in untabulated tests, we compute the average market-adjusted buy-and-hold stock return (HPR) from the discovery date to one day before the media reporting date and find that it (0.002) is not significant, suggesting no information leakage prior to the attack announcements.

24

a non-target control firm that has the closest propensity score with a caliper of 0.1 and a common support

range of 0.1 to 0.9 (Caliendo and Kopeinig (2008)).

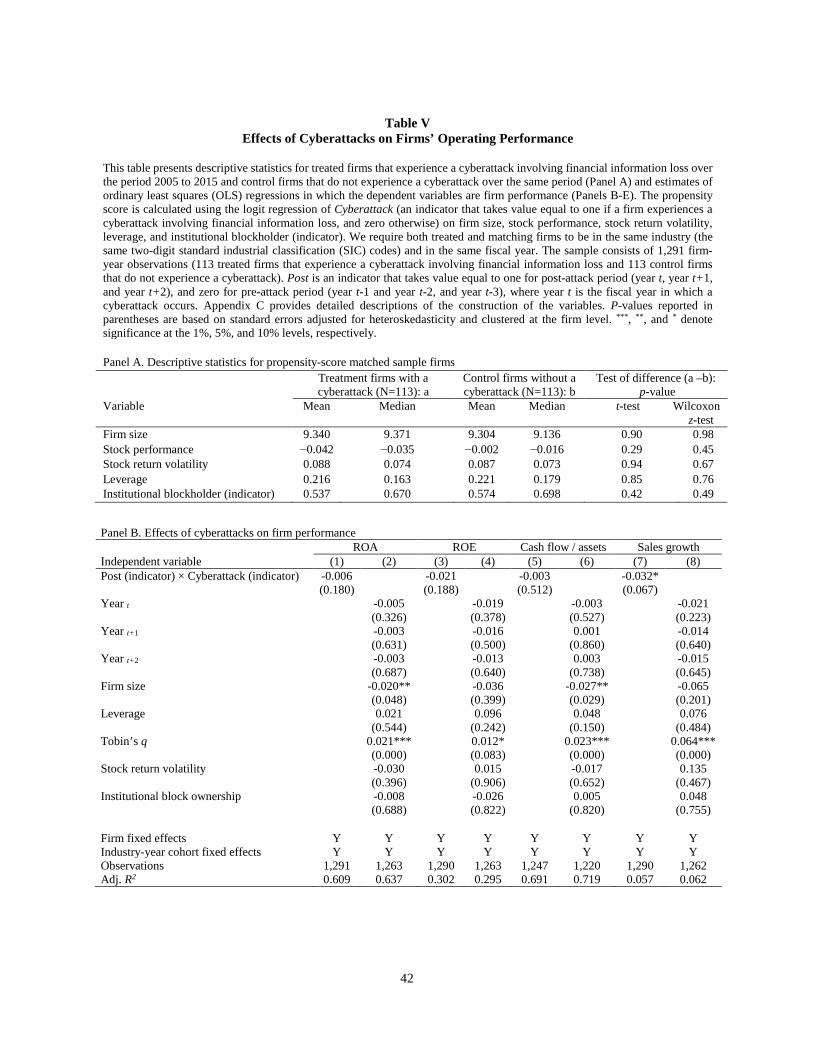

Panel A of Table V presents descriptive statistics for a sample of 226 propensity-score matched

sample firms (113 firms with a cyberattack that results in financial information loss and their 113 matching

firms).18 We find no significant difference between targets and their matching non-targets, suggesting our

matching approach identifies matching firms that are very similar to treatment firms.

