Embed Size (px)

Citation preview

WORLDPAY CONSUMER BEHAVIOUR AND PAYMENTS REPORT 2017

What’s driving today’s consumers?

Collect

IntroductionWelcome

Section 1How today’s consumers shop

Section 2Exploring the payment experience

Section 3Security & identity

Key takeawaysReport overview

Discover WorldpayWho we are, what we do

In June 2017 we surveyed over 2,500 consumers across the UK, analysing their behaviour across the different buying channels.

We’ve split out the findings by age

range to highlight the interesting

differences between each

generation’s shopping habits.

Gen Z (16-20)

Gen Y (21-34)

Gen X (35-50)

Boomers (51-69)

Our consumers

Consumer Behaviour & Payments Report 20174 5Consumer Behaviour & Payments Report 2017

Vicky DringSenior Product Manager - Digital — Boots UK

James FrostCMO — Worldpay UK

Introduction

At Boots, customer insight is an integral part of our business.

So when Worldpay contacted us about this report we were delighted to get involved. We wanted to use this research to help understand how shoppers interact with technology in-store, and what that means for their journey as a whole. It’s essential for an omni-channel business like ours to continually look at how our different channels can interact and benefit our customers.

We were also keen to find out how consumers want to engage with brands through mobile, and understand their receptiveness to communications through their phones. I am pleased to say that this report provides us with real insights that we can take action from, alongside interesting behavioural data that will help inform our strategic approach.

Welcome to Worldpay’s Consumer Behaviour and Payments Report 2017.

We wanted to carry out this research to provide detailed insights into how consumers shop and pay in the UK to get an understanding of what they expect from brands.

This year, we’re focusing on three key areas. Firstly, we’ll look at consumer shopping behaviour across in-store and online, answering key questions like: how important are store employees in the overall shopping experience? Which online retailer is easiest to buy from?

We’ll then explore payments, finding out how important they are to the customer journey in retail and hospitality, and asking what consumers think of different payment methods, including contactless via mobile versus contactless cards. The answers are quite revealing.

Lastly, we will examine the world of social media and identity, unpicking consumer attitudes to biometrics, and how they feel about making payments through messenger apps.

We hope you enjoy these insights.

6 Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017 77

How today’s consumers shop

Whether consumers buy online, in-store or a combination of the two, accommodating their diverse shopping preferences is essential for retailers to stay ahead of the competition.

Consumer Behaviour & Payments Report 2017

8 9Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

In-store Online Mobile Phone

78+22MGen X

78%35-50 61+39MBoomers

61%51-6979+21MGen Z

79%16-20 82+18MGen Y

82%21-34

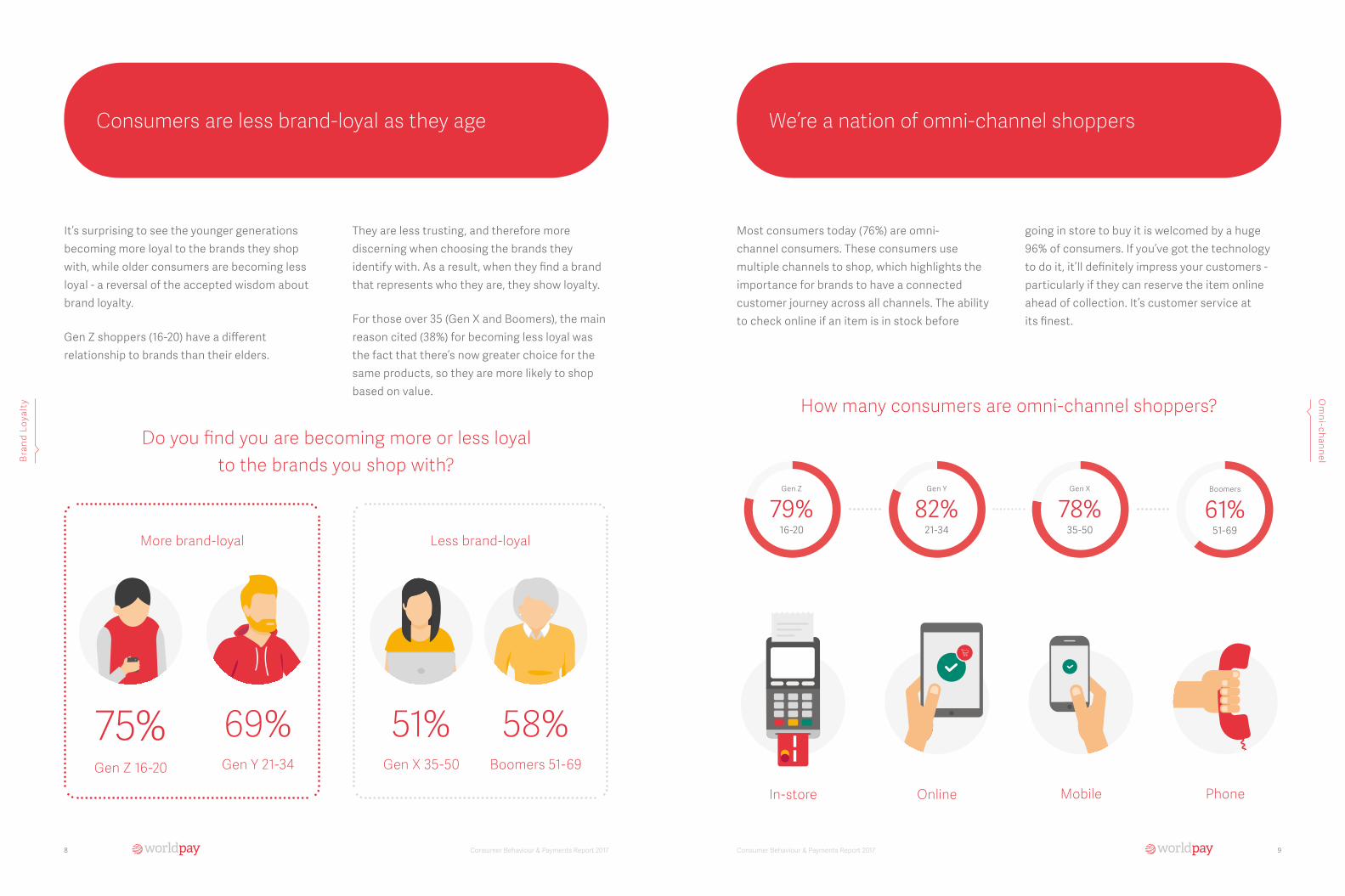

75%Gen Z 16-20

69%Gen Y 21-34

51%Gen X 35-50

58%Boomers 51-69

More brand-loyal Less brand-loyal

Do you find you are becoming more or less loyal to the brands you shop with?

How many consumers are omni-channel shoppers?

Bra

nd L

oyal

ty

Consumers are less brand-loyal as they age We’re a nation of omni-channel shoppers

It’s surprising to see the younger generations becoming more loyal to the brands they shop with, while older consumers are becoming less loyal - a reversal of the accepted wisdom about brand loyalty.

Gen Z shoppers (16-20) have a different relationship to brands than their elders.

They are less trusting, and therefore more discerning when choosing the brands they identify with. As a result, when they find a brand that represents who they are, they show loyalty.

For those over 35 (Gen X and Boomers), the main reason cited (38%) for becoming less loyal was the fact that there’s now greater choice for the same products, so they are more likely to shop based on value.

Most consumers today (76%) are omni-channel consumers. These consumers use multiple channels to shop, which highlights the importance for brands to have a connected customer journey across all channels. The ability to check online if an item is in stock before

going in store to buy it is welcomed by a huge 96% of consumers. If you’ve got the technology to do it, it’ll definitely impress your customers - particularly if they can reserve the item online ahead of collection. It’s customer service at its finest.

