Embed Size (px)

Citation preview

2015–2016 ANNUAL REPORT

3 WorkCover Queensland annual report 2015–2016

WELCOME ............................... 4

ABOUT WORKCOVER ............ 5 CUSTOMER SERVICE COMMITMENT .................. 6

2015–2019 CORPORATE PLAN .......................... 7

STATEMENT OF CORPORATE INTENT 2015–2016 ...................................................... 9

HIGHLIGHTS ......................... 13

LEADERSHIP ......................... 15 CHAIR AND CEO REPORT ................................ 15

BOARD OF DIRECTORS .................................... 18

EXECUTIVE TEAM ............................................ 20

ENGAGED PEOPLE................ 22

STATISTICS ............................ 25

CORPORATE GOVERNANCE 30 ETHICS, COMPLIANCE AND RISK MANAGEMENT .............................................. 32

FINANCIAL PERFORMANCE 36 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME ............................. 41

CONSOLIDATED STATEMENT OF FINANCIAL POSITION ....................................................... 42

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY ........................................................... 43

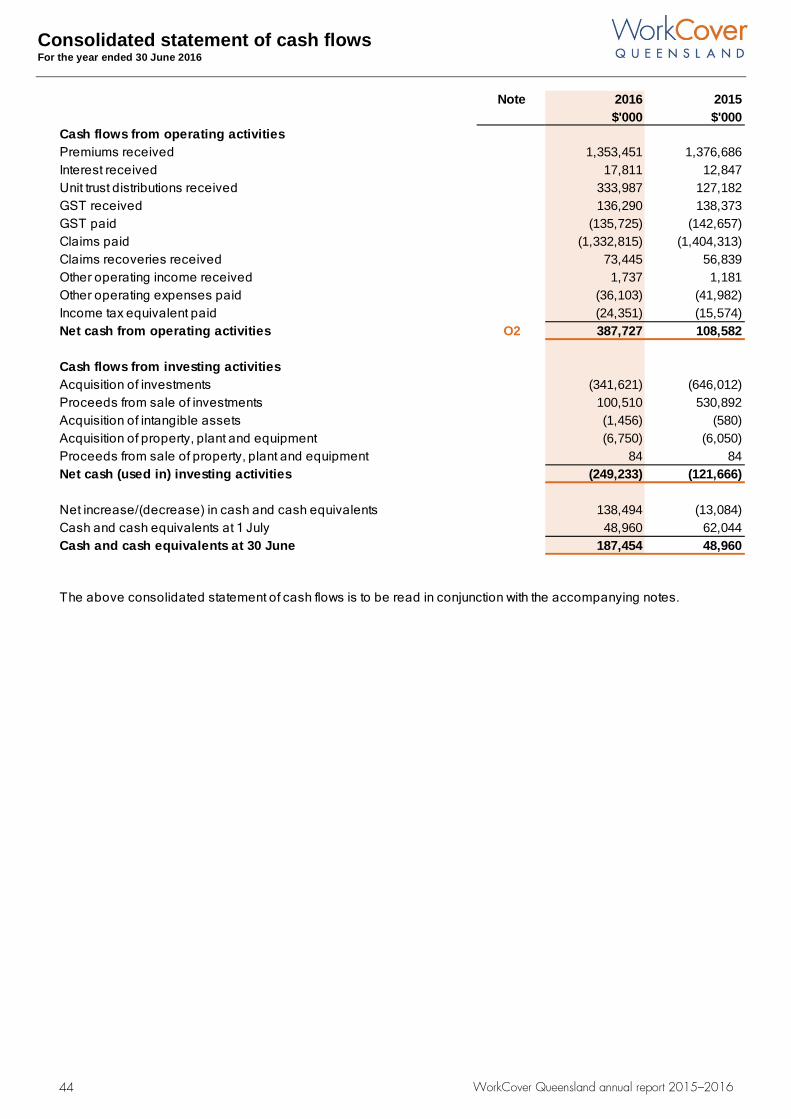

CONSOLIDATED STATEMENT OF CASH FLOWS 44

DECLARATION BY DIRECTORS .......................... 76

INDEPENDENT AUDIT REPORT .......................... 77

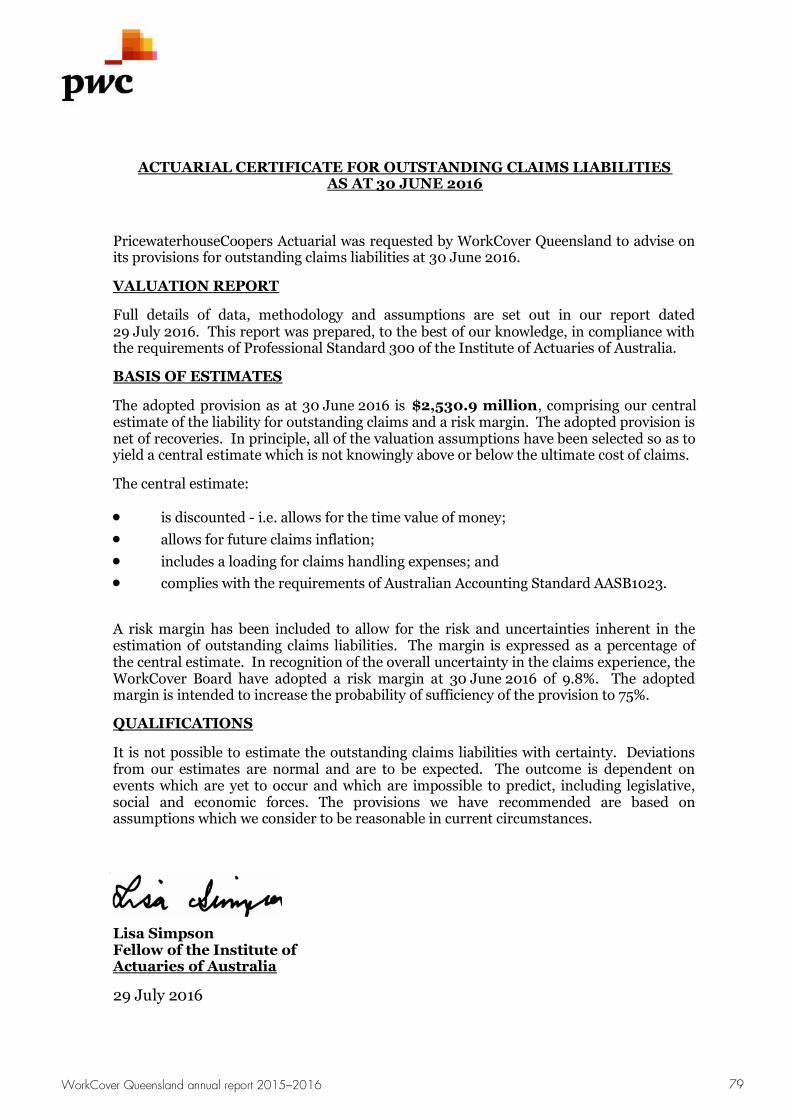

ACTUARIAL CERTIFICATE ON NET OUTSTANDING CLAIMS LIABILITIES ........................................... 79

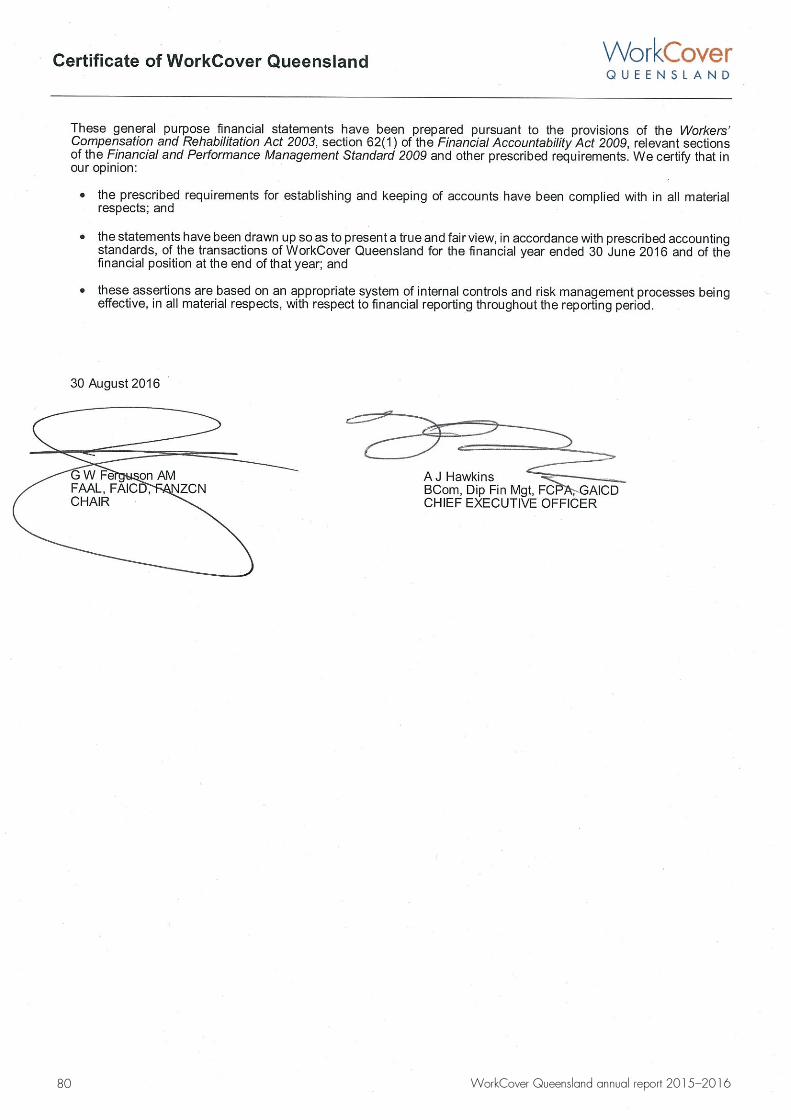

CERTIFICATE OF WORKCOVER QUEENSLAND .. 80

COMPLIANCE CHECKLIST ................................ 81

GLOSSARY ...................................................... 82

NOTES ................................... 45 BASIS OF PREPARATION .................................... 45

SIGNIFICANT ACCOUNTING POLICIES ............... 45

ACCOUNTING JUDGEMENTS AND ESTIMATES ..... 45

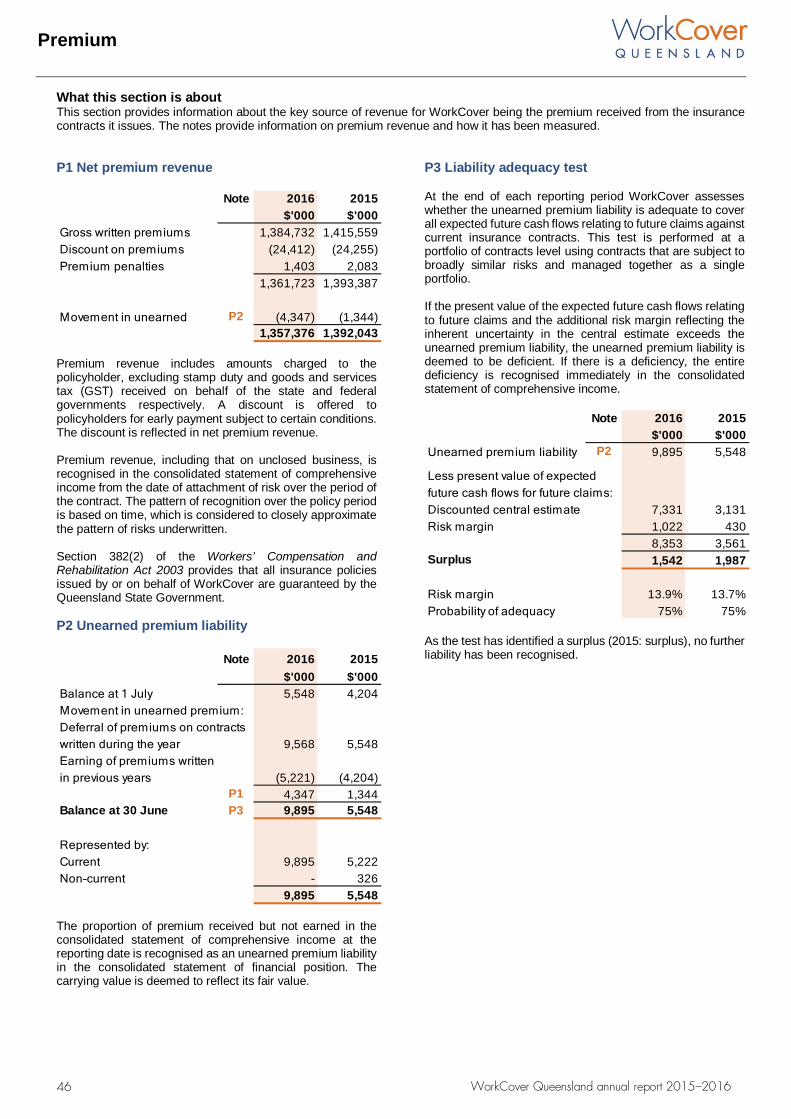

PREMIUM .......................................................... 46

P1 NET PREMIUM REVENUE ................................ 46

P2 UNEARNED PREMIUM LIABILITY ....................... 46

P3 LIABILITY ADEQUACY TEST ............................. 46

CLAIMS ............................................................. 47

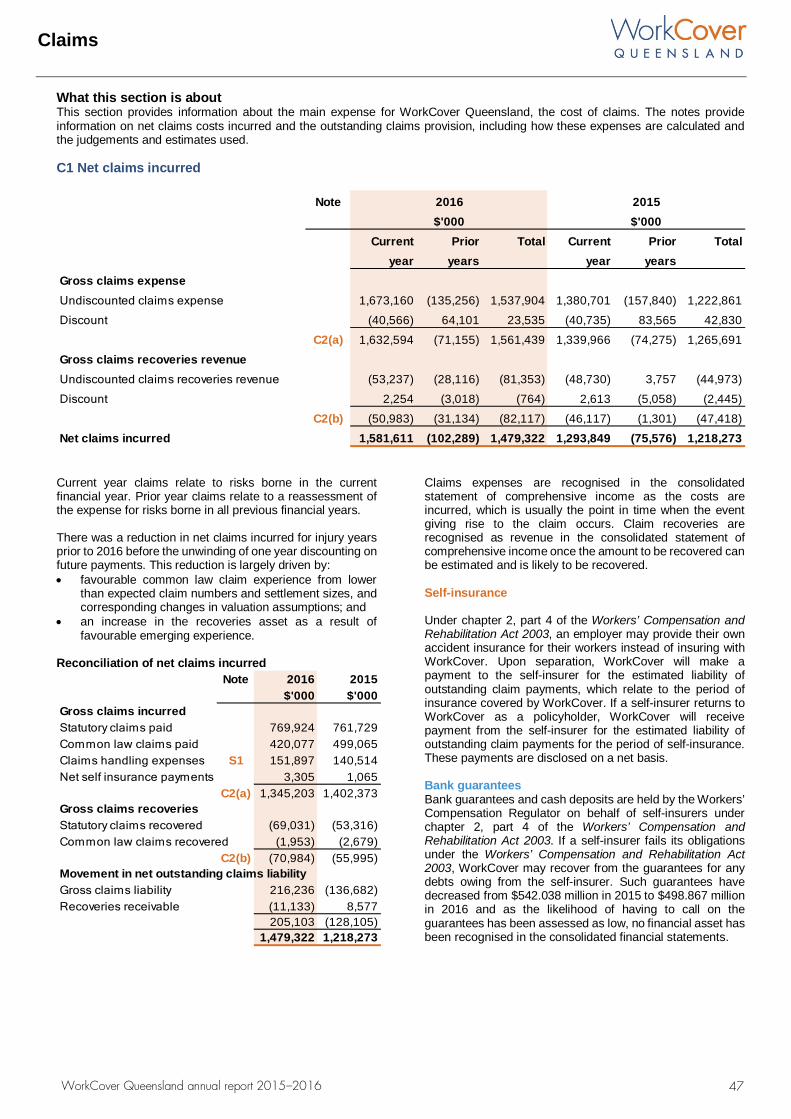

C1 NET CLAIMS INCURRED................................ 47

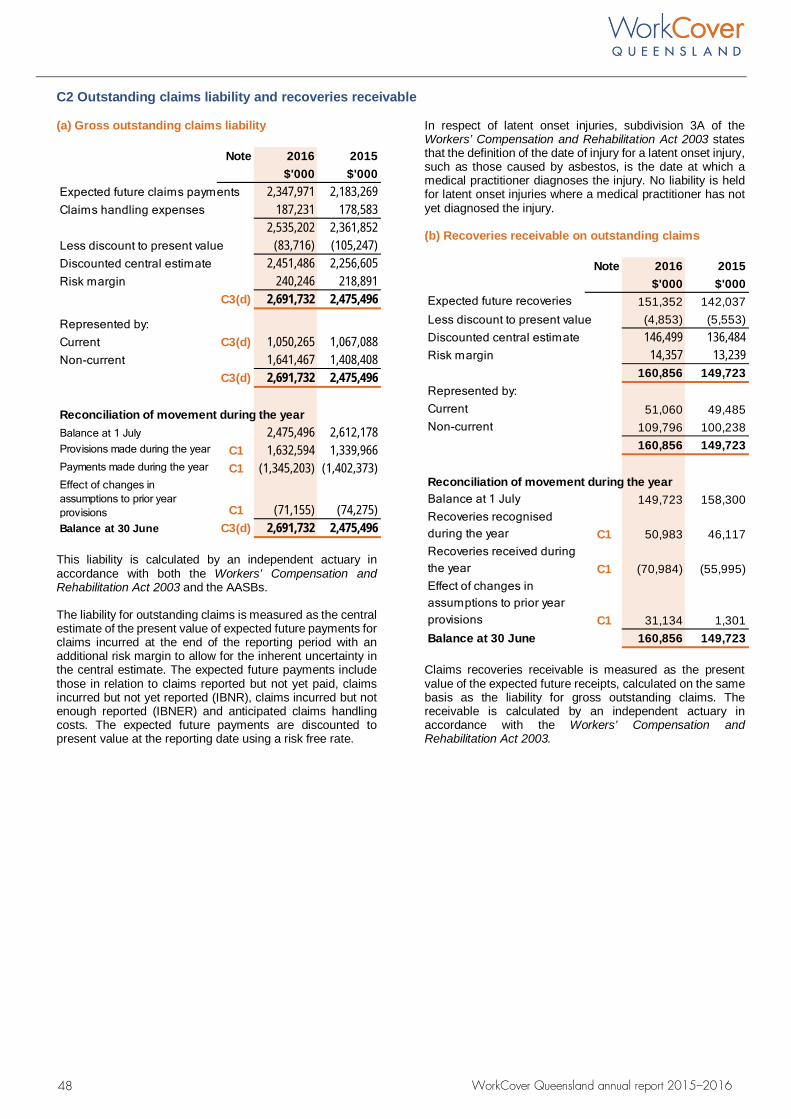

C2 OUTSTANDING CLAIMS LIABILITY AND RECOVERIES RECEIVABLE ................................... 48

C3 INSURANCE RISK ........................................ 52

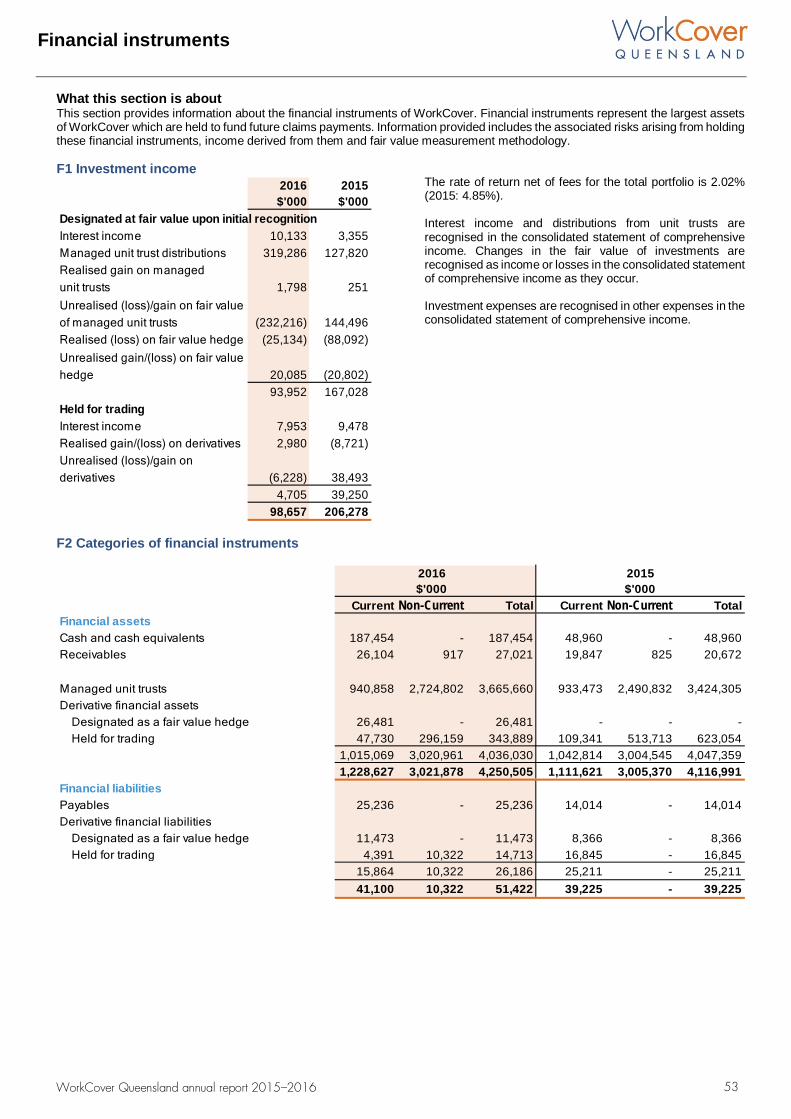

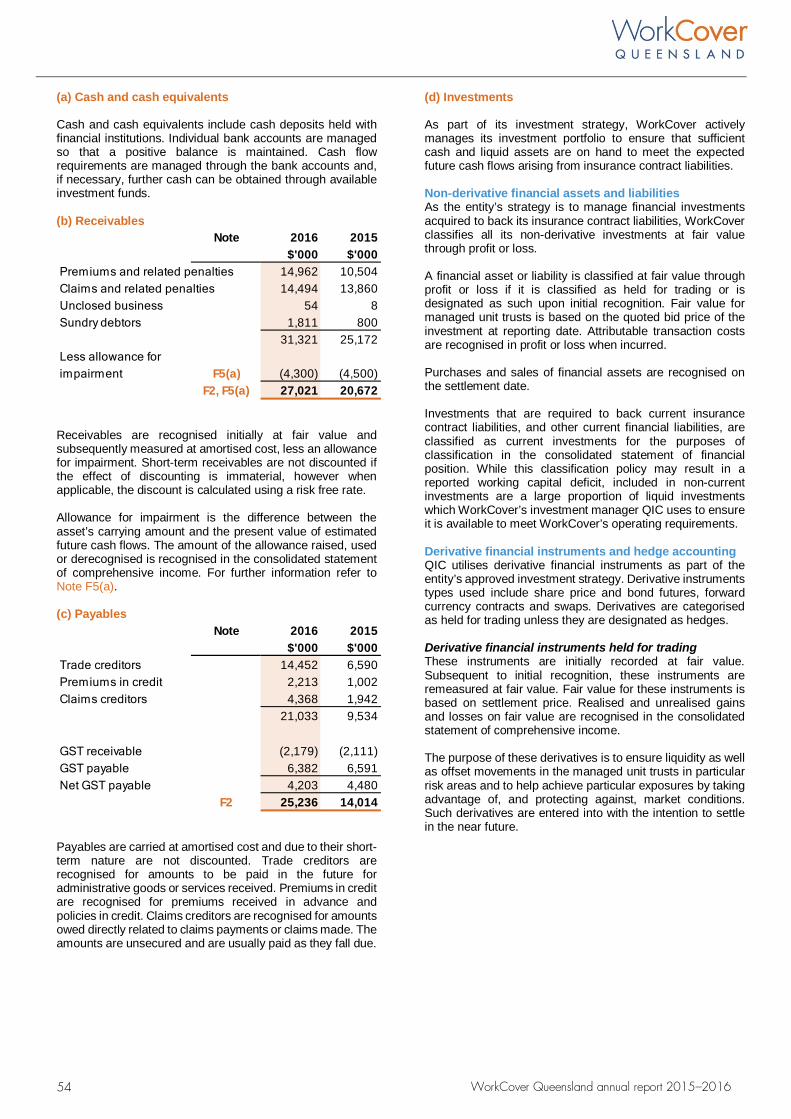

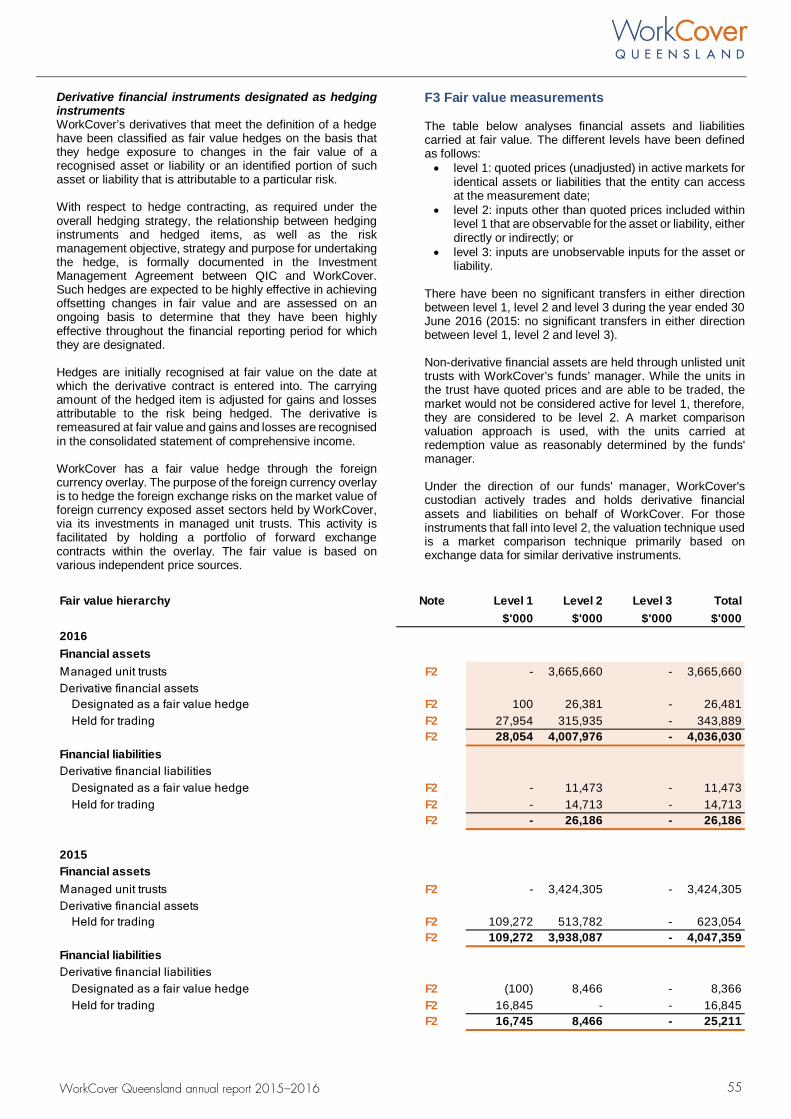

FINANCIAL INSTRUMENTS ................................. 53

F1 INVESTMENT INCOME ................................. 53

F2 CATEGORIES OF FINANCIAL INSTRUMENTS .... 53

F3 FAIR VALUE MEASUREMENTS.......................... 55

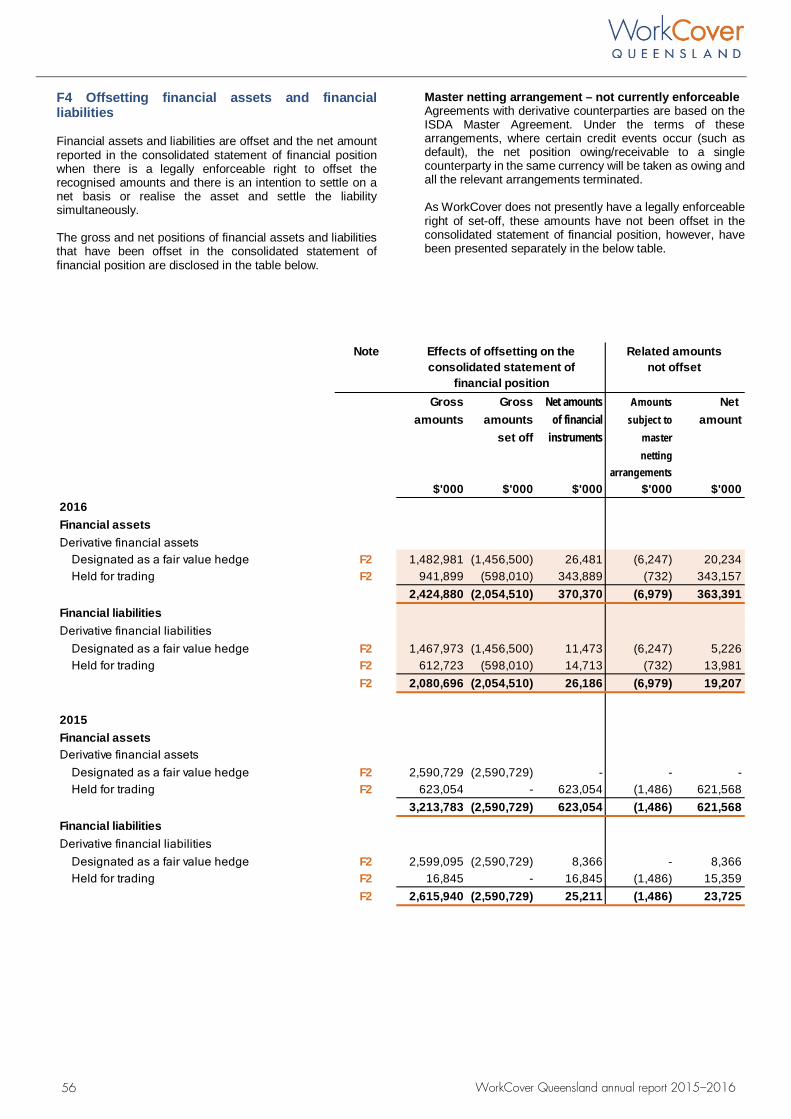

F4 OFFSETTING FINANCIAL ASSETS AND FINANCIAL LIABILITIES ........................................................ 56

F5 FINANCIAL RISK MANAGEMENT .................... 57

SUPPORTING OUR BUSINESS ............................. 61

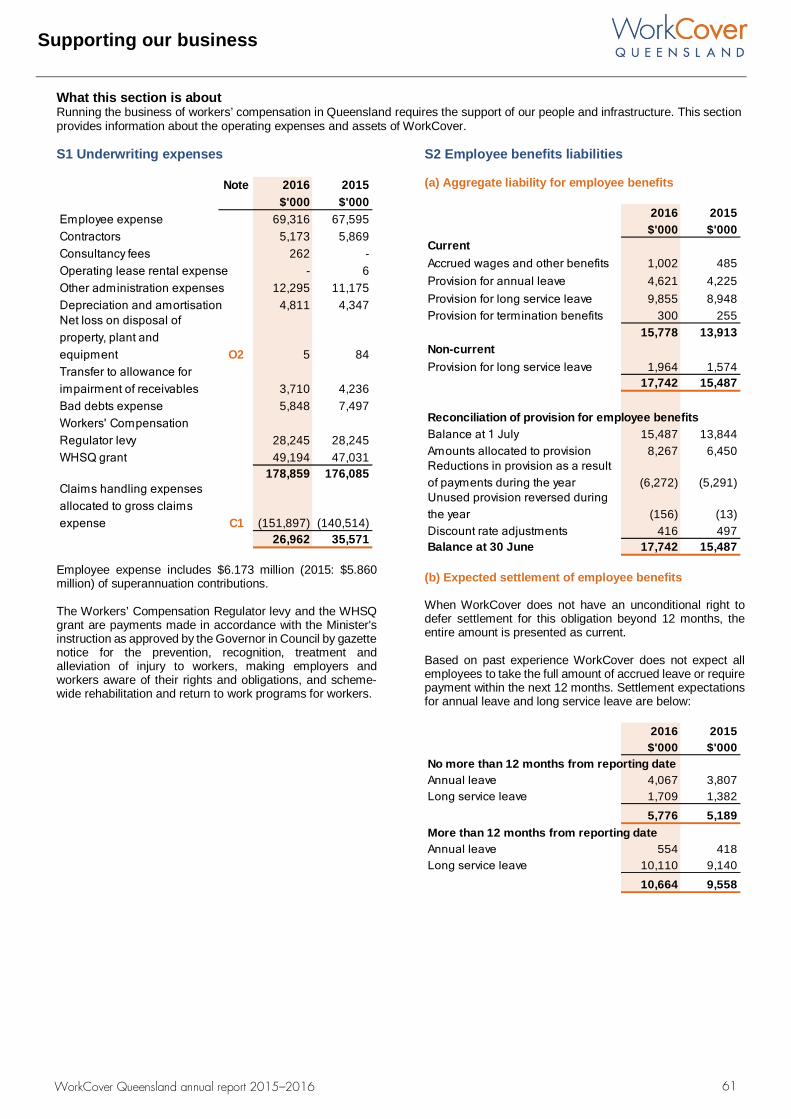

S1 UNDERWRITING EXPENSES ........................... 61

S2 EMPLOYEE BENEFITS LIABILITIES ...................... 61

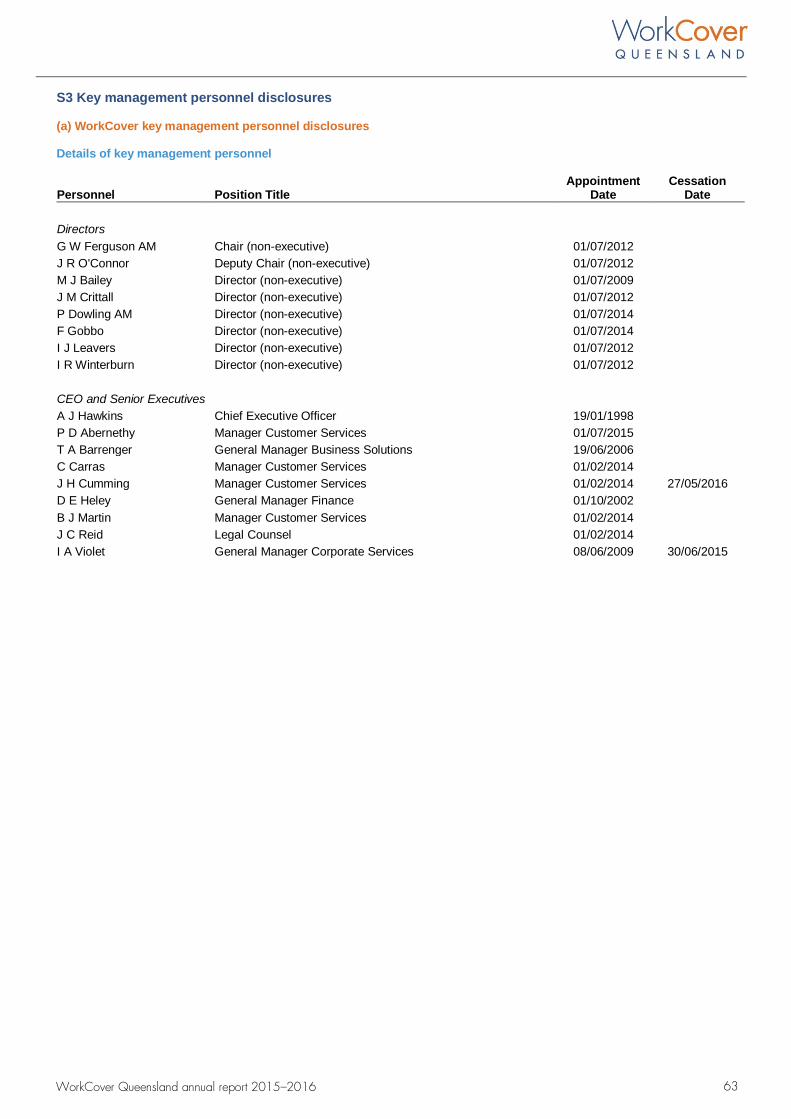

S3 KEY MANAGEMENT PERSONNEL DISCLOSURES 63

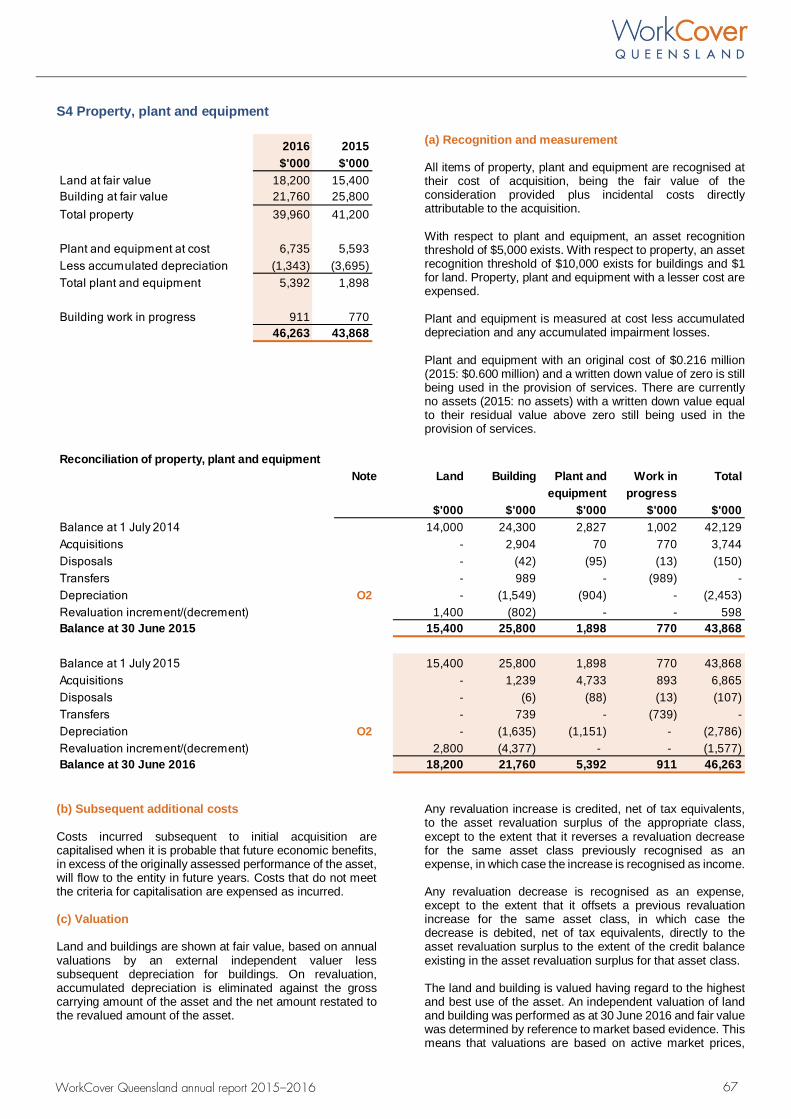

S4 PROPERTY, PLANT AND EQUIPMENT ............... 67

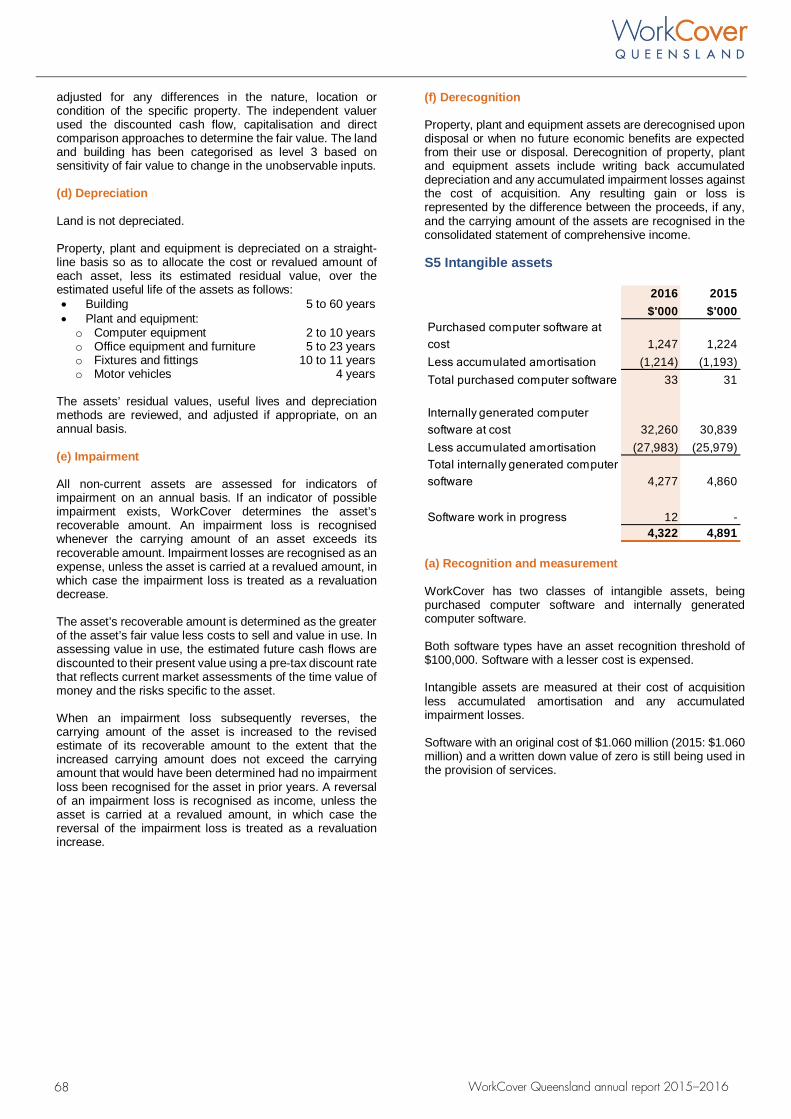

S5 INTANGIBLE ASSETS .................................... 68

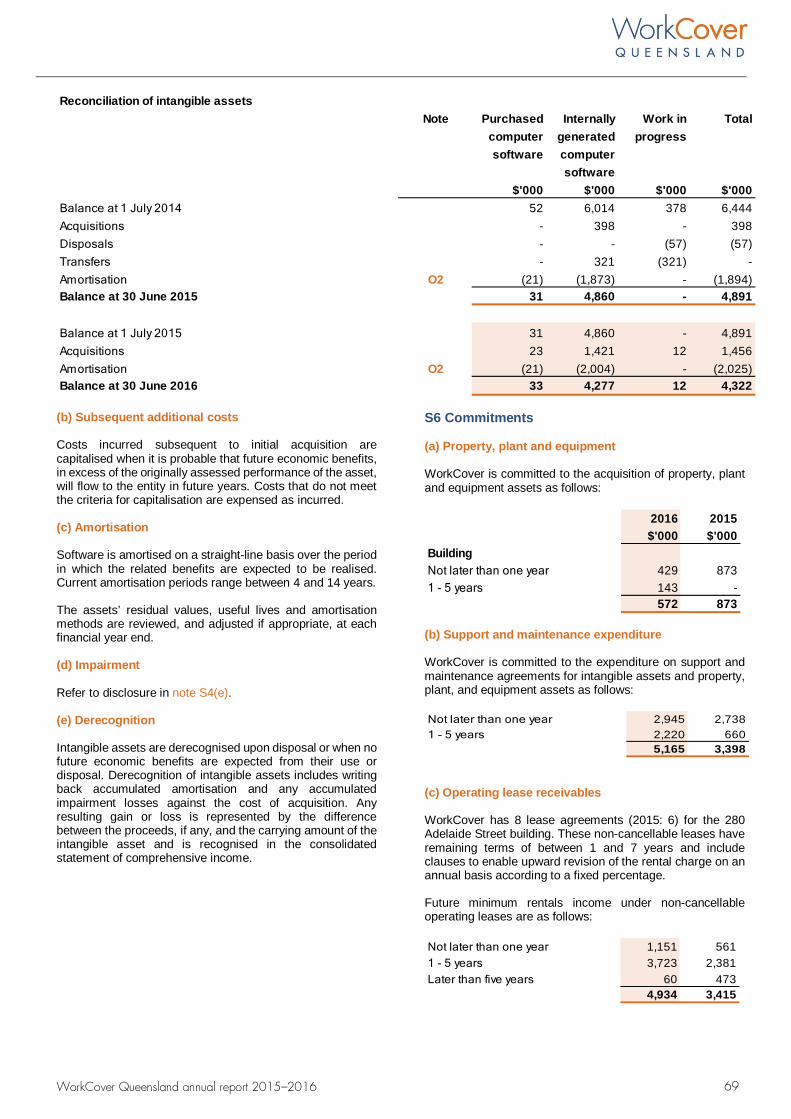

S6 COMMITMENTS .......................................... 69

OTHER .............................................................. 70

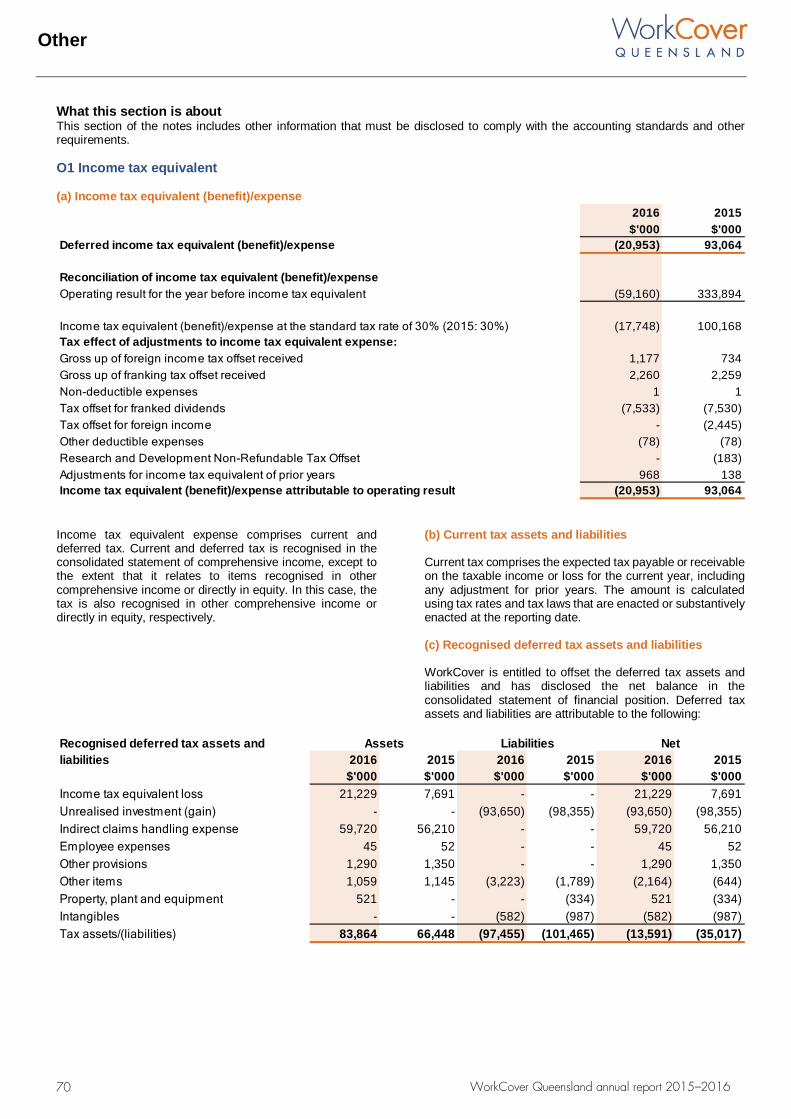

