Embed Size (px)

Citation preview

Document of M CThe World Bank

FOR OMFCIAL USE ONLY

RpWt No. P-2849-IN

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE

INTERNATIONAL DEVELOPMENT ASSOCIATION

TO THE

EXECUTIVE DIRECTORS

ON A

PROPOSED CREDIT AND LOAN

TO INDIA

FOR THE

FARAKKA THERMAL POWER PROJECT

June 9, 1980

ITb docauent ha a restrited dlbos and may be ndb recbpients emily i he popfman Itheir official duoits comtents siy ot oterwtie he diod wiaot wor flsk autherlmtio.|

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

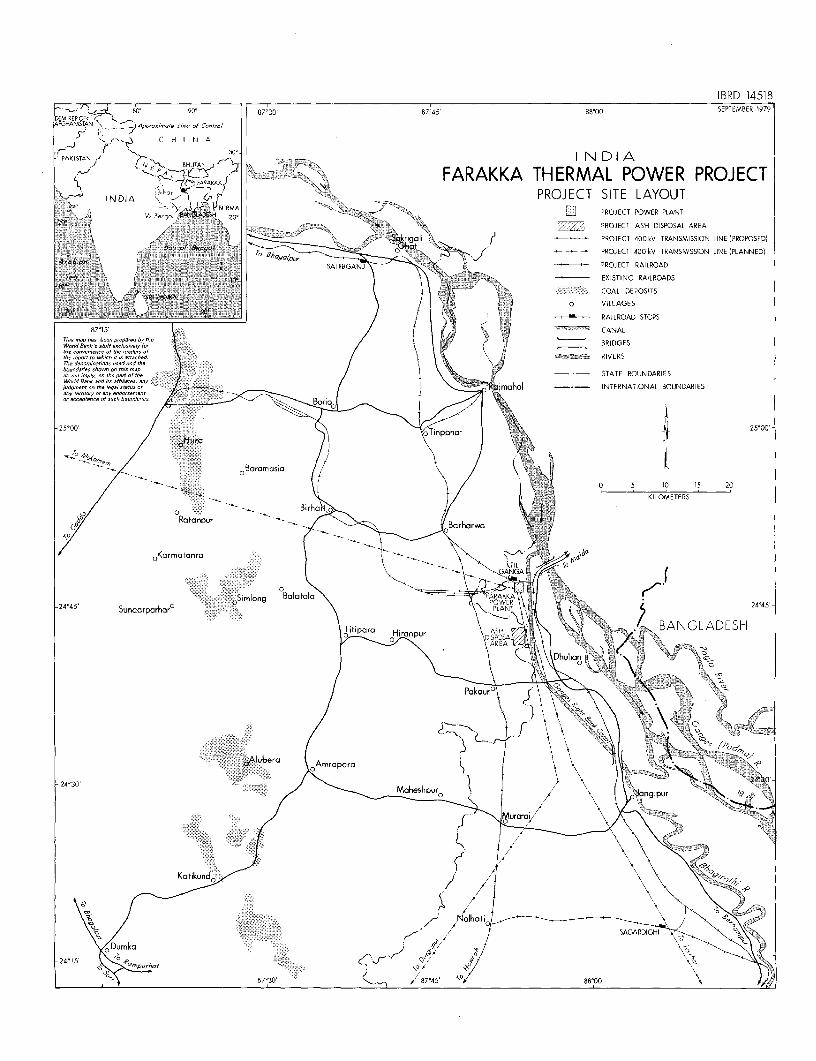

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENT

Currency Unit - Rupee (Rs)Rs 1 - Paise 100US$1 - Rs 8.4Rs 1 US$0.1190Rs I million = US$116,047.62

(Since September 24, 1975, the Rupee has been officiallyvalued relative to a "basket" of currencies. As thesecurrencies are now floating, the U.S. Dollar/Rupee ex-change rate is subject to change. As of May 30, 1980,the exchange rate was Rs 7.9 to US$1.0).

FISCAL YEAR

April 1 - March 31

ABBREVIATIONS AND ACRONYMS USED IN THIS REPORT

ARDC - Agriculture Refinance and Development Corporation LimitedGOI - Government of IndiaCEA - Central Electricity AuthorityDVC - Damodar Valley CorporationNHPC - National Hydro Power Corporation, LimitedNTPC - National Thermal Power Corporation, LimitedREB - Regional Electricity BoardREC - Rural Electrification Corporation, LimitedSEB - State Electricity BoardUNDP - United Nations Development Program

kV - kilovolt - 1,000 voltskWh - kilowatt-hour - 1,000 watt-hoursMW - megawatt = 1,000 kilowattsGWh - gigawatt-hour - 1,000,000 kilowatt-hours

FOR OFFICIAL USE ONLY

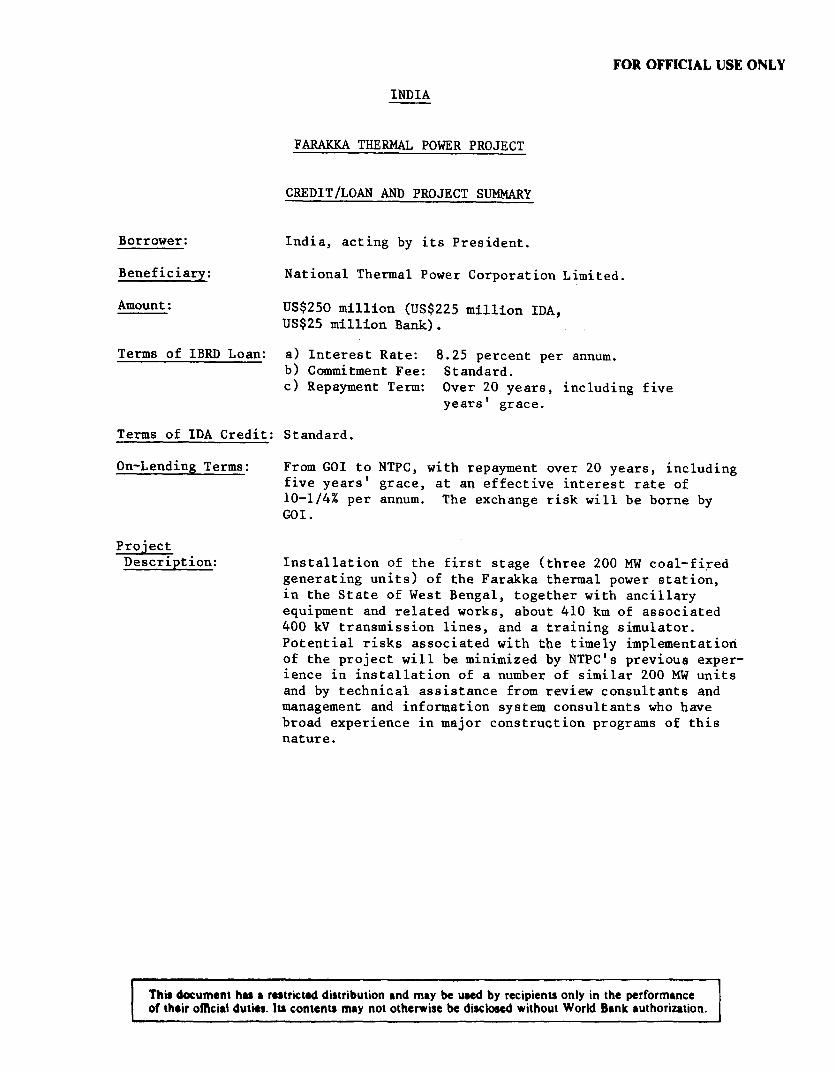

INDIA

FARAKKA THERMAL POWER PROJECT

CREDIT/LOAN AND PROJECT SUMMARY

Borrower: India, acting by its President.

Beneficiary: National Thermal Power Corporation Limited.

Amount: US$250 million (US$225 million IDA,

US$25 million Bank).

Terms of IBRD Loan: a) Interest Rate: 8.25 percent per annum.b) Commitment Fee: Standard.c) Repayment Term: Over 20 years, including five

years' grace.

Terms of IDA Credit: Standard.

On-Lending Terms: From GOI to NTPC, with repayment over 20 years, includingfive years' grace, at an effective interest rate of10-1/4% per annum. The exchange risk will be borne by

GOI.

ProjectDescription: Installation of the first stage (three 200 MW coal-fired

generating units) of the Farakka thermal power station,in the State of West Bengal, together with ancillaryequipment and related works, about 410 km of associated400 kV transmission lines, and a training simulator.Potential risks associated with the timely implementationof the project will be minimized by NTPC's previous exper-

ience in installation of a number of similar 200 MW units

and by technical assistance from review consultants andmanagement and information system consultants who have

broad experience in major construction programs of this

nature.

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- 1.1 -

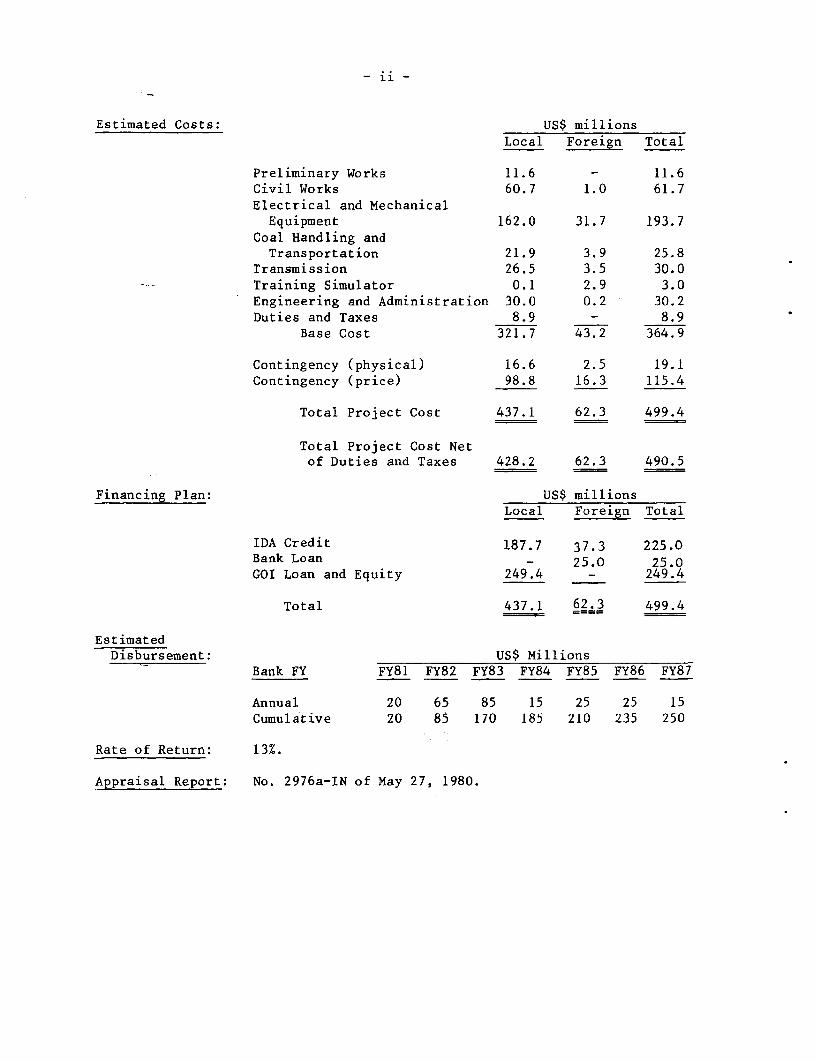

Estimated Costs: US$ millions

Local Foreign Total

Preliminary Works 11.6 - 11.6Civil Works 60.7 1.0 61.7Electrical and MechanicalEquipment 162.0 31.7 193.7

Coal Handling andTransportation 21.9 3.9 25.8

Transmission 26.5 3.5 30.0Training Simulator 0.1 2.9 3.0Engineering and Administration 30.0 0.2 30.2Duties and Taxes 8.9 - 8.9

Base Cost 321.7 43.2 364.9

Contingency (physical) 16.6 2.5 19.1Contingency (price) 98.8 16.3 115.4

Total Project Cost 437.1 62.3 499.4

Total Project Cost Netof Duties and Taxes 428.2 62.3 490.5

Financing Plan: US$ millionsLocal Foreign Total

IDA Credit 187.7 37.3 225.0Bank Loan - 25.0 25.0GOI Loan and Equity 249.4 - 249.4

Total 437.1 62.3 499.4

EstimatedDisbursement: US$ Millions

Bank FY FY81 FY82 FY83 FY84 FY85 FY86 FY87

Annual 20 65 85 15 25 25 15Cumulative 20 85 170 185 210 235 250

Rate of Return: 13%.

Appraisal Report: No. 2976a-IN of May 27, 1980.

