Embed Size (px)

Citation preview

Employee Benefits

Anita Robinson, E.A., NTPI Fellow

360.719.9221

www.synergytax.net

2021

Anita Robinson has been in the accounting and tax preparation business for over than 20 years.

A Licensed Tax Consultant in Oregon since 1994 and an Enrolled Agent since 1996, an AdvancedCertified QuickBooks Pro Advisor since 2007, Anita has been a member of Intuit’s Advisor &Customer Council and has served as a Writing Committee Member for the Oregon Licensed TaxConsultants, Oregon Licensed Tax Preparers, as well as, the Enrolled Agents Exam.

Anita has taught tax classes for several local and nationwide organizations.

Taxable & Nontaxable Employee Benefits

Course Description

This course will give an overview of various employee fringe benefits. The subject matter includes taximplications of employee benefits and reporting requirements.

Learning Objectives

Identify different types of employee benefits, identify how to correctly report employee benefits andLearn to differentiate between who is an employee and who is not for benefit purposes.

DisclaimerSeminar materials are intended to stimulate thought and discussion and to provide attendees with useful ideas and

guidance in the areas of federal taxation. These materials, as well as, the comments of the instructor do not constitute and

should not be treated as tax advice regarding the use of any particular tax procedure, tax planning technique, or suggestion

or any consequences associated with them. This information is provided for educational purposes only.

Although the author has made every effort to ensure the accuracy of the materials, neither the author, nor the presenter

assumes any responsibility for any individual's reliance on the written or oral information presented during the

presentation. Each attendee should verify independently all statements made in the materials and during the seminar

presentation before applying them to a particular fact pattern and should determine independently the tax and other

consequences of using any particular technique or suggestion before recommending the same to a client or implementing

the same on a client's or on his or her own behalf.

These materials are the property of Anita Robinson and may not be used orcopied without her express written permission.

Employee Benefits

Table of Contents

I. Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

A. Cafeteria Plans IRC §125. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

B. Accident and Health Benefits §105. . . . . . . . . . . . . . . . . . . . . 6

C. Health Savings Accounts §223. . . . . . . . . . . . . . . . . . . . . . . . . . 7

D. Dependent Care Assistance §129. . . . . . . . . . . . . . . . . . . . . . 10

E. Flexible Spending Arrangements §125 . . . . . . . . . . . . . . . . . 11

F. Meals & Lodging §119. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

G. Transportation Benefits §132(f). . . . . . . . . . . . . . . . . . . . . . . 13

H. Achievement Awards §274(j)(4). . . . . . . . . . . . . . . . . . . . . . . 14

I. Athletic Facilities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

J. Health Reimbursement Arrangements §105(b). . . . . . . . . 16

ReferencesThe WebLibrary ‐ The TaxBook IncPublication 15‐B – Employer’s Tax Guide to Fringe BenefitsPublication 503 – Child and Dependent Care Expenses Publication 535 – Business ExpensesPublication 969 – Health Savings Accounts and other Tax Favored Health PlansPublication 970 ‐ Tax Benefits for EducationForm 8889 Health Savings Accounts and InstructionsForm 1099 SA and InstructionsSchedule A Instructions

I. Introduction

Under Internal Revenue Code §61 all employee compensation is taxable unlessspecifically excluded by law. Some compensation may be fully taxable, some nontaxableand some partially taxable.

Typically fringe benefits are only offered to common law employees.

C Corporation shareholders can generally take advantage of tax free benefits, butpartners in a partnership and more than 2% shareholders in an S‐Corporation cannotexclude most benefits from income.

More than 2% S‐Corporation shareholders for this purpose are treated as partners in apartnership (IRC §1372). Furthermore, family members are also considered 2%shareholders or partners. (IRC §318).

Some benefits are available tax free to volunteers and members of the board ofdirectors.

Nondiscrimination rules are designed to prevent business owners from taking tax freebenefits only for themselves without offering those same benefits to their employees.

If only key employees receive benefits the value of those benefits must be included intaxable income subject to all payroll taxes.

The terms highly compensated and key employee can have different meaningsdepending on the type of fringe benefit offered.

Please refer to the most recent IRS Publication 15‐B for the definition of highlycompensated and key employees.

Under an accountable plan all reimbursements are excluded from income if

1. there is a business purpose for the expense,

2. there is adequate accounting, and

3. any excess reimbursements are returned to the employer within a specified timeperiod.

Payments made under a non‐accountable plan are taxed as wages

Page 4 of 24

Nondiscrimination Rules Chart

Key Employees:Officer with annual pay of more than:2019 : $180,0002020 : $185,0005% owner‐employee1% owner‐employee with annual pay over $150,000

Group Term Life Insurance

Highly compensated employees:5% owner‐employee at any time during the current or precedingyearEmployee with annual pay in the preceding year of more than:2019 : $125,0002020 : $125,000You can choose to ignore test (2) if the employee wasn't also in the top 20% ofemployees when ranked by pay for the preceding year.

Adoption AssistanceDependent Care AssistanceEducational AssistanceEmployee DiscountsHealth Savings AccountsMeals at employer provided eatingfacilitiesNo additional cost service

Highly compensated employees:One of the five highest paid officersEmployee owning more than 10% of the employer’s stockHighest paid 25% of all employees

Self‐insured MedicalReimbursement Plans

Key Employees:Officer with an annual salary of more than:2019 : $180,0002020 : $185,0005% owner‐employee1% owner‐ employee with annual pay over $150,000

Highly compensated employees:Officer of corporationMore than 5% shareholderHighly‐compensated employee based on facts & circumstancesSpouse or dependent of above

Cafeteria Plans

Page 5 of 24

A. A cafeteria plan is a written plan, established by an employer to provide pretaxbenefits to employees.

Eligible employers may set up a Simple Cafeteria Plan for Small Businesses.

