Embed Size (px)

Citation preview

AFEASIBILITY REPORT

ON

‘ BAKERY ’

GROUP ‘C’THIRD YEAR M.BA

2010-11

K.S. SCHOOL OF BUSINESS MANAGEMENTGUJARAT UNIVERSITYAHMEDABAD-380009

1

CERTIFICATE

This is to certify that members of group of Third year M.B.A. of K.S School of

Business Management and Research have successfully completed their

feasibility report on BAKERY for the academic year 2009-2010 and have duly

submitted the report to the institute.

Date of submission : March 10, 2011

Project Guide : Mrs. Anjali Gokhru

Signature :

K.S School of Business Management Gujarat University,Ahmedabad -380009

2

MEMBERS OF GROUP ‘C’

S.No ROLL NO. NAME1. 3022 KINJAL MAKWANA2. 3026 HELLY MODI3. 3028 RICHITA MODI4. 3031 VIDHI PADSALA5. 3032 ANKITA PANCHAL6. 3057 CHARMI SHAH7. 3081 AMISHA RAI8. 3097 GRISHMA JOSHI9. 3102 PARUL LAKUM

10. 3114 SHWETA SAGAR

3

TABLE OF CONTENTSS.No PARTICUALAR PAGE NUMBER

1. ACKNOWLEDGMENT 52 PREFACE 63 EXECUTIVE SUMMARY 74. INTRODUCTION TO

FESIBILITY9

5. INTRODUCTION TO BAKERY 126. ENVIRONMENTAL

SCANNING19

7. LEGAL FEASIBILTY 268. TECHNICAL FEASIBILTY 359. HUMAN RESOURCE

FEASIBILTY61

10. MARKETING FEASIBILTY 7111. FINANCIAL FEASIBILTY 10012. CONCLUSION 13013. BIBLIOGRAPHY/

WEBOGRAPHY132

14. APPENDIX 134

4

ACKNOWLEDGEMENT

How does a person say “thank you” when there are so many people to thank?

Obviously this project is a thank you to our faculty guide Mrs. Anjali Gokhru for her inspiring guidance.

We would also like to thank our director Dr. Sarla Achuthan, the powerful driving force of K.S. School of Business Management.

We are also greatly indebted to the consumers and the dealers for their co-operation and support. Without their active participation this feasibility project could not have been completed successfully.

Last, but not the least, we are deeply indebted to K.S. School of Business Management for providing us the opportunity to enhance our inner ability and improve our knowledge and skills.

Finally, we express our warm gratitude to all the people, who have been directly or indirectly involved in this project and made it an enjoyable and meaningful experience.

5

PREFACEFeasibility reports address things like where and how the business will operate. They provide in-depth details about the business to determine if and how it can succeed, and serve as a valuable tool for developing a winning business plans.

This project studies and analyses various parameters that decide the establishment of a bakery and whether the venture shall be feasible or not.

The project has been divided into four major branches of feasibility study, namely, technical, human resource, marketing and financial.

Our team has made an all out effort to present a comprehensive feasibility report and depict the feasibility of the project.

We hope that this project will receive a warm welcome from K.S. School of Business Management.Valuable suggestions from the teachers and students are welcome for the improvement of the project.

6

EXECUTIVE SUMMARY

This project is a feasibility report for establishing a bakery. The name of our partnership firm has been decided as ‘Cravings Bakery’. We will enter into the business with breads, buns, toasts, khari and cream rolls as our chief products. Legal, technical, marketing & financial feasibility have been covered in this project.

For the legal feasibility, we have shown laws that govern bakery production and

products.

Technical feasibility includes raw materials, machineries required for production

and the production process for different products. These have been decided after

visiting bakeries in Ahmedabad and conducting a small survey for dealers.

Marketing feasibility covers the marketing mix for our firm, marketing strategy

adopted and the market research conducted for consumers and dealers of bakery

products. The analyses of these surveys show the customer trends for bakery

products and the pattern of demand and supply in the bakery industry.

The workforce required by the firm is specified in human resource feasibility.

Estimated costs, sales, profits make the financial feasibility. Ratio analysis and

break even sales are also covered in this part.

7

8

INTRODUCTION

9

FEASIBILITY

10

DEFINITION OF FEASIBILITY A feasibility report looks at the viability of an idea with an emphasis on identifying potential problems and attempts to answer one main question: Will the idea work and should you proceed with it?

Before you begin writing your business plan you need to identify how, where, and to whom you intend to sell a service or product. You also need to assess your competition and figure out how much money you need to start your business and keep it running until it is established.

Feasibility studies address things like where and how the business will operate. They provide in-depth details about the business to determine if and how it can succeed, and serve as a valuable tool for developing a winning business plan.

Why Are Feasibility Reports so Important?Feasibility reports contain comprehensive, detailed information about your business structure, your products and services, the market and help you to know the logistics of how you will actually deliver a product or service, the resources you need to make the business run efficiently, as well as other information about the business.

The Components of a Feasibility Report Description of the Business: The product or services to be offered and

how they will be delivered. Market Feasibility: Includes a description of the industry, current market,

anticipated future market potential, competition, sales projections, potential buyers, etc.

Technical Feasibility: Details how you will deliver a product or service (i.e., materials, labour, transportation, where your business will be located, technology needed, etc.).

Financial Feasibility: Projects how much start-up capital is needed, sources of capital, returns on investment, etc.

Organizational Feasibility: Defines the legal and corporate structure of the business (may also include professional background information about the founders and what skills they can contribute to the business).

Conclusions: Discusses how the business can succeed. Be honest in your assessment because investors won’t just look at your conclusions they will also look at the data and will question your conclusions if they are unrealistic.

11

INTRODUCTION TOBAKERY

HISTORYBaking is the technique of prolonged cooking of food by dry heat acting by convection, normally in an oven, but also in hot ashes, or on hot stones. It is

12

primarily used for the preparation of bread, cakes, pastries, pies, cookies, biscuits and crackers. Such items are sometimes referred to as "baked goods," and are sold at a bakery. A person who prepares baked goods as a profession is called a baker. It is also used for the preparation of baked potatoes, baked apples, baked beans, and various other foods.

Many commercial ovens are provided with two heating elements: one for baking, using convection and conduction to heat the food, and one for broiling or grilling, heating mainly by radiation.

The baking process does not require any fat to be used to cook in an oven. Some makers of snacks such as potato chips or crisps have produced baked versions of their snack items as an alternative to the usual cooking method of deep-frying in an attempt to reduce the calorie or fat content of their snack products.

In ancient history, the first evidence of baking occurred when humans took wild grass grains, soaked them in water, and mixed everything together, mashing it into a kind of broth-like paste. The paste was cooked by pouring it onto a flat, hot rock, resulting in a bread-like substance. Later, this paste was roasted on hot embers, which made bread-making easier, as it could now be made anytime fire was created.

Baker putting a bread into an oven with a peel, 1568

Baking flourished in the Roman Empire. In about 300 BC, the pastry cook became an occupation for Romans. This became a respected profession because pastries

13

were considered decadent, and Romans loved festivity and celebration. Thus, pastries were often cooked especially for large banquets, and any pastry cook who could invent new types of tasty treats was highly prized. Around 1 AD, there were more than three hundred pastry chefs in Rome, and wrote about how they created all sorts of diverse foods, and flourished because of those foods.. A great selection of bakery products like breads and pastries, with many different variations, different ingredients, and varied patterns, were often found at banquets and dining halls. The Romans baked bread in an oven with its own chimney, and had mills to grind grain into flour.

Eventually, because of Rome, the art of baking became known throughout Europe, and eventually spread to the eastern parts of Asia. Bakers often baked goods at home and then sold them in the streets. In London, pastry chefs sold their goods from handcarts. This developed into a system of delivery of baked goods to households, and demand increased greatly as a result. In Paris, the first open-air café of baked goods was developed, and baking became an established art throughout the entire world, thus leading to the successful birth of bakeries and baked products.

SCENARIO OF BAKERY IN INDIA14

The bread and bakery products market has struggled with numerous challenges over many years. As a mature and saturated market, it has had to rely on continual investment in new product development (NPD) and marketing to ensure growth. The higher unit cost of bread, rather than increases in volume consumption, has led to a 9% increase in household expenditure on bread and bakery products during 2010. The traditional white bread sector was the largest in the total bread market until 2006, when the growing focus on healthy eating, among other factors, led some consumers to switch to other types of bread and bakery products. However, despite falling consumption, rising prices have meant that total household expenditure on white bread rose steeply in 2009 and in 2010. The brown and whole meal bread sector has experienced a strong revival since 2005 — something which can be linked mainly to renewed interest in healthy eating. The sector has retained a share of the total bread market of more than 18% since 2007. The specialty breads sector has shown steady growth during the past 5 years. It overtook white bread as the largest sector in 2006, and in 2009 had sales at a similar level to white bread. In India, there are 85,000 bakery units, of which 75,000 operate in unorganized sector occupying 65% of the market share. The per capita consumption of bakery products as it stands today is 1-2 kg per annum, which compares very low with that in the advanced countries, which is 10-50 kg per annum. The urban areas hog a major share of the Indian Bakery, comprising 77.5 % of the total market, owing to 2 vital factors – rising disposable incomes and time constraints in the working population residing in these areas. The Indian Bakery Market is estimated to be worth Rs. 6,900 Crores, growing at a healthy CAGR of 7 % per annum. Out of this bread and biscuits hold about 82% of the share. The major players in these segments are Britannia, Parle, Bakeman, ITC Foods Ltd and HUL and the major brands are Britannia, Parle, Bakeman, Priya Gold, Cremica, Dukes and Horlicks. Another segment worth mentioning is Cakes and Pastries, which is dominated by Monginis, a Cake brand based at Mumbai.

15

Some of the major consumer trends in the Indian Bakery Market worth mentioning are,

With globalization and cultural integration, eating habits of the discerning urban and rural consumer are fast changing. Bakery joints are slowly becoming popular hangout places. A typical trend is for a variety of bakery snacks, top quality products and value for money. The present day consumer looks for new bakery products, better appeal, taste and convenience from bakery foods. With a population of 1 billion plus, India has the largest middle-income consumers, who demand varieties in food, clothing, transport and improved living standards, also wish to eat out. Another fastest growing segment in India, is Bakery Cafes and Restaurants, who cater fast foods. Consumers are increasingly concerned about their health and are well aware of the relationship between nutritious food and optimal health. Various concerns have caused consumers to demand for healthier bakery products. The concerns like, the growing media coverage on health, the rising incidence of health conditions (obesity, diabetes and cardiac problems) etc. have resulted in the introduction of low/light, functional, wholemeal, multigrain, natural and organic products in the market. In addition to healthier products, consumers also are purchasing products that satisfy their taste buds. With lifestyles becoming increasingly stressful, consumers may indulge in food for comfort. On-site manufacturing of bakery products in bakeries and supermarkets directly contributes to this trend, as it is well known that the smell of freshly baked breads and other products is a strong motivational factorin subsequent purchases. Indulgence/luxury products like cakes and pastries are becoming more pronounced as a key trend in the bakery industry. Consumers increasingly seek for premium, gourmet and exotic products to satisfy their desire to indulge.

