Embed Size (px)

Citation preview

Yale School of Management

Sharpening Sharpe Ratios

Will Goetzmann

Jonathan Ingersoll

Matthew Spiegel

Ivo Welch

Yale School of Management

Background

Sharpe Ratio Performance evaluation in practice. Asset pricing research.

Limitations Misleading when shape of distribution changes. Problematic in presence of derivatives.

Yale School of Management

Example

Perfect foresight timer btw. US. Stocks and U.S. bonds.

Sharpe 1926-2003 = 1Throwing all returns over 30%/year away

Sharpe 1926-2003 = 1.06Smoothing works even better.

Yale School of Management

Our Approach

What strategy maximizes Sharpe ratio? How much can it matter? Implications for risk-control.Dynamic strategies.Are there any measures that cannot be

manipulated?

Yale School of Management

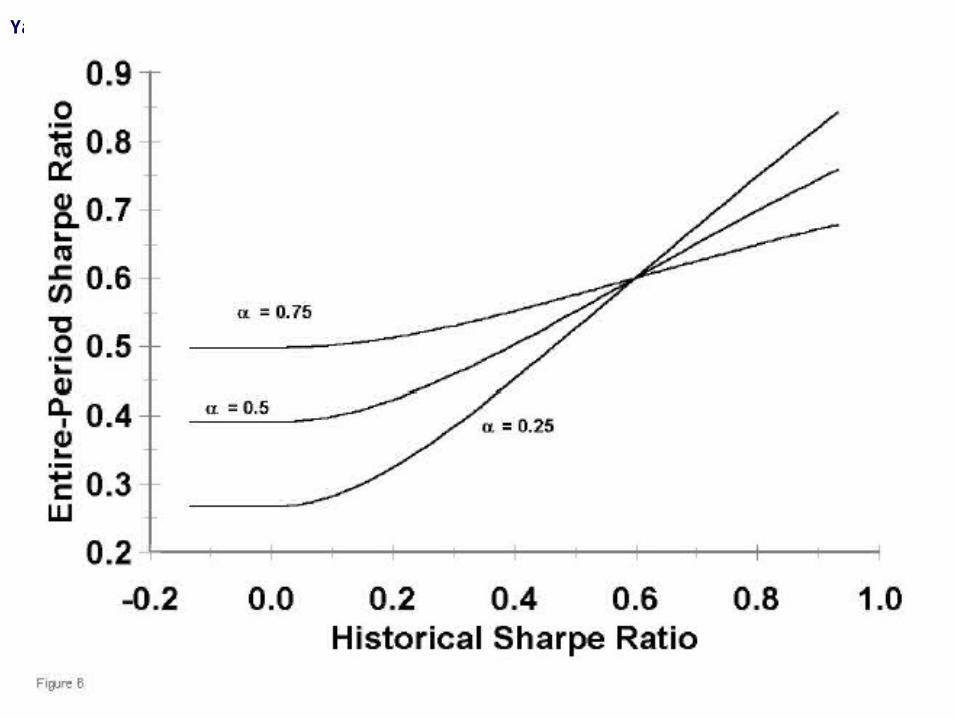

Optimal Sharpe Ratio Distribution

Left-skewed.Fat-tailed.Very sensitive to small-sample.Hard to distinguish luck vs. skill.

Yale School of Management

Manipulation-Free Statistic

Exists only under specification of utility.Provides a method to test the efficacy of the

Sharpe ratio.Sharpe ratio does well under “normal”

conditions.New measure is useful under non-normal

conditions.

Yale School of Management

Hedge Fund Applications

Hedge funds unconstrained from dynamic and derivative strategies.

Hedge funds often evaluated by Sharpe Ratio. Absolute return benchmark: Libor or T-bills

Hedge funds seem prone to occasional, spectacular disasters.