INTERNATIONAL DEVELOPMENT ASSOCIATION

REPORT AND RECOMMENDATION OF THE PRESIDENTTO THE EXECUTIVE DIRECTORS ON A PROPOSED CREDIT

AND LOAN TO INDIA FOR THEFARAKKA THERMAL POWER PROJECT

1. I submit the following report and recommendation on a proposeddevelopment credit to India in an amount equivalent to US$225 million onstandard IDA terms, and a proposed loan to India in an amount equivalent toUS$25 million, to help finance a project for the construction of the firstphase of a proposed Farakka thermal power station. Amortization of the loanwould be over 20 years, including five years' grace, at the standard Bankinterest rate. The proceeds of the credit and loan would be onlent by theGovernment to the National Thermal Power Corporation Limited, for 20 years,including five years' grace, at an interest rate of 10-1/4% per annum.

PART I - THE ECONOMY 1/

2. An economic report, "Economic Situation and Prospects of India"(2933-IN, dated May 1, 1980), was distributed to the Executive Directorson May 12, 1980. Country data sheets are attached as Annex I.

Background

3. India is a large and diverse country with a population of 663 mil-lion (in mid-1980) and an annual per capita income of US$180. Agriculturecontinues to dominate India's economy, employing over two-thirds of thelabor force. However, the land base is not sufficient to provide an adequatelivelihood to all those engaged in agricultural activities, especially thelandless or nearly landless who have only an insecure grasp on the means ofexistence. The share of agriculture in GDP at factor cost (measured in 1970/71prices) has declined from 59.6% in 1950/51 to 40.7% in 1978/79. The shareof industry has increased over the same period from 14.5% to 22.7%. Butindustrialization has not been rapid enough to absorb the growing labor force,nor to bring about the substantial economic transformation that has led tohigher productivity and rapid urbanization in some other developing countries.The urban population was 18% of the total in 1960, and is 21% now.

4. Economic growth has been slow in the past. The trend growth rate ofGDP was 3.7% per annum from 1950/51 to 1978/79. Slow growth in agriculture --2.5% per annum over the same period -- has constrained overall growth, not onlybecause of the high share of agriculture in GDP but also because scarce foreignexchange has often been required to import food. Industrial valued-added hasgrown more rapidly, at 5.4% per annum between 1950/51 and 1978/79, but thisgrowth has not been as high as in many other countries, nor as high as requiredif the overall growth of the economy is to be accelerated. Slow growth has

1/ Parts I and II of this report are the same as Parts I and II of thePresident's Report for the Rajasthan Water Supply Project (Report No.P-2831-IN), dated June 2, 1980.

- 2 -

persisted despite a quite creditable domestic saving and investment performance.

Gross domestic saving more than doubled from 10% of GDP in 1950/51 to 24% in

1978/79. Similarly, gross domestic investment as a fraction of GDP rose from

10% in 1950/51 to just over 24% in 1978/79. Foreign savings have never financed

a large portion of domestic investment: a peak of about 20% was reached during

the early 1960s; by the end of the 1970s, the proportion had returned to much

lower levels. External assistance has been low both as a percentage of GDP and

in per capita terms. Net external assistance has never risen above 3% of GDP.

5. Except during periods of balance of payments crisis, exports have

received relatively little emphasis in India, which has primarily pursued a

strategy of import subsitution. As a result, India's share of world trade

has fallen consistently since 1950/51. The volume growth of exports between

1950/51 and 1978/79 averaged only 3.0 per annum. The volume of growth of

imports over the same period has slightly exceeded that of exports. During

the early 1970s, India's terms of trade, which had remained roughly constant

during the 1960s, deteriorated drastically, spurring a relatively rapid period

of export growth through the mid-1970s. For the five years ending in 1976/77

the volume of India's exports grew on average over 10% per annum, demonstrating

that sustained rapid growth was possible. While expanding world markets, par-

ticularly in the near-by Middle East, contributed to this process, adjustmentsin trade policies designed to improve the profitability of exports played a

major role.

Recent Trends

6. Over the period 1975/76 to 1978/79, growth in real GDP (at factor

cost), agricultural value-added and industrial value-added averaged 4.7%,

2.8% and 7.3% per annum, respectively. These trends represent a marginally

better growth performance than the long-term trends from 1950/51 to 1975/76.

However, GNP is expected to have declined by about 3% in 1979/80 as a result

of the drought-induced decrease in agricultural production and input con-

straints in other sectors, bringing recent trends back in line with the long-

term picture. Industrial production stagnated in 1979/80, largely due to

shortfalls in the production of major inputs such as coal, steel and cement,

as well as constraints in the provision of infrastructure, notably power and

transportation. As a consequence of these developments, the remarkable price

stability that characterized the Indian economy after 1975 came to an abrupt

end at the close of fiscal year 1978/79. During the Spring and Summer of

1979 the price index rose sharply, so that by September it stood at 18.4%

above that of the previous September. Foodgrain prices rose over the Summer

and Fall of 1979 but in most markets still prevailed close to the Government's

ration prices. Low income groups in urban areas were assured adequate sup-

plies of grain at stable prices through the public distribution system. The

substantial stocks of foodgrains also provided resources for a large-scale

drought relief employment program for low income groups in rural areas.

7. In agriculture the positive results of large investments and appro-

priate policies over the past few years are becoming increasingly evident and

have withstood the test of a severe drought. Agricultural production, which

had increased by 14.5% in 1977/78 and 3.4% in 1978/79 to record levels each

year, fell about 8-9% in 1979/80. Foodgrain production is estimated to have

- 3 -

declined from 131.4 million tons in 1978/79 to 118-120 million tons in 1979/80.

Considering that 1979/80 was a year of acute drought, coming after two succes-

sive years of record output, the foodgrain production achieved - still the

fourth highest in Indian history - provides a measure of the contribution that

expanded irrigation, extension and other inputs have made to Indian agriculture.

Furthermore, the capacity of India's irrigation potential to counteract drought

conditions was not adequately tested because of the diesel shortages which

inhibited the utilization of groundwater resources. Rapid growth in the use

* of basic inputs for agricultural production has continued. Additions to the

area under irrigation have almost doubled from 1.3 million hectares during the

five-year period ending in 1973/74 to about 2.5 million additional hectares a

year during the most recent three-year period. Fertilizer consumption in

1979/80 exceeded five million nutrient tons, a level almost 80% higher than

in 1975/76.

8. As the new decade begins, the Indian economy is shifting from a

situation of resource surplus, which had been a temporary phenomenon of the

late 1970s, to one of resource scarcity. Investment has again overtaken

domestic savings, and the scope for further increases in the latter appears

limited. Marginal savings rates have recently been well above 30% in the

household sector. Future increases in savings will depend largely on enhanced

profitability of public sector enterprises. Impeding resource scarcity is

even more apparent in the foreign sector. Between 1975/76 and 1978/79 India's

current account deficit had remained comfortably small in relation both to GDP

and to a growing pipeline of aid commitments. This was primarily due to

favorable terms of trade movements and rapidly growing net invisibles which

masked adverse underlying trends in the volume of exports, which has barely

grown since 1976/77. Particularly serious is the evident decline in the

quantum of manufactured non-traditional exports which had contributed much to

the export growth of the first half of the decade. A combination of strong

domestic, and slack international demand, exacerbated until recently by

apparent lessened interest in export promotion, have been the major casual

factors.

9. In constrast, imports have grown rapidly in volume terms and there

have been important changes in composition. As a result of the accumulation

and maintenance of foodgrain stocks, foodgrain imports - which had been a

traditional item in the balance of payments - have declined to insignificant

levels since 1977/78. Reflecting the impact of the liberalized import policy

adopted by the Government, non-foodgrain imports increased sharply, so that

their level in 1978/79 was over 80% higher than in 1975/76. In large part,

the liberalization in import policy and increase in imports were limited to

raw materials, basic commodities and intermediate goods; consumer goods

remained banned and capital goods imports were permitted only on a selective

basis. Strong new pressures on the balance of payments have developed during

1979/80. The terms of trade again deteriorated markedly as a consequence of

unexpectedly large increases in petroleum prices, which caused the oil import

bill to double in 1979/80, accounting for more than 80% of the total estimated

US$2.5 billion increase in imports, and bringing India's total import bill to

about US$11 billion. Petroleum imports as a proportion of exports now exceed

50%.

-4-

Development Prospects

10. The experience of recent years illustrates that India does have thecapacity to grow and develop at a more rapid pace. Although the industrialsector is small compared to the size of the economy, it nevertheless has ahighly diversified structure and is capable of manufacturing a wide varietyof consumer and capital goods. Basic infrastructure--irrigation, railways,telecommunications, roads and ports--is extensive compared to many countries,although there is considerable scope for expansion as well as improvement inthe utilization of existing capacity. India is also well-endowed with humanresources and with institutional infrastructure for development. Finally,India has an extensive natural resource base in terms of land, water, andminerals (primarily coal and ferrous ores, but also gas and oil). With goodeconomic policies and sufficient access to foreign savings, India has thecapability for managing these considerable resources to accelerate its long-term growth.

11. The new Indian Government installed in January 1980 is in the processof formulating its policies and programs. A new Plan for the period 1981-86 isbeing prepared to replace the Draft Five-Year Plan for 1978-83. At this stageit is not possible to comment on the new development strategy; however, it isunlikely that the priorities accorded to agriculture and power will be lessened.Furthermore, developments in India as well as in the world economy during1979/80 have brought to the surface urgent issues which will need the attentionof policy-makers, irrespective of the broader context of development strategythat the new Government may adopt. Among these issues are the following:(a) the bottlenecks in infrastructure and related constraints in productionof several basic industrial inputs; (b) the new policy options emerging inagriculture; (c) the need to substitute less costly energy sources for importedpetroleum; and (d) the anticipated deterioration of the balance of payments inthe near future.

12. The higher capital formation rates of the past few years augur wellfor future income growth. However, there are signs that, relative to existingdemands, the past investment program has led to disproportionally low growthin certain crucial sectors, namely power, coal, transport services, steel andcement. Potential output growth in sectors which have benefitted from largeinvestments in the recent past may not materialize unless these input bottle-necks are alleviated. In the case of coal, steel and cement, domestic produc-tion appears to be clearly justified on grounds of comparative advantage, andthe aim of policy is self-sufficiency. All these are tradeable commodities.Although in 1979/80 they were not imported in sufficient amounts to eliminatethe shortages, increased short-term reliance on imports may be necessary toalleviate slowdowns and dislocation in using industries. In the case ofsectors in which there is no option to import--power and transportation--the planning of capacity expansion becomes even more crucial. Although thereis scope for improvement in the shortrun performance of these sectors, majorinvestments in balancing and modernization programs as well as new capacityare needed in order to provide adequate and stable growth in the medium term.The presence of infrastructural constraints and shortages of basic industrialinputs demonstrates that the expansion of industrial outout leads to competingclaims on scarce resources which must be efficiently allocated among differentindustries.

- 5 -

13. The substantial increase in the world price of petroleum in 1979,together with the expectation that this pattern will not be reversed in thenear future, raises several issues concerning energy prospects for India.India imports the equivalent of about 50% of its petroleum consumption. Inorder to implement its policy of minimizing dependence on foreign oil, theGovernment intends to rapidly expand its oil exploration program, to increasethe utilization of its vast coal reserves and to increase the development ofIndia's considerable hydroelectric potential. However, recent shortages ofcoal and power are symptomatic of operational problems reflecting, in part,past planning and investment decisions which are inhibiting the timely imple-mentation of India's long-term conversion program. The interdependencies inthe economy currently make petroleum demand a residual which is contingenton the operation of many other sectors and which has significant implicationsfor the balance of payments.

14. In agriculture, despite the 1979 drought, economic policies, devel-opment programs and secular trends all seem favorable for sustaining a periodof high growth during the 1980s. India should end the 1979/80 rabi seasonwith grain stocks of about 15 million tons, without having imported foodgrainsduring the year. This is partly due to the bumper crop of 1978/79, but alsoreflects the trends of the last decade which point to a consistent improvementin foodgrain availability in the economy. In view of the acceleration in theuse of agricultural inputs and the projected fall in the population growth rate,the long-run prospects for foodgrain supply and demand balances look favorable.Persistent shortage seems unlikely, and it is probable that a wide range ofpolicy options will become much more practical as the overriding emphasis onfoodgrains can be somewhat relaxed. These options include a slowly fallingreal price of foodgrains to increase the affordability of foodgrains to low-income families, further rationalization of domestic markets and prices, anddiversification to the production of other higher value crops. This prospectwill involve only a gradual shift in emphasis rather than a dramatic breakwith past policies.

15. Foreign exchange reserves still provide some cushion that can helpthe Government of India in short-term supply management, but this situationis likely to be short-lived. Rising import prices and uncertainties in theprospects for exports and invisible receipts have led to a serious and rapiddeterioration in India's balance of payments prospects. Reserves were onlymarginally higher in March 1980 than the level of a year earlier and, in termsof import coverage, fell below the 8-month level for the first time since 1977.A sharp decline in the reserve level is expected in 1980/81. At best, India'sreserves may provide a cushion for two more years, and even that is conditionalon the maintenance of aid flows and workers' remittances and on moderation inoil price rises.

