Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No.: 17779

IMPLEMENTATION COMPLETION REPORT

PERU

DEBT AND DEBT SERVICE REDUCTION(LOAN NO. 4133-PE)

May 6, 1998

Country Management UnitBolivia, Paraguay and PeruLatin America and the Caribbean

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosed withoutWorld Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTSCurrency Unit - Nuevo Sol (S/.)

Exchange Rate(as of April 21, 1998)US$1.00 = S/. 2.82

FISCAL YEAR OF BORROWERJanuary 1 to December 31

ABBREVIATIONS AND ACRONYMS

BEP - Buyback Equivalent PriceCOFIDE - Corporacion Financiera de Desarrollo

(Development Finance Corporation)DDSR - Debt and Debt Service ReductionDRE - Debt Reduction EquivalentEFF - Extended Fund FacilityFLIRB - Front-Loaded Interest Reduction BondGDP - Gross Domestic ProductIDB - Inter-American Development BankIFI - International Financial InstitutionIMF - International Monetary FundJEXIM - Export-Import Bank of JapanLIBOR - London Interbank Offer RateMOP - Memorandum of the PresidentPDI - Past-Due InterestPDP - Post-Deal PricePRAL - Pension Reform Adjustment LoanSDR - Special Drawing Right

Vice President: Shahid Javed BurkiDirector: Isabel Guerrero

Lead Economist: Ernesto MayTask Manager: Fred Levy

FOR OFFICIAL USE ONLY

TABLE OF CONTENTSPage

Evaluation Summary ........................................................... i

Part I: Program Implementation Assessment ...................................... IA. Statement and Evaluation of Objectives ........................................................... 1B. Achievement of Objectives ........................................................... 2

Reduced Debt Burden ........................................................... 2Flexibility of Debt ........................................................... 8Access to External Financing and Investment ........................................................ 8Reserves, capital inflows, and exchange rate ......................................................... 8Terms of external financing ........................................................... 9Domestic financial markets .......................................................... 12Macroeconomic Performance .......................................................... 12

C. Bank Performance .......................................................... 13D. Borrower Performance .......................................................... 13E. Lessons Learned .......................................................... 14

List of Text TablesTable 1: Debt and Debt Service Reduction Operation ................................................... 3Table 2: Debt Reduction Equivalent ........................................................... 5Table 3: Equivalent Buyback Prices, Break-even Prices, and Post-deal Prices ............ 6Table 4: Debt Service Relief ........................................................... 7Table 5: Financial Indicators .......................................................... 10Table 6: Macroeconomic Performance .......................................................... 12

Part II: Statistical Annexes .......................................................... 15Table 1: Summary of Assessments .......................................................... 16Table 2: Related Bank Loans .......................................................... 17Table 3: Project Timetable .......................................................... 18Table 4: Cumulative Loan Disbursements .......................................................... 19Table 5: Project Cost .......................................................... 20Table 6: Project Financing (US$M) .......................................................... 21Table 7: Status of Legal Covenants .......................................................... 22Table 8: Bank Resources .......................................................... 23Table 9: Bank Missions .......................................................... 24

Annex I: Project Implementation Review from Borrower's Perspective ....................... 25

Map

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosed withoutWorld Bank authorization.

DEBT AND DEBT SERVICE REDUCTION LOANPERU

(Loan No. 4133-PE)

Evaluation Summary

The Debt and Debt Service Reduction (DDSR) Loan to Peru was approved onFebruary 11, 1997 and fully disbursed on March 6, 1997. The US$183 million DDSR Loan, inconjunction with US$50 million set aside from the Pension Reform Adjustment Loan (PRAL)approved at the same time, helped Peru to purchase the collateral required for implementation ofthe DDSR operation agreed with its commercial bank creditors, which closed on March 7, 1997.Together with parallel support from the IMF and IDB, the DDSR Loan financed about 47 percentof the upfront costs of the DDSR operation. Cofinancing from the Export-Import Bank of Japanprovided coverage for an additional 7 percent of the upfront costs of the operation.

Program Objectives

The interrelated objectives of the DDSR loan were to reduce the burden of future debtservice to a level consistent with Peru's debt servicing capacity, thereby reducing marketuncertainties and encouraging the investment, both foreign and domestic, needed to sustain andrealize the benefits of Peru's economic reform efforts. The reduction of market uncertainty wasexpected to be reflected in improved access to international capital and financial markets.

The DDSR operation covered more than US$10 billion of public and publicly guaranteeddebt to commercial banks and private suppliers, including contractual interest of more than US$6billion. Creditors elected to convert 41 percent of principal into front-loaded interest-reductionbonds (FLIRBs), 25 percent into discount bonds, and 4 percent into par bonds. The remaining 30percent of principal was retired via buyback. Contractual interest was reduced by a recalculationat interest rates below originally contracted levels. Remaining eligible interest was retired byconversion into a PDI bond (61 percent), 30 percent via buyback, and 9 percent with cashpayments made before and at closing. The DDSR Loan thus enabled Peru to restructure about 40percent of its public and publicly guaranteed debt and to reduce its face value by more than US$3billion, not counting interest forgiveness.

Achievement of Objectives

Implementation of the DDSR operation resulted in a debt reduction equivalent (DRE) of56 percent of the eligible debt and 11 percent of total public and publicly guaranteed debt, notcounting the estimated interest forgiveness. The projected net present value of the cash-flowsavings amounted to more than US$2 billion (3.3 percent of GDP), with an internal rate of returnof 27 percent. In addition, interest rate risk was substantially reduced by the conversion of 85percent of the eligible debt, after buyback, into fixed-rate instruments for the next 10 years.

ii

Completion of the DDSR operation naturally reduced somewhat Peru's ability to adjustfuture debt service obligations through rescheduling, as the post-operation share of bonds in thepublic and publicly guaranteed debt was increased to 14 percent. Nevertheless, Peru's highinternational reserves and enhanced access to external financing provides greater room formaneuver in its overall debt management.

A principal benefit from the completion of the DDSR operation was the enhancement ofPeru's creditworthiness in the eyes of external lenders and investors. A number of indicatorsover the course of 1997 suggest that the operation was achieving this objective. For example,between the announcement of an agreement in principle with private external creditors inOctober 1995 and the end of 1997, Peru's international reserves grew by more than US$4 billion,or more than 70 percent. Capital inflows from foreign private direct investments, exclusive ofprivatizations, rose steadily from a quarterly average of about US$361 million in the first threequarters of 1995 to US$433 million from the last quarter of 1995 through the first half of 1996,and to US$464 million from mid-1996 through September 1997. The quarterly flow of foreignportfolio investment doubled over the same period.

