Embed Size (px)

Citation preview

Work Sheet, Financial Statements, and Adjusting Entries

© Paradigm Publishing, Inc. 1

Chapter 6 & 7

1. Prepare three basic financial statements.

2. Explain the need for adjusting entries.

3. Make adjusting entries for supplies used, expired insurance, depreciation, and unpaid wages.

4. Complete a work sheet for a service business.

5. Prepare financial statements from a work sheet.

6. Journalize and post adjusting entries.

© Paradigm Publishing, Inc. 2

Learning Objectives

Learning Objective 1

© Paradigm Publishing, Inc. 3

Prepare three basic financial statements

Financial Statements

Summaries of financial activities

Used to communicate important accounting information to users

The three basic types:Income Statement

Statement of Owner’s Equity

Balance Sheet

© Paradigm Publishing, Inc. 4

Financial Statements

© Paradigm Publishing, Inc. 5

Financial Statements

Income StatementA summary of a business’s revenue and expenses for a specific period of time, such as a month or year

Statement of Owner’s Equity A summary of the changes that have occurred in owner’s equity during a specific period of time

Balance SheetA listing of a firm’s assets, liabilities, and owner’s equity at a specific point in time

© Paradigm Publishing, Inc. 6

© Paradigm Publishing, Inc. 7

Salaries expense would appear on a firm’s

Quick Check

a. statement of owner’s equity.

b. balance sheet.

c. income statement.

d. balance sheet and statement of owner’s equity.

e. balance sheet and income statement.

Relationships Among Statements

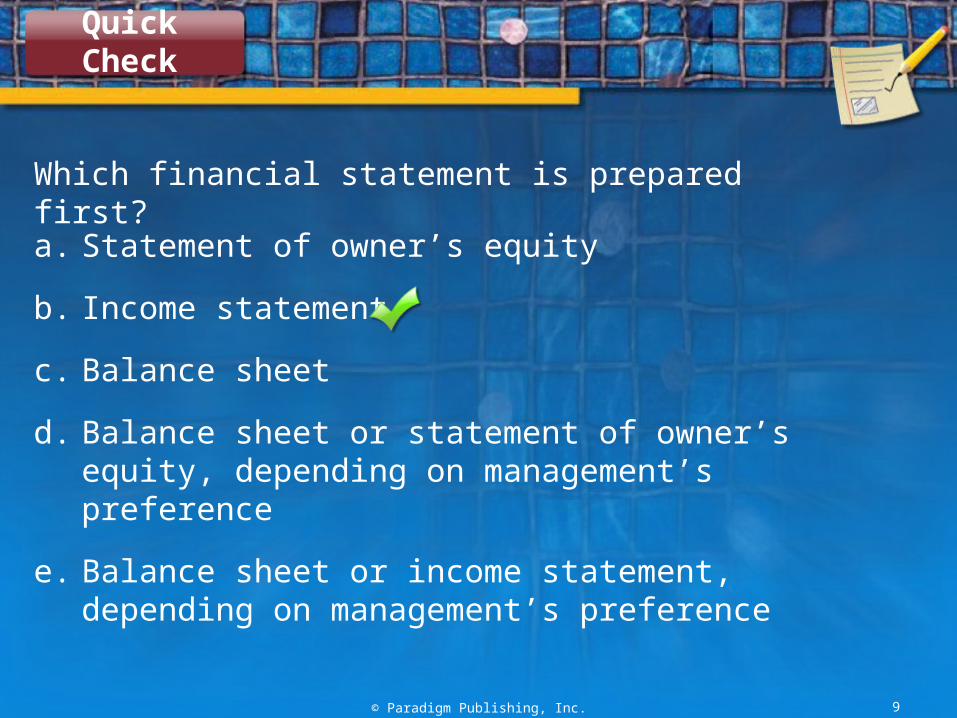

Income StatementPrepared first

To determine a firm’s net income

Net Income Is shown on the statement of owner’s equity

Part of determining ending owner’s equity

Ending Owner’s EquityShown on the balance sheet

© Paradigm Publishing, Inc. 8

© Paradigm Publishing, Inc. 9

Which financial statement is prepared first?

Quick Check

a. Statement of owner’s equity

b. Income statement

c. Balance sheet

d. Balance sheet or statement of owner’s equity, depending on management’s preference

e. Balance sheet or income statement, depending on management’s preference

© Paradigm Publishing, Inc. 10

Net income would appear

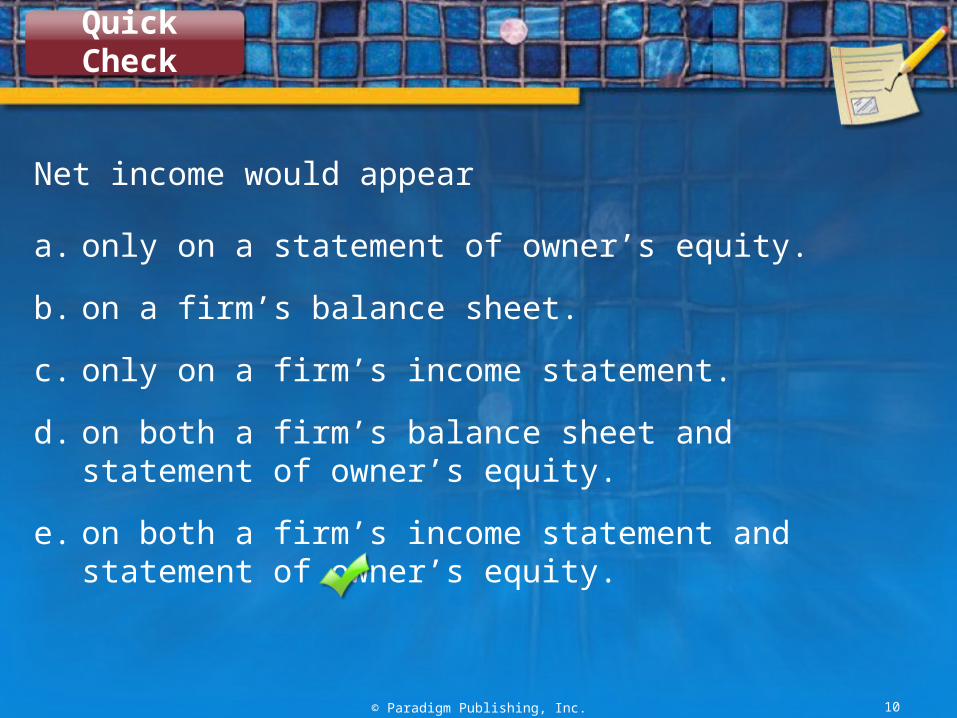

Quick Check

a. only on a statement of owner’s equity.

b. on a firm’s balance sheet.

c. only on a firm’s income statement.

d. on both a firm’s balance sheet and statement of owner’s equity.

e. on both a firm’s income statement and statement of owner’s equity.

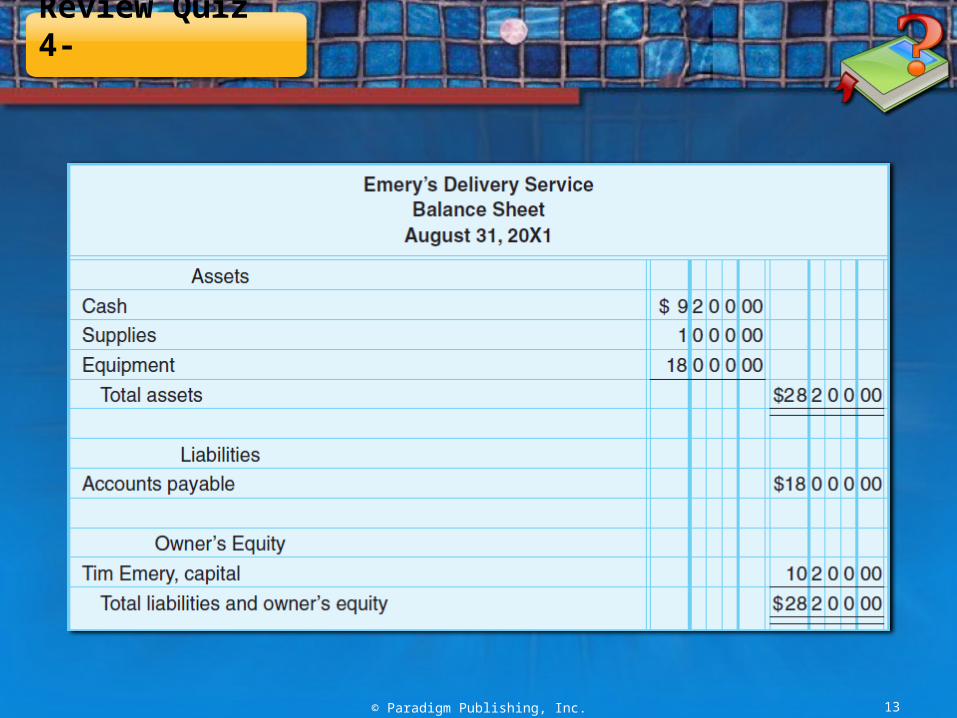

Review Quiz 4-

© Paradigm Publishing, Inc. 11

Review Quiz 4-

© Paradigm Publishing, Inc. 12

Review Quiz 4-

© Paradigm Publishing, Inc. 13

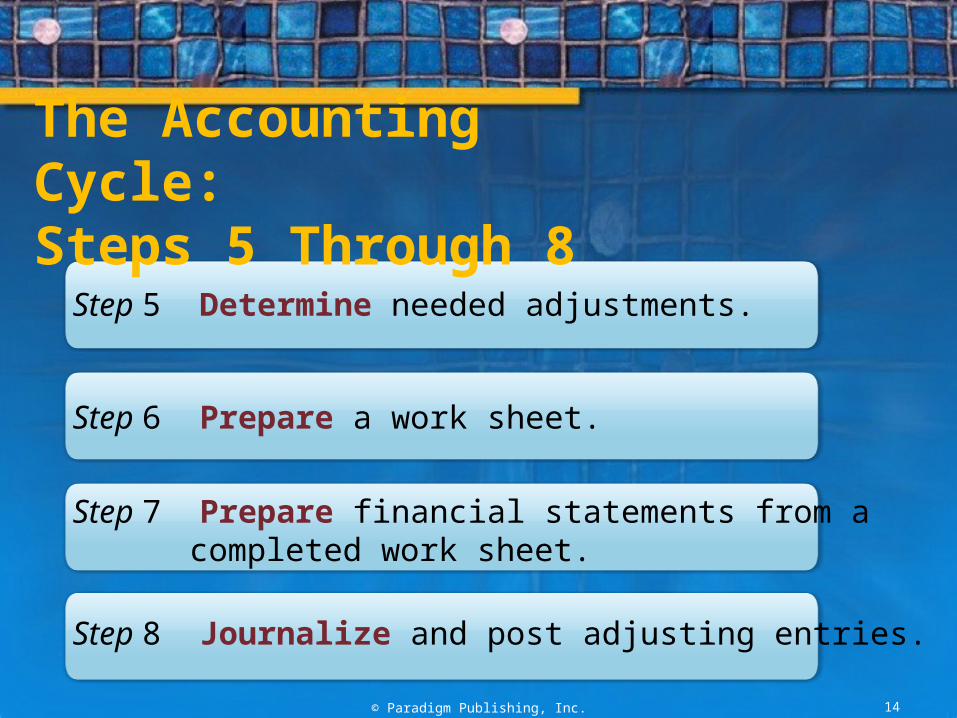

The Accounting Cycle: Steps 5 Through 8

Step 5 Determine needed adjustments.

Step 6 Prepare a work sheet.

Step 7 Prepare financial statements from a completed work sheet.

Step 8 Journalize and post adjusting entries.

