Embed Size (px)

Citation preview

WITS - IJW POWER REPORTING WORKSHOP

SEPTEMBER 2007

Centre For Investigative Journalism

Forensic Accounting LLP

HOW TO READ ACCOUNTS

• Profit or Loss?

• Asset or Liability?

• Cash flow in or out?

• What’s in the small print?

• Who’s in charge?

Introduction

Objectives

De-mystifying accounts•Provide a basic understanding of accounts

•Provide some pointers as to what you should look for and where you should look

Understand the motivation and pressure for earnings management

What’s your interest?

Why are you looking at the accounts of this particular company?

Where do you look?

•Company is important local employer or has won local contracts •Directors have political interest•Company doing well but not clear why•Something odd about the activities of the company or its directors•Complex web of companies •Is it safe to invest?

Motivation

Private Companies

• Depress ‘Earnings’

Why? – Delay taxes

Hide data from competitorsand customers

Public Companies

• Enhance ‘Earnings’

Why? -“THE NUMBER”Earnings per Share (EPS)

Impacts upon:

•performance bonuses

•stock options

•share price

Motivation – Public Companies

‘The Number’ is very important!

• Enron

• WorldCom

Failure to make ‘The Number’ can result in serious embarrassment and loss of reputation.

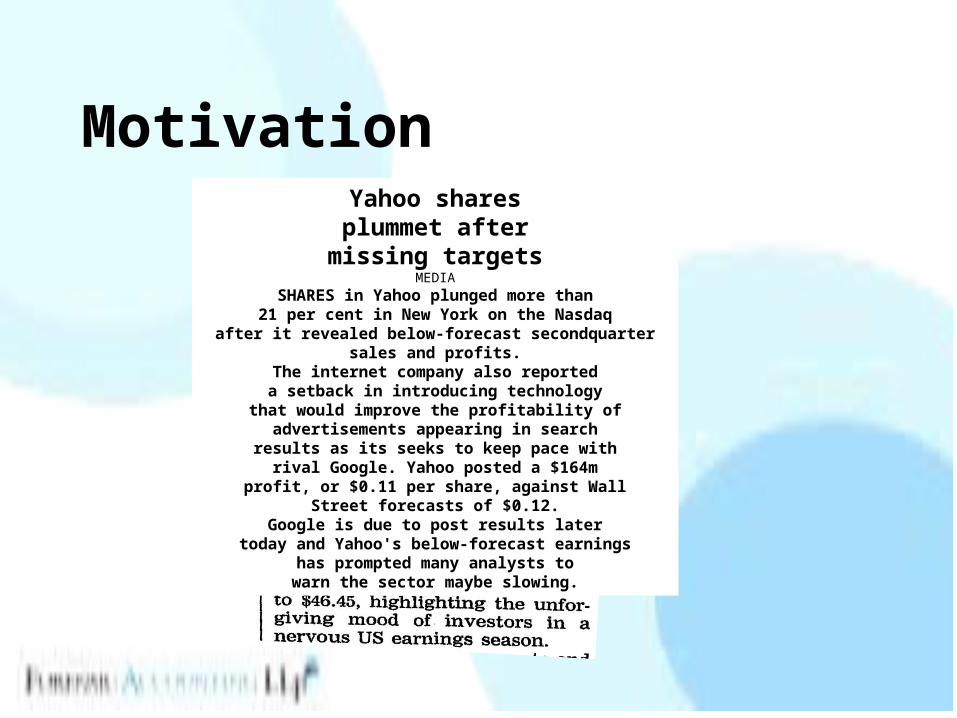

MotivationYahoo sharesplummet aftermissing targets

MEDIA

SHARES in Yahoo plunged more than21 per cent in New York on the Nasdaq

after it revealed below-forecast secondquartersales and profits.

The internet company also reporteda setback in introducing technology

that would improve the profitability ofadvertisements appearing in searchresults as its seeks to keep pace withrival Google. Yahoo posted a $164m

profit, or $0.11 per share, against WallStreet forecasts of $0.12.

Google is due to post results latertoday and Yahoo's below-forecast earnings

has prompted many analysts towarn the sector maybe slowing.