Om

ni-channel

10 11Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

CHECK OUT OUR

Latest Offers

HAM SALAD SANDWICH

£1.50

1 LITRE SIX PACK OF WATER

£3.00

2 FOR 1 ON DEODORANT

£2.00

Gre

at

If re

leva

nt

Pref

er n

ot

Too

intr

usiv

e

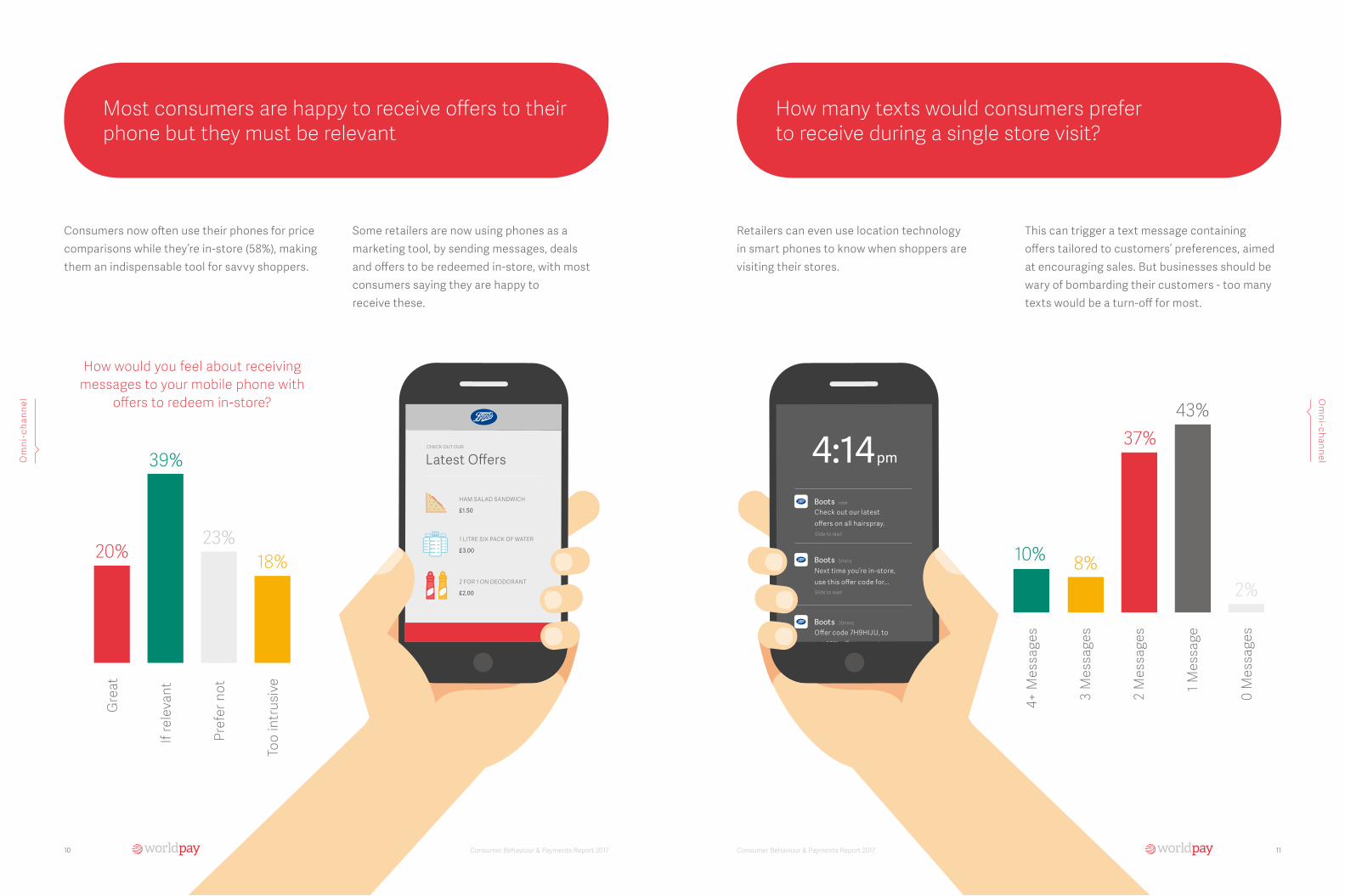

20%

39%

23%18%

How would you feel about receiving messages to your mobile phone with

offers to redeem in-store?

4:14pm

Boots now

Slide to read

Boots 5mins

Slide to read

Boots 20mins

Check out our latest offers on all hairspray.

Next time you’re in-store,use this offer code for...

Offer code 7H9HIJU, to get 10% off your next...

4+ M

essa

ges

3 M

essa

ges

2 M

essa

ges

1 Mes

sage

0 M

essa

ges

10% 8%

37%43%

2%

Most consumers are happy to receive offers to their phone but they must be relevant

Consumers now often use their phones for price comparisons while they’re in-store (58%), making them an indispensable tool for savvy shoppers.

Some retailers are now using phones as a marketing tool, by sending messages, deals and offers to be redeemed in-store, with most consumers saying they are happy to receive these.

Om

ni-c

hann

el

How many texts would consumers prefer to receive during a single store visit?

Retailers can even use location technology in smart phones to know when shoppers are visiting their stores.

This can trigger a text message containing offers tailored to customers’ preferences, aimed at encouraging sales. But businesses should be wary of bombarding their customers - too many texts would be a turn-off for most.

Om

ni-channel

12 13Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

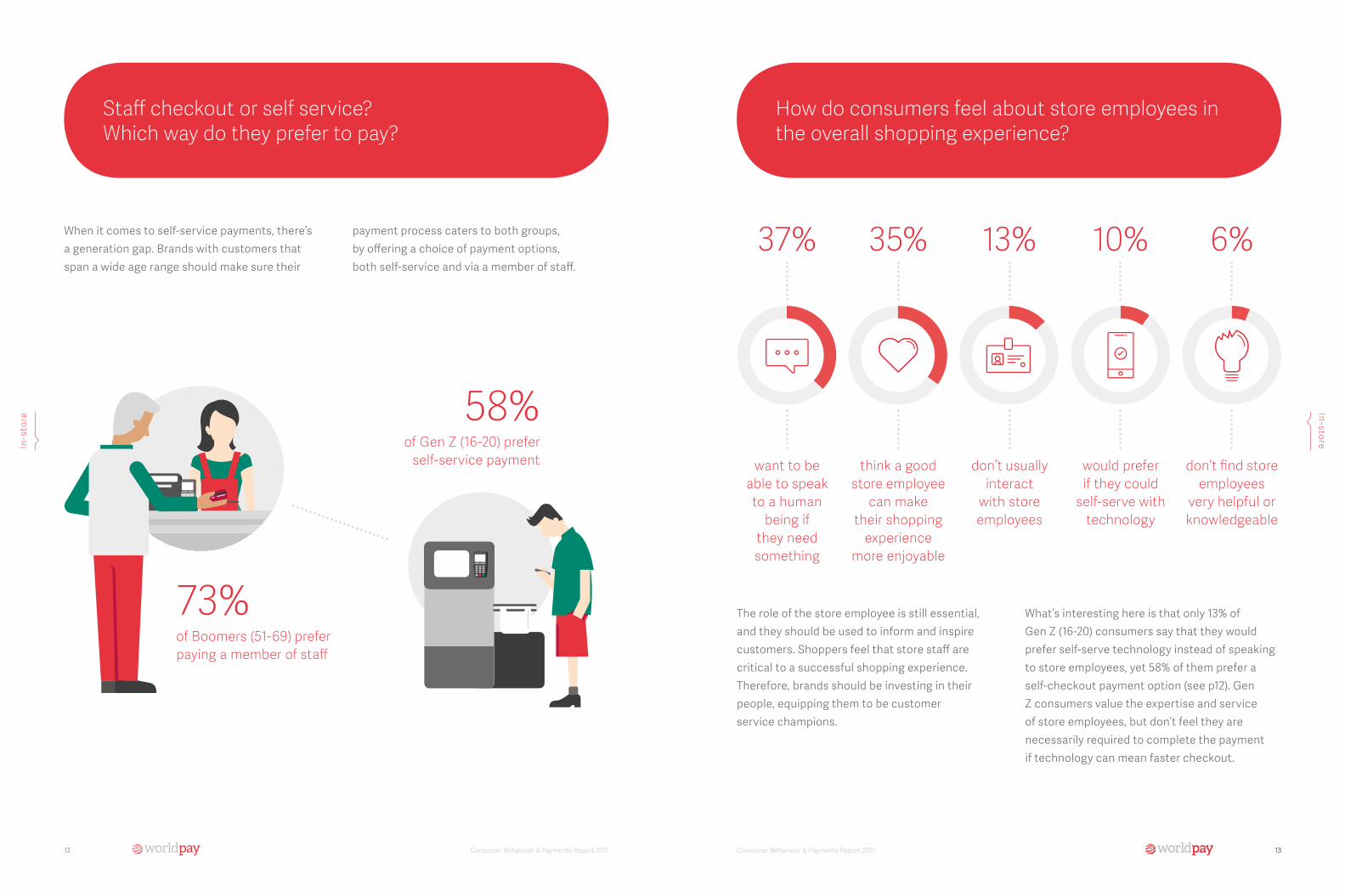

37+63Mwant to be

able to speak to a human

being if they need something

37%

35+65M35%

think a good store employee

can make their shopping

experience more enjoyable

13+87M13%

don’t usually interact

with store employees

10+90M10%

would prefer if they could

self-serve with technology

6+94M6%

don’t find store employees

very helpful or knowledgeable

73%

58%

of Boomers (51-69) prefer paying a member of staff

of Gen Z (16-20) prefer self-service payment

13

Staff checkout or self service? Which way do they prefer to pay?