Yale School of Management

Hedge Fund Strategies

Fung and Hsieh (1997) Brown and Goetzmann (1997)Agarawal and Naik (2001) Contract-related non-linearity

Yale School of Management

Yale School of Management

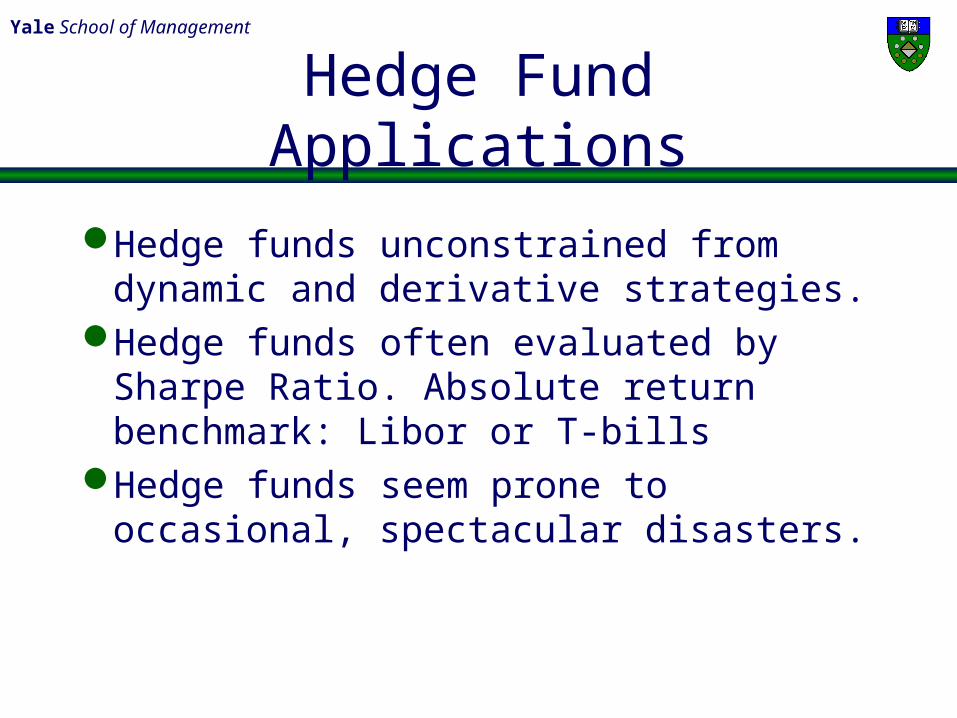

Art Institute vs. Integral

Integral boasted “The highest Sharpe Ratio in the business.”

Options-based strategy. Performance-based contract.Guaranteed 1% to 2% in flat or rising

markets.Losses possible only if stocks dropped

more than 30% (which they did).