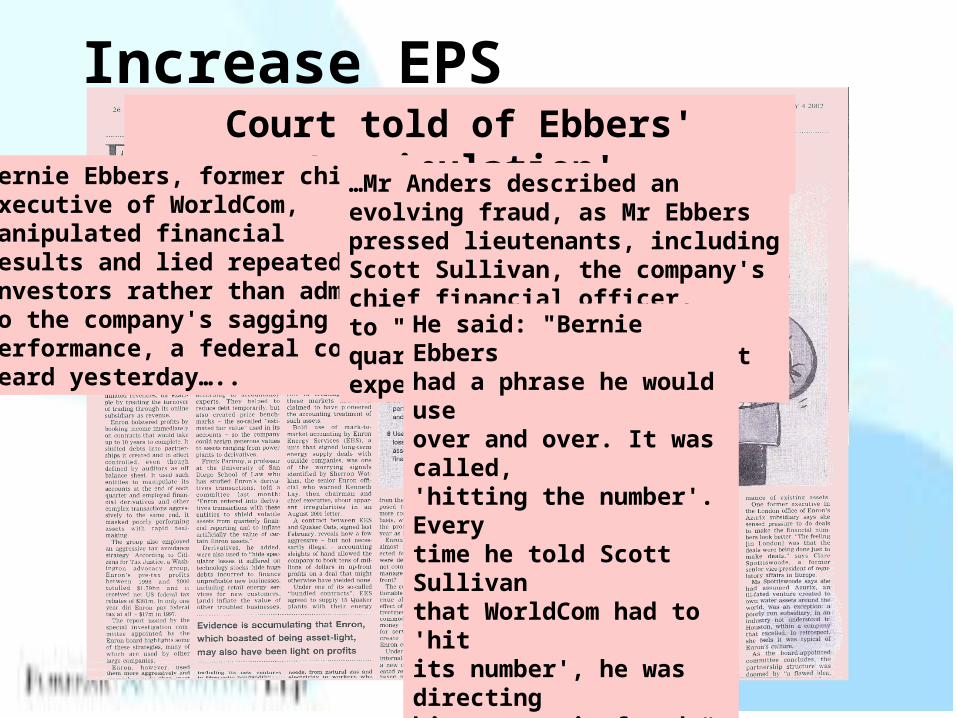

Increase EPSCourt told of Ebbers' 'manipulation'

Bernie Ebbers, former chiefexecutive of WorldCom,manipulated financialresults and lied repeatedly toinvestors rather than admitto the company's saggingperformance, a federal courtheard yesterday…..

…Mr Anders described anevolving fraud, as Mr Ebberspressed lieutenants, includingScott Sullivan, the company'schief financial officer,to "hit the numbers" eachquarter and meet Wall Streetexpectations.

He said: "Bernie Ebbershad a phrase he would useover and over. It was called,'hitting the number'. Everytime he told Scott Sullivanthat WorldCom had to 'hitits number', he was directinghim to commit fraud.“…

HOW TO READ ACCOUNTS

• PROFIT OR LOSS

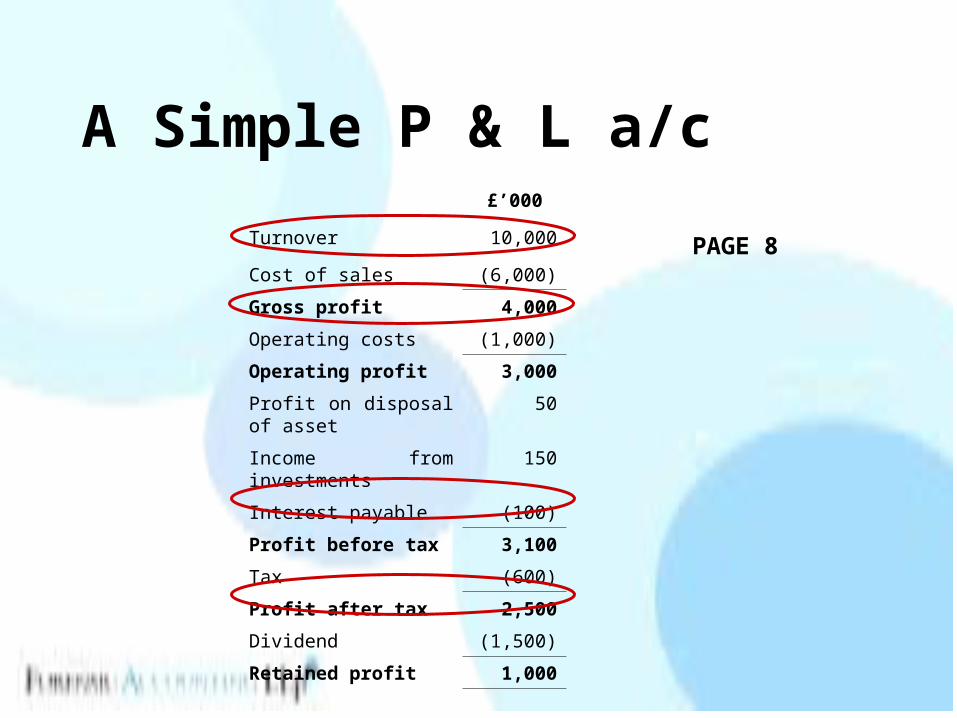

A Simple P & L a/c£’000

Turnover 10,000

Cost of sales (6,000)

Gross profit 4,000

Operating costs (1,000)

Operating profit 3,000

Profit on disposal of asset 50

Income from investments 150

Interest payable (100)