Following completion of the operation, ceilings on Peru risk were raised, and term creditsas long as ten years became available after several years in which only short-term money hadbeen available. The share of external credit lines in the total liabilities of the Peruvian bankingsystem rose from 16 percent at the end of 1996 to 24 percent in November 1997, and the share offoreign capital in the total capital of the banking system increased from 27 percent to 41 percentduring the year. Spreads on foreign loans to prime borrowers fell some 40-60 percent to as lowas 30 basis points over LIBOR. Spreads on short-tern working capital loans were reported(before the Asian crisis) to have fallen around 1 00 basis points during 1997. By the end of theyear, Standard & Poors had upgraded its evaluation of Peruvian sovereign debt, rating it at thesame level as that of Argentina and Mexico.

GDP growth accelerated strongly in 1997, exceeding 7 percent as compared to 2.8percent in 1996. This resurgence of growth was accompanied by falling inflation and a reducedcurrent account deficit. The impact of the El Nifio phenomenon will dampen this performance in1998, but these generally positive trends should be sustainable through the end of the decade.

Bank Performance

Peru's successful DDSR operation could not have been completed without the financialsupport of the Bank, IMF and IDB. The Bank's performance in bringing this operation tofruition, including the close working relationship maintained with its IFI partners, was highlysatisfactory. A Briefing Note was sent to the Board in November 1995, one month following theannouncement of the agreement in principle between Peru and its creditors. The loan wasdisbursed less than a month after Board approval and closed three weeks later. Direct costs inthe preparation and supervision of the loan totaled just over US$74,000.

Borrower Performance

The Government of Peru, under the leadership of the Ministry of Economy and Finance,brought together an expert team of advisers and negotiators, which worked with patience anddetermination to complete the DDSR operation and assure the achievement of its objectives. TheGovermment was thus successful in its strategy for restoring Peru's creditworthiness as one of theprinciple elements of its reform program.

Lessons Learned

The long process leading up to Peru's DDSR operation reconfirms (i) the costliness to aneconomy of breaking its links to the international economy and adopting a go-it-alone strategy;and (ii) that success in reestablishing international creditworthiness ultimately depends on thequality of the country's macroeconomic management and reforms. While the Bank and the otherIFIs can play an important catalytic role, as they did in the Peruvian case, the quality of thecountry's own program and will to implement it are the decisive elements in making theoperation successful.

PART I: PROGRAM IMPLEMENTATION ASSESSMENT

A. Statement and Evaluation of Objectives

1. After the debt crisis of 1982, the Government of Peru suspended most debt servicepayments to its external creditors. Arrears grew rapidly, and the moratorium was progressivelyextended to debt service owed to the IFIs and to debts owed by private sector borrowers. In1986, Peru was declared ineligible for IMF borrowing; it was placed in non-accrual status by theWorld Bank in 1987 and by the IDB in 1989. Faced with the threat of expulsion, current debtservice was resumed to the IMF in mid-1 989. Nevertheless, Peru remained effectively isolatedfrom the international financial community.

2. The new Government elected in July 1990 introduced a deep and comprehensivestabilization and reform program and began initiatives to restore the country's links to theinternational financial community. Arrears were cleared to the IDB in September 1991, and withthe IMF and the Bank in March 1993. Successive rescheduling agreements were reached withParis Club members in 1991, 1993, and 1996, the last including a multi-year restructuringintended to eliminate the need for future reschedulings. In October 1995, the Government ofPeru and the Bank Advisory Committee, representing private, commercial creditors, announcedan agreement in principle to restructure and reduce the present value of outstanding debt andarrears to commercial banks and suppliers.

3. The Government requested support from the Bank, IMF, IDB, and the Export-Import Bankof Japan (JEXIM) to help finance the up-front costs of the debt and debt service reductionagreement (DDSR). Bank support included the US$183 million DDSR loan and US$50 millionset-aside from a parallel US$100 Pension Reform Adjustment Loan (PRAL). These operationswere approved by the Executive Directors on February 11, 1997, and the loans were signed onFebruary 26. The DDSR agreement between Peru and its commercial creditors was closed onMarch 7, 1997. Support from the IMF included SDR 149.95 million in funds set aside from itsexisting Extended Fund Facility (EFF) and an SDR 71.66 million Augmentation Loan. IDBprovided a stand-alone DDSR loan of US$233 million. The JEXIM's support consisted ofUS$100 million in cofinancing for the Bank's PRAL and the IMF's EFF. The remaining costs(about US$688 million) were financed by the Government from its own resources.

4. The interrelated objectives of the DDSR Loan were to reduce the burden of future externaldebt service to a level consistent with Peru's debt servicing capacity, and thereby also to reducemarket uncertainty over Peru's ability and willingness to meet its debt service obligations. TheDDSR would thus serve to lower inhibitions to private investment, both domestic and foreign,and enhance the country's ability to sustain its reform efforts. The reduction of marketuncertainty was expected to be reflected in improved access to international capital markets withlengthening maturities and a falling country-risk premium on debt and an increasing flow of

2

private direct investment. This, in turn, would be reflected in strong macroeconomicperformance and would provide additional support to the reforms.

5. Given the quality of macroeconomic management sustained over six years and thecontinuing reform program, investor and lender attitudes toward Peru were already visiblyimproving prior to approval of the DDSR operation, particularly as expectations rose that fullrestoration of relations with creditors would soon be realized. Thus, the objectives of the Loanwere reasonable and realistic. At the same time, sustaining the reform effort was essential forachieving the growth and poverty objectives central to the Government's program and to theBank's assistance strategy.'

B. Achievement of Objectives

Reduced Debt Burden

6. The DDSR agreement covered US$10,576 million of public and publicly guaranteed debtto commercial banks and private suppliers, including contractual interest of US$6,370 million(Table 1).2 The menu of options for debt principal included a debt buyback and three debtexchange instruments: a par bond, a discount bond, and a front-loaded interest reduction bond(FLIRB). The principal amounts of the discount and par bonds were fully collateralized by thepledge of US Treasury zero-coupon bonds; in addition, payment of six months interest on thosebonds were secured on a rolling basis by the pledge of cash or permitted investments.4 Theprincipal of the FLIRB was not collateralized, but six months interest was secured on a rollingbasis for the first 11 years. Contractual interest was reduced as a result of a recalculation ofinterest rates. The remaining eligible interest was reduced via partial payments prior to closing,cash payments on the closing date, and an exchange for PDI bonds. The agreement allows therepurchase of bonds at any price and time, provided certain conditions are met by theGovernment of Peru.5

Inasmuch as this was a one-tranche, fast-disbursing operation, with implementation effected at the signing of theagreement with creditors and the simultaneous disbursement of the Loan funds, project implementation was notan issue.

