Embed Size (px)

Citation preview

Zakat and Economic Justice: Emerging International

Models and their Relevance for Egypt

Takaful 2013Third Annual Conference on Arab Philanthropy and Civic Engagement

June 4-6, 2013Tunis, Tunisia

Dr. Jennifer BremerProfessor of Practice and Chair,

Department of Public Policy and AdministrationAmerican University in Cairo

AbstractZakat, one of the five pillars of Islam, is a charitable donation incumbent upon all Muslims with assets above a specified level. Eight purposes are defined in the Qur’an for the use of zakat donations, of which the most important is the support of the poor and unfortunate. Although reliable estimates of zakat generation are not available, anecdotal evidence indicates that very large sums are generated annually, in the range of several billion or tens of billions of dollars. A debate has arisen in recent years over how to manage and use zakat, encompassing three main areas. First, scholars and practitioners disagree as to whether zakat must be used for direct donation to individuals or can be used to support institutions that serve individuals or to combat poverty through development projects such as microfinance. Second, conservative scholars argue that only Islamic governments can collect zakat, which constitutes one of the few permitted sources of taxes to an Islamic government while reformists promote private nonprofit organizations as equally appropriate. Zakat funds relying on the latter model are spreading in the West, even as professional managers of zakat funds in Islamic countries are moving to explore greater use of financial management and marketing tools drawn from business models. A third issue surrounds the use of a share of zakat collections for program administration by private parties. Other issues include how to respond to demands by reformers for increased transparency and accountability from state or private institutions that manage zakat collection and distribution; how to expand the definition of the purposes for which zakat can be used; and the extent to which zakat can or should serve to redistribute wealth across a society to achieve social justice.

This article explores these issues based on field research and a review of the literature to examine current practices, with an emphasis on emerging innovative models of zakat for development (Z4D) management and how they differ from traditional practice. Indonesian and Malaysian experiences, including corporate and public-private models, and analysis of emerging US and UK zakat funds provides insights into such new practices. A case study of Egypt is provided based on preliminary field work, interviews with the official zakat organization, Nasser Social Bank, a review of regulations and fatwas issued, and a case study of one highly successful application of Z4D in a Delta village, Tafahna al-Ashraf. The case study sheds light on how the use and management of zakat are evolving in Egypt and points the way to the development of modernized models that build on traditional zakat institutions to meet Egypt’s development needs. Reform of zakat along the lines pioneered in Southeast Asia, particularly a shift from traditional charity to incorporate greater support to sustainable poverty alleviation, would potentially mobilize greater zakat donation, raise transparency and accountability, expand the scope for collaboration with community-based civil society groups and corporations, and increase the impact of this central Islamic institution.

IntroductionZakat is one of the five pillars of Islam, the elements of the faith that are obligatory for all believers. Zakat is the only pillar that deals with finance and also the only one that relates directly to Islamic governance. Unlike the statement of faith (the shahada), the five daily prayers (salat), fasting during Ramadan (sawm), and the pilgrimage to Mecca (the haj), zakat is an obligation to society and to specific classes of individuals within that society.

Zakat is unique among the five pillars in that it cannot be performed alone. While each of the other pillars unquestionably plays an important part in Islamic societies -- shaping rituals of faith that bring Muslims together as families (to break the Ramadan fast), as a community (to pray, especially in the Friday prayer), or as a broader society (joining in the annual haj pilgrimage or the lesser omrah as representatives of the global umma community) -- zakat is the only pillar that requires the participation of others beside the person performing it: there must be a receiver as well as a giver. Each partner in the zakat exchange must perform his or her own duties and meet the obligations of the zakat system in order for the other partner to fulfill his or her role.

The zakat obligation is fundamental to the concept of social justice in Islamic society. Payment of zakat establishes a direct link between the well-off in society and those in need. Zakat is not only a means of providing for the social welfare of those at the bottom of society, but also a practical mechanism to set some limits around inequality. As zakat obligations are based on assets, at least in principle, payment of zakat transfers a share of the assets of those who have accumulated wealth to the poorest.

The structure of zakat thus explicitly promotes equity and social justice by working at both ends of the income spectrum. At the upper end, zakat serves to prevent over-concentration and excessive accumulation of wealth by mandating that a share of all wealth remaining in the donor’s hands at the end of the year over and above the family’s needs be redistributed to those in need. At the lower end, it specifies the categories within the needy population that should receive assistance. Although the rate of zakat assessment, 2.5 percent (one-fortieth) for the most common forms of assets, may not seem to be a very high amount, over time, it can make a significant contribution to equity, but, as will be discussed in some detail later in this paper, that contribution can come at an equally significant cost in the form of reduced growth if zakat is devoted exclusively to supporting short-term consumption.

Zakat, used properly, has the potential to foster a greater degree of equality within society, putting a floor under the living standards of the poorest members of society, but also slowing the accumulation of wealth by those who are generating a surplus beyond their requirements and thus contributing to social equity.

Jen

nif

er B

rem

er

51

52

This paper examines how Muslim societies are reshaping the institutions of zakat to make it a more effective tool for social justice and development in the modern world. Its aim is to explore the use of zakat to fund development programs that have a lasting impact on poverty and social inequality, as opposed to the short-term consumption impact of distributing cash or in-kind donations to individuals.

The need to reexamine such a key institution as zakat is urgent because the current period constitutes an extremely challenging time for Muslim societies, particularly in the Middle East. We are witnessing an era that is bringing to power governments with a strong Islamic, even Islamist, ideology. At the same time, social change and economic stresses are raising the salience of issues such as social justice, equity, poverty, job creation, and growth. Governments in the region have failed for decades to address social equity concerns effectively, and early indications of how Islamist parties will perform are hardly more encouraging in this regard. At the same time, civil society and philanthropic institutions in the region are evolving rapidly (John D. Gerhart Center, 2008), but the ability of civil society to contribute to addressing these urgent challenges depends to no small degree on the availability of resources. Many organizations have historically been reliant on Western funders, but the international donors have thus far not been able to reach a modus operandi with the new Islamist governments, nor are the latter welcoming to foreign funding, at least to date.

This combination of pressures on social equity institutions makes it imperative to reexamine every tool available to Muslim-majority societies to address social justice. Traditional funding mechanisms, in particular, must be reexamined to find ways to support civil society and development programs more generally, including those, such as zakat, that have been widely used by Islamist organizations, drawing on their own international as well as domestic sources (Siam, 2012).

Zakat is not only one of the most important of these tools, but it is one that has itself been going through a period of innovation and critical reexamination during the past two decades, although primarily in Muslim-majority countries outside the Middle East. In the West and in the Far East, Muslim leaders in the private sector and civil society and Islamic scholars are reconsidering the implications of the Islamic principles of social justice, Islamic governance, and Islamic economics for zakat management in the modern era. This reexamination is part of a broader consideration of how Islamic principles can be applied more concretely, making the transition from idealized religious and historic models into operational institutions that can meet the very real challenges of the present. It has arguably progressed more rapidly among Muslim communities in the West and Southeast Asia, but is really just beginning in the Arab world. The political changes witnessed over the past two years, and by no means concluded at this writing, press Arab leaders to join the search for solutions to pressing social and economic problems. Throughout the past decades of failure to achieve inclusive broad-based growth and social justice, Muslim commentators in the Arab world could attribute these shortcomings to the generation of Mubarak and Ben Ali, their Western supporters, and the corrupt regimes that they created. Now that the Islamists have themselves moved into positions of power, they cannot escape the responsibility to address the social justice, governance, and economic challenges facing the Middle East.

In confronting the huge reform challenges before them, it is natural for the new Islamists to look to the experiences of other Muslim-majority countries -- Turkey, Malaysia, Indonesia, and others -- that are repeatedly turning in high and quite steady rates of growth, addressing poverty, and making progress on governance. Seeing their success, it is appropriate to ask, what can be learned from these experiences about how Islamic institutions can contribute to the remaking of Arab economies, societies, and governance.

Although this paper limits its consideration to one such institution, zakat, it deals with issues central to these broader concerns. As zakat is an institution at the heart of Islam not only as a religion, but as the source of development approaches from Islamic finance to Islamic social justice, zakat’s effectiveness and its contribution to progress on the Islamic reform agenda are both of the highest importance.

The remainder of this paper will be organized around how zakat as an institution is to be governed and how zakat’s potential as a tool for economic development and social justice can be realized. Following a discussion of the hypotheses and conceptual framework underlying the analysis, it explores new models and emerging experience in countries outside the Middle East and, within the region, in Egypt. The discussion closes with a brief consideration of several current controversies that relate to how zakat is to be generated, managed, and distributed, with a specific focus on issues affecting Zakat 4 Development (Z4D).

The first section, addressing emerging practices in zakat governance, examines the organizational models being used to govern the collection and distribution of zakat. In this area, the key controversy surrounds the question of public vs. private institutional roles. To address this controversy, the paper will look at the growth of private zakat institutions in the West, in Southeast Asia, and in Egypt. How can these models contribute to increasing the flow of zakat, which is self-evidently a precondition to achieving significant increases in impact?

The second section examines zakat’s potential as an economic development tool. It considers, first, the effect of zakat payments and receipts on the return to capital and thus on the growth of assets. It presents the economic rationale for repositioning zakat from the traditional model of unconditional cash transfer to a model that puts greater emphasis on generating an economic return, the pathway to transforming zakat recipients ultimately into zakat donors. Second, it considers how zakat could be put to work more effectively to realize this potential

Jenn

ifer Brem

er

and to become a contributor to economic development. Finally, it addresses one of the main controversies that surrounds use of zakat for development: to what extent can zakat be devoted to economic development projects or programs rather than only to individual-to-individual transfers? To address this question, it looks at recent rulings, at new models developed in zakat programming outside the Arab world, and also at some promising experiments in Egypt.

The final section considers how zakat institutions are addressing the challenges of modernizing zakat, including how a number of controversies in zakat management are being dealt with. The most important of these is arguably the redefinition of the eight Qur’anic categories of recipients eligible for zakat to broaden the utility of zakat to address the needs of a 21st Century society. In matters of religious doctrine, especially in Islam, there will always be many who argue for the strict interpretation of how zakat is to be implemented, particularly with regard to matters that are dealt with very specifically in Quranic language. Nonetheless, a great deal of creative rethinking is also emerging to reinterpret the categories and other Zakat requirements in light of modern social needs.