1. An eligible employer has an average of 100 or fewer employees during either ofthe two preceding years. If the plan is established while the employer is aneligible employer, it is considered an eligible plan in future years until the yearthe employer averages 200 or more employees.

2. All employees with at least 1000 hours of service in the preceding year areeligible to participate and may elect any benefit available under the plan.

3. The employer may exclude the following employees from the plan:

a. under age 21

b. less than 1 year of service

c. covered under a collective bargaining agreement

d. nonresident aliens working outside the US

4. For more detail please refer to Pub 15‐B and IRC §125.

B. Accident and Health Benefits

1. Contributions to an accident or health insurance plan are tax free to theemployee. The employer can pay for the cost or the employee can contributebefore tax money.

2. For this purpose the following are considered employees:

a. current common‐law employees

b. full time life insurance agents who are current statutory employees

c. retired employees

d. widows or widowers of retired employees or employees who died whileemployed

Page 6 of 24

3. 2% S‐Corporation shareholders do not qualify as employees, neither do partners.

4. S‐corporation shareholders need to add the cost of health insurance to box 1 oftheir W2, subject to federal and state withholding, but not subject to otherpayroll taxes, unless a state imposes payroll taxes on this benefit. The healthinsurance is then deducted on Form 1040 of the shareholder as an adjustment toincome.

5. Partners include the cost in guaranteed payments and should see a footnote onSchedule K‐1.

C. Health Savings Accounts (HSA) IRC §223

1. A health savings account is a tax exempt account owned by a qualified individualand set up with a qualified HSA trustee. It is used to pay for unreimbursedout‐of‐pocket medical expenses incurred by the taxpayer, spouse anddependents. It can also be used to pay for COBRA or Long‐term Care payments,as well as, health insurance for retirees.

a. The individual must be covered by a High Deductible Health Plan in order tocontribute to a Health Savings Account. If the high deductible plan isdiscontinued, the HSA will still be in place and distributions can be made, butcontributions are no longer allowed.

b. The employer, as well as the employee may make tax deductiblecontributions to a Health Savings Account. If the employer makescontributions, they are not taxed to the employee and should be noted inbox 12 of the W2 with code W.

2. There are limits for Health Savings Accounts:

a. Must be covered by a high deductible health plan (HDHP) and cannot beeligible for any other health insurance coverage.

b. A qualifying HDHP must have a deductible of at least a specified amount,indexed to inflation, for self‐only coverage and family coverage and

c. it must limit annual out‐of‐pocket expenses (deductibles, co‐payments andother amounts, but not premiums) to a specified amount, indexed toinflation, for self‐only coverage and for family coverage.

d. Joint accounts are not allowed.

Page 7 of 24

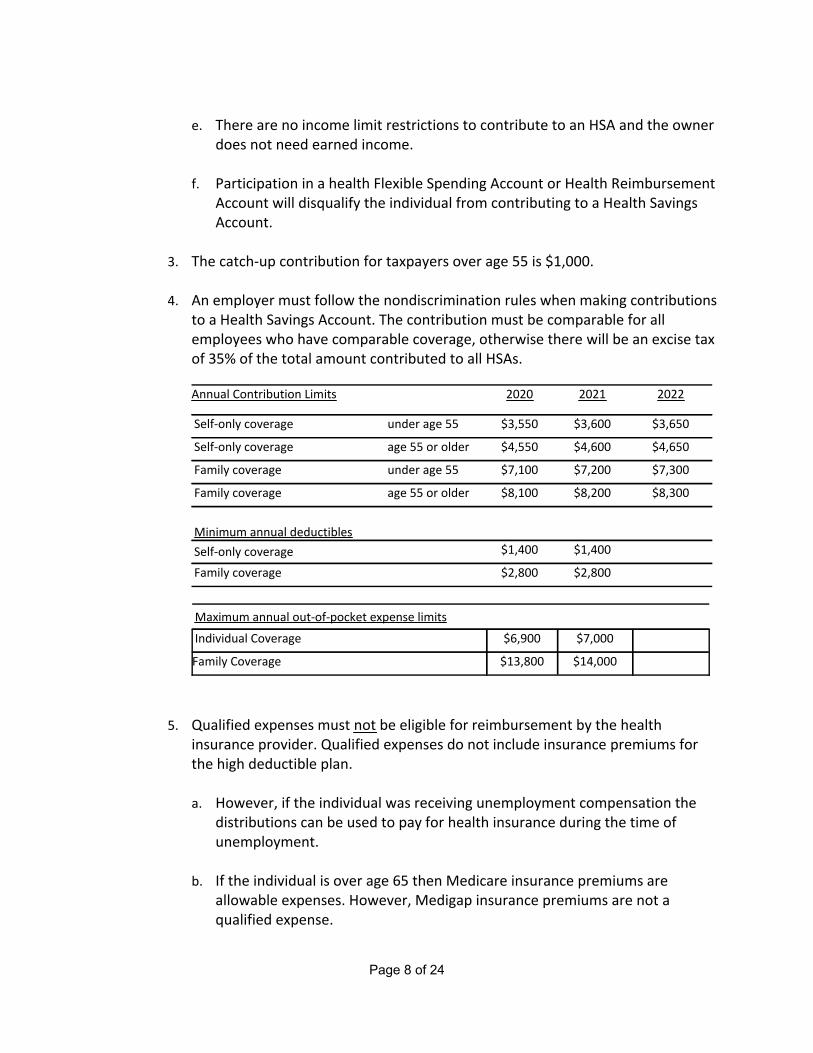

e. There are no income limit restrictions to contribute to an HSA and the ownerdoes not need earned income.

f. Participation in a health Flexible Spending Account or Health ReimbursementAccount will disqualify the individual from contributing to a Health SavingsAccount.