2The final figures shown here differ slightly from those foreseen at the time of the Memorandum of the President(Report No. P-7030-PE of November 25, 1996). According to Government calculations, past due interest wasreduced, by US$2,417 million as a result of a recalculation at interest rates lower than those originallycontracted. Not included in the above figures is US$593.5 million in principal and interest exchanged inprivatization agreements.

3Details of the terms of the exchange instruments for both principal and eligible interest are given in the DDSRMOP, op.cit., Table 1, p. 4.

4Interest collateral was based on a reference annual interest rate of 7 percent for the discount bond, and on the basisof a gradually rising interest rate for the par bond (3 percent in years 1-15, 4 percent in years 16-25, and 5percent in years 26-30).

5These conditions are set out in full on page 111-10 of the "Republic of Peru, Term Sheet for the 1996 FinancingPlan."

Table 1: PERU - Debt and Debt Service Reduction Operation(US$ Millions)

Eligible for DDSR Applicable to DRETotal Debt $8159 1/ $8159 1/

Principal $4,206 $4,206Interest Arrears $3953.3 1/ $3953.3 1/

On Principa On Past Due InterestPar Bond 4.3% $183 Partial Payments $121Discount Bond 24.7% $1,041 Downpayment upon Closing $225FLIRB 40.8% $1,715 PDI Bond $2,402Buyback 30.1% $1,267 Buyback $1,205

Total 100% $4,206 $3,953

Summary of DDSROld Debt (including PDI) $8159 1/ Uses of FundsNew Debt $4,873 Total Funds Required $1,475 L

Forgiveness (from PDJ) $2,417 for cash payments on PDI $346for Buyback payments $950

Face Value of Debt Reduction $3,286 for enhancements $180o/w Discount Bond $468 Par Bond $38o/w cash payments on PDI $346 Discount Bond $114o/w Principal & Interest Retired in Buyback $2,472 FLIRB $28

Sources of Funds 100.0% $1,475NPV of Interest Payment Reduction $555 Multilateral 46.6% $687

World Bank 15.8% $233Commercial Bank DRE (% of Eligible Debt) 55.78% IDB 15.8% $233Secondary Market Price of Debt (cents on the dollar) $ 0.379 IMF 15.0% $222Buyback Equivalent Price (BEP) (cents on the dollar) $ 0.315 JEXIM 6.8% $100BEP - IMF Methodology (cents on the dollar) $ 0.307 Local Funds 46.6% $688

1/ This number excludes US$2,417 million of past due interest reduction as referred to in footnote 2 of the text.

4

7. From the menu, creditors elected to convert 40.8 percent of principal into FLIRBs, 24.7percent into discount bonds, and 4.3 percent into par bonds; the remaining 30.1 percent ofprincipal was retired via buyback at a weighted average price of about 36 cents on the dollar. Asregards eligible interest, 60.8 percent was converted into the PDI bond, 30.5 percent was retiredvia buyback, with the remaining 8.7 percent retired with cash payments before and at closing.

8. The DDSR Loan thus enabled Peru to restructure about 40 percent of its public andpublicly guaranteed debt and to reduce its face value by US$3.2 billion, excluding forgiveness ofinterest.6 The debt reduction equivalent (DRE) was US$4,551 million, or 55.8 percent of theeligible debt7 and 11.4 percent of total public and publicly guaranteed debt (Table 2). The DDSRoperation thus achieved debt relief for Peru at a significantly lower financial cost than a market-based debt reduction (Table 3). At 31.5 cents on the dollar, the buyback equivalent price (BEP)was 55 percent lower than the post-deal price (PDP), a discount greater than that achieved inmost previous Brady deals.

9. The cash-flow savings and interest rate relief provided by the deal (compared to acounterfactual scenario) are shown in Table 4. The up-front costs of the agreement totaledUS$1,475 million, of which $346 million consisted of cash payments to reduce the amount ofeligible interest, $950 million to the debt buyback, and the remainder to the costs of principal andinterest collateral for the new bonds. After an initial negative impact on cash flow (-US$230million) in the first year, compared to the counterfactual projection, annual debt service relief insubsequent years is projected to average about US$167 million. The projected net present valueof the cash-flow savings amounted to US$2,045 million (3.3 percent of GDP), with an internalrate of return (compared to counterfactual debt service) of 27 percent.8 In addition, interest raterisk was substantially reduced via the conversion of 85 percent of the eligible debt (afterbuyback) into fixed-rate instruments for the next 10 years.9

6 The estimated interest forgiveness is not included in the calculations of the impact of the DDSR agreement.Inclusion of PDI forgiveness would raise the DRE estimate to 66 percent of eligible debt.

s The details of this calculation may be found in DDSR MOP, op.cit., pp. 12-13.9 Taking post-Brady bond conversions into account, the percentage of Brady bonds outstanding with fixed interest

rates for the next 10 years has risen to 92.5.

Table 2: PERU - Debt Reduction Equivalent(USS Millions)

Face Value of Chanae | Adjusttents Debt Reduction Bquivalcot (DRE)

Flce Face New NetFee Falue Pf t Peyt N Comm. Aditional Total TotW Totd DRE DRE

Value Value Mawe Vale of Vathe of Value of EquMinet Adjust. Debt OfliciS Debt Extemal as %of as%of

Eigib}c Debt Conan. New Intterest of Reduction Lending Reduction Debt Tobl GDP

Debt Reduction Debt Comm. Svioce Colatera Equvalent Equivent Debt

Reduction Debt Reducton (DRE)

(1) (2) (3) (4) (5 (6) (7) tE) (9) (10) (11) (12) (13) (14) ('5

[(2>.(3)] [(l)-(4)] 1(6M]7) K(4)1M 1(9X(1)J [(10)-(11)1 1(12)((13)]

Pe159 3,286 * 3,286 4,873 1,035 IS0 IM 4,551 55.3% 737 3,764 32,061 11.7% 6.4%

?,^_lw 4,206 1,735 0 1,735 2,471 555 180 735 2,470 58.70A

DiscourntBond 1,041 468 0 468 572 0 114 11 582 56.0%

Pu Bond 183 0 0 0 183 97 38 135 135 74.0%

FLIRB Bornd 1,715 0 0 0 1,715 458 28 486 486 28.3Y%

BuyE-k 1,267 1,267 0 1,267 0 0 0 0 1,267 100.0%Y

aatflua 3,953 1,551 0 1,551 2,402 530 0 530 2,081 52.6%

PDI'Bond 2.402 0 0 0 2.402 530 0 530 530 22.1%

PDI Down Payment 346 346 0 346 0 0 0 0 346 100.0%

PDIRetired inByback 1,205 1,205 0 1,205 0 0 0 0 1,205 100.0%A

3,906 730 0 730 3,176 383 96 479 1,209 31.0% 90 1,119 5.806 19.3% 15.1

* 7.429 1,315 0 1,315 6,114 1,031 528 1,559 2,874 38.7% 305 2,569 12,522 20.5Y 15.5

4exico 47,170 7,061 1,027 6,034 41,136 7,090 7,166 14,256 20,290 43.0% 3,732 16,558 81,205 20.4% .0Y

