Embed Size (px)

Citation preview

WIN In-House Counsel Day Melbourne Wednesday 16 March 2016

PREPARING YOUR BOARD FOR WINNING FROM

THE THREAT AND OPPORTUNITY OF NEW

TECHNOLOGIES

Joel Cox

David Hallam

TECHNOLOGY IS IN FOCUS FOR

GOOD REASON….

18 March 2016 WIN In-House Counsel Day, Melbourne 2

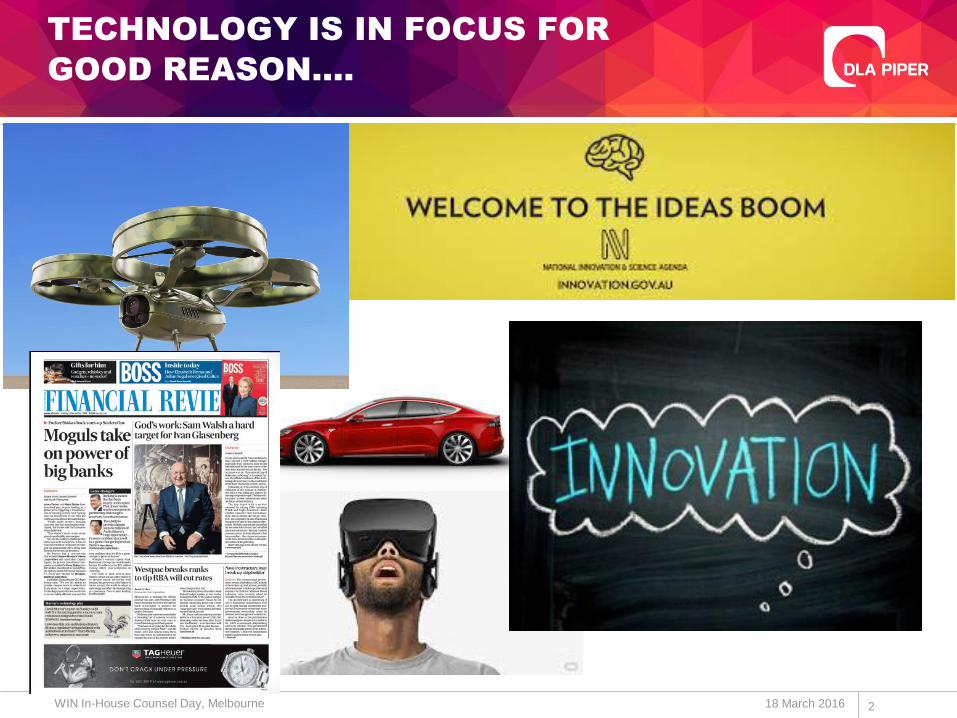

THE US HAS EXPERIENCED THE

BOOM…

18 March 2016 WIN In-House Counsel Day, Melbourne 3

US VC INVESTMENT AT 2 X PRE-RECESSION IN 2015

Source: PitchBook 2015 Annual US Venture Industry Report and Upfront Ventures 2016 Review

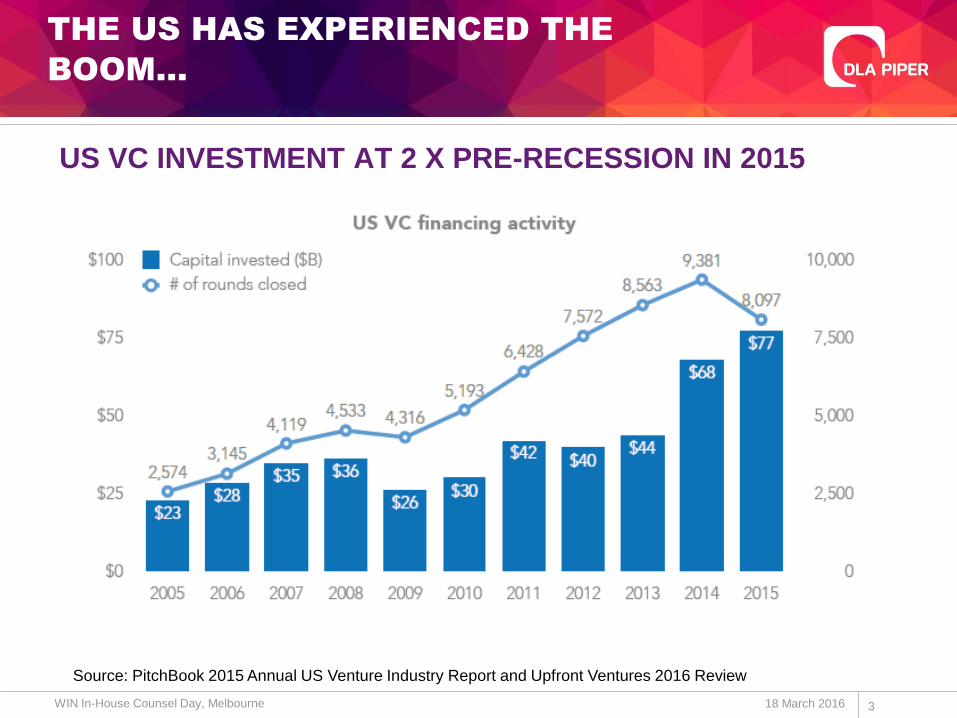

STRONG ANGEL, SEED AND LATER ROUND GROWTH

THE US HAS EXPERIENCED THE

BOOM…

18 March 2016 WIN In-House Counsel Day, Melbourne 4

Source: PitchBook 2015 Annual US Venture Industry Report and Upfront Ventures 2016 Review