We use the following difference-in-differences regression specification:

OPit = α + βPostit × Cyberattackit + γt + ωi + εit, (1)

where OPit is operating performance for firm i at time t. We measure firm operating performance using four

variables: ROA, ROE, cash flow/assets, and sales growth. In subsequent analyses, we replace OP with the

variables that measure firm risk and corporate policies. Postit is an indicator that takes value equal to one

for firm-years in the post-attack period (year t, year t+1, and year t+2), and zero for the pre-attack period

(year t-1, year t-2, year t-3), where year t is the fiscal year in which a cyberattack occurs. Cyberattackit is

an indicator that takes value equal to one if firm i at time t experiences a cyberattack, and zero if firm i at

time t is a non-target control firm. Our key independent variable of interest is the interaction term between

Post and Cyberattack. We include industry (Fama-French 48 industries)-year-cohort fixed effects (γt) since

the effects of cyberattacks that occur in a specific industry in recent years may be different from those that

occur in the industry in earlier years due to the changing nature of cyberattacks over time. We include firm

fixed effects (ωi) to account for unobserved heterogeneity across firms and to allow the heterogeneity to

vary across paired groups. Note that we do not control for time-varying firm-specific variables in the

regression since these firm characteristics can be affected by cyberattacks and thus including them in the

regression biases estimates of the interaction term between Post and Cyberattack.

18 We find that nine (two) out of 113 (113) control (treatment) firms are delisted as a result of mergers or voluntary delisting within three years of cyberattacks. Delisting of two control firms are triggered by performance-related reasons (delisting codes 500, 505 to 588) (Shumway and Warther (1999)). Thus, survivorship bias is unlikely to be a concern for our matching sample.

25

In a separate regression, we also break down the interaction term between Post and Cyberattack into

interaction terms for three subperiods in the post-attack period: Yeart, Yeart+1, and Yeart+2. In this

regression, we include firm-specific variables as additional controls. The reason for including controls is

that firm characteristics in years after the attack could affect operating performance in these years. Hence,

the interpretation of the coefficient on the interaction term involving Post for year t+1, for instance, would

be the impact of the attack at t+1 given how firm characteristics have evolved up to that year.19 The number

of firm-year observations differs across the regressions depending on the availability of variables computed

using Compustat, CRSP, and ExecuComp data.

