-

8/7/2019 Why the 31st Dil should not be the default Dil -

Paschal Donohoe TD

1/4

WHY THE 31ST DIL SHOULD NOT BE THE DEFAULT DIL

Paschal Donohoe TD

Default is a term that Ireland is becoming all too familiar

with. So many people are now no

longer able to pay their home mortgages. Too many home owners

have now either

defaulted or face the prospect of defaulting on these loans,

with tragic and severe

consequences and the idea that Ireland should default on

sovereign debt is gaining

momentum.

Default advocates point to our level of national debt as proof

of why default is necessary.

Even with no increase in the cost of rescuing our banking system

the debt challenges are

immense. Our gross debt levels will increase from 148 billion in

2010 to 184 billion in

2014. The consequent rise in our debt service costs is huge,

approximately 8 billion in

2013.

This paper analyses what sovereign default actually means and

reviews recent examples of

default showing what the likely consequences would be for

Ireland.

What is a Sovereign Default?A sovereign debt default occurs when

a country, the sovereign, decides not to pay its debt.

This decision is made by the government.

Sovereign debt consists (mostly) of government bonds. The

holders of these bonds

therefore incur the immediate impact of this decision. The

Government of the defaulting

state decide either not to pay back the capital on their bonds

or the rate of interest on their

debt. This imposes a loss on the bond holder and a reduction in

the liability of the

defaulting state.

Why do Sovereigns Default?They tend to occur in bad times

according to a comprehensive review of defaultliterature, theory

and history1. A number of key factors cause the majority of

defaults.

First, sovereign defaults occur after a period of intense credit

growth. The end of this

credit growth tends to be associated with the onset of a banking

crisis.

Second, levels of national borrowing are too high and a small

shock to this level of

borrowing triggers a default. This tends to be associated with a

change in the interest rate

on the debt.

Third, during economic contraction where national debt exceeds

national income, and a

Government cannot credibly borrow on international capital

markets.

A Brief History of DefaultsA long and varied history of

sovereign defaults exists. The first recorded default occurred

in fourth century B.C., when ten Greek municipalities in the

Attic Maritime Associationdefaulted on loans from the Delos

Temple!

An IMF study2 indicates that 257 defaults have occurred between

1824 and 2004.

1 The Economics and Law of Sovereign Defaults, Ugo Panizza,

FredericoSturzenegger and Jeromin Zettelmeyer, Journal of Economic

Literature 47:3,

-

8/7/2019 Why the 31st Dil should not be the default Dil -

Paschal Donohoe TD

2/4

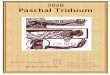

0

50

100

150

1824- 2004

200 Years of Defaults

Af r i c aAs i aEast EuropeLatin AmericaWest Europe

As indicated above a distinct geographical allocation exists

across defaults. Latin America

and Africa account for 74% of all defaults. A sovereign default

has not occurred in Western

Europe since the Great Depression.

Defaults tend to come in waves. The first wave of defaults, in

the period covered by this

study, occurred between 1824 and 1840, following a lending boom

by newly independent

Latin American countries. The next cluster commenced in 1861 and

ended in 1920, with

most of the defaults again occurring within Latin America. The

last default peak occurred

between 1921 and 1940 when 39 sovereign defaults occurred, as

governments grappled

with the impact of the Great Depression.

More recent prominent defaults are noted below.

Country Date DefaultRussia 1998 Occurred in aftermath

of Asian crisis and

collapse of LTCMColombia 1999 Defaulted on Brady

Bonds

Argentina 2001 Defaulted on 82

billion after bankingcrisis

This long and varied history allows an understanding of what

happens when the sovereign

defaults.

The consequences of Sovereign Defaults

- Swift Budgetary Adjustment: When a sovereign defaults, their

ability to borrow ishugely and quickly reduced as the Government

loses access to capital markets. A

defaulting government can only spend what it can directly raise

through taxation or

through significantly lower borrowing. Such economies tend to be

in deficit where

current spending is greater than taxes raised. In the immediate

period after default

the Government either balances their budget or moves to a

current surplus to pay

interest on restructured debt. Indeed, the median primary

surplus during the three

2 The Costs of Sovereign Default, Eduardo Borenstein & Ugo

Panizza, IMF

-

8/7/2019 Why the 31st Dil should not be the default Dil -

Paschal Donohoe TD

3/4

years after default was about 2% of GDP in the sample consisting

of all economies that

defaulted since 1976..3.

- Exclusion from capital markets. As losses are imposed on bond

holders they arewary of supplying credit to defaulting governments

for fear of incurring future loss.

During the 1980s defaulting countries were excluded from capital

markets for an

average period of 4 years. A recent study of exclusion concluded

that sovereign

defaulters between 1980 and 2005 regain(ed) partial market

access after 5.7 years

on average (median of 3.0 years) while it takes 8.4 years on

average (median of 7.0

years) to regain full market access..4.

- Higher Cost of Borrowing. In the period after the default the

cost of borrowingincreases. This is in recognition of the greater

risk to the lender of dealing with a

defaulting sovereign. A study on the impact of bond spreads for

defaulting

economies stated that a default in year t 1 has a large and

statistically significant

effect on spreads amounting to 400 basis points5. The same study

concluded that the

risk premium moved to 250 points in the second year before

returning to normal

trends.

- Reputational Damage. Literature in this area concludes that

the reputation ofgovernments is impacted by sovereign defaults. If

a government defaults once, the

market expectation is that a future default is always likely.

This assessment drives

all of the above reactions.

All of these assessments are based on empirical studies of

decades of defaults. However

there are a number of reasons why an Irish default would be

unprecedented and unique.

What makes Ireland different?

The Irish economy has 3 factors that are vital in consideration

of default consequences.

First, Ireland is a member of a single currency zone. An

immediate step taken by all

modern defaulting economies has been to devalue their currency.

This is to provide a

quick stimulus of export competitiveness. As Ireland does not

have a national currency

this option is not open to an Irish Government.

Second, Ireland is a developed country. All recent academic

research focuses on the impact

of defaults in emerging economies. The collateral impact of a

developed economy default

will be larger due to greater integration with the European

economy.

Third, the lender of last resort is already present in the Irish

State. Defaulting economies

make recourse to the IMF. Ireland has already done so with our

participation in the

IMF/EU support programme. A default involving non payment to our

lenders of last resort

would be unprecedented and history offers little guidance as to

their reaction.

3 Defaults in Todays Advanced Economies: Unnecessary,

Undesirable, and

Unlikely, Carlo Cottarelli, Lorenzo Forni, Jan Gottschalk &

Paolo Mauro, IMF StaffPosition Note, September 2010.4 Duration of

Capital Market Exclusion: Stylized Facts and Determining

Factors,

Christine Richmond and Daniel Dias, March 2009.5 The Costs of

Sovereign Default, Eduardo Borensztein and Ugo Panizza, IMF

-

8/7/2019 Why the 31st Dil should not be the default Dil -

Paschal Donohoe TD

4/4