Yale School of Management

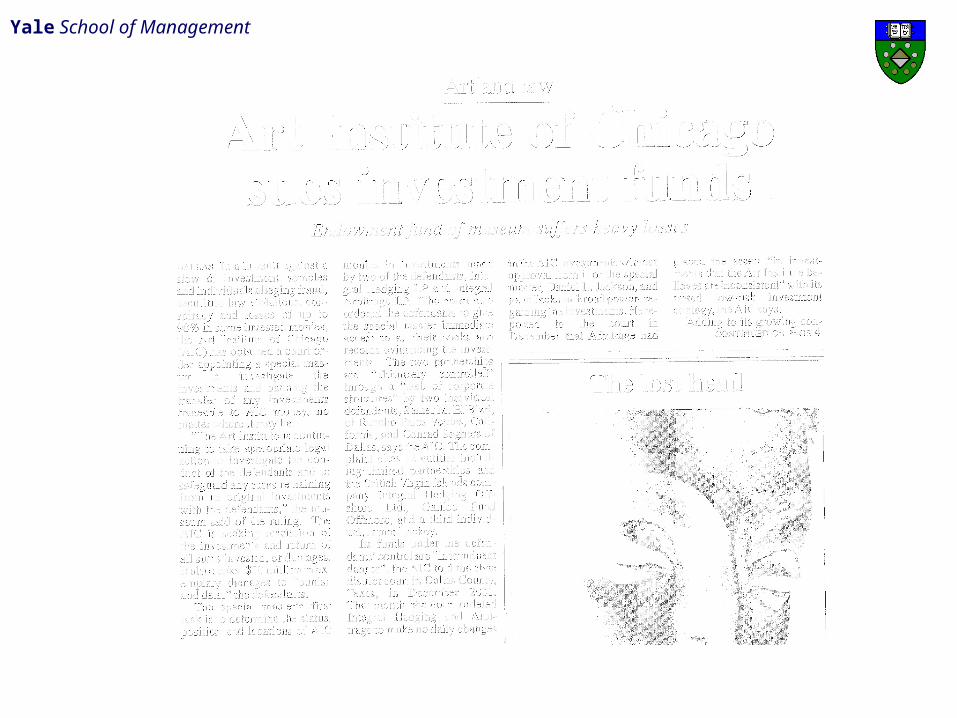

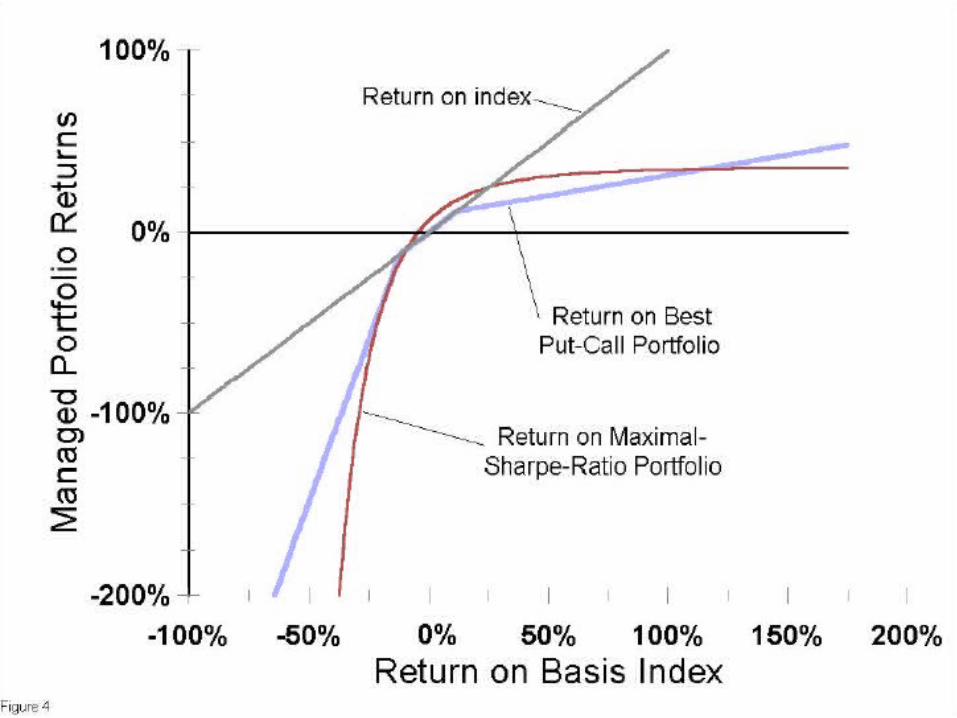

Maximal Sharpe Ratio in a Complete Market

MSR is linear in the likelihood ratio of the state price per unit probability.

Sell high-priced, low probability payoffs.Leverage does not change shape. Possible to nearly match it with a limited

liability portfolio. Any basis asset is possible.

