Embed Size (px)

Citation preview

The Guardian Life Insurance Company of AmericaNew York, NY 10004

Who Is An Employee?

Qualified RetirementPlans

Not for Distribution or Use by the General Public.

Advisor’s Version

The information in this presentation isdesigned to be general in nature and foreducational purposes only. Guardian, itsagents and employees do not give tax orlegal advice. For specific advice, seek andrely upon the advice of a qualified taxadvisor or attorney.

Qualified Retirement Plans

• Qualified Retirement Plans–Tax Deductible Contributions

–Must Include Most of Employees

Fully Insured PlanVery Good Prospect

Owner 52 230,000 364,825 100%Age Salary Contribution ** % Total Contrib.

*Based on 2008 max. benefits, max. dollar limits Indexed for inflation & may increase in the future,uses 74-307 death benefit & PTW3Gold policies, Pref. , NRA 62

Fully Insured PlanFew Employees on Census

Owner 52 230,000 364,825 95

A 29 29,120 11,430B 20 27,040 7,285

Employee Totals 18, 715

% Total

Age Salary Contrib * Contrib.

*Based on 2008 max. benefits, max. dollar limits Indexed for inflation & may increase in the future,uses 74-307 death benefit & PTWL3Gold -B policies, Pref. , NRA 62

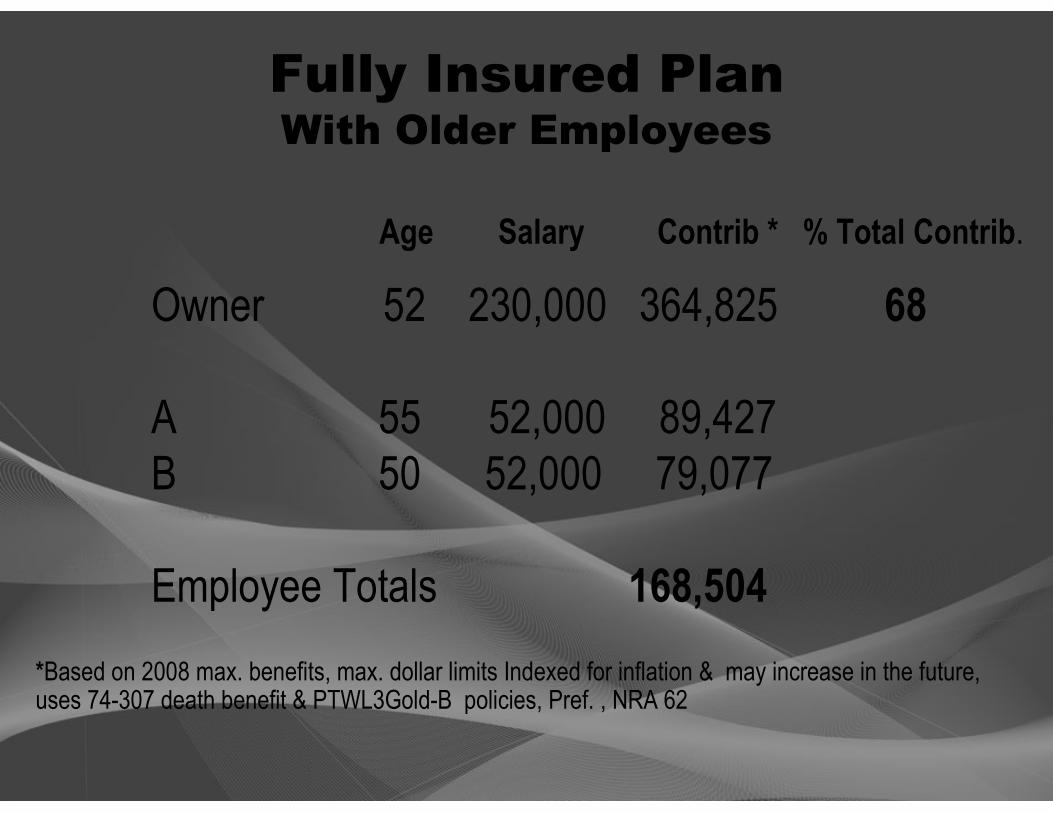

Fully Insured PlanWith Older Employees

Owner 52 230,000 364,825 68

A 55 52,000 89,427B 50 52,000 79,077

Employee Totals 168,504

Age Salary Contrib * % Total Contrib.

*Based on 2008 max. benefits, max. dollar limits Indexed for inflation & may increase in the future,uses 74-307 death benefit & PTWL3Gold-B policies, Pref. , NRA 62

Fully Insured Plan

Owner 52 230,000 364,825 68%

A 50 15,880 24,546B 36 39,520 22,083C 34 42,078 21,105D 29 29,120 11,430E 20 27,040 7,285F 55 52,000 89,427Employee Totals $175,592

Age Salary Contrib * % Total Contrib.

*Based on 2008 max. benefits, max. dollar limits Indexed for inflation & may increase in the future,uses 74-307 death benefit & PTWL3 Gold & PTAPRA–3B policies, Pref. , NRA 62

Not Included in Plan Tests

• Those Not Eligible to be in Plan

– Under Age 21

– Less Than Two Years of Service

• Part-Time

– Under 1,000 Hours in 12 Month Period

• Union Employees

Highly CompensatedEmployees

• Highly Compensated Employees– Own 5% of Business

– Earn $105,000* or more

– Family Members of Owners

*2008 Limit, indexed for inflation & may increase in future

ParticipationRequirements

• Defined Benefit Plans Only– Including Fully Insured Plans

– Must Include Greater* of• 40% All Eligible Employees or

• 2 Employees

*Plans with less than 50 lives

ParticipationRequirements

• Defined Benefit Plans - 40% Rule– 10 Eligible Employees

• 2 Partners

• 8 Non Highly Compensated Employees

How Many Must Be Included in the Plan?

ParticipationRequirements

• Defined Benefit Plans - 40% Rule– 10 Employees X 40% = 4

– Four Must Be Included

– Exclusions Must be Nondiscriminatory• Cannot Just Exclude Non Highly

Compensated Employees

How Many Must Be Included in the Plan?

ParticipationRequirements

• Defined Benefit Plans - 40% Rule– 2 Employees

• 1 Owner

• 1 Secretary (Non Highly Comp.)

How Many Must Be Included in the Plan?

ParticipationRequirements

• Defined Benefit Plans - 40% Rule– Must Include:

– 2 Employees- Boss & Secretary• Greater of 40% or 2 Employees

– Two Must Be Included

How Many Must Be Included in the Plan?