6,600 2,603 828 1,775 4,825 1,107 472 1,579 3,354 50.8% 465 2,889 26.004 11.1% 6.6M

Rica 1.608 1,029 0 1,029 579 115 37 152 1,181 73.4% 177 1,004 3,979 25.2% 19.2'

teneniel 19,011 1,921 1,166 755 18,256 2,491 1,729 4,220 4,975 26.2% 687 4,288 26,170 16.4% 9.8

buglay 1,610 628 89 539 1,071 158 111 269 80S 50.2% 140 668 4,625 14.4% 8.4%

{igea 5.339 3,310 0 3,310 2,029 612 357 969 4,279 80.1% 0 4,279 34,625 12.4% 12.55

29,335 3,265 0 3,265 26,070 5,159 3,032 8,191 11,456 39.1% 2,117 9,339 58,426 16.0% 4.1

ocdan 895 142 0 142 753 114 120 234 376 42.0% 0 376 7,184 5.2% 7.9e

57.600 3,994 350 3,644 53,956 3,196 3,783 6,979 10,623 18.4% 0 10,623 93f573 11.4% 2.15

8,174 3,146 0 3,146 5,028 302 389 691 3,837 46.9% 231 3,606 12,211 29.5% 34.85

Republe 1,186 687 0 687 500 0 5S 58 745 62.8% 0 745 4,214 17.4% 7.85

bband 14.333 6,7S0 135 6,645 7,688 1,425 599 2,024 8,669 60.5% 380 8,29 43,623 19.0% 9.

ihed Av_a 36.6% 16.0% 5.5

1) I desUSS315 million of dowvannt and p l payments towud PDI.

2) Discount of 45 peaent appied to face value ofdiscount bonds.

3) New money wa not included as part ofth agreenmnt

e NPVof iert avn reltive to mnazet rates as of September 12, 1996 (LIBOR+13/16).

7) Face valu ofpricipa and interet coae.

9) F teake into account the expected present vale of i_e service r recapture clauses, whee apphcable.

13) At the begting of te year in which the DDSR operaton was concluded. Iclus Long-Term and Medium-Tenn Public Debt,

ne_etb reas this debt ad nt uae ofIM reoure.

I) GDP 6gu for 1995.Eliibk debt does not include USS582 milion of PDI forees.

* Tre Philippins operation was concluded in two phas.

Table 3: PERU - Equivalent Buyback Prices, Break-even Prices, and Post-deal Prices

Marlxt Markeat Break-Even Buyback Equinknt Post-Deal Saviprelativto Preal Distrbto

Valu of Vahie of Price (BE) Price (BFP) Pnice (PDP) martet bWck Pncoe (PD) of Gain

Enhaceents (ME) a/ New Ins numf (MNI) bW cents per dollar c/ cents per dolla dt cents per dolla e/ (PDP-BEY PDP oents per dollar 0 (PDP-BE)t

(USS milin (US$ mirlli-) (PDP-PD)

0 ~~ ~ ~ ~~ ~ ~ ~~ ~ ~~(1) (2) (3) (4) (5) (6)-[(5-3Y5] (7) (8)=[(5-3Y(5-7)]

Peru 1,434 3,953 48.45 31.51 69.82 30.6% 37.90 66.9% A

Panm 167 2,249 59.69 13.83 79.96 25.4% 54.78 80.5%

Ecuador 528 2,759 37.14 23.06 48.97 24.2% - -

Me3dco 5,252 20,206 41.00 25.88 52.00 21.2% 36.00 68.8%

Philippie 670 3,749 46.00 - 52.00 11.5% 40.00 50.0%

Costa Rica 210 383 24.00 17.78 39.00 38.5% 12.00 55.6%

Venezuea 1,819 10,678 50.00 36.56 61.00 18.0Y. 37.00 45.8%

Uruua 423 1,048 60.00 52.35 74.00 18.9% 56.00 77.8%

Nigeria 1,623 2,131 40.00 37.93 45.00 11.1% 21.00 20.8%

Philippiln gt 986 2,504 52.00 49.37 76.00 31.6% 52.00 100.0%

Argentina 3,086 13,425 46.00 26.94 56.00 17.9% 18.00 26.3%

Bulgaria 628 1,978 24.00 16.37 30.00 20.0% 20.00 60.0%

Poland 1,951 5,381 51.00 22.51 84.00 39.3% 30.00 61.1%

Averag 1,445 5,541 44.24 29.33 58.16 23.1% 34 25 58.8%

a/ ME: Prepament of coateral (interat oaer vaed at Iinus the average pr of 'when-and-ifisued innents as of July 1996), pluh downpayment on PDland cash for buyback.

b MNI: For Persbased on average quotatom of when-and-ifissued" i ientsas of July 1996.

ct BE - MNltED. The BE mmus Ihe aerage pre at which the DDSR occuredd/ BEP = ME/DRE.et PDP - (MNI-MEy(Ebigible Debt-DRE).f Price - of October 27, 1995.g/ Phase 2

Table 4: PERU - Debt Service Relief(USS Milions )

1997 1998 1999 2000 2001 2002-2017 a/ 2018-2028 a/

UpaK AMpnent(I) Cah for Buyback 950

(2) Dowupaytet on PDI 346(3) CoDaterl Pubases IS0 0 0 0 0 0 0

(4) Interst Payments 79 160 212 223 225 230 53

(5) Amorfizain 0 0 0 0 0 257 79

(6) Interest Earnis on coliateal 3 6 7 7 7 5 3

Additional Official Lendin bI(7) Loan Amount 787

(8) Intrt Payments 24 51 54 55 57 30 0

(9) A-octzaion 0 0 0 0 0 49 0

Co dc/(10) Downpayment on PDI 346(I1)Amorfizafion 0 0 0 0 0 433 93

(12) Interest Payments 0 456 480 492 494 394 14

(13) Up-front LiqWdity Impact of DDSR[(10)+(7)-(3>-(2)-(1)] -343 0

DDSR Debt Servie Rehlef(14)InteestReliefofDDSR[(12>(8)+(6)-(4)] 113 252 274 221 219 140 -36

(15) Amortization Rehief[(11)-(9)-(5)] 0 0 0 0 0 127 13

(16) Total Debt Service Rehef[(15)+(14)+(13)] -230 252 274 221 219 267 -23

a/Annual averages.V/ From IDRB. IDB, IMF, and JEXIM Ban1kcl Coulerfichia conits of two MYRAS (1996 and 2000) and PDI. The MYRAs are 4 by 20 and bear iterest rate of LIBOR + 13/16 percent PDI is the same as in Brady.

