Embed Size (px)

Citation preview

1

OBJECTIVE OF THE STUDY

Primary objective:

To study and detailed analysis about the awareness of women insurance among peoples belongs to different class.

And the companies that provide women insurance like Life insurance corporation of India, HDFC’S smart women insurance policy, TATA AIG’S well assurance etc.

Secondary objective:

The main purpose and objective of this study is to analyze the need and importance of women insurance for women’s in India. And the companies providing women insurance taking it seriously or not. The level of customer satisfaction is proper or not.

Mainly the objectives are as follows:

To analyze the improvement of women’s satisfaction. To determine how insurance companies are providing services to them. To find out the expectations of women’s towards the insurance as well as

insurance companies. To find the improvement in the women’s after taking a policy. To find out whether the women insurance policy is profitable or is

something else as motioned in the terms and condition. To determine the usefulness of women insurance to the illiterate as well as

literate women’s in India. To analyze the level of awareness of women insurance policy among people

and the responses of people after the introduction of the policy. To find out the overall impact of women insurance to the different class of

women’s in India.

2

SCOPE OF THE STUDY

The scope of the study is wider as it is extended to the women’s in India belonging to different categories.

To full fill the objective of the research the study is undertaken to analyze the

awareness of women insurance and its benefits towards women’s in India.

RESEARCH METHODOLOGY:

The data collection involves both primary and secondary data collection and they

are collected from the respective sources.

The primary data is collected by the help of a survey and cross analysis for

identifying the level of awareness of women insurance in India.

The secondary data is collected from online database, books and journals available

as sources of information.

3

EXECUTIVE SUMMARY

Women’s are the god gifted they should be treated equally. They should be given respect and honor in all aspect. The increasing crimes against women’s in India places emphasis on the need of some appropriate remedial measures. This project is regarding the improving awareness of insurance for women’s in India. The insurance companies have planned the women insurance policy. The women’s working at home, women’s who are educated but cannot afford to work due to the responsibility of her house and families. They can also take the fruitful benefit of the policy. Basically the insurance companies have taken many initiatives to improve the awareness through effective advertising, seminars, workshops etc.

4

CHAPTER: 1

INSURANCE

Human life is exposed to many risks, which may result in heavy financial losses. Insurance is one of the devices by which risks may be reduced or eliminated in exchange for premium. In words of Chief Justice Tindal, “Insurance is a contract in which a sum of money is paid by the assured in consideration of the insurer's incurring the risk of paying larger sum upon a given contingency”. In its legal aspects it is a contract whereby one person agrees to indemnify another against a loss which may happen or to pay a sum of money to him on the occurring of a particular event. All contracts of insurance (except marine insurance) may be verbal or in writing, but practically contracts of assurance are included in a document.

DEFINITION

Risk-transfer mechanism that ensures full or partial financial compensation for the loss or damage caused by event(s) beyond the control of the insured party. Under an insurance contract, a party (the insurer) indemnifies the other party (the insured) against a specified amount of loss, occurring from specified eventualities within a specified period, provided a fee called premium is paid. In general insurance, compensation is normally proportionate to the loss incurred, whereas in life insurance usually a fixed sum is paid. Some types of insurance (such as product liability insurance) are an essential component of risk management, and are mandatory in several countries. Insurance, however, provides protection only against tangible losses. It cannot ensure continuity of business, market share, or customer confidence, and cannot provide knowledge, skills, or resources to resume the operations after a disaster.

5

CHAPTER: 2

BASIC PRINCIPLES OF INSURANCE

The following are the basic essentials ‘or requirements of insurance irrespective of the type of insurance concerned.

9. UTMOST GOOD FAITH

All types of contracts of insurance depend upon the contracts of utmost good faith. Both parties (insurer and the insured) in the contract must disclose all material facts for the benefit of each other. False information or non-disclosure of any important fact makes the contract avoidable. So the conditions to show utmost good faith are very strict on the part of the insured.

2. INSURABLE INTEREST

The insured must possess an insurable interest in the object insured. It may be defined as a financial interest in the subject matter of contract. The presence of insurable interest is a legal requirement. So an insurance contract without the

1. UTMOST GOOD FAITH

2. INSURABLE INTEREST

3. PRINCIPLE OF INDEMNITY

6. CANCELLATION

5. DOCTRINE OF PROXIMATE

CAUSE

4. DOCTRINE OF SUBROGATION

7. ATTACHMENT OF RISK

8. MITIGATION OF LOSS

9. ARBITRATION

6

existence of insurable interest is not legally valid and cannot be claimed in a Court. The object of this principle is to prevent insurance from becoming a gambling contract.

3. PRINCIPLE OF INDEMNITY

All types of contracts except life and personal accident insurance are contract of indemnity. According to them, the insurer undertakes to indemnify the insured against a loss of the subject matter of insurance due to insured cause. In life assurance the question of loss and, therefore, of its indemnification does not rise. Because the loss of life cannot be estimated in term of money. The principles of indemnity are based on the idea that the assured in the case of loss only shall be compensated against the actual total loss. But if no event happens, the insured has not to receive any amount, so in this case the premiums paid by him become the profit of the Insurance.

4. DOCTRINE OF SUBROGATION

This principle applies to the contract of indemnity only i.e. marine and fire. It lays down a principle which is quite equitable. According to this doctrine, where a loss occurs and the insurer pays as for a total loss, he is entitled to all the rights and remedies which the insured has against a third party in respect of loss so paid for. It prevents the insured being indemnified from two sources in respect of the same loss. Suppose ‘A’ has damaged ‘B’ is motor car negligently. If he pays ‘B’ is loss in full. B cannot collect the same from the insurance company. On the other hand if B applied to his insurance company for indemnity under his policy, he will not be permitted to collect the damages from A. In the latter case the insurance company will be entitled to collect that amount.

5. DOCTRINE OF PROXIMATE CAUSE

This principle is found very useful when the loss occurred due to series of events. It means that in deciding whether the loss has arisen through any of the risks insured against, the proximate or the nearest cause should be considered. To take an illustration in one case where a policy holder sustains an accident while hunting. He was unable to walk after the accident and as a result of lying on wet ground before being picked up, he suffered pneumonia. There was an unbroken change of cause between the accident and the death, and the proximate cause of the death, therefore, was the accident and not the pneumonia.

7

6. CANCELLATION

Both parties have right to cancel the policy before its expiry date. The period of .the policy comes to an end on the cancellation of policy. So the protection provided by the insurer to the insured stops from the date of such cancellation. The premium received by the insurance company is also returnable to the insured.

7. ATTACHMENT OF RISK

Without the attachment of definite risk to the policy, the contract of insurance cannot be in force. So in this case the consideration fails and the premium received by the insurance company must be returned.

8. MITIGATION OF LOSS

When the event insured against takes place, the policy holder must do every thing to minimize the loss and to save what is left. This principle makes the insured more careful in respect of this insured property.

9. ARBITRATION

Most fire and accident insurance policies contain an arbitration clause which provides for referring’ to differences to an arbitration. The arbitrator is to be appointed in writing by the parties in difference. The object of this clause is to reduce litigation.

8

CHAPTER: 3

WHY WOMEN NEED LIFE INSURANCE

With greater economic power, comes greater responsibility Strong, smart, empowered, and independent – women are a force everywhere, from the boardroom to the classroom and beyond. Just consider these facts.

Women make up 51% of the population and represent the majority of college graduates.

More than half of the entire labor force is comprised of women.

Nearly 4 in 10 mothers (39.3%) are primary breadwinners for their family.

Nearly two-thirds (62.8%) of women are breadwinners or co-breadwinners, bringing home at least a quarter of the family’s earnings.

With all this economic power, however, comes greater responsibility, for women’s finances, and for the next generation.

Today, women have more financial responsibilities than ever before. How will their family or loved ones manage financially if they die? Whether they are single, married, employed, or a stay-at-home mom, they probably need life insurance. At the very least, life insurance can help pay for the costs of funeral and burial services, estate administration, outstanding debts, estate taxes, and the uninsured expenses of final illness.

1.Take Control of Future with Life Insurance:Whether women’s are a parent or a professional, just starting their career, in transition, or nearing retirement, they need to ensure their future – and that of the people they love – is bright and secure. Life insurance can help them do that – consider some of the benefits. Life insurance can:

2. Provide a lump sum of money to help pay expenses and generate an income:

9

Life insurance can’t replace them, but it can replace some or all of their income if they die. It can cover the cost of final expenses and help pay off debts, as well as day-to-day expenses, like food, clothing, and housing.

For the longer term, life insurance can help pay for their kids’ college education or help ensure their spouse or partner’s retirement dreams are realized.