ParticipationRequirements

• Defined Benefit Plans - 40% Rule– Profit Sharing Plan

– 100 Employees• 10 Owners (5%)

• 90 Non Highly Compensated Employees

How Many Must Be Included in the Plan?

ParticipationRequirements

• Defined Benefit Plans - 40% Rule– 40% Rule Does Not Apply to Profit Sharing

Plans

– 10 Owners & 90 Non Highly Comp.

– Minimum Possible: 8 Employees

How Many Must Be Included in the Plan?

Coverage Tests

• In Addition to Participation Test

• Qualified Plans Must Satisfy One ofTwo Coverage Tests

– Ratio Percentage Test

– Average Benefits Test

Average Benefits Test

• Three Part Test

• Complex… Must Be Done by Computer

• Perform Test if Ratio Percentage TestFails

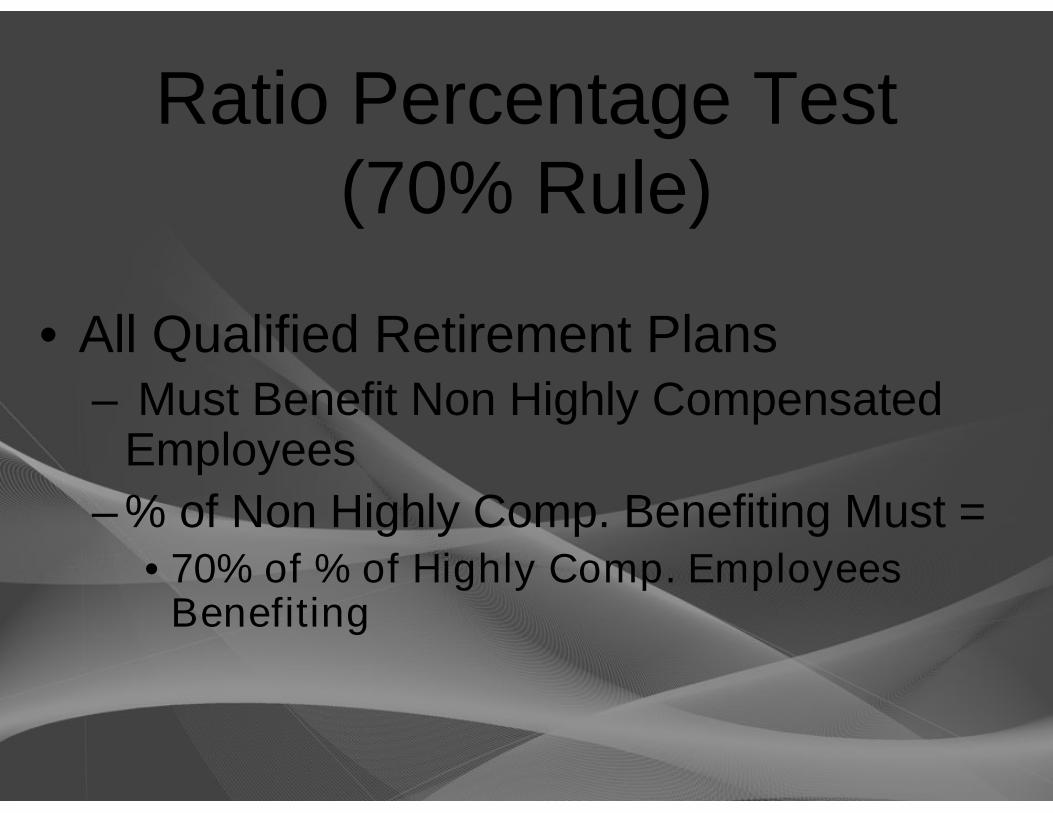

Ratio Percentage Test(70% Rule)

• All Qualified Retirement Plans– Must Benefit Non Highly Compensated

Employees

– % of Non Highly Comp. Benefiting Must =• 70% of % of Highly Comp. Employees

Benefiting

Ratio Percentage Test

• Profit Sharing Plan– 100 Employees

• 10 Owners - Highly Compensated (HCE)

• 90 Non Highly Compensated (NHCE)

– 10 Owners Participate in the Plan

How Many Must Benefit from the Plan?

Ratio Percentage Test

• Profit Sharing Plan– % of HCE Benefiting - 100%

• 10/10 Owners= 100% x 70% = 70%

– % of NHCE Who Must Benefit• 90 NHCE x 70% = 63

– 63 NHCE Must Participate

How Many Must Benefit in the Plan?

