Embed Size (px)

Citation preview

THEISLAMICFINANCIALSERVICESACT2013

Zulkifli Hasan (Ph.D) Faculty of Syariah and Law

University Sains Islam Malaysia

1

Contents

• Introduction • About the IFSA • Significant Features of

the IFSA

• Implications, Issues and Challenges

• Conclusion

2

• Considerablegrowthwith16full-fledgedIB,12TakafuloperatorsandsixDFI.

• Significantprogresswithmarketshareincreasedupto25%in2014(40%in2020)ofthetotalbankingsystem.

• TotalIslamicfinancingconMnuedtogrow16.6%andrepresented26.9%oftotalloans/financinginthebankingsystem.

• 799Shari’ah-compliantsecuriMeswerelistedonBursaMalaysia,represenMng87.7%ofthetotallistedsecuriMes,withamarketcapitalizaMonofRM995.7billionor63.7%ofthetotalmarketcapitalizaMon.

3

An Overview of IF in Malaysia

• Theexis,ngframeworkofIslamicfinanceinvariousjurisdic,onsdemonstratesdiverseprac,cesanddis,nctmodels.Malaysiaastheproponentofregulatory-basedapproachhasins,tutedseveralini,a,vestopromotefinancialstabilityandthisincludethenewlaw,theIslamicFinancialServicesAct2013.

• FeaturesofthisAct/Newdimensions/Legalconsequencesintheaspectsofdemarca,onbetweenIslamicbankinganditsconven,onalcounterpart,elementofconsumerism,interestofdepositorsandIAH,corporategovernance,Shari’ahcompliance,liabili,es,judicialoversightandproductsandservices

4

Introduction

ABOUT THE IFSA

5

• TheIslamicBankingAct1983,theTakafulAct1984,theBAFIA1989andtheSecuriMesCommissionAct1993.

• TheCentralBankofMalaysiaAct2009• MalaysianFinancialSectorBlueprint2011-2020:tostrengthentherelevantregulatoryandlegalframework.

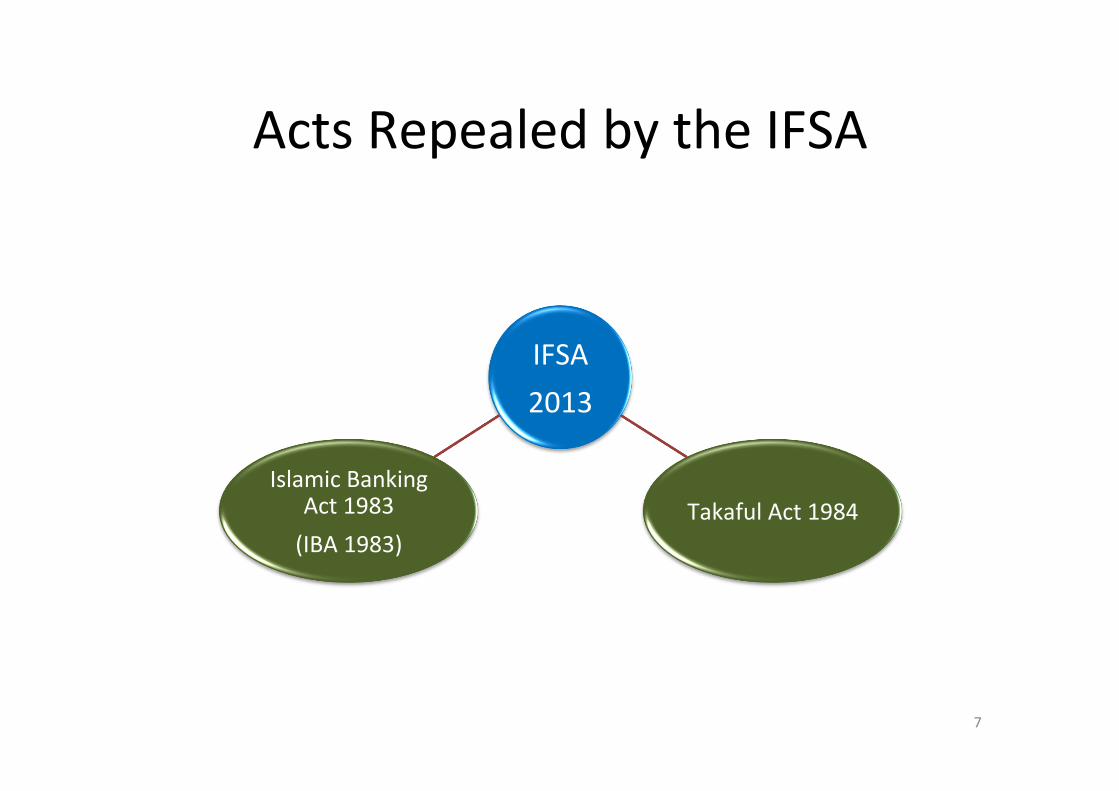

• TheIFSA:ConsolidatestheIBAandtheTAandrepealsbothActs.RoyalAssenton18March2013,gazeYedon22March2013andcameintoeffectinJune2013.

