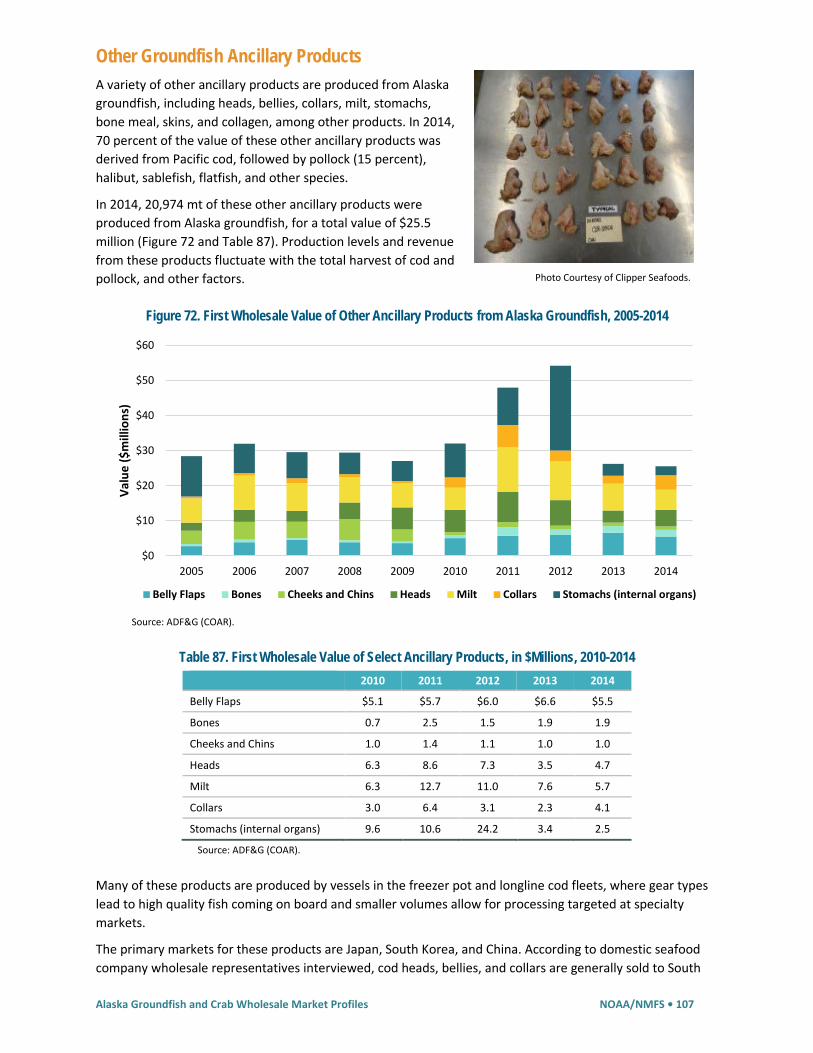

Embed Size (px)

Citation preview

Prepared by: McDowell Group

Wholesale

Market Profiles

for Alaska Groundfish

and Crab Fisheries

May 2016

Authors and Contributions:From NMFS-Alaska Fisheries Science Center: Ben Fissel (PI, project oversight, project design, and editor), Ron Felthoven (project oversight, project design), Brian Garber-Yonts (editor). From McDowell Group, Inc.: Jim Calvin (project oversight and editor), Andy Wink (lead author/analyst), Stephanie Warpinski (author/analyst), Garrett Evridge (author/analyst), Dan Lesh (author/analyst). From Pacific States Marine Fisheries Commission: Bob Ryznar (project oversight and sub-contractor management), Jean Lee (data compilation and analysis)

This report was produced and funded by the National Marine Fisheries Service’s Alaska Fisheries Science Center. Funding was awarded through competitive contracts to the Pacific States Marine Fisheries Commission and McDowell Group, Inc.

The analysis was conducted during the summer and fall of 2015, based primarily on 2014 harvest and market data. A final review by Alaska Fisheries Science Center staff was completed in February 2016 and the document was finalized in March 2016. Data throughout the report was compiled in July-Sept. 2015. Revisions to source data after this time may not be reflected in this report. Typically, revisions to economic fisheries data are not substantial and data presented here accurately reflect the trends in the analyzed markets. For data sourced from NMFS and the Alaska Fisheries Information Network (AKFIN) the reader should refer to the Economic Status Report of the Groundfish Fisheries Off Alaska, 2014 and Economic Status Report of the BSAI King and Tanner Crab Fisheries Off Alaska, 2014 for the official and most recent data publicly available at (http://www.afsc.noaa.gov/REFM/Socioeconomics/SAFE/default.php).

The findings and conclusions in the paper are those of the author(s) and do not necessarily represent the views of the National Marine Fisheries Service, NOAA.

Reference to trade names does not imply endorsement by the National Marine Fisheries Service, NOAA.

All images are for illustrative and informational purposes only and their use does not imply endorsement by the National Marine Fisheries Service, NOAA. With regards to images obtained through the World Wide Web (e.g., Wikipedia, Wikimedia) every attempt has been made to comply with the stated use standards and give appropriate attribution. The National Marine Fisheries Service, NOAA, is a not for profit organization.

This document should be cited as follows:Alaska Fisheries Science Center. 2016. Wholesale market profiles for Alaska groundfish and crab fisheries. 134 p. Alaska Fish. Sci. Cent., NOAA, Natl. Mar. Fish. Serv., 7600 Sand Point Way NE, Seattle WA 98115.

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • iii

Table of Contents

Table of Contents ........................................................................................................................................ iii List of Tables .................................................................................................................................... v List of Figures .................................................................................................................................. vii Executive Summary ............................................................................................................... ix Key Markets for Alaska Groundfish and Crab .....................................................................xi Glossary of Terms and Abbreviations ............................................................................................... xiv Abbreviations and Acronyms ......................................................................................................... xiv Glossary of Terms ........................................................................................................................... xv Global Groundfish Production and Key Markets .................................................................................. 1 Alaska Groundfish Production and Market Summary ..................................................................... 1 Global Whitefish and Other Marine Fish Production ...................................................................... 1 Alaska’s Position in the Global Whitefish Market ............................................................................ 3 Summary of Key Alaska Groundfish Markets .................................................................................. 5 Wholesale Market Profiles for Alaska Pollock Products ....................................................................... 7 Fishery Summary.............................................................................................................................. 7 Alaska Pollock Production ................................................................................................................ 9 Wholesale Market Profile of Alaska Pollock Fillets ........................................................................ 13 Wholesale Market Profile of Alaska Pollock Surimi ....................................................................... 23 Wholesale Market Profile of Alaska Pollock Roe ........................................................................... 30 Wholesale Market Profile of Alaska H&G Pollock.......................................................................... 35 Global Pollock Production and Competing Supply ........................................................................ 39 Wholesale Market Profile for Pacific Cod .......................................................................................... 42 Fishery Summary............................................................................................................................ 42 Production Summary ..................................................................................................................... 44 Production Volume and Value of H&G and Fillets ......................................................................... 45 Product Description and Supply Chain of H&G and Fillets ............................................................ 47 Key Markets for Pacific Cod ........................................................................................................... 50 Global Production and Competing Supply ..................................................................................... 54 Wholesale Market Profile for Yellowfin Sole ..................................................................................... 57 Fishery Summary............................................................................................................................ 57 Product Description and Supply Chain .......................................................................................... 58 Production Volume and Value ....................................................................................................... 59 Wholesale Market Profile for Rock Sole ............................................................................................ 60 Fishery Summary............................................................................................................................ 60 Product Description and Supply Chain .......................................................................................... 61 Production Volume and Value ....................................................................................................... 62 Key Markets for Alaska Sole Species .............................................................................................. 63 Global Production and Competing Supply ..................................................................................... 67 Wholesale Market Profile for Atka Mackerel .................................................................................... 69 Fishery Summary............................................................................................................................ 69 Product Description and Supply Chain .......................................................................................... 71 Production Volume and Value ....................................................................................................... 71 Key Markets for Atka Mackerel ..................................................................................................... 72 Global Production and Competing Supply ..................................................................................... 73 Wholesale Market Profile for Pacific Ocean Perch ............................................................................. 75 Fishery Summary............................................................................................................................ 75 Product Description and Supply Chain .......................................................................................... 76 Production Volume and Value ....................................................................................................... 77

