Embed Size (px)

Citation preview

XBRL Canada Fourth Annual Conference October 7, 2010

10:30 a.m. – 4:30 p.m.

Quality Assurance for XBRL-Related

Documents and Computer-Assisted

Auditing Techniques (CAATs) for

XBRL

University of Waterloo

Efrim Boritz

Iowa State University

Won Gyun No

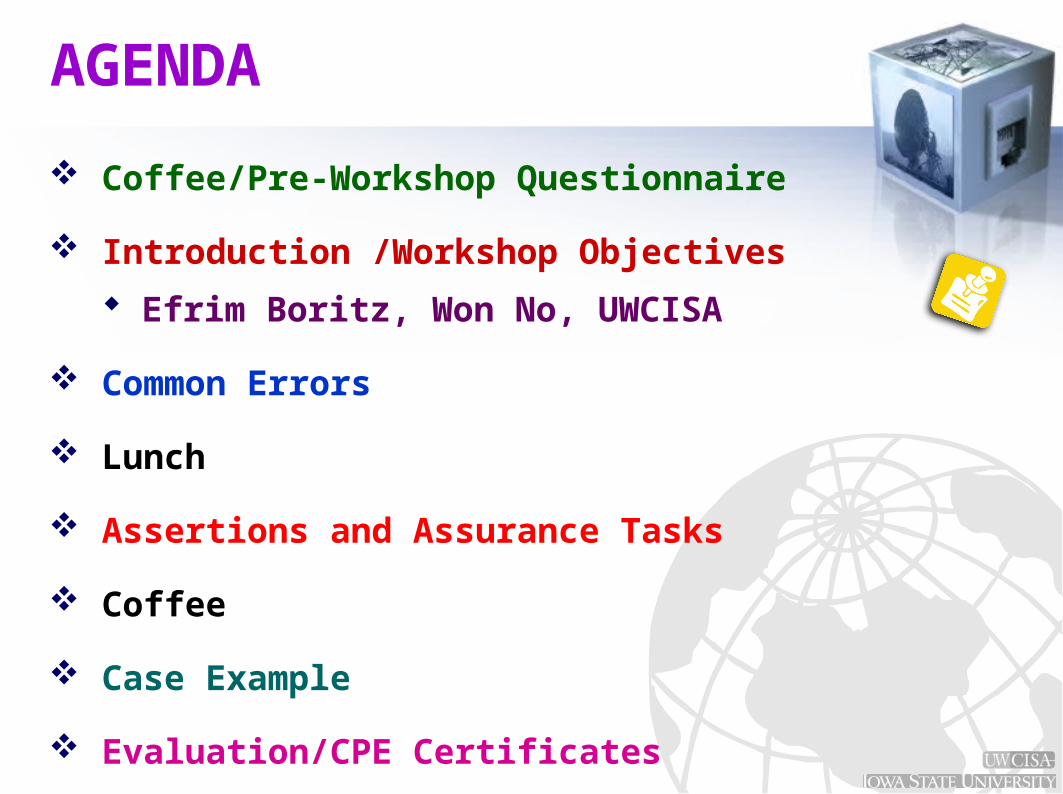

Coffee/Pre-Workshop Questionnaire

Introduction /Workshop Objectives

Efrim Boritz, Won No, UWCISA

Common Errors

Lunch

Assertions and Assurance Tasks

Coffee

Case Example

Evaluation/CPE Certificates

AGENDA

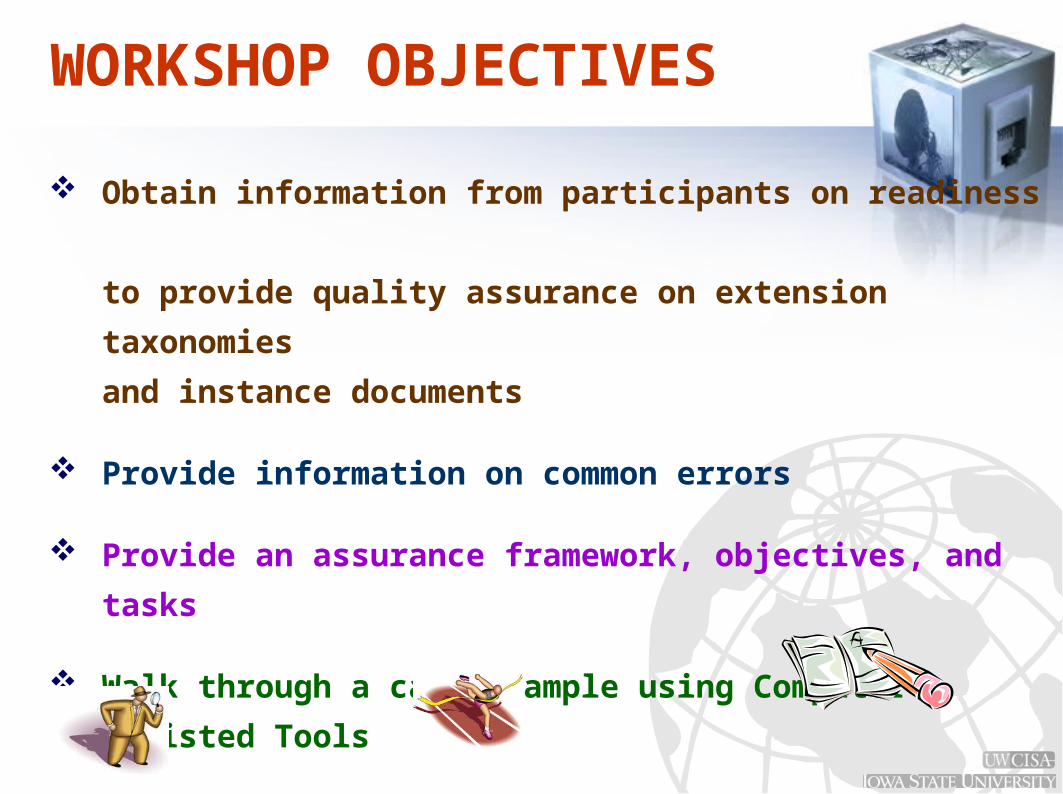

WORKSHOP OBJECTIVES Obtain information from participants on readiness

to provide quality assurance on extension

taxonomies

and instance documents

Provide information on common errors