• GuidelinesforIFIs:Eg.GuidelinesontheDisclosureofReportsandFinancialStatementsofIslamicBanksandtheShari’ahGovernanceFramework.

6

Background

ActsRepealedbytheIFSA

7

IFSA2013

TakafulAct1984IslamicBanking

Act1983(IBA1983)

• “TheregulatoryandsupervisoryframeworkforthefinancialsectorwasstrengthenedwiththecomingintoforceoftheFSAandIFSAon30June2013.ThisensuresthatlawsgoverningtheconductandsupervisionoffinancialinsMtuMonsinMalaysiaconMnuetoberelevantandeffecMveinmaintainingfinancialstability,supporMngasustainable,balancedandinclusivegrowthoftheeconomy,aswellasprovidingadequateprotecMonforconsumers.ThelawsfurtherstrengthenBNM’ssupervisoryandregulatorypowers,includingcomprehensivepowerstocarryoutconsolidatedsupervisionoffinancialgroupsandtoextendtheregulatoryperimetertosystemicallyimportantnon-bankenMMesthatundertakefinancialintermediaMonacMviMes”.

8

IMF Country Report No 14/80

Summary of the IFSA

9

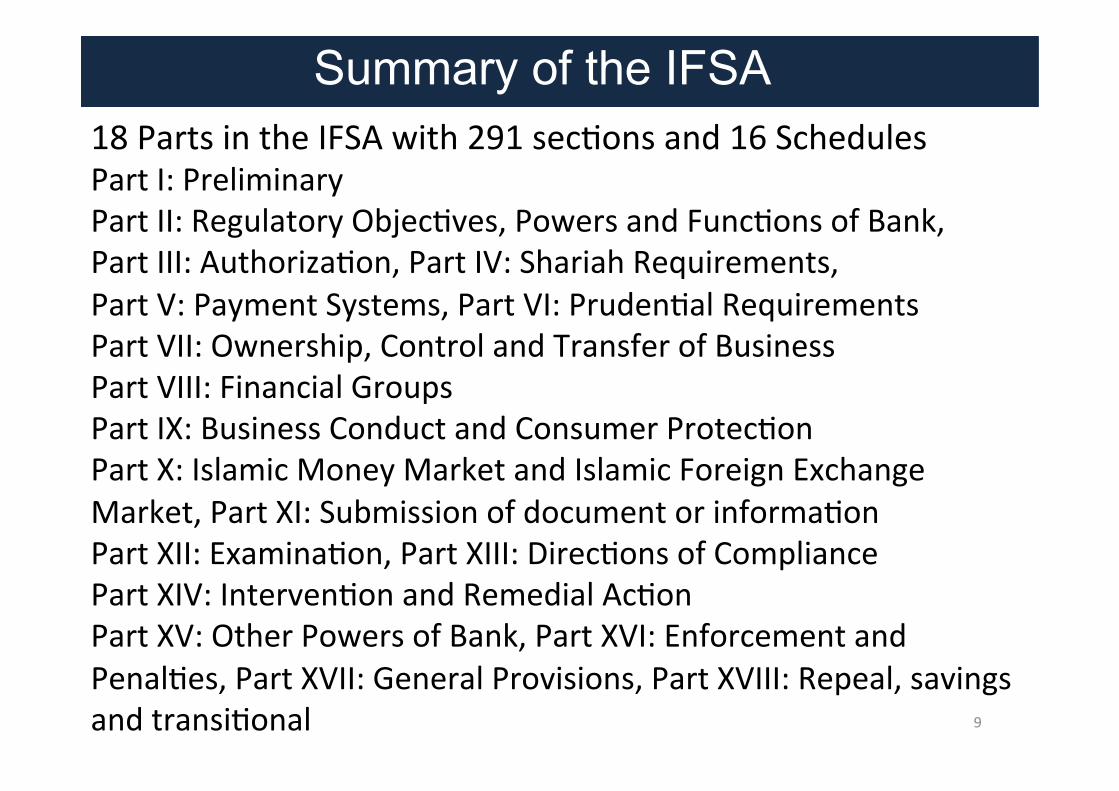

18PartsintheIFSAwith291secMonsand16SchedulesPartI:PreliminaryPartII:RegulatoryObjecMves,PowersandFuncMonsofBank,PartIII:AuthorizaMon,PartIV:ShariahRequirements,PartV:PaymentSystems,PartVI:PrudenMalRequirementsPartVII:Ownership,ControlandTransferofBusinessPartVIII:FinancialGroupsPartIX:BusinessConductandConsumerProtecMonPartX:IslamicMoneyMarketandIslamicForeignExchangeMarket,PartXI:SubmissionofdocumentorinformaMonPartXII:ExaminaMon,PartXIII:DirecMonsofCompliancePartXIV:IntervenMonandRemedialAcMonPartXV:OtherPowersofBank,PartXVI:EnforcementandPenalMes,PartXVII:GeneralProvisions,PartXVIII:Repeal,savingsandtransiMonal