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • iv

Key Markets for Pacific Ocean Perch ............................................................................................. 78 Global Production and Competing Supply ..................................................................................... 80 Wholesale Market Profile for Sablefish ............................................................................................. 81 Fishery Summary............................................................................................................................ 81 Product Description and Supply Chain .......................................................................................... 83 Production Volume and Value ....................................................................................................... 84 Key Markets for Alaska Sablefish ................................................................................................... 86 Global Production and Competing Supply ..................................................................................... 89 Wholesale Market Profile for Pacific Halibut ..................................................................................... 90 Fishery Summary............................................................................................................................ 90 Product Description and Supply Chain .......................................................................................... 91 Production Volume and Value ....................................................................................................... 93 Key Markets for Pacific Halibut ...................................................................................................... 94 Global Production and Competing Supply ..................................................................................... 96 Wholesale Market Profile for Ancillary Products ............................................................................... 98

Key Products Analysis ............................................................................................................................ 100 Fish Meal ...................................................................................................................................... 101 Fish Oil .......................................................................................................................................... 104 Other Groundfish Ancillary Products ........................................................................................... 107 Wholesale Market Profile for Snow Crab ........................................................................................ 109

Fishery Summary ................................................................................................................................... 109 Product Description and Supply Chain ........................................................................................ 111 Production Volume and First Wholesale Value ........................................................................... 112 Production Analysis ...................................................................................................................... 114 Key Markets for Snow Crab ......................................................................................................... 115 Global Production and Competing Supply ................................................................................... 118 Wholesale Market Profile for King Crab .......................................................................................... 120

Fishery Summary ................................................................................................................................... 120 Product Description and Supply Chain ........................................................................................ 122 Production Volume and First Wholesale Value ........................................................................... 123 Production Analysis ...................................................................................................................... 125 Key Markets for King Crab ........................................................................................................... 126 Global Production and Competing Supply ................................................................................... 128

References .......................................................................................................................... 131

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • v

List of Tables Executive Summary Tables

Executive Summary Table 1. Average First Wholesale Value per Metric Ton, 2010-2014................................................................ xi Executive Summary Table 2. Primary Sales of First Wholesale Alaska Groundfish and Crab Products by Market, 2010-2014 ............................................................................................................................................... xi Executive Summary Table 3. Alaska Groundfish and Crab Production and Market Summary, 2014............................................... xii Executive Summary Table 4. Changes in Relevant Currency Exchange Rates, October 2013 vs. October 2015 ............................. xiii Tables Table 1. Alaska Groundfish Production and Market Summary, 2014 ............................................................................................... 1 Table 2. Global Whitefish and Other Marine Fish Species Production (mt), 2013 ............................................................................ 2 Table 3. Imports of Tilapia and Pangasius Products, United States and Europe vs. Other Markets, 2012-2014 .............................. 5 Table 4. Wholesale Sales of Alaska Groundfish Meat Products (mt), 2014 ...................................................................................... 6 Table 5. Summary Profile of Alaska Pollock Wholesale Production and Markets, 2014 ................................................................... 7 Table 6. Alaska Pollock Harvest Volume in Federal and State Fisheries (mt), 2010-2014 ................................................................ 8 Table 7. Production Volumes and Recovery Rates for Common Alaska Pollock Products, 2014 .................................................... 10 Table 8. Alaska Pollock Production Composition, by First Wholesale Volume, 2005-2014 ............................................................ 11 Table 9. Alaska Pollock Production Composition, by First Wholesale Value, 2005-2014................................................................ 12 Table 10. Unit Value per Metric Ton for Major Alaska Pollock Products, 2005-2014 ..................................................................... 12 Table 11. First Wholesale Value, Alaska Pollock Fillets, $Millions .................................................................................................. 16 Table 12. Alaska Pollock Fillet Unit Value per Metric Ton and Production Composition, 2010-2014 ............................................. 16 Table 13. Sales of Alaska Pollock Fillets to Key Markets (mt), 2010-2014 ...................................................................................... 17 Table 14. European Imports of Pollock Fillets from Major Producers (mt), 2010-2014 ................................................................. 19 Table 15. Estimated U.S. Pollock Fillet Market Supply (mt), 2010-2014 ......................................................................................... 21 Table 16. Brazil Imports of Frozen Pollock and Salted/Dried Fish from China and United States................................................... 22 Table 17. Pollock Fillet Production from Alaska and Russia (mt), 2010-2014 ................................................................................. 23 Table 18. First Wholesale Value, Alaska Pollock Surimi, $Millions ................................................................................................. 25 Table 19. U.S. Exports of Alaska Pollock Surimi by Country (mt), 2010-2014 ................................................................................. 26 Table 20. Japan Surimi Imports from Major Producers (mt), 2010-2014 ....................................................................................... 27 Table 21. Total and Unit Value of Japan Surimi Imports, 2010-2014 .............................................................................................. 28 Table 22. Global Surimi Production (mt), 2010-2014 ..................................................................................................................... 29 Table 23. First Wholesale Value, Alaska Pollock Roe, $Millions...................................................................................................... 31 Table 24. Exports of Alaska Pollock Roe by Country (mt), 2010-2014 ............................................................................................ 33 Table 25. Japan Pollock Roe Imports (mt), 2010-2014 ................................................................................................................... 33 Table 26. Value of Japan Pollock Roe Imports, 2010-2014 ............................................................................................................. 34 Table 27. South Korean Pollock Roe Trade (mt), 2012-2014 .......................................................................................................... 35 Table 28. First Wholesale Value, Frozen H&G Alaska Pollock, $Millions ........................................................................................ 36 Table 29. Imports of Alaska H&G Pollock by Country (mt), 2012-2014 .......................................................................................... 38 Table 30. China Imports of Frozen H&G Pollock by Country (mt), 2012-2014 ................................................................................ 38 Table 31. Chinese Re-exports of Frozen Alaska Pollock Fillets, by Market, 2014............................................................................ 39 Table 32. Global Pollock Harvest by Major Producer (mt), 2010-2014 ........................................................................................... 40 Table 33. Competing Whitefish Supply Trends ............................................................................................................................... 41 Table 34. Summary Profile of Pacific Cod Wholesale Production and Markets, 2014 .................................................................... 42 Table 35. Pacific Cod Harvest Volume for Federal and State Fisheries (mt), 2010-2014 ................................................................ 43 Table 36. First Wholesale Value, Alaska Pacific Cod, $Millions ....................................................................................................... 44 Table 37. Alaska Pacific Cod Production Volume and First Wholesale Value, by Region, 2014 ...................................................... 46 Table 38. Common Pacific Cod Products, Alaska Production, and Recovery Rates, 2014 .............................................................. 47 Table 39. Sales of H&G Alaska Pacific Cod to Key Markets (mt), 2010-2014 .................................................................................. 51 Table 40. Sales of Alaska Pacific Cod Fillets to Key Markets (mt), 2010-2014 ................................................................................ 51 Table 41. Total Cod Imports into U.S. Market, Volume and Value, 2010-2014 .............................................................................. 52 Table 42. Total Imports and Price/kg for Cod Fillets into the U.S. Market, 2012-2014 .................................................................. 52 Table 43. Primary Export Markets for Chinese Twice-Frozen Cod Fillets (mt), 2012-2014 ............................................................. 53 Table 44. Alaska Pacific Cod Export Volume to Major Asian Markets (mt), 2010-2014 .................................................................. 53 Table 45. European Imports of Cod Fillets from Major Producers (mt), 2012-2014 ....................................................................... 54 Table 46. Major Cod Producing Nations (Thousands mt), 2012-2014 ............................................................................................ 55 Table 47. Summary Profile of Yellowfin Sole Wholesale Production and Markets, 2014 ............................................................... 57 Table 48. Yellowfin Sole Harvest Volume in Federal Fisheries (mt), 2010-2014 ............................................................................. 58 Table 49. First Wholesale Value of Alaska Yellowfin Sole, in $Millions ........................................................................................... 59 Table 50. Summary Profile of Rock Sole Wholesale Production and Markets, 2014 ...................................................................... 60 Table 51. Rock Sole Harvest Volume in Federal Fisheries (mt), 2010-2014 .................................................................................... 61 Table 52. Alaska Rock Sole Production Volume and Value, 2014 ................................................................................................... 62