How do consumers feel about store employees in the overall shopping experience?

When it comes to self-service payments, there’s a generation gap. Brands with customers that span a wide age range should make sure their

payment process caters to both groups, by offering a choice of payment options, both self-service and via a member of staff.

The role of the store employee is still essential, and they should be used to inform and inspire customers. Shoppers feel that store staff are critical to a successful shopping experience. Therefore, brands should be investing in their people, equipping them to be customer service champions.

What’s interesting here is that only 13% of Gen Z (16-20) consumers say that they would prefer self-serve technology instead of speaking to store employees, yet 58% of them prefer a self-checkout payment option (see p12). Gen Z consumers value the expertise and service of store employees, but don’t feel they are necessarily required to complete the payment if technology can mean faster checkout.

In-s

tore

In-store

14 15Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

Collect

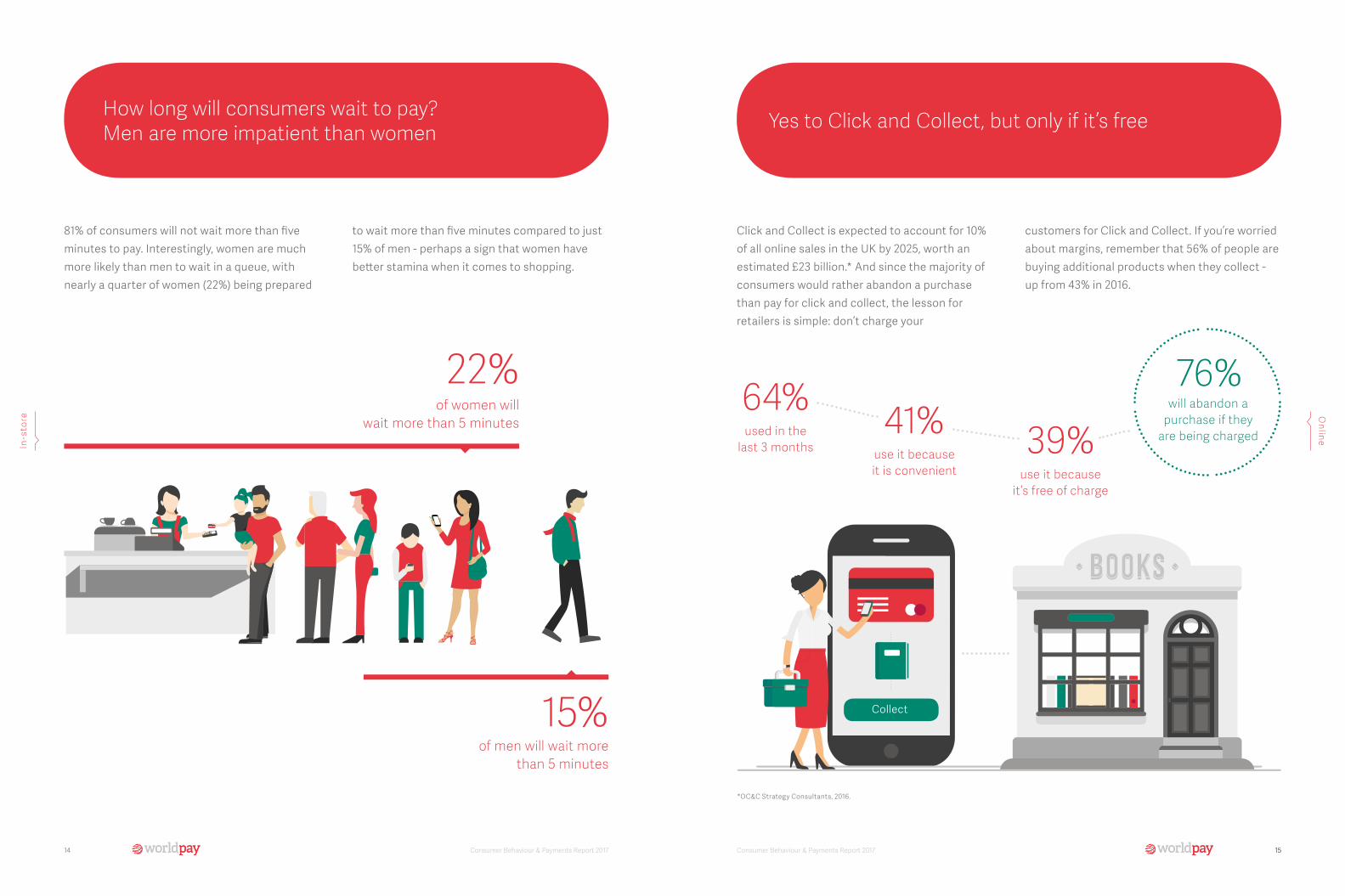

64% 41% 39%used in the last 3 months

76%will abandon a

purchase if they are being charged

use it because it is convenient use it because

it’s free of charge

22%of women will

wait more than 5 minutes

15%of men will wait more

than 5 minutes

15

Click and Collect is expected to account for 10% of all online sales in the UK by 2025, worth an estimated £23 billion.* And since the majority of consumers would rather abandon a purchase than pay for click and collect, the lesson for retailers is simple: don’t charge your

customers for Click and Collect. If you’re worried about margins, remember that 56% of people are buying additional products when they collect - up from 43% in 2016.

How long will consumers wait to pay? Men are more impatient than women Yes to Click and Collect, but only if it’s free

81% of consumers will not wait more than five minutes to pay. Interestingly, women are much more likely than men to wait in a queue, with nearly a quarter of women (22%) being prepared

to wait more than five minutes compared to just 15% of men - perhaps a sign that women have better stamina when it comes to shopping.

In-s

tore

Online

*OC&C Strategy Consultants, 2016.