© Paradigm Publishing, Inc. 14

© Paradigm Publishing, Inc. 15

Explain the need for adjusting entries

Learning Objective 2

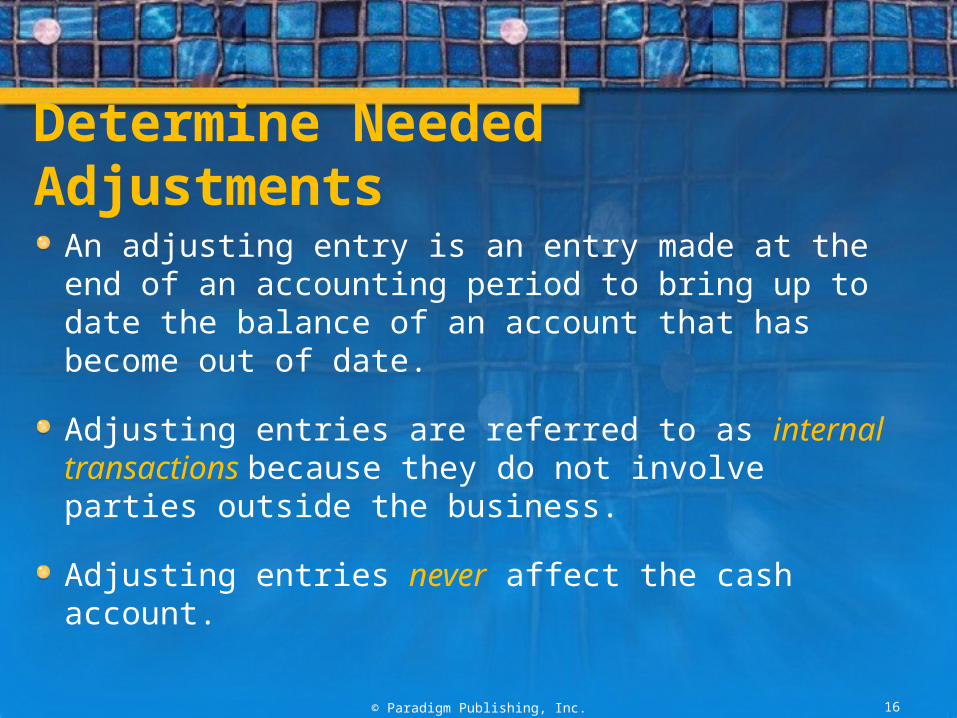

Determine Needed Adjustments

An adjusting entry is an entry made at the end of an accounting period to bring up to date the balance of an account that has become out of date.

Adjusting entries are referred to as internal transactions because they do not involve parties outside the business.

Adjusting entries never affect the cash account.

© Paradigm Publishing, Inc. 16

© Paradigm Publishing, Inc. 17

Make adjusting entries for supplies used, expired insurance,

depreciation, and unpaid wages

Learning Objective 3

Example

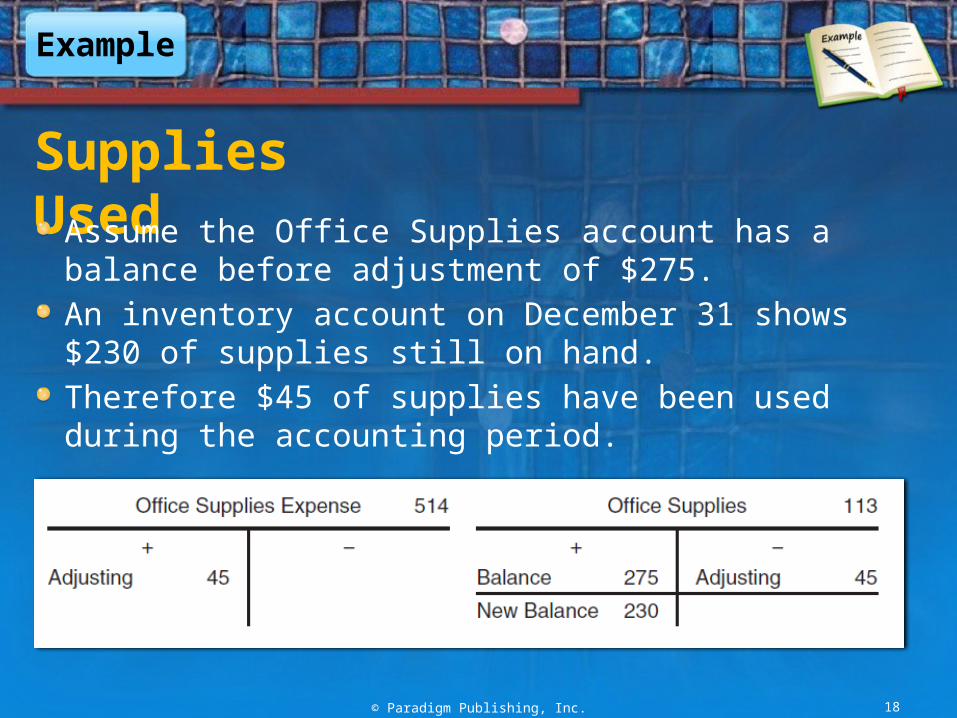

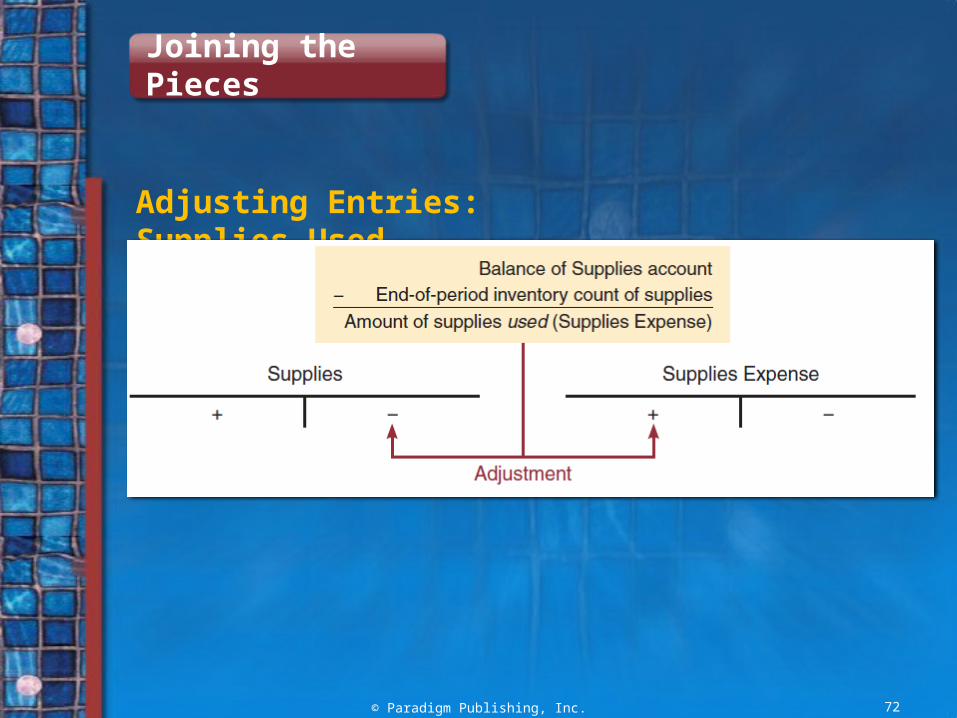

Supplies Used

© Paradigm Publishing, Inc. 18

Assume the Office Supplies account has a balance before adjustment of $275.An inventory account on December 31 shows $230 of supplies still on hand.Therefore $45 of supplies have been used during the accounting period.

Example

© Paradigm Publishing, Inc. 19

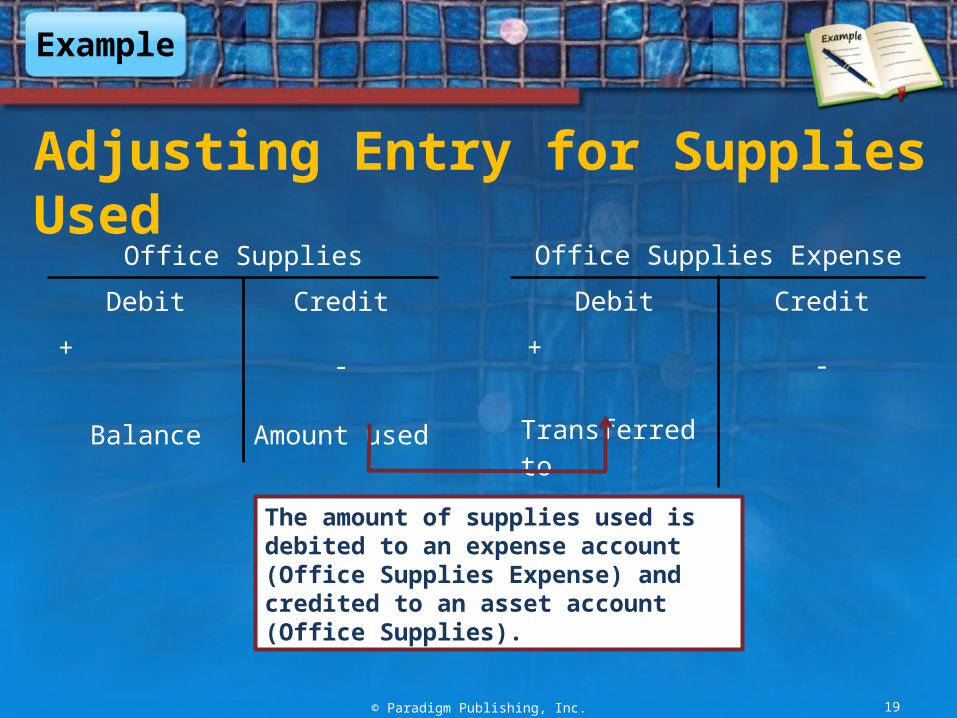

Adjusting Entry for Supplies Used

Office Supplies

Debit Credit

+ -

BalanceAmount

used

Office Supplies Expense

Debit Credit

+ -

Transferred to

The amount of supplies used is debited to an expense account (Office Supplies Expense) and credited to an asset account (Office Supplies).

© Paradigm Publishing, Inc. 20

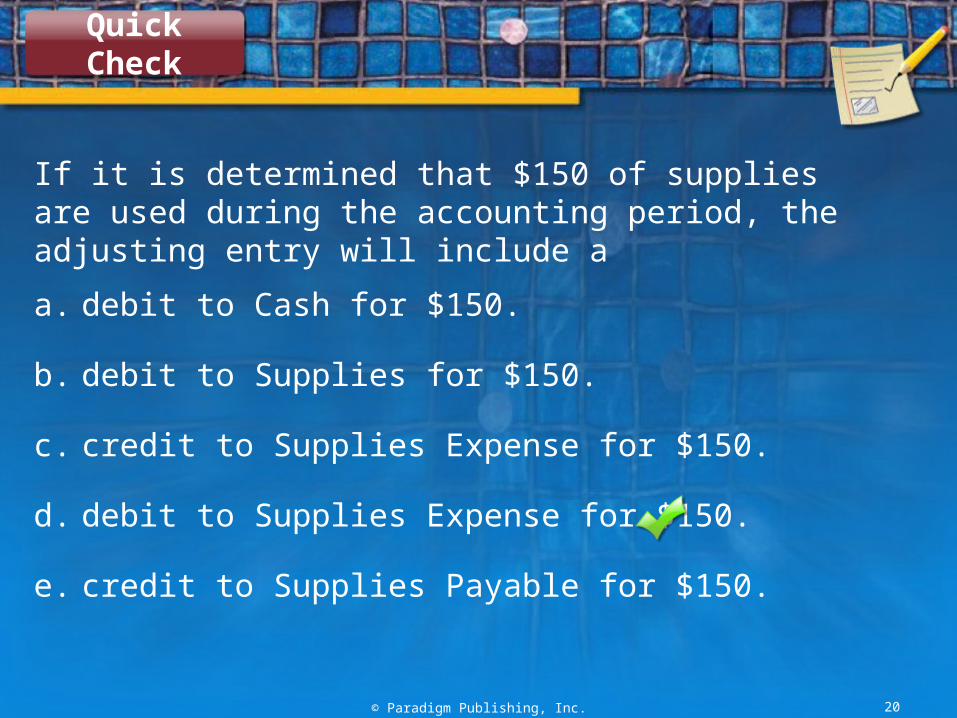

If it is determined that $150 of supplies are used during the accounting period, the adjusting entry will include a

a. debit to Cash for $150.

b. debit to Supplies for $150.

c. credit to Supplies Expense for $150.

d. debit to Supplies Expense for $150.

e. credit to Supplies Payable for $150.

