Embed Size (px)

Citation preview

7/25/2019 Wisco Newsletter Q415

http://slidepdf.com/reader/full/wisco-newsletter-q415 1/4

Investment Advisors: Stephen Share [email protected] Greg Schroeder [email protected]

Fourth Quarter 2015

DEAR CLIENTS & FRIENDS;

Both the domestic and international equity markets performed better in the fourth quarter, rising 6% and 3%

respectively, recovering some of the losses experienced in the rst three quarters of the year. However, the

equity markets failed to return to positive territory for the full year, as the domestic equity market ended 2015

more or less at while international equities, in aggregate, nished the year down mid-single digits.

Fixed income markets were down modestly in the fourth quarter with the Barclays aggregate bond indexdeclining 1%. Although anticipated for some time, the Federal Reserve raised its short-term borrowing rate in

December (the rst hike in nearly 10-years), indicating its belief that the U.S. economy has nally stabilized

following the nancial crisis of 2008. Correspondingly, the 10-year U.S. treasury rate increased from 2.1% at

the beginning of the quarter to 2.3% at year end.

Commodity markets also fared poorly in the fourth quarter with the Dow Jones-UBS commodity index falling

13%. Agricultural and medal prices were both down across the board (i.e., corn and gold prices were down 7%

and 5%) while crude oil prices plummeted another 19% this period.

As a reminder, our policy is to rebalance client portfolios on a semi-annual basis (in January & July). This allows

us to realign the positioning of your portfolio with our current market expectations. To that end, we recently

completed our January 2016 realignment decisions and will be rebalancing portfolios over the course of thenext few weeks.

We would also like to remind you that this is often a good time of year to meet with us to discuss recent

portfolio performance as well as to review your current investment objectives, risk tolerance and nancial

goals for 2016. Please don’t hesitate to give us a call to schedule a meeting. In addition, this is also a good

time to make sure that all of your personal information is current in our database, such as your communication

preferences, IRA distribution dates, beneciaries, etc. Lastly, remember that the 2015 IRA contribution deadline

is right around the corner (tax day) so let us know if we can help.

At Wisco, we believe our approach of designing well-

diversied, low-cost investment portfolios is the

best way to produce favorable results over time.

We would like to thank you for providing us

with the opportunity to work with you as your

investment adviser. We appreciate your

business!