3. The catch‐up contribution for taxpayers over age 55 is $1,000.

4. An employer must follow the nondiscrimination rules when making contributionsto a Health Savings Account. The contribution must be comparable for allemployees who have comparable coverage, otherwise there will be an excise taxof 35% of the total amount contributed to all HSAs.

$2,800$2,800Family coverage

$1,400$1,400Self‐only coverage

Minimum annual deductibles

$8,300$8,200$8,100age 55 or olderFamily coverage

$7,300$7,200$7,100under age 55Family coverage

$4,650$4,600$4,550age 55 or olderSelf‐only coverage

$3,650$3,600$3,550under age 55Self‐only coverage

202220212020Annual Contribution Limits

$14,000$13,800Family Coverage

$7,000$6,900Individual Coverage

Maximum annual out‐of‐pocket expense limits

5. Qualified expenses must not be eligible for reimbursement by the healthinsurance provider. Qualified expenses do not include insurance premiums forthe high deductible plan.

a. However, if the individual was receiving unemployment compensation thedistributions can be used to pay for health insurance during the time ofunemployment.

b. If the individual is over age 65 then Medicare insurance premiums areallowable expenses. However, Medigap insurance premiums are not aqualified expense.

Page 8 of 24

c. Insurance premiums for long‐term care insurance are also a qualifiedexpense.

6. Contributions are not allowed once the taxpayer turns age 65.

7. Qualified expenses are medical expenses that would otherwise be deductible onSchedule A under IRC §213. See IRS Publication 502.

8. Funds remaining at the end of the year carry over to the next year. Theparticipant is fully vested at all times.

9. Expenses paid with Health Savings Account funds cannot be used as a deductiblemedical expense on Schedule A of the tax return.

10. Distributions used for nonmedical purposes are subject to a 20% penalty, unlessthe participant has reached age 65 or is deceased.

11. Partners and 2% S‐Corporation shareholders are not eligible for pretax HSAcontributions. These employer contributions would be included in income, eitheras guaranteed payments for partners or box 1 wages for 2% S‐Corporationshareholders. However, partners and S‐Corporation shareholders can contributeto their own personal HSA outside of the business.

12. Employer HSA contributions are reported on Form W2 box 12 with code W. Theamount coded W also includes pretax employee contributions. Distributions arereported by the custodian on form 1099‐SA.

13. If the HSA participant dies and the spouse is the beneficiary, the spouse istreated as the participant in the HSA. If someone other than the spouse inheritsthe HSA the fair market value is taxable to the beneficiary. Any taxable amount isreduced by qualified medical expenses paid within one year after the date ofdeath.

14. Earned income is not required to contribute to an HSA.

For more information please refer to IRS Publication 969, Health Savings Accounts andthe instructions to Form 8889.

Page 9 of 24

D. Dependent Care Benefits IRC §129

1. Up to $5,000 ($2,500 MFS) can be set aside for dependent care expenses eitheras a pretax benefit or funded fully or partially by the employer. Benefitsprovided to more than 5% S‐Corporation shareholders and partners in apartnership cannot exceed 25% of the total paid by the employer for allemployees (IRC 129 (a)(4)).

2. The following are treated as employees for this benefit:

a. current employees

b. leased employees

c. a sole proprietor

d. a partner who performs services for a partnership

3. A sole proprietor can set up a dependent care benefit plan and pay for his/herown daycare expenses through the business.

4. Highly compensated employees do not qualify for the exclusion from incomeunless the benefits do not favor highly compensated employees. Highlycompensated for this purpose is anyone owning 5% or more of the company oranyone who received more than $120,000 in the prior year.

5. Consolidated Appropriations Act, 2021

a. Unused benefits from a 2020 plan year may carry over to a 2021 plan year.Unused benefits from a 2021 plan year may carry over to 2022.

b. As an alternative, the employer may extend the claims period for a 2020 or2021 plan year by 12 months after the end of the plan year.

Example:

The employee elects $5,000 for the 2020 plan but incurs no daycare expenses. Theemployer’s FSA allows for the carryover from the 2020 plan year to the 2021 planyear. In 2021 the employee elects $10,500 of pretax benefits and incurs a total of$15,500 of daycare expenses. The entire amount is excluded from income.

6. The American Rescue Plan Act of 2021 increased the limit to $10,500 MFJ and$5,250 for MFS.

For more information refer to IRS Publication 503, Child and Dependent Care Expenses and theinstructions to Form 2441 and IRS Notices 2021‐15 and 2021‐26.

Page 10 of 24

E. Flexible Spending Arrangements (FSA) IRC §125

1. Flexible Spending Arrangements (FSA’s) allow employees to choose whichbenefit they would like to take advantage of and exclude from income to be usedfor medical or dependent care expenses. A Flexible Spending Arrangement canbe funded by pretax salary reduction, employer contributions or a combinationof both.

2. Employees must be covered by an employer sponsored group health plan for amedical FSA.

a. The employer must have a written plan.

b. Employees may be able to choose between qualified nontaxable benefits ortaxable cash.

3. Employees may set aside up to $2,750 for 2020 and 2021 for a medical FlexibleSpending Account.

4. After tax year 2012 the employer may adopt a $500 carryover provision formedical FSA’s which allows the employees to carry $500 over to the next yearfor expenses incurred in that next year. This does not reduce the available salarydeduction for the following year. However, if the $500 rule has been establisheda grace period cannot be used.

5. In lieu of the $500 rule the plan may adopt a grace period which permits anyunused funds to be used by March 15 of the following year for expenses incurredeither in the prior year or the current plan year.