Quick Check

Example

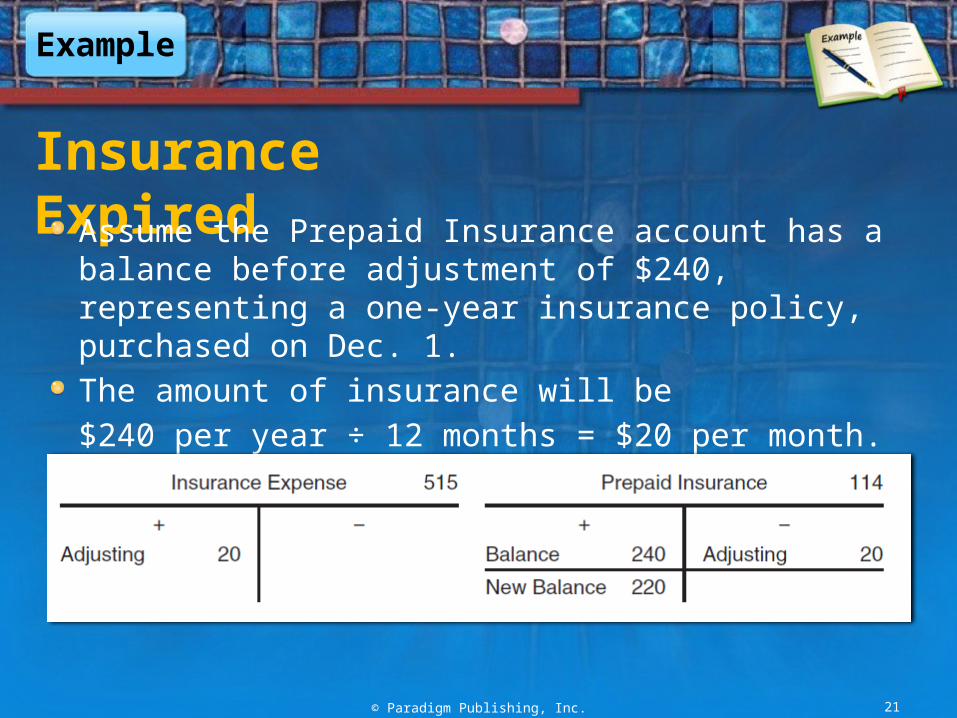

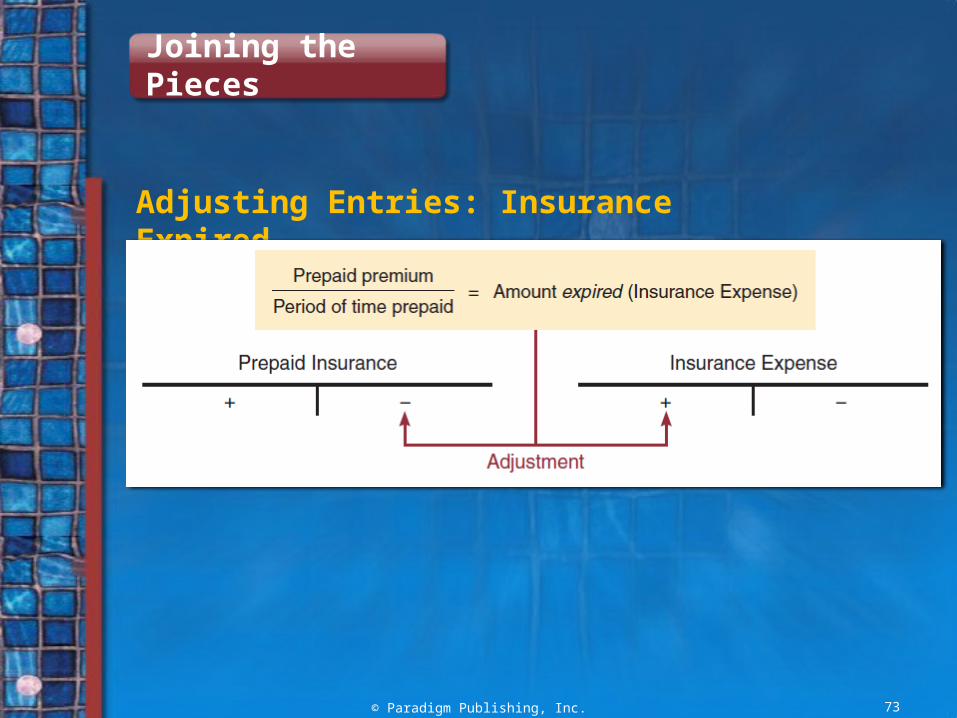

Insurance Expired

© Paradigm Publishing, Inc. 21

Assume the Prepaid Insurance account has a balance before adjustment of $240, representing a one-year insurance policy, purchased on Dec. 1.The amount of insurance will be $240 per year ÷ 12 months = $20 per month.

Example

© Paradigm Publishing, Inc. 22

Adjusting Entry for Insurance Expired

Prepaid Insurance

Debit Credit

+ -

BalanceAmount of coverage expired

Insurance Expense

Debit Credit

+ -

Transferred to

The amount of insurance expired is debited to an expense account (Insurance Expense) and credited to an asset account (Prepaid Insurance).

© Paradigm Publishing, Inc. 23

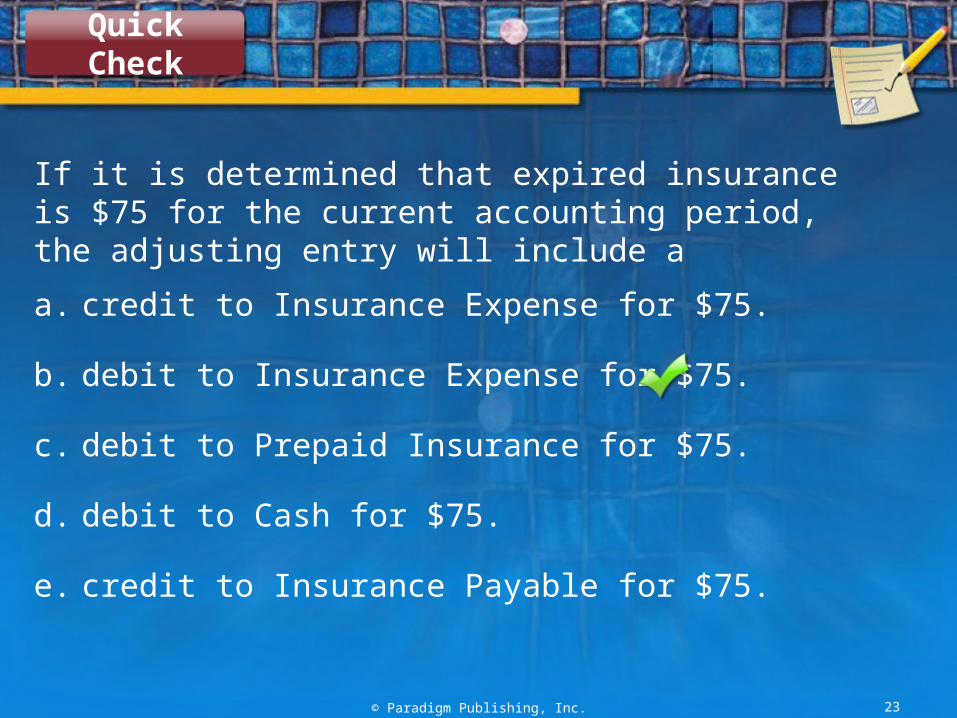

If it is determined that expired insurance is $75 for the current accounting period, the adjusting entry will include a

a. credit to Insurance Expense for $75.

b. debit to Insurance Expense for $75.

c. debit to Prepaid Insurance for $75.

d. debit to Cash for $75.

e. credit to Insurance Payable for $75.

Quick Check

Depreciation of Office Equipment and Office Furniture

Depreciation describes the expense that results from the loss in usefulness of an asset due to age, wear and tear, and obsolescence.

The purpose of depreciation accounting is to spread the cost of an asset over its useful life rather than treating the asset’s cost as an expense in the year it was purchased.

© Paradigm Publishing, Inc. 24

Depreciation Calculations Straight-Line Method

One of the most popular depreciation methods

Yields the same amount of depreciation for each full period an asset is used

Formula:

© Paradigm Publishing, Inc. 25

Cost of asset – Trade-in value= Annual depreciation expense

Estimated years of usefulness

Example

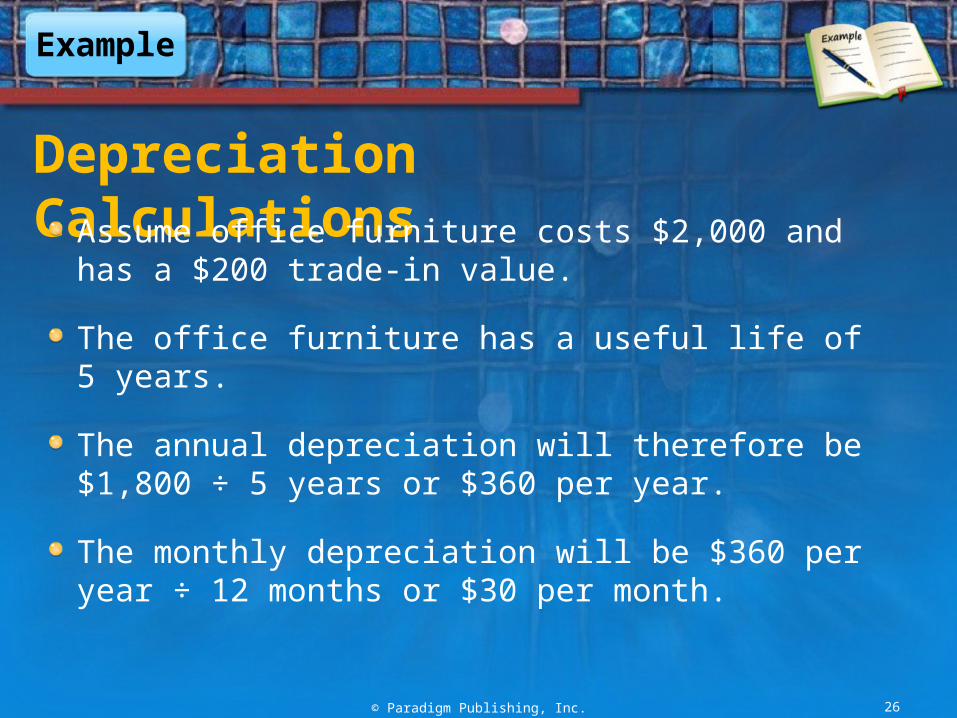

Depreciation Calculations

© Paradigm Publishing, Inc. 26

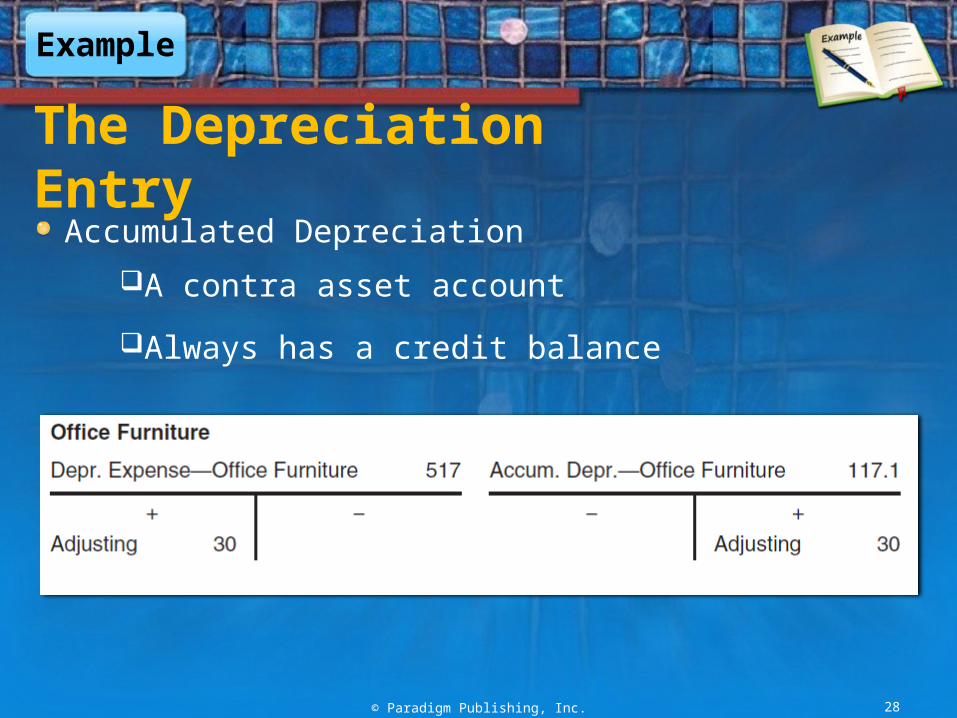

Assume office furniture costs $2,000 and has a $200 trade-in value.