Sincerely,

The Wisco Team

7/25/2019 Wisco Newsletter Q415

http://slidepdf.com/reader/full/wisco-newsletter-q415 2/4

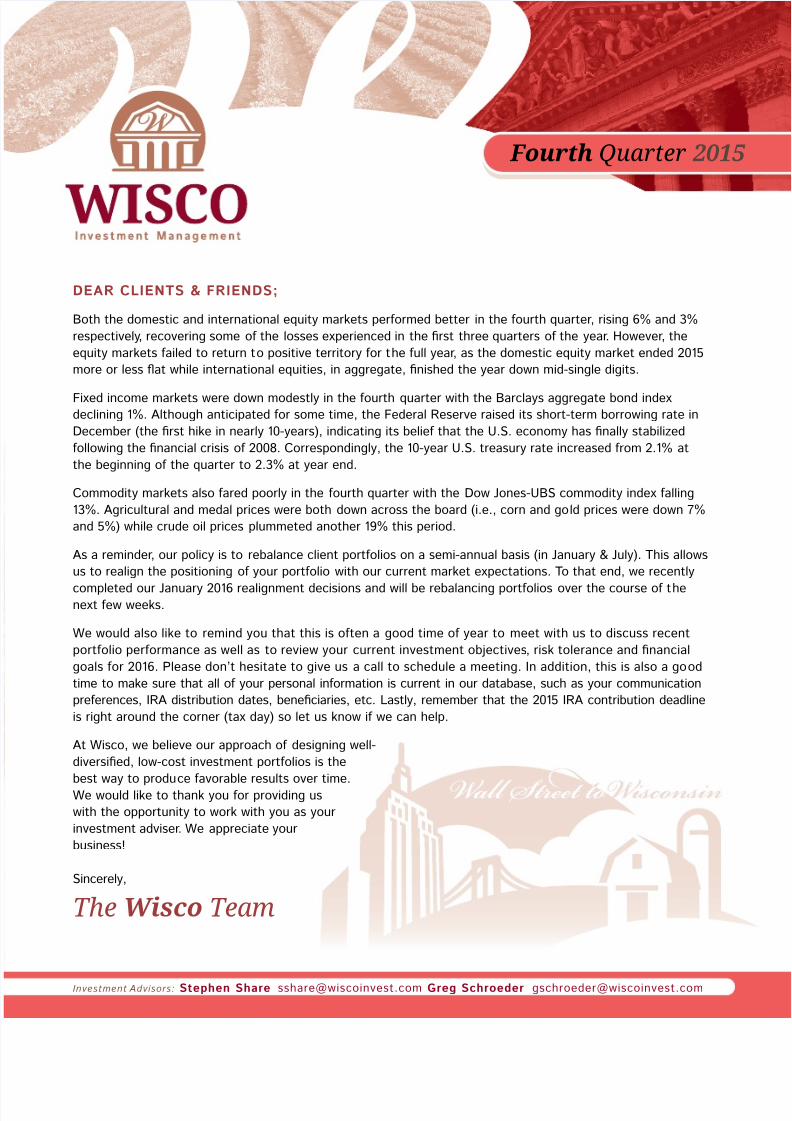

The domestic equity market increased 6% in

the quarter recovering much although not all of

3Q15’s loss. For the year, equities posted a modest

increase, with large cap stocks (+1%) outperforming

mid-cap stocks (0%) and small-cap stocks (-4%).

The S&P 500 closed the quarter at 2044, off the

all-time high of 2135 reached May 20th. S&P 500

3Q15 earnings were essentially at compared to

3Q14, and 3Q15 GDP posted a 2.0% gain. Once

again, a strong dollar and poor earnings from Energy

companies were a substantial headwind to corporate

earnings. Going forward, we feel 2016 corporate

earnings could grow in the mid-single digit range

while GDP is likely to grow in the low single digits.

In 2016, the headwinds from low Energy earnings

and a strong dollar will likely dissipate, while a

stronger economy and better consumer spending

could drive earnings higher. These earnings’

tailwinds could be partially offset by the Federal

Reserve modestly increasing short term interest

rates throughout 2016.

Despite investor concerns, we feel there arereasons to be optimistic about the domestic equity

market. The S&P 500 is trading at a P/E of 16x 2016

consensus operating earnings which seems like a

reasonable valuation especially if earnings can grow

in the mid-single digits in 2016. Therefore, we remain

constructive on the domestic stock market and feel

positive returns are again possible in 2016. With

that in mind, Wisco continues to have signicant

domestic equity exposures in all our client portfolios.

Fourth Quarter 2015 Market Review

Wisco Investment Management

Wisco model portfolios are constructed using ve different asset classes; Domestic Equity, International Equity,

Domestic Fixed Income, Alternative Investments and Cash. Our current model portfolio asset class allocationsare as follows:

Fourth Quarter 2015

WISCO MODEL PORTFOLIOS

Conservative Balanced Balanced Growth Growth Aggressive

Domestic Equity 29% 38% 43% 50% 65%

International Equity 7% 12% 19% 24% 29%

Domestic Fixed Income 50% 39% 29% 18% 0%

Alternative Investments 5% 5% 5% 5% 5%

Money Market 8% 6% 4% 2% 1%

Total 100% 100% 100% 100% 100%

Target Volatility* 6% 8% 10% 12% 14%

*Target Volatility is our estimate for the annual standard deviation of portfolio returns.

Source: Wisco Investment Management LLC

Source: Dow Jones U.S. Broad Stock Market Index and Wisco.