Source: World Bank StaffEstmates.

8

Flexibility of Debt

10. The DDSR agreement, coupled with the additional lending from the IFIs, resulted in anincrease in the relative exposure of IFIs (including use of IMF credit), from 20 percent of Peru'spublic and publicly guaranteed debt before the agreement to 28 percent in 1997. In addition, thepost-agreement share of bonds in public and publicly guaranteed debt rose to 14 percent.Consequently, Peru's flexibility to adjust future debt service obligations via rescheduling wasreduced. Nevertheless, Peru's high international reserves and enhanced access to externalfinancing (see below) provides greater room for maneuver in its overall debt management.

Access to External Financing and Investment

11. A principal benefit expected from the completion of the DDSR agreement was thereduction of uncertainty regarding Peru's ability and willingness to service and repay its financialobligations. Indicators of creditworthiness in the eyes of external lenders and investors may besignaled by changes in international reserves, trends of real interest rates in the domestic market,and exchange rate movements. More specific indicators include the amounts, interest rates, andrepayment periods of financing available from external lenders, the number and type of lendersand investors demonstrating willingness to commit funds to Peru, prices in international marketsof the bonds issued in the DDSR debt exchange, flows of direct and portfolio investments.Recent developments for some of these indicators are presented in Table 5.

12. Greater confidence on the part of savers and investors, both national and foreign, wasalso expected to strengthen economic growth prospects and sustain reform efforts. Table 6compares recent macroeconomic performance with expectations at the time of the DDSR loan.

13. Peru's economic performance and perceptions of its creditworthiness are discussed in theparagraphs below. It must be recognized, however, that Peru's creditworthiness, access toexternal resources, and overall economic trends respond to many factors beyond the signing ofthe DDSR agreement. Arriving at the agreement in the first place depended on debt holdershaving become convinced of the Government's seriousness in meeting the new commitments tobe undertaken, as reflected in its negotiating positions and, more importantly, in its overallprogram of macroeconomic stabilization, structural reform, and reintegration into theinternational economy and financial system. At the same time that the DDSR agreement wasnecessary to underpin the sustainability of the Government's economic program, it was the verycredibility of the economic program that laid the basis for the DDSR agreement and itssustainability through time. The indicators discussed below, therefore, necessarily reflect manyfactors and actions taken over time, and not just the signing of an agreement at a moment in time.Growing appreciation of Peru's track record and related expectations of the increasingimminence of the agreement are thus reflected in improving indicators prior to the agreement.

Reserves, capital inflows, and exchange rate

14. Table 5 shows recent trends for international reserves, the nominal exchangerate, domestic financial markets, and private long-term capital flows. Between the

9

announcement of an agreement in principle with private external creditors in October1995 and the end of 1997, Peru's international reserves grew by more than US$4 billion,or almost 70 percent. The exchange rate moved approximately in line with inflationdifferentials with major trading partners between September 1995 and the beginning of1997, remaining stable in nominal terms through the first 10 months of 1997 in reflectionof the growing capital inflows, and depreciating only slightly during the last two monthsin the wake of the Asian financial crises. Capital inflows from foreign private directinvestments, exclusive of privatizations, rose steadily from a quarterly average ofUS$361 million in the first three quarters of 1995 to $433 million from the last quarter of1995 to mid-1996, and to $464 million from mid-1996 through September 1997. Foreignprivate portfolio investments grew similarly, averaging quarterly US$46 million, $87million, and $93 million, respectively, for the same periods.

Terms of external financing

15. Available information suggests that the completion of the DDSR agreement has had asignificant impact on the terms of foreign financing to Peruvian private borrowers, despite onlysmall reductions so far in the high mandatory provisioning requirements demanded by bankregulatory agencies in the originating countries, particularly in Europe. Ceilings on Peru riskhave been raised and, in contrast to two years ago when only short-term credit was available,banks are now offering term credits, in some cases as long as ten years to prime borrowers.External lines of credit available to the Peruvian banking system have increased significantly,and the share of such funds in total bank liabilities rose from 16 percent to 24 percent betweenend-1966 to November 1997.

16. New sources of finance, including foreign pension and mutual funds are reportedlyentering the market. Many private borrowers are now able to access external funds directly, andspreads to prime private borrowers have reportedly fallen by 40-60 percent, to as low as 30 basispoints over LIBOR.10 Interest rates on short-term working capital loans were reported to havedropped about 100 basis points during 1997 (prior to the Asian financial crisis), with interestrates on foreign trade financing falling some 25-50 basis points. By late 1997, COFIDE, thestate-owned, second tier development bank, was going to the external market for funds withoutseeking a government guarantee and was attracting funds at 50-75 basis points less than a yearearlier.

17. Another factor reportedly improving Peru's perceived creditworthiness and access toexternal financing has been significant investment by foreign banks over the past year in thelocal market. The share of foreign capital in the total capital of the banking system increasedfrom 27 percent to 41 percent during 1997. One effect of this foreign participation has beenincreased competition within the banking system, reflected in falling spreads.

10 In this regard, lenders responded to Peru's improved creditworthiness more rapidly than the rating agencies, withPeruvian borrowers being accorded better terms than similar borrowers in other Latin American countrieshaving higher ratings. Standard & Poor's has recently upgraded its evaluation of Peruvian sovereign debt,rating it at the same level as that of Argentina and Mexico.

10

Table 5: Peru - Financial Indicators

1995 1996

Indicators Sep Mar Apr May Jun Jul Aug Sep Oct Nov Dec

International reserves of CentralBank (US$m) a/ 6157 6819 6753 6865 7207 8326 8372 8482 8262 8422 8'40

Nominal exchange rate(SolesNUS$)_b/ 2.25 2.36 2.37 2.41 2.44 2.45 2.47 2.49 2.55 2.58 2.58

Interest rates on dollar loans anddeposits c/

Loans 16.6 17.1 17.0 16.8 16.6 16.5 16.6 16.7 16.9 16.9 16.8Deposits 6.2 6.2 6.2 6.2 6.2 6.2 6.1 6.0 5.9 5.8 5.7

Lima Stock Exchange Indexdeflated by US$ exchangerate (Dec.'91=100) 519 f/ 493 542 547 562 621 566 538 534

Private Sector bonds outstanding(US$ millions) gl 491 613 767 952 1054of which, financial companies 336 394 514 532 682

nonfinancial companies 155 219 253 420 4 72

Prices of Brady bonds - b/FLIRBs 48.9 53.01 56.3 55.9PDI 56.1 59.6 61.4 SIX 1

Foreign private capital flows(US$ millions) d/Direct investment(ex-privatizations) 230 423 422 526 511

Privatization investment 20 14 17 1464 193Portfolio investment e/ 64 47 206 104 -16Long-term loans (gross disburs.) 298 242 274 258 225

Notes:a/ End of periodb/ Period average.c/ Weighted averages for period.d/ Quarterly data for period ending in month indicated.e/ Foreign share purchases in Lima Stock Exchangeand net purchases of bonds and other long-termfinancial instruments.Quarterly data for period ending in month indicated.fl December 1995g/ Only includes bonds registered with the NationalSupervisory Commission for Companies and Securties(CONASEV).