3. Help with household needs:

If women’s are a parent, think of all the work they do on a daily basis. The endless scope of activities – combined for many with a busy career – can be stressful, and leave little time for ourselves. They are – after all – the CEO of anyone’s family: determining how finances are utilized, being a classroom parent, finding day care, or helping on that science project.

However many hats wear, the work they do is they invaluable toothier family. Life insurance can help pay for the vital household services that they “provide,” such as childcare, transportation and household chores.

4. Provide benefits they can use during their lifetime:

If they choose whole life insurance, the cash value in their policy – the “living benefits” – can be borrowed against to help pay for life’s events such as buying a home, paying for a wedding, or getting that Master’s Degree you’ve been wanting to earn. As they can pay the premiums of their whole life policy, the cash value builds and they can access those funds via policy loans. Some important things to keep in mind: loans accrue interest and decrease the death benefit and cash value.

5. Leave a lasting legacy:

Life insurance can create a financial legacy – for their kids, their spouse, their partner – even their favorite charity or alma mater.

6.Play an important role in retirement plan:

Whether they are single, an “empty nester,” or have people who depend on them, life insurance can play an important role in their retirement plan. How? Consider

10

their financial obligations such as a home mortgage, outstanding debts or medical expenses. The proceeds from their life insurance policy can help ensure these are settled and preserve the retirement plan them to work hard to put in place.

WHO NEEDS LIFE INSURANCE?

1).Working women

Increasingly, families depend on the income of two working parents. If they are a working mother, their income can have a significant impact on the quality of their family’s lifestyle. Their income helps cover the cost of ordinary living expenses such as food, clothing, and utilities, and it provides savings for their children’s college education, and for your retirement. Life insurance protects their family by providing proceeds that can be used to replace their lost income if they die prematurely.

2).Single women

Often, women, like men, think that it’s not necessary to buy life insurance because they have no dependents. What’s often overlooked is that life insurance can provide necessary funds to pay off car loans, education loans, debts, a mortgage, taxes, and funeral expenses that might otherwise be the responsibility of family members. Also, the cash value of permanent life insurance may be used to supplement retirement income.

3).Single moms

Whether she is divorced, widowed, or simply a single mom, she is most likely primarily responsible for her child’s support. If she die prematurely, life insurance can provide ongoing income to cover child-care costs, medical expenses, debts, and future college costs.

4).Stay-at-home moms

Maintaining a household is a full-time job, and they have many important roles and duties. The cost of the services performed by a stay-at-home mom could be quite significant if someone had to be hired to do them. If she die, her surviving spouse may have to pay for services such as child care, transportation for her children, and housekeeping. Taking over these added responsibilities could cause her spouse to

11

shorten work hours, resulting in a reduction in income. Proceeds from her life insurance can help her spouse pay for services that keep the household running and allow her spouse to keep working.

5).Family caregiver

Many women find themselves providing care for both children and elderly family members. Caring for an aging parent or family member can include paying for the costs of adult day care, uninsured medical expenses, and extra transportation. Adding these expenses to the costs of maintaining a household, child care, and college tuition can be financially overwhelming. Unfortunately, these added financial responsibilities often continue after their r death. Life insurance provides a source of funds that can be used to help pay for these expenses.

6).Business owner

She may be one of the increasing numbers of women business owners. If she die while owning her business, life insurance can be used to provide cash for company expenses such as payroll or operating costs while her estate is being settled. Also, life insurance can be a useful tool for business owners structuring buy-sell arrangements or providing benefits to key employees.

4 REASONS WHY WOMEN NEED TERM LIFE INSURANCE

49% of women are now in the workforce. Yet, 43% of these working women have no life insurance. This means that a very large percentage of families are dependent on the female income, yet that income isn’t insured. A good portion of married couples are dual-income providers and both incomes should be properly insured for worst-case scenarios. It is even more essential for single moms to have solid coverage to protect their family. Stay-at-home moms are not left out of this, as they provide high value in the service and care they perform for their family. Women need to be insured plain and simple.

4. Dual Income Dependence:

According to the Population Reference Bureau, in 2002 only 7% of American households consisted of married couples with children in which only the husband worked. That number has declined even further in the financial turmoil of recent

12

years. Families are dependent on both parents’ incomes and, in turn, both those incomes should be adequately insured to provide family security.

2. Single Moms:

The US Census Bureau found that 79% of custodial single mothers are gainfully employed. 50% work full time. Despite other sources of income, such as alimony or child support, the income of a single mom is critical to the family she supports. Many single moms are raising their children with little or no help from the outside. What would happen if she was no longer able to provide?

3. Stay-at-Home Moms:

For the family that has Mom at home, sacrifices are usually made to make that happen. The service and care she provides ads up quickly in value when tallied. That value balances out the income not gained by her not being in the work force. This means stay-at-home moms have tremendous importance in value that requires being insured. If something were to happen, her spouse would be required to add the cost of those services to his solo family income. That’s a recipe for disaster.

4. Women Have Arrived:

Just think, roughly 100 years ago women weren’t even allowed to purchase insurance. The value of what women did wasn’t considered worth insuring. Obviously our nation has changed dramatically, and that’s a ridiculous thing to consider now. All women provide financial value to their family, and insurance provides the safety net if she can no longer provide for whatever reason.

13

CHAPTER: 4

LIFE INSURANCE TYPES AND OPTIONS

Life insurance comes in many different sizes and shapes, and determining the policy that meets her needs may depend on a number of factors. Understanding the basic types of life insurance can help her to find the policy that’s best for her.

Term life insurance

Term life insurance provides a simple death benefit for a specified period of time. If she dies during the coverage period, the beneficiary name in the policy receives the death benefit. If she lives past the term period, her coverage ends, and she get nothing back. The cost, or premium, for the coverage can be fixed for the duration of the policy term (usually 1 to 30 years) or it can be “annually renewable” meaning that the premium can increase each year as she get older. However, the premium for term insurance usually costs less than the premium for permanent insurance when all factors are the same, including the death benefit.

Whole life insurance

Whole life is permanent or cash value insurance that provides insurance coverage for her entire life. With most whole life policies, part of their premium is added to the cash value account, which earns interest. Some whole life policies also pay a dividend, which represents a portion of the company’s profits made during the prior year. The cash value grows tax deferred and can either be used as collateral to borrow from the insurance company or be directly accessed through a partial or complete surrender of the policy. It is important to note, however, that a policy loan or partial surrender will reduce the policy’s death benefit, and a complete surrender will terminate coverage altogether.

Universal life insurance

Universal life is another type of permanent life insurance with a death benefit and a cash value account. A universal life insurance policy will generally provide very broad premium guidelines (i.e.., minimum and maximum premium payments), but within these guidelines she can choose how much and when she pay premiums.

14

She is also free to change the policy’s death benefit directly (again, within the limits set out by the policy) as her financial circumstances change. But if she wants to raise the amount of coverage, she’ll need to go through the insurability process again, probably including a new medical exam, and her premiums will increase.

Variable life insurance

Variable life insurance is a type of cash value coverage that allows her to choose how her cash value account is invested. A variable life policy generally contains several investment options, or unaccounted, that are professionally managed to pursue a stated investment objective. Choices can range from a fixed interest unaccounted to an international growth unaccounted. Variable life insurance policies require a fixed annual premium for the life of the policy and may provide a minimum guaranteed death benefit. If the cash value exceeds ascertain amount, the death benefit will increase.

Variable universal life insurance

Variable universal life combines all of the options and flexibility of universal life with the investment choices of a variable policy. She can decide how often and how much her premium payments are to be, within policy guidelines. With most variable universal life policies, she get no guaranteed minimum cash value or death benefit, but she can direct how your premium payments are invested among policy unaccounted.

Joint and survivor life insurance

She and her spouse may choose to buy a single policy of permanent insurance that covers both of their lives. With first-to-die, the death benefit is paid at the death of the spouse who dies first. With second-to-die, no death benefit is paid until both spouses are deceased. Second-to-die policies are commonly used in estate planning to pay estate taxes and other expenses due at the death of the second spouse. Other than the fact that two people are insured by one policy, the policy characteristics remain the same.

Bottom line

15

Life insurance protection for women is equally as important as it is for men. However, women’s life insurance coverage is often inadequate. It may be time to consult an insurance professional who can help her to assess her life insurance needs, and offer information about the various types of policies available.

16

CHAPTER: 5

TYPES OF WOMEN INSURANCE POLICIES AVAILABLE IN INDIA

LIC JEEVAN BAHRTI

FEATURES

IntroductionLIC’s Jeevan Bharati-I – is a plan exclusively for women. It is a with profit plan having special features considering the needs of women. The plan also provides for Accident Benefit, Critical Illness Benefit and Congenital Disability Benefit as optional Riders

Types of women insurance

17

A. SPECIAL FEATURES

1. Encashment of Survival Benefit as and when needed:The policyholder at her option may avail the survival benefit any time on or after its due date. If opted to avail later, increased survival benefit at the rate decided by the corporation from time to time will be payable.