O1 INCOME TAX EQUIVALENT ........................... 70

O2 RECONCILIATION OF CASH FLOWS FROM OPERATING ACTIVITIES ..................................... 72

O3 AUDITORS’ REMUNERATION ......................... 72

O4 CONTINGENT LIABILITIES ............................. 72

O5 EVENTS AFTER REPORTING DATE ................... 72

O6 DIFFERENCES BETWEEN WORKCOVER CONSOLIDATED FINANCIAL STATEMENTS AND WORKCOVER QUEENSLAND FINANCIAL STATEMENTS ................................................... 72

O7 SUMMARY OF ADDITIONAL SIGNIFICANT ACCOUNTING POLICIES ................................... 74

CONTENTS

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS .................................................. 45

4 WorkCover Queensland annual report 2015–2016

QAS paramedic Anthony Windle returned to work with the support of WorkCover Customer Advisor Rebecca Pyke

WELCOME Welcome to WorkCover Queensland’s annual report. This annual report summarises WorkCover’s results, outlook and financial position for 2015–2016.

ABOUT THIS REPORT Under the Workers’ Compensation and Rehabilitation Act 2003, WorkCover is required to produce an annual report. This report has been prepared to meet the needs of stakeholders and the accountability requirements under the Financial Accountability Act 2009.

WorkCover is committed to providing accessible services to Queenslanders from all culturally and linguistically diverse backgrounds. If you have difficulty in understanding the annual report, you can contact us on 1300 362 128 and we will arrange an interpreter to effectively communicate the report to you.

To view this and previous reports, please visit our website worksafe.qld.gov.au.

If you wish to speak to us about this report, please contact:

Communications WorkCover Queensland GPO Box 2459, Brisbane Qld 4001 1300 362 128 [email protected]

ISSN 1329-6539 © WorkCover Queensland 2016

Licence: This annual report is licensed by WorkCover Queensland under a Creative Commons Attribution (CC BY) 4.0 Australia licence.

CC BY Licence Summary Statement: In essence, you are free to copy, communicate and adapt this annual report, as long as you attribute the work to WorkCover Queensland. To view a copy of this licence, visit https://creativecommons.org/licenses/by/4.0/

Attribution: Content from this annual report should be attributed as: WorkCover Queensland annual report 2015–2016

LETTER OF COMPLIANCE

1 September 2016

The Honourable Grace Grace MP Minister for Employment and Industrial Relations Minister for Racing and Minister for Multicultural Affairs GPO Box 611 BRISBANE QLD 4001

Dear Minister

I am pleased to present the 2015–2016 WorkCover Queensland annual report.

I acknowledge the contributions of our Board and, most of all, the hard work and dedication of our people, each of whom have helped us to care about our customers and provide appropriate workers’ compensation cover.

I certify that this annual report complies with:

• the requirements under the Workers’Compensation and Rehabilitation Act2003

• the prescribed requirements of theFinancial Accountability Act 2009 and the Financial Performance Management Standard 2009, and

• the detailed requirements set out in theAnnual report requirements for Queensland Government agencies.

A checklist outlining the annual reporting requirements can be found at page 43.

Yours sincerely

Glenn Ferguson AM

Chair

5

WorkCover Queensland annual report 2015–2016

Who we are

WorkCover Queensland is a self-funded statutory authority providing tailored workers’ compensation insurance solutions to over 150,000 Queensland businesses since 1997.

WorkCover strives to maintain Australia’s lowest average premium rate by continuously investing in efficient online customer services and experienced in-house claims management capability to support employers and injured workers.