Yale School of Management

Yale School of Management

Yale School of Management

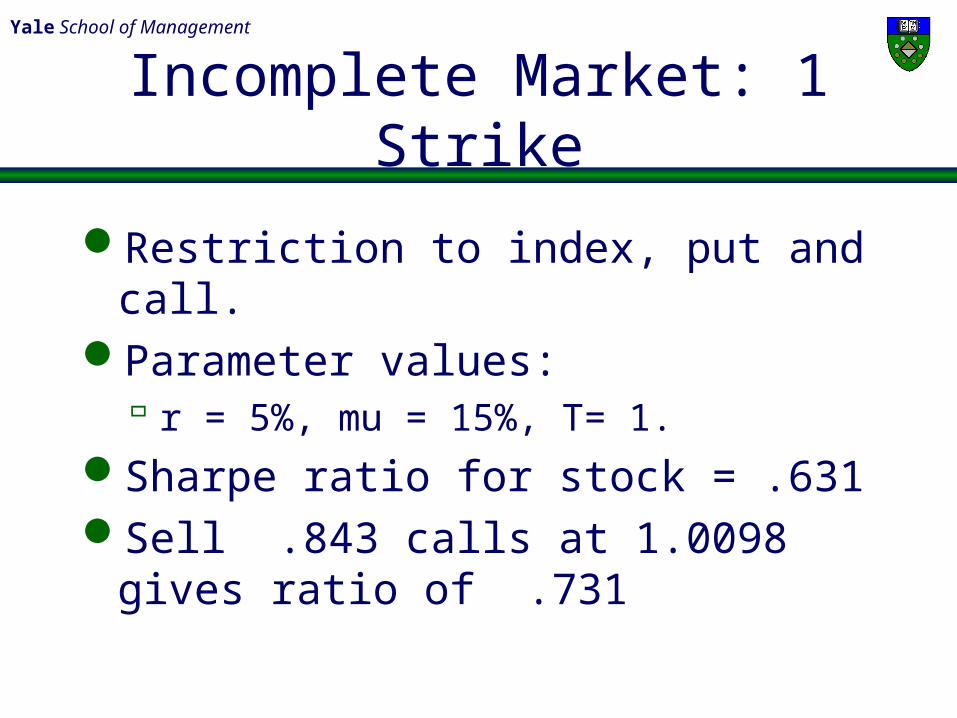

Incomplete Market: 1 Strike

Restriction to index, put and call.Parameter values:

r = 5%, mu = 15%, T= 1.

Sharpe ratio for stock = .631Sell .843 calls at 1.0098 gives ratio

of .731

Yale School of Management

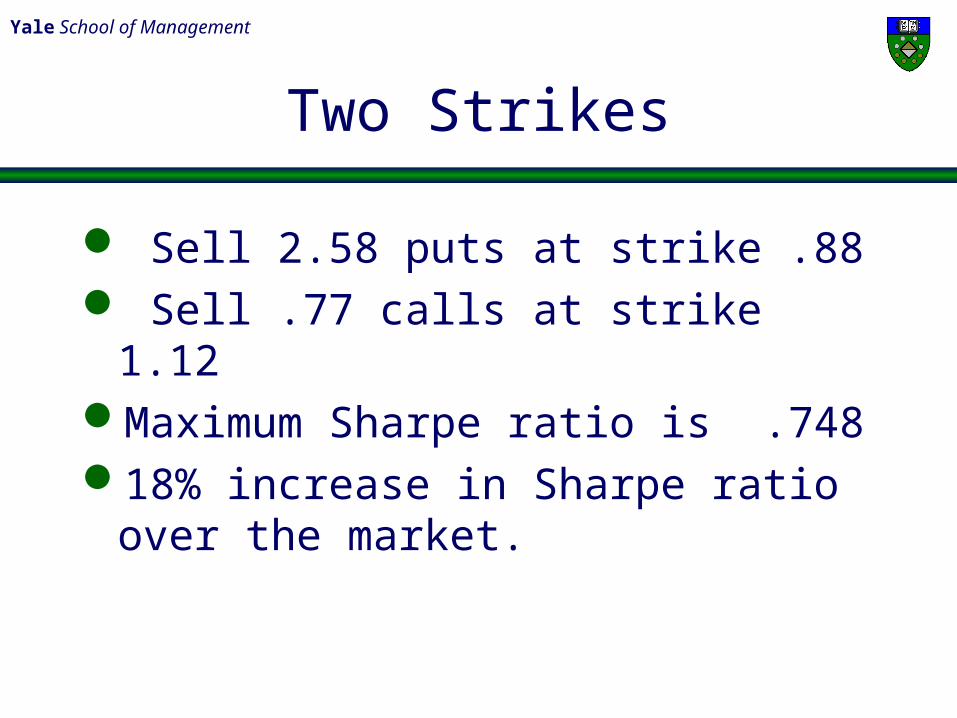

Two Strikes

Sell 2.58 puts at strike .88 Sell .77 calls at strike 1.12Maximum Sharpe ratio is .74818% increase in Sharpe ratio over the

market.