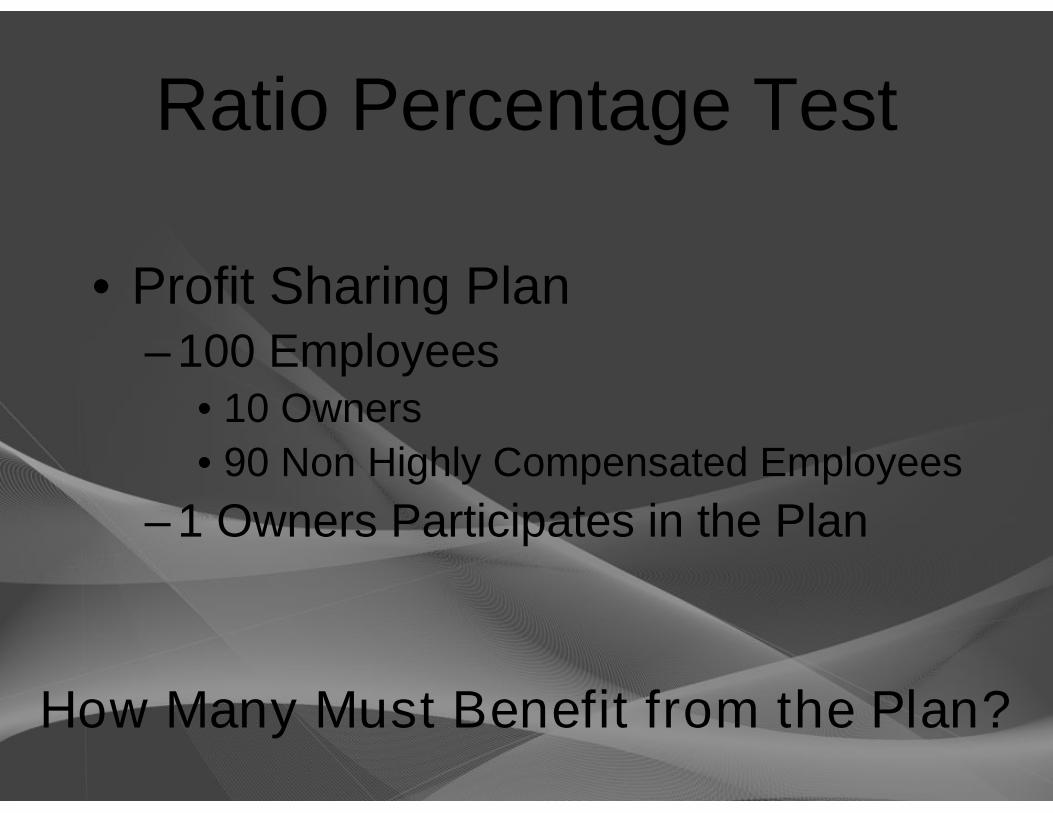

Ratio Percentage Test

• Profit Sharing Plan– 100 Employees

• 10 Owners

• 90 Non Highly Compensated Employees

– 1 Owners Participates in the Plan

How Many Must Benefit from the Plan?

Ratio Percentage Test

• Profit Sharing Plan– % of HCE Benefiting - 10%

• 1/10 Owners = 10% x 70% = 7%

– % of NHCE Who Must Benefit• 90 NHCE x 7% = 7

– 7 NHCE Must Benefit

How Many Must Benefit in the Plan?

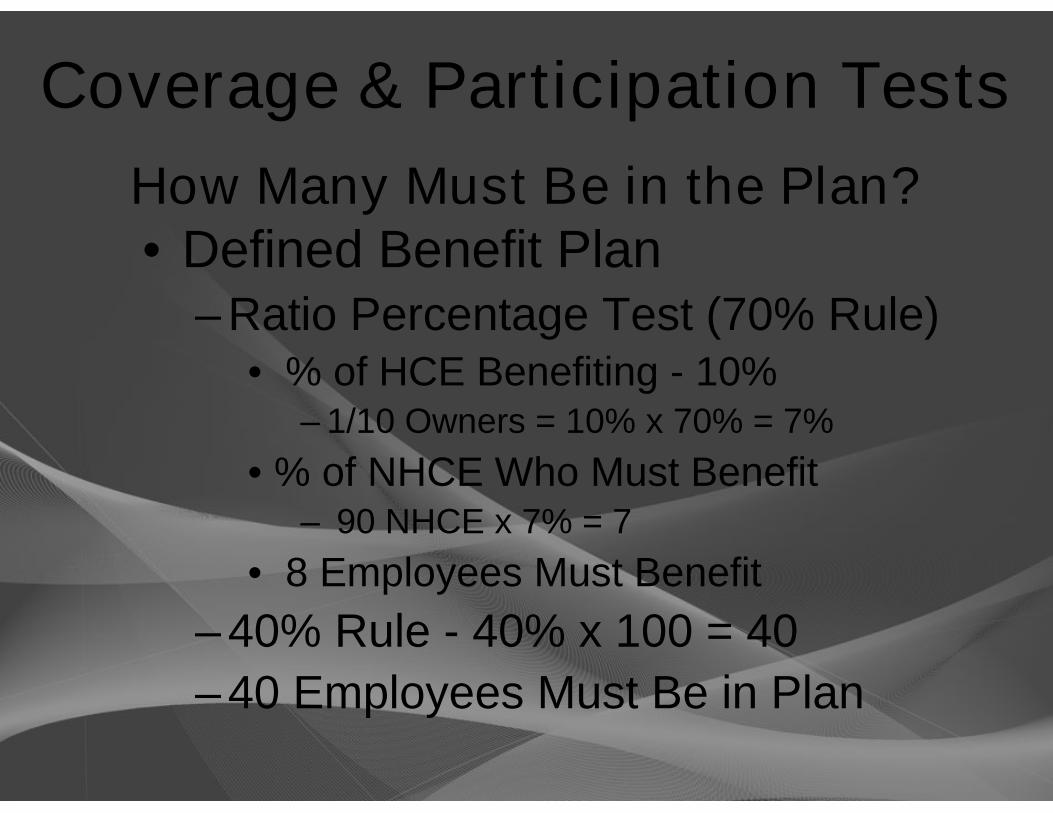

Coverage & Participation Tests

• Defined Benefit Plan– 100 Employees

• 10 Owners

• 90 Non Highly Compensated Employees

– 1 Owner Participates in the Plan

How Many Must Be in the Plan?

Coverage & Participation Tests

• Defined Benefit Plan– Ratio Percentage Test (70% Rule)

• % of HCE Benefiting - 10%– 1/10 Owners = 10% x 70% = 7%

• % of NHCE Who Must Benefit– 90 NHCE x 7% = 7

• 8 Employees Must Benefit

– 40% Rule - 40% x 100 = 40

– 40 Employees Must Be in Plan

How Many Must Be in the Plan?

Hidden Employees

• Owners Often Look for Ways toExclude Employees– Avoid Cost of Employee Benefits

• Tricks Don’t Work

Watch Out for Hidden Employees

• Types of Hidden Employees– Leased Employees

– Multiple Businesses

– “Walks Like a Duck” Employees

Leased Employees

• Employees Hired from AnotherCompany

Leased Employees ExampleDoctor Jeff

• Numerous Employees in Office– Receptionist, Nurse, Technician, etc.

• He Says He Has “No Employees”– Entire Staff Hired from a Leasing

Company

Leased Employees

• Doctor’s View

– They Are Not His Employees

– Leasing Firm Should Provide AnyBenefits

Leased Employees

• IRS’s View

– They May Have to Be Included in thePlan Tests

– Doctor Jeff May Have to ProvideRetirement Benefits for Them

Leased Employees

• Must Be Included In Plan Tests if:

– Work Full-time for a Year

– More Than 20% of Non HighlyCompensated Work Force

• If Less Than 20% Can Exclude if:

– Leasing Company Has Special Retirement Plan

Leased Employees

• Leasing Organization’s SpecialRetirement Plan– Money Purchase Plan

• Immediate Participation

• Full & Immediate Vesting

• Flat 10% of Pay Contribution Formula

Multiple Businesses

• Employer Owns Two Companies– Company X

• No Non Owner Employees

– Company Y• 10 Non Owner Employees

Can He Have a Plan Which Covers Justthe Owner in Company X?

