Embed Size (px)

DESCRIPTION

Would the Balanced Scorecard have helped in recent financial scandals?

Citation preview

CIMA Financial Management

Would the Balanced Scorecard have helped?

Miss Archchana Vekneswaran - 12501207

Individual Assignment – Accounting and Management Control Systems

Date of Submission: 4th March, 2013

Submitted in partial fulfillment for the degree of

Bachelor of Arts (Hons) Sustainable Performance Management

Word Count: 2193

| March 2013 1

Would the Balanced Scorecard have helped?By: Archchana Vekneswaran

Overview

ue to significant changes in technology and product proliferation (Wongrassamme et al,

2003, p.14), companies started to evolve from being domestic to multinationals and into

global corporations (Dyment, 1987, p.20). During this process they had to find ways to achieve

sustainable competitive advantages in the volatile market by establishing proactive internal

controls and continuous performance improvements to suit the changes in each strategic business

units across national borders to match the global strategy (Wongrassamme et al, 2003, Lee &

Colbert, 1997 and Dyment, 1987).

D

BBC (2012) reported that “a number of scandals have engulfed the global financial

system” and various banking institutions are under investigations and scrutiny by regulators. As

Merchant & Van der Stede (2007, p.3) and Dyment (1987, p.20) argue, failed management

controls could bring in collateral damages like reputation risks and bankruptcy. Therefore

companies had to invest in methods which could provide higher return on investment (Ghalayini

and Noble, 1990 cited in Wongrassamme et al, 2003, p.14). One such model is Kaplan and

Norton’s “Balanced Scorecard” (BSC) – which celebrates its 20th anniversary. The following

article discusses about the model and the part it could have played in mitigating recent banking

scandals.

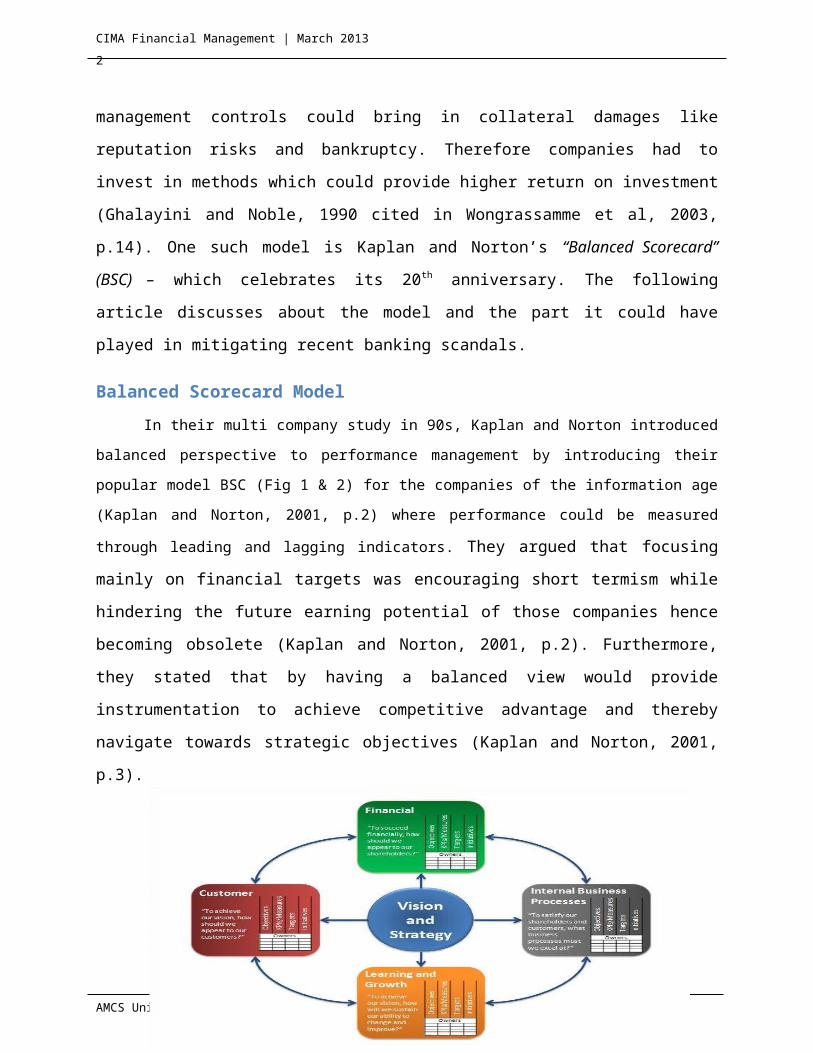

Balanced Scorecard Model

In their multi company study in 90s, Kaplan and Norton introduced balanced perspective to

performance management by introducing their popular model BSC (Fig 1 & 2) for the companies of the

information age (Kaplan and Norton, 2001, p.2) where performance could be measured through leading

and lagging indicators. They argued that focusing mainly on financial targets was encouraging

short termism while hindering the future earning potential of those companies hence becoming

obsolete (Kaplan and Norton, 2001, p.2). Furthermore, they stated that by having a balanced

view would provide instrumentation to achieve competitive advantage and thereby navigate

towards strategic objectives (Kaplan and Norton, 2001, p.3).

AMCS Unit Assessment - MMU

Balanced Scorecard - one of the versatile models – could have helped the global organizations such as HSBC and Barclays to avoid recent scandals and to drive towards corporate targets with

enhanced controls and sustainable performance management solutions.

