Embed Size (px)

Citation preview

WIN – Week In a Nutshell 1 18th Jan 2013

WEEK IN A NUTSHELL

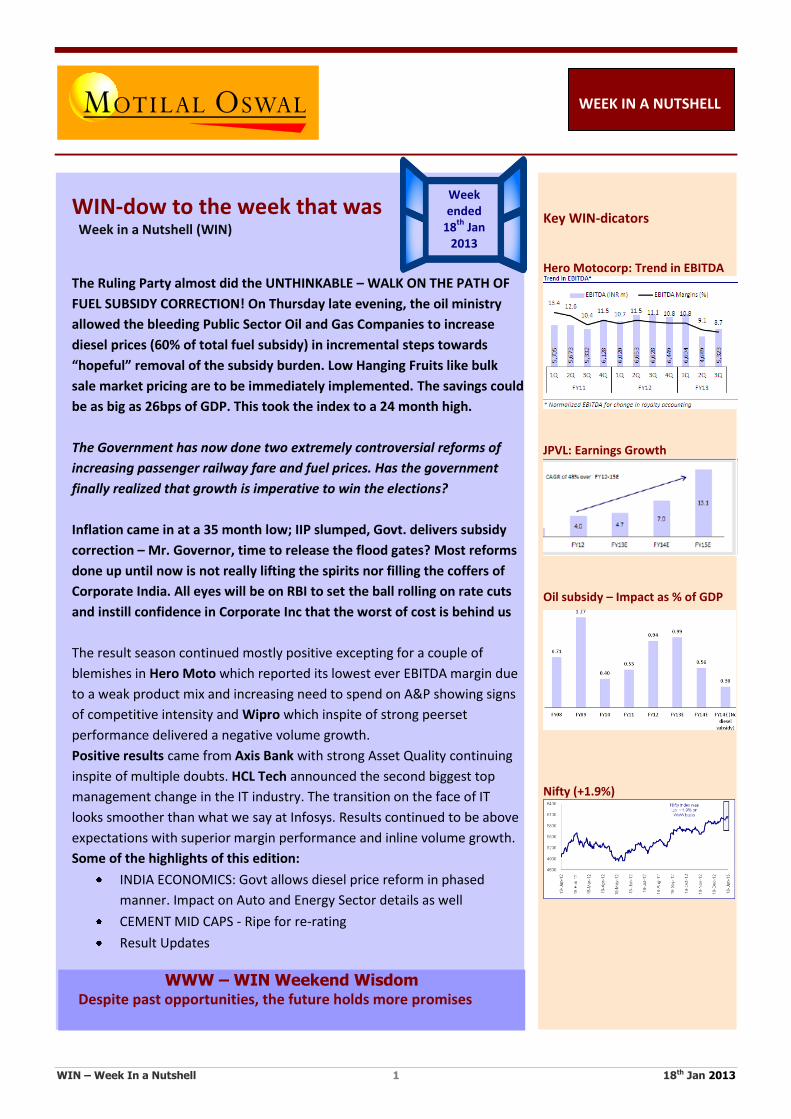

WIN-dow to the week that was Week in a Nutshell (WIN) The Ruling Party almost did the UNTHINKABLE – WALK ON THE PATH OF

FUEL SUBSIDY CORRECTION! On Thursday late evening, the oil ministry

allowed the bleeding Public Sector Oil and Gas Companies to increase

diesel prices (60% of total fuel subsidy) in incremental steps towards

“hopeful” removal of the subsidy burden. Low Hanging Fruits like bulk

sale market pricing are to be immediately implemented. The savings could

be as big as 26bps of GDP. This took the index to a 24 month high.

The Government has now done two extremely controversial reforms of

increasing passenger railway fare and fuel prices. Has the government

finally realized that growth is imperative to win the elections?

Inflation came in at a 35 month low; IIP slumped, Govt. delivers subsidy

correction – Mr. Governor, time to release the flood gates? Most reforms

done up until now is not really lifting the spirits nor filling the coffers of

Corporate India. All eyes will be on RBI to set the ball rolling on rate cuts

and instill confidence in Corporate Inc that the worst of cost is behind us

The result season continued mostly positive excepting for a couple of

blemishes in Hero Moto which reported its lowest ever EBITDA margin due

to a weak product mix and increasing need to spend on A&P showing signs

of competitive intensity and Wipro which inspite of strong peerset

performance delivered a negative volume growth.

Positive results came from Axis Bank with strong Asset Quality continuing

inspite of multiple doubts. HCL Tech announced the second biggest top

management change in the IT industry. The transition on the face of IT

looks smoother than what we say at Infosys. Results continued to be above

expectations with superior margin performance and inline volume growth.

Some of the highlights of this edition:

INDIA ECONOMICS: Govt allows diesel price reform in phased

manner. Impact on Auto and Energy Sector details as well

CEMENT MID CAPS - Ripe for re-rating

Result Updates

Key WIN-dicators Hero Motocorp: Trend in EBITDA

JPVL: Earnings Growth

Oil subsidy – Impact as % of GDP

Nifty (+1.9%)

Week ended

18th

Jan 2013

WWW – WIN Weekend Wisdom Despite past opportunities, the future holds more promises

WIN – Week In a Nutshell 2 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

[W]INside this week’s edition

WIN-teresting data points ................................................................................................................................... 4

WIN-ning charts & chats ..................................................................................................................................... 5

The most polluted cities of the world's largest economies ............................................................................................. 5

Results expected this week ............................................................................................................................................. 6

Concall Details ................................................................................................................................................................. 6

WIN-conomics .................................................................................................................................................... 7

INDIA ECONOMICS: Govt allows diesel price reform in phased manner. ....................................................................... 7

Dec-12 trade deficit remains high on oil; measures by govt and proposed gold curb by RBI to help ............................ 7

Nov-12 IIP de-grows again past the seasonal spike of Oct-12; rate cut hopes gets a fillip ............................................. 8

Dec-12 WPI inflation steady at 7.2%, core drops to 4.2%; Expect 50bp rate cut in Jan-13 ............................................ 8

GAAR – Govt. accepts major proposals of Shome Committee, defers till Apr-16 and eases conditions ........................ 8

WIN-sights from management interaction ........................................................................................................... 9

Tata Motors: Rolling up sleeves; Capex focused on CVs, PVs product development ..................................................... 9

Bajaj Auto - Rajiv Bajaj, MD ............................................................................................................................................. 9

Cement Stockists and Dealers Association - Sanjay Ladiwala, President ........................................................................ 9

Exide - AK Mukherjee, Director of Finance and CFO ....................................................................................................... 9

Maruti Suzuki - RC Bhargava, chairman ........................................................................................................................ 10

WIN Sector Updates .......................................................................................................................................... 11

AUTOS: Diesel de-regulation is a blessing for cars, but UVs and CVs might be impacted in short term ...................... 11

BANKING: Deposit growth at 11% least since 1990; Achieving RBI targeted business growth a challenge ................. 11

CEMENT MID CAPS - Ripe for re-rating: Catalysts - Improving utilization, narrowing operating performance gap ..... 12

INDIA ENERGY: Diesel De Regulation – A Game Changing Event. ................................................................................. 13

METALS WEEKLY: Iron ore prices may have peaked; HRC price hike not sticking in India ........................................... 13

WIN Corporate Corner ...................................................................................................................................... 14

AXIS BANK 3QFY13: Above est.; Healthy margin and asset quality trends; Strong traction in retail ............................ 14

BAJAJ AUTO 3QFY13: Above est led by higher margins; Upgrading FY14 EPS by 3%; Buy........................................... 14

BHARTI AIRTEL: Top management change for India business. ...................................................................................... 15

DENA BANK: Strong growth to continue; Asset quality remains healthy but challenges persist; Neutral ................... 15

FEDERAL BANK 3QFY13: In-line; Growth picks up; Trades at 1.2x FY14 PBV; Buy ....................................................... 16

HCLT 2QFY13: Revenue in line; Beat on PAT and EBITDA margin driven by higher utilization ..................................... 16

HERO MOTO 3QFY13: Below est; lowest ever EBITDA margins impacted.Cutting EPS; Buy ........................................ 16

WIN – Week In a Nutshell 3 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

INFOSYS 3QFY13: Significant beat to estimates and healthy 4Q guidance. Upgrading estimates. Buy........................ 17

L&T: Divestment of stake in Dhamra Port; Monetization of matured assets is a key ROE trigger ............................... 18

NIIT Technologies 3QFY13: Below estimates; Guidance of margin improvement from FY14 ...................................... 18

PETRONET LNG 3QFY13: Above est. led by higher volumes; Kochi delayed to Apr-13; Buy ........................................ 19

South Indian Bank 3QFY13: Business growth moderates; NIM and Asset quality improves ........................................ 19

TATA MOTORS: JLR's Dec-12 wholesale dispatches in-line at 32,282 (+4% YoY). ......................................................... 20

TATA MOTORS: JLR Dec-12 retails grew 15.5% YoY to 33,589 units; New RR retails commences. .............................. 20

TCS 3QFY13: Volume disappoints; Outlook on CY13 and discretionary spending positive for industry....................... 20

YES BANK 3QFY13: Another strong quarter; Traction in SA continues; NIM and Asset quality improves .................... 21

WIN Collage ...................................................................................................................................................... 23

The risks of a clash between China and Japan are rising—and the consequences could be calamitous ..................... 23

Nifty Valuations at a glance ............................................................................................................................... 24

WIN – Week In a Nutshell 4 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

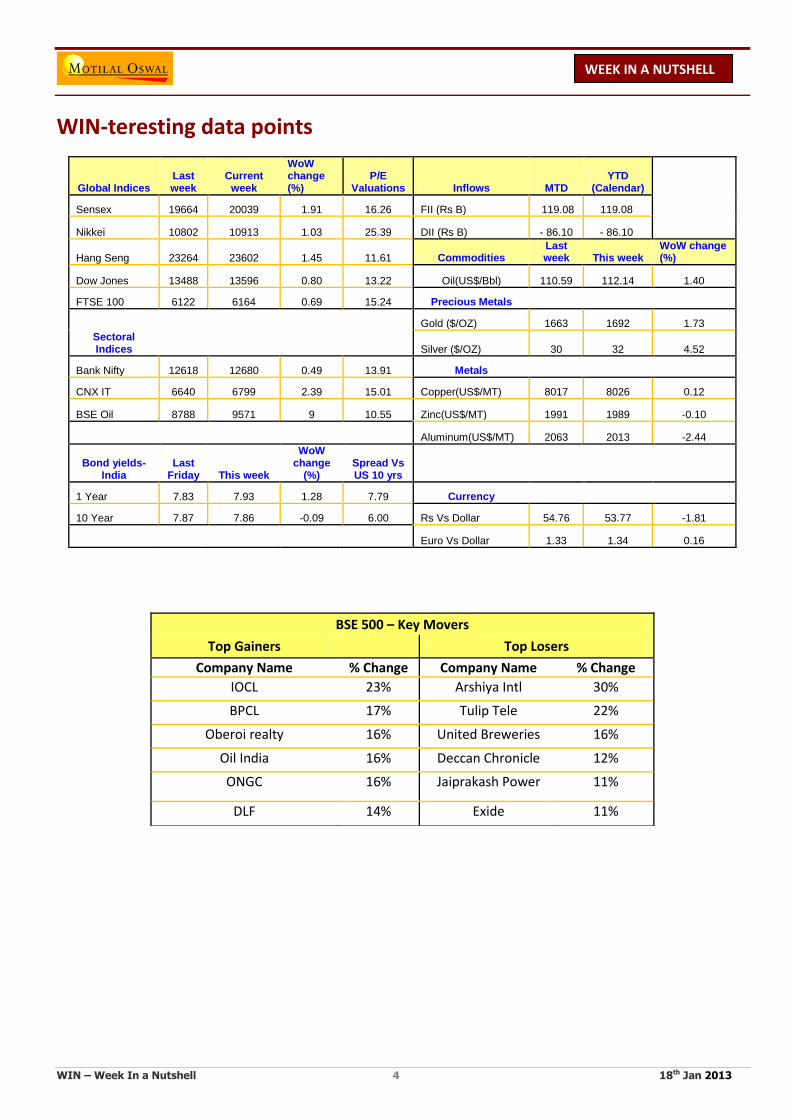

WIN-teresting data points

Global Indices Last week

Current week

WoW change (%)

P/E Valuations Inflows MTD

YTD (Calendar)

Sensex 19664 20039 1.91 16.26 FII (Rs B) 119.08 119.08

Nikkei 10802 10913 1.03 25.39 DII (Rs B) - 86.10 - 86.10

Hang Seng 23264 23602 1.45 11.61 Commodities Last week This week

WoW change (%)