Study hypotheses and conceptual frameworkAlthough all of the evidence available suggests that most zakat is intended by the giver to be used for short-term consumption, this use does not fit well with the role assigned to zakat in Islamic doctrine as a means to build social justice and equity. This paper explores alternative distribution mechanisms, with a specific emphasis on how zakat can contribute to economic development. Charitable support to short-term consumption needs of the poor -- zakat’s main intended beneficiaries -- can undoubtedly relieve the burden of poverty, but such assistance cannot achieve a sustained improvement in their lives, lift them out of poverty, nor contribute in a meaningful way to the broad-based, inclusive economic development that is the best and arguably the only path that can lead a society as a whole out of poverty.

On the contrary, to the extent that zakat redirects resources from long-term productive investment into short-term consumption, the improvement in living standards by the zakat recipients will come at the cost of growth in the economy over the long-term. The inescapable implication of this logic is that an overemphasis on charity as a strategy for managing zakat will over time undermine the very aim of zakat, which is to promote a more equitable and socially just society, by raising the living standard and dignity of those at the bottom of the income distribution and by promoting continuing advancement within the society and the economy, which includes social justice.

How, then, can zakat be directed to have a greater impact on development? This paper offers an exploratory analysis of this question, based on the following two hypotheses:

H1 - Use of zakat is evolving through the creation and application of new models that increase impact on development, including greater zakat use for income generation in contrast to charity, emergence of innovative collection and distribution institutions, particularly outside the government, and better governance.

H2 - Egypt’s zakat institutions are participating in this evolution, perhaps not to the full extent needed to maximize zakat’s effectiveness as a development tool, but in ways that contribute to the global repositioning of zakat.

The study reported here applied a three-part methodology to gather evidence for the assessment of these two hypotheses. First, a literature review was conducted focused on the use of zakat for development. Although there is a tremendous volume of writing on zakat, only a small portion of it focuses on Z4D or issues related to this topic. Even so, this is a fast-evolving area of analysis and writing within the Islamic finance and development literature, drawing increasing attention from scholars; no claim is made to an exhaustive review of this literature, particularly to the newest work in Arabic and Asian languages (Malay, Bahasa Indonesia, Hindi, Urdu, Bengali, etc.).

Second, information was collected on new zakat models, new institutions, and innovations in zakat governance by analyzing information on the websites of selected public and private zakat institutions, primarily in the Middle East, United States, United Kingdom, and Indonesia. In the case of the United States, publicly available information in selected tax returns and annual reports of a selection of the zakat institutions identified were also analyzed. Particular attention was given to the current status and evolution of zakat models in Egypt on the basis of interviews with experts and officials involved in zakat, examination of models developed, a review of recent fatwas on zakat, and preparation of brief case studies of several noteworthy examples of innovation. While most of the case studies are in line with global experiences, one case examines the experience of a Delta village, Tafahna al-Ashraf, that has quite literally transformed itself over the past twenty years through a locally-initiated and locally-led Z4D process.

Third, based on the information collected, an analysis of the options for strengthening Z4D programming was conducted with the aim of identifying recommendations for advancing zakat’s effectiveness as a tool for economic and social development in Egypt and the Islamic world more generally. This analysis addressed two main sets of issues: 1) improvements to the governance of zakat institutions and 2) Z4D strategies to maximize zakat’s potential as an economic development tool.

Jen

nif

er B

rem

er

53

54

Because much of the analysis presented is based on secondary sources, this article will not follow the usual structure of literature review-methodology-data analysis. Instead, the article will be organized around the two main sets of issues identified above- governance and economic development- and discussion of the literature will be integrated into each of these. Following this introductory section, each of those will be dealt with in turn. The article will conclude with a discussion of the implications of Z4D for national development strategies in countries with a large Muslim population, and possible next steps in both research and practice.

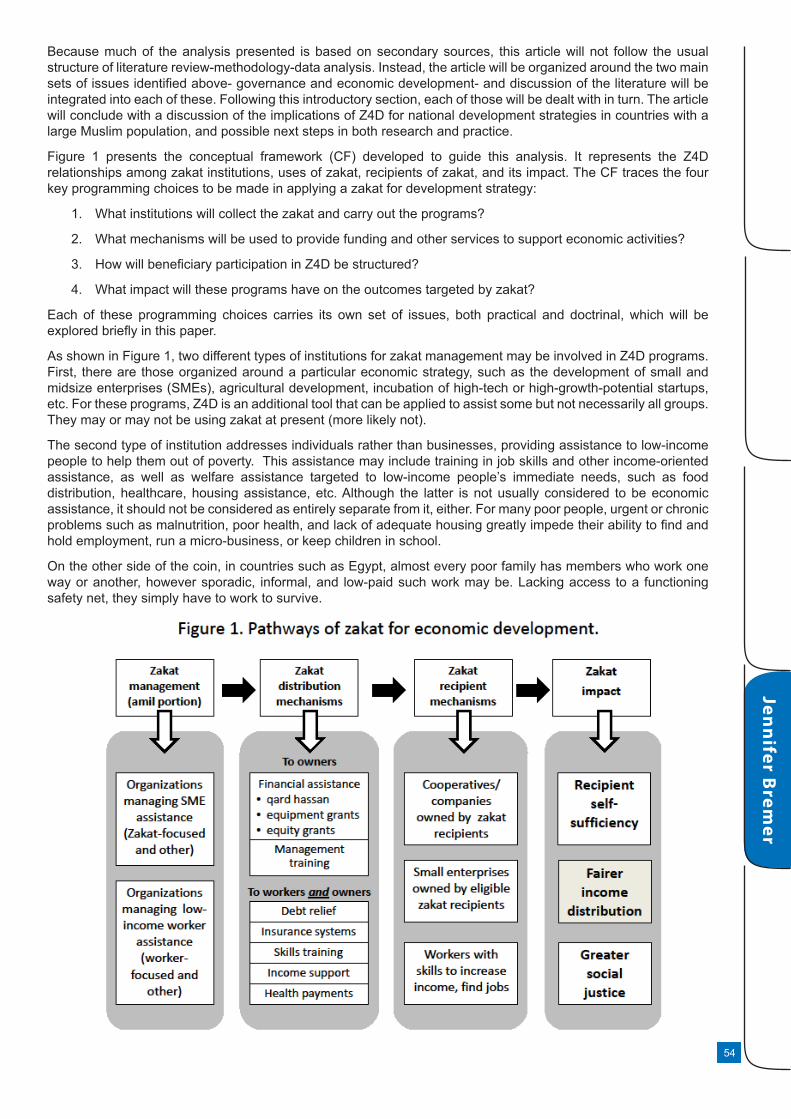

Figure 1 presents the conceptual framework (CF) developed to guide this analysis. It represents the Z4D relationships among zakat institutions, uses of zakat, recipients of zakat, and its impact. The CF traces the four key programming choices to be made in applying a zakat for development strategy:

1. What institutions will collect the zakat and carry out the programs?

2. What mechanisms will be used to provide funding and other services to support economic activities?

3. How will beneficiary participation in Z4D be structured?

4. What impact will these programs have on the outcomes targeted by zakat?

Each of these programming choices carries its own set of issues, both practical and doctrinal, which will be explored briefly in this paper.

As shown in Figure 1, two different types of institutions for zakat management may be involved in Z4D programs. First, there are those organized around a particular economic strategy, such as the development of small and midsize enterprises (SMEs), agricultural development, incubation of high-tech or high-growth-potential startups, etc. For these programs, Z4D is an additional tool that can be applied to assist some but not necessarily all groups. They may or may not be using zakat at present (more likely not).

The second type of institution addresses individuals rather than businesses, providing assistance to low-income people to help them out of poverty. This assistance may include training in job skills and other income-oriented assistance, as well as welfare assistance targeted to low-income people’s immediate needs, such as food distribution, healthcare, housing assistance, etc. Although the latter is not usually considered to be economic assistance, it should not be considered as entirely separate from it, either. For many poor people, urgent or chronic problems such as malnutrition, poor health, and lack of adequate housing greatly impede their ability to find and hold employment, run a micro-business, or keep children in school.

On the other side of the coin, in countries such as Egypt, almost every poor family has members who work one way or another, however sporadic, informal, and low-paid such work may be. Lacking access to a functioning safety net, they simply have to work to survive.

Jenn

ifer Brem

er

These two types of programs -- those aimed at businesses and those aimed at individuals-- overlap in the area of microenterprise, including microfinance. By definition, the microentrepreneur is an individual usually living in poverty or close to it. Although the institutions providing micro-credit may consider themselves as belonging firmly to the first category, economic development, for their clients the distinction may be quite meaningless. Indeed, the failure of microfinance programs to recognize and deal with the reality that many microentrepreneurs have urgent family welfare problems, or are only an illness or accident away from financial calamity, arguably limits the effectiveness of such programs as a pathway out of poverty).

Moving to the second column in Figure 1, we argue that Z4D programs can make use of a variety of different zakat distribution mechanisms, which, like the institutional options shown in the first column, may be directed to current or potential business owners, to workers and their families, or to both owners and workers (and many microenterpreneurs are both business owners and employed somewhere else).

Seven assistance approaches are identified, although in practice an effective program would generally combine several if not all of these. Building on the points made above, the second category of Z4D tools offers assistance that is potentially important for small business owners as well as workers. Not all of the former are by any means assured of earning a reliable income that meets the zakat standard of a dignified standard of living for their families.

Two categories of assistance make up Z4D. The first is assistance to current or potential business owners, which may include financial assistance taking various forms, and management assistance, which would generally provide training or technical assistance. Three principal types of financing can be provided using zakat, including qard hassan (interest-free loans), equipment grants, and equity grants. Both of the first two are well known and widely used in zakat programs, but the third category is generally not found in the literature. A key point argued here is that, for the small business or microenterprise, equity grants are in fact the most useful form of assistance and the one best suited to zakat.