We maintain one of Australia’s best return to work rates by partnering with our customers, unions, industry associations, medical and allied health providers.

We are passionate about striking the right balance between keeping premium costs low for employers and providing injured workers with access to rehabilitation and return to work services.

The principal place of business for WorkCover Queensland is 280 Adelaide Street, Brisbane, Queensland 4000.

Working together

WorkCover partners with various government agencies to give Queensland businesses and the broader community efficient access to specialist advice on safety, rehabilitation, return to work and workers’ compensation matters.

ABOUT WORKCOVER

6 WorkCover Queensland annual report 2015–2016

CUSTOMER SERVICE COMMITMENT WorkCover Queensland is committed to providing exceptional service and partnering with our customers and stakeholders.

Our values of excellence, integrity, responsiveness and respect are incorporated into everything we do.

Service

WorkCover’s aim is to deliver excellent customer service and to make doing business with us easy. We will always strive to meet our customers’ expectations by:

• personally answering calls during business hours• listening first, then responding in a timely way• communicating openly and in plain language• providing contact details of a person to assist• being fair and impartial in all our interactions.

Engagement WorkCover cares about its customers and stakeholders and wants to engage with them in a positive way for mutual benefit through:

• understanding individual requirements• asking how we can improve• providing regular updates• proactively building relationships• offering value added services.

Recovery from injury WorkCover is here to support the often difficult and emotional experience of a work-related injury. We are committed to assisting people to recover at work and liaising with all parties involved to achieve the best possible outcome by:

• communicating regularly with everyone involved• undertaking necessary rehabilitation• facilitating early, safe and appropriate return to work• providing support to reduce the impact of the injury• assisting to reduce the disruption an injury can cause.

Information and feedback WorkCover values customer and stakeholder feedback to help continually improve services. We are also committed to protecting the privacy of our customers. We take all reasonable precautions to protect the information given to us by:

• storing your personal information securely• allowing access to information quickly and easily.

7

WorkCover Queensland annual report 2015–2016

CORPORATE PLAN 2015–2019 Who we are

WorkCover Queensland is the main provider of workers’ compensation insurance in Queensland. We are a government owned statutory body established under the Workers’ Compensation and Rehabilitation Act 2003.

Our vision

To excel in workers’ compensation insurance by providing the best possible benefits and return to work programs for workers, at the lowest possible sustainable premium for employers.

Our values

Excellence

To deliver customer satisfying services

Integrity

To always do the right thing

Responsiveness

To respond in a timely and welcoming way and deliver solutions

Respect

To be considerate of the rights and dignity of others

Our customers

Our customers are injured workers and employers, supported by various stakeholder groups.

Challenges

• influencing employers to prevent and better manage injuries • achieving optimal stay at/return to work outcomes • engaging with customers and stakeholders to achieve mutually beneficial outcomes • delivering focused/relevant customer communication and education • retaining a financially viable customer base • streamlining and enhancing customer experience through the use of technology • maintaining an engaged workforce.

