Embed Size (px)

Citation preview

W H I T E P AP E R

C o m p e t i t i v e n e s s As s e s s m e n t o f t h e M o l d o v a n I T M a r k e t , 2 0 1 1

Sponsored by: USAID

Madalin Lazarescu Dana Samson

November 2011

I D C O P I N I O N

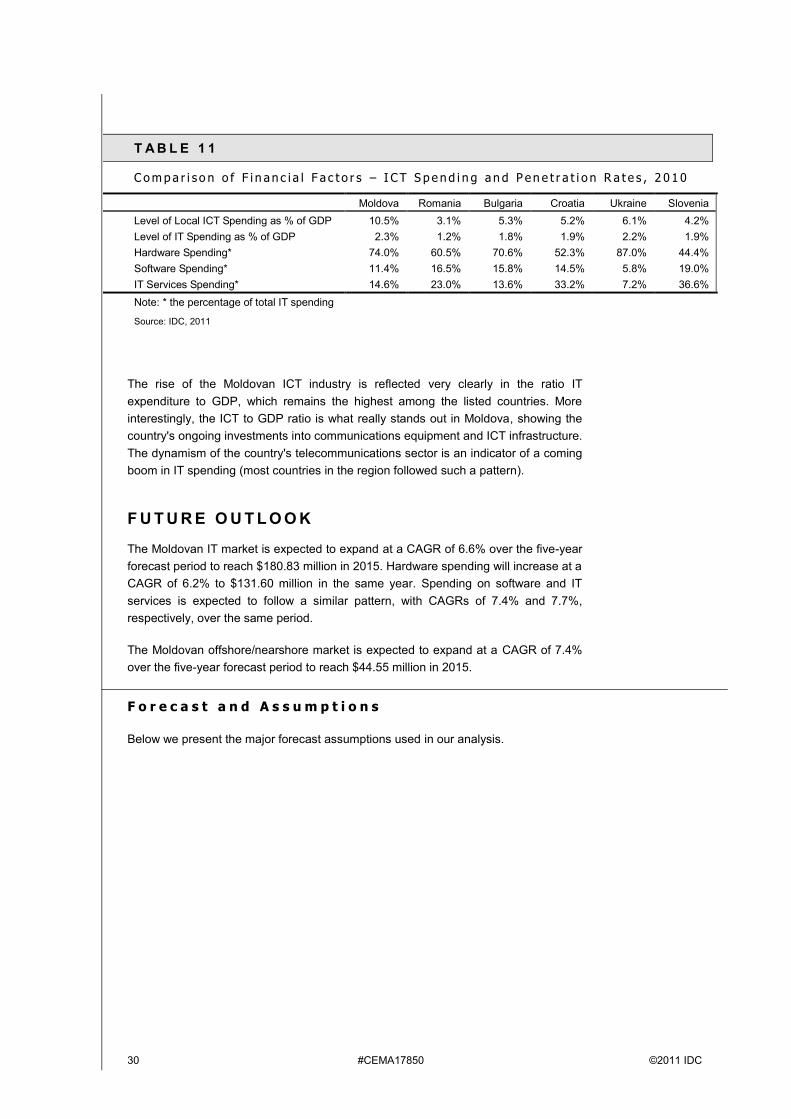

In 2010, the domestic IT market in Moldova expanded 2.4% year on year and

reached a total value of $131.44 million. The IT market has quickly recovered from

the effects of the global crisis and returned to growth after the steep decline of 13.3%

suffered in 2009.

The Moldovan IT market remains hardware-centric, with most spending derived

from hardware acquisitions, hardware-related services, and software associated

with the purchase of new hardware (e.g., system software).

The main reasons behind market growth in 2010 are year-on-year gross

domestic product (GDP) expansion of 6.9% (one of the highest growth rates

among Central and Eastern European, or CEE, countries), a recovery of exports,

growth in private consumption (a 9.0% increase compared with 2009), and a slow

but steady return to investment on the part of the government.

Current government purchasing programs remain quite constrained, but public

spending continues to be sustained by ongoing public investment projects. Gross

investments continued to grow, recording an impressive 17.2% year-on-year

expansion rate in 2010, while foreign direct investment (FDI) was up 55.6% to

$198.9 million for the year. However, FDI is still a long way behind the levels

reached in 2008, when FDI was four times greater. As real wages began to rise

and the availability of credit increased, consumer spending returned to growth in

2010, which had a positive effect on the low end of the hardware market

(notebooks, inkjet printers, handheld devices, etc.)

Other factors will continue to hinder the development of the IT market, such as

political uncertainty, high food and energy costs, high inflation, lack of IT

education and so forth. For example, in most CEE countries, IT spending grows

at a faster pace than GDP, which was not the case in Moldova in 2010 (6.9%

GDP growth versus a 2.4% increase in IT spending), which indicates that IT

investments deserve greater attention from the business community and political

decision makers in order for organizations and government bodies to exploit IT's

full potential as an effective driver of the country's economy as a whole.

In terms of offshore/nearshore activities, in the eight years prior to 2010, Moldova

became one of the preferred sourcing locations across Southeastern Europe

(SEE). This was heavily reflected in the volume of exports of services, which

grew tenfold within this period. Moldova is expected to remain one of the favorite

offshoring locations in the near future due to its advantages in terms of costs,

geographic position, and availability of human resources – all factors that will

continue to give Moldova a strong competitive advantage over its direct

competitors in the region.

Str

. Lt. A

v.

Gheorg

he C

ara

nda n

r. 1

5,

Secto

r 6, B

ucure

sti

#CEMA17850 ©2011 IDC

T A B L E O F C O N T E N T S

P

In This White Paper 1

Methodology ............................................................................................................................................. 1

Situat ion Overview 2

Executive Summary .................................................................................................................................. 2 Drivers and Inhibitors ................................................................................................................................ 3

Drivers ............................................................................................................................................... 3 Inhibitors ............................................................................................................................................ 4

Overview of the Hardware Market ............................................................................................................ 5 Overview of the Software Market .............................................................................................................. 8 Overview of the IT Services Market .......................................................................................................... 9 Analysis of the Offshore Market in Moldova ............................................................................................. 11

Overview and Structure of the Moldavian Offshore Market ............................................................... 11 Analysis of the Main Players and Offshore Destinations ................................................................... 12 Assessment of Key Competitive Factors and Offshore Industry Constraints ..................................... 14

Offshore and Nearshore Competitive Factors ............................................................................ 14 High Broadband Speed ....................................................................................................... 14 Unique Economic and Cultural Advantages ........................................................................ 14 Low Taxation ....................................................................................................................... 14 Compatibility with Western European Office Hours ............................................................. 15 Workforce ............................................................................................................................ 15 Continuous Efforts to Improve the Quality of Tertiary Studies ............................................. 15 Foreign Languages ............................................................................................................. 15 Strong Tradition in Technical Education .............................................................................. 15 Lower Business Costs ......................................................................................................... 16 Expertise in High Value-Added Services ............................................................................. 16

Offshore and Nearshore Industry Constraints ............................................................................ 16 Coverage of Communication Infrastructure ......................................................................... 16 Underdeveloped Management Practices ............................................................................ 16 Insufficient Training ............................................................................................................. 17 Lower IT Education ............................................................................................................. 17 Lower Productivity ............................................................................................................... 17

Government Investment Promotion Strategies ......................................................................................... 18 Current Promotion Strategies ............................................................................................................ 18

Free Economic Zones ................................................................................................................ 18 Industrial Parks ........................................................................................................................... 19 Fiscal Incentives for New Investments in the Economy .............................................................. 20

New Promotional Strategies and Specific Future Initiatives .............................................................. 20 Human Resources and Education Strategies ............................................................................. 20 Knowledge Economy Strategies ................................................................................................. 21

Success Stories ........................................................................................................................................ 23 Allied Testing ..................................................................................................................................... 23

Company Overview .................................................................................................................... 23 Services Portfolio and Strategy .................................................................................................. 23 Focus Markets – Verticals, Geographies, and Marquee Customers .......................................... 23

Endava .............................................................................................................................................. 23 Company Overview .................................................................................................................... 23 Services Portfolio/Strategy ......................................................................................................... 23 Focus Markets – Verticals, Geographies, and Marquee Customers .......................................... 24

Pentalog High Tech ........................................................................................................................... 24

©2011 IDC #CEMA17850

T A B L E O F C O N T E N T S — C o n t i n u e d

P

Company Overview .................................................................................................................... 24 Services Portfolio/Strategy ......................................................................................................... 24 Focus Markets – Verticals, Geographies, and Marquee Customers .......................................... 25

IT Moldovan Market Benchmark Analysis: Moldova and Southeastern Europe ....................................... 25

Future Outlook 30

Forecast and Assumptions ....................................................................................................................... 30 Key Forecast Assumptions for the IT Market ..................................................................................... 31 Key Forecast Assumptions for the Offshore/Nearshore Market......................................................... 34

SWOT Analysis......................................................................................................................................... 36

Essential Guidance 36

Key Recommendations ............................................................................................................................. 36

Learn More 38

Definitions ................................................................................................................................................. 38 Offshore ............................................................................................................................................. 38 Nearshore .......................................................................................................................................... 39 Engineering and R&D Services ......................................................................................................... 39 BPO ................................................................................................................................................... 39 Managed Services ............................................................................................................................. 39 Customization Services ..................................................................................................................... 39