SIGNIFICANT PICK UP IN AUSTRALIAN TECH AND VC

ACTIVITY…BUT THE SECTOR IS SMALL

FY2016 to see circa 2 x capital raising by Australian VC funds

compared to FY2015

Significant increase in tech IPOs on ASX

VC exits in FY2016 likely to be highest for many years

Tech M&A experienced significant growth in CY2015

Global - $422.5B compared to $224.1B

Asia Pac - $95.36B compared to $49.3B

AUSTRALIAN INVESTMENT IN TECH

HAS POSITIVE MOMENTUM…

18 March 2016 WIN In-House Counsel Day, Melbourne 5

Source: AVCAL Yearbook FY2015, Merger Market 2015 Report and DLA Piper analysis

CORPORATE AND MULTI-NATIONAL ACTIVITY IN TECH IS

STRONG IN AUSTRALIA

AUSTRALIAN INVESTMENT IN TECH

HAS POSITIVE MOMENTUM…

18 March 2016 WIN In-House Counsel Day, Melbourne 6

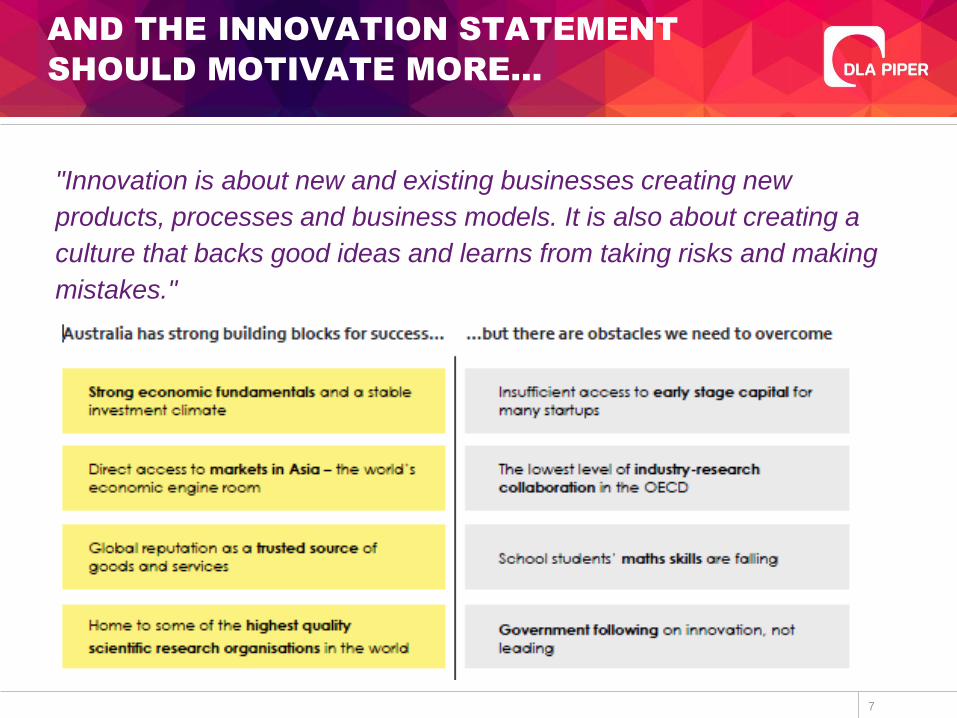

AND THE INNOVATION STATEMENT

SHOULD MOTIVATE MORE…

7

"Innovation is about new and existing businesses creating new

products, processes and business models. It is also about creating a

culture that backs good ideas and learns from taking risks and making

mistakes."

BUT THE TECH SECTOR IN

AUSTRALIA IS SMALL….

8

MAKING US RIPE FOR MISSING THE

BOAT….

9

AND INCREASING THE NEED FOR

SUPPORT…

10

OUR RECOMMENDATIONS….

11

Assist key persons to ask the right questions about tech

Collaborate

Understand venture capital

Understand corporate venture capital

Skill more legal members in IP procurement

Strengthen IT governance

Consider how the legal, finance, HR and strategic functions can

promote (rather than frustrate) innovation

Understand emerging innovation strategies

18 March 2016 WIN In-House Counsel Day, Melbourne

ASSIST KEY PEOPLE TO ASK THE

RIGHT QUESTIONS…

12

WHAT ARE THE OPPORTUNITIES AND THREATS FROM

TECHNOLOGY?

Who is responsible for technology?

How is technology creating emerging competitors and changing the

strategies of our direct competitors? Are we prepared for these

changes?

What is the lead time to develop emerging technology and how quickly

can we realistically adopt it?

How can technology equip us to enter new markets?

How should technology and innovation influence our HR, legal and

finance function?

What are our key IT risks to our day to day operations and are we

comfortable with them?

How are new technologies increasing customer expectations?

18 March 2016 WIN In-House Counsel Day, Melbourne

BUILD RELATIONSHIPS AND

STRATEGIES TO COLLABORATE….