2. Flexibility to pay premiums in advance:The mode of premium payment is only yearly under this plan. However, policyholder may pay the next yearly premium in advance in installments (maximum up to 3 installments) during the year. If premiums are paid in advance a premium rebate may be allowed as may be decided by the Corporation from time to time

3. Option to receive maturity proceeds in the form of an annuity: The policyholder shall have the option to receive the maturity proceeds in the form of annuity. The rate of annuity will be based on the annuity rates prevalent at the time of stipulated Date of Maturity.

4. Auto Cover:

After two years premiums have been paid, whenever premium payment is discontinued, the life cover for full sum assured will continue for 3 years from the due date of first unpaid premium.

If death occurs during the Auto Cover period, then death benefit after deducting unpaid premiums, with interest is payable along with the vested bonus, if any.

The auto cover shall not be available for rider benefits.

B. OPTIONAL RIDERS:The following riders are available under this plan:

(a). CRITICAL ILLNESS (CI) RIDER : An amount equal to the Critical Illness Rider Sum Assured will be payable in case of diagnosis of defined categories of critical illnesses. A person is eligible for this benefit up to a maximum age of 60 years but subject to a maximum of the policy

18

term. This benefit can be availed for a minimum Sum of Rs 50000 and for a maximum Sum equal to the Sum assured under the basic plan subject to the maximum of Rs 5 lakh overall limit taking all critical illness riders under all existing policies of the Life Assured.

(For details refer the sales brochure of Critical Illness rider)

(b). ACCIDENT BENEFIT RIDER:An additional amount equal to the Accident Benefit Rider Sum Assured is payable upon death or total and permanent disability due to accident during the policy term.

This benefit can be availed for a minimum sum of Rs 50000 and for a maximum sum equal to the Sum Assured under the Basic Plan subject to the maximum of Rs.50 lakhs.

(c). CONGENITAL DISABILITIES BENEFIT (CDB) RIDER:

This rider can be opted for by a female between the ages of 18yrs and 35 years.An amount equal to 50% of the CDB Sum Assured is payable if the Life Assured gives birth to a child with specified congenital disabilities. This benefit is available for a maximum of two such children and this benefit ceases at the age of 40 years. This benefit can be availed for a minimum Sum of Rs 50000 and a maximum sum of Rs 500000.

3. ELIGIBILITY CONDITIONS (For Basic Plan):

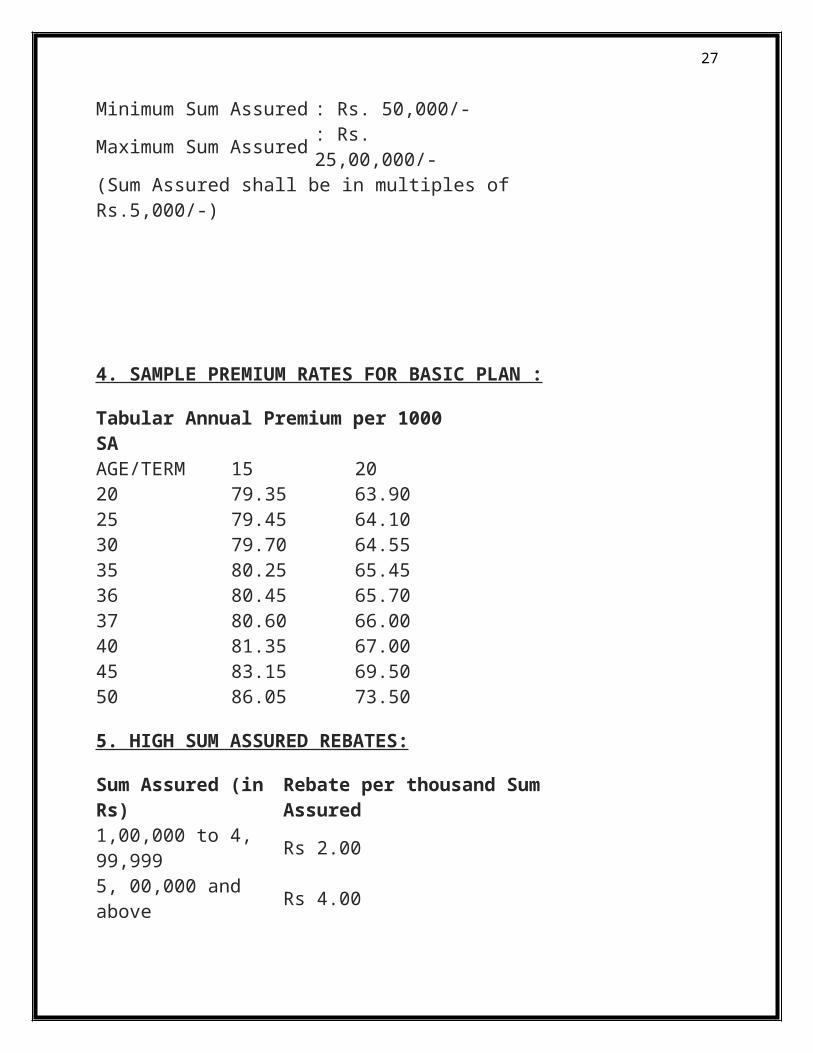

Minimum age at entry : 18 years (completed)Maximum age at entry : 55 years (nearest birthday)Maximum age at maturity : 70 years (nearest birthday)Policy term : 15 and 20 yearsMinimum Sum Assured : Rs. 50,000/-Maximum Sum Assured : Rs. 25,00,000/- (Sum Assured shall be in multiples of Rs.5,000/-)

19

4. SAMPLE PREMIUM RATES FOR BASIC PLAN :

Tabular Annual Premium per 1000 SAAGE/TERM 15 2020 79.35 63.9025 79.45 64.1030 79.70 64.5535 80.25 65.4536 80.45 65.7037 80.60 66.0040 81.35 67.0045 83.15 69.5050 86.05 73.50

5. HIGH SUM ASSURED REBATES:

Sum Assured (in Rs) Rebate per thousand Sum Assured1,00,000 to 4, 99,999 Rs 2.005, 00,000 and above Rs 4.00

6. LOAN:Loan is available under the plan after the policy acquires paid-up value.

7. GRACE PERIOD:A grace period of one-month but not less than 30 days will be allowed for payment of premium .

8. REVIVAL:

A. REVIVAL DURING THE AUTO COVER PERIOD:(i) If Critical Illness Rider is not opted for:During the Auto Cover Period, the Life Assured can pay one or more instalments of premiums with interest without submission of any evidence of health. On payment of part or full arrears of premiums with interest, the Auto Cover Period of 3 years from the due date of new FUP shall again be available during the term of the Policy.

If any survival benefit falls due during the above 3-year auto cover period the same will be paid after deduction of unpaid premiums with interest until the due date of the survival benefit, provided it is more than the unpaid premiums with interest. If

20

the survival benefit is insufficient to cover the arrears of premiums with interest up to the due date of such survival benefit, then the survival benefit will be payable only on payment of such arrears of premiums with interest , during the period of the aforesaid 3 years or on revival of the policy thereafter.(ii) If Critical Illness Rider is opted for:During the auto cover period, the policy can be revived by payment of full arrears of premium together with interest and subject to submission of proof of continued insurability of the Life Assured to the satisfaction of the Corporation. The Corporation reserves the right to accept at original terms, accept at revised terms or decline the revival of the policy. The revival of the policy shall take effect only after the same is approved by the Corporation and is specifically communicated to the Life Assured.

If any survival benefit falls due during the above 3-year auto cover period the same will be paid only after revival of the policy as stated above.

B. REVIVAL OTHER THAN DURING AUTO COVER PERIOD : If the Policy has lapsed, and the policy is not under the period of auto cover, the policy can be revived within a period of 5 years from the date of first unpaid premium and before the date of maturity by payment of full arrears of premium together with interest and subject to submission of proof of continued insurability of the Life Assured to the satisfaction of the Corporation. The Corporation reserves the right to accept at original terms, accept at revised terms or decline the revival of a discontinued policy. The revival of discontinued policy shall take effect only after the same is approved by the Corporation and is specifically communicated to the Life Assured.

The Rider/s shall be revived along with the Basic plan and not in isolation.

9. PAID UP VALUE: If after at least three full years’ premiums have been paid and any subsequent premium not paid, this policy shall not be wholly void after the expiry of three years Auto Cover Period ,but shall continue as a paid up policy. The Sum Assured of the policy shall be reduced in the same proportion as the number of premiums actually paid bears to the total number of premiums stipulated for in the policy , less any survival benefit paid. This reduced Sum is called the paid up value.