Methodology ............................................................................................................................................. 40 Resource Skill Factors ....................................................................................................................... 40 Economic and Political Factors.......................................................................................................... 40 Infrastructure Factors ........................................................................................................................ 40 Business and Regional Factors ......................................................................................................... 40 Financial Factors ............................................................................................................................... 40 Note ................................................................................................................................................... 41

#CEMA17850 ©2011 IDC

L I S T O F T A B L E S

P

1 Forecast and Analysis of Hardware Spending (US$M) in Moldova, 2010–2015 .......................... 7

2 Forecast and Analysis of Software Spending (US$M) in Moldova, 2010–2015 ........................... 9

3 Forecast and Analysis of IT Services Spending (US$M) in Moldova, 2010–2015 ........................ 11

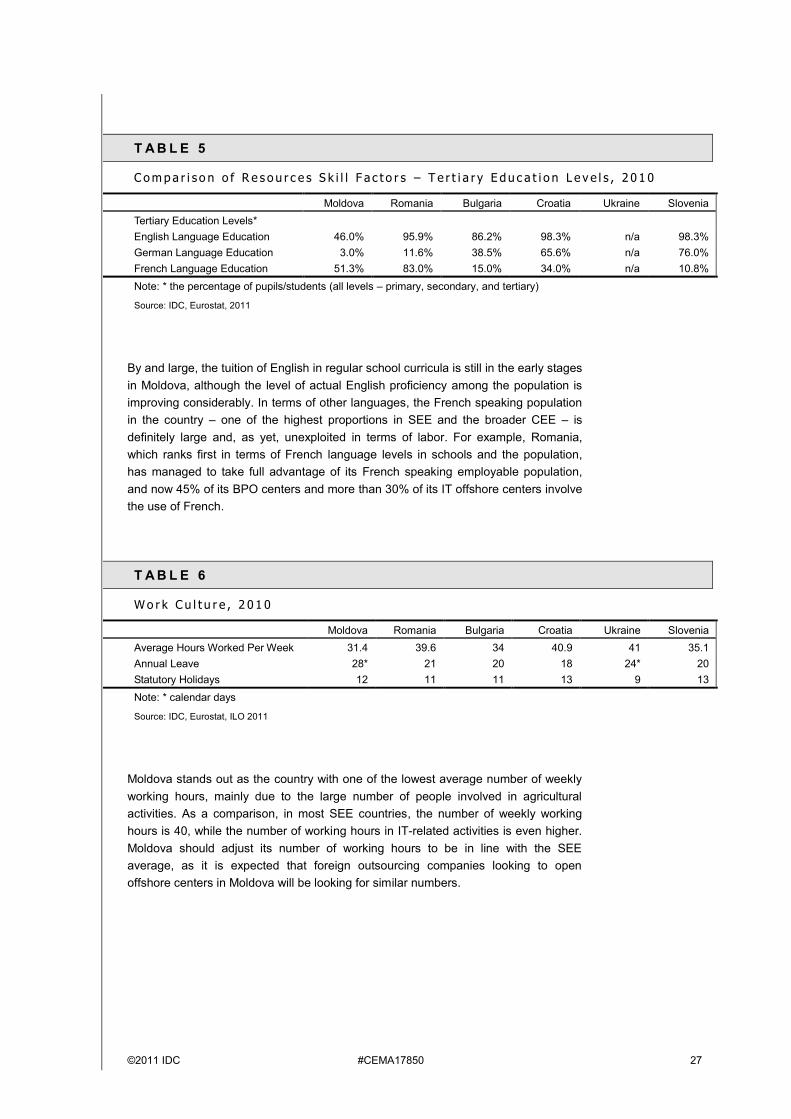

4 Comparison of Resources Skill Factors – Tertiary Education Levels, 2010 ................................. 26

5 Comparison of Resources Skill Factors – Tertiary Education Levels, 2010 ................................. 27

6 Work Culture, 2010 ...................................................................................................................... 27

7 Comparison of Economic and Political Factors – Economy, 2010 ............................................... 28

8 Comparison of Infrastructure Factors – ICT Infrastructure, 2010 ................................................. 28

9 Comparison of Business and Regional Factors – Market Experience, 2010 ................................ 29

10 Comparison of Financial Factors – Tax and Country-Specific Costs, 2010 ................................. 29

11 Comparison of Financial Factors – ICT Spending and Penetration Rates, 2010 ......................... 30

12 Key Forecast Assumptions for the IT Market in Moldova, 2011–2015 ......................................... 31

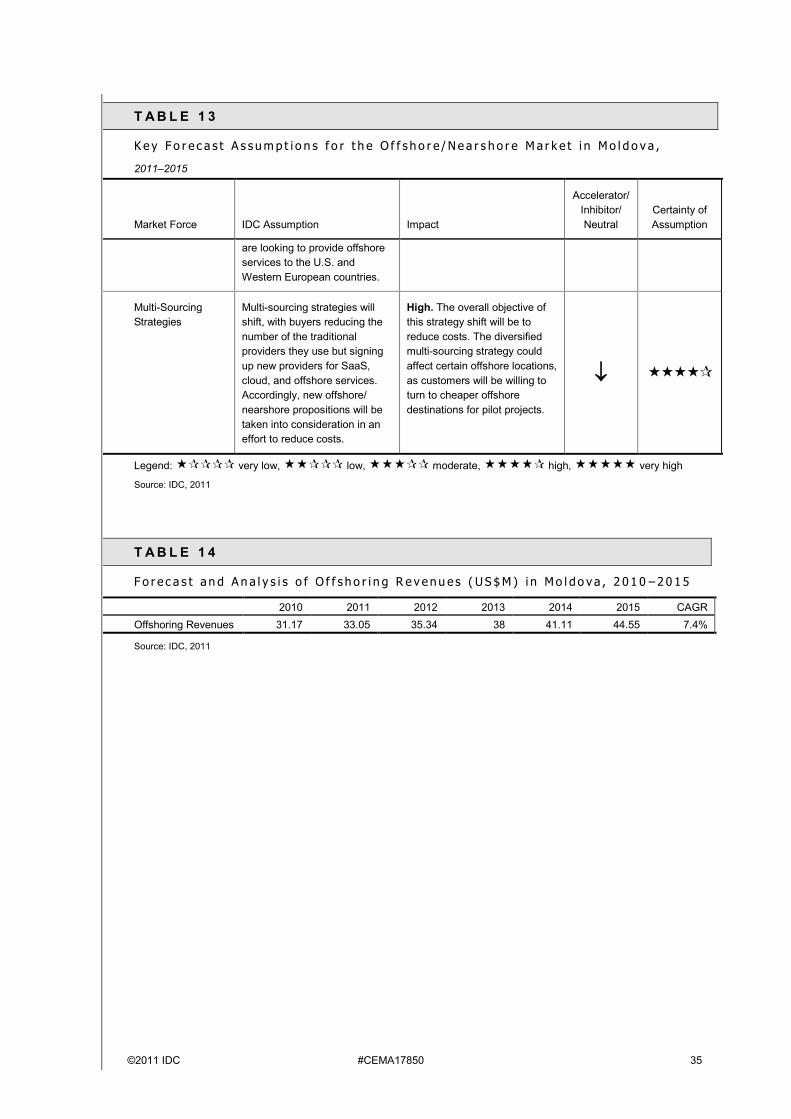

13 Key Forecast Assumptions for the Offshore/Nearshore Market in Moldova, ................................ 34

14 Forecast and Analysis of Offshoring Revenues (US$M) in Moldova, 2010–2015 ........................ 35

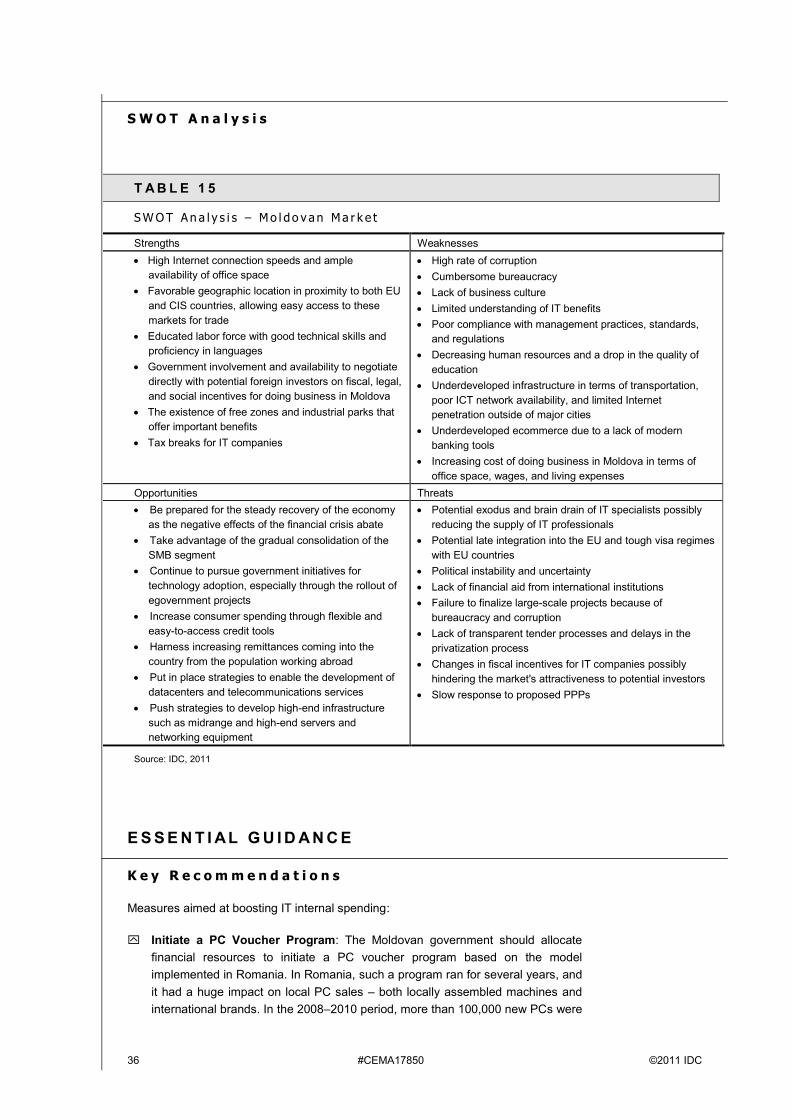

15 SWOT Analysis – Moldovan Market ............................................................................................. 36