Dow Jones 13488 13596 0.80 13.22 Oil(US$/Bbl) 110.59 112.14 1.40

FTSE 100 6122 6164 0.69 15.24 Precious Metals

Gold ($/OZ) 1663 1692 1.73

Sectoral Indices Silver ($/OZ) 30 32 4.52

Bank Nifty 12618 12680 0.49 13.91 Metals

CNX IT 6640 6799 2.39 15.01 Copper(US$/MT) 8017 8026 0.12

BSE Oil 8788 9571 9 10.55 Zinc(US$/MT) 1991 1989 -0.10

Aluminum(US$/MT) 2063 2013 -2.44

Bond yields-India

Last Friday This week

WoW change

(%) Spread Vs US 10 yrs

1 Year 7.83 7.93 1.28 7.79 Currency

10 Year 7.87 7.86 -0.09 6.00 Rs Vs Dollar 54.76 53.77 -1.81

Euro Vs Dollar 1.33 1.34 0.16

BSE 500 – Key Movers

Top Gainers

Top Losers

Company Name % Change Company Name % Change

IOCL 23% Arshiya Intl 30%

BPCL 17% Tulip Tele 22%

Oberoi realty 16% United Breweries 16%

Oil India 16% Deccan Chronicle 12%

ONGC 16% Jaiprakash Power 11%

DLF 14% Exide 11%

WIN – Week In a Nutshell 5 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

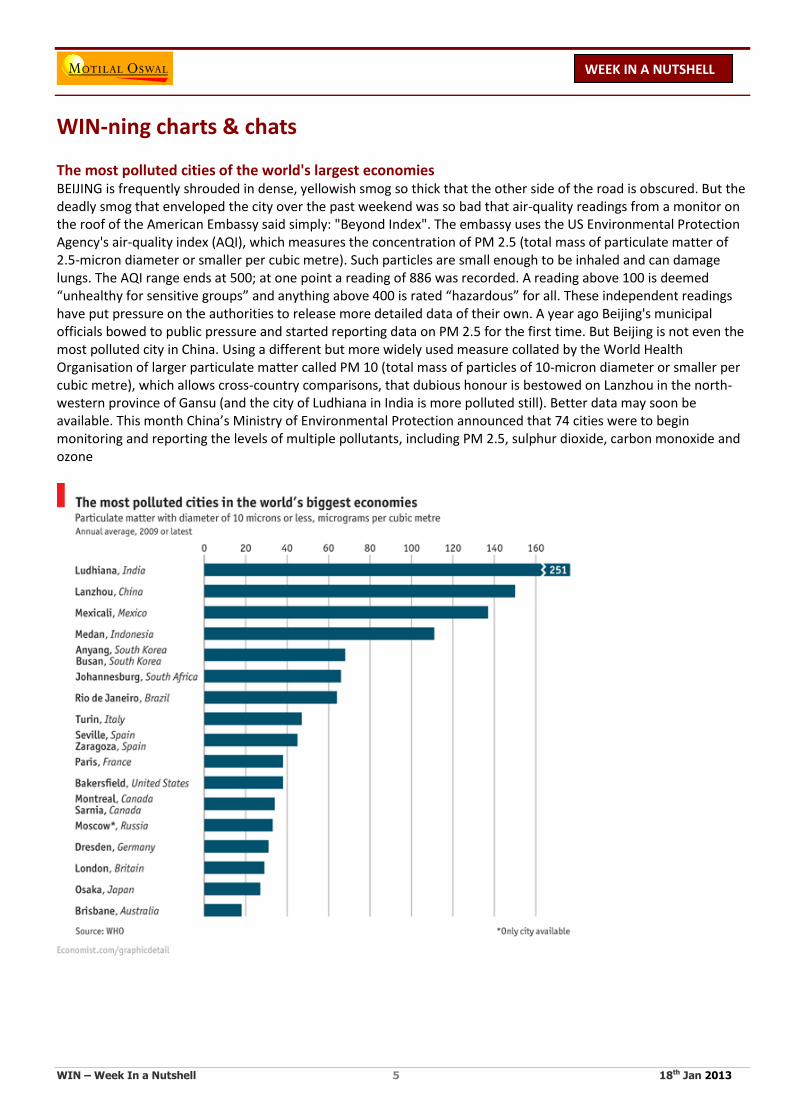

WIN-ning charts & chats The most polluted cities of the world's largest economies BEIJING is frequently shrouded in dense, yellowish smog so thick that the other side of the road is obscured. But the deadly smog that enveloped the city over the past weekend was so bad that air-quality readings from a monitor on the roof of the American Embassy said simply: "Beyond Index". The embassy uses the US Environmental Protection Agency's air-quality index (AQI), which measures the concentration of PM 2.5 (total mass of particulate matter of 2.5-micron diameter or smaller per cubic metre). Such particles are small enough to be inhaled and can damage lungs. The AQI range ends at 500; at one point a reading of 886 was recorded. A reading above 100 is deemed “unhealthy for sensitive groups” and anything above 400 is rated “hazardous” for all. These independent readings have put pressure on the authorities to release more detailed data of their own. A year ago Beijing's municipal officials bowed to public pressure and started reporting data on PM 2.5 for the first time. But Beijing is not even the most polluted city in China. Using a different but more widely used measure collated by the World Health Organisation of larger particulate matter called PM 10 (total mass of particles of 10-micron diameter or smaller per cubic metre), which allows cross-country comparisons, that dubious honour is bestowed on Lanzhou in the north-western province of Gansu (and the city of Ludhiana in India is more polluted still). Better data may soon be available. This month China’s Ministry of Environmental Protection announced that 74 cities were to begin monitoring and reporting the levels of multiple pollutants, including PM 2.5, sulphur dioxide, carbon monoxide and ozone

WIN – Week In a Nutshell 6 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

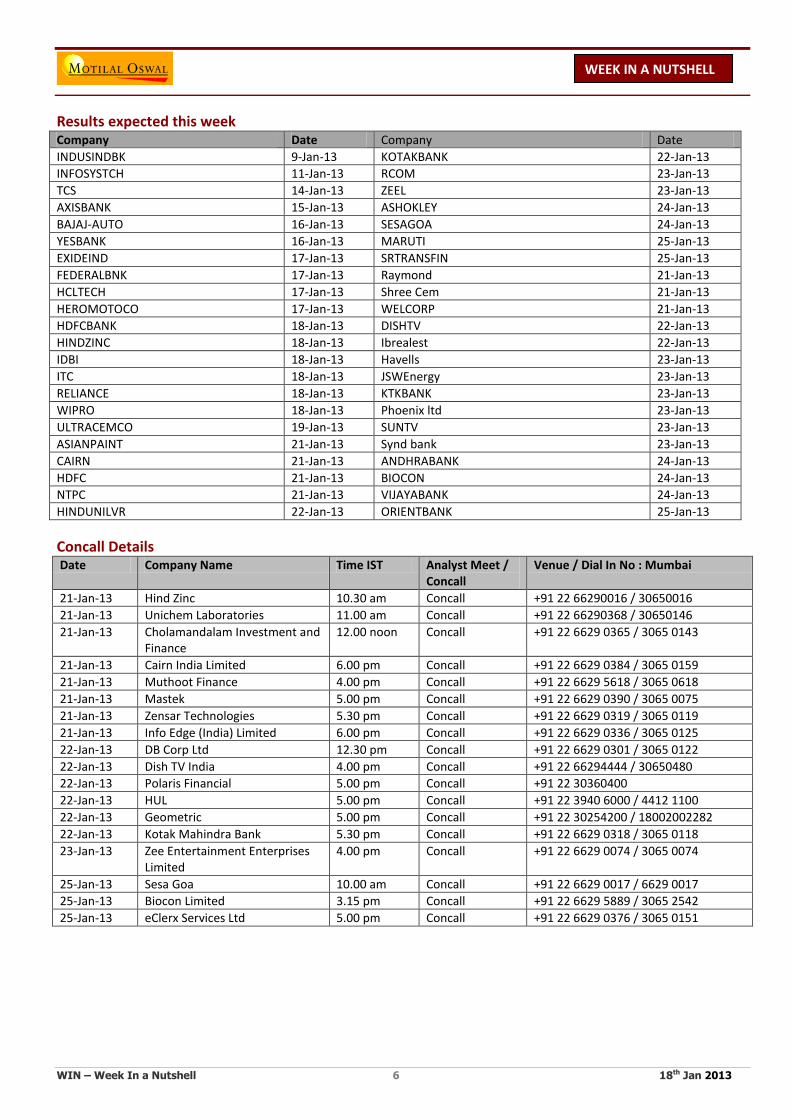

Results expected this week Company Date Company Date

INDUSINDBK 9-Jan-13 KOTAKBANK 22-Jan-13

INFOSYSTCH 11-Jan-13 RCOM 23-Jan-13

TCS 14-Jan-13 ZEEL 23-Jan-13

AXISBANK 15-Jan-13 ASHOKLEY 24-Jan-13

BAJAJ-AUTO 16-Jan-13 SESAGOA 24-Jan-13

YESBANK 16-Jan-13 MARUTI 25-Jan-13

EXIDEIND 17-Jan-13 SRTRANSFIN 25-Jan-13

FEDERALBNK 17-Jan-13 Raymond 21-Jan-13

HCLTECH 17-Jan-13 Shree Cem 21-Jan-13

HEROMOTOCO 17-Jan-13 WELCORP 21-Jan-13

HDFCBANK 18-Jan-13 DISHTV 22-Jan-13

HINDZINC 18-Jan-13 Ibrealest 22-Jan-13

IDBI 18-Jan-13 Havells 23-Jan-13

ITC 18-Jan-13 JSWEnergy 23-Jan-13

RELIANCE 18-Jan-13 KTKBANK 23-Jan-13

WIPRO 18-Jan-13 Phoenix ltd 23-Jan-13

ULTRACEMCO 19-Jan-13 SUNTV 23-Jan-13

ASIANPAINT 21-Jan-13 Synd bank 23-Jan-13

CAIRN 21-Jan-13 ANDHRABANK 24-Jan-13

HDFC 21-Jan-13 BIOCON 24-Jan-13

NTPC 21-Jan-13 VIJAYABANK 24-Jan-13

HINDUNILVR 22-Jan-13 ORIENTBANK 25-Jan-13

Concall Details Date Company Name Time IST Analyst Meet /

Concall Venue / Dial In No : Mumbai

21-Jan-13 Hind Zinc 10.30 am Concall +91 22 66290016 / 30650016

21-Jan-13 Unichem Laboratories 11.00 am Concall +91 22 66290368 / 30650146

21-Jan-13 Cholamandalam Investment and Finance

12.00 noon Concall +91 22 6629 0365 / 3065 0143

21-Jan-13 Cairn India Limited 6.00 pm Concall +91 22 6629 0384 / 3065 0159

21-Jan-13 Muthoot Finance 4.00 pm Concall +91 22 6629 5618 / 3065 0618

21-Jan-13 Mastek 5.00 pm Concall +91 22 6629 0390 / 3065 0075

21-Jan-13 Zensar Technologies 5.30 pm Concall +91 22 6629 0319 / 3065 0119

21-Jan-13 Info Edge (India) Limited 6.00 pm Concall +91 22 6629 0336 / 3065 0125

22-Jan-13 DB Corp Ltd 12.30 pm Concall +91 22 6629 0301 / 3065 0122

22-Jan-13 Dish TV India 4.00 pm Concall +91 22 66294444 / 30650480

22-Jan-13 Polaris Financial 5.00 pm Concall +91 22 30360400

22-Jan-13 HUL 5.00 pm Concall +91 22 3940 6000 / 4412 1100

22-Jan-13 Geometric 5.00 pm Concall +91 22 30254200 / 18002002282

22-Jan-13 Kotak Mahindra Bank 5.30 pm Concall +91 22 6629 0318 / 3065 0118

23-Jan-13 Zee Entertainment Enterprises Limited

4.00 pm Concall +91 22 6629 0074 / 3065 0074

25-Jan-13 Sesa Goa 10.00 am Concall +91 22 6629 0017 / 6629 0017

25-Jan-13 Biocon Limited 3.15 pm Concall +91 22 6629 5889 / 3065 2542

25-Jan-13 eClerx Services Ltd 5.00 pm Concall +91 22 6629 0376 / 3065 0151

WIN – Week In a Nutshell 7 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN-conomics INDIA ECONOMICS: Govt allows diesel price reform in phased manner. Event: Indian government has announced the landmark decisions for the Indian energy sector. The key

decisions announced are:

OMC’s to make small revisions to diesel prices until it is at par with market prices – To hike prices by INR0.5/ltr per month;

Sales to bulk diesel buyers at market price - constitute ~12-17% of OMC’s diesel sales;

LPG cylinder cap increased from 6 to 9 per year per household from April 2013;

LPG and kerosene prices unchanged as of now.

FY14 oil subsidy bill reduces by INR350b: it translates into a reduction of near INR350b (~ 46bp of GDP) in oil subsidy bill in FY14. Significantly another INR300b (26bp of GDP) saving is possible if diesel prices are completely deregulated under the prevailing oil prices and exchange rate. This would restrain the overall subsidy bill to 2% of GDP – the principle laid out in the Union Budget for FY13, a significant improvement from 2.4% estimated in FY13.

Still releases INR200b for Food Security Bill: Apart from fiscal correction, it would also release INR200b for the proposed food subsidy bill. Thus the move makes implementation of Food Security Bill from FY14 a reality.

Positive impact on investment climate and credit rating: The move singularly addresses the fiscal deficit issue, cited as the key reason behind the possibility of a rating downgrade. The improving investment climate is expected to result in a growth recovery with a timelag too. Both these are positive for rating and investment flows.

Inflation gets a nudge of 50bp in FY14 narrowly missing the 5% target: This would alter the inflation path higher at a monthly run rate of 6-7bp and going up to 70bp in Mar-14. The FY14 average inflation that was slated at 5.0% earlier, could now nudge to 5.5%. This however, still leaves enough headroom to effect significant cuts by RBI from the near peak interest rates prevailing now. We expect RBI to cut interest rates by 100bps in 2013 with a likely 50bps cut in Jan-13.

Dec-12 trade deficit remains high on oil; measures by govt and proposed gold curb by RBI to help Export de-growth coupled with import growth takes trade deficit higher: Falling exports coupled with resilient

imports resulted in continued high trade deficit in Dec-12 at USD18b, closer to the peak value of USD21b in Oct-12. In recent months, deficit remains closer to 1% of GDP each month.

