Embed Size (px)

Citation preview

SWP-603Worldwide Investment Analysis

The Case of Aluminum

Martin BrownAlfredo Dammert

Alexander MeerausArdy Stoutjesdijk

WORLD BANK STAFF WORKING PAPERSNumber 603

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

WORLD BANK STAFF WORKING PAPERSNumber 603

Worldwide Investment AnalysisThe Case of Aluminum

Martin BrownAlfredo Dammert

Alexander MeerausArdy Stoutjesdijk

The World BankWashington, D.C., U.S.A.

Copyright (© 1983

The Intemational Bank for Reconstructionand Development/THE WORLD BANK

1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing July 1983Second printing January 1985

This is a working document published informally by the World Bank. To present theresults of research with the least possible delay, the typescript has not been preparedin accordance with the procedures appropriate to formal printed texts, and the WorldBank accepts no responsibility for errors. The publication is supplied at a token chargeto defray part of the cost of manufacture and distribution.

The World Bank does not accept responsibility for the views expressed herein, whichare those of the authors and should not be attributed to the World Bank or to itsaffiliated organizations. The findings, interpretations, and conclusions are the resultsof research supported by the Bank; they do not necessarily represent official policy ofthe Bank. The designations employed, the presentation of material, and any maps usedin this document are solely for the convenience of the reader and do not imply theexpression of any opinion whatsoever on the part of the World Bank or its affiliatesconcerning the legal status of any country, territory, city, area, or of its authorities, orconcerning the delimitation of its boundaries, or national affiliation.

The full range of World Bank publications, both free and for sale, is described in theCatalog of Publications; the continuing research program is outlined in Abstracts ofCurrent Studies. Both booklets are updated annually; the most recent edition of each isavailable without charge from the Publications Sales Unit, Department T, The WorldBank, 1818 H Street, N.W, Washington, D.C. 20433, U.S.A., or from the EuropeanOffice of the Bank, 66 avenue d'I6na, 75116 Paris, France.

When this paper was first published Martin Brown was an economist with theOrganisation for Economic Cooperation and Development; Alfredo Dammert was aneconomist in the Economic Analysis and Projections Department of the World Bank;Alexander Meeraus was chief of the Analytic Support Unit in, and Ardy Stoutjesdijkdirector of, the Bank's Development Research Department.

Library of Congress Cataloging in Publication Data

Worldwide investment analysis.

(World Bank staff working papers ; no. 603)Bibliography: p.Includes index.1. Aluminum industry and trade. 2. Metals as an

investment. I. Brown, Martin S. II. World Bank.III. Series.ED9539.A6W68 1983 338.2'3 83-101T2ISBN 0-8213-0212-8

Abstract

This study focuses on the likely long-term trends in investment,production and trade patterns in the world aluminum industry. It firstintroduces the non-specialist reader to the technical characteristics ofbauxite mining and the production of alumina and aluminum. Special emphasisis placed on the critical importance of energy requirements. Next, a verbaldescription of the method of analysis is presented. A detailed technicalstatement of the mathematical programming model, and the associated data inputare provided in two annexes to the study.

The results obtained are mostly of a normative nature rather thanpredictions. Therefore, tariffs and levies are not considered in mostscenarios. Extensive sensitivity analysis is carried out, focusing on analternative demand forecast, higher capital costs, varying cost andavailability of electricity, and different trade strategies. In that context,an attempt is made to determine the impact of tariffs and levies.

The main conclusion drawn from the analysis is that the emergingpattern of investment, production and trade is very robust in the light of thechanges that were made in the main parameters, particularly for bauxite andaluminum. The abundance of relatively accessible bauxite and low-costelectricity from hydrosources and natural gas in many developing countriesappears to have caused a noticeable shift in comparative advantage, in thesense that most of the required additional productive capacity for bauxite,alumina and aluminum would be located there in the future. However, Australiais under certain circumstances an attractive location for bauxite productionand processing activities while Canada, due to its abundant hydroelectricresources, shows potential for additional aluminum smelter capacity.Furthermore, considering the expected long-term conditions, already installedplants in OECD countries could remain competitive, as long as they are able tosurvive through the current depressed situation of the industry.

Most alumina and aluminum plants in OECD countries will continueoperating for two main reasons. First, capital expenditures have already beenmade, thus representing a sunk cost, and additional investment requirements tomodernize and increase efficiency of these plants are low compared to the costof establishing new plants. By contrast, new investments in developingcountries require not only expenditures for plant and equipment but also forinfrastructure development. Second, although electricity costs for newprojects may be significantly lower in the developing countries with cheapenergy sources, they are significantly higher than before. Moreover, long-term contracts on low-cost electricity supplies for existing smelters and thepossibility of generating medium-cost electricity from coal and nuclear powershould moderate the difference in electricity costs among regions. Therefore,although new aluminum projects implemented in the regions with low costelectricity may result in energy cost savings over some existing smelters,these savings may not compensate for the capital costs which would be incurredin developing the new projects and building the required infrastructure.

Contents

Page

Preface

1. Introduction ......... ............................... 1

1.1 Approach and Aims of the Analysis .... ......... 11.2 Organization of the Study ..................... 2

2. The Aluminum Sector ................................. 3

2.1 General Overview ...... ........................ 32.2 Bauxite Deposits and Characteristics . . 62.3 Alumina Refining .............................. 112.4 Aluminum Smelting ............................. 13

3. Data and Assumptions ................................ 16

3.1 Forecasting the Demand for Aluminum .... ....... 163.2 Investment and Operating Costs for Bauxite .... 203.3 Investment and Operating Costs for Alumina .... 253.4 Investment and Operating Costs for Aluminum,

Including Energy Costs ...................... 323.5 Transport Costs ............................... 413.6 Taxation Policies of Bauxite Producing

Countries ........ . . .......................... 483.7 Import Tariffs on Bauxite, Alumina

and Aluminum ................................ 51

4. Framework of Analysis ............................... 57

4.1 Problem Formulation ........................... 574.2 A Model of the Aluminum Sector .... ............ 584.3 Uses and Limitations .. ........................ 59

5. Results .................. ........................... 61

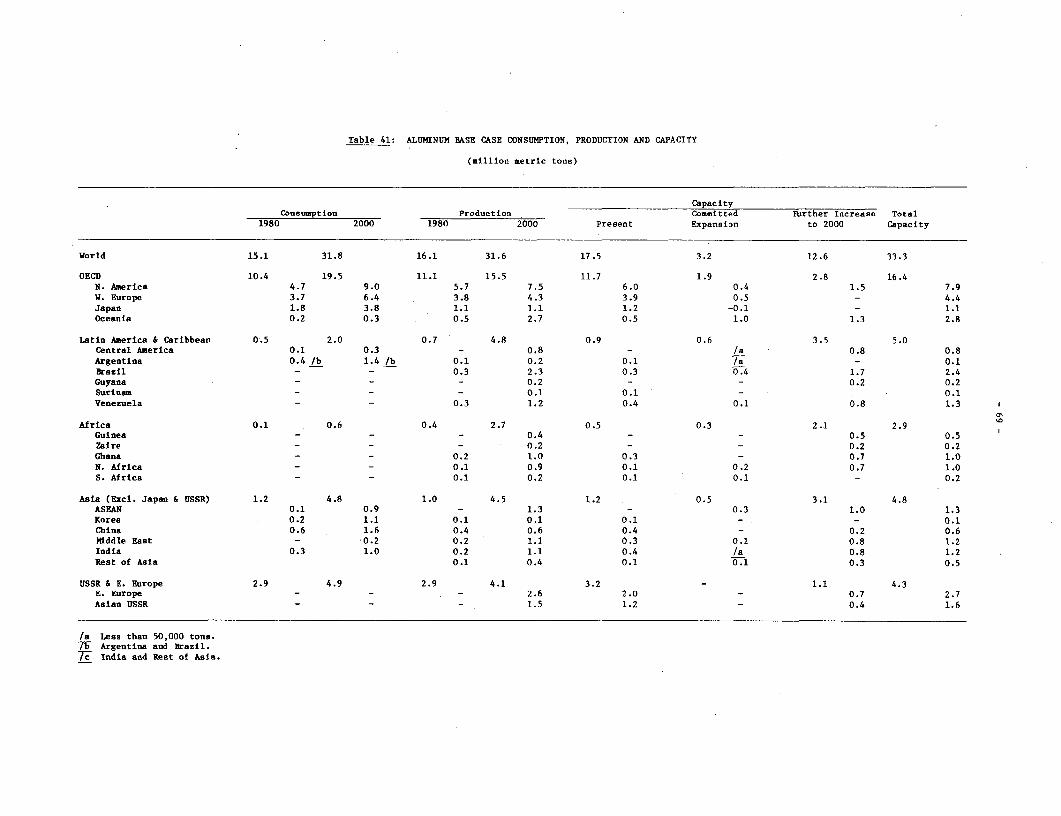

5.1 The Base Case: Low Demand ..... ............... 615.2 Sensitivity Analysis .......................... 745.3 The Impact of Tariffs & Levies .... ............ 84