©2011 IDC #CEMA17850

L I S T O F F I G U R E S

P

1 IT Spending Share in Moldova, 2010 ........................................................................................... 2

2 Systems Spending Share in Moldova by Form Factor, 2010 ....................................................... 6

©2011 IDC #CEMA17850 1

I N T H I S W H I T E P AP E R

The government of Moldova is developing new strategic initiatives to boost domestic

sales and exports while increasing the attractiveness of the country for investors. The

IT sector is a part of this strategy, and the sector's contribution to Moldovan GDP has

become significant, as is evident from the healthy growth prior to 2009 and the strong

recovery posted in 2010.

This study is part of the USAID-funded Competitiveness Enhancement and Enterprise

Development II (CEED II) project, which aims to enhance Moldovan enterprises'

ability to compete in the global marketplace and to support the expansion of

Moldova's key industries.

The data and results of this study will serve as a tool for understanding the key

constraints that might hinder the competitiveness of the Moldovan IT industry in the

near future, as well as for identifying the necessary corrective steps that would enable

the central authorities to overcome these constraints. Finally, the overall assessment

of the IT Moldovan industry's competitiveness will be used to develop an action plan

to promote the country as a viable IT destination regionally and globally, thus

attracting further investments into the local IT industry.

The findings and results of this study are grouped into two major parts:

The first part of the report focuses on the current Moldovan IT market size and

structure, reflecting internal demand and the development of internal IT spending

over the next five years. This analysis is based on quantitative data related to the

development of the main IT segments; namely hardware, software, and IT

services. This analysis is important, as it provides the framework for the

development of the IT industry over recent years, and it outlines the increasing

importance and contribution of this industry to the country's future economic

development. The analysis will also assess the Moldovan IT market's current

strengths and weaknesses, as well as the future in terms of opportunities and

threats.

The second part of this report focuses on Moldova's ability to further increase its

capabilities for hosting nearshore and offshore operations and the steps and

initiatives that local and central authorities should undertake in order to increase

Moldova's competitiveness and attractiveness for future foreign investments in

the IT sector.

This analysis presents the key competitive factors, positioning, capacity, and

development of Moldova as a hub for nearshore and offshore activities. It also

outlines the major development constraints and the corrective actions that should be

undertaken in order to achieve the milestones of transition. Several critical success

factors will be analyzed, including education levels, language proficiency, resource

availability, work culture, political commitment, administrative burden, intellectual

property, and national infrastructure.

M e t h o d o l o g y

See the Learn More section at the end of this document for information on the

methodology.

2 #CEMA17850 ©2011 IDC

S I T U AT I O N O V E R V I E W

E x e c u t i v e S u m m a r y

In 2010, the information technology market in Moldova reached a value of $131.44

million, up 2.4% from the previous year. The Moldovan IT market is in its infancy and

therefore very hardware-centric, with a relatively small share of software and IT

services spending. Hardware accounted for the majority of expenditure, at

approximately 74%, while software and services together account for only around

26% of total IT spending.

In terms of IT revenue distribution by vertical market, the bulk of investments

continued to be undertaken by large companies from the public sector, finance,

telecom, and utility verticals. However, while investments from small and medium-

sized businesses (SMBs) and sectors such as agriculture, manufacturing, and

business services are only just beginning, it is safe to say that their share of overall IT

spending is likely to increase, as Moldova relies on exports from subsectors such as

food and beverage processing, textiles, and clothing.

The Moldovan IT market hit its spending peak in 2008, when investments into IT

reached $148.22 million. The IT market is not expected to reach that value again until

2012. IT spending in the country declined substantially in 2009, after several years of

consecutive growth, but IDC predicts that, due to economic recovery, overall IT

spending will expand at a compound annual growth rate (CAGR) of 6.6% over the

five-year forecast period to reach approximately $180 million in 2015.

F I G U R E 1

I T S p en d i n g S h a r e ( %) i n M o l d o v a , 2 0 1 0

Source: IDC, 2011

©2011 IDC #CEMA17850 3

D r i v e r s a n d I n h i b i t o r s

Drivers

Rapid Economic Recovery: After a sharp drop of 6.0% in GDP in 2009 caused

by the global economic crisis, Moldova managed to recover quickly and post

6.9% GDP growth in 2010, while further growth of 5.0% is expected for 2011.

The economic recovery will lead to the creation of new businesses and increased

budgets, of which some will be allocated to IT.

Focus on eGovernment: The e-Government Center, founded in the second half

of 2010, aims to ensure the country's sustainable growth, increase transparency,

and improve access for citizens to public information. The first steps involved

launching three portals: the Government to Citizen (G2C) portal, Access to Open

Government Data, and the e-Reporting for Business system. The project's initial

budget of $20 million has already been secured from a World Bank loan. All

these initiatives will increase government spending on IT infrastructure, cloud

computing, and software solutions.

Internet Penetration: One of the most powerful drivers of IT spending within the

home-user and SMB segments is the fast-growing Internet penetration rate.

Double-digit growth was recorded in the number of Moldovan Internet

connections in 2009 and 2010, with increased provider efforts to cover the

market as fast as possible. Given the persistence of difficult living conditions in

rural areas and generally of all the areas outside of major cities, it is likely that

fixed broadband adoption will soon slow unless a program for universal access is

rolled out successfully in the near future.

PC Market Growth: Accounting for roughly 43% of IT spending, PCs are the

main driver of the IT market, automatically generating demand for software and

hardcopy peripherals. At present, PC penetration in Moldova remains relatively

low, even within the Southeastern European region. However, this gap should

narrow in the coming years.

Privatization: The privatization process is far from complete in Moldova, but it

has been set as a priority area in a recent agreement signed with the

International Monetary Fund (IMF). Among the most important state-owned

companies that will be privatized in the near future are Moldtelecom, Air

Moldova, and the Savings Bank. After privatization, businesses tend to invest

significantly into upgrading their internal IT infrastructures.

Remittances Growth: Since a high proportion of Moldova's population (an

estimated 25%) works abroad, either within the European Union (EU) or the

Commonwealth of Independent States (CIS), remittance transfers represent a

very important driver for domestic consumption and economic growth. It is

expected that remittances will continue to fuel IT consumption over the next few

years.

Competition Among Telcos: Competition on the local telecom market is

becoming fierce, as local and international providers are fighting for a relatively

small but underpenetrated market, especially in the area of mobile services. As a

result, investment in network infrastructure can be expected to grow rapidly.

Free Zones and Other Tax Incentives: Although not specifically tailored for the

IT industry, free zones offer fiscal incentives for registered residents, including

4 #CEMA17850 ©2011 IDC

value added tax (VAT) and excise exemptions. Moreover, in an attempt to attract

as many investments as possible, the corporate income tax was as low as 0%

starting in 2008, although it is expected to increase to 12% in 2012. Additional

fiscal facilities were offered to software developers. All of these contribute to

increased budgets for IT and a growing number of greenfield IT-related

investments.

Unique Geographic Position: Moldova has a unique geographic position,

bordered to the east by the EU (Romania) and to the west by the CIS (Ukraine),

having secured free trade with CIS states and being authorized to trade on EU

markets. This advantage is likely to attract new investors, which will increase IT

spending on the local market.

Inhibitors

Budget Deficit: Moldova, according to its agreement with the IMF, has to reduce

its general budget deficit from 5.9% in 2010 to 3.4% in 2011 and to 2.6% in 2012,

which will be quite difficult given the rigidity of social spending. To achieve this

goal, the Moldovan government must introduce public-sector reforms, which are

likely to generate social pressures, as well as cut public spending, which implies

IT spending cuts.

Lack of Market Education: Many SMBs in Moldova are still unaware of, or lack

confidence in, the clear improvements in efficiency that IT can bring. While

vendors are making efforts to educate the market and align their offers to the

needs of SMBs, these organizations are still restricting investments to those with

immediate and tangible returns on investment (ROI), such as machinery,

production facilities, marketing, sales, and fixed assets, without realizing how

these can be complemented by IT solutions.

