Embed Size (px)

Citation preview

What You Don’t Know Can Hurt YouSecurities Law Issues for Estate Planners

Anna T. PinedoMayer Brown LLPNew York, New York

Jay D. WaxenbergProskauer Rose LLPNew York, New York

I. Federal Securities Law

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners2

3

Securities Act of 1933

Overview • The Securities Act of 1933 (the “Securities Act”) regulates the offer and sale of

securities• Every offer and sale of securities must be registered with the SEC unless it is

exempt from registration (Section 5). Securities Act mantra: - Every offer and sale of securities is either:

- Registered - Exempt; or - Illegal

• Various exemptions from SEC registration are available, including exemptions for sales to sophisticated investors that do not require the protections of an SEC registration statement.

4

Registration or Exemption?

Registration:Section 5 of the Securities Act:• Section 5(c): No offers or sales until a registration statement has been filed with the SEC. • Section 5(b): After filing, all written offers must be made pursuant to the statutory prospectus. • Section 5(a): No sales of securities unless the SEC declares the registration statement “effective.” What does Section 5 registration provide investors? • Complete, fair and accurate information • Time to evaluate the information • A put right if the information turns out to be materially false

5

Definition of “Security”

Section 2(a)(1) • Under Section 2(a)(1) of the Securities Act, the term “security” is defined

broadly as: - Any note, stock, treasury stock, security future, security-based swap, bond, debenture, evidence

of indebtedness, certificate of interest or participation in any profit-sharing agreement, collateral-trust certificate, preorganization certificate or subscription, transferable share, investment contract, voting-trust certificate, certificate of deposit for a security, fractional undivided interest in oil, gas, or other mineral rights, any put, call, straddle, option, or privilege on any security, certificate of deposit, or group or index of securities (including any interest therein or based on the value thereof), or any put, call, straddle, option, or privilege entered into on a national securities exchange relating to foreign currency, or, in general, any interest or instrument commonly known as a “security”, or any certificate of interest or participation in, temporary or interim certificate for, receipt for, guarantee of, or warrant or right to subscribe to or purchase, any of the foregoing.

6

Definition of “Security,” cont’d

Howey Test• In order to determine whether an instrument should be considered a security, the Supreme

Court’s Howey case and subsequent case law have found that an “investment contract” exists when there is an investment of money in a common enterprise with a reasonable expectation of profits to be derived from the efforts of others.

• The form of the security (whether it is a formal certificate or nominal interest in the physical assets employed by the enterprise) is irrelevant.

• The “Howey test” applies to any contract, scheme, or transaction, regardless of whether it has any of the characteristics of typical securities.

• Once an instrument is determined to be a security, it is important to consider the status of the security and whether the offer of the security is subject to, or exempt from, registration. SEC v. W.J. Howey Co., 328 U.S. 293 (1946).

• Although the definition of a “security” in Howey differs from the Securities Act definition noted above, the Court has referred to the two definitions as being “virtually identical.”

7

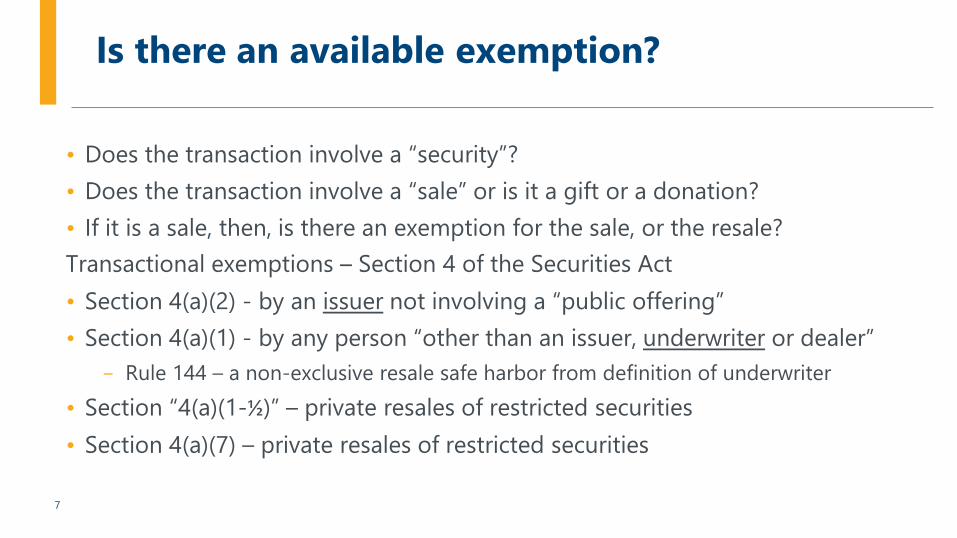

Is there an available exemption?

• Does the transaction involve a “security”?• Does the transaction involve a “sale” or is it a gift or a donation?• If it is a sale, then, is there an exemption for the sale, or the resale?Transactional exemptions – Section 4 of the Securities Act • Section 4(a)(2) - by an issuer not involving a “public offering” • Section 4(a)(1) - by any person “other than an issuer, underwriter or dealer”

- Rule 144 – a non-exclusive resale safe harbor from definition of underwriter • Section “4(a)(1-½)” – private resales of restricted securities • Section 4(a)(7) – private resales of restricted securities

8

Resale exemptions

• Resale exemptions include: - Rule 144: Non-exclusive safe harbor for public resale of restricted and control

securities subject to compliance with certain conditions - “Section 4(a)(1½)”: Technique developed by bar to facilitate private resales similar

to 4(a)(2) private placements - Rule 144A: Private resales to QIBs - Regulation S under Securities Act: Resales of securities in “offshore transactions”

with no “directed selling efforts” in United States

9

Restricted Securities

• Securities that were acquired in unregistered, private or exempt sales from the issuer or from an affiliate of the issuer. Restricted securities include:- Securities acquired directly or indirectly from the issuer, or from an affiliate of the

issuer, in a transaction or chain of transactions not involving any public offering;- Securities acquired from the issuer that are subject to the resale limitations of

Rule 502(d) of Regulation D or Rule 701(c) (securities issued under certain exempt employee benefit plans);

- Securities acquired in a transaction or chain of transactions meeting the requirements of Rule 144A; and

- Equity securities of domestic issuers acquired from the issuer, a distributor, or any of their respective affiliates in a transaction subject to the conditions of Rule 901 or Rule 903 of Regulation S.

10

Control Securities

• An affiliate of an issuer is defined to include “a person that directly, or indirectly through one or more intermediaries, controls, or is controlled by, or is under common control with such issuer” – Rule 144(a)(1)

• The term control means the possession, direct or indirect, of the power to direct or cause the direction of the management and policies – Rule 405

• The question of affiliate status often turns on the facts and circumstances of each particular case - Executive officers, directors or 10 percent or greater stockholders are generally

considered affiliates. - Lesser ownership might be sufficient in some cases to create affiliate status, and

ownership of a greater percentage might not create affiliate status where the facts support a conclusion that no control relationship is present.

11

Control Securities (cont’d)

• Securities of an issuer owned by an affiliate of the issuer. • How does Rule 144 control resales of control securities? See Rule 144(b)(2):

“Any affiliate of the issuer, or any person who was an affiliate at any time during the 90 days immediately before the sale, who sells restricted securities, or any person who sells restricted or any other securities for the account of an affiliate of the issuer of such securities, or any person who sells restricted or any other securities for the account of a person who was an affiliate at any time during the 90 days immediately before the sale, shall be deemed not to be an underwriter of those securities within the meaning of section 2(a)(11) of the [Securities] Act if all of the conditions of this section are met.” (Emphasis added.)

• The SEC takes the view that transactions, not securities, are registered. As a result, securities that were previously issued in registered offerings can become control securities, requiring an exemption (such as Rule 144) for, or registration of, their public resale.