8 WorkCover Queensland annual report 2015–2016

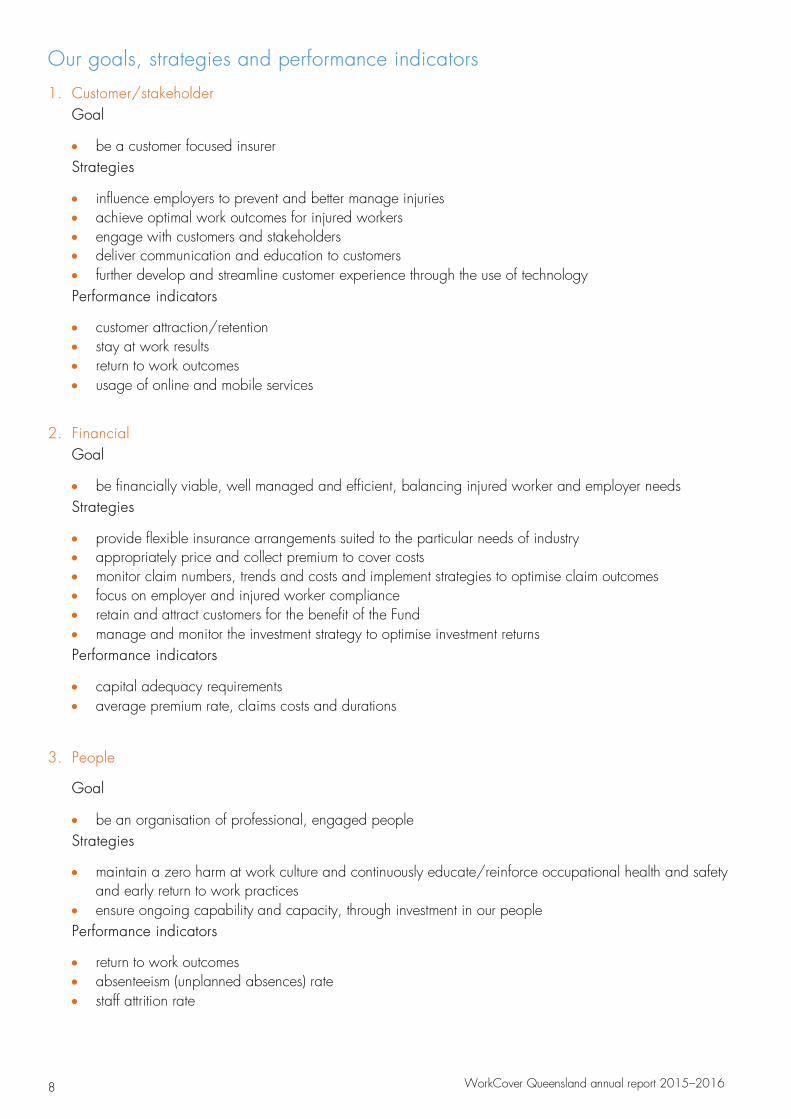

Our goals, strategies and performance indicators

1. Customer/stakeholderGoal

• be a customer focused insurerStrategies

• influence employers to prevent and better manage injuries• achieve optimal work outcomes for injured workers• engage with customers and stakeholders• deliver communication and education to customers• further develop and streamline customer experience through the use of technologyPerformance indicators

• customer attraction/retention• stay at work results• return to work outcomes• usage of online and mobile services

2. FinancialGoal

• be financially viable, well managed and efficient, balancing injured worker and employer needsStrategies

• provide flexible insurance arrangements suited to the particular needs of industry• appropriately price and collect premium to cover costs• monitor claim numbers, trends and costs and implement strategies to optimise claim outcomes• focus on employer and injured worker compliance• retain and attract customers for the benefit of the Fund• manage and monitor the investment strategy to optimise investment returnsPerformance indicators

• capital adequacy requirements• average premium rate, claims costs and durations

3. People

Goal

• be an organisation of professional, engaged peopleStrategies

• maintain a zero harm at work culture and continuously educate/reinforce occupational health and safetyand early return to work practices

• ensure ongoing capability and capacity, through investment in our peoplePerformance indicators

• return to work outcomes• absenteeism (unplanned absences) rate• staff attrition rate

9 WorkCover Queensland annual report 2015–2016

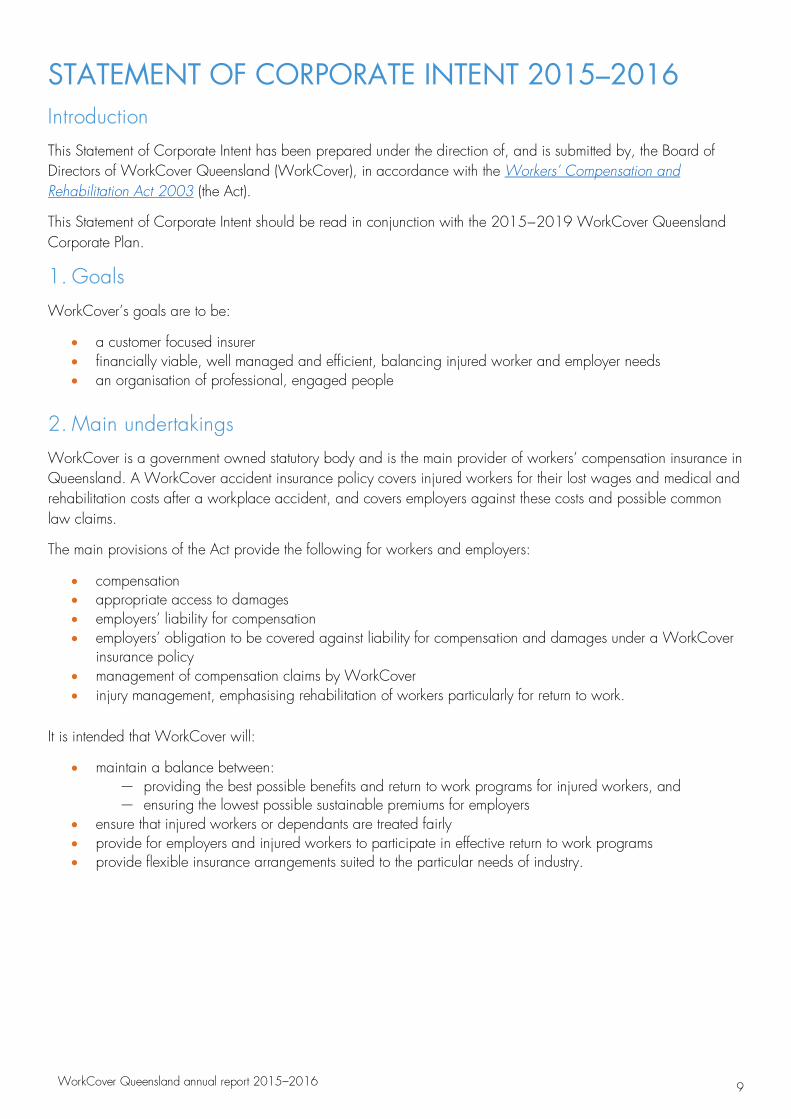

STATEMENT OF CORPORATE INTENT 2015–2016 Introduction

This Statement of Corporate Intent has been prepared under the direction of, and is submitted by, the Board of Directors of WorkCover Queensland (WorkCover), in accordance with the Workers’ Compensation and Rehabilitation Act 2003 (the Act).

This Statement of Corporate Intent should be read in conjunction with the 2015−2019 WorkCover Queensland Corporate Plan.

1. Goals

WorkCover’s goals are to be:

• a customer focused insurer• financially viable, well managed and efficient, balancing injured worker and employer needs• an organisation of professional, engaged people

2. Main undertakings

WorkCover is a government owned statutory body and is the main provider of workers’ compensation insurance in Queensland. A WorkCover accident insurance policy covers injured workers for their lost wages and medical and rehabilitation costs after a workplace accident, and covers employers against these costs and possible common law claims.

The main provisions of the Act provide the following for workers and employers:

• compensation• appropriate access to damages• employers’ liability for compensation• employers’ obligation to be covered against liability for compensation and damages under a WorkCover

insurance policy• management of compensation claims by WorkCover• injury management, emphasising rehabilitation of workers particularly for return to work.

It is intended that WorkCover will:

• maintain a balance between:— providing the best possible benefits and return to work programs for injured workers, and — ensuring the lowest possible sustainable premiums for employers

• ensure that injured workers or dependants are treated fairly• provide for employers and injured workers to participate in effective return to work programs• provide flexible insurance arrangements suited to the particular needs of industry.

10 WorkCover Queensland annual report 2015–2016

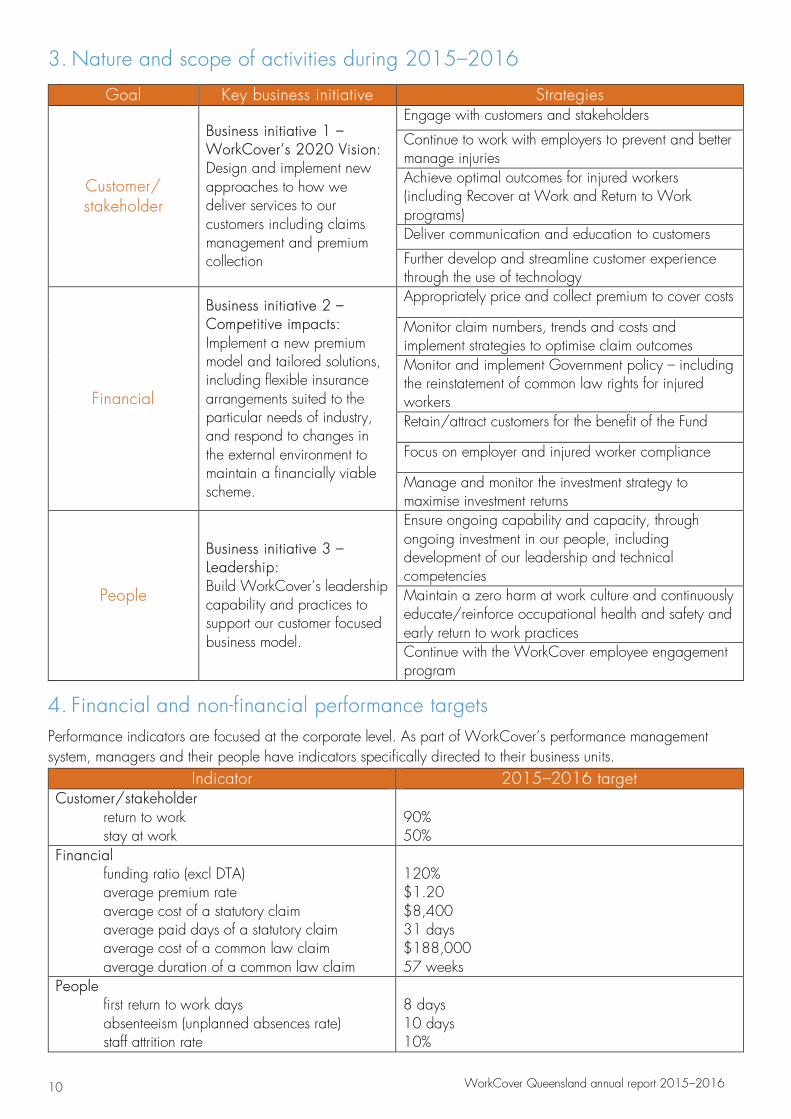

3. Nature and scope of activities during 2015–2016

Goal Key business initiative Strategies

Customer/ stakeholder

Business initiative 1 – WorkCover’s 2020 Vision: Design and implement new approaches to how we deliver services to our customers including claims management and premium collection

Engage with customers and stakeholders

Continue to work with employers to prevent and better manage injuries Achieve optimal outcomes for injured workers (including Recover at Work and Return to Work programs) Deliver communication and education to customers

Further develop and streamline customer experience through the use of technology

Financial

Business initiative 2 – Competitive impacts: Implement a new premium model and tailored solutions, including flexible insurance arrangements suited to the particular needs of industry, and respond to changes in the external environment to maintain a financially viable scheme.

Appropriately price and collect premium to cover costs

Monitor claim numbers, trends and costs and implement strategies to optimise claim outcomes Monitor and implement Government policy – including the reinstatement of common law rights for injured workers Retain/attract customers for the benefit of the Fund

Focus on employer and injured worker compliance

Manage and monitor the investment strategy to maximise investment returns

People

Business initiative 3 – Leadership: Build WorkCover’s leadership capability and practices to support our customer focused business model.

Ensure ongoing capability and capacity, through ongoing investment in our people, including development of our leadership and technical competencies Maintain a zero harm at work culture and continuously educate/reinforce occupational health and safety and early return to work practices Continue with the WorkCover employee engagement program

4. Financial and non-financial performance targetsPerformance indicators are focused at the corporate level. As part of WorkCover’s performance management system, managers and their people have indicators specifically directed to their business units.

Indicator 2015–2016 target Customer/stakeholder

return to work stay at work

90% 50%

Financial funding ratio (excl DTA) average premium rate average cost of a statutory claim average paid days of a statutory claim average cost of a common law claim average duration of a common law claim

120% $1.20 $8,400 31 days $188,000 57 weeks

People first return to work days absenteeism (unplanned absences rate) staff attrition rate

8 days 10 days 10%

11 WorkCover Queensland annual report 2015–2016

5. Capital structure and payments to the consolidated fund

In accordance with the Act, WorkCover is taken to be fully funded if it is able to meet its liabilities for compensation and damages payable from its funds and accounts and maintain capital adequacy as required under the Workers’ Compensation and Rehabilitation Regulation 2014 (the Regulation). The Regulation states that in order to maintain capital adequacy, WorkCover’s total assets must at least be equal to total liabilities (this correlates to a funding ratio of 100%).

The Act allows for payments to be made to the consolidated fund. The WorkCover Board will make a recommendation to the Minister with respect to such a payment (if any) following certification of the 2014−2015 financial statements.

WorkCover will also contribute to levies administered by the Regulator by way of an annual levy.

6. Borrowings made, proposed to be made

WorkCover currently has no borrowings and there are none planned for the immediate future. Investment funds are used to manage all cash flow requirements. WorkCover’s borrowing policy is outlined in 7.3.

7. Policies adopted to minimise and manage risk of investments andborrowings that may adversely affect financial stability

7.1 Investment risk

WorkCover currently invests all excess funds with QIC. WorkCover maintains a balanced investment profile with a long-term outlook commensurate with being a long-term insurance operation. Derivative instruments are used as part of the investment strategy to hedge foreign exchange risks and rebalance asset classes.

An Investment Management Agreement governs the arrangement. In addition, the WorkCover Board monitors investment on a monthly basis and receives at least quarterly presentations from QIC. The Board reviews the investment strategy annually.

7.2 Business risk

WorkCover has a risk management program in place. Risk registers are maintained and monitored by each business division. Strategies to manage risk are incorporated into each division’s business planning process. The WorkCover Risk and Audit Committee is responsible for overseeing the risk management program, including reviewing and monitoring WorkCover’s top strategic risks on a quarterly basis.

7.3 Borrowing risk

The Act provides the framework for WorkCover’s procedures for borrowing. WorkCover may enter into such arrangements to procure equipment up to an amount and on such terms as it considers appropriate. All financing arrangements will be made in conjunction with Queensland Treasury Corporation in order to establish that applicable rates are competitive and conditions are appropriate. Board approval will be required for all financing arrangements over pre-defined expenditure limits. All limits are as stated in the WorkCover delegations manual.

8. Policies and procedures relating to acquisition and disposal of major assets

In acquiring or disposing of major assets, WorkCover complies with the Financial and Performance Management Standard 2009 and Queensland Treasury guideline—Non-Current Asset Policies for the Queensland Public Sector.

Major assets may be acquired via purchase, finance lease agreement, donations, or transfer from other government entities. A business case must be submitted to the CEO and/or General Manager Finance seeking approval. The CEO will present any major initiatives to the Board for approval. Approval limits are as stated in the WorkCover delegations manual.

12 WorkCover Queensland annual report 2015–2016

In disposing of major assets, approval must be sought from the appropriate delegated authority. Approval limits are as stated in the WorkCover delegations manual.

9. Accounting policies applying to preparation of accounts

WorkCover’s accounting policies are outlined each year in the Annual Report and are reviewed as part of the financial statements audit process. Further information on accounting policies is provided in WorkCover’s Financial Management Practice Manual (FMPM).

10. Community service obligations

It is not envisaged that the government will require WorkCover to perform any specific community service obligations.

11. Employment and industrial relations plan

WorkCover prepare an Employment and Industrial Relations Plan annually in accordance with the Act. Refer to Attachment 1 for a copy of WorkCover Queensland’s Employment and Industrial Relations Plan.

12. Information to be reported to the Minister

12.1 Quarterly reporting

A quarterly report will be provided to the Minister within one month of the end of the relevant quarter as required by the Act. The report will contain information regarding WorkCover’s performance against the Statement of Corporate Intent.

12.2 Annual reporting

A full annual report will be provided to the Minister in accordance with the Act and in compliance with the Financial and Performance Management Standard 2009, which requires WorkCover to give the annual report to the Minister to allow the report to be tabled in the Legislative Assembly within three months after the conclusion of each financial year.

13

WorkCover Queensland annual report 2015–2016

EMPLOYERS DECLARED THEIR WAGES ONLINE IN 2015

600

EMPLOYERS RECEIVED CASE MANAGEMENT ASSISTANCE IN INJURY PREVENTION AND MANAGEMENT PROGRAM

1,000

108,000 10,200

150,000

LendLease Injury Management Advisor (Qld) Shane Ham with WorkCover Customer Services Manager Tammy Constant

HIGHLIGHTS

INJURED WORKERS RETURNED TO WORK

EMPLOYERS INSURED

OVER EMPLOYERS USE WORKCOVER CONNECT

EMPLOYERS VISITED IN QLD BY OUR COMPLIANCE AND EDUCATION ADVISORS

OVER

OVER

14

WorkCover Queensland annual report 2015–2016

PERFORMANCE SCORECARD The following scorecard provides an overview of our performance, including targets from our Statement of Corporate Intent.

AIM WHAT DID WE ACHIEVE?

CUSTOMER/STAKEHOLDER

90% return to work 92%

50% stay at work 49.6%

FINANCIAL

Funding ratio (excl DTA) of 120% 162%

Average premium rate of $1.20 $1.20

Average cost of a statutory claim: $8,400 $8,252

Average paid days of a statutory claim: 31 days 27.8 days

Average cost of a common law claim: $188,000 $172,557

Average duration of a common law claim: 57 weeks 58.2 weeks

PEOPLE

First return to work days : 8 4.3 days

Absenteeism (unplanned absences rate): 10 days 10.8 days

Staff attrition rate: 10% 9.2%

15

WorkCover Queensland annual report 2015–2016

We are pleased to present the WorkCover Queensland Annual Report for 2015–2016. During the year, we continued to work together with our customers and stakeholders to provide the best possible rehabilitation and return to work support for workers and sustainable premiums for employers.

Maintained lowest premium rate in Australia

For the third consecutive year, we are pleased to maintain an average premium rate of $1.20 per $100 of wages for 2016–2017, the lowest rate in Australia. We are committed to working with and educating our customers on the benefits of maintaining safe and healthy work environments and assisting workers to return to work quickly and safely following injury.

Implementing legislative reforms

During the year, WorkCover worked closely with stakeholders to support the implementation of legislative reforms, including provisions for specified diseases developed by firefighters and the removal of the common law threshold.

WorkCover will continue to work with all stakeholders associated with these legislative reforms to ensure consistent and fair coverage is provided for customers.

Co-creating tailored solutions

This year we worked with our customers to tailor solutions which can optimise their business outcomes. We supported employers through the Prevention and Performance Initiative, a grant program designed to help innovative businesses reduce injuries and enhance return to work outcomes. Over 130 applications were received from businesses across all industry sectors. Together with these businesses, WorkCover is co-funding initiatives which will be implemented throughout 2016.

During the year, we launched employer education and awareness campaigns aimed at reducing the cost and frequency of claims associated with mental health disorders and musculoskeletal injuries.

Employer feedback for our mental health campaign was positive, with employers indicating they are now more confident in managing health and wellbeing issues in the workplace. Employers welcomed the tailored advice and injury data provided by our people, with many indicating they are likely to increase their investment in mental health and wellbeing management.

Promoting the health benefits of good work

During the year, our Recover at Work program facilitated successful temporary employment placements at host employers for injured workers who are unable to return to work with their pre-injury employer.

We also maintained our focus on delivering positive return to work outcomes. Working closely with medical and allied health providers, we promoted the benefits of good work, early rehabilitation and return to work support following an injury and regular communication between all parties to an injury.

CHAIR AND CEO REPORT

16

WorkCover Queensland annual report 2015–2016

Enhancing our service delivery experience

In late 2015, we launched WorkCover Connect, an online service for employers that delivers industry specific trends, claims and injury tracking, and up-to-date data and policy analytics. Over 10,200 employers are using WorkCover Connect as their platform of choice to manage their workers’ compensation policy.

During the year, we engaged with our customers and stakeholders to better understand which aspects of our service they value and how they want to work with us in the future. We have incorporated this feedback into our planning for the coming year as we continually improve the way we work and provide a customer experience that delivers excellent return to work outcomes for workers at the lowest cost for Queensland businesses.

Committed and engaged people

In April, we received approval from the Queensland Industrial Relations Commission for the WorkCover Employing Office Certified Agreement (CA). The Agreement, which expires on 30 September 2018, demonstrates WorkCover’s commitment to work closely with union representatives through our consultative committee to ensure a positive working relationship that will benefit WorkCover’s people.

