Embed Size (px)

Citation preview

What’s Next: Trade, North America and the World

Presentation by Joel Kotkin, Chapman University, to TMC Conference Long

Beach, CA March 4th, 2014

Long Term Fundamentals

• Regional diversity is key to US future

• U.S. only advanced country with large, growing population

• Huge resource base

• Economic system most resilient among advanced countries

• Dispersion of trade and growth of Third Coast

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

400,000,000

1960 1970 1980 1990 2000 2010 2030 2050

More Crowding to Come: US Population Growth 1960-2050

Source: Bureau of the Census, CensusScope

Labor Force Growth

U.S. Census Bureau, International Database

United States, 37%

Korea, -30%

Europe, -21%

China, -10%

Japan, -39%

-45%

-35%

-25%

-15%

-5%

5%

15%

25%

35%

45%

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Growth in Age 15-64

0.12

0.26

0.36

0.09

0.19

0.45

0.53

0.82

0.37 0.34

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

China Europe Japan Singapore United States

65

& O

ver

Pe

rso

ns

pe

r U

nd

er

15

2010

2050

Ratio of Elderly to Working Age Population 65 & OVER PERSONS PER 15-64 YEARS

Calculated from

UN Population Prospects:

2010 Revision

$0

$3

$6

$9

$12

$15

$18

1995 2000 2005 2010

Trill

ion

s

United StatesChinaIndiaJapanGermany

5 Largest World Economies GDP-PPP: 1994-2012

Source of Data:

World Bank

In a post-industrial age, stuff still matters…

America’s Opportunity

Food and Agriculture Organization of the United Nations

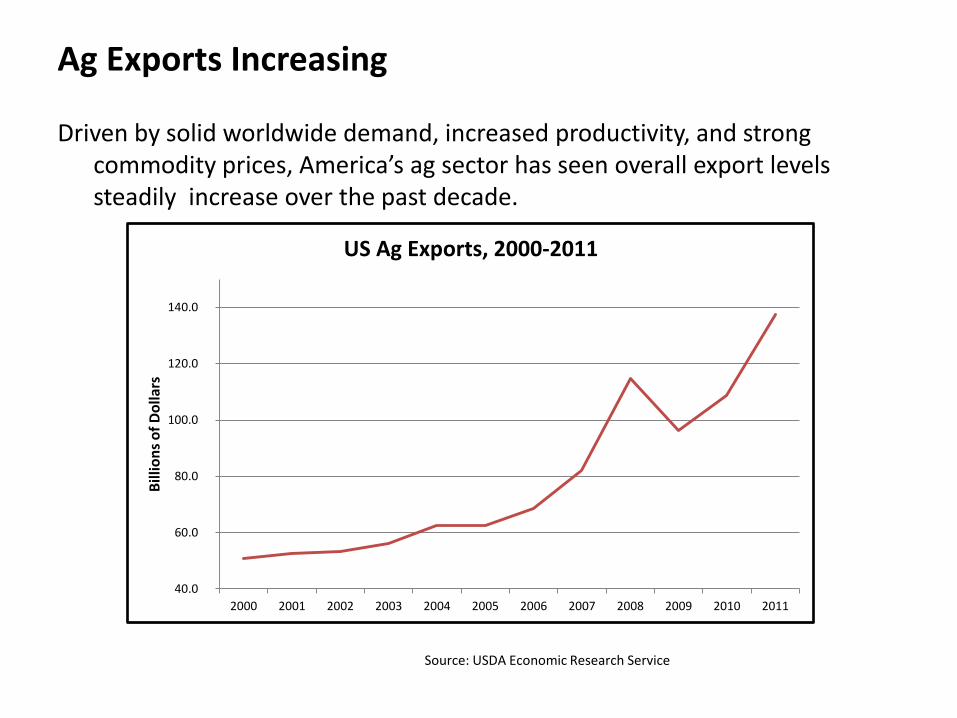

Ag Exports Increasing

Driven by solid worldwide demand, increased productivity, and strong commodity prices, America’s ag sector has seen overall export levels steadily increase over the past decade.