Yale School of Management

Yale School of Management

Dynamic Strategies

Conditioning on past performance. Brown, Harlow and Starks, Chevalier and

Ellison, Brown, Goetzmann and Park, Carpenter and others.

Result: poor performance implies increasing leverage.

Good performance, implies decreasing expected return towards market.

Yale School of Management

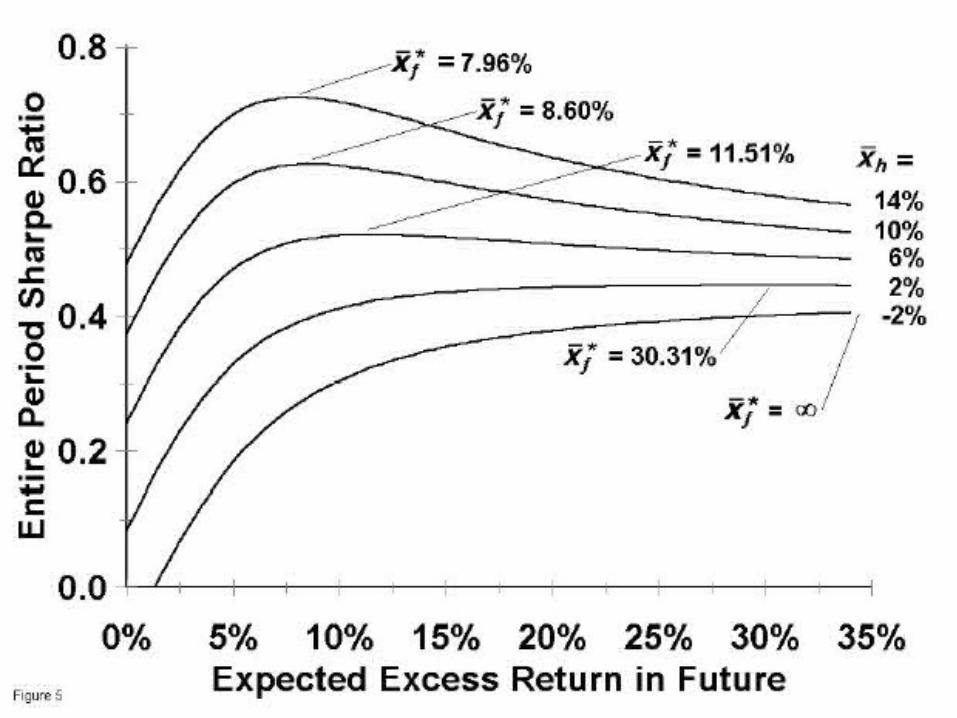

Intuition

Conditional return in the first period, you can minimized expected variance over the whole period by choosing an expected return equal to it.

Dynamic strategy is like static option strategy in that it moves state payoffs from one period to another to improve Sharpe ratio.

Yale School of Management

Yale School of Management

Yale School of Management

Manipulation-Free

Manipulation = rebalancing of the portfolio away from the benchmark even when there exists no informational reason to do so.

Yale School of Management

Requirements

Should provide a unique ranking of funds for a meaningful set of investors.

Should be “memoryless” – no dynamic strategy should allow improvement.

Implies time-separable, concave utility.Wealth-independent – power utility.Uninformed investor should hold market.

Implies a single risk aversion parameter.