During the year, we strengthened the leadership capabilities and behavioural competencies of our people with the delivery of an integrated training program targeting championing change and innovation through teamwork and collaboration, enhancing customer relationships and maximising strategic effectiveness with a focus on operational excellence.

Financial and investment performance

Against the backdrop of a challenging national economic environment and a transitioning Queensland economy, WorkCover’s operating result for 2015–2016 was a loss of $38.2 million, after tax.

The net return on our investment portfolio was 2.02% (2014–2015: 4.85%) reflecting adverse financial market conditions experienced during the year.

QIC manages WorkCover’s investments and as at 30 June 2016, the net market value in funds invested was $4.01 billion (30 June 2015: $4.022 billion). We will continue to work with QIC to ensure our portfolio achieves its long term objectives.

WorkCover continues to be fully funded and will maintain a strong financial position as a direct result of our disciplined financial management, prudent investment approach and cost control focus.

Outlook

Over the next 12 months, WorkCover will continue to work with our people, customers and stakeholders to improve our service delivery, ensuring our people and customers are supported by technology and data analytics to achieve the best possible outcomes.

We will continue to enhance our innovative online services for employers and workers, so they receive a high quality experience across our service channels.

Our state-wide compliance and education activities program will target under-insured and uninsured businesses, ensuring they have the right cover and every Queensland employer is paying their fair share.

WorkCover will also work with stakeholders to implement arrangements to support the introduction of legislative reforms.

Thank you

We would like to thank and acknowledge the hard work of our Board members, Executive Management Team, and all our people for their commitment to achieving the best results for Queensland’s workers and employers.

17 WorkCover Queensland annual report 2015–2016

We also thank the Minister for Employment and Industrial Relations, the Honourable Grace Grace MP, and the Queensland Government for their support.

Glenn Ferguson Tony Hawkins

Chair CEO

Postscript to this report – message from the Chair, Glenn Ferguson

The Board wishes to announce that WorkCover CEO, Tony Hawkins will retire in December 2016. During 19 years of outstanding service, Tony has worked with Government, the Board and WorkCover’s people and customers to build an organisation that is financially sustainable and providing the best possible rehabilitation and return to work support for workers at Australia’s lowest premium rates.

The Board and WorkCover’s Executive Management Team would like to thank Tony for his commitment and significant leadership contribution in transforming WorkCover’s operations. He leaves the organisation in outstanding shape and well placed to deliver on our strategy of making WorkCover the best workers’ compensation insurer in Australia.

18 WorkCover Queensland annual report 2015–2016

BOARD OF DIRECTORS Glenn Ferguson AM, FAAL, FAICD, FANZCN, FCOL Chair

Glenn is a Director of Ferguson Cannon, Lexon Insurance and the Queensland Law Foundation. He is a Solicitor of the High Court of Australia and the Supreme Court of Queensland. He was made a Member of the Order of Australia in 2015.

Justin O'Connor BA Deputy Chair

Justin is a Director at Intrust Super Fund and IS Financial Planning Pty Ltd and recently retired as Chief Executive of the Queensland Hotels Association Union of Employers. Justin is a member of the Queensland Responsible Gambling Advisory Committee and delegate to the National Executive of the Australian Hotels Association.

Melinda Bailey BCom (Hons), FCPA, FAICD Director

Melinda is the Director, Regulatory Reform at NSW Maritime and Road Services. Melinda is a Fellow CPA and is a Fellow of the Australian Institute of Company Directors. Melinda is also the Chairperson of WorkCover's Risk and Audit Committee.

John Crittall BEcon (Hons), MAdmin (IR) Director

John has extensive experience providing strategic guidance in the key areas of industrial relations, workplace health and safety and legislative compliance. He was formerly a Director at Master Builders, a role he held for over 10 years. John is a Director of the Work Health and Safety Queensland Board and CIPQ.

Peter Dowling AM, BA (Acc), FCPA, FAICD Director

Peter is an accountant and company director, a Fellow of CPA Australia and Chartered Accountants Australia and New Zealand, and a Fellow of The Australian Institute of Company Directors. He was formerly a partner with international accounting firm Ernst & Young, is a Centenary of Federation Medal recipient and was made a Member of the Order of Australia in 2007.

19

WorkCover Queensland annual report 2015–2016

Flavia Gobbo BA/LLB, GAICD Director

Flavia is a Solicitor of the High Court of Australia and the Supreme Court of Queensland and has extensive experience as a senior corporate lawyer with one of Australia’s top publicly listed companies. She was previously Chair of Q-COMP and is a Director of Rowing Australia and SecondBite.

Ian Leavers Director

Ian is General President and CEO of the Queensland Police Union of Employees and has held this position since 2009. He has been involved with the Queensland Police Union and as a Union official since 1997. Ian is also a Director of the Work Health and Safety Queensland Board.

Roslyn McLennan BEcon Director

Roslyn was appointed to the Board on 7 July 2016. She is currently General Secretary of the Queensland Council of Unions, a Director of Sunsuper and was formerly Assistant General Secretary of the Queensland Independent Education Union.

Ian Winterburn Dip Acc, BEcon, MBEcon (Hons) Director

Ian is the Deputy Chairperson of the National Retail Association. He has a wide range of senior financial and operational management experience in the construction, hotel, manufacturing and retail industries and has been associated with major Queensland and national companies over the past 40 years.

20 WorkCover Queensland annual report 2015–2016

EXECUTIVE TEAM Tony Hawkins BCom, Dip Fin Mgt, FCPA, GAICD Chief Executive Officer

Tony has led WorkCover Queensland as Chief Executive Officer since 1998. Prior to this, Tony had 13 years' insurance experience with the AXA Group and 14 years' mining experience with CSR. As Chief Executive Officer, Tony has continued to guide WorkCover with a clear focus on continuing excellence and delivering customer focused services.

Trevor Barrenger BA, GAICD General Manager Business Solutions

Trevor has had extensive experience in the delivery of business solutions and technology systems in a number of global consulting organisations. He has had the opportunity to work on large projects across Europe, America and Australia, and his experience supports his ability to deliver technology solutions to meet WorkCover's business needs and customer service outcomes.

David Heley BAdmin, FCPA, DFP, AGIA, GAICD General Manager Finance

David has more than 20 years' experience in the finance and insurance sector. As General Manager Finance, David ensures WorkCover maintains a strong financial position. His division provides financial strategy, reporting and analysis, taxation, treasury, compliance, and audit functions that support the business. David is also the company secretary.

Paul Abernethy MBA Lead Customer Experience, Trade Services

Paul has worked in the workers’ compensation industry for over 15 years and is passionate about delivering an outstanding customer experience. Within the industry aligned customer service model, he is responsible for construction, labour hire, mining, and security and safety industries. He is also responsible for WorkCover’s contact centre. His background supports his ability to lead people in the delivery of customer-focused services to achieve quality outcomes for injured workers, at the lowest cost for employers.

Christina Carras BComm, ACA, SIA (Aff), AGIA, GAICD Lead Customer Experience, Professional Services

Christina oversees the claims, premium and relationship management of our industry aligned customer service model. She is responsible for the health and community care, education, tourism and technical industries, and plays an integral role in delivery changes that benefit both our employers and injured workers, while at the same time engaging with our people to deliver the best outcomes.

21 WorkCover Queensland annual report 2015–2016

Barbara Martin BBehSc, MRehabCounsel Lead Customer Experience, Logistics and Supply Services

Barbara has contributed to the vision of the personal injury industry for the last 14 years. She is responsible for the agriculture, manufacturing, logistics and supply sectors and provides leadership to a range of management groups. Barbara’s passion for injury prevention and the health benefits of work has influenced positive outcomes for customers and stakeholders. Her comprehensive knowledge of the scheme provides for integrity in our information and education, within a changing business environment.

Janine Reid BLaws, MBA, GIA (Cert), GAICD Legal Counsel

Janine has worked in personal injuries for over 20 years. Her knowledge and experience in personal injuries support her ability to manage our common law strategy and legal panel. She is also responsible for providing legal advice to the business and the WorkCover Board and engaging with external stakeholders.

22 WorkCover Queensland annual report 2015–2016

WorkCover aims to be an organisation of committed, creative people with strong leadership. The recruitment and retention of capable people, the delivery and reinforcement of a competency framework and performance culture, and the alignment of learning and development activities with business goals and customer experience are critical to the ongoing success of the organisation.

Overview of workforce

• 714 full-time equivalent employees• 69% of workforce is female• Permanent separation rate: 7.9%

Supporting health and wellbeing

WorkCover has proactively targeted the impacts of mental and physical wellbeing for our people, mirroring our education and awareness campaign for our customers. Over the past year, we have delivered:

• health and wellbeing presentations• musculoskeletal education campaign• mental health education campaign• mental health awareness training for our managers• influenza vaccinations• skin cancer checks• information on managing stress/personal issues, including services offered by our employee assistance

program• monthly workplace health and safety toolbox talks on topics such as emergencies in the workplace, being

sun smart, and deciphering food labels and nutritional information.

WorkCover’s graduating class celebrate on the completion of a Certificate III in Personal Injury Management

ENGAGED PEOPLE

23 WorkCover Queensland annual report 2015–2016

Our Workplace Health and Safety Committee and champions meet regularly to promote and raise awareness of safety at work.

We have also continued to encourage a healthy work-life balance through flexible working hours, parental leave, part-time and job share opportunities.

Professional development

Induction

Our induction day is an opportunity to welcome our new starters, introduce the way we work and support our formal on-boarding program. Our new starters engage in a workshop about our organisational values and how they guide our behaviour as well as their role in fostering a diverse and inclusive workplace. Our CEO also talks about the journey of WorkCover and the importance of creating a customer experience, no matter what your role.

Leadership development

WorkCover has identified six leadership competencies, which are a combination of the knowledge, skills and behaviours needed to perform a leadership role effectively. The six competencies set a high standard for leadership throughout WorkCover.

• Strive for operational excellence• Enhance customer relationships• Champion change and drive innovation• Foster teamwork and collaboration• Lead and develop people• Maximise strategic effectiveness

WorkCover uses these competencies to guide our recruitment, selection and development of employees across the organisation. The competencies help us to:

• deliver the corporate strategy• optimise our performance• contribute our best and maximise our potential• build sustainable relationships with customers and other stakeholders• create a culture of leadership and accountability• structure our leadership development programs and initiatives.

All WorkCover leaders participated in a corporate education initiative, attending one-day workshops on topics such as Behavioural economics, Systems thinking to manage complexity, Coaching as essential leadership practice, Intellectual asset management and protection, Leading change organisational renewal, and Cyber safety.

Leadership sessions were also delivered in-house and included sessions on: Leading with emotional intelligence, Fostering a culture of lifelong learning, and Recognising, responding and referring employees experiencing Domestic Violence.

Developing our people

WorkCover seeks people who believe in and are committed to our vision and values. We have captured the behavioural expectations in four key competencies that are designed to empower our people to achieve their full potential.

• We foster teamwork and collaboration in our daily work practices• We enhance relationships with our customers• We strive for operational excellence everyday• We champion change and drive innovation in the way we work

24 WorkCover Queensland annual report 2015–2016

To deliver the best outcomes for our customers, we believe it is important that our people are experts in workers’ compensation. Our people have the opportunity to learn and gain skills across all areas of the business, from claims support through to claims management and ultimately managing and fostering client relationships.

As part of our learning programs and career development options, we offer our people the opportunity to undertake a Certificate III in Personal Injury Management (Claims Management) with the Personal Injury Education Foundation. This certificate is a national vocational qualification that is recognised within the personal injury industry.

Recruitment and retention

Attracting suitably qualified candidates has been a core focus over the past year. A holistic approach to recruitment has seen the use of psychometric evaluations, in-house assessment centres and robust pre-employment checks to inform our selection decisions. A workforce planning methodology has been used to identify future people requirements. This methodology has been piloted across the Customer Experience Division and Customer Support divisions of our business and coincides with the annual budgeting and planning cycle. It is anticipated this methodology will be fully integrated in 2016–2017.

To improve our practices for the year ahead, we will be focusing on developing manager capability across recruitment, defining our talent profiles and using online platforms to make hiring more efficient. We will be working on better understanding our candidate experience to ensure we are communicating our employer brand accurately to attract and retain our future talent.

Industrial and employee relations

The Consultative Committee meets 10 times each year, one meeting per calendar month excluding December and January. It is comprised of the Manager Human Resources, the General Manager Finance as the management representative and Together Queensland representatives and workplace delegates. The Consultative Committee is used to consult on a broad range of issues, including the modernisation of the WorkCover Queensland Employees Award – State 2015, and the negotiation of the 2016 Certified Agreement.

25

WorkCover Queensland annual report 2015–2016

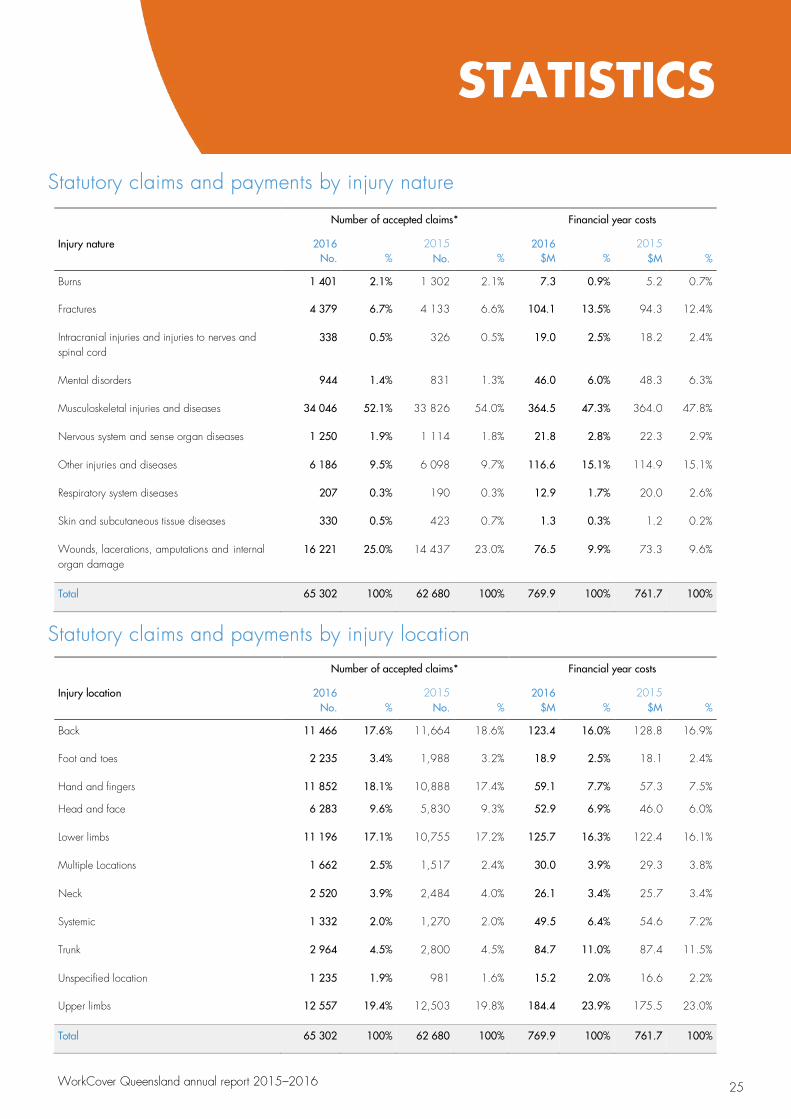

Statutory claims and payments by injury nature

Number of accepted claims* Financial year costs

Injury nature 2016 No.

%

2015 No.

%

2016 $M

%

2015 $M

%

Burns 1 401 2.1% 1 302 2.1% 7.3 0.9% 5.2 0.7%

Fractures 4 379 6.7% 4 133 6.6% 104.1 13.5% 94.3 12.4%

Intracranial injuries and injuries to nerves and spinal cord

338 0.5% 326 0.5% 19.0 2.5% 18.2 2.4%

Mental disorders 944 1.4% 831 1.3% 46.0 6.0% 48.3 6.3%

Musculoskeletal injuries and diseases 34 046 52.1% 33 826 54.0% 364.5 47.3% 364.0 47.8%

Nervous system and sense organ diseases 1 250 1.9% 1 114 1.8% 21.8 2.8% 22.3 2.9%

Other injuries and diseases 6 186 9.5% 6 098 9.7% 116.6 15.1% 114.9 15.1%

Respiratory system diseases 207 0.3% 190 0.3% 12.9 1.7% 20.0 2.6%

Skin and subcutaneous tissue diseases 330 0.5% 423 0.7% 1.3 0.3% 1.2 0.2%

Wounds, lacerations, amputations and internal organ damage

16 221 25.0% 14 437 23.0% 76.5 9.9% 73.3 9.6%

Total 65 302 100% 62 680 100% 769.9 100% 761.7 100%

Statutory claims and payments by injury location

Number of accepted claims* Financial year costs

Injury location 2016 No.

%

2015 No.

%

2016 $M

%

2015 $M

%

Back 11 466 17.6% 11,664 18.6% 123.4 16.0% 128.8 16.9%

Foot and toes 2 235 3.4% 1,988 3.2% 18.9 2.5% 18.1 2.4%

Hand and fingers 11 852 18.1% 10,888 17.4% 59.1 7.7% 57.3 7.5%

Head and face 6 283 9.6% 5,830 9.3% 52.9 6.9% 46.0 6.0%

Lower limbs 11 196 17.1% 10,755 17.2% 125.7 16.3% 122.4 16.1%

Multiple Locations 1 662 2.5% 1,517 2.4% 30.0 3.9% 29.3 3.8%

Neck 2 520 3.9% 2,484 4.0% 26.1 3.4% 25.7 3.4%

Systemic 1 332 2.0% 1,270 2.0% 49.5 6.4% 54.6 7.2%

Trunk 2 964 4.5% 2,800 4.5% 84.7 11.0% 87.4 11.5%

Unspecified location 1 235 1.9% 981 1.6% 15.2 2.0% 16.6 2.2%

Upper limbs 12 557 19.4% 12,503 19.8% 184.4 23.9% 175.5 23.0%

Total 65 302 100% 62 680 100% 769.9 100% 761.7 100%

STATISTICS

26

WorkCover Queensland annual report 2015–2016

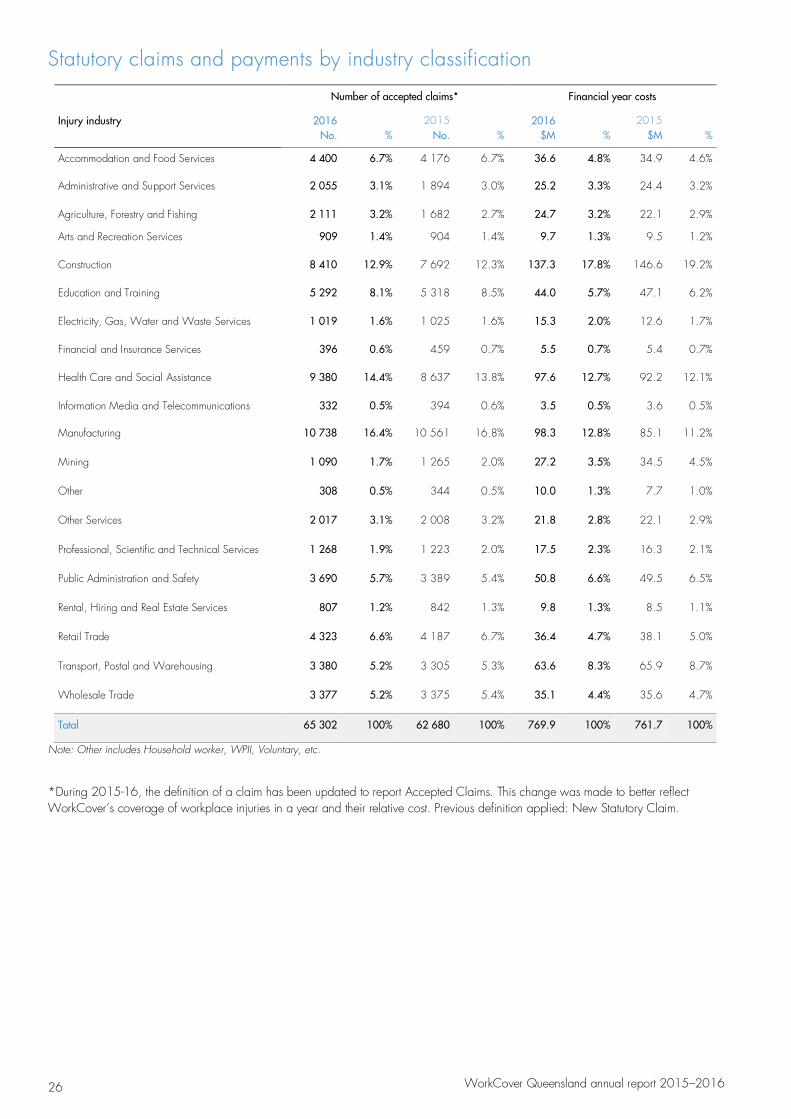

Statutory claims and payments by industry classification

Number of accepted claims* Financial year costs

Injury industry 2016 No.