| March 2013 2

AMCS Unit Assessment - MMU

| March 2013 3

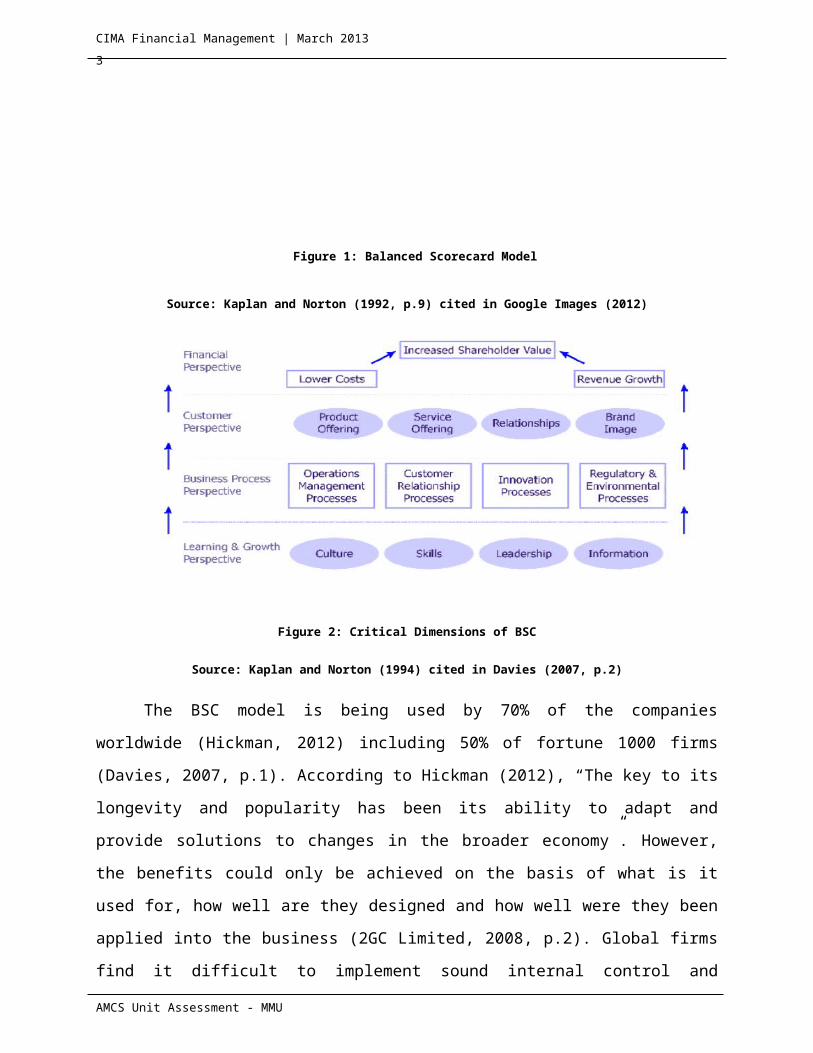

Source: Kaplan and Norton (1992, p.9) cited in Google Images (2012)

Figure 2: Critical Dimensions of BSC

Source: Kaplan and Norton (1994) cited in Davies (2007, p.2)

The BSC model is being used by 70% of the companies worldwide (Hickman, 2012)

including 50% of fortune 1000 firms (Davies, 2007, p.1). According to Hickman (2012), “The

key to its longevity and popularity has been its ability to adapt and provide solutions to changes

in the broader economy”. However, the benefits could only be achieved on the basis of what is it

used for, how well are they designed and how well were they been applied into the business

(2GC Limited, 2008, p.2). Global firms find it difficult to implement sound internal control and

performance measures. Such issues and how BSC could address these issues are discussed

below.

Difficulties in establishing effective controls and performance management in

global organizations

Maznevski et al (2007) exhibited four main complexities that lead to these control PM issues

in global firms:

AMCS Unit Assessment - MMU

Figure 1: Balanced Scorecard Model

| March 2013 4

Diversity

Global organization such as HSBC and Barclays face diversity from internal and external

sources where the management finds it difficult to manage each business unit in the similar way.

From the internal perspective, due to internationalization management of HR pool has to be

unique (Maznevski et al., 2007, p.1). Moreover, the ways in which each business unit achieves it

financial or corporate targets are different. There could be complexities in integrating managing

different management systems. External environment imposes diversity in terms of heterogenic

customer requirements and variation on stakeholder claims, diverse political, legal and

technological environment and varying degrees of competitor strategies (Maznevski et al., 2007,

p.1). Devising management controls while absorbing the diversities is difficult and the factors

are volatile in nature.

Interdependence

When the companies operate across borders interdependence increases to a greater extent where

each and every aspect of the business becomes related (Maznevski et al., 2007, p.2). Value webs

have replaced the value chains and other aspects of the business such as reputation, financial

flow, top management and corporate governance issues have reached their maximum while

erasing the boundaries of a company (Maznevski et al., 2007, p.2). Furthermore these issues

increase the reliance on each other and exposed companies such as HSBC to issues on frictions,

negative trends, loss in share price etc imposing difficulties in managing the companies in

effective manner (Maznevski et al., 2007, p.2.).

Ambiguity

Maznevski et al (2007, p.2) says “The business world today is characterized by too much

information with less clarity on how to interpret and apply insights”. Diversity in financial

standards along with studies surveys, scenarios etc. becoming less reliable due to volatile

business world, made the numeric figures and business forecasts ambiguous due to uncertainties

(Maznevski et al., 2007, p.2.). It is also found that many companies find it difficult to identify the

core value drivers of their existence making the cause – effect relationships less useful

(Maznevski et al., 2007, p.2.).

Flux

AMCS Unit Assessment - MMU

| March 2013 5

If the managers find ways to resolve above issues, the situation of business could change on the

very next day where the solution becomes outdated (Maznevski et al., 2007, p.2.). Companies

have to have ongoing monitoring process to continuously devise strategies to match the existing

control gap in organizations.

Lack of credibility

Supervisors of global workforce find it difficult to monitor all the staff to measure the

performance. Lack of knowledge, expertise, and understanding of the global context and poor

credibility of the feedback has diluted the effectiveness of PM (Rowley and Poon, 2009, p.1).

Furthermore, employees have to report to various superiors such as headquarters, country

manager, regional manager etc. has increased the challenges (Rowley and Poon, 2009, p.1).

Standardization of PM and national culture in workplace

Many organizations tries to standardize the PM systems across countries where the effectiveness

could be influenced by factors such as cultural differences, institutional isomorphism, global

integration V global adaptation, risk attitude etc. which questions the effectiveness of

standardized PM solutions (Rowley and Poon, 2009, p.2).

Above factors form the reasons behind why an effective control and PM system couldn’t be

established in global organizations like recent banking scandals. Could BSC have help to manage

the above issues while avoiding the scandals if it was implemented in the above banks? The

following section analyses tries to answer the above question.

Recent Banking Scandals and Failed Controls – A Recap

Money Laundering and Terrorist Financing– HSBC

The global banking giant HSBC is operating since 1865, with 89 million customers

across 85 countries (Dailymail, 2012). Today, a bank with such a long history has failed to

maintain sufficient Anti Money Laundering (AML) controls indicating insufficient awareness

over the ethical and lawful transactions (HK company law blog, 2013).