Profit before tax 3,100

Tax (600)

Profit after tax 2,500

Dividend (1,500)

Retained profit 1,000

PAGE 8

SASOL

• 2006 accounts

• Page 50

• Lots of lines but focus on main four

• Dividends given per share with listed companies. Need to check how much dividend cost - see Cash Flow statement or Note 45

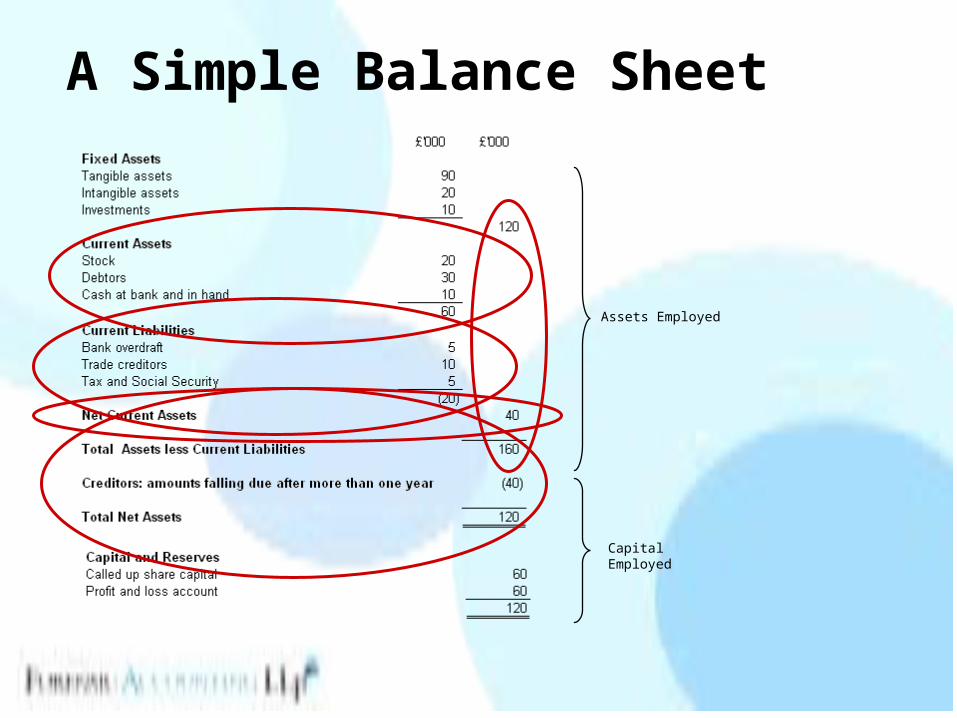

HOW TO READ ACCOUNTS

• TOO BIG TO FAIL

A Simple Balance Sheet

Assets Employed

Capital Employed

Vodacom Group

• 2007 accounts

• Page 92

• Compare current assets and liabilities

HOW TO READ ACCOUNTS

• NO CASH NO BUSINESS

Cash Flow Statement

• Profit does not equal Cash

• Profit is the vanity. Cash is sanity…

“Cash is King”

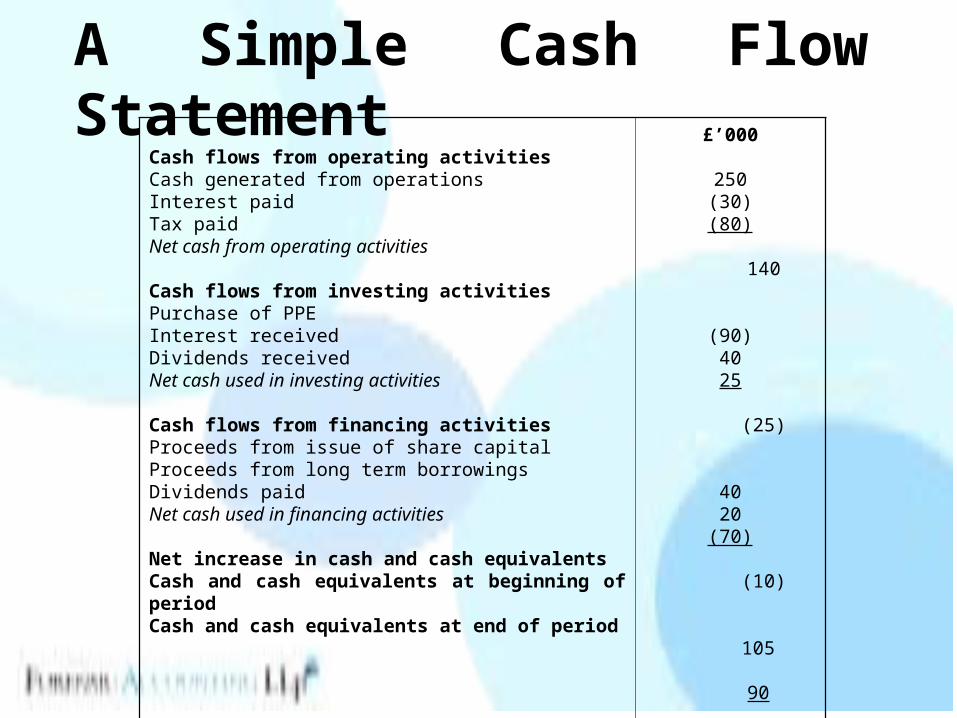

A Simple Cash Flow StatementCash flows from operating activitiesCash generated from operationsInterest paidTax paidNet cash from operating activities