YTDFY13 too showed an expansion in trade gap: Trade deficit during Apr-Dec 2012 has already reached 8% of GDP and is slated to reach 10.8% by end-FY13. However, the rise in trade deficit was entirely a result of higher oil imports that resulted nearly equally from a price increase and fall in domestic production. Latest balance of payments indicators reveal that capital flows (both in debt and equity) have been barely sufficient to close the current account deficit.

Oil spoils the correction in trade deficit: The oil bill has increased by 12% during YTDFY13. While nearly half of it is attributable to price increase the rest half is due to fall in domestic production particularly from KG D6. Non-oil imports have witnessed a slightly higher decline of 6.4% than exports (-6.0%) during YTDFY13. Thus, barring USD14b increase in oil imports, trade deficit would have been lower by USD5b. The Government has stopped releasing the commodity wise break up of trade data barring details of oil imports. Hence, data on other major item of import, viz., gold is available only upto 1HFY13 which showed a drop to USD20b from USD29b in 1HFY12. However, latest reports indicated a pick up in gold demand in the festive season.

INR outlook tentative, policy incentives to yield results in the medium term: Government has taken a slew of measures recently to incentivize exports including extension of interest subvention for one more year and encompassing a far wider range of products. It has also made provision for cheaper long term credit, besides direct incentives for near term exports and policies towards import substitutions. The RBI on its part has suggested various measures to curb gold imports including higher taxes and restrictions, circulating domestic gold, innovative financial products obviating need for gold imports, etc. While these measures are expected to yield benefits in the medium term, we expect INR to hover in the range of 53-55 in large part of CY13 with phases of high volatility expected.

WIN – Week In a Nutshell 8 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

Nov-12 IIP de-grows again past the seasonal spike of Oct-12; rate cut hopes gets a fillip Nov-12 IIP: growth slipped to -0.1% after a seasonal spike of 8.3% in Oct-12. This is the fifth month of de-growth

in eight months of FY13 so far. All sectors displayed either negative or very low single-digit growth.

Apr-Nov FY13 IIP growth: stands at 1%, down from 1.2% growth a month back. CMIE’s data on projects confirms the empty middle hypothesis – for the latest Dec-12 quarter, value of outstanding project investments is still going down when adjusted for cost escalation.

See FY13 IIP growth at 1.0%; a fillip to rate cut expectations: We have cut our FY13 IIP estimate to 1.0% from 1.4% earlier while leaving the GDP growth for FY13 unchanged at 5.2%. We have placed our initial estimate of FY14 IIP at 5.6%, consistent with a moderate recovery in GDP growth to 6.5%. The latest IIP print has raised expectations of a 50bp rate cut by RBI in its January 29, 2013 policy, provided inflation data for Dec-12 confirms easing.

Dec-12 WPI inflation steady at 7.2%, core drops to 4.2%; Expect 50bp rate cut in Jan-13 Dec-12 inflation at 7.2% was somewhat lower than expectations. Near-flat underlying WPI (wholesale price

index) for the last four months suggests absence of any generalized price pressures on the economy.

High food inflation (given base effect despite a fall in prices) more than offset easing non-food and minerals inflation, pushing primary inflation too.

Fuel group inflation eased from double digit levels as both oil prices and INR remained stable.

Core inflation plummeted to 4.2% (33-month low); Manufacturing inflation also eased to 5.0% (26-month low), also around RBI’s comfort level.

Led by base effect of food prices, CPI (Rural Urban) inflation for Dec-12 accelerated to 10.6% (from 9.9% in Nov-12). The divergence between WPI and CPI is expected to remain for two more months before starting to converge from Mar-13.

Recent data releases suggesting both, near-stagnant industrial output and easing inflationary pressures, are strongly supportive of a decisive shift in the monetary policy. We expect RBI to (1) cut policy rates by 50bp on January 29, and (2) significantly lower its forecasts for FY13 growth and Mar-13 inflation.

GAAR – Govt. accepts major proposals of Shome Committee, defers till Apr-16 and eases conditions The government has formally announced acceptance of most major recommendations of the Shome

Committee.

While it clarified that GAAR has already became part of the law as per Finance Act 2012 through insertion of Chapter X-A titled ‘General Anti- Avoidance Rule’ in the Income-tax Act, 1961. However, even under current provisions, Chapter X-A was to come into force with effect from April 1, 2014. The Government has now deferred its implementation till April 1, 2016.

Apart from this, the Government pruned the scope of the applicability of GAAR provisions by i) defining applicability of the provisions narrowly; ii) laying down procedural safeguards for invoking of GAAR including ensuring right to defend and time bound recourse by the assessee; iii) according large number of exclusions including FIIs and NRIs in certain cases, minimum threshold of INR30m, grandfathering of investments before Aug-10 and avoiding double taxation of any manner; iv) instituting appropriate intermediary between assessee and the Income Tax Authority who would work on the principle of arms length. It also places a responsibility on the statutory auditors of reporting instance of tax avoidance.

Minor tweaking on the recommendations of the Shome Committee has been done in specifying Aug-10 as the cutoff date for grandfathering and prescribing no time limit for intermediaries and recourse by the assessee.

Suggestions on many areas has still been left out including i) abolition of capital gains and increase of STT, ii) exemption on invoking GAAR on willingness to pay during assessment proceedings, iii) exemptions in certain cases like setting up of branch/subsidiary, unit in SEZ, funding through debt or equity, purchase or lease of a capital asset, etc.

We believe the official deferment and dilution of GAAR provisions comprehensively addresses investors’ concerns in this regards.

WIN – Week In a Nutshell 9 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN-sights from management interaction Tata Motors: Rolling up sleeves; Capex focused on CVs, PVs product development We met Mr Karl Slym, MD (India Operations), Tata Motors Key takeaways:

Organizational changes under new India MD to improve competitiveness, aim to be credible #2 player in PVs by 2020 & maintain market leadership in CVs.

Has set up a road map to revive PV business by focusing on consumers and offering exciting product portfolio, improving quality and improving overall consumer experience in sales and service. While product portfolio changes would need at least 2 years.

Plans to maintain its leadership by offering technologically superior products, with lowest total cost of ownership and superior service network. It expects M&HCV industry to post 10-15% CAGR over the next 5-10 years, while LCVs structural growth remains intact.

Traes at 8.2x FY14E cons. EPS of INR40 and 7.6x FY15E cons. EPS of INR43. The DVR stock trades at 4.6x FY14E and 4.2x FY15E cons. EPS. Buy with a target price of INR385 (FY15 SOTP based) for ordinary share and INR231 for DVR (~40% discount to ordinary share's target price).

Bajaj Auto - Rajiv Bajaj, MD Two factors for the improvement in exports. One, although there has been a big impact in this quarter both on

the top- and the bottom-line of exports. A very good quarter for exports particularly for three-wheelers

125cc and above which is where Bajaj is mainly focused, our market-share continues to be in the region of 40 percent

In the other 65 percent, which is the 100cc space, we have now come up to a 20 percent market share

I have seen nothing to suggest that the Dream Yuga is a super success nor have I seen anything to suggest that it is beginning to wane. I think it will remain stable and steady.

I think the market-share can be improved it because with new Discover-100

Our profitability will also rise for many reasons and going into the next year, we are going to realise about Rs 54 to the dollar

EBITDA should go up as a weighted average by 2-to-3 percent

Cement Stockists and Dealers Association - Sanjay Ladiwala, President Cement Price has been increased in the range of Rs 18-25 across the board in different regions.

There is no pickup in demand in south and it will not happen soon in south. It may take a month or so. However, it should percolate in east.

Next 15 days will be crucial, which will be the test of the sustenance because there is not much pickup in demand

margins will improve because the cost have also been steady, though we have seen slight increases in fuel and now maybe freight is also in the offing but barring that there has not been much cost pressure

Capacity utilisation still lies low. We are averaging at about 73 percent across the country, much lower in the south than in the north. That will also move up as the demand picks up

We are expecting about 20 odd million tonne to come in FY14. This year 14 million tonne has been added, sevwen million is in the offing and it will come before March and another 20 odd million tonne coming in the next fiscal is likely to add pressure to the prices.

This is the first major price increase after monsoon

Exide - AK Mukherjee, Director of Finance and CFO There are couple of factors which affected the results like lead cost push of about 8 percent and currency

depreciation of about 4 percent. We had a very depressed demand from the Original Equipment Manufacturer (OEM) segment.

Uninterrupted Power Supply (UPS) batteries demand was low because of early onset of winter

The price increase that we had at the beginning of this quarter was primarily to take care of cost push we had in Q2

WIN – Week In a Nutshell 10 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

We are slowly regaining the market share and this quarter as well we had regained some market share. It is on the positive direction.

Coming quarter will also be quite challenging.

We are quite bullish that the volume in the replacement segments, we will continue to grow further

Maruti Suzuki - RC Bhargava, chairman Diesel price hike will not affect our sales at all. Our diesel sales will continue to be at the level of our production

capacity.

I don’t think that even if diesel prices reach Rs 10 level projected today, as being required to stop under recoveries, I don’t think diesel car sales will drop below 50 percent of the market.

WIN – Week In a Nutshell 11 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

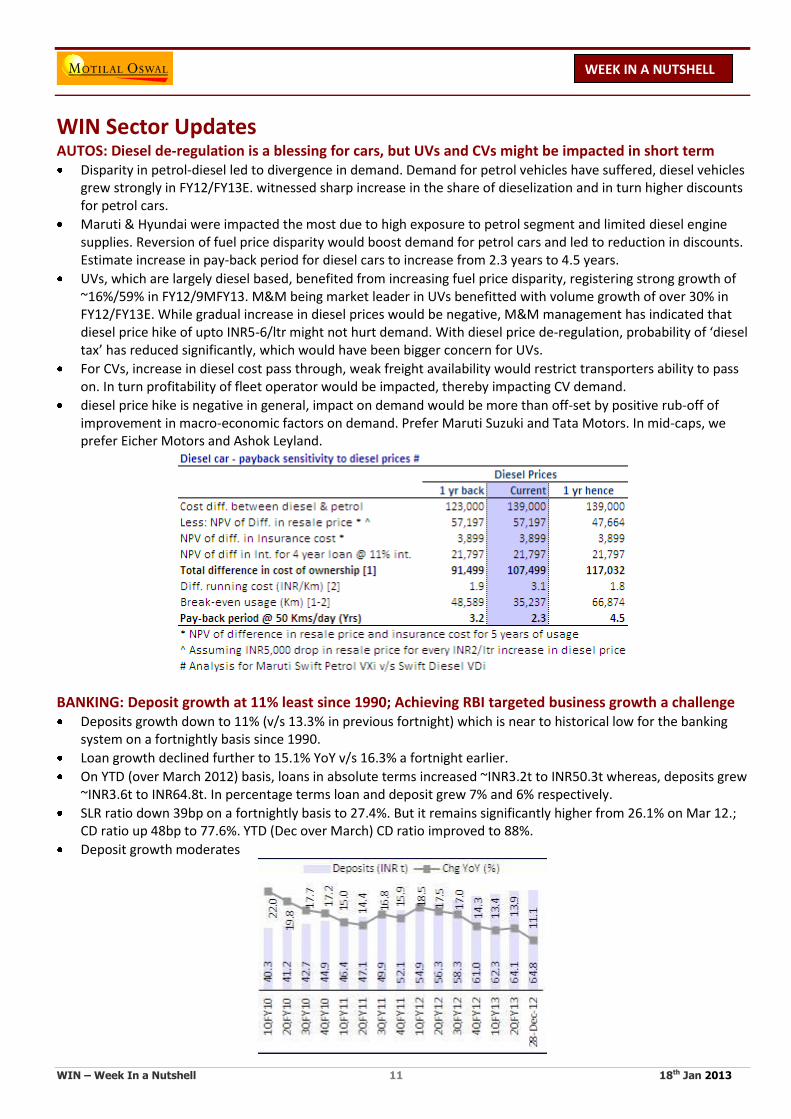

WIN Sector Updates AUTOS: Diesel de-regulation is a blessing for cars, but UVs and CVs might be impacted in short term Disparity in petrol-diesel led to divergence in demand. Demand for petrol vehicles have suffered, diesel vehicles

grew strongly in FY12/FY13E. witnessed sharp increase in the share of dieselization and in turn higher discounts for petrol cars.

Maruti & Hyundai were impacted the most due to high exposure to petrol segment and limited diesel engine supplies. Reversion of fuel price disparity would boost demand for petrol cars and led to reduction in discounts. Estimate increase in pay-back period for diesel cars to increase from 2.3 years to 4.5 years.

UVs, which are largely diesel based, benefited from increasing fuel price disparity, registering strong growth of ~16%/59% in FY12/9MFY13. M&M being market leader in UVs benefitted with volume growth of over 30% in FY12/FY13E. While gradual increase in diesel prices would be negative, M&M management has indicated that diesel price hike of upto INR5-6/ltr might not hurt demand. With diesel price de-regulation, probability of ‘diesel tax’ has reduced significantly, which would have been bigger concern for UVs.

For CVs, increase in diesel cost pass through, weak freight availability would restrict transporters ability to pass on. In turn profitability of fleet operator would be impacted, thereby impacting CV demand.

diesel price hike is negative in general, impact on demand would be more than off-set by positive rub-off of improvement in macro-economic factors on demand. Prefer Maruti Suzuki and Tata Motors. In mid-caps, we prefer Eicher Motors and Ashok Leyland.

