Embed Size (px)

Citation preview

www.smithsdetection.com © 2009 by Smiths Detection: Proprietary Data

Smiths Detection Investor Day

Wiesbaden, 27 January 2009

Opportunities to create value

© 2009 by Smiths Detection: Proprietary Data | 2

Philip Bowman,Chief Executive, Smiths Group Plc

© 2009 by Smiths Detection: Proprietary Data | 3

Observations on Smiths Detection: an attractive business model

Global market leader with leading edge technologies

Presence in all the key Detection segments

Strong growth track record

Growth driven by threats, legislation & new technologies - provides some resilience

Strong routes to market based on customer relationships and reputation

Expertise in complex product engineering

© 2009 by Smiths Detection: Proprietary Data | 4

Objectives for today

Outline the business strategy

Explore the key drivers of future growth

Demonstrate how we are managing the growth challenges

Recent developments in R&D

Visit our manufacturing facility and product demonstrations

Opportunity to meet the management team

1

2

3

4

5

6

© 2009 by Smiths Detection: Proprietary Data | 5

Stephen Phipson, President, Smiths Detection

© 2009 by Smiths Detection: Proprietary Data | 6

Today’s agenda

• 08:30 - Presentation

• Stephen Phipson -Covering the dynamics of the business

Cherif Rizkalla, Security & Inspection operationsMal Maginnis, Military & Emergency response operationsBill Mawer, Diagnostics.

• Q & As

• 11:00 - Transfer to Smiths Detection facility

• 11:30 - Tour of X-ray R&D and manufacturing facilities, including product demonstrations

• 13:00 - Lunch

• 14:00 - Transport to airport

© 2009 by Smiths Detection: Proprietary Data | 7

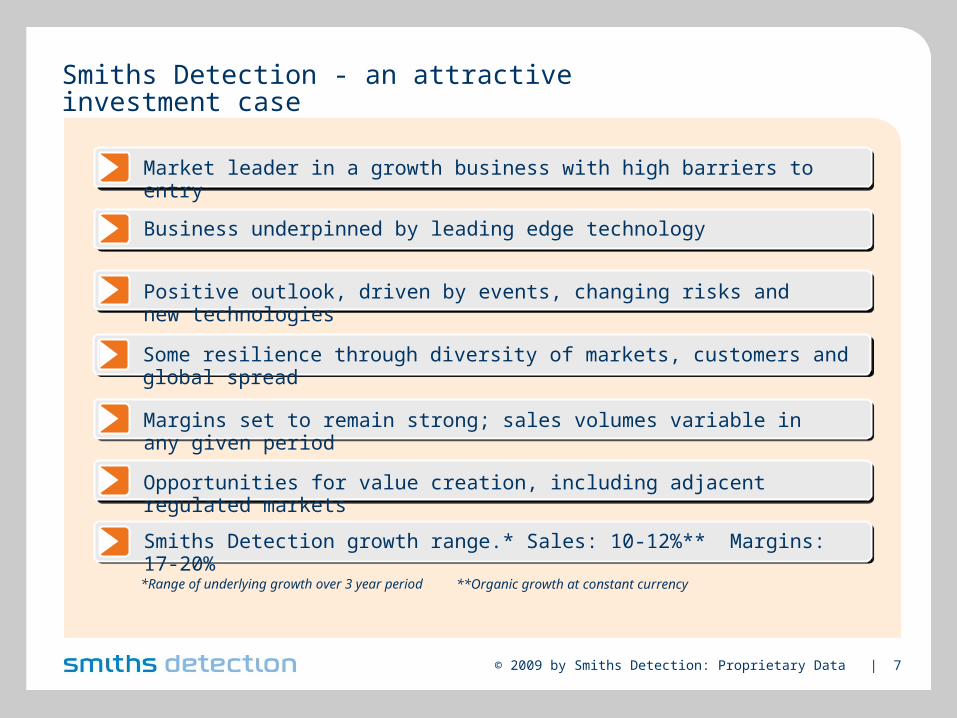

Smiths Detection - an attractive investment case

Market leader in a growth business with high barriers to entry

Smiths Detection growth range.* Sales: 10-12%** Margins: 17-20%

**Organic growth at constant currency *Range of underlying growth over 3 year period

Positive outlook, driven by events, changing risks and new technologies

Business underpinned by leading edge technology

Some resilience through diversity of markets, customers and global spread

Margins set to remain strong; sales volumes variable in any given period

Opportunities for value creation, including adjacent regulated markets

© 2009 by Smiths Detection: Proprietary Data | 8

Smiths Detection historical overview

Smiths Detection is:

• The world leader in the provision of Government regulated systems to detect and identify CBRNE materials - more than double the size of its nearest competitor.

• A prime contractor with 85% of sales to more than 100 governments globally

CBRNE: Chemical, biological, radiological, nuclear, explosives

Sales growth since 2001 (£m)

Underlyinggrowth

Financial performance 2008

£m

Sales 509 +12%

Trading profit 93 +2%

Margin 18%

© 2009 by Smiths Detection: Proprietary Data | 9

Worldwide security market ~ £75bn

Personnel services - guards, consultancy, etc…

Other: e.g. access control. IT security, fire & alarm, etc

We compete in ~ 4% of the market

SensorsSensors Sensorintegration

Sensorintegration

Sensornetworking

Sensornetworking

Total systems

Total systems

Expanding theaddressable market

Where Smiths Detection sits in the security sector

£3.5bn

Detectionsystems

© 2009 by Smiths Detection: Proprietary Data | 10

Transportation

Military

Emergency responders

Ports & Borders

Critical infrastructure

Non-security

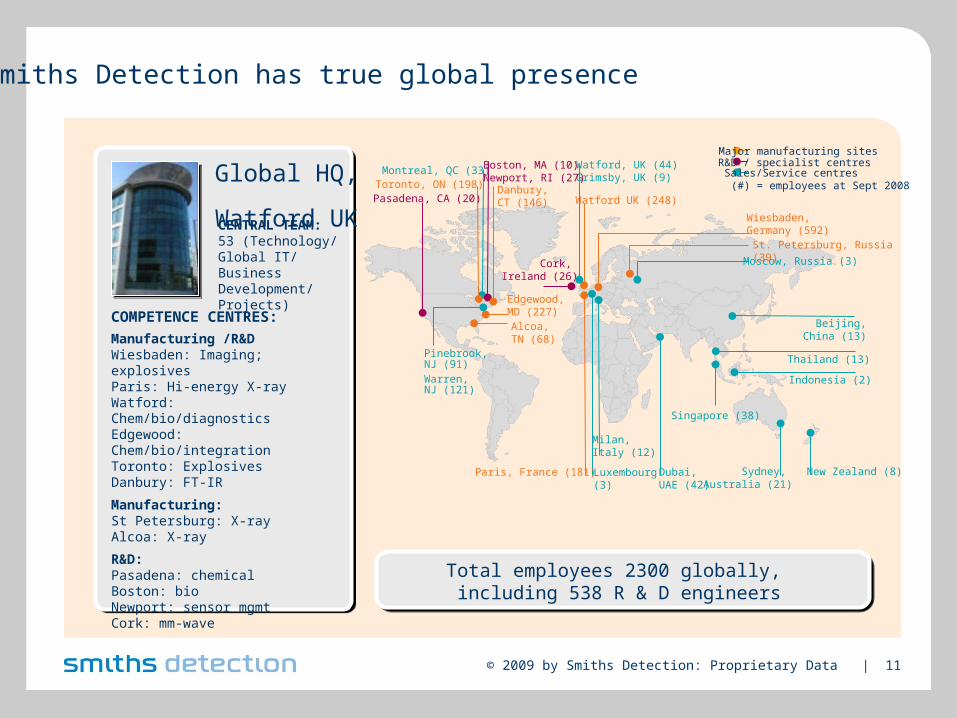

Smiths Detection fact file

Sales 2008: £509m

Americas

RoW

EU

• 8 manufacturing centres occupying 86,500 sq metres/0.9m sq. ft. 14 regional sales offices