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • vi

Table 53. U.S. Yellowfin Sole Exports by Major Country (mt), 2013-2014 ...................................................................................... 64 Table 54. U.S. Rock Sole Exports by Major Country (mt), 2013-2014 ............................................................................................. 64 Table 55. China Flatfish Exports, by Value and Volume, 2012-2014 ............................................................................................... 64 Table 56. U.S. Rock Sole Exports to Japan (mt), 2010-2014 ............................................................................................................ 65 Table 57. Summary Profile of Atka Mackerel Wholesale Production and Markets, 2014 .............................................................. 69 Table 58. Atka Mackerel Harvest Volume in Federal Fisheries (mt), 2010-2014 ............................................................................ 70 Table 59. Atka Mackerel TACs in All Federal Fisheries (mt), 2010-2016 ......................................................................................... 71 Table 60. First Wholesale Value of Atka Mackerel, in $Millions, 2005-2014 .................................................................................. 72 Table 61. Alaska Atka Mackerel Exports by Major Country (mt), 2010-2014 ................................................................................. 72 Table 62. Summary Profile of Pacific Ocean Perch Wholesale Production and Markets, 2014 ...................................................... 75 Table 63. Pacific Ocean Perch Harvest Volume in Federal Fisheries (mt), 2010-2014 .................................................................... 76 Table 64. Pacific Ocean Perch TACs in All Alaska Federal Fisheries (mt), 2012-2016 ..................................................................... 76 Table 65. First Wholesale Value of Alaska Rockfish Species, in $Millions, 2005-2014 .................................................................... 78 Table 66. Alaska Rockfish Exports by Major Country (mt), 2014 .................................................................................................... 79 Table 67. Japan Imports of Rockfish by Major Trading Partner (mt), 2013 and 2014..................................................................... 80 Table 68. Summary Profile of Sablefish Wholesale Production and Markets, 2014 ....................................................................... 81 Table 69. Sablefish Harvest Volume for Federal and State Fisheries (mt), 2010-2014 ................................................................... 82 Table 70. Common Sablefish Products, 2014 Alaska Production Volume, and Recovery Rates (Pct.) ............................................ 83 Table 71. First Wholesale Value, Alaska Sablefish, $Millions .......................................................................................................... 84 Table 72. Alaska Sablefish First Wholesale Volume and Value by Top Ports, 2014 ........................................................................ 86 Table 73. U.S. Sablefish Exports to Global Markets, 2014 .............................................................................................................. 86 Table 74. Japan Frozen H&G Sablefish Imports, by Major Trade Partner, 2009-2014 .................................................................... 87 Table 75. Estimated U.S. Sablefish Market Supply (mt), 2010-2014 ............................................................................................... 88 Table 76. Summary Profile of Pacific Halibut Wholesale Production, 2014 .................................................................................... 90 Table 77. Alaska Commercial Halibut Landings, in Metrics Tons, 2010-2014 ................................................................................. 91 Table 78. Common Halibut Products: 2014 Alaska Production Volume and Recovery Rates (Pct.) ............................................... 92 Table 79. Alaska Halibut First Wholesale Volume and Value by Top Ports/Regions, 2014 ............................................................. 94 Table 80. Estimated U.S. Halibut Market Supply (mt), 2010-2014 ................................................................................................. 96 Table 81. Summary Profile of Ancillary Products Wholesale Production and Markets, 2014......................................................... 98 Table 82. First Wholesale Value and Ancillary Products as Percent of Total Wholesale Value, 2005-2014 ................................... 99 Table 83. Alaska Groundfish Fish Meal First Wholesale Value, in $Millions, 2005-2014 .............................................................. 102 Table 84. First Wholesale Value per Metric Ton of Alaska Fish Meal Products, by Species, 2014 ................................................ 102 Table 85. Exports of Alaska Fish Meal, 2010-2014 ........................................................................................................................ 103 Table 86. Total First Wholesale Value of Alaska Groundfish Oil Production, in $Millions, 2005-2014 ......................................... 105 Table 87. First Wholesale Value of Select Ancillary Products, in $Millions, 2010-2014 ................................................................ 107 Table 88. Summary Profile of Alaska Snow Crab Wholesale Production and Markets ................................................................. 109 Table 89. Alaska Snow Crab Harvest/TAC for Federal and State Fisheries, in Millions lb., 2011-2016 ......................................... 111 Table 90. Alaska Snow Crab Volume and Wholesale Value by Region, 2014 ................................................................................ 113 Table 91. Volume and Wholesale Value of Snow Crab Products, 2014 ........................................................................................ 114 Table 92. First Wholesale Value of Snow Crab Sections, in $Millions, 2005-2014 ........................................................................ 115 Table 93. Estimated Sales of Alaska Snow Crab to Key Markets, in Millions lb., 2010-2014 ........................................................ 115 Table 94. Estimated U.S. Snow Crab Market Supply, in Millions lb., 2010-2014 .......................................................................... 116 Table 95. Japanese Imports of Snow Crab, 2010-2014 ................................................................................................................. 117 Table 96. Summary Profile of Alaska King Crab Wholesale Production and Markets, 2014 ......................................................... 120 Table 97. Alaska King Crab Harvest/TAC in Federal and State Fisheries, in Millions lb., 2010-2015 ............................................. 122 Table 98. King Crab Section Sizing ................................................................................................................................................ 122 Table 99. Alaska King Crab First Wholesale Volume and Value by Region, 2014 .......................................................................... 124 Table 100. Production Volume and First Wholesale Value of King Crab Products, 2014 .............................................................. 125 Table 101. First Wholesale Value of Alaska King Crab Sections, in $Millions, 2004-2014 ............................................................ 125 Table 102. Estimated Sales of Alaska King Crab to Key Markets, in Millions lb., 2010-2014 ........................................................ 126 Table 103. Estimated U.S. King Crab Market Supply, in Millions lb., 2010-2014 .......................................................................... 127 Table 104. Japanese Imports of King Crab, 2010-2014 ................................................................................................................. 128