Before turning to discuss these financing mechanisms in somewhat more detail, however, it may be useful to explore briefly what types of economic activities are encompassed within the concept of Z4D. Although most programs appear to focus on microenterprises, the current fascination of many donors, in fact the development of midsize enterprises is essential for the creation of well-paying jobs and for economic growth in general. Like the villagers in Garrett Hardin’s famous “Tragedy of the Commons”, microenterprises may enter a limited market in competition with each other without actually increasing the total income generated. Each new firm simply takes a small part of the market of every other entrant, eking out a small income for himself at the expense of further impoverishment of his peers. When congestion and other costs rise beyond a certain point(as may happen when too many vendors cluster in a limited space, for example), gross and net income may even fall as the number of entrants increases but customers are driven away not only from the vendors themselves, but from other shop and businesses in the area.

While microenterprises and programs to support them undoubtedly have a role to play in economic development, they are hardly a one-size-fits-all approach to income generation and other models deserve greater attention. Such models include not only the full range of private enterprise structures – sole proprietorships, family-owned businesses, partnerships and joint stock corporations, etc. – but also potentially other collective structures such as cooperatives. Cooperatives may bring together formal or informal small and micro-enterprises for collaborative investment, purchasing, or marketing as well as individuals, depending on their purpose and sector.

Whether corporation or cooperative, these models for collective action permit the business to begin on a larger scale than a simple microenterprise and to mobilize a greater level of experience and management expertise, yet do not tie the business down with a large wage-bill in its early days (because owners do not get paid fully or indeed may forgo payment entirely until the business begins to turn a profit).

As the Tafahna al-Ashraf example discussed below demonstrates, nonprofit enterprises such as schools and hospitals can also be supported with zakat and can make an important contribution to local economic development, job creation, and expansion of services to local communities. For reasons of brevity, these various forms will not be discussed further here, but many of the mechanisms discussed apply equally to for-profit and nonprofit enterprises, both of which are recognized as important to development and social justice.

A degree of controversy surrounds the use of zakat and other tools of Islamic philanthropy to support these ventures, however, as discussed in the third section below. In particular, the use of zakat for construction, institutional development, or other applications that do not directly transfer the funds zakat as an asset to the poor and destitute, the primary targets for zakat giving, raise doctrinal issues. Controversy also surrounds the use of zakat to support program administration where the implementer is not an Islamic government.

A review of zakat and other Islamic finance websites suggests that qard hassan programs are among the most common programming components used. Their popularity may owe more to the desire to emulate microfinance or to the perceived absence of alternatives than to the effectiveness of such programs or their suitability to zakat financing. Indeed, qard hassan programs may fail both of these tests, particularly as they are connected in the case of zakat financing.

Jen

nif

er B

rem

er

55

56

The first problem arises because a condition of zakat validity is that the recipient become the owner of the funds provided, whereas a qard hassan is a loan. Various sophistries can be used to get around this, but at the end of the day it is not possible to impose a sanction for failing to return the funds, which undercuts the program.

Second, the inability to charge interest means that other funds must be found to cover administrative costs and any losses to preserve the value of the fund. Both of these problems can generally be addressed by relying on the amil portion and/or supplementing the zakat with sadaqa or other funds that have fewer constraints than zakat.

Grants of equipment, such as carpentry tools, are an established element in zakat programs (as discussed extensively in Ibrahim, n.d.), having been part of zakat practice for centuries. Sarif and Kamri (2009, 478) quote a commentary of al-Nawawi, a leading collector of hadiths from the 13th Century, to the effect that, “A craftsman would be given an amount sufficient to buy tools and equipment that allow him to work and gain his sustenance.” Grants of livestock also fall within this category, as does any item that permits the zakat recipient (the mustahiq) to generate income. Today, this approach may also be preferred to cash to ensure or at least encourage the use of the support for income generation rather than consumption.

The third approach discussed here, grants of equity, do not appear to have been used systematically. This is difficult to understand as equity is more valuable than equipment, because it can be put to any purpose, and is more consistent with the rule of tamleek, being an owned asset.

Grants of equity must be managed in a way that maintains a certain degree of pressure, whether social or financial, on the recipient, however, to ensure that the funds are used to build the business. Several of the mechanisms that could accomplish this have other important advantages, moreover, and would be likely to increase the program’s effectiveness overall. These include:

• The possibility of repeat infusions of equity over time, with future grants conditioned on how well the first grants are used;

• Continuing collaboration with the business in ways that go beyond the grant to include advice, business relationships such as purchase of the goods, etc.; and

• Formation of partnerships or cooperatives such that the investors pool their zakat to launch an enterprise.

This last approach has the potential to accelerate growth, as the enterprise starts at a higher scale, can benefit from partners’ diverse skills, and can exert social pressure through the other partners to keep each recipient on track. As with any enterprise with multiple shareholders, care would be necessary in assembling the investors to ensure, to the extent possible, that they are all committed to the business, that they each bring an important skill, and that they are trustworthy. Such an approach could be particularly effective in enabling preexisting groups, such as women participating in a longstanding rotating credit and savings association (ROSCA or Egyptian gamaiyya), to start a collaborative revenue-generating business, such as a tailoring workshop or cheese-making operation. Continuing involvement of the donor as an advisor and, after the zakat investment ceases, even as an investor would also be desirable.

It should be noted that there is no reason to assume that the zakat recipient(s) are starting a new business, rather than buying into an existing one. For example, grants of zakat could be used to enable workers in a small enterprise to become co-investing partners over time, provided that all of the other zakat provisos are met (such as the lack of benefit to the donor). This might be especially appropriate for small enterprises where the owner is retiring without a family member to take it over, in which the zakat payments would eventually leave him with a retirement fund and the workers as the business owners.

While zakat can be used to finance training and management assistance directly, it is perhaps better to look for ways that in-kind donations of services can be used to meet this need. This approach was also used in Tafahna al-Ashraf, with formal pledges of assistance being solicited from professionals resident in the community. Such assistance would more commonly be treated as sadaqa rather than zakat, however. Use of zakat to fund third-party services may also raise tamleek problems to the extent that the small business owners do not place sufficient priority on such services. In the author’s experience, small enterprises are rarely willing to pay the market price for technical assistance or training and the small scale of their business may in fact make such expenditure unprofitable.

The second type of distribution mechanism applies zakat to the benefit of both workers and owners. It applies standard zakat payments to the purpose of assisting the small businessperson to generate income by addressing the constraints that often undermine business success. The following categories exemplify but may not exhaust such applications:

• Debt relief: use of this standard zakat category could assist small business owners or workers to get out from under debt accrued from previous business-related or personal financial setbacks, thus giving them a fresh start.

Jenn

ifer Brem

er

• Insurance systems: mutual insurance programs, such as takafol, address an important barrier to business success and continued earnings by low-income community members, whose lack of assets makes them highly vulnerable to such setbacks as theft or fire.

• Skills training: voluntary use of zakat payments to buy a place in a training program can constitute an investment in the future success of a worker or business owner.

• Health payments: low-income workers and small business owners are often more subject to health issues (their own or their family members’), which can derail the business or their ability to work; payments for medical treatment, another standard zakat use, can thus support the business as well as the individual.

• Income support: While the business is in the early stage of establishment, building up production and sales and incurring investment costs, there may be a need for continuing some level of income support for the owner and for those workers eligible for this assistance; by separating this support from equity infusions, at least conceptually, the distinction between the two types of support would remain clearer, which would help to promote sound management of both types of financial transfer by the recipient.

One of the most intriguing debates in the field of zakat is the distinction made by some authors between what is permitted with respect to the first four categories (the poor, the needy, converts, and the zakat collectors) and to the final four. As discussed in Senturk (2007,130), these last are differentiated by use of a different preposition and by being stated as a purpose (freeing of slaves, serving the cause of Allah, and assisting those in debt or stranded travelers). The former are considered, in this interpretation, to be governed by the rule of tamleek (they must receive and exercise control over the resources as individuals) and to have, in effect, an ownership interest in the zakat even before it is given, and therefore a right to receive it. The latter, however, do not have these rights and thus zakat may be expended on their assistance indirectly, for example by supporting an institution that delivers services to people in these categories.

This distinction has perhaps been a driving force behind the reinterpretation of these categories to permit, for example, supporting research or education that frees minds or the society more generally from the “slavery” of ignorance, or by interpreting refugees as equivalent to stranded travelers, as discussed in the third section below.

The category of “serving the cause of Allah” is arguably the one most subject to reinterpretation, however. Depending on the author, it may be defined as anything from support to jihad fighters to broad support for social programs and institutions, such as schools and hospitals, extending to construction and general operation, as well as to the direct delivery of services.

These interpretations and the flexibility inherent in the zakat collector’s portion open the door to using zakat to support a wide range of institutions that support economic development through training, education, investment in income-generating projects, and so forth. They thus implicitly permit the comingling of zakat funds with funds from other sources.

As discussed elsewhere in this paper, zakat institutions in Indonesia have institutionalized such comingling through the concepts of ZIS (zakat-infaq-sadaqa) and ZISWAF (adding the waqf or endowment mechanism as a repository for zakat as well as other proceeds from charitable giving or income generating activities). The proceeds of infaq and sadaqa contributions -- which are voluntary and, unlike zakat proceeds, are not bound to specific uses -- can be used to fund institutional vehicles within which zakat distributions to the poor more effectively, covering administrative expenses or other program elements that are not zakat-fundable. For example, infusions of zakat as equity into a business owned by the poor could be coupled with training programs or marketing assistance, say, funded by the other charitable tools or by funds from non-religious sources. The institutions managing both types of funding can themselves be supported by the collector’s portion and/or by resources from infaq, sadaqa, awqaf, or from any non-religious source (as also discussed in the third section below).

In the search for institutional models that can meet the more complex requirements of economic development in the 21st Century, the flexibility of the waqf mechanism deserves greater recognition. Unlike other charitable institutions, zakat-based or otherwise, the waqf structure positively requires that the investment be used to generate income, as this is a prerequisite to having funds to allocate to the charitable purpose.