• Sales to 160 countries

• R&D in 6 countries

• 2300 employees

• 538 engineers and scientists

By sector By geography

© 2009 by Smiths Detection: Proprietary Data | 11

COMPETENCE CENTRES:

Manufacturing /R&DWiesbaden: Imaging; explosivesParis: Hi-energy X-rayWatford: Chem/bio/diagnostics Edgewood: Chem/bio/integrationToronto: Explosives Danbury: FT-IR

Manufacturing: St Petersburg: X-ray Alcoa: X-ray

R&D: Pasadena: chemicalBoston: bioNewport: sensor mgmtCork: mm-wave

Global HQ, Watford UKCENTRAL TEAM:53 (Technology/ Global IT/ Business Development/ Projects)

Major manufacturing sites

Sales/Service centres(#) = employees at Sept 2008

R&D / specialist centres

Pinebrook, NJ (91)Warren, NJ (121)

Sydney, Australia (21)

Montreal, QC (33) Watford, UK (44)Grimsby, UK (9)

Dubai,UAE (42)

New Zealand (8)

Thailand (13)

Beijing, China (13)

Indonesia (2)

Singapore (38)

Pasadena, CA (20)

Boston, MA (10)Newport, RI (27)

Cork, Ireland (26)

Danbury,CT (146)

Alcoa, TN (68)

Edgewood, MD (227)

Wiesbaden,Germany (592)

Paris, France (181)

Watford UK (248)

St. Petersburg, Russia (39)

Milan, Italy (12)

Luxembourg(3)

Toronto, ON (198)

Total employees 2300 globally, including 538 R & D engineers

Moscow, Russia (3)

Smiths Detection has true global presence

© 2009 by Smiths Detection: Proprietary Data | 12

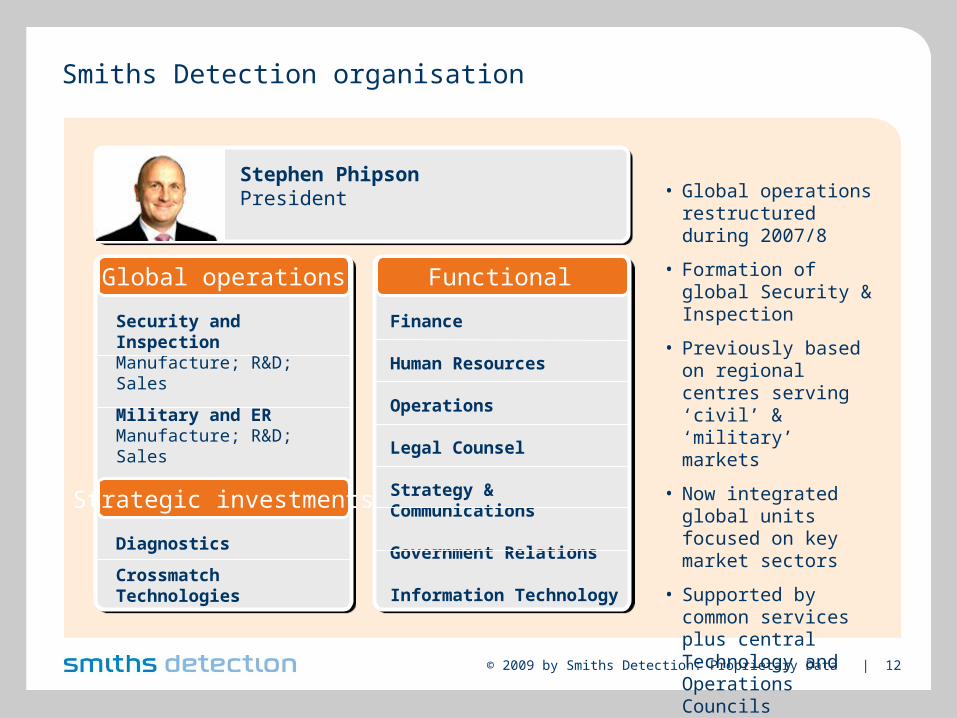

Smiths Detection organisation

Stephen Phipson President

Security and InspectionManufacture; R&D; Sales

Military and ERManufacture; R&D; Sales

Asia Pacific, Sales

Global operations

Diagnostics

Crossmatch Technologies

Strategic investments

Functional

Finance

Human Resources

Operations

Legal Counsel

Strategy & Communications

Government Relations

Information Technology

• Global operations restructured during 2007/8

• Formation of global Security & Inspection

• Previously based on regional centres serving ‘civil’ & ‘military’ markets

• Now integrated global units focused on key market sectors

• Supported by common services plus central Technology and Operations Councils

© 2009 by Smiths Detection: Proprietary Data | 13

There are growth opportunities in all our markets over time

Total addressable market CAGR 10-12%

Core markets

2007

~ £2.6bn

Coremarkets

2012

~ £4.3bn

Adjacent markets

Adjacentmarkets

Total market~ £ 3.5bn

Total market~ £ 5.8bn

• Security remains high on governments‘ agendas - long term forecast remains positive

• Contuinuous technology evolution for changing threats

• Contracts are becoming bigger

• Demand for integrated systems - from sensor supply to complete solutions

• Higher dependency on key projects/ customers

• Economic downturn will influence procurement in some market sectors, slowing growth rates

• Competition is becoming more difficult

• Further market consolidation expected

Market dynamics are becoming more challenging but may create opportunities

© 2009 by Smiths Detection: Proprietary Data | 14

The security sector - strongly varying market characteristics

Market contains varied customer groups in key sectors with different characteristics:

Transportation

• Technologies highly government regulated

• Event driven

• Overriding need to increase passenger throughput

Ports & Borders

• Moving from unregulated to greater government influence

• Investment subject to discretionary governmental budgets

Military

• Major contracts, principally with US, UK, India, Japan

• Long development and acceptance times

• Subject to fluctuating government budgets

Common characteristic - high barriers to entry

• Technology regulation by governments

• High R&D investment delivering high level IP

• Certification/QA - long process

• Extended contractual process

• High service levels required

Example - automatic explosives detection software development required ½ million man hours

© 2009 by Smiths Detection: Proprietary Data | 15

Smiths has a broad range of technologies for different markets

Chemical Biological Rad/Nuc Explosives

Technologies IMS/ FTIR PCR/ (bio) Hi-energy X-ray incl. mm-wave IMS/ trace (Chem ident.) X-ray hi-energy Backscatter trace

Spectrometry

Markets

Transportation

Ports & Borders

Critical Infra.