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • vii

List of Figures Executive Summary Figures

Executive Summary Figure 1. Composition of Total First Wholesale Volume and Value for Alaska Seafood, by Species, 2014 ...... ix Executive Summary Figure 2. Total First Wholesale Volume and Value of Alaska Groundfish and Crab, by Product Type, 2014 ..... x Executive Summary Figure 3. First Wholesale Volume and Value of Alaska Groundfish and Crab Species, 2010-2014 ................... x Figures Figure 1. Total Farmed Tilapia and Pangasius Production (mt), 1990-2013 ..................................................................................... 4 Figure 2. Pollock Harvest Volume in Alaska (mt), 1977-2014 ........................................................................................................... 8 Figure 3. First Wholesale Volume and Value for Alaska Pollock, 1992-2014 .................................................................................... 9 Figure 4. Alaska Pollock First Wholesale Production Volume and Value, by Product Type, 2014 .................................................. 10 Figure 5. Alaska Pollock Fillet Supply Chain .................................................................................................................................... 15 Figure 6. First Wholesale Volume and Value for Alaska Pollock Fillets, 2005-2014 ........................................................................ 16 Figure 7. Alaska Pollock Fillets Volume and Value by Processing Sector, 2005-2014 ..................................................................... 17 Figure 8. Exports of Alaska Pollock Fillets to Major European Markets, 2010-2014 ....................................................................... 19 Figure 9. Alaska Pollock Surimi Supply Chain .................................................................................................................................. 24 Figure 10. First Wholesale Volume and Value for Alaska Pollock Surimi, 2005-2014 ..................................................................... 25 Figure 11. Alaska Pollock Surimi First Wholesale Volume and Value by Processing Sector, 2004-2014. ........................................ 25 Figure 12. Alaska Pollock Roe Supply Chain .................................................................................................................................... 31 Figure 13. First Wholesale Volume and Value for Alaska Pollock Roe, 2005-2014 ......................................................................... 31 Figure 14. Alaska Pollock First Wholesale Value and Roe as Percent of Total Value, 1992-2014 ................................................... 32 Figure 15. Alaska Pollock Roe Production and Harvest Volume (mt), 2010-2014 .......................................................................... 32 Figure 16. Alaska Pollock Head & Gut Supply Chain ....................................................................................................................... 36 Figure 17. First Wholesale Volume and Value for Frozen H&G Alaska Pollock, 2005-2014 ............................................................ 36 Figure 18. Head and Gut Production Share, 2003-2014 ................................................................................................................. 37 Figure 19. Alaska Pollock H&G Volume and Value, by Processing Sector, 2004-2014 .................................................................... 37 Figure 20. Global Harvest Volume of Alaska Pollock (mt), 1977-2014 ............................................................................................ 40 Figure 21. Pacific Cod Harvest Volume in Alaska (mt), 1977-2014 ................................................................................................. 43 Figure 22. Share of Alaska Pacific Cod Harvest by Gear Type, 2014 ............................................................................................... 44 Figure 23. First Wholesale Volume and Value for Alaska Pacific Cod, 2005-2014 .......................................................................... 44 Figure 24. Volume and Value of Pacific Cod Wholesale Production in Alaska, by Product Type, 2014 .......................................... 45 Figure 25. Pacific Cod H&G Production in Alaska, by Volume and Value, 1992-2014 .................................................................... 46 Figure 26. Alaska Pacific Cod Supply Chain (Meat Products Only) .................................................................................................. 47 Figure 27. Alaska Pacific Cod H&G Wholesale Production and Exports, 2007-2014 ....................................................................... 48 Figure 28. H&G as Percent of Total Alaska Pacific Cod Exports, 2007-2014 ................................................................................... 49 Figure 29. First Wholesale and Export Values for Alaska Pacific Cod Fillets, in $Thousands, 2010-2014 ....................................... 50 Figure 30. Total Alaska Pacific Cod Exports, by Volume and Value, 2007-2014.............................................................................. 50 Figure 31. U.S. Imports of Cod Fillets from Major Trading Partners (mt), 2012-2014 .................................................................... 52 Figure 32. Global Supply of Pacific Cod (mt), 1950-2013 ................................................................................................................ 55 Figure 33. Global Supply of Pacific and Atlantic Cod (mt), 1950-2013 ............................................................................................ 56 Figure 34. Comparison of Shatterpack Cod Value between Alaska and Competitors, 2005-2014 ................................................. 56 Figure 35. Yellowfin Sole Harvest Volume in Alaska (mt), 1983-2014 ............................................................................................ 58 Figure 36. First Wholesale Volume and Value of Alaska Yellowfin Sole, 2010-2014 ...................................................................... 59 Figure 37. Rock Sole Harvest Volume in Alaska (mt), 1985-2014 ................................................................................................... 61 Figure 38. Alaska Rock Sole Supply Chain ....................................................................................................................................... 62 Figure 39. First Wholesale Volume and Value for Alaska Rock Sole, 2010-2014 ............................................................................ 63 Figure 40. Share of U.S. Imports of Sole, by Region/Country, 2014 ............................................................................................... 65 Figure 41. Cost/Value Added to Sole by Chinese Secondary Processors, 2007-2015 ..................................................................... 66 Figure 42. Composition of Alaska Flatfish Production, by Species, by First Wholesale Volume, 2010-2014 .................................. 67 Figure 43. Average Composition of Global Production of Flatfish, by Species, by Volume, 2010-2013 ......................................... 68 Figure 44. Global Flatfish Supply and Alaska Harvest of Yellowfin and Rock Sole, 1975-2013 ....................................................... 68 Figure 45. Atka Mackerel Harvest Volume in Alaska (mt), 1986-2014............................................................................................ 70 Figure 46. First Wholesale Volume and Value for Atka Mackerel, 2005-2014 ................................................................................ 72 Figure 47. Global Atka Mackerel Harvest (mt), 1980-2013 ............................................................................................................. 74 Figure 48. Pacific Ocean Perch Harvest Volume in Alaska (mt), 1977-2014 ................................................................................... 75 Figure 49. First Wholesale Volume and Value for Alaska Rockfish Species, 2005-2014 ................................................................. 78 Figure 50. Global Rockfish (Sebastes spp.) Harvest (mt), 1980-2013 ............................................................................................. 80 Figure 51. Alaska Sablefish Supply Chain ........................................................................................................................................ 84 Figure 52. First Wholesale Volume and Value of Alaska Sablefish, 2005-2014............................................................................... 84 Figure 53. Alaska Wholesale and Ex-Vessel Prices per Pound, 1995-2014 ..................................................................................... 85

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • viii

Figure 54. U.S. Exports of Sablefish by Top 5 Asia Countries (excluding Japan), in $Thousands, 2009-2014 ................................. 88 Figure 55. Global Supply of Sablefish (mt), 2003-2014 ................................................................................................................... 89 Figure 56. Alaska Halibut Harvests/TACs (mt), 1950-2014 ............................................................................................................. 91 Figure 57. Alaska Halibut Supply Chain ........................................................................................................................................... 92 Figure 58. First Wholesale Volume and Value of Pacific Halibut in Alaska, 1985-2014 .................................................................. 93 Figure 59. Alaska Halibut First Wholesale and Ex-Vessel Price per Pound, 1995-2014 ................................................................. 94 Figure 60. North American Halibut Supply and Wholesale Price, 2005-2015 ................................................................................. 95 Figure 61. Global Supply of Pacific Halibut (mt), 1950-2013 .......................................................................................................... 96 Figure 62. Pacific and Atlantic Halibut Harvest Volume (mt), 2004-2013 ....................................................................................... 97 Figure 63. First Wholesale Volume and Value of Ancillary Products from Alaska Groundfish, 2005-2014..................................... 99 Figure 64. Alaska Ancillary Product Wholesale Production Value, by Key Species, 2005-2014 ...................................................... 99 Figure 65. Alaska Ancillary Product First Wholesale Value and Volume, by Key Groundfish Species, 2014 ................................. 100 Figure 66. Alaska Groundfish Ancillary Product First Wholesale Value, by Product Type, 2005-2014 ......................................... 100 Figure 67. Alaska Ancillary Product First Wholesale Value and Volume, by Product Type, 2014 ................................................. 101 Figure 68. Alaska Fish Meal Production and Value, 2005-2014 .................................................................................................... 102 Figure 69. Exports of Alaska Fish Meal, 2010-2014 ...................................................................................................................... 103 Figure 70. First Wholesale Value and Volume of Alaska Groundfish Fish Oil Production, 2005-2014 .......................................... 105 Figure 71. Exports of Alaska Fish Oil, 2010-2014 .......................................................................................................................... 106 Figure 72. First Wholesale Value of Other Ancillary Products from Alaska Groundfish, 2005-2014............................................. 107 Figure 73. Annual Snow and King Crab Harvests in Alaska, in Millions lb., 1967-2014 ................................................................. 110 Figure 74. Alaska Snow Crab Supply Chain ................................................................................................................................... 112 Figure 75. First Wholesale Production Volume of Alaska Snow Crab, in Millions lb., 2005-2014 ................................................. 113 Figure 76. First Wholesale Production Value of Alaska Snow Crab, in $Millions, 2005-2014 ....................................................... 114 Figure 77. First Wholesale Value and Volume of Snow Crab Sections, 2005-2014 ....................................................................... 115 Figure 78. Estimated Source of Snow Crab Consumed in the United States, 2014 ...................................................................... 116 Figure 79. U.S. Snow Crab Exports to China, 2007-2014............................................................................................................... 117 Figure 80. Global Harvest Volume of Snow Crab, in Millions lb., 2005-2013 ................................................................................ 119 Figure 81. Global Snow Crab Harvest by Country, 2013 ............................................................................................................... 119 Figure 82. Annual King Crab Landings in Alaska, in Millions lb., 1950-2014 ................................................................................. 121 Figure 83. Alaska King Crab Supply Chain ..................................................................................................................................... 123 Figure 84. First Wholesale Production Volume Alaska King Crab, in Millions lb., 2004-2014 ....................................................... 124 Figure 85. First Wholesale Value of Alaska King Crab, in $Millions, 2004-2014 ........................................................................... 124 Figure 86. First Wholesale Volume and Value of King Crab Sections, 2004-2014 ......................................................................... 125 Figure 87. Estimated Source of King Crab Consumed in the United States, 2014 ........................................................................ 127 Figure 88. U.S. Red King Crab Exports to Japan, 2005-2014 ......................................................................................................... 128 Figure 89. Estimated Global Supply of King Crab, in Millions lb., 2004-2013 ............................................................................... 129 Figure 90. Estimated Proportions of Global King Crab Supply, 2013 ............................................................................................ 130