Yale School of Management

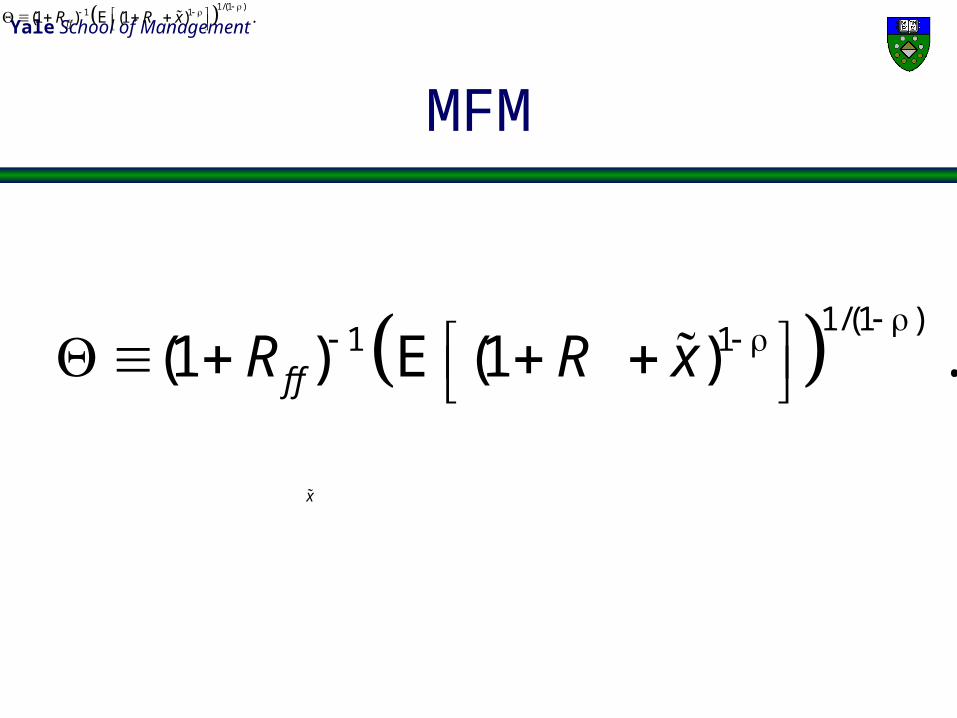

MFM

1/(1 )1 1(1 ) (1 ) .f fR R x

E

1/(1 )1 1(1 ) (1 ) .f fR R x

E

x

Yale School of Management

Risk-Aversion Parameter

Representative investor holds mkt:

= 0: Rank on Arithmetic Average = 1: Rank on Geometric Mean >2: Higher Risk Aversion