%

2015 No.

%

2016 $M

%

2015 $M

%

Accommodation and Food Services 4 400 6.7% 4 176 6.7% 36.6 4.8% 34.9 4.6%

Administrative and Support Services 2 055 3.1% 1 894 3.0% 25.2 3.3% 24.4 3.2%

Agriculture, Forestry and Fishing 2 111 3.2% 1 682 2.7% 24.7 3.2% 22.1 2.9%

Arts and Recreation Services 909 1.4% 904 1.4% 9.7 1.3% 9.5 1.2%

Construction 8 410 12.9% 7 692 12.3% 137.3 17.8% 146.6 19.2%

Education and Training 5 292 8.1% 5 318 8.5% 44.0 5.7% 47.1 6.2%

Electricity, Gas, Water and Waste Services 1 019 1.6% 1 025 1.6% 15.3 2.0% 12.6 1.7%

Financial and Insurance Services 396 0.6% 459 0.7% 5.5 0.7% 5.4 0.7%

Health Care and Social Assistance 9 380 14.4% 8 637 13.8% 97.6 12.7% 92.2 12.1%

Information Media and Telecommunications 332 0.5% 394 0.6% 3.5 0.5% 3.6 0.5%

Manufacturing 10 738 16.4% 10 561 16.8% 98.3 12.8% 85.1 11.2%

Mining 1 090 1.7% 1 265 2.0% 27.2 3.5% 34.5 4.5%

Other 308 0.5% 344 0.5% 10.0 1.3% 7.7 1.0%

Other Services 2 017 3.1% 2 008 3.2% 21.8 2.8% 22.1 2.9%

Professional, Scientific and Technical Services 1 268 1.9% 1 223 2.0% 17.5 2.3% 16.3 2.1%

Public Administration and Safety 3 690 5.7% 3 389 5.4% 50.8 6.6% 49.5 6.5%

Rental, Hiring and Real Estate Services 807 1.2% 842 1.3% 9.8 1.3% 8.5 1.1%

Retail Trade 4 323 6.6% 4 187 6.7% 36.4 4.7% 38.1 5.0%

Transport, Postal and Warehousing 3 380 5.2% 3 305 5.3% 63.6 8.3% 65.9 8.7%

Wholesale Trade 3 377 5.2% 3 375 5.4% 35.1 4.4% 35.6 4.7%

Total 65 302 100% 62 680 100% 769.9 100% 761.7 100%

Note: Other includes Household worker, WPII, Voluntary, etc.

*During 2015-16, the definition of a claim has been updated to report Accepted Claims. This change was made to better reflect WorkCover’s coverage of workplace injuries in a year and their relative cost. Previous definition applied: New Statutory Claim.

27

WorkCover Queensland annual report 2015–2016

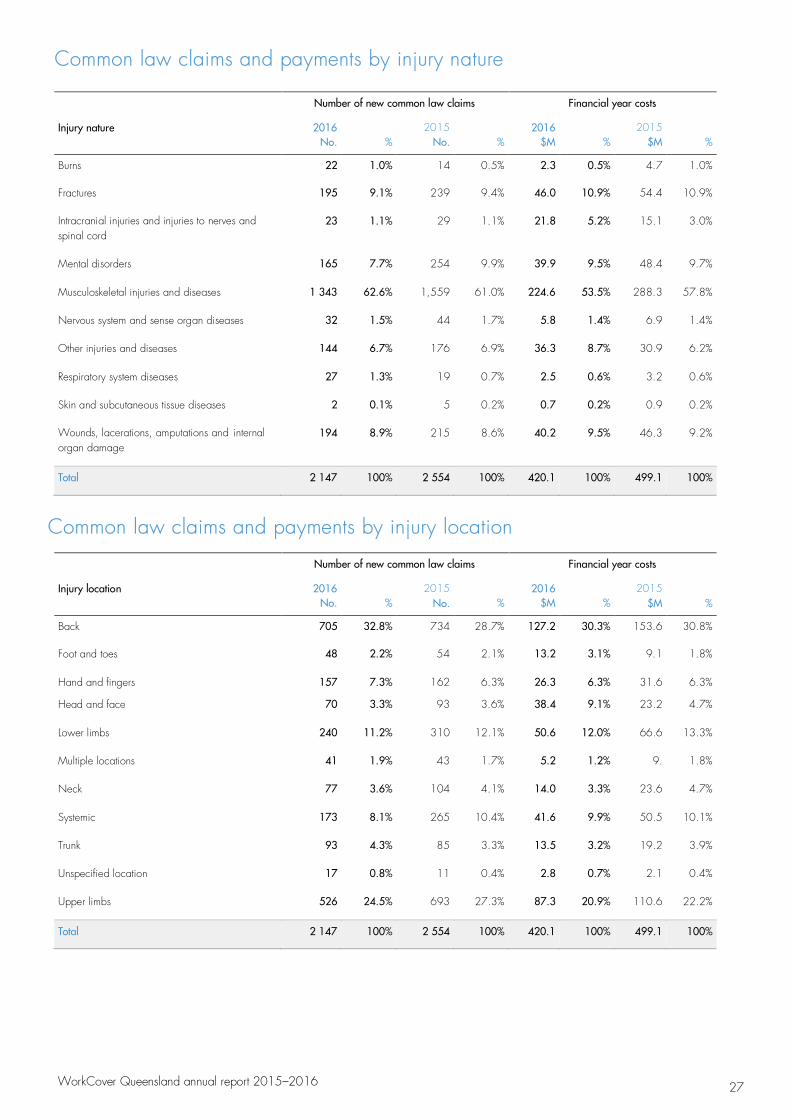

Common law claims and payments by injury nature

Number of new common law claims Financial year costs

Injury nature 2016 No.

%

2015 No.

%

2016 $M

%

2015 $M

%

Burns 22 1.0% 14 0.5% 2.3 0.5% 4.7 1.0%

Fractures 195 9.1% 239 9.4% 46.0 10.9% 54.4 10.9%

Intracranial injuries and injuries to nerves and spinal cord

23 1.1% 29 1.1% 21.8 5.2% 15.1 3.0%

Mental disorders 165 7.7% 254 9.9% 39.9 9.5% 48.4 9.7%

Musculoskeletal injuries and diseases 1 343 62.6% 1,559 61.0% 224.6 53.5% 288.3 57.8%

Nervous system and sense organ diseases 32 1.5% 44 1.7% 5.8 1.4% 6.9 1.4%

Other injuries and diseases 144 6.7% 176 6.9% 36.3 8.7% 30.9 6.2%

Respiratory system diseases 27 1.3% 19 0.7% 2.5 0.6% 3.2 0.6%

Skin and subcutaneous tissue diseases 2 0.1% 5 0.2% 0.7 0.2% 0.9 0.2%

Wounds, lacerations, amputations and internal organ damage

194 8.9% 215 8.6% 40.2 9.5% 46.3 9.2%

Total 2 147 100% 2 554 100% 420.1 100% 499.1 100%

Common law claims and payments by injury location

Number of new common law claims Financial year costs

Injury location 2016 No.

%

2015 No.

%

2016 $M

%

2015 $M

%

Back 705 32.8% 734 28.7% 127.2 30.3% 153.6 30.8%

Foot and toes 48 2.2% 54 2.1% 13.2 3.1% 9.1 1.8%

Hand and fingers 157 7.3% 162 6.3% 26.3 6.3% 31.6 6.3%

Head and face 70 3.3% 93 3.6% 38.4 9.1% 23.2 4.7%

Lower limbs 240 11.2% 310 12.1% 50.6 12.0% 66.6 13.3%

Multiple locations 41 1.9% 43 1.7% 5.2 1.2% 9. 1.8%

Neck 77 3.6% 104 4.1% 14.0 3.3% 23.6 4.7%

Systemic 173 8.1% 265 10.4% 41.6 9.9% 50.5 10.1%

Trunk 93 4.3% 85 3.3% 13.5 3.2% 19.2 3.9%

Unspecified location 17 0.8% 11 0.4% 2.8 0.7% 2.1 0.4%

Upper limbs 526 24.5% 693 27.3% 87.3 20.9% 110.6 22.2%

Total 2 147 100% 2 554 100% 420.1 100% 499.1 100%

28

WorkCover Queensland annual report 2015–2016

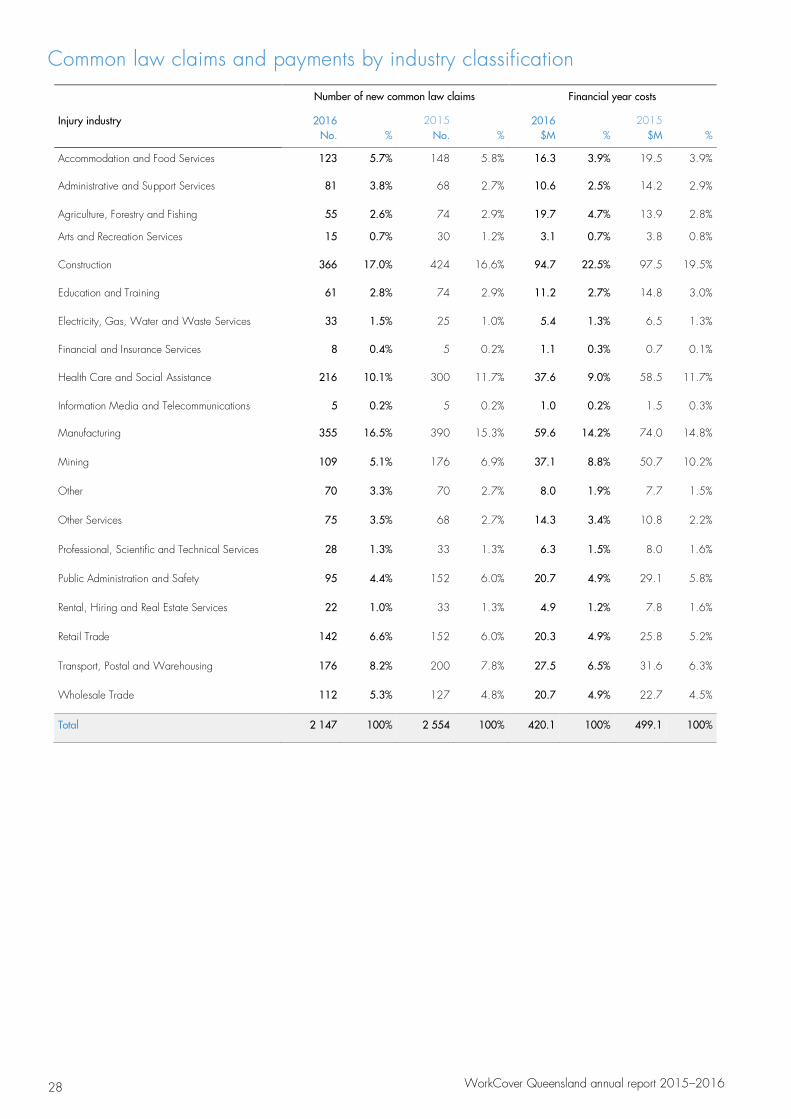

Common law claims and payments by industry classification

Number of new common law claims Financial year costs

Injury industry 2016 No.

%

2015 No.

%

2016 $M

%

2015 $M

%

Accommodation and Food Services 123 5.7% 148 5.8% 16.3 3.9% 19.5 3.9%

Administrative and Support Services 81 3.8% 68 2.7% 10.6 2.5% 14.2 2.9%

Agriculture, Forestry and Fishing 55 2.6% 74 2.9% 19.7 4.7% 13.9 2.8%

Arts and Recreation Services 15 0.7% 30 1.2% 3.1 0.7% 3.8 0.8%

Construction 366 17.0% 424 16.6% 94.7 22.5% 97.5 19.5%

Education and Training 61 2.8% 74 2.9% 11.2 2.7% 14.8 3.0%

Electricity, Gas, Water and Waste Services 33 1.5% 25 1.0% 5.4 1.3% 6.5 1.3%

Financial and Insurance Services 8 0.4% 5 0.2% 1.1 0.3% 0.7 0.1%

Health Care and Social Assistance 216 10.1% 300 11.7% 37.6 9.0% 58.5 11.7%

Information Media and Telecommunications 5 0.2% 5 0.2% 1.0 0.2% 1.5 0.3%

Manufacturing 355 16.5% 390 15.3% 59.6 14.2% 74.0 14.8%

Mining 109 5.1% 176 6.9% 37.1 8.8% 50.7 10.2%

Other 70 3.3% 70 2.7% 8.0 1.9% 7.7 1.5%

Other Services 75 3.5% 68 2.7% 14.3 3.4% 10.8 2.2%

Professional, Scientific and Technical Services 28 1.3% 33 1.3% 6.3 1.5% 8.0 1.6%

Public Administration and Safety 95 4.4% 152 6.0% 20.7 4.9% 29.1 5.8%

Rental, Hiring and Real Estate Services 22 1.0% 33 1.3% 4.9 1.2% 7.8 1.6%

Retail Trade 142 6.6% 152 6.0% 20.3 4.9% 25.8 5.2%

Transport, Postal and Warehousing 176 8.2% 200 7.8% 27.5 6.5% 31.6 6.3%

Wholesale Trade 112 5.3% 127 4.8% 20.7 4.9% 22.7 4.5%

Total 2 147 100% 2 554 100% 420.1 100% 499.1 100%

29

WorkCover Queensland annual report 2015–2016

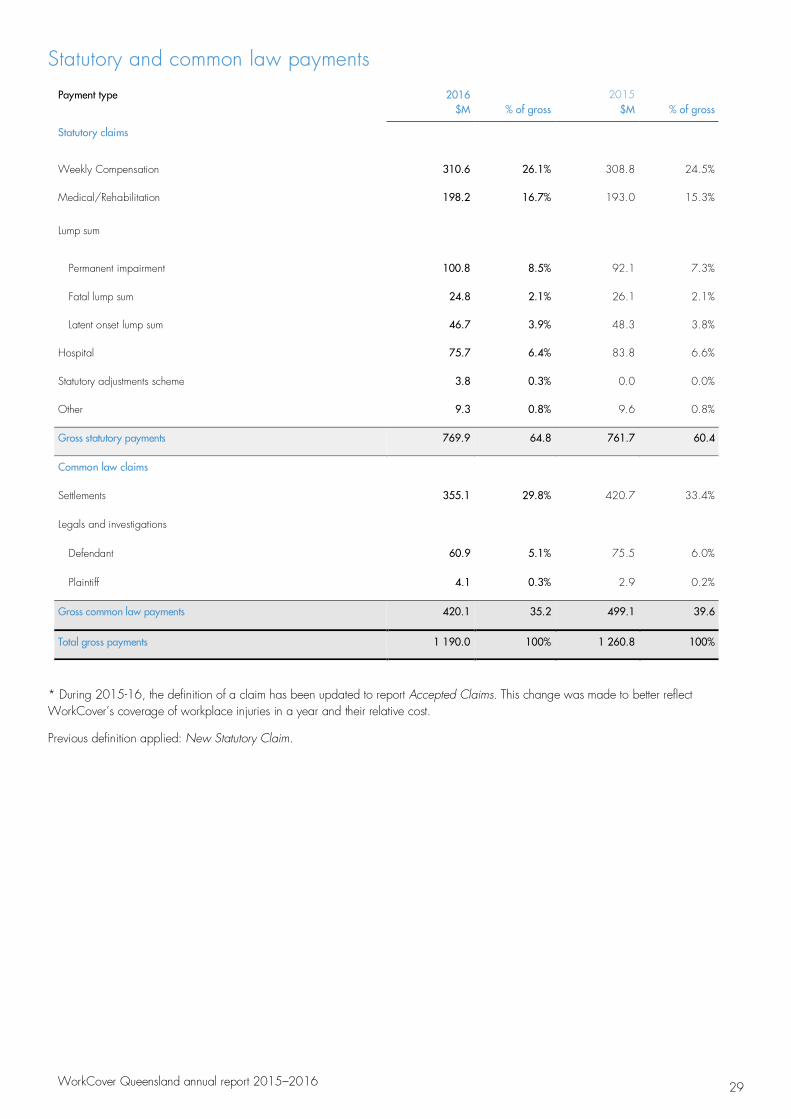

Statutory and common law payments

Payment type 2016 $M

% of gross

2015 $M

% of gross

Statutory claims

Weekly Compensation 310.6 26.1% 308.8 24.5%

Medical/Rehabilitation 198.2 16.7% 193.0 15.3%

Lump sum

Permanent impairment 100.8 8.5% 92.1 7.3%

Fatal lump sum 24.8 2.1% 26.1 2.1%

Latent onset lump sum 46.7 3.9% 48.3 3.8%

Hospital 75.7 6.4% 83.8 6.6%

Statutory adjustments scheme 3.8 0.3% 0.0 0.0%

Other 9.3 0.8% 9.6 0.8%

Gross statutory payments 769.9 64.8 761.7 60.4

Common law claims

Settlements 355.1 29.8% 420.7 33.4%

Legals and investigations

Defendant 60.9 5.1% 75.5 6.0%

Plaintiff 4.1 0.3% 2.9 0.2%

Gross common law payments 420.1 35.2 499.1 39.6

Total gross payments 1 190.0 100% 1 260.8 100%

* During 2015-16, the definition of a claim has been updated to report Accepted Claims. This change was made to better reflect WorkCover’s coverage of workplace injuries in a year and their relative cost.