Military

Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 16

Competitorexamples

Chemical Biological Rad/Nuc Explosives

Technologies IMS/ FTIR PCR/ (bio) Hi-energy X-ray incl. mm-wave IMS/ trace (Chem ident.) X-ray hi-energy Backscatter trace

Spectrometry

Competitive landscape by technology

© 2009 by Smiths Detection: Proprietary Data | 17

Strong programme expenditure maintainedby key US government departments

DHS budgets - Annual growth beyond 2009 is forecast at ~5% pa to 2012

Major Smiths Detection DHS contracts:

•TSA (airports) - Automatic explosives detection x-ray

•CBP (border protection) - Cargo screening systems

•DNDO (nuclear detection) - Development of portable radiation detection system

© 2009 by Smiths Detection: Proprietary Data | 18

Chem/bio sensors market forecast 2007-12. CAGR - 16.1%. DoD comprises 70% of total world market

Strong programme expenditure maintainedby key US government departments

Forecasts - Frost & Sullivan

Major Smiths Detection JPEO contracts:

• JCAD personal sensor -Development & build contracts

• CBPS (collective protection) - Development & build contracts

© 2009 by Smiths Detection: Proprietary Data | 19

Risk matrix

Probability of incidence

Co

ns

eq

ue

nc

e

Radiological attack(“dirty bomb”)

Chemicalattack

Biologicalattack

Nuclearattack

Explosivesattack

Explosivesattack

Key points

• Rising probability of a dirty/ nuclear bomb incident

• Increasing fear of chemical agent attack

• Liquid explosives increase complexity of threat scenario

• Illegal trafficking of nuclear radiation material

• Training & information for terrorists broadly available

• Terrorism increasingly associated with weapons of mass destruction

The changing nature of the threat - from hijacking to imaging

Source: Civitas

© 2009 by Smiths Detection: Proprietary Data | 20

New technology start-ups often only focus

here

New technology start-ups often only focus

here

Revenuegeneration

Revenuegeneration

Perceptionof threator event

GovernmentRegulation

TechnologyDevelopment

Certificationor qualityapproval

Governmentor private

contractualprocess

DeploymentService

and support

Evolution orreplacement(new threats,

etc.)

Getting more important with increasing

standardisation and requires investment

Getting more important with increasing

standardisation and requires investment

LobbyingInternal/external

R&D investUnderstand +

influence process

Revenuegeneration

Route to market - Sales cycle in regulated markets, e.g. airports

3-12 Months Product lifecycle 3-8 years

6 months - 2 years 1-3 years 1-3 years

Often underestimated by new entrants

Often underestimated by new entrants

Good service performance is key to ensure repeat business

Good service performance is key to ensure repeat businessProcess applies to 70-75% of SD business

Reputation, customer understanding and

expertise are critical

Reputation, customer understanding and

expertise are critical

Marketing& Sales

© 2009 by Smiths Detection: Proprietary Data | 21

Products are based on approved government technology standards

Products are based on approved government technology standards

Revenuegeneration

Revenuegeneration

Perception ofthreat or event

Technologycustomisation

Sales and contractual

processDeployment

Serviceand support

Upgrade andreplacement

Internal/externalR&D invest

Revenuegeneration

Route to market - Private Industry - Critical Infrastructure

1-3 Months Product lifecycle 3-8 years

6 months - 2 years

Customers are less specialised & information/ consulting is more critical

Customers are less specialised & information/ consulting is more critical

Marketing& Sales

Mainly only internal R&D required

Mainly only internal R&D required

© 2009 by Smiths Detection: Proprietary Data | 22

Sector characterised by variable sales phasing

• Order intake is lumpy, dependent on contract size/timing and government fiscal periods

• Number and size of large contracts is increasing - % of revenue from contracts >£5m in 2008 was 35% (2007 - 30%)

Reported sales

Smiths Detection - Sales

0FY06 FY07 FY08

200

400

600

£m

H1 H2

Smiths Detection - Monthly Order IntakeMonthly order intake

… as a result sales growth may vary outside 10-12% range in any reporting period

© 2009 by Smiths Detection: Proprietary Data | 23

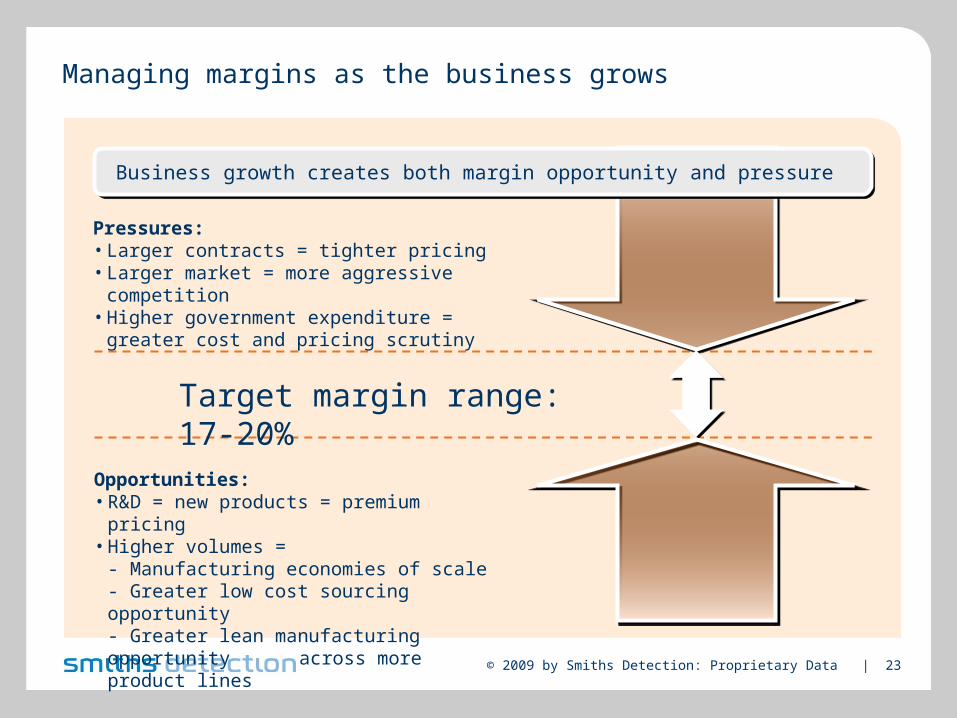

Managing margins as the business grows

Pressures: • Larger contracts = tighter pricing• Larger market = more aggressive competition• Higher government expenditure =

greater cost and pricing scrutiny

Opportunities:• R&D = new products = premium pricing• Higher volumes =

- Manufacturing economies of scale- Greater low cost sourcing opportunity- Greater lean manufacturing opportunity

across more product lines

Target margin range: 17-20%

Business growth creates both margin opportunity and pressure

© 2009 by Smiths Detection: Proprietary Data | 24

Opportunities for margin enhancement: recent examples

aTiX cost optimisation

Detector manufacturing optimisation

Sourcing: Lower cost component sourcing eg cabinet supplier from Eastern Europe

Design changes: Replacement of one major component, linear motor by servo motor

Lean manufacturing: New manufacturing layout; improved material flow; KANBAN principles; reduced non-value added work; outsourcing non-core components.