2( ) /m mr

Yale School of Management

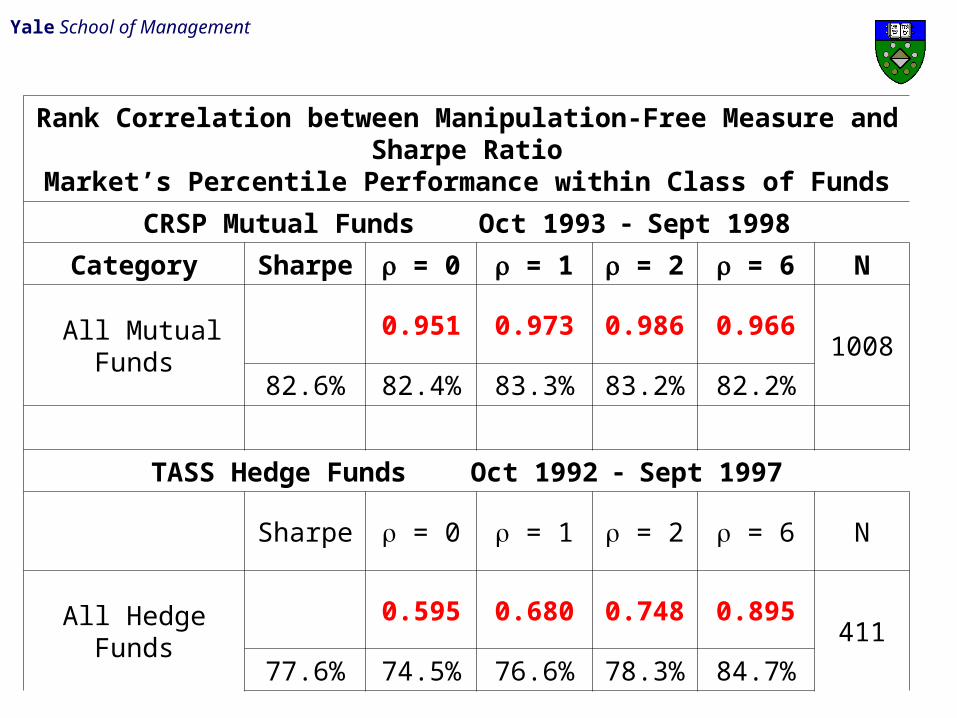

Empirical Tests

A test of the Sharpe ratio.Equity mutual fund returns 1993 – 2003.Hedge fund returns 1992 – 2002.Examine rank correlations of Sharpe and

MFM.Does skewness affect ranking differences?Parameter and time-period sensitivity.

Yale School of Management

Rank Correlation between Manipulation-Free Measure and Sharpe RatioMarket’s Percentile Performance within Class of Funds

CRSP Mutual Funds Oct 1993 Sept 1998

Category Sharpe = 0 = 1 = 2 = 6 N

All Mutual Funds0.951 0.973 0.986 0.966

1008

82.6% 82.4% 83.3% 83.2% 82.2%

TASS Hedge Funds Oct 1992 Sept 1997

Sharpe = 0 = 1 = 2 = 6 N

All Hedge Funds0.595 0.680 0.748 0.895

411

77.6% 74.5% 76.6% 78.3% 84.7%

Yale School of Management

Rank Correlation between Manipulation-Free Measure and Sharpe RatioMarket’s Percentile Performance within Class of Funds

