Embed Size (px)

Citation preview

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 1/19

Part I: Building a Trading Strategy in Zignals

For this article I am working with the Zignals MarketPortal which gives full access to

all of our services (trading system, stock alerts, stock charts, stock screener,

watchlist and portfolio manager) in a single application. The key advantage to the

MarketPortal over stand-alone applications is the seamless switching between

applications and is recommended for users wishing to publish their own trading

strategies.

The first strategy will be built around a price cross above a 20-day Simple Moving

Average (SMA). This will be a long only strategy.

On loading the Trading System interface you will be greeted with a grid-interface;

along the top is a set of menu options and on the left is a series of steps, numbered

1 to 5, which are required to create a strategy.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 2/19

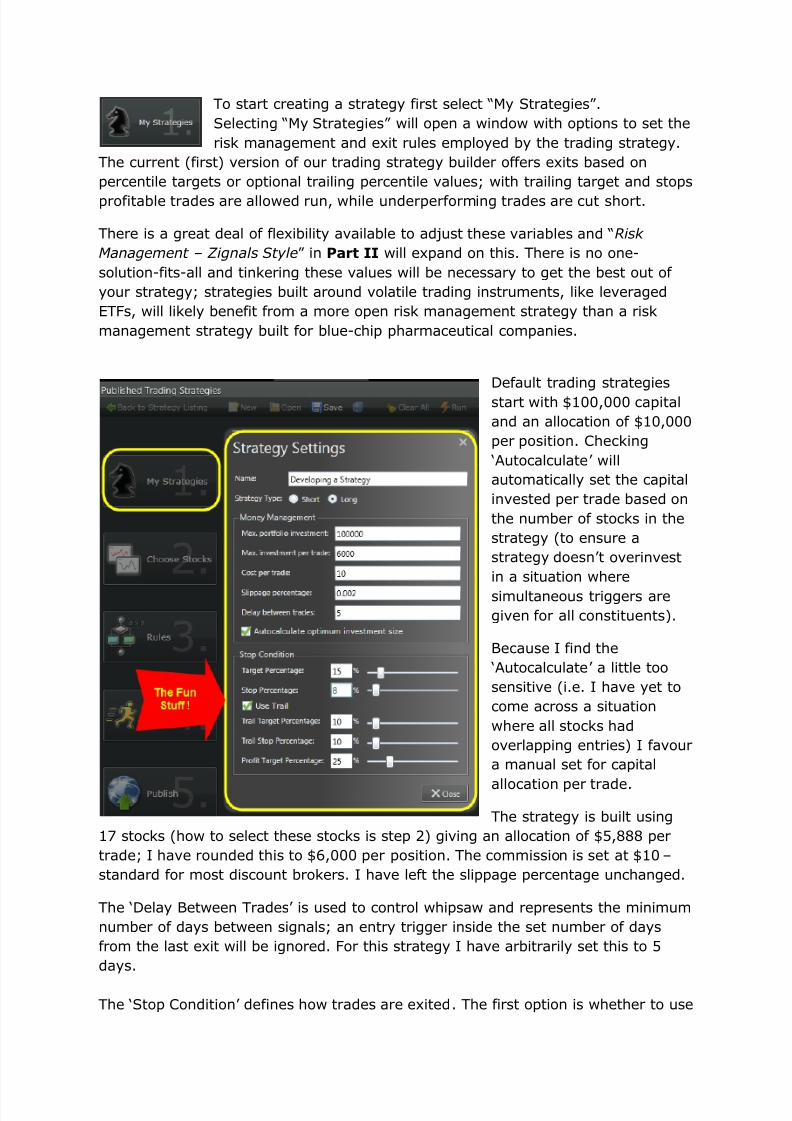

To start creating a strategy first select “My Strategies” .

Selecting “My Strategies” will open a window with options to set the

risk management and exit rules employed by the trading strategy.

The current (first) version of our trading strategy builder offers exits based on

percentile targets or optional trailing percentile values; with trailing target and stops

profitable trades are allowed run, while underperforming trades are cut short.

There is a great deal of flexibility available to adjust these variables and “Risk

Management – Zignals Style” in Part II will expand on this. There is no one-

solution-fits-all and tinkering these values will be necessary to get the best out of

your strategy; strategies built around volatile trading instruments, like leveraged

ETFs, will likely benefit from a more open risk management strategy than a risk

management strategy built for blue-chip pharmaceutical companies.

Default trading strategies

start with $100,000 capital

and an allocation of $10,000

per position. Checking

„Autocalculate‟ will

automatically set the capital

invested per trade based on

the number of stocks in the

strategy (to ensure a

strategy doesn‟t overinvest

in a situation where

simultaneous triggers are

given for all constituents).

Because I find the

„Autocalculate‟ a little too

sensitive (i.e. I have yet to

come across a situation

where all stocks had

overlapping entries) I favour

a manual set for capital

allocation per trade.

The strategy is built using

17 stocks (how to select these stocks is step 2) giving an allocation of $5,888 per

trade; I have rounded this to $6,000 per position. The commission is set at $10 –

standard for most discount brokers. I have left the slippage percentage unchanged.