BANKING: Deposit growth at 11% least since 1990; Achieving RBI targeted business growth a challenge Deposits growth down to 11% (v/s 13.3% in previous fortnight) which is near to historical low for the banking

system on a fortnightly basis since 1990.

Loan growth declined further to 15.1% YoY v/s 16.3% a fortnight earlier.

On YTD (over March 2012) basis, loans in absolute terms increased ~INR3.2t to INR50.3t whereas, deposits grew ~INR3.6t to INR64.8t. In percentage terms loan and deposit grew 7% and 6% respectively.

SLR ratio down 39bp on a fortnightly basis to 27.4%. But it remains significantly higher from 26.1% on Mar 12.; CD ratio up 48bp to 77.6%. YTD (Dec over March) CD ratio improved to 88%.

Deposit growth moderates

WIN – Week In a Nutshell 12 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

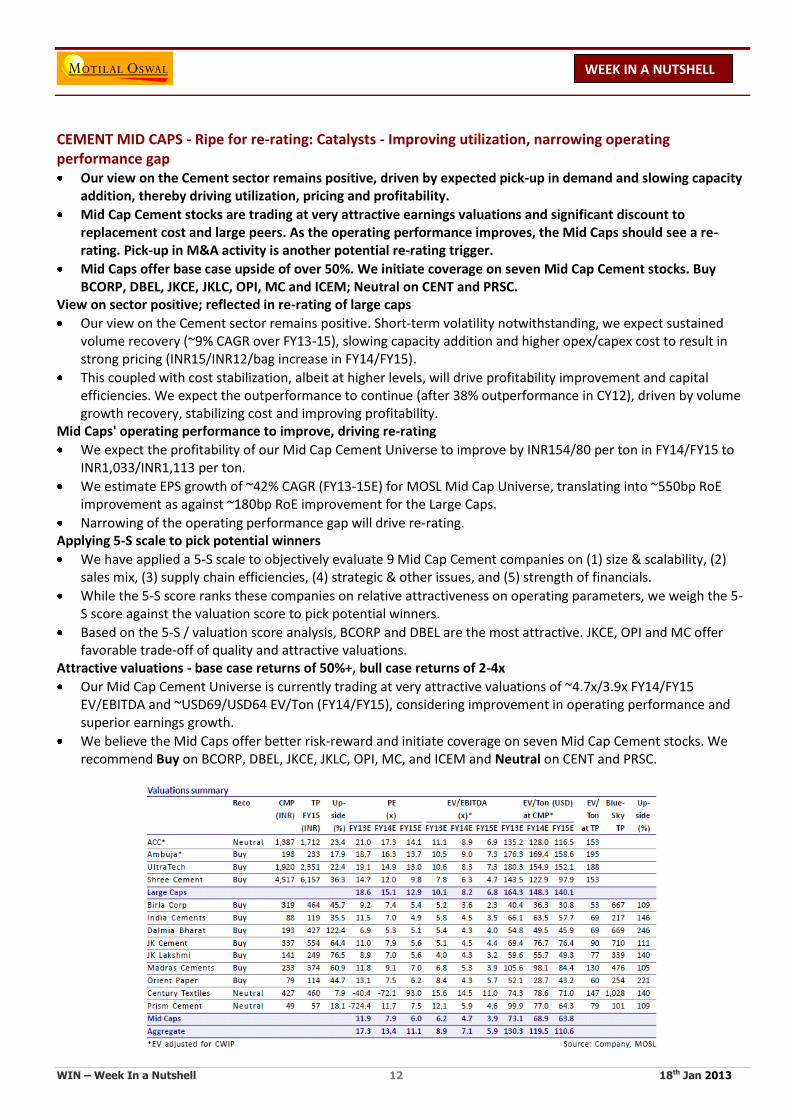

CEMENT MID CAPS - Ripe for re-rating: Catalysts - Improving utilization, narrowing operating performance gap Our view on the Cement sector remains positive, driven by expected pick-up in demand and slowing capacity

addition, thereby driving utilization, pricing and profitability.

Mid Cap Cement stocks are trading at very attractive earnings valuations and significant discount to replacement cost and large peers. As the operating performance improves, the Mid Caps should see a re-rating. Pick-up in M&A activity is another potential re-rating trigger.

Mid Caps offer base case upside of over 50%. We initiate coverage on seven Mid Cap Cement stocks. Buy BCORP, DBEL, JKCE, JKLC, OPI, MC and ICEM; Neutral on CENT and PRSC.

View on sector positive; reflected in re-rating of large caps

Our view on the Cement sector remains positive. Short-term volatility notwithstanding, we expect sustained volume recovery (~9% CAGR over FY13-15), slowing capacity addition and higher opex/capex cost to result in strong pricing (INR15/INR12/bag increase in FY14/FY15).

This coupled with cost stabilization, albeit at higher levels, will drive profitability improvement and capital efficiencies. We expect the outperformance to continue (after 38% outperformance in CY12), driven by volume growth recovery, stabilizing cost and improving profitability.

Mid Caps' operating performance to improve, driving re-rating

We expect the profitability of our Mid Cap Cement Universe to improve by INR154/80 per ton in FY14/FY15 to INR1,033/INR1,113 per ton.

We estimate EPS growth of ~42% CAGR (FY13-15E) for MOSL Mid Cap Universe, translating into ~550bp RoE improvement as against ~180bp RoE improvement for the Large Caps.

Narrowing of the operating performance gap will drive re-rating. Applying 5-S scale to pick potential winners

We have applied a 5-S scale to objectively evaluate 9 Mid Cap Cement companies on (1) size & scalability, (2) sales mix, (3) supply chain efficiencies, (4) strategic & other issues, and (5) strength of financials.

While the 5-S score ranks these companies on relative attractiveness on operating parameters, we weigh the 5-S score against the valuation score to pick potential winners.

Based on the 5-S / valuation score analysis, BCORP and DBEL are the most attractive. JKCE, OPI and MC offer favorable trade-off of quality and attractive valuations.

Attractive valuations - base case returns of 50%+, bull case returns of 2-4x

Our Mid Cap Cement Universe is currently trading at very attractive valuations of ~4.7x/3.9x FY14/FY15 EV/EBITDA and ~USD69/USD64 EV/Ton (FY14/FY15), considering improvement in operating performance and superior earnings growth.

We believe the Mid Caps offer better risk-reward and initiate coverage on seven Mid Cap Cement stocks. We recommend Buy on BCORP, DBEL, JKCE, JKLC, OPI, MC, and ICEM and Neutral on CENT and PRSC.

WIN – Week In a Nutshell 13 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

INDIA ENERGY: Diesel De Regulation – A Game Changing Event. Event: The Indian government announced the landmark decisions for the Indian energy sector: OMC’s to make

small revisions to diesel prices until it is at par with market prices – To hike prices by INR0.5/ltr per month; and Sales to bulk diesel buyers at market price - constitute ~12-17% of OMC’s diesel sales;

Expect INR465b (30%) savings in under recoveries in next 12 months through INR0.5/ltr per month price hike in diesel: Current under recoveries stand at INR9.6/ltr in diesel, INR30.6/ltr in Kerosene and INR490/cylinder in LPG and FY13E under recoveries are estimated at INR1.6t (v/s INR1.4t in FY12). Assuming INR0.5/ltr diesel price hike over the 12-month period, we estimate under recoveries reduction of INR465b to INR1.1t in FY14.

Valuation and view:

Upstream companies (ONGC/Oil India) better placed: We remain positive on ONGC and Oil India in upstream space and apart from subsidy rationalization, gas price hike is a common trigger for both the companies. We remain Neutral on Gail India due to headwinds for incremental gas, which could result in network underutilization and lower return ratios.

ONGC: Preferred bet - Even if the govt. were to increase upstream subsidy burden from 40% to 55%, it would be EPS accretive. For every USD1/bbl improvement in the net realization ONGC’s EPS will increase by INR0.7/share.

BPCL is top pick in OMC’s: In OMC’s, BPCL (BPCL IN, Mkt Cap USD5.3b, CMP INR396, Buy) is our top pick due to its E&P upside potential. Assuming ~25% savings in the interest cost over the next 2 years, OMC’s fair value would increase by 22%/33%/35% for HPCL/BPCL/IOCL respectively.

METALS WEEKLY: Iron ore prices may have peaked; HRC price hike not sticking in India Chinese steel price continue to rise as HRC and Rebar prices increased 2.3% and 2.8% WoW respectively.

Current HRC prices in China are at 8-month high levels while Rebar prices continue to remain subdued. Steel prices were flat in North America, CIS and Europe.

Indian long steel price (TMT Mumbai) and flat steel prices (Import parity) increased 1.4% and 0.4% WoW respectively. Sponge iron and scrap iron prices decreased by 0.9% and 1.4% WoW respectively.

Although import HRC prices have increased in last 2 months, yet domestic prices haven't moved up similarly.

Iron ore prices remained flat WoW at USD154/ton DMT amid heightened volatility. During the week, the prices rose to USD160/ton before correcting back to USD154/ton as buying thinned out. Coking coal prices increased by USD3.5 WoW to USD163.5/t due to supply side concerns.

Base metals prices were mixed with aluminum and copper increasing 1% WoW each while Zinc and Lead prices declined 1% WoW.

The Shah Commission is expected to present its report on mining scam in Odisha to the Central government by the end of this month.

WIN – Week In a Nutshell 14 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

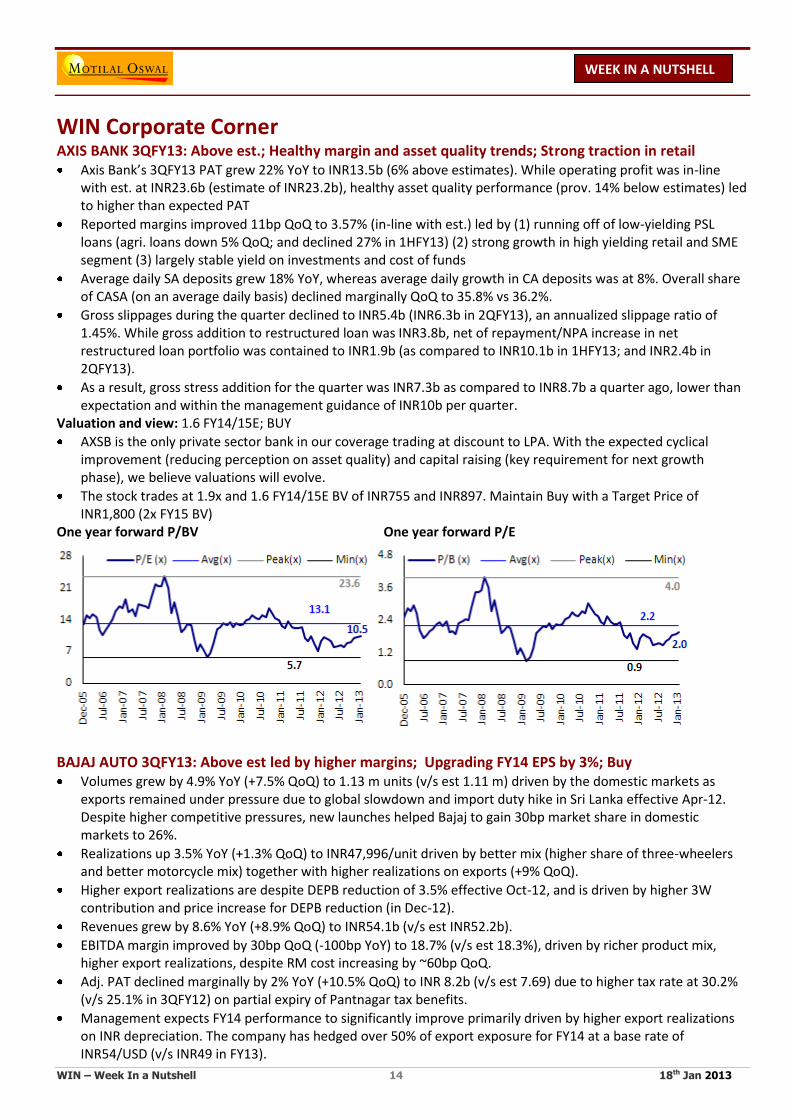

WIN Corporate Corner AXIS BANK 3QFY13: Above est.; Healthy margin and asset quality trends; Strong traction in retail Axis Bank’s 3QFY13 PAT grew 22% YoY to INR13.5b (6% above estimates). While operating profit was in-line

with est. at INR23.6b (estimate of INR23.2b), healthy asset quality performance (prov. 14% below estimates) led to higher than expected PAT

Reported margins improved 11bp QoQ to 3.57% (in-line with est.) led by (1) running off of low-yielding PSL loans (agri. loans down 5% QoQ; and declined 27% in 1HFY13) (2) strong growth in high yielding retail and SME segment (3) largely stable yield on investments and cost of funds

Average daily SA deposits grew 18% YoY, whereas average daily growth in CA deposits was at 8%. Overall share of CASA (on an average daily basis) declined marginally QoQ to 35.8% vs 36.2%.

Gross slippages during the quarter declined to INR5.4b (INR6.3b in 2QFY13), an annualized slippage ratio of 1.45%. While gross addition to restructured loan was INR3.8b, net of repayment/NPA increase in net restructured loan portfolio was contained to INR1.9b (as compared to INR10.1b in 1HFY13; and INR2.4b in 2QFY13).

As a result, gross stress addition for the quarter was INR7.3b as compared to INR8.7b a quarter ago, lower than expectation and within the management guidance of INR10b per quarter.

Valuation and view: 1.6 FY14/15E; BUY

AXSB is the only private sector bank in our coverage trading at discount to LPA. With the expected cyclical improvement (reducing perception on asset quality) and capital raising (key requirement for next growth phase), we believe valuations will evolve.