6. Distributions can only be used for qualified medical expenses. Those areexpenses that would qualify to be deducted on Schedule A. The taxpayer thenmust reduce any medical expenses by the amount reimbursed by the FlexibleSpending Account.

7. Employees are allowed to withdraw the entire pretax amount before they havefully funded the FSA with salary reductions.

8. Due to COVID midyear changes were allowed in 2020.

Page 11 of 24

F. Meals and Lodging IRC §119

1. Lodging may be excluded from wages if provided on the employer’s premisesand is for the convenience of the employer and it is a condition of the job.

2. Meals may be excluded from income if they are:

a. furnished on the employers premises, and

b. are for the convenience of the employer.

3. Beginning in 2018 qualified employee meals are 50% deductible. After 2025 theyare not deductible to the employer.

4. Everyone receiving this benefit is treated as an employee, except highlycompensated employees who eat free at an employer provided facility that is notavailable to all employees on the same terms. In that case the cost of the meal isincluded in wages.

5. Meals on the employer’s business premises and for the employer’s convenienceare not taxable compensation under the following conditions:

a. If more than half of employees receive meals for the employer’s conveniencethen all employee meals are excluded from wages.

b. Meals for food service employees provided during or immediately before orafter working hours are considered for the employer’s convenience.

c. When employees have to be available for emergency calls during mealperiods employer provided meals may be considered as furnished for theemployer’s convenience. Facts and circumstances dictate the taxability.

d. Meals provided by the employer because proper meals are not otherwiseavailable, for example there are very few eating establishments near theworkplace.

e. When the meal periods are too short to go eat anywhere else.

6. This exclusion does NOT apply to 2% shareholders

7. After 2025 no deduction for meals will be allowed.

8. De minimis meals, such as coffee, donuts, soft drinks or occasional meals to workovertime are excludable from income and 50% deductible to the employer.Anyone receiving de minimis meals is considered an employee.

9. The cost for employee picnics and parties are 100% deductible.

10. Consolidated Appropriations Act, 2021 added IRC §274(n)(2)(D). (IRS Notice2021‐25)

Page 12 of 24

a. Meals at restaurants are 100% deductible

b. Meals at non‐restaurant businesses are 50% deductible

Tax Professional Note:

In Oregon, meals and lodging are subject to unemployment tax, except when providedfor agricultural labor or domestic service or are reimbursable travel expenses. (OAR471‐31‐020)

Meals are also subject to withholding and transit taxes unless furnished for theconvenience of the employer and provided on the employer’s premises. (OAR150‐316.162(2)‐(A))

Lodging is subject to both withholding and transit taxes, unless furnished on theemployer’s premises, for the employer’s convenience and as condition of employment.

G. Transportation Benefits IRC §132(f)

1. Certain transportation benefits can be excluded from income.

2. These benefits can be paid directly by the employer or reimbursed through anaccountable plan.

3. Transit passes of up to $270 per month for 2020 and 2021 are excludable fromwages. However, the employer cannot deduct the expense.

4. Parking reimbursement at the business location of up to $270 per month for2020 and 2021 is excludable from income, but not deductible to the employer.

5. Transportation benefits also include reimbursements for bicycle commuting ofup to $20 per month for each qualified bicycle commuting month. A qualifiedbicycle commuting month is any month in which the employee regularly uses hisor her bicycle for a substantial portion of travel between the employee’s homeand the place of employment and the employee does not receive any othertransportation benefit for that month. Receipts are not required.

After 2017 this benefit is taxable to the employee.

6. Self‐employed individuals, partners and 2% S‐Corporation shareholders do notqualify for transportation benefits. Do not treat the benefit as an increase indistributions to the 2% shareholder, it is an addition to wages.

Page 13 of 24

7. De minimis transportation benefits up to $21 per month can be excluded fromemployee wages and are deductible by the employer.

8. Nondiscrimination rules do not apply.

9. Frequent Flyer Miles

a. The tax treatment of frequent flyer or similar programs has been infrequentlyaddressed by the Internal Revenue Service. It could be argued that theawards are excludable from income to the employees as working conditionfringe benefits. Even though the employer did not directly provide thebenefit, the employer did pay the original travel expenses that caused theissuance of the award. Although the IRS has attempted to tax these benefits(see P.J. Charley), especially in cases where the employer pays for milesearned by its employees, it indicated following the release of IRS LetterRuling 9547001 that it has no special enforcement program for frequent flyermiles.

b. Announcement 2002‐18 specifically addresses frequent flyer miles. Itindicates that the IRS does not plan to pursue enforcement:

“The IRS will not assert that any taxpayer has understated his federal taxliability by reason of the receipt or personal use of frequent flyer miles.”

The announcement deals only with frequent flyer miles a taxpayer earnsfrom business or official travel, not with frequent flyer miles given to ataxpayer as part of a product promotion. Consistent with prior unofficialpolicy, frequent flyer miles earned as the result of business or governmenttravel are not be used in determining taxable income.

c. However, the conversion into cash of frequent flier miles earned duringbusiness is taxable as wages. P.J. Charley vs Commissioner 96‐2USTC (9thCircuit)

H. Achievement Awards IRC §274(j)(4)

1. Awards for length of service or safety achievements are excludable from incomeas long as they are personal property and do not exceed $1,600 in fair marketvalue per calendar year under a qualified plan or $400 under a non‐qualifiedplan.

2. The award must be given for length of service or safety and must be awarded aspart of a presentation and cannot be disguised as wages.

Page 14 of 24

3. Cash and cash equivalents, such as gift certificates, event tickets, etc. are taxablecompensation. Prizes won at random drawings or awards for job performancesuch as employee of the month awards are also taxable compensation.