The policy thereafter shall be free from all liabilities for payment of the premiums, but shall not be entitled to the future bonuses. The existing vested reversionary bonuses, if any, will remain attached to the reduced paid-up Policy. This paid up

21

value shall be payable on the date of maturity or at Life Assured’s prior death. No survival benefit shall be payable under paid up policies.

The rider benefits will cease to apply if the policy is in lapsed condition and will not acquire any paid up value.

10. SURRENDER VALUE:The Guaranteed Surrender value will be available after the expiry of 3 policy years provided the premiums have been paid for at least three years. The Guaranteed Surrender Value is equal to 30% of the total amount of premiums paid excluding the premiums paid for the first year, any premiums paid towards riders, all extra premiums that may have been paid less the amount of survival benefits paid earlier. The cash value of any existing bonuses, if ,any will also be paid .Corporation may, however, pay special surrender value as the discounted value of Paid up sum assured and vested bonus, if any, as applicable on date of surrender, provided the same is higher than guaranteed surrender value.

11. EXCLUSIONS:Suicide: This policy shall be void if the Life Assured commits suicide (whether sane or insane at that time) at any time on or after the date on which the risk under the policy has commenced but before the expiry of one year from the date of commencement of risk under the policy and the Corporation will not entertain any claim by virtue of this policy except to the extent of a third party’s bonafide beneficial interest acquired in the policy for valuable consideration of which notice has been given in writing to the branch where the Policy is being presently serviced (where the policy records are kept), at least one calendar month prior to death.

12. COOLING OFF PERIOD:If women are not satisfied with the “Terms and Conditions” of the policy, women may return the policy to us within 15 days.

BENEFITS

A. Survival Benefits:

22

On Survival the following benefits are payable:

For 15 Years Term20% of the Sum Assured payable at the end of 5 years.20% of the Sum Assured payable at the end of 10 years.60% of the Sum Assured payable together with vested bonus, and Final Additional Bonus, if any, at the end of 15 years.

For 20 Years Term20% of the Sum Assured payable at the end of 5 years.20% of the Sum Assured payable at the end of 10 years.20% of the Sum Assured payable at the end of 15 years.40% of the Sum Assured payable together with vested bonus and Final Additional Bonus, if any at the end of 20 years.

B. Death Benefit:In case of death of the life assured during the policy term, the full sum assured is payable irrespective of the survival benefits paid earlier. The vested bonuses and Final Additional Bonus, if any are also payable.

Statutory warning:“Some benefits are guaranteed and some benefits are variable with returns based on the future performance of women Insurer carrying on life insurance business. If women policy offers guaranteed returns then these will be clearly marked “guaranteed” in the illustration table on this page. If women policy offers variable returns then the illustrations on this page will show two different rates of assumed future investment returns. These assumed rates of return are not guaranteed and they are not the upper or lower limits of what women might get back, as the value of women policy is dependent on a number of factors including future investment performance.”

23

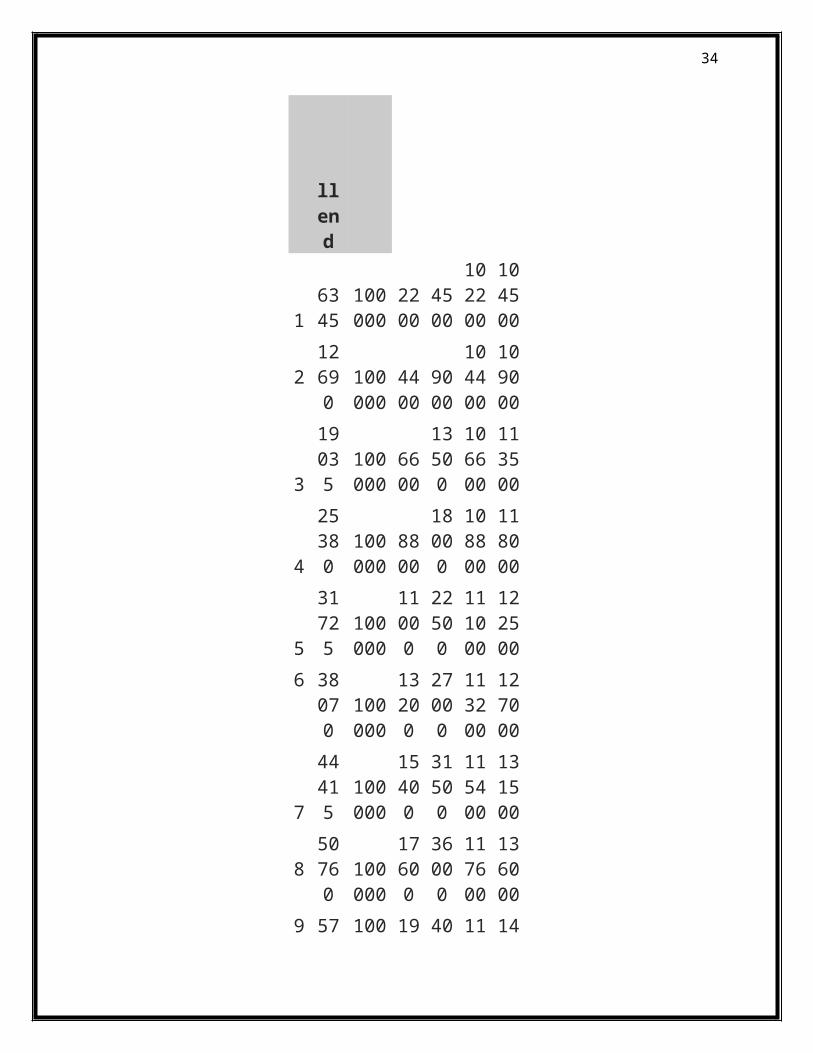

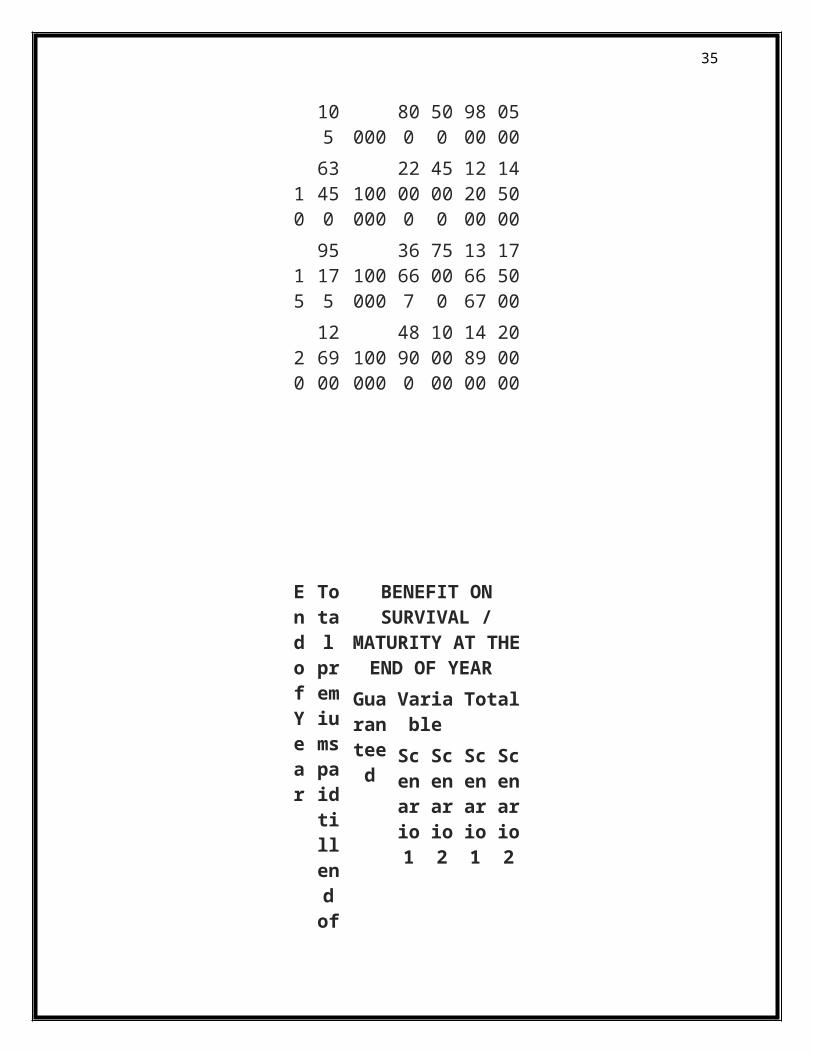

Benefit IllustrationAge of LA (Yrs.) 35Term (Yrs.) 20Sum Assured(Rs.) 100000Annual Premium 6345