Lean manufacturing: Greater automation; multiple machine operation; outcome - more productive time.

Sourcing: Lower cost component sourcing

Production focus: Greater outsourcing, shift working efficiencies, manufacturing optimisation, better sub-contractors’ network; automatic software loading

Increased HCVM manufacturing capacity at existing site

© 2009 by Smiths Detection: Proprietary Data | 25

The working capital profile has changed

• Working capital requirements vary based on contract size, timing and payment terms.

• Payment terms vary by customer and working capital requirements can range between 30% - 70% of total contract value as a result.

• As trend toward bigger contracts continues payment terms are becoming a more important part of contract negotiations with customers.

Project with no Advance Payment Project with a 30% Advance Payment

Sep Nov Jan Mar May Jul Sep Nov Jan Mar May

Year End Year End

Sep Nov Jan Mar May Jul Sep Nov Jan Mar May

Working Capital @ 70% ofProject Value

Working Capital @ 40% ofProject Value

© 2009 by Smiths Detection: Proprietary Data | 26

Manufacturing focused on centres of excellence…

Manufacturing focused at major centres of excellence (inc. R&D)

• Wiesbaden - Imaging and explosive• Paris - High energy X-ray• Toronto - Explosives• Watford - Chemical/biological• Edgewood - Integrated military systems & chemical• Danbury - Chemical identification

Looking at distribution of manufacturing but limitations on moving production:

• Maintain link with R&D centres of excellence• Manufacturing is increasingly about in-house assembly• Products are “classified”

Increasing Military production in US

© 2009 by Smiths Detection: Proprietary Data | 27

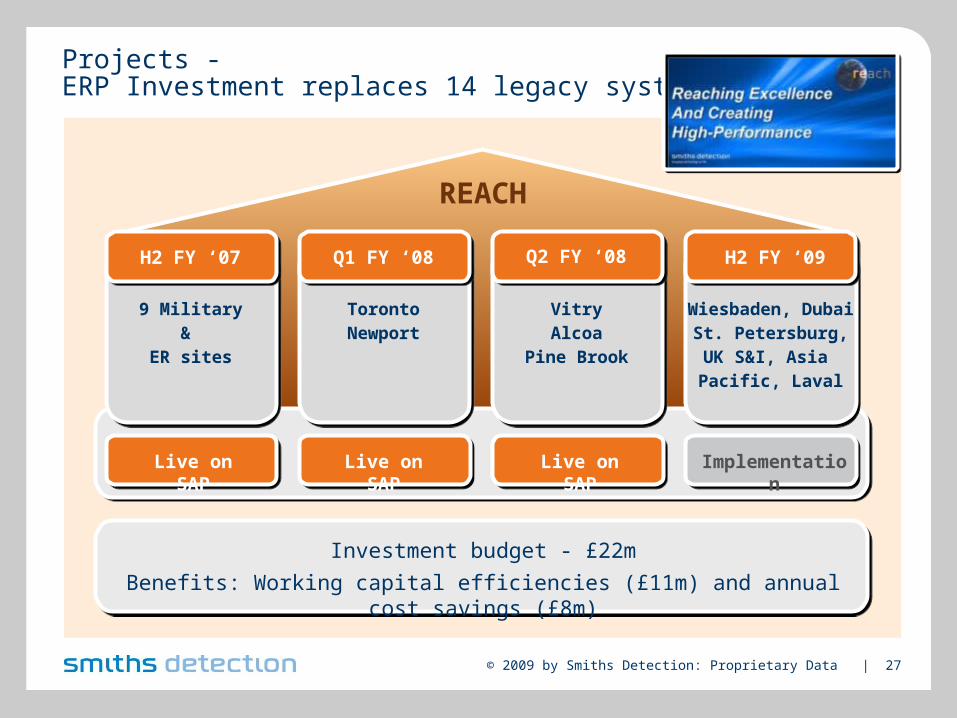

Projects -ERP Investment replaces 14 legacy systems

REACH

VitryAlcoa

Pine Brook

TorontoNewport

Live on SAP

Investment budget - £22m

Benefits: Working capital efficiencies (£11m) and annual cost savings (£8m)

Wiesbaden, DubaiSt. Petersburg,UK S&I, Asia Pacific, Laval

Live on SAP Live on SAP Implementation

H2 FY ‘07 Q1 FY ‘08 Q2 FY ‘08 H2 FY ‘09

9 Military & ER sites

© 2009 by Smiths Detection: Proprietary Data | 28

Projects - Investment aligned with growth opportunities

Edgewood• 130,000 sq. ft / 12,000 sq. m• Production of sensors and integrated systems• Target completion Summer 2009

Wiesbaden• 43,000 sq. ft / 4,000 sq. m • Expansion to meet growth of x-ray, including aTiX• Completed July 2008

Alcoa• Adding 90ft high gantry system testing bay• Provides first HCV showcase facility in the US• Facility to support CBP contract• Completed 2008

Capital projects to expand manufacturing capacity

© 2009 by Smiths Detection: Proprietary Data | 29

Investing for the future to enhance capability

Company-funded R&D investment 2008 - £29m - up 10% on FY07

• Company funded investment is 5.7% of sales

• Customer funding of £9m adds another 1.7% of sales with total spend of £38m

• Continued investment in performance improvement and product cost reduction

• Programmes mostly address specific issues, often government initiated

Continuous strong investment record in R&D

£30m £33m £38m Total R&D investment

Customer funded

Company funded

£m

% of sales

1

3

5

77.2% 7.5% 7.4%

5.9% 5.4% 5.7%

Total R&D as % of sales

Company R&D as % of sales

© 2009 by Smiths Detection: Proprietary Data | 30

Investing for the future to enhance capability

Targeted R&D expenditure in:

• X-ray screening - Cargo screening - Airport checkpoint explosive detection

• Chemical and trace - Handheld detectors

• Millimetre wave system - Product launched October 2008

• Biological detection - Veterinary and clinical applications

HazMatID Ranger Hand-held FT-IR chemical identifier

HPRID Hand-held radioisotope identifier

SABRE CENTURION II Air monitoring system

MMTD Hand-held multi-threat detector

SmartBio Sensor Real time bio-agent detector

FirstView Security systems management

Six new products launched at major US security show September 2008 following internal development

© 2009 by Smiths Detection: Proprietary Data | 31

Strategic investment - Diagnostics

• Taking Smiths Detection technologies and experience into new growth markets

• Building on existing experience of developing fast detection technologies, built into ruggedised instruments easily operated in the field

• Heavily regulated sector - similar type of customer base to security

• Opportunities to develop through partnerships

Strategicinvestments

© 2009 by Smiths Detection: Proprietary Data | 32

Rapid disease diagnosis for vets

• Providing rapid on-site diagnosis of diseases instead of lengthy lab analysis

• Portable, lightweight, rugged, easily decontaminated, easy-to-use

• World’s first portable vet diagnostic laboratory, initially for Avian Flu and Foot & Mouth Disease

• Trials to validate system- January: Institute of Animal Health- February: Field trials

• Principal opportunities: Interest from USA (DHS and USDA), Australia, Ireland, South America, Vietnam

• Advantages: Currently sample sent to labs. Field test allows vet to deal with sick animal on site.

