Embed Size (px)

Citation preview

Chapter 16

What Should Central Banks Do? Monetary PolicyGoals, Strategy, and Tactics

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-2

The Price Stability Goal

• Low and stable inflation• Inflation

Creates uncertainty and difficulty inplanning for futureLowers economic growthStrains social fabric

• Nominal anchor• Time-inconsistency problem

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-3

Other Goals of Monetary Policy

• High employment

• Economic growth

• Stability of financial markets

• Interest-rate stability

• Foreign exchange market stability

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-4

Should Price Stability be thePrimary Goal?

• In the long run there is no conflict between the goals

• In the short run it can conflict withthe goals of high employment and interest-rate stability

• Hierarchical mandate

• Dual mandate

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-5

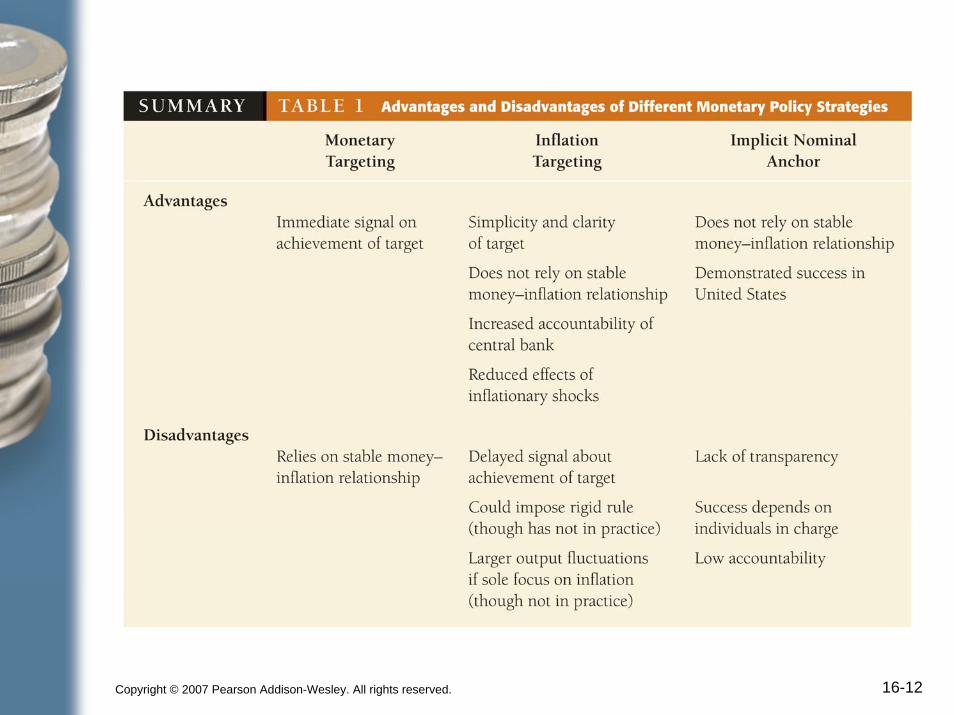

Monetary Targeting

• Flexible, transparent, accountable

• AdvantagesAlmost immediate signals help fix inflation expectations and produce less inflationAlmost immediate accountability

• DisadvantagesMust be a strong and reliable relationshipbetween the goal variable and the targeted monetary aggregate