The office furniture has a useful life of 5 years.

The annual depreciation will therefore be $1,800 ÷ 5 years or $360 per year.

The monthly depreciation will be $360 per year ÷ 12 months or $30 per month.

© Paradigm Publishing, Inc. 27

The Depreciation Entry

Depreciation is always recorded by

Debiting an expense account entitled Depreciation Expense

Crediting an account entitled Accumulated Depreciation

Example

Example

© Paradigm Publishing, Inc. 28

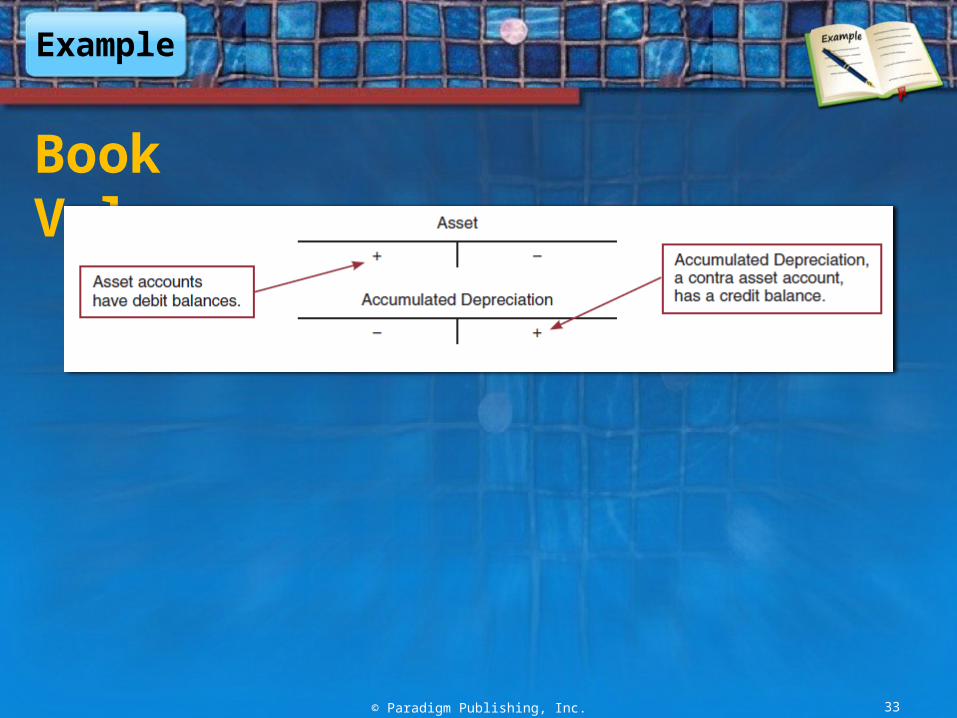

The Depreciation Entry

Accumulated Depreciation

A contra asset account

Always has a credit balance

Example

© Paradigm Publishing, Inc. 29

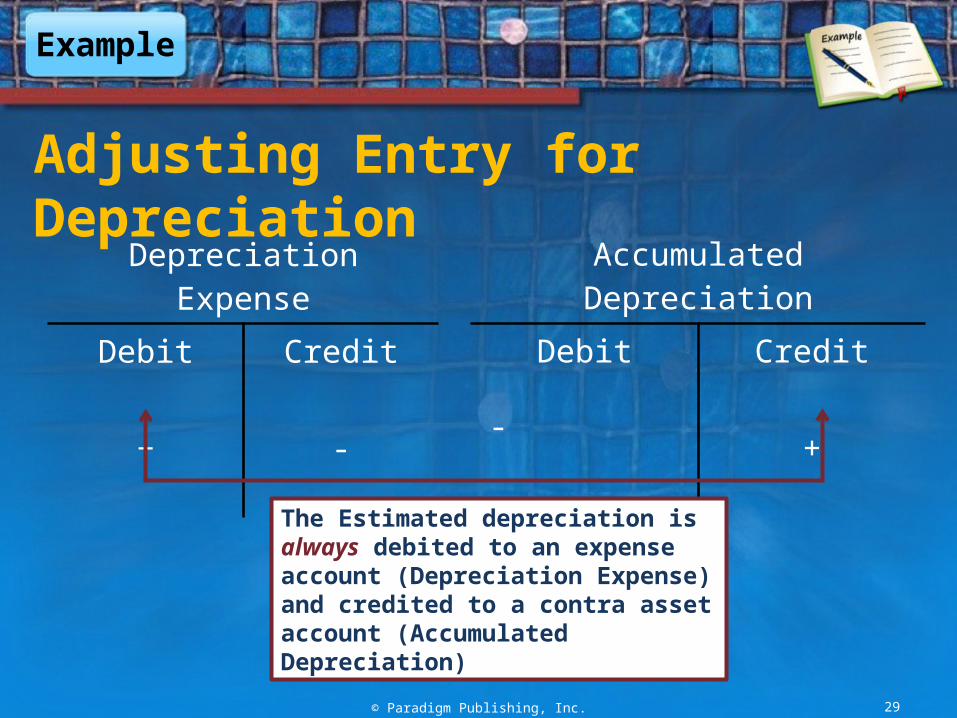

Adjusting Entry for Depreciation

Depreciation Expense

Debit Credit

+ -

Accumulated Depreciation

Debit Credit

- +

The Estimated depreciation is always debited to an expense account (Depreciation Expense) and credited to a contra asset account (Accumulated Depreciation)

© Paradigm Publishing, Inc. 30

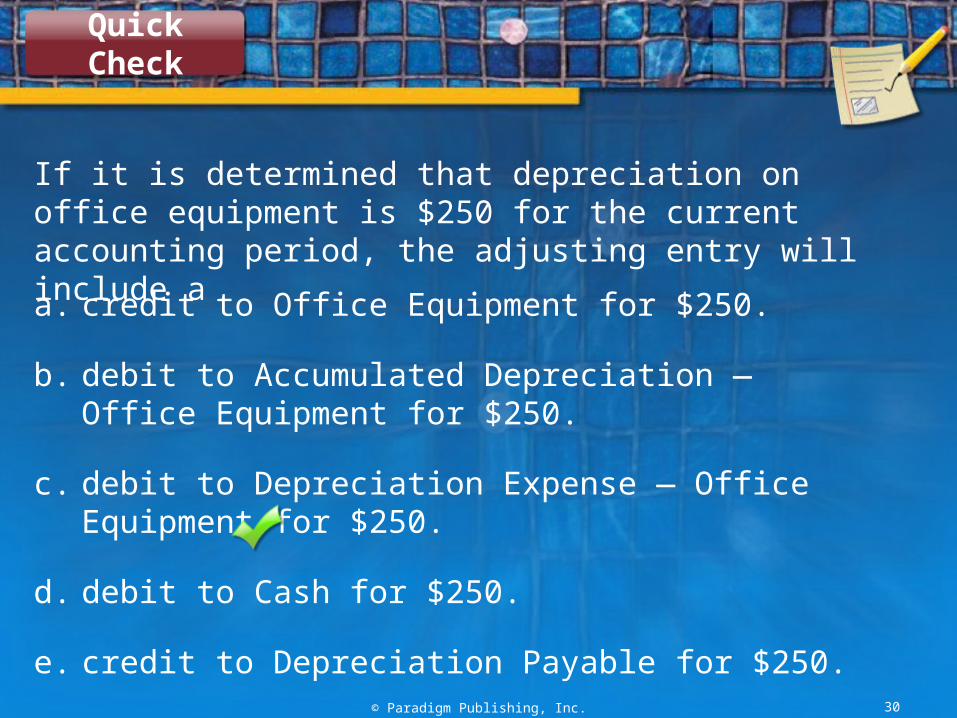

If it is determined that depreciation on office equipment is $250 for the current accounting period, the adjusting entry will include a

a. credit to Office Equipment for $250.

b. debit to Accumulated Depreciation — Office Equipment for $250.

c. debit to Depreciation Expense — Office Equipment for $250.

d. debit to Cash for $250.

e. credit to Depreciation Payable for $250.

Quick Check

Book Value

The difference between the cost of an asset and its accumulated depreciation

Shown on the balance sheet

© Paradigm Publishing, Inc. 31

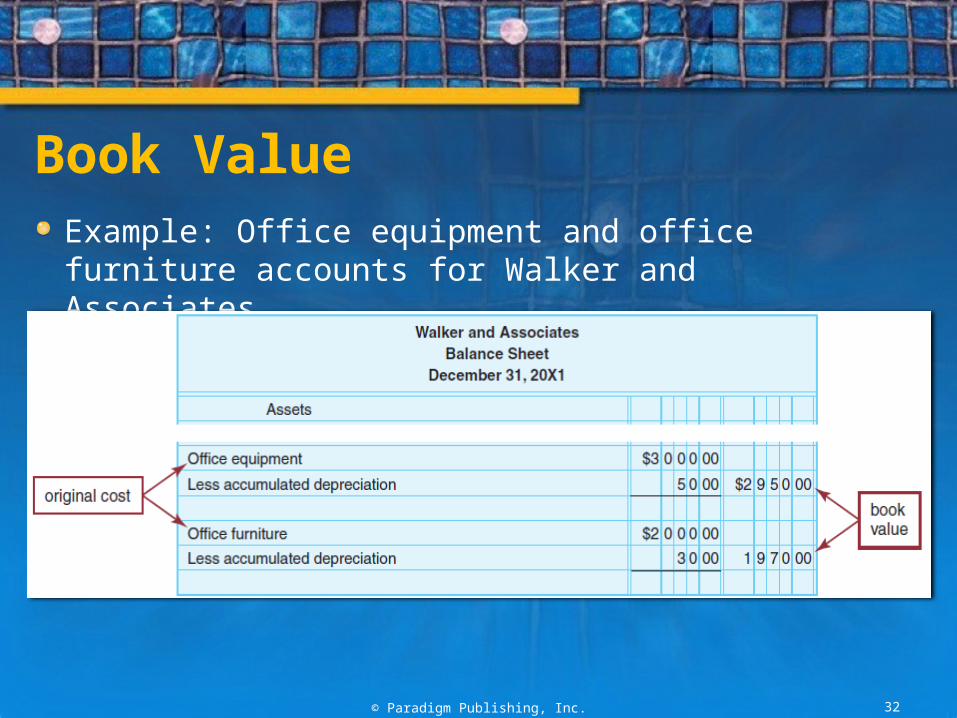

Book ValueExample: Office equipment and office furniture accounts for Walker and Associates

© Paradigm Publishing, Inc. 32

Example

Book Value

© Paradigm Publishing, Inc. 33

© Paradigm Publishing, Inc. 34

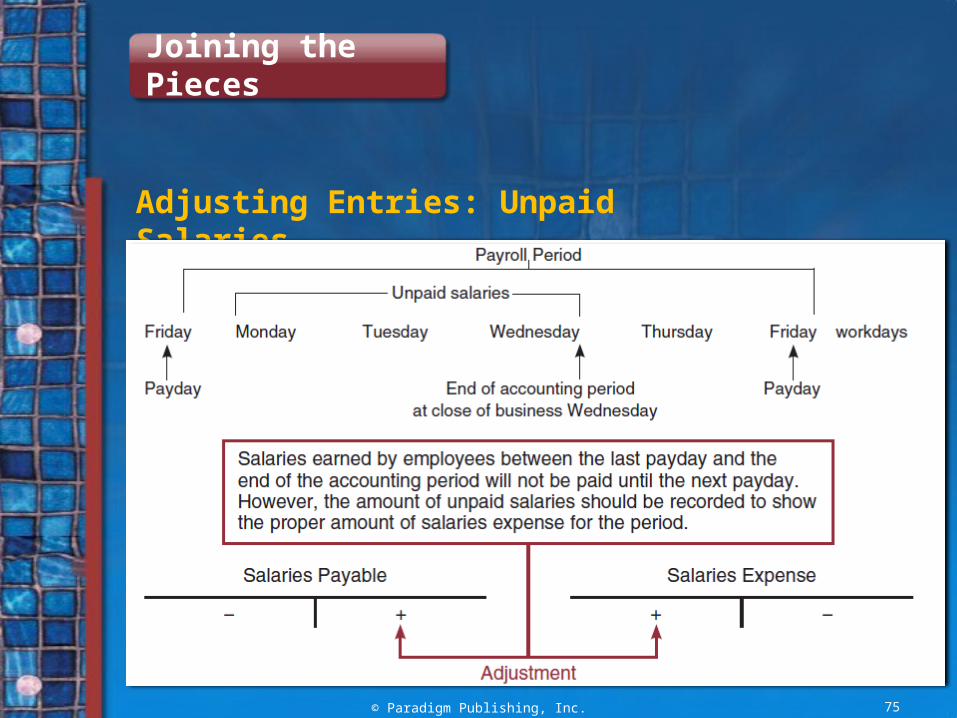

Unpaid Salaries

Assume A business has 3 employees each earning

$150 per day.