DOMESTIC EQUITY

35%

30%

25%

20%

15%

10%

5%

0%

-5%

-10% 4 Q1 5

3 Q1 5

2 Q1 5

1 Q1

5

4 Q1 4

2 0 1

5

2 0 1

4

2 0 1

3

2 0 1

2

2 0 1

1

Quarterly Returns13%

33%

0%1%

16%

5%

-7%

6%

2%0%

7/25/2019 Wisco Newsletter Q415

http://slidepdf.com/reader/full/wisco-newsletter-q415 3/4

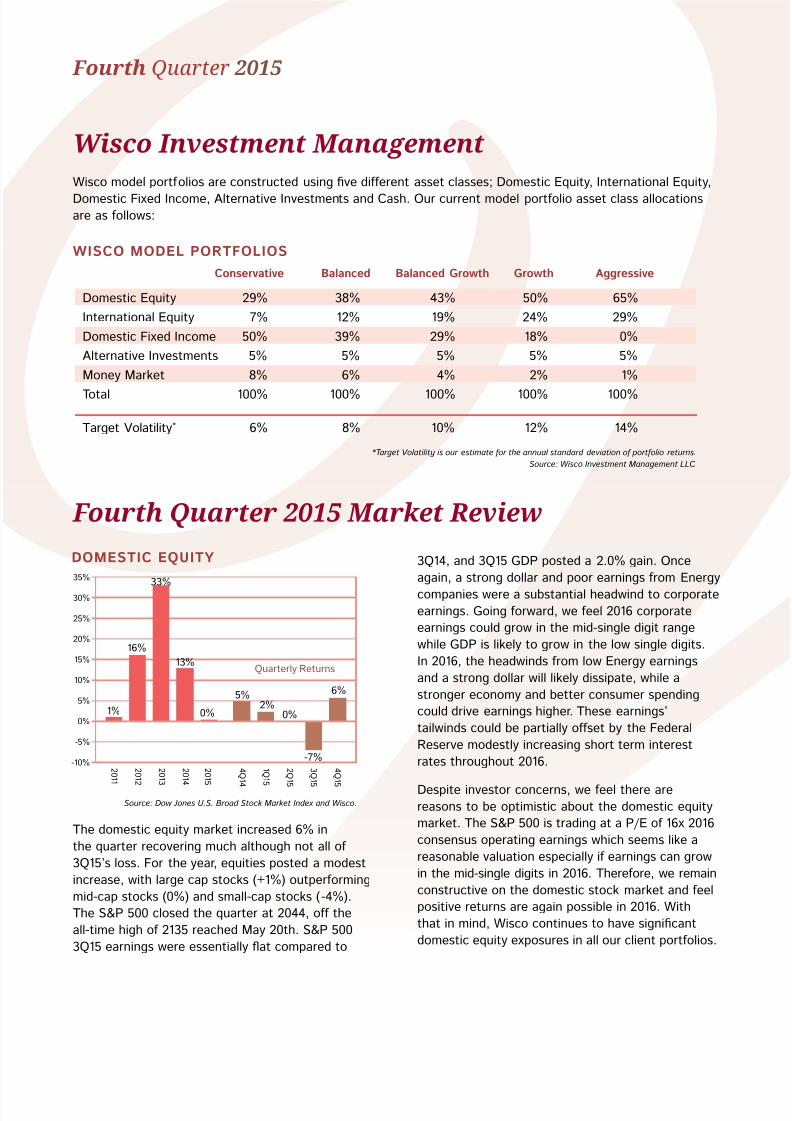

International equity also recovered in 4Q15

increasing 3%. For the year, international equity

declined 6%, with the developed market (-3%)

performing much better than emerging markets

(-16%). In Europe, the STOXX 50 increased 2%

in 4Q15. The Euro area GDP continues to post

modest yet positive results with GDP up 1.6% in

3Q15. Germany (+8%), Belgium (+8%) and Hungary

(+10%) were among the strongest performers in

4Q15, while Poland (-8%) lagged. In Asia, the Nikkei

225 increased 9% and the Shanghai composite

(+13%) recovered from a tough 3Q15. The FTSE

Emerging Market Index was down 1% in 4Q15 anddeclined 16% for the year.

2015 marked the six consecutive year in which

domestic equities outperformed international

equities. This has resulted in international stocks

trading at a signicant discount to domestic stocks.

Turning to fundamentals, Wisco feels the ECB’s

quantitative easing program and a strong U.S. dollar

could accelerate growth in the developed nations,

while low commodity prices could hinder growth

in emerging nations. Therefore, we are increasing

our exposure to International Equities focusing on

developed markets and avoiding emerging markets.