EndofYear

Total

premiums paid

till end of

year

Death Benefit during the year

Guaranteed

Variable

Total

Scenario 1

Scenario 2

Scenario 1

Scenario 2

16345

100000

2200

4500

102200

104500

2 12690

100000

4400

9000

104400

109000

319035

100000

6600

13500

106600

113500

425380

100000

8800

18000

108800

118000

531725

100000

11000

22500

111000

122500

6 380 1000 13 27 11 12

24

70 00200

000

3200

7000

744415

100000

15400

31500

115400

131500

8 50760

100000

17600

36000

117600

136000

957105

100000

19800

40500

119800

140500

10

63450

100000

22000

45000

122000

145000

15

95175

100000

36667

75000

136667

175000

20

126900

100000

48900

100000

148900

200000

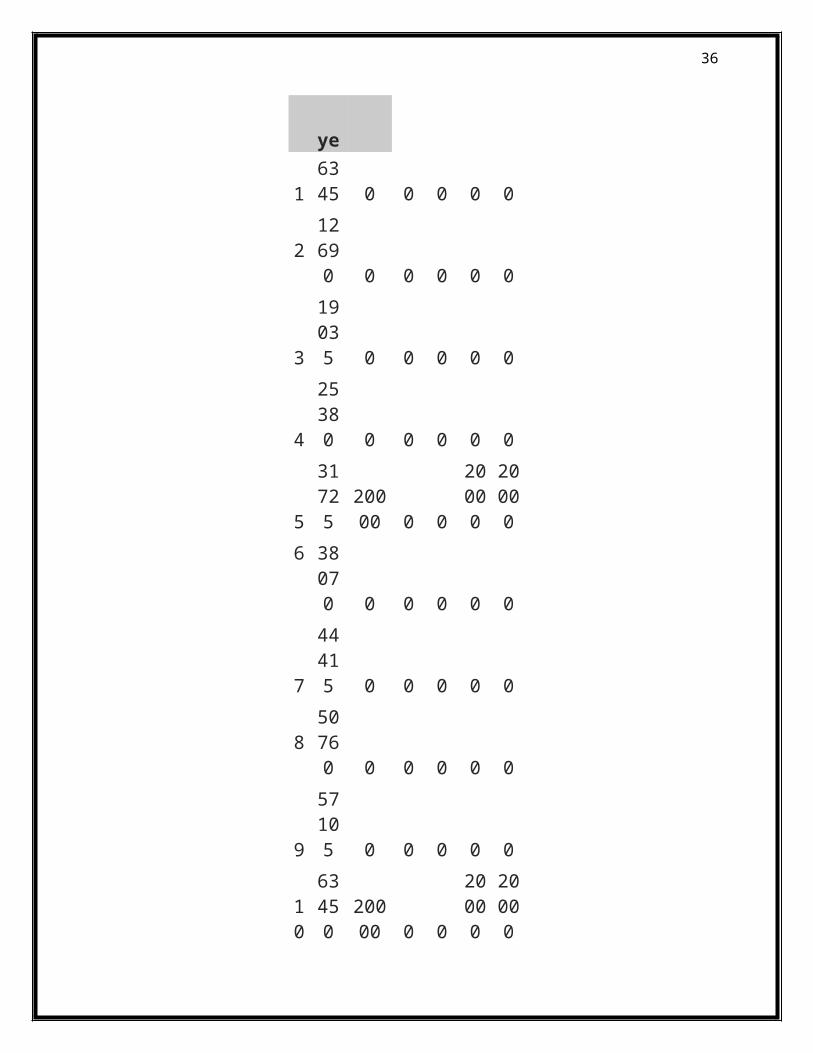

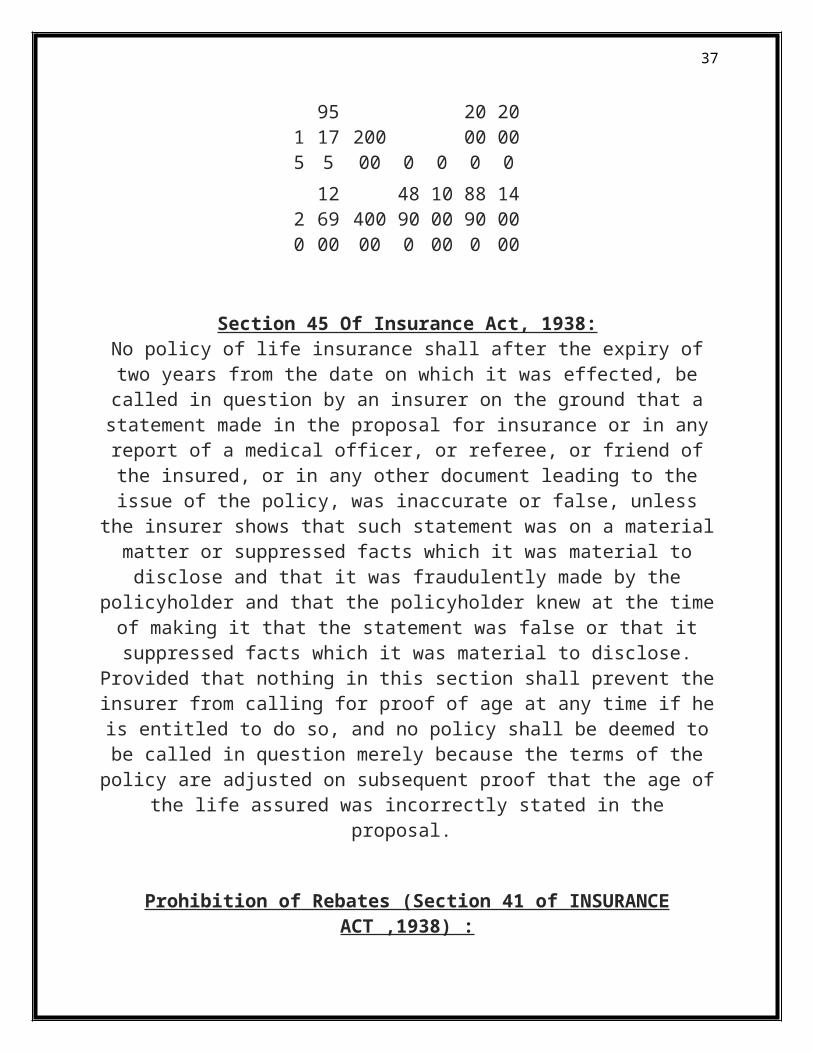

EndofYear

Total

premiums paid

till end of

yea

BENEFIT ON SURVIVAL /

MATURITY AT THE END OF

YEAR

Guaranteed

Variable

Total

Scenario

Scenario

Scenario

Scenario

25

r1 2 1 2

16345 0 0 0 0 0

212690 0 0 0 0 0

319035 0 0 0 0 0

425380 0 0 0 0 0

531725

20000 0 0

20000

20000

6 38070 0 0 0 0 0

744415 0 0 0 0 0

850760 0 0 0 0 0

957105 0 0 0 0 0

10

63450

20000 0 0

20000

20000

15

95175

20000 0 0

20000

20000

20

126900

40000

48900

100000

88900

140000

Section 45 Of Insurance Act, 1938:No policy of life insurance shall after the expiry of two years from the date on which it was effected, be called in question by an insurer on the ground that a

statement made in the proposal for insurance or in any report of a medical officer, or referee, or friend of the insured, or in any other document leading to the issue of

26

the policy, was inaccurate or false, unless the insurer shows that such statement was on a material matter or suppressed facts which it was material to disclose and

that it was fraudulently made by the policyholder and that the policyholder knew at the time of making it that the statement was false or that it suppressed facts which it was material to disclose. Provided that nothing in this section shall prevent the insurer from calling for proof of age at any time if he is entitled to do so, and no policy shall be deemed to be called in question merely because the terms of the

policy are adjusted on subsequent proof that the age of the life assured was incorrectly stated in the proposal.

Prohibition of Rebates (Section 41 of INSURANCE ACT ,1938) :(1) No person shall allow or offer to allow, either directly or indirectly, as an

inducement to any person to take out or renew or continue an insurance in respect of any kind of risk relating to lives or property in India, any rebate of the whole or part of the commission payable or any rebate of the premium shown on the policy

nor shall any person taking out or renewing or continuing a policy accept any rebate except such rebates as may be allowed in accordance with the published prospectuses or tables of the insurer provided that acceptance by an insurance

agent of commission in connection with a policy of life insurance taking out by himself on his own life shall not be deemed to be acceptance of a rebate of

premium within the meaning of this sub-section if at the time of such acceptance the insurance agent satisfies the prescribed conditions establishing that he is a bona

fide insurance agent employed by the insurer.