16. India's medium-term development prospects are mixed. Progress hasbeen made and continues to be made, particularly in agriculture, but theeconomy faces a period of difficult adjustments in the coming years. Invest-ments required to relieve short-term supply constraints must compete withlonger-term programs to accelerate growth and to develop India's considerable

physical and human resources. The balancing of these objectives will place adifficult burden on the framers of India's next Five-Year Plan. The primaryfocus must be on the implementation of appropriate domestic adjustment policies,although the aid community can and should play an important role in ensuringthat India's efforts do not fail due to inadequate foreign resources.

17. The annual population growth rate declined from 2.2% in the late1960s to below 2% at present and is expected to continue falling to around1.6% by the latter half of the 1980s. Despite the declining trend in the rateof population increase, a net reproduction rate of one (replacement level)will only be achieved around the year 2020. At that time, the population ofIndia is estimated to reach 1.2 billion persons, an increase of about 81% overthe mid 1980 level of 663 million. Family planning has played an importantrole in achieving the fertility decline in the past decade, and the extent ofa further decline will be greatly influenced by the continuation of a success-ful official family planning program. The family planning performance datafor 1978/79 and the first ten months of 1979/80 clearly indicate a come backfrom the sharp decline observed in virtually all major contraceptive methodsduring 1977/78. Except for male sterilizations, the number of acceptors forall contraceptive methods surpassed the 1974/75 levels in 1978/79. While theincrease in the total acceptors of IUD and conventional contraceptives wasmodest, female sterilizations increased by about 40% between 1977/78 and1978/79. Data for the first ten months of 1979/80 confirm a secular upwardtrend in overall performance. So far, policy makers have not made majorattempts to accelerate the male sterilization program. Instead, they haveopted for policies that would yield relatively modest but sustainable resultswith increased emphasis on non-terminal methods.

18. Beyond the effects of overall economic growth and constrained popula-tion growth, the reduction of poverty in India requires special attention toways of raising the income and productivity of low-income groups. More thanone-third of the world's poor live in India, and more than 80% of the Indianpoor belong to the rural households of landless laborers and small farmers.In addition to marginal holdings of physical assets, the poor are ill-endowedwith human resources, being disproportionately represented among the illiterate,the malnourished and those having otherwise poor health status. Improvementsin the living standards of the poor will depend to a large extent on the over-all growth of the economy, mainly on productivity increases in agricultureand non-farm rural employment, but also on the expansion of employment oppor-tunities in urban areas. These developments will have to stem largely frommarket forces which, however, can be greatly facilitated by appropriate gov-ernment policies and investment priorities. There is also a role for directgovernment actions in faster implementation of land reform (though the scopefor significant reduction in poverty through redistribution is quite limitedin India), in increasing the supply of credit available to small farmers andrural artisans and finally in broadening the provision of those serviceswhich enhance the human capital of the poor and improve living standards.Many of the latter are elements of the Minimum Needs Program which has beenan integral part of Indian planning for the past decade. Progress has beenslow but steady in the expansion of primary education, the extension of rural

- 7 -

health facilities and the provision of secure village water supplies. Recent

innovations, including the community health volunteer program and the national

adult literacy campaign, are encouraging evidence that well-targetted, rela-

tively low-cost programs can lead to enhanced prospects for India's poor.