6. Conclusions ......... ................................ 91

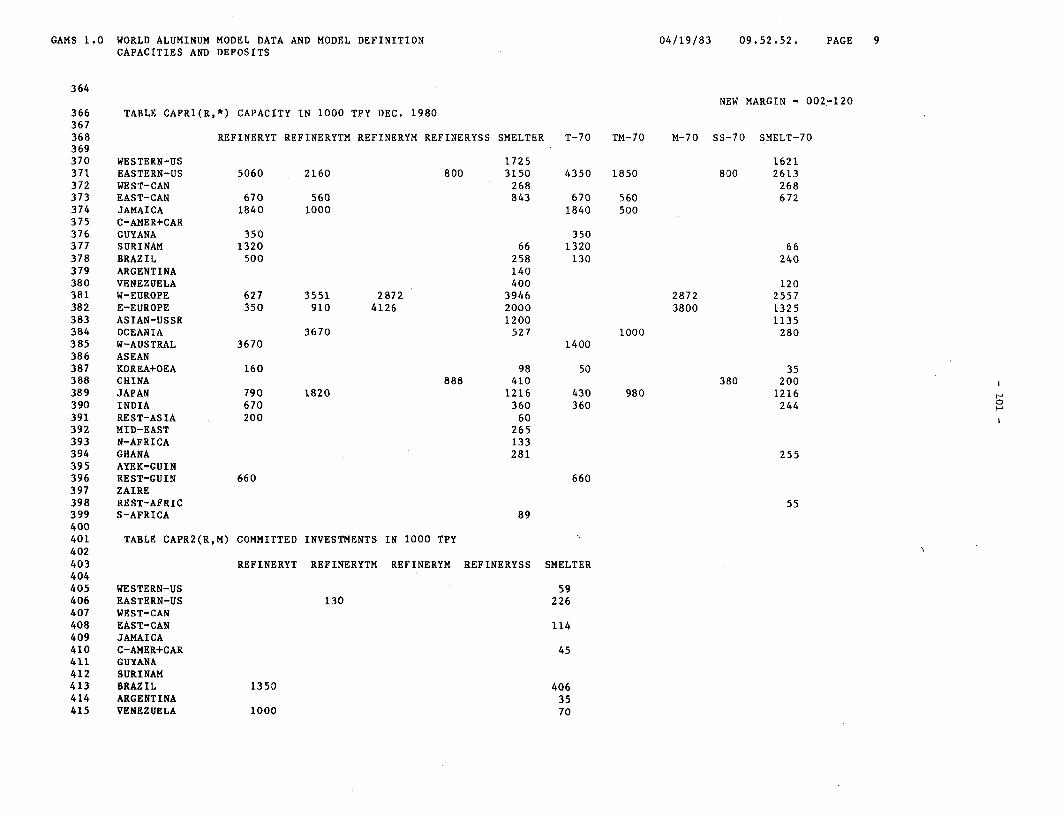

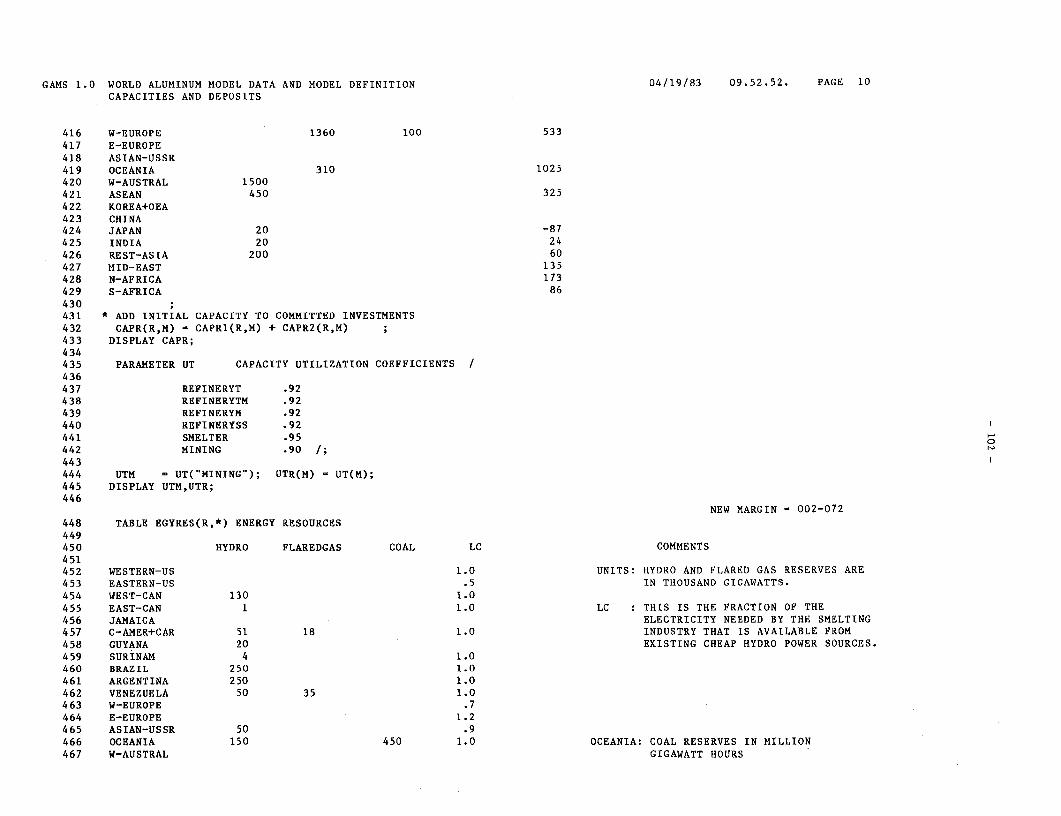

Annex 1 Computer Printout for the World Aluminum Model .93

Annex 2 A Mathematical Statement of the World AluminumModel .. 148

Bibliography .166

Text Tables

1. Characteristics of Bauxite Deposits .... ............. 9

2. Consumption of Aluminum by End Uses, 1980 ........... 15

3. Estimates of Aluminum Consumption - High Case ....... 17

4. Estimates of Aluminum Consumption - Low Case ........ 18

5. Regional Breakdown for Aluminum Consumption ......... 19

6. Estimates of Bauxite Production for Non-MetalUses, 1980 .21

7. Estimate of Alumina Production for Non-MetalUses, 1980 ........ ............................... 21

8. Capital Cost for Mines .............................. 22

9. Location Factors for Mine Capital Costs .... ......... 23

10. Operating Costs for Bauxite Mining, Year 2000 ....... 24

11. Total Costs of Bauxite Production, Year 2000 ........ 26

12. Capital Cost for Alumina Refineries .... ............. 27

13. Location Factors for Capital Costs forRefineries (IFR) and Smelters (IFS) .28

14. Alumina Refineries: Processing and InputRequirements for Selected Bauxites .29

15. Prices of Inputs for Alumina Refining,1980, Excluding Labor ................... ........ 30

16. Labor Costs at Alumina Refineries ... ................ 30

17. Production Costs for Alumina, Selected Sites,Year 2000 . .......................................... 31

18. Capital Cost for Smelters ........................... 33

19. Inputs for Aluminum Smelters ........................ 34

20. Prices of Other Inputs at Aluminum Smelters ......... 36

21. Cost of Electric Power for Aluminum Smelters(Costed at Generating Sites) ..... ................ 37

22. Undeveloped Energy Resources ........................ 22

23. Electricity Supplies Available for AluminumSmelting .......... ............................... 39

24. Aluminum Production Costs at Selected Sites,Year 2000 (New Plants) .............................. 40

25. Estimated Average Distances from BauxiteMines to Ports and Local Refineries.. . 42

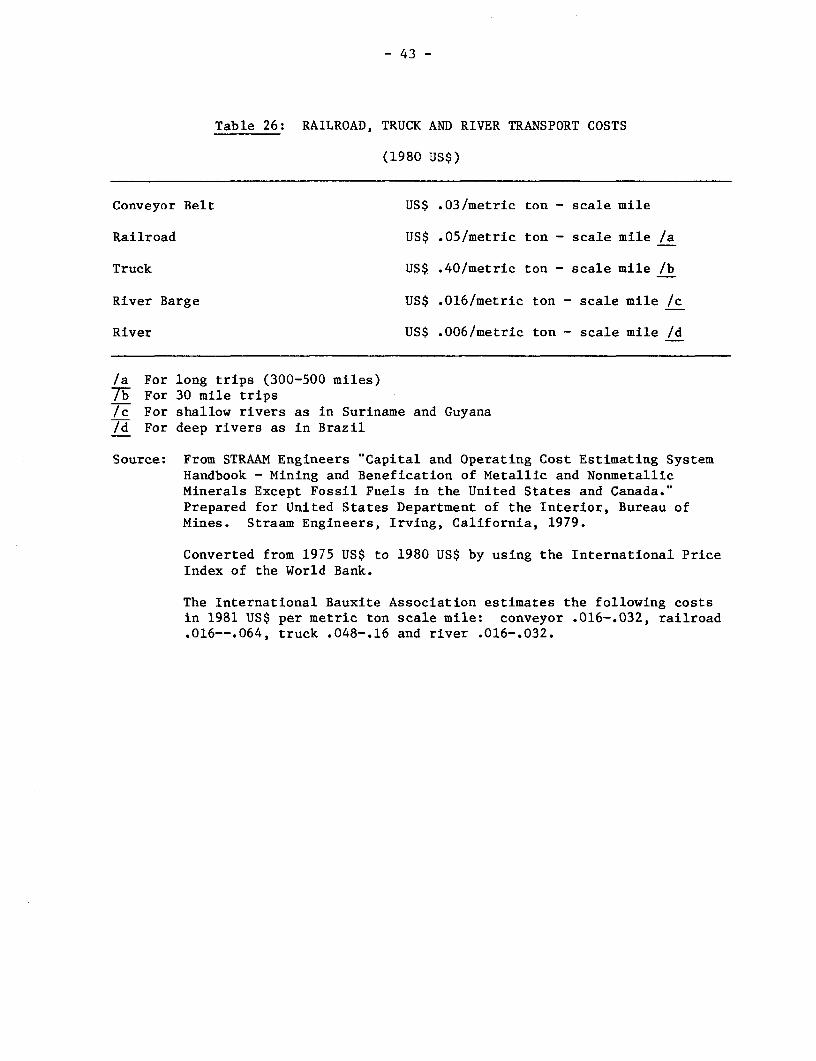

26. Railroad, Truck and River Transport Costs . . .43

27. Ocean Transport Costs . . 45

28. Maximum Vessel Size at Each Port .. .46

29. Taxation Systems in the Bauxite Sector .. .49

30. Income Tax Calculations for New Projects . . .52

31. Levy Calculations - Bauxite. 53

32. Levy Calculations - Bauxite and AluminaIntegrated Operation .53

33. Tariffs on Bauxite and Alumina Imports .. .54

34. Tariffs on Aluminum Imports .. .55

35. Effect of Import Duties on Aluminum:Cost of Delivered Aluminum from New Plants,Year 2000 ......... ............................... 56

36. Existing and New Capacity, 2000, Bauxite Mining,Alumina Refining, and Aluminum Smelting .......... 62

37. Nominal Capacity and Production, Low Demand,2000, Bauxite, Alumina, Aluminum ................. 63

38. Production and Destination of Bauxite, Aluminaand Aluminum, 2000 (Low Demand); ExcludingNon-Metal Uses ................................... 64