What is even less recognized, moreover, is that the investment side of waqf management can be as important in expanding economic opportunity and social equity as the charitable activities funded. For example, a waqf formed by a donation of urban land can be used to establish a facility for local small businesses, with the revenue going to provide healthcare for their families, training for their workers, or other purposes that support both equity and growth. Such models were extremely common in medieval awqaf, which often found a mosque or hospital surrounded by small businesses renting shops built with waqf resources on the waqf land and providing revenue to support the mosque or hospital. Modern financial management offers a broader range of creative financing tools to leverage the asset base of the waqf for inclusive growth than did medieval or even Ottoman finance, particularly in view of the entry of major banks and investment houses into Islamic finance.

Jen

nif

er B

rem

er

57

58

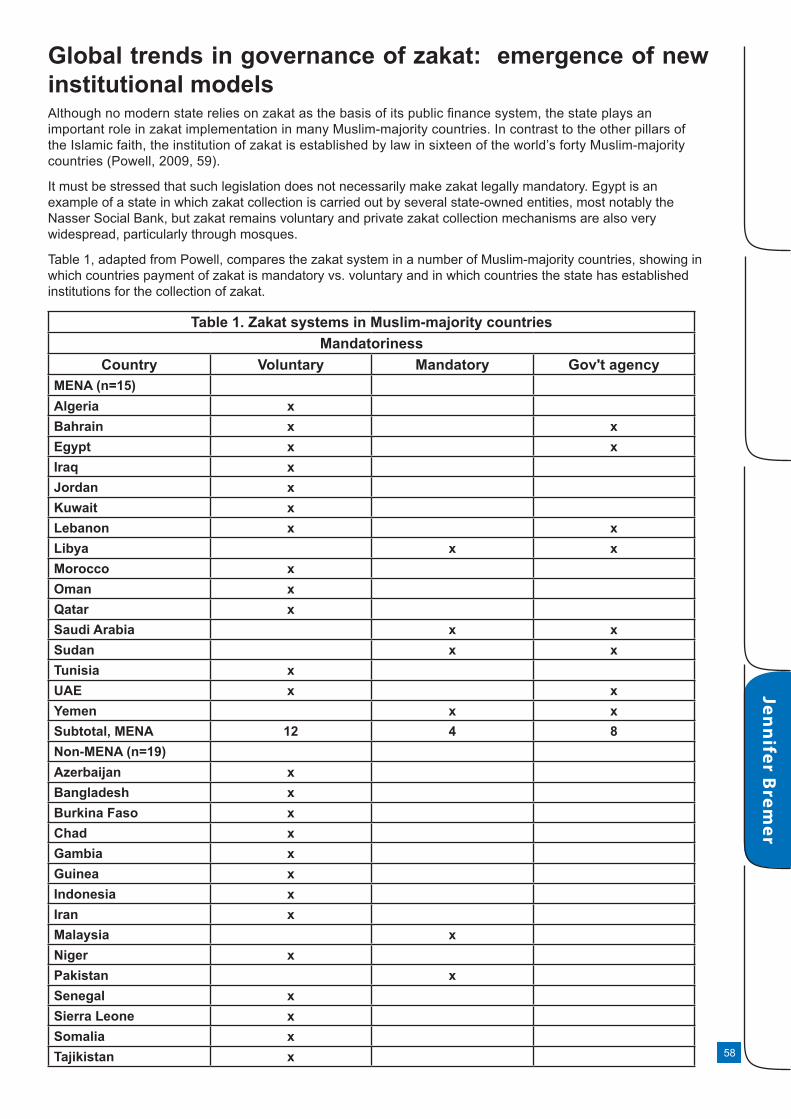

Global trends in governance of zakat: emergence of new institutional modelsAlthough no modern state relies on zakat as the basis of its public finance system, the state plays an important role in zakat implementation in many Muslim-majority countries. In contrast to the other pillars of the Islamic faith, the institution of zakat is established by law in sixteen of the world’s forty Muslim-majority countries (Powell, 2009, 59).

It must be stressed that such legislation does not necessarily make zakat legally mandatory. Egypt is an example of a state in which zakat collection is carried out by several state-owned entities, most notably the Nasser Social Bank, but zakat remains voluntary and private zakat collection mechanisms are also very widespread, particularly through mosques.

Table 1, adapted from Powell, compares the zakat system in a number of Muslim-majority countries, showing in which countries payment of zakat is mandatory vs. voluntary and in which countries the state has established institutions for the collection of zakat.

Table 1. Zakat systems in Muslim-majority countriesMandatoriness

Country Voluntary Mandatory Gov't agencyMENA (n=15)Algeria xBahrain x xEgypt x xIraq xJordan xKuwait xLebanon x xLibya x xMorocco xOman xQatar xSaudi Arabia x xSudan x xTunisia xUAE x xYemen x xSubtotal, MENA 12 4 8Non-MENA (n=19)Azerbaijan xBangladesh x xBurkina Faso xChad xGambia xGuinea xIndonesia x xIran xMalaysia x xNiger xPakistan x xSenegal xSierra Leone xSomalia xTajikistan x

Jenn

ifer Brem

er

Turkey xTurkmenistan xUzbekistan x Subtotal, non-MENA 16 2 4Total (34) 28 6 12

Source: Moneyjihad website and Powell (2009).

Conversely, where zakat is mandatory, the state collects it. Pakistan and Saudi Arabia are both examples of this combination. Even where zakat is mandated, however, government collection agencies are rarely if ever the only channel for zakat. Despite the existence of a formal system, mandatory or not, individuals may choose to make direct donations as part of their effort to ensure that they meet their zakat obligation, especially where they may feel that the receipt of donations to the government system by qualified recipients is not ensured.

The degree to which zakat is mandatory is an area of evolving practice. For example, Sudan’s Zakat and Taxation Act made zakat mandatory in 1984 (Otto, 2010, 217). More recently Egypt’s now-disbanded parliament had been considering a bill to recreate the Bait al-Mal (an Islamic equivalent to the national treasury, which collects and distributes zakat as well as various taxes; Suleiman,2012; see Namawi, n.d., for a description of this institution and its role in zakat). A news account of this proposal merits quoting at length because of the potential importance of this development and the insight it gives into the give-and-take in legislation on Islamic matters in post-revolution Egypt:

One bill, proposed by MP (Member of Parliament) Mohamed Talaat, provides for the establishment of a Bait al-Mal – “treasury-house” – which would collect money paid annually by Egyptian Muslims as zakat and ushur – religiously-decreed charitable donations and tithes. Talaat declared that the establishment of this institution would signal “the beginning of the dream of the restoration of the Islamic Caliphate.” His bill was approved by parliament’s religious affairs committee, chaired by the FJP’s (Freedom and Justice Party) Sayed Askar, and forwarded to a sub-committee for drafting. However, two key amendments were made: paying zakat into the Bait al-Mal would not be obligatory, but voluntary; and the new institution would not replace the existing tax authorities, as the bill originally envisaged. Former state-appointed Chief Mufti of Egypt Nasr Farid Wasel applauded the initiative and a proposal to establish a board of trustees to oversee the fund. He revealed that the Dar al-Ifta [the Egyptian institution headed by the mufti and responsible for issuance of authoritative fatwas] had itself put forward a similar idea in 1997, but it was blocked at the time by parliament and the Cabinet – then as now headed by Prime Minister Kamal al-Ganzouri.

(Kassab and Khawly, 2012)

It is difficult to say whether this bill will be reintroduced through the new parliament or Shura Council, when finally seated.

At this point, there is substantially more innovation in the governance of zakat through private channels. The expansion of the Muslim population in the West and the rising financial well-being of many families in this diaspora community have led to the creation of zakat institutions in the U.S. and the U.K. over the past several years. It is difficult to form a clear picture of the magnitude of this new activity, but data collected and analyzed from the Foundation Center’s database of the mandatory reports made by nonprofit organizations and foundations to the U.S. Internal Revenue Service (Form 990s), gives some idea of how zakat funds are growing.

For this analysis, zakat funds were identified through two procedures. First, the Foundation Center listings were searched for the term zakat, which not surprisingly occurs in the names of several organizations that collect zakat. Second, a web search was conducted to identify additional organizations and then to seek their IRS 990 reports in the database (this report is mandatory for all nonprofits seeking a tax exemption). The results of this analysis were then compiled for analysis.

It must be stressed that it is highly likely that a number of funds were missed; no claim is made that these figures capture the total zakat giving through institutional channels. The information is more useful as an indication of how some of the more prominent funds are growing and the increase in the number of funds that are explicitly focused on collecting zakat, although not necessarily exclusively.

This count also excludes both zakat payments that are made through mosques, which are not required to report to the IRS under the U.S. rules on the separation of religion and the state, and zakat payments that are distributed privately. Based on the management of zakat in other countries, it can by hypothesized that these two flows account for the largest share of all zakat payments.