B. Impact on Operating Performance

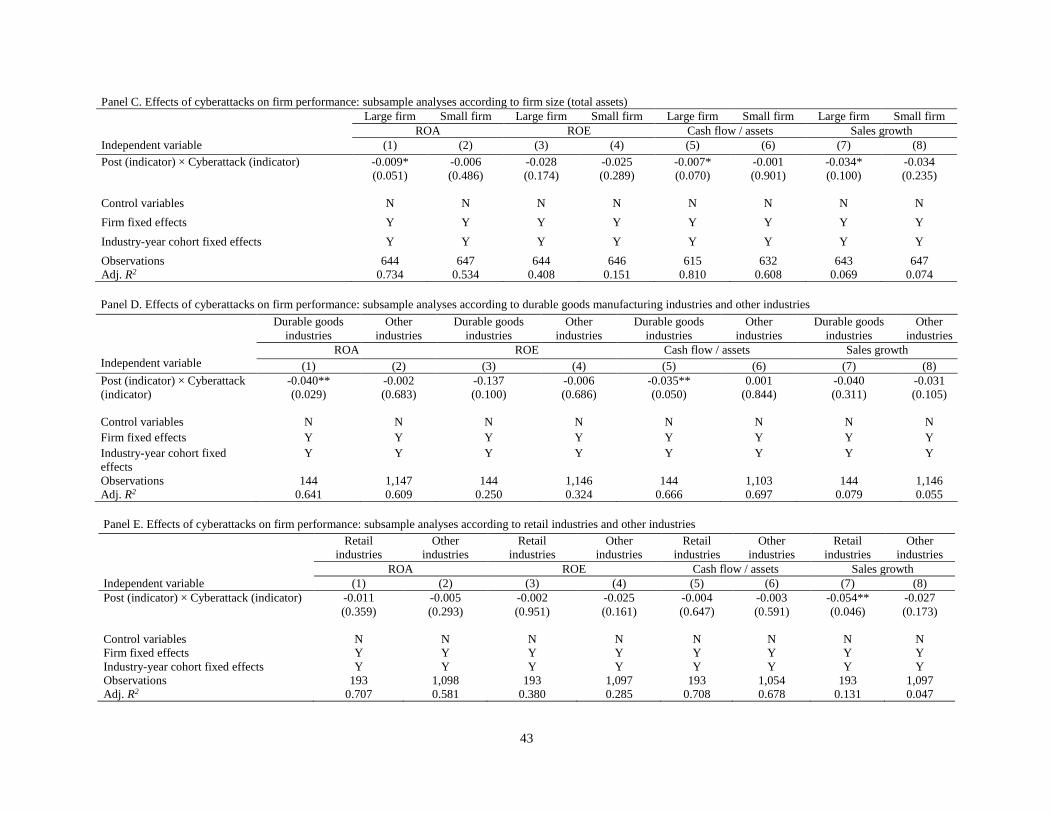

Panel B of Table V reports regression estimates using a firm’s operating performance as the dependent

variable. We find no significant impact of cyberattacks on ROA, ROE, and cash flow/assets but a significant

negative impact on sales growth. The lack of significance of ROA, ROE, and cash flow/assets for the full

sample may be due to the fact that the impact of cyberattacks on operating performance varies across firms

and industries. We show in Panels C, D, and E of Table V that this heterogeneity across firm types and

industries indeed matters to explain the impact of cyberattacks on operating performance. In Panel C, we

divide the sample into two subgroups according to median firm size (total assets). We find that large firms

experience a significant decrease in ROA, cash flow, and sales growth after the attacks. The decrease in

sales growth is of 3.4 percentage points (Regression (7)), which is large compared to the average sales

growth of 8 percent the year before the attack for the sample of targets. We see in Panel D that ROA and

cash flow deteriorate significantly for firms in durable goods industries, which produce more unique

products and impose higher liquidation costs on customers than other industries (Titman (1984)) following

19 In untabulated tests, we also divide the sample according to the sample median values of the Kaplan and Zingales’ (1997) index, the Whited and Wu’s (2006) index, and the S&P credit rating score, and whether the firm is a dividend payer in a given year and reestimate all the regressions in Tables V through X. We find no systematic evidence that firms’ performance, financial health, or corporate policies in the post-attack periods are affected by extent to which they are financially constrained.

26

attacks. In Panel E, we find that sales growth falls by 5.4 percentage points following attacks for firms in

retail industries. Hence, for subsamples of large firms, firms in durable goods manufacturing industries,

and firms in retail industries, the negative impact of cyberattack on operating performance is more severe.