Cash flows from investing activitiesPurchase of PPEInterest receivedDividends receivedNet cash used in investing activities

Cash flows from financing activitiesProceeds from issue of share capitalProceeds from long term borrowingsDividends paidNet cash used in financing activities

Net increase in cash and cash equivalentsCash and cash equivalents at beginning of periodCash and cash equivalents at end of period

£’000

250(30)(80)

140

(90)4025

(25)

4020

(70) (10)

105 90

195

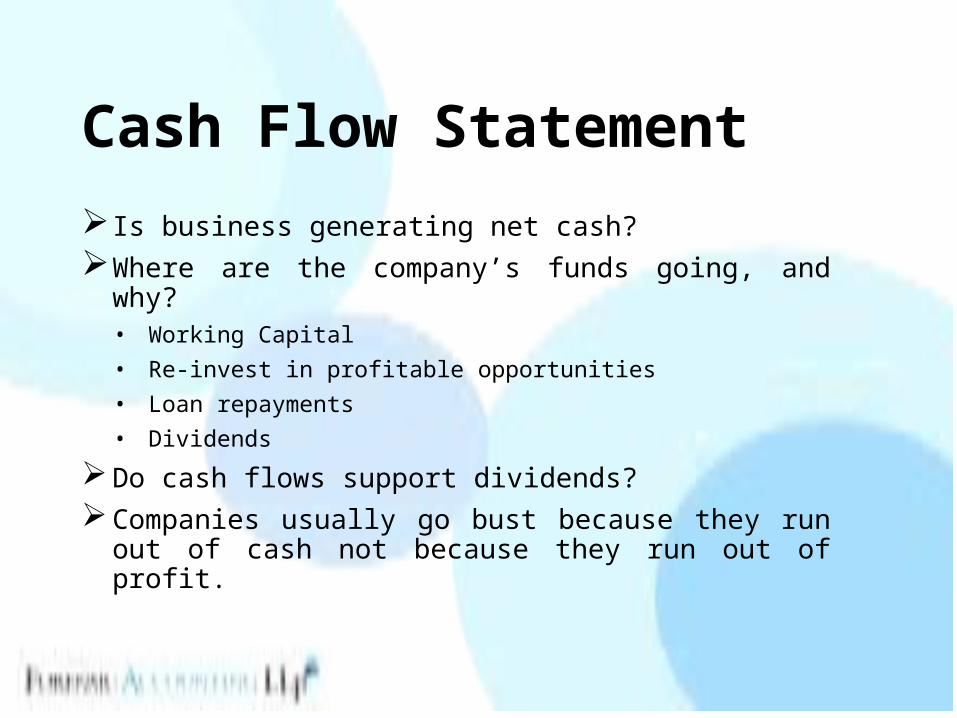

Cash Flow Statement

Is business generating net cash?

Where are the company’s funds going, and why?• Working Capital

• Re-invest in profitable opportunities

• Loan repayments

• Dividends

Do cash flows support dividends?

Companies usually go bust because they run out of cash not because they run out of profit.

Jubilee Platinum

• 2006 accounts

• Page 31

• Cash from share issues or loans - usual with new mining companies as no revenues

Growthpoint Properties

• 2006 accounts

• Page 39

• Less cash year on year

HOW TO READ ACCOUNTS

• THE SMALL PRINT

Notes to the Accounts

• The “small print” is always at the back of the accounts or prospectus so worth reading from the end forwards

• Gives clues as to what is hidden in the figures.

• No point in reading the figures without reading the small print.

Notes to the Accounts

• Directors remuneration

• Post balance sheet events

• Taxation

• Related Party Transactions

• Going Concern

• Exceptional items

• Ultimate ownership (UK only)

• Contingent liabilities

• The notes must disclose directors’ rewards:

– Basic salary/fees and possibly other benefits

– Performance related bonuses / share plans

– Share options

– Deferred Share Bonus Awards / other Deferred Share Awards

Remuneration

ABSA Group

• 2006 Accounts

• Remuneration report

• Pages 33-43

• The notes to the accounts must analyse the tax charge/credit :

– Income or other company tax

– Deferred taxation

– Prior year’s charge

• The note will also show whether the company is paying the full rate of tax or less because of tax breaks so perhaps not a good corporate citizen.