12

Control Securities – Examples

Examples of registered securities that become control securities if owned by an affiliate of the issuer: • Registered securities issued in an offering registered on Form S-8 to an

affiliate of the issuer under an employee benefit plan; • Registered securities acquired by an affiliated dealer of the issuer (typically

in a market-making transaction); and • Any other securities (including registered securities) acquired by an affiliate

of the issuer (perhaps through a gift).

13

Who is an Underwriter?

Section 2(a)(11) of the Securities Act defines underwriter as any person who: • Buys from an issuer, or its affiliates, with a view to distribution; • Offers or sells for an issuer, or its affiliates, in connection with the

distribution of a security; • Participates, or has a direct or indirect participation, in such distribution; or • Participates or has a participation in the direct or indirect underwriting of

such distribution. An “affiliate” steps into the shoes of the issuer in this analysis

14

Rule 144 – Background

• Originally enacted in 1972, most recent amendments became effective in 2008. • Objective non-exclusive safe harbor that allows purchasers of privately-placed

securities, affiliates of the issuer, and professional intermediaries to demonstrate that their unregistered public resales do not require registration under Section 5 of the Securities Act.

• Allows for public sale of a limited volume of securities in ordinary trading transactions where there is adequate public information about the issuer

• Applies to sales of: - Restricted securities - whether held by affiliates or non-affiliates - Control securities - securities of an issuer held by affiliates of that issuer

15

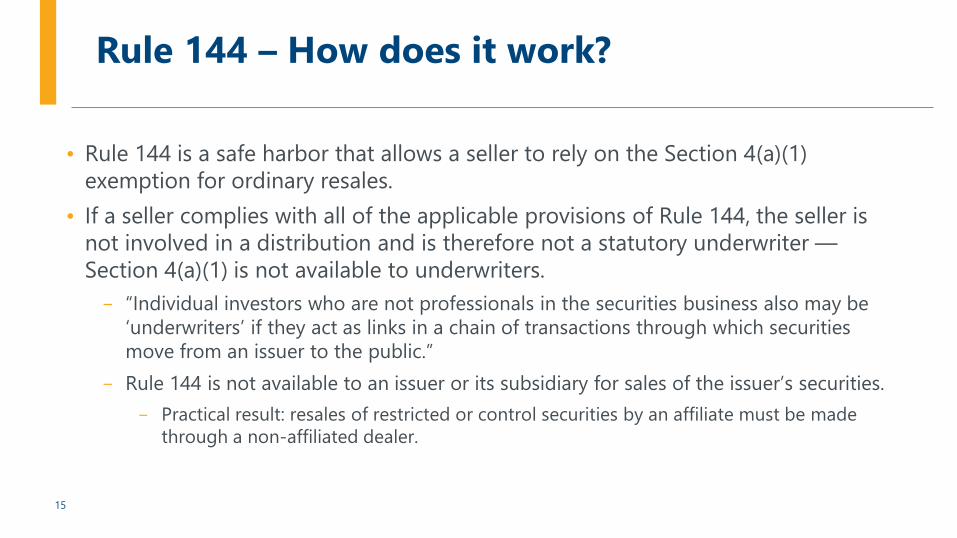

Rule 144 – How does it work?

• Rule 144 is a safe harbor that allows a seller to rely on the Section 4(a)(1) exemption for ordinary resales.

• If a seller complies with all of the applicable provisions of Rule 144, the seller is not involved in a distribution and is therefore not a statutory underwriter —Section 4(a)(1) is not available to underwriters. - “Individual investors who are not professionals in the securities business also may be

‘underwriters’ if they act as links in a chain of transactions through which securities move from an issuer to the public.”

- Rule 144 is not available to an issuer or its subsidiary for sales of the issuer’s securities. - Practical result: resales of restricted or control securities by an affiliate must be made

through a non-affiliated dealer.

16

Basic Requirements of Rule 144

• Current public information - 144(c) • Holding period for restricted securities - 144(d) • Volume limitations - 144(e) • Manner of sale requirements - 144(f) and (g) • Filing of Form 144 - 144(h)

17

Payment by Promissory Note

• Payment by a note or other obligation to the issuer is not deemed full payment of the purchase price unless the note or obligation: - Provides for full recourse against the purchaser; - Is secured by collateral, other than the securities purchased, having a fair market

value at least equal to the purchase price of the securities; and - Has been discharged by payment in full prior to sale of the securities.

18

Tacking of Holding Periods for Rule 144 Purposes

• Shares acquired from affiliates: - Generally, acquiring restricted securities from an affiliate will start a new holding

period. Tacking is permitted only in specified circumstances, generally in which there is an identity of interest between the affiliate/transferor and the transferee.

• Stock splits and recapitalizations • Convertible securities - if acquired by conversion without payment of additional

consideration to the issuer • Warrants – “net exercise” provision required; doesn’t apply to employee options • Pledged securities - only if bona fide pledgee with recourse • Gifts and donations • Estates – tacking permitted • Limited partnerships; if pro-rata distribution – aggregation required • REIT common stock acquired upon the redemption of UPREIT units

19

Release of Restrictions on Securities Held by Non-Affiliates – Rule 144(b)(1)

• Under Rule 144(b)(1)(i): - Non-affiliates of a reporting company may freely resell restricted securities held

for at least six months subject only to the Rule 144(c) current public information requirement until the securities have been held for one year

- Non-affiliates of non-reporting companies may freely resell restricted securities held for at least one year

- For non-affiliates there are no longer any restrictions on volume, manner of sale or notice.

- A non-affiliated seller is one who is not an affiliate of the issuer at the time of the sale and has not been an affiliate for the preceding three months

20

Volume Limitations Applicable to Affiliates

• For affiliates – Amount of securities that can be sold under Rule 144 during any three-month period (a “running” three months, not a calendar three months) may not exceed the greater of: - One percent of the outstanding securities of the class or - The average weekly trading volume in the security during the four calendar week

period preceding the filing of the notice of sale • Aggregation provisions in Rule 144 combine certain sales for purposes of

determining compliance with volume limitations (Rule 144(e)(3))

21

Manner of Sale Requirements For Affiliates

• Securities sold by affiliates under Rule 144 must be sold in either: - Brokers’ transactions – generally includes a transaction in which the broker does

no more than execute the order as agent, receives no more than the usual and customary broker’s commission and does not solicit the buy order;

- Directly to a market maker; or - Riskless principal transactions

• No manner of sale requirements for debt securities • No solicitation of orders to buy the securities in anticipation of or in

connection with the transaction • No payment to any person other than to the broker or dealer who executes

the transaction

22

Filing of Form 144

• A Form 144 must be filed if the amount of securities to be sold in reliance on Rule 144 during any period of three months will exceed 5,000 shares or have an aggregate sales price in excess of $50,000.

• Three copies of the notice must be sent to the SEC’s Washington, D.C. office concurrently with the placing of an order to sell with the broker or the execution of a sale directly with a market maker.

• Submission electronically via EDGAR is voluntary • One copy of the notice must also be filed with any principal national securities exchange on

which such securities are listed for trading • Persons filing a Form 144 must have a bona fide intention to sell the securities referenced

therein within a reasonable time after the filing of such notice • To accommodate Rule 10b5-1 trading plans, the seller’s representation regarding lack of non-

public information that is material adverse information about the issuer, the representation is either as of the date of the Form 144 or as of the date the Rule 10b5-1 trading plan was adopted.

23

Recap of Rule 144

Affiliate or Person Selling on Behalf of an Affiliate Non-Affiliate (and Has Not Been an Affiliate During the Prior Three Months)

Restricted Securities of

Reporting Issuers

During six-month holding period:No resales under Rule 144 permitted.After six-month holding period:May resell in accordance with all Rule 144 requirements including:•Current public information•Volume limitations;•Manner-of-sale requirements for equity securities; and•Filing of Form 144.

During six-month holding period:No resales under Rule 144 permitted.After six-month holding period but before one year:Unlimited public resales under Rule 144 except that the current public information requirement still applies.After one-year holding period: Unlimited public resales under Rule 144; need not comply with any other Rule 144 requirements.