Previous definition applied: New Statutory Claim.

30

WorkCover Queensland annual report 2015–2016

Strategic planning

A four-year Corporate Plan and Statement of Corporate Intent are prepared annually and approved by the Minister in accordance with the Workers’ Compensation and Rehabilitation Act 2003. The Corporate Plan summarises our vision, values, goals, strategies and performance indicators. The plan forms the basis for divisional business plans, which define operational strategies to meet our business objectives. The divisional business plans outline our key financial and operational performance indicators, which we monitor monthly. Our Statement of Corporate Intent outlines our objectives and major activities, and specifies various financial and nonfinancial performance targets for the financial year.

Board of Directors

The statutory role and requirements of the Board are set out in section 427 of the Workers’ Compensation and Rehabilitation Act 2003, and chapter 8 outlines the powers and functions of WorkCover. The WorkCover Board charter specifies the role and responsibilities of the Board in detail and is available on our website.

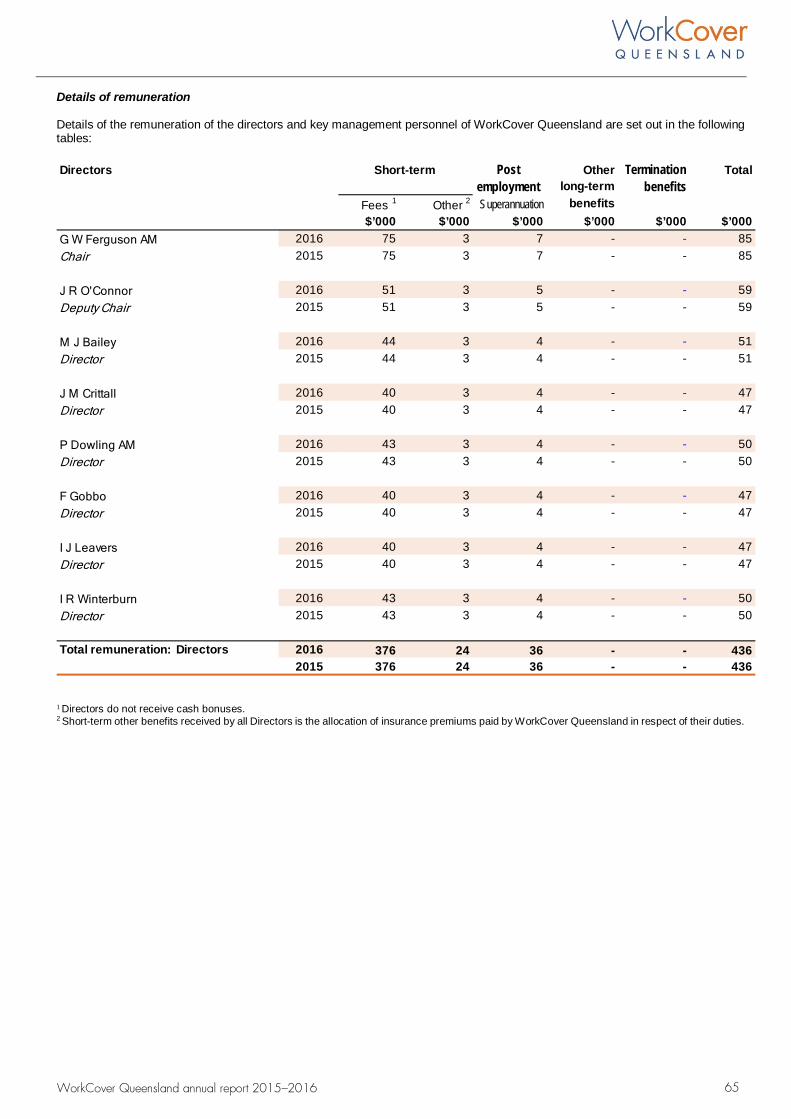

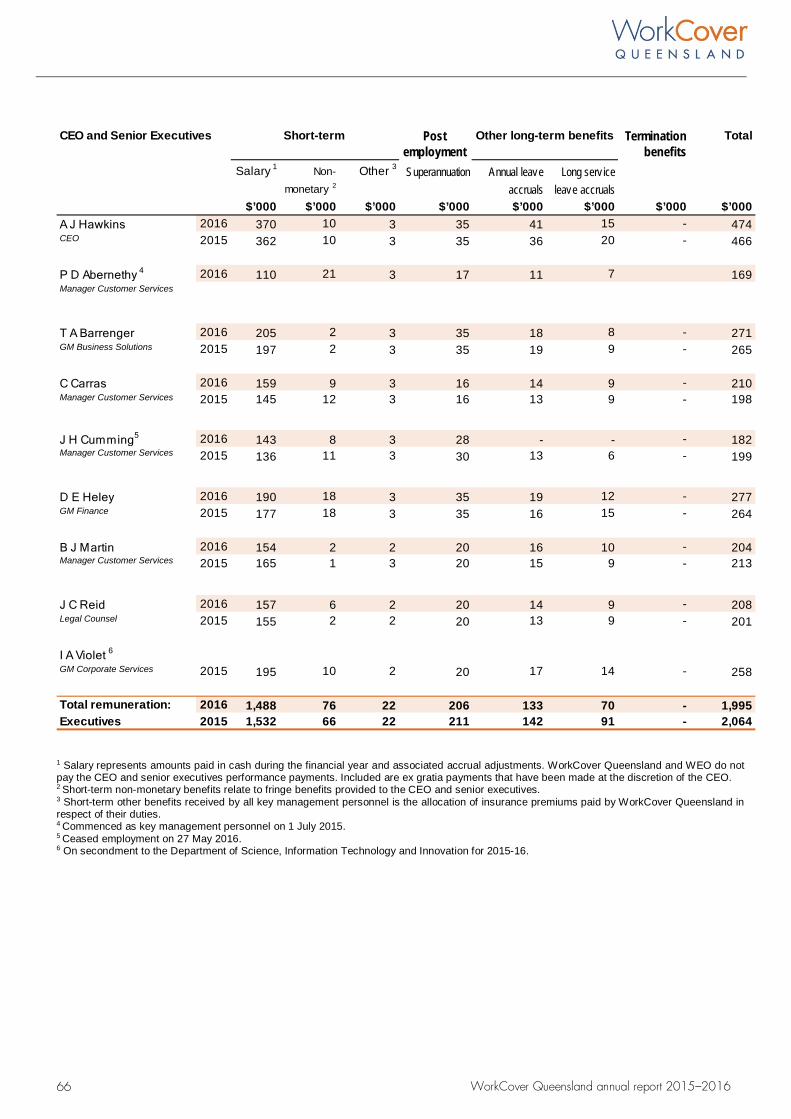

The WorkCover Board consists of independent non-executive directors appointed by the Governor in Council who is responsible for appointing directors, based on experience and knowledge, and determining their remuneration. Information on directors’ and executives’ benefits is detailed within note S3 of the financial statements.

Kylie Easton returned to work after injury with Recover@Work host employer LendLease

CORPORATE GOVERNANCE

31

WorkCover Queensland annual report 2015–2016

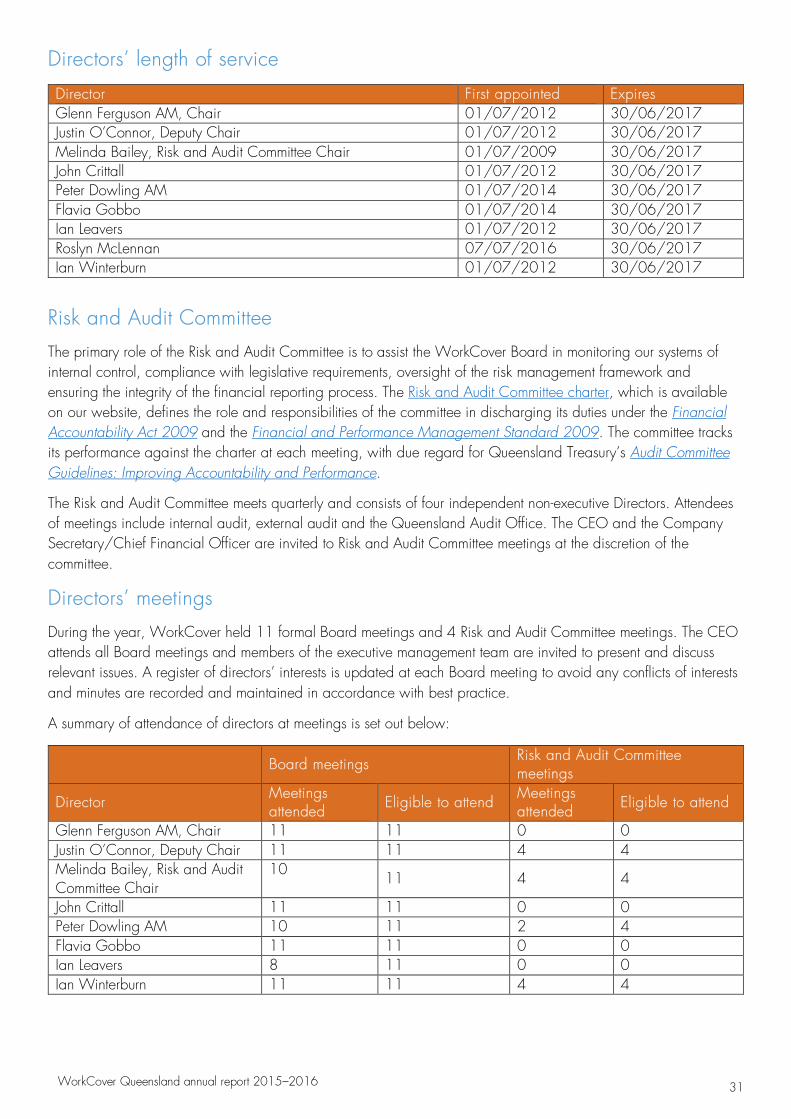

Directors’ length of service

Director First appointed Expires Glenn Ferguson AM, Chair 01/07/2012 30/06/2017 Justin O’Connor, Deputy Chair 01/07/2012 30/06/2017 Melinda Bailey, Risk and Audit Committee Chair 01/07/2009 30/06/2017 John Crittall 01/07/2012 30/06/2017 Peter Dowling AM 01/07/2014 30/06/2017 Flavia Gobbo 01/07/2014 30/06/2017 Ian Leavers 01/07/2012 30/06/2017 Roslyn McLennan 07/07/2016 30/06/2017 Ian Winterburn 01/07/2012 30/06/2017

Risk and Audit Committee

The primary role of the Risk and Audit Committee is to assist the WorkCover Board in monitoring our systems of internal control, compliance with legislative requirements, oversight of the risk management framework and ensuring the integrity of the financial reporting process. The Risk and Audit Committee charter, which is available on our website, defines the role and responsibilities of the committee in discharging its duties under the Financial Accountability Act 2009 and the Financial and Performance Management Standard 2009. The committee tracks its performance against the charter at each meeting, with due regard for Queensland Treasury’s Audit Committee Guidelines: Improving Accountability and Performance.

The Risk and Audit Committee meets quarterly and consists of four independent non-executive Directors. Attendees of meetings include internal audit, external audit and the Queensland Audit Office. The CEO and the Company Secretary/Chief Financial Officer are invited to Risk and Audit Committee meetings at the discretion of the committee.

Directors’ meetings

During the year, WorkCover held 11 formal Board meetings and 4 Risk and Audit Committee meetings. The CEO attends all Board meetings and members of the executive management team are invited to present and discuss relevant issues. A register of directors’ interests is updated at each Board meeting to avoid any conflicts of interests and minutes are recorded and maintained in accordance with best practice.

A summary of attendance of directors at meetings is set out below:

Board meetings Risk and Audit Committee meetings

Director Meetings attended Eligible to attend Meetings

attended Eligible to attend

Glenn Ferguson AM, Chair 11 11 0 0 Justin O’Connor, Deputy Chair 11 11 4 4 Melinda Bailey, Risk and Audit Committee Chair

10 11 4 4

John Crittall 11 11 0 0 Peter Dowling AM 10 11 2 4 Flavia Gobbo 11 11 0 0 Ian Leavers 8 11 0 0 Ian Winterburn 11 11 4 4

32 WorkCover Queensland annual report 2015–2016

Senior executives

The CEO assesses performance of senior executives on an annual basis as part of the organisation’s performance review process. The Board also assesses the performance of the CEO as part of this process.

Stakeholder feedback

WorkCover maintains a complaints management policy in accordance with the AS ISO10002–2014: Guidelines for complaints management in organisations and section 219A of the Public Service Act 2008. This policy is published on our website for easy customer access and is routinely monitored and audited to ensure compliance with statutory, policy and reporting requirements.

WorkCover recognises the importance of complaints management as part of delivering a quality customer experience. We support the rights of our customers and stakeholders to have their complaints heard and actioned appropriately. We are committed to resolving complaints quickly and objectively and believe that all customer and stakeholder feedback, both positive and negative, presents opportunities for continuous improvement.

Our centralised complaints management system is used to record, monitor and respond to complaints. In addition, the Board and executive management review complaints data quarterly.

In 2015–2016, we recorded 266 complaints, of which 83 resulted in further action and 183 required no further action. The Queensland Ombudsman received 14 complaints relating to WorkCover, of which 11 were declined for investigation by the Ombudsman. Where the complaints required further action, we reviewed our processes and implemented improvements, including staff training to enhance customer experience.

Mandatory open data reporting

WorkCover has reported online information for consultancies and overseas travel in accordance with mandatory reporting requirements.

ETHICS, COMPLIANCE AND RISK MANAGEMENT Ethics

Ethics provide the overarching principles and rules that govern the behaviour of WorkCover’s people and also consider the impact on the community and environment. WorkCover’s ethics program aims to provide a framework to ensure the organisation has high standards of ethical behaviour in compliance with relevant legislative requirements and promotes an ethical culture consistent with our values.

Code of Conduct

WorkCover’s Board members and employees are expected to maintain the highest level of ethical standards whilst performing their duties. WorkCover’s code of conduct supports our values providing a framework for high ethical standards and has been written to align with the requirements of the Public Sector Ethics Act 1994 (PSEA). The assertions of integrity and accountability are integrated into WorkCover’s strategies, objectives and actions. The code of conduct is communicated to our people through the corporate induction program and is available on the WorkCover intranet and website. Our staff receive annual refresher training on this document and the PSEA in general. All relevant internal policies and practices align with the code and the PSEA, including the ethics principles and values detailed in this Act. All WorkCover staff are required to comply with the code of conduct. Any noncompliance may result in disciplinary action, which could include termination of employment.

The WorkCover Board is bound by ethical standards outlined in the Workers’ Compensation and Rehabilitation Act 2003 (the Act), which requires directors to act honestly, disclose interests, exercise due diligence and not use information or their position inappropriately. Directors are bound by the PSEA and as such, WorkCover’s code of

33 WorkCover Queensland annual report 2015–2016

conduct, on which they annually receive the same training as staff. Additionally, the Board follows the guidelines set out in Welcome Aboard: A Guide for Members of Government Boards, Committees and Statutory Authorities as issued by the Department of Premier and Cabinet.

Compliance

We maintain a number of policies and procedures detailing our compliance obligations in relation to relevant legislation, regulations, and codes of practice. We continually monitor our systems and processes to ensure these obligations are met. WorkCover’s obligations are managed through the Risk and Audit Committee and progress is reported in the annual compliance calendar at quarterly meetings.

Internal audit

Internal audit supports WorkCover’s Risk and Audit Committee in meeting its charter by providing an independent function that evaluates and provides impartial advice on the effectiveness of WorkCover’s governance, internal controls and corporate governance processes to executive management and the Board. The internal audit function is managed by Ernst & Young, who are both independent from management and WorkCover’s external auditors, and operate in accordance with WorkCover’s internal audit charter. This charter outlines the objectives, roles and responsibilities for the internal audit function and is consistent with all key internal audit and ethical standards.

Both the strategic and annual audit plans prepared by the internal auditors are approved by the Risk and Audit Committee and the Board. This Risk and Audit Committee operates with due regard for Treasury’s Audit Committee Guidelines, including the monitoring of the effectiveness, efficiency and economy of the internal audit function. Significant financial and operational risks identified by the internal auditors are reported through to the Risk and Audit Committee, as per the Internal Audit Charter. Risks are reviewed regularly through the use of an assurance map.

In 2015–2016, a total of 13 internal audit engagements were completed in line with the annual internal audit plan. All recommendations from these audits have been implemented or are on track to be implemented within agreed timeframes.

Quality assurance reviews

Our quality assurance reviews are designed to confirm that the controls in place to manage risks are effective and identify potential areas for improvement to our processes, policies, and procedures.

Compliance training

WorkCover is committed to ensuring the ongoing capability and capacity of our people through the continued investment and development of our leadership and technical training competencies delivered throughout the year. As part of this commitment, all staff complete regular training to keep up-to-date with compliance requirements in key areas, including:

• Australian consumer legislation• Code of conduct• Privacy and record keeping• Fraud, corruption and risk• Technology use• Our people policies and workplace health and safety• PSEA

34

WorkCover Queensland annual report 2015–2016

Customer compliance and education

WorkCover has a dedicated compliance and education team to ensure Queensland employers are aware of their obligations to maintain adequate cover when engaging workers. We maintain a balanced compliance strategy by providing targeted education and compliance activities across the state.

The compliance and education team educate stakeholders, conduct audits and site visits with businesses who appear to contravene their requirements, including failing to insure or not maintaining the correct level of cover, by underinsuring.

The following results were achieved during the year:

• 1,013 random site visits were conducted including 573 regional site visits • 142 non-compliant employers identified representing a 14% non-compliance detection rate • 1,660 targeted audits were conducted • 634 employers were non-compliant with the Act representing a 38% non-compliance rate.

Recordkeeping

All staff at WorkCover are responsible for keeping and maintaining records which are maintained through WorkCover’s Claims and Policy Information System (CPIS) for our claims and policy records and through an integrated electronic records system for all corporate records. Annual compliance training is completed to ensure that all staff are aware of their obligations under the Public Records Act 2002. This is essential training given that all of our claims and policy records have been digitised since 2008 and corporate records have been successfully transitioned to digital records during the financial year. WorkCover is now maintaining all records electronically.

The approach to recordkeeping was reviewed throughout the year to ensure continuous improvement strategies are implemented to maintain the quality and compliance of all records.

Public records are being retained in line with WorkCover’s recordkeeping policy, the Queensland State Archives’ General Retention and Disposal Schedule for Administrative Records and WorkCover’s Queensland State Archives approved Retention and Disposal Schedule, which was last reviewed in May 2014. No records were transferred to the Queensland State Archives during the 2016 financial year. Additionally, no breaches of the retention and disposal schedules were noted during the year, with no records being reported as missing or lost during this same period.