Tables 2 and 3 summarize the results of this analysis. Whereas in 2001 only one institution was identified as collecting zakat and this organization, the Islamic-American Zakat Foundation, reported less than $39,000 in assets; by 2010 there were eleven organizations with a total of $46.7 million in assets. Between 2009 and 2010

Jen

nif

er B

rem

er

59

60

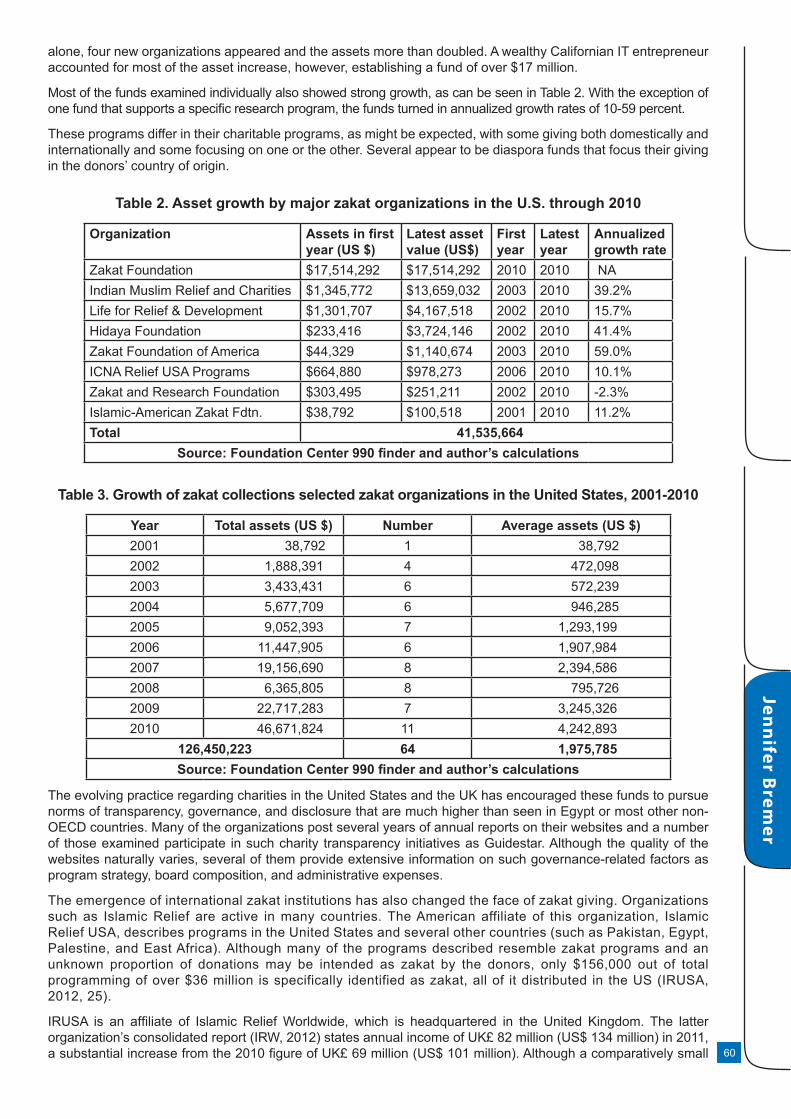

alone, four new organizations appeared and the assets more than doubled. A wealthy Californian IT entrepreneur accounted for most of the asset increase, however, establishing a fund of over $17 million.

Most of the funds examined individually also showed strong growth, as can be seen in Table 2. With the exception of one fund that supports a specific research program, the funds turned in annualized growth rates of 10-59 percent.

These programs differ in their charitable programs, as might be expected, with some giving both domestically and internationally and some focusing on one or the other. Several appear to be diaspora funds that focus their giving in the donors’ country of origin.

Table 2. Asset growth by major zakat organizations in the U.S. through 2010

Organization Assets in first year (US $)

Latest asset value (US$)

First year

Latest year

Annualized growth rate

Zakat Foundation $17,514,292 $17,514,292 2010 2010 NAIndian Muslim Relief and Charities $1,345,772 $13,659,032 2003 2010 39.2%Life for Relief & Development $1,301,707 $4,167,518 2002 2010 15.7%Hidaya Foundation $233,416 $3,724,146 2002 2010 41.4%Zakat Foundation of America $44,329 $1,140,674 2003 2010 59.0%ICNA Relief USA Programs $664,880 $978,273 2006 2010 10.1%Zakat and Research Foundation $303,495 $251,211 2002 2010 -2.3%Islamic-American Zakat Fdtn. $38,792 $100,518 2001 2010 11.2%Total 41,535,664

Source: Foundation Center 990 finder and author’s calculations

Table 3. Growth of zakat collections selected zakat organizations in the United States, 2001-2010

Year Total assets (US $) Number Average assets (US $)2001 38,792 1 38,792 2002 1,888,391 4 472,098 2003 3,433,431 6 572,239 2004 5,677,709 6 946,285 2005 9,052,393 7 1,293,199 2006 11,447,905 6 1,907,984 2007 19,156,690 8 2,394,586 2008 6,365,805 8 795,726 2009 22,717,283 7 3,245,326 2010 46,671,824 11 4,242,893

126,450,223 64 1,975,785 Source: Foundation Center 990 finder and author’s calculations

The evolving practice regarding charities in the United States and the UK has encouraged these funds to pursue norms of transparency, governance, and disclosure that are much higher than seen in Egypt or most other non-OECD countries. Many of the organizations post several years of annual reports on their websites and a number of those examined participate in such charity transparency initiatives as Guidestar. Although the quality of the websites naturally varies, several of them provide extensive information on such governance-related factors as program strategy, board composition, and administrative expenses.

The emergence of international zakat institutions has also changed the face of zakat giving. Organizations such as Islamic Relief are active in many countries. The American affiliate of this organization, Islamic Relief USA, describes programs in the United States and several other countries (such as Pakistan, Egypt, Palestine, and East Africa). Although many of the programs described resemble zakat programs and an unknown proportion of donations may be intended as zakat by the donors, only $156,000 out of total programming of over $36 million is specifically identified as zakat, all of it distributed in the US (IRUSA, 2012, 25).

IRUSA is an affiliate of Islamic Relief Worldwide, which is headquartered in the United Kingdom. The latter organization’s consolidated report (IRW, 2012) states annual income of UK£ 82 million (US$ 134 million) in 2011, a substantial increase from the 2010 figure of UK£ 69 million (US$ 101 million). Although a comparatively small

Jenn

ifer Brem

er

amount of this is directly identified as zakat (including UK£ 363,000 from the Kuwait Zakat House and UK£ 263,000 from IR Mauritius), it is reasonable to assume that many individual donations were in fact zakat payments.

The Islamic Relief Worldwide network was established in the UK in 1987 and now works in 30 countries. In addition to the UK operation, the IRW network includes affiliated IR entities in Belgium, Canada, Germany, Italy, Malaysia, The Netherlands, South Africa, Sweden, Switzerland, the US, and Australia. The network also works through: 1) registered offices in Ireland and Mauritius, 2) independent legal entities for program implementation in Bangladesh, Egypt, India, Kenya, Pakistan, 3) its own offices for project implementation in Afghanistan, Albania, Bosnia and Herzegovina, Chad, Egypt, Ethiopia, Haiti, Indonesia, Iraq, Jordan, Kosovo, Lebanon, Libya, Malawi, Mali, Niger, the Occupied Palestinian Territories, the Russian Federation, Somalia, South Sudan, Sudan, Tunisia, and Yemen, and 4) partnerships for project implementation with local organizations in India, China, Sri Lanka, and Japan.

This network is certainly the largest global network as measured by institutional presence, but it is not possible to say where it falls in comparison to other zakat collection and distribution organizations, given the non-transparency of reporting by many of the funds in the government sector.

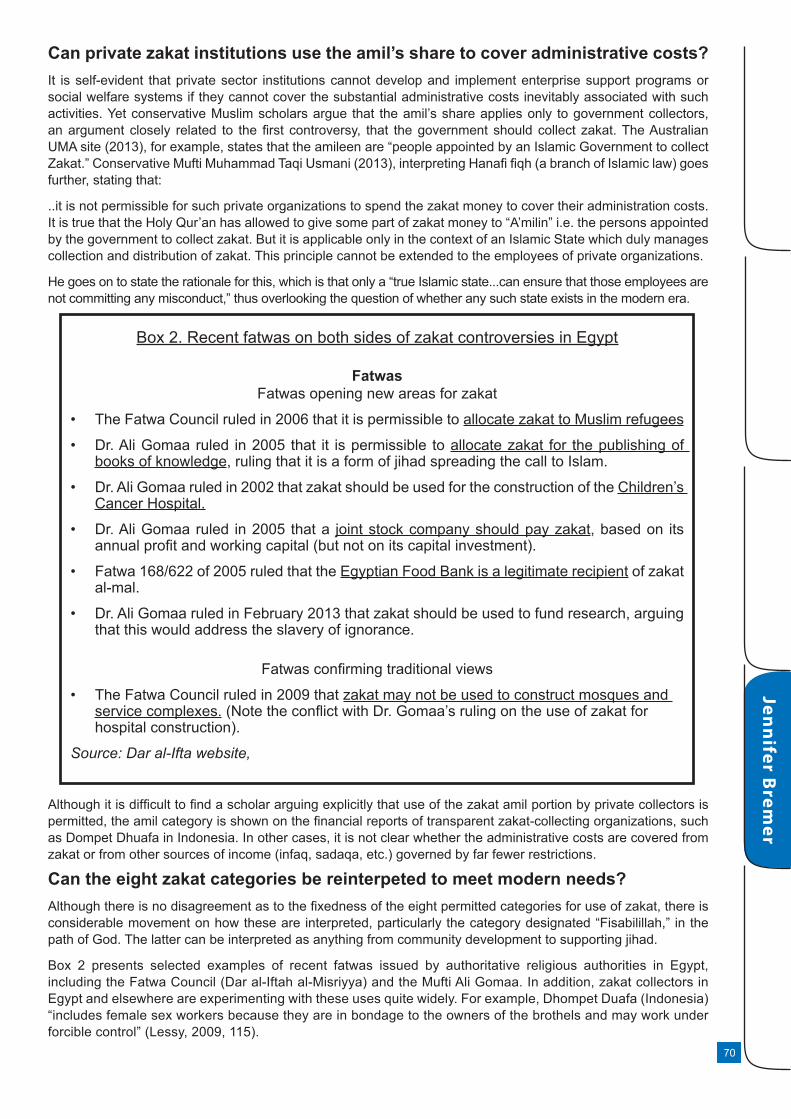

Within Egypt and the Middle East more generally, new models are also emerging. Box 1 summarizes two different models for zakat collection that have emerged recently.