The „Delay Between Trades‟ is used to control whipsaw and represents the minimum

number of days between signals; an entry trigger inside the set number of days

from the last exit will be ignored. For this strategy I have arbitrarily set this to 5

days.

The „Stop Condition‟ defines how trades are exited. The first option is whether to use

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 3/19

a trailing stop. If a trail is not used a position will be exited at either the target or

stop percentage from price at entry. E.g. A stock entered at $100 with a 15% target

and 8% stop will exit at $115 or $92.

To maximise the benefit of following a trend we will use a trailing exit (check the

„Use Trail‟ box). In this case the trail kicks in once the initial Target Percentage isreached, but a position will exit if prices reach the Stop Percentage before the trail

starts. Once the Target Percentage is hit the rolling target and stop defined by the

Trail Percentages is activated. Positions are exited at the Profit Target or the Trailing

Stop – whichever is hit first. E.g. In the case of 15% Target, 8% Stop, 10% Trail

Target and Stop with a 25% Profit Target, a stock entered at $100 will kick in the

trail at $115 or exit at $92. If the stock gets to $115 a new trailing target will be

$126.50 with a trailing a stop at $103.50. If the stock gets to $125 then the position

is sold (so the position is exited before the next trailing target is reached).

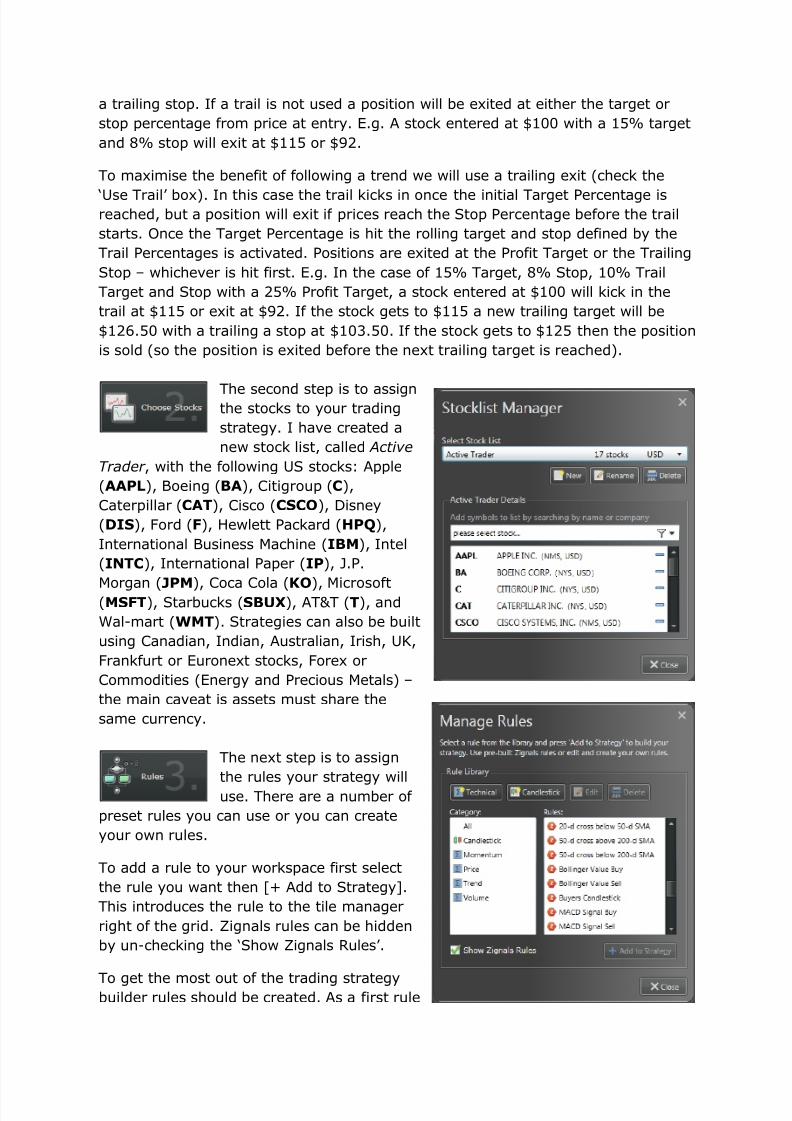

The second step is to assignthe stocks to your trading

strategy. I have created a

new stock list, called Active

Trader , with the following US stocks: Apple

(AAPL), Boeing (BA), Citigroup (C),

Caterpillar (CAT), Cisco (CSCO), Disney

(DIS), Ford (F), Hewlett Packard (HPQ),

International Business Machine (IBM), Intel

(INTC), International Paper (IP), J.P.

Morgan (JPM), Coca Cola (KO), Microsoft(MSFT), Starbucks (SBUX), AT&T (T), and

Wal-mart (WMT). Strategies can also be built

using Canadian, Indian, Australian, Irish, UK,

Frankfurt or Euronext stocks, Forex or

Commodities (Energy and Precious Metals) –

the main caveat is assets must share the

same currency.

The next step is to assign

the rules your strategy will

use. There are a number of

preset rules you can use or you can create

your own rules.