Lack of IT Specialists on End-User Side: Most human resource challenges for

the Moldovan IT industry reside in a lack of development specialists. Another

hindrance to IT uptake is a shortage of IT consultants on the end-user side. Until

these HR issues are resolved, end-user organizations will have little to rely on in

terms of in-house guidance and expertise, making them less open to sales

pitches from IT vendors.

Software Piracy: The software piracy rate in Moldova was 90% in 2010. The

Business Software Alliance (BSA) declared that, if licensed, the illegal software

currently used in Moldova would bring in another $36 million to the leading

software market players.

Public Contracts Limited by Price Sensitivity and Lack of Transparency: In

the public sector, most contracts are awarded on the basis of price, which

pressures distributors to keep profit margins at a minimum. Furthermore, levels

of transparency and fairness regarding tender proceedings have been

questioned on several occasions. This serves to discourage bidding by qualified

firms, not to mention undermining FDI.

Low Purchasing Power: Moldova has one of the lowest average wage rates in

the region. As price controls are lifted on utilities and basic commodities,

Moldovans, especially those located outside Chisinau, the capital, are seeing

their already limited purchasing power deteriorate. As a result, basic IT

equipment, such as a PC, is beyond the financial reach of the overwhelming

majority of Moldovans. For the same reason, the country has a relatively low

Internet penetration rate.

©2011 IDC #CEMA17850 5

Depletion of HR Pool: In the past few years, the massive exodus of workers to

the EU and CIS has led to shortages in certain labor markets. Demand for IT

professionals is now greater than ever, the consequences of which are marked

salary increases and an inability to satisfy demand. Salary pressure also

markedly reduces profit margins and revenue that would normally be reinvested

into generating organic growth, especially in the case of local companies.

Low Rate of Employable Graduates: In addition to suffering from a depleted

HR pool, most IT companies consider the rate of employable fresh graduates

from IT-related faculties and colleges to be too low and the training period

required for such graduates to be too long (longer than the European average).

As a consequence, investors in the IT field keep their operations in Moldova

small, despite the fiscal incentives offered, or they relocate to neighboring

countries, which are often more expensive but have larger pools of employable

graduates.

O v e r v i e w o f t h e H a r d w a r e M a r k e t

The hardware market in Moldova reached $97.27 million in 2010, up 2.1% compared

with the previous year. The bulk of revenue came from PC shipments, which

accounted for 62.4% of total hardware spending. The second- and third-largest

hardware categories were peripherals and networking equipment, with values of

$17.24 million and $16.56 million, respectively. Spending on storage hardware is still

very low in Moldova, with a value of $2.61 million in 2010 and 2.7% share of total

hardware spending.

The Moldovan PC market is still dominated by local assemblers, which continued to

be responsible for the bulk of PC shipments in the country. However, their share of

total PC shipments declined slowly, from 62.6% in 2009 to 57.0% in 2010. The

dominance of local assemblers is mainly due to the low direct presence of

international vendors, which, in most cases, work exclusively through local partners.

In terms of distribution channels, direct shipments account for 53.5% of total

hardware shipments, with vendor stores representing 40.0% of this channel. Indirect

shipments make up the remaining 46.5%, dominated by traditional dealers, which

claim 29.0% of shipments in this channel. In the absence of substantial corporate and

public-sector projects, the direct channel is expected to continue driving the market in

the coming years. However, retail is also expected to increase its share of overall

hardware shipments once the home-user segment recovers, fuelled by increasing

purchasing power, more accessible consumer credit, and growth in remittances from

the population working abroad.

In terms of form factor, the Moldovan PC market is heavily dominated by desktop

shipments, which accounted for 62.7% of total PC spending in 2010. Local

assemblers benefited from this, as they are able to offer the lowest prices and

customize specific models for the Moldovan small office/home office (SOHO) end-

user segment. Most end-user segments of the Moldovan IT market are hugely

underpenetrated in terms of notebook PCs, and IDC anticipates double-digit growth in

this technology segment in the coming years.

Similar to other emerging countries of Central and Eastern Europe observed years

ago, Moldova recorded the most dynamic growth in the notebook segment in 2010,

with signs of a demand shift toward mobility. However, the notebook segment still

accounted for a small share of total PC shipments (36.0%) last year, up

6 #CEMA17850 ©2011 IDC

approximately 4 percentage points compared with 2009. IDC expects the notebook

segment's share of the overall hardware market to increase steadily in the years to

come.

The x86 server market is very small in Moldova, accounting for less than 1% of

overall PC shipments. In the absence of a strong corporate sector and with

investments from public sector bodies still low, this category is expected to remain

small over the next few years.

F I G U R E 2

S y s t em s S p e n d i n g S h a r e ( % ) i n M o l d o v a b y F o r m F a c t o r , 2 0 1 0

Source: IDC, 2011

Several factors will continue to hinder the development of the systems market in

Moldova in the coming years, including the following:

The online sales model for PCs is still in its infancy in the country for numerous

reasons. First, a lack of credit cards and low PC penetration mean consumers

and small businesses are prevented from making online transactions, and

therefore the online channel for PC acquisitions is underdeveloped. Second, the

market is still in an early stage of development, with customers preferring to see

and examine such technical and expensive items before purchasing them.

Finally, most vendors do not see the online channel as an essential part of their

sales strategies for reaching end users.

Illegally imported PCs and components sold outside of official channels are still a

major problem for legitimate vendors, which are unable to match the low prices of

such illegal imports (no VAT charges). Improved customs controls on Moldova's

borders, however, might limit these practices. Furthermore, the increasing

popularity of on-credit purchases will eventually make it almost impossible to

conduct business without registering VAT.

©2011 IDC #CEMA17850 7

Moldova is among the most price-sensitive nations in Eastern Europe due to low

average incomes. Consequently, vendors tend to reduce prices and configure

low-end machines for the home and small-business segments. These market

characteristics have created one of the region's lowest average sales prices

(ASP) for PCs.

The prevailing worldwide economic climate is causing businesses to shift their

focus from expansion to conservation. This minimal investment strategy is having

an effect on every facet of operations, and IT is no exception. Organizations are

evaluating ways to reduce IT spending across the board, often by stretching

existing resources. Hardware lifecycles are being extended, and PC upgrades

are viewed as a low priority behind security, storage, networks, and management

software.

Many companies in Moldova regard IT systems as an expense rather than an

investment. The concept of ROI is not well established in the private sphere, and

medium-sized businesses across the country are still using valuable resources to

maintain obsolete systems without realizing the long-term costs.

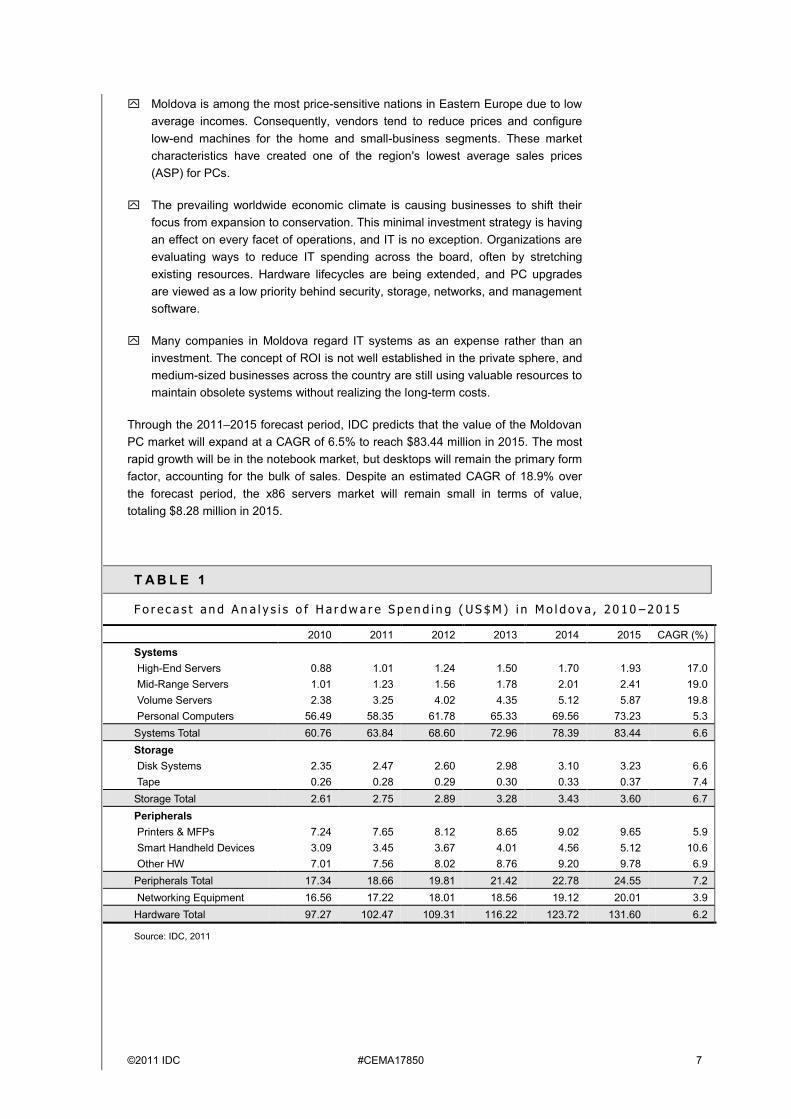

Through the 2011–2015 forecast period, IDC predicts that the value of the Moldovan

PC market will expand at a CAGR of 6.5% to reach $83.44 million in 2015. The most

rapid growth will be in the notebook market, but desktops will remain the primary form

factor, accounting for the bulk of sales. Despite an estimated CAGR of 18.9% over

the forecast period, the x86 servers market will remain small in terms of value,

totaling $8.28 million in 2015.