CRSP Mutual Funds Oct 1998 Sept 2003

Category Sharpe = 0 = 1 = 2 = 6 N

All Mutual Funds0.981 0.962 0.886 0.552

3248

42.7% 42.5% 45.8% 49.5% 55.7%

TASS Hedge Funds Oct 1997 Sept 2002

Sharpe = 0 = 1 = 2 = 6 N

All Hedge Funds0.765 0.848 0.881 0.856

799

9.3% 8.8% 10.5% 13.5% 18.4%

Yale School of Management

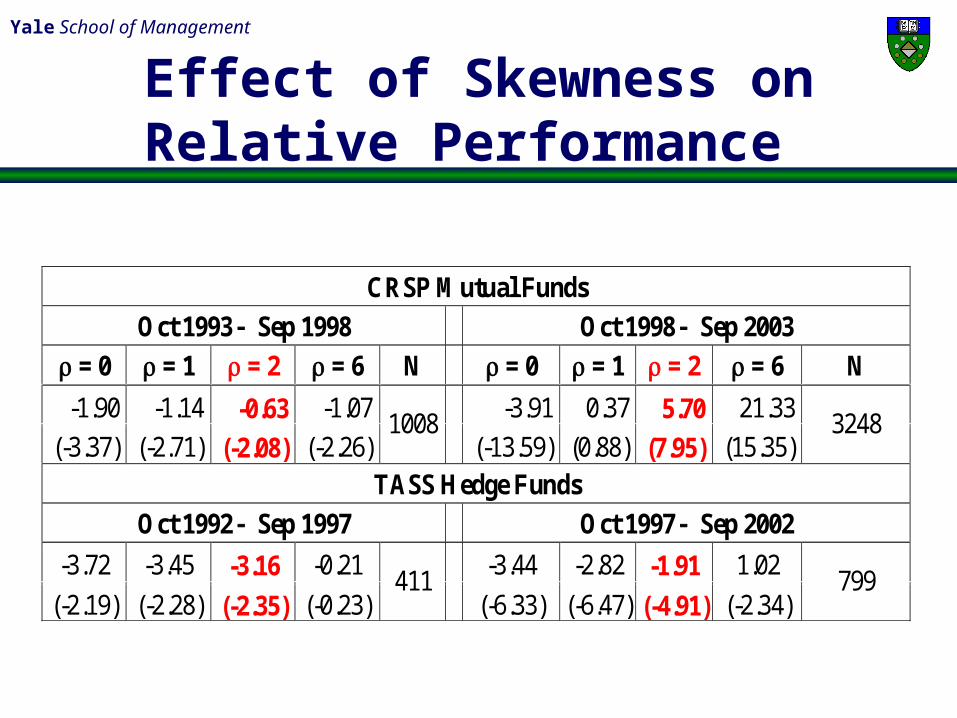

CRSP Mutual Funds

Oct 1993 Sep 1998 Oct 1998 Sep 2003

= 0 = 1 = 2 = 6 N = 0 = 1 = 2 = 6 N

-1.90 -1.14 -0.63 -1.07 -3.91 0.37 5.70 21.33

(-3.37) (-2.71) (-2.08) (-2.26) 1008

(-13.59) (0.88) (7.95) (15.35) 3248

TASS Hedge Funds

Oct 1992 Sep 1997 Oct 1997 Sep 2002

-3.72 -3.45 -3.16 -0.21 -3.44 -2.82 -1.91 1.02

(-2.19) (-2.28) (-2.35) (-0.23) 411

(-6.33) (-6.47) (-4.91) (-2.34) 799

Effect of Skewness on Relative Performance

Yale School of Management

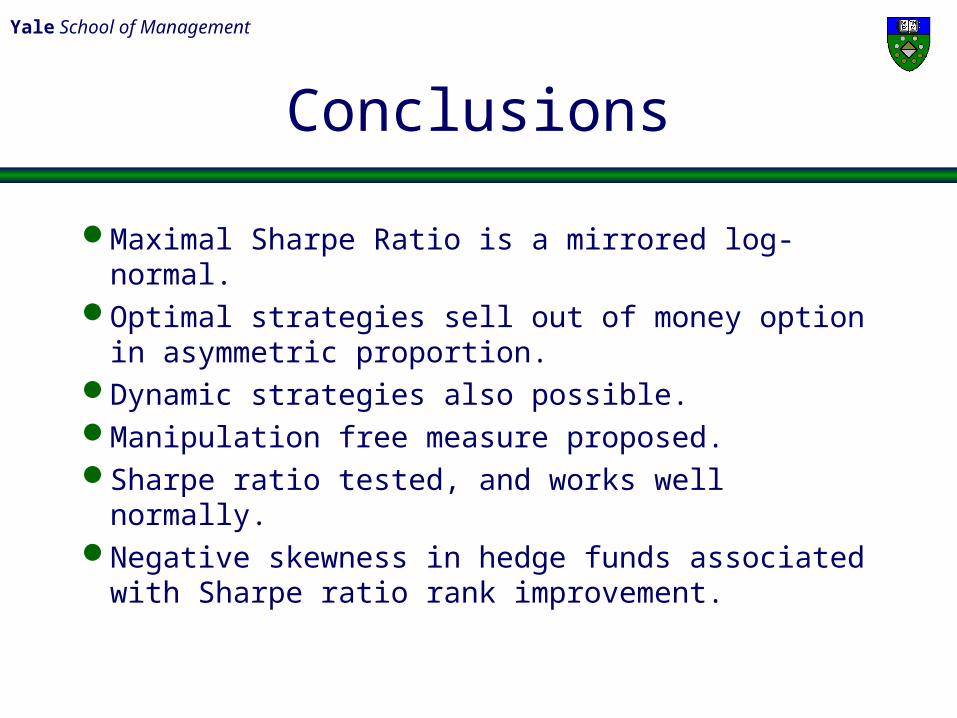

Conclusions

Maximal Sharpe Ratio is a mirrored log-normal.Optimal strategies sell out of money option in

asymmetric proportion.Dynamic strategies also possible.Manipulation free measure proposed.Sharpe ratio tested, and works well normally.Negative skewness in hedge funds associated with

Sharpe ratio rank improvement.