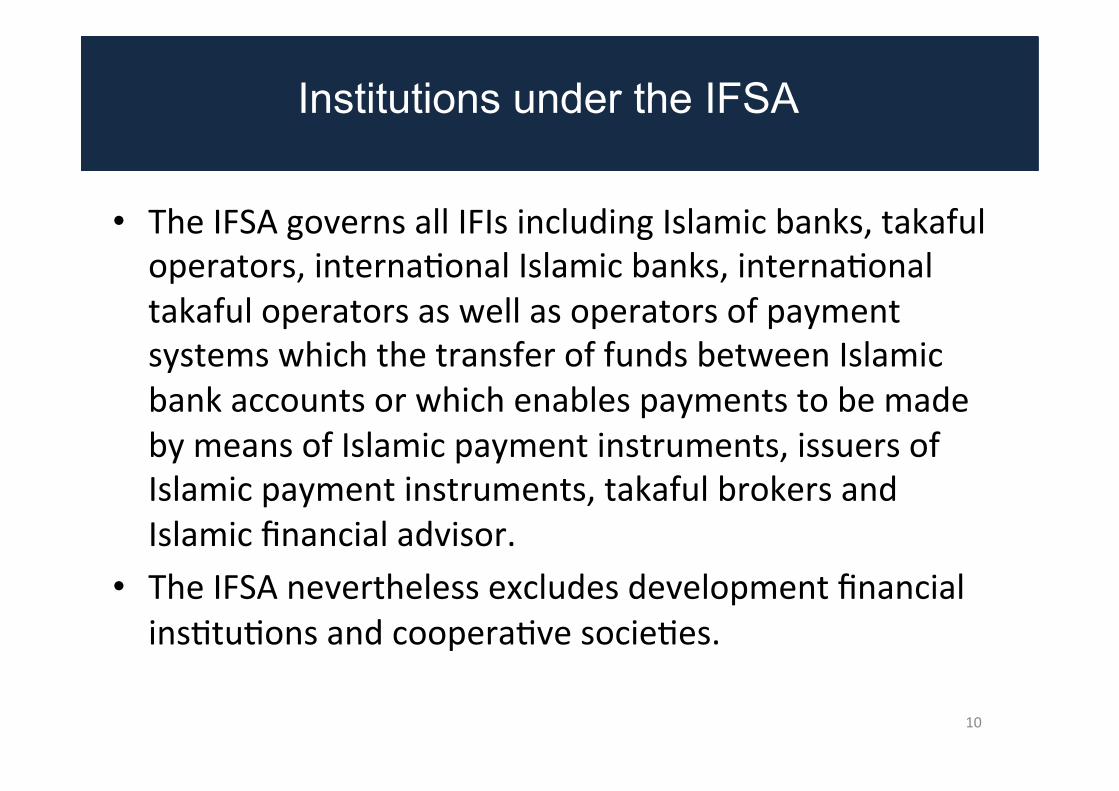

• TheIFSAgovernsallIFIsincludingIslamicbanks,takafuloperators,internaMonalIslamicbanks,internaMonaltakafuloperatorsaswellasoperatorsofpaymentsystemswhichthetransferoffundsbetweenIslamicbankaccountsorwhichenablespaymentstobemadebymeansofIslamicpaymentinstruments,issuersofIslamicpaymentinstruments,takafulbrokersandIslamicfinancialadvisor.

• TheIFSAneverthelessexcludesdevelopmentfinancialinsMtuMonsandcooperaMvesocieMes.

