Embed Size (px)

Citation preview

Accessing Federal Stimulus Funds (Non-Profits)

What’s Available & How To ApplyApril 2, 2020

Prepared & Presented By: Inner City Law Center

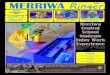

Process Flow & Timeline

Application Approval Loan OriginationSpending Window

Request for Forgiveness

Repayment Begins

Application Loan Origination

Approval at Bank takes

~2-3 weeks, with an

additional one (1) week

at SBA

Accepted 4/3/2020

through 6/30/2020

Date money is received!

1 3

1 2 3 4 5 6

Approval2

Spending Window Repayment Begins

ASAP once 8-week

Spending Window is

complete

Open Window; however for

forgiveness consideration, funds

must be spent within 8 weeks

from Loan Origination

6 months after

origination date or 12

months with extension

4 6Request for Forgiveness5

2

Coronavirus Aid, Relief, & Economic Security Act

• Passed by Congress on March 27, 2020

• Administered by the Treasury Department

• Allocates Funds to Non-Profit Organizations

• Non-Profit Organizations = an organization defined in section 501(c)(3) of

the Internal Revenue Code and exempt from taxation under section 501(a)

of the IRS code

• Primary Loan Program = Paycheck Protection Program [PPP]

• Statutory Bars to Receiving Funds:

• Current bankruptcy proceedings

• Delinquent or defaulted SBA loans within the past 7 years

CARES Act

3

Paycheck Protection Program: Overview

• Emergency Small Business Loans (SBA 7(a) loans)

• Aggregate loan amount is capped at $10 million

• Maximum interest rate of 4%

• Treasury Guidance – 0.5%

• Available through June 30, 2020

• No personal guarantee or collateral is required

• Total SBA 7(a) loan amount cannot exceed the amount of pre-existing SBA

loans being refinanced under the program

• Loan cannot exceed 2.5 times the average monthly payroll cost during the

year prior to the loan

PPP

4

Paycheck Protection Program: Calculation

• List of all employees in 2019 with all compensation

• Possible Sources

• ADP has report

• Same data as provided for 401k if prepared

• Box 5 of each employee W-2

• Compensation for each employee is either Box 5 or $100,000, whatever is greater.

• Total it all up and divide by 12

• Multiply by 2.5

• Amount to apply for

How large of a Loan are you eligible for?

5

Paycheck Protection Program: Utilization

• The Loan Can Cover:

• Payroll

• Healthcare Costs

• Mortgage Interest Payments

• Rent

• Utility Payments

• Debt Service

• Interest on any other debt obligations that were incurred before the

covered period

What you can spend the Loan on…

6

Alternative: Employee Retention Payroll Tax Credit

• Available to organizations that do not receive PPP funds

• If you receive PPP funds, you are ineligible for the ERPTC

• Operations must be fully or partially suspended due to COVID-19 related shutdown orders

• Gross receipts must have declined more than 50% compared to the same quarter in the prior

year

• Refundable payroll tax credit equal to 50% of “qualified wages”

• For eligible employers with more than 100 employees, those are wages paid to an employee

even though the employee is unable to work due to a governmental “stay at home” order

• For eligible employers with 100 or fewer employees, “qualified wages” include all wages paid

whether the employer is open for business or subject to a shutdown order

• Qualified wages includes health plan expenses

ERPTC

7

Paycheck Protection Program: Forgiveness

• Subject to the direct lender’s approval

• The amount forgiven is lowered by reductions in full-time employment and

where total salaries and wages fall by more than 25% from the applicable prior

period

• This can be mitigated by rehiring employees

• Forgiveness Application must identify financial information including:

• Aggregate amount of payroll payments

• Interest payments on mortgage obligations

• Rent payments and utility payments made during the eight-week period following loan

origination (expected to be limited to 25% of forgiveness amount)

8

Process & Parameters for Forgiveness

Paycheck Protection Program: Covered Costs?

• Will Cover:

• Salary, wage, commission, or similar compensation; payments of cash, tip or

equivalent; payment of vacation, parental, family medical or sick leave; allowance

for dismissal or separation

• Will Not Cover:

• Compensation of an employee in excess of $100,000/year ($8,333/month;

$1,923/week) prorated for February 15, 2020 through June 30, 2020

• Federal income taxes

• Compensation for employees who principally reside outside the US

• Qualified sick and family leave wages for which a borrower receives a credit under

7001 and 7003 of the Families First Coronavirus Response Act (FFCRA)

Payroll Costs

9

Paycheck Protection Program: Covered Costs?

Healthcare & Retirement Benefits• Will Cover:

• Group Healthcare Benefits, including insurance premiums

• Payroll Taxes

• Retirement Benefits:

• 401K or 403B

• Payments to independent contractors that are not greater than $100,000 in 1

year, as prorated for the covered period

• Will Not Cover:

• Shall not include compensation of an individual employee in excess of annual salary of

$100,000 as prorated for the covered period. (Pages 10 through 13 of CARES Act)

10

Paycheck Protection Program: Application

Administered though existing SBA approved lenders

Treasury Department has indicated that they will work to certify new

lenders

Must certify that current economic uncertainty makes the loan request

necessary

Documentation in addition to application – depends on bank. Expect to

include:

Organization Documents – Articles of Incorporation, By-Laws, Board

Roster, Tax-Exempt Letter

Board Authorization – Reach out to ICLC for Sample

PPP

11

Paycheck Protection Program: Spending Timeline?

• NO…The remaining funds do not need to be fully spent before the 8

week period.

• Remaining balances are guaranteed by the SBA and have a maximum

maturity of 10 years from the date on which the borrower applies for

loan forgiveness under Sec. 1106

• Borrowers must “make a good faith certification”, that they will

“acknowledge that funds will be used to retain workers and maintain

payroll or make mortgage payments, lease payments, and utility

payments…” CARES Act

Must all the Funds Be Spent before the 8 Week “Covered Period”

12

Paycheck Protection Program: Next Steps

• Assess financial need/risk

• Apply as soon as possible

• We are here to assist with applications

• Wait for funds to be dispersed

• Apply funds to proper use

• Request forgiveness, as applicable

PPP

13

Questions & Answers14

Follow-Up: Points of Contact

• For any additional questions or assistance:

• Adam Murray, Executive Director; [email protected]

• Jennifer Hirsch, Director of Finance; [email protected]

• Charles Kohorst, Staff Attorney; [email protected]

• Hector Pena, Senior Paralegal; [email protected]

15