Analysis in less than 90 minutes - big potential for LATE-PCR in other markets

Strategicinvestments

© 2009 by Smiths Detection: Proprietary Data | 33

Diagnosing infectious diseases at the Point of Care

Next step - clinical diagnostics • Uses same technology platform as the

veterinary instrument

• 5-25 simultaneous tests

• Genuine sample in-Answer out platform suitable for operation at the point of care

• Developing tests for MRSA and clostridium difficile

• Will follow with further tests for patient screening and critical care

• Potential application in cancer diagnostics

• Seeking partners

Strategicinvestments

© 2009 by Smiths Detection: Proprietary Data | 34

StrategicinvestmentsStrategic investment - Cross Match

• Cross Match - leader in biometric identity management• Fingerprint, palm and full-hand scanners, facial recognition

systems, iris scanning technology, document readers• Merged with Smiths Heimann Biometrics in 2005• Smiths holds 34% stake• Addressable biometrics identification market 2009 - $1bn• Current turnover - c.$90 million• Approx half of sales from US Government departments

and agencies• National programmes include

- US DoD (battlefields and bases)- US Department of State (embassies)- US DHS (immigration and border control)- US Department of Justice (booking and prosecution)- UK Home Office (UK visas program)

www.smithsdetection.com

Coffee Break

© 2009 by Smiths Detection: Proprietary Data | 36

More technologies in more sectors in more countries than any other company

Taking detection technologies into key markets

Security and Inspection

Established businesses Airport security Ports & Borders Critical infrastructure

Military CBRN detection Integrated systems Emergency responseEstablished businesses

Military and Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 52

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 53

Wide range of technologies

Explosives Trace Detection

Checkpoint X-Ray Explosives Detection System

Sensormanagement

Cargo X-RayMillimetrewave

Searching for: explosives, weapons & contraband in a wide range of markets

Airport Security Critical Infrastructure Ports & Borders

Security and Inspection marketSecurity& Inspection

© 2009 by Smiths Detection: Proprietary Data | 54

Current characteristics of the sector

Continuous terrorist threat is driving industry forward

• Market driven by threat levels & events

• Trend towards larger contracts

• Governments moving to increased regulation

• Buyers looking for:- greater speed of detection- fewer false alarms- increased throughput

• Steady innovation stream

• Increasing levels of systems integration

• Increasingly competitive landscape

2003 Indonesia

2004 Madrid

2007 Glasgow

2008 Mumbai

2001 New York 2005 London

2002 Bali 2006 liquids

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 55

No clear no.2 company in market, behind Smiths Detection

Security and Inspection - market position

• Global Leader

• More than 50,000 X-Ray machines sold worldwide

• Recognized technology leader in X-Ray and explosives trace detection

• Broadest range of technology

Independent survey of the global market for weapons and contraband detection equipment 2006, sensors only. Not military or ER markets.

Source IMS Research

Smiths

GE

L-3

Rapiscan

Nuctech

AS&E

Reveal

CEIA

SAIC

Gilardoni

Others

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 56

Focus on aviation security market

Airport security focuses on:

• Checkpoint (plus staff screening)

• Checked baggage screening

• Air cargo screening

• Service

Relative levels of airport security investment plans worldwideSource - Smiths Detection estimates

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 57

Focus on aviation security market

Description: Screening of passengers, bags, cargo and airline staff, to detect weapons and explosives

Key features

• Highly regulated, high barriers to entry

• Long product introduction cycle

• Different process in US and ROW

Customers: Combination of Government regulators and airport operators. Key customers: TSA, BAA, German Ministry of Interior, Siemens

Trends:

• New technology for screening of people

• Automated explosives detection; liquids

• Focus on improving passenger throughput

• System integration

• Increasing focus on air cargo

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 58

Airports - Hand baggage & passenger screening

New threats and increasing passenger numbers require new solutions

Passenger traffic currently slowing down but only a temporary drop as overall trend is steady growth

Growth drivers:• Increased throughput in existing terminals (automation)• New airports / terminals being constructed• New threats (ceramics, plastics, liquids)• More data requirements and integration of technologies

Actions• Strong ongoing internal R&D• Moving from single products to more complete systems• Partnerships considered for non-core technologies

required• Working with airports, airlines and governments to

drive continuous technology evolution and help define future standards

“Demand for flights (annually) in Europe will rise from 10 million today to 20.4 million in 2030” Source - The ‘Challenges of Growth’ published December 2008 by EUROCONTROL, the European Organisation for the Safety of Air Navigation.

Airports have to process more passengers in shorter time

Sou

rce:

EU

trav

el r

esea

rch

1600

400

1973 200319931983

Pas

seng

ers

carr

ied

(m)

Oil crisis Gulf crisis WTC attack

Historical passenger growth

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 59

Aviation security: R&D for checkpoint of the future

aTiX automatic explosives detection x-ray system• Launched October 2007• Platform based solution with software upgrades (requiring certification) for

- Laptops in bag- Liquids identification

• Designed with iLane for increased throughput• Pricing reflects technology providing staff cost savings, equipment replacement

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 60

aTiX automatic explosives detection in actionSecurity& Inspection

Detecting a sheet explosive hidden behind electronic device

© 2009 by Smiths Detection: Proprietary Data | 61

Aviation security: R&D for checkpoint of the future

eqo people screening portal

• Launched October 2008

• Safe millimetre-wave technology

• Live image presentation

• High resolution images of concealed threats

• Simple and rapid passenger processing

• Minimal footprint

• Privacy issue solutions a priority

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 62

eqo in action - people screening for wide range of threats

Security& Inspection

• Multi threat detection- Security threats- Non-security threats

• Full motion

• Video like image

• Real time - live

• High resolution

© 2009 by Smiths Detection: Proprietary Data | 63

Airports - Hold Baggage Screening

Opportunities:• Internal R&D to match new standards• Development and partner for next generation EDS• Good government relations required to support legislation change