The future of bakery industry in India is indeed bright, as 70 - 80% of the market is still being served by the unorganized segments of the market. Larger companies have continued to place a high emphasis on branding and marketing in an effort to differentiate their products from those of their competitors.

16

PROJECT AT A

GLANCE

17

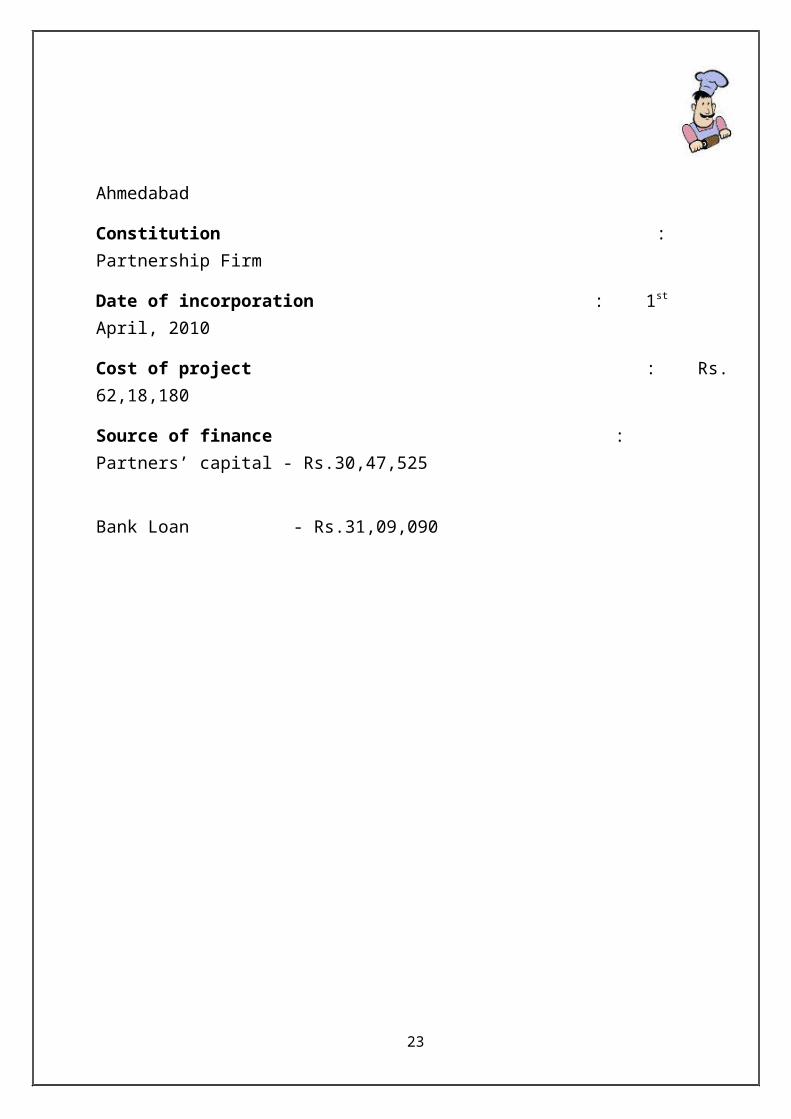

Name : Cravings Bakery

Product : Breads, buns, Cream rolls, Tea cakes Status : Medium Scale

Address : Phase-2, GIDC, Changodar,

Ahmedabad

Constitution : Partnership Firm

Date of incorporation : 1st April, 2010

Cost of project : Rs. 62,18,180

Source of finance : Partners’ capital - Rs.30,47,525

Bank Loan - Rs.31,09,090

18

ENVIRONMENTALSCANNING

PEST ANALYSIS

19

A PEST analysis is an analysis of the external macro-environment that affects all firms. P.E.S.T. is an acronym for the Political, Economic, Social, and Technological factors of the external macro-environment. Such external factors usually are beyond the firm's control and sometimes present themselves as threats. For this reason, some say that "pest" is an appropriate term for these factors. However, changes in the external environment also create new opportunities and the letters sometimes are rearranged to construct the more optimistic term of STEP analysis.

Many macro-environmental factors are country-specific and a PEST analysis will need to be performed for all countries of interest. The following are examples of some of the factors that might be considered in a PEST analysis.

Political Analysis Political stability Pricing regulations Taxation - tax rates and incentives

20

PEST

POLITICAL

TECHNOLOGICAL

SOCIAL

ECONOMIC

Wage legislation - minimum wage and overtime Work week Mandatory employee benefits Industrial safety regulations Product labeling requirements

Economic Analysis Government intervention in the free market Skill level of workforce Labour costs Business cycle stage (e.g. prosperity, recession, recovery) Economic growth rate Unemployment rate Inflation and interest rates

Social Analysis Demographics Class structure Education Culture (gender roles, etc.)

Technological Analysis Level of technology used for production. Innovation in production techniques.

The number of macro-environmental factors is virtually unlimited. In practice, the firm must prioritize and monitor those factors that influence its industry. Even so, it may be difficult to forecast future trends with an acceptable level of accuracy.

SWOT ANALYSIS

21

A scan of the internal and external environment is an important part of the strategic planning process. Environmental factors internal to the firm usually can be classified as strengths (S) or weaknesses (W), and those external to the firm can be classified as opportunities (O) or threats (T). Such an analysis of the strategic environment is referred to as a SWOT analysis.

The SWOT analysis provides information that is helpful in matching the firm's resources and capabilities to the competitive environment in which it operates. As such, it is instrumental in strategy formulation and selection.

The SWOT Analysis of our firm is

Strength The prices of our products are very reasonable and less than our

competitors. New and different varieties of breads have been introduced which shall give

us the benefit of product differentiation. Our sales are through tie-ups with grocery stores and supermarkets across

Ahmedabad. This gives us a wide consumer base and a chance to serve different levels of customers.

The firm also gives a little more commission to its distributors to encourage dealership.

The labour required does not need any specific qualification & skill and hence can be made easily available.

22

Weakness Bakery products are perishable items hence need to be sold as soon as

possible to gain maximum benefit. The customers also prefer fresh products. But the far location of the factory can increase the time between baking and actual selling.

Our bakery has introduced few bakery items from the possible product lines. We are not making cakes, pastries, chocolates and other various products. This limited menu can be seen as a weakness.

We are not introducing our own outlets but are selling through tie-ups across the city. This delays our brand establishment time.

Opportunity Expansion of the product line in the future with the introduction of biscuits

and cakes and pastries. Scope for expansion with the establishment of our own outlets and bakery

cafés Growing concern for health and multigrain food products shall become a

reason for increase of our sales of food items such as brown breads, tomato-spinach bread and white-coriander bread.

Threats Severe competition in the industry with well-established players like Modern

breads, Britannia, Havmor, Italian Bakery, Moti bakery etc.

23

LEGAL CRITERIANumerous laws has been stipulated by ministry of food and related ministry to check consumer interest and stop malpractices by manufacturers.

Following are the acts inacted by Government of India :

Food Safety and Standards Act , 2006 Prevention of Food Adulteration Act (PFA) 1954 and Environment Protection

Act, 1986. Pollution Control (Ministry of Environment and Forests). Industrial Licenses. BIS Act, 1986.

In addition to Commercial licenses and registration following are major laws to be followed by bakeries

Factories Act (Occupational related issues ) Air and Water pollution Act (Pollution Control ) Petroleum Act ( Storage of LPG in factory premises)

A brief introduction to some of the major laws in food industry and bakery is as follows:

Prevention of Food Adulteration Act, 1954The objectives of this Act are:

1. To protect the public from poisonous and harmful foods.2. To prevent the sale of substandard foods3. To protect the interest of the consumers be eliminating fraudulent practices.

Our firm adheres to the requirements of this Act and uses no adulterant substance in production.

The Bureau of Indian Standards Act, 1986An Act to provide for the establishment of a Bureau for the harmonious development of the activities of standardization, marking and quality certification of goods and for matters connected therewith or incidental thereto.

24

Food Safety and Standards Act, 2006 This act replaces the Prevention of Food Adulteration Act(PFA)1954. The objective of the new act is to consolidate the laws relating to food and to curb Food Adulteration by prescribing higher penalties for violation of food laws. It established Food Safety Management System for ensuring availability of safe and wholesome food for human consumption. Food Safety and Standards Authority of India was also established for enforcing the food safety standards.

Labour LawsThere are certain labour and employment laws that also need to be followed:A) Laws related to Industrial Relations:

i. The Trade Union (Amendment) Act, 2001ii. Industrial Employment (Standing Order) Act, 1946iii. The Industrial Dispute Act, 1947

B) Laws related to wages:

i. Payment of wages (Amendment) Act, 2005.ii. The Minimum Wages Act, 1948iii. The Payment of Bonus Act, 1965

25

LEGAL FEASIBILITY

PARTNERSHIP DEED26

Partnership is an association of two or more people who come together for achieving some common goals. A written document which binds them and gives them a legal enforcement right is called a partnership deed.

The partnership deed of Cravings Bakery is as follows:

1) Date of Execution:

“This deed of partnership is executed on April 1, 2011

Details of Partners:

S.NO NAMEOF PARTNER ADDRESS

1 KINJAL MAKWANA A/305,shrinandnagar-2,Vejalpur

2 HELLY MODI 1271, Raja Mehta ni pole, Kalupur.

3 RICHITA MODI 1534,Fafda ni Pole, Sarangpur.

4 VIDHI PADSALA 2, Raviraj Society, Science City.

5 ANKITA PANCHAL K-3/453, Nikita Park, Naroda.

6 CHARMI SHAH B/3 Kirtan App., Nava vadaj.

7 AMISHA RAI 13, Sakansh App., Ambavadi

8 GRISHMA JOSHI C-76, GIDC, Naroda.

9 PARUL LAKUM A/5 F/3, Shivalay So., Vejalpur.

10 SHWETA SAGAR A-214, Purshottam Park, D-Cabin.

.