AMCS Unit Assessment - MMU

| March 2013 6

As per the Homeland Securities and Government Affairs (2012), “HSBC compliance

culture has been pervasively polluted for a long time” and analysts propose that “HSBC is too

large to manage in an effective manner” (HK company law blog, 2013). The US Senate

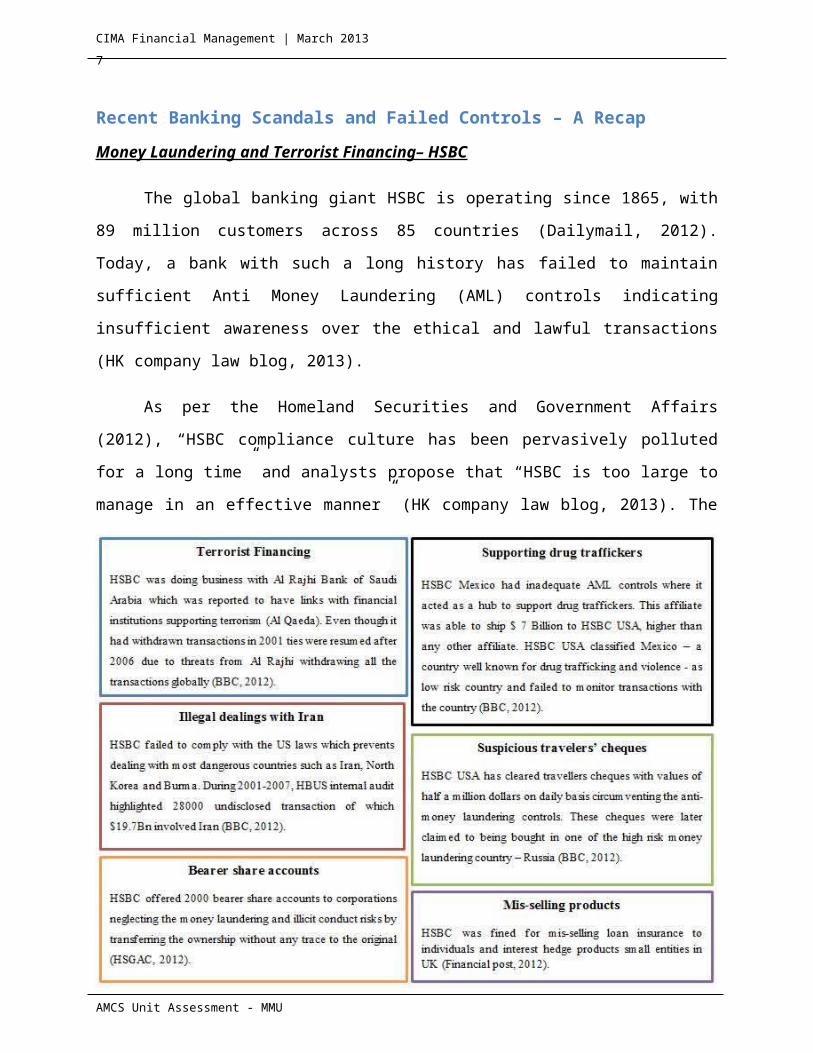

Committee reports that HSBC was guilty on following grounds:

Source: Compiled by Author based on US Senate Committee Repot (2012)

Due to above scandals HSBC was imposed with fines worth $2 billion, and a downgrade

on standards and poor outlook (BBC, 2012). It should be noted that having a proper AML

program incorporating AML internal controls, AML compliance officer, AML training and

independent testing on the AML program’s effectiveness would have prevented the bank from

facing legal consequences (US Senate, 2012). Financial Crisis Inquiry Commission (FCIC)

strongly believes that the crisis was mainly due to “human mistakes, misjudgments and misdeeds

that resulted in systemic failures” (Sathye, 2012).

AMCS Unit Assessment - MMU

Figure 3 : HSBC Scandals

| March 2013 7

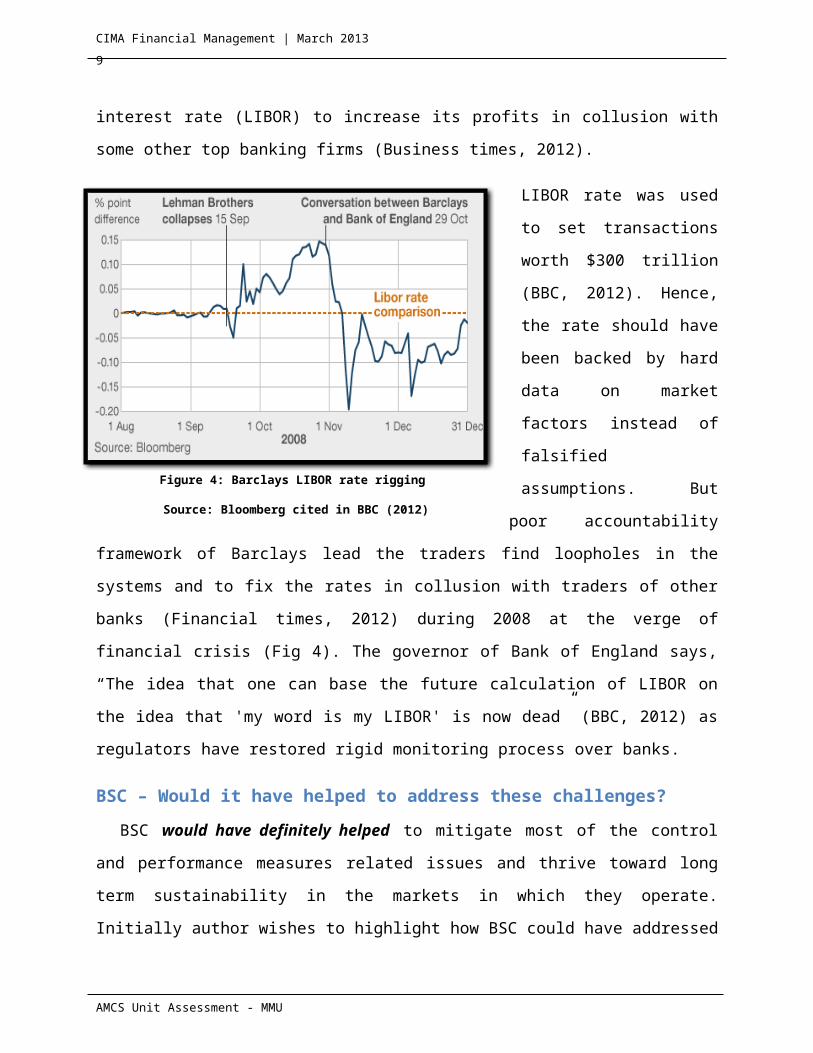

Manipulation of LIBOR – Barclays

With over 300 years of history of banking (Barclays, 2012), Barclays was one of world’s

renowned brands of all time. However, the corporate image was tarnished by consequences of

recent LIBOR rate rigging scandal and socked with $453 million to UK and USA regulators

(Business times, 2012). It was proved that the bank was involved in producing false reports to

manipulate the interest rate (LIBOR) to increase its profits in collusion with some other top

banking firms (Business times, 2012).