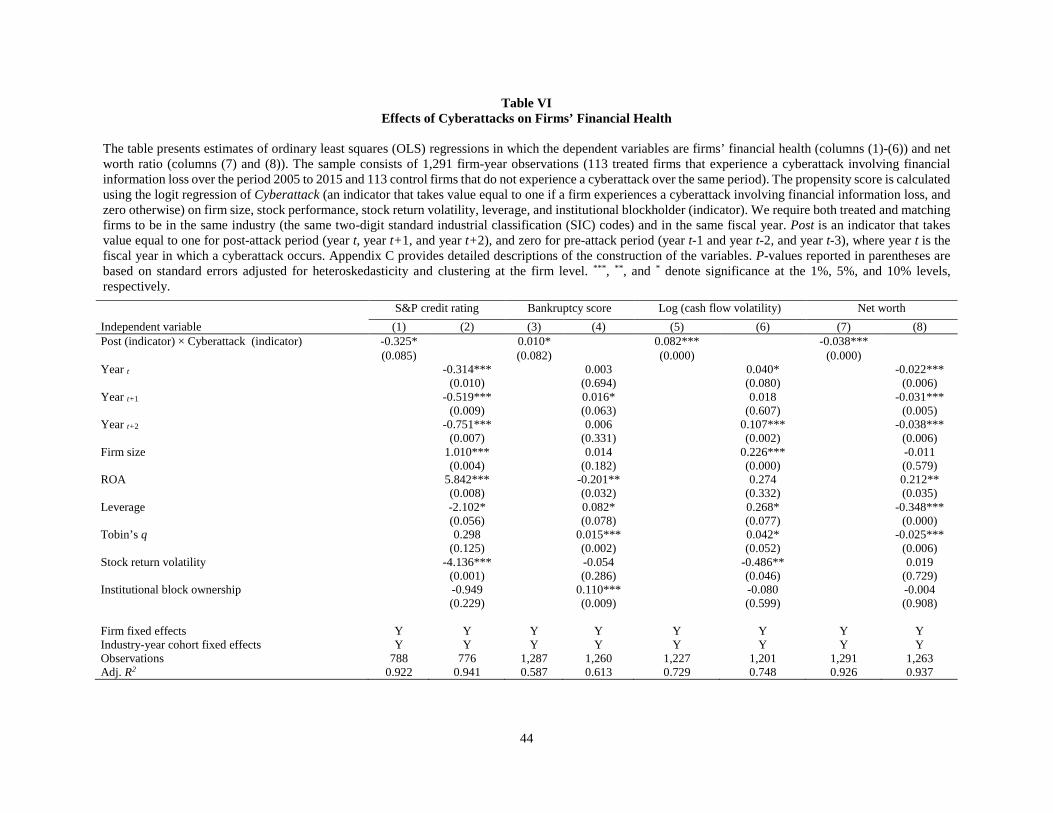

C. Impact on Financial Health

We next examine how cyberattacks affect a firm’s financial health. We use four measures of financial

health: Standard & Poor (S&P) credit rating, bankruptcy score, cash flow volatility, and net worth to total

assets. Table VI reports estimates of OLS regressions in which the dependent variables are these four

measures of financial health, respectively. Regressions (1) and (2) use S&P credit ratings as a measure of

financial health. We convert alphabetical symbols of S&P domestic long-term issuer credit ratings from

AAA+ to D into rating scale numbers (highest = 23, lowest =1) with higher numbers indicating better

ratings. There are 503 firm-year observations (39.0%) with no credit rating available. We exclude these

firms in estimating Regressions (1) and (2).20 We find that the coefficient on the interaction term between

Post and Cyberattack is negative and significant at the 10% level in Regression (1), suggesting that targets

experience deteriorating credit ratings in the post-attack period. The average three-year impact is -0.325

which corresponds to one third of a rating notch. Focusing on each post-attack year separately (i.e., years

t, t+1, and t+2) in Regression (2), we find that the decrease in credit rating is persistent for each of three

years after the attack.

In Regressions (3) and (4), we use the bankruptcy score (Shumway (2001)) as a measure of financial

health. We find that the coefficient on the interaction term between Post and Cyberattack is positive and

significant at the 10% level in Regression (3) for the three-year average. The coefficient is also positive and

significant for year t+1 in Regression (4), providing some evidence of an increase in bankruptcy probability.

20 In untabulated tests, we assign a rating scale number of zero for firms with no credit rating available, include an indicator that takes the value one for these firms in Regressions (1) and (2), and then reestimate the regressions. We find that our results do not change.

27

Greater cash flow volatility increases the risk that the firm will be short of cash. Regressions (5) and

(6) assess the impact of cyberattacks on cash flow volatility. Cash flow volatility is measured as the standard

deviation of quarterly cash flows from operations that are available from the statement of cash flows

(quarterly basic earnings per share before extraordinary items adjusted for stock splits) in a given fiscal

year. We find that the coefficients on the interaction term between Post and Cyberattack are positive and

significant in Regressions (5) and (6) except for Yeart+1, suggesting that targets experience a significant

increase in cash flow volatility.

Finally, in Regressions (7) and (8), we assess the impact of cyberattacks on the ratio of net worth

(stockholder equity) to total assets. A lower ratio of net worth to total assets means that the firm has less of

a cushion to cope with adversity. We see a significant reduction in this ratio for targets after the attack.