39. Bauxite Mining: Base Case Production andCapacity Expansion, 2000 ...... ................... 67

40. Alumina Base Case Production, CapacityExpansion and Consumption in 2000 .............. .. 68

41. Aluminum Base Case Consumption, Productionand Capacity .... 69

42. Bauxite: Base Case Trade Flows in 2000 .70

.,~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

43. Alumina Base Case: Trade Flows in 2000 .... .......... 71

44. Aluminum: Trade Flows in the Base Case, 2000 ....... 72

45. Cost Elements for the Base Case - Low Demand,No Levies or Tariffs .............................. 73

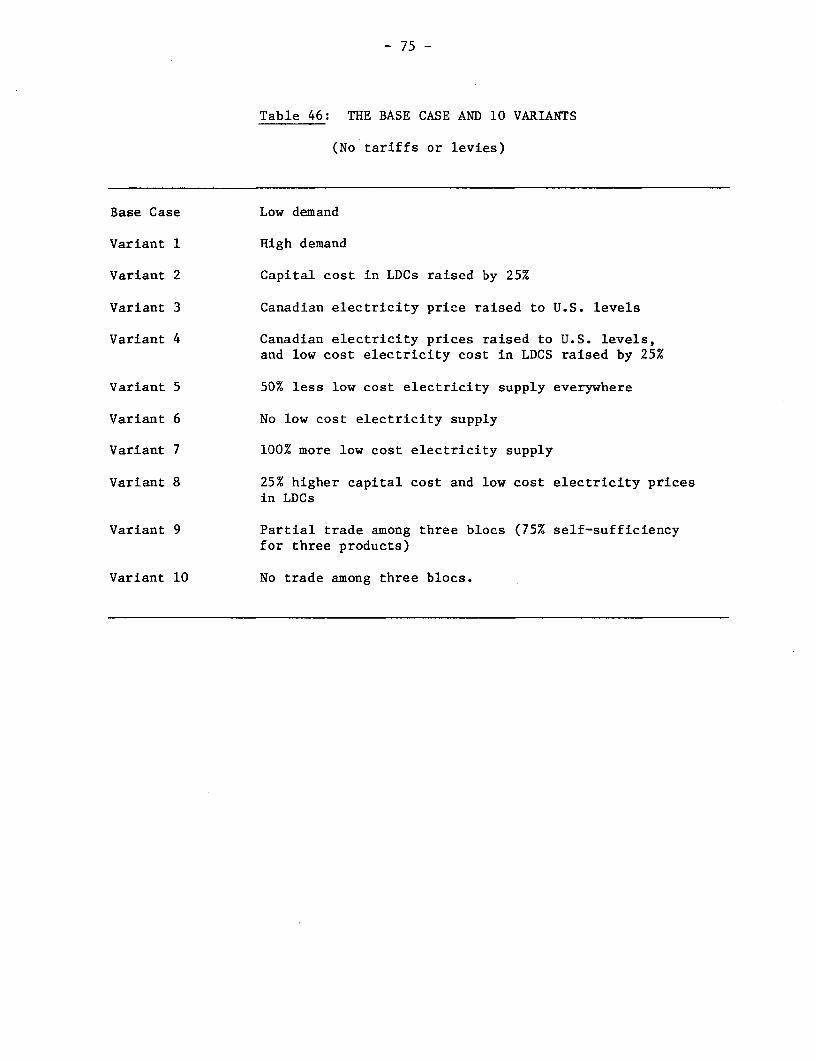

46. The Base Case and Ten Variants ....................... 75

47. Production Levels: The Base Case andTen Variants, 2000 ................................ 76

48. Costs: Ten Variants of the Base Case .... ............ 79

49. Bauxite Mining: Capacity Expansion Summary .... ...... 80

50. Alumina: Capacity Expansion Summary .... ............. 81

51. Aluminum: Capacity Expansion Summary .... ............ 82

52. Capacity Expansion with and WithoutTariffs and Levies 1980-2000 .85

53. Bauxite Capacity Expansion 1980-2000,Variant with Tariffs and Levies .86

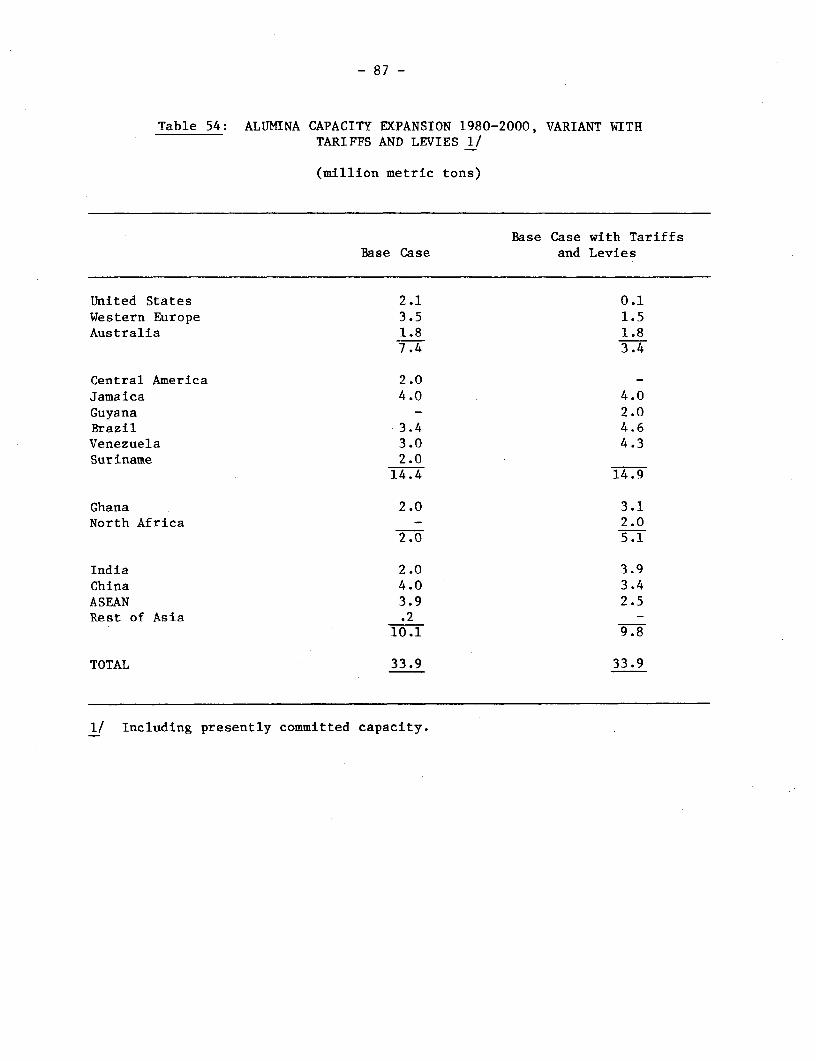

54. Alumina Capacity Expansion 1980-2000,Variant with Tariffs and Levies .87

55. Aluminum Capacity Expansion 1980-2000,Variant with Tariff and Levies .88

56. Costs of the Base Case, With andWithout Tariffs and Levies .90

Text Figures

1. Plants and Products of the Aluminum Industry 4

Preface

This is a study that the World Bank and the OECD have conductedfocusing on possible shifts in comparative advantage in the aluminum sector.While emphasizing the preliminary nature of our results, we gratefullyacknowledge the advice and assistance that we have received from industryspecialists. Mr. Richard C. Roberts, consultant, has provided us withconstant advice throughout the study, and has, in particular, helped usunderstand the technical and economic characteristics of the aluminumindustry, based upon a lifetime of practical experience.

We are also grateful to OECD for the opportunity to present anearlier version of this study to the Group of Delegates on the AluminumIndustry in Paris, November 1981. We received many important suggestions andcomments from industry representatives at that meeting and are especiallygrateful to ALCAN Aluminum Ltd. for subsequent detailed comments andcriticism.

One of the authors visited the International Bauxite Association inKingston, Jamaica several times during the study; we gratefully acknowledgethe help of the IBA staff, and would like to mention specifically Messrs. RobRobson, Paul Frame, Luke Baumgardner, Aldo Barsotti and Gary Peterson of theU.S. Bureau of Mines, who were very helpful. Professor Ebbe Yndgaard of theUniversity of Aarhus, Denmark, provided useful suggestions on the study.

Within the World Bank, we benefited from the assistance and commentsof several colleagues, in particular, Mrs. Marianne Haug, Messrs. KenjiTakeuchi, James Fish, Edwin Moore and John Strongman. We are grateful tothem. We are deeply indebted to Messrs. Piet Bleyendaal and Sethu Palaniappanfor their meticulous assistance in the numerical analysis.

I

1. Introduction

1.1 Approach and Aims of the Analysis

International discussions on the future structure of world industry,and concomitant trading patterns, have often not been based on systematicanalysis of comparative advantage. This is regrettable, as it may be assumedthat most of the important decisions with regard to future investment,production and trade patterns will continue to be heavily influenced by costconsiderations which are amenable to such analysis, rather than by target-setting by international agencies, or by arguments based upon some perceptionof equity as often expressed on behalf of the developing countries as a group.

At the same time, it should be recognized that the systematicanalysis of an industry, even if confined to a single industrial sub-sector,on a world-wide basis, is fraught with difficulties. First, and foremost, theestablishment of a good data base is a major undertaking. It is one thing toreach a certain degree of agreement on information that describes thetechnological characteristics of a given industrial activity, such as thespecification of input-output relationships. It is quite another thing toarrive at a consensus with regard to data that require a certain amount ofjudgment, such as the availability and quality of factors of production,future market requirements, investment costs, and so on. Finally, there arefactors which are difficult to quantify, or that can be quantified by proxyonly, mostly related to risk and uncertainty. Opinions may not only differwith regard to the nature of such factors and the weight to be attached tothem, but also to the appropriate manner of treatment.

In addition to severe data problems, difficulties arise with regardto the appropriate method of analysis. Some of us have described in detailthe complexities associated with sector-wide industrial investment analysis,even in a single country, and in particular, for industrial activities thatexhibit economies of scale. 1/ In fact, it is now commonly acknowledged thatone is dependent upon computerized manipulation of the data and assumptions ifone wishes to carry out systematic investment analysis that explicitly takesinto account interdependencies among decisions on timing, location, scale,technology and product mix of new productive investment. Clearly, if suchanalysis is difficult for a single country, it must cause serious problems inthe case of a world-wide analysis.

To assess the feasibility of a systematic analysis of an industry ona worldwide basis and achieve results that are meaningful from a policy pointof view, we have selected the world aluminum industry as the subject of a casestudy. From the start, we should emphasize that the objective of this studyis not to present a blueprint for the world-wide development of thisparticular industry, but that it is considerably more modest in its aims.

1/ See, for example, David Kendrick and Ardy Stoutjesdijk, The Planning ofIndustrial Investment Programs, Vol. 1 in: Alex Meeraus and Ardy

Stoutjesdijk (Eds.) The Planning of Investment Programs, 1978.

-2-

First, we have made an attempt to put together a data base for the industry.We were in a relatively favorable position to do so. Both the OECD and theWorld Bank have direct access to primary information on the industry andinternational trade in its product§, the former by virtue of its coordinatingfunction vis-a-vis OECD member countries, the latter through its projectlending activities, and the extensive commodity analysis that feeds into itsproject appraisal. Moreover, in the course of the study, we have benefittedfrom the detailed advice of several of the large aluminum companies, theInternational Bauxite Association, and individual consultants with specialexpertise in this field. Finally, we have been able to survey systematicallythe available published information on the industry from a wide variety ofsources, including World Bank project documents.

Nevertheless, we recognize--and emphasize--that the data basepresented in this study, and underlying the analysis, is no more than a firstattempt at assembling one and leaves considerable room for improvement. Tothe extent deficiencies lie in the technical quality of the data used,subsequent efforts at verification or improvement are needed. When theyrelate to judgmental data, however, it is important to establish close linksto potential users of this type of analysis in order to ascertain their viewson appropriate magnitudes. Most of the data, assumptions and projections usedin our analysis fall into the latter category, and it should therefore not besurprising that we make no attempt to present the study as a definitive one inany way. The emphasis will be on the type of results that can be attainedwith the analytic approach we have selected, in the hope that this willprovide an incentive to some of our diverse audiences to assist us in acontinuing process of improvement of data, assumptions and projections.

The second objective of our study is to demonstrate that it ispossible to design a framework of analysis that incorporates the maincharacteristics of the industry's structure, and employ it efficiently toaddress a number of pertinent questions regarding its future development. Indescribing this framework, we shall emphasize the multitude of uses to whichit can be put, recognizing that different audiences may have diverse needs.

1.2 Organization of the Study

In the next section, we shall give a brief description of theindustry. This is followed by Section 3 in which we present most of the data,assumptions and projections used in the analysis. In Section 4, some of themain economic questions to be addressed in a worldwide study of the industryand the method of analysis will be presented, and, in annexes to that section,a complete statement of the model and its numerical information, in GAMSlanguage, is given. 1/ In Section 5 the types of results that can be obtainedwith this model are described, including a certain amount of sensitivityanalysis. Section 6 contains the main conclusions.

1/ GAMS is a computer-readable language to describe a model and associateddata that places minimal demands upon non-specialists for understandingthe model's structure.

-3-

2. The Aluminum Sector

In this section, we shall provide a brief technological descriptionof the industry, primarily addressed to those that are not familiar with thecharacteristics of products and processes that are important to the sector.Readers that are familiar with the technical aspects of the aluminum sectorcan skip this section without loss of continuity.

2.1 General Overview

Bauxite, a rock consisting chiefly of hydrated alumina and hydroxideminerals is the principal raw material for aluminum. Most of the bauxiteproduced in the world is processed into alumina at refineries, and the latterproduct is converted into aluminum in electrolytic smelters. Additionally,there are also smelters that process new and used aluminum scrap intosecondary aluminum. Minor amounts of bauxite and alumina, both hydrated andcalcined, are consumed by the refractory, abrasive and chemical industries.(Figure 1 presents a flow chart of the sector, for reference throughout thissection).

Aluminum has varied applications: its strength, low density andpleasant appearance have made it useful in motor vehicles, in machinery andequipment and in construction; due to its low density and high electricalconductivity, aluminum has displaced copper in a series of electrical uses;because of its resistance to corrosion it has partially replaced tin and steelin the packaging industries.

The aluminum industry is vertically and horizontally integrated.Over sixty percent of the world's productive capacity for bauxite and aluminaand over half of the world's aluminum capacity (excluding Centrally PlannedEconomies) is owned and operated by six corporations: ALCOA, ALCAN, Pechiney(PUK), Reynolds, Alusuisse and Kaiser. Because of trading patterns, highinvestment requirements, economies of scale, as well as proprietarytechnology, these multinational companies have tended to be associated withmany new projects in the sector. However, more or less independent producersare emerging, particularly in developing countries, which may have importantlong-run consequences for the international structure of the industry.

Prices of bauxite, alumina and aluminum reflect the high degree ofconcentration of the industry. There are no market price quotations forbauxite or alumina, prices being set mainly by companies for their internalaccounting and/or to comply with host government regulations. In the case ofaluminum, producer prices of the major producers set the price patterns (about80 percent of primary aluminum production is transferred from the primaryproducer/smelters to subsidiary operations producing semifabricates); dealeror free market prices are also quoted; and since 1977 aluminum has been quotedin the London Metal Exchange. 1/

1/ See: World Bank, "Bauxite and Aluminum Handbook," Washington, D.C.,February 1981.

- 4 -

Figure 1: PLANTS AND PRODUCTS OF THE ALUMINUM INDUSTRY

Bauxite

Scrap LeCnryCalcination Chemical

Collectors Plants Industry

Calcined

New Alumina Bauxiteanew (Refractory

Scrap Nscerwap S > or Abrasive}Scrap Scrap Specialty

Aluminas

Secondary Primary Refractory

Smelter Smelter andAbrasiveIndustries

AluminumJ, Aluminum

New L Mills and FoundriScrap.

Bar, Sheet, Rod,Plate, Wire, Tube,Powder, etc.