LIBOR rate was used to set

transactions worth $300 trillion

(BBC, 2012). Hence, the rate

should have been backed by

hard data on market factors

instead of falsified assumptions.

But poor accountability

framework of Barclays lead the

traders find loopholes in the

systems and to fix the rates in

collusion with traders of other

banks (Financial times, 2012)

during 2008 at the verge of

financial crisis (Fig 4). The governor of Bank of England says, “The idea that one can base the

future calculation of LIBOR on the idea that 'my word is my LIBOR' is now dead” (BBC, 2012)

as regulators have restored rigid monitoring process over banks.

BSC – Would it have helped to address these challenges?

BSC would have definitely helped to mitigate most of the control and performance measures

related issues and thrive toward long term sustainability in the markets in which they operate.

Initially author wishes to highlight how BSC could have addressed the challenges mentioned

above in implementing sound internal control and performance management solutions in global

firms.

AMCS Unit Assessment - MMU

Figure 4: Barclays LIBOR rate rigging

Source: Bloomberg cited in BBC (2012)

| March 2013 8

Diversity Management (DM)

According to Schmidt (2012), DM “involves the consideration and appreciation of diversity as

well as the active use and promotion of diversity to increase the economic success”. This helps to

match the differences and similarities in terms of strategic objectives of the company. Inclusion

of diversity in mission statement was highly appreciated by global work force and has resulted in

reduced absenteeism motivation and productivity (Schmidt, 2012). Few questions that could

become BSC controls related to DM are as follows (Schmidt, 2012):

Financial perspective: What are the costs of non- introduction of DM measures?

Customer perspective: How many diverse customer groups does the company serve?

Process perspective: What % does diversity contributes in profit generation and cost

cutting?

Staff and innovation perspective: How diversity has improved the productivity? How

many new innovations were proposed by diverse work teams?

Proactive promotions and cultural diversity appreciation has improved the learning and sharing

among heterogeneous groups and lead to innovations (Schmidt, 2012). It has helped many global

firms to address complex problems. But BSC alone would not ensure diversity but it should be

jointly used with other comprehensive DM models such as outcome mapping (Schmidt, 2012).

Internal Benchmarking (IB)

It is identified that interdependence of business units has imposed significant challenges. One

best way in which BSC could help global firms to resolve the challenge is by carrying out

internal benchmarking practices where one subsidiary in one destination is compared against the

best subsidiary of the specific global company. This balanced review on performance would

highlight the issues in subsidiaries and would help to decide solutions to be implemented to

reduce or avoid the existing issue in the subsidiary. For example, banking industry in Sri Lanka

is heavily regulated and monitored by Central Bank of Sri Lanka. So, HSBC USA could

benchmark its statutory controls against HSBC Sri Lanka.

Addressing ambiguity and flux

BSC could be implemented along with IT solutions which could be regularly updated with

external environment factors which could affect the performance of the global company. In this

way BSC could have helped to endure that the information is up to date and makes the forecasts,

AMCS Unit Assessment - MMU

| March 2013 9

controls and PM more reliable and less ambiguous. This BSC model could help to arrive at cause

and effect relationships which would help to identify the issues behind BSC perspectives and to

make informed decisions based on reliable sources.

Better PM feedback and learning

BSC helps the top level managers to identify how they could address the challenges enforced by

external environment. If a company couldn’t achieve its established targets then BSC requires

top management to look in the organizations resources and capabilities and establish necessary

measures to suit the new strategies. This process would act as a feedback loop to support

decision making at all levels (Procurement Executives Association, n.d).

It is essential to be noted that HSBC was using BSC to measure the performance of the

senior management says HSBC sustainability report 2007 which is known as an executive BSC

which is only a part of establishing a complete BSC program (Creamer and Freund, 2010,

p.366). However BSC program was not in place at Barclays. BSC could have helped in

following ways in avoiding banking scandals:

Positive change in management focus

HSBC and Barclays evaded most of the mandatory regulatory requirements due to short term

focus of the management to earn quick profits. Bruce (2012, p.18) states that corporate leaders

like a politician, see them in power for a shorter period of time and tries to focus on initiatives

that gives short term profits rather than sustainable longer term profitability. BSC encourages

management to switch focus on long term strategic objectives rather than shorter time horizon.

BSC has strategy at its core and could have helped the banks to focus on future rather than today.

Establishment of performance culture

A common criticism over the banking scandals is

that the corporate culture is polluted to a greater extent.

BSC would support the management to enhance a

strategy oriented performance culture throughout its

operations.

Treanor (2004) says that banks could deploy

diverse rewards systems whereas sales were the only angle of HSBC. When BSC implemented,

AMCS Unit Assessment - MMU

“The beauty of BSC is that the act of measurement forces somewhat vague and ambiguous concepts such as culture to be defined precisely”

Kaplan and Norton (2004)

| March 2013 10

US and European subsidiaries would change their focus to other strategic indicators their

respective business (Mooraj et al, 1999, p.483) rather than short term preferences. This attitude

could have been changed by performance driven culture imposed by BSC. Due to the switch in

culture, the attitude towards innovation, collaboration and teamwork, rewards and incentives,

risk attitudes etc would change favourably and align employee performance to strategy of the

banks.

Enhanced performance management

BSC would have helped to move from performance measurement to performance management

(Procurement Executives Association, n.d). Senior management would get involved in the

process of developing PM systems which are linked to company’s achievement of four key

perspectives as per BSC and strategy at the end. Employees would get better understanding on

what they should and should not do to reach the set targets. Employees who reached the target

could be awarded with monitory or non-monitory rewards as token of appreciation. By this the

rewards would be aligned to the overall strategy of the banks.

BSC would also improve the accountability of the staff as they gain a sense of ownership

when individual attainment of target helps the organization in achieving the corporate targets.

However, the individual should have required skills and should be given with necessary authority

to perform their targets to remain accountable. In the context of HSBC, certain compliance

division consisted of inexperienced divisional heads and staff without authorities to handle their

duties (US Senate, 2012) which indicate that HR policies should be adjusted first to reap the

benefits of accountability.