Restricted Securities of

Non-Reporting

Issuers

During one-year holding period:No resales under Rule 144 permitted. After one-year holding period may resell in accordance with all Rule 144 requirements, including:•Current public information;•Volume limitations;•Manner-of-sale requirements for equity securities; and•Filing of Form 144.

During one-year holding period:No resales under Rule 144 permitted.After one-year holding period: Unlimited public resales under Rule 144; need not comply with any other Rule 144 requirements.

Unrestricted Securities

No holding period:May resell in accordance with all Rule 144 requirements, including:•Current public information•Volume limitations•Manner-of-sale requirements for equity securities; and•Filing of form 144.

No holding period:Unlimited public resales under Section 4(a)(1) of the Securities Act.Former affiliates cannot freely resell securities for a period of 90-days after they cease to be affiliates.

24

Exempt Sales under the Securities Act

Section 4(a)(2)• Issuer exemption • Most utilized exemption • Application of the private placement exemption, however, has been the

subject of significant debate due in large part to the brevity of its wording • Not a “public offering” has been defined by case law and SEC interpretation

and one may look to safe harbors as well

25

Exempt Sales under the Securities Act (cont’d)

The “4(a)(11/2) exemption”• The Section 4(a)(11/2) exemption has evolved in practice, without the benefit

of any official rulemaking. • It is a hybrid consisting of:

- A Section 4(a)(1) exemption which exempts transactions by anyone other than an “issuer, underwriter or dealer,” and

- A Section 4(a)(2) analysis to determine whether the seller is an “underwriter,” i.e., whether the seller purchased the securities with a view to a distribution.

• In 1980, the SEC recognized the Section 4(a)(11/2) exemption, which although not specifically provided for in the Securities Act “[is] clearly within its intended purpose,” provided that the established criteria for sales under both Sections 4(a)(1) and 4(a)(2) are satisfied.

26

Exempt Sales under the Securities Act (cont’d)

When is the “4(a)(11/2) exemption” used?• The Section 4(a)(11/2) exemption can be used by institutional investors to

resell restricted securities purchased in a private placement. • The Section 4(a)(11/2) exemption can also be used by affiliates for the sale of

control securities when Rule 144 is unavailable.

27

Exempt Sales under the Securities Act (cont’d)

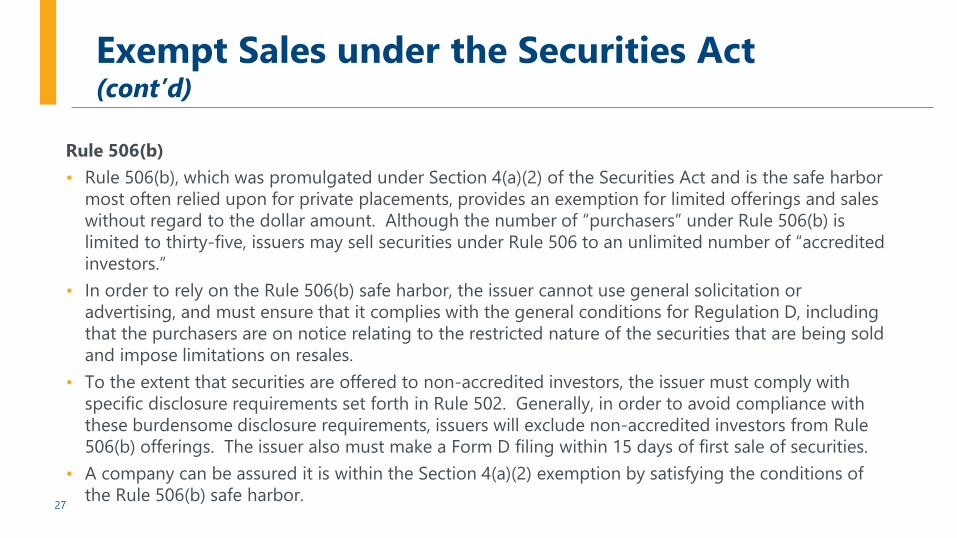

Rule 506(b) • Rule 506(b), which was promulgated under Section 4(a)(2) of the Securities Act and is the safe harbor

most often relied upon for private placements, provides an exemption for limited offerings and sales without regard to the dollar amount. Although the number of “purchasers” under Rule 506(b) is limited to thirty-five, issuers may sell securities under Rule 506 to an unlimited number of “accredited investors.”

• In order to rely on the Rule 506(b) safe harbor, the issuer cannot use general solicitation or advertising, and must ensure that it complies with the general conditions for Regulation D, including that the purchasers are on notice relating to the restricted nature of the securities that are being sold and impose limitations on resales.

• To the extent that securities are offered to non-accredited investors, the issuer must comply with specific disclosure requirements set forth in Rule 502. Generally, in order to avoid compliance with these burdensome disclosure requirements, issuers will exclude non-accredited investors from Rule 506(b) offerings. The issuer also must make a Form D filing within 15 days of first sale of securities.

• A company can be assured it is within the Section 4(a)(2) exemption by satisfying the conditions of the Rule 506(b) safe harbor.

28

Definition of “Accredited Investor”

• The current definition includes:- Natural persons meeting net worth or net income tests- Institutional accredited investors - Other entities (non-trusts) - Trusts- Director, executive officer, or general partner of the issuer - Employee benefit plans

• The SEC has proposed amendments to the current definition that would have the effect of expanding the types of persons and entities that would be considered “accredited investors”

29

Definition of “Accredited Investor”(cont’d)

• The proposed changes would include:

- Allowing individuals to qualify as accredited based on professional knowledge, certifications or experience

- Treating “knowledgeable employees” of private funds as accredited investors for purposes of investing in their funds

- Adding “family offices” with at least $5 million of AUM and their “family clients”

- Adding LLCs to the list of entities eligible to be accredited investors and QIBs

• The SEC also proposed amending Rule 144A to permit institutional accredited investors with an entity type not already included in the QIB definition to qualify as QIBs provided that the Rule 144A $100 million threshold for securities owned and invested is satisfied

30

Definition of “Insider”

• Federal law defines an “insider” as a “company’s officers, directors, or someone in control of at least 10% of a company’s equity securities” (an “Insider” and collectively, “Insiders”).

• Congress has criminalized these insiders’ use of non-public information under the theory that the use fraudulently violates a fiduciary duty with which the company has charged the insider. Companies are required to report trading by corporate officers, directors, or other company members with significant access to privileged information to the SEC.

• Under Section 16(a) of the Exchange Act, reports on Form 3, Form 4 and Form 5 of beneficial ownership are required to be filed with the SEC by Insiders.

31

Section 16: Reporting Requirements

Form 3: “Initial Statement of Beneficial Ownership”• The Form 3 initial statement of beneficial ownership details each Insider’s

direct and indirect beneficial ownership of equity securities of the company (and options, warrants and other rights relating to such securities).

• The initial filing (on Form 3) is due on or prior to the effective date of the IPO registration statement.

• Persons who become Insiders of the company after a company’s IPO must file a Form 3 report within ten days after first becoming an Insider.

32

Section 16: Reporting Requirements (cont’d)

Form 4: “Statement of Changes in Beneficial Ownership”• Changes in an Insider’s holdings of company securities must be reported on

Form 4.- Transactions include:

- Grants, awards and other acquisitions from the company;- Dispositions of securities by an Insider to the company;- “Discretionary transactions” under employee benefit plans (although delayed reporting

is available under certain circumstances); and- Open-market purchases and sales.

- Must be filed within two business days after the date on which a change occurs in an Insider’s direct or indirect beneficial ownership (i.e., the trade date, not settlement date).

33

Section 16: Reporting Requirements (cont’d)

Form 5: “Annual Statement of Changes in Beneficial Ownership” • Form 5: A Form 5 is required to be filed annually by an Insider if:

- The Insider had any exempt transactions (other than acquisitions of company common stock under the company compensation plans) that were not previously reported on a Form 4 filing for the fiscal year to which the Form 5 relates, or

- The Insider failed to file a required Form 3, Form 4 or Form 5 report for the fiscal year covered by the Form 5.