The above partners have come together to carry on the business of a bakery enterprise, as from April 1, 2011. The terms and conditions of partnership in writing as agreed upon, are as follows.

a. Name

The business of the firm will be carried on under the name “Cravings”. However partners shall be entitled to change the name of the firm as may be mutually agreed upon.

27

b. Business of partnership

The partnership will carry on the business of bakery, making, distributing and selling bakery products as agreed by the partners.

c. Date of CommencementThis partnership shall be deemed to have been commenced on and with effect from April 1, 2011.

d. Place of businessThe principal place of the business of the firm shall be at Phase-2, GIDC, Changodar, but the partners shall be at liberty to shift it to any other place Or places and to open branch or branches at any other place or places as may be agreed upon.

e. Duration

That the duration of this partnership is not fixed and it shall be partnership at will.

f. Accounting YearThe accounting year of the company shall commence from April 1 and will end on March 31 every year. The first accounting year of the firm will be from 1-04-2011 to 31-03-2012.

g. Accounts and Records

Proper and regular accounts and records of the affairs and transaction of the firm shall be maintained and kept at the principal place or any other relevant or appropriate place or places in accordance with the requirements of the business of the firm.

h. Final Accounts

The balance sheet as on the last day of the accounting year and profit and loss account for the year shall be prepared at the end of each accounting year. The profit and loss as the case may be of the year shall be worked out and be allocated between the partners as per the profit –loss sharing ratio.

28

i. Capital

The initial capital of the firm shall be Rs. out of which 40% shall be contributed by all the partners equally and remaining will be the loan from the bank.

j. Drawings

The drawing shall be made by partners as many times in the year as per the wish to the partners taking into consideration the respective accounts.

k. Borrowing Power

The firm shall be entitled to secure deposits, borrow money and take loans from banks, financial institution and other corporate bodies or non-corporate parties. The partners can also provide loans to the firm.

l. Bank Account

Bank account in one or more banks will be operated in the names of the firm by any one or more of the partners and they shall be authorized to avail all types of facilities in the name of the firm that are generally allowed by the banks. Partners are also entitled to authorize any other person for operation of bank account through a power of attorney signed by all the partners.

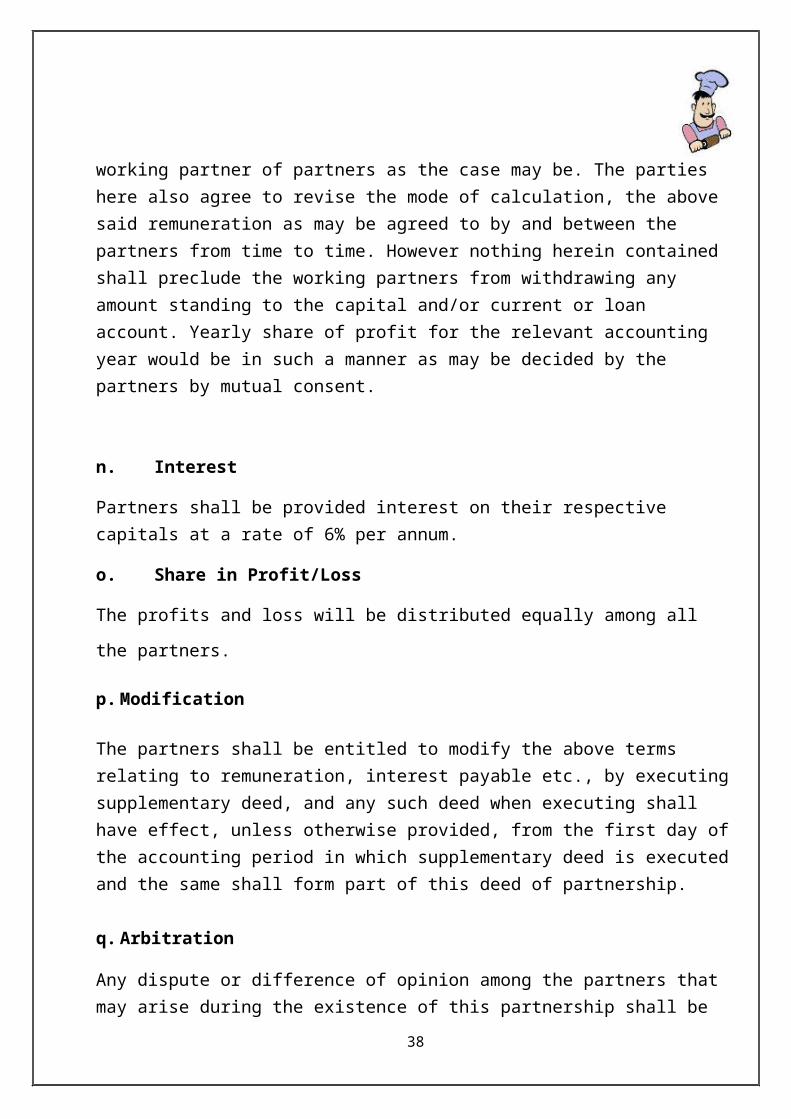

m. Remuneration

It is hereby agreed that in consideration of the working partners keeping themselves actively engaged in the conduct of the affairs of the firm as working partners they shall be entitled to draw remuneration with effect from April 1, 2011 as under:

For the purpose of above calculation book profit shall be calculated on basis as defined in explanation 3 to section 40(b) of the income tax act, 1961 or any other applicable provision as may be in force for the income tax assessment of the partnership firm for the relevant accounting period.

In case of loss remuneration will be paid to the working partners as paid in the case of profit.

The partners shall be entitled to increase the above remuneration and may agree to pay remuneration to other working partner of partners as the case may be. The

29

parties here also agree to revise the mode of calculation, the above said remuneration as may be agreed to by and between the partners from time to time. However nothing herein contained shall preclude the working partners from withdrawing any amount standing to the capital and/or current or loan account. Yearly share of profit for the relevant accounting year would be in such a manner as may be decided by the partners by mutual consent.

n. Interest

Partners shall be provided interest on their respective capitals at a rate of 6% per annum.

o. Share in Profit/Loss

The profits and loss will be distributed equally among all the partners.

p. Modification

The partners shall be entitled to modify the above terms relating to remuneration, interest payable etc., by executing supplementary deed, and any such deed when executing shall have effect, unless otherwise provided, from the first day of the accounting period in which supplementary deed is executed and the same shall form part of this deed of partnership.

q. Arbitration

Any dispute or difference of opinion among the partners that may arise during the existence of this partnership shall be referred to arbitration and in such cases the provision of Indian Arbitration Act, 1940 shall be made applicable.

r. Amendment and Alteration

The partners shall, by mutual, oral, and/or written agreement, be at liberty to amend, alter, vary, or add to the aforementioned terms and conditions.

30

Declaration:

After hearing the translation of this partnership deed and complete understanding of the terms and conditions, we the partners agree to the above deed.

BANK OF BARODA Ashram Road, Ahmedabad

No.: BR:ADV/3/180

M/s. Cravings Bakery Date: 2 February, 2011

31

Phase-II, GIDC ChangodarAhmedabad.

Dear Sir/Ma’am

Ref: Sanction of Credit

With reference to your application letter dated 7/8/2010 we are pleased to sanction the credit facilities on the following terms and conditions:

1. Nature of facility: Term loan of Rs.

2. Purpose: Purchase of fixed assets

3. Rate of Interest: 11% per annum

4. Period/ Repayment: 5 years

Other terms and conditions:a.) You will periodically submit the monthly statement of stock, sales and purchase.b.) You will submit a copy of the audited/unaudited Balance sheet, Trading amount and

profit and loss account within three months from the close of the accounting year.c.) Bank will have the right to carry out inspection of books of Cravings Bakery and the

charges thereof will be borne by you.

Even though the above-mentioned facility is granted to you for a period of 60 months, the bank reserves the right to recall the facility or alter the terms and conditions at any time during the currency of the facility.

Yours faithfully

Senior ManagerBank of Baroda

32

33

34

TECHNICAL FEASIBILITY

INTRODUCTION

The term “technical feasibility” establishes that the product or service can operate in the desired manner. Technical feasibility means “achievable”. This has to be

35

proven without building the system. The proof is defining a comprehensive number of technical options that are feasible within known and demanded resources and requirements. These options should cover all technical sub-areas.

Our technical feasibility includes location analysis, procurement of raw materials, specification of machinery and production process

LOCATION ANALYSISThe selection of location plays a vital role for the growth. We have decided to establish our production unit as well as the administrative office in our factory building in Changodar.

36

Factory & Administrative office address:

Cravings bakery,

Phase-2, GIDC Changodar,

Ahmedabad.

Area: 3600 sq. feet Cost of land: 16, 42,000 including documentation charges and agent’s

commission. Reason for selecting the site:

• Fast growing area• Easy availability of land and building at reasonable rates.• Easily accessible location• Easy availability of raw materials and amenities like electricity and

water as the whole area is an industrial site.• Easy availability of the labour in industrial aree.

PLANT LAYOUT

37

The plant layout of the factory building and the planned interior setup is depicted below:

PROCUREMENT OF RAW MATERIALSThe estimated daily requirement of ingredients is:

S.NO INGREDIENTDAILY REQUIREMENT

(in Kgs.)PRICE PER

Kg./Ltr.

38

1. Maida 400 172. Wheat Flour 50 173. Yeast 12 1804. Milk 57 225. Vegetable Oil 12 606. Sugar 23 307. Butter 15 1008. Brown Sugar 4 409. Baking Powder 2.5 9010. Curd 8 5011. Salt 10 512. Spinach leaves 5 1713. Tomato 5 3014. Cumin powder 0.2 10015. Red chili powder 0.2 25016. Cinnamon 0.2 10017. Coriander 0.7 10018. Ginger 0.350 75

Apart from the above mentioned ingredients, we shall also need the following ingredients on weekly basis.

S.No. INGREDIENT WEEKLY REQUIREMENT

PRICE PER Kg/gms.

1. Tutti-Fruity 1.5 kg 802. Chocó powder 300 gms 2003. Cocoa powder 300 gms 200

The ingredients will be purchased from local suppliers at Jamaalpur and Kalupur markets.