T A B L E 1

F o r e c a s t a n d A n a l y s i s o f H a r dw a r e S p en d i n g ( US $ M ) i n M o l d o v a , 2 0 1 0 –2 0 1 5

2010 2011 2012 2013 2014 2015 CAGR (%)

Systems

High-End Servers 0.88 1.01 1.24 1.50 1.70 1.93 17.0

Mid-Range Servers 1.01 1.23 1.56 1.78 2.01 2.41 19.0

Volume Servers 2.38 3.25 4.02 4.35 5.12 5.87 19.8

Personal Computers 56.49 58.35 61.78 65.33 69.56 73.23 5.3

Systems Total 60.76 63.84 68.60 72.96 78.39 83.44 6.6

Storage

Disk Systems 2.35 2.47 2.60 2.98 3.10 3.23 6.6

Tape 0.26 0.28 0.29 0.30 0.33 0.37 7.4

Storage Total 2.61 2.75 2.89 3.28 3.43 3.60 6.7

Peripherals

Printers & MFPs 7.24 7.65 8.12 8.65 9.02 9.65 5.9

Smart Handheld Devices 3.09 3.45 3.67 4.01 4.56 5.12 10.6

Other HW 7.01 7.56 8.02 8.76 9.20 9.78 6.9

Peripherals Total 17.34 18.66 19.81 21.42 22.78 24.55 7.2

Networking Equipment 16.56 17.22 18.01 18.56 19.12 20.01 3.9

Hardware Total 97.27 102.47 109.31 116.22 123.72 131.60 6.2

Source: IDC, 2011

8 #CEMA17850 ©2011 IDC

O v e r v i e w o f t h e S o f t w a r e M a r k e t

The software market in Moldova remains underdeveloped, despite having registered

a 3.4% year-on year increase in 2010. Software spending reached $14.93 million for

the year and accounted for only 11.4% of domestic IT spending. As a comparison, in

first-tier CEE countries such the Czech Republic and Hungary, software accounts for

over 20% of the total IT market; in second-tier countries like Poland and Romania,

software represents almost 15% of total domestic spending. In terms of primary

markets, spending on applications is split as follows: 35.2% on system infrastructure

software, 21.8% on application development and deployment, and the remaining

43.0% on applications.

The small size of the domestic market is the result of low demand for software

solutions. A number of factors are responsible for this, including, but not limited to,

low wages, high software piracy rates, limited demand for productivity enhancement

tools, and financial constraints. Because of relatively low domestic demand,

Moldovan IT companies have less incentive to develop packaged software. The

majority of software packages sold on the domestic market are accounting and

financial applications for large enterprises and banks.

The applications market is dominated by basic enterprise software solutions, such as

accounting and financial applications, a clear sign that the enterprise application

software (EAS) market is just emerging. Usually, this is the first step that clients take

in order to streamline one of the most important functions in the organization –

accounting. Very few customers already have an integrated EAS system; those that

have include the recently privatized large telecom operators, utility providers, and

banks. In terms of BI applications, the adoption rate is almost insignificant; the first

such module was only implemented in 2010.

However, the situation is likely to change soon, as the Moldovan government has

emphasized that privatization will be one of its main short-term priorities, which will

provide a significant boost to integrated EAS solutions. The main players in the

applications market are Russian software companies that sell versions of their own

EAS, such as 1C. Romanian vendors like Siveco, TotalSoft, and Wizrom have also

made several attempts to penetrate the Moldovan market, but they were not very

successful because the Moldovan accounting system is closely related to Russian

financial reporting. Large international vendors such as SAP, Oracle, and Microsoft

have a very limited presence.

Revenue in the systems infrastructure software space derives mostly from operating

systems (mainly Microsoft) and very basic security software solutions. Large

companies in the finance, oil and gas, and telecom sectors usually have more

complex security solutions in place and at least basic storage software functions,

such as data protection and recovery. Joint efforts by international vendors, the

Moldovan government, and local independent IT associations to reduce piracy will

spur growth in the Moldovan systems infrastructure software market in the near

future, driving it above the average growth of the overall software market.

The penetration rate for database management software, which still represents the

largest part of the application development and deployment primary software market,

is low, partly due to a limited number of large contracts. The negligible installed base

of servers requires very few installations of middleware applications, and the infant

stage of EAS software penetration limits investments into advanced analytics

solutions.

©2011 IDC #CEMA17850 9

Moldova was one of the very few CEE countries to post significant GDP growth in

2010, at 6.9%, with agriculture and industrial production recovering very well after a

contraction in 2009. Unfortunately, the structure of the Moldovan economy, which is

heavily reliant on agriculture and lower-margin manufacturing like food processing

and textiles, and the economic issues faced by the country's main export markets in

the EU and Russia, were major inhibitors to software spending last year.

Most large international software vendors do not have a direct presence in Moldova.

Those that are present, such as Microsoft, focus on reducing the piracy rate rather

than being actively involved in business development. According to BSA, the piracy

rate in Moldova is constantly deceasing, but it was still at a huge 90% in 2010 (down

2 percentage points). Software piracy represents one of the biggest inhibitors to the

expansion of the Moldovan IT market. Vendors such as Oracle are only present

through partners. In most cases, large vendors coordinate their activities in Moldova

either from Romanian or Ukrainian offices, a situation that leads to reduced flexibility

and limited go-to-market strategies customized for the domestic market.

IDC believes the Moldovan packaged software market will expand at a CAGR of 7.4%

though 2015 to reach $21.37 million. Software's share in the total Moldovan IT market

will increase to 11.8%, mainly at the expense of hardware.

T A B L E 2

F o r e c a s t a n d A n a l y s i s o f S o f t w a r e S p en d i n g ( US $ M ) i n M o l d o v a , 2 0 1 0 – 2 0 1 5

Packaged Software 2010 2011 2012 2013 2014 2015 CAGR (%)

System Infrastructure Software 5.25 5.56 6 6.76 7.23 8.03 8.9

Appl. Development and Deployment 3.26 3.5 3.73 4.09 4.56 5.02 9

Applications 6.42 6.44 6.7 7.31 7.56 8.32 5.3

Packaged Software Total 14.93 15.5 16.43 18.16 19.35 21.37 7.4

Source: IDC, 2011

O v e r v i e w o f t h e I T S e r v i c e s M a r k e t

The IT services market in Moldova reached $19.24 million in 2010, up 3.7% on 2009.

The IT services market accounted for 14.6% of total IT spending in 2010. The low

level of IT spending on services is also influenced by the fact that most large state-

owned companies have their own IT subsidiaries, providing a whole range of

additional services – a very common phenomenon in underdeveloped markets.

The dominant IT services category by far is the implementation activity group, which

is no surprise given that Moldova is still a hardware-centric IT market. The second-

largest activity group is that of support services, in direct correlation with the growth of

the hardware installed base. In most cases, the support activity group only consists of

basic services such as post-installment warranty support.

Demand for IT services is at an early stage, mainly because of an underdeveloped

large and very large enterprise segment and a lack of large projects in public

institutions, which account for large proportions of spending on IT services in more

developed countries. The adoption of IT services in all segments of the market is also

hindered by the price sensitivity of most end-user organizations. Frequently, IT

10 #CEMA17850 ©2011 IDC

purchase decisions revolve around the dual tasks of acquiring basic software and

hardware infrastructure along with the needed technical assistance for

implementation. In such cases, services are often viewed as being of secondary

importance to the overall infrastructure that is being acquired.

However, the Moldovan government has some initiatives regarding the IT market,

with an egovernment project being the core of its strategy. The plan is to build up an

integrated eplatform for Moldova based on private cloud. This project will certainly

attract major players in the IT market and might represent a huge opportunity for

attracting further investments if it is well managed. Two of the biggest issues related

to public acquisition processes in Moldova are a lack of transparency and the

government's unjustifiable inclination to favor local state-owned IT providers that

might not have the expertise or the capacity to manage large-scale projects.

The delayed adoption of IT technology could have its advantages, as Moldova could

skip some costly and now unnecessary intermediary stages in technology

deployments and take steps toward newer delivery models such as cloud computing.

However, the issue of Internet availability outside of major cities should be addressed.

Moldova has very fast Internet speeds (among the top 20 in the world), but, outside of

Chisinau, Internet availability is quite scarce. Improving this situation will involve

massive investment into networking and communications equipment.

Lately, concerns about meeting inflation-rate targets imposed by the IMF (0.8% in

2011) were raised; measures for keeping prices in certain product categories under

control may not turn out to be as successful as planned. In addition, the deficit target

for 2012 may not be met, leading to delays in implementing some scheduled public

infrastructure projects. This will make it more difficult to divert money from

expenditure savings to infrastructure improvements, endangering any projects

dependent on domestic budgets.

