Embed Size (px)

Citation preview

Why Events Overseas Matter to Gasoline Retailers and Consumers

WTI and Retail Gasoline Prices Generally Move In Unison

10

15

20

25

30

35

40

Jan

-00

Ap

r-00

Jul-

00

Oct

-00

Jan

-01

Ap

r-01

Jul-

01

Oct

-01

Jan

-02

Ap

r-02

Jul-

02

Oct

-02

Jan

-03

Ap

r-03

Jul-

03

Oct

-03

Do

llar

s P

er B

arre

l

100

125

150

175

Cen

ts p

er G

allo

n

Retail Gasoline Price

WTI Spot Price

What Comprises theGasoline Price?

43%

23%

26%

8%

Taxes

Distribution &Marketing Costsand Profits

Refining Costs andProfits

Crude Oil

Retail $1.62 August 2003

Spot Gasoline Price

Glo

bal

Reg

ion

al

Main Reasons BehindGasoline Price Spikes

• High Crude Oil Prices, and/or

• Regional Gasoline Infrastructure Problems, and/or

• High Demand with Low Inventories

Analysis of 3 Recent Gasoline Price Spikes

• Midwest Price Spike of 2001

• March 2003 Price Spike

• August 2003 Price Spike

Analysis of 3 Recent Gasoline Price Spikes

• Midwest Price Spike of 2001

• March 2003 Price Spike

• August 2003 Price Spike

Low Total OECD Oil Stocks* Keep Market Balance Tight

*Total includes commercial and government stocks.

3,400

3,500

3,600

3,700

3,800

3,900

4,000

4,100

Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00

Mil

lio

n B

arre

ls

Normal Actual

OECD Total Petroleum Inventories

Source: Energy Information Administration, April 2001.

OPEC 10 Production Cutin First Half of 2001

0

5 0

1 9 9

9 Q 1

2 0 0

1 Q 4

OPEC 10 (OPEC excluding Iraq) Iraq0

5 0

1 9 9 9 Q 1 2 0 0 1 Q 3

OPEC 10 (OPEC excluding Iraq) Iraq

0

5 0

1 9 9

9 Q 1

2 0 0

1 Q 4

OPEC 10 (OPEC excluding Iraq) Iraq

15

17

19

21

23

25

27

29

31

'98 Q1 '98 Q3 '99 Q1 '99 Q3 '00 Q1 '00 Q3 '01 Q1

Mill

ion

Ba

rre

ls p

er

Da

y

OPEC 10 Crude Oil Production Iraq

Source: Energy Information Administration.

Quarterly World Oil Demand Growth from Previous Year

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01

Mil

lio

n B

arre

ls p

er D

ay

Source: Energy Information Administration.

Overview of Market Fundamentals• Tight balance in global petroleum market • Tight balance means low inventories• Low inventories mean upward price pressure

and potential for increased volatility• Exacerbating regional volatility factors

– Refinery system runs near maximum during summer

– U.S. distribution system showing signs of strain -- local ramifications

– Increasing distinct types of gasoline

• All of the above contributing to prices this year

Midwest RFG Prices RiseDue to Tight Supplies

0

20

40

60

80

100

120

140

160

180

Feb-1 Mar-1 Apr-1 May-1 Jun-1 Jul-1 Aug-1

Cen

ts P

er G

allo

n

Chicago RBOB Daily Spot Prices

20002001

Source: Reuters database.