11

Table 5: Peru - Financial Indicators(continued)

________________________ 1997Indicators Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

International reserves ofCentral Bank (US$m) a! 8648 9099 9173 9409 9674 9556 9769 9874 9768 10186 10202 10169

Nominal exchange rate(Soles/US$) b/ 2.63 2.64 2.63 2.66 2.66 2.66 2.65 2.65 2.64 2.67 2.72 2.72

Interest rates on dollar loansand deposits c/

Loans 16.7 16.5 16.4 16.4 16.2 16.1 16.0 15.8 15.7 15.6 15.6 15.6Deposits 5.7 5.6 5.6 5.6 5.6 5.6 5.6 5.6 5.5 5.4 5.3 5.2

Lima Stock Exchange Indexdeflated by US$ exchangerate (Dec.'91 -100) 566 595 613 640 774 789 748 722 734 668 635 635

Private Sector bondsoutstanding

(US$ millions) 9/ 1101 1131 1224of which, financialcompanies 618 643 702nonfinancial companies 483 488 522

Prices of Brady bonds - blFLIRBs 55.5 61.3 56.1 53.0 58.4 60.4 60.8 59.9 61.9 52.0 57.5 59.4PDI 60.5 66.5 62.2 59.6 64.1 65.5 66.5 65.9 67.4 58.0 62.5 66.0

Foreign private capital flows(US$ millions) d/Direct investment(ex-privatizations) 386 500 398

Privatization investment 5 12 5Portfolio investment e/ 104 265 10

Long-term loans 424 267 356(gross disburs.)

Notes:a!/ End of periodb/ Period average.cl Weighted averages for period.dl Quarterly data for period ending in month indicated._/ Foreign share purchases in Lima Stock Exchange andnet purchases of bonds and other long-term financialinstruments.Quarterly data for period ending in month indicated.fl December 1995g/ Only includes bonds registered with the NationalSupervisory Commission for Companies and Securties(CONASEV).

12

Domestic financial markets

18. Peru's improving access to external capital has been reflected both in domestic interestrates for foreign currency deposits and in the growth of the Lima stock exchange. As seen inTable 5, average interest rates for dollar accounts in the commercial banks have fallen steadilysince September 1995, with the decline particularly marked for term deposits since mid-1996,after a brief run-up in the first half of the year. The Lima Stock Exchange Index rose steadilyover the period (up some 41 percent between September 1995 and September 1997), beforebeing impacted by the Asia crisis. Foreign participation in the Exchange doubled from anestimated US$2.6 billion at the end of 1995 to US$5.2 billion by September 1997.

Macroeconomic Performance

19. The Peruvian economy went through a period of adjustment in 1996 after experiencingvery high growth rates in 1994 and 1995. The Government's demonstrated detertnination toprevent overheating of the domestic economy, to maintain external accounts viability, and topursue a debt agreement with its creditors reinforced Peru's growing reputation for soundeconomic management, reassured investors and the international financial community, andestablished the basis for a strong economic performance in 1997 and beyond (see Table 6). GDPgrowth exceeded 7 percent in 1997, compared to 2.8 percent in 1996, led by increases in exportsand rising private investment. This resurgence of growth occurred in the context of fallinginflation (below 7 percent), improved fiscal accounts, and a reduced current account deficit. Theimpact of the El Nifno phenomenon is likely to dampen this performance in 1998, but thesegenerally positive trends should be sustainable through the end of the decade.

Table 6: Macroeconomic Performance

Actual Projected EstimatedIndicators Av. 1991-95 1996 1997-2006a 1997

GDP Growth Rate, real (%) 5.5 2.9 5.7 7.5

National Accounts (% current GDP)Gross fixed investment 19.6 23.5 24.6 24.7

Public sector 3.4 3.8 4.3 3.9Private sector (include. stock 16.1 19.7 20.3 20.8change)

Gross national savings 14.5 17.6 20.8 19.5Exports, gnfs 10.9 12.0 12.1 12.7Imports, gnfs 13.8 16.4 14.8 16.7Current account balance -5.0 -5.9 -3.8 -5.2

Public sector (% current GDP)Total revenues 16.1 18.2 18.0 17.6Current expenditures 16.0 12.2 13.8 11.6Interest payments 3.3 2.3 2.1 1.7Capital expenditures 4.4 4.3 4.3 4.2Overall balance -2.5 -1.1 -0.1 -0.3

Inflation (CPI, end of period) 46.1 11.8 5.1 6.5

1MOP, op.cit., p. 15 I I I

13

20. Structural reforms have continued, albeit not at the pace of the early years of the presentGovernment. In addition to the reforms undertaken under the Pension Reform Adjustment Loan,continued privatizations, particularly of the holdings of Petroperu, the state petroleum company,enabled disbursement of the Bank's Privatization Adjustment Loan by January 1998. Otherprivatizations were carried out, most notably in the mining and fisheries sectors; a new programfor the concessioning of major infrastructure investments was launched, and first steps weretaken toward the rationalization and privatization of the costly state sugar cooperatives andcoastal hydraulic projects; good start-up progress was achieved in the titling and registration ofinformal urban properties; and important steps were taken to improve access to and the efficiencyof the judicial system. Progress has been less even in the trade area, with some additionalprotection for the agriculture sector reducing the benefits of an overall lowering of average tarifflevels. Other pending actions for the modernization and decentralization of government and theclosing of some gaps in the legal framework--e.g., the passage of a new water law--remain to beimplemented.

C. Bank Performance

21. The Bank, in close collaboration with the IMF and the IDB, played a key role over sevenyears in the process of completing Peru's reintegration into the international economy andfinancial system. In its early stages, this role consisted of assisting the Government in the designof its stabilization and reform program and in organizing the workout of its arrears with the IFIs.Completion of the arrears workout permitted a series of adjustment loans in support of thereforms undertaken and the reinitiation of investment lending. The Bank throughout maintaineda close dialogue with the economic team and the sector ministries. These efforts helped toestablish the basis for the sustained economic growth necessary to restore Peru's debt-servicingcapacity and attractiveness to new capital inflows. Bank staff also assisted Peru and its creditorsin various stages of the negotiations, making presentations to creditors' meetings andparticipating in the "roadshows".