13 18 March 2016 WIN In-House Counsel Day, Melbourne

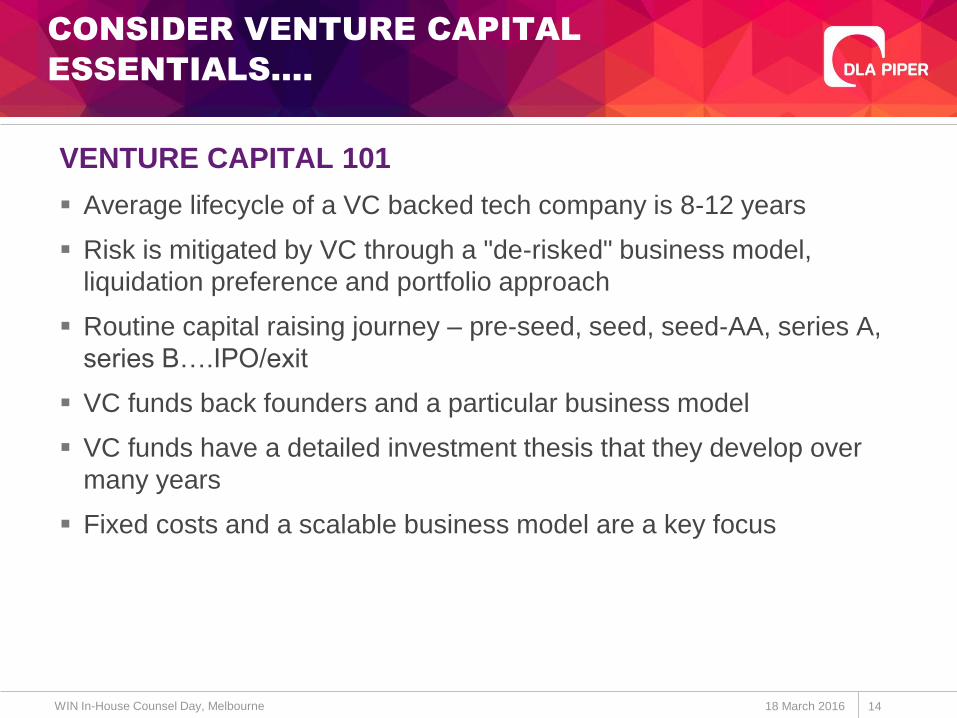

CONSIDER VENTURE CAPITAL

ESSENTIALS….