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-6

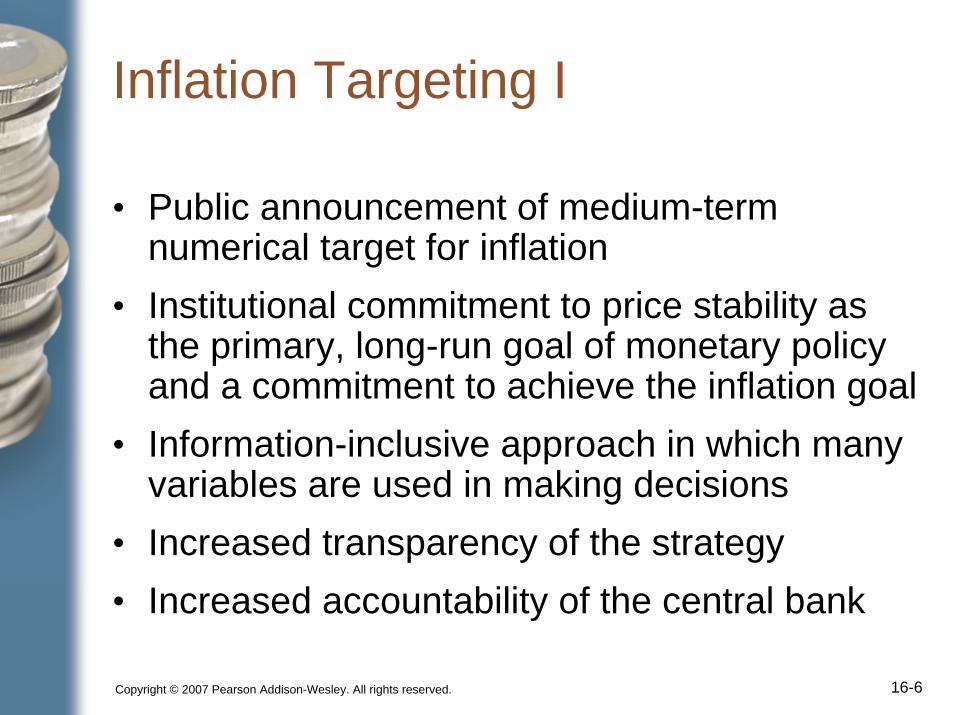

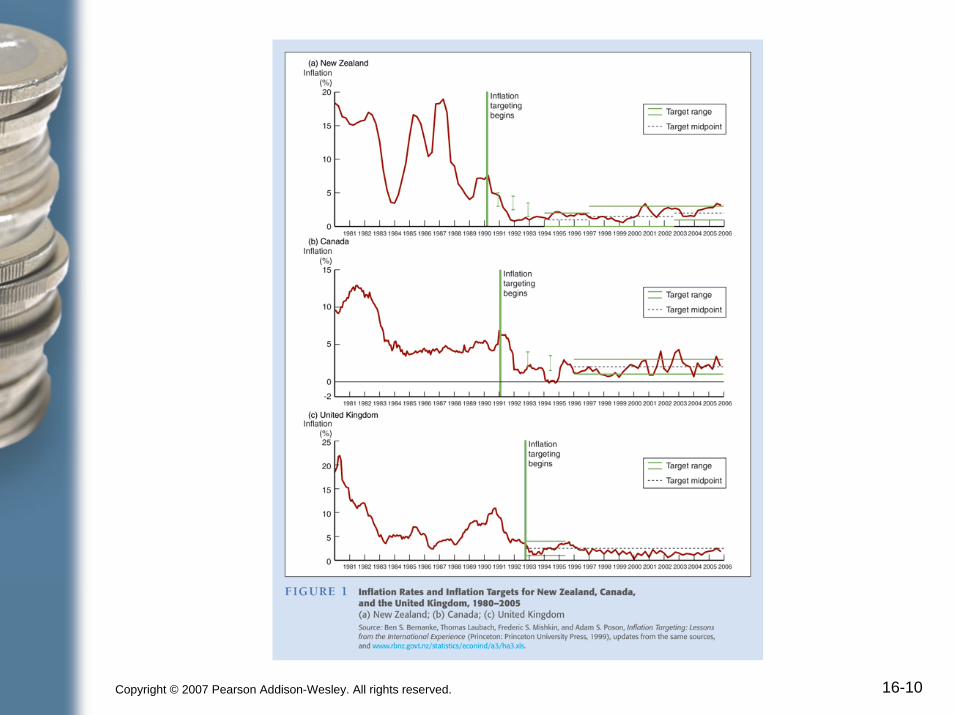

Inflation Targeting I

• Public announcement of medium-term numerical target for inflation

• Institutional commitment to price stability as the primary, long-run goal of monetary policy and a commitment to achieve the inflation goal