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • ix

Pollock45%

Pacific Cod12%

Salmon18%

Halibut/ Sablefish

1%

Crab2%

Flatfish14%

Other8%

Volume

Executive Summary

This comprehensive series of wholesale market profiles examines federally managed groundfish and crab species caught in Alaska commercial fisheries. Each profile summarizes the fishery and provides in-depth information of wholesale production volume and value, product mix, supply chain, competing supply, and key markets.

Alaska’s commercial fisheries are the most productive in the Nation, accounting for 60 percent of total 2014 U.S. commercial fishery harvest volume. In 2014, first wholesale production of 1.28 million metric tons of all Alaska species combined was valued at $4.27 billion (Executive Summary Figure 1).1 The majority of Alaska seafood is exported, with overall exports estimated at 1.12 million metric tons valued at $3.28 billion.2 Alaska groundfish and crab species covered in this report accounted for 78 percent of Alaska’s total wholesale production volume in 2014, and 65 percent of the first wholesale value. Alaska pollock is the most plentiful and most valuable species, accounting for 45 percent of total production volume and 33 percent of the total production value.

Executive Summary Figure 1. Composition of Total First Wholesale Volume and Value for Alaska Seafood, by Species, 2014

In 2014, the Bering Sea/Aleutian Islands (BSAI) region produced 86 percent of total wholesale groundfish production volume and 83 percent of the value. The Gulf of Alaska (GOA) and Southeast Alaska region

1 See glossary defining first wholesale volume/value and other terms commonly used in this report. 2 Here, export volume (shipping weight) includes the weight of packaging materials, while production volume (net weight) excludes the weight of packaging materials). Export value is the value upon exiting the country, including costs/profits associated with shipping. First wholesale value is generally equal to the value of product as it leaves Alaska.

Pollock33%

Pacific Cod11%

Salmon33%

Halibut/Sablefish

5% Crab9%

Flatfish5%

Other5%

Value 1.28 million mt $4.27 billion

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • x

H&G/Whole Fish42%

Surimi18%

Fillets20%

Roe3%

Ancillary/Other14%

Crab Sections

3%

Volume

produced the remainder: 13 percent of total wholesale groundfish production volume and 16 percent of the volume.

The majority of these products are considered intermediate products, which undergo secondary processing outside Alaska to create finished products for retail and food service buyers around the world. Executive Summary Figure 2 summarizes first wholesale production volume and value of key groundfish and crab products by general product type.

Executive Summary Figure 2. Total First Wholesale Volume and Value of Alaska Groundfish and Crab, by Product Type, 2014

Executive Summary Figure 3. First Wholesale Volume and Value of Alaska Groundfish and Crab Species, 2010-2014

Source: AKFIN.

The total value of Alaska groundfish and crab has remained steady over the last 5 years (2010-2014, see Executive Summary Figure 3). Value per metric ton for each species category are shown below in Executive Summary Table 1. Changes in value are the result of numerous factors, summarized on page xii and examined in greater detail in this report.

1 million mt $2.79 billion

$2,000

$2,200

$2,400

$2,600

$2,800

$3,000

$3,200

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2010 2011 2012 2013 2014

Valu

e ($

mill

ions

)

Volu

me

(mt)

Volume (in mt) Value (in $millions)

H&G/Whole Fish34%

Surimi15%

Fillets25%

Roe6%

Ancillary/Other7%

Crab Sections

13%

Value

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • xi

Executive Summary Table 1. Average First Wholesale Value per Metric Ton, 2010-2014

2010 2011 2012 2013 2014 Pct. Change in 2014 from Prior 4-yr. Avg.

Alaska Pollock $2,906 $2,772 $2,874 $2,443 $2,425 -12%

Pacific Cod 3,042 3,484 3,154 2,735 3,053 -2%

Yellowfin Sole 1,154 1,400 1,387 1,287 1,043 -20%

Rock Sole 1,368 1,705 1,990 1,333 1,290 -19%

Pacific Halibut 14,659 17,693 15,508 14,419 17,194 10%

Sablefish 15,247 19,220 14,316 12,250 14,776 -3%

Pacific Ocean Perch 2,459 3,560 3,137 2,259 2,578 -10%

Atka Mackerel 1,861 2,292 2,480 2,705 3,032 30%

Snow Crab 7,277 12,054 10,559 11,052 11,650 14%

King Crab 25,273 32,573 27,144 24,370 23,968 -12%

Source: AKFIN.

Key Markets for Alaska Groundfish and Crab The United States, Europe, and Japan are the largest markets for finished products derived from Alaska groundfish and crab, typically accounting for more than 80 percent of first wholesale value. Approximately one-third of the Alaska groundfish and crab production volume is reprocessed in China (Executive Summary Table 2). After secondary processing in China a large share of these products are re-exported to markets in Europe, the United States, and Japan. A significant amount of product exported to South Korea is held in cold storage facilities or reprocessed before re-exported to Japan and Europe.

Executive Summary Table 2. Primary Sales of First Wholesale Alaska Groundfish and Crab Products by Market, Estimated Annual Average Volume and Value, 2010-2014

Market First Wholesale Value ($millions)

Est. Pct. of Market Share (Value) Sales Volume (mt)

Est. Pct. of Market Share (Volume)

China* $615 22% 281,533 33%

Japan 454 16% 144,936 17%

Europe 495 17% 168,026 19%

South Korea* 313 11% 108,432 13%

Other Countries 220 8% 60,030 7%

Export Markets Total $2,097 74% 762,957 89%

Est. Domestic Market $736 26% 99,779 11%

*Primarily re-export markets.Source: AKFIN, ADF&G (COAR), ASMI Alaska Seafood Export Database, and McDowell Group estimates.

Species profiled in this report represent a significant proportion of the global seafood trade between nations; however, most species face market competition from fisheries in other countries. Executive Summary Table 3 summarizes first wholesale production volume and value of Alaska groundfish and crab products, the percent of global harvest volume, and key initial markets for each species.