4. After 12/31/2017 nontaxable achievement awards can no longer include thefollowing:

a. cash & cash equivalents

b. gift cards, gift coupons and certificates

c. vacations

d. meals

e. lodging

f. tickets to theater or sporting events

5. All the following are considered employees for this benefit:

a. current employees

b. former common‐law employees the employer maintains coverage for basedon an agreement relating to prior service

c. leased employees who have worked for the employer for a least one year ona substantially full time basis

6. More than 2% S Corporation shareholders are not considered employees.

7. Safety awards given to managers, clerical workers, administrators or professionalemployees are taxable compensation.

8. In addition, if more than 10% of employees have already received a safety award,then any additional awards will be taxable as wages.

Page 15 of 24

I. Athletic Facilities IRC §132(j)(4)

1. The use of fitness facilities on the employer’s premises is a tax‐free benefit.

2. The following are considered employees for this benefit:

a. current employees

b. former employees who retired or left on disability

c. widows of an employee

d. widows of a former employee who retired or left on disability

e. leased employees

f. partners who performs services for the partnership

g. 2% shareholders of an S‐Corporation

J. Health Reimbursement Arrangement (HRA) IRC §105(b)

1. The Qualified Small Employer HRA option took effect January 1, 2017 foremployers with fewer than 50 employees, that do not offer health coverageplans to their workers.

a. Employees under the age of 25 and those who have not worked for theemployer for at least three years can be excluded.

b. There is no minimum or maximum requirement for out‐of‐pocketdeductibles.

c. The employer may set limits lower than IRS limits.

d. Distributions are tax‐free if used for qualified medical expenses.

e. Distributions for nonmedical purposes are subject to a 20% penalty

2. Rules for Qualified Small Employer Health Reimbursement Arrangements:

a. Employer annual contributions for 2020 are capped at $5,250 for a singleemployee and $10,600 for an employee with a family. These numbers areindexed for inflation. For 2021 the limits are $5,300 and $10,700.

Page 16 of 24

b. Participation in a Qualified Small Employer Health ReimbursementArrangement will not disqualify participants from Marketplace subsidies,but monthly HRA reimbursements will be included in income calculationsfor determining eligibility for any subsidy.

c. Generally, employers must make the same contributions to all eligibleemployees; amounts may vary based on family status.

d. Employees must have minimum essential coverage in order to participate.They must fill out an attestation and show proof of coverage to theemployer.

e. HRAs are solely funded by an eligible employer.

f. HRAs are not pre‐funded.

g. Out‐of‐pocket medical expenses can be written off beginning the first ofthe month in which the small business owner establishes the QSEHRA.

h. Unused amounts can be carried over to reimburse medical expenses infuture years or can be offered as a use it or lose it feature.

i. Medical expenses of adult children may be reimbursed through anemployee’s HRA as long as the child is under age 27 at the end of theyear.

j. The HRA amount will be reported on Form W2 with code FF.

3. On June 13, 2019, the Internal Revenue Service, the Department of Labor andthe Department of Health and Human Services issued final rules regardingIndividual Coverage Health Reimbursement Arrangements (ICHRA) and otheraccount‐based group health plans. Specifically, the final rules allow HRAs andother account‐based group health plans to be integrated with individualhealth insurance coverage or Medicare, if certain conditions are satisfied (anindividual coverage HRA).

a. Employers will have more flexibility setting up HRAs beginning 1/1/2020.

i. Combine with §125 Plans

ii. With group health insurance

iii. With individual health insurance

b. Participants must be covered by a health insurance plan that coverspreventive care and has no annual or lifetime limit.

Page 17 of 24

c. Participants may opt out.

d. Employers have notification requirements.

e. Participants are not allowed to receive premium tax credits if they obtainhealth insurance through the Marketplace.

f. For more information go to:

https://www.irs.gov/newsroom/health‐reimbursement‐arrangements‐hras

4. Excepted Benefit HRAs can be offered beginning 1/1/2020 by employers whoprovide traditional group health insurance to their employees. The annuallimit is $1,800 for tax years 2020 and 2021.

a. Excepted benefits are those that are not covered under a traditionalhealth insurance plan:

i. Accident‐only coverage

ii. Disability insurance

iii. Dental coverage

iv. Vision coverage

v. Specific disease or illness coverage

vi. Copays and deductibles not covered by group insurance

Page 18 of 24

Page 6 of 34 Fileid: … tions/P15B/2021/A/XML/Cycle06/source 11:55 - 5-Feb-2021The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

• Contributions to a separate trust or fund that directly or through insurance provides accident or health ben-efits.

• Contributions to Archer MSAs or HSAs (discussed in Pub. 969).

This exclusion also applies to payments you directly or indirectly make to an employee under an accident or health plan for employees that are either of the following.

• Payments or reimbursements of medical expenses.• Payments for specific permanent injuries (such as the

loss of the use of an arm or leg). The payments must be figured without regard to the period the employee is absent from work.

Accident or health plan. This is an arrangement that provides benefits for your employees, their spouses, their dependents, and their children (under age 27 at the end of the tax year) in the event of personal injury or sickness. The plan may be insured or noninsured and doesn't need to be in writing.Employee. For this exclusion, treat the following individ-uals as employees.

• A current common-law employee.• A full-time life insurance agent who is a current statu-

tory employee.• A retired employee.

Table 2-1. Special Rules for Various Types of Fringe Benefits(For more information, see the full discussion in this section.)

Treatment Under Employment TaxesType of Fringe Benefit Income Tax Withholding Social Security and Medicare

(including Additional Medicare Tax when wages are paid in

excess of $200,000)1

Federal Unemployment (FUTA)

Accident and health benefitsExempt,2 except for long-term care benefits provided through a flexible spending or similar arrangement.

