Embed Size (px)

Citation preview

Strictly Private and Confidential

Why Mining & Metals in Africa ?

25 October 2010

2

Table of contents

SECTIONS Page

1. Africa as a mining destination 3

2. Challenges Facing Mining in Africa 8

3. Trade with Africa 11

4. Chinese investment in infrastructure ? 15

5. What Africa needs 17

Disclaimer 21

3

Section 1

Africa as a mining destination

4

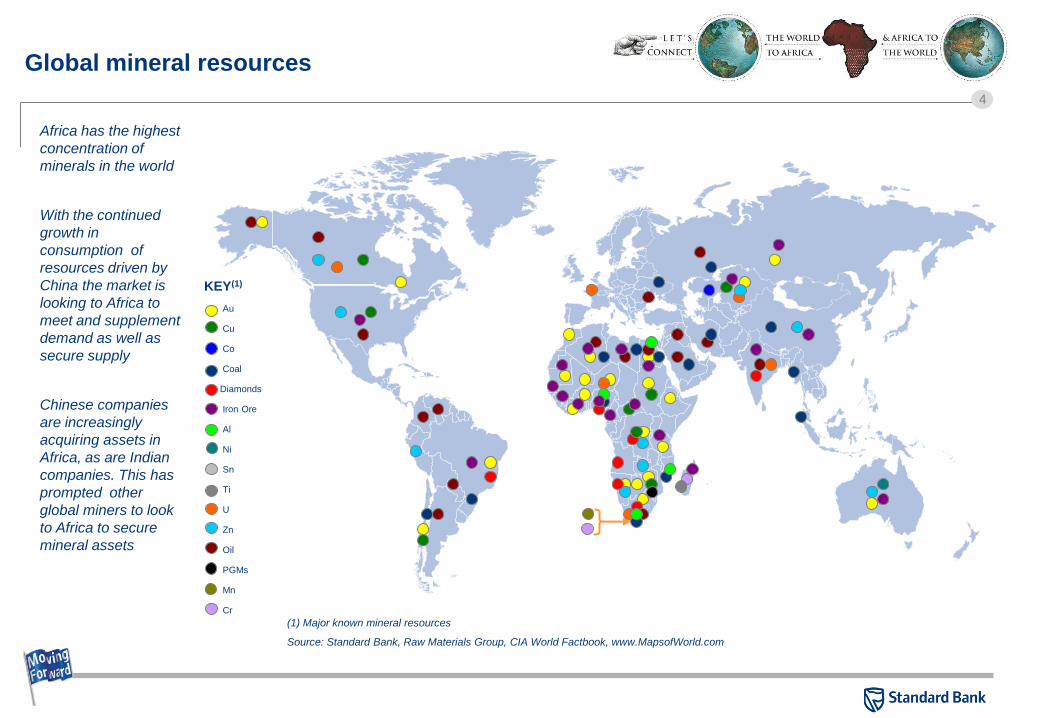

Global mineral resources

(1) Major known mineral resources

Source: Standard Bank, Raw Materials Group, CIA World Factbook, www.MapsofWorld.com

Africa has the highest

concentration of

minerals in the world

With the continued

growth in

consumption of

resources driven by

China the market is

looking to Africa to

meet and supplement

demand as well as

secure supply

Chinese companies

are increasingly

acquiring assets in

Africa, as are Indian

companies. This has

prompted other

global miners to look

to Africa to secure

mineral assets

KEY(1)

Au

Cu

Co

Coal

Diamonds

Iron Ore

Al

Ni

Sn

Ti

U

Zn

Oil

PGMs

Mn

Cr

5

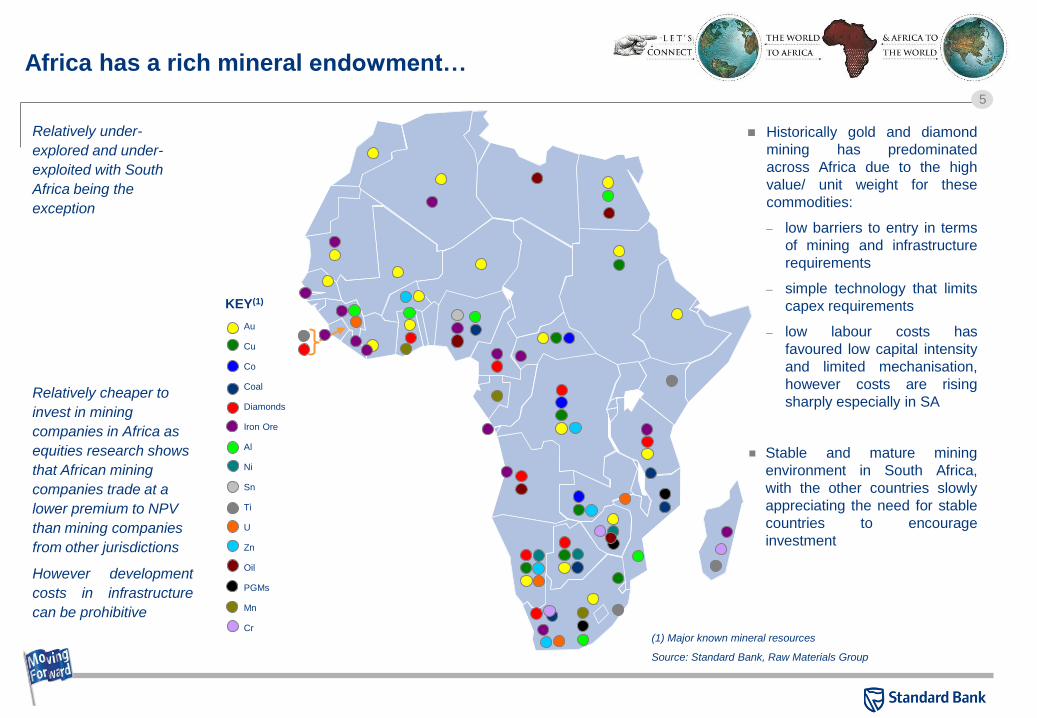

Africa has a rich mineral endowment…

(1) Major known mineral resources

Source: Standard Bank, Raw Materials Group

Historically gold and diamond

mining has predominated

across Africa due to the high

value/ unit weight for these

commodities:

– low barriers to entry in terms

of mining and infrastructure

requirements

– simple technology that limits

capex requirements

– low labour costs has

favoured low capital intensity

and limited mechanisation,

however costs are rising

sharply especially in SA

Stable and mature mining

environment in South Africa,

with the other countries slowly

appreciating the need for stable

countries to encourage

investment

Relatively under-

explored and under-

exploited with South

Africa being the

exception

Relatively cheaper to

invest in mining

companies in Africa as

equities research shows

that African mining

companies trade at a

lower premium to NPV

than mining companies

from other jurisdictions

However development

costs in infrastructure

can be prohibitive

KEY(1)

Au

Cu

Co

Coal

Diamonds

Iron Ore

Al

Ni

Sn

Ti

U

Zn

Oil

PGMs

Mn

Cr

6

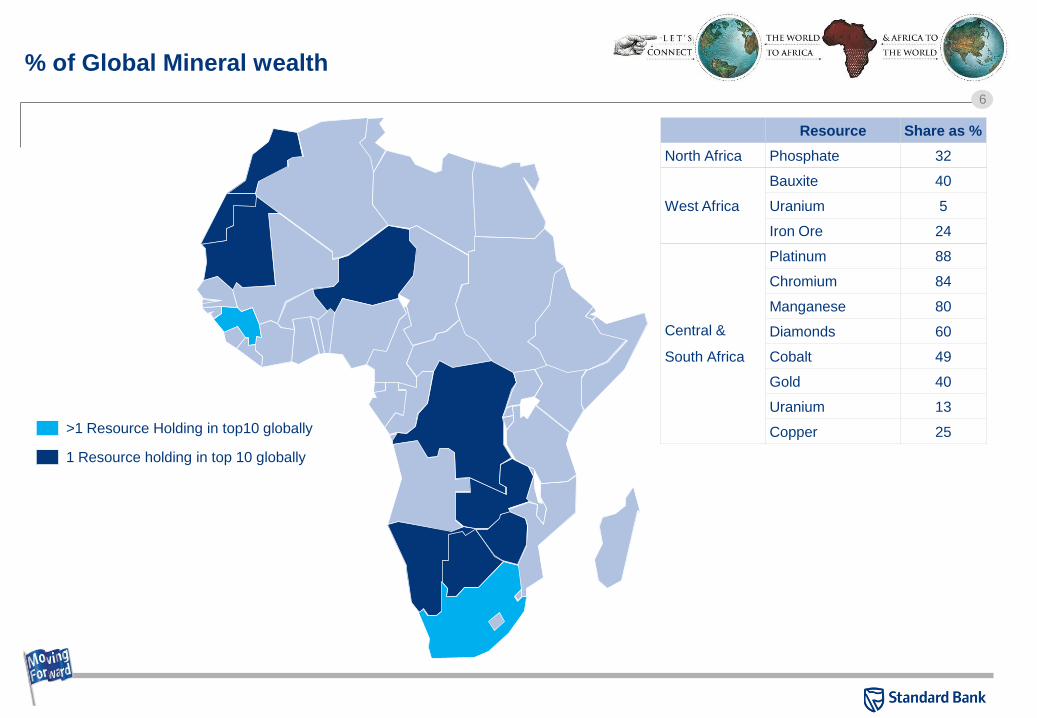

% of Global Mineral wealth

>1 Resource Holding in top10 globally

1 Resource holding in top 10 globally

Resource Share as %

North Africa Phosphate 32

West Africa

Bauxite 40

Uranium 5

Iron Ore 24

Central &

South Africa

Platinum 88

Chromium 84

Manganese 80

Diamonds 60

Cobalt 49

Gold 40

Uranium 13

Copper 25

7

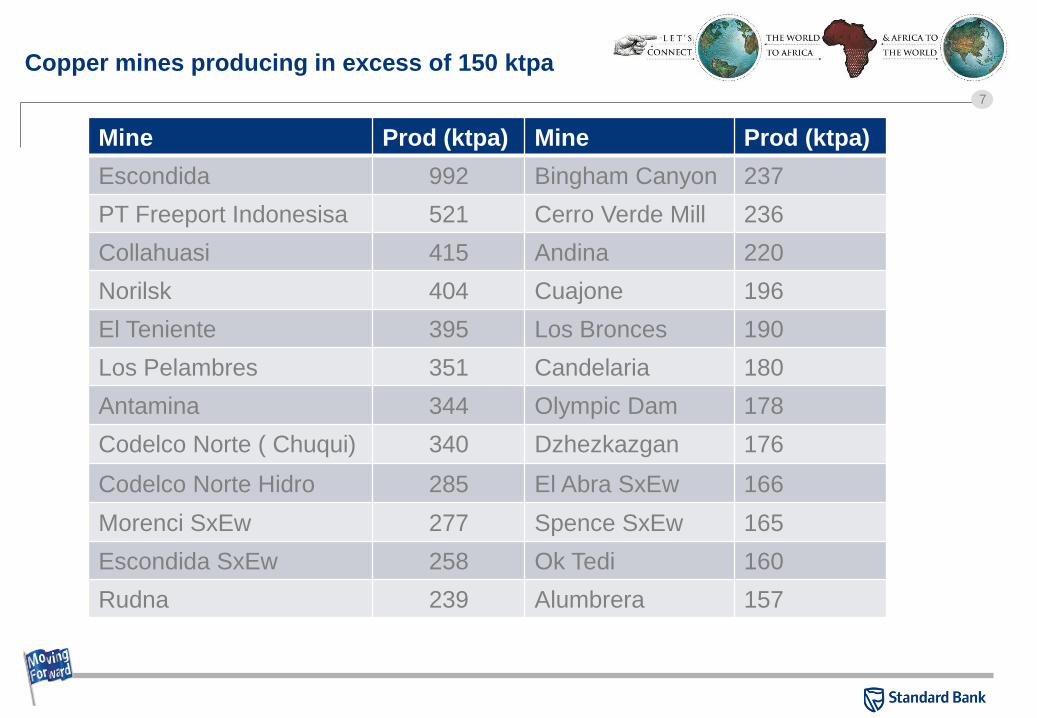

Copper mines producing in excess of 150 ktpa

Mine Prod (ktpa) Mine Prod (ktpa)