SPECIFICATION OF MACHINERY

1.) DECK OVEN39

NAME Deck oven(in-built proofer)QUANTITY PURCHASED 1

SUPPLIER Canon engineering industriesPRICE Rs. 2,64,000

WEIGHT 490 kgCAPACITY 9 trays

FUEL Gas-fired

2.) DOUGH MIXER

40

NAME Dough MixerQUANTITY PURCHASED 3

SUPPLIER Canon Engineering IndustriesPRICE PER UNIT Rs. 46,500

WEIGHT 285 kgCAPACITY 25 kg

FUEL Electric fired

3.) DOUGH MOULDER

41

NAME Dough moulderQUANTITY PURCHASED 2

SUPPLIER Canon Engineering IndustriesPRICE PER UNIT Rs. 42,350

WEIGHT 290 kgsCAPACITY 80 kg/hour

FUEL Electric fired

4.) SUGAR GRINDER

42

NAME Sugar Grinder

QUANTITY PURCHASED 1

SUPPLIER Kaps Engineers

PRICE Rs. 35,000

WEIGHT 250 kg

CAPACITY 135 kg/hour

5.) PACKING MACHINE

43

NAME Packing Machine

QUANTITY PURCHASED 2

SUPPLIER Apple Bakery Machinery Pvt. Ltd.

PRICE Rs. 47,650

WEIGHT 265 kgs

6.) BREAD/TOAST SLICER44

NAME Bread Slicer

QUANTITY PURCHASED 2

SUPPLIER Canon Engineering IndustriesPRICE Rs. 38,000

WEIGHT 270 kgsCAPACITY 300 loaves per hour

Capable of slicing bread upto 25 cm long

45

7.) FREEZER

NAME Freezer

QUANTITY PURCHASED 2

SUPPLIER KPM Industries

PRICE Rs. 16,400

WEIGHT 300 kgs

46

8.) MIXER GRINDER

NAME Mixer Grinder

QUANTITY PURCHASED 1

SUPPLIER Local Shop

PRICE Rs. 3,600

47

9.) ROLLING RACKS

NAME Rolling Racks

QUANTITY PURCHASED 6

SUPPLIER KPM Industries

PRICE Rs. 7500

CAPACITY 7 storey

48

10.) TRAYS

NAME Trays

QUANTITY PURCHASED 100

SUPPLIER KPM Industries

PRICE PER UNIT Rs. 200

49

11.) STAINLESS STEEL UTENSILS AND TOOLS

NAME Stainless steel utensils

SUPPLIER Local Shops

PRICE Rs.83,400

50

PROCESS

BREAD:

51

PACKAGING

SLICING

COOLING

BAKING

PROOFING

SHAPING

PRE-SHAPING

MIXING

Starter Often referred to as sourdough, this is a pre-made mixture of flour water and naturally occurring yeast. A portion of the starter from the previous day is included in the next day’s starter. The starter is a continuous and dynamic mixture. It is allowed to develop until it has reached itsmaturity for many hours and then it is included in the mixing process.Starter imparts a sour flavor and develops a distinctive crust.

MixingIn the mixing step the ingredients of the recipe are incorporated into a homogeneous mixture and then developed. This is a two stage process.

First everything (flour, water, salt and leavening) is mixed together and water is added gradually on a low speed. After the appropriate amount of water is added the second stage of gluten formation and development begins.

In gluten development, or strength, the gluten is formed by the combining of the water and protein in the flour. The gluten is developed by the stretching and folding of the strands (or kneading). Gluten development becomes the foundation and structure for the bread. Here begins the first fermentation stage. (fermentation

is the conversion of carbohydrates (sugars) to alcohol and CO2) At this point the dough will spring back when touched.

Pre shape

In this step the dough is given a shape and divided into proportional sizes

52

In our process we shape all loaves first into rounds. Here some of the developing gas is worked out by hand. Once rounded the dough is allowed to rest. Generally we cover the dough to keep from drying and crusting over. In our case the resting is usually 10-20 minutes.

ShapingOnce the dough is relaxed the final shape is given.

Here the excess gases are expelled very gently by pressing and squeezing the dough by hand. The expulsion of the gases makes for a more uniform loaf of bread and less air pockets. By expelling the gases the fermentation process is also rejuvenated and slightly accelerated. Once shaped, the dough is placed on flour lined pans or boards.

ProofingAt this point fermentation is allowed to take its course in a warm and humid atmosphere while the dough is covered.

This type of proofing, combined with other details of the bread making process, gives our bread its uniqueness, depth of flavor and crispy crust. Here the dough ferments (or rises) to a desired volume and consistency. Ideally the dough should be soft and slightly pliable. If pushed with a finger it should leave an impression.

53

BakingDuring the initial baking there is a tremendous burst of gas that occurs called oven spring.

To allow for controlled tearing the bakers score (make cuts to) the loaves. The cuts create a weak area for the expansion to occur. This is where the final result can be experienced. The sight of warm fresh baked bread being pulled from the oven, the smell of freshly baked bread and the sound of the crackling crust is where the results of all the hard work are realized.

Cooling The bread formed is then allowed to cool for some time.

PackingThe ready bread is then packed and wrapped. The seal and logo of the firm is imprinted on the packing. Thus the final product is ready to be sold.

54

TOAST :

The process for making toast starts with bread as the raw material.

Cut the slices of bread in the desired shape of toasts. Butter it up liberally Add salt and pepper to taste Pour hot milk over the toast Let all that soak in.

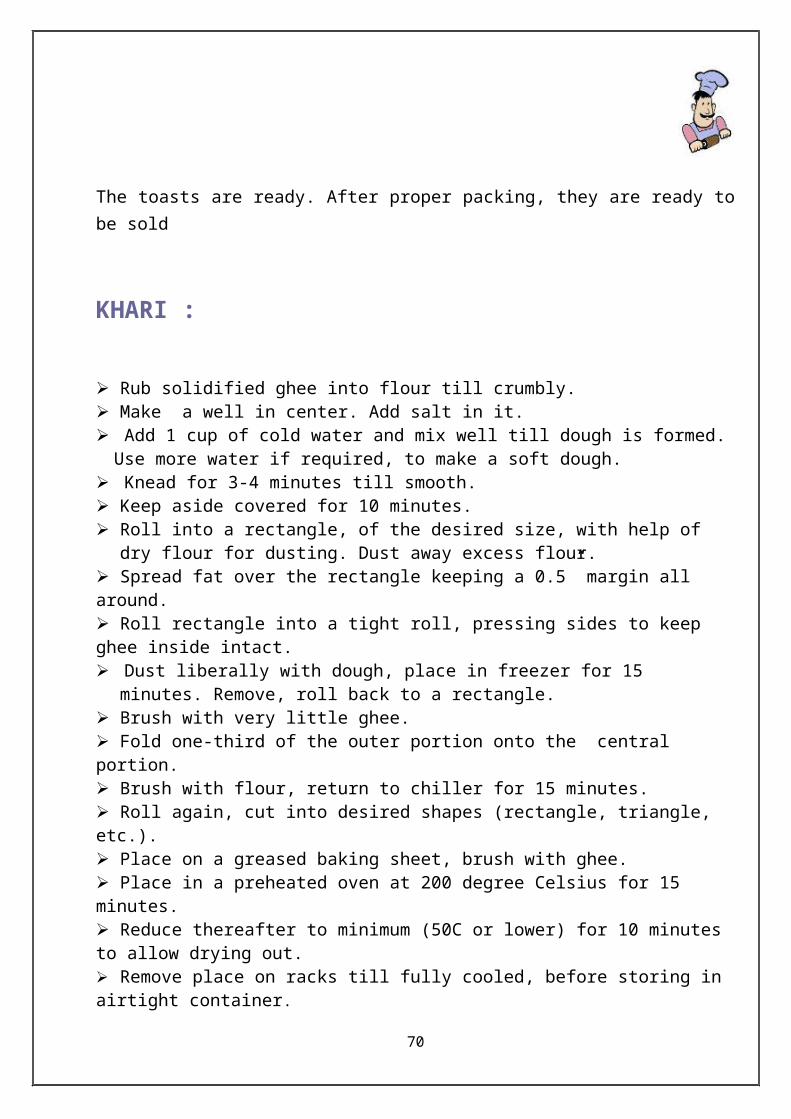

The toasts are ready. After proper packing, they are ready to be sold

KHARI :

Rub solidified ghee into flour till crumbly. Make a well in center. Add salt in it. Add 1 cup of cold water and mix well till dough is formed. Use more water if

required, to make a soft dough. Knead for 3-4 minutes till smooth. Keep aside covered for 10 minutes. Roll into a rectangle, of the desired size, with help of dry flour for dusting. Dust

away excess flour. Spread fat over the rectangle keeping a 0.5” margin all around. Roll rectangle into a tight roll, pressing sides to keep ghee inside intact. Dust liberally with dough, place in freezer for 15 minutes. Remove, roll back to a

rectangle. Brush with very little ghee. Fold one-third of the outer portion onto the central portion. Brush with flour, return to chiller for 15 minutes. Roll again, cut into desired shapes (rectangle, triangle, etc.).

55

Place on a greased baking sheet, brush with ghee. Place in a preheated oven at 200 degree Celsius for 15 minutes. Reduce thereafter to minimum (50C or lower) for 10 minutes to allow drying out. Remove place on racks till fully cooled, before storing in airtight container.

OUR PRODUCTS

BREADS

WHITE BREAD

BROWN BREAD

WHITE CORIANDER BREAD

56

TOMATO SPINACH BREAD

BUNS

PAV

DABELI

57

PIZZA

CREAM ROLLS

58

TOASTS

59

KHARI

60

TEA CAKES

TUTTI FRUITY

61

CHOCOLATE

62

HUMAN RESOURCE FEASIBILTY

ORGANISATION CHART

63

64

PARTNERS

FACTORY MANAGER

PRODUCTION SUPERVISOR

MASTER BAKER

UTILITY WORKERS

FINANCE MANAGER

ACCOUNTANT

MARKETING MANAGER

JOB ANALYSIS

Job analysis includes mainly two things:

1) Job description

Job description is the process by which organization ensured that it has right number and kind of people at the right place and capable of effectively and efficiently completing the task at hand. It describes the functions, duties to be performed and responsibilities of the job holder.

2) Job specification

Job specification states the minimum acceptable qualification that the candidate must possess to perform the job successfully. Job specification identifies the knowledge, skills and abilities to do the job effectively.

65

1. Production Supervisor

66

Job Description:

Job Title : Production Supervisor

Reporting to : Supervisor, Production Department

Function :

To achieve production targets in specific period.To arrange manpower &other sources for production.Planning, have control over the process & check the deviation.To co-operate with administrative department for implementation of

policies & plans.