Taxation

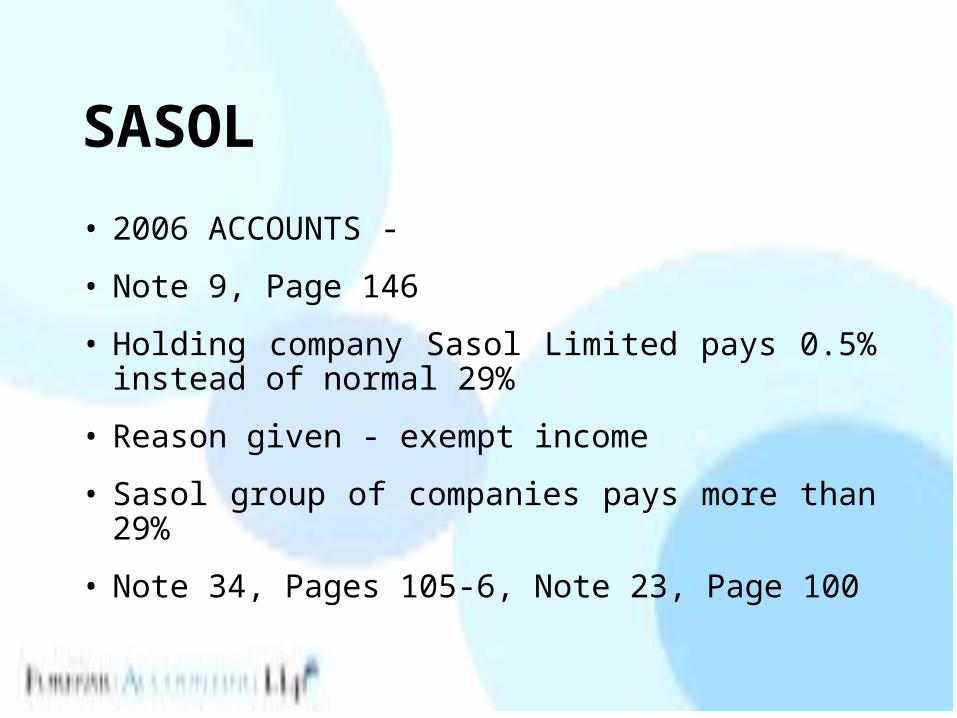

SASOL

• 2006 ACCOUNTS -

• Note 9, Page 146

• Holding company Sasol Limited pays 0.5% instead of normal 29%

• Reason given - exempt income

• Sasol group of companies pays more than 29%

• Note 34, Pages 105-6, Note 23, Page 100

The note will include:

• Events since the financial year end but before the accounts were signed - usually a gap of several months

• If material, the nature and potential financial impact.

Post Balance Sheet Events

Anglo American Corporation

• 2006 accounts

• Note 39, Page 124

• Usually found at the end of the notes but can also be in the Directors’ report at the beginning of the annual report

• The company’s financial position and results may be affected by material transactions involving related parties.

• Relationships between parents and subsidiaries must be disclosed.

• Disclosure of transactions between related parties such as directors or families:

– The nature of the relationship

– Information regarding the transactions

– Outstanding balances

Related Party Transactions

Cape Diamonds

• 2006 accounts

• Note 24, Pages 31-32

• Series of transactions between company and directors/shareholders

• Such deals always worth checking - are they at arms-length or is the company/shareholders losing out

Growthpoint Properties

• 2006 accounts

• Note 34, Page 68-9

• Series of deals with significant shareholder Investec which is also banker and business partner

• Who gains most?

• Financial statements are prepared on the basis that the entity will continue for the foreseeable future - if necessary with the backing of a director or shareholder.

• The company has no intention or need to liquidate the company

• The company has no intention or need to curtail materially the scale of its operations

• Management must look up to 12 months from the balance sheet date

Going Concern (1)