The stock trades at 1.9x and 1.6 FY14/15E BV of INR755 and INR897. Maintain Buy with a Target Price of INR1,800 (2x FY15 BV)

One year forward P/BV One year forward P/E

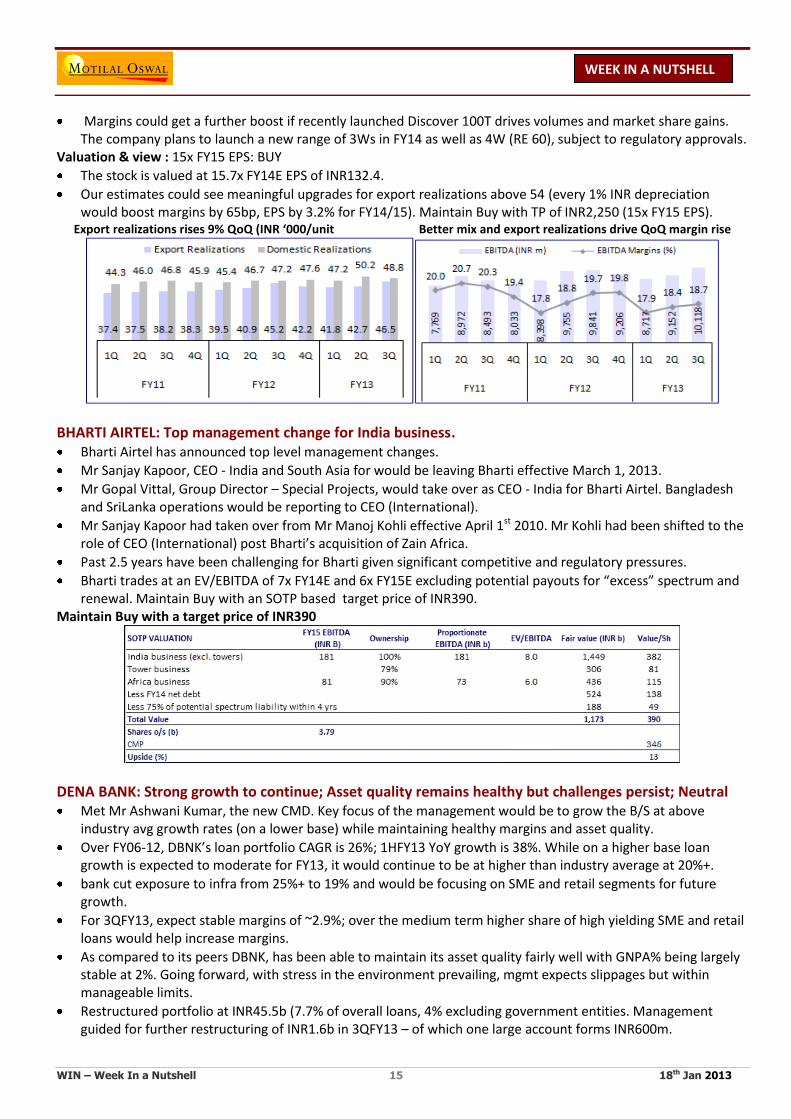

BAJAJ AUTO 3QFY13: Above est led by higher margins; Upgrading FY14 EPS by 3%; Buy Volumes grew by 4.9% YoY (+7.5% QoQ) to 1.13 m units (v/s est 1.11 m) driven by the domestic markets as

exports remained under pressure due to global slowdown and import duty hike in Sri Lanka effective Apr-12. Despite higher competitive pressures, new launches helped Bajaj to gain 30bp market share in domestic markets to 26%.

Realizations up 3.5% YoY (+1.3% QoQ) to INR47,996/unit driven by better mix (higher share of three-wheelers and better motorcycle mix) together with higher realizations on exports (+9% QoQ).

Higher export realizations are despite DEPB reduction of 3.5% effective Oct-12, and is driven by higher 3W contribution and price increase for DEPB reduction (in Dec-12).

Revenues grew by 8.6% YoY (+8.9% QoQ) to INR54.1b (v/s est INR52.2b).

EBITDA margin improved by 30bp QoQ (-100bp YoY) to 18.7% (v/s est 18.3%), driven by richer product mix, higher export realizations, despite RM cost increasing by ~60bp QoQ.

Adj. PAT declined marginally by 2% YoY (+10.5% QoQ) to INR 8.2b (v/s est 7.69) due to higher tax rate at 30.2% (v/s 25.1% in 3QFY12) on partial expiry of Pantnagar tax benefits.

Management expects FY14 performance to significantly improve primarily driven by higher export realizations on INR depreciation. The company has hedged over 50% of export exposure for FY14 at a base rate of INR54/USD (v/s INR49 in FY13).

WIN – Week In a Nutshell 15 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

Margins could get a further boost if recently launched Discover 100T drives volumes and market share gains. The company plans to launch a new range of 3Ws in FY14 as well as 4W (RE 60), subject to regulatory approvals.

Valuation & view : 15x FY15 EPS: BUY

The stock is valued at 15.7x FY14E EPS of INR132.4.

Our estimates could see meaningful upgrades for export realizations above 54 (every 1% INR depreciation would boost margins by 65bp, EPS by 3.2% for FY14/15). Maintain Buy with TP of INR2,250 (15x FY15 EPS).

Export realizations rises 9% QoQ (INR ‘000/unit Better mix and export realizations drive QoQ margin rise

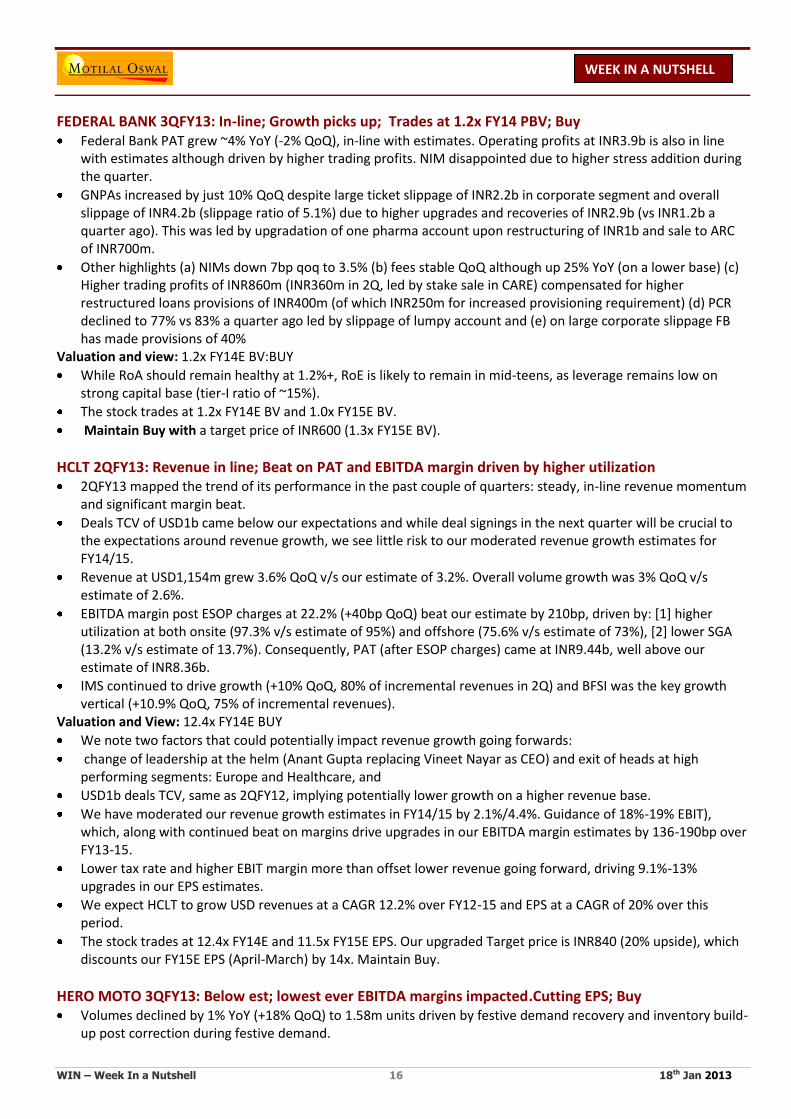

BHARTI AIRTEL: Top management change for India business. Bharti Airtel has announced top level management changes.

Mr Sanjay Kapoor, CEO - India and South Asia for would be leaving Bharti effective March 1, 2013.

Mr Gopal Vittal, Group Director – Special Projects, would take over as CEO - India for Bharti Airtel. Bangladesh and SriLanka operations would be reporting to CEO (International).

Mr Sanjay Kapoor had taken over from Mr Manoj Kohli effective April 1st 2010. Mr Kohli had been shifted to the role of CEO (International) post Bharti’s acquisition of Zain Africa.

Past 2.5 years have been challenging for Bharti given significant competitive and regulatory pressures.

Bharti trades at an EV/EBITDA of 7x FY14E and 6x FY15E excluding potential payouts for “excess” spectrum and renewal. Maintain Buy with an SOTP based target price of INR390.

Maintain Buy with a target price of INR390

DENA BANK: Strong growth to continue; Asset quality remains healthy but challenges persist; Neutral Met Mr Ashwani Kumar, the new CMD. Key focus of the management would be to grow the B/S at above

industry avg growth rates (on a lower base) while maintaining healthy margins and asset quality.

Over FY06-12, DBNK’s loan portfolio CAGR is 26%; 1HFY13 YoY growth is 38%. While on a higher base loan growth is expected to moderate for FY13, it would continue to be at higher than industry average at 20%+.

bank cut exposure to infra from 25%+ to 19% and would be focusing on SME and retail segments for future growth.

For 3QFY13, expect stable margins of ~2.9%; over the medium term higher share of high yielding SME and retail loans would help increase margins.

As compared to its peers DBNK, has been able to maintain its asset quality fairly well with GNPA% being largely stable at 2%. Going forward, with stress in the environment prevailing, mgmt expects slippages but within manageable limits.

Restructured portfolio at INR45.5b (7.7% of overall loans, 4% excluding government entities. Management guided for further restructuring of INR1.6b in 3QFY13 – of which one large account forms INR600m.

WIN – Week In a Nutshell 16 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

FEDERAL BANK 3QFY13: In-line; Growth picks up; Trades at 1.2x FY14 PBV; Buy Federal Bank PAT grew ~4% YoY (-2% QoQ), in-line with estimates. Operating profits at INR3.9b is also in line

with estimates although driven by higher trading profits. NIM disappointed due to higher stress addition during the quarter.

GNPAs increased by just 10% QoQ despite large ticket slippage of INR2.2b in corporate segment and overall slippage of INR4.2b (slippage ratio of 5.1%) due to higher upgrades and recoveries of INR2.9b (vs INR1.2b a quarter ago). This was led by upgradation of one pharma account upon restructuring of INR1b and sale to ARC of INR700m.

Other highlights (a) NIMs down 7bp qoq to 3.5% (b) fees stable QoQ although up 25% YoY (on a lower base) (c) Higher trading profits of INR860m (INR360m in 2Q, led by stake sale in CARE) compensated for higher restructured loans provisions of INR400m (of which INR250m for increased provisioning requirement) (d) PCR declined to 77% vs 83% a quarter ago led by slippage of lumpy account and (e) on large corporate slippage FB has made provisions of 40%

Valuation and view: 1.2x FY14E BV:BUY

While RoA should remain healthy at 1.2%+, RoE is likely to remain in mid-teens, as leverage remains low on strong capital base (tier-I ratio of ~15%).

The stock trades at 1.2x FY14E BV and 1.0x FY15E BV.

Maintain Buy with a target price of INR600 (1.3x FY15E BV).

HCLT 2QFY13: Revenue in line; Beat on PAT and EBITDA margin driven by higher utilization 2QFY13 mapped the trend of its performance in the past couple of quarters: steady, in-line revenue momentum

and significant margin beat.

Deals TCV of USD1b came below our expectations and while deal signings in the next quarter will be crucial to the expectations around revenue growth, we see little risk to our moderated revenue growth estimates for FY14/15.

Revenue at USD1,154m grew 3.6% QoQ v/s our estimate of 3.2%. Overall volume growth was 3% QoQ v/s estimate of 2.6%.

EBITDA margin post ESOP charges at 22.2% (+40bp QoQ) beat our estimate by 210bp, driven by: [1] higher utilization at both onsite (97.3% v/s estimate of 95%) and offshore (75.6% v/s estimate of 73%), [2] lower SGA (13.2% v/s estimate of 13.7%). Consequently, PAT (after ESOP charges) came at INR9.44b, well above our estimate of INR8.36b.

IMS continued to drive growth (+10% QoQ, 80% of incremental revenues in 2Q) and BFSI was the key growth vertical (+10.9% QoQ, 75% of incremental revenues).

Valuation and View: 12.4x FY14E BUY

We note two factors that could potentially impact revenue growth going forwards:

change of leadership at the helm (Anant Gupta replacing Vineet Nayar as CEO) and exit of heads at high performing segments: Europe and Healthcare, and

USD1b deals TCV, same as 2QFY12, implying potentially lower growth on a higher revenue base.

We have moderated our revenue growth estimates in FY14/15 by 2.1%/4.4%. Guidance of 18%-19% EBIT), which, along with continued beat on margins drive upgrades in our EBITDA margin estimates by 136-190bp over FY13-15.

Lower tax rate and higher EBIT margin more than offset lower revenue going forward, driving 9.1%-13% upgrades in our EPS estimates.