Employees are paid every Friday for a 5-day week ending on Friday.

December 31 falls on a Wednesday.

Example

Example

© Paradigm Publishing, Inc. 35

Unpaid Salaries

An adjusting entry must be prepared

On Wednesday, December 31 for salaries owed to employees for Monday, Tuesday, and Wednesday.

For 3 employees × $150 per day × 3 days = $1,350.

Example

© Paradigm Publishing, Inc. 36

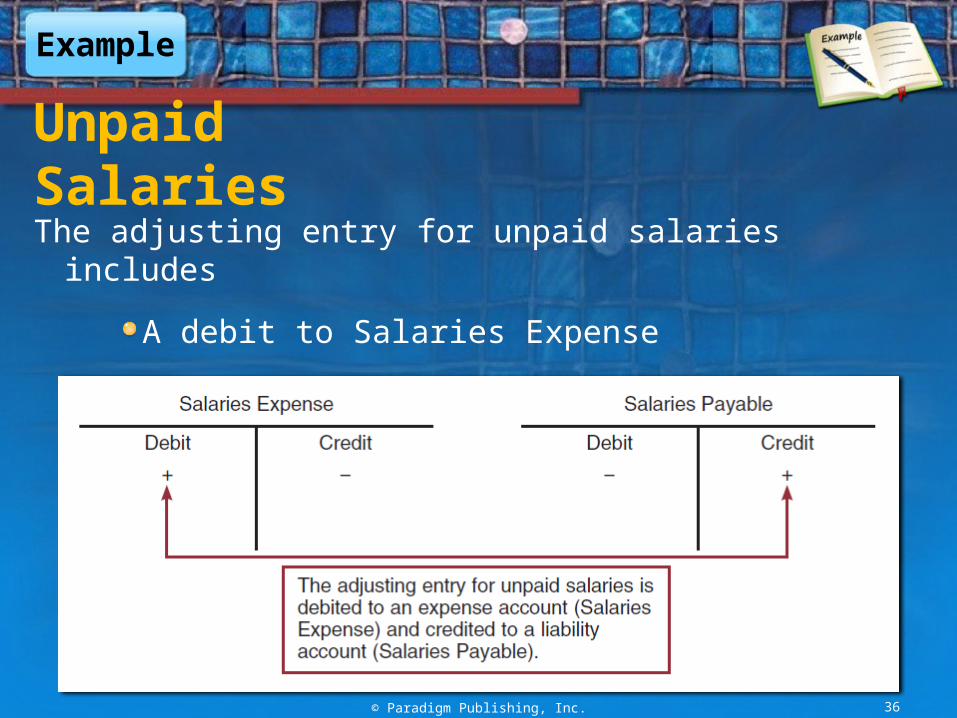

Unpaid SalariesThe adjusting entry for unpaid salaries includes

A debit to Salaries Expense

A credit to Salaries Payable

© Paradigm Publishing, Inc. 37

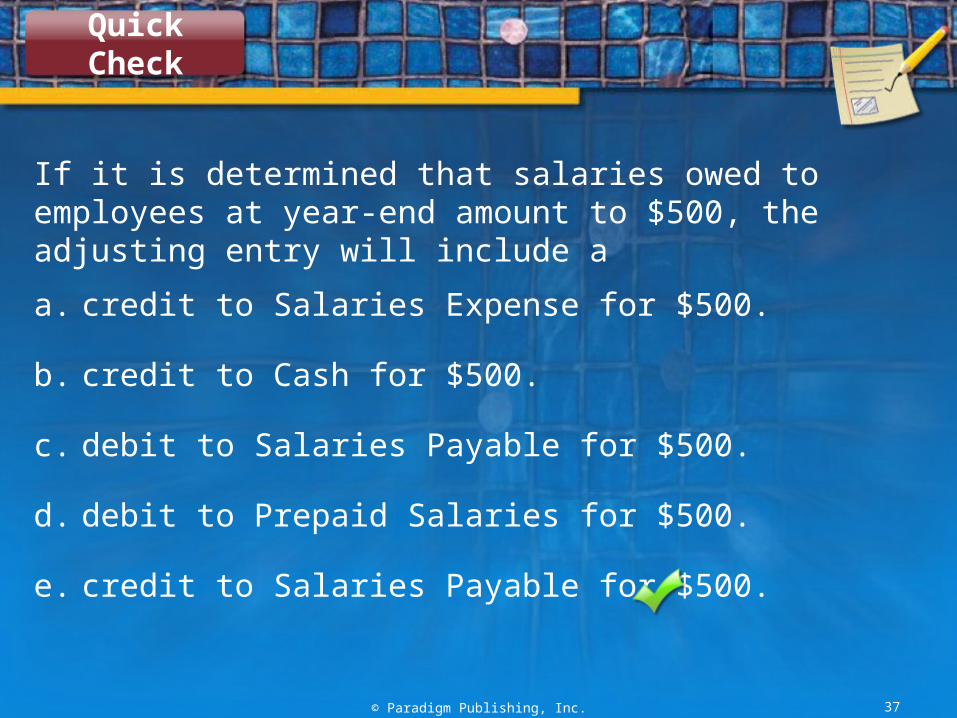

If it is determined that salaries owed to employees at year-end amount to $500, the adjusting entry will include a

a. credit to Salaries Expense for $500.

b. credit to Cash for $500.

c. debit to Salaries Payable for $500.

d. debit to Prepaid Salaries for $500.

e. credit to Salaries Payable for $500.

Quick Check

Matching Principle

Revenue and expenses are recorded in the accounting period in which they occurred.

Adjusting entries are needed to properly match expenses and revenue.

Although adjusting entries may be made any time, they are normally adjusted at the end of a month or the end of the year.