Multiple Businesses

• Multiple Businesses Must BeIncluded in Plan Tests if:– Controlled Group

– Affiliated Service Group

Multiple Businesses

• What Do You Need to Know?– Controlled Group

• Percentage of Ownership

– Affiliated Service Group• Percentage of Ownership

• Function of Each Company

• Who Are Their Customers?

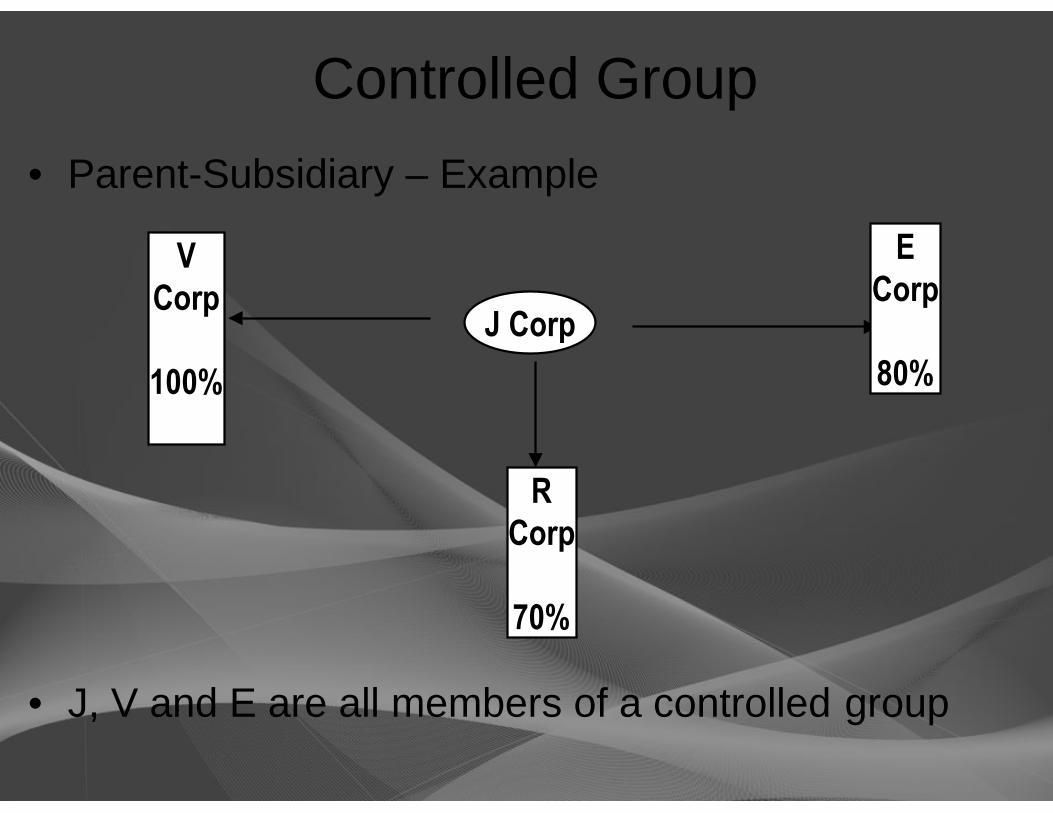

Controlled Group

• Parent-Subsidiary Group– Connected through 80% Stock

Ownership

• Brother-Sister Group– 5 or Fewer People Own 80% Plus

– Same 5 or Fewer Own More than 50%• Only Count Identical Ownership

Controlled Group

• Parent-Subsidiary – Example

• J, V and E are all members of a controlled group

J Corp

VCorp

100%

ECorp

80%

RCorp

70%

Controlled Group

• Brother-Sister Group– 5 or Fewer People Own 80% Plus

– Same 5 or Fewer Own More than 50%• Only Count Identical Ownership

Controlled Group Example #1

• Ralph Owns Two Companies– Violin Repair Shop

• No Non Owner Employees

– Fish Restaurant• 10 Non Owner Employees

Can Ralph Have a Plan Which Covers Just theEmployees in the Violin Shop?