Given the small size of the Moldovan IT services market, it is more likely that only

local vendors will be active and directly involved in the market; the activities of large

regional and global players will generally be limited to working with channel partners,

systems integrators, and solutions partners, which have greater flexibility and can

adapt better to the specific realities and requirements of the local market. As a

general trend, very large vendors such as IBM, Oracle, and HP usually try to win new

markets through global strategies, products, solutions, and offerings, an approach

that is usually successful on large underdeveloped domestic markets but less so on

small ones such as Moldova.

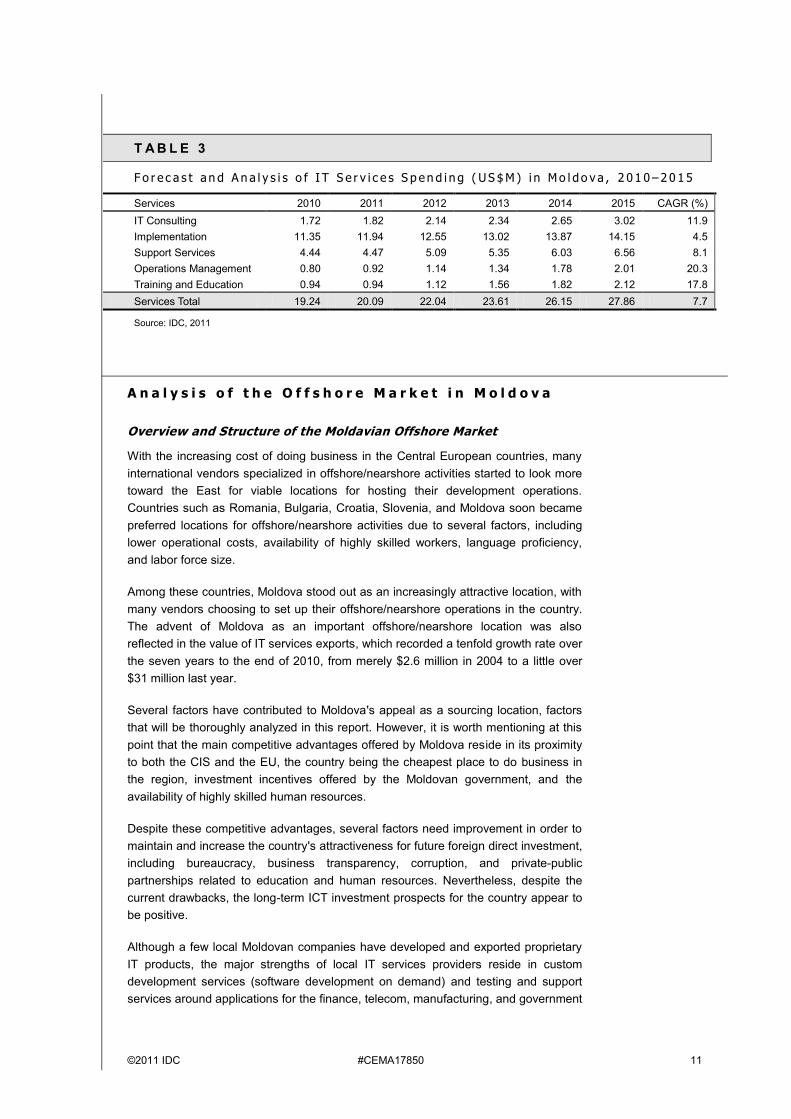

IDC believes that the Moldovan IT services market will expand at a CAGR of 7.7%

over the forecast period to reach 27.86 million in 2015 and account for 15.4% of total

IT spending. The operations management activity group will be the most dynamic,

driven by the expansion of the outsourcing market. Revenue from training activities

will also grow at a fast rate, as new investments will create the need to educate

customers on the use and utility of newly implemented solutions. This will lead to

increased awareness of the advantages of enhanced solutions and technologies,

which, in turn, will drive other areas of the IT services market.

©2011 IDC #CEMA17850 11

T A B L E 3

F o r e c a s t a n d A n a l y s i s o f I T S e r v i c e s S p en d i n g ( US $ M ) i n M o l d o v a , 2 0 1 0 – 2 0 1 5

Services 2010 2011 2012 2013 2014 2015 CAGR (%)

IT Consulting 1.72 1.82 2.14 2.34 2.65 3.02 11.9

Implementation 11.35 11.94 12.55 13.02 13.87 14.15 4.5

Support Services 4.44 4.47 5.09 5.35 6.03 6.56 8.1

Operations Management 0.80 0.92 1.14 1.34 1.78 2.01 20.3

Training and Education 0.94 0.94 1.12 1.56 1.82 2.12 17.8

Services Total 19.24 20.09 22.04 23.61 26.15 27.86 7.7

Source: IDC, 2011

A n a l y s i s o f t h e O f f s h o r e M a r k e t i n M o l d o v a

Overview and Structure of the Moldavian Offshore Market

With the increasing cost of doing business in the Central European countries, many

international vendors specialized in offshore/nearshore activities started to look more

toward the East for viable locations for hosting their development operations.

Countries such as Romania, Bulgaria, Croatia, Slovenia, and Moldova soon became

preferred locations for offshore/nearshore activities due to several factors, including

lower operational costs, availability of highly skilled workers, language proficiency,

and labor force size.

Among these countries, Moldova stood out as an increasingly attractive location, with

many vendors choosing to set up their offshore/nearshore operations in the country.

The advent of Moldova as an important offshore/nearshore location was also

reflected in the value of IT services exports, which recorded a tenfold growth rate over

the seven years to the end of 2010, from merely $2.6 million in 2004 to a little over

$31 million last year.

Several factors have contributed to Moldova's appeal as a sourcing location, factors

that will be thoroughly analyzed in this report. However, it is worth mentioning at this

point that the main competitive advantages offered by Moldova reside in its proximity

to both the CIS and the EU, the country being the cheapest place to do business in

the region, investment incentives offered by the Moldovan government, and the

availability of highly skilled human resources.

Despite these competitive advantages, several factors need improvement in order to

maintain and increase the country's attractiveness for future foreign direct investment,

including bureaucracy, business transparency, corruption, and private-public

partnerships related to education and human resources. Nevertheless, despite the

current drawbacks, the long-term ICT investment prospects for the country appear to

be positive.

Although a few local Moldovan companies have developed and exported proprietary

IT products, the major strengths of local IT services providers reside in custom

development services (software development on demand) and testing and support

services around applications for the finance, telecom, manufacturing, and government

12 #CEMA17850 ©2011 IDC

sectors. Moldovan IT services companies should thus continue to capitalize on their

ability to develop integrated solutions in these areas.

In terms of export revenue structure, the overwhelming majority of IT services

revenue comes from customization services (including custom application

development services and application customization) and support services. These

two categories accounted for over 80% of total IT services exports in 2010. The other

traditional outsourcing services, such as business process outsourcing (BPO),

managed services, and research and development services, are less popular in

Moldova, together accounting for less than 20% of total IT services exports. Since

Moldova is one of the smallest countries in the region and has a limited pool of

human resources, companies involved in offshore/nearshore activities with more

specialized operations tend to set up here, as opposed to those with large-scale

activities, such as BPO services, which require huge pools of human resources.

The second half of 2008, which also marked the beginning of the economic crisis in

the region, including Moldova, did not affect the growth of IT exports in the country.

Moreover, once the crisis has fully receded, countries in southern and eastern

Europe, including Moldova, will still be able to make their cases based on

comparatively low costs, which will continue to be the major consideration for

companies looking to source all or parts of their IT operations.

Local and central authorities should endeavor to increase the market's attractiveness

for offshore/nearshore operations through the following actions (among others):

Creating innovative incentive plans to attract top global players, which will help

keep highly skilled professionals and graduates at home

Continuing to upgrade transport infrastructure and develop ICT networks

Continuing to make the business environment more open and transparent, while

reducing the administrative burden

Keeping current fiscal incentive policies

Maintaining the free trade zones and investing in creating new ICT industrial

parks

Continuing to invest in education and encouraging the public/private partnerships

(PPP) in this area

Analysis of the Main Players and Offshore Destinations

Worldwide offshore IT services appear to be more popular than the classic delivery

model. IDC forecasts that the worldwide offshore IT services market will grow 19.7%

(at constant currency), from $33.9 billion in 2010 to $40.6 billion in 2011, with a five-

year CAGR of 15.3% through 2015, when the total offshore IT services market will

reach $69.2 billion. The Moldovan IT services export market, which reached

approximately $31.17 million in 2010, will expand at a similar rate. This assumption

rests upon on the current development of the Moldovan market. Based on IDC's

experience and benchmarking exercises undertaken with other emerging economies,

IDC believes that the Moldovan market will grow little beyond revenue of $50 million

through the end of 2015. In absolute terms, the market reached approximately $31

million in 2004. Although the total value of the IT market in Moldova over the seven

years up to the end of 2010 increased by an average of $4 million per annum, 2009

©2011 IDC #CEMA17850 13

and 2010 were way below this average due to the difficult global economic conditions.

As a result, IDC's 2011–2015 forecast tends on the side of caution.