To add a rule to your workspace first select

the rule you want then [+ Add to Strategy].

This introduces the rule to the tile manager

right of the grid. Zignals rules can be hidden

by un-checking the „Show Zignals Rules‟.

To get the most out of the trading strategybuilder rules should be created. As a first rule

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 4/19

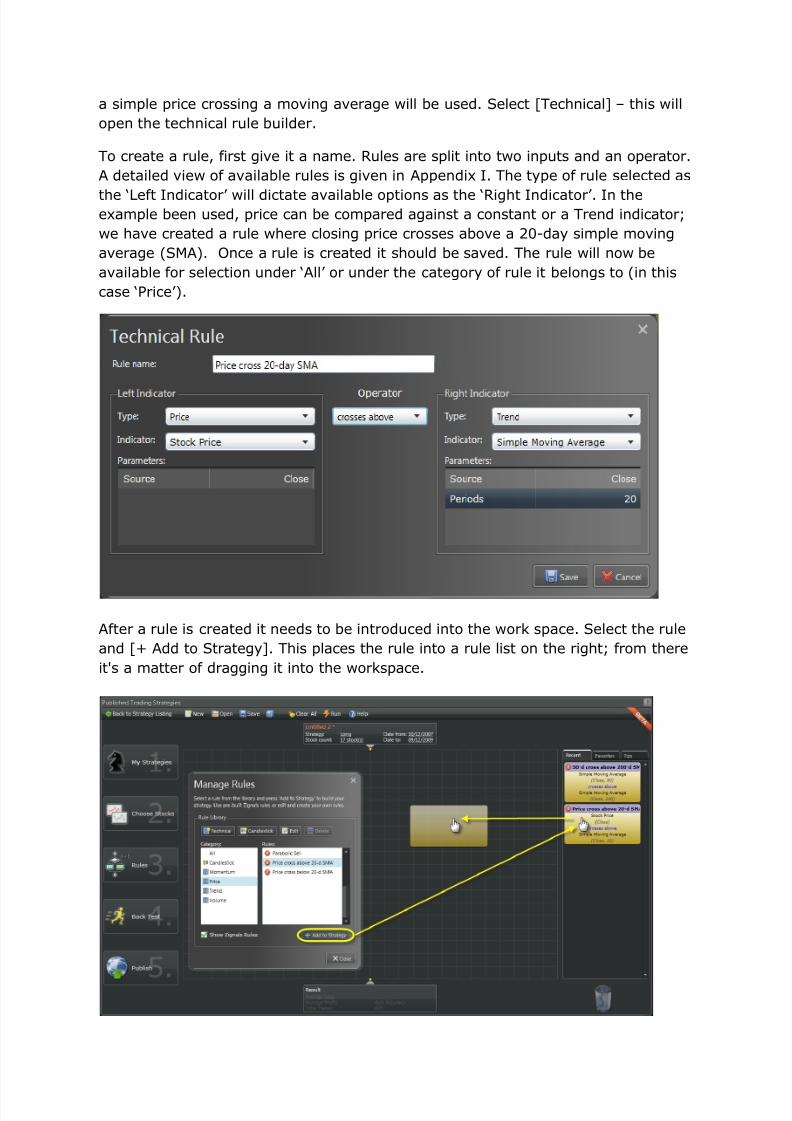

a simple price crossing a moving average will be used. Select [Technical] – this will

open the technical rule builder.

To create a rule, first give it a name. Rules are split into two inputs and an operator.

A detailed view of available rules is given in Appendix I. The type of rule selected as

the „Left Indicator‟ will dictate available options as the „Right Indicator‟. In theexample been used, price can be compared against a constant or a Trend indicator;

we have created a rule where closing price crosses above a 20-day simple moving

average (SMA). Once a rule is created it should be saved. The rule will now be

available for selection under „All‟ or under the category of rule it belongs to (in this

case „Price‟).

After a rule is created it needs to be introduced into the work space. Select the rule

and [+ Add to Strategy]. This places the rule into a rule list on the right; from there

it's a matter of dragging it into the workspace.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 5/19

The first rule dragged-in will automatically connect to the starting point. Other rules

you drag-in can either be connected to existing rules, or by dragging the top box

down to the new rule, connect to the dragged-in rule (see below).

Multiple rule paths are possible (see below); the key thing is to ensure rules are

connected from top to bottom. With multiple rule paths only one signal is supported

i.e. trades in a given stock are only entered once – there is no doubling, trebling etc.