• Information-inclusive approach in which many variables are used in making decisions

• Increased transparency of the strategy• Increased accountability of the central bank

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-7

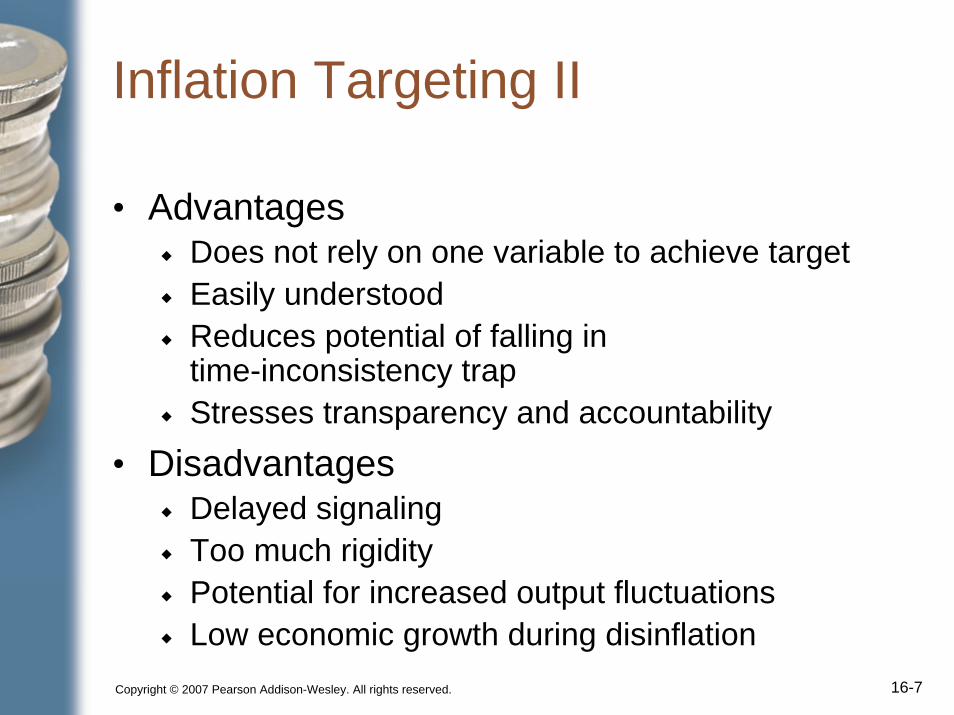

Inflation Targeting II

• AdvantagesDoes not rely on one variable to achieve targetEasily understoodReduces potential of falling intime-inconsistency trapStresses transparency and accountability

• DisadvantagesDelayed signalingToo much rigidityPotential for increased output fluctuationsLow economic growth during disinflation