New standardisation is driving market for AT systems

2006

Standard 1

Standard 2

Standard 3

2018

We have

2012

Continuouslyraisingstandards

We have

must meet

introduced

Currently being definedby European legislator

Further technology-driven opportunities

From lobby to in-line solution

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 64

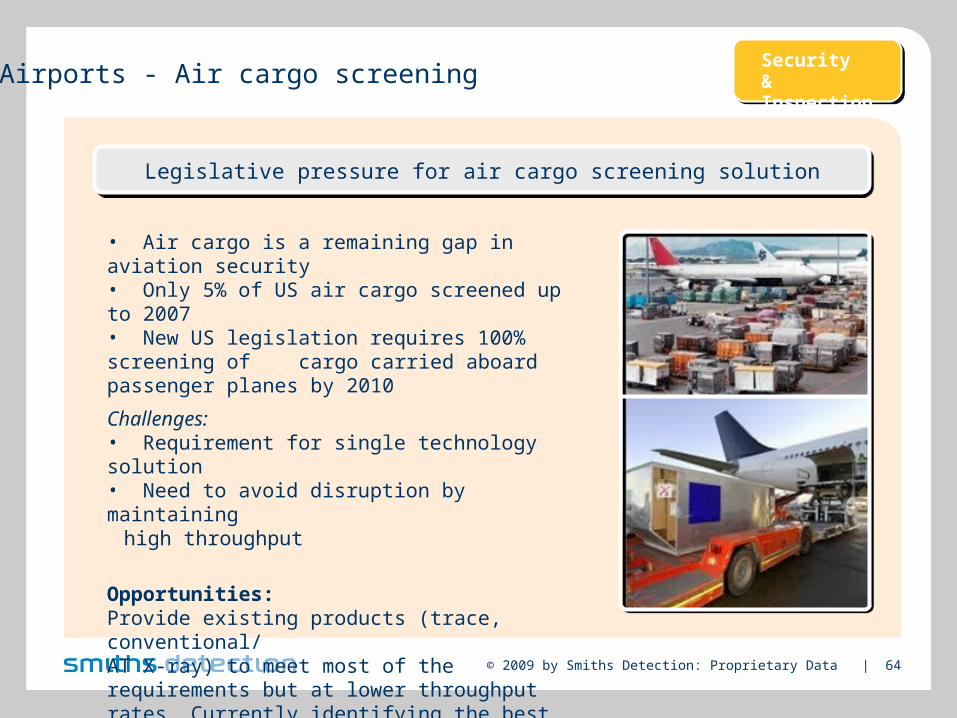

Airports - Air cargo screening

• Air cargo is a remaining gap in aviation security• Only 5% of US air cargo screened up to 2007• New US legislation requires 100% screening of

cargo carried aboard passenger planes by 2010

Challenges:• Requirement for single technology solution • Need to avoid disruption by maintaining

high throughput

Opportunities:Provide existing products (trace, conventional/AT X-ray) to meet most of the requirements but at lower throughput rates. Currently identifying the best replacement technology

Legislative pressure for air cargo screening solution

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 65

Description: Screening cargo and freight at ports, airports and borders to prevent transit of weapons, drugs and contraband

Key features• High growth as governments move towards 100% inspection• Increasing convergence of customs & border security operations• US focus on ‘dirty bomb’ materials• Crowded and competitive market place

Market drivers: • US pushing pre-shipment screening• High throughput requirement needing greater automation• Search for reliable automatic explosives detection• Improved Rad/Nuc detection

Ports and borders market

Evolution of screening

Manual inspection

Non-invasive inspection

Integrated security

Fully integrated port systems

100%screening

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 66

Market position in Ports & Borders

HCV Stationary

HCV Mobile (US and EU)

Market size 2008 - £480m Source - Smiths Detection (estimate, incl. Rad/Nuc)

Source - University of Le Havre study, 2008

Security& Inspection

Smiths Detection

Nuctech

SAIC

AS&E

Rapiscan

Others

HCV Gantry

© 2009 by Smiths Detection: Proprietary Data | 67

Investment aligned with growth opportunities

• Cargo product range enhancements

• New HCVP (Passthru), speeds scanning process for higher throughput.

• Networking for remote analysis - container information can be analysed during journey

• High Resolution imaging for detailed views

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 68

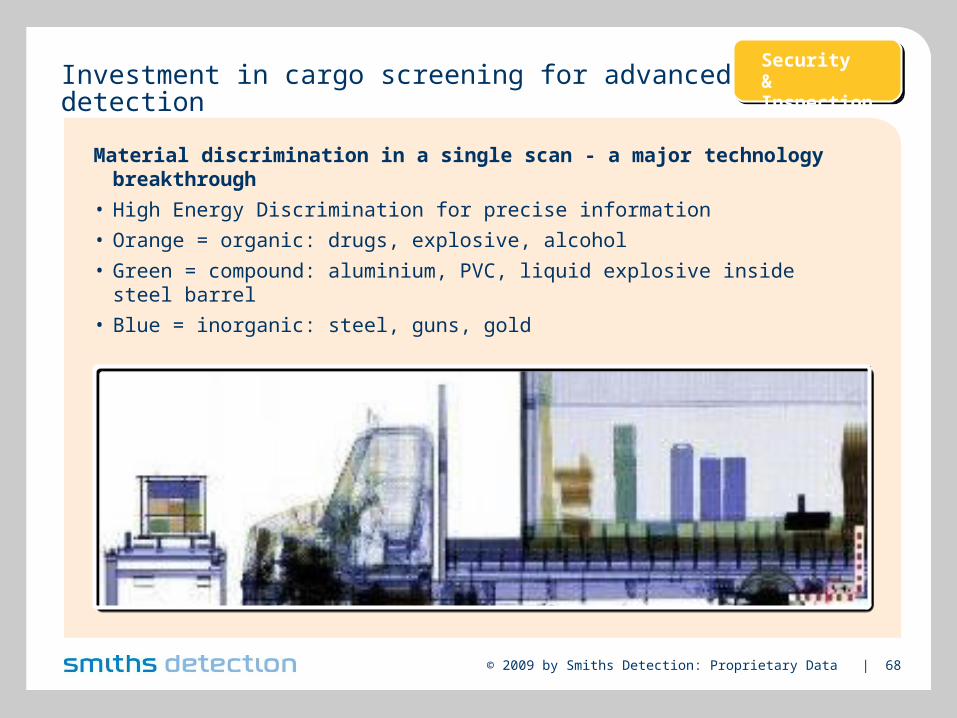

Investment in cargo screening for advanced detection

Material discrimination in a single scan - a major technology breakthrough

• High Energy Discrimination for precise information

• Orange = organic: drugs, explosive, alcohol

• Green = compound: aluminium, PVC, liquid explosive inside steel barrel

• Blue = inorganic: steel, guns, gold

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 69

• Strong requirement by Russian Government to protect extensive borders - illegal and dangerous shipments