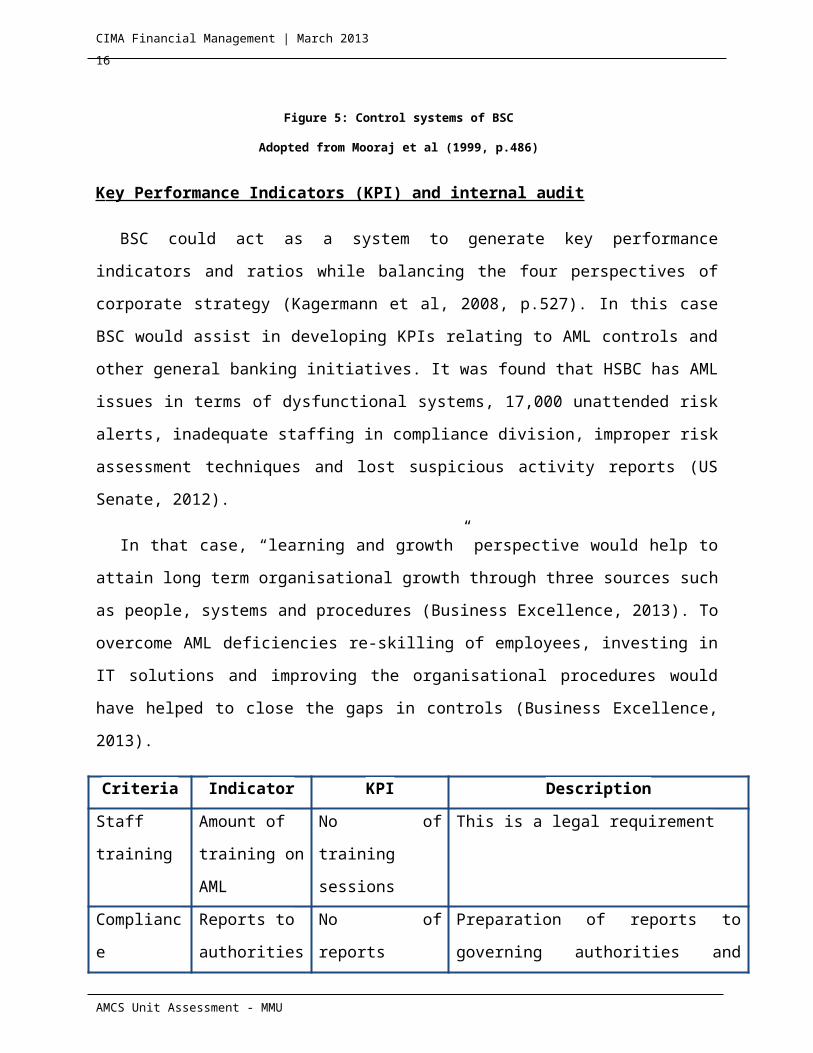

Better control environment

Both companies under review has suffered poor control environment as indicated by the

failed controls. BSC consists of 3 control mechanisms which help the management to keep track

of the day to day operation of the banks as indicated in Fig 5 below.

Interactive control systems enable the management to conduct 3600 feedback control over the

activities and to interact with the related parties such as customers and staff to ensure controls are

in place and to make necessary changes (Mooraj et al., 1999, p.486). If this was in place HSBC

could have avoided terrorist financing activities and Barclays could have mitigated risks of

falsified reports used for rate rigging.

AMCS Unit Assessment - MMU

| March 2013 11

Diagnosis lagging controls would have helped to trace whether necessary objectives were

reached as expected without any irregularities. This might have helped to trace financing

activities from Mexican HSBC and analyze into sources to avoid money laundering.

Boundary controls ensures that all the employees are very familiar with the intended

objectives and vision of the banks which could have eliminated the sub optimization due to self-

interest prioritized over the company’s strategies especially in the case of Barclays where traders

acted in misconduct to raise their bonuses through rate rigging mechanisms.

K ey Performance Indicators (KPI) and internal audit

BSC could act as a system to generate key performance indicators and ratios while balancing

the four perspectives of corporate strategy (Kagermann et al, 2008, p.527). In this case BSC

would assist in developing KPIs relating to AML controls and other general banking initiatives.

It was found that HSBC has AML issues in terms of dysfunctional systems, 17,000 unattended

risk alerts, inadequate staffing in compliance division, improper risk assessment techniques and

lost suspicious activity reports (US Senate, 2012).

In that case, “learning and growth” perspective would help to attain long term organisational

growth through three sources such as people, systems and procedures (Business Excellence,

2013). To overcome AML deficiencies re-skilling of employees, investing in IT solutions and

improving the organisational procedures would have helped to close the gaps in controls

(Business Excellence, 2013).

AMCS Unit Assessment - MMU

Figure 5: Control systems of BSC

Adopted from Mooraj et al (1999, p.486)

| March 2013 12

Criteria Indicator KPI Description

Staff training Amount of

training on

AML

No of training

sessions

This is a legal requirement

Compliance Reports to

authorities

No of reports Preparation of reports to governing

authorities and reports leading to

prosecution

Management

of AML

effectiveness

Comparison of

AML controls

per reqirement

Number of updates

and checking on

AML effectiveness

Qualitative reports and numeric assessments

has to be conducted

Table 1: KPIs for AML controls

Source: Adopted from Schoenbein et al (2001)

Due to comprehensive nature and integration of qualitative measures, BSC could accelerate

KPI based internal audit (Kagermann et al, 2008, p.528). Internal audit is one of the statutory

requirements for any registered company which indicates that KPI based internal control issues

could have been tracked in the case of banking scandals.

Enhanced risk management

It is visible that poor risk management in the organizations has also lead the companies

towards legal consequences due to events such as negligence of alerts, knowingly producing

false reports, poor client checks which lead to drug money laundering disputes and evading laws

and regulations etc.

BSC would have helped the top management to develop strategic maps where each input,

process and outcomes of every move of the company is clearly defined (Frigo, 2012, p.52). Then

the management could be able to identify “strategic risks” associated with each and every

component after which these risks elements could be placed in a 2X2 risk map by giving scale

based on likelihood and severity (Frigo, 2012, p.53). By this management could identify and

devise plans to mitigate the risks. The above control could have enhanced the control

environment of the banks under review and would have satisfied one of the requirements of

Sarbanes Oxley Act USA by ensuring a sound control environment which would have mitigated

certain control issues.