Controlled Group Example #180% Test

• Violin Repair Shop– Ralph Owns 90%

– Bill Owns 10%

• Fish Restaurant– Ralph Owns 50%

– Bill Owns 50%

5 or Fewer Employees Own 80% of Each

Controlled Group Example #1Identical Ownership Test

Ralph 90% 50% 50%

Bill 10% 50% 10%

Total Identical Ownership 60%

Violin Shop Restaurant Identical

% Owned % Owned Ownership

Identical Ownership of Over 50%It IS a Controlled Group

All Employees from Both Companies MustBe Included in Plan Tests

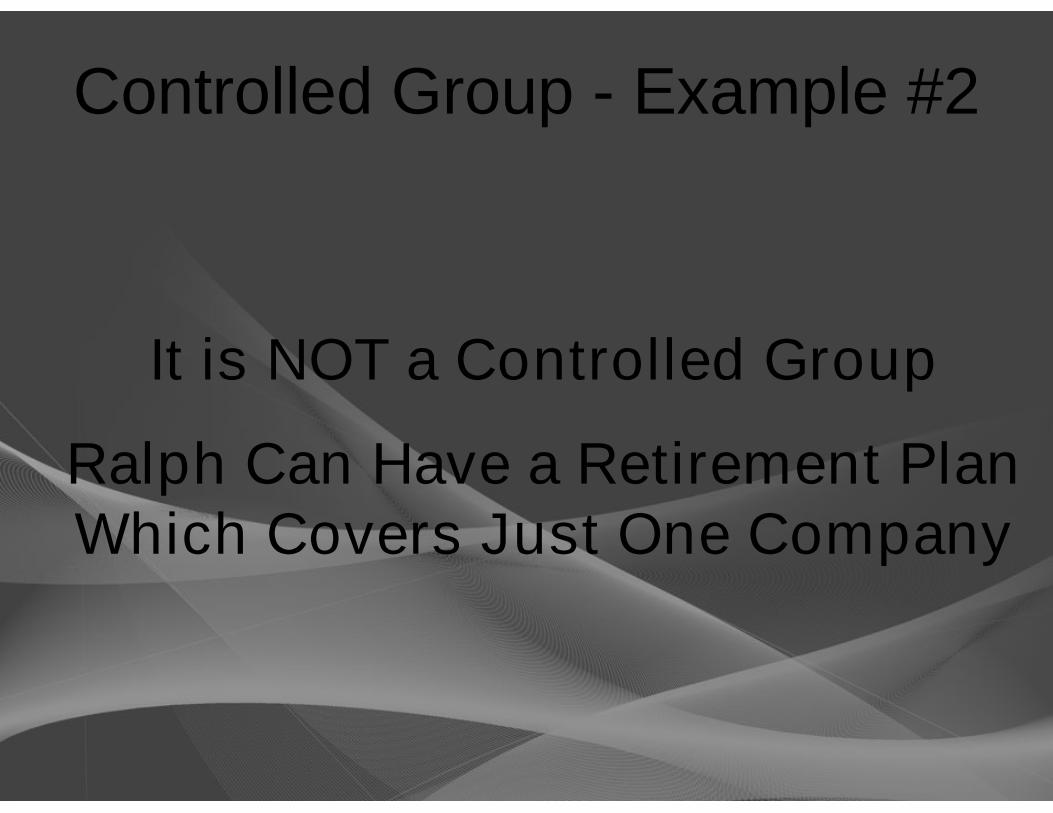

Controlled Group - Example #280% Test

• Violin Repair Shop– Ralph Owns 100%

• Fish Restaurant– Ralph Owns 60%

– Bill Owns 40%

5 or Fewer People Do Not Own 80%You Need Not Count Anyone Who Doesn’t

Own Part of Both Companies

Controlled Group - Example #2

It is NOT a Controlled Group

Ralph Can Have a Retirement PlanWhich Covers Just One Company

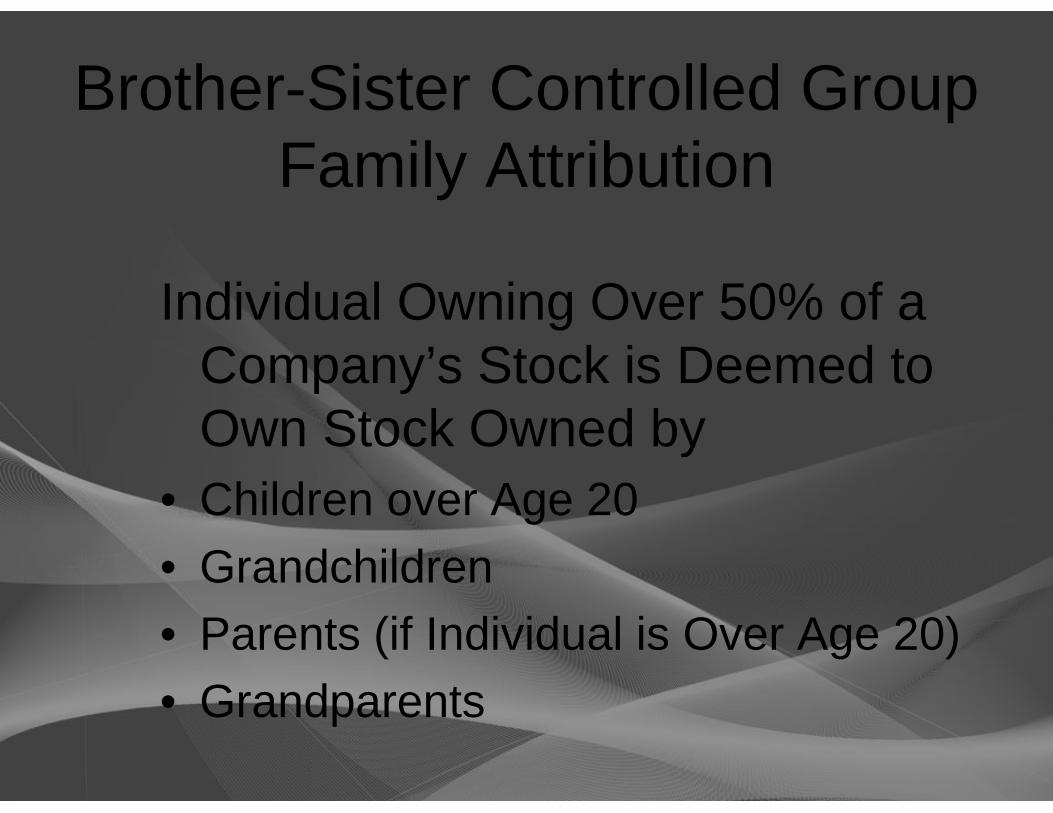

Brother-Sister Controlled GroupFamily Attribution

• Individual is Deemed to Own StockOwned by Spouse* and Children UnderAge of 21

• Children Under Age 21 are Deemed toOwn Stock Owned by Parent

*Also True for Parent-Subsidiary Controlled Group

Brother-Sister Controlled GroupFamily Attribution

Individual Owning Over 50% of aCompany’s Stock is Deemed toOwn Stock Owned by

• Children over Age 20

• Grandchildren

• Parents (if Individual is Over Age 20)

• Grandparents

Brother Sister Controlled GroupFamily Attribution

• Rule

– Individual Assumed to Own Stock Owned by Spouse

• No Spousal Attribution Applies if

– No Ownership in Spouse’s Company

– Not Employee, Director, or Manager in Spouse’sCompany

– No More than 50% of Gross Income from Royalties,Rent, Dividends, Interest, Annuities, etc.

– There Are No Stock Restrictions on Disposal

Controlled Group Example #3

• Nancy Owns a Medical Practice– 6 Employees

• Her Spouse Steve Is a Tax Accountant– Owns 100% of His Business

– No Employees,

• They Live in NJ & Have No Children

Can Steve Have a Plan for his FirmWhich Covers Just Him?

Controlled Group Example #3Not a Controlled Group

• Due to the Spousal Exception - SteveCan Have a Retirement Plan Just forhis Firm

• He Doesn’t Need to Include theEmployees from Nancy’s Practice inhis Plan Tests

Controlled Group Example #4

What if Steve & Nancy Lived inCalifornia?

Could Steve Still Have aPlan Just for Himself?