Duties, Responsibilities & Authorities:

Responsible for production schedules & arrangement of labors. Regular check of stock, purchase, manpower condition.

Job Specification:

Education: Graduate in mechanical engineer from reputed institute

Skills & Requirement:

Capable of leading team of workers. Good communication skills & ability to undertake work from

subordinates.

2. Finance manager

3. Supervisor

67

Job Description:

Job Title: Finance manager

Reporting to: Supervisor

Function:

To make proper policies for condition of companyTo provide appropriate rate of depreciation reserve & surplusTo ascertain budgets for all plans & projectsTo decide upon investment of funds of the company

Duties, Responsibilities, & authority:

To check discrepancies in company’s financial resources To ensure optimum & fare use of company’s financial resources To co-ordinate well with an accountants & director. Analyze financial position of regular intervals.

Job Specification:

Job Title: Finance manager

Education: MBA with finance/CA

Skills Requirements:

Sharp & Speedy in calculation Good analytical skill Division making ability Physical health: Smart & fit

Experience: At least 5 years in similar role.

68

Job Description:

Job Title : Supervisor

Reporting to : Factory Manager

Function :

To perform work efficiently given by production manager.To supervise production process.To give suggestion for better quality of production.To instruct skilled, unskilled labors for effective work.

Duties, Responsibilities & Authorities:

Check daily performance of labors. Responsible for non performance of work of skilled & unskilled

labors.

Job Specification:

Job Title: Supervisor.

Education: Qualified from Industrial Training Institue

Skills & Requirement:

Good relations with workers. Physical Health: Good temperament, Co-operation.

Experience: minimum 2 years.

4. Worker

69

Job Description:

Job Title : Worker

Reporting to : Production Manager

Function :

To perform work efficiently given by supervisor. To work with co-operation.

Duties, Responsibilities & Authorities:

Follow instruction of supervisor. To inform manager immediately for any kind of default.

Job Specification:

Job Title: Worker.

Education: S.S.C or H.S.C. pass

Skills & Requirement:

Technical knowledge about their work and machines should be able to do the job assigned to them.

Physical Health: Capable of working at least 8 hours.

Experience: Not necessary

5. Marketing Manager

70

Job Description:

Job Title : Marketing Manager

Reporting to : Director

Function :

To decide advertising plan & promotional plans. To act as bridge between company & customer.

Duties, Responsibilities & Authorities:

To decide & achieve the target. Responsible for any customer or dealer’s complaint about his

service.

Job Specification:

Job Title: Marketing Manager.

Education: Graduate.

Skills & Requirement:

Knowledge of surrounding market. Should have innovative ideas

Physical Health: Good presence of mind &Good co operation.

Experience: Minimum 1 year in relevant field or fresher can also apply.

6. Peon

7. Security Guard

8. Driver

71

Job Specification

Job Title : Peon Education : S.S.C. or H.S.C Physical health : Healthy Mental Ability : The candidate should be of sound mind.

Job Specification

Job title : Security Guard Education : S.S.C. or H.S.C. & having security training Physical & health : Healthy, polite & able to convince. Special Ability : He should be strong enough to stop any

stranger to the premises. Guard the place from thieves.

Job Specification

Job title : Driver Education : S.S.C. Physical health : Physically fit, good eyesight and no addiction.

AMENITIES TO EMLOYEES.

Following amnesties shall be provided to the workers at the factory:

I. Drinking water:

Effective arrangements have been made to provide wholesome drinking water for all the employees. Drinking water coolers have been established at different spots within the factory.

II. Lavatory:

There are clean lavatories separate for males and females conveniently situated within the building.

III. First Aid:

Adequate first aid kits have been provided for all the employees to avoid unforeseen mishaps and accidents during operations.

IV. Provision for lunch:

Since the shift requires continuous 8 hours of work, afternoon lunch and evening tea shall be provided to all the employees at reasonable affordable prices.

72

MARKETING FEASIBILITY

73

MARKETING MIX

74

MARKETING MIX

PRODUCT

PROMOTION

PRICE

PLACE

PRODUCT

The product is the heart of the marketing exchange. Customers buy product to solve problems or enhance their lives and thus the marketer has to ensure that the product can fully satisfy the customers, not just in functional terms but also in psychological terms.

“A product is physical good, service, idea, person or place that is capable of offering tangible and intangible attributes that individuals or organization regard as to necessary, worthwhile or satisfied that they are prepared to exchange money, patronage or some other unit of value in order to acquire it.”

In this report, our products are breads and buns, cream rolls, toasts and khari and tea cakes.

75

PRODUCT LEVEL

76

POTENTIAL LEVEL

AUGMENTED LEVEL

EXPECTED LEVEL

BASIC PRODUCTCORE

BENEFIT

PRODUCT LEVEL CHART FOR BAKERY

CORE BENEFIT

Core benefit includes the benefit that the product provides to the customers to satisfy their needs.

To satisfy hunger

BASICPRODUCT

In the basic product the marketer has to turn the core benefit into a basic product. This is the actual tangible item that people purchase.

Bakery products like Breads

Toasts/ Khari

Tea cakes

Cream rolls

EXPECTED PRODUCT

At this level, the marketer prepares an expected product, a set of attributes and conditions buyers normally expect when they purchase this product.

Good taste

Good quality

Varieties

Purity and no adulteration

Attractive packaging

AUGMENTED PRODUCT

This is the non tangible elements that are perhaps provided in addition to the physical parts. The marketer prepares an augmented product that exceeds customer expectations. Brand positioning & competition takes place at this level.

Diet products

Sugar free or low calorie products

Free home delivery

POTENTIAL PRODUCT

At this level, the potential product encompasses all the possible augmentation and transformations.

The product or offering might undergo future.

Mix flavour bread having different flavours in the same slice

Breads and butter-jam-cheese-chopped vegetables-ketchup in

77

the same packet

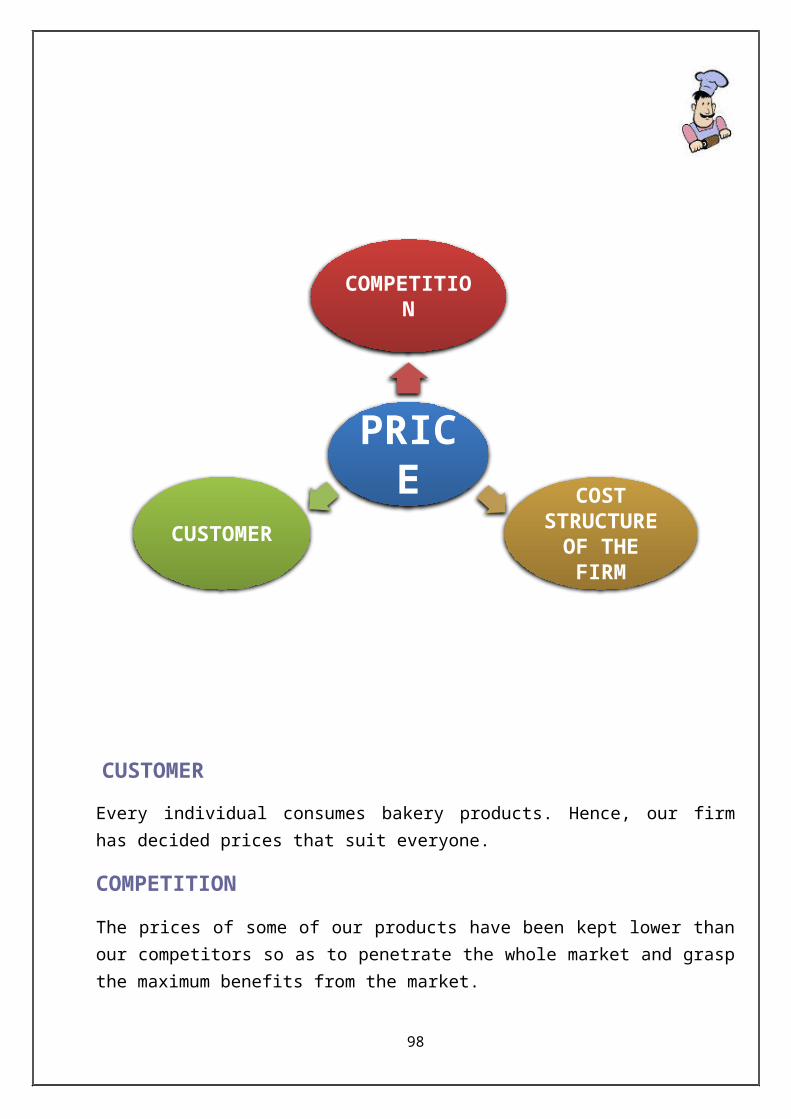

PRICEThe price is the only component in the mix that generates revenue, while other components generate costs.

Price means consideration of any goods or services that a customer paid to the producer.

78

To a manufacturer, price represents the quality of money received by the firm on sales of its products. To a customer, it represents monetary scarifies and hence his perception of the value of the products.

Depending on the objective, the bakery can set the prices. As far as bakery is concerned, it has the objective of the selling its products to the consumer at reasonable price and offer good quality.

In order to arrive at an acceptable price level, the manufacturer needs to have the information on the 3 C’s namely Customer, Competition and Cost structure of the firm.

CUSTOMER

79

PRICE

COMPETITION

COST STRUCTURE

OF THE FIRMCUSTOMER

Every individual consumes bakery products. Hence, our firm has decided prices that suit everyone.

COMPETITIONThe prices of some of our products have been kept lower than our competitors so as to penetrate the whole market and grasp the maximum benefits from the market.

COST STRUCTURE OF THE FIRMAn optimum cost structure has been adopted that enables the firm to earn a reasonable profit and minimizes wastage of resources and losses. We have priced our product somewhere near the prices of the competitors considering the following objectives:

Survival:

As we shall face intense competition survival in the market is our short-term objective. In the long run, we shall work for new innovative varieties offering our customers wider choices.

Maximization of market share:

Our long-term objective is to become a role player in this market. We shall try to achieve this by charging less than our competitor’s price.