10

Institutions under the IFSA

11

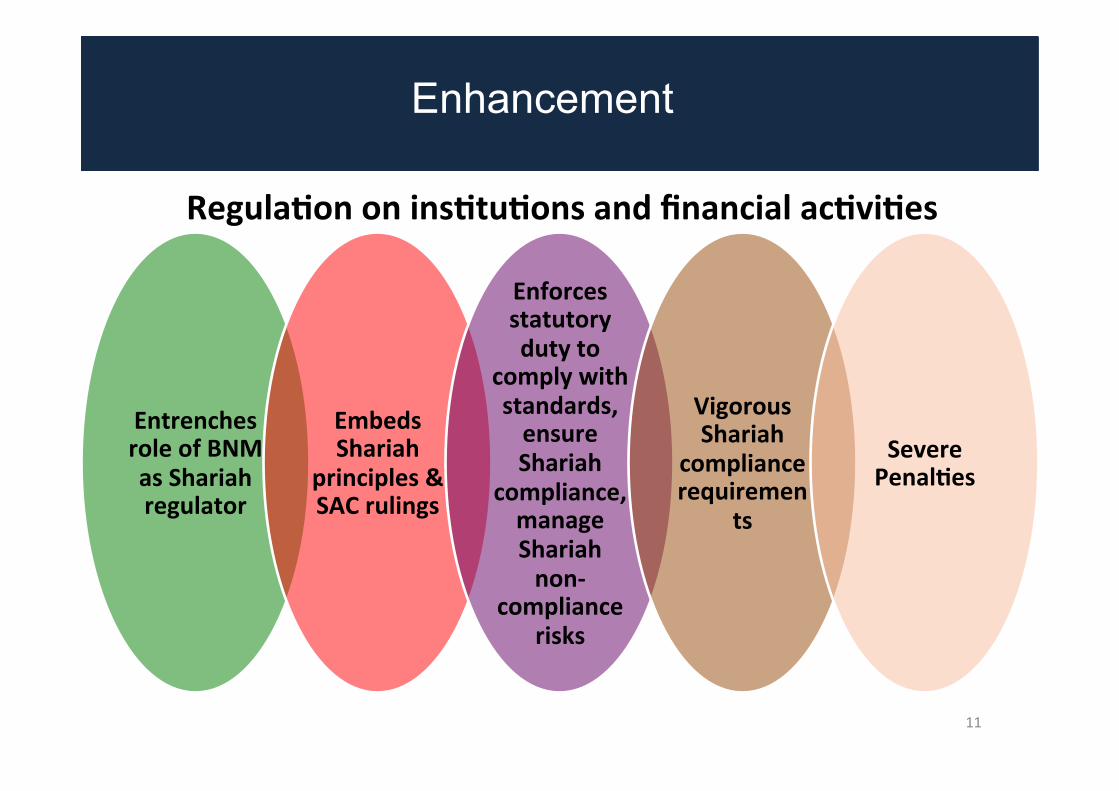

Enhancement

EntrenchesroleofBNMasShariahregulator

EmbedsShariah

principles&SACrulings

Enforcesstatutorydutyto

complywithstandards,ensureShariah

compliance,manageShariahnon-

compliancerisks

VigorousShariah

compliancerequiremen

ts

SeverePenalOes

RegulaOononinsOtuOonsandfinancialacOviOes

Significant Features of the IFSA

12

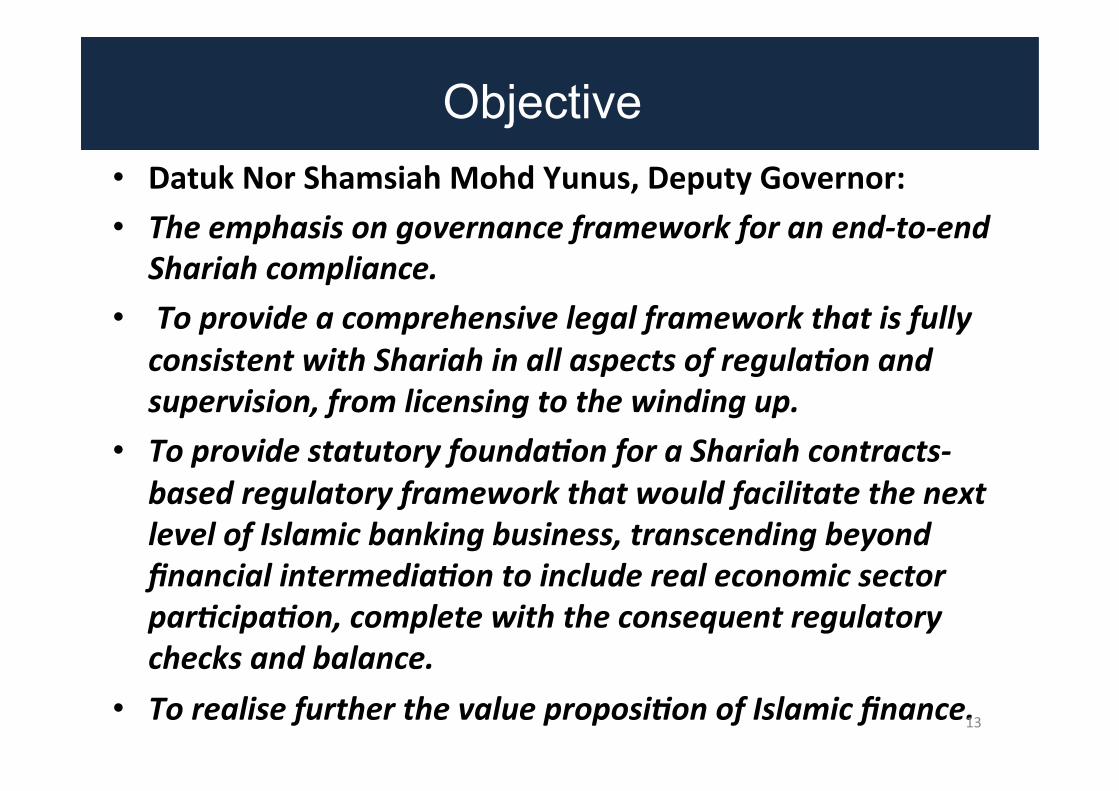

• DatukNorShamsiahMohdYunus,DeputyGovernor:• Theemphasisongovernanceframeworkforanend-to-end

Shariahcompliance.• Toprovideacomprehensivelegalframeworkthatisfully

consistentwithShariahinallaspectsofregula;onandsupervision,fromlicensingtothewindingup.