We expect HCLT to grow USD revenues at a CAGR 12.2% over FY12-15 and EPS at a CAGR of 20% over this period.

The stock trades at 12.4x FY14E and 11.5x FY15E EPS. Our upgraded Target price is INR840 (20% upside), which discounts our FY15E EPS (April-March) by 14x. Maintain Buy.

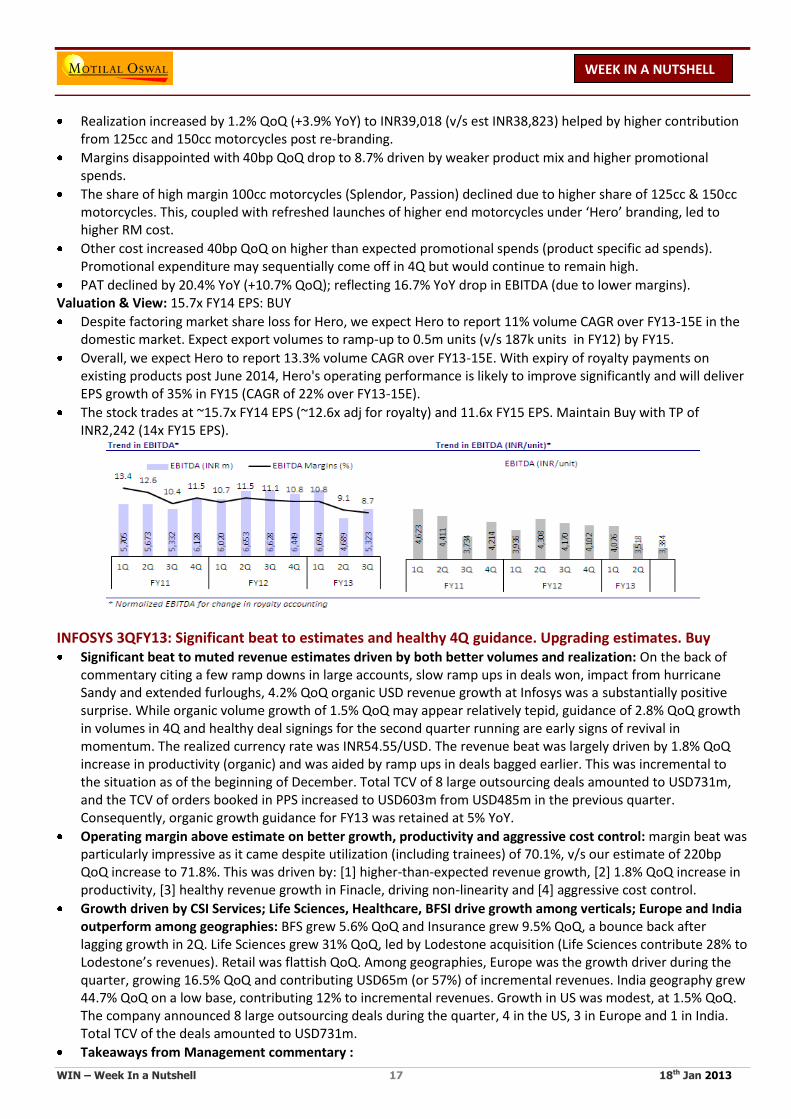

HERO MOTO 3QFY13: Below est; lowest ever EBITDA margins impacted.Cutting EPS; Buy Volumes declined by 1% YoY (+18% QoQ) to 1.58m units driven by festive demand recovery and inventory build-

up post correction during festive demand.

WIN – Week In a Nutshell 17 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

Realization increased by 1.2% QoQ (+3.9% YoY) to INR39,018 (v/s est INR38,823) helped by higher contribution from 125cc and 150cc motorcycles post re-branding.

Margins disappointed with 40bp QoQ drop to 8.7% driven by weaker product mix and higher promotional spends.

The share of high margin 100cc motorcycles (Splendor, Passion) declined due to higher share of 125cc & 150cc motorcycles. This, coupled with refreshed launches of higher end motorcycles under ‘Hero’ branding, led to higher RM cost.

Other cost increased 40bp QoQ on higher than expected promotional spends (product specific ad spends). Promotional expenditure may sequentially come off in 4Q but would continue to remain high.

PAT declined by 20.4% YoY (+10.7% QoQ); reflecting 16.7% YoY drop in EBITDA (due to lower margins). Valuation & View: 15.7x FY14 EPS: BUY

Despite factoring market share loss for Hero, we expect Hero to report 11% volume CAGR over FY13-15E in the domestic market. Expect export volumes to ramp-up to 0.5m units (v/s 187k units in FY12) by FY15.

Overall, we expect Hero to report 13.3% volume CAGR over FY13-15E. With expiry of royalty payments on existing products post June 2014, Hero's operating performance is likely to improve significantly and will deliver EPS growth of 35% in FY15 (CAGR of 22% over FY13-15E).

The stock trades at ~15.7x FY14 EPS (~12.6x adj for royalty) and 11.6x FY15 EPS. Maintain Buy with TP of INR2,242 (14x FY15 EPS).

INFOSYS 3QFY13: Significant beat to estimates and healthy 4Q guidance. Upgrading estimates. Buy Significant beat to muted revenue estimates driven by both better volumes and realization: On the back of

commentary citing a few ramp downs in large accounts, slow ramp ups in deals won, impact from hurricane Sandy and extended furloughs, 4.2% QoQ organic USD revenue growth at Infosys was a substantially positive surprise. While organic volume growth of 1.5% QoQ may appear relatively tepid, guidance of 2.8% QoQ growth in volumes in 4Q and healthy deal signings for the second quarter running are early signs of revival in momentum. The realized currency rate was INR54.55/USD. The revenue beat was largely driven by 1.8% QoQ increase in productivity (organic) and was aided by ramp ups in deals bagged earlier. This was incremental to the situation as of the beginning of December. Total TCV of 8 large outsourcing deals amounted to USD731m, and the TCV of orders booked in PPS increased to USD603m from USD485m in the previous quarter. Consequently, organic growth guidance for FY13 was retained at 5% YoY.

Operating margin above estimate on better growth, productivity and aggressive cost control: margin beat was particularly impressive as it came despite utilization (including trainees) of 70.1%, v/s our estimate of 220bp QoQ increase to 71.8%. This was driven by: [1] higher-than-expected revenue growth, [2] 1.8% QoQ increase in productivity, [3] healthy revenue growth in Finacle, driving non-linearity and [4] aggressive cost control.

Growth driven by CSI Services; Life Sciences, Healthcare, BFSI drive growth among verticals; Europe and India outperform among geographies: BFS grew 5.6% QoQ and Insurance grew 9.5% QoQ, a bounce back after lagging growth in 2Q. Life Sciences grew 31% QoQ, led by Lodestone acquisition (Life Sciences contribute 28% to Lodestone’s revenues). Retail was flattish QoQ. Among geographies, Europe was the growth driver during the quarter, growing 16.5% QoQ and contributing USD65m (or 57%) of incremental revenues. India geography grew 44.7% QoQ on a low base, contributing 12% to incremental revenues. Growth in US was modest, at 1.5% QoQ. The company announced 8 large outsourcing deals during the quarter, 4 in the US, 3 in Europe and 1 in India. Total TCV of the deals amounted to USD731m.

Takeaways from Management commentary :

WIN – Week In a Nutshell 18 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

o CY13 - continued cost takeout to drive growth amid flat-to-marginally down budgets o Recovery protracted but clients confident: at the micro level clients are getting more confident, even in the

event of a flat budget, offshoring will increase YoY in CY13. o Pricing pressures remain but realization to stay in a narrow band o Managing utilization and pricing remain key from margin standpoint o Expect traction to continue at BPO, India: Healthy growth in 3Q was significantly a factor of performance at

Finacle, BPO and India (all 3 segments headed by Bala). Valuation and View: BUY

Upgrading FY14/15 Revenue estimates by 3.1-4.5%, EPS by 4.2-5.7%:

We are rolling over our target price to FY15E estimates, we are revising our target price upwards to INR3,110, which discounts by FY15E EPS by 16x. Maintain Buy.

L&T: Divestment of stake in Dhamra Port; Monetization of matured assets is a key ROE trigger Adani group has reportedly agreed to buy out 100% stake in Dhamra Port (50:50 JV between L&T and Tata

Steel) for a total enterprise value of USD1b (INR55b). However, any announcement in this regard is yet to be made by the JV partners. L&T has made a total investment of INR6910m (INR3240m of equity investment and INR3670m of subordinate debts) in the venture.

We believe the development is a positive for L&T as it will have a positive impact on consolidated ROE and will also substantiate management’s seriousness and ability in getting out of non-core activities as well as monetization of matured assets.

The transaction will lead to a 6% (~INR20b) reduction in the consolidated net debt of L&T which stands at INR350b. The deal will also help in improving the consolidated ROE through capital rationalization as the JV has posted a loss of INR4580m during FY12 (L&Ts share is INR2290m; losses were expected to come down).

L&T’s E&C business has remained largely unscathed all through the challenging environment. This is reflected in standalone RoE (i.e. net of investments in subsidiaries) being maintained at a robust 31% in FY12.

The company has been making serious attempts to correct its capital structure and improve returns on capital. We believe that the roadmap towards meaningful improvement in RoE would be led by segment-specific three-pronged strategy: i) Manufacturing businesses: attempt will be to defend its investments, given the long-term growth potential, sacrificing near-term return ratios ii) Infrastructure development: attempt will be to monetize the assets and churn the portfolio iii) Service businesses (IT, Finance, etc): focus will be to build scale

Valuation & view: BUY

We expect L&T to report standalone revenue CAGR of 16% and PAT CAGR of 14% over FY13-15; consolidated PAT CAGR would be 13%.

We maintain Buy with a SOTP-based target price of INR2000 . We have valued LT standalone at 14x FY15EPS and subsidiaries at INR581/share.

NIIT Technologies 3QFY13: Below estimates; Guidance of margin improvement from FY14 NIIT Technologies 3QFY13 reported revenues at INR5,144m grew 2.9% QoQ, above our estimate of INR5,001m.

Revenue growth in constant currency was 4.4% QoQ, v/s our estimate of 3.9% QoQ. However, excluding hardware components, constant currency revenue growth was only 1.8% QoQ.

EBITDA margin declined 120bp QoQ to 15.8%, v/s our estimate of 50bp QoQ expansion to 17.5%. Key factors driving sequential margin decline include: [1] Lower profitability in the traditionally higher margin segments – GIS and NITL (~60bp as per our calculations), [2] Transition costs in the new deal bagged from Morris in the last quarter (~40bp impact). PAT was INR561m, marginally higher than our estimate of INR550m due to forex gain of INR103m.

The company signed USD83m worth TCV of orders in 3QFY13. Executable order book over the next 12 months is USD242m, staying within the band of USD230-255m for the sixt consecutive quarter. The management however guided for an improvement in the metric in the next quarter, which is seasonally the strongest for the company.

WIN – Week In a Nutshell 19 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

The company re-iterated its outlook of FY13 revenue growth exceeding 14%, despite a non-exciting first half. It also guided for improvement in margins going forward, with a slight uptick in 4Q and a significant turnaround in the trajectory not before the beginning of FY14.

Valuation and View:

We have revised our EBIT margin estimates downwards for FY14/15 by 71bp/115bp, driving 6.1%/4.8% cut in our EPS estimates. We expect the company to grow its USD revenues at a CAGR of 15.5% over FY13-15E and EPS at a CAGR of 9.5% during this period. NITEC trades at a significant discount to its peer group. Turnaround in growth rates at NITL and GIS and improvement in margin profile of existing and new large deals over time will be key drivers to a change in our view. Maintain Neutral.

PETRONET LNG 3QFY13: Above est. led by higher volumes; Kochi delayed to Apr-13; Buy Petronet LNG reported highest ever quarterly PAT of INR3.2b (v/s est INR2.9b, +8% YoY/+1% QoQ) due to

higher than expected throughput of 141 tbtu’s (estimated 134 tbtu) and continued high marketing margins. Implied marketing margins stood at USD0.75/mmbtu (v/s est of USD0.74/mmbtu).

Capacity utilization at 112%, despite higher spot LNG prices: 3QFY13 re-gasified volumes were up 4% QoQ (5% higher than our expectations) at 141tbtu (2.8mmt) v/s 135btu (2.7mmt) in 2QFY13. Higher than expected volumes were largely driven by higher long-term contract volumes.

However, despite higher QoQ LNG prices in second half of 3QFY13, third-party/spot volumes were resilient and believe was due to higher volumes in the first half 3QFY13.

Long term volume stood at 97tbtu (-2%YoY; +7% QoQ); third-party re-gas volumes at 14tbtu (-35% YoY; -19% QoQ) and pure short term volumes were at 30tbtu (-19% YoY; +9% QoQ).

Commercial operations of Kochi terminal are expected to start by Apr-13 (v/s earlier guidance of March-13) once consumers are ready (conversion/up-gradation of equipment is complete) to off-take gas.

2nd jetty project at Dahej to complete by Dec-13/Jan-14,

Capacity expansion to 15 mmt by 2HFY16 (taking Dahej capacity to 18mmt) and

Commissioning of Gangavaram terminal by CY15-end and interim FSRU facility (through leasing) by CY14-end.