PART II - BANK GROUP OPERATIONS IN INDIA

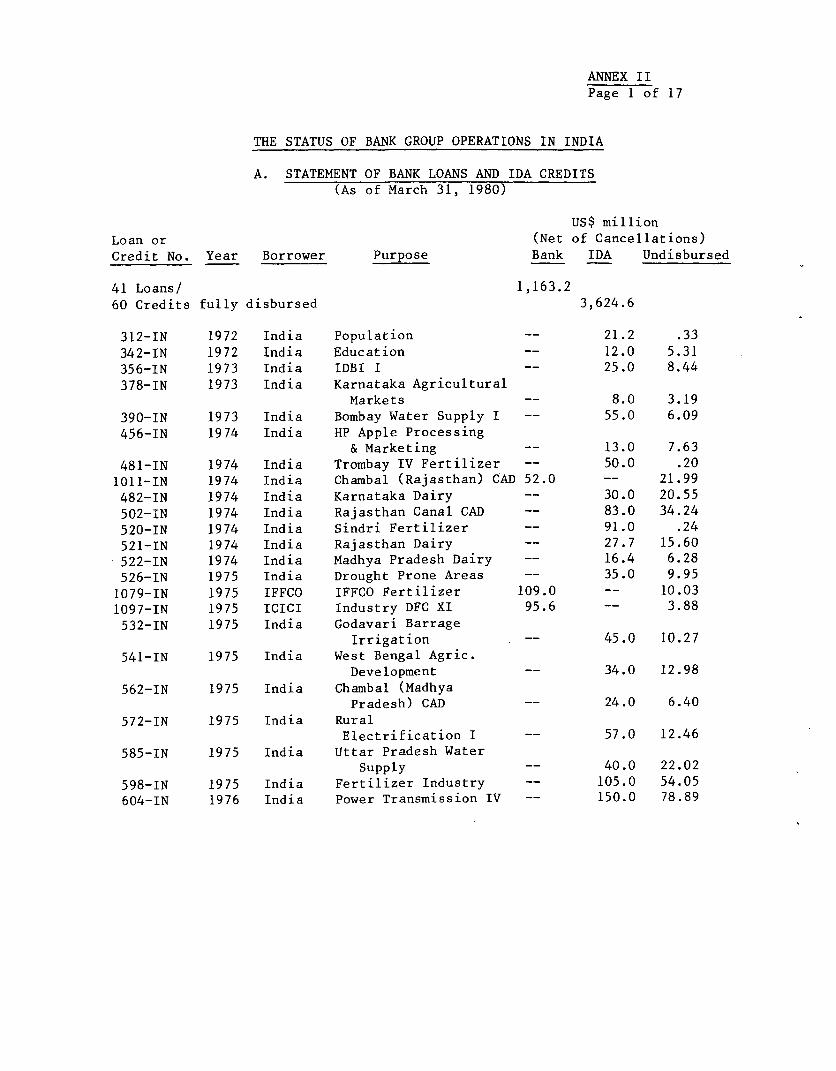

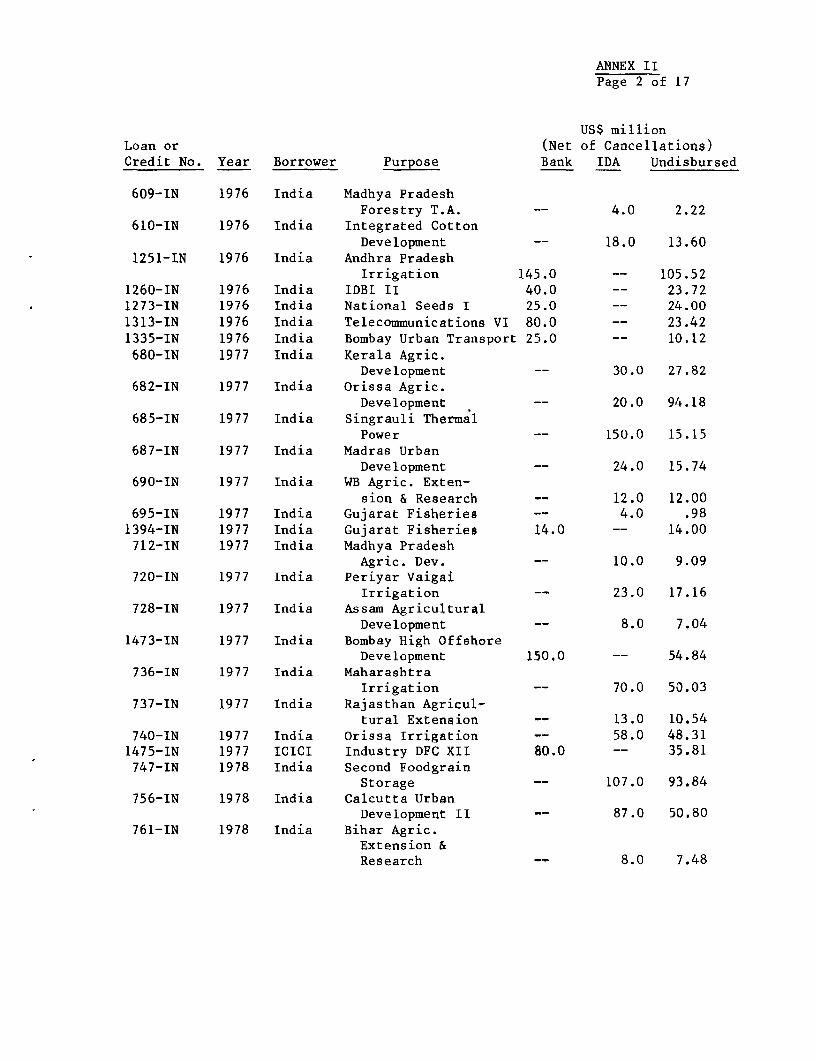

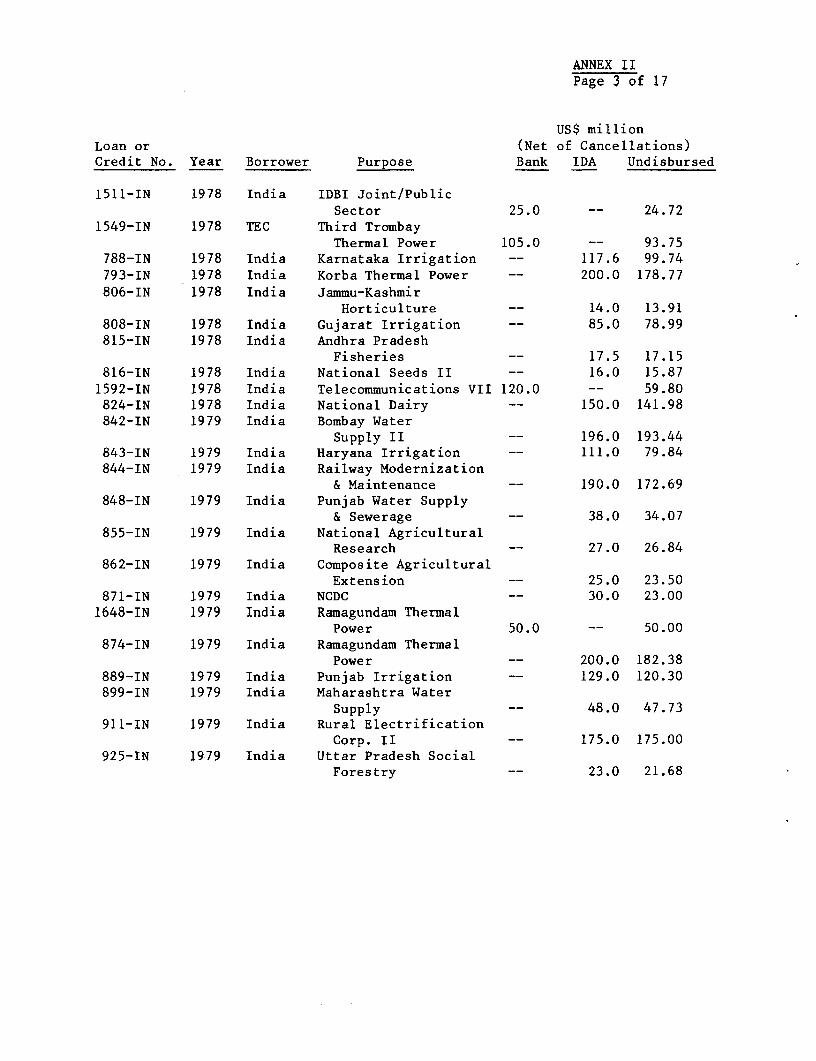

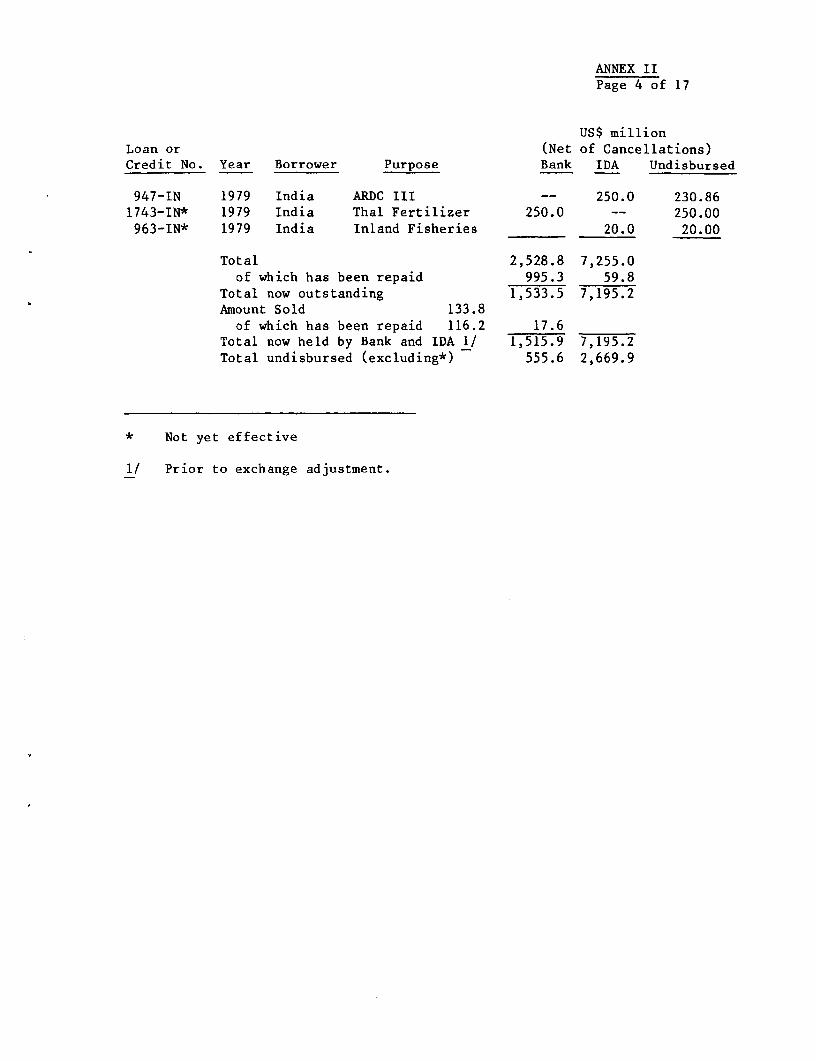

19. Since 1949, the Bank Group has made 57 loans and 118 development

credits to India totalling US$2,529 million and US$7,255 million (both net

of cancellation), respectively. Of these amounts, US$1,055 million had

been repaid, and US$3,226 million was still undisbursed as of March 31, 1980.

Bank Group disbursements to India in the current fiscal year through March 31,

1980, totalled US$517 million, representing an increase of about 44% over the

same period last year. Annex II contains a summary statement of disbursements

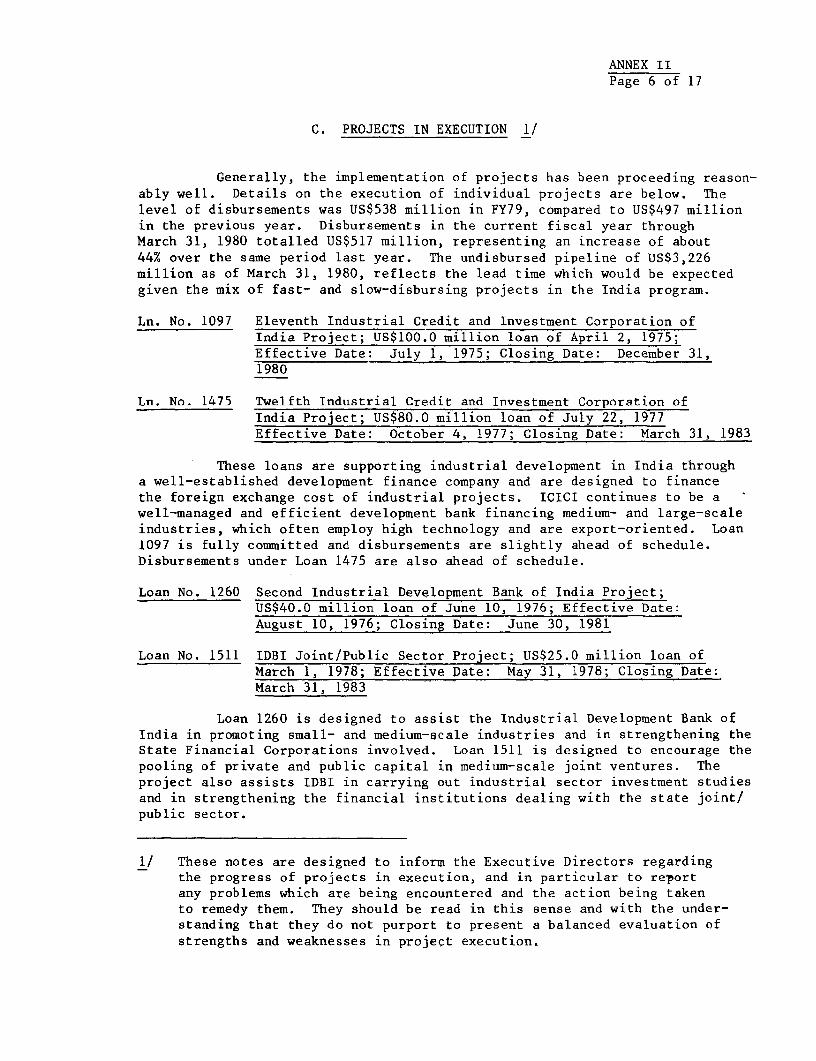

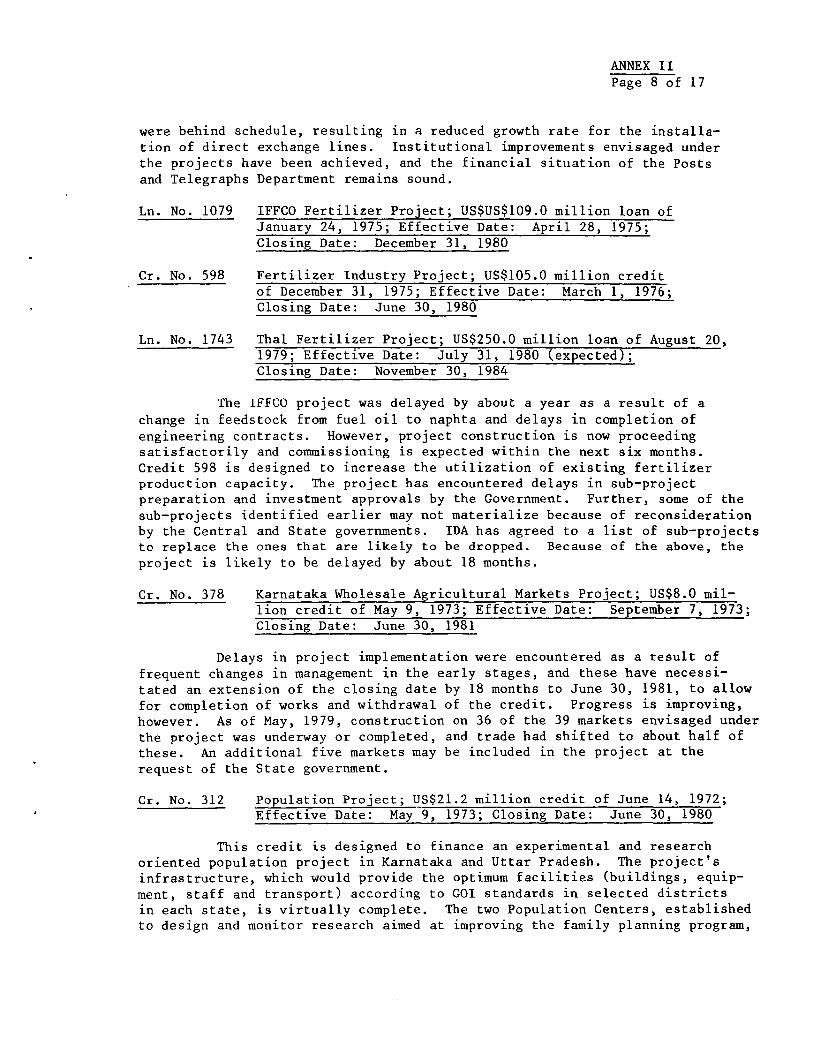

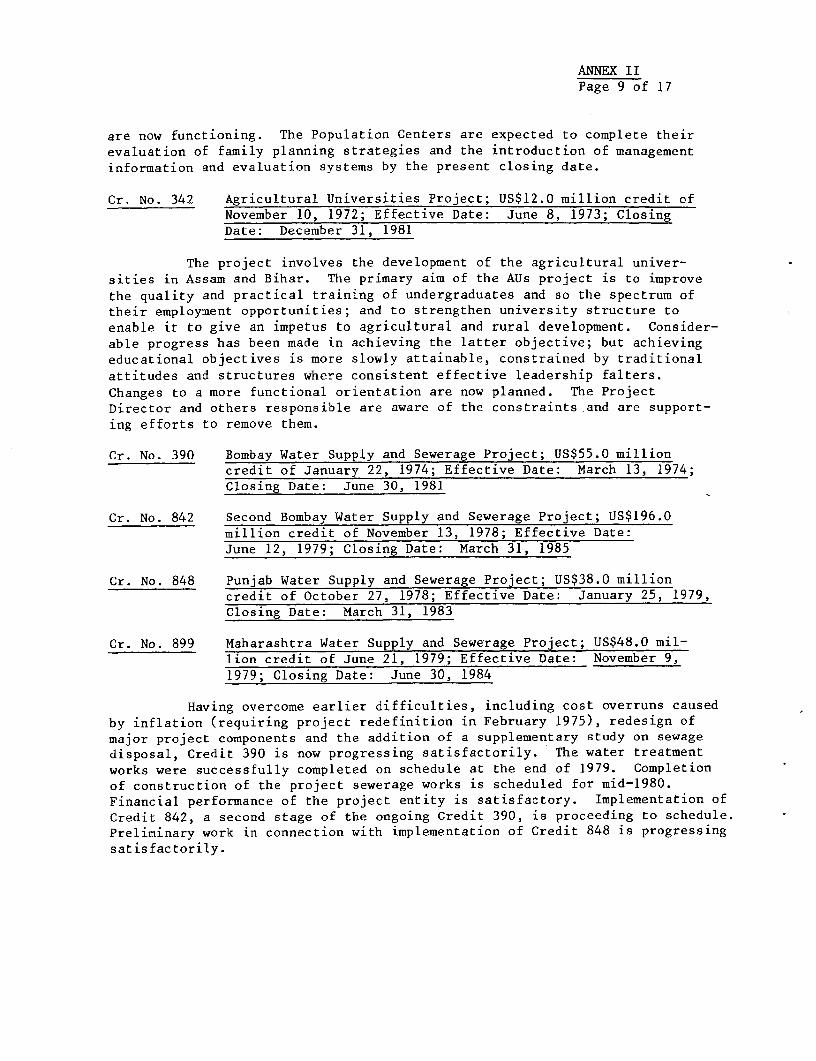

as of March 31, 1980, and notes on the execution of ongoing projects.

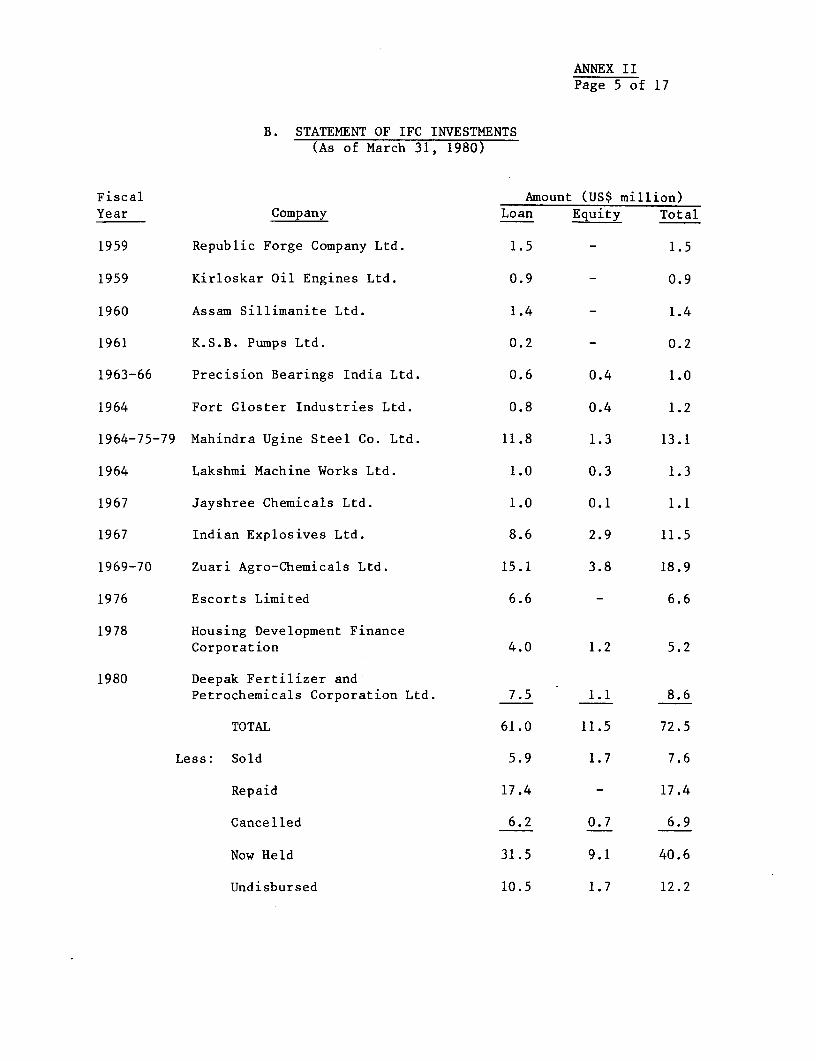

20. Since 1959, IFC has made 18 commitments in India totalling US$72.5

million, of which US$17.4 million has been repaid, US$7.6 million sold and

US$6.9 million cancelled. Of the balance of US$40.6 million, US$31.5 mil-

lion represents loans and US$9.1 million equity. A summary statement of

IFC operations as of March 31, 1980, is also included in Annex II (page 5).