• Toprovidestatutoryfounda;onforaShariahcontracts-basedregulatoryframeworkthatwouldfacilitatethenextlevelofIslamicbankingbusiness,transcendingbeyondfinancialintermedia;ontoincluderealeconomicsectorpar;cipa;on,completewiththeconsequentregulatorychecksandbalance.

• Torealisefurtherthevalueproposi;onofIslamicfinance.

13

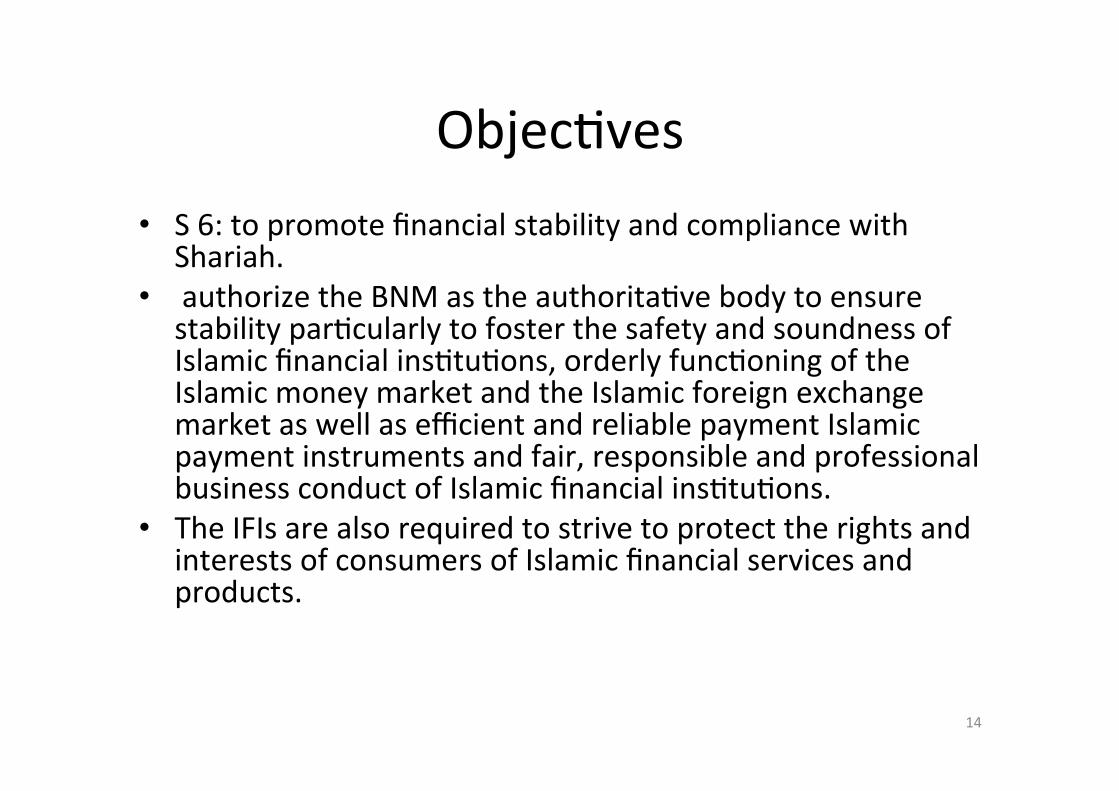

Objective

ObjecMves• S6:topromotefinancialstabilityandcompliancewith

Shariah.• authorizetheBNMastheauthoritaMvebodytoensure

stabilityparMcularlytofosterthesafetyandsoundnessofIslamicfinancialinsMtuMons,orderlyfuncMoningoftheIslamicmoneymarketandtheIslamicforeignexchangemarketaswellasefficientandreliablepaymentIslamicpaymentinstrumentsandfair,responsibleandprofessionalbusinessconductofIslamicfinancialinsMtuMons.