of positions.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 6/19

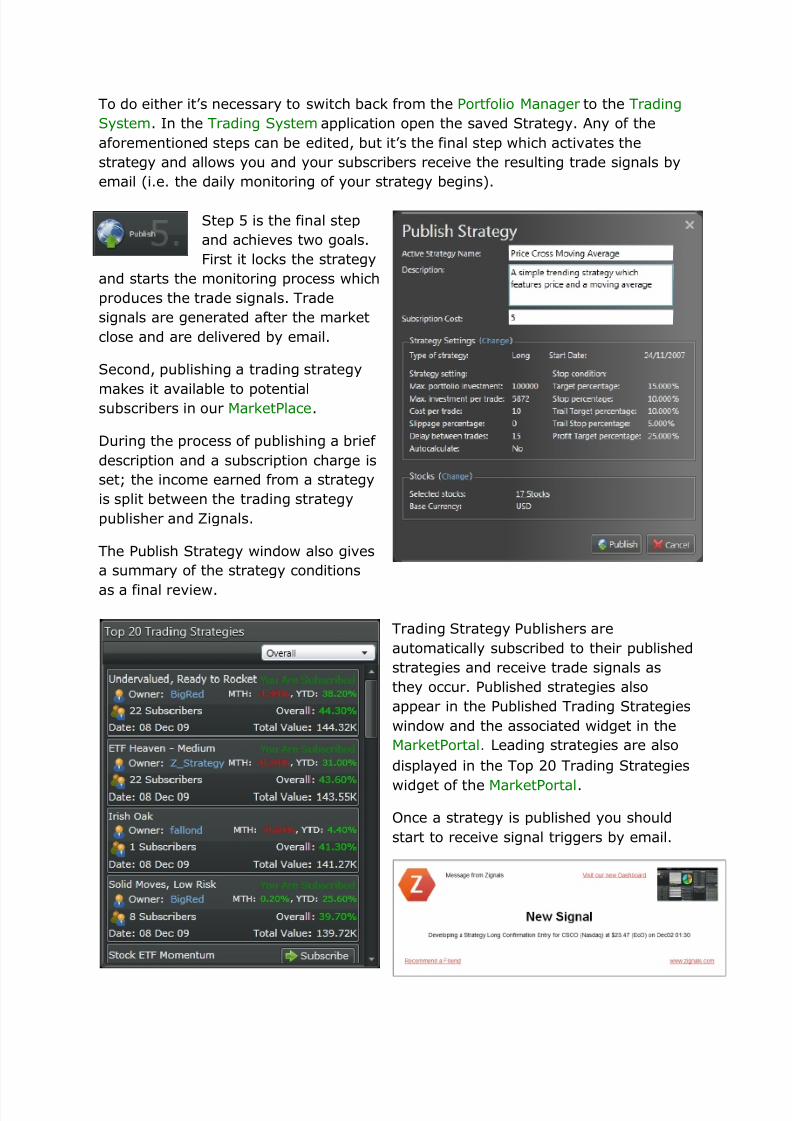

The final step is to connect the price-cross-SMA rule

to the end-point to complete the rule flow.

Once you are happy with your strategy it should

then be saved.

Step 4 defines the back-test period.

The default period is the past 2-

years from the previous day, but the

back-test period can be run for any period back to

2001 (for US stocks).

When a back test is run an historical portfolio is

created displaying all the trades over the test

period. The portfolio can be given a name (or the

default name will be used – usually „Untitled x ‟ ) and

will be listed in the drop-down menu of the Portfolio

Manager application. The option to view the

portfolio is offered at the end of the back test run.

After viewing a back-test portfolio two options are available:

[1] The strategy rules can be further edited, with updated portfolios produced OR

[2] The strategy can be Published so that the trading signals can be received

by email.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 7/19

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 8/19

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 9/19

Trailing Target is hit the Trailing Stop is updated. If at any point the Trailing Stop is

hit then the position is exited. The Trailing Target continues until the Profit Target is

hit. Once a Profit Target is hit the position is exited.

The strategy was based on a long entry following a price cross above a stock‟s 20-

day SMA.

For the back-test period the dates 24th Nov 2007 to 23rd Nov 2009 were used.

What were the returns based on default ‘Stop Condition’ settings?

Target Percentage: 15%

Stop Percentage: 10%

Trail Used: Yes

Trail Target Percentage: 10%

Trail Stop Percentage: 10%

Profit Target Percentage: 25%

No. of Trades: 142

Profitable Trades: 47%

Net Profit: 17%

What happened when ‘Stop Conditions’ were changed?

The adjustment to the initial „Stop Percentage‟ generated the following returns:

The relatively close-to-market Beta of our component stocks allowed for a relatively

strong return with a tight stop of 4%, even though there was a sharp drop in the

percentage of winning trades.

Taking the 6% stop as a fixed point and adjusting the „Target Percentage‟ (the price

at which the Trailing prices kicked in) brought an improvement in the percentage of

profitable trades. Dropping the Target price from 15% to 10% increased the

percentage of profitable trades to a morale boosting 57% with an additional kick on

the resulting percentage profit.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 10/19