Provide an assurance framework, objectives, and

tasks

Walk through a case example using Computer-

Assisted Tools

Obtain feedback

KEY PHASES IN ELECTRONIC FINANCIAL REPORTING

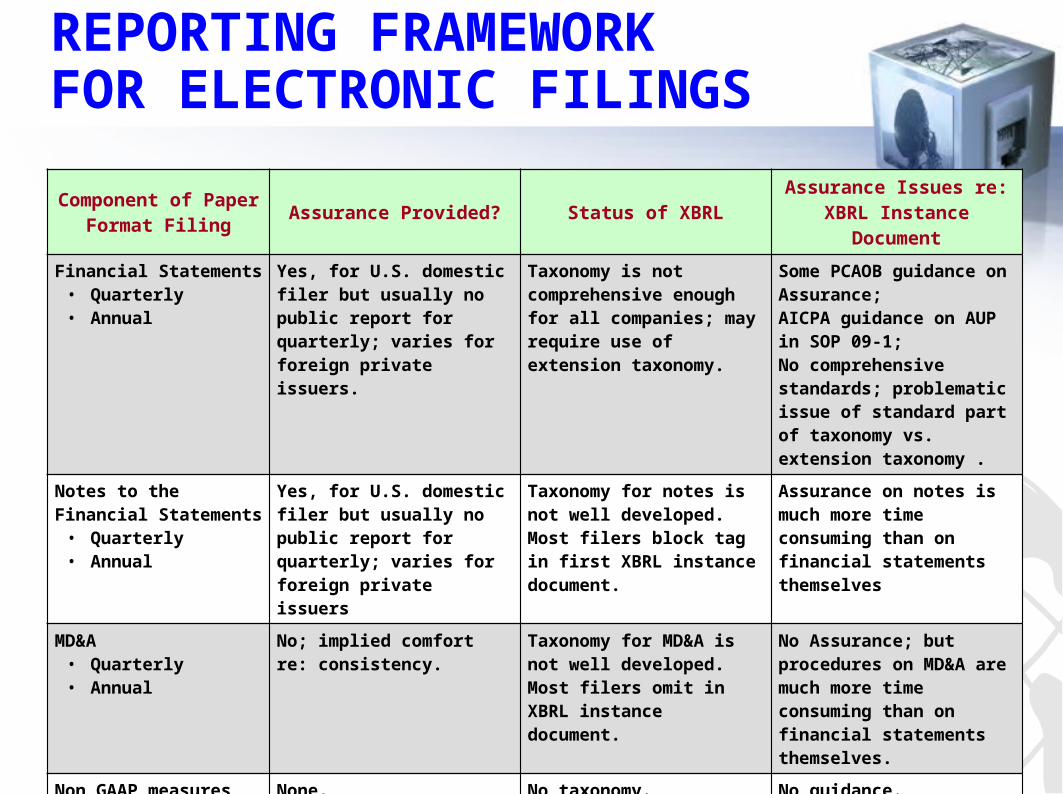

Component of Paper Format

FilingAssurance Provided? Status of XBRL

Assurance Issues re: XBRL Instance

Document

Financial Statements• Quarterly• Annual

Yes, for U.S. domestic filer but usually no public report for quarterly; varies for foreign private issuers.

Taxonomy is not comprehensive enough for all companies; may require use of extension taxonomy.

Some PCAOB guidance on Assurance;AICPA guidance on AUP in SOP 09-1;No comprehensive standards; problematic issue of standard part of taxonomy vs. extension taxonomy .

Notes to the Financial Statements• Quarterly• Annual

Yes, for U.S. domestic filer but usually no public report for quarterly; varies for foreign private issuers

Taxonomy for notes is not well developed. Most filers block tag in first XBRL instance document.

Assurance on notes is much more time consuming than on financial statements themselves

MD&A• Quarterly• Annual

No; implied comfort re: consistency.

Taxonomy for MD&A is not well developed. Most filers omit in XBRL instance document.

No Assurance; but procedures on MD&A are much more time consuming than on financial statements themselves.

Non GAAP measures linked to financial statements

None. No taxonomy. No guidance.

Investor relations web pages that interact with above items

None. No taxonomy. No guidance.