AMCS Unit Assessment - MMU

| March 2013 13

BSC as a self-diagnosis tool accompanied by strategic maps treats risk management as senior

management’s responsibility rather than compartmentalizing risk areas into functional categories

(Frigo, 2012, p.53). This practice would have enhanced comprehensive integrated process of risk

management process (Frigo, 2012, p.53) across the organization and to establish sophisticated

risk control to avoid irregularities and to protect the corporate reputation.

Benefits vs. Limitations of BSC

Some additional benefits of adopting BSC as control and performance measurement tool are

discussed below:

BSC requires active involvement of the users throughout its designing process which makes

the framework more comprehensive (2GC Limited, 2008, p.2) thus would improve stakeholder

confidence due to transparency in reporting and would also improve the corporate governance

dimension (BSC Institute, 2012, p.1).

Due to immense competition in today’s business world, it is essential for a company to focus

and invest in intangible intellectual sources such as research and development, IT technology,

branding and persuasive marketing initiatives (Pandey, 2005, p.64). As BSC’s leading indicators

provide logic to achieve these intellectual assets it would help the banks drive towards the future

and sustain in their respective markets (Pandey, 2005, p.65). BSC links three leading indicators

which are hard to manipulate due to intangible nature and day to day monitoring hels to avoid

window dressing.

Having analyzed the benefits of the model, it should also be noted that the model consists

of certain limitations which has to be considered.

1. Requires change management

BSC implementation process is a transformational change initiative where long term

commitment has to be required in terms of generating metrics to measure performance.

Employees have to be educated and should be trained to adapt to BSC environment. This is

timely and expensive (Murphy and Gould, 2005, p.24). Employee resistance to such significant

change by which their performance are going to monitored, conflicts within the organizations

which might end up conflict of interest dilemma.

AMCS Unit Assessment - MMU

| March 2013 14

2. Key personnel change would question the sustainability

BSC requires significant involvement from the top management when implementing and

reporting the findings. Key personnel would also determine underlying principle and how the

performance is going to be managed (Murphy and Gould, 2005, p.25). If there are any changes in

the top management, BSC initiatives can falter if the new management has totally different view

on performance evaluation. So it is essential to ensure that the new management is not deviating

from company’s original initiatives towards BSC (Murphy and Gould, 2005, p.25).

3. Inward Focused

It should also be noted that inward focused measure (Murphy and Gould, 2005, p.26). It avoids

integrating changes in the external environment such as in SWOT or PESTEL measures.

4. Difficulties in establishing linkages

Another criticism on the BSC is that it is difficult to establish linkages between the four

perspectives put forward by Kaplan and Norton (Murphy and Gould, 2005, p.25). There could be

unidentified time lags between the actions taken and results generated while trying to create

linkage between financial and non-financial measures and this would be pointless when devising

decisions (Murphy and Gould, 2005, p. 25).

5. Other limitations

Most organizations try to implement BSC simply because their competitors are doing it. This

would erode the popularity of the model because every company is unique and requires well

built in performance metrics. Furthermore, if departments (marketing, HR etc.) are allowed to

devise their own BSC measures based on what they know well it would lead to lack of goal

congruence as the measures would not lead the overall company towards the corporate strategy

but only the departments to reach individual targets.

It is evident that BSC could act as a useful tool if carefully devised. However, global

firms face tremendous pressures and complexities in implementing such sound measures to

control the performance and to keep the company on the path to reach the corporate objective.

AMCS Unit Assessment - MMU

| March 2013 15

Recommendations

In order to attain the benefits from BSC author recommends global firms to adapt to risk

based IT driven BSC systems in their operations. This BSC is also known as 4 th generation BSC

(Tomura, 2006) which integrates internal control requirements per regulations such as Sarbanes

Oxley Act in USA, with risk elements by operating on IT platform (Fig 6). As discussed above

BSC would be a solution for most of the control and performance management concern of global

firms.

Figure 6: 4th Generation Balances Score Card

Source: Tomura (2006)

As per the above diagram, the integration of internal control and risk would help the

global organizations to address statutory as well as internal requirements where as usual BSC

itself helps to reach PM targets. KRI and KCI could be established with owners and could act as

an effective tool in internal audit programs and to trace the accountability of any failed control.

This could also act as an effective communication medium with stakeholders to ensure that

company has been undertaking regular internal control reviews which enhance transparency

(Tomura, 2006). Integration of risk aspects to the traditional BSC would enhance the detection

and rectification of risk due to the use of IT software (Tomura, 2006). Preventive measures taken

AMCS Unit Assessment - MMU

| March 2013 16

to control the irregularities would lead to Kaizen for the next period due to step by step

improvement in organisational performance (Tomura, 2006).

It should be noted that in order reach the benefits of successful BSC there are certain

prerequisites that the global firms should consider. Initially the top management should have

wide knowledge on the reason why they are implementing BSC and they should be committed

throughout the process (Pandey, 2005, p.63). This would act as a cultural control where the

management gives the impression that it is committed for better performance. Next the

companies should be able to identify what are the critical success factors (CSF) that drive the

organization’s success and clearly define metrics to suit each factor (Pandey, 2005). A best

example could be Toyota which drives through quality in each of its operations (Maznevski et

al., 2007, p.4). Companies should also have a sophisticated tracking system to measure the

performance and to enhance controls. If these prerequisites were met implementing BSC would

drive the company towards success.

As global companies are subject to complexities due to borderless operations, author

recommends if possible the management structure could be decentralized to a certain extent

where the country managers would have the autonomy to devise BSC measures that best suits

the nation’s conditions while country’s manager’s performance could be measured by regional

headquarters.

In the case of Barclays and HSBC, quick profit motive has hindered the performance of

the companies. As per Tilley (2012, p.65), “individual bonuses should be paid in equities and

placed into their pensions….. Executive incentive schemes that encouraged excessive risk taking

and short term gains directly contributed to the economic crisis”. It is essential that the

remuneration packages should be linked performance based on BSC to avoid short termism

(Pandey, 2005, p.63).

Apart from the additions to the conventional BSC model, global firms and especially the

banks should give more attention towards their recruitment policies. This is because in order

maintain good code of conduct and performance culture exceptional professionalism is required.

Even a very sound control could be evaded by collusion between individuals or institutions such

as in the case of rate rigging scandal where Barclays collided with several other firms to

manipulate the LIBOR rate. However, Barclays has decided to recruit based on good citizenship

tests and decided to redesign their compensation policies by basing them on BSC where

AMCS Unit Assessment - MMU

| March 2013 17

performance would be measured through reputation and business conduct test and client

satisfaction ratings (telegraph, 2012). This should be welcomed and sustained in future.