Exempt, except for certain payments to S corporation employees who are 2% shareholders.

Exempt

Achievement awards Exempt2 up to $1,600 for qualified plan awards ($400 for nonqualified awards).Adoption assistance Exempt2,3 Taxable Taxable

Athletic facilities Exempt if substantially all use during the calendar year is by employees, their spouses, and their dependent children, and the facility is operated by the employer on premises owned or leased by the employer.

De minimis (minimal) benefits Exempt Exempt ExemptDependent care assistance Exempt3 up to certain limits, $5,000 ($2,500 for married employee filing separate return).Educational assistance Exempt up to $5,250 of benefits each year. (See Educational Assistance, later in this section.)Employee discounts Exempt3 up to certain limits. (See Employee Discounts, later in this section.)Employee stock options See Employee Stock Options, later in this section.Employer-provided cell phones Exempt if provided primarily for noncompensatory business purposes.

Group-term life insurance coverageExempt Exempt2,4,6 up to cost of $50,000 of

coverage. (Special rules apply to former employees.)

Exempt

Health savings accounts (HSAs) Exempt for qualified individuals up to the HSA contribution limits. (See Health Savings Accounts, later in this section.)

Lodging on your business premises Exempt2 if furnished on your business premises, for your convenience, and as a condition of employment.

Meals Exempt2 if furnished on your business premises for your convenience.Exempt if de minimis.

No-additional-cost services Exempt3 Exempt3 Exempt3

Retirement planning services Exempt5 Exempt5 Exempt5

Transportation (commuting) benefitsExempt2 up to certain limits if for rides in a commuter highway vehicle and/or transit passes ($270) or qualified parking ($270). (See Transportation (Commuting) Benefits, later in this section.)Exempt if de minimis.

Tuition reduction Exempt3 if for undergraduate education (or graduate education if the employee performs teaching or research activities).

Working condition benefits Exempt Exempt Exempt1 Or other railroad retirement taxes, if applicable.2 Exemption doesn't apply to S corporation employees who are 2% shareholders. 3 Exemption doesn't apply to certain highly compensated employees under a program that favors those employees.4 Exemption doesn't apply to certain key employees under a plan that favors those employees.5 Exemption doesn't apply to services for tax preparation, accounting, legal, or brokerage services.6 You must include in your employee's wages the cost of group-term life insurance beyond $50,000 worth of coverage, reduced by the amount the employee paid toward the insurance. Report it as wages in boxes 1, 3, and 5 of the employee's Form W-2. Also, show it in box 12 with code “C.” The amount is subject to social security and Medicare taxes, and you may, at your option, withhold federal income tax.

Page 6 Publication 15-B (2021)

Page 41 of 50 Fileid: … ations/P15/2021/A/XML/Cycle07/source 14:20 - 4-Feb-2021The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

15. Special Rules for Various Types of Services and PaymentsSection references are to the Internal Revenue Code unless otherwise noted.

Special Classes of Employment and Special Types of Payments

Treatment Under Employment Taxes

Income Tax Withholding Social Security and Medicare (including

Additional Medicare Tax when wages are paid in

excess of $200,000)

FUTA

Aliens, nonresident. See Pub. 515 and Pub. 519.Aliens, resident:1. Service performed in the U.S. Same as U.S. citizen. Same as U.S. citizen.

(Exempt if any part of service as crew member of foreign vessel or aircraft is performed outside U.S.)

Same as U.S. citizen.

2. Service performed outside the U.S. Withhold Taxable if (1) working for an American employer, or (2) an American employer by agreement covers U.S. citizens and residents employed by its foreign affiliates.

Exempt unless on or in connection with an American vessel or aircraft and either performed under contract made in U.S., or alien is employed on such vessel or aircraft when it touches U.S. port.

Cafeteria plan benefits under section 125. If employee chooses cash, subject to all employment taxes. If employee chooses another benefit, the treatment is the same as if the benefit was provided outside the plan. See Pub. 15-B for more information.

Deceased worker:1. Wages paid to beneficiary or estate in

same calendar year as worker's death. See the General Instructions for Forms W-2 and W-3 for details.

Exempt Taxable Taxable

2. Wages paid to beneficiary or estate after calendar year of worker's death.

Exempt Exempt Exempt

Dependent care assistance programs. Exempt to the extent it is reasonable to believe amounts are excludable from gross income under section 129.

Disabled worker's wages paid after year in which worker became entitled to disability insurance benefits under the Social Security Act.

Withhold Exempt if worker didn't perform any service for employer during the period for which payment is made.

Taxable

Employee business expense reimbursement:1. Accountable plan.

a. Amounts not exceeding specified government rate for per diem or standard mileage.

Exempt Exempt Exempt

b. Amounts in excess of specified government rate for per diem or standard mileage.

Withhold Taxable Taxable

2. Nonaccountable plan. See section 5 for details.

Withhold Taxable Taxable

Family employees:1. Child employed by parent (or

partnership in which each partner is a parent of the child).

Withhold Exempt until age 18; age 21 for domestic service.

Exempt until age 21

2. Parent employed by child. Withhold Taxable if in course of the son's or daughter's business. For domestic services, see section 3.

Exempt

3. Spouse employed by spouse. Withhold Taxable if in course of spouse's business.

Exempt

See section 3 for more information.Fishing and related activities. See Pub. 334.Foreign governments and international organizations.