80

PLACE81

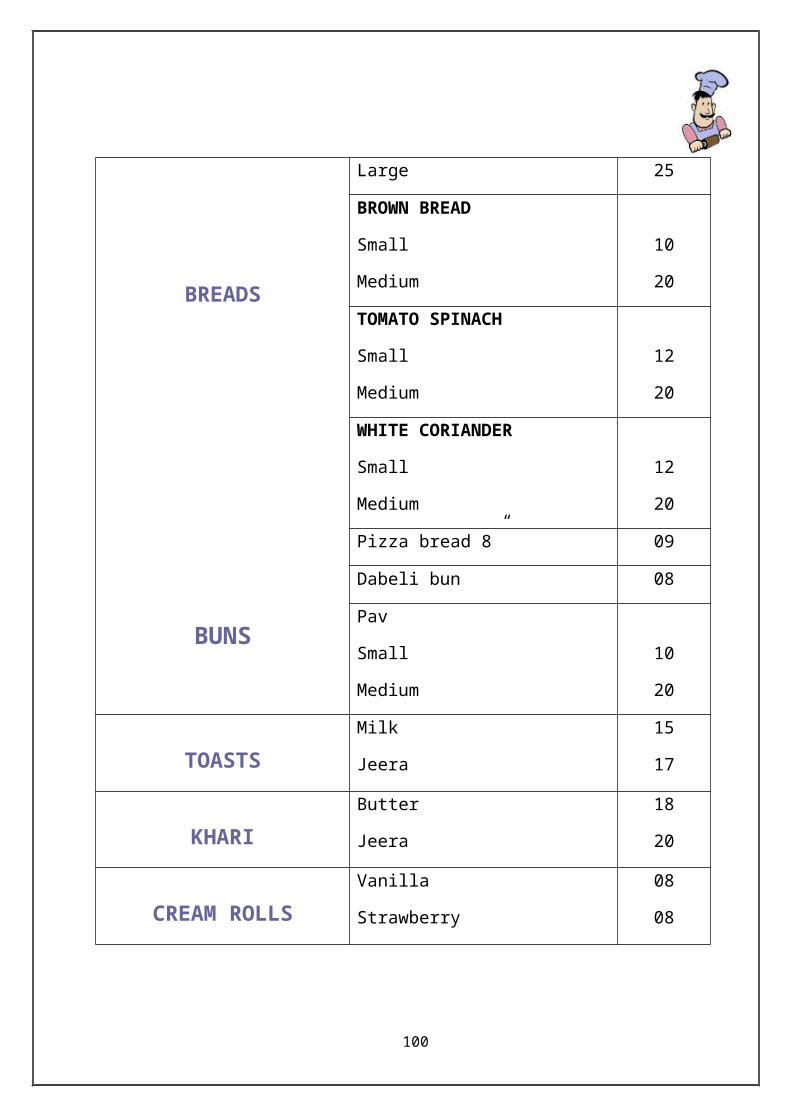

ITEM VARIETY PRICE

BREADS

BUNS

WHITE BREAD

Small

Medium

Large

09

15

25

BROWN BREAD

Small

Medium

10

20

TOMATO SPINACH

Small

Medium

12

20

WHITE CORIANDER

Small

Medium

12

20

Pizza bread 8” 09

Dabeli bun 08

Pav

Small

Medium

10

20

TOASTSMilk

Jeera

15

17

KHARIButter

Jeera

18

20

CREAM ROLLSVanilla

Strawberry

08

08

The location of the plant is a very important aspect in economic analysis of any project as it plays a vital role in continuing life of the business as in future. The firm has to leverage the advertisement while operating with location of plant as the biggest constraint.

Location of plant and industry means a specific site in the region where the business units is to be started for selecting location or the pertinent factors influencing the location have to be considered and weighted out very carefully.

Place: Ahmedabad

Address: Phase-2, GIDC, Changodar,

Ahmedabad.

Why have we chosen Ahmedabad?•Native place•An emerging mega city•Easy availability of building•To create the brand image•Easily accessible location.

Area: 3600 sq. feet.

Distribution channel:

It means the channel through which goods passed from source to destination that is from manufacture to retailer.

Company should pay attention to how the product is distributed. They should have proper distribution channel so that consumers may get rid of the problems regarding unavailability of the product.

Our firm uses the following distribution channel

82

The ready bakery goods are distributed to grocery stores and supermarkets having our dealership. These stores then make the final sale to the consumers.

PROMOTION

83

FACTORY

DEALERS i.e.

SUPERMARKETS AND GROCERY

STORES

CUSTOMERS

Promotion is the part of the marketing mix that many people consider to be "marketing" but this is really the end result of all your hard work in defining products to satisfy needs and pricing it accordingly.

Promotion decisions are those related to communicating and selling to potential consumers.

The success of any business entity depends on how well it has been able to create awareness about its products or services in its target segment so as to induce its consumption by customers.

Promotion is the marketing communication.

There are traditionally 5 promotional tools:

1. Advertisement2. Sales Promotion3. Public relation4. Direct marketing5. Personal Selling

Our firm shall use advertisement tools to create awareness among the public, about our products and the bakery.

ADVERTISEMENTAdvertising is used to build up a long-term image for a product and can reach geographically dispersed buyers.

Advertisement is an informal way of communication which induces customers to buy the product and services and which also creates awareness among consumers.

Types of advertisement:

(a) Informative advertisement : - Informative advertisement is that from which the consumer gets the necessary information about our products and other relevant details.

(b) Influential advertisement : -Influential advertisement shall influence the customers to buy our products.

84

5 M’s OF ADVERTISING

85

ADVERTISING

MONEY

MISSION

MESSAGEMEDIA

MEASUREMENT

1. MISSION:

It is all about setting the advertisement goal in the initial stage.

We have printed information brochures that includes list of our products and varieties, commission rates, terms of sale etc. These shall be distributed to the grocery stores and supermarkets to make them aware of our firm and products and generate their interest in dealership.

Apart from these we shall also advertise by putting up floor signboards at banners at our distributor stores to catch the eye of the public and create awareness and interest about our products.

2. MONEY:

Deciding on the advertising budget

We have considered the following factors while deciding our advertising budget:

a) Stage in life cycle: In the initial stage, our advertising budget is high because we want to introduce our product to the customers and dealers. Afterwards, it will be low compared to the first year.

b) Market share and consumer base: When the firm covers enough market shares, it will require less marketing budget because it will have a set of loyal buyers and recognition in the market.

c) Competition: in the initial stage, we shall face good competition from the well established players in the market, such as Modern breads, Brittannia, Havmor. Therefore, we shall have to advertise more in order to get some public attention.

d) Advertising frequency: When advertising frequency is high, advertising budget will be high and when it is low, required money will be less.

86

3. MESSAGE:

Our message is to give the customer such a delicious taste that they don’t forget hence truly ‘An unforgettable taste’

4. MEDIA:

It includes the decision regarding media vehicles, deciding on media timings and deciding on geographical allocation. Major media types are print media which includes pamphlet, newspapers, hoardings, magazines and television media

Our firm prints pamphlets 4 times in a year to be distributed along with the vernacular newspaper in the areas in which we have tie-ups with the stores.

5. MEASUREMENT

Our company tries to measure the communication effect of an advertisement – that is, its potential effect on awareness, knowledge or preference.

MARKET RESEARCH87

Managers need information in order to introduce products and services that create value in the mind of the customer. But the perception of value is a subjective one, and what customers’ value this year may be quite different from what they value next year. As such, the attributes that create value cannot simply be deduced from common knowledge. Rather, data must be collected and analyzed. The goal of marketing research is to provide the facts and direction that managers need to make their more important marketing decisions.

To maximize the benefit of marketing research, those who use it need to understand the research process and its limitations.

Marketing Research vs. Market Research These terms often are used interchangeably, but technically there is a difference.

Market research deals specifically with the gathering of information about a market's size and trends. It is directed towards a very specific i.e. particular market area,

Marketing research covers a wider range of activities.

While it may involve market research, marketing research is a more general systematic process that can be applied to a variety of marketing problems. It is concerned specifically about marketing process.

Marketing research can be further expanded into two specific domains: consumer-related marketing research and business-to-business marketing (B2B) research.

I. PROBLEM IDENTIFICATION AND DEFINITION

88

This is the introductory phase of the marketing research process. Basically, it involves a clear and precise understanding of the problem at hand. It is crucial that the research team identifies, understands and defines the problem in its entire capacity, as it affects all the subsequent activities involved in the research process. Research teams make use of customer feedback, internal and external data reports, sales graphs, purchasing patterns, etc. to come up with an accurate problem definition.

Problem statement:

The problem statement of this research is to analyze the determinants of the consumer behaviour like income, lifestyle etc. regarding the consumption pattern of bakery products so as to give us a better understanding of the trends of the market.

II. DEVELOPING YOUR APPROACH

Once your problem is better defined, you can move onto developing your approach. Generally speaking, your approach should be developed almost exclusively around a defined set of objectives. This stage includes decisions on the data sources, research approaches, research instruments, sampling plan, and contact methods.

DATA SOURCES

The researcher can gather secondary data, primary data, or both.

Secondary data are data that were collected for another purpose and already exist somewhere.

Primary data are data freshly gathered for a specific purpose or for a specific research project.

Researchers use secondary data to see whether the problem can be partly or wholly solved without collecting costly primary data. When the needed data do not exist or are dated, inaccurate, incomplete, or unreliable, the researcher will have to collect primary data.

The primary source used in our project is surveys each for dealer & consumers.

The secondary data source was the information collected from dealers in the form of pamphlets, internet, marketing books and newspaper articles.

RESEARCH APPROACHES

89

This process mainly involves a lot of field-related work activities such as outdoor interviews, survey campaigns

The instrument used in this project is survey research method.

SURVEY RESEARCH

Surveys are best suited for descriptive research.

Organizations undertake surveys to learn about people’s knowledge, beliefs, preference and satisfaction. Generally questionnaires are used for this.

We have drafted separate questionnaires each for consumers and manufactures of the bakery products, to understand the demand and supply pattern of the bakery industry. Our questionnaire consisted of both open-ended and close-ended questions and covered various decision-making parameters like income, preferences etc.

SAMPLING PLAN

This includes deciding four areas namely:

1. Sampling unit: Who is to be surveyed?

The marketing researcher must define the target population that will be sampled. We have surveyed the people of Ahmedabad city as it is our resident place.

2. Sample size: How many people should be surveyed?

In our survey the primary information is collected through a sample size of 600 consumers and 5 bakeries

3. Sampling procedure: How should the respondents be chosen?

In this project, convenience sampling has been used.

CONTACT METHOD.

The marketing researcher must decide how to contact the subjects: by mail, by telephone, in person or online.

For this research, personal interviews and face-to-face conversations were used as the contact methods.

90

III. COLLECTION OF DATA.Often called data collection or survey fielding, this is the point at which the finalized questionnaire (survey instrument) is used in gathering information among the chosen sample segments.