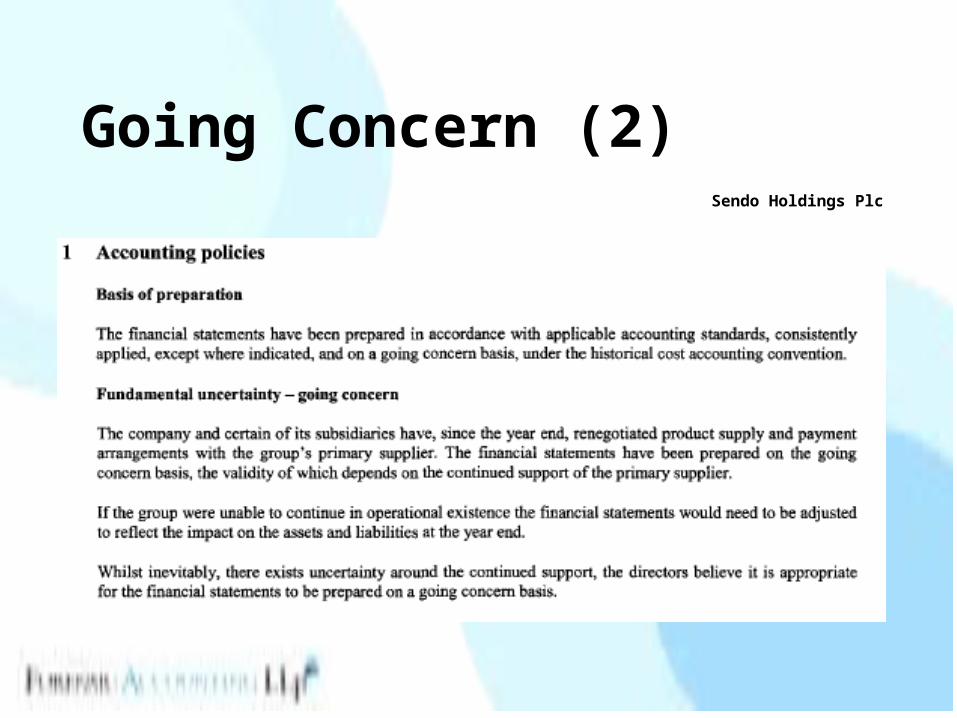

Going Concern (2)Sendo Holdings Plc

Exceptional Items• Material gains or losses which arise outside of

normal business activity and are therefore required to be disclosed separately. The note must give:

– A break down of each separate exceptional item, either individually or as an aggregate of items of a similar type.

– An adequate description of each exceptional item so it’s nature can be understood

De Beers

• 2006 accounts

• Page 7 - special items

• Explained on page 9

• Special or exceptional items should not happen again.

• Look closely at a company where exceptional items seem to happen every year

• A UK company must disclose its parent company and, if different, the ultimate controlling party.

• If neither the company’s parent nor the ultimate controlling party produces financial statements available for public use, the name of the next most senior parent that does so shall also be disclosed.

• Note that in some cases, the controlling party may not be the ultimate beneficiary

Ultimate Ownership (1)

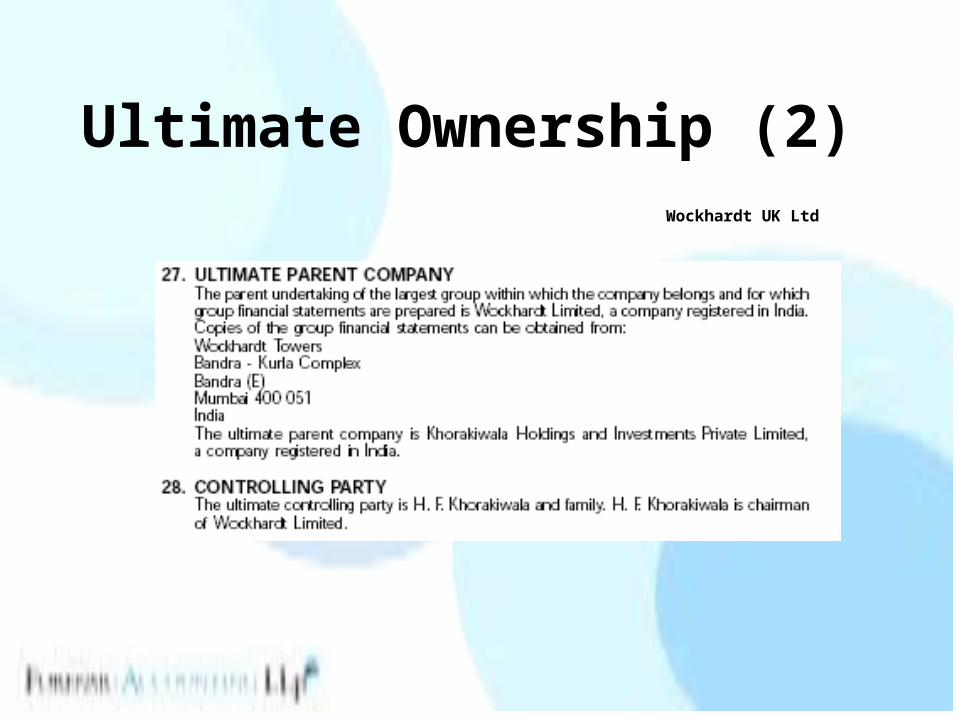

Ultimate Ownership (2)Wockhardt UK Ltd

Contingent Liabilities • A contingent liability is essentially:

– A possible or present obligation stemming from something that has happened in the past.