14

VENTURE CAPITAL 101

Average lifecycle of a VC backed tech company is 8-12 years

Risk is mitigated by VC through a "de-risked" business model,

liquidation preference and portfolio approach

Routine capital raising journey – pre-seed, seed, seed-AA, series A,

series B….IPO/exit

VC funds back founders and a particular business model

VC funds have a detailed investment thesis that they develop over

many years

Fixed costs and a scalable business model are a key focus

18 March 2016 WIN In-House Counsel Day, Melbourne

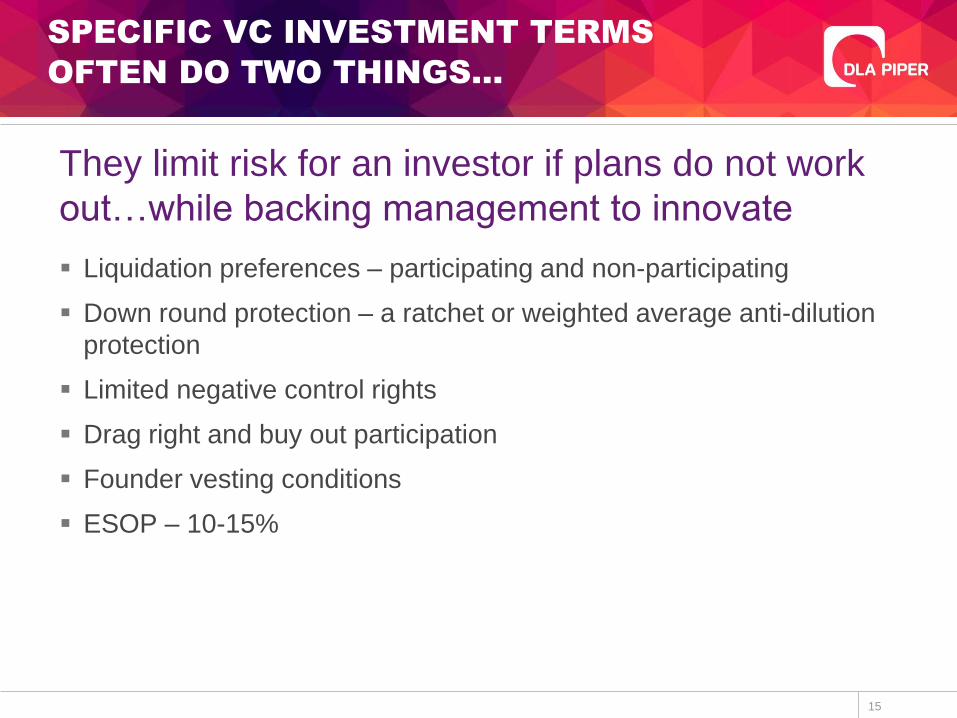

SPECIFIC VC INVESTMENT TERMS

OFTEN DO TWO THINGS…

They limit risk for an investor if plans do not work

out…while backing management to innovate

Liquidation preferences – participating and non-participating

Down round protection – a ratchet or weighted average anti-dilution

protection

Limited negative control rights

Drag right and buy out participation

Founder vesting conditions

ESOP – 10-15%

15

16

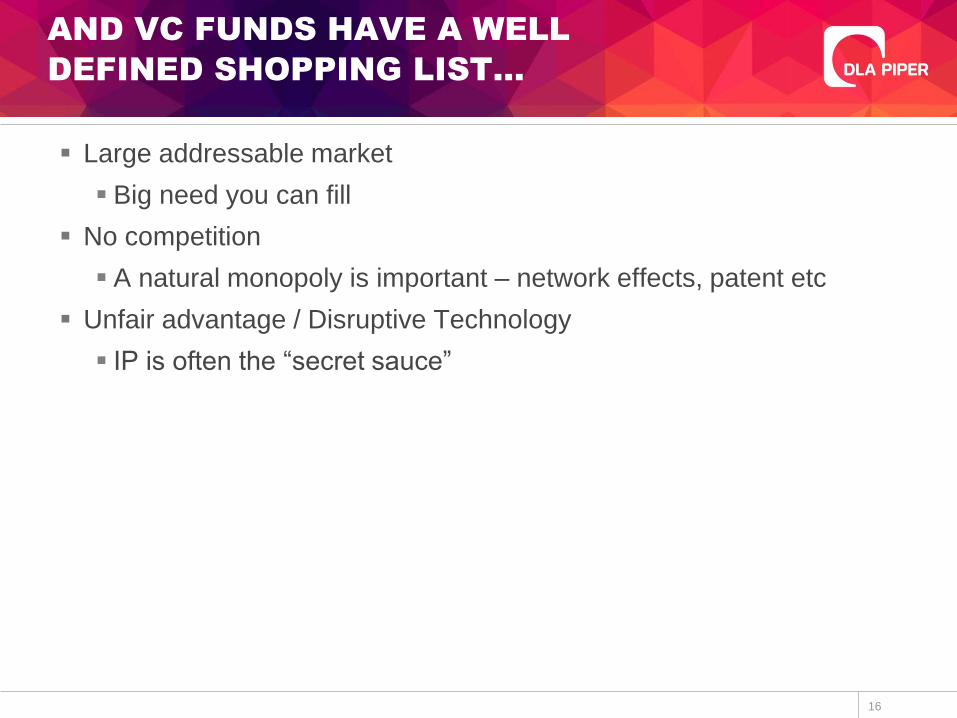

AND VC FUNDS HAVE A WELL

DEFINED SHOPPING LIST…

Large addressable market

Big need you can fill

No competition

A natural monopoly is important – network effects, patent etc

Unfair advantage / Disruptive Technology

IP is often the “secret sauce”

17

AND VC FUNDS HAVE A WELL

DEFINED SHOPPING LIST…

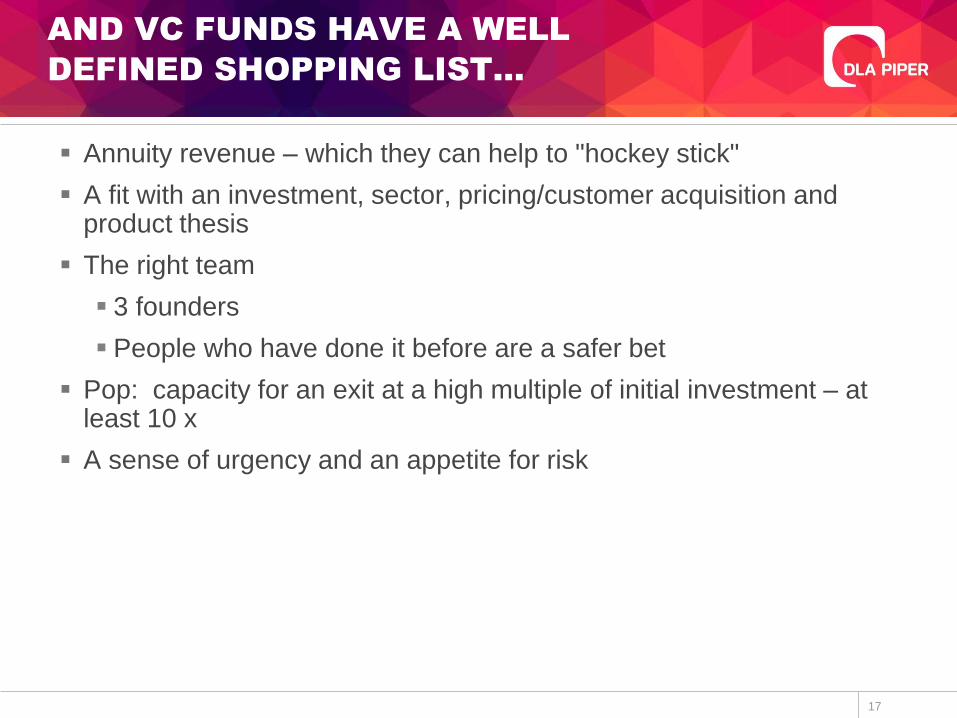

Annuity revenue – which they can help to "hockey stick"

A fit with an investment, sector, pricing/customer acquisition and product thesis

The right team

3 founders

People who have done it before are a safer bet

Pop: capacity for an exit at a high multiple of initial investment – at least 10 x