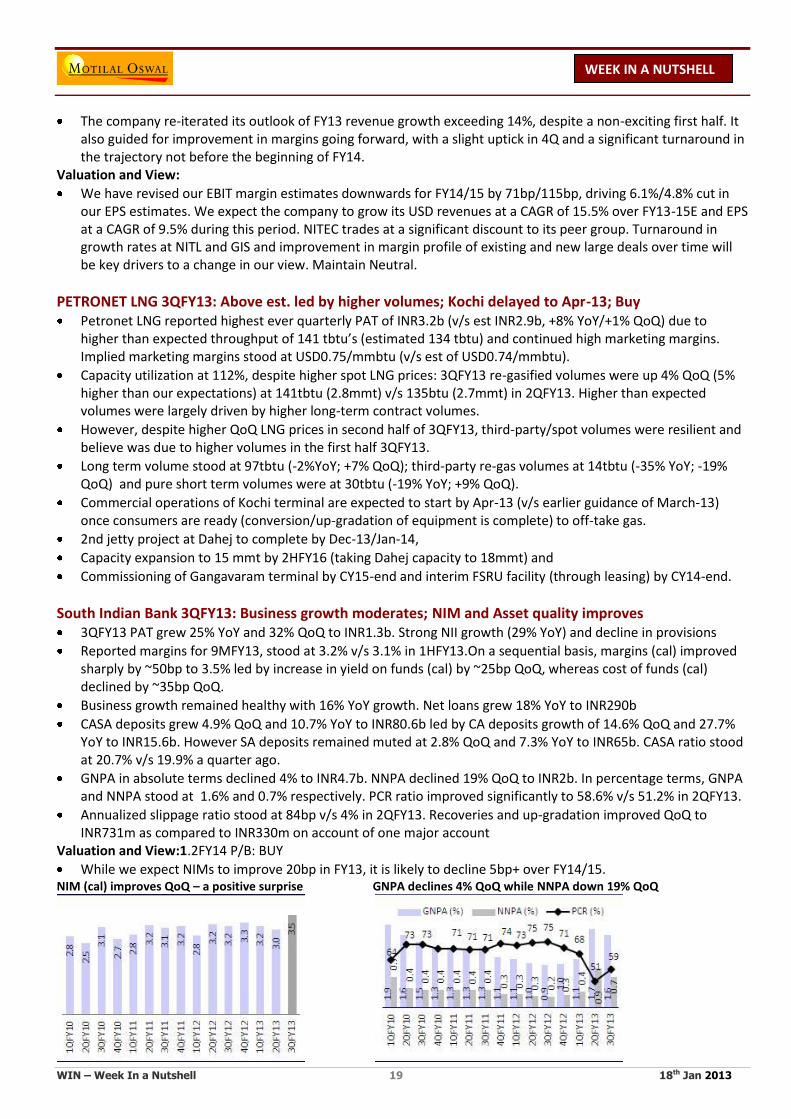

South Indian Bank 3QFY13: Business growth moderates; NIM and Asset quality improves 3QFY13 PAT grew 25% YoY and 32% QoQ to INR1.3b. Strong NII growth (29% YoY) and decline in provisions

Reported margins for 9MFY13, stood at 3.2% v/s 3.1% in 1HFY13.On a sequential basis, margins (cal) improved sharply by ~50bp to 3.5% led by increase in yield on funds (cal) by ~25bp QoQ, whereas cost of funds (cal) declined by ~35bp QoQ.

Business growth remained healthy with 16% YoY growth. Net loans grew 18% YoY to INR290b

CASA deposits grew 4.9% QoQ and 10.7% YoY to INR80.6b led by CA deposits growth of 14.6% QoQ and 27.7% YoY to INR15.6b. However SA deposits remained muted at 2.8% QoQ and 7.3% YoY to INR65b. CASA ratio stood at 20.7% v/s 19.9% a quarter ago.

GNPA in absolute terms declined 4% to INR4.7b. NNPA declined 19% QoQ to INR2b. In percentage terms, GNPA and NNPA stood at 1.6% and 0.7% respectively. PCR ratio improved significantly to 58.6% v/s 51.2% in 2QFY13.

Annualized slippage ratio stood at 84bp v/s 4% in 2QFY13. Recoveries and up-gradation improved QoQ to INR731m as compared to INR330m on account of one major account

Valuation and View:1.2FY14 P/B: BUY

While we expect NIMs to improve 20bp in FY13, it is likely to decline 5bp+ over FY14/15. NIM (cal) improves QoQ – a positive surprise GNPA declines 4% QoQ while NNPA down 19% QoQ

WIN – Week In a Nutshell 20 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

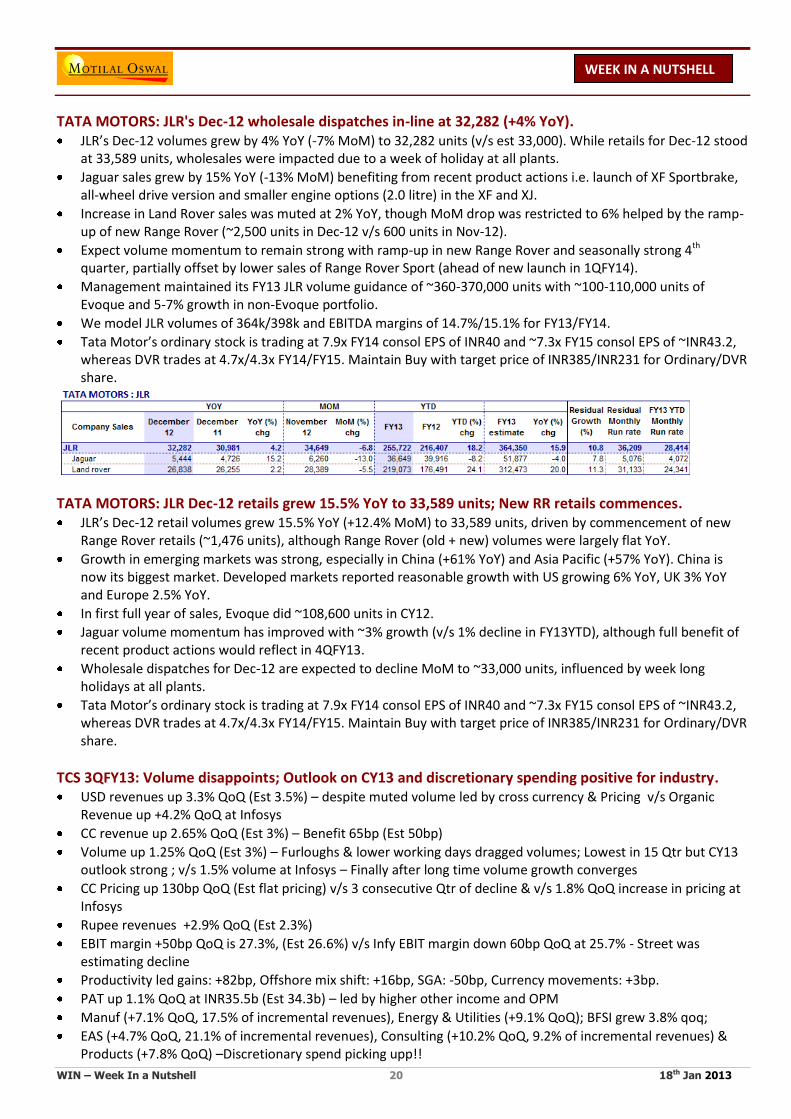

TATA MOTORS: JLR's Dec-12 wholesale dispatches in-line at 32,282 (+4% YoY). JLR’s Dec-12 volumes grew by 4% YoY (-7% MoM) to 32,282 units (v/s est 33,000). While retails for Dec-12 stood

at 33,589 units, wholesales were impacted due to a week of holiday at all plants.

Jaguar sales grew by 15% YoY (-13% MoM) benefiting from recent product actions i.e. launch of XF Sportbrake, all-wheel drive version and smaller engine options (2.0 litre) in the XF and XJ.

Increase in Land Rover sales was muted at 2% YoY, though MoM drop was restricted to 6% helped by the ramp-up of new Range Rover (~2,500 units in Dec-12 v/s 600 units in Nov-12).

Expect volume momentum to remain strong with ramp-up in new Range Rover and seasonally strong 4th quarter, partially offset by lower sales of Range Rover Sport (ahead of new launch in 1QFY14).

Management maintained its FY13 JLR volume guidance of ~360-370,000 units with ~100-110,000 units of Evoque and 5-7% growth in non-Evoque portfolio.

We model JLR volumes of 364k/398k and EBITDA margins of 14.7%/15.1% for FY13/FY14.

Tata Motor’s ordinary stock is trading at 7.9x FY14 consol EPS of INR40 and ~7.3x FY15 consol EPS of ~INR43.2, whereas DVR trades at 4.7x/4.3x FY14/FY15. Maintain Buy with target price of INR385/INR231 for Ordinary/DVR share.

TATA MOTORS: JLR Dec-12 retails grew 15.5% YoY to 33,589 units; New RR retails commences. JLR’s Dec-12 retail volumes grew 15.5% YoY (+12.4% MoM) to 33,589 units, driven by commencement of new

Range Rover retails (~1,476 units), although Range Rover (old + new) volumes were largely flat YoY.

Growth in emerging markets was strong, especially in China (+61% YoY) and Asia Pacific (+57% YoY). China is now its biggest market. Developed markets reported reasonable growth with US growing 6% YoY, UK 3% YoY and Europe 2.5% YoY.

In first full year of sales, Evoque did ~108,600 units in CY12.

Jaguar volume momentum has improved with ~3% growth (v/s 1% decline in FY13YTD), although full benefit of recent product actions would reflect in 4QFY13.

Wholesale dispatches for Dec-12 are expected to decline MoM to ~33,000 units, influenced by week long holidays at all plants.

Tata Motor’s ordinary stock is trading at 7.9x FY14 consol EPS of INR40 and ~7.3x FY15 consol EPS of ~INR43.2, whereas DVR trades at 4.7x/4.3x FY14/FY15. Maintain Buy with target price of INR385/INR231 for Ordinary/DVR share.

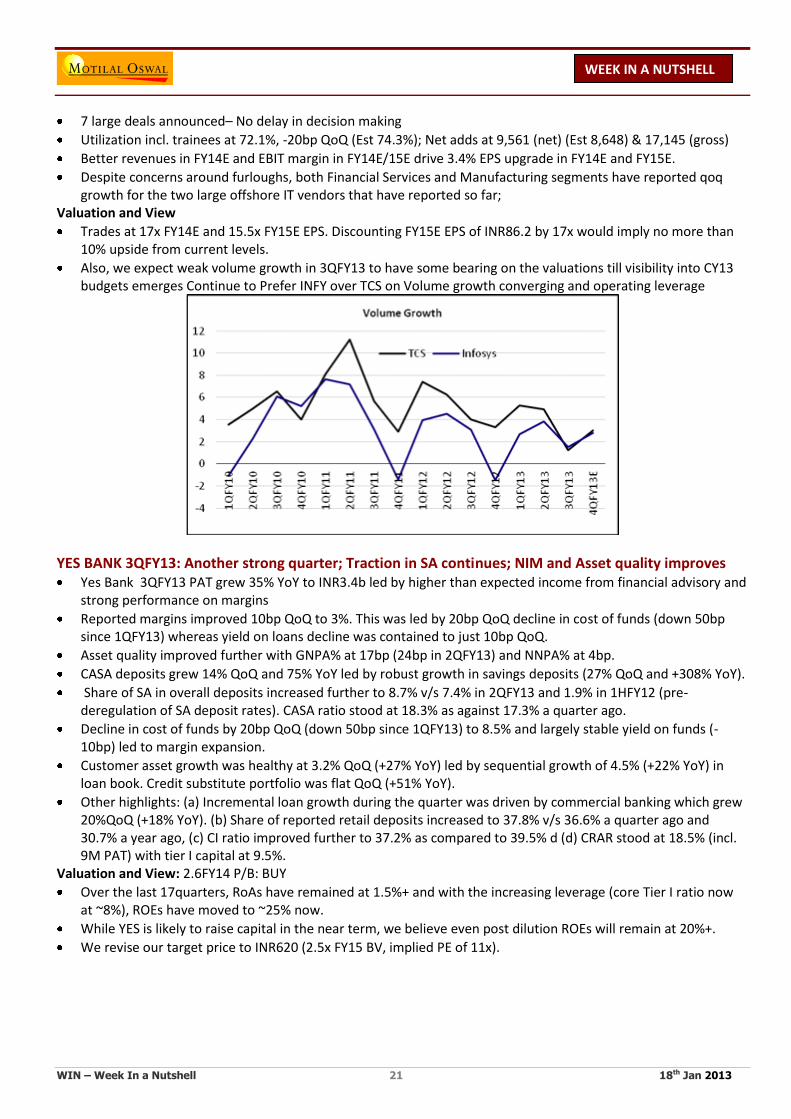

TCS 3QFY13: Volume disappoints; Outlook on CY13 and discretionary spending positive for industry. USD revenues up 3.3% QoQ (Est 3.5%) – despite muted volume led by cross currency & Pricing v/s Organic

Revenue up +4.2% QoQ at Infosys

CC revenue up 2.65% QoQ (Est 3%) – Benefit 65bp (Est 50bp)

Volume up 1.25% QoQ (Est 3%) – Furloughs & lower working days dragged volumes; Lowest in 15 Qtr but CY13 outlook strong ; v/s 1.5% volume at Infosys – Finally after long time volume growth converges

CC Pricing up 130bp QoQ (Est flat pricing) v/s 3 consecutive Qtr of decline & v/s 1.8% QoQ increase in pricing at Infosys

Rupee revenues +2.9% QoQ (Est 2.3%)

EBIT margin +50bp QoQ is 27.3%, (Est 26.6%) v/s Infy EBIT margin down 60bp QoQ at 25.7% - Street was estimating decline

Productivity led gains: +82bp, Offshore mix shift: +16bp, SGA: -50bp, Currency movements: +3bp.