• TheIFIsarealsorequiredtostrivetoprotecttherightsandinterestsofconsumersofIslamicfinancialservicesandproducts.

14

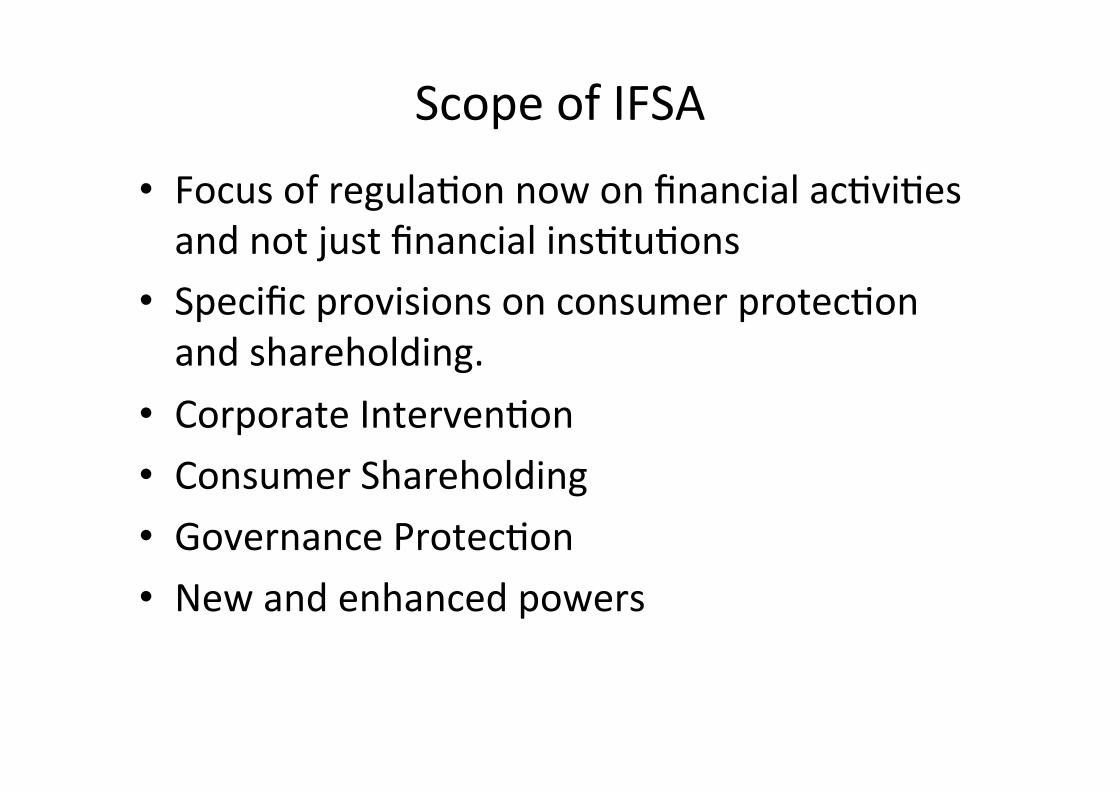

ScopeofIFSA• FocusofregulaMonnowonfinancialacMviMesandnotjustfinancialinsMtuMons

• SpecificprovisionsonconsumerprotecMonandshareholding.

• CorporateIntervenMon• ConsumerShareholding• GovernanceProtecMon• Newandenhancedpowers