(2) Any person making default in complying with the provision of this Section shall be punishable with a fine, which may extend to 500 rupees.

WHAT DOES LIFE INSURANCE FOR WOMEN COVER?

Life insurance for women covers what it does for men – it is a way of ensuring that in the event of women death, women will leave women family or dependants with a lump sum that will allow them to continue with a standard of living that they enjoyed while women were still here.

As more women than ever are now the main breadwinners in the family, making sure women have life cover is essential, because if women were to die unexpectedly or are taken seriously ill, women income – the main source of income – would cease. This would cause significant problems for women loved

27

ones, who would potentially find themselves out of the family home if they could no longer afford to meet the mortgage payments.

Despite this, many women still fail to get life cover to protect their family, in some cases it is because they are staying at home to care for their family and don’t see their role at home as having any monetary value. But what many stay-at-home mums forget is that the role they have is worth a lot of money, even if they are not specifically getting paid for doing the work.

It could impact on the household finances further as the main breadwinner could find themselves taking time off work to look after the children, which means that not only would women family lose the value of the work of one parent, the second parent may also see their income reduced as they need to reduce the hours they are working.

SAVE MONEY ON WOMEN LIFE INSURANCE

Q.1) What types of life insurance is there for women?

Both men and women can get term assurance and whole of life cover. Term assurance is a policy which is in force for a specific period of time and is usually sold alongside a mortgage.

Lenders will generally want a way of getting their money back if women die, and that is why one of the conditions is that women have life cover alongside the mortgage. Term assurance is perfect for this as it can be in force for as long as the mortgage term. So often, these policies are in place for 25 years – if women die within this time, women will get a lawwomen. But if women live longer than the policy is in place, it will simply expire and women will no longer get a lawwomen if women die.

There are two types of term assurance: level term and decreasing term. Level term means the lawwomen that is made if women make a claim within the period the policy is in force stays the same throughout the entire policy term.

Decreasing term means the lawwomen will reduce over the term of the policy,

28

usually this is in line with how the mortgage it is written alongside is reducing over time. The premiums should also fall as the lawwomen falls. an I take out life insurance during pregnancy

Life insurance during pregnancy will be no different to a policy women would get without being pregnant. But women may need to consider some of women answer to the questions that the insurer bases the premium calculations on.

Women weight, for example, will be higher than normal if women are pregnant. So women should give the weight that women were immediately before women became pregnant.

The amount of alcohol women drink and whether women smoke or not may also is different – women would probably not be doing either while women are pregnant – so women need to take that into consideration too. How women deal with it will depend on the questions women are asked, as some policies will be specific about whether women have recently been advised ‘for medical reasons’ to give up alcohol. This will allow women to explain the reason.

If this is not an option, women should speak to women insurer directly to make sure women give all of the information that is needed. Not doing so could result in women policy being deemed invalid.

Once women have children, women may also want to consider taking out a joint life policy so that if women or women partner or spouse dies, women children will be taken care of. Joint policies are usually cheaper than buying two separate policies, and women can have joint life first death or, more rarely, joint life second death.

With the former, the payment will be made when the first of the two people named on the policy dies. The latter will only lawwomen when the second person named on the policy dies, which is why it is rarer.

The difference in premiums for men and women

29

Historically women have paid less for life insurance than men because statistically they are likely to live longer and therefore have more time to pay the premiums for an equivalent lawwomen.

However, from December 2012, a ruling from the European Court of Justice will be enforced which will mean it is no longer legal for insurers to base premium costs solely on gender differences.

Q.2) Will the cost of life insurance for women rise?

As yet, it is not clear whether prices for women will rise, or they will fall for men, or they will meet somewhere in the middle.

But if women had a policy in place before December 2012 with fixed premiums, women should not see any premium increases as a result of the change in the law.

The measures can take as a woman are the same as those taken by a man. Changing some of the risk factors that insurers base their premium calculations on will help to cut costs.

For example, if women are obese and women lose weight, women premiums should fall. Similarly if women drink less alcohol, or stop smoking and lead a healthier lifestyle, these will all be looked favorably on by women insurer. Alcohol consumption, weight and smoking all increase the amount women pay, so changing any or all of these will cut costs.

30

HDFC LIFE SMART WOMAN PLAN

HDFC Life Smart Woman Plan, a life insurance policy for women that gives wings to your aspirations. The plan ensures your savings grow leaving you free to pursue your career and continue making a difference to those around you.

Women always wanted to make a difference in the lives of their loved ones. This is what gives true happiness. In their own way, women did what it took to keep them happy with their satisfaction always being a priority for you.

Now that you are independent and have complete charge of your finances, some amount of planning can go a long way in fulfilling dreams for yourselves and your loved ones.

Presenting, HDFC Life Smart Woman Plan, a life insurance policy for women that give wings to their aspirations. The plan ensures their savings grow leaving them free to pursue their career and continue making a difference to those around them.

31

It also provided options which cater to specific life events of women with respect to their health, career and marriage.

FEATURESOptions to choose from 5 funds to suit risk appetite:

1. Short-term Fund: Low capital risk as exposure is only to the short – term instruments (Max 3-year residual maturity)

2. Income Fund: Higher potential returns due to higher duration and credit exposure

3. Balanced Fund: Dynamic equity exposure to enhance the returns while the debt allocation reduces the volatility

4. Blue chip Fund: Investments in large cap equities5. Opportunities Fund: Investments in mid-cap equities

You can select any of the 3 Benefit Options, each created to meet specific needs such as:

1. Pregnancy complications or birth of child with congenital disorder2. Diagnosis of malignant cancer of female organs3. Death of spouse (Only with Elite option)

Classic – Under this option you can avail of premium waiver benefit with funding of next 3 years’ premiums.

Premier – Under this option you can avail of premium waiver benefit with funding of next 3 years’ premiums and periodic cash payouts of 100% of next 3 years’ premiums.

Elite – Under this option you can avail of premium waiver benefit with funding of next 3 years’ premiums and periodic cash payouts of 100% of next 3 years’ premiums along with coverage for death of spouse.

Flexibility to choose the sum assured Convenience to choose policy tenure of 10/15 years.

ADVANTAGES

Uninterrupted savings with waiver and funding of premiums for next 3 years on the following events

1. Pregnancy complications or birth of child with congenital disorder2. Diagnosis of malignant cancer of female organs3. Death of spouse (Only with Elite option)

Additional periodic cash payouts under Premier and Elite options Flexibility to make partial withdrawals to meet contingencies Avail of hassle-free annual premium payment option

32

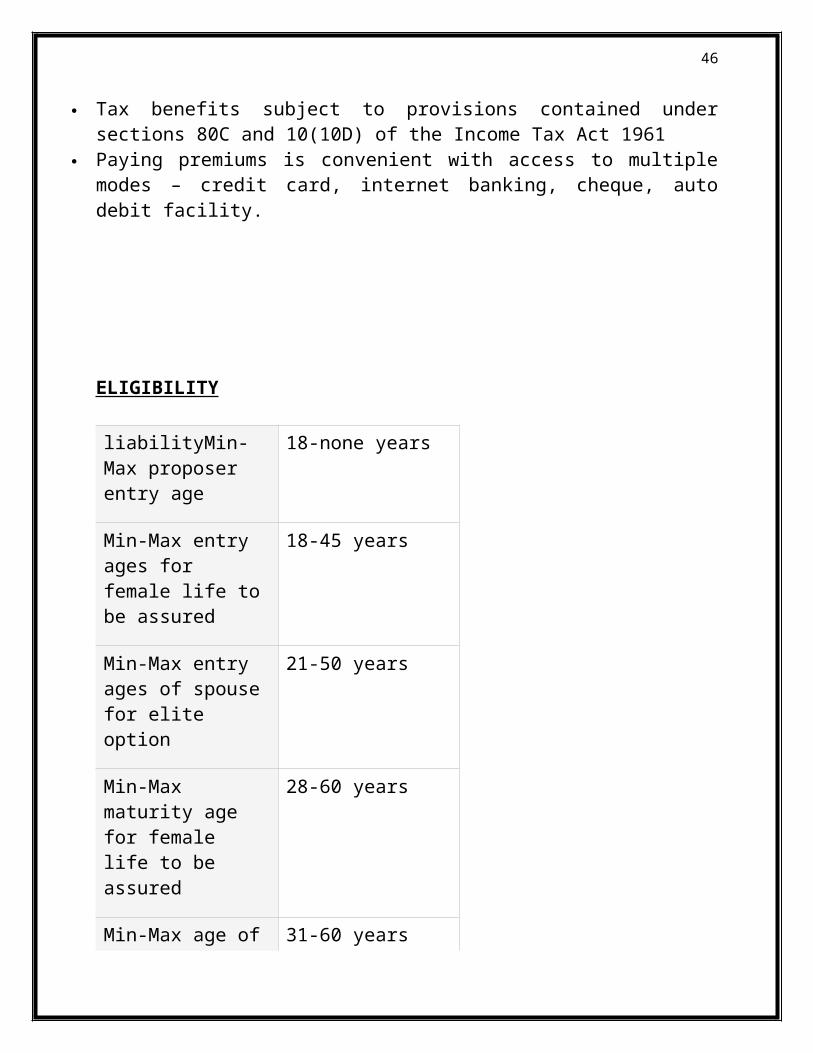

Tax benefits subject to provisions contained under sections 80C and 10(10D) of the Income Tax Act 1961

Paying premiums is convenient with access to multiple modes – credit card, internet banking, cheque, auto debit facility.