21. In recent years, the emphasis of Bank Group lending has been on

agriculture. The Bank Group has been particularly active in supporting minor

irrigation and other on-farm investments through agricultural credit operations

and in providing direct support to major and medium irrigation. Marketing,

seed development, agricultural extension, and dairying are other agricultural

activities supported by the Bank Group. Also, the Bank Group has been active

in financing the expansion of output in the fertilizer sector and, through its

sizeable assistance to development finance institutions, in a wide range of

geographically scattered medium- and small-scale industrial enterprises. IDA

financing of industrial raw materials and components for selected priority

sectors has been instrumental in facilitating better capacity utilization in

industry. The Bank Group has also been active in supporting infrastructure

development for power, telecommunications, and railways. Family planning,

water supply development, and urban investments have also received Bank

Group support in recent years.

22. The direction of assistance under the Bank/IDA program has been

consistent with India's needs and the Government's priorities. The emphasis

of the program on agriculture, power, water supply and other infrastructure

sectors remains highly relevant. Projects designed to foster agricultural

production through the provision of essential inputs, particularly water and

credit for on-farm investments, will continue to receive emphasis. Improved

water management and intensification and streamlining of extension systems

form an important institution-building aspect of the Bank Group's program for

the next several years. Special emphasis will be given to projects benefit-

ting small farmers. The Bank Group's continuing role in the fertilizer sector

also assists India in the more efficient provision of another key input in

the agricultural growth process. Projects supporting water supply, sewerage,

- 8 -

and urban development also form an integral part of the Bank's lending

strategy to India for the next several years. Lending in support of infra-

structure and industrial investments will focus on those subsectors which

have recently emerged as key constraints on India's overall growth, primarily

power and transportation.

23. The need for a substantial net transfer of external resources in

support of the development of India's economy has been a recurrent theme of

Bank economic reports and of the discussions within the India Consortium.

Thanks in part to the response of the aid community, India successfully

adjusted to the changed world price situation of the mid 1970s. However,

the need for increased foreign assistance to adjust to an even greater deter-

ioration in balance of payments prospects during the 1980s by augmenting

domestic resources and stimulating investment, remains. As in the past, Bank

Group assistance for projects in India should include, as appropriate, the

financing of local expenditures. India imports relatively few capital goods

because of the capacity and competitiveness of the domestic capital goods

industry. Consequently, the foreign exchange component tends to be small in

most projects. This is particularly the case in such high-priority sectors

as agriculture, irrigation, and water supply.

24. India's poverty and needs are such that as much as possible ofIndia's external capital requirements should be provided on concessionary

terms. Accordingly, the bulk of the Bank Group assistance to India has been,

and should continue to be, provided from IDA. However, the amount of IDAfunds that can reasonably be allocated to India remains small in relation

to India's needs for external support, and India should be regarded as credit-

worthy for some supplemental Bank lending. The ratio of India's debt service

to the level of exports was 12% in 1978/79 and is projected to remain below

20% through 1995/96. As of March 31, 1980, outstanding loans to India held

by the Bank totaled US$1,516 million, of which US$556 million remained to be

disbursed, leaving a net amount outstanding of US$960 million.

25. Of the external assistance received by India, the proportion con-

tributed by the Bank Group has grown significantly. In 1969/70, the Bank

Group accounted for 34% of total commitments, 13% of gross disbursements,

and 12% of net disbursements as compared with an estimated 62%, 27% and 38%,

respectively, in 1978/79. On March 31, 1979, India's outstanding and dis-

bursed external public debt was US$15.3 billion, of which the Bank Group's

share was US$4.6 billion or 30% (IDA's US$4.0 billion and IBRD's US$0.6 bil-

lion). Because Bank Group assistance to India is predominantly in the form

of IDA credits, debt service to the Bank Group will rise slowly. In 1978/79,

about 17.5% of India's total debt service payments were to the Bank Group.

PART III - THE POWER SECTOR

Background

26. The performance of the Indian power supply industry and the economy

as a whole are closely linked, and economic growth and improvement of the

- 9 -

standard of living depend critically on the development of the power sector.

Since alternative sources of energy are not readily available in the amounts

needed, shortage of power has an immediate impact on activities of the economy.

In recent years, energy matters have been receiving top priority consideration

in policy planning of Central and State Governments, on a par with food pro-

duction and distribution. Resources allocated to the power sector have signi-

ficantly increased during this period. 1/ While per capita consumption of

electricity has been rising in India, it remains among the lowest in the world

at about 130 kWh per annum. Although investment in the development of the

power sector has been emphasized, demand for power has been outstripping sup-

ply. The direct loss of value added due to power shortages is estimated at

about 3% of GDP.

Development of the Power Sector

27. In the past, investments in power generation, transmission and dis-

tribution were made largely by the States and, while transfer of power between

States took place as the power system expanded and demand grew, there was

limited attempt at the development of power on a broad Regional or national

basis. Promising hydro power sites were identified throughout India, but

budget constraints, water rights problems between States, and other consider-

ations prevented any large-scale development, leaving hydro power potential

largely untapped except for relatively few developments.

28. Overall Power Supply and Demand of Power. In the 1950s and 1960s,

installed capacity and power generation managed to keep pace with the nation's

demand for power, both growing at an average annual rate of about 12%. Since

1970, the situation has deteriorated. Delays in commissioning new power proj-

ects, operation and maintenance problems and insufficient investment under

severe budget constraints have led to a critical situation in which demand for

power outstrips supply. This was exacerbated by monsoons and an unstable coal

supply caused by disruptions in coal mining and transport. Between 1970/71 and

1974/ 75, growth in power generation averaged only 5% annually. In the follow-

ing years, 1975/76 and 1976/77, the situation improved as the result of two

successive good monsoons, improved coal supply, and a concerted effort to

improve project implementation, thermal capacity utilization and overall power

system management. Capacity grew by 10% in 1975/76 and 8% in 1976/77, while

generation increased by 13% and 11.5%, respectively, reflecting improved

capacity utilization. In 1977/78, however, generation increased by less than

4% in spite of a 9% increase in capacity, due mainly to longer outage periods

than normal and longer periods required for commissioning new plants than

expected. The higher growth trend resumed in 1978/79, with an increase of

about 12% in installed capacity and 7% in power generation. Even so, power

shortages persisted in many parts of the country, particularly in the Eastern

Region, and India's economic activity, particularly in the industrial sector,

was adversely affected. Total installed generating capacity as of March 1979

was about 29,000 MW, including non-utility plant. Of this total generating

capacity, about 60% was conventional thermal, 38% hydro and the balance nuclear.

1/ From 16% of public sector outlays during the Fourth Plan to 19% in the

Fifth Plan and an estimated 23% earmarked in the draft Sixth Plan.

- 10 -

Although additional new generation capacity of about 10% (3,000 MW) is expected

to have been commissioned in 1979/80, power shortages will continue to prevail.

Industry consumes about 66% of all electricity sold, while agriculture (mainly

irrigation) accounts for another 14-15%. As a result of accelerated agricul-

tural development programs, there has been a marked growth of power consumption

in the rural areas where more than 80% of India's population live. The number

of electrified villages, for example, grew from just over 3,000 in 1950/51 to

some 230,000, or over one-third of all the villages in India, by March 1979.

During the five-year period 1979/80-1983/84, new generating capacity is ex-

pected to grow at an annual rate of about 11% to total some 18,900 MW, of

which about 13,000 would be thermal and 4,700 MW hydro and 900 MW nuclear.

The construction of some 15,000 km of 400 kV transmission is planned to dis-

tribute the power output through the integrated Regional systems.

29. Power Supply and Demand in the Eastern Region. In the Eastern

Region, installed capacity as of March 1979 was 4,700 MW, consisting of

3,800 MW thermal and 900 MW hydro. During 1979/80-1983/84 new capacity of

about 3,000 MW is expected to be commissioned, which would bring the installed

capacity to about 7,700 MW. In 1980/81, the Eastern Region is likely to have

a capacity deficit of some 8%, and the anticipated shortfall is still likely

to be 8% (or about 400 MW) in 1983/84. Power shortages will, therefore,

continue to persist until well beyond 1984.

30. Recent Development. With the rapid growth of the power sector

accompanied by the increasing complexity of its operation, the need to under-

take an integrated national approach to sectoral development is recognizel by

GOI. Some encouraging developments have been initiated. For example, the

unified operation of power systems on a Regional basis has commenced. The

Southern Regional grid has been in operation since 1972 with interconnected

220 kV transmission, and progressive integration of power systems in other

Regions is intended to pave the way for a national grid. GOI undertook under

the Fourth Power Transmission project (Credit 604-IN) to carry out, with

assistance of consultants, a 400 kV system study designed to establish primary

grid configurations to be adopted in developing the national power grid. The

400 kV system study was commenced by CEA and the first phase of the study has

been completed. The study provides essential inputs for formulating sound

policies for future development of the sector; GOI intends to continue it as

part of ongoing long-term national power planning. The operation of Regional

systems, which will be ultimately integrated into a national grid, requires

large numbers of technical personnel trained to use sophisticated load dispatch

equipment to control interconnected systems operation. A UNDP project designed

to assist CEA in developing programs for staff training for operation of the

future load dispatch centers is expected to be implemented shortly upon sub-

mission of a project proposal by GOI.

Sector Institutions

31. The institutional structure of the Indian power sector is complex.

One of the main reasons is that electricity supply is a concurrent subject,

within the jurisdiction of both the Central Government and the State Govern-

ments under the Indian Constitution and the Electricity (Supply) Act, 1948.

- 11 -

This means that the responsibility for supplying power is shared between the

Central Government and the State Governments, and full agreement between the

Center and the States is required for the implementation of most actions.

With the rapid expansion of the power sector, there has been the increasing

need to coordinate the activities in the power industry beyond State bound-

aries, and various agencies have been established with a view to promoting

integrated power development in the country. The principal agencies in the

sector are: (i) the State Electricity Boards (SEBs); (ii) Regional Electricity

Boards (REBs); (iii) the Central Electricity Authority (CEA); (iv) the two

Central power corporations--the National Thermal Power Corporation (NTPC) and

the National Hydro Power Corporation (NHPC); and (v) the Rural Electrification

Corporation (REC).

32. State and Regional Electricity Boards. The SEBs were established

by the State Governments under the Electricity (Supply) Act, 1948. Their major

task at the time of establishment was to bring together the small individual,

often independent privately owned power plants and facilities within their

respective States. The SEBs continue to promote the coordinated development

of the generation, supply and distribution of power within their respective

States and to control and regulate private sector power supply undertakings.

At the present time, the States own or control about 90% of India's power

generation facilities. While the SEBs are corporate entities in their own

right and enjoy some autonomy in the management of their day-to-day operations,

they are under the effective control of their State Governments in such policy

matters as capital investment, finance, tariff changes and personnel. As a

means of improving collaboration between the SEBs and establishing power

systems on a broader Regional basis, four Regional Electricity Boards (REBs)

were established between 1964 and 1966 by common resolution of the State

and Central Governments, to help develop integrated power systems in their

respective Regions, and thus prepare for the transition from separate power

systems at State level to Regional systems and finally to an interconnected

national grid. The chairmanship of each REB is assumed in rotation by the

Chairmen of the SEBs in the Region, and engineers of constituent SEBs are

seconded to the REBs. At present, the REBs function in an advisory capacity

for coordination of maintenance programs, generation schedules, interstate

power transfer and pricing. The potential role of the REBs in the light of

the progressive integration of Indian power sector operations is being reviewed

by the Government of India (GOI). The SEBs of Orissa, West Bengal and Bihar

and the Damodar Valley Corporation (DVC) are the major power supply authorities

in the Eastern Region, and will be the recipients of power from the Farakka

station.

33. Central Electricity Authority. The CEA was set up in 1950 to be

responsible for developing a national policy for power development, and to

coordinate the activities of the various planning agencies involved in elec-

tricity supply. As a result of the amendments to the general provisions of

the Electricity (Supply) Act, 1948, which became effective in October 1976,

the scope of the CEA's functions was expanded. In addition to its general

responsibility outlined above, CEA was made responsible for the formulation

of power development plans, optimization of investments in the power sector,

training of personnel, interconnected system operations, and research and

development. The SEBs are required to submit their investment proposals to

the CEA for technical and economic appraisal in a national context.