A sense of urgency and an appetite for risk

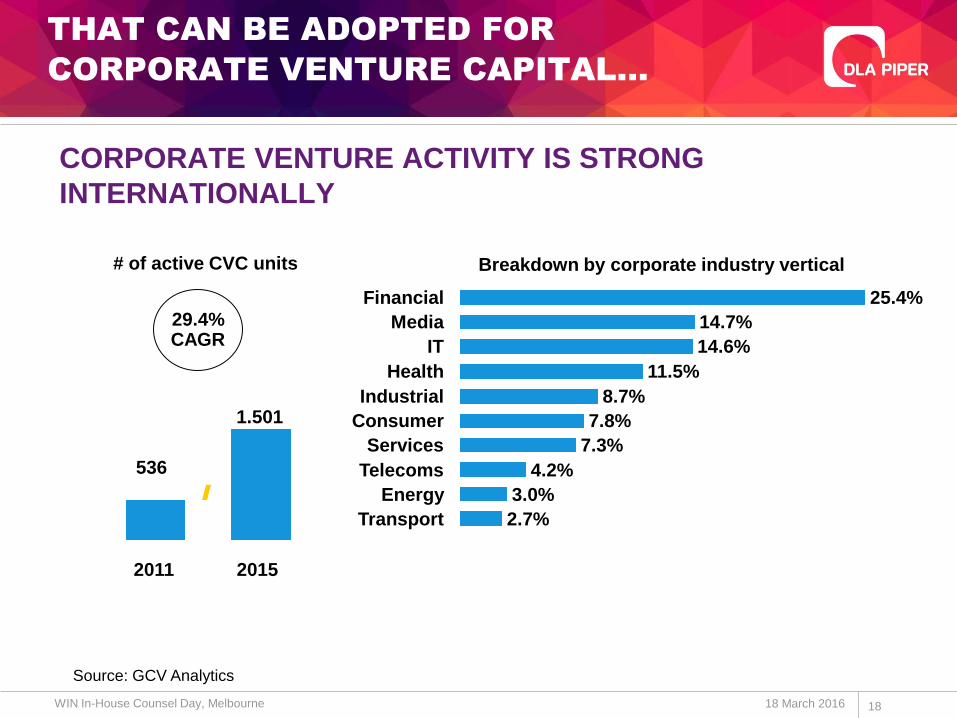

CORPORATE VENTURE ACTIVITY IS STRONG

INTERNATIONALLY

THAT CAN BE ADOPTED FOR

CORPORATE VENTURE CAPITAL…

18 March 2016 WIN In-House Counsel Day, Melbourne 18

1.501

2015

29.4% CAGR

2011

Industrial

7.8% Consumer

7.3%

IT 14.6%

25.4% Financial

14.7% Media

Services

4.2%

8.7%

11.5% Health

Telecoms

Breakdown by corporate industry vertical

Transport

Energy 3.0%

2.7%

# of active CVC units

536

Source: GCV Analytics

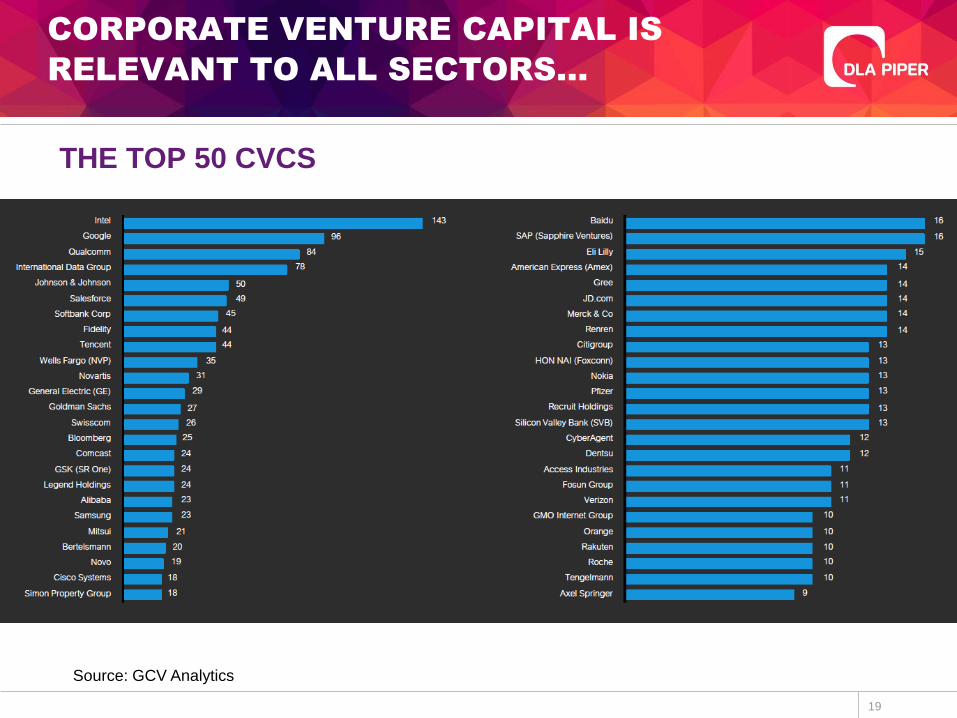

CORPORATE VENTURE CAPITAL IS

RELEVANT TO ALL SECTORS…

19

Source: GCV Analytics

THE TOP 50 CVCS

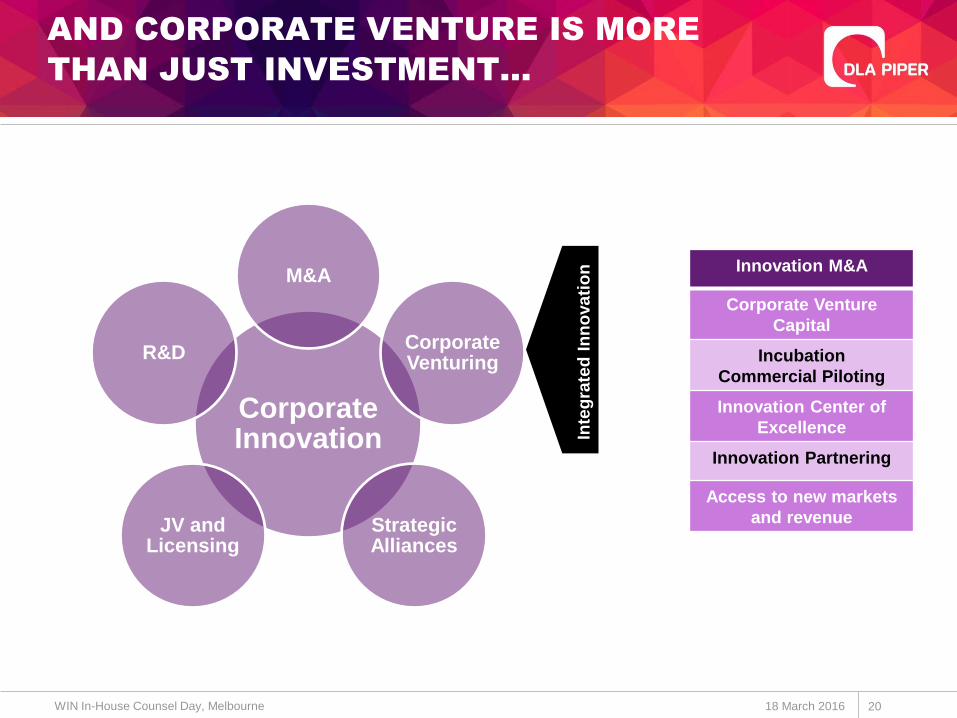

AND CORPORATE VENTURE IS MORE

THAN JUST INVESTMENT…

20 18 March 2016 WIN In-House Counsel Day, Melbourne

Innovation M&A

Corporate Venture

Capital

Incubation

Commercial Piloting

Innovation Center of

Excellence

Innovation Partnering

Access to new markets

and revenue

Corporate Innovation

M&A

Corporate Venturing

Strategic Alliances

JV and Licensing

R&D

Inte

gra

ted

In

no

va

tio

n

AND INVOLVES EMERGING

INNOVATION STRATEGIES….