New Manufacturing PlantsScrap

Old Buildings, Houses, Automobiles,

Scrap Transmission Lines, Machinery,

Cans, etc.

Source: World Bank, Economic Analysis and Projections Department,Commodities and Export Projections Division, February 1981.

5-

Until the decade of the forties, bauxite, alumina and aluminum wereproduced mainly in Europe, the Soviet Union, the United States and to a lesserextent in the Guianas (only bauxite). Thus, during this period, the entireproduction cycle remained principally concentrated in the industrial nationsnear to the major metal markets. Cost considerations drove the aluminumcompanies to seek new supplies of bauxite after World War II which wasreflected in the rise of Guyana and Suriname as the main producers of bauxite,supplying mainly North America. The bauxite/aluminum industry followed apattern of increased internationalization with the appearance of new importantproducers: Jamaica in the early fifties and Australia and Guinea in thesixties. This distinction between producing and consuming countries wasemphasized in 1974 by the creation of the International Bauxite Associationwhich was composed solely of bauxite producing nations.

Since the period of the early 1960-s the geographical distribution ofalumina production has followed partially that of bauxite. By locatingalumina refineries near to the mines, transport costs as well as someprocessing costs are reduced (per ton of aluminum content); but in lessdeveloped areas investment costs may be higher; and in some cases some privatesector companies have concern about the security of their large investments.In 1979, developing countries produced 51% of world bauxite production,centrally planned economies 13%, and industrial nations produced 36% (includesAustralia at 31%); alumina production in this same period was 20%, 17% and 63%respectively. 1/

Primary aluminum production is energy intensive, approximately 13,500kwh of electricity being needed to produce one metric ton of aluminum, withtoday's technology. Thus, the availability of sufficient supplies of low costenergy is one of the critical factors determining the location of smelters. Alarge number of smelters built before the 1973 energy crisis, are located inindustrial countries which previously had access to relatively inexpensiveoil, natural gas, or hydroelectric power. Some of these smelters are nowbeing forced to close down, due to rising energy costs, since their fuelsources have alternative markets. Japan has been the most striking case,where aluminum smelting capacity is being reduced by one-third. Some smeltersin the U.S., mainly those which depend on natural gas, are also closingdown. Meanwhile, some plants have their own captive sources of energy orpossess long term contracts for the supply of power permitting longer-termadjustment to changed relative prices.

These trends point toward a shift in aluminum industry patterns: newsmelters will be located in regions with untapped energy sources which havelittle or no alternative uses, as may be the case of hydropower, flared gasand low quality coal. Since these relatively low cost sources of energy aremostly located in developing countries and in Australia, consuming countriesare likely to become more dependent on imported aluminum. This is reflectedin the fact that while primary aluminum output from developing countries was3.2 percent of world output in 1960, it increased to 13.7 percent in 1979. Atthe same time, developed countries in 1960 produced 77 percent of world

1/ Ibid.

-6-

primary aluminum and consumed 74 percent, while by 1979 they produced 65percent and consumed 67 percent of world aluminum.

One source of uncertainty for these trends relates to the future ofnuclear energy. The large scale development of nuclear power could reversethe trend and improve the competitive position of the industrial countries inenergy-intensive industries.

2.2 Bauxite Deposits and Characteristics

Aluminum is the most abundant metal in nature, representing about 8.2percent of the earth's crust. Unlike many other metals it is not found in theearth in metallic form, but it is a common constituent of many minerals, whereit is normally present in combination with silicon and oxygen, with hydroxylgroups, with iron, titanium, calcium and to a lesser extent, with fluorine,phosphorus and boron. 1/

The bauxite ores, gibbsite, boehmite and diaspore, which arecurrently the main sources of aluminum, account for only a small part of thealuminum found in the world. Other potential sources of aluminum may beclassified as follows:

a. Igneous rocks, the most important being anorthosite,nepheline syenite and phonolite. Of these, nephelinesyenite has the highest commercial importance occurringin sufficient quantity for commerical development inCanada, the USSR, Norway and the United States.

b. Sedimentary rocks, such as clays and shales. Althoughthe high-alumina clays constitute a potential source ofalumina, these have high commercial value due to theirapplications in the ceramics, refractories, chemicaland paper industries. Shales have low alumina content;therefore, alumina from shales is economically feasibleonly as a byproduct.

c. Metamorphic and metasomatized rocks, of which alunite isthe most promising. The main problem with alunite as asource of alumina, is that the larger deposits containnumerous impurities which interfere with the extractionprocess, and that the sale of various commercial byproductsis necessary for the economic viability of the process.

In summary, aluminum is technically obtainable from non-bauxite sources, andtherefore, these could be developed for strategic considerations, but atpresent the Bayer bauxite process has significantly lower costs than those of

1/ Bliss, Neil, "Non Bauxite Sources of Alumina with Particular Reference toALCAN's Recent Investigations," in: The Journal of the Geological Societyof Jamaica--Proceedings of Bauxite Symposium IV, Kingston, Jamaica, June1980.

A

-7-

alternative processes. Therefore, since it is unlikely that any of these non-bauxite sources of alumina will become important for the aluminum industryduring the twentieth century, the remainder of this section focuses on thedistribution and characteristics of the world's bauxite resources. 1/

Bauxite deposits may be divided into two classes: karstic andlateritic. 2/ Karstic bauxites are associated with limestones, are usuallyfiner than lateritic bauxites and tend to have a higher iron content.Lateritic bauxites are found with aluminosilicate rocks and are much coarsergrained. The structure of the deposits and the impurities found are differentfor these two classes of deposits.

From the point of view of bauxite processing conditions at aluminarefineries, the most important classification distinguishes bauxites accordingto the aluminum oxyhydroxide minerals present, which influence mainly thetemperature and pressure required for refining: 3/

a. Trihydrate type, A1203 . 3H20, with gibbsite as the main mineral andboehmite content of less than 3 percent.

b. Monohydrate boehmite type, A1203 . H2 0, including monohydratebauxite with low amounts of diaspore.

c. Mixed types, which contain gibbsite as the predominant aluminummineral but with boehmite content over 5 percent of the aluminumore.

d. Monohydrate mixed bauxite, where boehmite is the predominantaluminum mineral but diaspore content exceeds 5 percent.

Of these types of bauxite, trihydrates are the cheapest to process, due tolower temperature and pressure requirements, and monohydrates the mostexpensive; while the processing costs for mixed tri-monohydrates are somewherein between. Among the monohydrates, diaspore is the most difficult to treat.

Apart from the bauxite types, some other factors are important indetermining the alumina plant design and processing conditions, consequentlyaffecting refining costs. The bauxite to alumina ratio ranges from 2:1 to3.4:1, and therefore establishes the amount of bauxite necessary to produceone ton of alumina and also provides an indication of the amount of impuritiespresent in the ore (a pure gibbsite would show a bauxite-alumina ratio of1.53). However, the type of impurities in the bauxite are as important as the

1/ Bliss (op. cit.) p. 223.

2/ Hill, V.G., "The Rational Development of Bauxite Resources in The Journalof the Geological Society of Jamaica, Proceedings of Bauxite Symposium IV,Kingston, Jamaica, June 1980.

31 The description of bauxite types was obtained from the InternationalBauxite Association.

-8-

bauxite-alumina ratio. The most objectionable impurity is reactive silica,which is chemically combined in clay mineral silicates; in many cases non-reactive silica is not particularly important and occurs as quartz, sand,chalcedony, etc. 1/ Some of the main impurities such as iron and titania areessentially insoluble, their main effect being that they require sufficientadditional equipment to separate them mechanicaly from the bauxite afterdigestion. The most prevalent of the insoluble impurities are iron, calcium,magnesium, titanium and manganese. Among other impurities worth mentioningare the highly soluble ones, which affect processing conditions but do notaffect alumina purity, such as organic carbon, carbonates, chlorides andsulfates. For a technical description of how impurities influence processingconditions and output quality, see Teas and Kotte. 2/

Besides the type and quality of the bauxite, mining costs must betaken into consideration in evaluating bauxite deposits. Infrastructurerequirements, dimension of the deposits, thickness of the overburden andtransportation needs, are factors which affect significantly the cost ofbauxite production. Another important set of issues affecting investmentdecisions in bauxite mines consists of government policies regarding taxation,mining laws, security of investment and other related aspects (see Section 3for taxation policies).

Table 1 presents the characteristics of main bauxite depositsthroughout the world. This table presents a summarized view on the locationof the deposits, estimates of economic reserves, amount of overburden asreflected in the strip ratio, type and quality of the bauxite and processrequirements, and average distances to ports or refineries. The data onreserves has been obtained from various sources (U.S. Geological Survey, U.S.Bureau of Mines, International Bauxite Association) and includes thosedeposits considered exploitable within the next two decades. The otherinformation, appearing in the table has also been obtained from a variety ofsources, including the use of a consultant with ample experience in theindustry. 3/

The total economic reserves shown in Table 1, amount to over 22.8billion metric tons, enough to supply the world's requirements for over onehundred years. It may be appreciated that the countries with the largestknown reserves, in order of importance include: Guinea, Australia, Brazil andJamaica, representing 70 percent of the world total. This table shows also,that most Western and Eastern European bauxites are expensive to mine becauseof the overburden and are also costly to process due to their diasporecontent. In The United States, because of low quality bauxite, a soda-sinterprocess is required for refining local bauxite into alumina. China uses a

1/ Reimers, "Pre-investment Data for the Aluminum Industry," Centre forIndustrial Development, United Nations, New York, 1966.

2/ Teas, E. Bruce and Jan J. Kotte, "The Effect of Impurities on ProcessEfficiency and Methods for Impurity Control and Removal," in The Journalof the Geological Society of Jamaica--Proceedings of Bauxite Symposium IV,Kingston, Jamaica, June 1980.

3/ Mr. Richard C. Roberts.

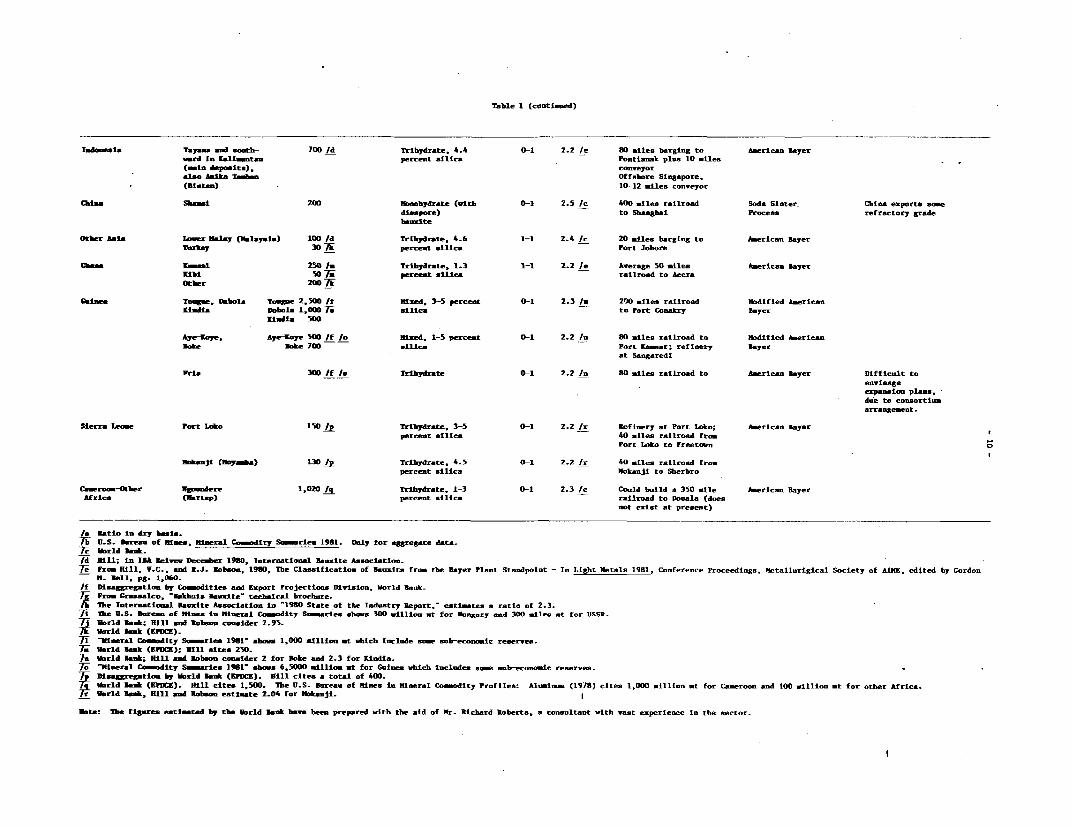

Table 1: CHARACTERISTICS OF BAUXITE DEPOSITS

Economic Bauxite Type ofReserves Strip Alumina Distance to Processing

Country/Region Location (million mt) Type of Bauxite Ratio Ratio a/ Port/Refinery Required Coments