The local IT services market was valued at $19.24 million last year, while experts

estimate that exports of services performed by freelancers amounted to an additional

30%.

According to the largest freelance European project hub, oDesk.com, an additional

$15–16 million can be attributed to Moldova's export of services. However, these

revenues are not officially counted or taxed and are received in the form of work

remittances. Although these freelancers' revenues can prove hard to track, register,

and collect taxes on, they show an additional pool of human resources already

existing on the local market that could solve Moldova's short-term qualified personnel

shortage. By comparison, Moldova's freelancers worked approximately 57% of the

total time worked by Romanian freelancers, even though Romania has a significantly

larger human resource pool. This indicates that significant numbers of former

freelance professionals from Romania have already been successfully hunted by

international corporations, a course that is likewise open to representative offices in

Moldova.

The global economic crisis in 2008 and 2009 did not put a stop to Moldova's IT

services export growth. Increasing numbers of U.S. and Western European

companies started to look for cheaper alternatives to their overwhelming personnel

costs. With the crisis curtailing salary inflation in the region, Eastern European

countries became more attractive. Moldova, for instance, has the lowest

compensation plans in the region – lower than in Romania, the Ukraine, or Bulgaria.

Due to the combination of skilled human resources, multilingual proficiency, and

relatively cheap infrastructure, Moldova's offshore/nearshore proposition became

even more valuable than Asian locations. It is no secret that even Indian-based

players use resources based in Eastern Europe to serve their international clients for

reasons of proximity and time-zone compatibility. However, Moldova has several

direct competitors in SEE: Romania, Bulgaria, Serbia, and the Ukraine (tier-one

competitors) and Montenegro, Croatia, Slovenia and the Baltic States (second-tier

competitors).

Regional players such as Endava, Allied Testing, Pentalog, and CEDACRI opened

local offices in Chisinau. Among the smaller players in terms of local business size

(up to 50 employees) are Q Systems, Tacit Knowledge, Computaris, and Amdaris.

Most of the projects are commissioned from the U.K. and the U.S., followed by

France, Germany, and Romania. The services offered are diverse, ranging from

hardware support to telecommunications solutions, EAS, and customer relationship

management (CRM) to portals, ecommerce, and payroll and billing solutions.

While the offshore IT services market will continue to grow at a substantial rate, the

rise of cloud services will challenge the offshore model. All offshore players will need

to make significant adjustments to their businesses to ensure longer-term success in

light of increased cloud services adoption. These include the following:

Pursuing transformational opportunities by helping customers shift to more host-

based models of services delivery (e.g., cloud), including rationalizing and

transforming application portfolios

14 #CEMA17850 ©2011 IDC

Investing heavily in automation across the full lifecycle of services, from

development and testing to operations and delivery of infrastructure and

application services to help drive down costs while meeting faster time-to-market

requirements

Investing more heavily in local (developed) markets to help ensure current and

future growth, with attention to supporting the shift to cloud services in key

industries (e.g., healthcare, energy, and government)

Developing application and infrastructure outsourcing, particularly datacenter

outsourcing – the basis of cloud services

Developing a portfolio of cloud-based services and solutions that aligns with core

competencies such as platform as a service (PaaS) for custom application

development, testing as a service (TaaS) for testing services, infrastructure as a

service (IaaS) for infrastructure outsourcing, and software as a service (SaaS) for

application outsourcing (AO)

Building partnership ecosystems for cloud-based services that include such

partners as cloud-based independent software vendors (ISVs),

telecommunications providers, and management system vendors for provisioning

utility-based operational and business services

Assessment of Key Competitive Factors and Offshore Industry

Constraints

Offshore and Nearshore Competit ive Factors

H i g h B r o a d b a n d S p e e d

Moldova has one of the highest Internet connection speeds in the world, especially in

the capital, Chisinau, where most offshore/nearshore companies are located. This

represents a huge advantage for developers/testers accessing remote applications,

databases, and so forth, as well as an important precondition for future cloud

investments.

U n i q u e E c o n o m i c a n d C u l t u r a l A d v a n t a g e s

Due to its geographic position and its cultural background, Moldova has affinities with

both Western European countries and Russia. Moldova is also the only CIS country

that has preferential economic agreements with the EU, while benefiting from the

advantages of preferential trade agreements within the CIS.

L o w T a x a t i o n

The overall taxation rate is quite low in Moldova: 31.3% forecast by the World Bank

for 2012, while most European countries have percentages of over 40% on profit.

This factor, along with the small number of taxes (only 48), ranks Moldova much

higher than most neighboring countries in the World Bank's Doing Business Report.

Moreover, during recent years, Moldova has continuously simplified the process of

opening a business, with only 10 days required compared with the European and

Central Asia average of 32 days and the worldwide average of 16.6 days. The total

cost of starting a business, at 10.9% of per capita GDP, is considerably lower than

the European and Central Asia average of 14.1%.

©2011 IDC #CEMA17850 15

C o m p a t i b i l i t y w i t h W e s t e r n E u r o p e a n O f f i c e H o u r s

Moldova is only GMT+2, which gives it a significant advantage over Asian countries,

especially for live support services, while costs are similar and European language

skills are better.

W o r k f o r c e

In 2010, approximately 6,000 specialists were employed in the software sector alone,

while the number of total employees in the ICT sector was around 20,000. Some 83%

of these employees are technical specialists, such as software engineers, analysts,

developers, and project managers. Management and business professionals

represent 17% of the total. Foreign companies have chosen Moldova as an offshore

development destination partly because of its inexpensive and efficient labor force.

However, due to a limited supply of qualified specialists and the appreciation of the

local currency, salary costs have increased in recent years. Nevertheless, Moldova is

still considered a low-cost offshore development location, one in which salaries are

lower than those of many European IT outsourcing countries such as Romania

(where the average salary is about $1,100/month in IT) and Bulgaria (with an average

of around $950/month in IT), not to mention more expensive offshoring locations such

as Hungary, Poland, and Russia. It is fair to say, however, that, in some cases,

Moldova's salary levels are comparable to those of neighboring countries, especially

for positions such as project manager and project leader.

Factors hindering the export of IT services include insufficient knowledge of Moldova

and its IT industry among the international business community; language issues,

although the problem is subsiding, as the young generation is becoming more

proficient in English and other European languages; and the country's relative

distance from some of the key Western European IT markets.

C o n t i n u o u s E f f o r t s t o I m p r o v e t h e Q u a l i t y o f T e r t i a r y S t u d i e s

In some cases, local IT professionals help tertiary educational institutions to align

their curricula and study programs to the latest industry trends and requirements.

Today, institutions are coming to recognize that, in addition to technical skills,

students need to be proficient in business areas.

F o r e i g n L a n g u a g e s

Teaching foreign languages such as English, French, and Russian is also considered

extremely important for developing high-quality ICT professionals, particularly those

aspiring to management positions. Despite recent improvements in the educational

system in Moldova, many consider current teaching methods to be inadequate and

thus unable to meet the IT industry's need for high-quality human resources.

S t r o n g T r a d i t i o n i n T e c h n i c a l E d u c a t i o n

Moldova has a strong tradition of higher technical education, with universities placing

great emphasis on training students in the fundamentals and educating them to

understand general engineering principals, reminiscent of the former Soviet system.

Today, this tradition is enhanced with new ideas and approaches resulting from

Moldova's adoption of free market principles. Nonetheless, despite recent

improvements in the educational system in Moldova, many consider current teaching

methods to be inadequate and thus unable to meet the IT industry's need for high-

quality human resources.

16 #CEMA17850 ©2011 IDC

ICT-related education is also becoming increasingly popular, and the number of

students and fresh graduates is increasing (2,233 fresh ICT graduates in 2011, 2,039

in 2010, and 1,642 in 2009). This shows that the ICT sector in Moldova is on a fast

ascent; as a comparison, the numbers of fresh ICT graduates in most other SEE

countries (e.g., Romania, Bulgaria, Slovenia, and Croatia) have declined by 5–10%

since 2008.

L o w e r B u s i n e s s C o s t s

According to Colliers International, rent in Chisinau for prime office space is around

EUR 20 per square meter, which is three or four times less than in Bucharest, for

example. In addition, salaries for all personnel, even for highly qualified senior

professionals, are significantly lower than in all other countries in Central and Eastern

Europe; the average monthly salary in June 2011 was EUR 219. Furthermore, the

government has extended exemptions for personal and security tax for IT specialists

until 2016.

E x p e r t i s e i n H i g h V a l u e - A d d e d S e r v i c e s

Moldovan ICT specialists should continue to capitalize on their proven long-term

experience in high-value-added services such as analysis and design, application

development, and testing services. In terms of applications types, three main areas

should continue to be exploited: business applications (especially financial, office

productivity, and BI applications), Web development applications, and mobile

applications (embedded systems). In terms of software, Moldova boasts long-term

experience in open source and proprietary (distributed client server) operating

systems.

Offshore and Nearshore Industry Constraints

C o v e r a g e o f C o m m u n i c a t i o n I n f r a s t r u c t u r e

Moldova may have managed to solve the issue of Internet speed, especially in large

cities, but the country still needs to address the issue of transport and

telecommunications infrastructure outside of Chisinau, unreliable Internet

connections, and high voice tariffs to North America and EU countries. Steps toward

remedying the last issue are already being taken as a part of tariff harmonization with

the EU.