Individuals should also be given necessary authority to be accountable for their duties.

Failed controls in the banking scandals were due to intentional fraudulent activities. In

order overcome this, anti – fraud culture should be promoted with sound anti-fraud controls such

as segregation of duties, authorization, physical controls etc. These measures could also be

integrated into BSC framework and could be monitored on a daily basis. It should also be

encouraged to nurture whistleblowers to fight irregularities by rewarding them appropriately

(Bartram, 2012, p.36). Mystery shoppers could also be established confidentially to check the

vigilance of the front end officers.

However, it is worth mentioning that the regulatory bodies were not efficient and vigilant

enough to track the loopholes in their operations and regulations. So, the governments of

respective countries should carryout robust restructuring to their usual monitoring process to

avoid any further scandals and financial crisis which has a chain effect on all over the world.

Conclusion

As per Treanor (2012), "Capital requirements, loan ratios, buffers, and ring-fencing are

important but not sufficient to restore confidence in our banking system. We also need a fresh

approach from the banks themselves”. One such reform is BSC which ensure sound internal

controls aimed at long term corporate targets and performance measures. It was identified that

this 20 year old model holds greater insights which with slight modifications could be adopted

by any firm to retain its market position. It would have definitely been able to play a vital role in

avoiding certain global banking scandal issues.

AMCS Unit Assessment - MMU

| March 2013 18

References

2GC Active Management (2012). What are the main benefits of a balanced scorecard? [Online]. Available from: http://2gc.eu/files/resources/2GC-FAQ2-080901.pdf [Accessed: 20th December, 2013]

Amaratunga, D., Haigh, R., Sarshar, M., and Baldry, D. (2002), Application of the balanced scorecard concept to develop a conceptual framework to measure facilities management performance within NHS facilities , International Journal of Health Care Quality Assurance, Vol. 15 Iss: 4 pp. 141 – 151

Barclays (2012). About Barclays Group [Online] Available from: http://group.barclays.com/about-barclays/about-us#barclays-history [Accessed: 26th December 2012]

BBC (2012). Libor – what is it and why does it matter? [Online] Available from: http://www.bbc.co.uk/news/business-19199683 [Accessed: 20 th December 2012]

BBC (2012). Standard & Poor's downgrades outlook for HSBC [Online] Available from: http://www.bbc.co.uk/news/business-19366415 [Accessed: 25 th December 2012]

BBC (2012). Timeline: Libor fixing scandal [Online] Available from: http://www.bbc.co.uk/news/business-18671255 [Accessed: 24th December 2012]

BBC. (2012). Global banking scandals: Who is under scrutiny?. [Online] Available from: http://www.bbc.co.uk/news/business-19323954 [Accessed: 10th December 2012]

BBC. (2012). HSBC money laundering report: Key findings [Online] Available from: http://www.bbc.co.uk/news/business-18880269 [Accessed: 20th December 2012]

Bonaque, B. (2012). The List. CIMA Financial Management. September 2012. P.36.

Bruce, B. (2012). Opinion. CIMA Financial Management. September 2012. P.18.

Business Excellence. (2012). The Balanced Scorecard. [Online] Available from: http://www.bexcellence.org/balanced-scorecard.html [Accessed: 19 th January 2013]

Business Time (2012). The Barclays LIBOR Scandal Is a Clear Case for Greater Consumer Protection [Online] Available from: http://business.time.com/2012/06/29/the-barclays-libor-scandal-is-a-clear-case-for-greater-consumer-protection/#ixzz2JXWqPUMd [Accessed: 29th December 2012]

Cremer, G. and Freund, Y. (2010). Learning a board balanced scorecard to improve corporate performance. Decision Support Systems. 49 (2010) p. 365–385.

Dailymail. (2012). HSBC let drug gangs launder millions: First Barclays, now Britain's biggest bank is shamed - and faces a £640 million fine. [Online] Available from: http://www.dailymail.co.uk/news/article-2174785/HSBC-scandal-Britains-biggest-bank-let-drug-gangs-launder-millions--faces-640million-fine.html#ixzz2JXL8toQh [Accessed: 23rd December 2012]

Davies, R. (2007). The Balanced Scorecard – Panacea or Poisoned Chalice? [online]. Available from: http://www.drrobertdavies.com/071128%20BALANCEDSCORECARD.pdf [Accessed: 19th December, 2012]

Dyment,J. (1987), Strategies and management controls for global corporations", Journal Strategy, Vol. 7 Iss: 4 p. 20 – 26

Financial Post. (2012). HSBC’s ‘shameful and embarrassing’ scandal to cost over $2-billion [Online] Available from: http://business.financialpost.com/2012/07/30/hsbcs-shameful-and-embarrassing-scandal-to-cost-over-2-billion/ [Accessed: 23rd December 2012]

Financial Times (2012). Tricky lessons for the players in Liborgate [Online] Available from: http://www.ft.com/cms/s/2/666bd90e-d006-11e1-bcaa-00144feabdc0.html#ixzz2HD0GrlB4 [Accessed: 21st

December 2013]

AMCS Unit Assessment - MMU

| March 2013 19

Frigo, M. L. (2012). The Balanced Scorecard: 20 years and counting. Strategic Finance. October 2012. P. 49 – 53

Google Images (2012). BSC Model [Online] Available from: http://www.google.lk/imgres?hl=en&sa=X&tbo=d&biw=1517&bih=752&tbm=isch&tbnid=CtQ5oWz0kKLOIM:&imgrefurl=http://www.smartkpis.com/blog/2010/05/&docid=m96QPKZAcLzcHM&imgurl=http://www.smartkpis.com/blog/wp-content/uploads/BSC-concept-BalancedScorecardReview.com_.jpg&w=771&h=579&ei=F_T3UL-GF8PRrQfnrYA4&zoom=1&iact=hc&vpx=192&vpy=142&dur=401&hovh=141&hovw=200&tx=148&ty=96&sig=111948838829519768685&page=1&tbnh=141&tbnw=200&start=0&ndsp=30&ved=1t:429,r:24,s:0,i:157 [Accessed: 20th December 2012]