21

Captive startups

A "build and solicit" strategy

Startups controlled by a corporate to achieve innovation in a silo

Often designed to pursue a new strategy, take opportunity of new

technologies or to benefit from a competitive gap

Repeat entrepreneurs are usually important and they require

equity

Fast follows

Innovation M&A

Acqui-Hires

Proprietary IP acquisition, SaaS and licensing

Joint ventures

18 March 2016 WIN In-House Counsel Day, Melbourne

EMERGING INNOVATION

STRATEGIES….

22

Emerging IP procurement practices

SaaS, network effects and fintech

Australia continues to be a high priority market for US tech multi-

nationals, creating great partnership opportunities

OnDeck Capital, HomeAway, Pandora, Uber and WeWork all

selected Australia as a key priority recently

Size of market is appealing for sandbox or beach head

strategies

18 March 2016 WIN In-House Counsel Day, Melbourne

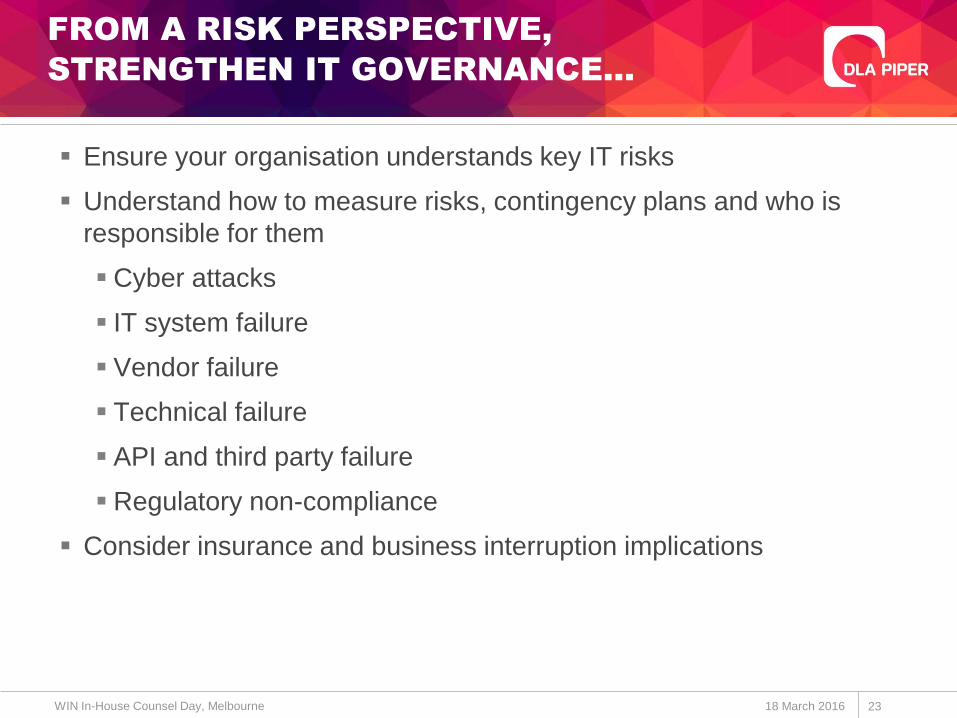

FROM A RISK PERSPECTIVE,

STRENGTHEN IT GOVERNANCE…

23

Ensure your organisation understands key IT risks

Understand how to measure risks, contingency plans and who is

responsible for them

Cyber attacks

IT system failure

Vendor failure

Technical failure

API and third party failure

Regulatory non-compliance

Consider insurance and business interruption implications

18 March 2016 WIN In-House Counsel Day, Melbourne

AND ASSIST TO PROMOTE

INNOVATION….

24

Ask how can the legal function better promote innovation?

Re-consider your approach to regulatory compliance with innovation

in mind

Many fast growth tech companies use business models that

require a re-assessment of the regulatory regime – i.e. peer to

peer lending and many other fintech models

Emerging technologies require creative legal thinking

Internet of things, bitcoin and blockchain, driverless and connected

cars and artificial intelligence all have regulatory hurdles to be

overcome

18 March 2016 WIN In-House Counsel Day, Melbourne

AND ASSIST TO PROMOTE

INNOVATION….