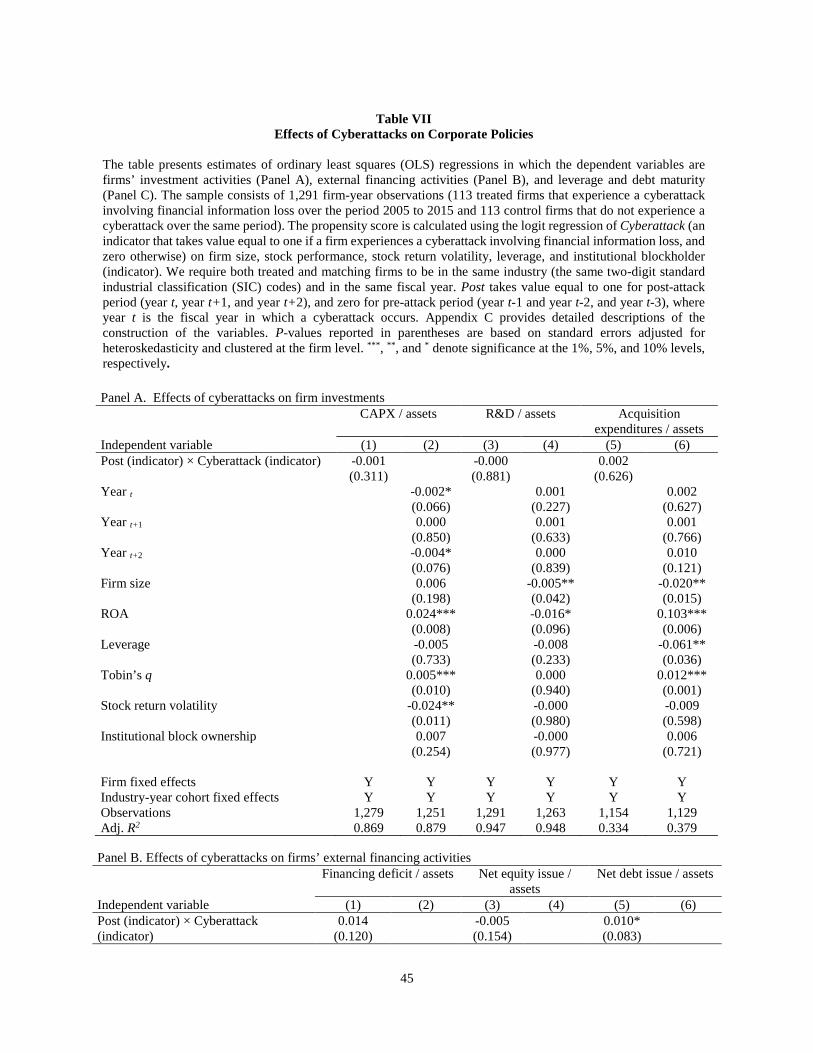

D. Impact on Investment and Financial Policies

In this subsection, we investigate how cyberattacks affect firms’ investment and financial policies. In

Panel A of Table VII, we break down a firm’s investment into three major components: capital

expenditures, research and development (R&D) expenditures, and expenses related to acquisitions. We find

no impact of cyberattacks on R&D expenditures and on expenses related to acquisitions. For capital

expenditures, we find an insignificant impact in Regression (1). However, when we investigate the impact

by year, we find a significant decrease in year t and in year t+2.

We next examine how firms’ external financing activities are affected by cyberattacks in Panel B of

Table VII. In Regressions (1) and (2), we first estimate the impact of a cyberattack on the firm’s financing

deficit. We find that the coefficient on the interaction term between Post and Cyberattack for the three-year

average is insignificant in Regression (1) but positive and significant for year t+1 in Regression (2),

providing weak evidence that a cyberattack increases a firm’s financing deficit. Regressions (3) and (4)

estimate the impact of a cyberattack on equity issuance. We see that firms do not attempt to reduce their

financing deficit by issuing equity. However, the next two regressions, Regressions (5) and (6), show that

a cyberattack leads targets to issue more debt than non-targets to make up their financing deficit.