Escondida 992 Bingham Canyon 237

PT Freeport Indonesisa 521 Cerro Verde Mill 236

Collahuasi 415 Andina 220

Norilsk 404 Cuajone 196

El Teniente 395 Los Bronces 190

Los Pelambres 351 Candelaria 180

Antamina 344 Olympic Dam 178

Codelco Norte ( Chuqui) 340 Dzhezkazgan 176

Codelco Norte Hidro 285 El Abra SxEw 166

Morenci SxEw 277 Spence SxEw 165

Escondida SxEw 258 Ok Tedi 160

Rudna 239 Alumbrera 157

8

Section 2

Challenges Facing Mining in Africa

9

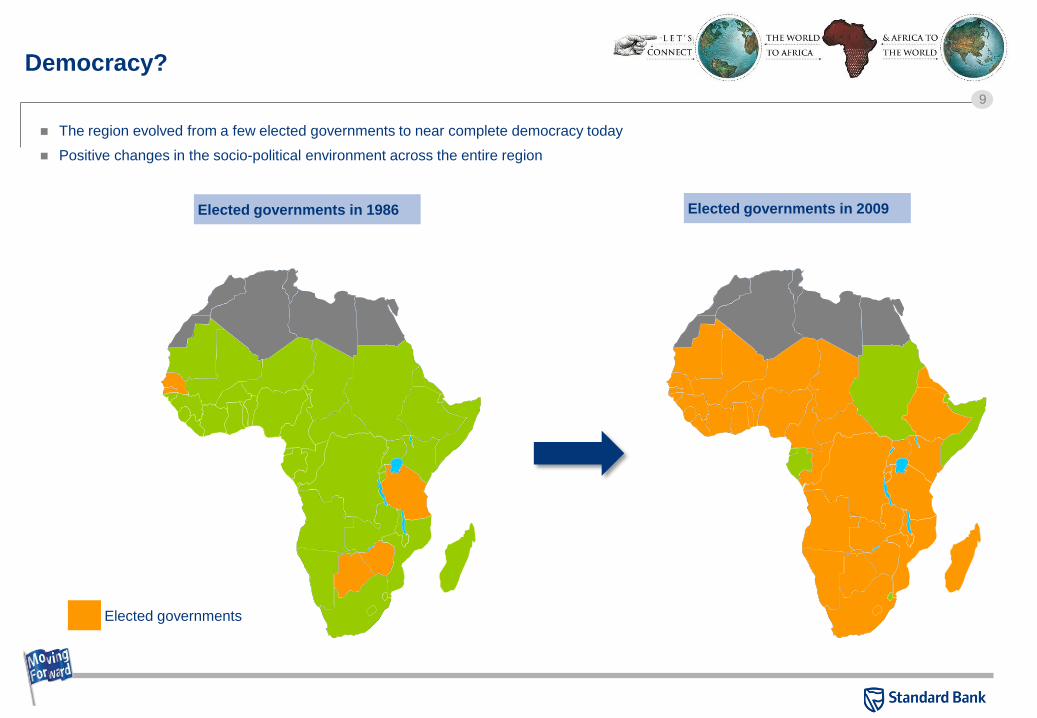

Democracy?

The region evolved from a few elected governments to near complete democracy today