PAT up 1.1% QoQ at INR35.5b (Est 34.3b) – led by higher other income and OPM

Manuf (+7.1% QoQ, 17.5% of incremental revenues), Energy & Utilities (+9.1% QoQ); BFSI grew 3.8% qoq;

EAS (+4.7% QoQ, 21.1% of incremental revenues), Consulting (+10.2% QoQ, 9.2% of incremental revenues) & Products (+7.8% QoQ) –Discretionary spend picking upp!!

WIN – Week In a Nutshell 21 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

7 large deals announced– No delay in decision making

Utilization incl. trainees at 72.1%, -20bp QoQ (Est 74.3%); Net adds at 9,561 (net) (Est 8,648) & 17,145 (gross)

Better revenues in FY14E and EBIT margin in FY14E/15E drive 3.4% EPS upgrade in FY14E and FY15E.

Despite concerns around furloughs, both Financial Services and Manufacturing segments have reported qoq growth for the two large offshore IT vendors that have reported so far;

Valuation and View

Trades at 17x FY14E and 15.5x FY15E EPS. Discounting FY15E EPS of INR86.2 by 17x would imply no more than 10% upside from current levels.

Also, we expect weak volume growth in 3QFY13 to have some bearing on the valuations till visibility into CY13 budgets emerges Continue to Prefer INFY over TCS on Volume growth converging and operating leverage

YES BANK 3QFY13: Another strong quarter; Traction in SA continues; NIM and Asset quality improves Yes Bank 3QFY13 PAT grew 35% YoY to INR3.4b led by higher than expected income from financial advisory and

strong performance on margins

Reported margins improved 10bp QoQ to 3%. This was led by 20bp QoQ decline in cost of funds (down 50bp since 1QFY13) whereas yield on loans decline was contained to just 10bp QoQ.

Asset quality improved further with GNPA% at 17bp (24bp in 2QFY13) and NNPA% at 4bp.

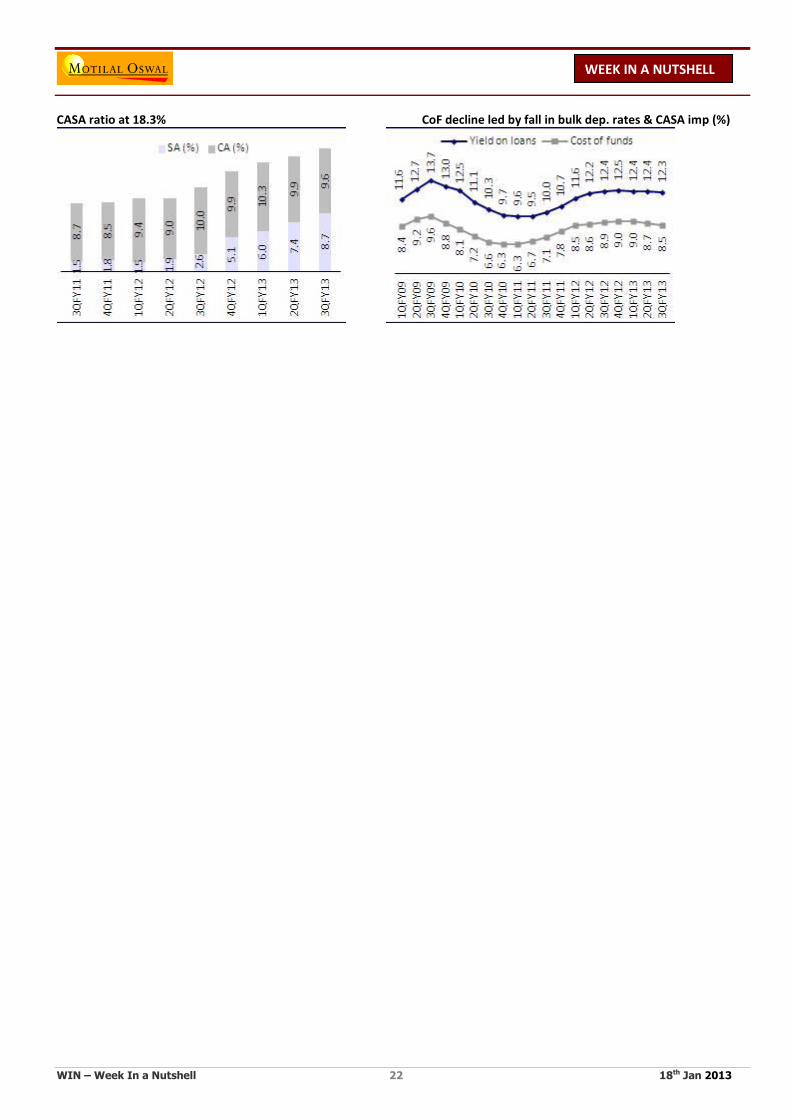

CASA deposits grew 14% QoQ and 75% YoY led by robust growth in savings deposits (27% QoQ and +308% YoY).

Share of SA in overall deposits increased further to 8.7% v/s 7.4% in 2QFY13 and 1.9% in 1HFY12 (pre-deregulation of SA deposit rates). CASA ratio stood at 18.3% as against 17.3% a quarter ago.

Decline in cost of funds by 20bp QoQ (down 50bp since 1QFY13) to 8.5% and largely stable yield on funds (-10bp) led to margin expansion.

Customer asset growth was healthy at 3.2% QoQ (+27% YoY) led by sequential growth of 4.5% (+22% YoY) in loan book. Credit substitute portfolio was flat QoQ (+51% YoY).

Other highlights: (a) Incremental loan growth during the quarter was driven by commercial banking which grew 20%QoQ (+18% YoY). (b) Share of reported retail deposits increased to 37.8% v/s 36.6% a quarter ago and 30.7% a year ago, (c) CI ratio improved further to 37.2% as compared to 39.5% d (d) CRAR stood at 18.5% (incl. 9M PAT) with tier I capital at 9.5%.

Valuation and View: 2.6FY14 P/B: BUY

Over the last 17quarters, RoAs have remained at 1.5%+ and with the increasing leverage (core Tier I ratio now at ~8%), ROEs have moved to ~25% now.

While YES is likely to raise capital in the near term, we believe even post dilution ROEs will remain at 20%+.

We revise our target price to INR620 (2.5x FY15 BV, implied PE of 11x).

WIN – Week In a Nutshell 22 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

CASA ratio at 18.3% CoF decline led by fall in bulk dep. rates & CASA imp (%)

WIN – Week In a Nutshell 23 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

WIN Collage The risks of a clash between China and Japan are rising—and the consequences could be calamitous

CHINA and Japan are sliding towards war. In the waters and skies around disputed islands, China is escalating actions designed to challenge decades of Japanese control. It is accompanying its campaign with increasingly blood-curdling rhetoric. Japan, says the China Daily, is the “real danger and threat to the world”. A military clash, says Global Times, is now “more likely…We need to prepare for the worst.” China appears to be preparing for the first armed confrontation between the two countries in seven decades (see article). China and Japan have well-known differences over history and territory—most pressingly over five islets, out in the East China Sea, which Japan controls and calls the Senkakus but which China lays claim to and calls the Diaoyus. Rational actors with deeply entwined economies are supposed to sort out their differences, or learn to put them safely to one side. At least, that was the assumption with China and But this changed in September, after Japan’s then prime minister, Yoshihiko Noda, nationalised the three islands Japan did not already own. It was a clumsy attempt to avoid them falling into the hands of Shintaro Ishihara, a right-wing China-baiter who was governor of Tokyo until late last year. Yet China insisted that the move was an anti-China conspiracy to strengthen Japan’s claim. It set out to blow a hole in Japanese pretensions to sole control of the waters and skies around the islands. Incursions by surveillance vessels came first. Then, in December, a patrol plane buzzed the islands; Japan scrambled fighter planes. This month Japanese and Chinese jets sought to tail each other near the islands’ air space. Japan, newspapers report, is considering ordering warning shots to be fired next time. A Chinese general says that would count as the start of “actual combat”. So long as China vies for control, conflict will be a hair-trigger away. This week senior American officials rushed to Tokyo to urge caution on Shinzo Abe’s hawkish new government. America is obliged to come to Japan’s aid if it is attacked, and being sucked into a conflict with China is almost too unbearable to contemplate. But in the face of repeated Chinese incursions, a Japanese reaction is understandable. Mr Abe has announced that after a decade of declining military budgets, defence spending will rise this year. This week he visited South-East Asia to shore up relations with countries that also have concerns about Chinese expansion. Mr Abe’s aims in South-East Asia were crude. But it may be that, short of simply handing the islands over, nothing that the Japanese government could do could satisfy China. This week an editorial in the China Daily acknowledged that Japan is working to build bridges with China, but immediately dismissed the efforts as part of a “two-faced strategy”. Japan, says China, is the threat—though, unlike China, it has not picked a military fight since 1945. Chinese diplomats accuse Japan of attempting to do down their country when it is beset by domestic challenges. Yet they bristle at the notion that Chinese incursions seek to take advantage of Japanese weaknesses, such as enfeebled governments and a sullen economy. China seems unwilling to entertain other perspectives or interests. The sources of this chauvinism are not entirely clear. It may be that the government is responding to the ultra-nationalist sentiments that people increasingly give voice to on the internet. Horrible history East Asian parallels from a century ago are hard to ignore. Then, as justification for continental expansion, a bullying Japan drank from a dangerous brew of nationalism and a manufactured sense of foreign aggression and victimhood. As China pursues a policy of maritime expansion, the rhetoric of victimisation is remarkably similar. The coming clash that China now talks about could be as calamitous as that previous one was. It would imperil not just China’s but the region’s peace and its momentous economic advances. The world, including America, has a duty to warn China before it is too late, though warnings will be interpreted as conspiracies. So who in China will speak out against this unfolding madness?

WIN – Week In a Nutshell 24 18th Jan 2013

WEEK IN A NUTSHELL

WEEK IN A NUTSHELL

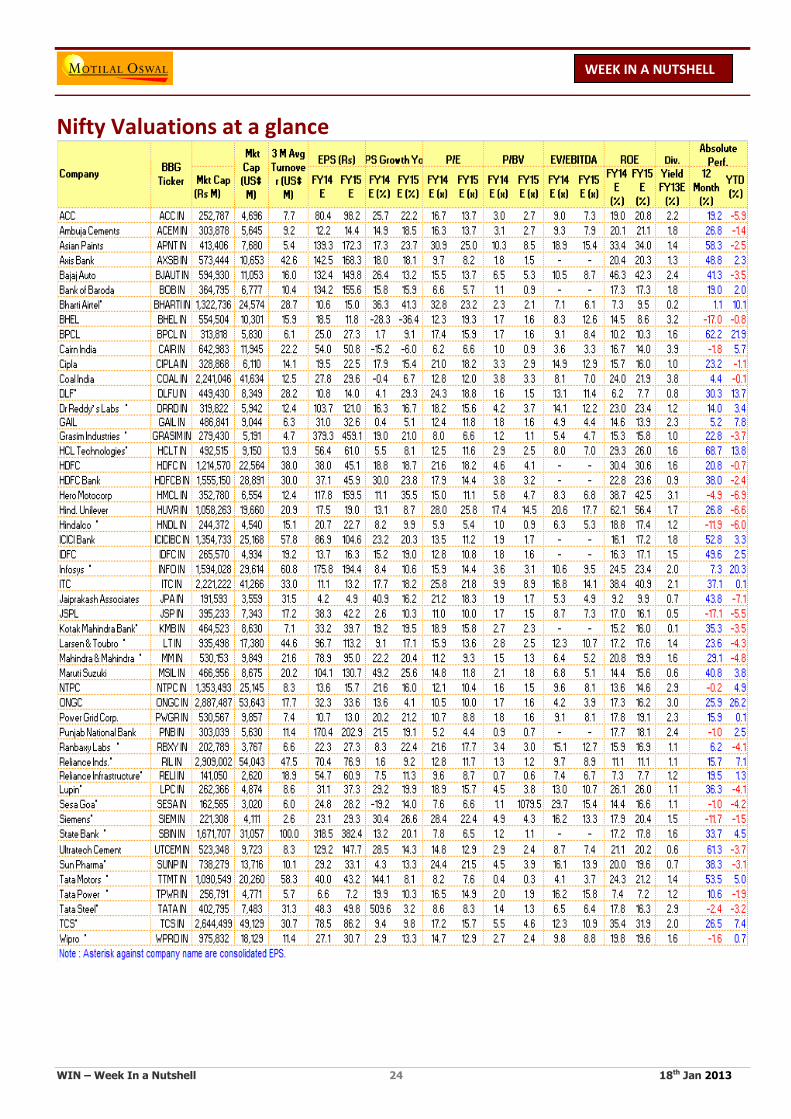

Nifty Valuations at a glance

![Transcript of the Concall with Investors [Company Update]](https://img.pdfslide.net/doc/110x75/577c87971a28abe054c4a93a/transcript-of-the-concall-with-investors-company-update.jpg)

![Concall Transcript [Company Update]](https://img.pdfslide.net/doc/110x75/577c79551a28abe0549247e6/concall-transcript-company-update.jpg)

![Earnings Concall Transcripts for Q4 FY 2015-16 [Company Update]](https://img.pdfslide.net/doc/110x75/577c7ba71a28abe0549822ab/earnings-concall-transcripts-for-q4-fy-2015-16-company-update.jpg)