• A contingent liability is disclosed by way of a note to the accounts. This note should contain:

– A brief description of the nature of the liability

– Estimate of the financial impact

– An indication of the uncertainties involved

– Possibility of any reimbursement

SASOL

• 2006 Accounts

• Notes 49(3);49(4);49(5);49(6)

• Litigation, regulatory action and other bad stuff usually make up contingent liabilities.

• A company will often say it will win until it does not and has to make a big provision for the bill

Auditors’ Report (1) Clean or unqualified opinion

Qualified opinion

Explanation of qualification

Going concern qualification

The duty of the auditor is to report to members whether the financial statements of the company have been properly prepared in accordance with the Companies Act.

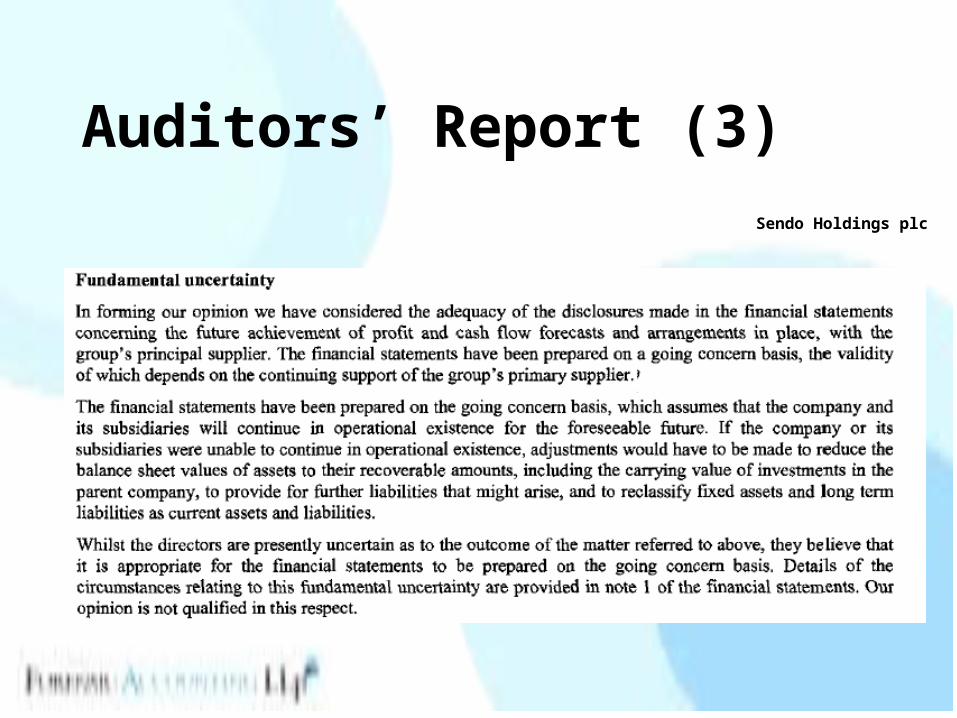

Auditors’ Report (3)

Sendo Holdings plc

Independent auditors?

• Anglo American

• Accounts 2006

• Note 4, Page 99

• Deloitte & Touche fees for audit twice fees for tax and consultancy

• Independence threatened if audit fees much less than fees from consultancy

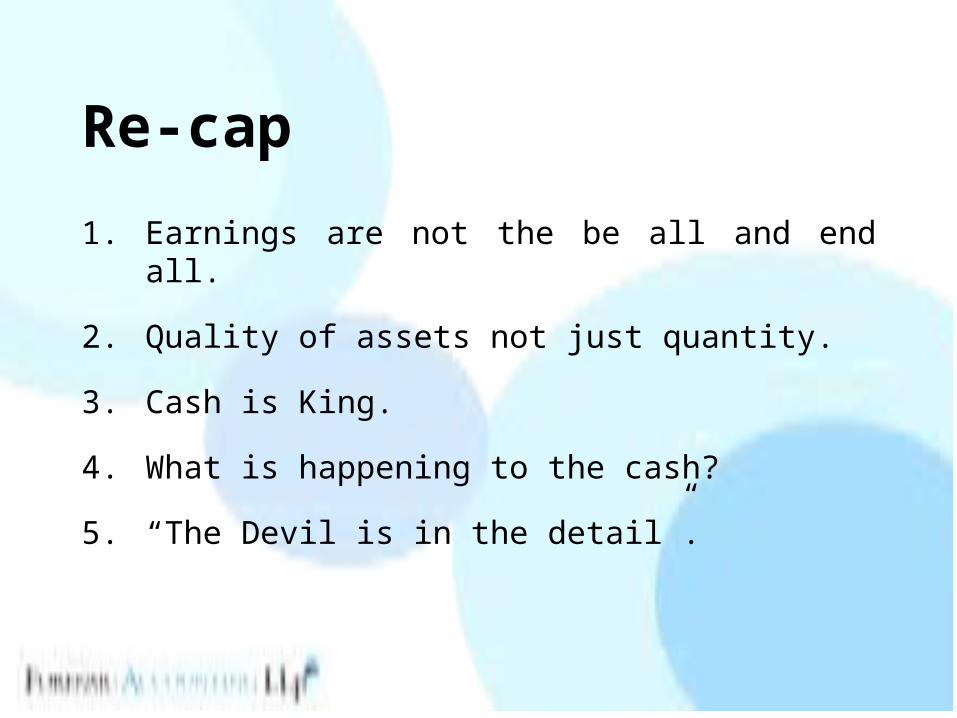

Re-cap

1. Earnings are not the be all and end all.

2. Quality of assets not just quantity.

3. Cash is King.

4. What is happening to the cash?

5. “The Devil is in the detail”.