© Paradigm Publishing, Inc. 38

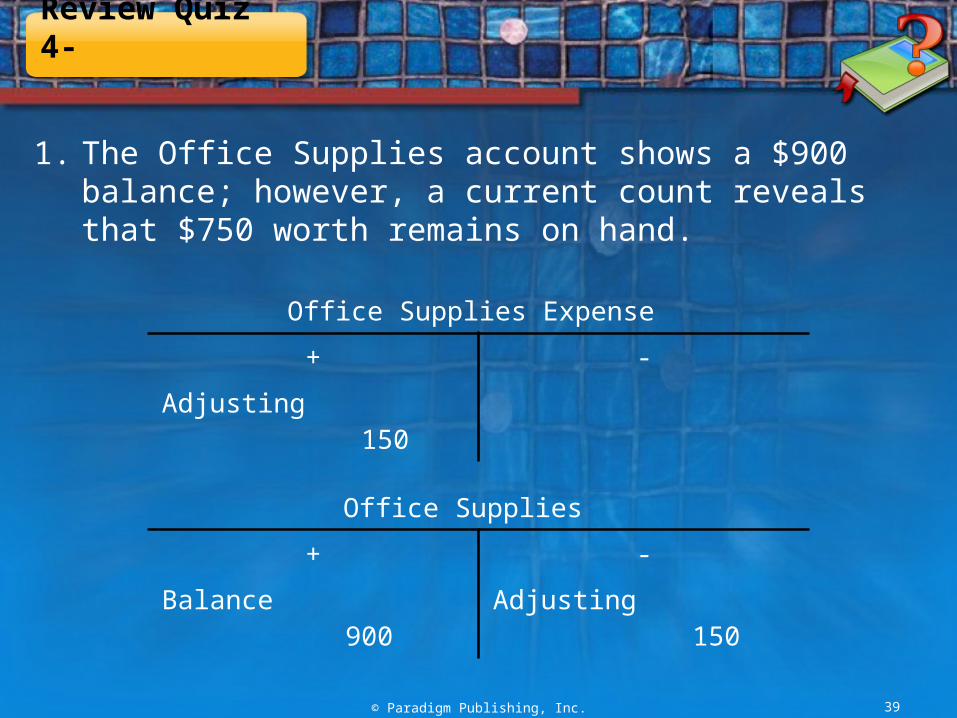

1. The Office Supplies account shows a $900 balance; however, a current count reveals that $750 worth remains on hand.

© Paradigm Publishing, Inc. 39

Office Supplies Expense

+ -

Adjusting 150

Office Supplies

+ -

Balance 900

Adjusting 150

Review Quiz 4-

Review Quiz 4-

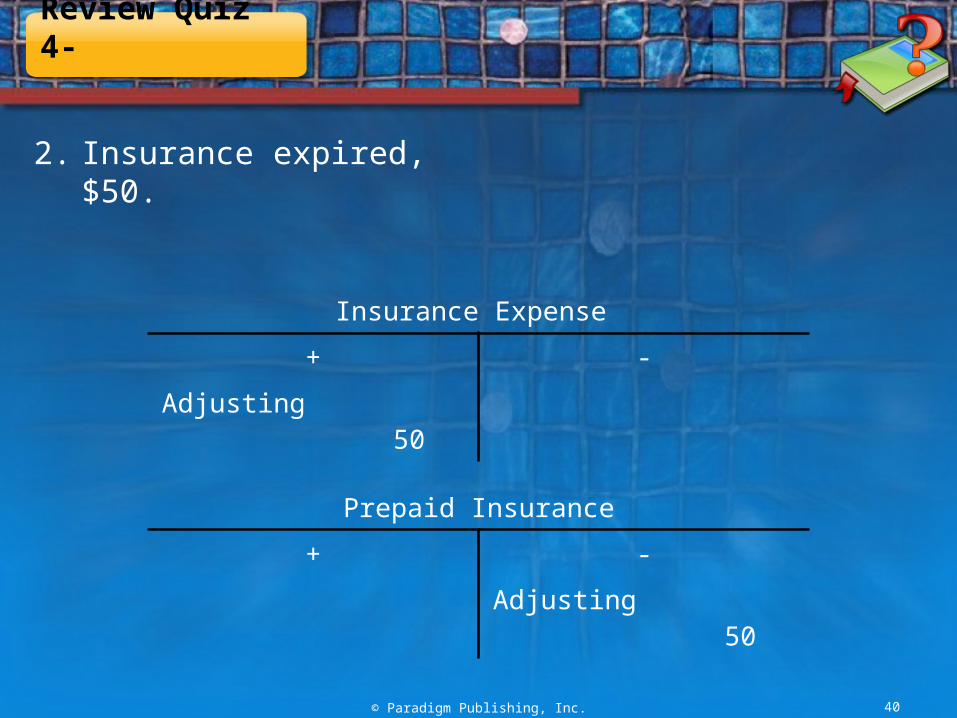

2. Insurance expired, $50.

© Paradigm Publishing, Inc. 40

Insurance Expense

+ -

Adjusting 50

Prepaid Insurance

+ -

Adjusting 50

Review Quiz 4-

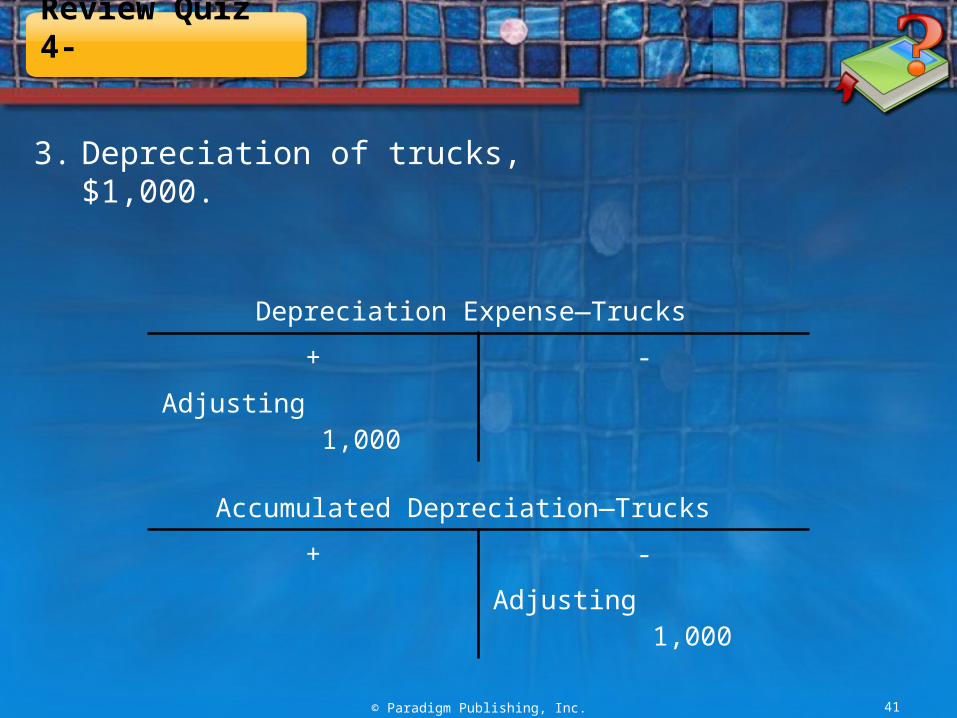

3. Depreciation of trucks, $1,000.

© Paradigm Publishing, Inc. 41

Depreciation Expense—Trucks

+ -

Adjusting 1,000

Accumulated Depreciation—Trucks

+ -

Adjusting 1,000

Review Quiz 4-

4. Unpaid salaries, $150.

© Paradigm Publishing, Inc. 42

Salaries Expense

+ -

Adjusting 150

Salaries Payable

+ -

Balance 900

Adjusting 150

© Paradigm Publishing, Inc. 43

Complete a work sheet for a service business

Learning Objective 4

The Work Sheet

Informal working paper

Used in preparing the financial statements and completing the work of the accounting cycle

The work sheet is used toOrganize dataLessen the possibility of overlooking an

adjustmentProvide an arithmetical check on the accuracy

ofworkArrange data in logical form for the preparation

of financial statements

© Paradigm Publishing, Inc. 44

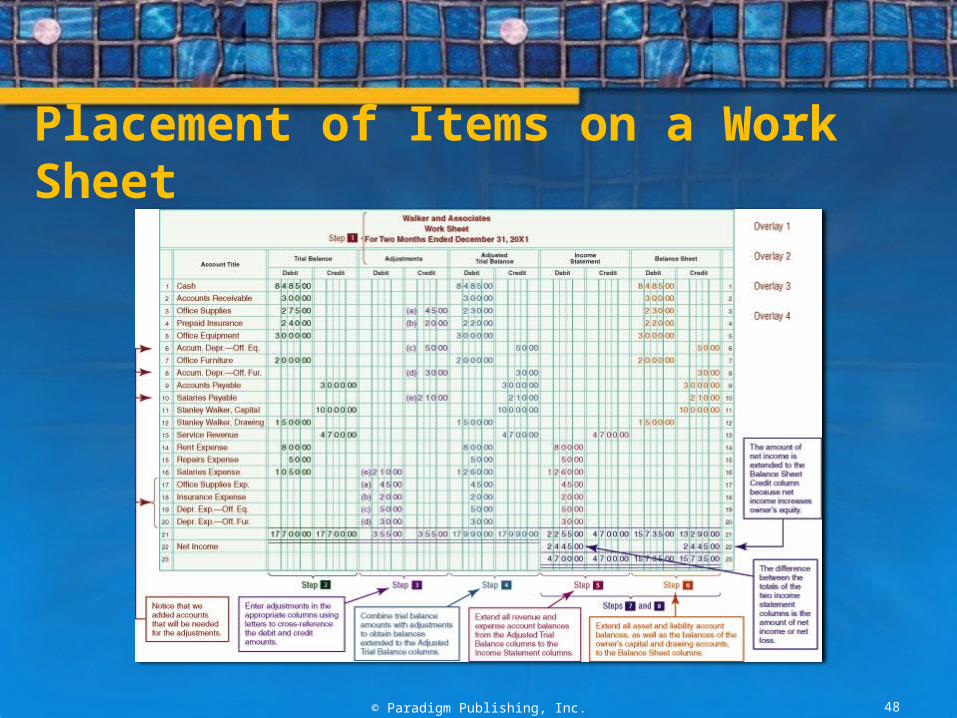

Steps in Completing the Work Sheet1. Enter the heading.

2. Enter the current trial balance in the Trial Balance columns.

3. Enter the adjustments in the Adjustments Debit and Credit columns.

4. Complete the Adjusted Trial Balance columns.

© Paradigm Publishing, Inc. 45

Steps in Completing the Work Sheet5. Complete the Income Statements columns.

6. Complete the Balance Sheet columns.

7. Total the Income Statement and Balance Sheet columns.

8. Determine the amount of net income or net loss, and balance the statement columns.

© Paradigm Publishing, Inc. 46

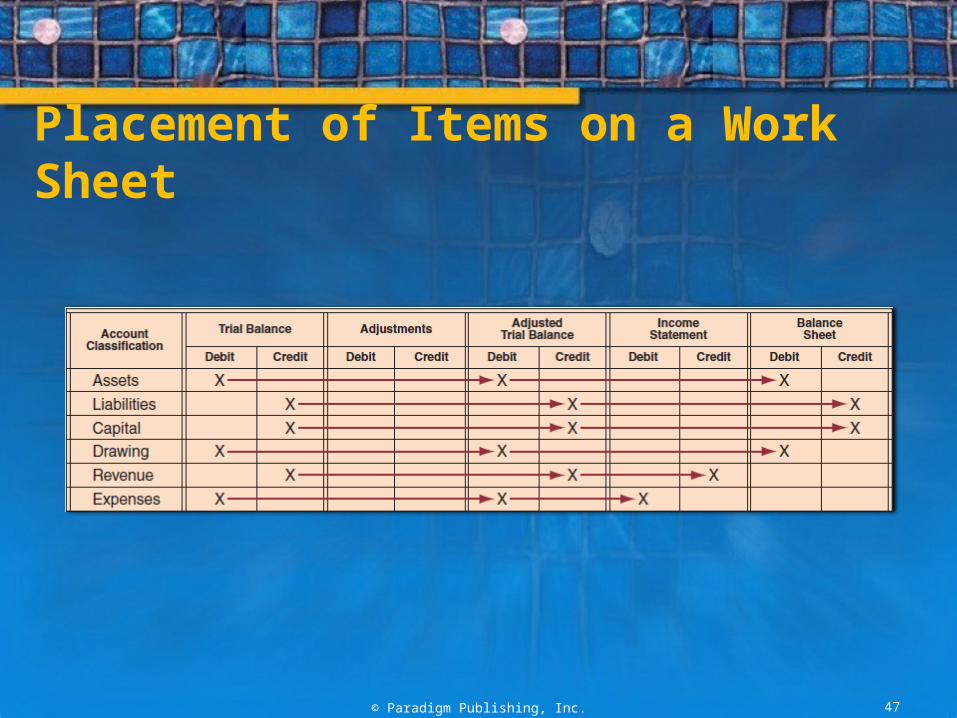

Placement of Items on a Work Sheet

© Paradigm Publishing, Inc. 47

Placement of Items on a Work Sheet

© Paradigm Publishing, Inc. 48

© Paradigm Publishing, Inc. 49

The owner’s drawing account appears on the work sheet in which set of columns?

a. Trial balance, income statement, and balance sheet

b. Adjustments, adjusted trial balance, and income statement

c. Trial balance, adjusted trial balance, and income statement

d. Trial balance, adjusted trial balance, and balance sheet

e. Income statement and balance sheet

Quick Check

Review Quiz 4-

On a completed work sheet, can the amount of net income (or net loss) be obtained by finding the difference between the total of the Balance Sheet Debit column and the total of the Balance Sheet Credit column? If so, why?

© Paradigm Publishing, Inc. 50

Yes.

Differences between revenue and expenses will either increase or decrease capital.

The difference between the totals of the Balance Sheet Debit and Credit columns of the work sheet reflects the net income or net loss that has not yet been transferred to the owner's capital account.

© Paradigm Publishing, Inc. 51

Prepare financial statements from a work sheet

Learning Objective 5

The Income Statement

Summary of revenue and expenses showing net income or net loss for an accounting period

Prepared directly from data in the Income Statements columns of the work sheet

Typically prepared at the end of each month, quarter, or year; however, can be prepared for any period of time

© Paradigm Publishing, Inc. 52

More on the Income Statement

Dated to cover a period of time

The revenue and expenses shown occurred over the entire period, not just the last date

© Paradigm Publishing, Inc. 53

The Statement of Owner’s Equity

Summarizes the changes that have occurred in owner’s equity during an accounting period, such as a month or a year.

Prepared from the information on the work sheet:1.The owner’s capital account balance in the

Balance Sheet Credit column

2.The owner’s drawing account balance in the Balance Sheet Debit column

3.The amount of net income or net loss, shown at the bottom of the Income Statement section

© Paradigm Publishing, Inc. 54

The Balance Sheet

Shows that assets = liabilities + owner’s equity

Data come from the Balance Sheet columns of the work sheet

The up-to-date amount for owner’s equity on the balance sheet is taken from the statement of owner’s equity

© Paradigm Publishing, Inc. 55

Preparing the Financial Statements1. Prepare the income statement

The net income or net loss calculated on the income statement is shown on the statement of owner’s equity.

2. Prepare the income statementThe ending equity is shown on the balance sheet.

3. Prepare the balance sheet using the ending equity calculated on the statement of owner’s equity.

© Paradigm Publishing, Inc. 56

Financial Statements

© Paradigm Publishing, Inc. 57

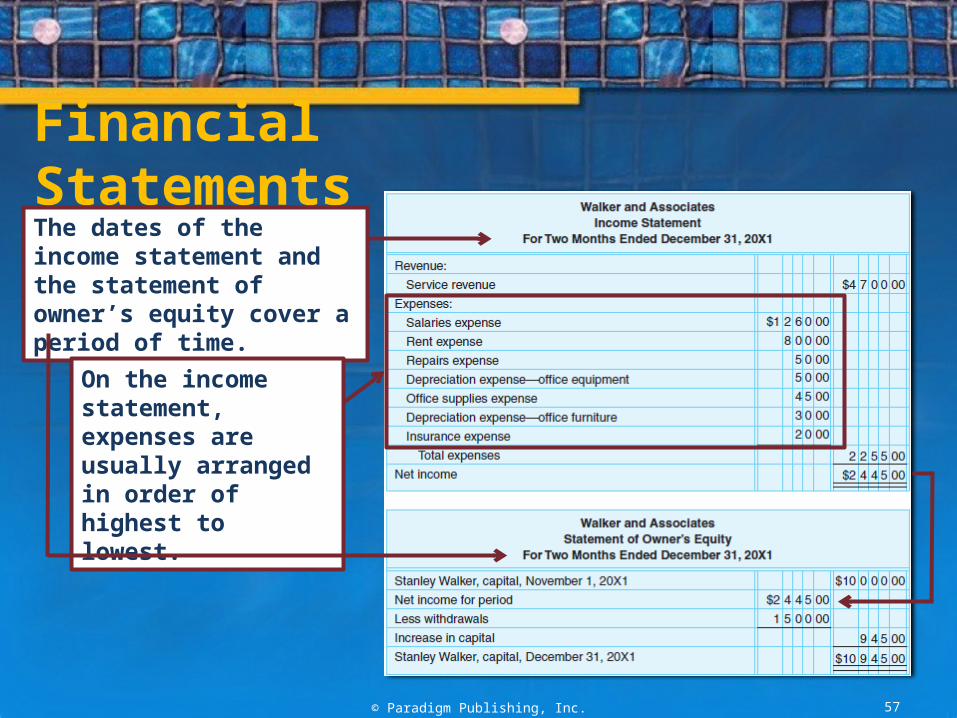

The dates of the income statement and the statement of owner’s equity cover a period of time.