• Delivered 50+ systems FY 07/08

Investment leads to major contract opportunities

Major market served by strong manufacturing presence, St Petersburg

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 70

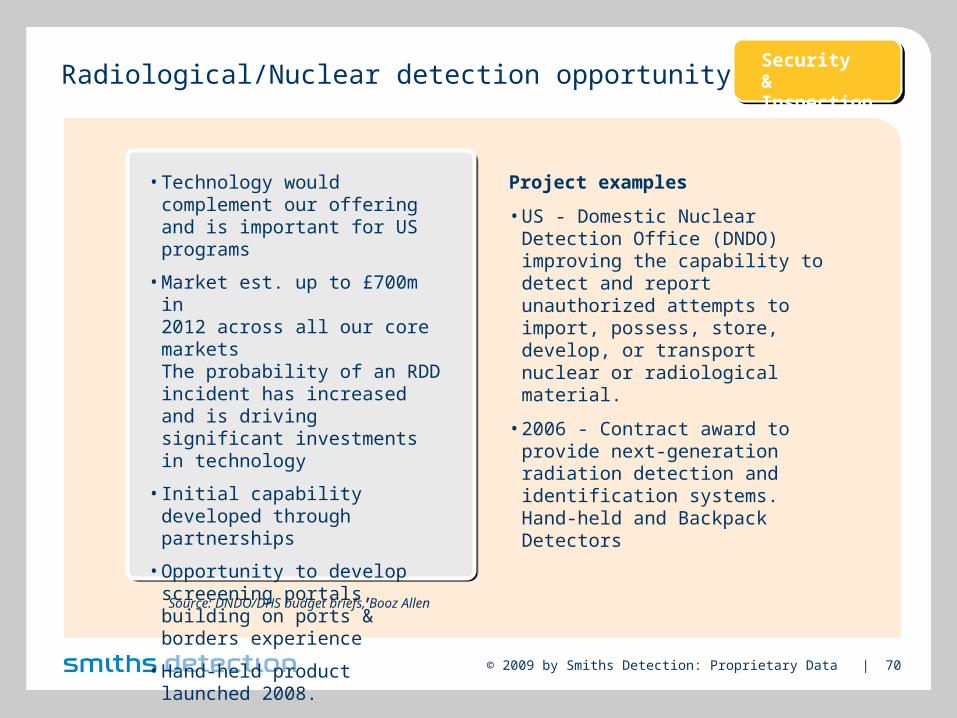

Radiological/Nuclear detection opportunity

• Technology would complement our offering and is important for US programs

• Market est. up to £700m in 2012 across all our core marketsThe probability of an RDD incident has increased and is driving significant investments in technology

• Initial capability developed through partnerships

• Opportunity to develop screeening portals, building on ports & borders experience

• Hand-held product launched 2008.

Source: DNDO/DHS budget briefs, Booz Allen

Project examples

• US - Domestic Nuclear Detection Office (DNDO) improving the capability to detect and report unauthorized attempts to import, possess, store, develop, or transport nuclear or radiological material.

• 2006 - Contract award to provide next-generation radiation detection and identification systems. Hand-held and Backpack Detectors

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 71

Critical Infrastructure characteristics

• Regulation is patchy• Insurance requirements creating an opportunity • Highly fragmented market

Key sectors• Mass Transit - successful trials leading to new business• Sports events - London Olympics opportunity. Special team formed.• Facilities - Utilities, large US market, government and high risk

buildings protection, including hotels

Opportunities:• Leverage existing government customer base• Requirement for high throughput checkpoint & integrated solutions• Partnerships for additional products