- The deadline for filing the Form 5 is 45 days after the end of the company’s fiscal year.

34

Section 16(b): Short-Swing Trading Profits

• The persons required to file reports on Forms 3, 4 and 5 are also subject to the “short-swing” provisions of Section 16(b) of the Exchange Act.- Section 16(b) is designed to prevent the unfair use of information that may be available to Insiders

of the company.• Section 16(b) provides: Any profit realized by an Insider within any six-month period from

matching purchases and sales, or matching sales and purchases, of company securities is recoverable by the company.

• Liability is strict — without regard to the purpose of the trades, whether or not material non-public information was actually misused, or whether or not the Insider intended any wrongdoing.

• SEC Rule 16b-3 exempts from Section 16(b) liability:- The receipt, expiration or cancellation of stock options under a stock option plan, and- Exercises of stock options granted under the plan.

• Suit to recover the profit may be instituted by the company, or a stockholder on behalf of the company (if the company fails or refuses to bring suit within 60 days after request or fails to prosecute the suit diligently).

35

Rule 10b-5: Insider Trading

• Rule 10b-5 of the Exchange Act makes it unlawful for directors, officers, employees, or their “tippees,” to trade for their benefit, or similarly recommend trading in securities, on the basis of material inside (non-public) information.- No director, officer, or employee of the company should trade when in possession of material non-

public information.- No one with knowledge of material inside information may provide “tips” for trading by others.

• An Insider’s family members and close associates might be presumed to have the Insider’s knowledge of any material inside information.

• Disclosure rules require the company to disclose material information if there is no legal or contractual reason to maintain its confidentiality.- The company must endeavor to make prompt, accurate and adequate disclosure information.- However, during a period when circumstances require that information be held in confidence,

persons having the information should not trade in company securities for any reason.• Legal liabilities for violating the insider trading laws include:

- Criminal penalties, civil damages to class action plaintiffs, and injunctions.

36

Rule 10b5-1 Trading Programs

• Rule 10b5-1 expands the opportunities for Insiders to sell (or purchase) company securities.

• Previously established trading arrangements are intended to give Insiders an affirmative defense to claims of insider trading liability under Rule 10b5-1 arising from transactions effected in accordance with the terms of those arrangements.- A properly designed trading program can provide Insiders who have access to material non-

public information with greater flexibility to enter into transactions involving company securities (notwithstanding restrictions of trading windows and blackout periods), while insulating the Insiders from potential insider trading liability.

• To comply with Rule 10b5-1, an Insider must, before becoming aware of any material non-public information:- Enter into a binding contract to purchase or sell securities,- Instruct another person to purchase or sell securities for the person’s account, or- Adopt a written plan for purchasing or selling the securities.

37

Rule 10b5-1 Trading Programs (cont’d)

• A trading program must contain one of the following elements:- It must specify the amount, price and date of the transaction(s);- It must include a written formula, algorithm or computer program for determining amounts,

prices and dates for the transaction(s); or- It must not permit the person to exercise any subsequent influence over how, when or whether

to make purchases or sales (and any other person exercising such influence under the program must not be aware of material non-public information).

• The trading arrangements under a program may include blind trusts or other trust agreements, pre-scheduled stock option exercises and sales, pre-arranged trading instructions, and other brokerage and third party arrangements.

• Transactions effected under a pre-established trading program may be better received by analysts and the investing public.

• It is in the interest of the company to reduce the risk of litigation and negative publicity and therefore, to reserve the right to approve or disapprove any proposed trading program.

38

Section 13: Beneficial Ownership Reports

• Section 13(d) under the Exchange Act requires disclosure of certain information to the company, to the stock exchange on which the company’s stock is traded and to the SEC within ten calendar days from the date on which any person or group of related persons becomes the direct or indirect beneficial owner of 5% of any class of the company’s equity securities (typically the common stock) whether or not pursuant to a tender offer.

• Section 13(d) rules provide for two types of filings for greater than 5% stockholders:- A long-form Schedule 13D, and- A short-form Schedule 13G (if stockholder meets “passive investor” criteria).

• A 5% stockholder who acquired common stock before a company’s IPO may use the short-form Schedule 13G to report its holdings regardless of the percentage of outstanding shares that those holdings represent.- The initial Schedule 13G of such a 5% stockholder must be filed with the SEC within 45 days after the

end of the calendar year in which a company completes its IPO, and- An amendment must be filed each year thereafter if there is a change in the 5% stockholder’s

holdings from the prior year.

39

Section 13: Beneficial Ownership Reports

• Other 5% stockholders who exceed the 5% threshold after the IPO must: - File an initial Schedule 13G within ten days after crossing the 5% threshold; and- An amendment must be filed by February 14 of the year following any changes in beneficial

ownership that occurred in the prior calendar year.• However, if a 5% stockholder’s holdings exceed 10% of the company’s common stock, the

stockholder must amend its original 13G filing “promptly” after its holdings exceed the 10% threshold or if it increases or decreases its ownership by more than 5%.

• 5% stockholders who are not eligible to file a short form Schedule 13G (as described above) generally must:- File a long-form Schedule 13D within ten days after their beneficial ownership exceeds 5% of the

outstanding securities of that class, and- Thereafter, are generally required to promptly amend their Schedule 13D filings to report any

material change in their holdings.- A change equal to greater than 1% of the common stock is presumptively “material” for this

purpose.

II. Estate Planning Transactions

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners40

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners41

II.A. In General• Federal securities law can affect the utility (and consequences)

of estate planning transactions. Accordingly, estate planning goals must be balanced with investment objectives and securities requirements.

• Estate planners must possess a basic understanding of securities rules to spot issues and anticipate registration requirements, reporting requirements and transfer restrictions applicable to estate planning activity.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners42

II.A. In General• Baseline example:

- Client is the founder of a U.S. company.- The company recently completed an IPO and has a class of

securities listed on a U.S. securities exchange.- Client serves on the board of directors and is an officer of the

company.- Client has a spouse and a child, neither of whom is an insider of

the company.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners43

II.B. Outright Lifetime Transfers• Example:

- Suppose our example client acquires shares of her company in a private offering and transfers them directly to her child.- What rules and/or reporting obligations apply to the donor-client?- Are there restrictions on the ability of the child-donee to re-sell the

transferred shares?- Must the child hold the transferred shares for a set period of time?- Are there differences in the treatment of shares acquired by gift versus

by sale?

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners44

II.B. Outright Lifetime Transfers (cont.)• Consequences to the Donor

- Disposition of beneficial ownership must be reported under Section 16(a) of the Exchange Act.

- Insider trading rules may apply (Rule 10b-5).- Short swing profit rules under Section 16(b) of the Exchange Act

will not apply if a transfer is by gift.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners45

II.B. Outright Lifetime Transfers (cont.)• Consequences to the Donee

- Shares transferred by a company insider may be subject to restrictions, even in the hands of the donee.- If the donor initially acquired the shares in a private offering, transferred shares

are “restricted” securities in the hands of the donee.- In our example, because they were acquired in a private offering, the

shares transferred to the child-donee are “restricted” in the child’s hands.- To sell or re-sell restricted securities, the donee must either (a) comply with

Rule 144 to avoid being treated as an “underwriter” under Section 4(1) of the Securities Act, or (b) qualify for another exemption to registration, such as “Section 4(a)(1½)” or Section 4(a)(7) (discussed further below).

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners46

II.B. Outright Lifetime Transfers (cont.)• Consequences to the Donee (cont.)

- Restricted Securities (Complying with Rule 144)- (1) “Holding Period” requirement (144(d))

- Donee must hold shares before sale for 6 or 12 months depending on the characteristics of the company (e.g., public/private, total asset value).- In our example, assume the child-donee’s holding period is six months, because the company

is listed on a US securities exchange and is subject to Sections 13 and 15(d) of the Exchange Act. (The holding period would be one year if the company were exempt from said Sections 13 and 15(d) for at least 90 days, or were a non-US company that is public in its home country.)