United States Arkansas 40 /b Trihydrate, 7.5-15 3-1 2.2 /c Average 400 miles Soda Sinter Process At present aluminapercent silica river to New Orleans beesuss of high silica (not bauxite) is'(mostly 15%) content shipped from Arkansas

Jamaica Various sites 1,050 Trihydrate, 1-3.5 0-1 2.4 /c Average 12 miles to American Bayer Additional 200 millionpercent silica port (Port Rhoades, at of lower quality

Port Kaiser, Ocho Rios) reserves

542 Mixed, 1-3.5 percent 0-1 2.7 /c Modified Americansilica Bayer

Baiti/Dominican Various sites 50 /d Mixed, 2.5 percent 0-1 2.7 /e Average 15 miles to Modified AmericanRepublic silica Hiragoane or other Bayer

port

Guyana Linden, Ewakani 700 /b Trihydrate, 3-4.5 2-1 2.0 /e 140 miles by river American Bayermnd Ituni percent silica barge fron Kwakwani;

60 miles by railroadfrom Ituni; to Everton

Suriname Moeago and 390 /b /f Trihydrate, 3.9-8 1-1 2.1 /e American BayerParanam percent silica

Bathuis 1OO /b /f Trihydrate, 3.5 0-1 2.5 /g 50 miles railroad American Bayerpercent silica from W. Suriname to

Apurs plus 200 milesriver barge to Paranama

Brazil Trombetas 4,070 Id Trihydrate, 3-5 2-1 2.1 /c 20 miles railroad plus American Bayer '°Paragominas percent silica 690 miles river to

Belem

Venezuela Los Pijiguajos 500 /d Trihydrate, 4 1-1 2.1 /c 20 miles railroad to American Bayerpercent silica Las Ventanas plus

250 miles riverbarge to Puerto Ordaz

Western Europe Greece 700 Moonohydrate (with 3-1 2.5 /c 20 miles truck to European Bayer The European BayerYugoslavia 460 diaspore), 6.5 2.5-1 2.4 7W /h 110 miles railroad process may beFrance 40 percent silica to Dubrovoic include partial

treatment of disapore

Eastern Europe Hungary 300 /d /i Monohydrate with 3-1 2.5 /c Average of 300 miles European Bayer 1. In Hungary whendiaspore) to Leningrad diaspore content is

high, they use a limesinter process.

USSR 300 /d /i Monohydrate (with 3-1 2.5 /c 2. Russia treats alsodiaspore) alunite and nephelinesyenite.

Australia Gove, Weips Gove 300 /b /f Mixed, 2-6.5 percent 0-1 2.2 /e 30 miles railroad to Modified AmericanWeipa 3,100 T7 7 silica Weipa Bayer

Western Australia 1,200 /b /f Trihydrate, 1.5 0-1 3.4 /4 90 miles railroad to American Bayer(Darling Ranges) percent silica Bunbury (port) 20 miles

to Wagerup (refinery)

India Panch Pat Mal 600 It /1 Tribydrate 0-1 2.4 /c 100 miles railroad to American Bayerdeposits in to VishakhapatnamOrissa (mainly) (S. East India)

(continued)

Table 1 (continned)

Indo*esia Tayana nd sooth- 700 /d Trihydrate, 4.4 0-1 2.2 / 80 siles barging to American Sayerward in Kalimanta percent silica Pontianas pI"s 10 miles(main depI its), conveyor*15o A-ibS TISSam Offshore Singapore.

(01-tan) 10-12 miles conveyor

Chia Sb, i 200 Moonbydrate (with 0-1 2.5 /c 400 miles railroad Soda Sinter China exports somedis pore) to Shanghai Process refractory gradebauxite

Otber Asia Iower "ata (Malaysia) 100 /d Trihydrare, 4.6 1-1 2.4 Ic 20 miles barging to American Bayer

Tnrke 30 7W percet sltica Port Jobore

Ga' a' 250 /I Trihdrate. 1.3 1-1 2.2 le Averge 50 miles American layerKibi 50 percent silUca railroad to AceraOtber 200 7W

Gansa Toge. Dnbola Tong8e 2,500 If nMed, 3-5 percent 0-1 2.3 In 200 iles railroad Nodified AmericanKildia Dobola 1,oao To silica tn Port Cnnakry layer

Kila 500

Aye-Ko, Aye-Koye 500 /f /n Mixed, 1-5 Percent 0-1 2.2 /n SO siles railroad to Modified Americanlobe Bok. 700 *ilica Port ar r; refinery layer

at Sangaredi

Fria 300 /f /o Trihydrate 0-1 2.2 n S0 miles railroad to American layer Difficult toenvisageexpansion plans,due to consortiumarrangement.

Sierra leone Part Labo 150 /P Tribdrate, 3-5 0-1 2.2 /r leinery at Port ioko; American layerpercent llica 40 miles railroad frm

Port Loko to Freetown

Janji (Moy_a) 130 /p Triydrate., 4.5 0-1 2.2 /r 40 miles railroad frempercent silics - obanji to Sherbro

Cameroo_-Otber Ugndere 1,020 /q Trihydrate, 1-3 0-1 2.3 /c Could build a 350 mile American layerAfrica (Martap) percent silica railroad tn Do-nla (does

not exist at present)

/a latin io dry bais.7i1 U.S. Brean of nis, Mineral Comdity S ries 1981. Only for aggregate data.7A World Rusa.Td Hill; in INA Reive, December 1980, International Blsoite Association.e P.ro Mill, V.C., and R.J. Robson, 1980, The Classification of lansits from tbe layer Plnt Standpoint - In Light Metals 1981, Conference Proceedings, netallurigical Society of ADMN, edited by Cordon

n. sell, Pg. 1,060.If Diisaggregaton by Comodities and Export Projections Dlviaion, World Bank.

From Grassalco, l-sbhni Bsoite techitcal brochure.i Tbe Internation laste Association in -l9l0 State of the Indnstry Report, estimates a ratio of 2.3.71 The U.S. Barean of Miein Mineral Conodity Sws-ies sh. 300 million t for Hungary end 300 silas t for USSR.

World lask; MUl and Robaon consider 2.95.WDlorld mk (KD().

717 i-mrat Comndity Sn_ries 1981 shows 1,000 million at shich inclde some nob-nomlc reserves.7A World lak (1POCK); Mill sites 250.To Vorld Bank; MilL and Robson conider 2 for loke nd 2.3 for Kindia.To Mineral Co_ndity S_ries 1981 shows 6,5000 million t for Ginmes .hich includes some b-economic reserves.A Disaggregatiom by World Sank (KFUM). Hill cites a total of 400.7. World lank (HPMCg). tlu cites 1,500. The U.S. Blrean of nems in Mineral Coiodity Profiles: Aloninom (1976) cite 1,000 million at for Cameroon and 100 million at for other AfricA.7ir World lank, Hill ad Robson estimate 2.04 for Monji. I

Sote: The fisres estimated by the Yorld Bank have been prepared vith the aid of Mr. Richard Roberts, a consultant tith vASt experience in the sector.

- 11 -

sinter process to recover alumina from diaspore. Among the deposits shown,those in Venezuela, Cameroon, Ghana, Kalimantan in Indonesia, andTougue/Dabola/Kindia in Guinea, are undeveloped, requiring heavy expendituresfor their exploitation and infrastructure development.

Most of the bauxite produced in the world is mined by open-pitmethods. In France, Greece, Turkey and Hungary, bauxite is also produced atunderground mines. Bauxite mining consists basically of three stages:extraction, crushing and drying; some bauxites also require beneficiation.Extraction involves removal of the overburden by bulldozers, drag-lines andlarge-wheel excavators, with the use of explosives for hard terrains. Then,the bauxite is removed by similar methods, and the overburden is replaced torestore the surface of the mines for re-use as forest or agricultural land.Where beneficiation processes are used, they generally consist of wetprocesses to increase the alumina content and to reduce silica and ironcontent.

Most bauxites require crttshiig for ease of processing. Caribbeanbauxite (Jamaica, Haiti, Dominican Rcpublic) is so fine-grained that it needslittle or no crushing.

The third stage is drying, which may be done at the mine site or atthe refinery. If the bauxite is to be shipped great distances, it is usuallydried at the mine in order to reduce transport costs. Drying is carried outin rotating kilns at moderate temperatures to remove the free moisture withoutaffecting the alumina hydrate. In this process, moisture is reduced by about5 percent arriving at moisture contents of 10 percent for Caribbean bauxitesand of 5 percent for other types. The fine grain of Caribbean bauxite makesit impractical to reduce humidity by more, since it would cause handlingdifficulties. If the alumina plant is near the mine, the bauxite is dried atthe former, where the use of heat recovered from the refining process cutsdrying costs by about fifty percent. Mines in the Dominican Republic andNorthern Australia (Gove, Weipa) use solar drying and therefore do not requiredrying fuel. Several of the Australian mines use a beneficiation process toreduce silica content.

2.3 Alumina Refining

Bauxite is refined into alumina almost exclusively by the Bayerprocess. Alternative technologies are available for obtaining alumina fromnon-bauxite sources, but as mentioned previously in this section, processingcosts are significantly higher. Such is the case of the leaching andsintering method employed in the Soviet Union to treat nepheline syenite andalunite ores. Because of high costs, neither the USSR nor other countrieshave any current plans for building new plants of this type. Since the Bayertechnology is likely to remain the most important for alumina refining in theforeseeable future, this section focuses on its main technical aspects.

Bayer alumina plants consist of two facilities operating in series:a hydrate plant and a calcination plant. The hydrate plant transforms bauxiteinto alumina hydrate in a process involving four major operations:

- 12 -

i. Grinding and slurrying where the crushed ore is fed toball or rod mills and caustic soda, lime, hot water andspent liquor are added to it, forming a slurry that goesinto the digestors. The consumption of caustic sodadepends principally on the reactive silica content andmud washing losses, with an average of 1.4 kilograms ofsoda (as NaOH) per kilogram or reactive silica. 1/ Limeis used to reduce carbonates, regenerate caustic soda andcontrol phosphates. About 0.1 metric tons of lime permetric ton of alutmina are assumed normal for a plantusing caustic soda and for a bauxite having minimumphosphorus.

ii. Digestion of the slurry containing bauxite and causticsoda at elevated temperatures and pressure. At thisstage, bauxite is dissolved, forming a solution of sodiumaluminate (NaAlO2), while the reactive silica combineswith alumina forming a insoluble sodium aluminum silicateand consuming caustic soda and alumina in the process.Other insolubles include non-reactive silica, iron oxideand titanium. The simplest digestors correspond to theAmerican Bayer process, characterized by a low temperaturedigest (about 2900F) which is designed to extract easilysoluble gibbsite (Guyana, Brazil, Suriname, West Australia,etc.), and which uses a relatively low caustic sodaconcentration (up to about 130 grams per liter of Na2 O).At the other extreme is the European technology forbauxites containing more difficult soluble boehmite(monohydrate) which requires temperatures up to 490°F andmuch higher caustic concentrations (up to 240 grams perliter of Na2O). This group of bauxites includes thoseof southern Europe and Eastern Europe. Between theextremes of these conditions, another technology existsknown as Modified American Bayer which is designed formixed bauxites containing principally gibbsite withminor amounts of boehmite, as in North Australia, Guineaand some deposits in Jamaica; for which process conditions areset for temperatures from 3500 to 470°F and causticconcentration up to about 150 grams per liter of Na2Q.Operating conditions of the American Bayer process willcause the solution of silica occurring only as a clayimpurity, while those of the European Bayer method willalso dissolve the silica contained in quartz.