Hickman, A., (2012). Norton: Balanced Scorecard must adapt to remain relevant.[online] Available from: http://www.cgma.org/Magazine/News/Pages/20126794.aspx?cm_mmc=CGMANL-_-09Nov12-_-Features-_ Norton&utm_source=cgmanl&utm_medium=09Nov12&utm_term=features&utm_content=Norton&utm_campaign=cgmanl [Accessed: 4th December, 2012]

HK Company Blog. (2012). Whose responsibility? The aftermath of HSBC scandal. [Online] Available from: http://hkcompanylawblog.com/2012/11/07/whose-responsibility-the-aftermath-of-hsbc-scandal/ [Accessed: 26th

December 2012]

Homeland Securities and Government Affairs. (2012). HSBC Exposed U.S. Financial System to Money Laundering, Drug, Terrorist Financing Risks [Online] Available from: http://www.hsgac.senate.gov/subcommittees/investigations/media/hsbc-exposed-us-finacial-system-to-money-laundering-drug-terrorist-financing-risks [Accessed: 20th December 2012]

HSBC (2007). Footprint Management – Sustainability Report [online]. Available from: http://reports.investis.com/reports/hsbc_sr_2007_en/pdf_cache/hsbc_sr_2007_en_extract_20.pdf [Accessed: 19th

January, 2013]

Kagermann, H et al (2008). Internal Audit Handbook. [Online] Heidelberg: Springer. Available from: http://books.google.lk/books?id=R8kzyri7ULwC&pg=PA527&lpg=PA527&dq=internal+controls+and+balanced+scorecard&source=bl&ots=sdNT-F6QzV&sig=Bfb1SeaIHD0C-811DVlJBHtKYkY&hl=en&sa=X&ei=p6P6UPWULYjirAe4wwE&ved=0CEMQ6AEwBA#v=onepage&q=internal%20controls%20and%20balanced%20scorecard&f=false [Accessed: 10 th January 2013]

Kaplan, R. S and Norton, D. P, (1996). Translating Strategy into Action: The Balances Scorecard. [Online] USA: Library of Congress Cataloging. Available: http://books.google.lk/books?hl=en&lr=&id=mRHC5kHXczEC&oi=fnd&pg=PR7&dq=Balanced+Score+Card&ots=ww3Xz7D4Ne&sig=UH_DRaG5OlBST18GLI2g5FJM4pA&redir_esc=y [Accessed: 20th December 2012]

Kaplan, R. S. and Norton, D.P (2004), Organization Capital: Supporting the change agenda that supports strategy execution, Balanced Scorecard Report, Vol 6 Iss: 1 p.1-16

Lee,M. and Colbert,J. (1997),"Analytical procedures: management tools for monitoring controls", Management Decision, Vol. 35 Iss: 5 pp. 392 – 397

Maznevski, M., Stegar, U. and Amann, W (2013), Manageing complexity in global organisations [online]. Available from: http://www.ft.com/intl/cms/d38ba8ea-d933-11db-9b4a-000b5df10621.pdf [Accessed: 19th January, 2013]

Merchant, K. A and Van der Stede, W.A, (2007). Management Control Systems: Performance Measurement, Evaluation and Incentives. Harlow: Pearson Education.

Murby, L and Gould, S (2005). Effective performance management with balanced scorecard: Technical Report, UK: CIMA

Pandey, I.M (2005). Balanced Scorecard: Myths and Reality, Vikalpa, Vol 30 (1) p. 51 – 66.

AMCS Unit Assessment - MMU

| March 2013 20

Procurement Executives’ Association (n.d). Guide to balanced scorecard performance management methodology. [Online]. Available from: http://energy.gov/sites/prod/files/maprod/documents/BalancedScorecardPerfAndMeth.pdf [Accessed: 5th February, 2013]

Punniyamoorthy, M. and Murali, R. (2008), Balanced score for the balanced scorecard: a benchmarking tool, Benchmarking: An International Journal, Vol. 15 Iss: 4 pp. 420 – 443

Rowley, C. and Poone, I. (2012). Performance Management for a Global Workforce: Aspects and Business Implications. [Online]. Available from: http://www.slideshare.net/Jackie72/performance-management-for-a-global-workforce-aspects-and [Accessed: 5th December, 2012]

Sathye. M, (2012). HSBC’s money laundering scandal is more than just risky business practice [Online] Available from: http://theconversation.edu.au/hsbcs-money-laundering-scandal-is-more-than-just-risky-business-practice-8309 [Accessed: 24th December 2012]

Schimidt, B.V (2012). Diversity Management and Balanced Scorecard. [Online]. Available from: http://www.idm-diversity.org/eng/infothek_schmidt_scorecard.html [Accessed: 6th January, 2013]

Schoenbein, O.S, Braunschweig, A., and Oetterli, G (2001). Social performance indicators for the financial industry. [Online] Zurich: E2 Management Consulting Ltd. Available from: http://www.logro.sk/na_stiahnutie/kpis_banks.pdf [Accessed: 3rd January 2013]

Schoenbein, O.S., Braunschweig, A. and Oetterli, G. (2001). Social and Performance Indicators for the financial industry [online]. Available from: http://www.logro.sk/na_stiahnutie/kpis_banks.pdf [Accessed: 20th December, 2013]

Telegraph (2012). Barclays slashes banker’s pay upto halfas profits fall. [Online]. Available from: http://www.telegraph.co.uk/finance/newsbysector/banksandfinance/9638367/Barclays-slashes-bankers-pay-by-up-to-half-as-profits-fall.html [Accessed: 6th December, 2012]

Tilley, C. (2012). CEO Column. CIMA Financial Management. September 2012. P.65.

Tomura, T. (2006). Beyond Sarbans – Oxley: Improving corporate value with a 4th generation BSC approach. [Online]. Available from: http://www.bptrends.com/publicationfiles/TWO%2012-06-ART-The4thBSCforSOX-Tomura.pdf [Accessed: 6th February, 2013]

Treanor, J. (2012). John Vickers says George Osborne's banking reforms don't go far enough. The Guardian. 14th

June. Available from: http://www.guardian.co.uk/business/2012/jun/14/vickers-george-osborne-banking-reforms [Accessed: 12 th January 2013]

US Senate (2012). U.S. Vulnerabilities to Money Laundering, Drugs, and Terrorist Financing: HSBC Case History. Washington : Permanent Subcommittee on Investigations

Wongrassamee, S., Gardner, P.D., and Simmons, J.E.L (2003), Performance Measurement tools: The balanced scorecard and business excellence model. Measuring Business excellence, Vol 7 (1) p14-29

AMCS Unit Assessment - MMU