Privacy

WorkCover is committed to protecting the privacy of customers, staff and third parties in accordance with the Information Privacy Act 2009 (IP Act), which governs how information is collected, used, stored and disclosed by Queensland government agencies. All disclosures of private and personal information by WorkCover are managed under this Act, the Right to Information Act 2009 (RTI Act) or the Workers’ Compensation and Rehabilitation Act 2003. WorkCover has a Privacy Committee responsible for the promotion of privacy principles throughout the organisation. The Committee actively encourages privacy awareness through initiatives such as the participation in the Privacy Awareness Week which highlighted the importance of the protection of personal information to our staff. Additionally, staff undertake annual privacy training in accordance with our compliance program.

Risk management

WorkCover’s risk management framework and policy is based on AS/NZS ISO 31000:2009 Risk Management – Principles and Guidelines. This framework involves the establishment of an appropriate structure and culture designed to systematically identify, analyse, treat, monitor and communicate key risks associated with its activities

35 WorkCover Queensland annual report 2015–2016

and operating environment. In 2015–2016, WorkCover has continued to enhance existing risk management processes and encourage a culture of risk awareness.

WorkCover has a Risk and Assurance team responsible for:

• informing the Risk and Audit Committee of WorkCover’s Corporate Risks• monitoring the risk management framework• assisting risk champions.

Our risk management policy is available on our website.

Workplace health and safety

WorkCover is committed to maintaining a safe working environment, preventing workplace injuries and appropriately managing injuries should they occur. The focus on safety culture and early intervention resulted in 100% of workers’ compensation claimants returning to work.

WorkCover provides and maintains safe equipment for staff and undertakes scheduled safety inspections throughout the year, while monitoring our compliance with the Work Health and Safety Act 2011.

We have continued to strive for employer excellence over the last year by maintaining our commitment to continuous evaluation of safety ergonomics, injury management strategies and processes, training, wellness, and the safety culture of the organisation.

WorkCover uses a software program for recording workplace incidents, which includes a workplace injury/illness, a dangerous event or a ‘near miss’. Reports from this system are used to provide information to our Workplace Health and Safety (WHS) Committee for review and setting of strategies to mitigate the risk of injuries. These reports are also presented to the Board to assist in meeting their obligations of due diligence to our people and maintaining a safe work environment.

Workplace induction updates and monthly WHS toolbox talks inform new and existing employees of the obligations, expectations and due diligence required of those who work within the organisation.

Our WHS Committee maintains its commitment to meeting on a monthly basis in accordance with WorkCover policy and the Work Health and Safety Act 2011, and fosters open communication with workers and transparency with executive management. In 2016, a WHS Champions group was established to deliver and communicate operational outcomes of the WHS Committee. The WHS Champions meet on a quarterly basis.

A review of emergency procedures has also seen the introduction of cardiac defibrillator machines in WorkCover’s office.

See the Engaged people section of our annual report for more information on other initiatives WorkCover delivered in 2015–2016 to promote a safe and healthy working environment for our people.

Business continuity management

Our business continuity and disaster recovery plan has been developed to minimise the impact of a crisis on customer service and our people. On a regular basis, plans are reviewed and tested and training is undertaken by key Business Continuity Plan personnel.

36

WorkCover Queensland annual report 2015–2016

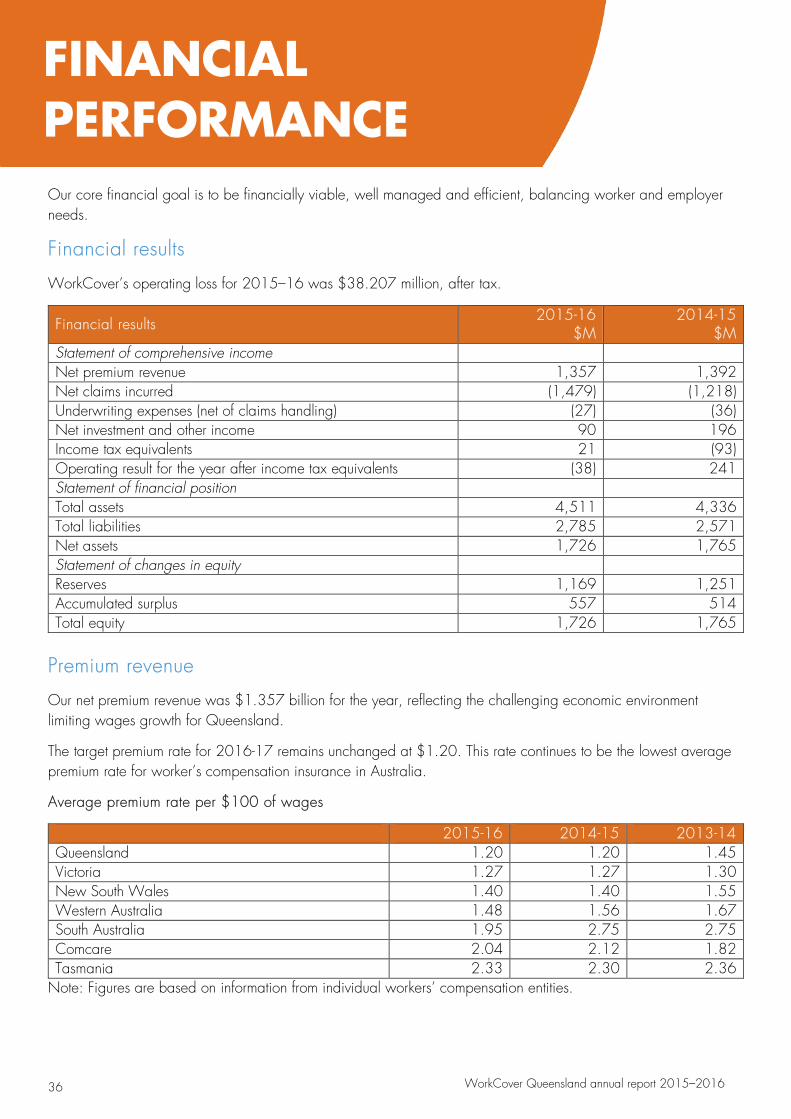

Our core financial goal is to be financially viable, well managed and efficient, balancing worker and employer needs.

Financial results

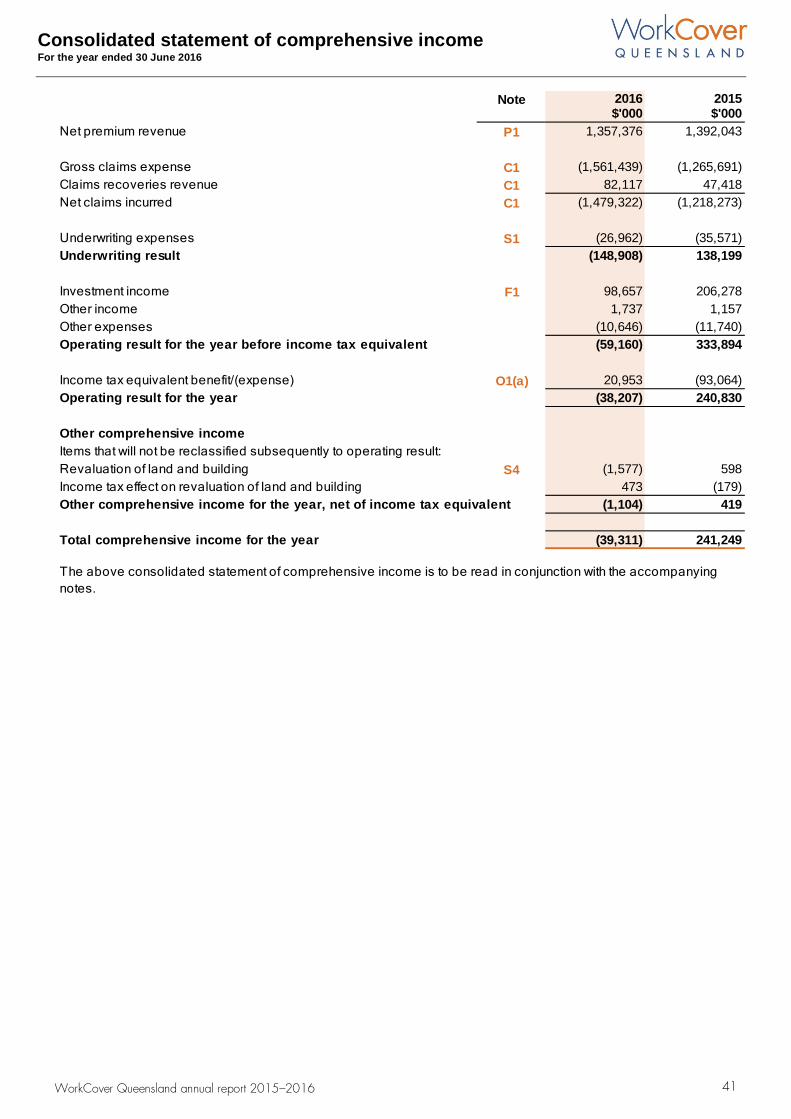

WorkCover’s operating loss for 2015–16 was $38.207 million, after tax.

Financial results 2015-16 $M

2014-15 $M

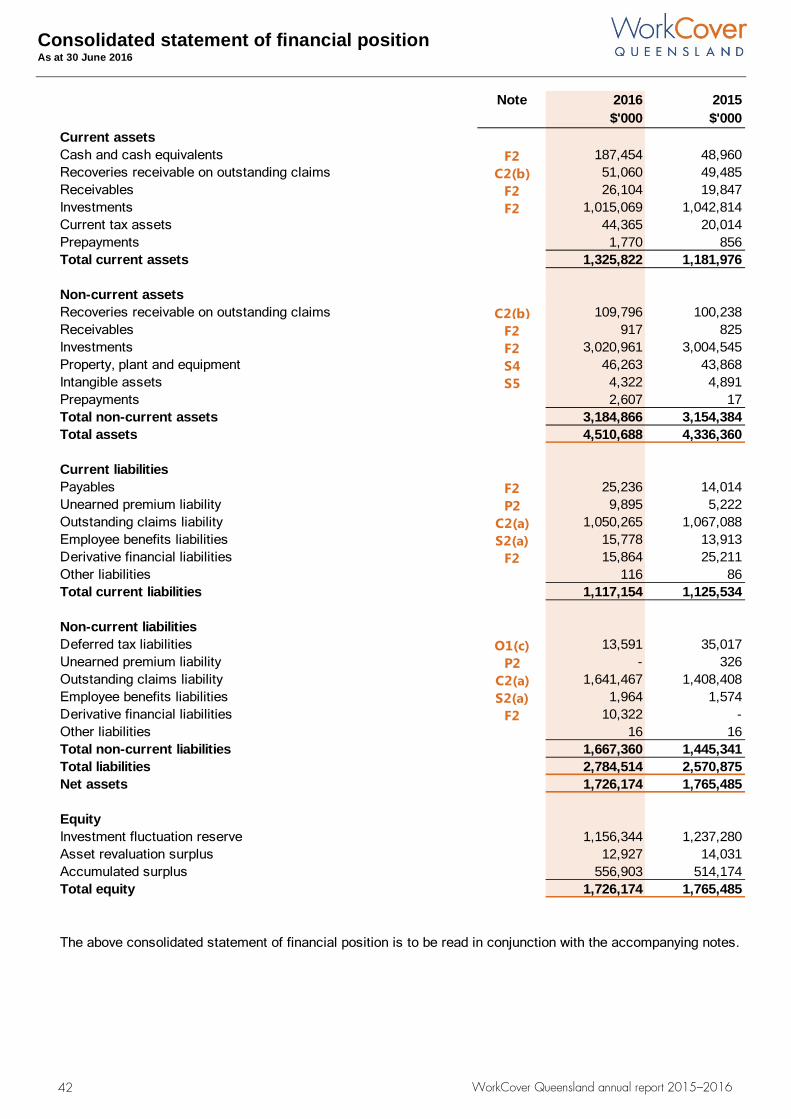

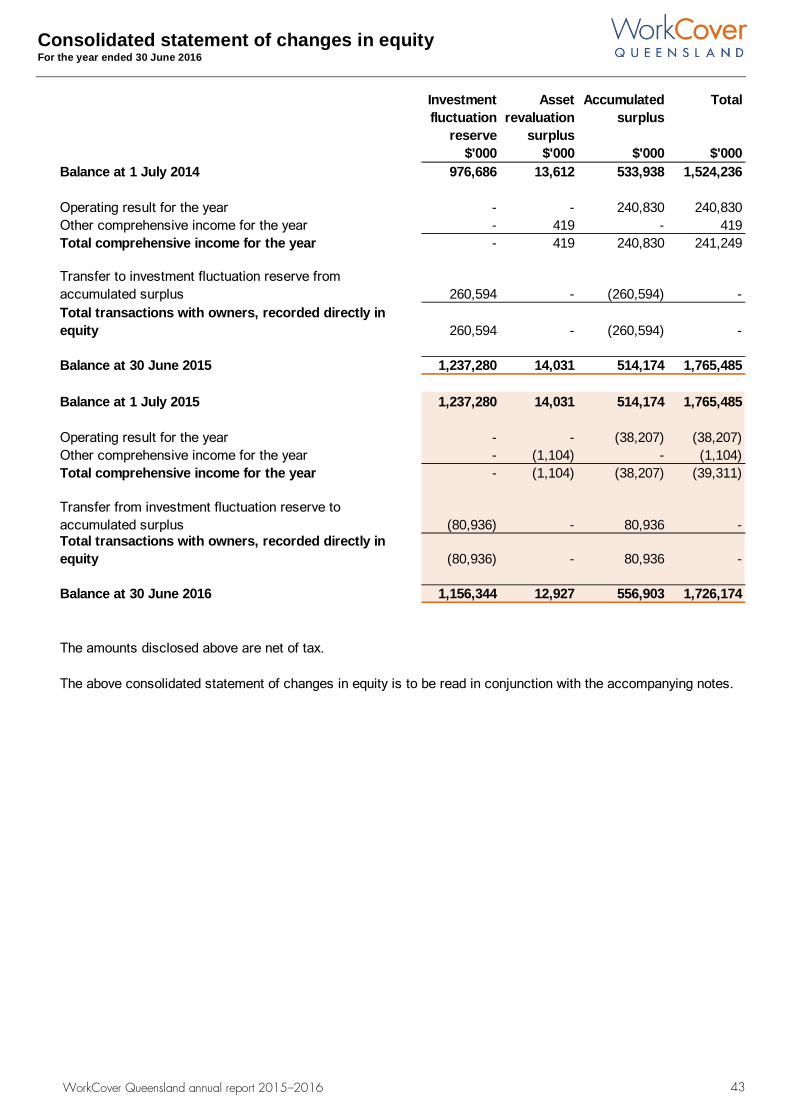

Statement of comprehensive income Net premium revenue 1,357 1,392 Net claims incurred (1,479) (1,218) Underwriting expenses (net of claims handling) (27) (36) Net investment and other income 90 196 Income tax equivalents 21 (93) Operating result for the year after income tax equivalents (38) 241 Statement of financial position Total assets 4,511 4,336 Total liabilities 2,785 2,571 Net assets 1,726 1,765 Statement of changes in equity Reserves 1,169 1,251 Accumulated surplus 557 514 Total equity 1,726 1,765

Premium revenue

Our net premium revenue was $1.357 billion for the year, reflecting the challenging economic environment limiting wages growth for Queensland.

The target premium rate for 2016-17 remains unchanged at $1.20. This rate continues to be the lowest average premium rate for worker’s compensation insurance in Australia.

Average premium rate per $100 of wages

2015-16 2014-15 2013-14 Queensland 1.20 1.20 1.45 Victoria 1.27 1.27 1.30 New South Wales 1.40 1.40 1.55 Western Australia 1.48 1.56 1.67 South Australia 1.95 2.75 2.75 Comcare 2.04 2.12 1.82 Tasmania 2.33 2.30 2.36

Note: Figures are based on information from individual workers’ compensation entities.

FINANCIAL PERFORMANCE

37 WorkCover Queensland annual report 2015–2016

Net claims incurred

Net claims incurred were $1.479 billion (2014-15: $1.218 billion) for 2015-16.

Net claims costs increased in 2015-16 following the latest valuation of the outstanding claims provision completed by our actuaries.

Underwriting expenses

Underwriting expenses include WorkCover’s management and operational expenses and the annual levy payable to the Workers’ Compensation Regulator and Workplace Health and Safety Queensland. To meet disclosure requirements under accounting standards, the claims handling expense portion of underwriting expenses is added to gross claims expense to reflect the total cost of administering claims during the year.

Investment portfolio

WorkCover’s investment portfolio is managed by QIC. The net market value in funds invested as at 30 June 2016 was $4.010 billion (30 June 2015: $4.022 billion).

The net return on our investment portfolio was 2.02% (2014-15: 4.85%). The long term investment strategy was revised by the Board with QIC during the year to position the investment portfolio to be able to balance the competing factors of maximising investment return whilst ensuring the portfolio is not exposed to excessive risk.

We will continue to work with our investment fund manager to effectively manage our investment risk to ensure our portfolio achieves its long term objectives.

Capital adequacy

The Workers’ Compensation and Rehabilitation Act 2003 and Workers’ Compensation and Rehabilitation Regulation 2014 outline specific requirements WorkCover must meet to be considered fully funded. As with other workers’ compensation schemes in Australia, WorkCover is fully funded if total assets are at least equal to its total liabilities. WorkCover’s funding ratio as at 30 June 2016 is 162%, achieving both our legislative requirements and management’s aim of maintaining a funding ratio of at least 120%.

As the funding ratio for WorkCover exceeded 120%, the excess of capital over this requirement has been transferred to the investment fluctuation reserve. The investment fluctuation reserve acts to mitigate the effects of future volatility in the investment return and supports stability in the setting of premium rates. The balance of the investment fluctuation reserve as at 30 June 2016 is $1.156 billion.

Looking to the future

We will continue to use prudent financial management to ensure a balanced, financially viable scheme for all customers and stakeholders. Part of this continuing prudent financial management entails a focus by WorkCover in continuing to operate within budget, achieving value for money, and more generally, ensuring WorkCover continues to minimise its costs and risks in relation to its liabilities. Premiums will be set, claims and operational expenses carefully managed in order to deliver this balance and we will continue our long term investment strategy built around a balanced portfolio.

0

2015-16 CONSOLIDATED

FINANCIAL REPORT Updated to the period ending 31 March 2016

Contents

Consolidated statement of comprehensive income ............................................................................................................... 441 Consolidated statement of financial position .......................................................................................................................... 442 Consolidated statement of changes in equity ......................................................................................................................... 443 Consolidated statement of cash flows .................................................................................................................................... 444 Notes to the consolidated financial statements

Basis of preparation ........................................................................................................................................................... 445 Significant accounting policies ........................................................................................................................................ 4455

Accounting judgements and estimates ........................................................................................................................... 445

Premium ............................................................................................................................................................................ 446 P1 Net premium revenue ............................................................................................................................................... 446

P2 Unearned premium liability ........................................................................................................................................ 446

P3 Liability adequacy test .............................................................................................................................................. 4466

Claims ................................................................................................................................................................................ 447 C1 Net claims incurred .................................................................................................................................................... 447

C2 Outstanding claims liability and recoveries receivable ............................................................................................. 4488

C3 Insurance risk ............................................................................................................................................................ 552