Exempt Exempt Exempt

Publication 15 (2021) Page 41

Page 42 of 50 Fileid: … ations/P15/2021/A/XML/Cycle07/source 14:20 - 4-Feb-2021The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Special Classes of Employment and Special Types of Payments

Treatment Under Employment Taxes

Income Tax Withholding Social Security and Medicare (including

Additional Medicare Tax when wages are paid in

excess of $200,000)

FUTA

Foreign service by U.S. citizens:1. As U.S. Government employees. Withhold Same as within U.S. Exempt2. For foreign affiliates of American

employers and other private employers.Exempt if at time of payment (1) it is reasonable to believe employee is entitled to exclusion from income under section 911, or (2) the employer is required by law of the foreign country to withhold income tax on such payment.

Exempt unless (1) an American employer by agreement covers U.S. citizens employed by its foreign affiliates, or (2) U.S. citizen works for American employer.

Exempt unless (1) on American vessel or aircraft and work is performed under contract made in U.S. or worker is employed on vessel when it touches U.S. port, or (2) U.S. citizen works for American employer (except in a contiguous country with which the U.S. has an agreement for unemployment compensation) or in the U.S. Virgin Islands.

Fringe benefits. Taxable on excess of fair market value of the benefit over the sum of an amount paid for it by the employee and any amount excludable by law. However, special valuation rules may apply. Benefits provided under cafeteria plans may qualify for exclusion from wages for social security, Medicare, and FUTA taxes. See Pub. 15-B for details.

Government employment:State/local governments and political subdivisions, employees of:1. Salaries and wages (includes payments

to most elected and appointed officials). See chapter 3 of Pub. 963.

Withhold Generally, taxable for (1) services performed by employees who are either (a) covered under a section 218 agreement, or (b) not covered under a section 218 agreement and not a member of a public retirement system (mandatory social security and Medicare coverage); and (2) (for Medicare tax only) for services performed by employees hired or rehired after March 31, 1986, who aren't covered under a section 218 agreement or the mandatory social security provisions, unless specifically excluded by law. See Pub. 963.

Exempt

2. Election workers. Election individuals are workers who are employed to perform services for state or local governments at election booths in connection with national, state, or local elections.

Exempt Taxable if paid $2,000 or more in 2021 (lesser amount if specified by a section 218 social security agreement). See Revenue Ruling 2000-6.

Exempt

Note. File Form W-2 for payments of $600 or more even if no social security or Medicare taxes were withheld.

3. Emergency workers. Emergency workers who were hired on a temporary basis in response to a specific unforeseen emergency and aren't intended to become permanent employees.

Withhold Exempt if serving on a temporary basis in case of fire, storm, snow, earthquake, flood, or similar emergency.

Exempt

U.S. federal government employees. Withhold Taxable for Medicare. Taxable for social security unless hired before 1984. See section 3121(b)(5).

Exempt

Page 42 Publication 15 (2021)

Page 43 of 50 Fileid: … ations/P15/2021/A/XML/Cycle07/source 14:20 - 4-Feb-2021The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Special Classes of Employment and Special Types of Payments

Treatment Under Employment Taxes

Income Tax Withholding Social Security and Medicare (including

Additional Medicare Tax when wages are paid in

excess of $200,000)

FUTA

Homeworkers (industrial, cottage industry):1. Common law employees. Withhold Taxable Taxable2. Statutory employees. See section 2 for

details.Exempt Taxable if paid $100 or

more in cash in a year.Exempt

Hospital employees:1. Interns. Withhold Taxable Exempt2. Patients. Withhold Taxable (Exempt for state

or local government hospitals.)

Exempt

Household employees:1. Domestic service in private homes. Exempt (withhold if both

employer and employee agree).

Taxable if paid $2,300 or more in cash in 2021. Exempt if performed by an individual under age 18 during any portion of the calendar year and isn't the principal occupation of the employee.

Taxable if employer paid total cash wages of $1,000 or more in any quarter in the current or preceding calendar year.

2. Domestic service in college clubs, fraternities, and sororities.

Exempt (withhold if both employer and employee agree).

Exempt if paid to regular student; also exempt if employee is paid less than $100 in a year by an income-tax-exempt employer.

Taxable if employer paid total cash wages of $1,000 or more in any quarter in the current or preceding calendar year.

Insurance for employees:1. Accident and health insurance

premiums under a plan or system for employees and their dependents generally or for a class or classes of employees and their dependents.

Exempt (except 2% shareholder-employees of S corporations).

Exempt Exempt

2. Group-term life insurance costs. See Pub. 15-B for details.

Exempt Exempt, except for the cost of group-term life insurance includible in the employee's gross income. Special rules apply for former employees.

Exempt

Insurance agents or solicitors:1. Full-time life insurance salesperson. Withhold only if employee

under common law. See section 2.

Taxable Taxable if (1) employee under common law, and (2) not paid solely by commissions.

2. Other salesperson of life, casualty, etc., insurance.

Withhold only if employee under common law.

Taxable only if employee under common law.

Taxable if (1) employee under common law, and (2) not paid solely by commissions.

Interest on loans with below-market interest rates (foregone interest and deemed original issue discount).

See Pub. 15-A.

Leave-sharing plans: Amounts paid to an employee under a leave-sharing plan.

Withhold Taxable Taxable

Newspaper carriers and vendors: Newspaper carriers under age 18; newspaper and magazine vendors buying at fixed prices and retaining receipts from sales to customers. See Pub. 15-A for information on statutory nonemployee status.

Exempt (withhold if both employer and employee voluntarily agree).

Exempt Exempt

Publication 15 (2021) Page 43

Page 44 of 50 Fileid: … ations/P15/2021/A/XML/Cycle07/source 14:20 - 4-Feb-2021The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Special Classes of Employment and Special Types of Payments

Treatment Under Employment Taxes

Income Tax Withholding Social Security and Medicare (including

Additional Medicare Tax when wages are paid in

excess of $200,000)

FUTA

Noncash payments:1. For household work, agricultural labor,

and service not in the course of the employer's trade or business.