Positive changes in the socio-political environment across the entire region

Elected governments

Elected governments in 1986 Elected governments in 2009

10

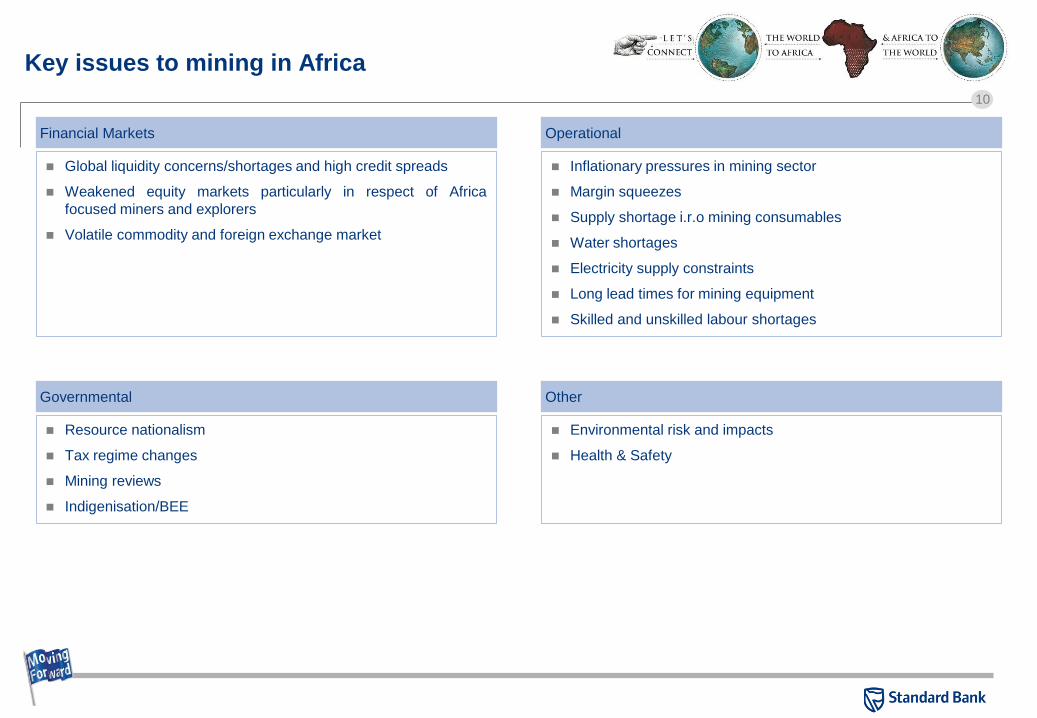

Key issues to mining in Africa

Financial Markets Operational

Global liquidity concerns/shortages and high credit spreads

Weakened equity markets particularly in respect of Africa

focused miners and explorers

Volatile commodity and foreign exchange market

Inflationary pressures in mining sector

Margin squeezes

Supply shortage i.r.o mining consumables

Water shortages

Electricity supply constraints

Long lead times for mining equipment

Skilled and unskilled labour shortages

Governmental Other

Resource nationalism

Tax regime changes

Mining reviews

Indigenisation/BEE

Environmental risk and impacts

Health & Safety

11

Section 3

Trade with Africa

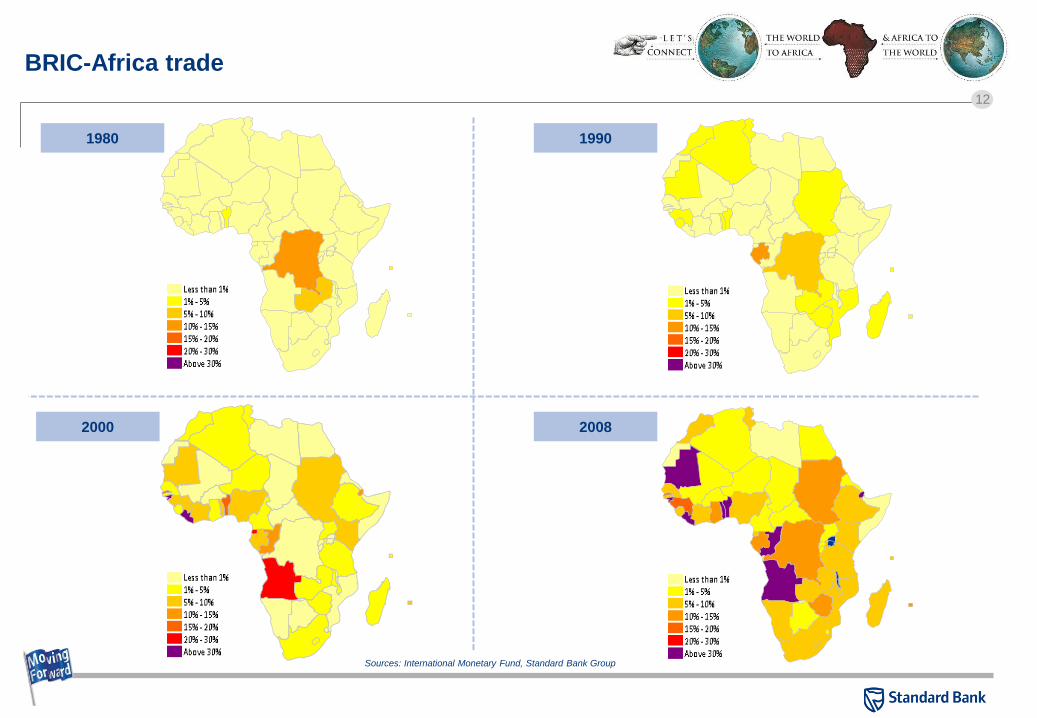

12

1980 1990

2000 2008

BRIC-Africa trade

Sources: International Monetary Fund, Standard Bank Group

13

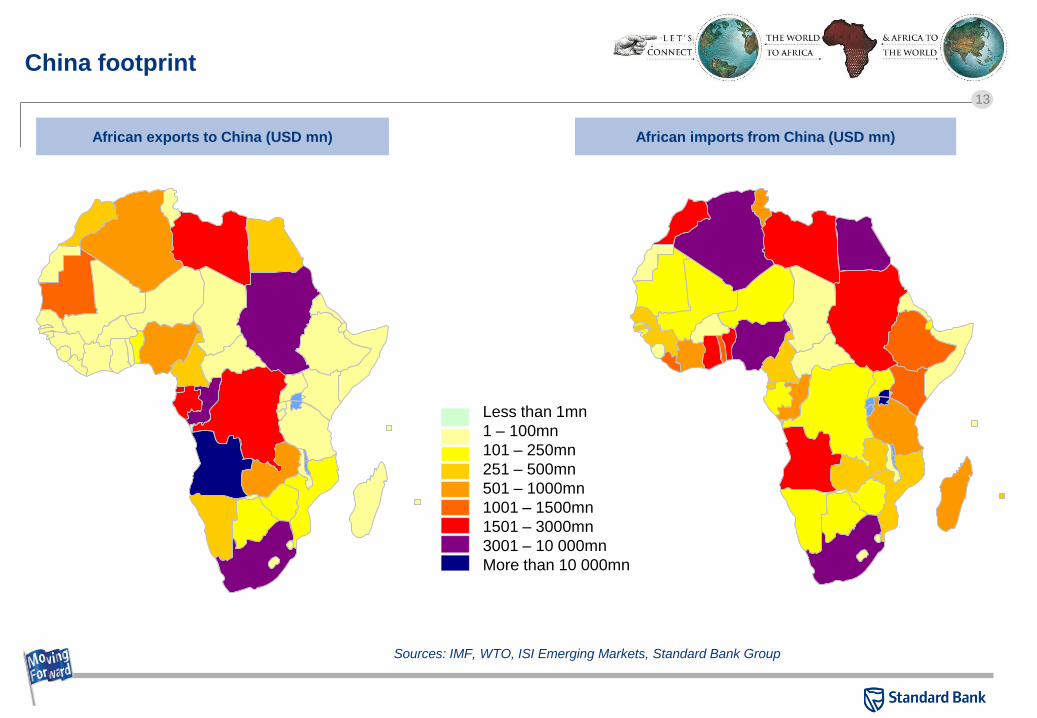

China footprint

Sources: IMF, WTO, ISI Emerging Markets, Standard Bank Group

African imports from China (USD mn)

Less than 1mn

1 – 100mn

101 – 250mn

251 – 500mn

501 – 1000mn

1001 – 1500mn

1501 – 3000mn

3001 – 10 000mn

More than 10 000mn

African exports to China (USD mn)