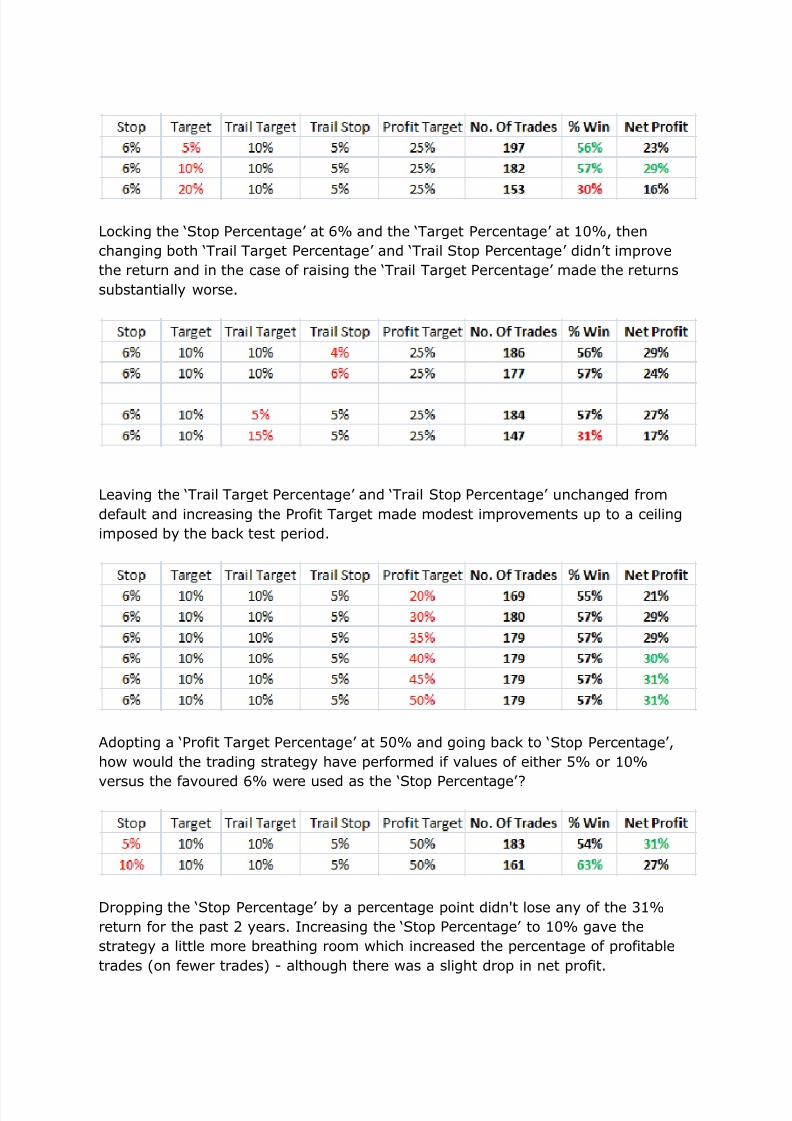

Locking the „Stop Percentage‟ at 6% and the „Target Percentage‟ at 10%, then

changing both „Trail Target Percentage‟ and „Trail Stop Percentage‟ didn‟t improve

the return and in the case of raising the „Trail Target Percentage‟ made the returns

substantially worse.

Leaving the „Trail Target Percentage‟ and „Trail Stop Percentage‟ unchanged from

default and increasing the Profit Target made modest improvements up to a ceiling

imposed by the back test period.

Adopting a „Profit Target Percentage‟ at 50% and going back to „Stop Percentage‟ ,

how would the trading strategy have performed if values of either 5% or 10%

versus the favoured 6% were used as the „Stop Percentage‟ ?

Dropping the „Stop Percentage‟ by a percentage point didn't lose any of the 31%

return for the past 2 years. Increasing the „Stop Percentage‟ to 10% gave the

strategy a little more breathing room which increased the percentage of profitable

trades (on fewer trades) - although there was a slight drop in net profit.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 11/19

For the purposes of building a new strategy the following settings are a good

starting point.

Stop Percentage: 10%

Target Percentage: 10%

Use Trail: Yes

Trail Target Percentage: 10%

Trail Stop Percentage: 5%

Profit Target Percentage: 25% (or 50%?)

For the simple one-rule strategy used on a core set of relatively price stable US

stocks, the largest impact on net profit and percentage of winning trades came from

adjustments in the initial „Target Percentage‟ and „Stop Percentage‟ values versus

changes in the values of „Trail Target Percentage‟ and „Trail Stop Percentage‟ .

However, trading strategies built around different assets and rule types will responddifferently to the risk management plan outlined here. For example, it‟s unlikely a

trading strategy built on x2 or x3 leveraged index ETFs will give as strong returns

with a 5% stop percentage as they might with a 10% stop percentage. Only by

testing different exit strategies is it possible to get the best out of your developed