Finally over a period of time, the data was properly assembled and arranged for analyzing.

IV. ANALYZE THE INFORMATION.The last step is to analyze the information collected in the previous step & present the finding and solutions to our problem statement.

For this, we used mathematical tools such as graphs, summations and percentages. Microsoft Excel was used extensively for the diagrammatic and graphic presentation of data.

91

ANALYSIS

92

Q.1. Approximate monthly family income (in Rs.) :

□ Below 5000 □ 5000 to 15000 □ 15000 to 25000 □ Above 25000

MONTHLY INCOME NUMBER OF RESPONDENTSBELOW 5000 52

5000 TO 15000 18815000 TO 25000 196ABOVE 25000 164

GRAND TOTAL 600

Below 5000; Series1; 52; 9%

5000 to 1500031%

15000 to 25000;

Series1; 196; 33%

Above 2500027%

Distribution of respondents as per income

We can see that majority of the respondents surveyed have annual family monthly income between Rs. 15000 to Rs 25000 i.e. 33%, closely followed by the respondents having annual monthly family income of Rs. 5000 to Rs. 15000, 31%.

93

Q.2. Which of the following bakery products you use ?

□ Breads □ Toasts/ Khari □ Biscuits/ Cookies □ Chocolates □ Cakes/ Pastries □ Other. Please specify______

BAKERY PRODUCTS NO. OF RESPONDENTSBREADS 440

TOASTS/ KHARI 400BISCUITS/ COOKIES 424

CHOCOLATES 398CAKES/ PASTRIES 340

OTHERS 10TOTAL 600

424400

440

398

340

10

DISTRIBUTION OF RESPONDENTS AS PER PRODUCT CONSUMED

Majority of our respondents consume breads among the bakery products, closely followed by biscuits and toasts. Whereas very few respondents lie in other category which includes cream rolls, puffs etc.

94

Q.3. Do you have preference for egg-less bakery products?

□ Yes □ No

PARTICULAR NUMBER OF RESPONDENTSYES 456NO 144

TOTAL 600

YES77%

NO23%

Distribution of respondent as per preference for egg-less products

A large number of the surveyed respondents i.e. 77% have preference for egg-less products while only 23% of the surveyed respondents do not have any such preference.

95

Q.4. Your demand for the following bakery product is:

Demand based Need based (On regular basis) (As and when needed)

1) Breads □ □2) Toast / Khari □ □3) Biscuits/Cookies □ □ 4) Cakes/ Pastries □ □5) Chocolates □ □6) Any other □ □

PRODUCTSNUMBER OF RESPONDENTSREGULAR NEED

BREAD 294 228TOAST 276 276

BISCUIT 376 168CAKES 76 464

CHOCOLATES 230 316OTHER 8 2

Bread; REG-ULAR; 294 Toasts; REG-

ULAR; 276

Biscuits; REG-ULAR; 376

Cakes; REG-ULAR; 76

Chocolates; REGULAR; 230

Others; REG-ULAR; 8

Bread; Need Based; 228

Toasts; Need Based; 276

Biscuits; Need Based; 168

Cakes; Need Based; 464

Chocolates; Need Based;

316

Others; Need Based; 2

DISTRIBUTION OF RESPONDENTS AS PER THE TYPE OF DEMAND

REGULAR Need Based

The above chart shows that bread and biscuits are such bakery product that are consumed on a regular basis i.e. demand based. On the other hand, products like cakes and chocolates, are consumed only when needed and not on a regular basis.

96

Q.5. How did you come to know of this bakery?

□ TV Ad □ Newspapers □ Radio □ Hoarding/Signboard □ Internet □ Friends/ Relatives □ Pamphlets □ Any other

SOURCE OF INFORMATION NUMBER OF RESPONDENTS

T.V. ADVERTISEMENTS 84HOARDINGS/SIGNBOARD 84

NEWSPAPER 88RADIO 24

INTERNET 52PAMPHLETS 52

FRIENDS 346OTHERS 44

TV Ad; Series1; 84;

11%

Hoarding; Series1; 84;

11%

Newspapers; Series1; 88; 11% Radio; Series1; 24; 3%

Internet; Series1; 52;

7%Pamphlets; Series1; 52;

7%

Friends; Series1; 346;

45%

Others; Series1; 44;

6%

DISTRIBUTION OF RESPONDENTS AS PER SOURCE OF INFORMATION

TV Ad Hoarding Newspapers Radio Internet Pamphlets Friends Others

Majority of the respondents surveyed (45%) came to know of the bakery through friends & relatives. TV ads, newspaper & hoardings are the second source of information for the customers with approximate contribution of 11% each.

97

Q.6. Why do you prefer this bakery?

□ Near location □ Good quality □ Affordable prices □ Variety in products □ Brand loyalty □ Any other

REASON FOR PREFERANCENUMBER OF

RESPONDENTSNEAR LOCATION 248GOOD QUALITY 388

PRICES 140BRAND 176

VARIETY 180

Near local area; Series1;

248; 22%

Good quality; Series1; 388; 34%

Prices; Series1; 140;

12%

Brand; Series1; 176;

16% Variety; Series1; 180; 16%

DISTRIBUTION OF RESPONDENTS AS PER REASON OF PREFERENCE

Maximum respondents i.e. 34% prefer purchasing from their respective bakery because of the good quality offered whereas 22% of the respondents prefer the bakery due to near location in their neighborhood.

98

Q.7. Do you buy more bakery products during special occasions and festive seasons? □ Yes □ No

ADDITIONAL PURCHASE

NUMBER OF RESPONDENTS

YES 302NO 298

GRAND TOTAL 600

Yes; Series1; 302; 50%

No; Series1; 298; 50%

DISTRIBUTION AS PER ADDITIONAL PURCHASE DUR-ING FESTIVALS

Our survey reveals that there is an equal distribution between the respondents who purchase more during festive season and those who don’t. Different varieties of biscuits, cookies, chocolates and pastries are among those products whose sales increase during festive seasons like Diwali and Christmas.

99

Q.8. Are you satisfied with the current prices of the bakery products?

□ Yes □ No

PARTICULAR NUMBER OF RESPONDENTS

YES 526NO 74

TOTAL 600

YES88%

NO12%

DISTRIBUTION OF RESPONDENTS AS PER SATIS-FACTION WITH PRICES

It can be clearly seen that, 88% of the respondents surveyed are satisfied with the current prices of the bakery products. 12% of the sample size feels that the prices of certain products like cakes and pastries are high and should be reduced.

Q.9. Would you like to try a new bakery?

100

□ Yes □ No □ Not thought of

PARTICULARNUMBER OF

RESPONDENTSYES 152NO 250

NOT THOUGHT OF 198GRAND TOTAL 600

YES25%

NO42%

NOT THOUGHT OF33%

DISTRIBUTION OF RESPONDENTS AS PER WILLIGNESS TO TRY A NEW BAKERY

Our survey reveals that 25% of the persons surveyed are willing to try a new bakery, while 33% of the sample size have not yet thought about it.

101

FINDINGS AND CONCLUSIONSThe findings from our survey can be listed as:

The demand and consumption for breads is highest among the other bakery products. Hence we have decided to manufacture bread as our key product and offer different varieties to create a brand differentiation.

In Ahmedabad, people prefer egg-less products. Hence no product of ours shall contain eggs.

Good quality of the product is the chief requirement of the customer during purchase, whereas near location and prices occupy a secondary place. Therefore our firm shall concentrate on keeping high quality standards. We shall cater to the guidelines of The Bureau of Indian Standards Act, 1986.

LIMITATIONSOur survey faced certain limitations such as:

The survey is limited to only 600 people of the city of Ahmedabad. The trends stated here may differ in different cities and sample population.

Some of the respondents are reluctant in answering certain questions such as income, leading to a bias in our findings.

102

FINANCIALFEASIBILITY

A STATEMENT SHOWING COST OF PROJECTSR. NO PARTICULAR AMOUNT (in Rs.)

1. Land 16428002. Building 2340000

103

3. Machinery 8793004. Furniture & Fixtures 122100

5. Equipments 3629006. Vehicles 4940007. Preliminary expenses 56800

8. Pre-operative Expenses 1205009. Working Capital 138215

10. Reserves for contingency 61565

TOTAL COST 6218180

MEANS OF FINANCENO. PARTICULAR AMOUNT1. Partners’ capital (50%) 30475252. Secured loans (50%) 31090903. Reserve and surplus 61565

TOTAL 6218180

Note: 1 Cost of Land

No. Particular Amount1. Basic Cost of Land 1480000

104

2. 1% Commission of Agent 14800

3. Stamp duty @ 10% 148000

TOTAL 1642800

Note: 2 Cost of Construction

No Particular Area(in sq. feet) Amount1. Production area 1813 13139502. Storage area 300 2305003. Administrative office 375 3217504. Water room & wash room 244 1746005. Finished goods storage 300 2375006. Loading Dock 168 1097007. Parking space 150 525008. Security cabin 56 274009. Open land 194 102600

TOTAL 3600 2340000

Note: 3 Machinery

No. Particular Quantity Price Amount1 Deck oven 1 264000 2640003 Dough mixer 3 46500 1395004 Dough molder 2 42350 847005 Sugar grinder 1 35000 350006 Packing machine 2 47650 953007 Toast slicer/bread slicer 2 38000 760008 Freezer 2 16400 328009 Mixer 1 3600 360010 Rolling racks 6 7500 4500011 Trays 100 200 2000012 Stainless steel

utensils/tools/equipment knives- - 83400

TOTAL 879300

Note: 4 Cost of Furniture

No. Particular Quantity Price Amount1 Sofa Set 2 10400 20800

105

2 Revolved Chairs 4 1500 60003 Comfort Chairs 8 950 76004 Office desk 3 3000 90005 Office Cupboard 1 8000 80006 Cabinet 1 11300 113007 Working table 1 9000 90008 Dustbin 4 100 4009 Air Conditioner 1 25000 2500010 Lights 50 40 200011 Fans 10 1200 1200012 Exhaust Fans 4 1500 600013 Others 5000

TOTAL 122100

Note: 5 Cost Of equipments

No. Particular Quantity Price Amount1 Computer 3 23900 717002 Telephone instruments 2 600 12003 Fire extinguisher equipment 3 5000 150004 Generator 1 25000 275000

TOTAL 362900

Note: 6 Cost Of Vehicle

No. Particular Quantity Price Amount1 Tempo 2 247000 494000

TOTAL 494000

Note: 7 Preliminary Exp.