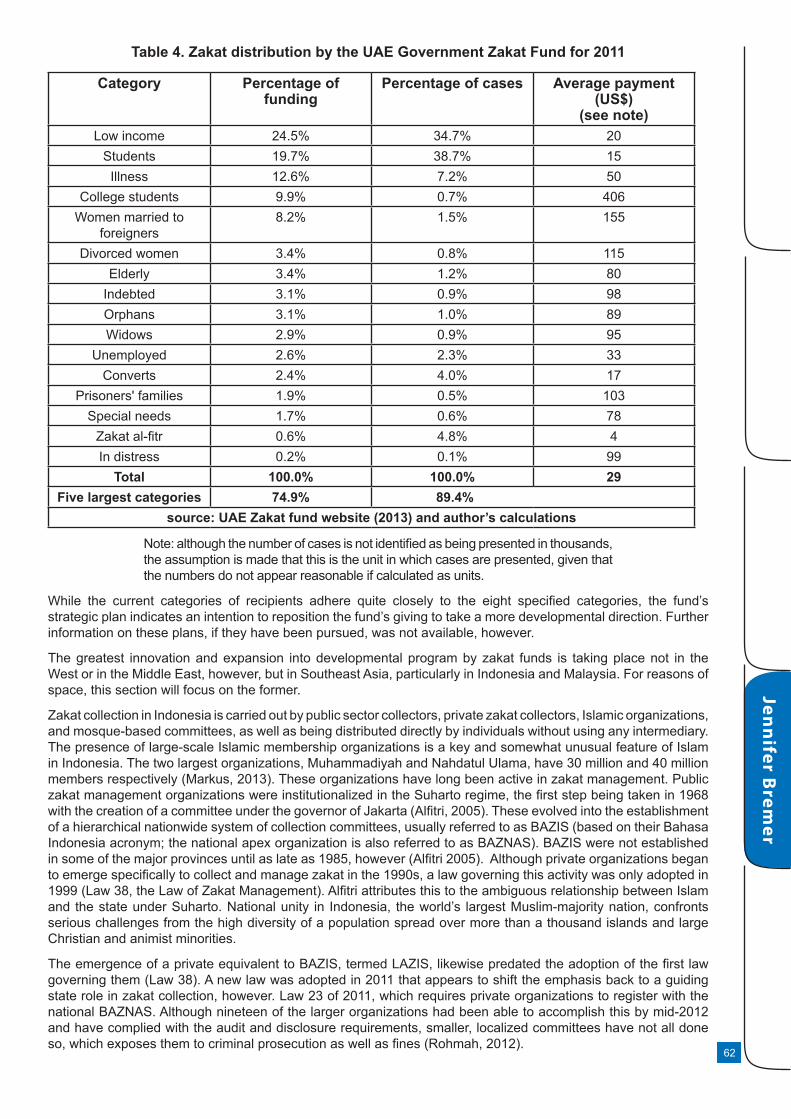

Elsewhere in the Middle East, the zakat fund of the United Arab Emirates sets a standard for transparency, providing fairly up-to-date quarterly financial reports as well as other information such as the board members and strategic plan on its website (UAE Zakat Fund 2013). This information makes it possible to calculate a reliable figure for government zakat disbursements for 2011, the last full year reported, broken out by category and number of recipients, as well as amounts dedicated to each category. A summary of this information is provided in Table 4. In 2011, the fund distributed the equivalent of US$ 229 million, including US$ 55 million for the poor, US$ 45 million for students, US$ 29 million for the sick, and US$ 23 million for college students, the four largest categories.

Box 1. Examples of new initiatives distributing or collecting zakat in EgyptLafakr.com http://www.lafakr.com/about.php

This web-based initiative, whose name means “no poverty,” was established by Mohamed El-Sawy, a well-known social activist. Its aim is to motivate donations, volunteering, and other collaboration in support of established charities. Although the website does not specifically mention zakat, the procedures described (identifying cases, following up to ensure impact, targeting the poorest) suggests at the least a zakat origin. This initiative’s website also describes its planned mechanism for distributing funds collected as being linked to three organizations that are quite involved in zakat collection and distribution and are widely seen as having religiously conservative leadership: Al-Orman, the Food Bank, and Resala.

National Bank for Development charitable accountswww.nbdegypt.com/personal-banking/charitable-accounts

AMEinfo (2013) reports that, “The state-owned NBD has established a program of “al-kheir” accounts. These accounts are described on the website as “an account opened by NBD in cooperation with ADIB [Abu Dhabi Islamic Bank] for the benefit of charities such as Children’s Cancer Hospital, Resala Institute and Dar Al Orman where the customers donate is in this account (Sadaka- Sadaka Gareya- Zakat).” ADIB is a publicly traded bank with substantial ownership by the Abu Dhabi’s leadership and state investment vehicles. ADIB has a joint venture bank in Egypt and, according to its website, its UAE bank also permits customers to make zakat payments by mobile phone and offers zakat advice by mobile.

Jen

nif

er B

rem

er

61

62

Table 4. Zakat distribution by the UAE Government Zakat Fund for 2011

Category Percentage of funding

Percentage of cases Average payment (US$)

(see note)Low income 24.5% 34.7% 20

Students 19.7% 38.7% 15Illness 12.6% 7.2% 50

College students 9.9% 0.7% 406Women married to

foreigners8.2% 1.5% 155

Divorced women 3.4% 0.8% 115Elderly 3.4% 1.2% 80

Indebted 3.1% 0.9% 98Orphans 3.1% 1.0% 89Widows 2.9% 0.9% 95

Unemployed 2.6% 2.3% 33Converts 2.4% 4.0% 17

Prisoners' families 1.9% 0.5% 103Special needs 1.7% 0.6% 78

Zakat al-fitr 0.6% 4.8% 4In distress 0.2% 0.1% 99

Total 100.0% 100.0% 29Five largest categories 74.9% 89.4%

source: UAE Zakat fund website (2013) and author’s calculations

Note: although the number of cases is not identified as being presented in thousands, the assumption is made that this is the unit in which cases are presented, given that the numbers do not appear reasonable if calculated as units.

While the current categories of recipients adhere quite closely to the eight specified categories, the fund’s strategic plan indicates an intention to reposition the fund’s giving to take a more developmental direction. Further information on these plans, if they have been pursued, was not available, however.

The greatest innovation and expansion into developmental program by zakat funds is taking place not in the West or in the Middle East, however, but in Southeast Asia, particularly in Indonesia and Malaysia. For reasons of space, this section will focus on the former.

Zakat collection in Indonesia is carried out by public sector collectors, private zakat collectors, Islamic organizations, and mosque-based committees, as well as being distributed directly by individuals without using any intermediary. The presence of large-scale Islamic membership organizations is a key and somewhat unusual feature of Islam in Indonesia. The two largest organizations, Muhammadiyah and Nahdatul Ulama, have 30 million and 40 million members respectively (Markus, 2013). These organizations have long been active in zakat management. Public zakat management organizations were institutionalized in the Suharto regime, the first step being taken in 1968 with the creation of a committee under the governor of Jakarta (Alfitri, 2005). These evolved into the establishment of a hierarchical nationwide system of collection committees, usually referred to as BAZIS (based on their Bahasa Indonesia acronym; the national apex organization is also referred to as BAZNAS). BAZIS were not established in some of the major provinces until as late as 1985, however (Alfitri 2005). Although private organizations began to emerge specifically to collect and manage zakat in the 1990s, a law governing this activity was only adopted in 1999 (Law 38, the Law of Zakat Management). Alfitri attributes this to the ambiguous relationship between Islam and the state under Suharto. National unity in Indonesia, the world’s largest Muslim-majority nation, confronts serious challenges from the high diversity of a population spread over more than a thousand islands and large Christian and animist minorities.

The emergence of a private equivalent to BAZIS, termed LAZIS, likewise predated the adoption of the first law governing them (Law 38). A new law was adopted in 2011 that appears to shift the emphasis back to a guiding state role in zakat collection, however. Law 23 of 2011, which requires private organizations to register with the national BAZNAS. Although nineteen of the larger organizations had been able to accomplish this by mid-2012 and have complied with the audit and disclosure requirements, smaller, localized committees have not all done so, which exposes them to criminal prosecution as well as fines (Rohmah, 2012).

Jenn

ifer Brem

er

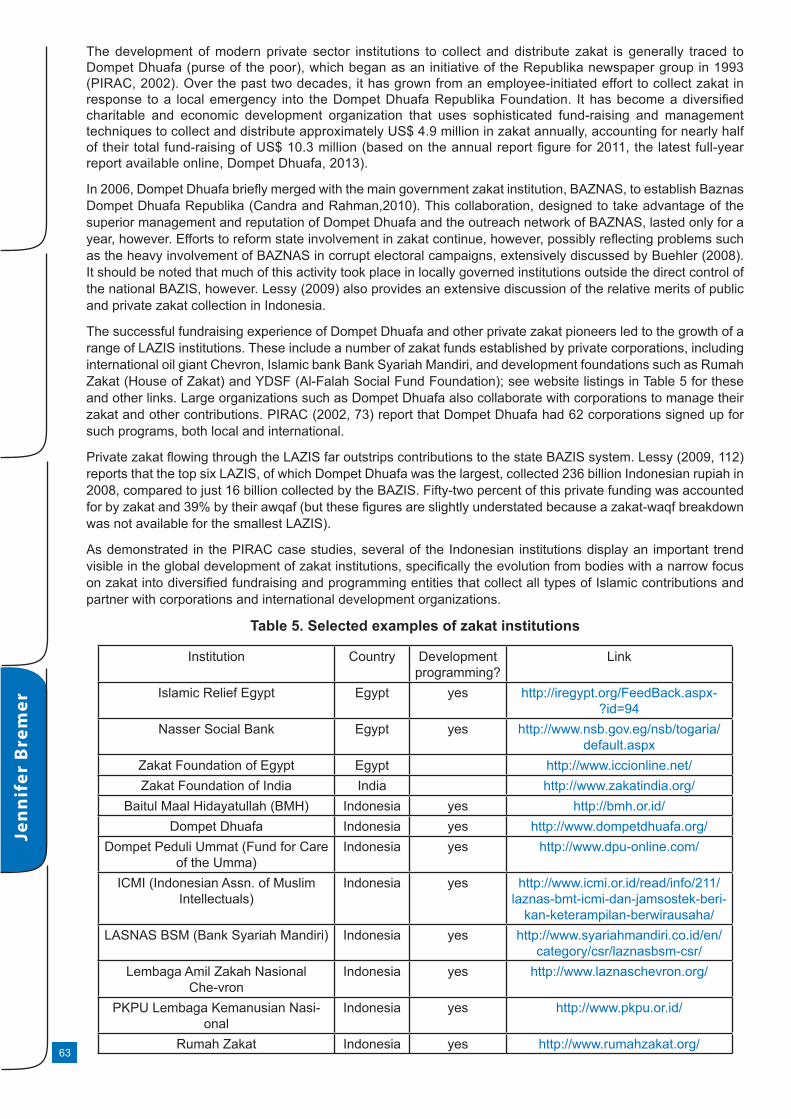

The development of modern private sector institutions to collect and distribute zakat is generally traced to Dompet Dhuafa (purse of the poor), which began as an initiative of the Republika newspaper group in 1993 (PIRAC, 2002). Over the past two decades, it has grown from an employee-initiated effort to collect zakat in response to a local emergency into the Dompet Dhuafa Republika Foundation. It has become a diversified charitable and economic development organization that uses sophisticated fund-raising and management techniques to collect and distribute approximately US$ 4.9 million in zakat annually, accounting for nearly half of their total fund-raising of US$ 10.3 million (based on the annual report figure for 2011, the latest full-year report available online, Dompet Dhuafa, 2013).