U n d e r d e v e l o p e d M a n a g e m e n t P r a c t i c e s

Significant differences exist between locally owned companies and branches of

foreign firms in terms of how companies are managed. The majority of local branches

of international firms do not engage in common practices such as business

development, marketing, and strategic management; such activities are handled by

head offices abroad. In addition, foreign companies, when compared with locally

owned firms, employ more advanced project management practices and use better

documented and designed methodologies. The reason is that, in most cases,

processes employed by the parent companies are simply copied to the Moldovan

branches. Commonly accepted management practices employed in free-market

economies have been slow to take hold in the Moldovan business community, the IT

sector in particular, since the collapse of the Soviet economy. As a result, many local

IT companies do not have sufficient experience or knowledge of the best

management practices widely employed by Western companies. The major reasons

are a lack of high-quality managers with appropriate education and background, the

©2011 IDC #CEMA17850 17

early stage of the newly developing market economy, and insufficient experience with

international clients.

However, as companies grow and develop, their management practices are

becoming more sophisticated. Western practices are becoming part of the day-to-day

management of, for example, local software firms. While, for many years, marketing

and project management functions were conducted by a company's director, most

firms now have separate departments dedicated to marketing, HR, operations, and

other areas. Companies now accept a larger number of business graduates than

previously and pay more attention to management training and professional

development.

I n s u f f i c i e n t T r a i n i n g

On average, around 25% of technical and business specialists received training in

2010. Training budgets are still very low, accounting for less than 5% of a company's

total turnover on average. Differences exist between locally owned companies and

foreign subsidiaries in terms of employee development. International firms present in

Moldova ensure constant employee training (i.e., training levels are maintained), both

locally and at head offices, as a part of their strategic management processes. In

addition, they have built resource centers and libraries to assist in training employees

and knowledge management. Employees of certain foreign branches in Moldova are

offered employee stock options and other non-salary incentives. International

branches normally enjoy low staff turnover rates and greater employee commitment.

In contrast, few local companies are able to provide training on a constant basis,

although they do accept training as an important part of development. Staff training is

greatly affected by the availability of funds and qualified trainers. One option for local

firms is that of free/low-cost training offered through government programs, which

tend to focus on general industry needs rather than specific companies' requirements.

Salary levels being lower than those adopted at local branches of international

companies and inadequate employee incentive plans were the major factors behind

the high staff turnover rates at local firms for many years. Recently, however, various

forms of incentive have become more widespread at local companies. During the last

few years, staff turnover rates at local organizations have decreased substantially as

a result of improving salaries, better working conditions, and the emergence of strong

teams within companies, among other factors.

L o w e r I T E d u c a t i o n

Even though the number of ICT-related fresh graduates is quite high, at around 2,000

per year (from approximately 28,000 annual graduates overall), in general,

representatives of large IT firms regard the existing number of students as

insufficient, especially for development plans involving larger offshore projects. In

addition, the quality of certain graduates is deemed inadequate, requiring on-the-job

training to become qualified enough to fill full-time positions.

L o w e r P r o d u c t i v i t y

Average annual productivity in Moldova's IT services industry in 2010 was around

$30,000 per year in revenue per technical employee involved in IT offshoring. The

figure is comparable to other CIS countries, such as Ukraine and Armenia, but it is

quite low when compared with the average numbers reported in major SEE offshoring

centers ($71,000 per year). However, it is important to note that this relatively low

number relates to the nature of the services that are offshored in Moldova at this

18 #CEMA17850 ©2011 IDC

stage and not to actual employees' performance. For example, Romania grew from

around $30,000 in revenue per year per technical employee in 2005 to almost

$75,000 per year in 2010, mainly due to the nature of the offshoring activities, which

moved from support-centered activities to consulting and customization activities.

Obviously, the industry needs to change the current economic model from low-end

outsourcing services, such as software support services, to higher-value activities,

such as software research and development (R&D). We are already seeing progress;

some companies, both foreign and domestic, have started offering software

engineering, design, and R&D services. It is important to improve productivity

considerably, since Moldova does not have the enormous workforce of India or

China, and focus should therefore be on boosting output per employee in order to

increase industry revenues. Moldovan IT services companies need to secure access

to foreign markets, as business abroad will boost revenues and provide necessary

experience via larger and more-complex projects to improve brand image and

company reputation, which will subsequently enable them to demand higher rates.

Providers of IT services that focus mainly on the domestic market are unlikely to see

significant gains in revenue per employee.

Several factors are responsible for the low productivity of Moldovan IT services

companies, including:

A small domestic market for software and IT services and thus low demand for

more complex software applications

A focus on low-end outsourcing services and insufficient emphasis on packaged

software and other higher-value segments, such as research & development,

customization services, and consulting services

A shortage of high-end software engineers, project managers, and general

business professionals with top-management skills

A lack of recognized management-process-related certifications, such as ISO

9001

A lack of specialized support facilities and instruments, such as venture capital

funds, startup incubators, and technology parks

G o v e r n m e n t I n v e s t m e n t P r o m o t i o n S t r a t e g i e s

Current Promotion Strategies

The Moldovan government has been actively promoting Moldova as an attractive

offshore/nearshore destination and has taken several steps in this regard over the

past seven years. Before undertaking any promotional or communication activities,

the Moldovan government focused on setting up an attractive business, legislative,

administrative, and fiscal framework. Several measures were initiated for this, with the

three main pillars being free economic zones, industrial parks, and fiscal incentives

for new investments.

Free Economic Zones

The free economic zones are a part of the customs territory of the Republic of

Moldova. These zones are distinct from the rest of the country in that they provide

beneficial conditions to new businesses of specific types, whether such companies

are backed by local or foreign investors. Several free economic zones and zones of

©2011 IDC #CEMA17850 19

similar status exist in the country: Expo-Business Chisinau, which is located in the

capital; Ungheni-Business, which is 107km to the northwest of Chisinau; Tvardita,

115km to the south of Chisinau; Otaci-Business, 220km to the north of Chisinau;

Valkanes, 200km to the southwest of Chisinau; Taraclia, 153km to the south of

Chisinau; the International Free Port of Giurgiulesti, 210km to the south of Chisinau;

and the Free International Airport of Marculesti, 126km to the north of Chisinau.

Companies operating in the free zones benefit from several advantages: lower

operating costs for infrastructure (transport, water, gas, and electricity); exemption

from VAT and customs and excise duties on goods imported into the free zones and

subsequently exported; a 0% corporate tax rate; and 10 years' protection against

adverse changes in legislation. More specifically, these benefits include:

Legal protection from the state on investments made within the territories of the

free zones

Legislation relating to the regulation and legal status of free zones being

prioritized

A guarantee of the current legislation's applicability for a period of 10 years from

establishment in a free-zone

The possibility to transfer profit abroad

The impossibility of free-zone businesses' assets being expropriated,

nationalized, requisitioned, or confiscated other than by court order

Exemption from import duties and from customs and excise duties on the import

and export of goods and services to/from the free zones

Exemption from quotas and licensing related to the import and export of goods

and services to/from the free zones

The possibility to transfer the ownership rights of the goods and services traded

in free zones from one business to another without additional taxation

Three years' exemption from all income tax on the export of goods and services

from free economic zones to territories outside of Moldova following investment

of at least $1 million in a free zone

Five years' exemption from all income tax on the export of goods and services

from free economic zones to territories outside of Moldova following investment

of at least $5 million in a free zone

Industr ial Parks

These are delimited zones in which economic activities, industrial production, the

provision of services, scientific studies, and technological development take place

with the aim of contributing to the development of a specific region by increasing

employment and making better use of locally available material resources. The fiscal

benefits provided for free zones are also provided to industrial parks. Three zones are

designated as industrial parks: Floresti, an area of 60ha close to the border with

Ukraine; Ungheni, 50ha close to the border with Romania; and Cainari, 23ha. The

main benefits derived from operating in an industrial park include the right to use the

agricultural land available in these parks for purposes other than agriculture, such as

20 #CEMA17850 ©2011 IDC

for buildings, without paying the costs associated with changing the land's designated

use. Essentially, no bureaucratic hurdles exist to investments made within an

industrial park.

Fiscal Incent ives for New Investments in the Economy

ICT companies investing in Moldova benefit of several fiscal incentives, such as 0%

corporate income tax, 0% income tax on all IT staff, and a low flat rate for social

welfare payments for employers. Other incentives for larger investments in the

Moldovan economy, not necessarily related to ICT, include the following:

Companies that are set up with operating capital of at least $250,000 and

companies making investments amounting to at least $250,000 pay 50% less

income tax for a period of five years provided that at least 80% of the tax break is

reinvested in product and/or service development.

Companies that are set up with operating capital of at least $5 million and

companies making investments amounting to at least $5 million are exempt from

all income tax for a period of four years.

In addition to the measures outlined above, the government of Moldova has signed

trade agreements with several EU, CIS, and other countries. The most important

trade agreements include:

EU: The Autonomous Trade Preferences (ATP) agreement, extended until 2015,

which is likely to be replaced by the Deep and Comprehensive Free-Trade Area

(DCFTA) agreement; and the Central European Free-Trade Agreement

(CEFTA), 2006