REPORTING FRAMEWORK FOR ELECTRONIC FILINGS

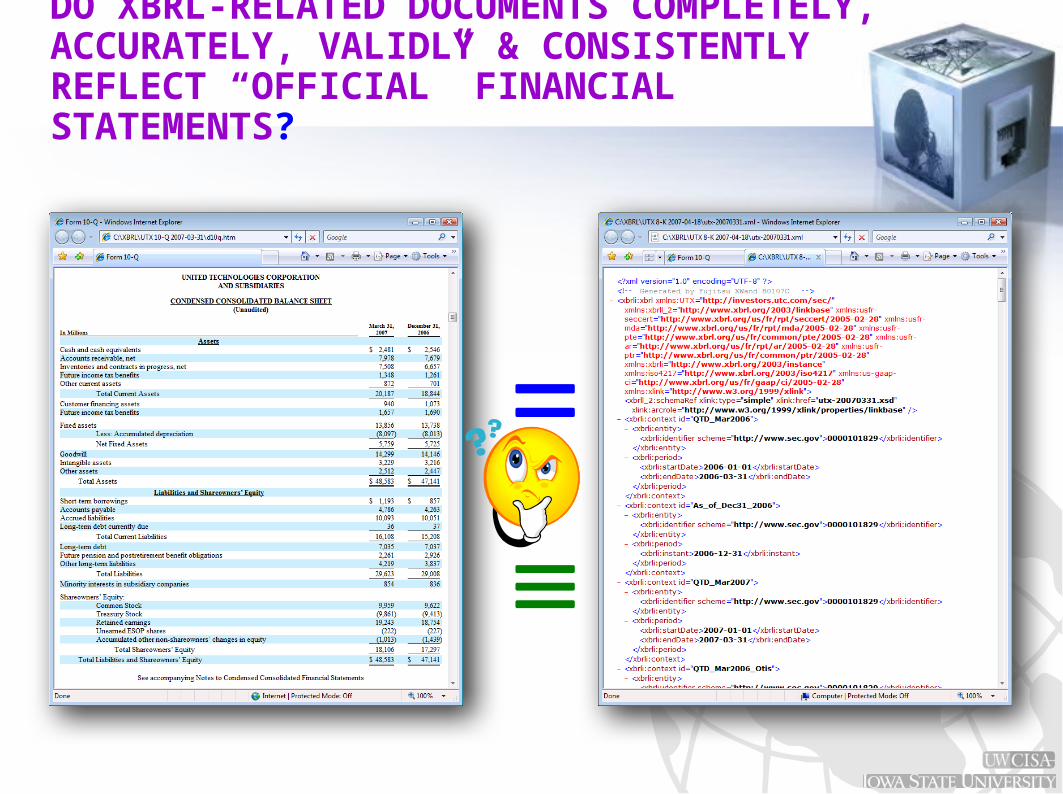

DO XBRL-RELATED DOCUMENTS COMPLETELY, ACCURATELY, VALIDLY & CONSISTENTLY REFLECT “OFFICIAL” FINANCIAL STATEMENTS?

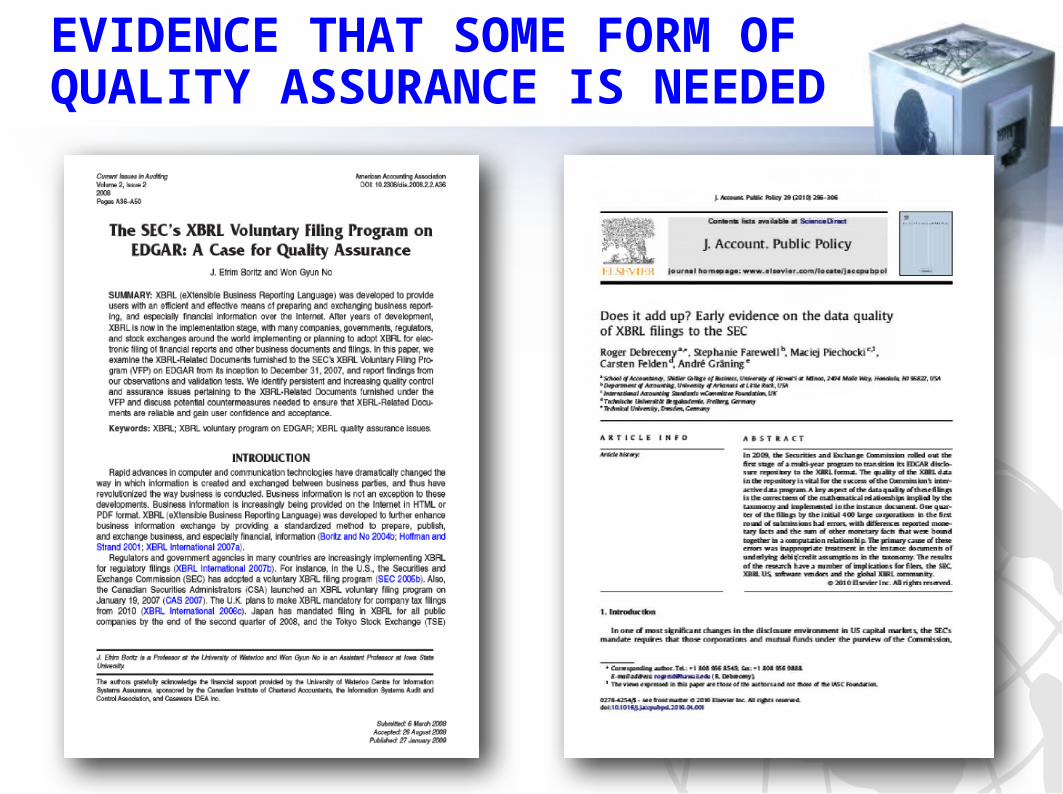

EVIDENCE THAT SOME FORM OF QUALITY ASSURANCE IS NEEDED