Controlled Group Example #4

• California is a community propertystate

• Steve is considered to own 50% ofNancy’s business

• Employees from Both Companies MayHave To Be Included in the Plan Tests

• Spousal exception may not apply

Controlled Group

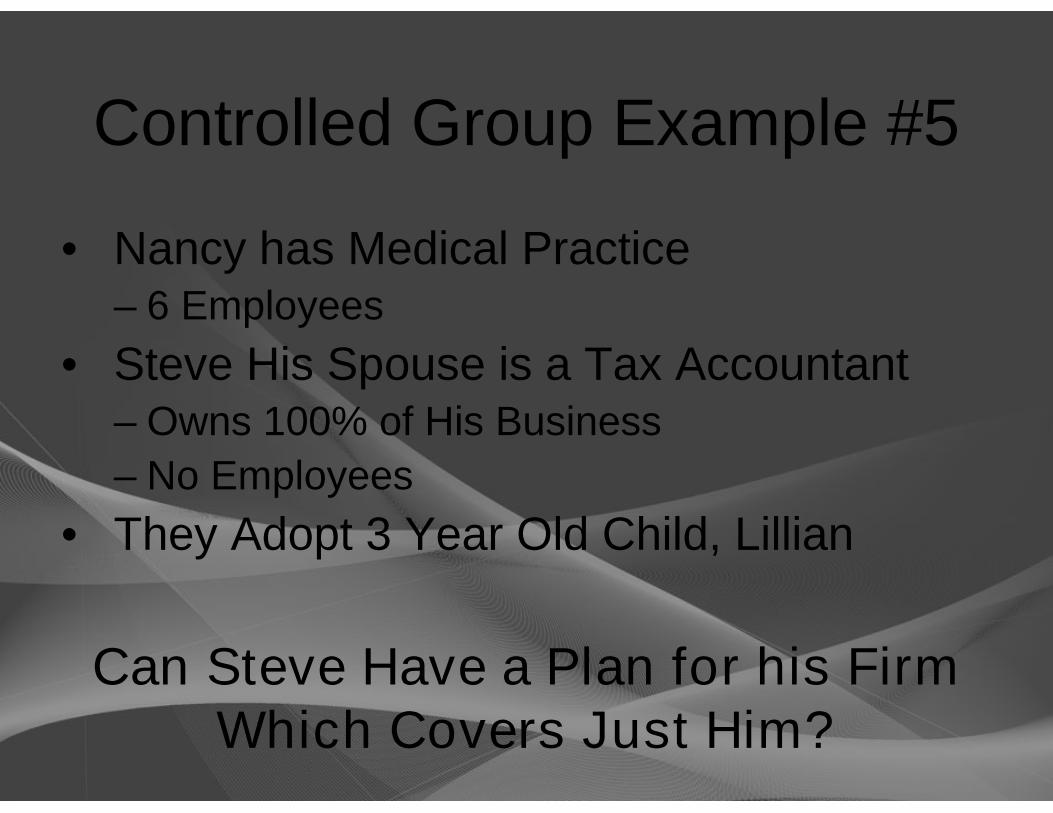

Controlled Group Example #5

• Nancy has Medical Practice– 6 Employees

• Steve His Spouse is a Tax Accountant– Owns 100% of His Business

– No Employees

• They Adopt 3 Year Old Child, Lillian

Can Steve Have a Plan for his FirmWhich Covers Just Him?

Controlled Group Example #5Family Attribution

• Lillian is Considered to Own– 100% of Nancy’s Medical Practice &

– 100% of Steve’s Business

• Their Businesses are in a Controlled Group

Steve Must Include the Employees inNancy’s Practice in His Plan Tests

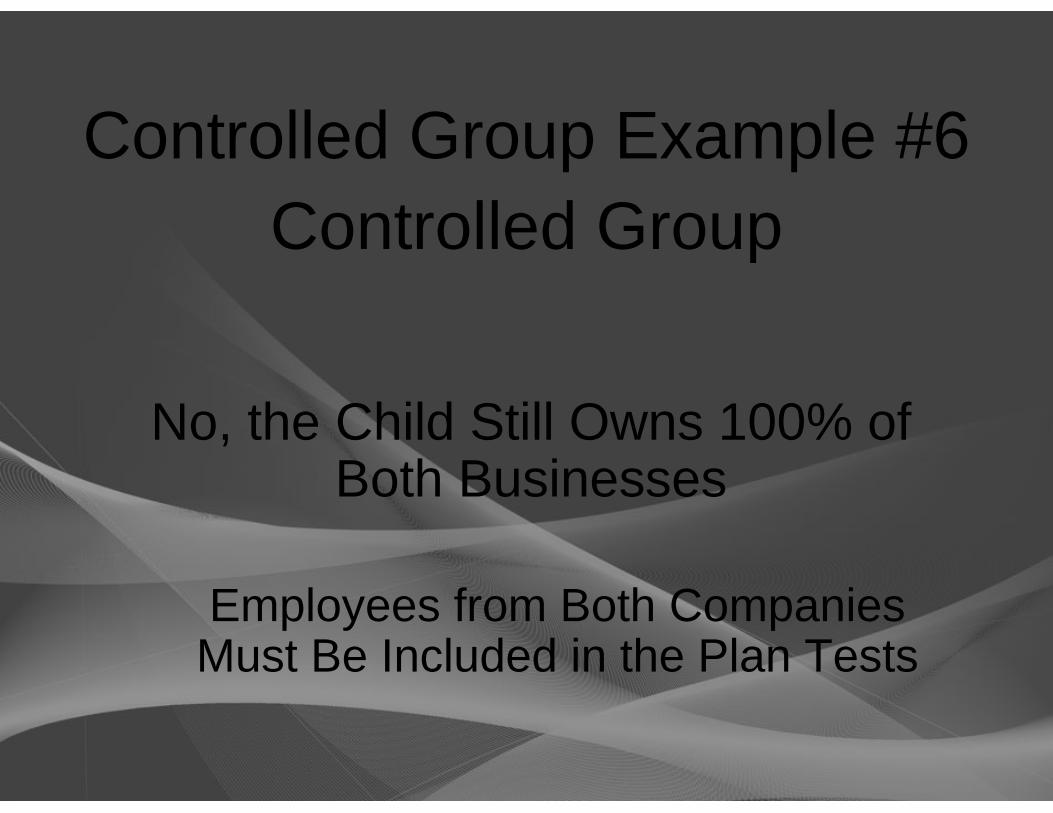

Controlled GroupExample #6

• Steve & Nancy adopt the three year old child

• Steve & Nancy get a divorce

Can Steve Have a PlanJust for Himself?

Controlled Group Example #6

Controlled Group

No, the Child Still Owns 100% ofBoth Businesses

Employees from Both CompaniesMust Be Included in the Plan Tests

Controlled Group Example #7

• Steve & Nancy don’t adopt a child

• Nancy Has a 13 year old daughter, Adele,from previous marriage– Adele Lives with Steve & Nancy

– Steve Has Not Adopted Adele

– Adele’s Father Is a Bookkeeper for a Toy Co.