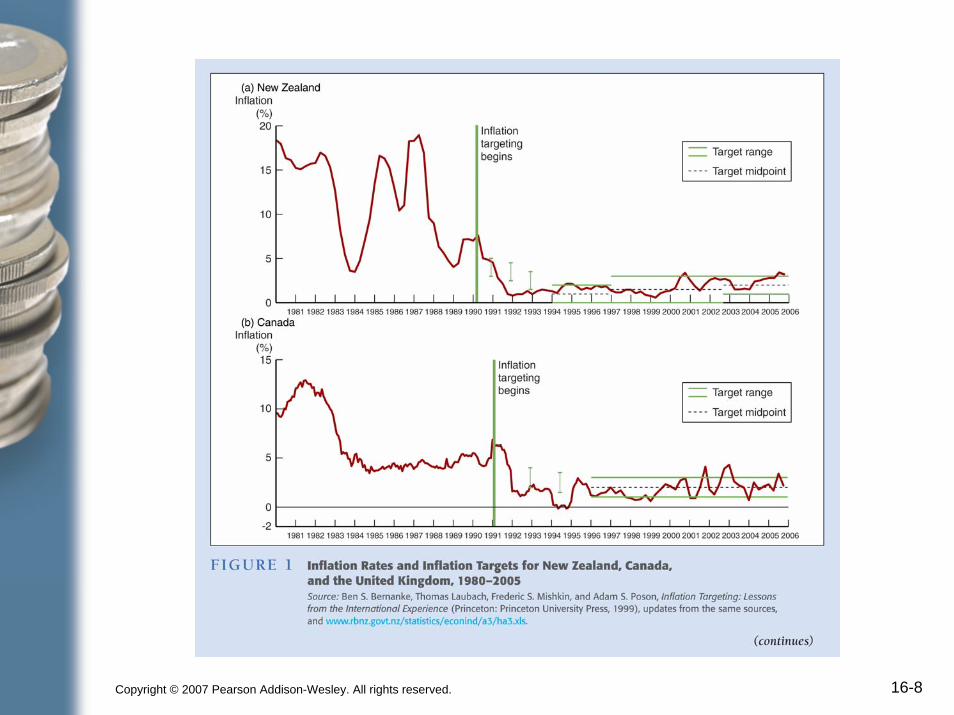

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-8

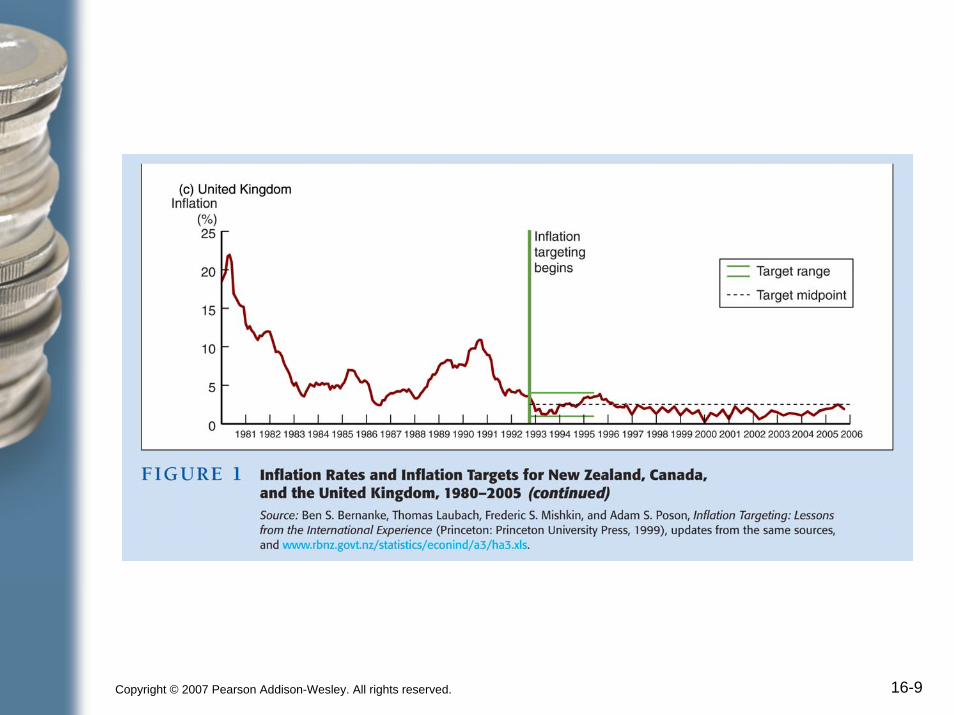

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-9

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-10

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-11

Implicit Nominal Anchor

• Forward looking and preemptive• Advantages

Uses many sources of informationAvoids time-inconsistency problemDemonstrated success