On the income statement, expenses are usually arranged in order of highest to lowest.

Financial Statements

© Paradigm Publishing, Inc. 58

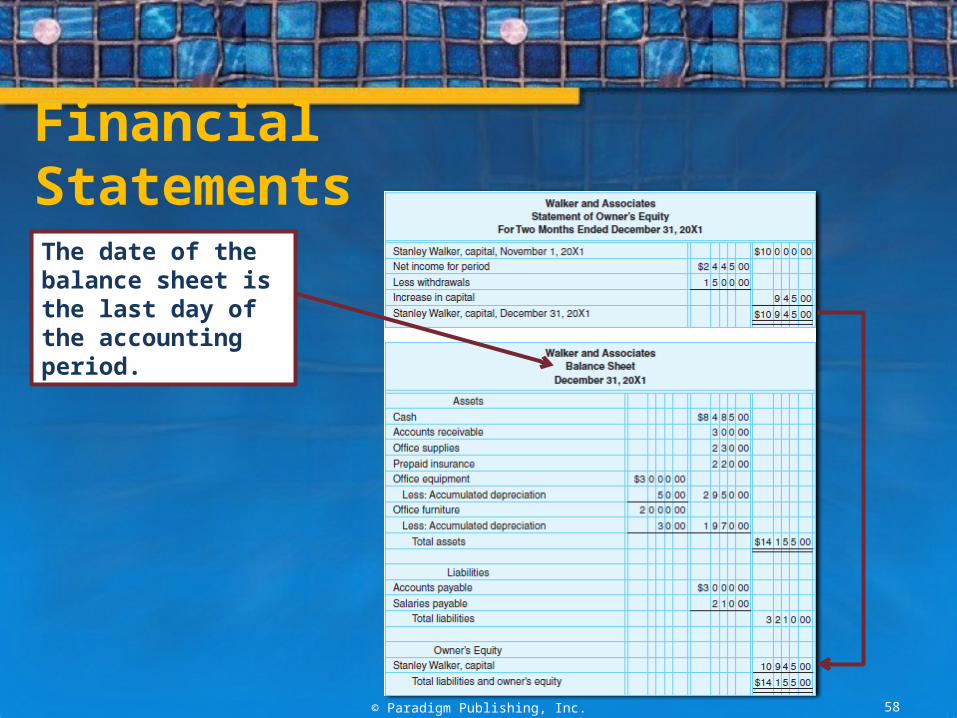

The date of the balance sheet is the last day of the accounting period.

© Paradigm Publishing, Inc. 59

Net income appears on the

a. balance sheet and the statement of owner’s equity.

b. statement of owner’s equity only.

c. income statement only.

d. income statement and statement of owner’s equity.

e. income statement and balance sheet.

Quick Check

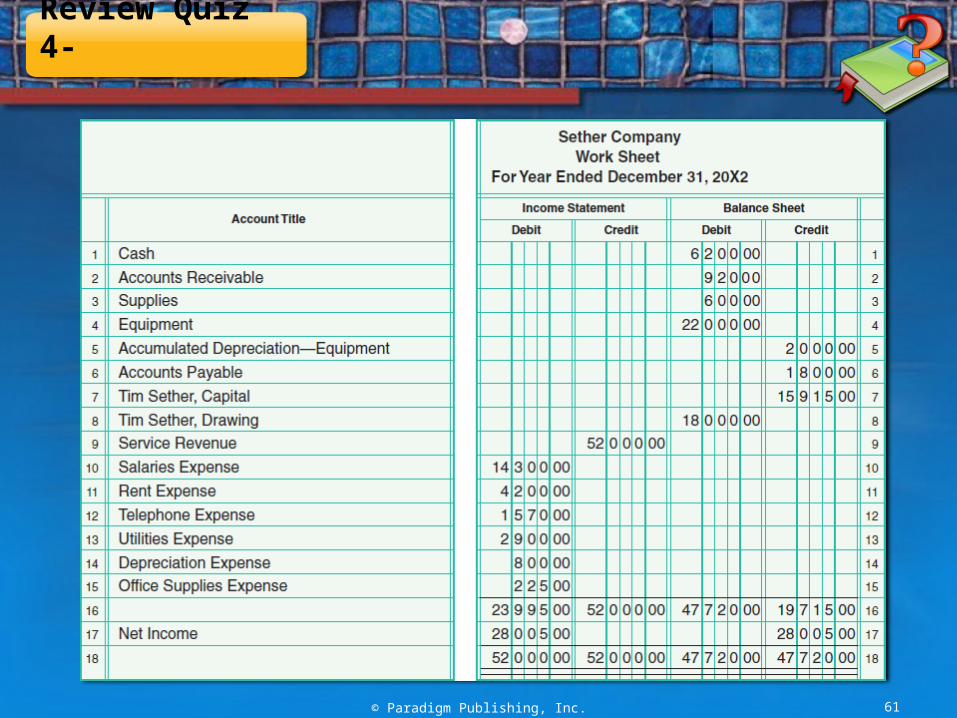

Review Quiz 4-

The financial statement columns of Sether Company’s work sheet are shown below.