Can Steve Still Have a PlanJust for Himself?

Controlled GroupExample #7

Adele Owns100% of Nancy’s Company

0% of Steve’s Company

Step Children - No Attribution

Steve Can Have a Plan Just for Himself

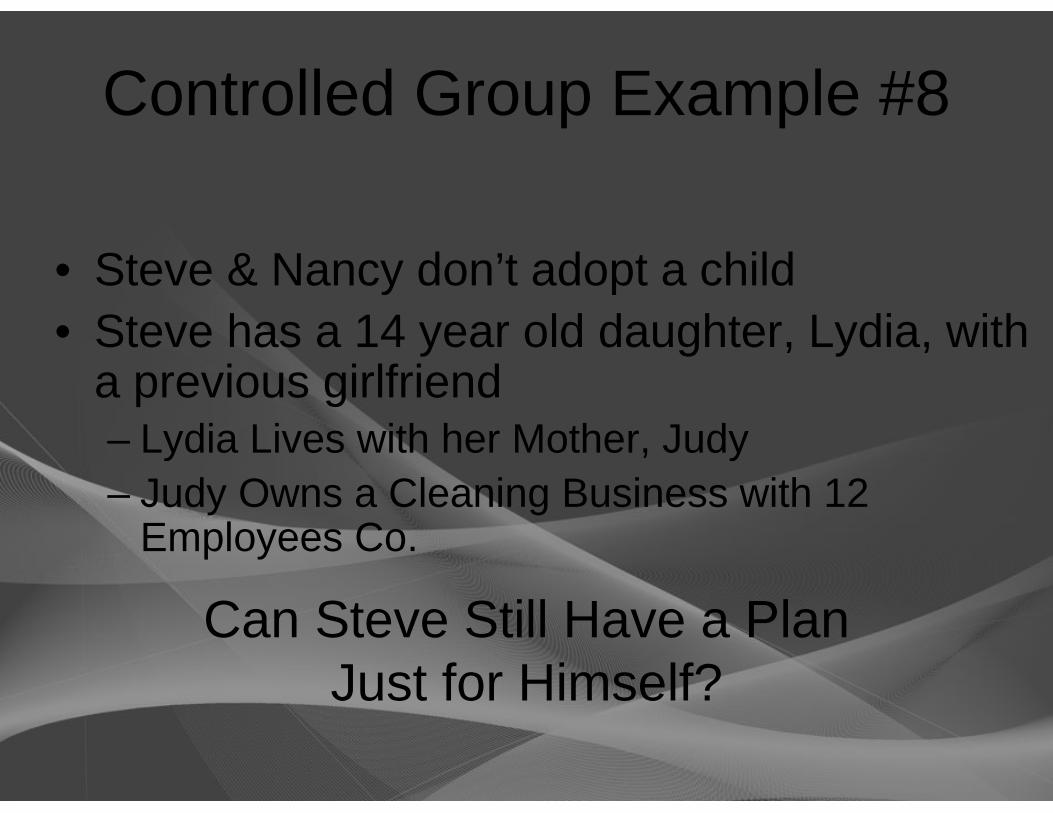

Controlled Group Example #8

• Steve & Nancy don’t adopt a child

• Steve has a 14 year old daughter, Lydia, witha previous girlfriend– Lydia Lives with her Mother, Judy

– Judy Owns a Cleaning Business with 12Employees Co.

Can Steve Still Have a PlanJust for Himself?

Controlled Group Example #8

Lydia Owns:

0% Nancy’s Company

100% Steve’s Company

100% Judy’s Company

Employees from Both Steve’s and Judy’sCompanies Must Be Included in the Plan Tests

Steve’s Business & Judy’s Business Arein a Controlled Group

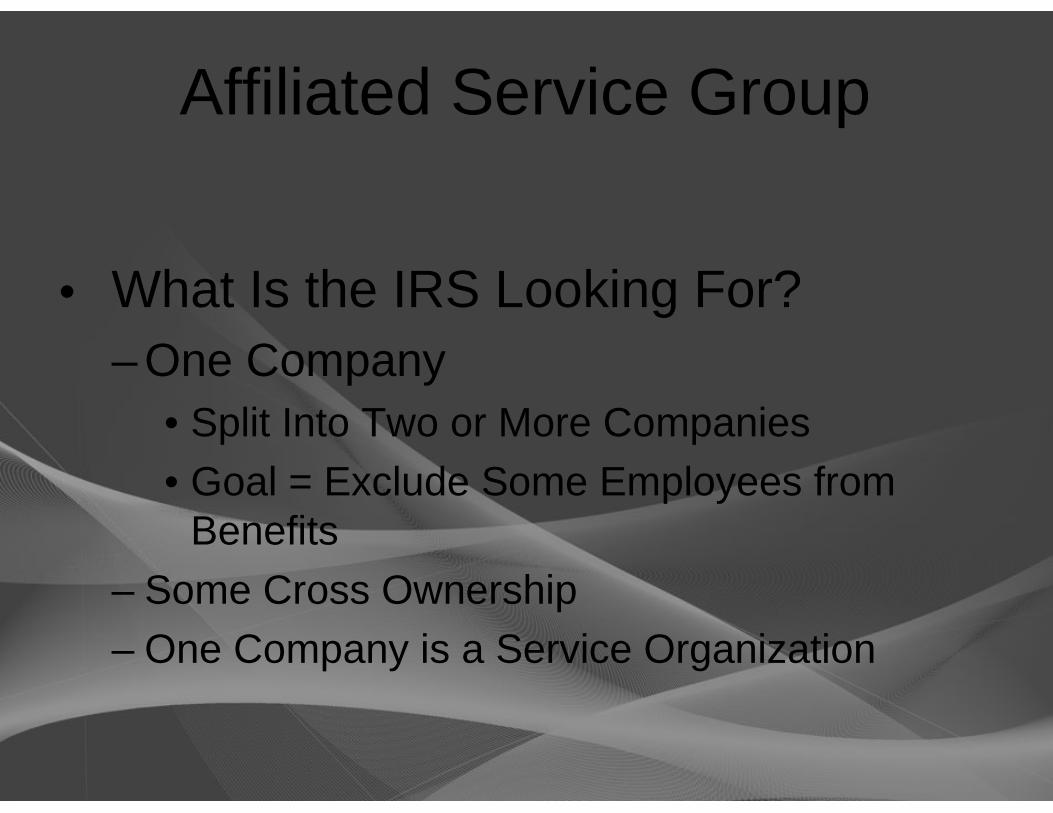

Affiliated Service Group

• Even if Businesses Pass ControlledGroup Test

• May Be Affiliated Service Group

Affiliated Service Group

• Company F – First Service Organization

• Company B– 10% Owned by Highly Comp. Employees of

Companies A or F

– Large Part of Company B’s Work is PerformingServices for Company A or F (or for both)

– Services Historically Done by Employees OfCompanies A or F

• Company A– Shareholder or Partner of Company F and

– Performs Services for Company F or

– Performs Services with Company F for 3rd Party

Affiliated Service Group

• What Is the IRS Looking For?