40.0

60.0

80.0

100.0

120.0

140.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Bill

ion

s o

f D

olla

rs

US Ag Exports, 2000-2011

Source: USDA Economic Research Service

Shale Plays in the World

Leading in Gas Production

611

589

182

152

139

117

106

97

85

85

84

83

United States

Russia

European Union

Canada

Iran

Qatar

Norway

China

Netherlands

Algeria

Saudi Arabia

Indonesia

Natural Gas Production, Billions of Cu M

CIA World Factbook

0 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 180,000 200,000

Texas

Oklahoma

Colorado

California

Louisiana

Pennsylvania

Kansas

Florida

New Mexico

North Dakota

Ohio

Wyoming

Arkansas

West Virginia

Illinois

Michigan

Mississippi

Alaska

Utah

Oil and Gas Extraction Job Growth, 2001-2011

Source: EMSI Complete Employment, 2011.4

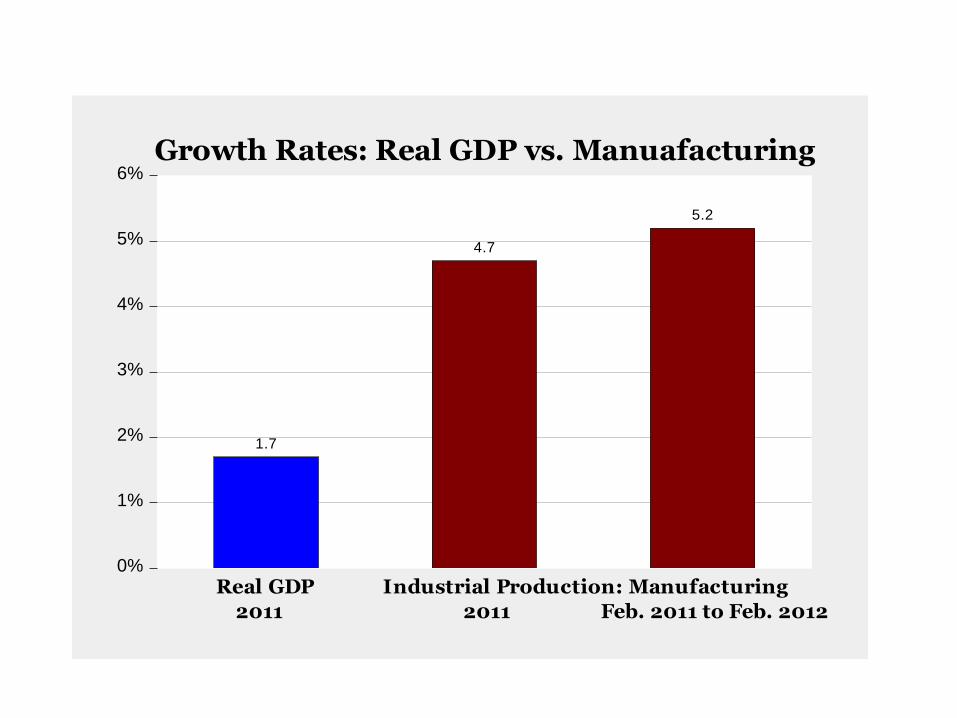

U.S. Share of Global Manufacturing Holds Steady

0%

1%

2%

3%

4%

5%

6%

1.7

4.7

5.2

Real GDP Industrial Production: Manufacturing

2011 2011 Feb. 2011 to Feb. 2012

Growth Rates: Real GDP vs. Manuafacturing

Top States for New Plants, 2010

11.5% 11.1% 10.9%

8.4%

9.4%

Third Coast TTU PlainsCounties

SoutheastManufacturing

Belt

IntermountainWest

Nation

Heavy Metal Manufacturing Job Growth 2010-2012

2013-2023 JOB GROWTH % CHANGE Research by EMSI, Inc.

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2013-2023 %change

2003-2013 %change

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

2003 2004 2005 2006 2007 2008 2009 2010 2011

Indexed Growth in Exports, 2003=1.0

Gulf Coast Ports

All Other US Ports

Source: U.S. Census Bureau: Foreign Trade Division. Total Value, All Commodities

CAFTA (Central Am.), 4.1

South America, 18.2

Africa, 6.2

European Union, 14

NAFTA (North Am.), 29.2

Asia, 26.2

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010

Bill

ion

s

Third Coast Exports by Destination

Where did my customers go?

….some moved, and their kids did too. America’s demography is changing in

ways that effect your business.

Gaining States

Losing States

Cities of Aspiration, Demographic Trends: DOMESTIC MIGRATION

2007-2012 (Excluding 2010) Divided by 2007 Population (Census Bureau)