ELIGIBILITY

liabilityMin-Max proposer entry age

18-none years

Min-Max entry ages for female life to be assured

18-45 years

Min-Max entry ages of spouse for elite option

21-50 years

Min-Max maturity age for female life to be assured

28-60 years

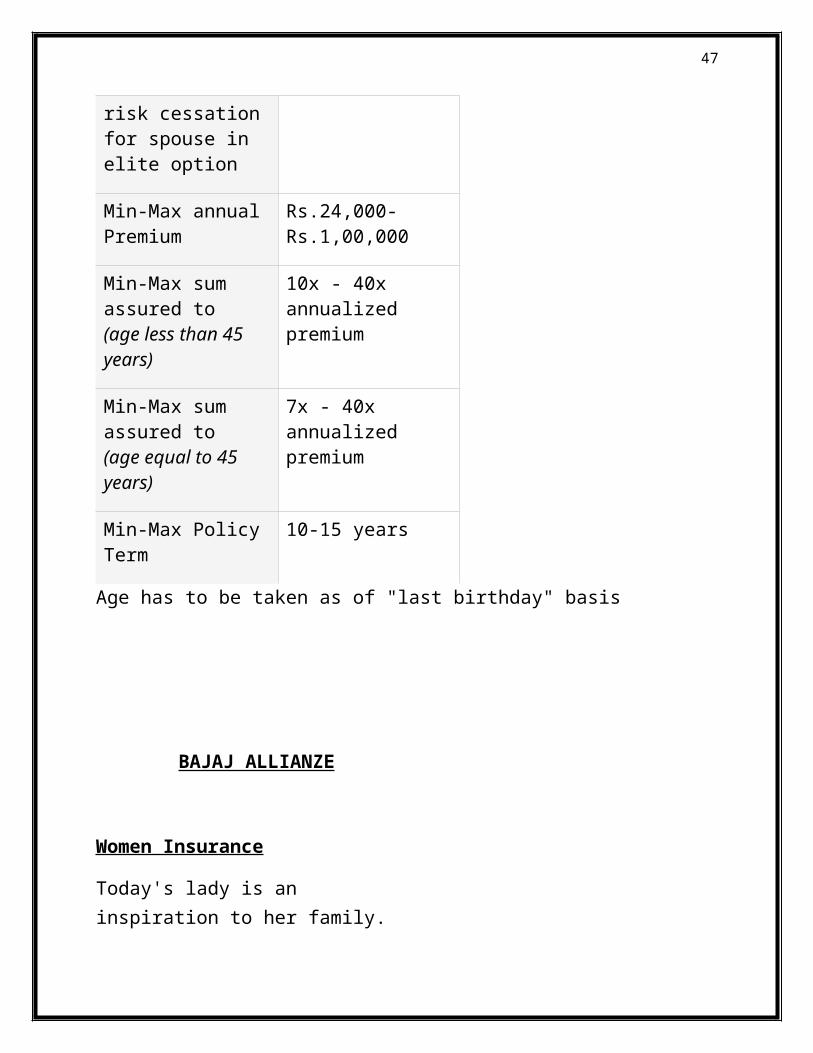

Min-Max age of risk cessation for spouse in elite option

31-60 years

Min-Max annual Premium

Rs.24,000-Rs.1,00,000

Min-Max sum assured to(age less than 45 years)

10x - 40x annualized premium

33

Min-Max sum assured to(age equal to 45 years)

7x - 40x annualized premium

Min-Max Policy Term

10-15 years

Age has to be taken as of "last birthday" basis

BAJAJ ALLIANZE

Women Insurance

Today's lady is an inspiration to her family.She takes important decisions in every household and at work. To cater to women's special needs we offer innovative women specific plans which provide investment benefits, savings, retirement solutions and medical insurance? Our special plans help mothers plan for their children’s education saves for the future and take care of all medical emergencies in the family. Regular investment and savings plan, offer:

Investments along with critical illness benefits which provide good returns, long term saving and protection in case of a medical emergency Investment plans with

34

accidental coverage Children's education planning Specialized retirement income plans for homemakers to provide a secure and financial future.

Education Plans for the Confident Girl Child Is your little girl destined for greatness? Will she grow up to be successful? Your princess can reach for the stars, but before she dreams you must do. Bajaj Allianz offers Child Education plans, which help a parent secure education for their child. A specialized plan known as Bajaj Allianz Child Gain offers a wide array of solutions that allows you to plan for your daughter's future, including schooling, higher education and marriage and also takes care of any uncertainties that may happen along the way

Plans for the Confident Young LadyAs a young, confident woman, you are either studying to make your career or are earning your own living and are financially independent. We at Bajaj Allianz offer many products, which help check, plan and keep all your finances in order, as well as take care of your other needs. Bajaj is a plan that helps you enter the Capital Markets with no fear. While our special Motor Insurance Package Policy with unique women-specific services makes sure that you can drive around, worry-free.Plans for the Confident Home MakerAs a home maker of today, you are also the decision maker, unlike before. You are equally aware of the outside world and are accustomed to being consulted by your

35

husband on decisions pertaining to finances. You also go out of your way to take care of your family with your warmth and support in case of any illness and ensure that your family members are treated with the best medical care. Saluting the confident home maker of today, Bajaj Allianz offers two plans - Bajaj Allianz Invest Gain and Bajaj Allianz Family CareFirst. Plans with a rider especially developed for today's woman to give her that extra bit of confidence.

Plans for the Confident Future Grand MotherA majority of women consider 'financial security' to be one of their top priorities, yet most women feel they do not have the knowledge to address financial matters. It is necessary to be financially independent, as it gives you a sense of worth and purpose. Bajaj Allianz Future Income Generator is one plan which suits all. Irrespective of age this is one plan which would ensure that you remain financially independent in your golden years of life.

INSURANCE POLICIES DESIGNED FOR WOMEN

Life insurance is supposed to protect income. If something untoward happens to the policyholder, the insurance policy provides money to replace his (or her)

36

income. Therefore, an insurance company will sell a large term cover only after checking the income profile and tax returns. Even financial planners say there is no need to buy insurance for a person who does not earn.

When the Hyderabad-based software professional was offered a term insurance cover for his homemaker wife Swetha, he immediately bought it. He is paying Rs 4,200 a year for a cover of Rs 50 lakh for Swetha for a term of 43 years.

The company, AEGON Religare Life Insurance, believes that even homemakers have an economic value for the household. "A homemaker has an intrinsic economic value, though it cannot be substantiated by pay slips or income tax returns. For instance, if she were to take up a job, it is obvious that the family will have to incur some expenses for running the household. Therefore, the company has decided to offer life cover to homemakers whose husbands (or wives) have bought online term policy.

There is a ceiling of Rs 1 crore, and you will have to go through medical checkups for covers of over Rs 30 lakh.

Many insurance products meant for women went off the shelves after the new guidelines for endowment plans came in. Still, there are some policies that offer benefits specifically aimed at women. While some of these benefits seem attractive, buyers need to evaluate them before taking a final call. It's their utility value, not the 'exclusively for women' label that should be the deciding factor.

37

TATA-AIG'S WELLSURANCE WOMAN :

While the need for life insurance for homemakers is debatable, there is no scope for such doubts as far as health insurance is concerned. It is essential for working women as well as homemakers. "Uninsured women are more likely to suffer serious health problems as they tend to wait too long to seek treatment because of the costs involved. Only 10% of the total women workforce has some kind of health cover

The Wellsurance Woman policy is a combo of hospitalization benefit and critical illness cover. It pays a lump sum in case the policyholder is diagnosed with any of 11 specified critical illnesses, including cancer, heart attack, and stroke and kidney failure. It also pays out a daily cash benefit in case of hospitalization. But such a

38

policy should be taken only as an addition to the basic health plan that covers hospitalization.