22. Peru's successful DDSR agreement could not have been completed without the financialsupport of the Bank, IMF, and IDB. The Bank's performance in bringing this operation tofruition, including the close working relationship maintained with its IFI partners, was highlysatisfactory. Direct costs in the preparation and supervision of the loan totaled just overUS$74,000, involving 24 staff-weeks spread over FYs 1996 and 1997. A Briefing Note was sentto the Board on November 19, 1995, one month after the announcement of an agreement inprinciple between Peru and its creditors to restructure the debt. Disbursement of the DDSR loantook place on March 6, 1997, and the loan closed on March 31, 1997.

D. Borrower Performance

23. The Government, under the leadership of the Ministry of Economy and Finance, broughttogether an expert team of advisers and negotiators, which worked with patience anddetermination to complete the DDSR agreement and assure the achievement of its objectives.The Government was thus successful in its strategy for restoring Peru's creditworthiness as oneof the principle elements of its overall reform program.

14

E. Lessons Learned

24. Rather than providing new lessons, the long process leading up to Peru's DDSRoperation and its ultimate completion reconfirm (i) the costliness to an economy of breaking itslinks to the international economy and adopting a go-it-alone strategy; and (ii) that success inreestablishing international creditworthiness ultimately depends on the quality of the country'smacroeconomic management and reforms. While the Bank and the other IFIs can play animportant catalytic role, as they did in the Peruvian case, the quality of the country's ownprogram and will to implement it are the decisive elements in making the operation successful.

PART II:

STATISTICAL ANNEXES

16

Table 1: PERU DDSR - Summary of Assessments

ghieV~rnent a1~ ~ftve~ 5 ,1[1 Negligible N/A

Macroeconomic Policies XSector Policies XFinancial Objectives XInstitutional Development XPhysical Objectives XPoverty Reduction XGender Concerns XOther Social Objectives xEnvironmental Objectives XPublic Sector Management XPrivate Sector Development XDebt and Debt Service Reduction X

Identification XPreparation Assistance XAppraisal XSupervision X

Preparation XImplementation X

I E. ~~~~x

Covepaatint Asspisance X

Apprisa xgE0|Lsl e D*a

17

Table 2: PERU DDSR - Related Bank Loans

Structural Adjustment Loan Structural adjustment 1992 Completed(L34520-PE) and institutional

development

Trade Policy Adjustment Loan Structural adjustment 1992 Completed

(L34370-PE) and institutional

development

Financial Sector Reform Loan Structural adjustment 1992 Completed(L34890-PE) and institutional

development

Privatization Adjustment Loan Structural adjustment 1993 Completed(L35950-PE) and private sector

development

Privatization Technical Assistance Loan Institutional and private 1993 Completed(L345400-PE) sector development

Electricity Privatization Adjustment Structural adjustment and 1995 Third trancheLoan (L3 81 00-PE) institutional and private pending

sector development

Pension Reform Adjustment Loan Structural adjustment 1997 Completed(L4134-PE) and institutional

development

18

Table 3: PERU DDSR - Project Timetable

Preparation 1995 Nov-95

Appraisal Sep-96 Sep-96

Negotiations Nov-96 18-Nov-96

Board Presentation 19-Dec-96 11-Feb-97

Signing 19-Dec-96 26-Feb-97

Effectiveness 20-Dec-96 28-Feb-97

Tranche Release 20-Dec-96 6-Mar-97

Project Completion Dec-96 28-Feb-97

Loan Closing Dec-96 31-Mar-97

19

Table 4: PERU DDSR - Cumulative Loan Disbursements

Appraisal Estimate (US$m) 183.0

Actual (US$m) 183.0

Actual as % of Estimate 100%

Date of Disbursement March 6, 1997

20

Table 5: PERU DDSR - Project Cost (US$M)

Cash paymentsonPDI 0 315 315 0 346 346

Buyback payments 0 939 939 0 950 950

Enhancements 0 181 181 0 180 180Par bond 38 38 38 38Discount bond 114 114 114 114FLIRB 29 29 28 28

TOTAL 0 1,435 1,435 0 1,476 1,476

21

Table 6: PERU DDSR - Project Financing (US$M)

O. ~Araslstmt Ac..i CLSS..*; Li Foreign Local Foreign

CPCS, Total C--- t

IBRD* 0 233 233 0 233 233

IMF 0 233 233 0 222 222

IDB 0 233 233 0 233 233

JEXIM 0 100 100 0 100 100

Peru 0 635 635 0 687 687

TOTAL 0 1,434 1,434 0 1,475 1,475*($233m includes $183m from DDSR and $50m set-aside from PRAL)

Table 7: PERU DDSR - Status of Legal Covenants

k H 5-m~~Tpe Sttu Di*

Loan No.4133-PE 2.03 10 C 3/31/97 The Loan Closing Date shall be March 31, 1997 or such later date Fulfilled

_______ ~~~~~~~~~as the Bank shall establish._____

3.01 (a) I C The Borrower shall maintain separate accounting records of the3_01_(a)_I__ payments financed out of the proceeds of the Loan. Fulfilled

The Borrower shall have the accounts and records for each fiscal3.01 (b) I C year audited by independent auditors acceptable to the Bank and Fulfilled

furnish the audit to the Bank no later than six months after the endof each such year.

For all withdrawals made from the Loan Account, the Borrower

3.01 (c) 1 C shall maintain records and retain them until at least 1 year after the FulfilledBank has received the audit report for the fiscal year in which thelast withdrawal from the Loan Account was made.

4.01 (a) 9 C The Borrower and the Bank shall, from time to time, exchange Fulfilledviews on the Programn and the 1996 Financing Plan.

4.01 (b) 9 C The Borrower shall provide the Bank a report on the Program in Fulfilledsuch detail as the Bank shall reasonably request.

The Borrower shall keep the Bank informed of all notices,4.02 (i) 9 C certificates and confrmations issued to or received by the Borrower Fulfilled

in respect of the Collateral.