– One Company

• Split Into Two or More Companies

• Goal = Exclude Some Employees fromBenefits

– Some Cross Ownership

– One Company is a Service Organization

Affiliated Service Group

• Company F – First Service Organization

• Company B– 10% Owned by Highly Comp. Employees of

Companies A or F

– Large Part of Company B’s Work is PerformingServices for Company A or F (or both)

– Services Historically Done by Employees OfCompanies A or F

• Company A– Shareholder or Partner of Company F and

– Performs Services for Company F or

– Performs Services with Company F for 3rd Party

Affiliated Service GroupExample

• Fat Cat Veterinary Practice– Owned 10% by Doctor Tom

– 20 Non Highly Compensated Employees

• Bite-Rite Veterinary Dental Practice– Owned 100% by Doctor Tom

– Only Employees – Doctor Tom & Vet Tech

Can Bite-Rite Have a Retirement Plan

Without Including Any of Fat Cat’s Employees?

Affiliated Service Group

• Affiliated Service Group Because

– 10% of Bite-Rite Owned by HCE of Fat Cat

– Bite-Rite’s Only Work – Doing Dental Work forFat Cat

– Dentistry Historically Done by GeneralVeterinary Practice

• Fat Cat’s Employees Must Be Included inTests for Bite-Rite’s Retirement Plan

Teddy Bear Manufacturer

• Objective: Suzette Wants to Set Up aPlan for Herself

– Owns 25% of Fluff & Stuff

– Owns 100% of Bear-o-tronics Company

Teddy Bear Manufacturer - Functions

• Fluff & Stuff Company– Sews & Sells the Stuffed Bears

• Bear-o-tronics Company– Manufactures the Sound Box with the Cute

Sayings for the Bear

– Works Exclusively for Fluff & Stuff

Teddy Bear Manufacturer - Employees

• Fluff & Stuff Company– 15 Employees

• Ages 25 - 47, Salaries $25,000 - $60,000

• Bear-o-tronics Company– One Employee, Suzette

Suzette Wants a Plan for Just Herself

Teddy Bear Manufacturer – Ownership

• Fluff & Stuff Company– Bob 25%

– Tom 25%

– Tim 25%

– Suzette 25%

• Bear-o-tronics Company– Suzette 100%

Not a Controlled Group

Teddy Bear Manufacturer

Not an Affiliated Service Group

• Fluff & Stuff & Bear-o-tronics Companiesdo not comprise an Affiliated ServiceGroup

– Fluff & Stuff Is not a “service organization”

Suzette Can Have a Plan Just for Herself

Affiliated Service GroupsService Organizations

• FSO Must Be a Service Organization

– Principal Business is Performance of Serviceson a Regular & Continuing Basis

– Capital is Not a Material Income-ProducingFactor

Affiliated Service GroupLawn Flamingo Manufacturer

• Objective: Annette Wants to set up a planfor herself

– Owns 33 1/3 of Flamingorama

– Owns 100% of Long Legs Management, Inc.

Lawn Flamingo Manufacturer -Functions

• Flamingorama, Inc.

– Manufactures Lawn Flamingos

• Long Legs Management, Inc.

– Manages Flamingorama, Inc.

– Works Exclusively for Flamingorama, Inc.

Lawn Flamingo Manufacturer -Employees

• Flamingorama, Inc.– 20 Employees

• Ages 22 – 50, Salaries $20,000 - $40,000

• Long Legs Management, Inc.– One Employee – Annette

Annette Wants A Plan Just for Herself

Lawn Flamingo Manufacturer -Ownership

• Flamingorama, Inc.– Alice 33 1/3%

– Annette 33 1/3%

– Elise 33 1/3%

• Long Legs Management, Inc.– Annette 100%

Not a Controlled Group

Lawn Flamingo Manufacturer

Affiliated Service Group

The Flamingo Firms are not serviceorganizations, but they are still an

affiliated service group

Annette CANNOT havea plan just for herself

WHY?

Affiliated Service GroupManagement Company

An affiliated service groupresults if one company

principally performsmanagement services for

another

Common Sense Rule

• Complex Rule– Who Directs the Work?

– Does the Individual Work for OtherOrganizations?

– Do They Work Full-Time?

– Are They Permanent or Temporary?

– Are the Individual’s Services Available toGeneral Public?

– Who Provides the Tools & Equipment?

– Where Do They Work?

Common Sense RuleEmployee Coverage

• If It Looks Like a Duck and

It Walks Like a Duck and

It Quacks Like a Duck,

• It Is a Duck!

“Walks Like A Duck” Example

• Wants Fully Insured Plan for Himself• Claims He Has “No Employees”• Mary Does His Secretarial Work

Architect Bob

“Walks Like A Duck” Example

• Mary is an Independent Contractor• Paid 1099 Income• She Is Not His Employee• Need Not Be Included in His Retirement

Plan

Architect’s View

“Walks Like A Duck” Example

• Mary

– Works Full-Time for Architect

– Architect Supplies All Equipment & WorkSpace

– Does Not Work for Anyone Else

• Considered Employee of Architect– Must Be Included in Plan Tests

IRS’s View

Key to a Satisfied ClientKnow Your Employees

• Right Plan for His Goals

• Client Happy– Both at Set-Up & at Retirement

– Refer Additional Clients

• Protect Client from Problems

Local Contacts

LANNY D. LEVIN AGENCY, Inc.

Lanny Levin Case Consultation 847-266-2244

Jerry Fox Illustrations 847-266-2235

Bryna Lee Jacobson Illustrations 847-266-2241

NATIONAL BENEFIT SERVICES, Inc.

Jerry Kalish Case Consultation 312-409-9080 x3