© Paradigm Publishing, Inc. 60

1) Prepare an income statement

2) Prepare a statement of owner’s equity

3) Prepare a balance sheet

© Paradigm Publishing, Inc. 61

Review Quiz 4-

Review Quiz 4-

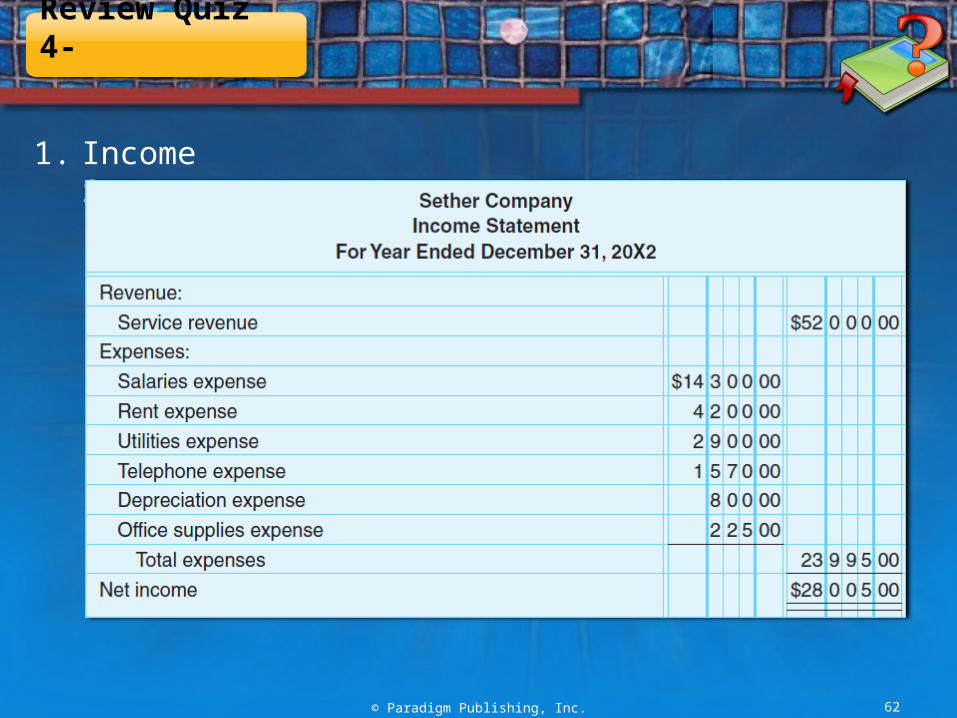

1. Income Statement

© Paradigm Publishing, Inc. 62

Review Quiz 4-

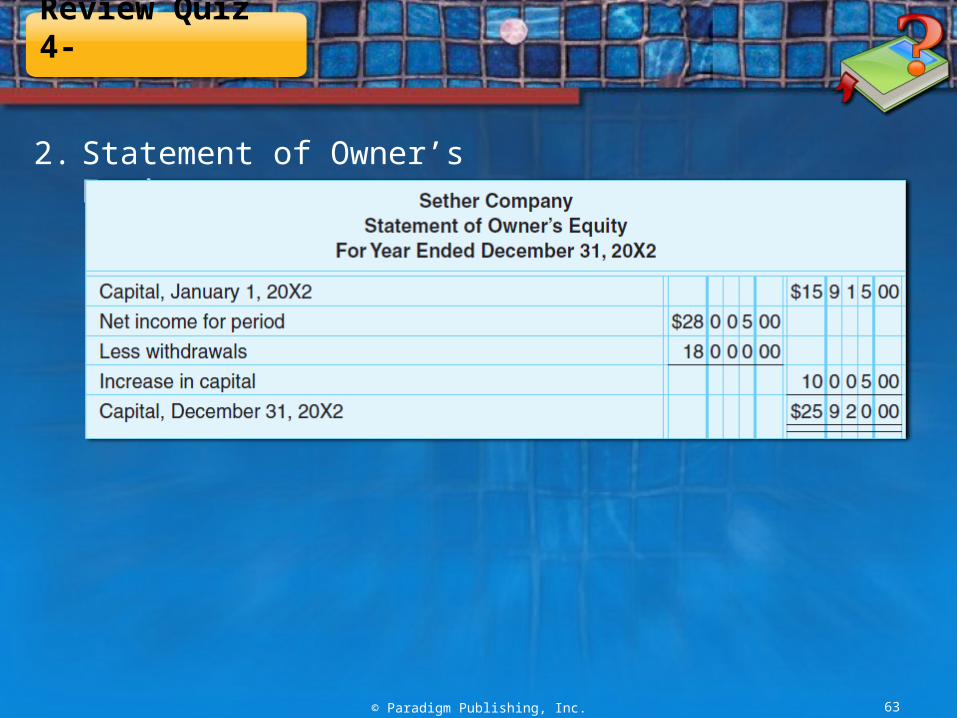

2. Statement of Owner’s Equity

© Paradigm Publishing, Inc. 63

Review Quiz 4-

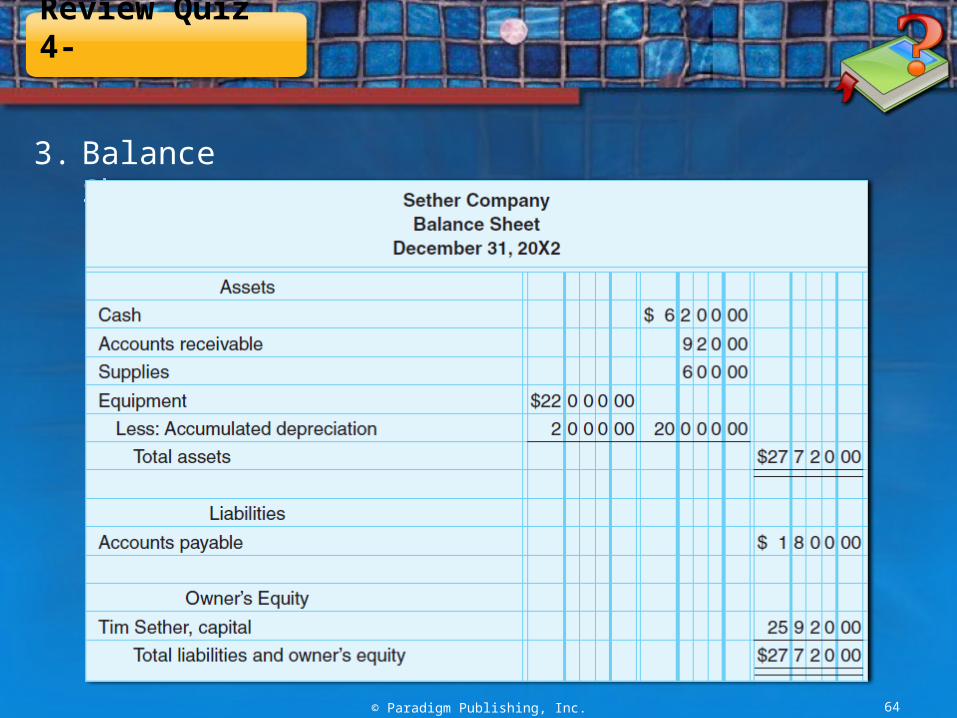

3. Balance Sheet

© Paradigm Publishing, Inc. 64

© Paradigm Publishing, Inc. 65

Journalize and post adjusting entries

Learning Objective 6

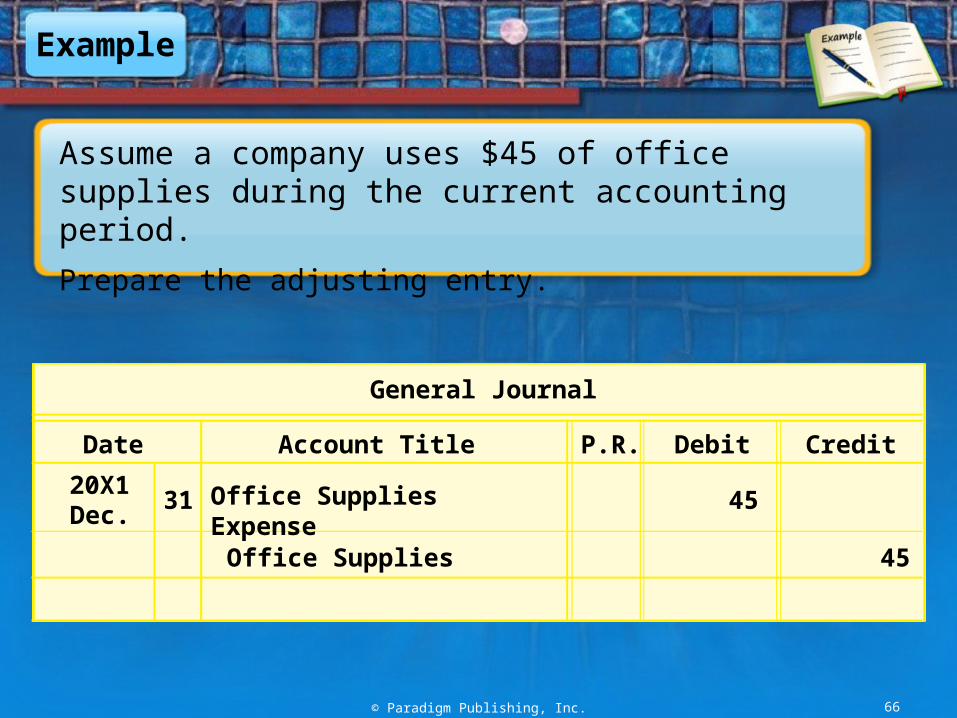

Example

Assume a company uses $45 of office supplies during the current accounting period.

Prepare the adjusting entry.

© Paradigm Publishing, Inc. 66

General Journal

Date Account Title P.R. Debit Credit

20X1Dec.

31 Office Supplies Expense 45

Office Supplies 45

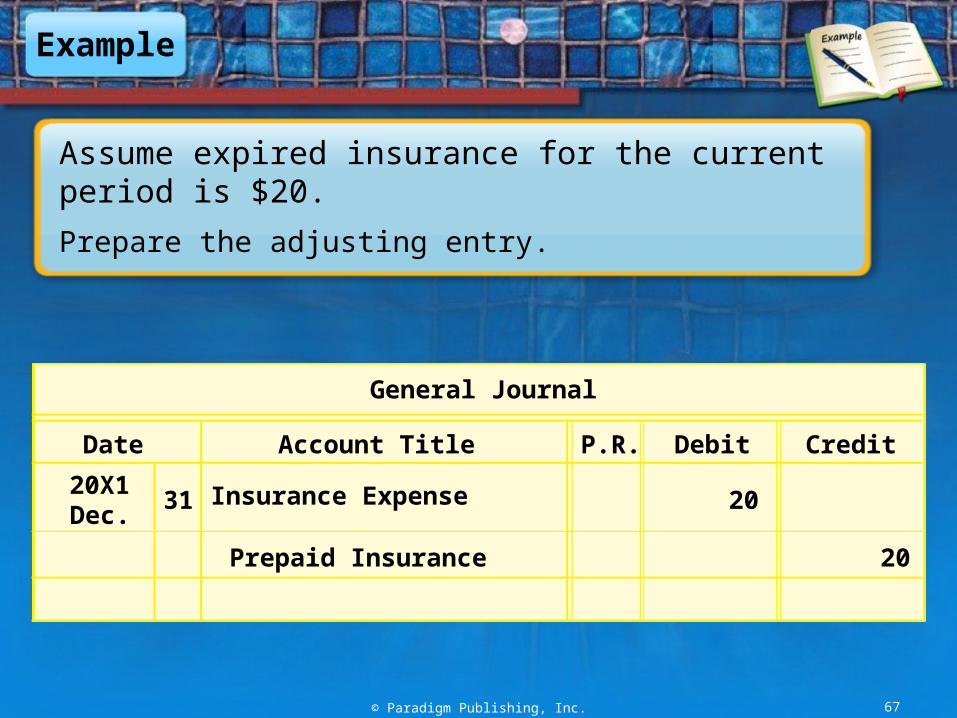

Example

Assume expired insurance for the current period is $20.

Prepare the adjusting entry.

© Paradigm Publishing, Inc. 67

General Journal

Date Account Title P.R. Debit Credit

20X1Dec.

31 Insurance Expense 20

Prepaid Insurance 20

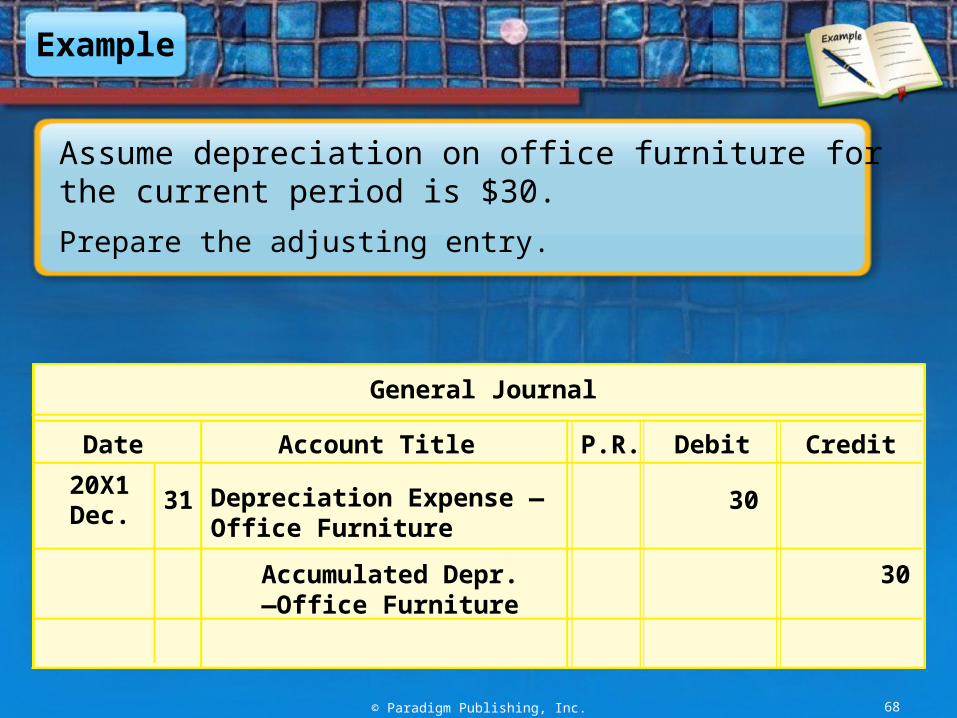

Example

Assume depreciation on office furniture for the current period is $30.

Prepare the adjusting entry.

© Paradigm Publishing, Inc. 68

General Journal

Date Account Title P.R. Debit Credit

20X1Dec.

31 Depreciation Expense —Office Furniture

30

Accumulated Depr. —Office Furniture

30

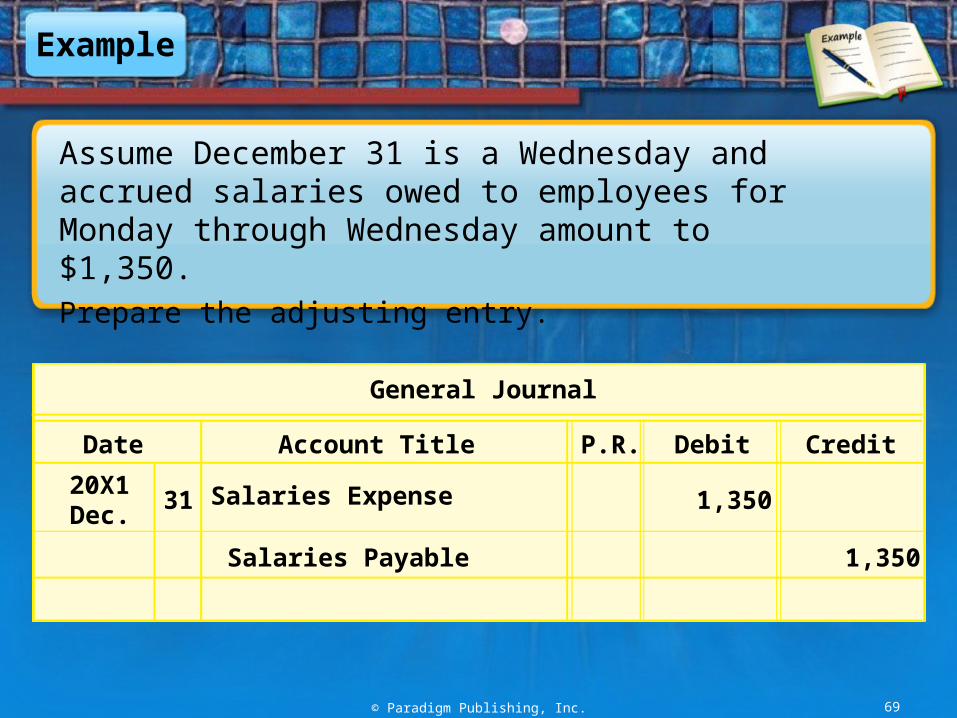

Example

Assume December 31 is a Wednesday and accrued salaries owed to employees for Monday through Wednesday amount to $1,350.Prepare the adjusting entry.

© Paradigm Publishing, Inc. 69

General Journal

Date Account Title P.R. Debit Credit

20X1Dec.

31 Salaries Expense 1,350

Salaries Payable 1,350

Review Quiz 4-

If adjusting entries are entered on the work sheet, why is it necessary to formally journalize them and post to the ledger?

© Paradigm Publishing, Inc. 70

It is necessary to make journal entries for adjustments because the work sheet is not a journal. It is an informal document used to organize data and facilitate the work at the end of an accounting period. However, no posting is made from the work sheet. After adjustments have been journalized and posted, the ledger will be up to date and will agree with the data presented on the financial statements.

Focus on Ethics

© Paradigm Publishing, Inc. 71

How does failing to close the books in a timely fashion enhance the current year’s net income?

Refer to the Focus on Ethics box on page 153 in your text.

© Paradigm Publishing, Inc. 72

Joining the Pieces

Adjusting Entries: Supplies Used

© Paradigm Publishing, Inc. 73

Joining the Pieces

Adjusting Entries: Insurance Expired

© Paradigm Publishing, Inc. 74

Joining the Pieces

Adjusting Entries: Depreciation of Long-Term Assets

© Paradigm Publishing, Inc. 75

Joining the Pieces

Adjusting Entries: Unpaid Salaries