16

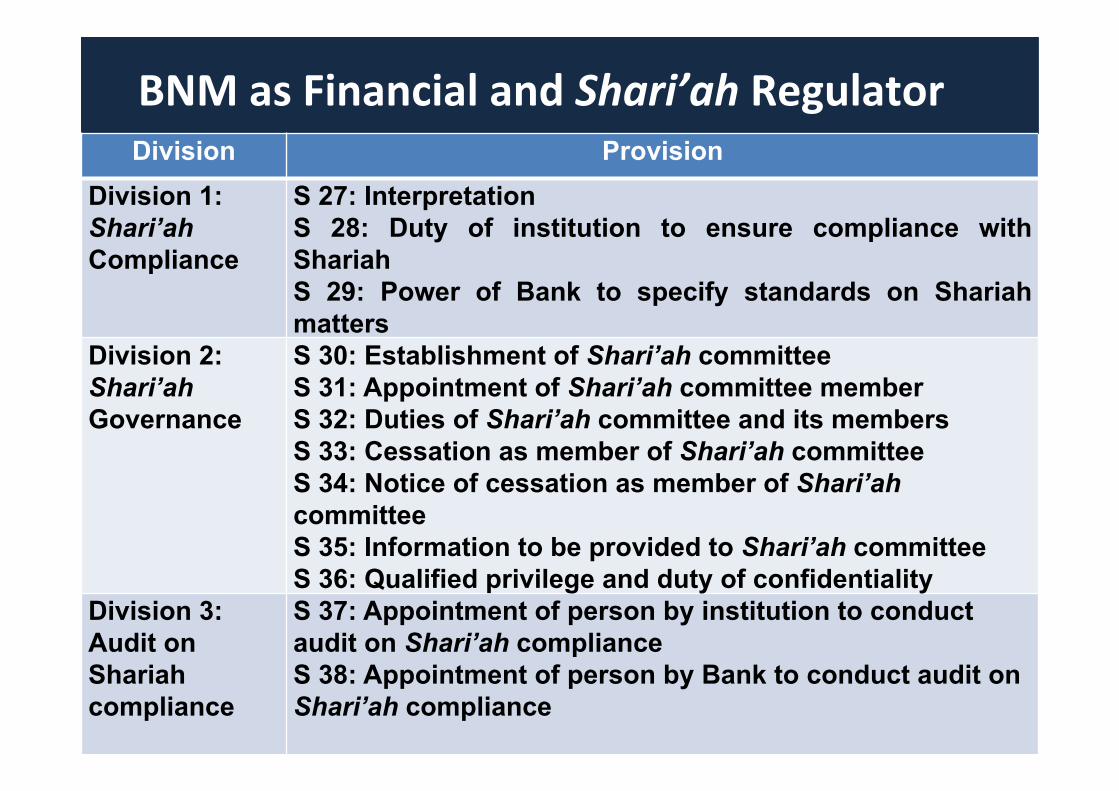

BNMasFinancialandShari’ahRegulatorDivision Provision

Division 1: Shari’ah Compliance

S 27: InterpretationS 28: Duty of institution to ensure compliance with Shariah S 29: Power of Bank to specify standards on Shariah matters

Division 2: Shari’ah Governance

S 30: Establishment of Shari’ah committeeS 31: Appointment of Shari’ah committee memberS 32: Duties of Shari’ah committee and its members S 33: Cessation as member of Shari’ah committee S 34: Notice of cessation as member of Shari’ah committee S 35: Information to be provided to Shari’ah committee S 36: Qualified privilege and duty of confidentiality

Division 3: Audit on Shariah compliance

S 37: Appointment of person by institution to conduct audit on Shari’ah complianceS 38: Appointment of person by Bank to conduct audit on Shari’ah compliance