- Tacking of the holding period is possible if gift is from an “affiliate” of the company (i.e., the donor-client) to any donee (affiliate or non-affiliate). Tacking is not permitted if shares are purchased in a private transaction.- In our example, tacking is permitted because the shares were received by gift from an affiliate.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners47

II.B. Outright Lifetime Transfers (cont.)• Consequences to the Donee (cont.)

- Restricted Securities (Complying With Rule 144) (cont.)- (2) “Amount sold” (volume) requirement (144(e))

- Limits the amount the donee can resell.- Must be aggregated with client-donor’s sales if the donee is tacking onto

client’s holding period.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners48

II.B. Outright Lifetime Transfers (cont.)• Consequences to the Donee (cont.)

- Restricted Securities (Complying With Rule 144) (cont.)- (3) “Manner of sale” requirement (144(f))

- Restricts the method of sale by the donee (requires donee to sell through a broker-dealer, passively, into public markets).

- Requirements do not apply to gifts (not considered sales).- (4) Notice requirement (144(h))

- Donee must file Form 144 with the SEC if he or she sells, in any three month period, more than 5,000 shares or shares with an aggregate sale price in excess of $50,000.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners49

II.B. Outright Lifetime Transfers (cont.)• Consequences to the Donee (cont.)

- Restricted Securities (Other Exemptions from Registration)- “Section 4(a)(1½)” Exemption

- A seller (including an affiliate) who cannot meet or prefers to avoid the Rule 144 requirements may resell restricted securities using the “Section 4(a)(1½)” exemption, which developed under case law without the benefit of official rulemaking.

- The exemption involves a “hybrid” transaction in the sense that it complies with the principles of both Section 4(a)(1) and Section 4(a)(2) of the Securities Act.- The Section 4(a)(1) exemption from registration requirements exempts transactions by anyone

other than an “issuer, underwriter or dealer.”- The Section 4(a)(2) exemption involves an analysis to determine whether a seller is an

“underwriter” (i.e., whether the seller purchased the securities with the intent to distribute).

- The transferee/purchaser in a 4(a)(1½) transaction receives restricted securities.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners50

II.B. Outright Lifetime Transfers (cont.)• Consequences to the Donee (cont.)

- Restricted Securities (Other Exemptions from Registration) (cont.)- Section 4(a)(7) Exemption

- A seller can also avoid Rule 144 (and resell restricted securities without registration requirements) if:- Each purchaser is an accredited investor.- Neither the seller nor anyone acting for the seller engages in general

solicitation.- In the case of certain non-reporting issuers, at the seller’s request, the

seller and prospective purchaser obtain from the issuer reasonable current information meeting the conditions for such exemption (subject to a few exceptions).

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners51

II.B. Outright Lifetime Transfers (cont.)• Consequences to the Company—Restricted Securities

- “Current public information” requirement under Rule 144(c)- The company must have filed all required reports under Section 13 or

15(d) of the Exchange Act (as applicable, other than 8-Ks) during the 12 months before a sale of restricted securities. Includes 10-K & 10-Q

- The SEC expects companies (“reporting issuers”) to establish reasonable procedures to avoid violations.

- Nevertheless, the burden is on the donee to comply with Rule 144. A child-donee should therefore contact a securities lawyer before reselling gifted restricted shares.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners52

II.C. Lifetime Transfers in Trust• Revocable Trusts: Example

- Our client is a founder, director and officer of a company listed on a U.S. securities exchange.

- Client’s revocable trust provides that, during the client’s life, the client is sole trustee and beneficiary, and the client can revoke the trust unilaterally.

- Client transfers securities to his revocable trust.- Are the securities restricted when held by the revocable trust under Rule 144?- What reporting requirements apply to the client?- What reporting requirements apply to the revocable trust?- Do the short-swing profit rules (Section 16(b)) apply?- Do insider trading rules apply?

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners53

II.C. Lifetime Transfers in Trust (cont.)• Revocable Trusts: Rule 144

- Shares transferred to a revocable trust will be “restricted” securities (in the hands of the trust and beneficiaries) if the client-donor acquired them in a private offering. Thus, Rule 144 applies.- Donee (revocable trust) is subject to Rule 144 holding period (tacking allowed), amount

sold, manner of sale and notice requirements. - Company is subject to current public information requirement.- When selling shares, consider whether Section 4(a)(1½) or 4(a)(7) exemptions apply.

- If the transferor-client is an affiliate of the company and acquired the shares in the public market, they will be “restricted” securities under Rule 144, but only while the transferor-client is an affiliate.- NB: Affiliate status does not expire due to death of the transferor.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners54

II.C. Lifetime Transfers in Trust (cont.)• Revocable Trusts: Section 16 of the Exchange Act

- Client is treated as the beneficial owner of shares transferred to a revocable trust if he or she retains (a) investment control and (b) the power to unilaterally revoke the trust.- Client must report the shares on Form 4/5 as indirectly owned by her.

- In our example, the client must report the revocable trust’s shares as indirectly owned by him, because he retained investment control and unilateral revocation power.

- The revocable trust itself and transfer of securities thereto (as opposed to the client’s indirect ownership) are exempt from Section 16, because there was no change in “pecuniary interest.”- In our example, the revocable trust itself does not need to report share ownership (the client reports

it as indirectly owned). The client does not need to report the transactions in which he transfers securities to the revocable trust.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners55

II.C. Lifetime Transfers in Trust (cont.)• Revocable Trusts: Rule 10b-5

- If the insider-grantor is a director or officer of the company and in possession of material nonpublic information, any trade made by the insider-grantor on behalf of the trust will be subject to the Rule 10b-5 insider trading rules.- In our example, the donor-client is an insider likely in possession of

material nonpublic information. Accordingly, Rule 10b-5 applies to trades the client makes as Trustee on behalf of the revocable trust.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners56

II.C. Lifetime Transfers in Trust (cont.)• Irrevocable Trusts: Example:

- Client (an insider) funds an irrevocable trust by selling publicly traded stock to the trust in an exempt sale (or private placement) transaction.

- The Trust provides that Trustees may distribute income and principal to any of the client’s descendants for health, education, maintenance and support. Upon the death of the survivor of the client and the client’s spouse, trust property is held in further separate, continuing trusts for the grantor’s descendants.

- Trustee is the client’s child (an adult who does not live with the client). - The trust holds less than 10% of the company’s outstanding shares. - Neither the client nor the client’s spouse may direct sales/investments.

- For purposes of Rule 144, is the client’s child, as Trustee, an affiliate of the company because the child acts as Trustee?

- Is the trust an affiliate of the company?

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners57

II.C. Lifetime Transfers in Trust (cont.)• Irrevocable Trusts (cont.)

- Note about Grantor trust status- Grantor trust

- Client is deemed the “owner” for income tax purposes and is responsible for taxes on trust income.

- The income tax status of a trust is not dispositive, but helps clarify the securities law implications of a transfer into a trust.- Some common estate planning vehicles that are structured as

grantor trusts (e.g., GRATs) are treated as alter-egos of the grantor, exempting them from reporting requirements.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners58

II.C. Lifetime Transfers in Trust (cont.)• Irrevocable Trusts (cont.)

- Rule 144 Implications- Affiliate Status of Trustee

- Trustee’s individual affiliate status is based on facts and circumstances. Often, a child of a client-affiliate who is independent and does not live with the client will not herself be deemed an affiliate.- In our example, the client’s child-Trustee is likely not an affiliate,

because the child is independent and does not live with the client.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners59

II.C. Lifetime Transfers in Trust (cont.)• Irrevocable Trusts (cont.)