16 17Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

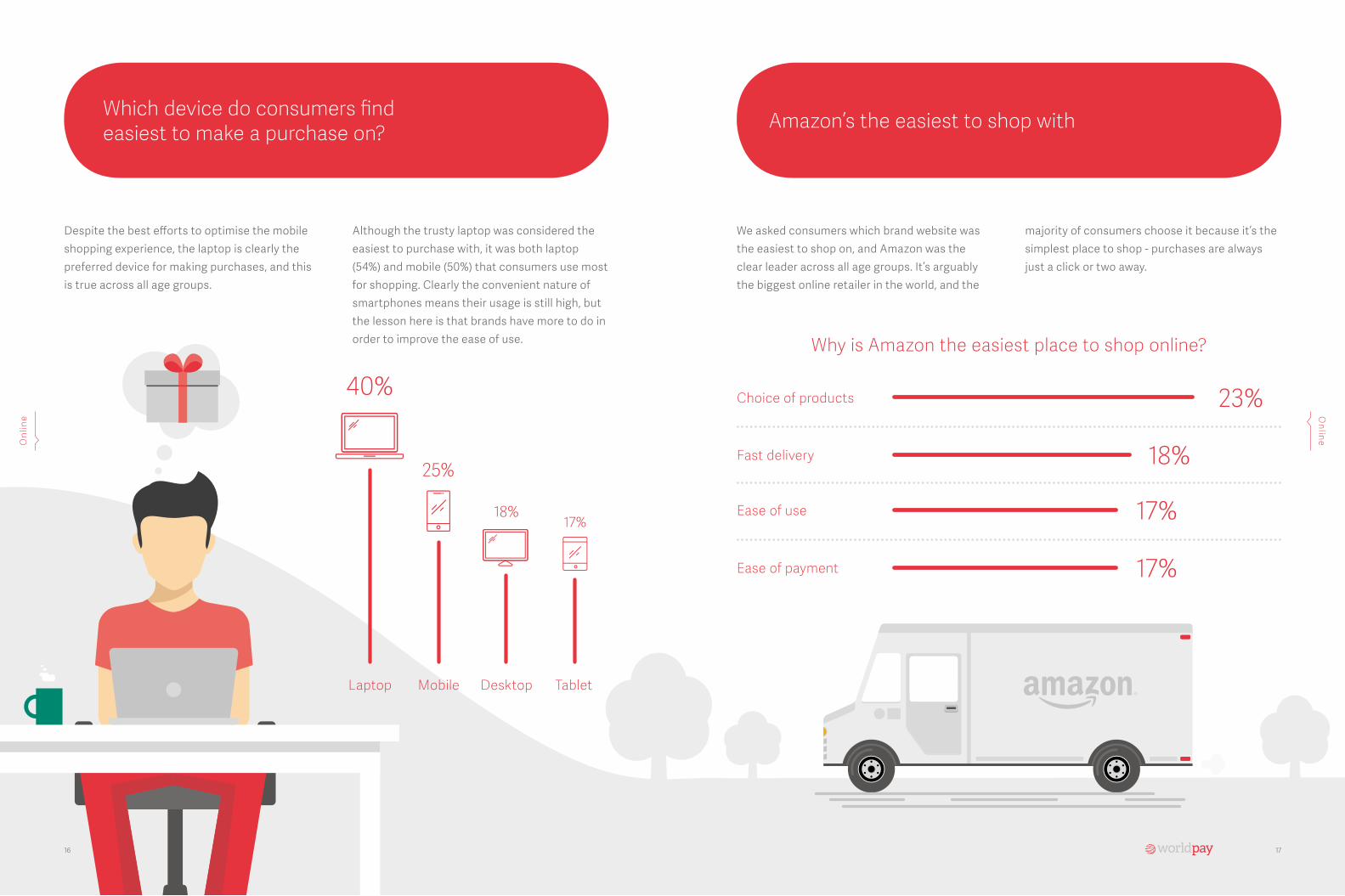

40%

25%

18%17%

Laptop Mobile Desktop Tablet

18%

17%

17%

23%

Why is Amazon the easiest place to shop online?

Choice of products

Fast delivery

Ease of use

Ease of payment

Onl

ine

1716

Amazon’s the easiest to shop withWhich device do consumers find easiest to make a purchase on?

Despite the best efforts to optimise the mobile shopping experience, the laptop is clearly the preferred device for making purchases, and this is true across all age groups.

Although the trusty laptop was considered the easiest to purchase with, it was both laptop (54%) and mobile (50%) that consumers use most for shopping. Clearly the convenient nature of smartphones means their usage is still high, but the lesson here is that brands have more to do in order to improve the ease of use.

We asked consumers which brand website was the easiest to shop on, and Amazon was the clear leader across all age groups. It’s arguably the biggest online retailer in the world, and the

majority of consumers choose it because it’s the simplest place to shop - purchases are always just a click or two away.

Online

18 Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017 19

Exploring the payment experience

Speed is key when it comes to payments in 2017, as the rise of contactless proves. However, consumers are not completely confident with payment via their smartphones.

20 21Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

Order confirmed! X 1 S PAC E R O C K E T

T O TA L £ 12 , 0 0 0

65%of Gen Z consumers expect they’ll mostly be paying with their

phones by 2022

In a galaxy, not so far away... in 2022

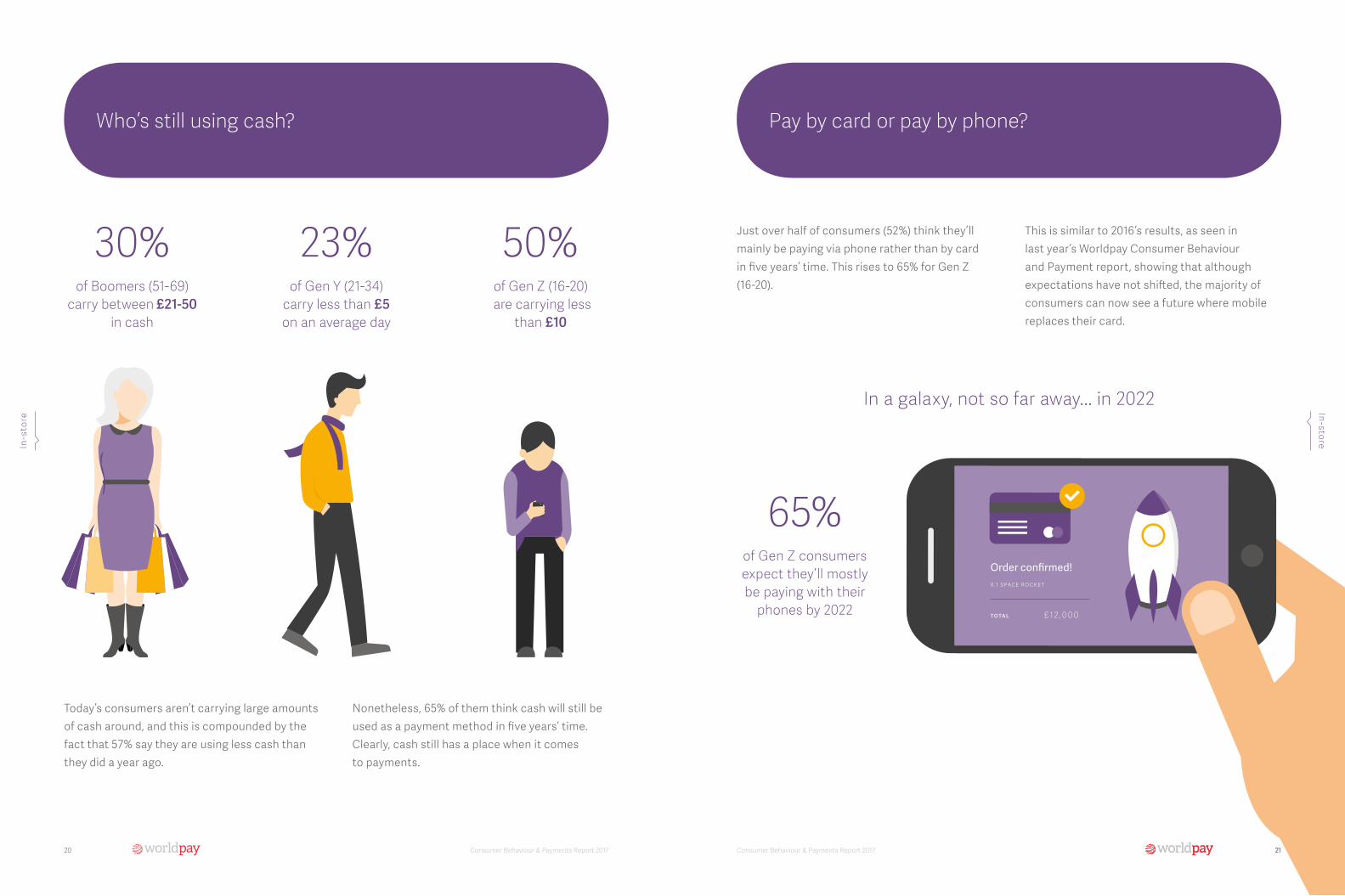

30%of Boomers (51-69)

carry between £21-50 in cash

23%of Gen Y (21-34)

carry less than £5 on an average day

50%of Gen Z (16-20)

are carrying less than £10

21

Who’s still using cash? Pay by card or pay by phone?

Just over half of consumers (52%) think they’ll mainly be paying via phone rather than by card in five years’ time. This rises to 65% for Gen Z (16-20).

This is similar to 2016’s results, as seen in last year’s Worldpay Consumer Behaviour and Payment report, showing that although expectations have not shifted, the majority of consumers can now see a future where mobile replaces their card.

Today’s consumers aren’t carrying large amounts of cash around, and this is compounded by the fact that 57% say they are using less cash than they did a year ago.

Nonetheless, 65% of them think cash will still be used as a payment method in five years’ time. Clearly, cash still has a place when it comes to payments.