14

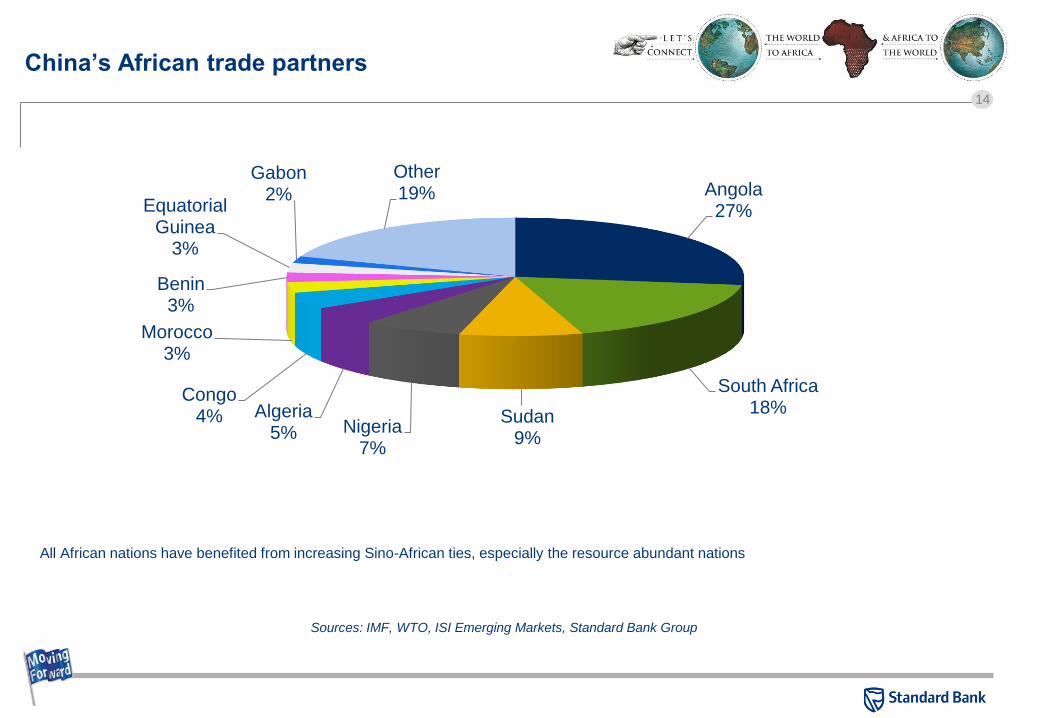

China’s African trade partners

All African nations have benefited from increasing Sino-African ties, especially the resource abundant nations

Sources: IMF, WTO, ISI Emerging Markets, Standard Bank Group

Angola27%

South Africa18%

Sudan9%

Nigeria7%

Algeria5%

Congo4%

Morocco3%

Benin3%

Equatorial Guinea

3%

Gabon2%

Other19%

15

Section 4

Chinese investment in infrastructure ?

16

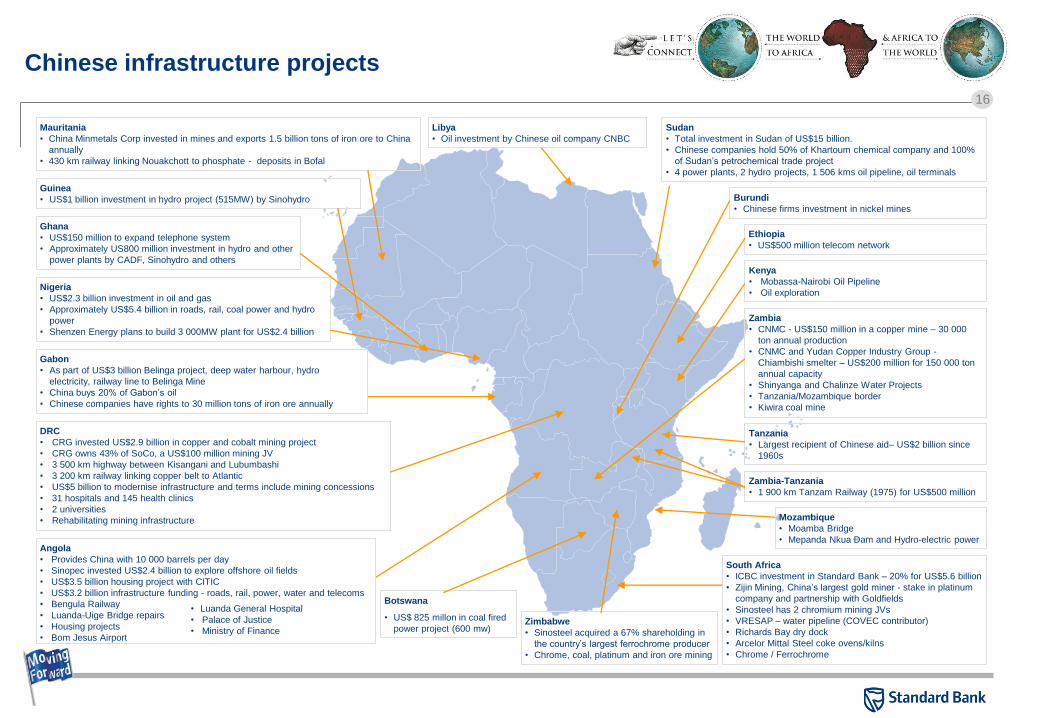

Chinese infrastructure projects

Gabon

• As part of US$3 billion Belinga project, deep water harbour, hydro

electricity, railway line to Belinga Mine

• China buys 20% of Gabon’s oil

• Chinese companies have rights to 30 million tons of iron ore annually

Ghana

• US$150 million to expand telephone system

• Approximately US800 million investment in hydro and other

power plants by CADF, Sinohydro and others

Guinea

• US$1 billion investment in hydro project (515MW) by Sinohydro

Nigeria

• US$2.3 billion investment in oil and gas

• Approximately US$5.4 billion in roads, rail, coal power and hydro

power

• Shenzen Energy plans to build 3 000MW plant for US$2.4 billion

Mauritania

• China Minmetals Corp invested in mines and exports 1.5 billion tons of iron ore to China

annually

• 430 km railway linking Nouakchott to phosphate - deposits in Bofal

Libya

• Oil investment by Chinese oil company CNBC

Burundi

• Chinese firms investment in nickel mines

Zambia

• CNMC - US$150 million in a copper mine – 30 000

ton annual production

• CNMC and Yudan Copper Industry Group -

Chiambishi smelter – US$200 million for 150 000 ton

annual capacity

• Shinyanga and Chalinze Water Projects

• Tanzania/Mozambique border

• Kiwira coal mine

Sudan

• Total investment in Sudan of US$15 billion.