Fixed Income posted a modest decline in 4Q15,

with Barclays Capital U.S. Aggregate Bond

Index decreasing less than 1%. For 2015, the

Aggregate Bond Index was essentially at, yet still

outperformed TIPS (-2%), Investment Grade Bonds

(-1%) and High Yield Bonds (-3%). The 10-year

treasury yield started the quarter at 2.06% and

ended 4Q15 at 2.27%. This increase corresponded

with the Federal Reserve’s decision to increase

short term rates. For the year, the 10-year treasury

yield traded in a relatively narrow range opening

2015 at 2.17%, bottoming at 1.65% on January 30th,

and peaking at 2.49% on June 10th.

The Federal Reserve nally started its tightening

cycle in December and forecasted an additional

1.0% of rate increases in 2016. Wisco feels the Fed

may not be as aggressive as this forecast suggests

because ination is still low with few signs of

accelerating and dollar strength could slow growth.

With this backdrop, we think Fixed Income could

return low-to-mid single digits in 2016 with limited

downside. Therefore, we continue to hold Fixed

Income in all but our most aggressive portfolios and

prefer government securities and investment grade

corporate bonds to high yield bonds.

DOMESTIC FIXED INCOMEINTERNATIONAL EQUITY20%

15%

10%

5%

0%

-5%

-10%

-15%

-20% 4 Q1 5

3 Q1 5

2 Q1 5

1 Q1 5

4 Q1 4

2 0 1 5

2 0 1 4

2 0 1 3

2 0 1 2

2 0 1 1

Quarterly Returns

-3%

-6%

17%14%

0%4%

-12%-14%

-3%

Source: MSCI ACWI ex USA and Wisco

3%

10%

8%

6%

4%

2%

0%

-2%

-4% 4 Q1 5

3 Q1 5

2 Q1 5

1 Q1 5

4 Q1 4

2 0 1 5

2 0 1 4

2 0 1 3

2 0 1 2

2 0 1 1

Source: Barclays Capital U.S. Aggregate Bond Index and Wisco.

2%

Quarterly Returns

6%

8%

3%

-2%

-1%

-2%

1%

0%

1%

7/25/2019 Wisco Newsletter Q415

http://slidepdf.com/reader/full/wisco-newsletter-q415 4/4

Wisco Investment Management LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend

to make an offer or solicitation for the sale or purchase of any specic securities product, service, or investment strategy. Investments involve

risk and unless otherwise stated, are not guaranteed. Be sure to rst consult with a qualied nancial adviser, tax professional, or attorney before

implementing any strategy or recommendation discussed herein.

ALTERNATIVE INVESTMENTS

The Dow Jones-UBS Commodity Index declined 13%

in the quarter. In agriculture, Corn prices decreased7%1 and Soybean prices decreased 2%1, as the

strong dollar along with a soft overseas demand

hurt results. We think consistently low prices could

result in less acres planted this Spring in North

America and Russia. Gold and silver prices both

declined 5%2,3 in the quarter, as the strong dollar

continues to pressure commodity prices. Real

Estate Investment Trusts (REIT) increased 8%4 in

the quarter as investors looked to purchase income

producing assets. Finally, Crude Oil prices declined

19%5 in 4Q15, as domestic producers weren’t able

to cut production fast enough to avoid inventories

reaching near all-time high levels for December. For

the year, oil prices declined 32%.

Wisco continues to include Alternative Investments

in our model portfolios. For lower risk portfolios, we

are holding gold and prefer agricultural commodities

in more aggressive portfolios. Finally, we arestarting to invest in a crude oil fund for our most

aggressive client portfolios.

MONEY MARKET

Wisco keeps a modest money market allocation in

all of our portfolios. The current yield of the Schwab

Money Market is 0.01%. Low Federal Funds rates

have held down short-term yields. If the Federal

Reserve continues to increase rates in 2016, the

yield for money markets may modestly increase.

Nevertheless, we think short-term interest rates will

remain low for an extended period of time.

1. Return calculation based on the near future contract as quoted in the Wall Street Journal.

2. Return calculation uses ETFS Physical Swiss Gold Shares (SGOL) as a proxy for gold.

3. Return calculation uses iShares Silver Trust ETF (SLV) as a proxy for silver.

4. Return calculation uses Schwab U.S. REIT ETF (SCHH) as a proxy for Real Estate Investment Trusts.

5. Return calculation uses Cushing, OK WTI spot price FOB as a proxy for oil.

402 Gammon Place, Suite 380 • Madison, WI 53719 • Office 608.442.5507 • Fax 608.237.2206