BAJAJ ALLIANZ'S CRITICAL ILLNESS COVERS:

The policy covers eight women-specific critical illnesses, including paralysis and cancers (breast, ovarian, cervical, uterine, and vaginal and fallopian tube). "The treatment protocol for such illnesses is not only lengthy but also expensive and involves a lot of lifestyle modifications, such as giving up of job, ergonomic modifications at home, and so on. Hence, the need for a product specifically targeting this segment.

SPECIAL BENEFITS

1. Enhanced Allocation Rate of 102.5% per annum from 11th policy year

2. Waiver of charges on withdrawal/Switch during motherhood. 12 partial withdrawals or switches will be waived, within one year from date of childbirth.

Bajaj Allianz Life Insurance Company in association with the winners of the Pantaloons Femina Miss India 2009 pageant has launched a range of women-specific plans.

The plans are available as: Child Gain for the girl child, Young Care for the young lady, Unit Gain plus Gold for the home maker, Invest Gain, Family Care First and Future Income Generator for the future grandmother and Motor Insurance for the lady driver.

Some of the highlights of the plans are home pick up facility for renewal premium payment, spot assistance for lady car drivers including assistance services like tier replacement, key locked inside and survey at doorstep in case of small claims.

39

CHAPTER: 6

RESEARCH AND FINDINGS

Q.1) How old are you?

20-30. 30-40. 40-50.

Age Response (%)20-30 3430-40 4640-50 20

40

20-30 30-40 40-5005

101520253035404550

Analysis: in this the responded between the age of 20-30 are 34%, 30-40 are 46% and 40-50 are 20%.

Q.2) what is your occupation?

Analysis: Here in this responses received from different kind of people belong to different categories. The categories are divided into two parts male and female. Like many of them were professors, teachers, student, housewives and others.

Q.3) Do you have Insurance Policy?

Yes No

Variable

Response(%)

YES 88%NO 12%

41

88%

12%

YESNO

Analysis: In this Question 88% people said that they have insurance policy and 12% do not have insurance policy.

Q.4) If Yes, which policies do you have?

Policy Name Response(%)Life Insurance 47%Health Insurance 29%Med claim Insurance 11%Vehicle Insurance 8%Others 5%

42

Life I

nsuran

ce

Health

Insu

rance

Medicla

im In

suran

ce

Vehicle

Insu

rance

Others0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Response(%)

Analysis: Here in this, 47% people have life insurance policy as everyone are concerned about their life and 29% have health insurance , med claim policy is used by 11% people 8% people have taken vehicle insurance for their respective vehicle and 5% is for other insurance policy.

Q.5) If No, why have you not taken?

Analysis: As mentioned in Question 3 that12% people have not taken insurance policy they gave many reasons like some of them said now they don’t need, some of them said there is not a specific reason.

Q.6) Are you interested in taking a policy?

Yes No

Variable

Response (%)

YES 65%

43

NO 35%

65%

35%

YESNO

Analysis: In this 65% people said that they are interested in taking policy and 35 % said no.

Q.7) which company’s policy have you taken?

Company Name

Response(%)

LIC 53%Bajaj Allianz 19%Birla Sun Life 17%

44

Others 11%

LIC

Bajaj A

llianze

Birla Su

n Life

Others0%

10%

20%

30%

40%

50%

60%

Response(%)

Analysis: People have taken policy from various companies leading in insurance business. 53% have taken policy of LIC, 19% of Bajaj Allianze, 17% Birla sun life and 11% other companies policy.

Q.8) Are you aware that there are special policies available for women?

Yes No

Variabl Response

45

e (%)YES 42%NO 58%

YES NO0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

42% 58% Response(%)

Analysis: Awareness of women insurance is relatively less as 58% people don’t know about women insurance. Only 42% people are aware about this policy.

Q.9) If Yes, do you have one?

Yes No

46

37%

63%

Response(%)

YESNO

Analysis: As awareness is not enough the number of policyholder is also less. Only 37% people have taken women insurance and remaining have not taken.

Q.10) If Yes, please mention the name.

Policy Name Response (%)LIC JEEVAN BHARTI 39%

Variable

Response(%)

YES 37%NO 63%

47

HDFC SMART WOMEN PLAN 33%Others 28%

39%

33%

28%

LICHDFC SMART WOMEN PLANOthers

Analysis: This is regarding the policyholder of women insurance. 39% have taken LIC Jeevan Bharti, 33% have taken HDFC Smart Women Plan and 28% belongs to others.

Q.11) If No, why have you not taken?

Analysis: Here in this question due to the lack of awareness of people regarding women insurance many of them have not taken policy. That said they have already taken another insurance policy and remaining said they are not interested.

48

Q.12) what is the benefit of this policy?

Analysis: As it is women insurance it gives large amount of benefits to them. When people invest somewhere of course they expect something in return. Here are benefits like benefits after retirement, it covers critical illness and there are some special benefits also like:

1. Enhanced Allocation Rate of 102.5% per annum from 11th policy year

2. Waiver of charges on withdrawal/Switch during motherhood. 12 partial withdrawals or switches will be waived, within one year from date of childbirth.

Q.13) How much premium do you pay?

Analysis: Premium is the most important aspect of insurance policy. Many of them pay monthly ranging between 5,000-7,000 quarterly ranging between 10,000-16,000 and yearly ranging between 20,000 and above.

Q.14) who pays the premium?

Self Spouse Husband

49

Self Spouse Husband0%

10%

20%

30%

40%

50%

60%

53%

27%20%

Analysis: The premium is paid by self is 53%, spouses paid premium of 27% and husbands pay premium of 20%.

Q.15) Are you aware of the benefits you get from women insurance policy?

Yes No

Particular Response (%)Self 53%Spouse 27%Husband 20%

50

Variables

Response(%)

YES 64%NO 36%

64%

36%

YESNO

Analysis: Here 64% people are aware about the benefits of women insurance policy and 36% people are not aware.

Q.17) Do you think that there should be improvement in the awareness of women insurance policy?

Yes

51

No

YES NO0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

94%

6%

Response(%)

Analysis: While talking about the improvement in the awareness 94% people said yes there should be improvement and 6% said no.

Q.17) what is your annual income?

Lower 1,00,000-2,00,000.Middle 2,10,000-4,000,000.

Variables Response (%)YES 94%NO 6%

52

Higher 4,100,00& Above.

Income Range Response (%)Lower 1,00,000-2,00,00 33%Middle 2,10,000-4,00,000 41%Higher 4,10,000 &Above 26%

33%

41%

26%

Lower 1,00,000-2,00,00Middle 2,10,000-4,00,000Higher 4,10,000 & Above

Analysis: Here 33% people belong to lower income group, 41% belongs to middle income group and 26% belongs to higher income group.

CHAPTER: 7

CONCLUSION

53

The existing research literature shows that while financial literacy is an important basis for effective financial decision-making there are significant differences by gender across a range of developed and developing countries.

People need insurance for a variety of reasons. In some cases insurance is required by law; however, there are policies that, though not mandatory to have, do give necessary protections should suffer a financial loss. And when people do have an insurance policy, there are certain rights and protections they have under law. Different stages of life will require different insurance needs, so it is important to review policies at least once a year to make sure that the best policy to fit one’s lifestyle.

Due to which working women’s as well as women who stay back at home suffers many problems. To empower the rights of women and ensuring the safety of women’s in India many insurance companies are taking initiative to improve the awareness of women insurance policy

Insurance companies have tied up with many other institutions to enhance their productivity as well as benefits associated with it.

Due to lack of awareness of women insurance policy many women’s are losing the opportunity associated with it.

Overall women are the beautiful gift of god. Their protection and safety is important which should be taken care each individual and citizens.

“HUMAN RIGHTS ARE WOMEN’S RIGHTS,

AND WOMEN RIGHTS ARE HUMAN RIGHTS”

-Hillary Clinton

CHAPTER: 8

RECOMMENDATION

54

As mentioned above there is lack of awareness of women insurance

policy the insurance companies should conduct seminars,

presentations, and awareness program.

It will ensure the greater productivity, profits, sales and income as

well as customer satisfaction.

The supervisors and managers need to explore the causes of the

dissatisfaction of women’s within the working environment.

The insurance companies must invest in and adopt strategy that will

help to increase productivity and women’s satisfaction.

The managers of the company should award and provides safety and

other special benefits to women’s working within the insurance

company.

BIBLIOGRAPHY

WWW.LIC.CO.IN

WWW.HDFC LIFE INSURANCE .COM

55

WWW.BAJAJ ALLIANZE.COM

WWW.TATA-AIG.COM

HTTP://WWW.MANAGEMENTSTUDYGUIDE.COM

WWW.SCRIBD SLIDESHARE.COM