- Rule 144 Implications (cont.)- Affiliate Status of Trust Itself

- General Rule 1: Just because a Trustee or beneficiary of a trust is an affiliate does not mean the trust itself is necessarily an affiliate.

- General Rule 2: If an affiliate is both the Trustee (holding investment powers) and a beneficiary of a trust, the trust itself will be an affiliate for Rule 144 purposes.- Our example trust is not an affiliate by reason of its Trustee, because the Trustee is the client’s

child, who is not himself an affiliate. Neither the client nor her spouse can direct sales or investments, so no affiliate exercises investment powers.

- General Rule 3: If a trust holds 10% or more of the company’s outstanding shares, the trust is generally an affiliate regardless of the Trustee’s individual status.- Our example trust is not an affiliate by reason of share ownership.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners60

II.C. Lifetime Transfers in Trust (cont.)• Irrevocable Trusts (cont.)

- Rule 144 Implications (cont.)- Manner of Transfer to Trust

- If securities are transferred to the trust via an exempt sale (or private placement), they are restricted when held by the trust, and the trust is an affiliate even if the grantor ceases to be an affiliate. - In our example, the irrevocable trust was funded when the client (an affiliate) sold

shares to the trust in a private placement transaction. Accordingly, the securities are restricted when held by the trust, and the trust will be an affiliate even if the client sheds her affiliate status.

- When re-selling shares, consider whether Section 4(a)(1½) or 4(a)(7) applies.

- If securities are transferred to the trust by gift, the securities are still restricted, but the trust is only an affiliate while the grantor is an affiliate.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners61

II.C. Lifetime Transfers in Trust (cont.)• Accredited Investors and Qualified Purchasers

- Particularly important for private equity and hedge fund managers. - Many funds will only admit investors who satisfy one of these

definitions.- For transfers by gift, qualified purchaser status is generally

imputed to the trust (but accredited investor status is not), whether trust is a grantor or non-grantor trust (limited exceptions apply).

- If a trust purchases interests in a fund (transfer for value), accredited investor/qualified purchaser status is probably not imputed, so the trust must qualify independently.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners62

II.C. Lifetime Transfers in Trust (cont.)• Accredited Investors and Qualified Purchasers (cont.)

- Trust independently qualifies as a qualified purchaser if:- Trust owns at least $5 million in investments and has at least 2 beneficiaries who are

siblings or spouses (including former spouses), direct lineal descendants, spouses of such persons, estates of such persons, or charities/trusts established by or for such persons (Investment Company Act (ICA) Section 2(a)(51)(A)(ii)).

- Trust has at least one beneficiary who is not a family member of the client, both the grantor (client) and trustee are qualified purchasers, and the trust was not created for the specific purpose of acquiring the client’s fund interests (ICA Section 2(a)(51)(A)(iii)).

- Trust owns at least $25 million in investments and was not created for the specific purpose of acquiring the client’s fund interests (ICA Section 2(a)(51)(A)(iv)).

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners63

II.C. Lifetime Transfers in Trust (cont.)• Accredited Investors and Qualified Purchasers (cont.)

- Trust independently qualifies as an accredited investor if:- Bank acts as Trustee (Rule 501(a)(1) of Regulation D). Note, however, that it is unclear

whether a trust company qualifies as a bank.- Trust owns assets in excess of $5 million, trust was not formed for the specific purpose of

acquiring the securities and a “sophisticated person” directs the trust’s investments (Rule 501(a)(7) of Regulation D).

- (1) Fund manager-grantor (client) is an accredited investor, (2) the trust is a grantor trust, (3) an accredited investor is the sole source of funding, (4) an accredited investor is the Trustee and has sole investment discretion, (5) the entire amount of the client’s contribution (plus a fixed rate of return) will be paid to the client or the client’s estate before any payments are made to beneficiaries and (6) creditors of the client can reach the client’s interest in the trust assets at all times (Rule 501(a)(8) of Regulation D, Herbert S. Wander SEC No-Action Letter). Trust in Wander case was a GRAT (discussed below).

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners64

II.C. Lifetime Transfers in Trust (cont.)• GRATs: Example:

- Client is a director and an officer of a publicly traded company. Client funds his GRAT with shares of the company during a “non-blackout” period.

- The client transfers less than 10% of the company’s outstanding stock to the GRAT.

- The GRAT agreement provides that the GRAT will pay the client an annuity for two years, then the remainder passes in further trust to the client’s spouse and children.

- The GRAT may reimburse the grantor for income taxes.- Client is the sole Trustee of the GRAT during the GRAT term.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners65

II.C. Lifetime Transfers in Trust (cont.)• GRATs: Example (cont.):

- What are the client-grantor’s reporting obligations with respect to his transfer into the GRAT?

- What are the client-grantor’s reporting obligations with respect to GRAT-owned shares? What about when the GRAT transacts with third parties?

- Does the GRAT itself have reporting obligations?- How are the annuity payments treated and reported for Rule 16

purposes?- What if the GRAT transfers securities back to the client to reimburse

her for paying income taxes on GRAT assets?

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners66

II.C. Lifetime Transfers in Trust (cont.)• GRATs (cont.)

- Section 16 Implications for GRAT Itself- The GRAT itself will only be required to report a transaction under Section

16 if the GRAT owns at least 10% of the company’s outstanding stock immediately prior to the transaction. Otherwise, the GRAT itself is exempt.

- Section 16 Implications for Beneficiary - A beneficiary need only report a transaction under Section 16 if the GRAT

owns at least 10% of the company’s outstanding stock immediately prior to the transaction, the beneficiary exercises “investment control” over the GRAT and the transaction is a purchase or sale.

- In our example, neither the GRAT nor the beneficiaries have reporting obligations (in such capacities) under Section 16.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners67

II.C. Lifetime Transfers in Trust (cont.)• GRATs (cont.)

- Section 16 (and other) Implications for Client (insider-grantor) - Funding and Annuity Payments.

- The client’s initial transfer to the GRAT and each annuity payment are exempt from Section 16 reporting requirements as long as (a) the company insider is both the grantor and the sole trustee having investment control, and (b) the insider-grantor receives annuity payments from the GRAT, as the sole annuitant, during the GRAT term (Peter J. Kight SEC No-Action Letter).

- However, the grantor must report GRAT shares as indirectly owned by him or her.- In our example, the client’s funding of the GRAT and the annuity payments are exempt from Section

16 reporting requirements. The client-grantor will need to report GRAT-held shares on Form 4/5 as indirectly owned by him. Although they are not reportable, the annuity payments (to the extent they are made in kind) will change the balance of shares owned outright by the client (reportable as directly owned) versus owned by the GRAT (reportable as indirectly owned by the client).

- Note: The GRAT itself is not exempt if it owns 10% or more of the company’s outstanding shares.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners68

II.C. Lifetime Transfers in Trust (cont.)• GRATs (cont.)

- Section 16 (and other) Implications for Client (insider-grantor) - Funding GRATs During Blackout Periods—Rule 10b-5.

- Estate planners must avoid funding GRATs during blackout periods, when such transfers are prohibited (other than under a Rule 10b5-1 plan).

- GRAT may expressly permit the Trustee to enter into a Rule 10b5-1 plan to avoid blackout limitations.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners69

II.C. Lifetime Transfers in Trust (cont.)• GRATs (cont.)

- Section 16 (and other) Implications for Client (insider-grantor) (cont.)- Transactions (Other than Annuity Payments) During the GRAT Term

- The GRAT is the grantor’s alter-ego for Section 16 reporting purposes (i.e., reporting changes in beneficial ownership). Thus, most transactions between grantor and GRAT are not reportable.

- However, in the landmark case Morales v. Quintiles, 25 F. Sup. 2d 369, the purchase of shares from a GRAT for a note was ruled a “purchase” by grantor subject Section 16(b) short-swing trading rules.

- Morales distinguished a purchase for a note from the annuity payments discussed in Kight—in Kight, annuity payments were fixed at the time the GRAT agreement was signed, whereas the transaction in Morales was timed to gain advantage, and therefore more appropriate to treat as a “purchase.”