- 12 -

34. NTPC and NHPC. In order to cope with the persistent inadequacy ofpower supply to meet the growing demand--a situation which has increasinglyprevailed since 1970--GOI made a policy shift and has undertaken to supplementthe efforts of the States by constructing large-scale Centrally-owned thermalpower stations at coal fields and hydro stations in the four Regions, as wellas associated high voltage transmission lines--a step to interconnect thesystems beyond conventional State boundaries. This would lead ultimately toan integrated national power grid. Accordingly, the National Thermal PowerCorporation (NTPC) and the National Hydro Power Corporation (NHPC) were estab-lished in November 1975 under the Companies Act, 1956, as public corporations,wholly owned by GOI, with authority to design, construct, own and operategenerating and associated transmission facilities and supply power in bulkdirectly to the States. The Centrally owned generating stations, includingthe Farakka plant, are designed to supplement the States' activities and addon new power generation capacity effectively within the shortest period oftime. They will be integrated in the future national power system and willsupplement power supply under bulk supply contracts to the States each in theRegion in which it is located.

35. Rural Electrification Corporation. To help SEBs undertake the taskof rural electrification, the REC was established in 1969 under the CompaniesAct, 1956 as a public corporation, wholly owned by the Government. Its maininstitutional objective is to finance rural electrification schemes preparedby SEBs throughout India, functioning as a financial intermediary with tech-nical expertise, and ensuring the efficient on-lending of funds drawn primarilyfrom GOI. In undertaking the task, REC is directed to coordinate its lendingoperations with the activities of other agencies, such as the AgriculturalRefinance and Development Corporation (ARDC), which provide financing forrural development. Although the amount of REC financial support is small inrelation to total SEB operations in the power sector, REC supports today morethan half of total rural electrification expenditures.

Bank Group Operations and Strategy in the Power Sector

36. Since 1954, the Bank has made nine loans to India for power projectsamounting to US$334.5 million and IDA thirteen credits totalling US$1,471 mil-lion. Of this amount, US$1,170.5 million is for financing of generating plant;US$23 million for the purchase of construction equipment for the Beas hydro-electric project; US$380 million for the provision of high voltage trans-mission; and US$232 million for the support of rural electrification schemes.Nine loans and credits for generating plant, the Beas project (Credit 89-IN)and the first three transmission projects (Loan 416-IN and Credits 242-IN and377-IN), have been completed. The Fourth Transmission project (Credit 604-IN)is proceeding satisfactorily notwithstanding initial delays in preparation ofspecifications and in contract awards for highly sophisticated load dispatchequipment; the credit proceeds of US$150 million were fully committed by theend of 1979. The loan to the Tata Electric Companies under the Third TrombayThermal Power project (Loan 1549-IN), which was approved in April 1978, isprogressing satisfactorily. The First Singrauli (Credit 685-IN of April 1977)and Korba (Credit 793-IN of May 1978) projects are also on schedule. The FirstRural Electrification project (Credit 572-IN of July 1975) has been fullycommitted. The Ramagundam project (Credit 874-IN and Loan 1648-IN of February

- 13 -

1979) and the Second Rural Electrification project (Credit 911-IN of June1979) are in the early stages of implementation. The Second Singrauli project(Credit 1027-IN) was approved recently.

37. The Bank Group has had a continuing dialogue with the Government inseeking solutions to a number of complex and politically sensitive problemswhich have confronted the Indian electricity supply industry since Indepen-dence. The sensitivity of Center-State relations and the political constraintsarising from the fact that electricity supply is within the concurrent juris-diction of the Central and State Governments, have dictated a policy of seek-

ing progress through cooperation. More specifically, the Bank Group's mainobjectives of lending operations to the Indian power sector are: (a) accel-erating the installation of generating capacity and promoting measures toimprove the technical levels of operation and maintenance of existing plant;(b) fostering development of comprehensive long-range Regional and nationalsystem plans which would assure implementation of a least-cost power devel-opment program; (c) strengthening of the sector organization; and (d)strengthening of the finances of the institutions involved in the sector,particularly of the SEBs.

38. Some noteworthy results have been achieved, which include: (i)amendment of the general provisions of the Electricity (Supply) Act in 1976,to strengthen the role of the CEA and to authorize the establishment of NTPCand NHPC; (ii) the establishment of the Regional Electricity Boards and laterof the Centrally-owned power companies, which mark the first important stepstowards nationwide power operation; (iii) the recent amendments to the finan-cial provisions of the Electricity (Supply) Act, which provide for the dev-elopment of SEBs on a more commercial basis through financing from internalsources a reasonable proportion of their investments; (iv) tariff studies bya number of SEBs with a view to reassessing tariff policies; (v) preparationof action plans by a number of SEBs, which are designed to restore the 9-1/2%rate of return through tariff increases, rationalization of manpower require-ments and other cost-effective schemes; and (vi) progress of NTPC's generation/transmission construction program with Bank Group assistance. Implementationof the program will make a significant contribution to the gradual eliminationof the shortfall of power; further improvements are anticipated.

39. Going beyond these achievements, Indian authorities have recognizedthat all aspects of the sector need to be reviewed in depth and that satisfac-tory solutions have to be found for outstanding sector development problems.Consequently, GOI established a high-level Committee on Power under the chair-manship of V.G. Rajadhyaksha, former Member of the Planning Commission, withseven working panels of leading experts in both public and private sectors toreview: (a) power planning; (b) project formulation and implementation; (c)operation and maintenance; (d) organization and management; (e) finance,financial management and tariffs; (f) rural electrification; and (g) researchand development. Draft reports by the seven expert panels assembled for thispurpose have been completed and have been reviewed by the Committee whichis expected to submit its findings and recommendations to GOI during 1980.The Bank Group will take a continuing interest in the Committee's findings andGOI's follow-up actions.

- 14 -

40. There remain a number of areas which have been a particular cause ofcontinuing concern to the Bank Group and also have been the subject of contin-uing dialogue with the Government. These include: (i) nationwide long-rangeplanning for power development; and (ii) the financial position of some SEBs.In the continued effort of the Bank Group in helping GOI deal with the long-range problems of the power sector in India, it was decided to concentrate onthe above two areas. During appraisal and negotiations for the SecondSingrauli Thermal Power project as well as this project, discussions were heldwith GOI, CEA, NTPC and NHPC on the content of a long-range national powerdevelopment study designed to prepare a least-cost power development programand CEA's capability to undertake such study with its own staff. The govern-ment agreed with the terms of reference for long term development suggested bythe Bank Group and stated that the study which has been commenced would becompleted by April 1982. From a commercial point of view, the financialperformance of several SEBs has been marginal and even in years where 9-1/2%rates of return were achieved, a number of SEBs were not able to meet theirdebt service requirements. There are several reasons for such performance--e.g., insufficient generating capacity which does not permit utilization ofthe market potential to the fullest extent, maintenance problems, lack ofmonsoon rains leading to severe load shedding and blackouts, disruptions intransport and coal mining resulting in insufficient coal supply, and lowtariff levels. There is scope for improvement in the finances of the agenciesconcerned through increased generation and sales, reduced auxiliary consumptionand lower transmission losses. There is also scope for more stringent costcontrols and more effective management, particularly in Bihar. Recognizingthe need to enhance financial performance of the Eastern Region SEBs, GOIthrough CEA held discussions with the State Governments concerned in late 1979and agreement was reached about enhanced monitoring and improved accountabilityto achieve improved operational and financial management of the SEBs. In thecontext of this project, special attention was directed to the Eastern States,the beneficiaries of Farakka power (paras 53-55).

PART IV - THE PROJECT

41. The project was appraised by a mission which visited India in May/June 1979. A report entitled "India - Farakka Thermal Power Project StaffAppraisal Report" (No. 2976a-IN, dated May 27, 1980) is being distributedseparately to the Executive Directors. Negotiations were held in Washingtonin May 1980. GOI and NTPC were represented by a delegation coordinated byMr. S.C. Jain of the Department of Economic Affairs, Ministry of Finance. Asupplementary Project Data Sheet is attached as Annex III.

Project Description

42. The proposed project represents the first stage of the fourth large-scale thermal power development in India, comprising three 200 MW coal-firedgenerating units, together with ancillary equipment and related works, about410 km of associated 400 kV transmission lines, and a training simulator. Thesite of the power station is in the Murshidabad District in the State of West

- 15 -

Bengal, on the west bank of the Farakka feeder canal. The total project is

expected to be commissioned by the end of 1985.

Project Cost and Financing

43. The project cost, including contingencies but excluding duties and

taxes, is estimated at about US$491 million equivalent, of which about US$62

million represents the estimated foreign exchange costs. Duties and taxes

add about US$9 million to the financing required. Physical contingencies of

10% on civil works, and of 5% on plant and transmission have been included.

Costs for equipment and erection have been escalated at 6% for 1979, 10% for

1980, 7% for the years 1981-1983 and 5% for the years after 1983.

44. The proposed credit and loan of US$250 million would provide about

51% of the cost of the project, excluding interest during construction and

duties and taxes. The balance of the funds required, aggregating about US$249

million equivalent, would be provided by the Government in the form of loan

and equity capital.

Procurement and Disbursement

45. The major items financed under the proposed credit and loan are

three 200 MW generating units; electrical and other power station equipment;

coal handling and transportation equipment, transmission facilities; a training

simulator and consultants' services for plant engineering work. All equipment

financed under the proposed credit and loan, would be procured by NTPC through

international competitive bidding in accordance with the Bank/IDA guidelines.

The proceeds of the credit would be disbursed against 100% of: (a) the c.i.f.

cost of imported items; (b) the ex-factory cost, net of duties and taxes, of

items procured from Indian suppliers; and (c) the cost of technical advisory

services by consultants. Indian manufacturers competing under international

competitive bidding would be granted a preference margin of 15% or the current

rate of import duty, whichever is less. It is expected that local manufac-

turers of equipment and machinery would submit the lowest conforming bids for

most of the items financed under the credit and loan. Documents for indivi-

dual contracts estimated to cost US$1,500,000 or more will be subject to prior

review by the Bank Group. All work not financed from the proposed credit and

loan will be subject to NTPC's procurement procedures, which are satisfactory.

Project Implementation

46. NTPC will implement the proposed project as part of its ongoing power

development program. NTPC has a Board of Directors, which presently consists

of seven members, two of whom are part time. A competent and experienced

Chairman and Managing Director was appointed in early 1976 and NTPC is making

good progress in building up its organization and manpower since then. As

a growing organization, NTPC places special importance on the training of

engineers, supervisors and operating staff as well as managerial and adminis-

trative staff, and is implementing an acceptable training program covering

spheres of activity such as planning, design, constuction and start-up

operation.

- 16 -

47. A master plan for project implementation has been prepared by NTPC.Preparatory civil works have commenced at the plant site. The detailedengineering and design work carried out for the ongoing Bank Group-assistedthermal power development is largely applicable to the proposed project.NTPC has developed a comprehensive project management and information system,including program coordination and supervision of construction of the powerstations. However, in view of the magnitude of its construction program,NTPC agreed to appoint, by October 15, 1980, consultants with broad exper-ience in major construction programs of this nature to review its projectmanagement and information system and their initial implementation (Section2.02 of Project Agreement).

48. Large reserves of coal are available at the Rajmahal coal field,some 50 km from the Farakka plant and coal will be transported by a "merry-go-round" rail transport system which will be installed for this purpose. TheGovernment has agreed to take all necessary steps to ensure adequate coalsupplies for the final installed capacity of the Farakka plant (Section 3.04of Development Credit Agreement). No problem is foreseen with regard to theavailability of adequate quantities for the proposed thermal power station.Cooling water arrangements are adequate.

49. Adequate measures will be taken to minimize potential adverse eco-logical effects of the project. The measures include stack emission controlby electrostatic precipitators and appropriate ash disposal facilities. Theapproval of the National Committee on Environmental Planning and Coordinationhas been obtained, and appropriate occupational safety standards will bestrictly enforced (Section 2.10 of Project Agreement).

NTPC Finances

50. NTPC would begin to earn revenues in 1981/82 when commissioning ofthe first 200 MW generating unit under the First Singrauli project (Credit685-IN) is scheduled. As the generating capacity increases, NTPC's annualrevenue is expected to increase at a faster rate than its operating expensesand produce rates of return on the capital base rising gradually to reach 9.5%by 1988/89 and about 11% by 1990/91. NTPC has agreed to achieve in 1988/89,and maintain thereafter, a rate of return of not less than 9.5% on the costof the average net fixed assets in service, and to set tariffs from the timeof commissioning of its first 200 MW generating unit at the Singrauli thermalpower station at levels not lower than those estimated to be required to meetthis target (Section 4.03 of Project Agreement). This would result in lowerreturns in the earlier years, but in view of the high initial capital invest-ment in the early stages of NTPC's power development and the time involvedin commissioning generating capacity, this approach to setting the tariffand reaching the target rate of return by 1988/89 is appropriate.