HOW TO READ ACCOUNTS

• ANY THE WISER?

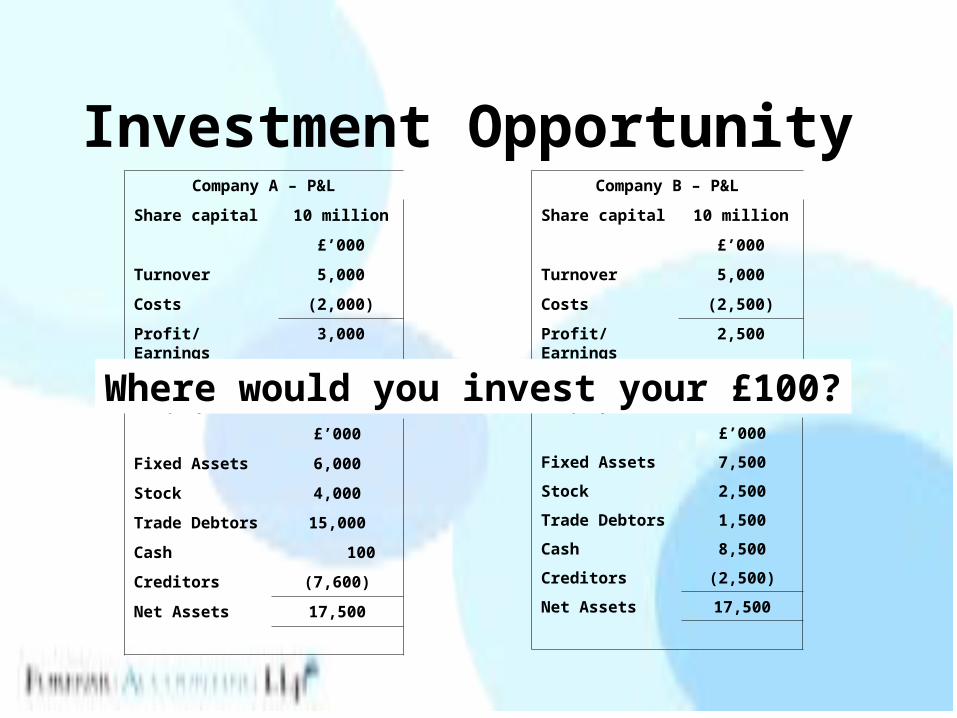

Investment OpportunityCompany A – P&L

Share capital 10 million

£’000

Turnover 5,000

Costs (2,000)

Profit/Earnings 3,000

EPS £0.30

Company B – P&L

Share capital 10 million

£’000

Turnover 5,000

Costs (2,500)

Profit/Earnings 2,500

EPS £0.25

Company A - Balance Sheet

£’000

Fixed Assets 6,000

Stock 4,000

Trade Debtors 15,000

Cash 100

Creditors (7,600)

Net Assets 17,500

Company B - Balance Sheet

£’000

Fixed Assets 7,500

Stock 2,500

Trade Debtors 1,500

Cash 8,500

Creditors (2,500)

Net Assets 17,500

Where would you invest your £100?

Who are the directors?

• Business background

• Don’t rely on the official version

• Check what happened before

Equator Exploration

• 2005 accounts

• Chief executive Wade Cherwayko

• Abacan Resources

• Promised much in Nigeria, delivered little

• Equator = Abacan 2

• Déjà vu all over again

Financial Check-up (1)Have the auditors expressed any concerns ?

Check the Auditors Report

How independent are they if they are paid more for non-audit work?

Check the Operating Profit Note

How much debt does the company have, and what is the nature of the debt?

Review the Balance Sheet and Long Term/Short Term Creditors Notes

Is the company generating cash? If so, what is it doing with the money?

Review the Cash Flow Statement

Financial Check-up (2)What is the management’s previous history?

Review Company Prospectus and public records

What is the level of directors’ remuneration?

Review Notes on Directors

Have there been any related party transaction?

Review Related Party Transactions Note

What has happened since the financial year ended?

Review the Post Balance Sheet Events Note

Centre For Investigative Journalism

2007

Forensic Accounting LLP