• DisadvantagesLack of transparency and accountabilityStrong dependence on the preferences, skills, and trustworthiness of individuals in chargeInconsistent with democratic principles

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-12

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-13

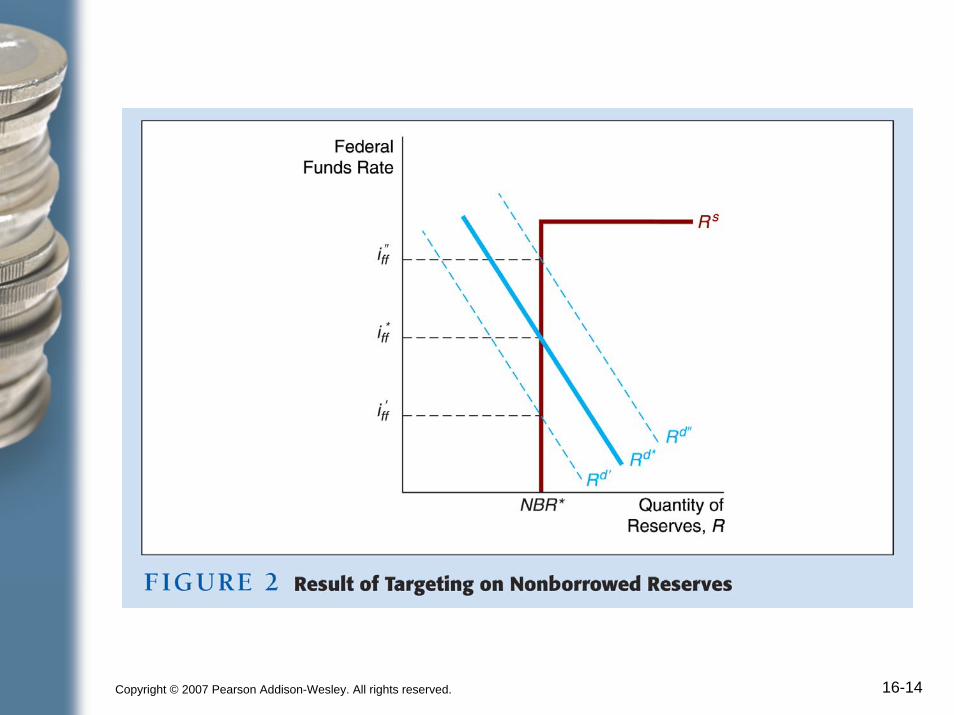

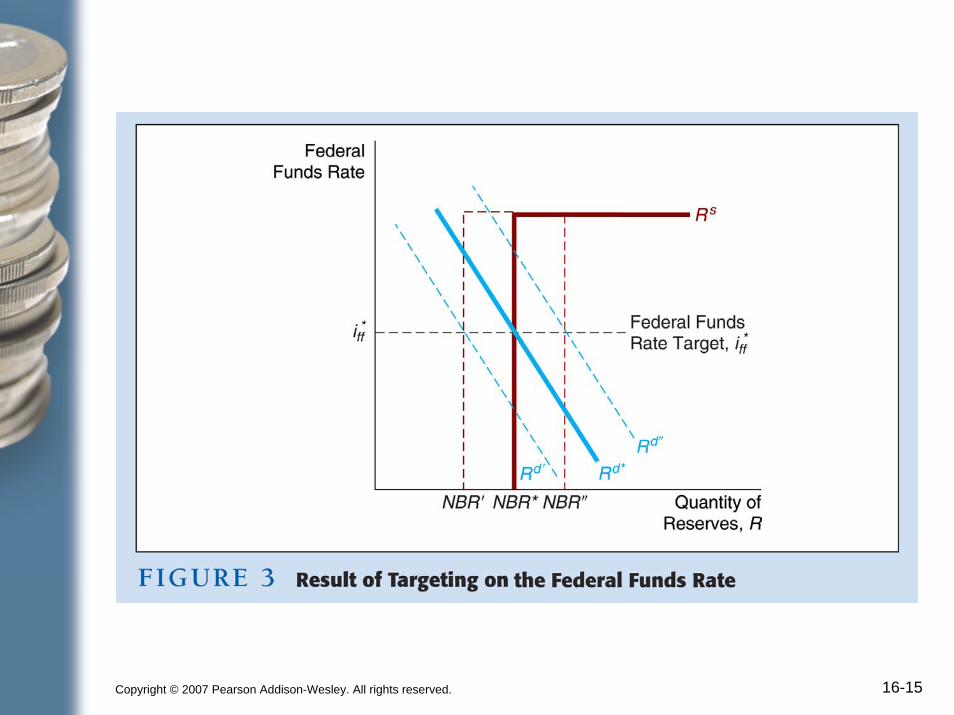

Tactics: Choosing the Policy Instrument

• ToolsOpen market operationReserve requirementsDiscount rate

• Policy instrument (operating instrument)Reserve aggregatesInterest ratesMay be linked to an intermediate target

• Interest-rate and aggregate targets are incompatible

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-14

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-15