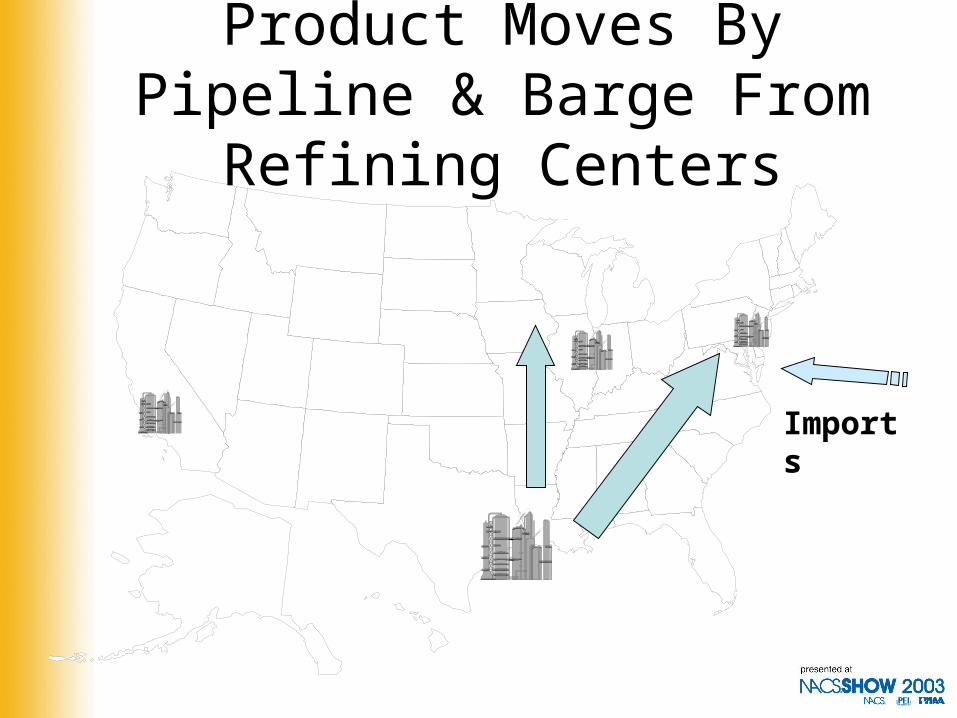

Product Moves By Pipeline & Barge From Refining Centers

Imports

Dependence on Distant Supply Can Increase Response Time

78%

28%

100%

22%

52%

16%

0%

25%

50%

75%

100%

Midwest East Coast Gulf Coast

Net Imports

Other USRegionalSupply

LocalProduction

Stock Draw

Typical July Supply as Percent of Demand

Source: Energy Information Administration.