• Chinese companies hold 50% of Khartoum chemical company and 100%

of Sudan’s petrochemical trade project

• 4 power plants, 2 hydro projects, 1 506 kms oil pipeline, oil terminals

South Africa

• ICBC investment in Standard Bank – 20% for US$5.6 billion

• Zijin Mining, China’s largest gold miner - stake in platinum

company and partnership with Goldfields

• Sinosteel has 2 chromium mining JVs

• VRESAP – water pipeline (COVEC contributor)

• Richards Bay dry dock

• Arcelor Mittal Steel coke ovens/kilns

• Chrome / Ferrochrome

Zimbabwe

• Sinosteel acquired a 67% shareholding in

the country’s largest ferrochrome producer

• Chrome, coal, platinum and iron ore mining

DRC

• CRG invested US$2.9 billion in copper and cobalt mining project

• CRG owns 43% of SoCo, a US$100 million mining JV

• 3 500 km highway between Kisangani and Lubumbashi

• 3 200 km railway linking copper belt to Atlantic

• US$5 billion to modernise infrastructure and terms include mining concessions

• 31 hospitals and 145 health clinics

• 2 universities

• Rehabilitating mining infrastructure

Ethiopia

• US$500 million telecom network

Zambia-Tanzania

• 1 900 km Tanzam Railway (1975) for US$500 million

Kenya

• Mobassa-Nairobi Oil Pipeline

• Oil exploration

Mozambique

• Moamba Bridge

• Mepanda Nkua Dam and Hydro-electric power

Tanzania

• Largest recipient of Chinese aid– US$2 billion since

1960s

Botswana

• US$ 825 millon in coal fired

power project (600 mw)

Angola

• Provides China with 10 000 barrels per day

• Sinopec invested US$2.4 billion to explore offshore oil fields

• US$3.5 billion housing project with CITIC

• US$3.2 billion infrastructure funding - roads, rail, power, water and telecoms

• Bengula Railway

• Luanda-Uige Bridge repairs

• Housing projects

• Bom Jesus Airport

• Luanda General Hospital

• Palace of Justice

• Ministry of Finance

17

Section 5

What Africa needs

18

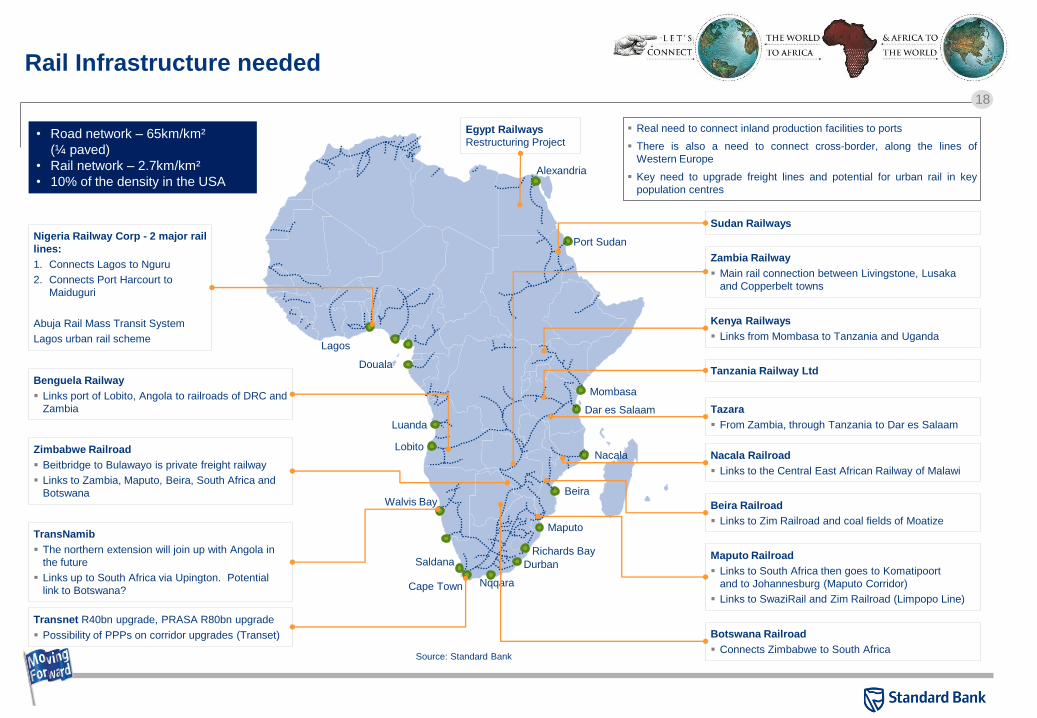

Rail Infrastructure needed

Lagos

Luanda

Lobito

Walvis Bay

Maputo

Beira

Nacala

Dar es Salaam

Mombasa

Port Sudan

Douala

Durban

Cape Town

Saldana

Alexandria

Richards Bay

Nqqara

Benguela Railway

Links port of Lobito, Angola to railroads of DRC and

Zambia

Nigeria Railway Corp - 2 major rail

lines:

1. Connects Lagos to Nguru

2. Connects Port Harcourt to

Maiduguri

Abuja Rail Mass Transit System

Lagos urban rail scheme

TransNamib

The northern extension will join up with Angola in

the future

Links up to South Africa via Upington. Potential

link to Botswana?