trading strategies.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 12/19

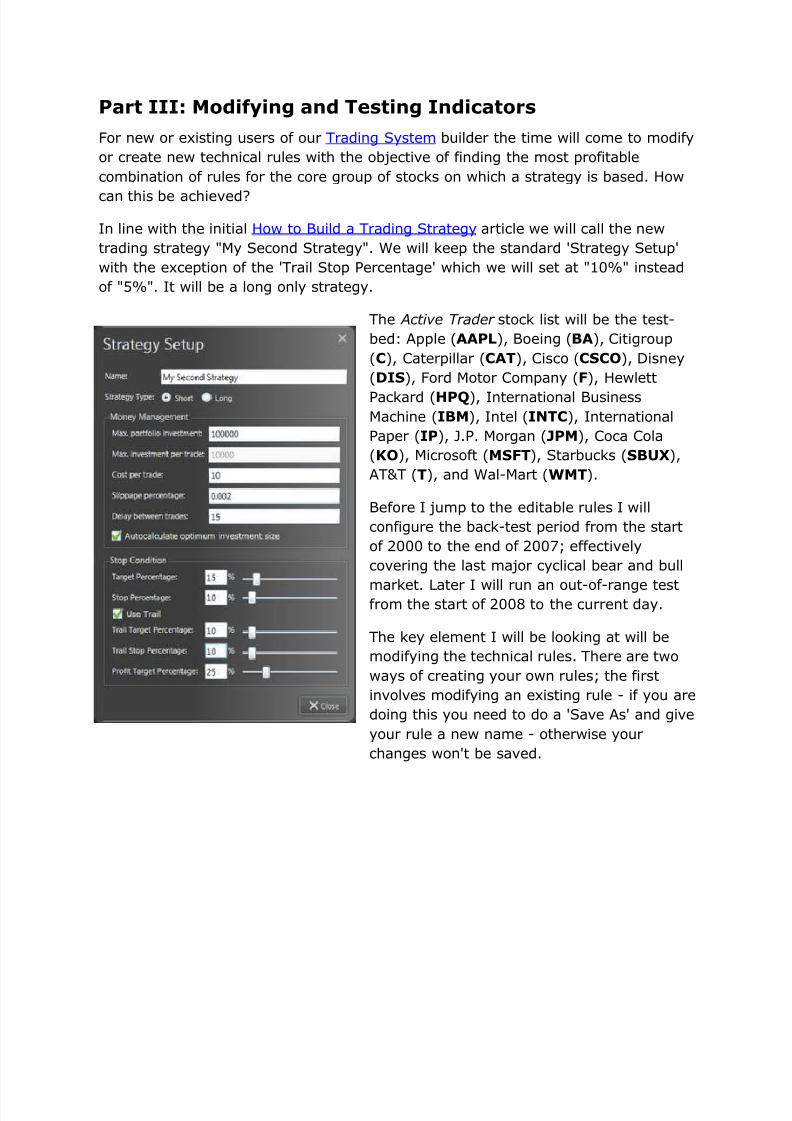

Part III: Modifying and Testing Indicators

For new or existing users of our Trading System builder the time will come to modify

or create new technical rules with the objective of finding the most profitable

combination of rules for the core group of stocks on which a strategy is based. How

can this be achieved?

In line with the initial How to Build a Trading Strategy article we will call the new

trading strategy "My Second Strategy". We will keep the standard 'Strategy Setup'

with the exception of the 'Trail Stop Percentage' which we will set at "10%" instead

of "5%". It will be a long only strategy.

The Active Trader stock list will be the test-

bed: Apple (AAPL), Boeing (BA), Citigroup

(C), Caterpillar (CAT), Cisco (CSCO), Disney

(DIS), Ford Motor Company (F), Hewlett

Packard (HPQ), International Business

Machine (IBM), Intel (INTC), International

Paper (IP), J.P. Morgan (JPM), Coca Cola

(KO), Microsoft (MSFT), Starbucks (SBUX),

AT&T (T), and Wal-Mart (WMT).

Before I jump to the editable rules I will

configure the back-test period from the start

of 2000 to the end of 2007; effectively

covering the last major cyclical bear and bull

market. Later I will run an out-of-range testfrom the start of 2008 to the current day.

The key element I will be looking at will be

modifying the technical rules. There are two

ways of creating your own rules; the first

involves modifying an existing rule - if you are

doing this you need to do a 'Save As' and give

your rule a new name - otherwise your

changes won't be saved.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 13/19