4.02 (ii) 9 C The Borrower shall provide the Bank monthly reports with respectto the Collateral within 15 days of the receipt thereof. Fulfilled

23

Table 8: PERU DDSR - Bank Resources

Through Appraisal N/A 21.9 67,257.00

Appraisal Through N/A 0.1 313.00Board Approval

Supervision N/A 2 6,676.00

Completion N/A 1.4 7,788.00

TOTAL 25.4 82,034.00

Table 9: PERU DDSR - Bank Missions

Through Appraisal Mar-95 to Aug-96 1 5 Economist

Appraisal through Sep-96 to Feb-97 - -

Board Approval

Supervision Mar-97

Completion Jan-98

ANNEX I

PROJECT IMPLEMENTATION REVIEW FROMBORROWERS PERSPECTIVE

LOAN NUMBER 4133-PE

REPUBLIC OF PERU

MINISTRY OF ECONOMY AND FINANCE

Project Implementation Review from Borrower's Perspective

RE: LOAN No. 4133 PE FOR US$ 183 MILLION

L Introduction

On February 26, 1997 Loan No. 4133-PE for US$183 million and Loan No. 4134-PE for US$50 million were signed by the Republic of Peru ("Peru") and the InternationalBank for Reconstruction and Development ("the Bank"). The loans have beensuccessfully disbursed and implemented and this is the first implementation reportsubmitted by Peru pursuant to their terms and conditions.

]L Overall Assessment of the Projects

1. Project Objectives

The general objective of the loans was to finance debt and debt service reduction(DDSR), normalizing relations with commercial creditors and reestablishingcreditworthiness.

The objectives of the Loan 4133-PE were'

From Peru's perspective, all the above objectives have been achieved successfully.

2. Peru's performance during the evolution of the Loans:

Savings: The savings were achieved through retroactive contractual interest raterecalculation of eligible interest, reduction in interest rates (Par Bonds, Flirbs and PDIBonds) and actual principal forgiveness (Discount Bonds). As can be seen in the tablebelow, the Brady Plan was a cost-effective transaction. From a total fUS$10.6 billion ofeligible debt, total savings amounted to US$5.4 billion.

In addition; US$50 million was set aside from Loan No. 4134-PE to finance a portion of the cost ofthe acquisition of collateral to secure principal on the Collateralized Discount Bonds andCollateralized Par Bonds.

SAVINGS OBTAINED IN THE BRADY PLAN(In million of US$ dollars)

Eligible Debt on March 7, 1997 10,575.7

1. Reduction in interest:- Recalculation 2,416.7- Buyback 711.5- PDI bonds 456.4

Total 3,584.7

II. Reduction in principal- Buyback 810.8- Discount bond 648.4- Par bond 85.9- PLIRB 404.8

Total 1,769.9

HI. TOTAL SAVINGS (I+1) 5,354.6

Other Benefits: In addition to the savings described above, DDSR has had abeneficial impact on the fiscal position and on the structural reforms program implementedby the current administration, due to the reduction of the debt service. Another veryimportant benefit relates to international capital markets at spreads lower than thoseoutstanding prior to the closing of the Brady deal. This is reflected in the observedappreciation of the Brady bonds in the secondary market. The above reflects a growingconfidence in Peru, which is supported by a perception of diminishing risk by bothPeruvian and international investors.

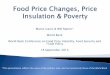

Peru: Total Public External Debt

3C.0 25.0 26.6 26.025.0 - 2 l 23|2 8|6

.C 2.0.

~ 5.0

=n10.0I 1, I1990 1991 1992 1993 1994 1995 1996 1997

Year

Note: End-year values, except for 1990 (July) and 1997 (June)

Peru has provided the Bank with the necessary information on the economic,financial, social, institutional, and other conditions related to the DDSR operation.

3. Bank's performance during the evolution of the Loans:

The loans were the result of a long and thoughtful process to structure DDSR forPeru. During negotiations, Bank staff were very helpful in explaining the Bank'sguidelines, policies and procedures, while being sensitive to Peru's concerns, needs andlimitations.

m. Operational Phase of Proiect.

The loans were one component of the Plan. The IDB, Eximbank of Japan and theIMF also supported this operation. Peru requested disbursal shortly before the closing andthis was accommodated under the loans. Operationally, the transactions and theobjectives have been met.

IV. Conclusion

The Loans together with the financial aid of other IFIs permitted Peru to normalizeand resolve commercial debt defaults that had existed since 1983. Peru has been pleasedwith the response of the international financial markets to both DDSR and the structuralreform programs implemented to globalize and modernize Peru's economy. Currently,Peru has access to less expensive capital to finance its various needs. This strategy shouldhave important social benefits in reducing poverty and creating a stable fiscal base as theeconomy expands.

MAP SECTION

I

IBRD 26572R

74- 20.~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~I

ECUADOR /) COLOMBIA

2' / / 2~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~2

2-~~~~~~~~~~~~7*~

TLJM-8cE I-''T ,

All.~ 0110 0 , ~' t ancorn( 5-

Toloro ~ b- "a,, ifr,o...P4 /'Oooo

L..b-y-q 9-Y-P~uierol 005WEA0Chl$RpyoA

CL RonoI0 AVEDROADS

Eisnntel*~ CAAMARCA" Ju----RALRAD

1- Mng olerro 0 RAILFERRY

Pocaoosoyo ,, 4 ~~~~~~~~~~~~~~~~~~AIRPORTSChioasO Ouc0 Qtn1ob-6. Toce OT

8' TEWILLO 0Soo~~~~~~~~~~n~~o ~~~co Poollo ~~~~~RIVERS.1. /"~~~~~~~~~~ ~~~ -. ~~~~DEPARTMENT BOUNDARiES

"> / '1,. ~~~~~INTERNATIONAL BOUNDARIES

ROOO i UANUCO0o

-10,~ ~ ~ ~~ .'-'1

P A C iF C ' ~~~~~~~~Y.,q.x.~ RCERRO DE QOV, '-.-P B RA ZI LP A C i F f C PtMia - PCASC 11n,. ,"--

H-oio- - fiPoro

Yooyo60PUERTO

Qs""' uill.b-6bo. MALDONA9l D

OACRLICA Z 0 - rS,m Viceot 6.Cpe. C-st-o,r-oo AYACIJCIi OIIros

C1hincls Al-C" 4-i

SnMn9 4ndh 0ANAI- Pi CUCVPorob

14' IDA ~~~~~~~~~~~~~~~~~~~~J-U~~~~~~~~~~ ~~~~~-uC ~ ~ ~ ~ ~ ~ ~ ~ 1

A u~ t - <

PER U 1 AcIi-

16' - -. Colorodo Tii- ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ ~ ~ 1

0 50 100 150 200 250 ~O 1 ~y MzWOOUEOU

KILOMETERSMleno

The oundaries, coin. de-omintions and any other W-oration,,- shaon -n this smp do not imply, as the part of the World 8ass Group, '- 4Mi 1 o

-18' any dgset on th eol mttr fay territory, or any esdortesnet B- *~

or aoetanoe o f suhbnais Boo del Rio ILEA

80O' 7,8' 7 4' 72 A,iHIL

MAY 1996