Zimbabwe Railroad

Beitbridge to Bulawayo is private freight railway

Links to Zambia, Maputo, Beira, South Africa and

Botswana

Botswana Railroad

Connects Zimbabwe to South Africa

Maputo Railroad

Links to South Africa then goes to Komatipoort

and to Johannesburg (Maputo Corridor)

Links to SwaziRail and Zim Railroad (Limpopo Line)

Beira Railroad

Links to Zim Railroad and coal fields of Moatize

Nacala Railroad

Links to the Central East African Railway of Malawi

Zambia Railway

Main rail connection between Livingstone, Lusaka

and Copperbelt towns

Tazara

From Zambia, through Tanzania to Dar es Salaam

Kenya Railways

Links from Mombasa to Tanzania and Uganda

Sudan Railways

Tanzania Railway Ltd

• Road network – 65km/km²

(¼ paved)

• Rail network – 2.7km/km²

• 10% of the density in the USA

Real need to connect inland production facilities to ports

There is also a need to connect cross-border, along the lines of

Western Europe

Key need to upgrade freight lines and potential for urban rail in key

population centres

Transnet R40bn upgrade, PRASA R80bn upgrade

Possibility of PPPs on corridor upgrades (Transet)

Egypt Railways

Restructuring Project

Source: Standard Bank

19

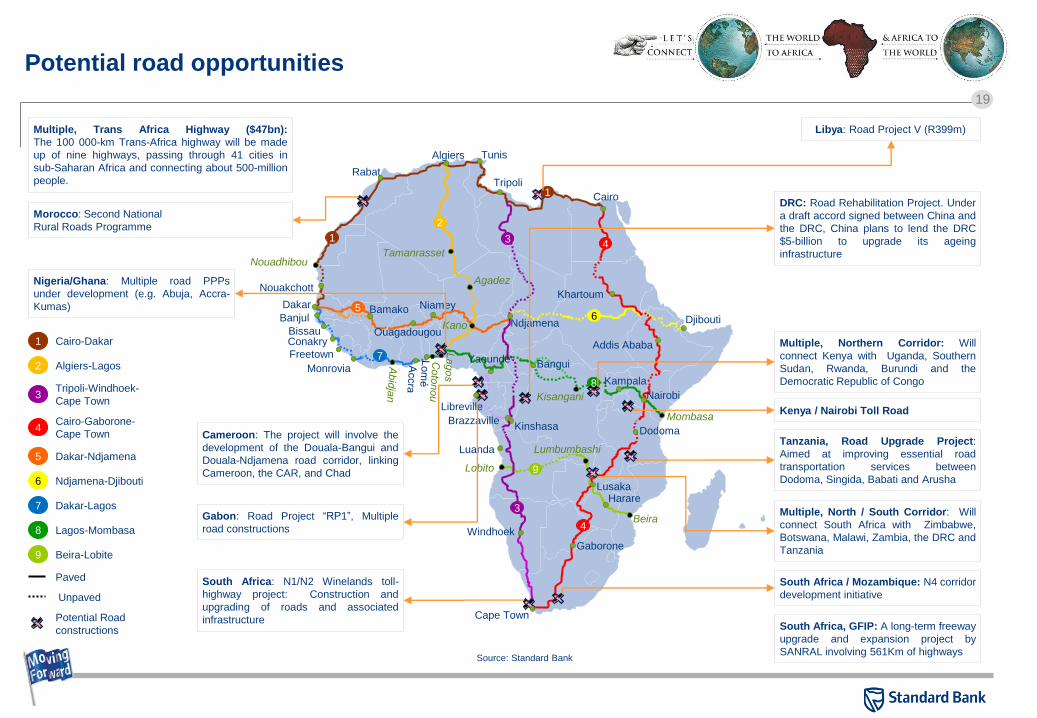

Potential road opportunities

Cairo

Tripoli

TunisAlgiers

Khartoum

Mombasa

Dodoma

Lusaka

Cape Town

Rabat

1

Nouadhibou

Nouakchott

Dakar 5 Bamako

Ouagadougou

Niamey

KanoBanjul

BissauConakry

Freetown

Monrovia

Kisangani

Bangui

8 Kampala

9

Lumbumbashi

Harare

Beira

Ndjamena6 Djibouti

Agadez

Tamanrasset

2

Kinshasa

Windhoek

3

3 4

Addis Ababa

4

7

Nairobi

Yaoundé

Gaborone

1

Libreville

Brazzaville

Luanda

Lobito

1 Cairo-Dakar

Paved

2 Algiers-Lagos

3Tripoli-Windhoek-

Cape Town

4Cairo-Gaborone-

Cape Town

5 Dakar-Ndjamena

6 Ndjamena-Djibouti

7 Dakar-Lagos

9 Beira-Lobite

Unpaved

8 Lagos-Mombasa

Potential Road

constructions

Morocco: Second National

Rural Roads Programme

Multiple, Trans Africa Highway ($47bn):

The 100 000-km Trans-Africa highway will be made

up of nine highways, passing through 41 cities in

sub-Saharan Africa and connecting about 500-million

people.

Libya: Road Project V (R399m)

Multiple, Northern Corridor: Will

connect Kenya with Uganda, Southern

Sudan, Rwanda, Burundi and the

Democratic Republic of Congo

South Africa, GFIP: A long-term freeway

upgrade and expansion project by

SANRAL involving 561Km of highways

South Africa: N1/N2 Winelands toll-

highway project: Construction and

upgrading of roads and associated

infrastructure

South Africa / Mozambique: N4 corridor

development initiative

Kenya / Nairobi Toll Road

Tanzania, Road Upgrade Project:

Aimed at improving essential road

transportation services between

Dodoma, Singida, Babati and Arusha

DRC: Road Rehabilitation Project. Under

a draft accord signed between China and

the DRC, China plans to lend the DRC

$5-billion to upgrade its ageing

infrastructure

Cameroon: The project will involve the

development of the Douala-Bangui and

Douala-Ndjamena road corridor, linking

Cameroon, the CAR, and Chad

Nigeria/Ghana: Multiple road PPPs

under development (e.g. Abuja, Accra-

Kumas)