1/ If, for example, a bauxite contains 2 percent reactive silica, to process1 metric ton of bauxite will require 1.4 Kg Soda x 20 Kg Silica

Kg Silica ton bauxite= 28 Kg of NaOH. If the bauxite alumina ratio is 2.2 : 1, the sodarequirement per ton of alumina is 2.2 x 28 = 61.6 Kg.

- 13 -

iii. Filtration and settling of the insoluble impurities(called red mud) separating them from the sodium aluminatesolution which in turn, is pumped into precipitators. Thered mud is usually discarded to disposal areas known as redmud lakes.

iv. Precipitation of the sodium aluminate which is seeded withaluminum hydrate crystals, causing about 50-60 percent ofthe alumina hydrate to dissociate from the soda andprecipitate out as crystals. The mixture is pumped to atleast 3 stages of thickeners which separate the crystalsfrom the caustic solution. The coarsest product is sentto the calcination department; the product of the last 2stages is recycled to the precipitators for seed to controlparticle size. The caustic solution is recycled for furtheruse while the alumina hydrate is sent to the calciners.

The calcination of alumina hydrate (A1203 e 3H20 or A1203 . H20) toalumina (A1203) involves the removal of moisture and of the chemically bondedhydroxide by roasting the hydrate at 1,150 to 1,2500C. Before the 1950srotary kilns were used, but afterwards the industry has tended to employ fluidbed calciners, which use 33 percent less fuel, are cheaper to install andrequire less maintenance. In some of these calciners, final calcinationoccurs in an updraft furnace into which both partially calcined hydrate andfuel are injected; followed by a fluidized holding vessel where alumina can beheld for the required time at the desired calcination temperature. Theresulting alumina is then cooled in a fluid bed cooler and stockpiled untilshipped to aluminum smelters.

2.4 Aluminum Smelting

Aluminum metal is produced by the Hall-Heroult process which consistsof the electrolysis of alumina (A1203) to separate aluminum from oxygen. Twotypes of reduction plants are currently in use: the prebaked anode plants andthe Soderberg anode plants. Given the importance of electricity as a majorinput for these processes, and under the pressure of rising energy costs,other routes are being tried, such as the ALCOA smelting process whichconsists of the chlorination of alumina and the subsequent electrolysis ofaluminum chloride. This process could reduce energy consumption by about 20percent with respect to the Hall-Heroult process, but it brings othercomplications such as the need to maintain the purity of aluminum chloride athigh levels. I1 If these and other difficulties are solved, this route foraluminum production may be applied commercially by the end of the century.

An aluminum reduction plant consists of electrolytic cells arrangedin series (known as potlines), holding furnaces for the molten aluminum, andcasting machines for the production of ingots of different shapes. The cells

1/ Grjotheim, Kai and Barry Welch, "Impact of Alternative Processes forAluminum Production on Energy Requirements," in Gordon M. Bell (ed.) LightMetals 1981, The Metallurigical Society of AIME, Pennsylvania, 1980.

- 14 -

consist of an outer iron shell with inner carbon lining which serves ascathode. The prebaked type anodes are blocks individually suspended by ironrods hanging above the electrolytic cells. The Soderberg system uses greencarbon paste as anode material which is fed into the top of the anodecasing. 1/

In the Hall-Heroult process, the alumina is dissolved in moltencryolite, which is a double fluoride of sodium and aluminum (Na3AlF6). Byelectrolysis, at about 1000°C, aluminum is deposited at the cathode in theform of a molten metal layer underneath the cryolite, while the oxygencombines with the carbon at the anode forming a mixture of carbon dioxide andcarbon monoxide. The metallic aluminum is periodically tapped off andtransported to the holding furnaces which feed the casting machines.Currently, with environmental concerns a major issue, special attention mustbe paid to pollution problems at aluminum smelters. Significant expendituresare required to control the fluorides resulting from the cell bath as well asthe alumina dust. Because of these problems, the use of Soderberg type anodesis being discontinued, as they produce more abundant fluoride compounds andtarry components.

Aluminum ingots of various shapes are shipped from the smelter tosemifabricating plants for further processing by a wide range of industries.The special characteristics and relative low cost of aluminum account for itsvaried applications. Some aluminum alloys combine lightness with greatstrength. Aluminum does not corrode easily and is unaffected by many chemicalreactions. Although its conductivity is only 60 percent of that of copper,due to its low density, an electric transmission line made of aluminum weighsonly 48 percent of an equivalent copper line. Due to these properties,aluminum has replaced steel, copper, lead, zinc and tin in a wide range ofuses. Nevertheless, manufacturers of the competing metals and of otherproducts such as plastics, are constantly developing new alloys and compositematerials which halt and reverse substitution of aluminum in many fields. 2/

A breakdown of aluminum consumption by main uses is shown in Table2. It should be noted that there may be definitional problems in breakingdown aluminum use, particularly in Western Europe. About one-fourth ofaluminum production is used for the transportation industry in motorcomponents, vehicle parts, electrical applications and paints. Near to 6percent of aluminum metal is for machinery and equipment (mechanicalengineering). The electrical engineering and communications sector accountsfor one-tenth of aluminum consumption. About one-fourth of aluminum consumedis used in building and construction, for doors and windows, heating and airconditioning, structures and other uses. Resistance to corrosion haspermitted the replacement of steel and other materials by aluminum inpackaging and canning. Almost 7 percent of aluminum is employed for theproduction of consumer durables, such as refrigerators, air conditioners,washing machines and other appliances.

1/ Reimers, "Pre-investment Data for the Aluminum Industry, Department ofEconomic and Social Affairs, United Nations, New York, 1966.

2/ Peach, W.N. and James A. Constantin, "Zimmermann's World Resources andIndustries (Third Edition)," Harper and Row, New York, 1972.

- 15 -

Table 2: CONSUMPTION OF ALUMINUM BY END USES, 1980

Western WorldEurope /a Japan U.S. Average

… __________________(%)…_ _-_____

Transport 27.9 26.1 19.3 22.8

Mechanical Engineering 6.8 4.8 5.4 5.6

Electrical Engineering 10.4 10.1 11.1 10.6

Building and Construction 18.3 32.9 21.4 22.9

Packaging 9.7 6.0 27.8 18.3

Domestic & Office Appliances 8.5 5.5 6.3 6.6

Metal Industries andMiscellaneous 18.4 14.6 8.7 13.2

100.0 100.0 100.0 100.0

/a Germany, France, United Kingdom, Italy.

Source: Metallgesellschaft, "Metal Statistics 1971-1981" 69th Edition,Frankfurt Am Main, 1982.

- 16 -

3. Data and Assumptions

In this section we shall describe the data and assumptions used inthe analysis. Following a section on demand, we discuss investment andoperating costs for mines, alumina refineries, and aluminum smelters. Giventheir importance, energy costs are given special attention. Finally, theavailable information on international transport costs, levies, taxes andimport duties is presented.

It should be emphasized once more that the information in thissection represents a first attempt at establishing a data base for worldwideinvestment analysis. Although the present data incorporate numerousrecommendations for improvement, further qualitative improvements arecertainly desirable. Moreover, given the limited degree of disaggregationthat the analytic framework allows, many data categories are no more than"stylized facts," fairly representative for groups of relatively comparablecountries, but in need of refinement for more detailed subsequent analysis.

3.1 Forecasting the Demand for Aluminum

The next two tables (3 and 4) provide a high and a low forecast ofthe demand for aluminum, for eighteen regions in which we have divided theworld. The countries included in each region are given in Table 5.Basically, the forecast was made on the basis of demand equations that relatethe demand for aluminum to either industrial production or Gross DomesticProduct, and the price of aluminum deflated by a price index. More detailedinformation on the forecasting methodology is available from the WorldBank. 1/

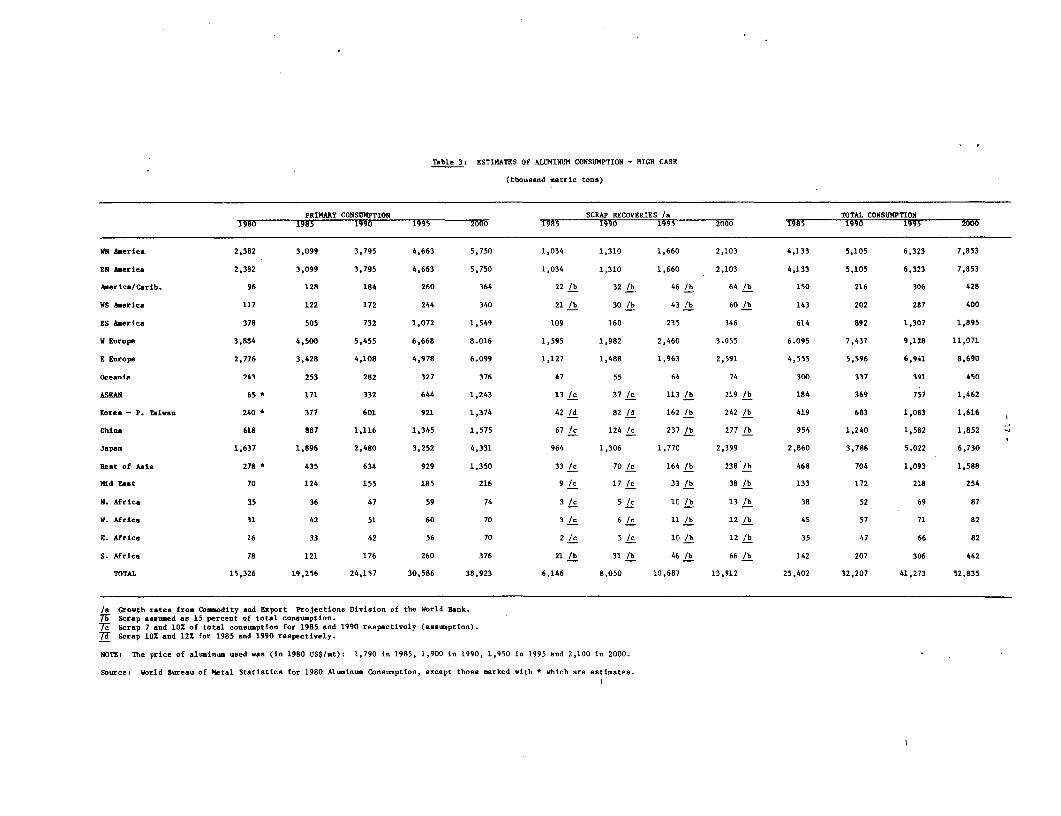

For the high case, primary aluminum consumption is expected to growby 4.8 percent per annum between 1980 and 2000, whereas in t1* low case thegrowth rate is reduced to 3.7 percent. The overall results -re consistentwith estimates from other studies. Thus, "Aluminum Annual Review" 2/ expectsan annual growth rate of primary aluminum consumption (excluding CentrallyPlanned Economies) of 3.6 percent for the period 1980 to 1988. Resources forthe Future, in "World Mineral Trends and U.S. Supply Problems," 3/ considersWorld Consumption of Refined Aluminum (including secondary ingot) to be 46.2million metric tons by the year 2000, compared with the projections shown herefor total consumption (primary and secondary aluminum) of 52.8 million metrictons for the high case and 43.6 million metric tons for the low case.

1/ Specifically the Commodity and Export Projections Division of the WorldBank.

2/ Anthony Bird Associates, op. cit.

3/ Fischman, op. cit.