- The result in Morales suggests that a grantor who withdraws or contributes shares from/to a GRAT at irregular intervals (i.e., any transaction other than an annuity payment) must comply with Section 16 reporting requirements, regardless of the general rule that the GRAT is the grantor’s alter-ego.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners70

II.C. Lifetime Transfers in Trust (cont.)• GRATs (cont.)

- Section 16 (and other) Implications for Client (insider-grantor) (cont.)- Transactions (Other than Annuity Payments) During the GRAT Term

(cont.)- Transactions between GRAT and third parties are reportable by insider-grantor as the

grantor’s own indirect transactions.- Transfers of securities from the GRAT to the grantor to reimburse the grantor for

income taxes are not reportable because the GRAT is the grantor’s alter-ego. - After the GRAT term (even if the final annuity payment has not been made), the

insider-grantor is no longer the GRAT’s alter-ego; the GRAT must then report its own transactions.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners71

II.C. Lifetime Transfers in Trust (cont.)• GRATs (cont.)

- Termination of GRAT (end of annuity term)- Grantor ceases to be the GRAT’s alter ego for Section 16 purposes.- GRAT’s distributions of shares to beneficiaries (including continuing

trusts) are reported by the insider-grantor as gifts on Form 4 or 5.- If, after the GRAT term, a GRAT beneficiary is deemed the grantor’s

alter-ego for Section 16 purposes, the beneficiary’s sales could be matched against a purchase by grantor.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners72

II.C. Lifetime Transfers in Trust (cont.)• Sales and Gifts to IDGTs

- IDGT: Intentionally defective grantor trust. Irrevocable trust that allows the grantor to transfer assets outside his or her estate, but is “defective” for income tax purposes so that the grantor pays income tax on trust assets.- May involve transferring assets by gift.- May involve a transfer by sale to the IDGT for an installment note

payable to the grantor.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners73

II.C. Lifetime Transfers in Trust (cont.)• Sales and Gifts to IDGTs: Example:

- Client is an insider of a publicly traded company.- Client creates an IDGT (intentionally defective grantor trust) and

sells shares of the public company to the IDGT for a note.- The client’s sibling (who is also an insider of the company) is sole

Trustee of the IDGT.- During the client’s life, distributions can be made to the client’s

children or spouse. On the death of the survivor of the client and her spouse, the principal splits into continuing trusts for the grantor’s children.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners74

II.C. Lifetime Transfers in Trust (cont.)• Sales and Gifts to IDGTs: Example (cont.):

- What are the client’s reporting obligations upon selling the shares to the IDGT?

- What are the client’s reporting obligations upon the expiration of the note?

- When is the client considered to have beneficial ownership of the shares held in the trust?

- What securities rules apply while the note is outstanding?

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners75

II.C. Lifetime Transfers in Trust (cont.)• Sales and Gifts to IDGTs (cont.)

- Transfers to IDGT by Gift- Shares of publicly traded company are exempt from short-swing profit

rule of Section 16(b).- Gift itself is eligible for deferred reporting on Form 5.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners76

II.C. Lifetime Transfers in Trust (cont.)• Sales and Gifts to IDGTs (cont.)

- Sales to IDGT by Installment Sale (Exchange for Note)- Generally, sales to IDGTs are subject to reporting requirements and

restrictions under Section 16(a) and 16(b) because they are treated as dispositions of the shares for value.

- Because the insider-grantor is receiving note payments, the grantor may be deemed to have beneficial ownership of the shares (must report ownership on Form 4/5).- In our example, the client need not report the sale to the IDGT as a change in beneficial ownership,

because the client receives note payments under the note used to purchase the shares. However, the client must report the shares as indirectly, rather than directly, owned.

- When the note expires, the grantor will no longer have beneficial ownership of the shares, unless the grantor retained investment control over the trust.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners77

II.C. Lifetime Transfers in Trust (cont.)• Decanting

- A transfer without consideration, to a trust with identical material terms, may be exempt from Section 16 requirements as a transaction that only changes beneficial ownership, but does not change pecuniary interests. (Rule 16a-13).- E.g., a decant to extend a trust term may be exempt from Section 16.

- A transfer changing material terms (e.g., changing the beneficiaries), may be considered a change of beneficial ownership not exempt from Section 16.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners78

II.C. Lifetime Transfers in Trust (cont.)• Substitutions of Property

- Under Morales v. Quintiles, a substitution of trust property for other property of equivalent value would likely be treated as a transfer for consideration for Section 16 purposes.

- Such transfer would not be exempt from Section 16(a) or 16(b); it would be reportable on Form 4 and subject to short-swing profit rules.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners79

II.C. Lifetime Transfers in Trust (cont.)• Issues Relating to Trustees

- If a Trustee is a company insider and the trust owns shares of said company, the Trustee him/herself may be deemed to have a pecuniary interest in the trust if:- Trustee is a beneficiary

- Pecuniary interest (proportionate to his/her share of the trust) reportable on Form 4/5.

- Trustee is paid a performance-based fee from the trust- Generally, a fee representing an interest in a share of trust profits (as opposed to an

asset-based fee) is reportable as a pecuniary interest (exceptions apply).

- Trustee exercises investment control- A Trustee (or other person, even if not a “Trustee”) who exercises investment control

will be found to have a pecuniary interest on the basis of acting as Trustee.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners80

II.C. Lifetime Transfers in Trust (cont.)• Issues Relating to Trustees (cont.)

- Consequences of Remove and Replace Powers- A grantor who retains removal powers is not deemed to be a

beneficial owner per se. (Exchange Act Release No. 34-28869, SEC Docket 255 (Feb. 26, 1991)).

- Unclear whether remove and replace powers together give rise to beneficial ownership.

- To be cautious, an insider-grantor should consider reporting remove and/or replace powers on a Form 4 (especially if grantor is a beneficiary or trust protector), and disclaiming share ownership for Section 16 reporting purposes.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners81

II.D. Testamentary Transfers• Affiliate Status and Rule 144

- If a client-affiliate owned less than 10% of a company’s shares, his or her estate will likely not be deemed an affiliate (on that basis).

- If a client-affiliate owned more than 10% of the company’s shares, the client, client’s estate and family member devisees (e.g., children) will be deemed affiliates upon receiving the shares. - “Holding period” requirement (Rule 144(d)). Estate and child-

beneficiary may tack onto the client’s holding period.- “Amount sold” requirement (Rule 144(e)). Estate and child must

aggregate shares made within three months of client acquiring shares.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners82

II.D. Testamentary Transfers (cont.)• Affiliate Status and Rule 144 (cont.)

- If a client (affiliate or not) acquired shares in a private placement transaction less than one year prior to death, the shares will be treated as restricted when held by the estate and devisees.

- Safe harbor (Rule 144(d)(3)(vii)—estates and beneficiaries that are not themselves affiliates are exempt from Rule 144.- NB: This safe harbor does not apply to trusts (Rule 144(d)(3)(vi)). - Reason not to fund revocable trust—let shares pass through estate.

- If an Executor is an affiliate but the estate is not, the Executor’s personal shares will be aggregated with the estate’s.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners83

II.D. Testamentary Transfers (cont.)• Section 16

- Transfers by will are exempt from Section 16 requirements.

• Rule 10b-5- A child-devisee should not be subject to Rule 10b-5 insider trading rules

unless he or she acquired material nonpublic information.

• Accredited Investor/Qualified Purchaser- Continuing testamentary trusts inherit the decedent’s qualified purchaser

status, but not accredited investor status. - Consider naming fiduciaries who meet one of these definitions to

preserve qualification.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners84

II.D. Testamentary Transfers (cont.)• Issues Relating to Executors and Trustees—Affiliate Status

- General Rule 1: Even where a company affiliate acts as Executor or as a testamentary Trustee, the estate/trust is not necessarily an affiliate of the company (on that basis alone).