25

Understand what is legal best practice for emerging technology

Fintech – legal teams needs to approve new ways of delivering

financial services

Block chain – requires a willingness to share information in the

public arena

Network effects – legal teams need to assist to foster natural

monopolies built by network effects

SaaS – customary contracting terms to promote annuity revenue

Data marketplace and analytic models – sharing of de-identified

information

Internet of things, artificial intelligence and robotics – require new

terms for IP procurement and contracting

18 March 2016 WIN In-House Counsel Day, Melbourne

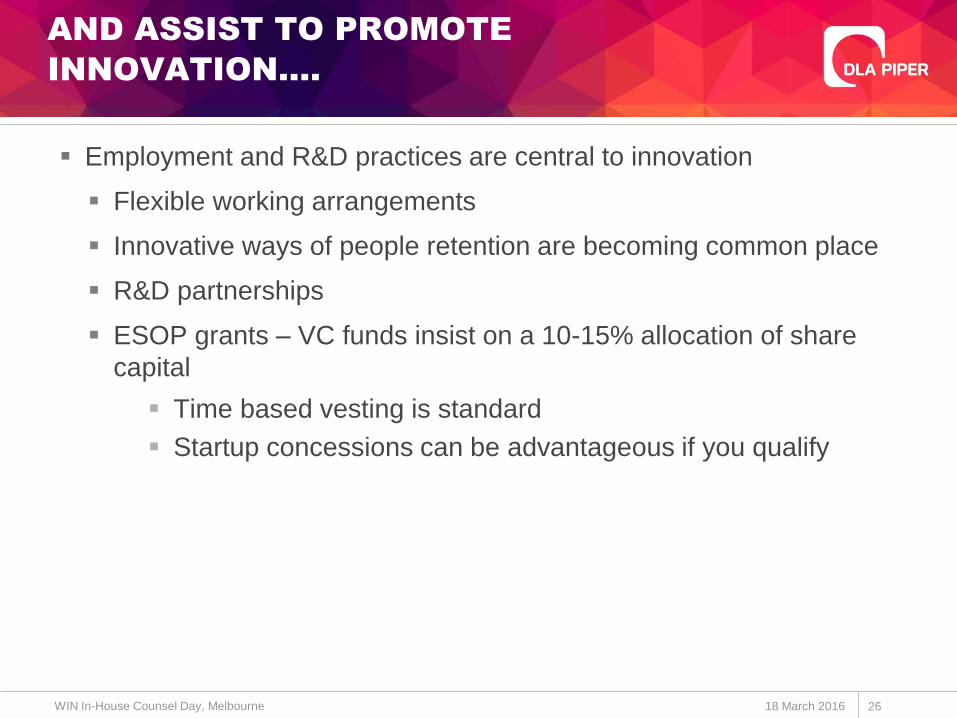

AND ASSIST TO PROMOTE

INNOVATION….

26

Employment and R&D practices are central to innovation

Flexible working arrangements

Innovative ways of people retention are becoming common place

R&D partnerships

ESOP grants – VC funds insist on a 10-15% allocation of share

capital

Time based vesting is standard

Startup concessions can be advantageous if you qualify

18 March 2016 WIN In-House Counsel Day, Melbourne

APPENDIX

27

18 March 2016 WIN In-House Counsel Day, Melbourne

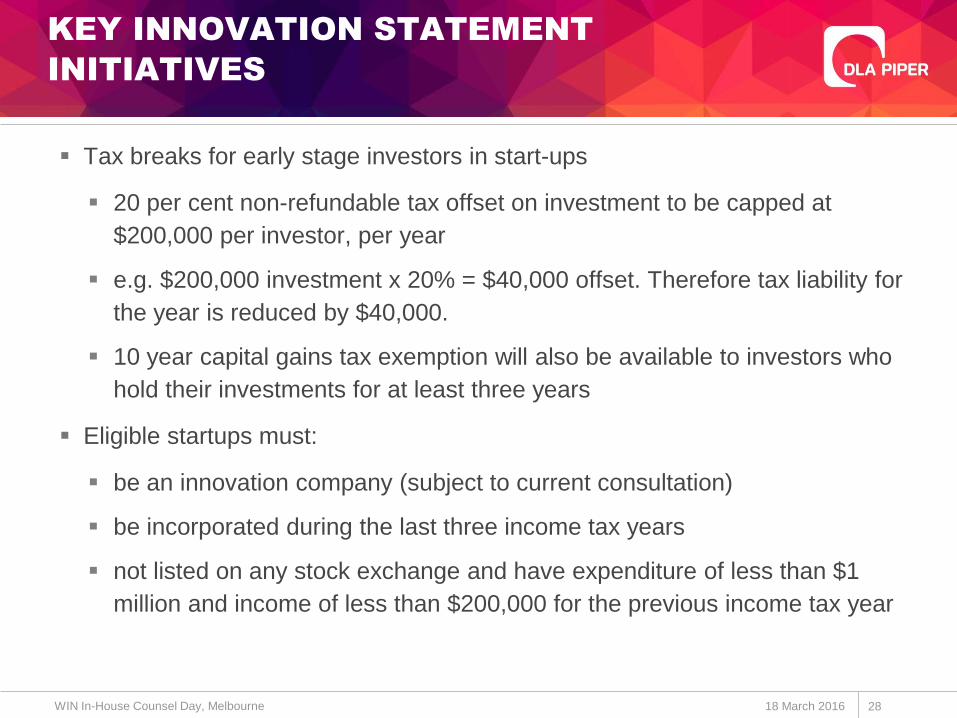

KEY INNOVATION STATEMENT

INITIATIVES

28

Tax breaks for early stage investors in start-ups

20 per cent non-refundable tax offset on investment to be capped at

$200,000 per investor, per year

e.g. $200,000 investment x 20% = $40,000 offset. Therefore tax liability for

the year is reduced by $40,000.

10 year capital gains tax exemption will also be available to investors who

hold their investments for at least three years

Eligible startups must:

be an innovation company (subject to current consultation)