Table 3: ESTIMATES OF ALUMINUM CONSUMPTION - HIGH CASE

(tbousand metric tons)

PRIKARY CONSUMPTION SCRAP RECOVERIES /a TOTAL CONSUMPTION1980 1985 1990 1995 2000 1985 1990 1995 2000 1985 1990 1995 2000

WM Aaerica 2,382 3,099 3,795 4,663 5,750 1,034 1,310 1,660 2,103 4,133 5,105 6,323 7,853

EN America 2,382 3,099 3,795 4,663 5,750 1,034 1,310 1,660 2,103 4,133 5,105 6,323 7,853

Asertca/Carib. 96 128 184 260 364 22 /b 32 /b 46 /b 64 /b 150 216 306 428

WS Amer1ca 117 122 172 244 340 21 /b 30 lb 43 /b 60 /b 143 202 287 400

ES America 378 505 732 1,072 1,549 109 160 235 346 614 892 1,307 1,895

W Europe 3,884 4,500 5,455 6,668 8.016 1,595 1,982 2,460 3.055 6.095 7,437 9,128 11,071

E Europe 2,776 3,428 4,108 4,978 6.099 1,127 1,488 1,963 2,591 4,555 5,596 6,941 8,690

Oceania 243 253 282 327 376 47 55 64 74 300 337 391 450

ASEAN 65 * 171 332 644 1,243 13 /c 37 /c 113 lb 219 /b 184 369 757 1,462

Korea - P. Taiwan 240 * 377 601 921 1,374 42 /d 82 /d 162 lb 242 /b 419 683 1,083 1,616

China 618 887 1,116 1,345 1,575 67 /c 124 /c 237 /b 277 /b 954 1,240 1,582 1,852 s

Japan 1,637 1,896 2,480 3,252 4,331 964 1,306 1,770 2,399 2,860 3,786 5.022 6,730

Rest of Aaia 278 a 435 634 929 1,350 33 /c 70 /c 164 /b 238 /b 468 704 1,093 1,588

Mid East 70 124 155 185 216 9 /c 17 /c 33 /b 38 lb 133 172 218 254

N. Africa 15 36 47 59 74 3 /c 5 /c 10 /b 13 /b 38 52 69 87

W. Africa 31 42 51 60 70 3 /c 6 /c 11 /b 12 /b 45 57 71 82

E. Africa 16 33 42 56 70 2 /c 5 /c 10 /b 12 /b 35 47 66 82

S. Africa 78 121 176 260 376 21 /b 31 /b 46 /b 66 /b 142 207 306 442

TOTAL 15,326 19,256 24,157 30,586 38,923 6,146 8,050 10,687 13,912 25,402 32,207 41,273 52,835

Ia Grovth rates from Commodity and Export Projections Division of the World Rank.7- scrap assumed as 15 percent of total consumption.7T Scrap 7 and 10X of total consumption for 1985 and 1990 respectively (assumption).7T Scrap 102 and 12X for 1985 and 1990 respectively.

NOTE: The price of aluminum used was (in 1980 US$/mt): 1,790 in 1985, 1,900 in 1990, 1,950 in 1995 Rnd 2,100 in 2000.

Source: World Bureau of Metal Statistics for 1980 Aluminum Consumption, except those marked with * which are estimates.

Table 4: ESTIMATES OF ALUMINUM CONSUMPTION - LOW CASE

(thousand metric tons)

PRIMARY CONSUMPTION SCRAP RECOVERIES /a TOTAL CONSUMPTION1980 1985 1990 1995 2000 1985 1990 1995 20600 1985 1990 1995 2000

UN America 2,382 3,011 3,418 4,004 4,489 989 1,196 1,446 1,748 4,000 4,614 5,450 6,237

EN Americo 2,382 3,011 3,418 4,404 4,489 989 1,196 1,446 1,748 4,000 4,614 5,450 6,237

C. Ameriea/Carib. 96 121 162 210 281 21 lb 28 lb 37 lb 49 lb 142 190 247 330

US America 117 116 151 200 263 20 lb 27 lb 35 lb 46 lb 136 178 235 309

ES America 378 489 693 989 1,407 106 153 220 315 595 846 1,209 1,722

U. Europe 3,884 4,240 4,847 5,583 6,398 1,542 1,859 2,240 2,699 5,782 6,706 7,823 9,097

E. Europe 2,776 3,244 3,696 4,242 4,884 7,094 1,389 1,765 2,241 4,338 5,085 6,007 7,125

Oceania 243 249 266 295 328 47 54 61 70 296 320 356 398

ASEAN 65 * 162 284 502 886 12 Ic 32 Ic 88 lb 156 lb 174 316 590 1,042 ,

Korea - P. Taiwan 240 * 362 542 788 1,120 40 Id 74 Id 139 lb 197 lb 402 616 927 1,317

China 618 887 1,116 1,345 1,575 67 Ic 124 Ic 237 lb 277 lb 954 1,240 1,582Z 1,852

Japan 1,637 1,891 2,360 2,999 3,762 934 1,221 1,596 2,086 2,823 3,581 4,595 5,848

Rest of Asia 278 * 403 546 735 987 30 Ic 61 Ic 130 lb 174 lb 433 607 865 1,161

Mid East 70 124 155 185 216 9 IC 17 Ic 33 lb 38 lb 133 172 218 254

S. Africa 35 35 44 55 70 3/c 5 Ic 10Ib 12 /b 38 49 65 82

W. Africa 31 42 51 60 70 3 /C 61 /ClI b 12 /b 45 57 71 82

E. Africa 16 25 30 37 46 2 /c 3 /c 7 /b 8 /b 27 33 44 54

S. Africa 78 118 171 248 361 21 lb 30 lb 44 lb 64 lb 139 201 292 425

TOTAL 15,326 18,530 21,950 25,781 31,632 5,929 7,475 9,545 11,940 24,459 29,425 36,026 43,572

/a Annual growth rate of scrap recoveries reduced with respect to the high case in pr~,portion to total consumption growth, i.e.,* US 3.9%, Canada 2.8%, ES America 7.5%, W. Europe 3.8% E. Europe 4.9%,Oceards 2.7Z, Japan 5.5%.

lb Scrap assumed as 15 percent of total consumption.7-c Scrap assumed as 7 and 10 percent of total consumption for 1985 and 1990.7d Scrap 10% and 12% for 1985 and 1990, respectively.

NOTE: The price of aluminum used was (in 1980 US$/at): 1,790 in 1985, 1,900 in 1990, 1,950 in 1995 and 2,000 in 2000.

Source: World Bureau of Metal Statistics for 1980 Aluminum Cons.umption, except those marked with * which are estimates.

- 19 -

Table 5: REGIONAL BREAKDOWN FOR ALUMINUM CONSUMPTION

Demand Region Countries Included /a

Western North America Western United States, West Canada

Eastern North America Eastern United States, East Canada

Central America & Caribbean Mexico

Western South America Colombia, Peru, Venezuela, Other SouthAmerica

Eastern South America Argentina, Brazil

Western Europe All Western European Countries includingYugoslavia

Eastern Europe USSR and all other Eastern EuropeanCountries

Oceania Australia, New Zealand

ASEAN Indonesia, Malaysia, Philippines, Thailand

Korea - P. Taiwan Korea, P. Taiwan, Hong Kong

China China, Other Eastern Asia

Japan Japan

Rest of Asia India, Turkey, Other Asia (excludingEastern Asia)

Middle East Bahrain, Iran, Israel, Lebanon

North Africa Egypt

West Africa Cameroon

East Africa Other Africa

South Africa Republic of South Africa

/a Correspond to data published in Metallgesellschaft, "Metal Statistics,"Frankfurt Am Main, various years. The countries specified on the righthand side are the only ones for which specific consumption figures aregiven in this source.

- 20 -

The reader should be aware of the fact that both bauxite and aluminahave uses outside the aluminum sector. According to King and Perlman 1/ about3 million metric tons of bauxite are allocated to non-aluminum uses. the mainproducing countries of non-metal grade bauxite-mainly clacined bauxite--areGuyana, Suriname, Australia and the United States. A breakdown of productionby country is shown in Table 6. The estimated growth rate of bauxite for non-metal uses, derived from this same source is 5.1 percent per year.

About 12.6 percent of aluminum consumption in the Western World isused for purposes other than aluminum production. 2/ This would amount toabout 2.3 million metric tons of non-metal alumina in 1980. Table 7 presentsan estimated production breakdown per region. Alumina for these other uses isexpected to grow at 3.5 percent per annum. 3/

3.2 Investment and Operating Costs for Bauxite

Investment costs for bauxite mines depend on the size of the mine,the strip ratio, locational factors and infrastructure requirements. Table 8presents a formula to estimate capital costs for mines as a function of thesefactors. Table 9 shows an estimate of location factors for various regions,taking into account variations in equipment and construction costs as well asphysical infrastructure. With the data from Tables 1, 8 and 9, we mayestimate that to open a mine of 4 million tons per year in Brazil, would costabout US$70/metric ton of bauxite 4/ per year while a mine in Guinea with thesame capacity would cost only US$51/metric ton of bauxite per year due to thelack of over-burden.

Mines in remote undeveloped locations require very heavy investmentsin infrastructure which need to be spread out by developing large projects.Thus, in the case of locations such as Los Pijiguajos in Venezuela, Cameroon,Kalimantan in Indonesia, and Tougue/Dabola/Kindia in Guinea, a minimum minesize of about 3 million metric tons per year would be required for a projectto be economical.

Estimates of operating costs for mines are given in Table 10.Besides the factors mentioned above, these costs consider the type of deposit,labor requirements and costs, and drying expenditures. Costs are given in1980 US dollars per metric ton of bauxite excluding moisture content, and theyinclude drying. Australian mines do not consume fuel for drying., since asmentioned before, they use solar drying. If bauxite is to be refined locally,drying costs shown in the table should be reduced by 50 percent.

1/ King, James and Louis Perlman, "Trends and Prospects in the Bauxite andAlumina Markets," Commodities Research Unit, Ltd. In: The Journal of theGeological Study of Jamaica, Proceedings of Bauxite Symposium IV, June1980.

2/ King and Perlman, op. cit.

3/ Derived from data in King and Perlman, op. cit.

4/ All values shown in 1980 US$ unless otherwise stated.

- 21 -

Table 6: ESTIMATES OF BAUXITE PRODUCTION FOR NON-METAL USES, 1980

(thousand metric tons of bauxite)

Bauxite Production of UsesOther than Alumina /a

United States 272Guyana 1,765Suriname 493Australia (Weipa) 230China 200

TOTAL 2,960

/a United States: Baumgardner, Luke and Ruth Hough, "Bauxite and Alumina"Reprint for the 1978-79 Bureau of Mines Mineral Yearbook, Bureau of Mines,United States Department of the Interior. 1980 estimates based on 1979data, assuming 5.1% annual growth. Suriname and Australia: World Bankestimates. Guyana: IBA data; 1980 estimate assuming 5.1% annualgrowth. Australia: Australian Government Publishing Service, "AustralianAluminum Industry Supply Potential," Canberra, 1980. China: World Bankdata.

Table 7: ESTIMATE OF ALUMINA PRODUCTION FOR NON-METAL USES, 1980

(thousand metric tons of alumina)

Alumina for Non-Metal Uses

United States 833Western Europe 808Japan 549India 36Guyana 51 /aBrazil 46 7W-

TOTAL 2,323

/a Aluminous cement.7Fb Estimate

Source: Estimated from International Primary Aluminum Institute, "StatisticalSummary," United Kingdom, 1980.

- 22 -

Table 8: CAPITAL COST FOR MINES

(US$ 1980)

Total capital cost including infrastructure, strip ratio and location factorsbut excluding railroads.

Mine Size Capital Cost

(Million tons per year) (Mill. US $)

0 - 1.6 sf x lf x (30 + 27.5 x size)1.6 - n x 1.6 sf x lf x ( 46.25 x size)n x 1.6 - sf x lf x ( 55.5 x size)

where sf: strip ratio factor

Strip Ratio Strip Ratio Factor

0:1 1.01:1 1.222:1 1.373:1 1.50

lf: location factor from Table 9

n: diseconomy of scale factor, between 2 and 4 depending on location.

Sources: Economies of scale factor, estimated from Bennett H., "AnEconomic Appraisal of the Supply o_ Copper from PrimaryDomestic Sources," U.S. Bureau of Mines, 1973.

World Bank consultant.

- 23 -

Table 9: LOCATION FACTORS FOR MINE CAPITAL COSTS

Country/Region Factor

United States 1.00

Western Europe (Greece, Yugoslavia, France) 1.00

Eastern Europe 1.00

China 1.00

Jamaica 1.10

Haiti/Dominican Republic 1.10

Guyana 1.10

Suriname 1.10

Brazil 1.10

Venezuela 1.10

Australia 1.10

India 1.10

Indonesia 1.10

Other Asia 1.10

Ghana 1.10

Guinea 1.10 - 1.25

Sierra Leone 1.15

Cameroon - Other Africa 1.25

Source: World Bank estimates.

