Embed Size (px)

Citation preview

Why do some MNCs relocate their headquarters overseas?

Julian Birkinshaw, LBS

Pontus Braunerhjelm, SNS

Ulf Holm, Uppsala

Siri Terjesen, LBS

Motivation for paper

• Increasing number of cases of MNCs moving HQs activities overseas – Ericsson, BHP-Billiton, Massey-Ferguson

• No prior studies of corporate HQ moving overseas

• Important implications for practice, and for the theory of the MNC

• Guiding question: How can we explain the internationalization of corporate HQs?

Background

• Literature on the role of the corporate HQ in the multi-business corporation– Corporate HQ often viewed as “middleman” between

business units and capital markets

• Definition of corporate HQ: consists of three elements– Legal entity– Top management team– Corporate functions (treasury, investor relations etc)

– Increasingly these three elements are not co-located

Traditional arguments for relocating corporate HQ overseas• Evolutionary process - corporate HQ

follows other activities overseas

• Location-specific factors – corporate HQ location depends on relative attractiveness of potential host countries

• Situation-specific reasons – merger, tax reasons etc.

Our argument for relocating corporate HQ overseas

• Corporate HQ sits between business units and external stakeholders (shareholders, customers, competitors)

• Historically, HQ co-located with business units

• Increasing globalization – corporate HQs more influenced by relative importance of internal and external stakeholders

Corp. HQ

Business Units

External stakeholders

Organization theory perspectives

• Resource dependency theory: Corporate HQ may move closer to major commercial centres to reduce their dependency on specific actors

• Institutional theory: Corporate HQ may move to signal its membership of a global industry group

• These theories provide complementary perspectives on underlying reasons why corporate HQ may move overseas

Hypotheses

H1. The greater the percentage of business unit activities overseas (sales, mfg, R&D), the more international the corporate HQ will be

H2. The less attractive Sweden is perceived as a location for corporate HQ, the more international corporate HQ will be

H3. The greater the international influence from shareholders (stock listings, % foreign) the more international corporate HQ will be

H4. The greater the international influence from customers (% outside Sweden, % outside Europe), the more international corporate HQ will be

H5. The greater the international influence from competitors (% outside Sweden, % outside Europe), the more international corporate HQ will be

Research Methods & Data

• Focused on largest 40 “Swedish” MNCs, 35 participated in the study

• Detailed questionnaire filled in, plus secondary data on shareholders, customers etc.

• HQ internationalization measured using– Categorical measure of legal domicile (6 of 35

overseas)– Continuous measure – combination of % functional

activities outside Sweden, % HQ employees outside Sweden, % top management and board non-Swedish

Results – correlates of HQ internationalization

• Some support for H1 – Percent R&D units abroad significant (r=.45), but percent sales and

manufacturing not significant

• No support for H2– Quality of Swedish government, Swedish cluster, taxation all non-

significant

• Strong support for H3– Overseas listing, number of exchanges, % foreign shareholders all

significant (r=.38, r=.41, r=.42)

• Strong support for H4– Sales outside Sweden, outside Europe both significant (r= .52, r=.46)

• Some support for H5– Percentage competitors outside Sweden significant (r=.41)

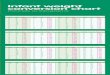

Results – multivariate analysisPredictors of HQ internationalization

Sales volume (control)

-.192

Percent foreign shareholders

.465**

Primary exchange abroad

.394*

Sales outside Sweden

.309†

Competitors outside Sweden

-.155

R-squared / Adjusted

.57 / .48

F 6.63***

Discussion / Conclusions

• Good support for argument that corporate HQ moves overseas in response to external influences

• Little support for traditional logic that HQ follows business activities overseas, or for purely locational reasons

• Need to extend this research to consider the relatedness of the corporation