be incorporated during the last three income tax years

not listed on any stock exchange and have expenditure of less than $1

million and income of less than $200,000 for the previous income tax year

18 March 2016 WIN In-House Counsel Day, Melbourne

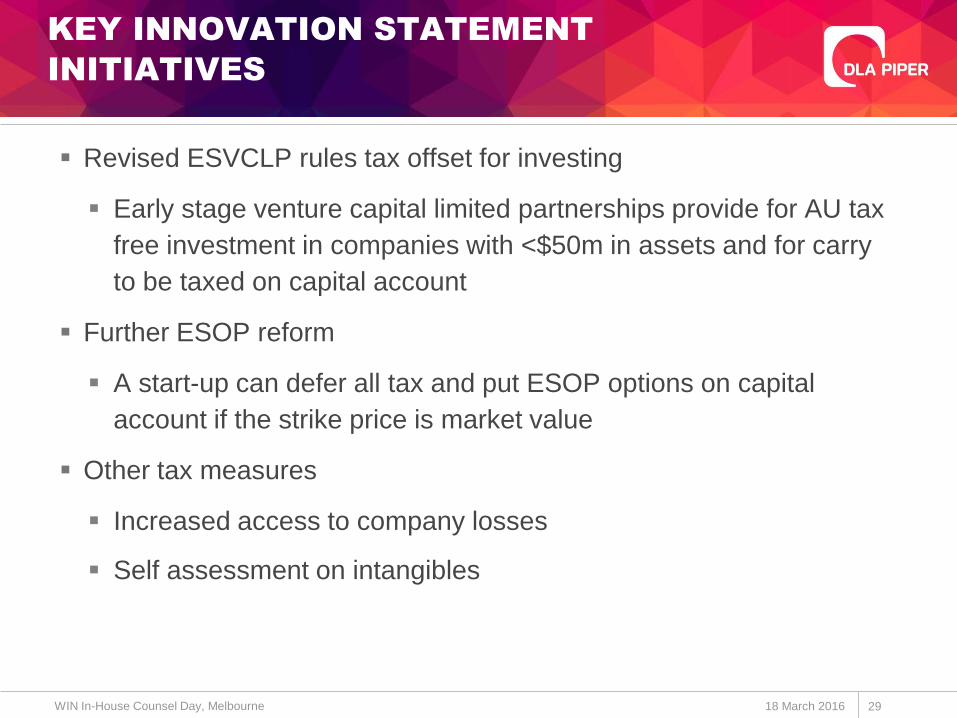

KEY INNOVATION STATEMENT

INITIATIVES

29

Revised ESVCLP rules tax offset for investing

Early stage venture capital limited partnerships provide for AU tax

free investment in companies with <$50m in assets and for carry

to be taxed on capital account

Further ESOP reform

A start-up can defer all tax and put ESOP options on capital

account if the strike price is market value

Other tax measures

Increased access to company losses

Self assessment on intangibles

18 March 2016 WIN In-House Counsel Day, Melbourne

CROWD FUNDING REFORM

30

Crowd funding to be legislated for Australian public companies with a

turnover and gross assets of less than $5 million

Eligible companies can raise up to $5 million

Individuals can contribute up to $10,000 per company per year

through crowd funding

Legislation awaiting royal assent and regulations pending

18 March 2016 WIN In-House Counsel Day, Melbourne

DLA PIPER RESOURCES -

CYBERSECURITY

DLA PIPER RESOURCES –

EMERGING TECH

Leading expertise Internet of Things

Data Centres

Cyber Security

Patent Wars

Big Data

IT Litigation

Emerging tech resources IT Contract Health check

Global Mobility

Technology Start-up Pack

IP Rights in Data

33

DLA PIPER RESOURCES –

SUPPORTING STARTUPS

An Introduction to DLA Piper's Emerging Growth and Venture Capital Practice

HOW CAN DLA PIPER ASSIST?

34

OUR DISRUPTION AND INNOVATION

GROUP

35

Bringing our Silicon Valley heritage to the world

A group dedicated to fast growth technologies and to the

transactions and legal support required to maximise returns

from them

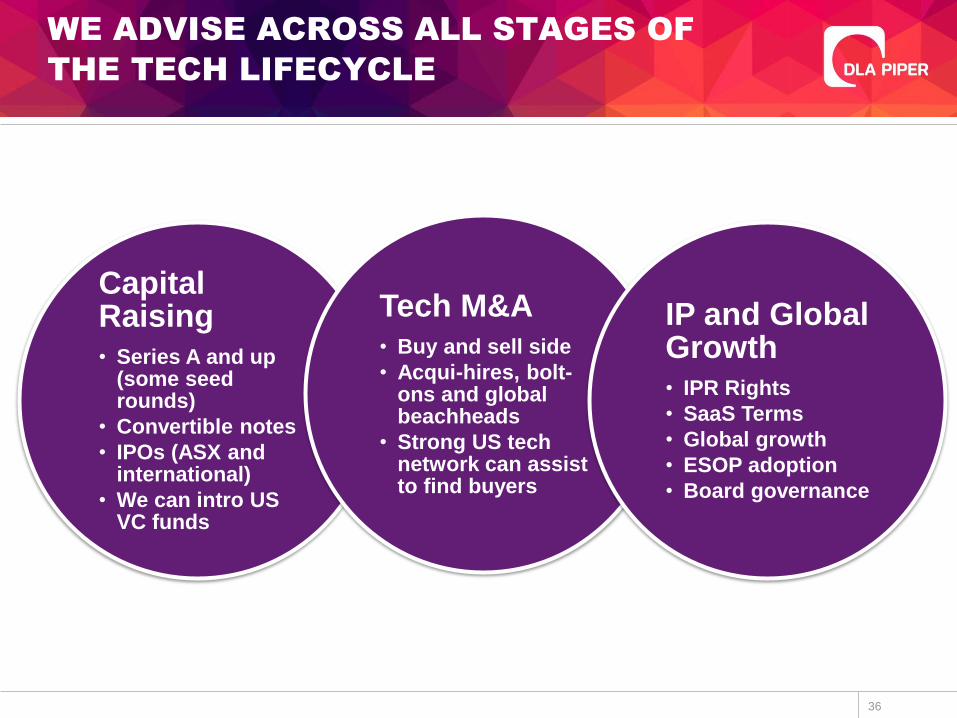

WE ADVISE ACROSS ALL STAGES OF

THE TECH LIFECYCLE

36

Capital Raising • Series A and up

(some seed rounds)

• Convertible notes

• IPOs (ASX and international)

• We can intro US VC funds

Tech M&A • Buy and sell side

• Acqui-hires, bolt-ons and global beachheads

• Strong US tech network can assist to find buyers

IP and Global Growth • IPR Rights

• SaaS Terms

• Global growth

• ESOP adoption

• Board governance

WE ADVISE INVESTORS AND

FUNDS ON ALL LEGAL ASPECTS

37

Fund set up • Fund

documentation

• All tax aspects

• Marketing

• Management terms

Investment process • Template

investment documents

• Streamlined due diligence

Exit Transactions • Dual Track

• US and ASX IPOs

• Further VC capital raising

REPRESENTATIVE VENTURE

FIRM CLIENTS

38 An Introduction to DLA Piper's Emerging Growth and Venture Capital Practice