In-s

tore

In-store

22 23Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

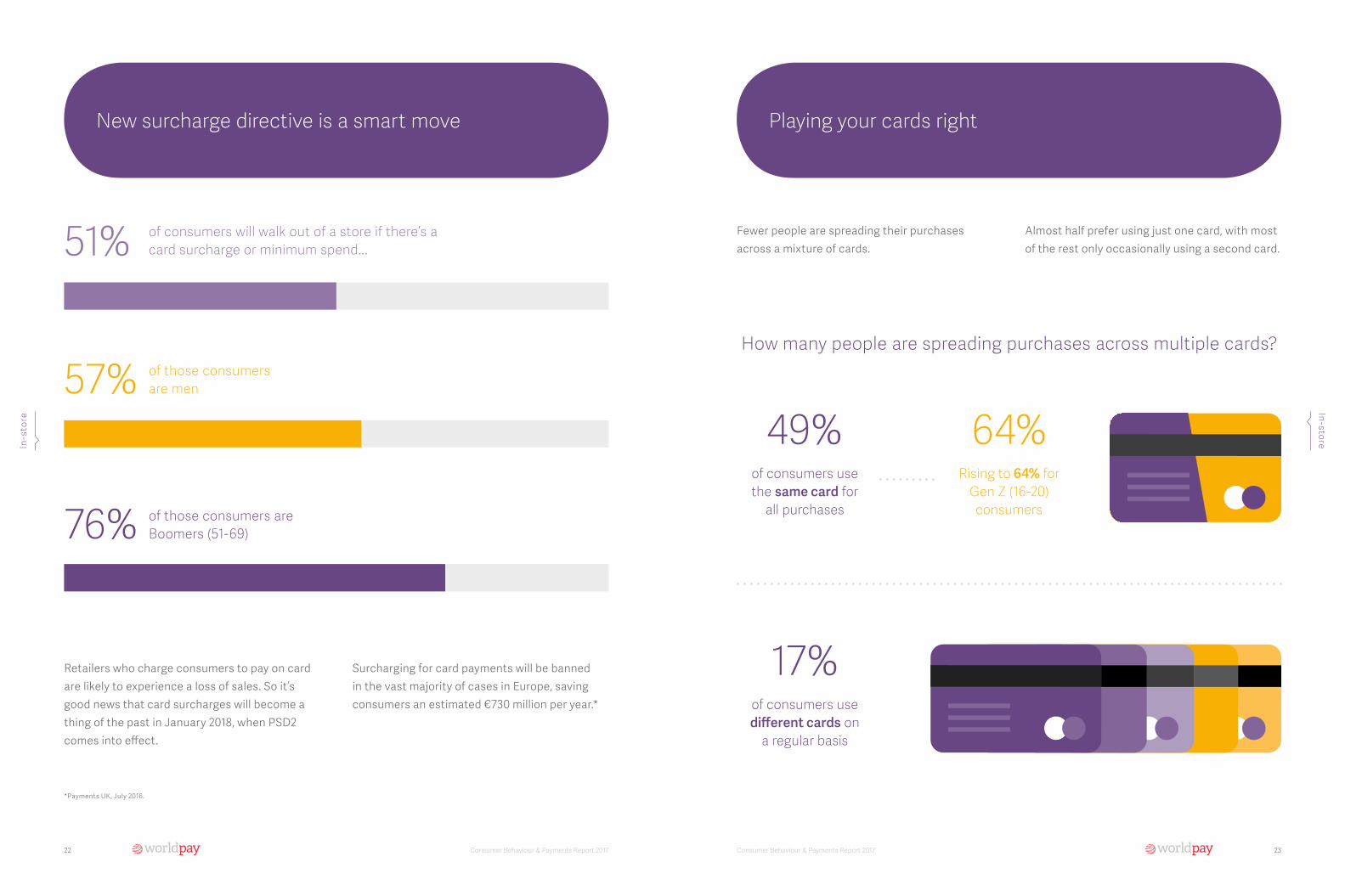

76%

57%

51% of consumers will walk out of a store if there’s a card surcharge or minimum spend...

of those consumers are men

of those consumers are Boomers (51-69)

How many people are spreading purchases across multiple cards?

17%of consumers use different cards on

a regular basis

49%of consumers use the same card for

all purchases

64%Rising to 64% for

Gen Z (16-20) consumers

New surcharge directive is a smart move Playing your cards right

Retailers who charge consumers to pay on card are likely to experience a loss of sales. So it’s good news that card surcharges will become a thing of the past in January 2018, when PSD2 comes into effect.

Surcharging for card payments will be banned in the vast majority of cases in Europe, saving consumers an estimated €730 million per year.*

Fewer people are spreading their purchases across a mixture of cards.

Almost half prefer using just one card, with most of the rest only occasionally using a second card.

In-s

tore

In-store

*Payments UK, July 2016.

24 25Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

of consumers would prefer emailed receipts

to paper receipts if given the choice

61+39M61%

30%of consumers have made a contactless payment with their

smartphone

75%prefer to make

contactless payments with their credit or

debit card

Cards still trump mobile Should receipts go digital?

Contactless has come a long way, and it’s now seen as a safe and reliable form of payment. 65% of consumers would be happy to make a contactless payment up to £50 on their card, including 71% of Gen Y (21-34).

But people are not yet in the habit of using their phones to make payments, although we expect this will change over time as phone payments become more commonplace and eventually, the norm. As we saw earlier (p21), most consumers think their phone will be their main method of payment in five years’ time.

With an estimated 11.2 billion paper receipts printed in the UK each year, at a cost of around £32 million, many businesses are looking at ways to provide an eco-friendly alternative.* Some retailers have already started offering electronic digital receipts instead, although the

challenge is in finding the easiest way to issue them. Retailers offering native apps, where customers can order and pay through their phone at the point of sale, make digital receipts a cinch.

In-s

tore

In-store

*Web Expenses, 2017.

26 27Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

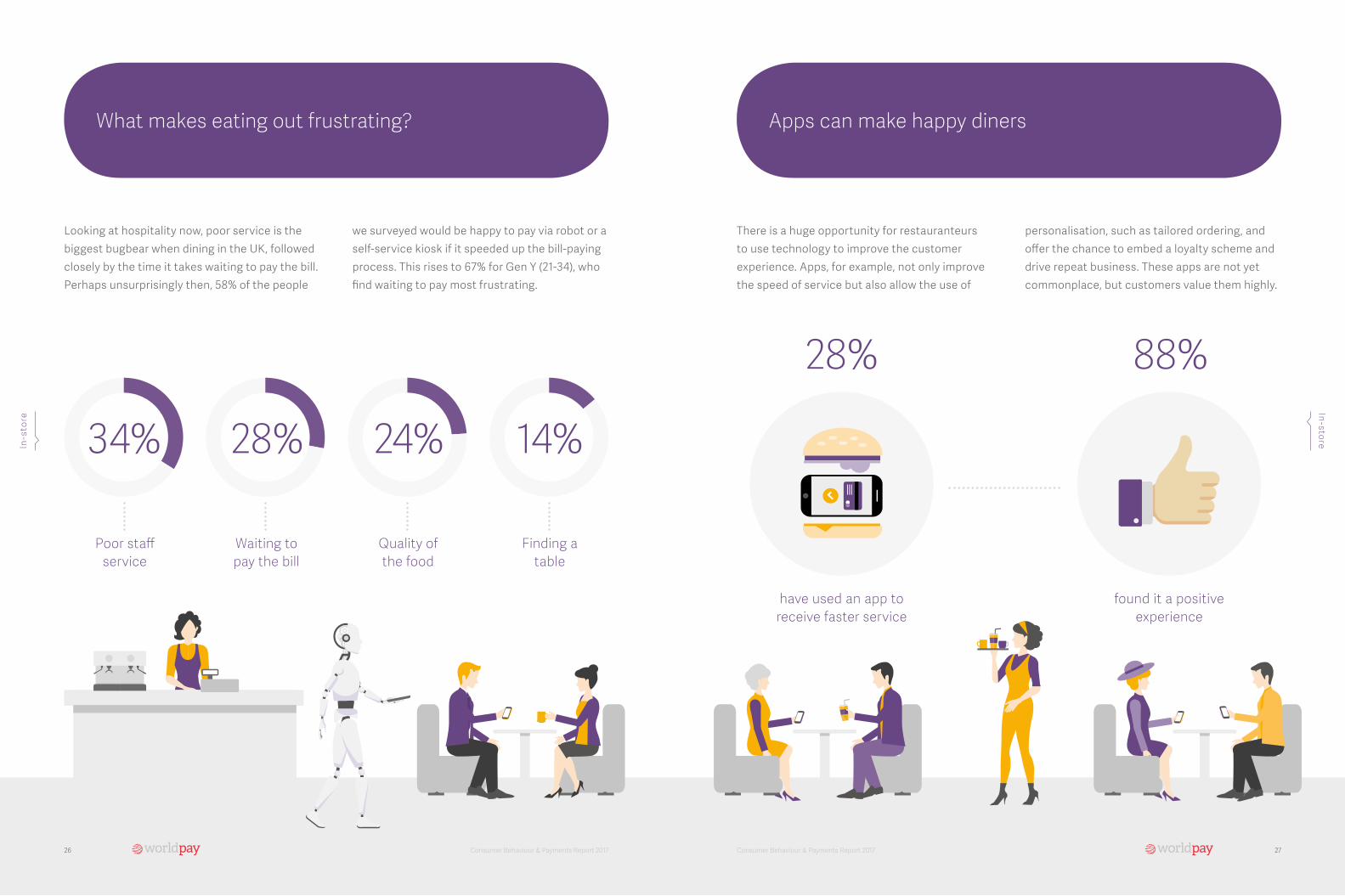

88%28%

have used an app to receive faster service

found it a positive experience

Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017 2726

28+72M

What makes eating out frustrating? Apps can make happy diners

34+66M 24+76M14+86MPoor staff

serviceWaiting to pay the bill

Quality ofthe food

Finding atable

34% 28% 24% 14%

Looking at hospitality now, poor service is the biggest bugbear when dining in the UK, followed closely by the time it takes waiting to pay the bill. Perhaps unsurprisingly then, 58% of the people

we surveyed would be happy to pay via robot or a self-service kiosk if it speeded up the bill-paying process. This rises to 67% for Gen Y (21-34), who find waiting to pay most frustrating.