51. In accordance with the provisions of the Companies Act, the Govern-ment would provide funds so that NTPC's debt/equity ratio would not exceed 1:1.NTPC's initial authorized share capital of Rs 1,250 million (US$149 million)was increased in May 1979 to Rs 3,000 million (US$357 million). Furtherprogressive increases of share capital are planned during the constructionperiod, reaching about Rs 22,000 million (US$2,620 million) by 1983/84. NTPCwould inform the Association of any proposal for modification of existing

- 17 -

limitations on NTPC's borrowing powers prior to submission to its annual

shareholders' meeting (Section 3.03 of Project Agreement). The proceeds of

the proposed credit and loan would be onlent to NTPC, and conclusion of a

subsidiary loan agreement satisfactory to the Association is a condition of

effectiveness (Section 5.01 (a) of Development Credit Agreement and Section

6.01 of Loan Agreement). The GOI loan would be for a term of 20 years,

including five years grace, with interest at the rate of 10-1/4% per annum.

This is the standard rate at which GOI currently lends to public sector

enterprises. The exchange risk will be borne by the Government. Inflation

in India between 1974/75 and 1978/79 averaged only 1.5% per annum. With the

sharp increase in oil prices during 1979 coinciding with a severe drought,

prices spurted by almost 15% between April and December 1979 and are anti-

cipated to increase another 10% during 1980/81. Given past GOI determination

and success in containing inflation, and the likelihood of a strong agricul-

tural recovery and improved supply of industrial inputs, the rate of price

increase over the project period is expected to average somewhat below 7%

per annum.

52. As in the case of the previous Bank Group-assisted projects,

Farakka's power output will be supplied in bulk to the Eastern Region SEBs

through 400 kV transmission lines. GOI has undertaken to obtain, not later

than October 10, 1980, undertakings from the recipient SEBs and Damodar Valley

Corporation (DVC) in the Eastern Region that they purchase at least 85% of

the power generated by the project units (three 200 MW units) of the Farakka

station (Section 3.05 of Development Credit Agreement). The remaining 15%

would be sold in accordance with priorities to be determined by GOI to the

States with the greatest need. NTPC has agreed to sell the output of power

under bulk supply contracts satisfactory to the Association (Section 2.09 of

Project Agreement). NTPC has prepared a draft bulk supply contract which is

presently being examined in the context of a proposal to study the feasibility

of an agency selling power from all central projects in a Region at a common

rate and to ensure that the tariff is consistent with overall economic consid-

erations and the financial viability aspects of NTPC. GOI has indicated that

agreement on the bulk supply of Farakka power would be reached at least six

months before the start of commercial operation of the first 200 MW unit of

the Farakka station scheduled for December 1984. The Bank Group will review

the commercial arrangements before they are finalized.

Operational and Financial Performance of SEBs

53. The operational and financial performance of SEBs has been the

subject of a continuous dialogue between GOI and the Bank Group. The Bank

Group has sought, under the previous lending operations, to improve their

performance and work toward a rate of return target of 9.5%. While actual

performance has varied among SEBs, the overall trend showed an improvement

through 1976/77, when seven out of the sixteen major SEBs reached the target

rate of return, compared with only four in the previous year, 1975/76. A

further two reached their targets in 1977/78 with the help of rural electri-

fication subsidies from their State Governments. Another SEB is expected

to achieve the agreed rate of return in 1979/80. Returns generally contracted

in 1977/78 and 1978/79 due to the adverse financial impact of forced plant

outages caused by the natural disasters of flooding and drought, increased

- 18 -

purchases of relatively expensive thermal power and disruptions in the coalmining industry and in the transport sector, leaving ten out of the sixteenSEBs, including two Eastern Region SEBs--Orissa and Bihar--unable to reachthe agreed rate of return. 1/ The situation faced by some hard-hit SEBs didnot constitute "normal circumstances", and it can be justifiably argued thatthe achievement of the 9.5% could not be realistically expected.

54. There are special problems associated with the power industry in

the Eastern Region which require special treatment. This Region is the mostvulnerable area in India as regards power availability. Installation ofadditional generating capacity has been constrained primarily because of alack of financial resources. The financial performance of the Eastern RegionSEBs and DVC was discussed in detail with GOI and CEA officials during appraisaland negotiations for the Second Singrauli Thermal Power project as well as thisproject; the performance of the DVC, a statutory body which was set up underGOI Act in 1948 and operates about 40% of the installed capacity in the EasternRegion, was satisfactory during recent years with a rate of return exceeding20%. This creditable performance is likely to be maintained for the immediatefuture. On the other hand, the financial records of the Eastern Region SEBs,particularly that of Bihar indicate their weak position partly because generat-ing stations have had operational problems which have curtailed electricity

output. The Bihar SEB has undertaken a thorough investigation of these prob-lems, and CEA was made responsible for monitoring this program of studies witha view to the introduction of an action plan for overall improvement. In thecircumstances, the immediate restoration of a rate of return of 9.5% cannotrealistically be expected. During negotiations, the GOI representativesundertook to send a report on the position of the Bihar SEB to the Bank Group

within the next six months. In the case of the Orissa SEB, the rate of Stateelectricity duty recovered from consumers is as high as 5% of capital base, asagainst a target of 1.5%. Consequently, if the gross return is compared withthe target of 11% (9.5% plus 1.5% for duties) the annual projections throughFY1983 show that the target rate of return will be achieved in FY1982. Thisperformance is acceptable, considering the periodic low availability of hydropower in recent years in what is a predominantly hydro system, coupled withlow output of some thermal plant. The West Bengal SEB exceeded its 9.5% rateof return in FY1979. However, because of the doubling of installed capacityprojected during the three years to March 1983 and the phased build up tostabilized generation by the new plant, additional revenues will not bereceived in proportion to increases in capital base. While efforts are beingmade to complete modifications and improvements in existing installed capacityin order to improve availability factors and boost revenues, rates of returnprojected for the four years ending March 1983 of 7% rising to 9.3% must beregarded as reasonable.

1/ Duties are levied on electricity sales in all States, except one.Inclusion of such taxes as a benefit to the States/SEBs would increasethe returns by up to 5 percentage points. Furthermore, a recentlyenacted GOI tax on kWh generated is equivalent to a return of additional

2-3 percentage points.

- 19 -

55. In November 1979, GOI through CEA held discussions with the StateGovernments and their SEBs. There was general consensus that concerted effortswere necessary to improve the operational performance of the Boards. Whileimprovements in operational efficiency and financial performance can be broughtabout over time, GOI and the State Governments and their SEBs have agreed tointroduce various monitoring measures, including a system of accountability,a monthly reporting system on project implementation and capacity utilization,and setting of targets for reducing transmission and distribution losses.Measures are in hand to accelerate the stabilization of newly installed thermalpower units, to better monitor breakdowns, to ensure adequate supplies ofspares and to initiate rehabilitation programs for units which require it.Training programs at all levels are being strengthened. The introduction ofthe above measures would bring greater surveillance over the operations andfinances of the SEBs. The Bank Group will receive comprehensive periodicinformation on the power sector which will enable it to monitor progress inthe implementation of these improvement measures. The financial provisionsof the Electricity (Supply) Act, 1948, have been amended to put the operationsof the SEBs on a more commercial basis by enabling them to finance from internalsources a reasonable portion of their investment program. The manner in whichthis will be achieved is a subject which has been under evaluation by both theState Governments in conjunction with their SEBs, and by the RajadhyakshaCommittee.

Project Justification and Risks

56. The proposed project is the least-cost solution to ease the acutepower shortages in the Eastern Region within reasonable time. Compared tothe practical alternative of smaller coal-based stations that would be in-stalled by individual SEBs in the absence of the project, the present valueof the cost stream of the proposed project is the least-cost alternative atdiscount rate up to 35%. The economic rate of return of the project, usingtariff revenues together with observed willingness to pay for continuous powersupply as a proxy for economic benefits, is 13%. This must be regarded aswell below the true economic rate of return on the proposed expansion of powergenerating capacity, since additional benefits which are expected from proj-ect implementation but whose quantification is difficult--e.g., industrial,agricultural and commercial output maintained by the reduction of shortages--are not included.

57. Project risks are no greater than can normally be expected withoperations of this type. The principal risk would be the possibility of delayin the scheduled commissioning of plant. The progress of project implementa-tion will be closely monitored during engineering and construction, and theuse of experienced review consultants and management and information systemconsultants would help minimize delays in project implementation. The factthat a number of 200 MW units will have been in operation in India beforethe project is commissioned will reduce the possibility of operational dif-ficulties during start-up and the early stages of operation.

- 20 -

PART V - LEGAL INSTRUMENTS AND AUTHORITY

58. The draft Development Credit and Loan Agreements between India, andthe Association and the Bank, respectively, the draft Project Agreementbetween the Association, the Bank and NTPC, the Recommendation of the Committeeprovided for in Article V, Section l(d) of the Articles of Agreement of theAssociation and the Report of the Committee provided for in Article III,Section 4 (iii) of the Articles of Agreement of the Bank are being distributedto the Executive Directors separately.

59. Special conditions of the project are listed in Section III ofAnnex III. Execution of a Subsidiary Loan Agreement between India and NTPChas been made an additional condition of effectiveness of the credit and loan(Sections 5.01 of Development Credit Agreement and Loan Agreement).

60. I am satisfied that the proposed credit and loan would comply withthe Articles of Agreement of the Association and the Bank.