Analysis of 3 Recent Gasoline Price Spikes

• Midwest Price Spike of 2001

• March 2003 Price Spike

• August 2003 Price Spike

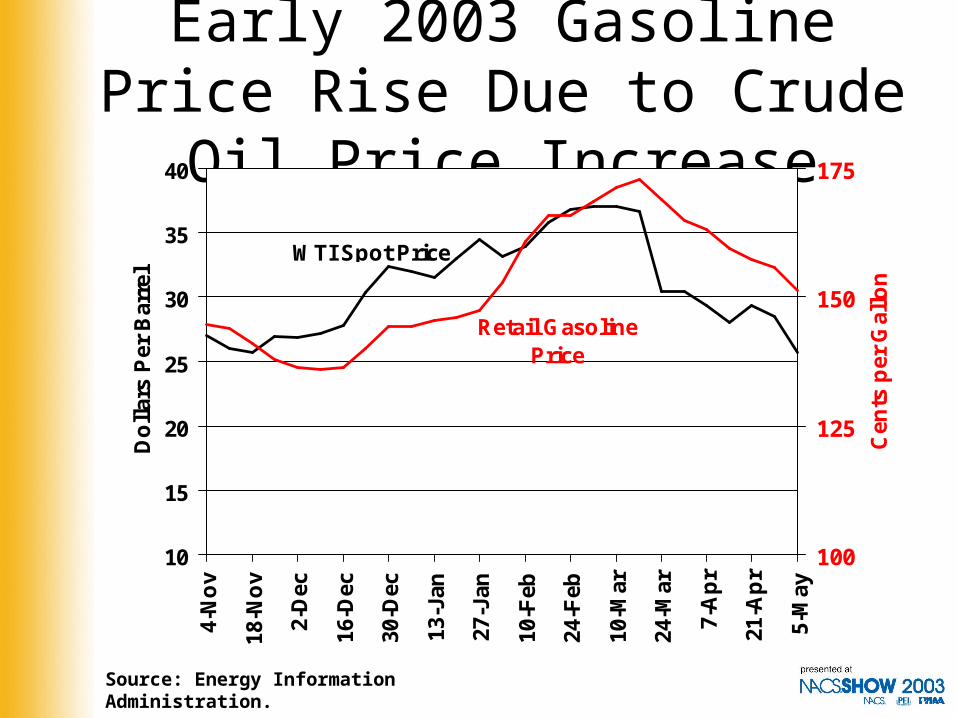

Early 2003 Gasoline Price Rise Due to Crude Oil Price Increase

10

15

20

25

30

35

40

4-N

ov

18-N

ov

2-D

ec

16-D

ec

30-D

ec

13-J

an

27-J

an

10-F

eb

24-F

eb

10-M

ar

24-M

ar

7-A

pr

21-A

pr

5-M

ay

Do

llar

s P

er B

arre

l

100

125

150

175

Cen

ts p

er G

allo

n

Retail Gasoline Price

WTI Spot Price

Source: Energy Information Administration.

OPEC 10 Production Much Lower in December and January

0

5 0

1 9 9

9 Q 1

2 0 0

1 Q 4

OPEC 10 (OPEC excluding Iraq) Iraq0

5 0

1 9 9 9 Q 1 2 0 0 1 Q 3

OPEC 10 (OPEC excluding Iraq) Iraq

0

5 0

1 9 9

9 Q 1

2 0 0

1 Q 4

OPEC 10 (OPEC excluding Iraq) Iraq

15

16

17

18

19

20

21

22

23

24

25

Oct '02 Nov '02 Dec '02 Jan '03

Millio

n B

arr

els

pe

r D

ay

Mar 2003 STEO Dec 2002 STEO

Sources: History: EIA; Projections: Short-Term Energy Outlook (STEO).

Crude Oil Production forVenezuela and Saudi Arabia

Sources: History: EIA; Projections: Short-Term Energy Outlook (STEO).

Venezuela Crude Oil Production

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

J-0

2

M-0

2

M-0

2

J-0

2

S-0

2

N-0

2

J-0

3

M-0

3

Mill

ion

Ba

rre

ls p

er

Da

y

Estimate Before VZ Strikes

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

J-0

2

M-0

2

M-0

2

J-0

2

S-0

2

N-0

2

J-0

3

M-0

3

Mill

ion

Ba

rre

ls p

er

Da

y

Saudi Arabia Crude Oil Production

Estimate Before VZ Strikes

2.3

2.4

2.5

2.6

2.7

2.8

2.9

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Bil

lio

n B

arre

ls

NOTE: Colored Band is Normal Stock Range

OECD Commercial Inventories

2003

Dec 2002 STEO

OECD Commercial Oil Stocks Remain Below Average in 2003

Source: International Energy Agency database, January 2003 andEIA’s Short-Term Energy Outlook, March 2003.

U.S. Crude Oil Inventories

260

270

280

290

300

310

320

330

340

350

360

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mil

lio

n B

arre

ls

Crude Oil Lower Operational Inventory

NOTE: Colored Bands are Normal Stock Ranges

Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2003.

2003

U.S. Total Gasoline Inventories

180

190

200

210

220

230

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mil

lio

n B

arre

ls

Gasoline Lower Operational Inventory

NOTE: Colored Band is Normal Stock Range

Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2003.