- General Rule 2: If an affiliate is both a beneficiary and an Executor/Trustee, the estate/trust is an affiliate subject to Rule 144.

- Affiliate Executor/Trustee must aggregate personal sales with the estate’s/trust’s sales. Executor/Trustee’s personal volume of sales (but not the estate’s/trust’s) is limited under Rule 144(e).

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners85

II.E. Transfers of Interests in LPs and LLCs• Example:

- Client is a principal in a private equity fund holding a GP interest, an LP interest, and a carried interest.

- Client wants to transfer a “vertical slice” of his interests in the fund to an LLC, and transfer his LLC interest to a trust for his children.

- The transferee trust provides that the client can substitute trust assets for property of equal value (grantor trust).

- During the client’s life, the trustee can distribute income and principal to the client’s children for any reason, and at the client’s death, the trust will split into continuing trusts for children.

- The holding LLC agreement provides that the client’s brother is the distribution manager, while the client is the investment manager of the LLC (effectively controlling trust investments).- What registration and other requirements will apply under the Securities Act?- What provisions of the Exchange Act apply (e.g., Section 16 reporting requirements)?

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners86

II.E. Transfers of Interests in LPs and LLCs (cont.) • Securities Law Implications Generally

- An LP interest (in a limited partnership) is considered a security because a LP cannot participate in management.

- A GP interest is generally not considered a security under the Howey test, because GPs have active management roles.

- Where a GP acts more like an LP in practice, his or her GP interest may be deemed a security.

- Nevertheless, transfers of LP and LLC interests are typically exempt from reporting requirements under Section 4(a)(2) of the Securities Act because they are usually nonpublic.

- Section 16 implications: None (shares of public company held by a fund remain held by the fund, even if interests in the fund are gifted to a trust)

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners87

II.E. Transfers of Interests in LPs and LLCs (cont.) • Securities Law Implications Generally (cont.)

- In our example, the structure described likely does not trigger any registration requirements under Section 4(a)(2) of the Securities Act because all of the interests are nonpublic.

- Our example also fails to trigger Section 16 of the Exchange Act. Even if the fund owns shares of a public company where the client is an insider (often the case for hedge funds in particular), Section 16 does not apply because, at all times, all shares of public companies have remained held by the fund, so no sales or transactions occur for Section 16 purposes.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners88

II.F. Transfers to Charitable Entities• Private Foundations: Example:

- Client is an insider of a publicly traded company, but does not own more than 10% of the company’s outstanding shares.

- The client creates a private foundation under a trust agreement.- All the client’s stock in the company has the same share value. However, the

client owns some long-held low basis stock in the company (5 years), as well as recently-acquired high basis stock in the company (acquired a month ago, built-in loss).

- Market quotations for the company’s stock are readily available on an established securities market.- How can the client make a donation to the foundation while achieving the maximum

possible income tax deduction?

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners89

II.F. Transfers to Charitable Entities• Transfers to Private Foundations: Deductibility

- In order for clients to achieve the desired charitable deduction at full market value (subject to taxpayer’s other deduction limits), a client’s donations must qualify as “qualified appreciated stock” (IRC § 170(e)(5)).

- Donations not of qualified appreciated stock are only deductible up to the client’s basis.

- Qualified appreciated stock:- Market quotations readily available on established securities market (stock will

not qualify if considered restricted for securities law purposes).- Stock must produce long term capital gain- All contributions of stock by donor and related parties total less than 10% of

company’s outstanding stock.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners90

II.F. Transfers to Charitable Entities• Transfers to Private Foundations (cont.)

- Qualified appreciated stock:- Stock must produce long term capital gain.- All contributions of stock by donor and related parties total less than 10% of company’s

outstanding stock.- Market quotations are readily available on established securities market (stock will not

qualify if considered restricted for securities law purposes).- Our client must take care that the shares she donates to his private foundation will not

be considered restricted for Rule 144 purposes.- The IRS has held that stock can meet this qualified appreciated stock requirement if it

is subject to Rule 144, the holding period has expired and the donor has agreed to limit his or her sales so as not to restrict the foundation’s sales under Rule 144.

- By contrast, Rule 144 shares for which the holding period has not run do not qualify.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners91

II.F. Transfers to Charitable Entities• Transfers to Private Foundations: Deductibility (cont.)

- Qualified appreciated stock:- In our example, to ensure that the client gets a full fair market deduction upon donating to

his private foundation, the client should donate her long-held low-basis stock. (The client’s recently-acquired stock will not meet the requirement of producing long-term capital gain).

- In addition, the client should enter into an agreement with the foundation to ensure that the stock will continue to satisfy the requirements of qualified appreciated stock.- Client must promise not to dispose of (or cause the disposition of) shares if such disposition would

limit the foundation’s ability to dispose of its shares. - Client must make this promise individually, as a fiduciary of the foundation, as a Trustee of client’s

family trusts and in all other capacities. Client must also promise on her own behalf and on behalf of her spouse, related parties and successors.

- Client must promise to take all reasonable steps, at her own expense, to ensure the transferred shares are freely disposable by the foundation (including by obtaining opinions of counsel to that effect).

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners92

II.F. Transfers to Charitable Entities (cont.)• Transfers to Private Foundations: Other Securities Rules

- A private foundation established by a company affiliate is not necessarily an affiliate of the founder’s company, even if it holds shares of the founder-affiliate’s company.

- An individual director/Trustee of a private foundation need not aggregate his or her personal sales with those of the foundation, unless he or she is acting “in concert” with the foundation in selling the securities (SEC Release No. 33-6099).

- (These rules apply to private foundations created under trust agreements and under corporate law.)

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners93

II.F. Transfers to Charitable Entities (cont.)• Charitable Trusts

- Split-interest trusts in which the current interest (e.g., annuity or unitrust interest) and remainder interest are split between a charitable and non-charitable beneficiary. - E.g., charitable remainder annuity trust, charitable remainder unitrust,

charitable lead trust. - Qualified appreciated stock deduction rules do not apply unless one of the

charitable beneficiaries may be a private foundation (public charities have more forgiving deduction rules).

- If acquired in a nonpublic offering, shares will be restricted when transferred to the charitable trust. If client is an “affiliate” under Rule 144, the requirements of that rule apply (e.g., holding period and amount sold requirements, aggregation of client and trust sales). (But consider whether Section 4(a)(1½) or 4(a)(7) applies.)

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners94

II.F. Transfers to Charitable Entities (cont.)• Charitable Trusts (cont.)

- In a charitable remainder trust (non-charitable person is the current beneficiary), if the grantor is the sole Trustee and current beneficiary, Kight should apply: the trust is exempt from Section 16.- However, the trust’s purchases and sales of company stock are reportable by

the client individually.- At the end of the trust term, distributions to charitable remainder beneficiaries

are reportable as gifts by the client-grantor.

- In a charitable lead trust (charity is the current beneficiary), funding of trust is a change in beneficial ownership reportable on Form 4/5.

What You Don't Know Can Hurt You: Securities Law Issues for Estate Planners95

II.G. Conclusion• For clients who are insiders of publicly traded companies and

private equity/hedge funds, estate planning transactions can have consequences beyond the intended tax and estate planning goals.

• Estate planners must have an understanding of securities law to spot potential registration requirements, reporting obligations and transfer restrictions.

• Planners must balance estate planning goals with investment goals and securities consequences.

The information provided in this slide presentation is not intended to be, and shall not be construed to be, either the provision of legaladvice or an offer to provide legal services, nor does it necessarily reflect the opinions of the firm, our lawyers or our clients. No client-lawyer relationship between you and the firm is or may be created by your access to or use of this presentation or any informationcontained on them. Rather, the content is intended as a general overview of the subject matter covered. Proskauer Rose LLP(Proskauer) is not obligated to provide updates on the information presented herein. Those viewing this presentation are encouragedto seek direct counsel on legal questions. © Proskauer Rose LLP. All Rights Reserved.