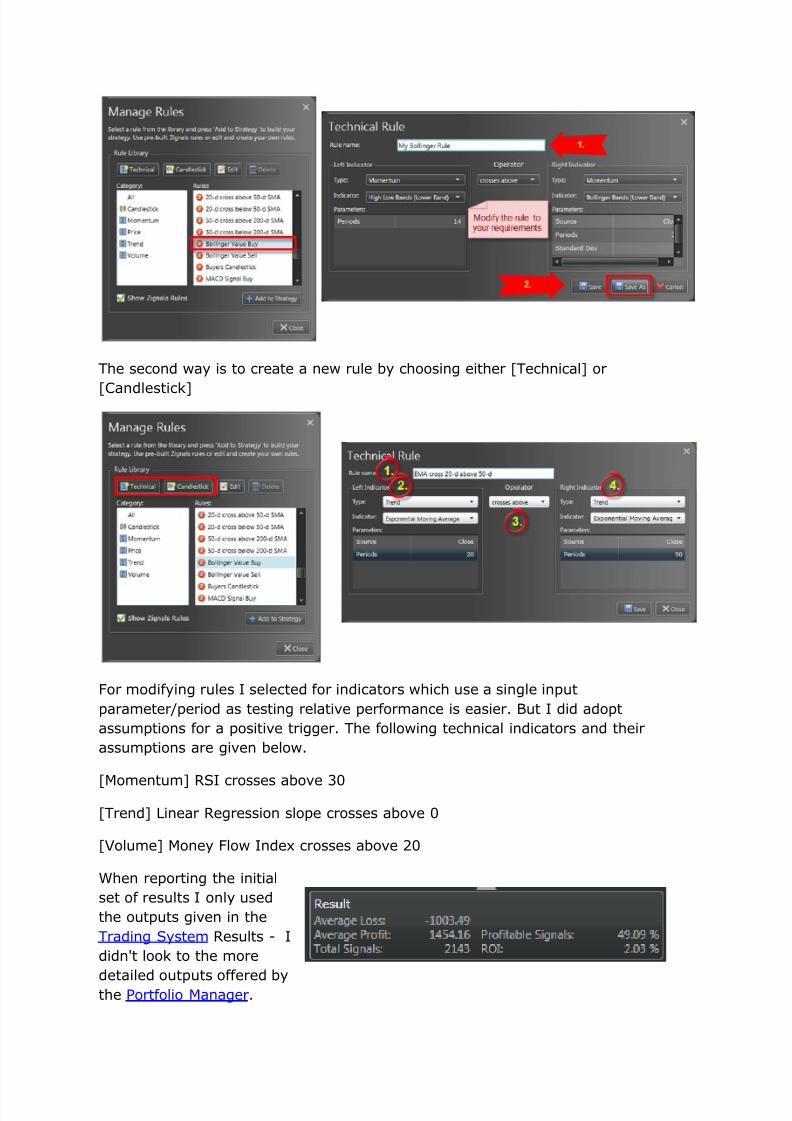

The second way is to create a new rule by choosing either [Technical] or

[Candlestick]

For modifying rules I selected for indicators which use a single input

parameter/period as testing relative performance is easier. But I did adopt

assumptions for a positive trigger. The following technical indicators and their

assumptions are given below.

[Momentum] RSI crosses above 30

[Trend] Linear Regression slope crosses above 0

[Volume] Money Flow Index crosses above 20

When reporting the initial

set of results I only used

the outputs given in the

Trading System Results - I

didn't look to the more

detailed outputs offered bythe Portfolio Manager.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 14/19

First Step

How did each indicator perform independently?

There were two strong performing indicators: RSI and Money Flow. In the case of

RSI the best returns came from using non-traditional period settings, although thetotal number of trades generated was low (which can skew the results). Similarly,

Money Flow also posted good returns using higher period settings. For both RSI and

Money Flow, period values of 20 days or more generated an average ROI of over 4%

per trade. The caveat is the use of trailing stops and defined targets - not the

traditional inverse 'sell' trigger for an exit - so this may in part explain the stronger

performance from the longer period range. When you consider the (non-)

performance of the S&P over the test period this is quite incredible.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 15/19

Second Step

We could probably stop here and just use either a long period RSI or Money Flow

indicator as our entry trigger. But is there a way to improve this return? Will a mix-

and-match offer a better return?

The first match was to use RSI [5] with Linear Regression Slope [5] and Money Flow

Index [5]. For each combination type there were a large number of signals,

increasing the probability for a good subset of results. For a trigger to be true, all

signals must occur on the close of business on the same day.

Pairing of the aforementioned indicators brought improved performance over

individual indicators. Better still, using all three in tandem brought the strongest

performance with a healthy 156 trades (approximately 22 a year) with an average

return of 5% per trade and nearly 60% winning trades. Of the paired indicators, a

combination of momentum (RSI) and trend (Linear Regression Slope) brought the

best returns at an ROI of just over 4% per trade with 56% winners.

A unique feature of the

Zignals Trading System

Builder is the ability to create

multiple trigger paths for a

trade. So while the

aforementioned examples

were created with simple

linear paths we can modify

them to allow for OR

scenarios.

A selection of OR

combinations did not improve

the ROI of the strategy and

was considerably worse than

the linear flow of all three

rules together. The additional

rule path also lowered the

ROI of the paired rule set.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 16/19

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 17/19

The last comparison paired Linear Regression (Slope) with Money Flow. As with the

earlier pairing of Linear Regression (Slope) with RSI, the number of generated

trades was low. Linear Regression (Slope) [5] matched with Money Flow [5] or [10]

had the most trades with a 3.40% and 2.42% ROI respectively - the worst return forany of the pairings.

Fourth Step

The final step extends the second step by looking at alternative period settings

for the three indicators together. But outside the initial set of RSI [5], Linear

Regression Slope [5] and Money Flow [5] there were very few trades.

Out-of-test

The final phase ran the two best set-ups from the start of 2008 to the current day.

The three-indicator set up - RSI [5], Linear Regression (Slope) [5], Money Flow [5] -

generated 37 trades with 65% winners and an ROI of 6.92%. RSI

[20] didn't perform as strongly with 58 trades on 52% winners and 2.26% ROI.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 18/19

Global Trading Strategies

Based on the aforementioned results I have published the following strategies

available in Trading Strategy MarketPlace:

Tri-Indicator US, Tri-Indicator UK, Tri-Indicator India, Tri-Indicator Aussie, Tri-Indicator Frankfurt, Tri-Indicator Forex, Tri-Indicator ETF, Tri-Indicator Irish, Tri-

Indicator Canada, and Tri-Indicator US Dividends.