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • xii

Executive Summary Table 3. Alaska Groundfish and Crab Production and Market Summary, 2014

Species/Product First Wholesale Value ($millions)

Alaska Production Volume (mt)

Pct. of Global Harvest (2013) ---------- Key Markets ----------

Alaska Pollock $1,407 580,120 43% Japan Europe U.S.

Pacific Cod $472 154,580 18% China* Europe U.S.

Flatfish $209 172,510 32% China* U.S. Europe

Pacific Halibut $109 6,160 57% U.S. Canada --

Sablefish $99 6,700 78% Japan China U.S.

Atka Mackerel $63 32,280 19% Japan China* Korea

Rockfish $81 20,880 28% China* Japan U.S.

King Crab $117 4,870 15% U.S. Japan --

Snow Crab $233 20,020 15% U.S. Japan China

*Denotes re-export market. Source: AKFIN, ADF&G (COAR), and McDowell Group estimates.

Current Market Issues The value of Alaska seafood is affected by a range of market forces. Species profiles contain detailed information about how these forces impact the value of Alaska production; noteworthy market factors are summarized by species below.

ALASKA POLLOCK • Marine Stewardship Council (MSC)

certification of Russia’s largest pollock fishery has depressed prices for pollock fillets in Europe, a market where certification is required by many large retailers.

• Increasing production volume and changing consumer preferences in Japan have reduced the value of pollock roe — an important high-margin product for Alaska pollock producers.

• Prices for Alaska pollock surimi blocks are trending up, due to lower production of competing products.

PACIFIC COD • Traditionally, markets in Europe substituted Pacific cod for declining Atlantic cod stocks. In recent

years, Atlantic cod production has rebounded. Larger supplies of competing product, a stronger U.S. dollar, and protective tariffs in the European Union (EU) has reduced the value of Pacific cod in recent years.

HALIBUT AND SABLEFISH • Halibut and sablefish processors have noted that moving inventory is not a problem due to high

demand. Prices have risen as harvest has been reduced for both fish.

• Prices for halibut and sablefish peaked in 2011, but remain high. Sablefish, traditionally sold almost exclusively to Japanese buyers, has seen increased demand from other markets.

Photo Courtesy of ASMI.

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • xiii

FLATFISH • Wholesale prices for Alaska flatfish products have been reduced as the value of the euro has fallen

and secondary processing costs have increased.

• Global flatfish and other competing whitefish production is up in recent years, putting downward pressure on prices for Alaska sole.

PACIFIC OCEAN PERCH AND ATKA MACKEREL • Declining harvests of Atka mackerel in Japan have increased prices for Alaska product.

• Reduced value of Asian currencies has decreased seafood imported for reprocessing, an important market for Pacific ocean perch and other rockfish species harvested in Alaska.

CRAB • The largest impact on market demand for crab from Alaska has been linked to changes in illegal,

unreported, and unregulated (IUU) fishing from Russia, which has historically produced a large volume of illegal crab products. King crab prices are most responsive to total Russian production volume, but snow crab prices are also affected.

• Increased king crab harvests in Argentina and Chile are adding more production to global supply, impacting the market value of Alaska’s king crab harvest.

ANCILLARY PRODUCTS • The global aquaculture industry is increasingly using plant-based feeds instead of higher priced fish

meals and oils. However, prices are expected to remain strong as Alaska’s groundfish meal is a unique product in high demand for eel and turtle farming.

• Increased use of fish oil for human consumption helps drive strong prices for fish oil. Strong demand, coupled with new product development by Alaska processors, is expected to result in increased sales of nutritional supplements made from Alaska groundfish.

Implication of Currency Exchange Rates In addition to the market issues described above, prices for Alaska groundfish and crab products have been negatively impacted by a stronger U.S. dollar in recent years. A stronger dollar, relative to the currencies of key export markets and competing suppliers, generally makes Alaska seafood more expensive and competing product less expensive from foreign consumers’ point of view. Over the past 5 years, approximately 89 percent of the state’s groundfish and crab production was sold to export markets – primarily in Europe and Japan.

Executive Summary Table 4 summarizes changes in foreign currency rates for key buyers and major competitors, versus the U.S. dollar, between 2013 and 2015. Exchange rates vary from year to year, but movements of this magnitude are unusual.

Executive Summary Table 4. Changes in Relevant Currency Exchange Rates, October 2013 vs. October 2015

Country/Market Currency Primary Role Pct. Change vs. U.S. Dollar

European Union Euro Buyer -17.6%

Japan Yen Buyer -18.6%

Canada Canadian Dollar Buyer and Competitor -20.8%

Russia Ruble Competitor -49.2%

Norway Kroner Competitor -28.1%

U.S. Dollar Index (value relative to a basket of foreign currencies) +20.9%

Source: OANDA Average Foreign Exchange Rates and Investing.com DXY historical data.

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • xiv

Glossary of Terms and Abbreviations

Abbreviations and Acronyms ADF&G Alaska Department of Fish and Game AKFIN Alaska Fisheries Information Network AFA American Fisheries Act BSAI Bering Sea/Aleutian Islands CDQ Community Development Quota COAR Commercial Operators Annual Report (published by Alaska Dept. of Fish and Game) DFO Canadian Department of Fisheries and Oceans EEZ Exclusive Economic Zone FAO United Nations Fisheries and Aquaculture Organization GOA Gulf of Alaska H&G Headed and gutted IFQ Individual Fishing Quota IPHC International Pacific Halibut Commission IQF Individual Quick Frozen mt Metric tons MSA Magnuson-Stevens Act of 1976 MSC Marine Stewardship Council NMFS National Marine Fisheries Service NPFMC North Pacific Fishery Management Council PACFIN Pacific Fisheries Information Network TAC Total Allowable Catch

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • xv

Glossary of Terms Demersal Fish Marine fishes that live near the bottom of the ocean, also known as

groundfish.

Exclusive Economic Zone Ocean area that extends past 3 nautical off the coast of Alaska to 200 miles off the coast of the United States, where exclusive federal fishery management occurs.

Export Value The free alongside (FOB) value of an export product as it leaves a U.S. port, including all transport/etc. costs needed to create and move the product to the port of exit.

Export Volume The weight of exported product in “product weight” terms, generally including the weight of all product and packaging, as it leaves a U.S. port.

Ex-Vessel Value/Price The amount paid to fishermen by a processor for harvested seafood, typically per pound round weight.

Fillet Blocks Frozen product that is uniformly skinless, boneless, or minced fish which is quick frozen in a plate freezer intended for further processing.

First Wholesale Value The value of a processed product when sold by a processor to an entity outside of their affiliate network. Typically refers to the value of product as it leaves Alaska.

First Wholesale Volume The weight of processed or packaged product, in net weight terms, produced for sale to another buyer outside of the primary processor’s affiliate network. Typically refers to the volume of processed product leaving Alaska.

Fixed Gear Refers to pot/trap or longline commercial fishing gear.

Landings The amount of seafood harvested by fishermen.

Net Weight A term commonly used to measure halibut harvest volume. Whereas harvests of most other species are counted in round weight terms, halibut harvests are tallied in net weight, which is equal to an average headed and gutted weight of the fish.

Production Volume/Value The term “production” is occasionally used as short-hand for first wholesale volume and value in this report.

Round Weight The weight of a whole seafood species as it is delivered to the processor in an unprocessed and uncut state.

Shatterpack Fillets Frozen fillets separate by a sheet that can be easily separated by dropping or shattering the carton.

Stock A species that can be managed as a single unit.

Surimi Frozen, minced seafood that is blended with other ingredients to create molded products, such as imitation crab meat.

Total Allowable Catch The total amount of a target species that can be harvested in a given time period.

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • xvi

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • 1

Global Groundfish Production and Key Markets

This chapter provides a broad overview of competing supply and key markets related to primary Alaska groundfish species and/or products. Each profile in this series contains detailed information about markets and competing supply for individual species or products, while this chapter contextualizes Alaska groundfish production and versus the rest of the world.