No. Particular Amt.1 Licence Fees 350002 Registration Fees (1%) 14800

106

3. Partnership deed 7000TOTAL 56800

Note: 8 Pre-operatives Exp.

No. Particular Amount1 Market Survey Exp. 25002 Connection Charges

1) A.E.C. (Three phase)2) Electricity connection charges

3) Plumbing4) Telephone charges

5) Gas pipe line charges

480001850090002500

40000

TOTAL 120500

DEPRECIATIONPARTICULARS 1ST 2ND 3RD YEAR 4TH 5TH

107

YEAR YEAR YEAR YEARMACHINERIES 15%Op balance 879300 747405 635294 540000 459000Less: depreciation 131895 112111 95294 81000 68850Closing balance 747405 635294 540000 459000 390150BUILDING 10%Op balance 2340000 2106000 1895400 1705860 1535274

Less: depreciation 234000 210600 189540 170586 153527Closing balance 2106000 1895400 1705860 1535274 1381747FURNITURE 10%Op balance 122100 109890 98901 89011 80110Less: depreciation 12210 10989 9890 8901 8011Closing balance 109890 98901 89011 80110 72099VEHICLE 40%Op balance 494000 296400 177840 106704 64022Less: depreciation 197600 118560 71136 42682 25609Closing balance 296400 177840 106704 64022 38413COMPUTERS 60%

Op balance 71700 28680 11472 4589 1836Less: depreciation 43020 17208 6883 2753 1101Closing balance 28680 11472 4589 1836 735Total depreciation

618725 469468 372743 305922 257099

Add Tempo -------- -------- 247000 148200 88920Less: depreciation -------- -------- 98800 59280 35568Closing balance -------- -------- 148200 88920 53352

TOTAL DEPRECIATION

618725 469468 471543 365202 292667

SALARYParticular

sNo. Monthl

y salary1ST

YEAR2ND

YEAR3RD

YEAR4TH

YEAR5TH

YEARFactory 1 13000 15600 156000 156000 163800 163800

108

manager 0Finance manager

1 13000 156000

156000 156000 163800 163800

Accountant 1 10000 ----------

120000 120000 120000 126000

Marketing manager

1 13000 156000

156000 156000 163800 163800

Production supervisor

1 8000 96000 96000 96000 100800 100800

Master baker

1 4500 54000 54000 54000 54000 54000

Utility workers

Varies

3500 210000

210000 420000 420000 546000

Drivers 2 3000 72000 72000 108000 110160 110160Security guard

1 3000 36000 36000 36000 37080 37080

Peon 1 3000 36000 36000 36000 37080 37080Total 13 64000 97200

0109200

0133800

0137052

0150252

0

BONUSParticulars No 1ST

YEAR2ND

YEAR3RD YEAR 4TH

YEAR5TH

YEARFactory manager

1 13000 13000 13000 13650 13650

Financial manager

1 13000 13000 13000 13650 13650

Marketing manager

1 13000 13000 13000 13650 13650

Accountant 1 ------ 12000 12000 12000 12600Production supervisor

1 8000 8000 8000 8400 8400

Master baker 1 4500 4500 4500 4500 4500Utility workers Varies 17500 17500 35000 35000 41000Drivers 2 6000 6000 9000 9300 9300Security guard 1 3000 3000 3000 3150 3150Peon 1 3000 3000 3000 3150 3150

Total 13 81000 93000 113500 116450 123050

FACTORY OVERHEAD EXPENSES109

PARTICULARS 1ST

YEAR2ND YEAR 3RD YEAR 4TH YEAR 5TH YEAR

SalaryFactory manager 156000 156000 156000 163800 163800Production supervisor

96000 96000 96000 100800 100800

Peon 36000 36000 36000 37080 37080Security guard 36000 36000 36000 37080 37080

BonusFactory manager 13000 13000 13000 13650 13650Supervisor 8000 8000 8000 8400 8400Peon 3000 3000 3000 3150 3150Security guard 3000 3000 3000 3150 3150

DepreciationMachinery 131895 112111 95294 81000 68850Building 234000 210600 189540 170586 153527

Insurance

Machinery 13190 11211 9529 8100 6885Building 4680 4212 3791 3412 3071Electricity charges 2,21,000 225694 285415 233598 235690Power and fuel 180000 205141 225984 226983 285741

Repairs and maintenance

Building 2340 2340 2340 2340 2340Machinery 8790 8790 8790 8790 8790

TOTAL 1146895 1131099 1171683 1101919 1041284

ADMINISTRATIVE OVERHEADS110

PARTICULARS 1ST

YEAR2ND YEAR 3RD YEAR 4TH YEAR 5TH YEAR

SalaryAccountant 120000 120000 120000 126000Finance manager 156000 156000 156000 163800 163800

BonusAccountant 12000 12000 12000 12600Finance manager 13000 13000 13000 13650 13650

DepreciationComputer 43020 17208 6883 2753 1101Furniture 12210 10989 9890 8901 8011Telephone 26000 17750 15310 21680 15650Stationery 5000 6550 6854 7045 7520Electricity charges 90000 92546 93568 94871 95862

TOTAL 345230 446043 433505 444700 444194

SELLING & DISTRIBUTION OVERHEADParticulars 1ST

YEAR2ND

YEAR3RD

YEAR4TH

YEAR5TH

YEARSalary

Marketing manager

156000 156000 156000 163800 163800

Driver 72000 72000 108000 110160 110160Bonus

Marketing Manager

13000 13000 13000 13650 13650

Driver 6000 6000 9000 9300 9300Depreciation of vehicle

197600 118560 169936 101962 61177

Fuel & maintenance of vehicle

155200 160580 165847 178450 182560

Advertisement 18500 20500 25000 25000 27000Commission on sales

175800 205150 226680 258100 269750

Insurance of vehicle

17290 15215 22034 16970 13481

TOTAL 811390 767005 895497 877392 850878

111

REPAYMENT OF LOANYear Principle

RemainingInstallment

PaidInterest Total Amt.

PaidBalance ofPrinciple

1st Year 3109090 621818 342000 963818 24872722nd Year 2487272 621818 273600 895418 18654543rd Year 1865454 621818 205200 827018 12436364th Year 1243636 621818 136800 758618 6218185th Year 621818 621818 68400 690218 _

TOTAL 3109090 1026000 4135090

STATEMENT OF INTEREST ON PARTNERS’ CAPITAL

Particular 1st Year 2nd Year 3rd Year 4th Year 5th YearOpening balance of capital

3047525 3136287 3581981 4063263 5027221

Add: Interest 182852 188177 214919 243796 301633Add: Profit 88762 445694 481282 963958 1091076

3319139 3770158 4278182 5271017 6419930Less: Interest (182852) (188177) (214919) (243796) (301633)

TOTAL 3136287 3581981 4063263 5027221 6118297

COST SHEET112

Particular 1st Year 2nd Year 3rd Year 4th Year 5th Year

Opening Stock of R.M. 0 30270 35200 38950 42150

Add:- Purchases 4540510 5297170 5853040 6664340 6964530Less:- Cl.

Stock of R.M. 30270 35200 38950 42150 45890Cost Of R.M. Consumed 4510240 5292240 5849290 6661140 6960790

Add:-Direct Labour 264000 264000 474000 474000 600000

Bonus 22000 22000 39500 39500 45500Prime Cost 4796240 5578240 6362790 7174640 7606290

Add:-Factory O.H. 1146895 1131099 1171683 1101919 1041284

Total Factory Cost 5722135 6709339 7534473 8276559 8647574Add:-

Office O.H. 345230 44604ss3 433505 444700 444194Cost of

Production 6067365 7155382 7967978 8721259 9091768Add:-

Opening stock of FG - 25870 27850 29950 30500Less:-

Closing Stock of FG 25870 27850 29950 30500 32950

Cost of Sales 6041495 7127532 7938028 8690759 9058818Add:- Selling & Distribution

Exp 811390 767005 895497 877392 850878Cost of

goods sold 6852885 7894537 8833525 9568151 9909696Add:- Profit 908115 1159813 1170975 1823089 1994674

TOTAL SALES

7761000 9054350 10004500 11391240 11904370

TRADING AND PROFIT & LOSS A/C113

Particulars 1st Year 2nd Year 3rd Year 4th Year 5th YearINCOME:-Cash Sales 7114250 8201750 8978600 10132840 10419370Credit Sales 646750 852600 1025900 1258400 1485000Total Sales Income 7761000 9054350 10004500 11391240 11904370Closing Stock of FG 25870 27850 29950 30500 32950Less:- Opening Stock of FG ------ 25870 27850 29950 30500Total Income 7786870 9056330 10006600 11391790 11906820Raw Material Consumed 4510240 5292240 5849290 6661140 6960790Direct Labour & Bonus 286000 286000 513500 513500 645500Factory Cost 781000 808388 886849 850333 818907Administrative Cost 290000 417846 416732 433046 435082Selling & Distribution Cost 613790 648445 725561 775430 789701Preliminary Expenses Written Off 35460 35460 35460 35460 35460Interest on Partners' Capital 182852 188177 214919 243796 301633Total Expenditure 6699342 7676556 8642311 9512705 9987073Gross Profit(PBDIT) 1087528 1379774 1364289 1879085 1919747Less:- Depreciation 618725 469468 471543 365202 292667PBIT 468803 910306 892746 1513883 1627080Interest- Long Term Loan @ 11% 342000 273600 205200 136800 68400PBT 126803 636706 687546 1377083 1558680Tax Paid @ 30% 38041 191012 206264 413125 467604

PAT 88762 445694 481282 963958 1091076BALANCE SHEET

114

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

SOURCE OF FUNDS

Owners Funds 3136287 3581981 4063263 5027221 6118297Reserve & Surplus

61565 61565 61565 61565 61565

Bank Loan 2487272 1865454 1243636 621818 0TOTAL SOURCE OF FUND

5685124 5509000 5368464 5710604 6179862

APPLICATION OF FUNDS

Fixed AssetsLand 1642800 1642800 1642800 1642800 1642800Building 2340000 2106000 1895400 1705860 1535274Less: Depreciation

234000 210600 189540 170586 153527

2106000 1895400 1705860 1535274 1381747Machinery 879300 747405 635294 540000 459000Less: Depreciation

131895 112111 95294 81000 68850

747405 635294 540000 459000 390150Furniture 122100 109890 98901 89011 80110Less: Depreciation

12210 10989 9890 8901 8011

109890 98901 89011 80110 72099Vehicle 494000 296400 424840 254903 152941Less: Depreciation

197600 118560 169937 101962 61177