Relative US, Relative UK, Relative India, Relative Aussie, Relative Frankfurt, Relative

Forex, Relative ETF, Relative Irish, Relative Canada, and Relative US Dividends

How did the strategy perform across market types? This time there was a clear

winner:

RSI [20] had an average ROI range of -2.86% to 4.04% with a Standard Deviation

of 2.66%.

RSI [5] + Money Flow [5] + Linear Regression (Slop) [5] had an average ROI of

4.03% with a range of 0.68% to 7.60% on a Standard Deviation of 2.45%

Summary

Single even triggers can offer strong returns but sacrifice consistency. Multiple

trigger events per trade can improve performance stability across market

conditions and market types, even if net return per trade can sometimes be lower.

8/8/2019 Zignals: Building a Trading Strategy

http://slidepdf.com/reader/full/zignals-building-a-trading-strategy 19/19

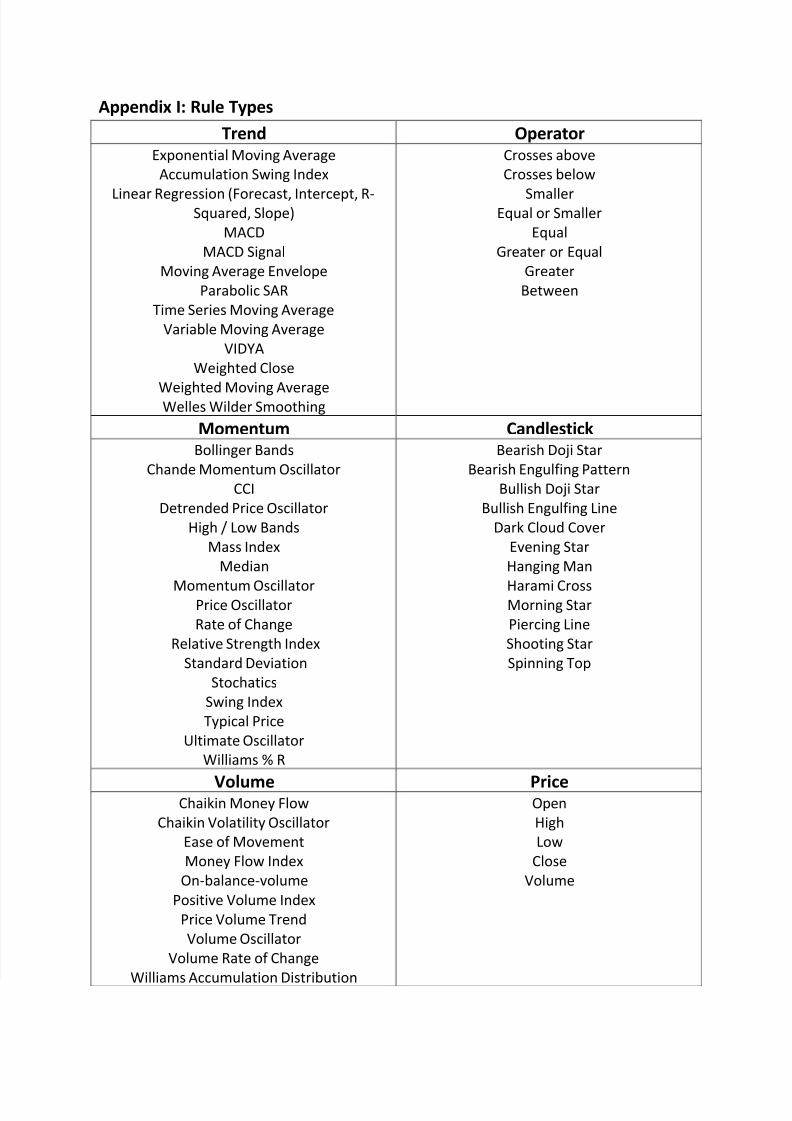

Appendix I: Rule Types

Trend Operator

Exponential Moving Average

Accumulation Swing Index

Linear Regression (Forecast, Intercept, R-Squared, Slope)

MACD

MACD Signal

Moving Average Envelope

Parabolic SAR

Time Series Moving Average

Variable Moving Average

VIDYA

Weighted Close

Weighted Moving AverageWelles Wilder Smoothing

Crosses above

Crosses below

SmallerEqual or Smaller

Equal

Greater or Equal

Greater

Between

Momentum Candlestick

Bollinger Bands

Chande Momentum Oscillator

CCI

Detrended Price Oscillator

High / Low Bands

Mass Index

Median

Momentum OscillatorPrice Oscillator

Rate of Change

Relative Strength Index

Standard Deviation

Stochatics

Swing Index

Typical Price

Ultimate Oscillator

Williams % R

Bearish Doji Star

Bearish Engulfing Pattern

Bullish Doji Star

Bullish Engulfing Line

Dark Cloud Cover

Evening Star

Hanging Man

Harami CrossMorning Star

Piercing Line

Shooting Star

Spinning Top

Volume PriceChaikin Money Flow

Chaikin Volatility Oscillator

Ease of Movement

Money Flow Index

On-balance-volume

Positive Volume Index

Price Volume Trend

Volume Oscillator

Volume Rate of Change

Williams Accumulation Distribution

Open

High

Low

Close

Volume