Multiple, North / South Corridor: Will

connect South Africa with Zimbabwe,

Botswana, Malawi, Zambia, the DRC and

Tanzania

Gabon: Road Project “RP1”, Multiple

road constructions

Source: Standard Bank

20

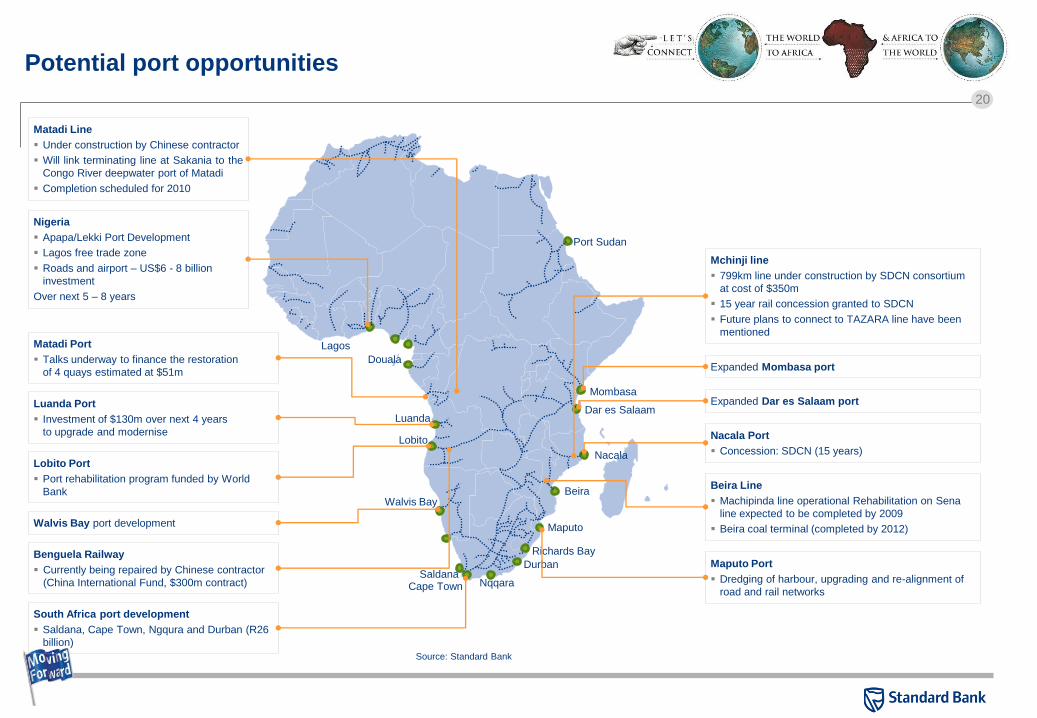

Potential port opportunities

Lagos

Luanda

Lobito

Walvis Bay

Maputo

Beira

Nacala

Dar es Salaam

Mombasa

Port Sudan

Douala

Cape TownSaldana

Nqqara

Durban

Richards Bay

Matadi Port

Talks underway to finance the restoration

of 4 quays estimated at $51m

Walvis Bay port development

Luanda Port

Investment of $130m over next 4 years

to upgrade and modernise

Maputo Port

Dredging of harbour, upgrading and re-alignment of

road and rail networks

Beira Line

Machipinda line operational Rehabilitation on Sena

line expected to be completed by 2009

Beira coal terminal (completed by 2012)

Mchinji line

799km line under construction by SDCN consortium

at cost of $350m

15 year rail concession granted to SDCN

Future plans to connect to TAZARA line have been

mentioned

Nacala Port

Concession: SDCN (15 years)

Expanded Mombasa port

Expanded Dar es Salaam port

South Africa port development

Saldana, Cape Town, Ngqura and Durban (R26

billion)

Source: Standard Bank

Nigeria

Apapa/Lekki Port Development

Lagos free trade zone

Roads and airport – US$6 - 8 billion

investment

Over next 5 – 8 years

Matadi Line

Under construction by Chinese contractor

Will link terminating line at Sakania to the

Congo River deepwater port of Matadi

Completion scheduled for 2010

Lobito Port

Port rehabilitation program funded by World

Bank

Benguela Railway

Currently being repaired by Chinese contractor

(China International Fund, $300m contract)

21

Disclaimer

Confidentiality and disclaimer

This document is provided on the express understanding that the information contained herein will be regarded and treated as strictly confidential and

proprietary to The Standard Bank of South Africa Limited (“Standard Bank”), its holding company Standard Bank Group Limited, and the subsidiaries of its

holding company (“the Standard Bank group”) . By retaining it the recipient undertakes that it is not to be delivered and nor shall its contents be disclosed to

anyone other than the intended recipient, and nor shall it be reproduced or used, in whole or in part, for any purpose other than for the purpose described

herein, without the prior written consent of Standard Bank.

Whilst every effort has been made to ensure the accuracy and completeness of the information contained in this document, no responsibility is accepted by the

Standard Bank group for the treatment by any court of law, tax, banking or other authorities in any jurisdiction of any transaction based on the information

contained herein. There may be tax implications to consider in any transaction and these should be identified and understood before investing. Separate tax

advice should therefore be sought when appropriate. Should anything contained herein contribute to the acquisition of a financial product the following must be

noted: there are intrinsic risks involved in transacting in any products; no guarantee is provided for the investment value in a product; any forecasts based on

hypothetical data are not guaranteed and are for illustrative purposes only; returns may vary as a result of their dependence on the performance of underlying

assets and other variable market factors and past performances are not necessarily indicative of future performances. Any client that is not a merchant banking

client as defined in the Financial Advisory and Intermediary Services Act must note that unless a financial needs analysis has been conducted to assess the

appropriateness of any product, investment or structure to its circumstances, there may be limitations on the appropriateness of any information provided by a

member of the Standard Bank group and careful consideration must be given to the implications of entering into any transaction, with or without the assistance

of an investment professional.

Peter von Klemperer

+27 11 631 3019