28

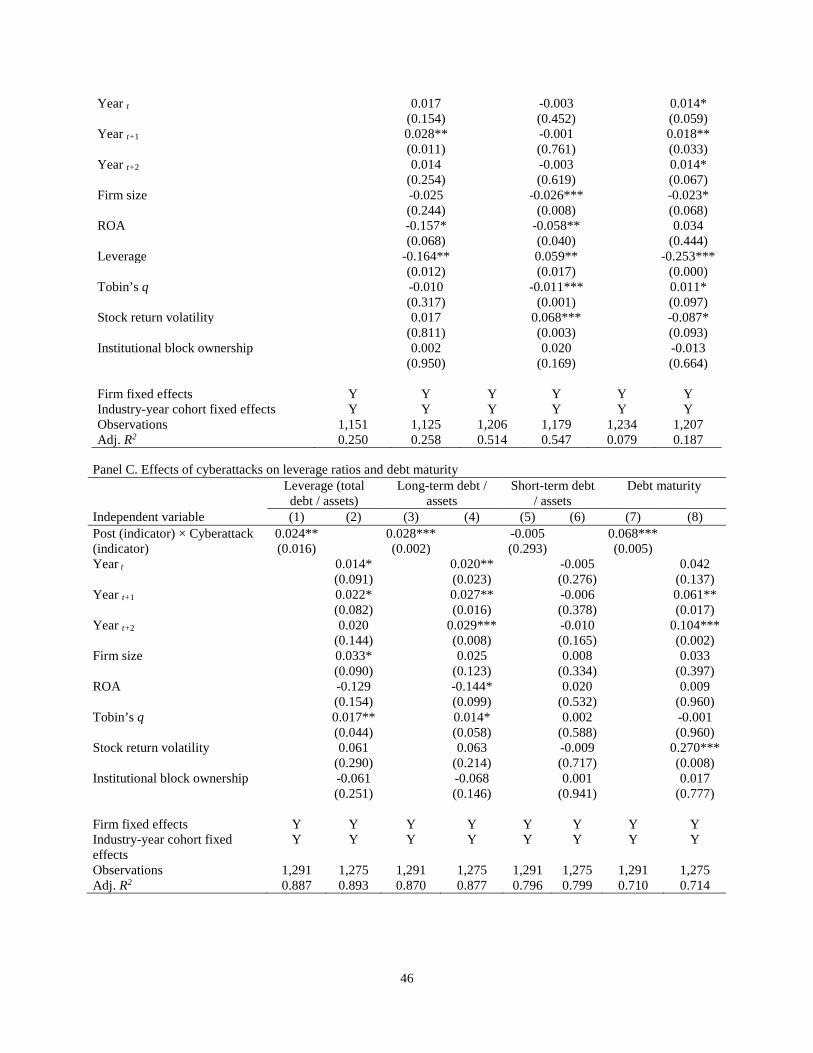

In Panel C of Table VII, we examine how the cyberattack affects a firm’s leverage and the composition

of its debt. Regressions (1) and (2) use the total debt ratio as the dependent variable. Consistent with the

results in the previous panel, we find that the coefficient on the interaction term between Post and

Cyberattack for the three-year average after the attack is positive and significant at the 5% level in

Regression (1). The coefficient estimate of 0.024 for the interaction term suggests that after the cyberattack,

targets experience a significant increase in their leverage ratio of 2.4 percentage points. Given that the mean

leverage ratio for the full sample is 22.3%, this increase corresponds roughly to a 10% increase in leverage.

Regressions (3) and (4) show the impact of the cyberattack on the long-term debt ratio. In Regression (3),

we find that the coefficient on the interaction term between Post and Cyberattack is a significant 0.028,

suggesting that the increase in target firms’ debt level mostly comes from an increase in long-term debt.