-5.00%

-3.00%

-1.00%

1.00%

3.00%

5.00%

7.00%

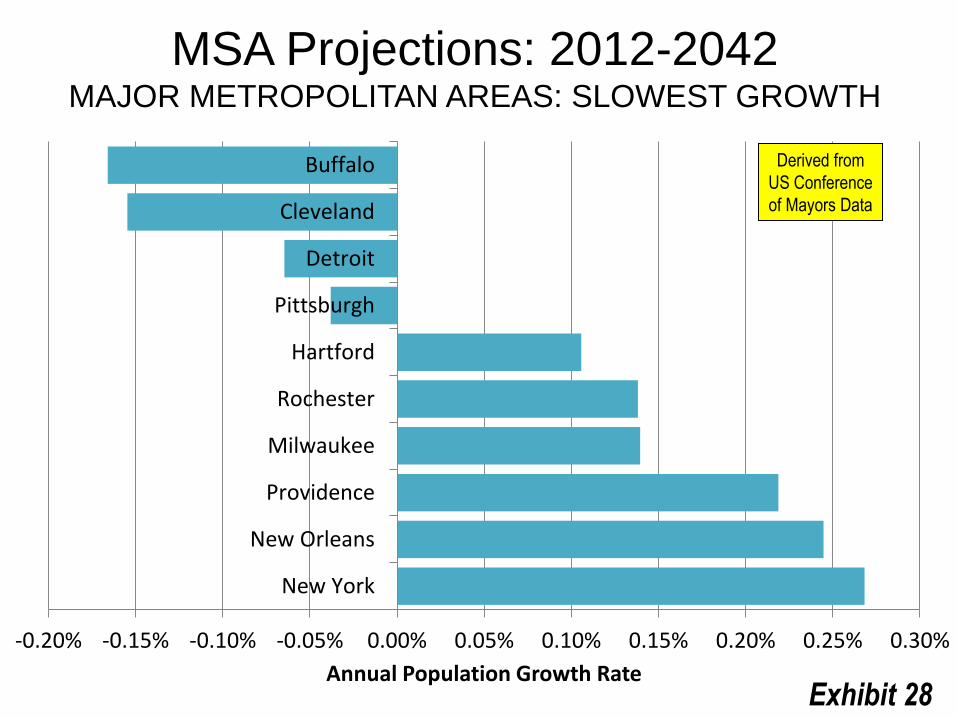

-0.20% -0.15% -0.10% -0.05% 0.00% 0.05% 0.10% 0.15% 0.20% 0.25% 0.30%

New York

New Orleans

Providence

Milwaukee

Rochester

Hartford

Pittsburgh

Detroit

Cleveland

Buffalo

Annual Population Growth Rate

MSA Projections: 2012-2042 MAJOR METROPOLITAN AREAS: SLOWEST GROWTH

Derived from

US Conference

of Mayors Data

Exhibit 28

0.00% 0.50% 1.00% 1.50% 2.00% 2.50%

Cape Coral

Provo

McAllen

Austin

Phoenix

Raleigh

Riverside-San Bernardino

Orlando

Boise

Atlanta

Annual Population Growth Rate

MSA Population Projection: 2012-2042 MAJOR METROPOLITAN AREAS: FASTEST GROWTH

NATIONAL AVERAGE Derived from

US Conference

of Mayors Data

Exhibit 29

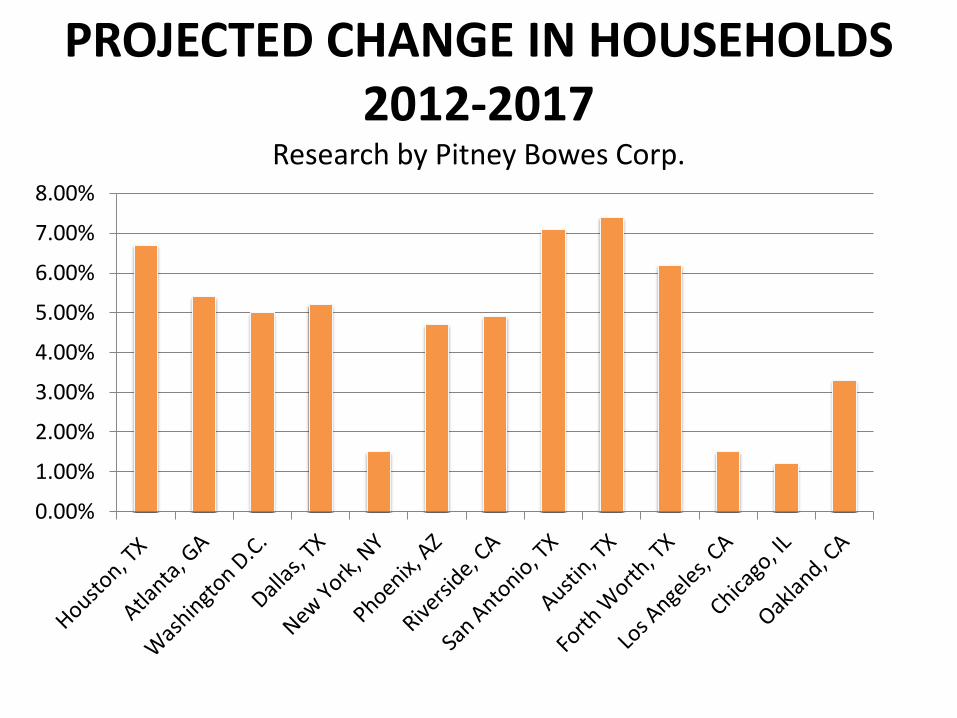

PROJECTED CHANGE IN HOUSEHOLDS 2012-2017

Research by Pitney Bowes Corp.

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Cities of Aspiration, Demographic Trends: CHANGES IN FOREIGN BORN POPULATION

2007-2011 Percentage Change: (ACS)

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

Looking Ahead: America and the World in the next

decade

• Growth and markets will shift to opportunity regions • New global centers emerging • Basic Industries key drivers

JOELKOTKIN.COM A vivid snapshot of America in 2050 focusing on the evolution of the more intimate units of American society—families, towns, neighborhoods, industries. It is upon the success or failure of these communities that the American future rests.

Questions and Comment

![Joel Kotkin PPT [Read-Only] - c.ymcdn.com · (PPIC) • 70% of downshifting boomers “retiring in place ... Microsoft PowerPoint - Joel Kotkin PPT [Read-Only]](https://img.pdfslide.net/doc/110x75/5c90882709d3f242278b78ff/joel-kotkin-ppt-read-only-cymcdncom-ppic-70-of-downshifting-boomers.jpg)