There is a huge opportunity for restauranteurs to use technology to improve the customer experience. Apps, for example, not only improve the speed of service but also allow the use of

personalisation, such as tailored ordering, and offer the chance to embed a loyalty scheme and drive repeat business. These apps are not yet commonplace, but customers value them highly.

In-s

tore

In-store

28 29Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

of consumers would be interested in a payment plan

offered at point of sale, enabling them to easily spread the cost of

expensive items

59+41M59%31%have been

offered to pay this way

80%found it

helped them get what

they wanted

69%described

it as personally engaging

70%got a better service and information

2928

Customers appreciate assisted selling, although it remains a rarity

Flexible payment plans get the thumbs-up from younger consumers

Assisted selling has a number of advantages for retailers. When sales assistants offer the chance to pay from anywhere in-store via mobile card machine, customers get a more personalised service. They are able to get information and purchase products they need more easily.

Missed sales can be reduced, even if items are out of stock, as they can be ordered by assistants at the point of sale. However, it’s not yet a widespread practice, despite the benefits to both customers and retailers.

The most obvious scenario for this type of purchase would be a high-value item, with the customer opting to pay in instalments at the point of sale via the card machine.

When this option is offered online - a service that’s already on the market - a higher 61% of customers would be interested.

Consumers are clearly receptive to such a service both in-store and online, although 63% are not happy to pay more for it.

However, around half of those surveyed in the most receptive age groups (Gens Y and Z, 16-34) are willing to pay a little bit extra for a product if they can pay in instalments.

In-s

tore

In-store

30 31Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

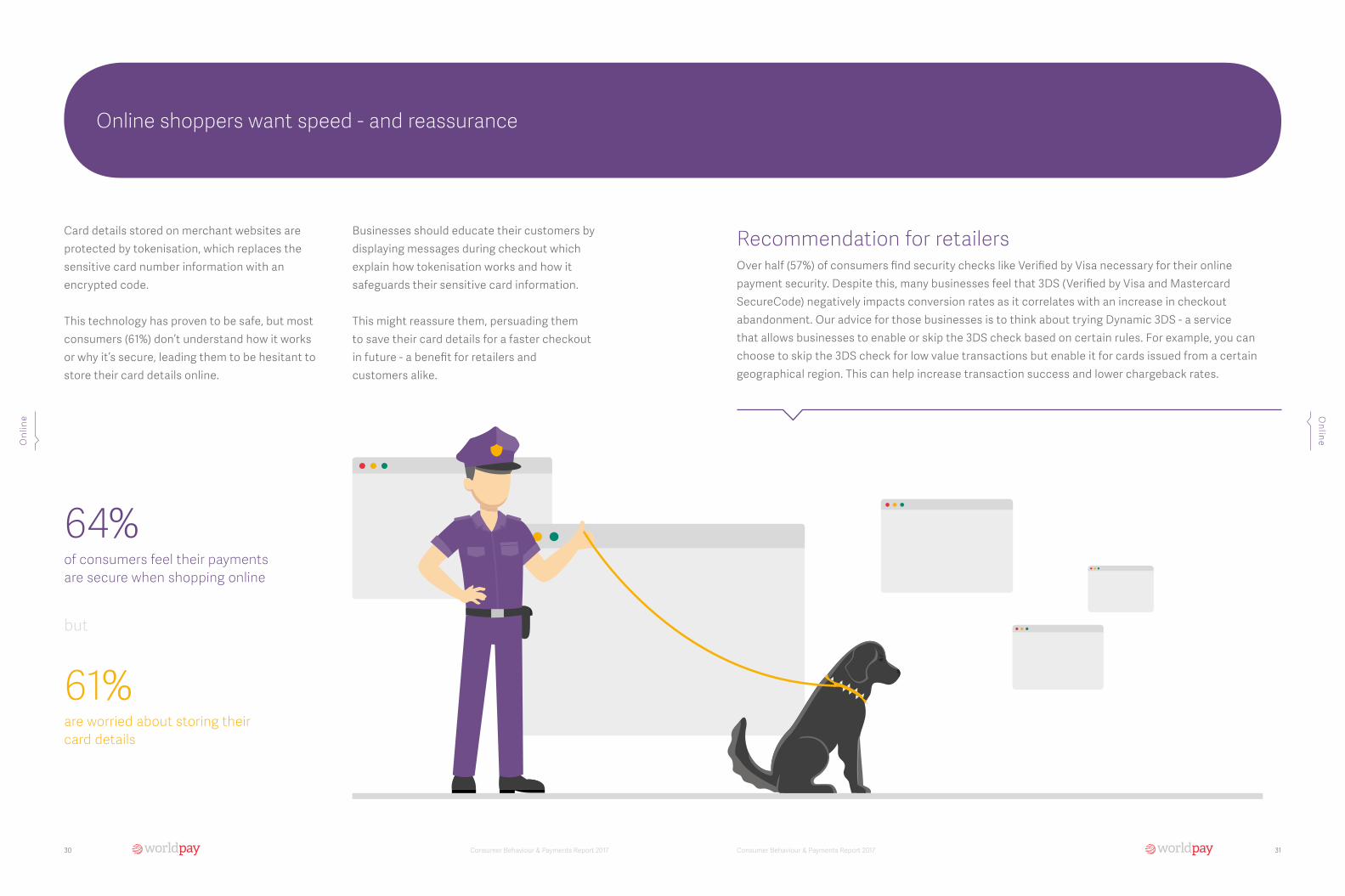

of consumers feel their payments are secure when shopping online

64%

are worried about storing their card details

61%

but

Online shoppers want speed - and reassurance

Card details stored on merchant websites are protected by tokenisation, which replaces the sensitive card number information with an encrypted code. This technology has proven to be safe, but most consumers (61%) don’t understand how it works or why it’s secure, leading them to be hesitant to store their card details online.

Businesses should educate their customers by displaying messages during checkout which explain how tokenisation works and how it safeguards their sensitive card information. This might reassure them, persuading them to save their card details for a faster checkout in future - a benefit for retailers and customers alike.

Recommendation for retailersOver half (57%) of consumers find security checks like Verified by Visa necessary for their online payment security. Despite this, many businesses feel that 3DS (Verified by Visa and Mastercard SecureCode) negatively impacts conversion rates as it correlates with an increase in checkout abandonment. Our advice for those businesses is to think about trying Dynamic 3DS - a service that allows businesses to enable or skip the 3DS check based on certain rules. For example, you can choose to skip the 3DS check for low value transactions but enable it for cards issued from a certain geographical region. This can help increase transaction success and lower chargeback rates.