PART VI - RECOMMENDATION

61. I recommend that the Executive Directors approve the proposedcredit and loan.

Robert S. McNamaraPresident

June 9, 1980

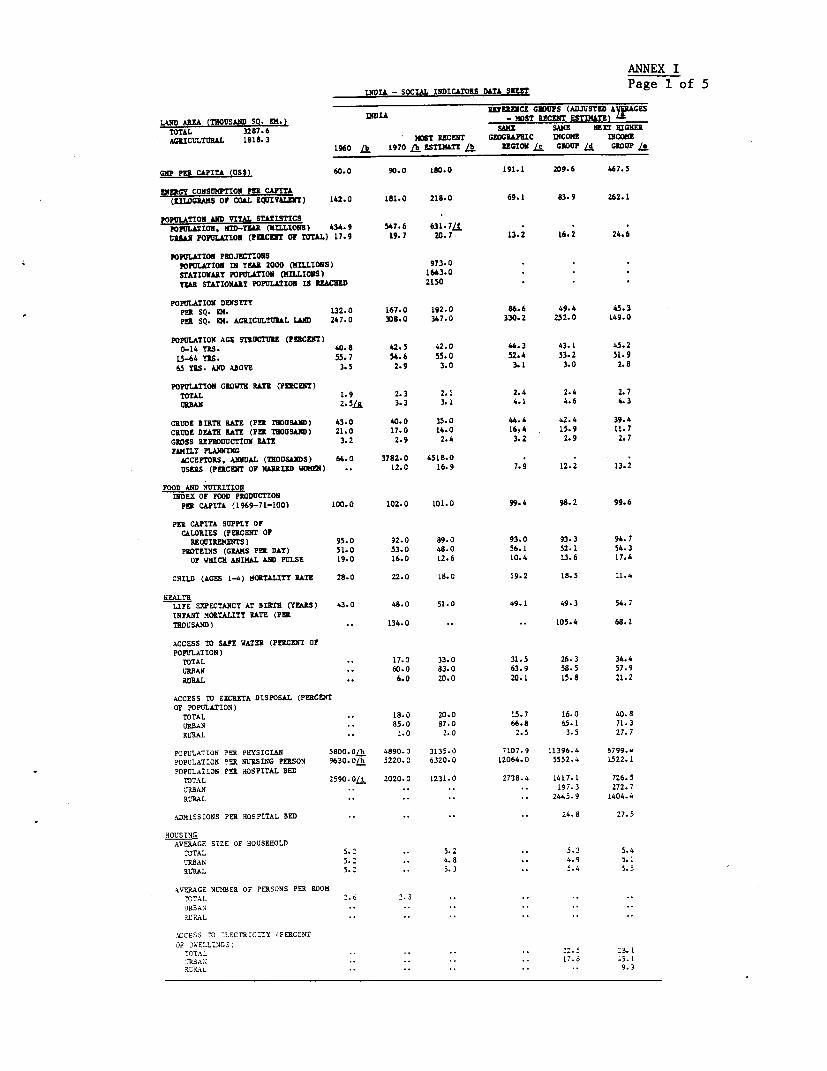

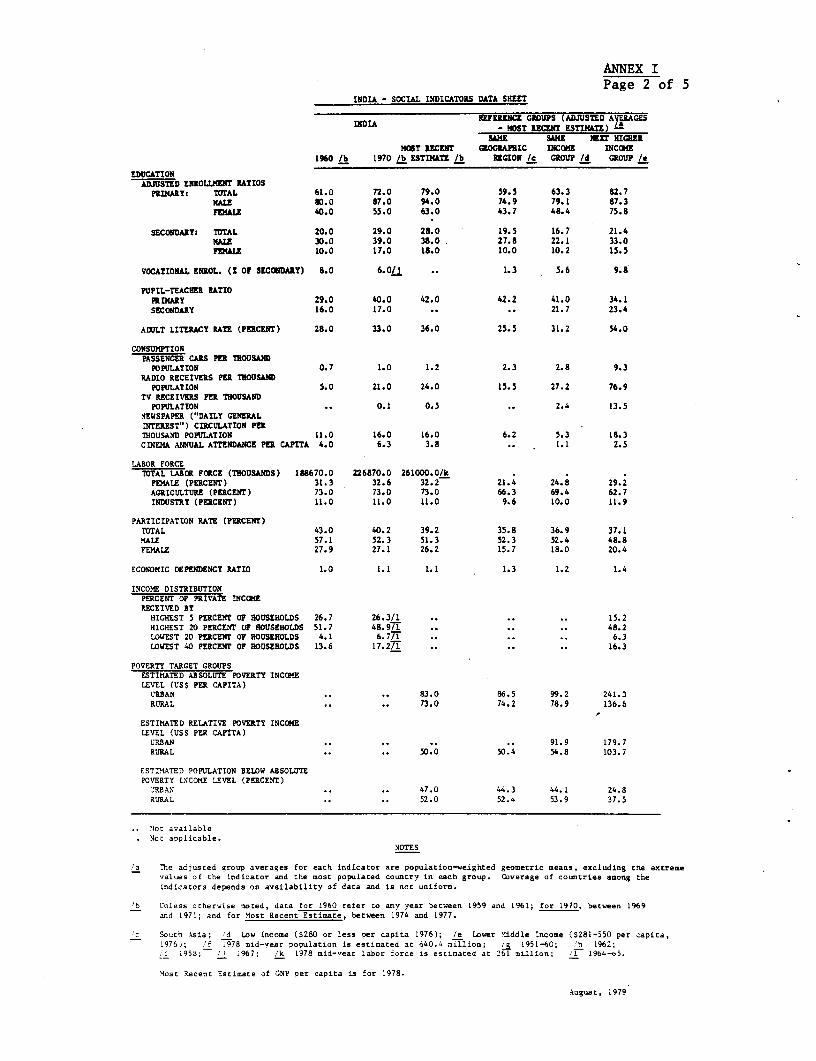

ANNEX I

INDIA - SOCIAL INDICATORS DATA SOM Page 1 of 5

REIENCE GRDUPS (ADJUSTED AyU&GES

LAND AMEA (THOUSAND SQ. m3.) nmDL - NOST RRCERT ESTIMTE)TOTAL 3287.6 SAME SAME IZXT HIGHEAGRECULTURAL 1818. 3 MOST RECmaT GEOGRAC INcoME INCOME

1960 Lb 1970 A ESTUITE /b REGION I CROVP ld GROUP S

GNP PeR CAPITA (US) 60.0 90.0 180.0 191.1 209.6 467.5

ENEaGY CONSUMVPTION P CAPITA(KiLoGRS or COAL EQV4LEII) 142.0 181.0 218.0 69.1 83.9 262.1

POPULATION AND VITAL STATISTICSPOPULATION, ID-TEA (DLIONS) 434.9 547.6 631. .L,.

IUSII POPULATION (PERCENT Or TOTML) 17.9 19.7 20.7J 13.2 16.2 24.6

POPULATION PROJECTIONSPOPULATION IN YEAR 2000 (MILLIONS) 973.0STATIONARY POPULATION (MILLIONS) 1643.0TEAR STATIONARY POPULATION IS REACHED 2150

POPULATION DENSIYPeR SQ. IN. 132.0 167.0 192.0 86.6 49.4 45.3PER SQ. DI. AGRICULTURL LAND 247.0 308.0 347.0 330.2 252.0 149.0

POPULATION AGE STRUCTUR (PUCMcT)0-14 TES. 40.8 62.5 42.0 44.3 43.1 45.2

15-64 TRS. 55.7 54.6 55.0 52.4 53.2 51.965 YES. AND ABOVE 3.5 2.9 3.0 3.1 3.0 2.8

POPULATION GROWTH RAE (PERCENT)TOTAL 1.9 2.3 2.1 2.4 2.4 2.7

UBAN 2

. 5L 3.3 3.1 4.1 4.6 4.3

CRUDE 3IRTR RATe (PUa THOUSAND) 43.0 40.0 35.0 44.4 42.4 39.4CRUDE DEATE RATE (PEu TSOUSAND) 21.0 17.0 14.0 16.4 15.9 11.7GROSS REPRODUCTION RATe 3.2 2.9 2.4 3.2 2.9 2.7FAMILY PLANNING

ACCEPTORS. ANNUAL (THOUSANDS) 64.0 3782.0 45LB.0USERS (PERCENT OF MARRIED WOHEN) .. 12.0 16.9 7.9 12.2 13.2

FOOD AND NUTRITION

INDEX OF FOWD PRODUCTIONPER CAPITA (1969-71-100) 100.0 102.0 101.0 99.4 98.2 99.6

PER CAPITA SUPPLY OFCALORIES (PERCENT OP

REQUIREMENTS) 95.0 92.0 89.0 93.0 93.3 94.7PROTEINS (GRAMS Pra DAY) 51.0 53.0 48.0 56.1 52.1 54.3

OP WHICH ANIMAL ND PULSE 19.0 16.0 12.6 10.4 13.6 17.4

CHILD (AGES 1-4) HORTALTY RATE 28.0 22.0 18.0 19.2 18.5 11.4

HEALTHLIFE EXPECTANCT AT 3IRTH (YEARS) 43.0 48.0 51.0 49.1 49.3 54.7

INFANT MORTALITY RATE (PERTHOUSAND) .. 134.0 .. .. 105.4 68.1

ACCESS TO SAFE WATZR (PERCENT OFPOPULATION)

TOTAL .. 17.0 33. 0 31.5 26.3 34.4URBAN .. 60.0 83.0 63.9 58.5 57.9RURAL .. 6.0 20.0 20.1 15.8 21.2

ACCESS TO EXCRETA DISPOSAL (PERCENT

OF POPULATION)TOTAL .. 18.0 20.0 15.7 16.0 40.8URBAN .. 85.0 87.0 66.8 65.1 71.3RVRAL .. 1.0 2.0 2.5 3.5 27.7

POPULATION PER PHYSICLN 58oo.0oh 4890.0 3135.0 7107.9 11396.4 6799..

POPULATION PER NURSING PERSON 9630.O/h 5220.0 6320.0 12064.0 5552.4 1522.1POPULATION PER HOSPITAL BED

TOTAL 259.0-Li Z020.0 1231.0 2738.4 1417.1 726.5

'R,AN .. .. .. .. 197.3 272.7

RLRAL .. .. .. .. 2445.9 1404.4

ADMISSIONS PER HOSPITAL BED . . 24.8 27.5

HOUSING

AVERAGE SIZE OF HOUSEHOLD

7OTAL 5.2 .. 5.2 . 5.3 5.4

URBAN 5.2 4. . .8 .. 4.9 5.1

RURAL 5.2 .. 5.3 5. .4 5.5

AVERAGE NUMBER OF PERSONS PER ROOM

-TAOL 2.6 2.3 ..

JRSAN ... .. ..

VIRAL .. .. ..

ACCESS 0 -L ECTRICITY PERCENT

OF 3WE'L.NGS,7CTAL .... .. .. .22. 5 .I

R3AN .. .. .. .. . .5.1RKRAL .. .. .. .. .. 9.3

ANNEX IPage 2 of 5

INDIA - SOCIAL INDICATORS DATA SHEET

INDIA REFERENCE GROUPS (ADJUSTED AEAGES- HOST RECENT ESTIN&SE) -

SAME SAKE NCST HIGHERMOST RECENT GROGRAPHIC INCOME INCOME

1f0 lb 1970 /b ESTIMATE lb REGION /c GROUP /d GROUP /e

EDUCATIONADJUSTED ENROLLMSNT RATIOS

PRIDARY: TOTAL 61.0 72.0 79.0 59.5 63.3 82.7MALE 80.0 87.0 94.0 74.9 79.1 87.3FaALE 40.0 55.0 63.0 43.7 48.4 75.8

SECONDARY: TOTAL 20.0 29.0 28.0 19.5 16.7 21.4MALE 30.0 39.0 38.0 27.8 22.1 33.0FEMALZ 10.0 17.0 18.0 10.0 10.2 15.5

VOCATIONAL ENROL. (Z OF SECONDARY) 8.0 6.01 .. 1.3 5.6 9.8

PUPIL-TEACHER RATIOPIMIARY 29.0 40.0 42.0 42.2 41.0 34.1SECONDARY 16.0 17.0 .. .. 21.7 23.4

ADULT LITERACY RATE (PERCENT) 28.0 33.0 36.0 25.5 31.2 54.0

CONSUmPTIONPASSENGER CARS PER THOUSAND

POPULATION 0.7 1.0 1.2 2.3 2.8 9.3RADIO RECEIVERS PER TOUSAND

POPULATION 5.0 21.0 24.0 15.5 27.2 76.9TV RECEIVERS PCR THOUSAND

POPULATION .. 0.1 0.5 .. 2.4 13.5NEWSPAPER ("DAILY GENERALINTEREST") CIRCULATION PERTHOUSAND POPULATION 11.0 16.0 16.0 6.2 5.3 18.3CINEMA ANNUAL ATTENDANCE PER CAPITA 4.0 6.3 3.8 .. 1.1 2.5

LABOR FORCETDTAL LABOR FORCE (THOUSANDS) 188670.0 226870.0 261000.0/k

FEMALE (PERCENT) 31.3 32.6 32.2 21.4 24.8 29.2AGRICULTURE (PERCENT) 73.0 73.0 73.0 66.3 69.4 62. 7INDUSTRY (PERCENT) 11.0 11.0 11.0 9.6 10.0 11.9

PARTICIPATION RATE (PERCENT)TOTAL 43.0 40.2 39.2 35.8 36.9 37.1MALE 57.1 52.3 51.3 52.3 52.4 48.8FEMALE 27.9 27.1 26.2 15.7 18.0 20.4

ECONOMIC DEPENDENCY RATIO 1.0 1.1 1.1 1.3 1.2 1.4

INCOME DISTRIBUTIONPERCENT OF PRIVATE INCOMERECEIVED BY

HIGHEST 5 PERCENT OP HOUSEHOLDS 26.7 26.3/1 .. .. 15.2HIGHEST 20 PERCENT OF HOUSEHOLDS 51.7 48.971 48.2LOWEST 20 PERCENT OF HOUSEHOLDS 4.1 6.771 .. .. .. 6.3LOWEST 40 PERCENT Or HOUSEHOLDS 13.6 17.27i .. .. .. 16.3

POVERTY TARGET GROUPSESTIMATED ABSOLUTE POVERTY INCOMELEVEL (USS PER CAPITA)

L'RBAN .. .. 83.0 86.5 99.2 241.3RURAL .. .. 73.0 74.2 78.9 136.6

ESTIMATED RELATIVE POVERTY INCOMELEVEL (USS PER CAPITA)URBAN .. .. .. .. 91.9 179.7RURAL .. .. 50.0 50.4 54.8 103.7

ESTIIMATED POPULATION BELOW ABSOLUTEPOVERTY INCOME LEVEL (PERCENT)

'RBAN .. .. 47.0 46.3 44.1 24.8RURAL .. .. 52.0 52.4 53.9 37.5

Not availableNoc applicable.

NOTES

ia The adjusred group averages for each indicator are population-weighted geometric means, excluding the extremevalues of the indicator and the most populaced country in each group. Coverage of countries among theindicators depends on availability of data and is not uniform.

lb Unless ocherwise noted, data for 1960 refer to any year between 1959 and 1961; for 1970, between 1969and 1971; and for Most Recent Estimate, between 1974 and 1977.

Ic Souch Asia; /d Low Income (S280 or less per capita 1976); /e Lower Middle income (S281-550 per capita,1976); 1' i978 mid-year population is estimated ac 640.4 nillion; /j 1951-60; 'h 1962;

- 1958; / i i967; /k 1978 mid-year labor force is estimated at 261 million; _ 1964-65.

Most Recenc Escitmate of GNP per capita is for 1978.

August. 1979

ANNEX IPEP5ITTIONS OF SOCIALIinDICATORS Page 3 of 5

No-tes: Although the data ar d-an fern soucegnealy Judged the sat a.thoebtmtie and reliable, it should an be noted that they sp not be inten--tIona lly o-p-rble be-.sa of the laos of standardisd defbnltioa and I.sa.ePt, used by differet coutries In colleting the data. The data are,nnteeou_eful to Idecorbe orders of Magitde, idicate treda, andoaaneis etain. major differer- beao outIs