Exempt (withhold if both employer and employee voluntarily agree).

Exempt Exempt

2. To certain retail commission salespersons ordinarily paid solely on a cash commission basis.

Optional with employer, except to the extent employee's supplemental wages during the year exceed $1 million.

Taxable Taxable

Nonprofit organizations. See Pub. 15-A.Officers or shareholders of an S corporation: Distributions and other payments by an S corporation to a corporate officer or shareholder must be treated as wages to the extent the amounts are reasonable compensation for services to the corporation by an employee. See the Instructions for Form 1120-S.

Withhold Taxable Taxable

Partners: Payments to general or limited partners of a partnership. See Pub. 541 for partner reporting rules.

Exempt Exempt Exempt

Railroads: Payments subject to the Railroad Retirement Act. See Pub. 915 and the Instructions for Form CT-1 for more details.

Withhold Exempt Exempt

Religious exemptions. See Pub. 15-A and Pub. 517.Retirement and pension plans:1. Employer contributions to a qualified

plan.Exempt Exempt Exempt

2. Elective employee contributions and deferrals to a plan containing a qualified cash or deferred compensation arrangement (401(k)).

Generally exempt, but see section 402(g) for limitation.

Taxable Taxable

3. Employer contributions to individual retirement accounts under simplified employee pension (SEP) plan.

Generally exempt, but see section 402(g) for salary reduction SEP limitation.

Exempt, except for amounts contributed under a salary reduction SEP agreement.

4. Employer contributions to section 403(b) annuities including salary reduction contributions.

Generally exempt, but see section 402(g) for limitation.

Taxable if paid through a salary reduction agreement (written or otherwise).

5. Employee salary reduction contributions to a SIMPLE retirement account.

Exempt Taxable Taxable

6. Distributions from qualified retirement and pension plans and section 403(b) annuities. See Pub. 15-A for information on pensions, annuities, and employer contributions to nonqualified deferred compensation arrangements.

Withhold, but recipient may elect exemption on Form W-4P in certain cases; mandatory 20% withholding applies to an eligible rollover distribution that isn't a direct rollover; exempt for direct rollover. See Pub. 15-A.

Exempt Exempt

7. Employer contributions to a section 457(b) plan.

Generally exempt, but see section 402(g) limitation.

Taxable Taxable

8. Employee salary reduction contributions to a section 457(b) plan.

Generally exempt, but see section 402(g) salary reduction limitation.

Taxable Taxable

Salespersons:1. Common law employees. Withhold Taxable Taxable2. Statutory employees. Exempt Taxable Taxable, except for full-time

life insurance sales agents.3. Statutory nonemployees (qualified real

estate agents, direct sellers, and certain companion sitters). See Pub. 15-A for details.

Exempt Exempt Exempt

Page 44 Publication 15 (2021)

Page 45 of 50 Fileid: … ations/P15/2021/A/XML/Cycle07/source 14:20 - 4-Feb-2021The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Special Classes of Employment and Special Types of Payments

Treatment Under Employment Taxes

Income Tax Withholding Social Security and Medicare (including

Additional Medicare Tax when wages are paid in

excess of $200,000)

FUTA

Scholarships and fellowship grants (includible in income under section 117(c)).

Withhold Taxability depends on the nature of the employment and the status of the organization. See Students, scholars, trainees, teachers, etc., below.

Severance or dismissal pay. Withhold Taxable TaxableService not in the course of the employer's trade or business (other than on a farm operated for profit or for household employment in private homes).

Withhold only if employee earns $50 or more in cash in a quarter and works on 24 or more different days in that quarter or in the preceding quarter.

Taxable if employee receives $100 or more in cash in a calendar year.

Taxable only if employee earns $50 or more in cash in a quarter and works on 24 or more different days in that quarter or in the preceding quarter.

Sick pay. See Pub. 15-A for more information. Withhold Exempt after end of 6 calendar months after the calendar month employee last worked for employer.

Students, scholars, trainees, teachers, etc.:1. Student enrolled and regularly attending

classes, performing services for the following.a. Private school, college, or

university.Withhold Exempt Exempt

b. Auxiliary nonprofit organization operated for and controlled by school, college, or university.

Withhold Exempt unless services are covered by a section 218 (Social Security Act) agreement.

Exempt

c. Public school, college, or university.

Withhold Exempt unless services are covered by a section 218 (Social Security Act) agreement.

Exempt

2. Full-time student performing service for academic credit, combining instruction with work experience as an integral part of the program.

Withhold Taxable Exempt unless program was established for or on behalf of an employer or group of employers.

3. Student nurse performing part-time services for nominal earnings at hospital as incidental part of training.

Withhold Exempt Exempt

4. Student employed by organized camps. Withhold Taxable Exempt5. Student, scholar, trainee, teacher, etc.,

as nonimmigrant alien under section 101(a)(15)(F), (J), (M), or (Q) of Immigration and Nationality Act (that is, aliens holding F-1, J-1, M-1, or Q-1 visas).

Withhold unless excepted by regulations.

Exempt if service is performed for purpose specified in section 101(a)(15)(F), (J), (M), or (Q) of Immigration and Nationality Act. However, these taxes may apply if the employee becomes a resident alien. See the special residency tests for exempt individuals in chapter 1 of Pub. 519.

Supplemental unemployment compensation plan benefits.

Withhold Exempt under certain conditions. See Pub. 15-A.

Tips:1. If $20 or more in a month. Withhold Taxable Taxable for all tips reported

in writing to employer.2. If less than $20 in a month. See section

6 for more information.Exempt Exempt Exempt

Worker's compensation. Exempt Exempt Exempt

Publication 15 (2021) Page 45