In 2006, Dompet Dhuafa briefly merged with the main government zakat institution, BAZNAS, to establish Baznas Dompet Dhuafa Republika (Candra and Rahman,2010). This collaboration, designed to take advantage of the superior management and reputation of Dompet Dhuafa and the outreach network of BAZNAS, lasted only for a year, however. Efforts to reform state involvement in zakat continue, however, possibly reflecting problems such as the heavy involvement of BAZNAS in corrupt electoral campaigns, extensively discussed by Buehler (2008). It should be noted that much of this activity took place in locally governed institutions outside the direct control of the national BAZIS, however. Lessy (2009) also provides an extensive discussion of the relative merits of public and private zakat collection in Indonesia.

The successful fundraising experience of Dompet Dhuafa and other private zakat pioneers led to the growth of a range of LAZIS institutions. These include a number of zakat funds established by private corporations, including international oil giant Chevron, Islamic bank Bank Syariah Mandiri, and development foundations such as Rumah Zakat (House of Zakat) and YDSF (Al-Falah Social Fund Foundation); see website listings in Table 5 for these and other links. Large organizations such as Dompet Dhuafa also collaborate with corporations to manage their zakat and other contributions. PIRAC (2002, 73) report that Dompet Dhuafa had 62 corporations signed up for such programs, both local and international.

Private zakat flowing through the LAZIS far outstrips contributions to the state BAZIS system. Lessy (2009, 112) reports that the top six LAZIS, of which Dompet Dhuafa was the largest, collected 236 billion Indonesian rupiah in 2008, compared to just 16 billion collected by the BAZIS. Fifty-two percent of this private funding was accounted for by zakat and 39% by their awqaf (but these figures are slightly understated because a zakat-waqf breakdown was not available for the smallest LAZIS).

As demonstrated in the PIRAC case studies, several of the Indonesian institutions display an important trend visible in the global development of zakat institutions, specifically the evolution from bodies with a narrow focus on zakat into diversified fundraising and programming entities that collect all types of Islamic contributions and partner with corporations and international development organizations.

Table 5. Selected examples of zakat institutions

Institution Country Development programming?

Link

Islamic Relief Egypt Egypt yes http://iregypt.org/FeedBack.aspx-?id=94

Nasser Social Bank Egypt yes http://www.nsb.gov.eg/nsb/togaria/default.aspx

Zakat Foundation of Egypt Egypt http://www.iccionline.net/Zakat Foundation of India India http://www.zakatindia.org/

Baitul Maal Hidayatullah (BMH) Indonesia yes http://bmh.or.id/Dompet Dhuafa Indonesia yes http://www.dompetdhuafa.org/

Dompet Peduli Ummat (Fund for Care of the Umma)

Indonesia yes http://www.dpu-online.com/

ICMI (Indonesian Assn. of Muslim Intellectuals)

Indonesia yes http://www.icmi.or.id/read/info/211/laznas-bmt-icmi-dan-jamsostek-beri-

kan-keterampilan-berwirausaha/LASNAS BSM (Bank Syariah Mandiri) Indonesia yes http://www.syariahmandiri.co.id/en/

category/csr/laznasbsm-csr/Lembaga Amil Zakah Nasional

Che-vronIndonesia yes http://www.laznaschevron.org/

PKPU Lembaga Kemanusian Nasi-onal

Indonesia yes http://www.pkpu.or.id/

Rumah Zakat Indonesia yes http://www.rumahzakat.org/

Jen

nif

er B

rem

er

63

64

YDSF (Al-Falah Social Fund Foun-da-tion)

Indonesia yes http://www.ydsf.org/

Crescent Medical Aid - Kenya Kenya http://www.crescent-medi-cal-aid-kenya.org/ourmission.htm

Zakat House of Kuwait - Egypt office Kuwait http://www.zakathouse.org.kw/Ax-CMSwebLive/ar_index_new.cms

Zakat Fund - Lebanon Lebanon yes http://www.zakat.org.lbTabung Amanah Zakat MMU Malaysia http://zakat.yum.org.my/

Qatar Charity Qatar yes http://www.qcharity.ogZakat Fund of the UAE UAE http://zakatfund.gov.ae/ZFP//web/

Page_disbursementzakat.aspxHuman Relief Foundation UK http://www.hrf.org.uk/dona-

tions-page/Islamic Relief Worldwide UK yes http://islamic-relief.com/Default.

aspx?depID=1Muslim Aid UK yes http://www.muslimaid.org/index.php/

National Zakat Foundation UK http://www.nzf.org.uk/Helping Hands for Relief and Devel-

opmentUS/

Canadahttp://www.hhrd.org/

Hidaya US/Can-ada

http://www.hidaya.org/

Islamic Circle of North America US/Canada

https://icnarelief.org/Apps/Donation/Donation.php?a=relief&b=&c=Zakat

Islamic Relief USA US/Canada

yes http://www.irusa.org/campaigns/zakah/

Islamic-American Zakat Foundation US/Canada

http://www.iazf.org/

Life for Relief and Development US/Canada

http://www.lifeusa.org/site/Page-Server

Muslim Welfare Center US/Canada

http://www.muslimwelfarecentre.com

Zakat Foundation of America US/Canada

yes http://www.zakat.org/what-we-do/development-sadaqa-jariyah/

More recently, leading Indonesian organizations have begun to establish awqaf, Islamic endowments. Candra and Rahman (2010) provide a case study of Dompet Dhuafa’s experience with its waqf, which is managed more like an investment fund than a traditional land-based waqf. In 2004, the government adopted Law 41, the awqaf law, to structure and provide oversight to the waqf movement. Dompet Dhuafa was formally recognized as a waqf shortly after its founding in 1994, however.

Many of the Indonesian programs place a strong emphasis on economic development, supporting small businesses and providing training for job-seekers, for example, even though the activities may be categorized into the traditional eight categories. Lessy (2009, 106) notes that “private LAZ institutions, such as Dompet Dhuafa, Pos Keadilan Peduli Umat, and RZI, are structured using modern zakat management techniques that enable them not only to fulfill the immediate needs of society, but also to launch long-term programs to empower the poor.”

A number of recent publications by Islamic scholars call for the broader use of such hybrid zakat institutions, combining zakat, infaq, sadaqa, and waqf (or ZISWAF, as it is termed in Indonesia). Atia (2009) discusses zakat used in combination with sadaqa and Islamic loans (qard hassan). El Daly’s dissertation and path-breaking study of Islamic philanthropy in Egypt (2003) explore the revival of the waqf, among other strategies. M. Hassan (2010) proposes a model to fund micro-finance using a combination of zakat and waqf. Yumna and Clark propose a similar model based on the case of Indonesia

It may be hoped that these new organizational structures will serve as models for zakat institutions in the Arab world. The experience in Tafahna al-Ashraf demonstrates the potential to transform a community through the systematic generation of zakat and its application to wealth-building programming rather than solely or even primarily to subsidize consumption. Considering these points in further detail is the aim of the next section.

Jenn

ifer Brem

er

Zakat as a tool of Islamic economic development Zakat is the pillar of the faith most closely tied to Islamic economics, to Islamic public finance (to the extent that such a field can be said to exist), and to the Islamic state itself. Zakat is considered to be the principle Islamic tax and the foundation of Islamic public finance. Ausaf Ahmed (1996, 74-75) quotes Mohamed Ariff as follows:

It has been accepted the system of zakat occupy a pivotal place in the fiscal theory and policy of the Islamic economy. The rightful and correct place of zakat system is in the realm of government finance. The system of public expenditure and taxation in an Islamic society will have to be designed and adjusted to take account of a zakat system in operation. That is why, zakat occupies a pivotal place in the theory of fiscal policy in Islamic economy.

In examining the economic impact of zakat, it may be useful to consider each of the linkages that connect zakat to its impact. In order for zakat to play its intended role in redistributing wealth from rich to poor, each of three functions must be performed reasonably well: 1) sufficient funds must be collected to meet the needs of at least the first two categories, the poor and the destitute, 2) the distribution of the funds must reach the appropriate beneficiaries, and 3) the impact of the funds received on the beneficiaries must actually be effective in raising their standard of living. El Daly (2010, 37) points to the distinction in this regard between the level needed for survival (hadd al-kefaya) and the higher level of sufficiency for a decent standard of living (hadd al-kafaf).

The first issue has attracted a great deal of attention in the vastly deep zakat literature, but most of it considers how the donor should calculate his or her zakat obligations, rather than how much zakat would in principle be needed to raise all of a society’s members to the level of kafaf or even kefaya. Thus one can find extensive discussions going into excruciating detail on the rules for zakat, the amount due under different conditions, how to calculate one’s obligation, how to interpret for the modern world rules developed at a time when financial institutions and instruments were much less complex than they are now, and so forth.

Less attention is devoted to the second issue, ensuring that the funds are distributed to those who are qualified to receive them, although this has become more complex in the modern era as well. In a traditional society, where communities were small and there were daily contacts between rich and poor, it was much easier to identify recipients who met the first two categories in particular, compared to the situation in modern societies, where the rich and poor live in increasingly segregated communities with declining personal interaction across income classes. This difficulty may in part explain the growth of formal institutions, both private and governmental, that take responsibility for collecting zakat from the donor and channeling it to appropriate recipients, a topic that will be discussed in some detail later in this paper.