2003

Analysis of 3 Recent Gasoline Price Spikes

• Midwest Price Spike of 2001

• March 2003 Price Spike

• August 2003 Price Spike

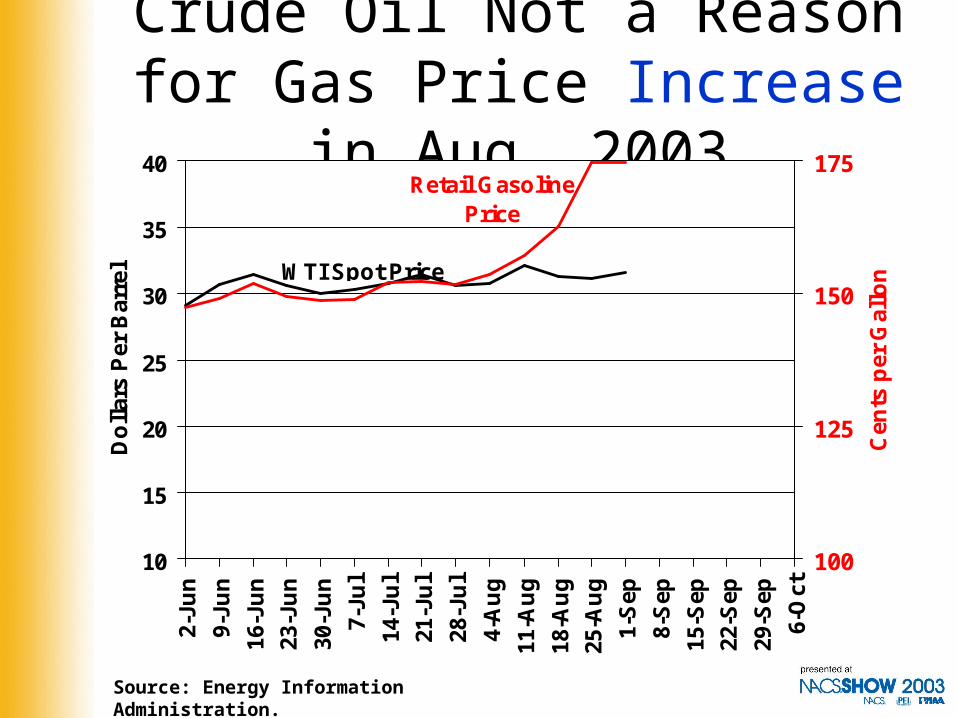

Crude Oil Not a Reason for Gas Price Increase in Aug. 2003

10

15

20

25

30

35

402-

Jun

9-Ju

n

16-J

un

23-J

un

30-J

un

7-Ju

l

14-J

ul

21-J

ul

28-J

ul

4-A

ug

11-A

ug

18-A

ug

25-A

ug

1-S

ep

8-S

ep

15-S

ep

22-S

ep

29-S

ep

6-O

ct

Do

llar

s P

er B

arre

l

100

125

150

175

Cen

ts p

er G

allo

n

Retail Gasoline Price

WTI Spot Price

Source: Energy Information Administration.

Reasons Behind August 2003 Gasoline Price Increase

• Tight Market– Record Gasoline Demand– Low Gasoline Inventories

• Refinery Outages– Due to Power Blackout in Midwest– California– East Coast

• Kinder-Morgan Pipeline Rupture in Arizona

Gasoline Refinery ProductionAcross Three Regions

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.26-

Jun

13-J

un

20-J

un

27-J

un

4-Ju

l

11-J

ul

18-J

ul

25-J

ul

1-A

ug

8-A

ug

15-A

ug

22-A

ug

29-A

ug

5-S

ep

12-S

ep

19-S

ep

26-S

ep

3-O

ct

Mil

lio

n B

arre

ls p

er D

ay

East Coast

West Coast

Midwest

Source: Energy Information Administration.

Gasoline Demand ReachedRecord Levels in August 2003

8

9

9

10

104

-Ja

n1

-Fe

b1

-Ma

r2

9-M

ar

26

-Ap

r2

4-M

ay

21

-Ju

n1

9-J

ul

16

-Au

g1

3-S

ep

11

-Oc

t8

-No

v6

-De

c3

-Ja

n3

1-J

an

28

-Fe

b2

8-M

ar

25

-Ap

r2

3-M

ay

20

-Ju

n1

8-J

ul

15

-Au

g1

2-S

ep

Mil

lio

n B

arr

els

pe

r D

ay

Source: Energy Information Administration.