• IP Video • Sensor integration• X-ray • Explosives detection

• Mail screening• HVAC chemical detection• Emergency response equipment

Applicable technologies

Sports/events

Facilities

Mass Transit

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 72

Two Critical Infrastructure examples

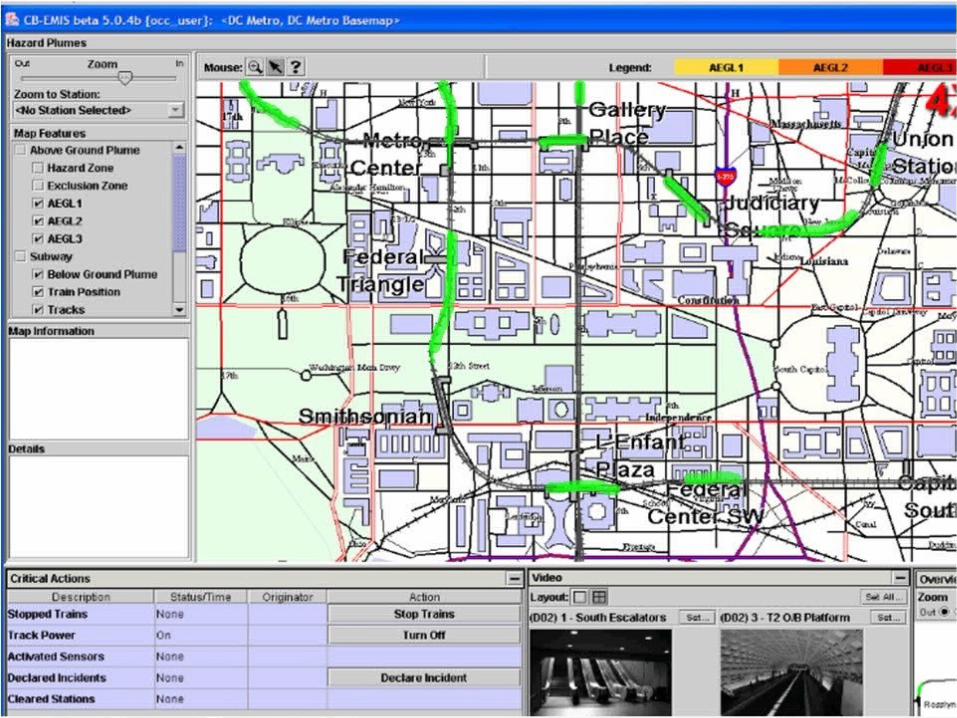

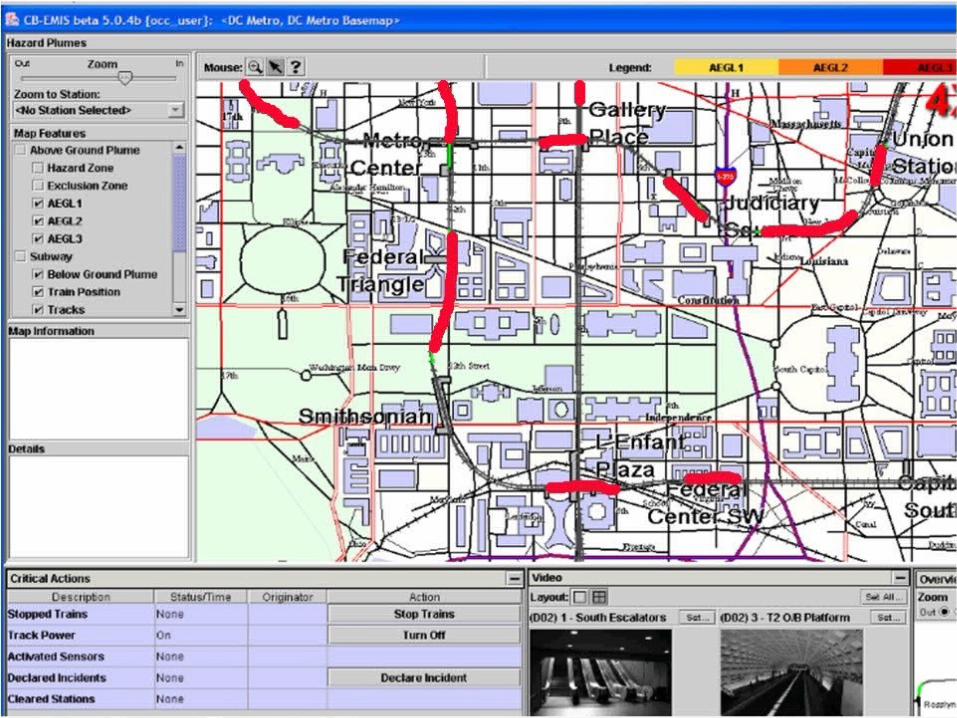

FirstView: Remote Cargo Inspection: Port Qasim, Pakistan

Protect: Danbury Station

Security& Inspection

FirstView Remote Cargo Inspection: Port Qasim, Pakistan

Waiting Area Rad Portal

Cargo X-Ray X-Ray Image

INTERNET

National Targeting Center, USA

Container ID: PSCU1044960

Container ID: JSE102163870

Container ID: JAE103059213

Maps

Real-time Sensor Data

Live Meteorological Data

ConOps, SOP’s, Recommended Actions,

Audit Trail

Wide Area Map & Live Video

A B

First Responder Jacks

Command & Control Field

Locations

Smiths Detection Inc.

END

© 2009 by Smiths Detection: Proprietary Data | 87

Security & Inspection market drivers - conclusions

Threats & events• Continuing terrorism • Sports & events (e.g. Olympic games)• Iraq investment to rebuild security infrastructure• New threats

Regulation• Legislation for checkpoint and EDS performance standards• Changes in restrictions - laptops; liquids• Passenger body screening (medium term)• US 100% cargo screening • Radiation screening

Investment • Continuing airport investment • Europe - development of pan-European high speed rail links

Global Cycle

Threats & events

Investment

Regulation

Security& Inspection

© 2009 by Smiths Detection: Proprietary Data | 88

Military & Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 89

Laboratory science in the hands of the professionals

Searching for and protecting against: chemical, biological, radiological, nuclear and explosive threats in two closely aligned markets

Military Emergency response

Military and Emergency ResponseMilitary & Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 90

Strategicpartner

Systems IntegrationThrough Life Capability

Research, technology & Knowledge base

Products and sub systems

Role of Smiths Detection Military - Working with Governments

© 2009 by Smiths Detection: Proprietary Data | 91

• Strong track record of supplying chemical & biological warfare detection capability now being expanded in adjacent areas

• Addressable market size: c. £300m pa • Increased emphasis on:

- Enhanced chemical detection- Integrated Systems- Multi-sensor and vehicle-based- Bio detection- Explosives/IED and RAD detection- X-ray screening

• Major contracts: - JCAD I; Profiler, Chem/Bio Protection System; - UK Light Role Team, Germany LCD

• Major opportunities: - JCAD II; - Chemical Standoff; Asia Pacific & EU

Military CBRN detection capability

The global market leader - 125,000 CW detectors deployed worldwide

Military & Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 92

Military - the changing market

Market characteristicsChanging dynamics: US administration/ budgets, Iraq war shift. Shift in emphasis to proven supplier with strong technical base and capacity

Technology driven marketStrong growth remains in new chem detectors, and in new systems of sensors and Integrated Systems and Explosives/IEDs.

Opportunities:• Continuous R&D to grow core business • Constantly reviewing emerging technologies• Building capabilities for integrated systems• Broadening offerings for main segments

(chem, bio, rad, protection, explosives, and integrated systems)

Military & Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 93

Integrated systems - becoming a prime contractor

• Tactical Meteorological Systems

• Customer requirements - highly mobile, self contained battlefield meteorological systems for various military missions

• Solutions - Building on generations of artillery support systems. New full met. system for Marines

• Additional customer benefits - strong user focus; advanced weather model packaged for military operations and support; shrinking footprint for improved ops and logistics

• Results - Selection to fulfil several generations of Army/Marines artillery support needs. 52 more systems recently ordered. Selected to develop broader all-mission system for Marines production decision within year. Contracts to date - $125 M.

Establishes Smiths Detection as a prime contractor for integrated systems

Military & Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 94

• Fast and reliable identification

• Ruggedised Systems

• Laboratory science in the hands of first responders

• Adding technologies - Raman, mass spectrometry

• Selling complementary products

Technology for Emergency Response Military & Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 95

Emergency Response Strategy based on a strong product pipeline

Expand product range Grow non-US sales Strategy

• HGVI - combination of civil and military technologies. New Market sector.

• HazmatID Ranger - complements and extends success of HazmatID.

Opportunities:• Growing sales outside US,

strong APAC and EU growth

• Expanding product range, vital to maintain our edge and leadership position

HPRID Radiation detectorHGVI Multi-sensor

chemical detector

MMTD multi threat detector

HazMatID Ranger chemical identifier

Recent product launches

Military & Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 96

Military & ER market drivers - conclusions

• Chem Detection - Product development will protect and grow global leadership base

• Collective Protection - (CBRNE) Taking capabilities into global markets. Potential Protection upsides in individual protective equipment and decontamination solutions.

• Integrated Systems - Major programs (MET, LRT) providing credentials, experience and organic assets to address growing market, esp. for CBRNE sensor integration.

• Explosive trace/X-ray Detection - Greater sales focus; further potential in IED and/or standoff detection.

• Bio and Rad Detection - New products launches into growing market.

Military & Emergency Response

© 2009 by Smiths Detection: Proprietary Data | 97

Summary - an attractive investment case

Market leader in a growth business with high barriers to entry

Smiths Detection growth range.* Sales: 10-12%** Margins: 17-20%

**Organic growth at constant currency *Range of underlying growth over 3 year period

Positive outlook, driven by events, changing risks and new technologies

Business underpinned by leading edge technology

Some resilience through diversity of markets, customers and global spread

Margins set to remain strong; sales volumes variable in any given period

Opportunities for value creation, including adjacent regulated markets

www.smithsdetection.com

© 2009 by Smiths Detection: Proprietary Data | 99

Welcome to Wiesbaden

3 facilities in Wiesbaden region

• Erbenheim - 15,400 m² Production of automated X-ray systems, generators & sensors; R&D Centre; Admin.New production hall 4,600 m² opened July 2008

• Nordenstadt 1 - 15,600 m²Conventional X-ray systems productionAdditional 10,900 m² added during 2008

• Nordenstadt 2 - 8,500 m²Mobile & cargo inspection systems

Home of the largest manufacturing facility in Smiths Group

© 2009 by Smiths Detection: Proprietary Data | 100

Groups for the site tour

Stefan Aust

Bernhard Semling

Hermann Ries

Hans Zirwes

Joachim May