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-16

Criteria for Choosing the Policy Instrument

• Observability and Measurability• Controllability• Predictable effect on Goals

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-17

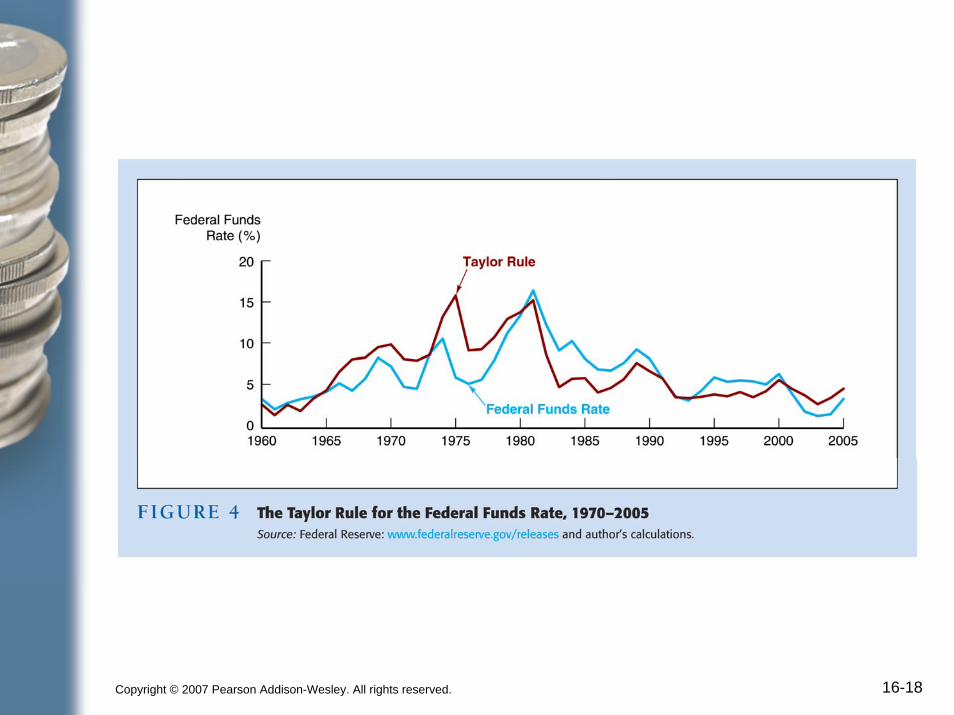

The Taylor Rule, NAIRU, and the Phillips Curve

Federal funds rate target =inflation rate+ equilibrium real fed funds rate

+1/2 (inflation gap)+1/2 (output gap)

• An inflation gap and an output gapStabilizing real output is an important concernOutput gap is an indicator of future inflation as shown by Phillips curve

• NAIRURate of unemployment at which there is no tendency for inflation to change

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 16-18