Onl

ine O

nline

32 Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017 33

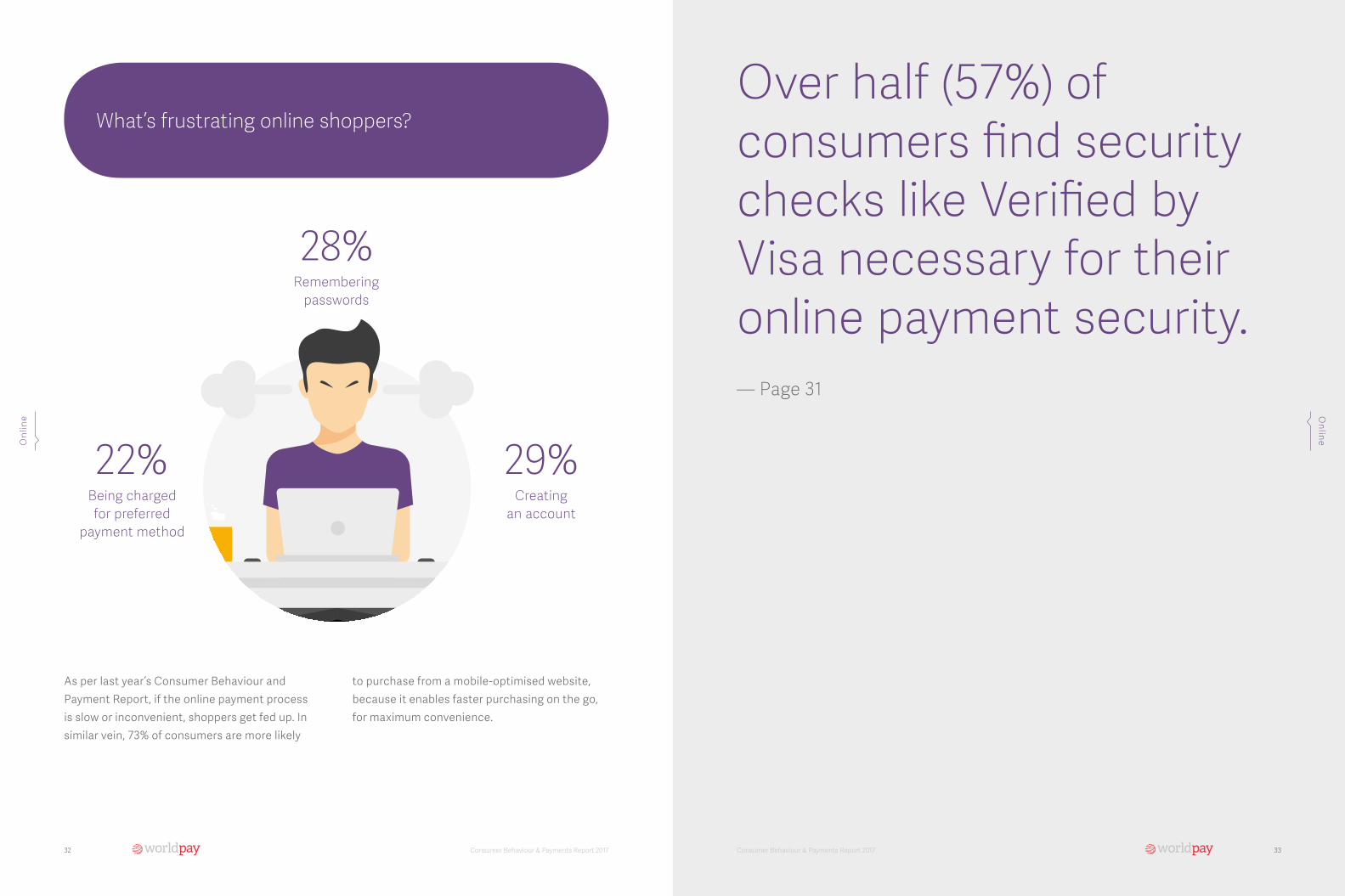

29%22%

28%Remembering

passwords

Being charged for preferred

payment method

Creating an account

What’s frustrating online shoppers?

As per last year’s Consumer Behaviour and Payment Report, if the online payment process is slow or inconvenient, shoppers get fed up. In similar vein, 73% of consumers are more likely

to purchase from a mobile-optimised website, because it enables faster purchasing on the go, for maximum convenience.

Onl

ine O

nline

Over half (57%) of consumers find security checks like Verified by Visa necessary for their online payment security. — Page 31

34 Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017 35

Security & identity Emerging security trends point towards what could be next.

36 Consumer Behaviour & Payments Report 2017

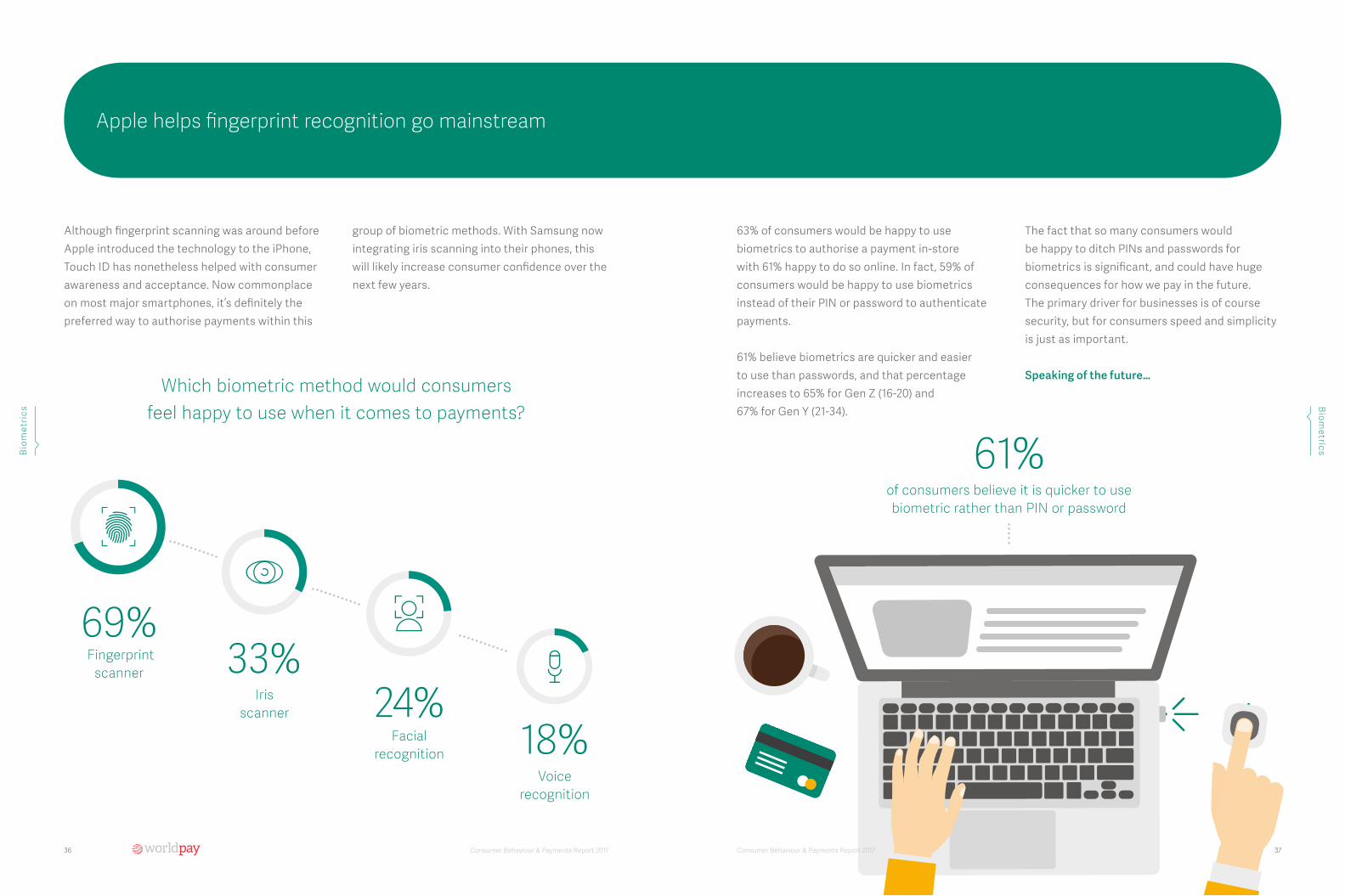

69+3169% 33+67

33% Fingerprint scanner

Iris scanner

24+7624%

Facial recognition

18+8218%

Voice recognition

Which biometric method would consumers feel happy to use when it comes to payments?

61%of consumers believe it is quicker to use biometric rather than PIN or password

37

Apple helps fingerprint recognition go mainstream

Although fingerprint scanning was around before Apple introduced the technology to the iPhone, Touch ID has nonetheless helped with consumer awareness and acceptance. Now commonplace on most major smartphones, it’s definitely the preferred way to authorise payments within this

group of biometric methods. With Samsung now integrating iris scanning into their phones, this will likely increase consumer confidence over the next few years.