Alaska Groundfish Production and Market Summary Table 1 summarizes production volume, value, key markets, and the percentage of global production for Alaska groundfish species and products. Overall, the largest markets for Alaska groundfish are Europe, Japan, and the United States. Although Alaska accounts for a significant share of production for many groundfish species, the state produced only 2.9 percent of global whitefish and other marine fish harvests in 2013.

Table 1. Alaska Groundfish Production and Market Summary, 2014

Species/Product First Wholesale Value ($millions)

Alaska Production (mt)

Pct. of Global Production (2013) ---------- Key Markets ----------

Pollock – Fillets $557 183,960 30% Europe U.S. Brazil

Pollock – Surimi 441 183,640 23% Japan Europe Korea

Pollock – Roe 148 24,120 N/A Japan Korea --

Pacific Cod 472 154,580 18% China* Europe U.S.

Flatfish 209 172,510 32% China* U.S. Europe

Pacific Halibut 109 6,160 57% U.S. Canada --

Sablefish 99 6,700 78% Japan China U.S.

Rockfish 81 32,280 28% China* Japan U.S.

Atka Mackerel 63 20,880 19% Japan China* Korea

*Denotes re-export market.Note: Alaska harvest/production volume from 2013 was compared to 2013 global harvest/production estimates. Global harvest/production data for 2014 is not yet available. Alaska production figures are rounded. Source: AKFIN, ADF&G (COAR), and McDowell Group estimates.

Global Whitefish and Other Marine Fish Production Whitefish generally refers to cod, pollock, haddock, hake, whiting, and benthic flatfish species, such as sole, plaice, flounder, and halibut. These species - primarily caught in wild fisheries - also compete in global seafood markets with notable aquaculture species such as tilapia and pangasius. Depending on the market, the scope of these whitefish species may be narrowed or supplemented with other local varieties. Although global fisheries harvest significant volumes of whitefish, there are many other marine species with significant harvest volumes. For the purposes of this section, these species are generally referred to as “other marine fish species.”

Capture fisheries and aquaculture production yielded 74 million metric tons of whitefish and other marine fish species in 2013 (round weight terms). The majority of production is used for meat, but fish meal, fish oil, and surimi production also utilize significant volumes of wild marine fish species. Fish meal and fish oil production required 16.3 million metric tons of wild capture fish species in 2012; however, about 35 percent of fish meal production was created using fish residues (ancillary products and waste rather than the whole fish).1

1 (Green, Stahl, Vaughn, Carroll, & Baldwin, 2014)

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • 2

Table 2. Global Whitefish and Other Marine Fish Species Production (mt), 2013 Species Harvest Volume (mt) Primary Uses

Alaska Pollock 3,239,719 Meat, Surimi, Meal/Oil

Hakes, Hoki, and Whiting 2,209,131 Meat, Surimi, Meal/Oil

Cod and Haddock 2,169,226 Meat

Other Flatfish (Sole/Flounder/etc.) 882,063 Meat

Saithe 318,371 Meat

Other Whitefish 221,986 -

Halibuts and Turbots 157,824 Meat

Total Wild Whitefish (Capture Fisheries) 9,198,320 -

Anchovies, Shads, and Menhaden 9,411,729 Meal/Oil

Herring and Sardines 8,056,155 Meal/Oil, Meat, Roe, and Bait

Mackerel and Saury 5,716,215 Meat and Meal/Oil

Jacks, Scads, and Carangids 2,582,584 Meat and Meal/Oil

Other Coastal Species 2,556,069 -

Eels, Congers, and Hairtails 2,439,811 Meat and Surimi

Croakers and Drums 1,761,530 Meat and Bait

Breams, Lizardfish, and Pomfrets 1,539,437 Surimi and Meat

Mullets and Goatfish 778,322 Meat

Capelin 758,735 Roe and Meal/Oil

Other Demersal Species 590,858 -

Other Pelagic Species 529,231 -

Groupers and Seabass 317,542 Meat

Snappers 264,286 Meat

Rockfish 213,337 Meat

Atka Mackerels 130,448 Meat

Mahi-mahi (Dolphin) 102,986 Meat

Monkfish 92,768 Meat

Sablefish and Patagonian Toothfish 46,508 Meat

Other Misc. Species - Capture Fisheries 20,422,968 -

Total Other Marine Species 58,311,519 -

Tilapias (Farmed) 4,823,312 Meat

Pangasius (Farmed) 1,671,825 Meat

Total - Tilapias and Pangasius 6,495,137 -

Total Whitefish and Other Marine Species 74,004,976 -

Total Alaska Groundfish Harvest (2013)* 2,169,200 Pct of Total: 2.9%

*Includes herring harvests, to make the figure more comparable to the broader range of groundfish included in the table. Note: Red-fleshed fish species (e.g. tuna) and diadromous fish (e.g. salmon) are not included in these figures. Source: FAO, compiled by McDowell Group.

The vast majority of fish shown in Table 2 can be processed into white fillets, and could represent a substitute for key Alaska groundfish species on a general level. However, culinary traditions and local tastes tend to limit the number of species palatable to individual markets. For example, cod is a staple fish in Europe but virtually non-existent in Southeast Asia, where it would be more common to find carp or milkfish

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • 3

filling the whitefish role. Cost is always a primary concern as well. Consumers generally will not substitute imported whitefish species for less expensive and traditionally palatable domestic species. There are also significant differences in the way different cultures prepare whitefish. Countries in emerging markets are generally more likely to cook fish whole while developed countries tend to use fillets or steaks. Differences in availability, price, taste, and fish size limit actual consumer substitution, despite the fact that most species listed in Table 2 could generally be categorized as white-fleshed fish.

Alaska’s Position in the Global Whitefish Market Alaska accounted for 2.9 percent of total global whitefish and other marine fish production in 2013. However, globally wild whitefish species (which constitute the majority of Alaska’s groundfish harvest) only accounted for 12.4 percent of total production in 2013. Alaska plays a bigger role in global production if the whitefish scope is narrowed to wild and farmed whitefish species (i.e. tilapias and pangasius). In 2013, Alaska production accounted for 13.5 percent of global wild and farmed whitefish production, a substantial figure in a global context.2 This is a notable comparison because wild whitefish species, such as cod, pollock, and sole, as well as farmed tilapias and pangasius, are more likely to be exported than other wild fish species, which are mainly sold into domestic markets or transformed into fish meal, fish oil, or surimi.

Alaska’s commercial fisheries produce larger harvests than every other U.S. state combined and 80 percent of Alaska’s harvest volume came from high-volume whitefish fisheries (pollock, cod, and flatfish) in 2013. Despite the impressive scale of its high-volume whitefish fisheries, Alaska is only a fractional part of global whitefish production. As a result, Alaska’s groundfish industry is a usually a price taker where the value of its cod, pollock, and flatfish are impacted by competing suppliers and competing whitefish species. Russia (cod/pollock/flatfish), China (tilapia), Norway (cod), Japan (pollock/cod), New Zealand (hoki), and Vietnam (pangasius) are the biggest competitors for Alaska’s groundfish industry, in terms of high-volume whitefish species.

Low volume Alaska whitefish species like halibut, sablefish, rockfish, and Atka mackerel have much more defined markets where Alaska is the primary export supplier and generally account for a larger percent of global supply in these niche markets. As a result, species substitution is less common in markets for these species and price is mostly a function of Alaska or local harvest volume.

Tradition, taste preferences, and familiarity are hurdles in developing new markets for Alaska groundfish species. However, culinary influences are blending and crossing borders faster than perhaps any other time in human history. Modern urban centers like Singapore, Sao Paulo, San Francisco, Sydney, Seoul provide a growing supply of unique seafood options. Expanding culinary options presents new marketing opportunities for Alaska’s seafood industry. Particularly since Alaska has a reputation for quality and a strong distribution network, having been in the business of exporting fish for decades. However, it may also present challenges in existing markets in years to come as consumers gain more exposure to seafood from other cultures.