Table 10: OPERATING COSTS FOR BAUXITE MINING, YEAR 2000

(1980 US$/mt bauxite)

CharacteriAtics of DepositStripRatio Fuel

Type /a (as Labor Drying Motor MaterialsRelative Slze of mined Mining and Wage Fuel for Fuel Fuel and andThickness Ore Bodies Basis) Maintenance Stripping Drying Rate /c Drying /d Costs /e Lubricant /f Services /g Total /h

(m-hr/mt) (m-hr/mt) (n-hr/nt) ($/m-hr) (Gal/mt) ……---------($/Mt)------------------------…

United States Thick/Large 3.5:1 .3 .32 .1 11 2.40 - 1.20 3.50 15.4Jamaica Medium/Small-Medis 0:1 .4 .10 .2 4 2.40 2.00 1.20 3.50 11.0daiti Thin/Small-Mediu 0:1 .4 .10 .2 2 2.40 2.00 1.20 3.50 11.0

Guyana Thick/Large 4:1 .4 .57 .2 4 2.40 2.00 1.20 3.50 12.6Suriname (bakhuis) Medium/Large 0:1 .4 .11 .2 6 2.40 2.00 1.20 3.50 11.0Brazil Thick/Large 2:1 .4 .23 .2 6 2.40 2.00 1.20 3.50 12.6Venezuela Thick/Large 1:1 .4 .13 .2 6 2.40 2.00 1.20 3.50 11.8Western Europe tedius/nediu- 3:1 .3 .40 .1 11 2.40 2.00 1.20 3.50 15.4(Greece principally)Eastern Europe Medium/Medium 3:1 .3 .32 .1 4 2.40 2.00 1.20 3.50 9.8Australia Thick/Large 0:1 .3 .15 .1 11 2.40 - 1.20 3.50 10.2(Gove/Weipa)

Australia (West) Medium/Medium 0:1 .3 .10 .1 11 2.40 2.00 1.20 3.50 10.2India Medium/Medium 1:1 .4 .14 .2 2 2.40 2.00 1.20 3.50 8.1Indonesia Medium/Large 1:1 .4 .14 .2 2 2.40 2.00 1.20 3.50 8.1China Medium/Large 1:1 .4 .14 .2 2 2.40 2.00 1.20 3.50 8.1Other Asia (Kalaysia) Medium/Medium 1:1 .4 .14 .2 2 2.40 2.00 1.20 3.50 8.4Ghana Medium/Medium 1:1 .4 .14 .2 5 2.40 2.00 1.20 3.50 10.9Guinea Thick/Large 1:1 .4 .12 .2 5 2.40 2.00 1.20 3.50 10.3Sierra Leone Medium/Medium 1:1 .4 .12 .2 4 2.40 2.00 1.20 3.50 10.3Cameroon Thick/Large 1:1 .4 .14 .2 4 2.40 2.00 1.20 3.50 10.3

/a Characteristics of Deposit:

Average Size of Ore Pocket:Thickness; Thick 15-40 ft Large 2-5 - tons each

Medium 10-20 ft Medium: 1-2 - tons eachThin 2-10 ft Small: 200-500 a tons each.

/b Mining Labor and Maintenance Labor (includes supervisors)For Industrialized Natiotns 0.28 a-hr/mtFor Developing Countries 0.43 -hr/mt

Drying LaborFor Industrialized Nations 0.14 -hr/mtFor Developing Countries 0.21 m-hr/nt

Stripping LaborFor each increment of strip ratio 0.33X of mining labor is added.

/c The wage rates were estimated from the International Labor Organization Statistics Yearbook and fron industry sources. Wages and salaries include payments in kind, contributions of employers tosocial security and other benefits.

/d Fuel for drying corresponds to 2.4 gallons of bunker fuel oil/mt bauxite in order to reduce moisture content by 5%. Jamaican and laitian bauxites are dried from an average of 15% to 10%moisture. All other bauxites are dried from 10% to 5% moisture. Dominican Republic and Northern Australia (Gove/Weipa) use solar drying and therefore do not use drying fuel. Note that ifbauxite is processed at a local refinery it is not dried at the mine but the moisture is evaporated at the refinery at about 50% savings.

/e Fuel costs at US$35/US Bbl or US$0.83/US Gal.

/f Motor fuels average about US$0.80/mt, lubricants about US$0.10/mt.

/g Include parts, supplies and miscellaneous.

/h Total costs include mine haul of up to six miles to local alumina plants or port facilities. Except for the U.S. and Western Australia all figures are for bauxite for exports (drying by 5%moisture using fuel or solar drying).

Note; The above represent an estimated average for each location. In sane nations there are multiple deposits which may vary both in character And analysis. Figures sho-n are all calculated on theaa e basis for comparative purposes one with another.

Source: World Bank and Mr. Richard Roberts (consultant).

- 25 -

The data from Tables 8 to 10, together with transportation costs andbauxite levies (the last two are detailed in sub-sections 3.5 and 3.6), areused to estimate total production costs for bauxite, which are presented inTable 11. This table shows that capital costs and levies are as important asoperating costs. Inland transportation costs are also significant in a numberof countries. Since Jamaica, Haiti, the Dominican Republic and Surinamecredit the levy against income taxes, its impact is greatly reduced if bauxiteis processed locally. This effect is shown in the last row of Table 11.

The figures on bauxite production costs from Table 11 must be usedtogether with information on bauxite quality and ocean transport costs to therefineries in order to make comparisons on the convenience of using aparticular bauxite. This comparison is made in the sub-section on aluminarefining for selected bauxites and locations.

3.3 Investment and Operating Costs for Alumina

Capital costs for alumina refineries vary according to the type ofprocess required, to the location and to the plant dimensions. Table 12 showsa formula to determine approximate investment costs taking these factors intoaccount. Thus, an American Bayer type refinery of one million metric tons peryear capacity, located in the United States, would cost US$1,050 per ton ofalumina; while if capacity doubles it would cost US$890 per ton. A ModifiedAmerican Bayer type refinery in Jamaica would cost US$1,220 per ton for a 1million ton capacity, and US$1,030 per ton for a plant twice that size.Differences in capital costs between regions and processes may go as high asUS$340 per metric ton (not considering the soda-sinter process) equivalent toabout US$40 in annualized terms.

The main inputs for alumina refining are, as pointed out previously,bauxite, caustic soda (NaOH), lime (CaO), energy, labor, and other inputs(including filter aid, floculants and chemicals). These inputs have beenquantified in Table 14 for different bauxites according to the refiningprocess required, as well as to the quality of the bauxite. For simplicity,representative averages for bauxite/alumina ratios and silica content havebeen taken over groups of countries. These averages represent only in anapproximate way specific bauxite deposits in each country, as may be comparedwith original data shown in Table 1. Besides differences in bauxiterequirements and caustic soda consumption, energy consumption also varies,being somewhat higher for the Modified American Bayer and European Bayerprocesses. The soda sinter process which includes a Bayer plant plusadditional sintering stages consumes considerable energy. Labor inputs arealso somewhat higher for the Modified American and European Bayer processes,and significantly higher for the soda-sinter process.

The prices of inputs for alumina refining excluding labor are shownin Table 15. Estimates of labor costs for various countries are given inTable 16. Tables 14 to 16, together with the capital cost estimates, and withdata on bauxite costs from the previous section permit us to compute somerepresentative alumina refining costs for new plants which are shown in Table17. It may be appreciated that alumina refining is capital intensive withcapital charges representing about 33 percent of alumina costs. Because of

Table 11: TOTAL COSTS OF BAUXITE PRODUCTION, YEAR 2000

(US$/metric ton dry bauxite)

Western

United Suriname Europe EasternStates Jamaica Haiti Guyana (Bakhuis) Brazil Venezuela (Greece) Europe

Operating Cost 15.40 11.00 11.00 12.60 11.00 12.60 11.80 15.40 9.80

Capital Charges 5.70 4.20 4.20 5.80 4.20 5.80 5.10 5.80 5.80

Inland Transportation 1.00 0.2 0.50 2.80 5.70 4.80 5.20 8.00 1.30

Levy - 10.00 /a 22.80 - 21.20 - - - -

Total for Export 22.10 25.40 38.50 21.20 42.10 23.20 22.10 29.20 16.90

Less (for Local Processing):

Savings in Income Tax - 9.50 10.30 - 10.30 - - - -

Savings in Drying - 1.50 1.50 1.60 1.60 1.60 1.60 1.60 1.60

Total for Local Processing 22.10 14.40 26.70 19.60 30.20 21.60 20.50 27.60 15.30

a,i

Australia Australia Other Sierra

(Gove,Weipa) (West) India Indonesia China Asia Ghana Guinea Leone Cameroon

Operating Cost 10.20 10.20 8.10 8.10 8.10 8.40 10.90 10.30 10.30 10.30

Capital Charges 4.20 4.20 4.20 4.20 3.80 5.10 5.10 4.20 4.40 4.80

Inland Transportation 1.20 0.90 4.90 4.00 8.70 0.30 2.50 3.70 1.90 18.00

Levy - - - 1.40 - - 2.50 9.90 - -

Total for Export 15.60 15.30 17.20 17.70 20.60 13.80 21.00 28.10 16.60 33.10

Less (For Local Processing)Savings in Income Tax - - - - - - - - - -

Savings in Drying - 1.30 1.60 1.60 1.60 1.60 1.60 1.60 1.60 1.60

Total for Local Processing 15.60 14.00 15.60 16.10 19.00 12.20 19.40 26.50 15.00 31.50

/a Corresponds to levies applied to additional production.

Source: Computed from Tables 8 and 10. Data on levies from Section III.

- 27 -

Table 12: CAPITAL COST FOR ALUMINA REFINERIES

(US$ 1980)

Total capital cost including infrastructure and location factors.

Refinery Size Capital Cost

(Million tons per year) (Million US$)

0 - 2.0 pf x lf x (330 + 720 x size)2.0 - n x 2.0 pf x lf x( 885 x size)n x 2.0 - pf x lf x ( 1,062 x size)

where pf: process factor

Process Process Factor

American Bayer 1.0Modified A. Bayer 1.06European Bayer 1.12Soda-Sinter 1.30

lf: location factors from Table 13.

n: diseconomy of scale factor, between 2 and 5 depending on location.

Sources: Woods, D. "Financial Decision Making in the Process Industry,"Prentice Hall, New Jersey, 1975.

World Bank consultant.

- 28 -

Table 13: LOCATION FACTORS FOR CAPITAL COSTS FOR REFINERIES (IFR)AND SMELTERS

Country/Region Factors IFR and IFS

Western United States 1.00Eastern United States 1.00Western Canada 1.00Eastern Canada 1.00Western Europe 1.00Japan 1.10Eastern Europe 1.10Jamaica 1.10Oceania 1.10Central America (mainly Mexico) 1.10Suriname 1.10Brazil 1.10Argentina 1.10Venezuela 1.10Korea - Prov. of Taiwan 1.10India 1.10Rest of Asia 1.10South Africa 1.10Guyana 1.10ASEAN 1.10China 1.10North Africa 1.25Asian USSR 1.25Middle East 1.25Ghana 1.25Guinea 1.25Zaire 1.25Cameroon - Rest of Africa 1.25

Source: World Bank Consultant and Industry estimates.

- 29 -

Table 14: ALUMINA REFINERIES: PROCESSING AND INPUT REQUIREMENTS FOR SELECTED BAUXITES

(Per metric ton of alumina)

American Bayer

B. Suriname (Moengo,Paranam), Brazil,Venezuela, Indonesia,Ghana, Guinea (Fria), C. Suriname (Bakhuis) D. Western Australia

A. Guyana Sierra Leone Jamaica (Main Plateau) (Darling Range)

Bauxite, mt. (Dry Basis) 0.2 2.2 2.4 3.4

Caustic soda, mt. 0.11 (4% Si02) 0.9 (3% Sic2) 0.10 (3% SiO2) 0.07 (1.5% Sic2)(silica X)

Lime, mt. 0.1