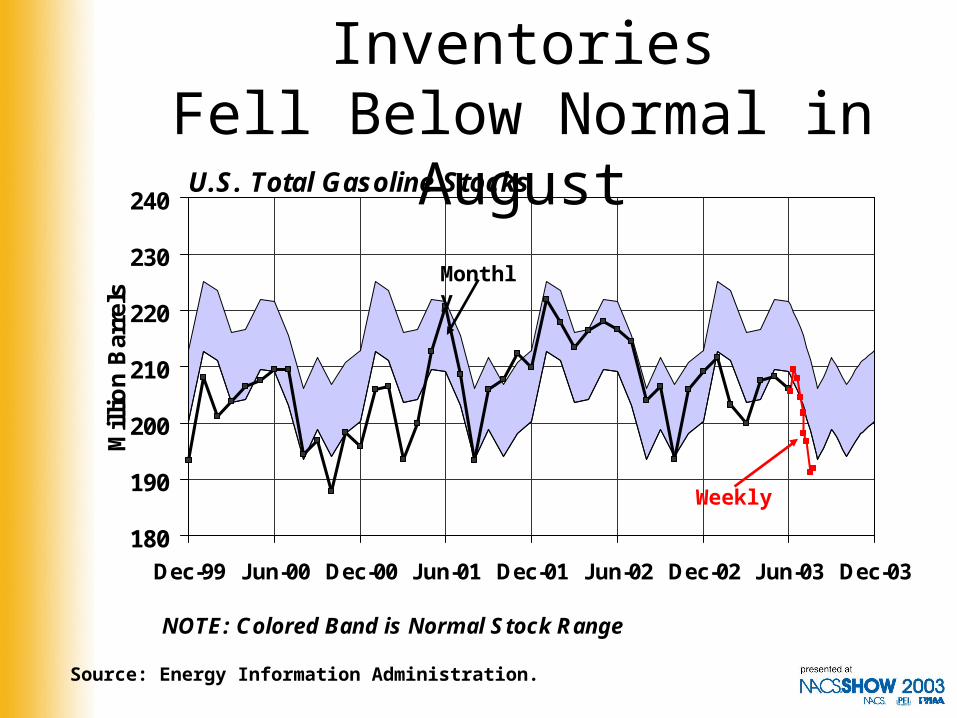

180

190

200

210

220

230

240

Dec-99 Jun-00 Dec-00 Jun-01 Dec-01 Jun-02 Dec-02 Jun-03 Dec-03

Mil

lio

n B

arre

ls

NOTE: Colored Band is Normal Stock Range

U.S. Total Gasoline Stocks

U.S. Gasoline InventoriesFell Below Normal in August

Monthly

Source: Energy Information Administration.

Weekly

Regular Gasoline Spot Prices

60

70

80

90

100

110

120

130

140

150

160

170

1/2/

2003

2/2/

2003

3/2/

2003

4/2/

2003

5/2/

2003

6/2/

2003

7/2/

2003

8/2/

2003

9/2/

2003

Cen

ts p

er G

allo

n

NYH RFGUSG Conv.Chi. Conv.LA CARBWTI c/gal

Source: Reuters database.

Gasoline Price Rise Varied Among Locations

Source: American Automobile Association

40.6

42.2

6.2

16.0

15.2

30.8

20.6

18.2

15.3

15.6

22.1

25.1

21.031.9

Numbers represent the difference, in cents per gallon, of the average price for retail regular gasoline between Aug. 29, 2003 and Aug. 1, 2003.

Important Web Sites

• From EIA– Gasoline and Diesel Fuel Update (Prices)– This Week In Petroleum– Weekly Petroleum Status Report– A Primer on Gasoline Prices (an EIA

Gasoline Brochure)

• AAA Prices by State and Locality– (http://www.aaanewsroom.net/Main.asp)