Competition from Tilapia and Pangasius Tilapia and pangasius, also known as basa, swai, tra, or catfish have become dominant species many global seafood markets. Combined aquaculture production of the two species reached nearly 6.5 million metric tons in 2013 (Figure 1).

2 Whitefish in this comparison includes tilapia, pangasius, cod, haddock, pollock, hakes, hoki, whiting, flatfish, and other wild cod-like groundfish species.

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • 4

Tilapia production continues to grow rapidly and consistently. China (including Hong Kong and Taiwan) produced 1.73 million metric tons, accounting for 35 percent of total tilapia production, in 2013. Several other countries have established themselves as major producers, such as Egypt (16 percent), Indonesia (15 percent), and the Philippines (5 percent). Tilapia production in Indonesia, Bangladesh, Brazil, and Mexico is growing especially fast. The vast majority of tilapia product imported by the United States and Europe consists of frozen fillets from China.

Pangasius production flattened out in 2013 after increasing nearly 10-fold during the previous decade. Vietnam is by far the largest producer of pangasius products, accounting for 81 percent of all

production. Industry reports suggest Vietnamese production remained stunted in 2014 and 2015 as high feed costs, weak demand in major markets, and low prices have led to a reduction in the number of farms. Production and domestic market demand is increasing in other Southeast Asian countries, such as Indonesia.3

Figure 1. Total Farmed Tilapia and Pangasius Production (mt), 1990-2013

Source: FAO.

Tilapia and pangasius fillets are major whitefish imports in the United States and Europe. Sourced primarily from China and Vietnam, imported frozen fillets of these two fish were worth $1.6 billion in 2014. The United States is the primary market for tilapia while Europe, collectively, is a slightly larger pangasius market than the United States.

Demand for tilapia fillets is strong in the United States and Europe, as evidenced by rising volumes and rising import prices in 2014 (Table 3). Total U.S. and Europe import value of frozen tilapia fillets was up 8.6 percent while the average value/mt increased 6.8 percent to $4,935. Meanwhile, western market demand for pangasius appears to be waning despite flat to declining supply. The average import value/mt was up slightly, but import volumes of pangasius fell 7.2 percent in the United States and Europe (combined) in 2014.

Tilapia and pangasius are becoming popular seafood choices in markets outside of the United States and Europe. The fastest growing major markets are Brazil (pangasius, +100 percent growth in volume during 2014), Iran (tilapia, +284 percent), Mexico (tilapia, +5 percent), Thailand (pangasius, +19 percent), and

3 (FAO Globefish Market Reports, 2014-2015)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Volu

me

(mt)

Tilapias and Other Cichlids Pangasius

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • 5

Columbia (pangasius, +11 percent). India and Indonesia, with a combined population of approximately 1.5 billion people, are also developing domestic supplies of farmed tilapia and pangasius. In contrast to western markets, the amount of pangasius imported by developing markets grew faster than tilapia in 2014. Outside of Brazil, Alaska exports relatively little groundfish product to these tilapia/pangasius markets.

Table 3. Imports of Tilapia and Pangasius Products, United States and Europe vs. Other Markets, 2012-2014

2012 2013 2014 YOY Pct. Change

U.S. & Europe (Combined)

Import Value ($millions)

Tilapia – Frozen Fillets $803.9 $845.3 $918.0 8.6%

Tilapia – Frozen Fish 54.9 82.5 92.4 12.0%

Pangasisus – Frozen Fillets 778.0 717.4 694.3 -3.2%

Import Volume (mt)

Tilapia – Frozen Fillets 187,130 182,956 186,021 1.7%

Tilapia – Frozen Fish 29,796 41,776 40,674 -2.6%

Pangasisus – Frozen Fillets 260,126 267,260 248,078 -7.2%

Import Value/mt

Tilapia – Frozen Fillets $4,296 $4,620 $4,935 6.8%

Tilapia – Frozen Fish 1,841 1,975 2,271 15.0%

Pangasisus – Frozen Fillets 2,991 2,684 2,799 4.3%

2012 2013 2014 YOY Pct. Change

Other Markets

Import Value ($millions)

Tilapia – Frozen Fillets $158.9 $282.4 $307.3 8.8%

Tilapia – Frozen Fish 24.2 53.0 46.3 -12.6%

Pangasisus – Frozen Fillets 310.0 428.3 500.6 16.9%

Import Volume (mt)

Tilapia – Frozen Fillets 43,796 73,238 76,246 4.1%

Tilapia – Frozen Fish 13,518 27,965 23,207 -17.0%

Pangasisus – Frozen Fillets 133,980 205,243 240,478 17.2%

Import Value/mt

Tilapia – Frozen Fillets $3,629 $3,856 $4,031 4.5%

Tilapia – Frozen Fish 1,790 1,894 1,994 5.3%

Pangasisus – Frozen Fillets 2,313 2,087 2,082 -0.2%

Source: Global Trade Atlas.

Summary of Key Alaska Groundfish Markets Export markets buy about 90 percent of Alaska groundfish meat products, and an even larger percentage of surimi, roe, and ancillary groundfish products are exported. China is the largest wholesale market for meat products, accounting for 44 percent of estimated sales volume in 2014 (Table 4). However, with the exception of sablefish, the vast majority of Alaska groundfish exported to China is re-exported to Europe, the United States, and Japan. Europe is the largest overall market for Alaska groundfish, due to the high volume of pollock and cod

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • 6

which eventually enters European markets. Japan is likely the second largest market followed by the United States, in terms of final sales volume.

Table 4. Wholesale Sales of Alaska Groundfish Meat Products (mt), 2014

Wholesale Production

United States (Est.) Europe China Japan Other Total

Exports

Alaska Pollock 252,809 39,961 137,209 53,390 4,512 17,737 212,848

Pacific Cod 134,206 30,394 20,975 57,195 16,571 9,071 103,812

Flatfish 167,185 40,045 717 107,486 5,356 13,581 127,140

Rockfish 32,192 8,390 58 15,566 6,861 1,317 23,802

Atka Mackerel 20,888 1,361 15 3,741 12,627 3,144 19,527

Sablefish 6,696 593 173 559 4,648 723 6,103

Pacific Halibut 6,159 4,093 0 16 0 2,050 2,066

Unknown Species - -58,740* 310 36,950 7,401 14,079 58,740

Total 620,134 66,096 159,457 274,903 57,976 61,702 554,038

Pct. of Total - 11% 26% 44% 9% 10% 89%

Note: Wholesale production of high-volume whitefish species only includes whole fish, H&G, and fillet production. Virtually all halibut and sablefish consists of edible products. *Unknown species likely represent exports of Alaska flatfish and other high-volume whitefish species, this non-specific volume is debited from estimates of U.S. supply. This amount could also represent part of the difference between how product weight is reported in export and production statistics. Source: AKFIN, ADF&G (COAR), and ASMI Alaska Seafood Export Database.

Alaska Groundfish and Crab Wholesale Market Profiles NOAA/NMFS • 7

Wholesale Market Profiles for Alaska Pollock Products

Note: Differentiating pollock by its place of origin, primarily Russia or Alaska, can be confusing due to the official species name (Alaska pollock). To avoid confusion, we typically use the term “pollock” to refer to Alaska pollock (Gadus chalcogrammus) from any country/place. References to pollock from a specific place are called out by name (e.g. “Alaska pollock” or “Russian pollock”).

Alaska pollock or walleye pollock (Gadus chalcogrammus) is currently the largest single species fishery in the world, with stocks concentrated in the North Pacific Ocean. Pollock are commercially harvested by several countries, but Alaska and Russia are the largest producers by a wide margin. Alaska pollock harvests are large on a national scale, accounting for 33 percent of total U.S. commercial fishery landings and 14 percent of wholesale production value in 2014.