63% of consumers would be happy to use biometrics to authorise a payment in-store with 61% happy to do so online. In fact, 59% of consumers would be happy to use biometrics instead of their PIN or password to authenticate payments.

61% believe biometrics are quicker and easier to use than passwords, and that percentage increases to 65% for Gen Z (16-20) and 67% for Gen Y (21-34).

The fact that so many consumers would be happy to ditch PINs and passwords for biometrics is significant, and could have huge consequences for how we pay in the future. The primary driver for businesses is of course security, but for consumers speed and simplicity is just as important. Speaking of the future…

Bio

met

rics

Biom

etrics

Consumer Behaviour & Payments Report 2017

38 39Consumer Behaviour & Payments Report 2017 Consumer Behaviour & Payments Report 2017

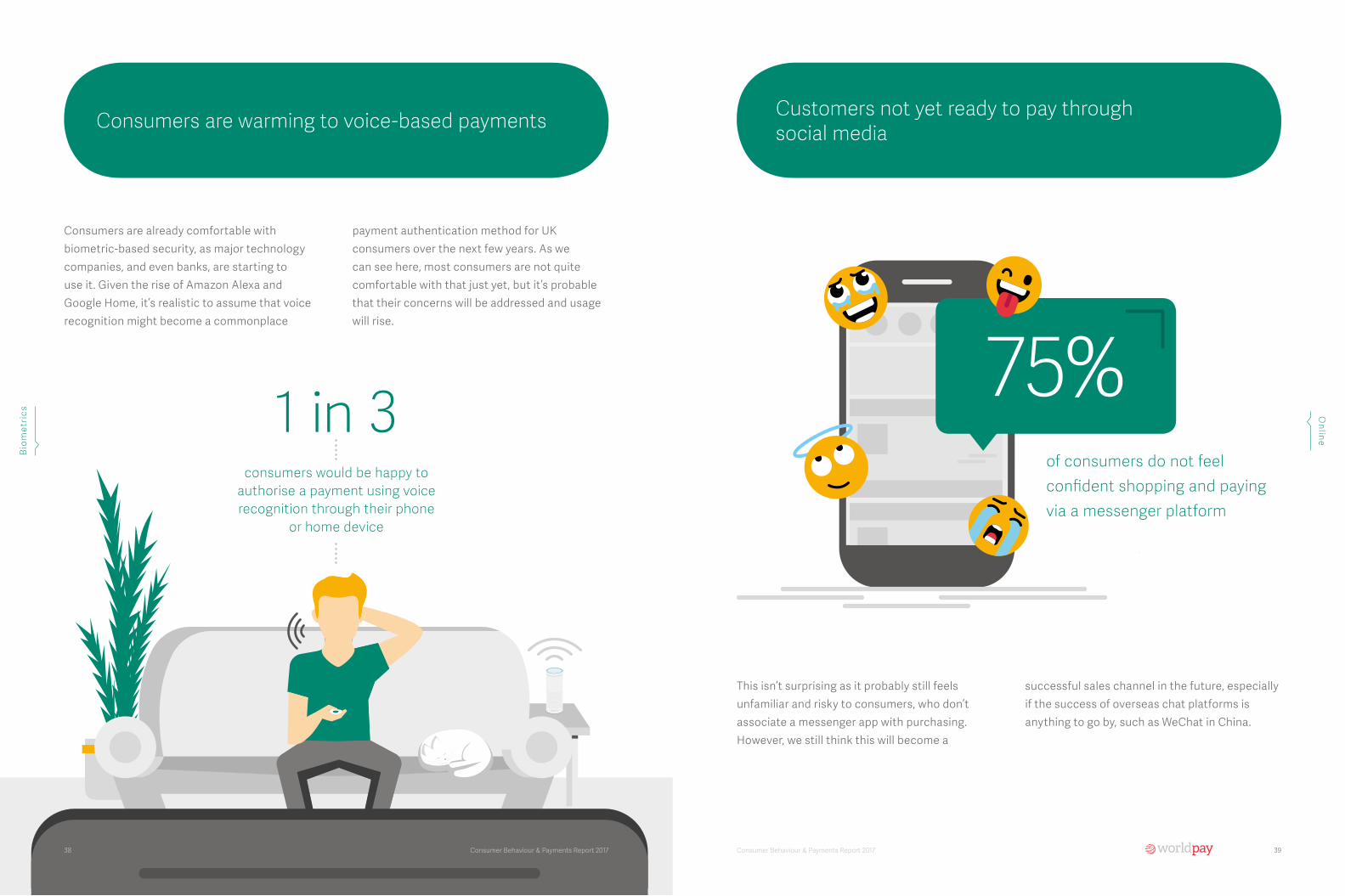

of consumers do not feel confident shopping and paying via a messenger platform

75%1 in 3consumers would be happy to

authorise a payment using voicerecognition through their phone

or home device

Consumers are warming to voice-based payments Customers not yet ready to pay through social media

Consumers are already comfortable with biometric-based security, as major technology companies, and even banks, are starting to use it. Given the rise of Amazon Alexa and Google Home, it’s realistic to assume that voice recognition might become a commonplace

payment authentication method for UK consumers over the next few years. As we can see here, most consumers are not quite comfortable with that just yet, but it’s probable that their concerns will be addressed and usage will rise.

Bio

met

rics

O

nline

This isn’t surprising as it probably still feels unfamiliar and risky to consumers, who don’t associate a messenger app with purchasing.However, we still think this will become a

successful sales channel in the future, especially if the success of overseas chat platforms is anything to go by, such as WeChat in China.

38 Consumer Behaviour & Payments Report 2017

40 Consumer Behaviour & Payments Report 2017

Discover Worldpay

Keytakeaways

Worldpay is one of the world’s leading payments providers. Driven by technology, our products and services are used by around 400,000 customers around the globe, allowing them to accept more than 300 different payment types from 146 countries and 126 currencies, helping their businesses flourish.

Worldpay enables businesses large and small to take card payments in-store, online, via telephone and on the move.

Find out more at: www.worldpay.com/uk/larger-businesses

Key

tak

eaw

ays

Store employees are more important than ever, with many consumers feeling that they genuinely enhance the customer experience. However, retailers must revise their role, focusing on how they interact and engage customers across the store, from service to payment.

1 Consumers want flexibility from brands, not only on which channel they pay through, but on how they pay as well. Instalment-based payment is something that consumers are receptive to, allowing them to spread the cost of larger payments without the need for finance.

4

Today’s impatient consumers prioritise speed and convenience when they shop and pay in-store and online - but they’re reluctant to pay extra for it. Surcharges and other price ‘add ons’, such as a premium for Click and Collect won’t wash with today’s consumers.

2 There is still uncertainty around the security of storing card details online. This in turn makes it harder to provide consumers with that all-important speedy checkout, as details have to be re-entered each time. By explaining to shoppers how they are protecting customer details, businesses can help alleviate their concerns.

5

Phones and apps are the future of payment, enabled by biometric security, but the mobile payment experience is still not what it could be. The potential for brands to connect with consumers and integrate loyalty is significant but in reality few have mastered it.

3

41Consumer Behaviour & Payments Report 2017

43Consumer Behaviour & Payments Report 2017Consumer Behaviour & Payments Report 201742 Consumer Behaviour & Payments Preference Report 43

© Worldpay 2017. All rights reserved.This document and its content are proprietary to Worldpay and may not be reproduced, published or resold. The information is provided on an “as is” basis for information purposes only. Worldpay makes no warranties of any kind in relation to the content. Terms and conditions apply to all services. Worldpay (UK) Limited (Company No. 07316500 / FCA No. 530923), Worldpay Limited (Company No. 03424752 / FCA No. 504504), Worldpay AP Limited (Company No. 05593466 / FCA No. 502597). Registered Office: The Walbrook Building, 25 Walbrook, London EC4N 8AF and authorised by the Financial Conduct Authority under the Payment Service Regulations 2009 for the provision of payment services. Worldpay (UK) Limited is authorised and regulated by the Financial Conduct Authority for consumer credit activities. Worldpay B.V. (WPBV) has its registered office in Amsterdam, the Netherlands (Handelsregister KvK no. 60494344). WPBV holds a licence from and is included in the register kept by De Nederlandsche Bank, which registration can be consulted through www.dnb.nl. Worldpay, the logo and any associated brand names are all trademarks of the Worldpay group of companies.

See how Worldpay can make payments work smarter for your business

Visit: www.worldpay.com/uk/larger-businessesCall us: 0808 301 9517