The third requirement, that the funds be distributed in a way that actually benefits the recipients, receives even less attention. Abdullah (1991, 53) cites the traditional maxim that zakat should be managed so as to transform the zakat receiver (mustihaq) into a zakat donor (muzakki), but how this is to be achieved, arguably the crux of the matter, remains under-studied.

It is not only the amount of funding that determines whether the recipient’s standard of living is raised, but also how the funds are used. In particular, if zakat receipts are used primarily for short-term consumption, then they cannot make a contribution to a sustained improvement in the economic status of the recipient. We will return to this issue in more detail in the third section, which explores innovation in programming to use zakat proceeds for income generation. In the remainder of this section, we will explore a somewhat different issue, which is the broader impact of zakat on the productivity and growth of the economy as a whole.

At its most basic level, zakat takes a portion of the wealth flowing by economic activity and transfers it from the person who generated it to another person who is in greater need. What is the impact of this activity on capital accumulation over time? This is an important question because future growth depends on investment and investment depends on the availability of the surplus to be invested (as well as a long list of other factors, of course). This issue does not appear to be addressed in the zakat literature, at least not in any systematic way. The following two subsections first discuss the powerful dynamic of repeated zakat payment over time and provide a concrete example from an inspiring example of this strategy used to transform a poor village in Egypt.

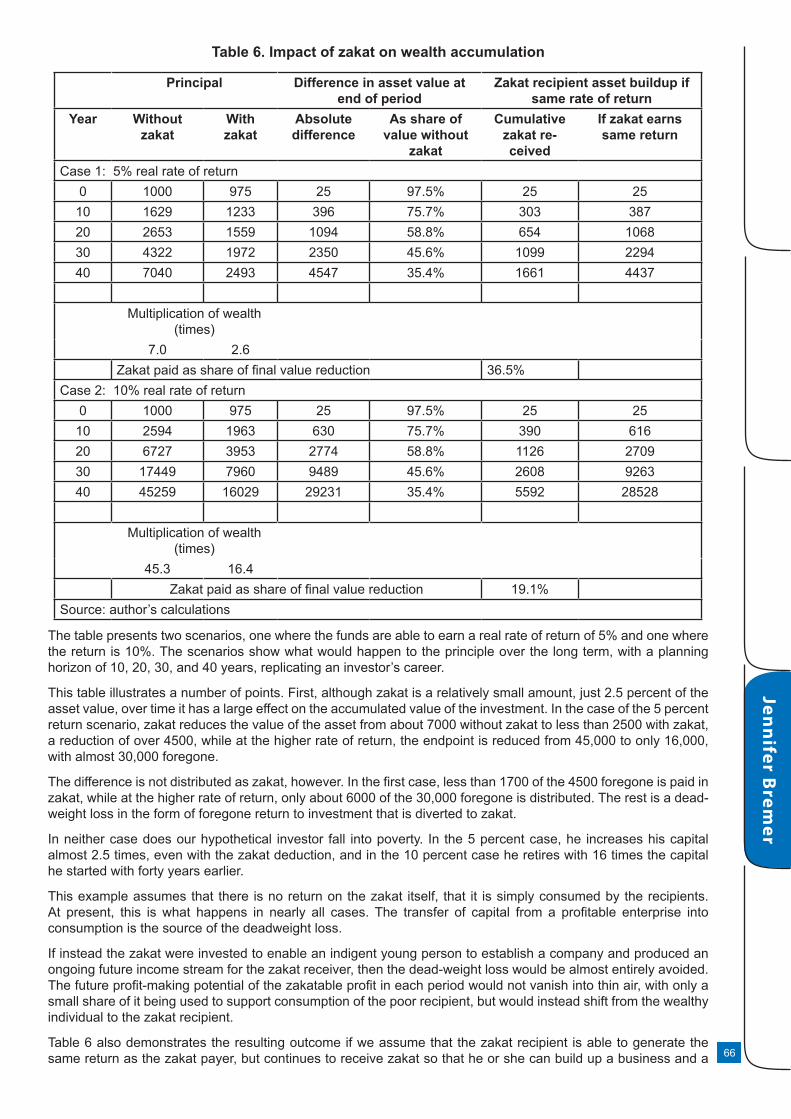

Z4D program dynamism: the power of compounding without interestTable 6 presents a highly simplified example of how payment of zakat on an initial balance of 1000 monetary units would affect the growth of the balance over time, under two scenarios. Each scenario assumes that the 1000 units are subject to a zakat of 2.5 percent (are “zakatable,” in the usual terminology) and fall above the minimum level that triggers a zakat obligation (the nisab). The calculation assumes that the full investable surplus is subject to zakat, which would generally be the case for commercial enterprises (other categories may involve a higher or lower rate of zakat). It does not allow for other deductions, such as income tax.

Jen

nif

er B

rem

er

65

66

Table 6. Impact of zakat on wealth accumulation

Principal Difference in asset value at end of period

Zakat recipient asset buildup if same rate of return

Year Without zakat

With zakat

Absolute difference

As share of value without

zakat

Cumulative zakat re-ceived

If zakat earns same return

Case 1: 5% real rate of return0 1000 975 25 97.5% 25 25

10 1629 1233 396 75.7% 303 38720 2653 1559 1094 58.8% 654 106830 4322 1972 2350 45.6% 1099 229440 7040 2493 4547 35.4% 1661 4437

Multiplication of wealth (times)

7.0 2.6Zakat paid as share of final value reduction 36.5%

Case 2: 10% real rate of return0 1000 975 25 97.5% 25 25

10 2594 1963 630 75.7% 390 61620 6727 3953 2774 58.8% 1126 270930 17449 7960 9489 45.6% 2608 926340 45259 16029 29231 35.4% 5592 28528

Multiplication of wealth (times)

45.3 16.4Zakat paid as share of final value reduction 19.1%

Source: author’s calculations

The table presents two scenarios, one where the funds are able to earn a real rate of return of 5% and one where the return is 10%. The scenarios show what would happen to the principle over the long term, with a planning horizon of 10, 20, 30, and 40 years, replicating an investor’s career.

This table illustrates a number of points. First, although zakat is a relatively small amount, just 2.5 percent of the asset value, over time it has a large effect on the accumulated value of the investment. In the case of the 5 percent return scenario, zakat reduces the value of the asset from about 7000 without zakat to less than 2500 with zakat, a reduction of over 4500, while at the higher rate of return, the endpoint is reduced from 45,000 to only 16,000, with almost 30,000 foregone.

The difference is not distributed as zakat, however. In the first case, less than 1700 of the 4500 foregone is paid in zakat, while at the higher rate of return, only about 6000 of the 30,000 foregone is distributed. The rest is a dead-weight loss in the form of foregone return to investment that is diverted to zakat.

In neither case does our hypothetical investor fall into poverty. In the 5 percent case, he increases his capital almost 2.5 times, even with the zakat deduction, and in the 10 percent case he retires with 16 times the capital he started with forty years earlier.

This example assumes that there is no return on the zakat itself, that it is simply consumed by the recipients. At present, this is what happens in nearly all cases. The transfer of capital from a profitable enterprise into consumption is the source of the deadweight loss.

If instead the zakat were invested to enable an indigent young person to establish a company and produced an ongoing future income stream for the zakat receiver, then the dead-weight loss would be almost entirely avoided. The future profit-making potential of the zakatable profit in each period would not vanish into thin air, with only a small share of it being used to support consumption of the poor recipient, but would instead shift from the wealthy individual to the zakat recipient.

Table 6 also demonstrates the resulting outcome if we assume that the zakat recipient is able to generate the same return as the zakat payer, but continues to receive zakat so that he or she can build up a business and a

Jenn

ifer Brem

er

capital from the business’s profits, while also benefiting from continuing zakat support. Under this scenario, the initial seed planted by the first zakat contribution of only 25 units grows very rapidly into a flourishing tree, boosted along by the annual infusions of additional capital.

If this scenario continued for the entire 40-year period used in the example, the very fortunate mustihaq would end up with a total capital accumulation at the end of the period much larger than the zakat payer! The zakat receiver accumulates his own nest-egg of 1000 units by year 20 at the 5% return and by year 13 at the 10% return, thus presumably accomplishing the goal of the system, which is to transform zakat recipients into zakat payers.

Of course, carrying on zakat contributions long after the recipient has ceased to be poor would not make sense to the zakat payer or to society as a whole. Before this point is reached, the donor would naturally redirect the funds to support another new enterprise, thus setting it on its way to growth, prosperity, and job creation.

In this manner, one donor would support the launch of several small businesses over his or her career, which in turn would create jobs and accumulate capital to the point where they, too, began to distribute zakat and support the growth of still more small businesses. Through this system, both the collection of zakat and its use could make a much more effective contribution to the realization of social equity and economic advancement.

The example given is strictly illustrative, of course. It assumes that the zakat donor would have the skill and time to be able to identify a poor person having a viable business opportunity that yields a market return and further assumes that the enterprise would in fact succeed. It assumes that all zakat is reinvested during the timeframe. These are quite strong assumptions, but is should also be recognized that, as with any venture capitalist, a few very successful ventures can make up for several unsuccessful ones and the 5 percent return posited in the low-return case provides a substantial margin for earnings to be withdrawn for the owner’s consumption.

In any case, the impact across the economic system as a whole of applying this approach consistently instead of supporting short-term consumption needs could have a very positive effect over time. Small companies engaged in low-capital enterprises such as trading can generate good returns and grow quickly, however, so it is not unrealistic to expect that they can earn a market return, at least in their early years.

A further consideration is that many people who would readily be categorized as poor (that is, lacking sufficient income to live a dignified life) are already engaged in small enterprises of one form or another. Undoubtedly some of them could transform these into successful and growing businesses, rather than merely subsistence activities, with the benefit of an infusion of zakat capital. The latter, it should be stressed differs from a normal investment or a loan in three key respects. First, there is no risk for the recipient: the funds do not have to be repaid as would a loan, interest-free or otherwise. Second, the capital itself is permanently transferred to the recipient and the giver retains no ownership interest in it or control over it. Subsequent support, however, would be dependent on how well the recipient uses the money, adding an incentive to stay on the straight and narrow. Third, in the model described, repeating payments are made regularly and predictably, over a period of several years, which increases their impact exponentially (quite literally).