17

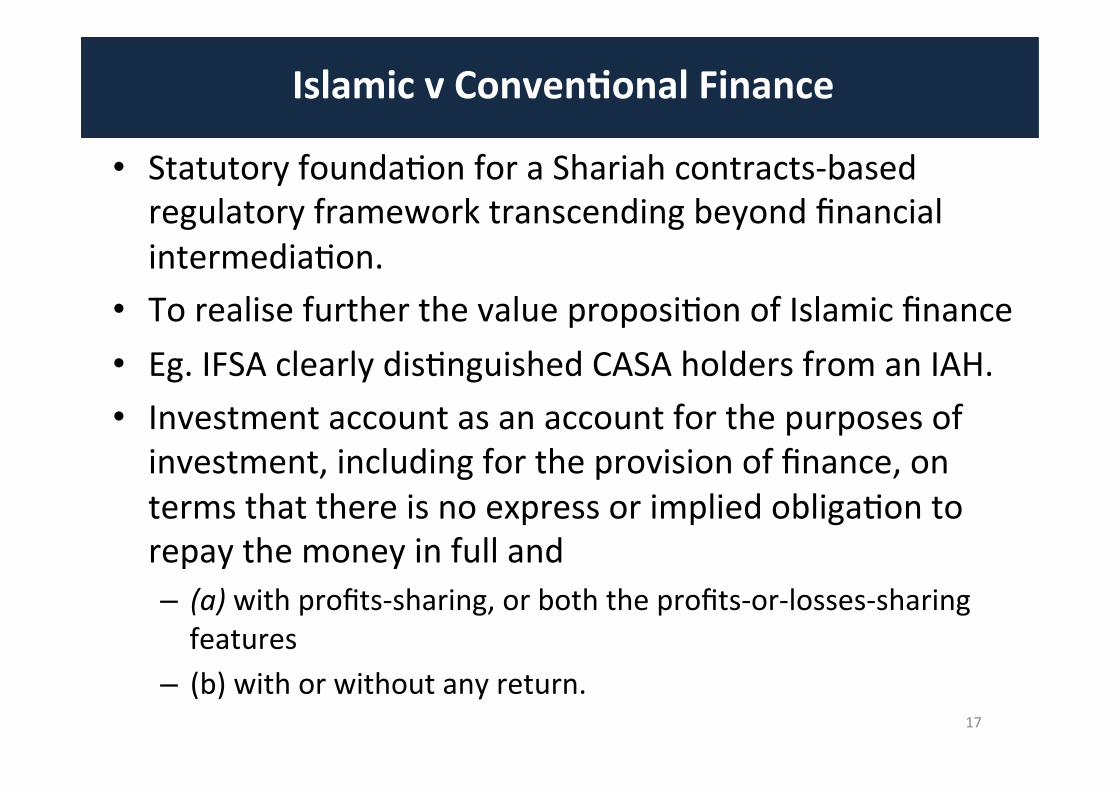

• StatutoryfoundaMonforaShariahcontracts-basedregulatoryframeworktranscendingbeyondfinancialintermediaMon.

• TorealisefurtherthevalueproposiMonofIslamicfinance• Eg.IFSAclearlydisMnguishedCASAholdersfromanIAH.• Investmentaccountasanaccountforthepurposesofinvestment,includingfortheprovisionoffinance,ontermsthatthereisnoexpressorimpliedobligaMontorepaythemoneyinfulland– (a)withprofits-sharing,orboththeprofits-or-losses-sharingfeatures

– (b)withorwithoutanyreturn.

IslamicvConvenOonalFinance

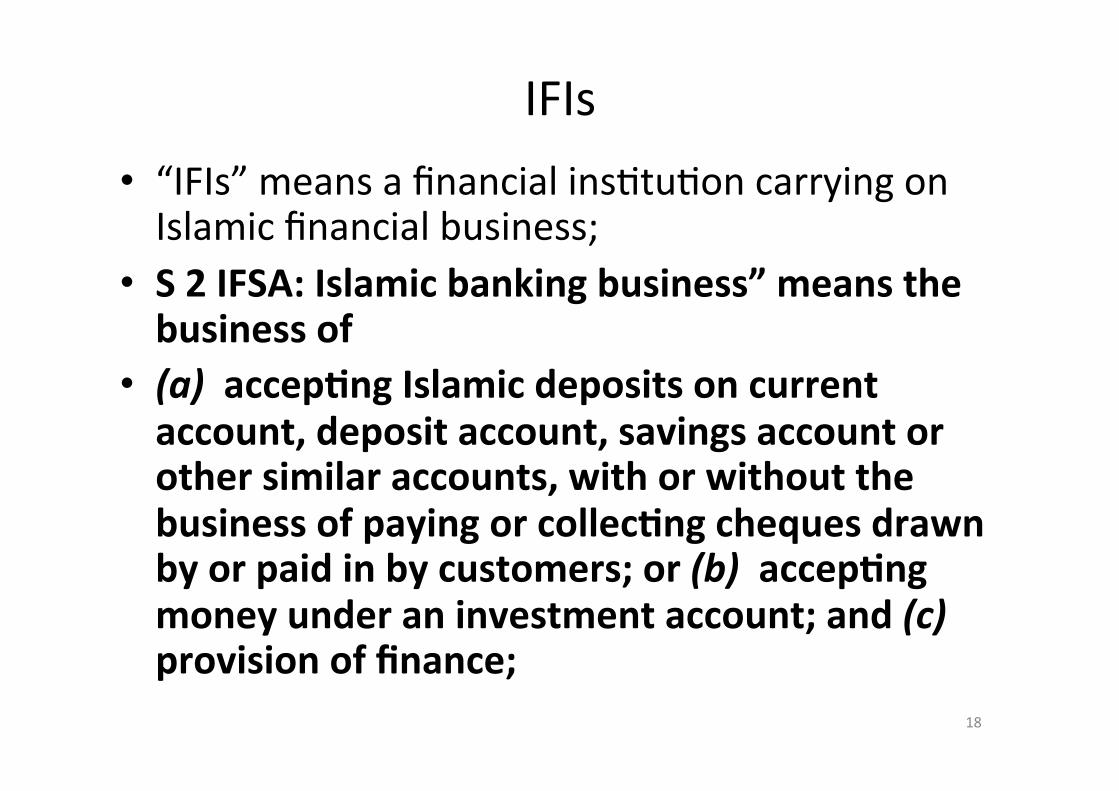

IFIs• “IFIs”meansafinancialinsMtuMoncarryingonIslamicfinancialbusiness;

• S2IFSA:Islamicbankingbusiness”meansthebusinessof

• (a)accepOngIslamicdepositsoncurrentaccount,depositaccount,savingsaccountorothersimilaraccounts,withorwithoutthebusinessofpayingorcollecOngchequesdrawnbyorpaidinbycustomers;or(b)accepOngmoneyunderaninvestmentaccount;and(c)provisionoffinance;

18

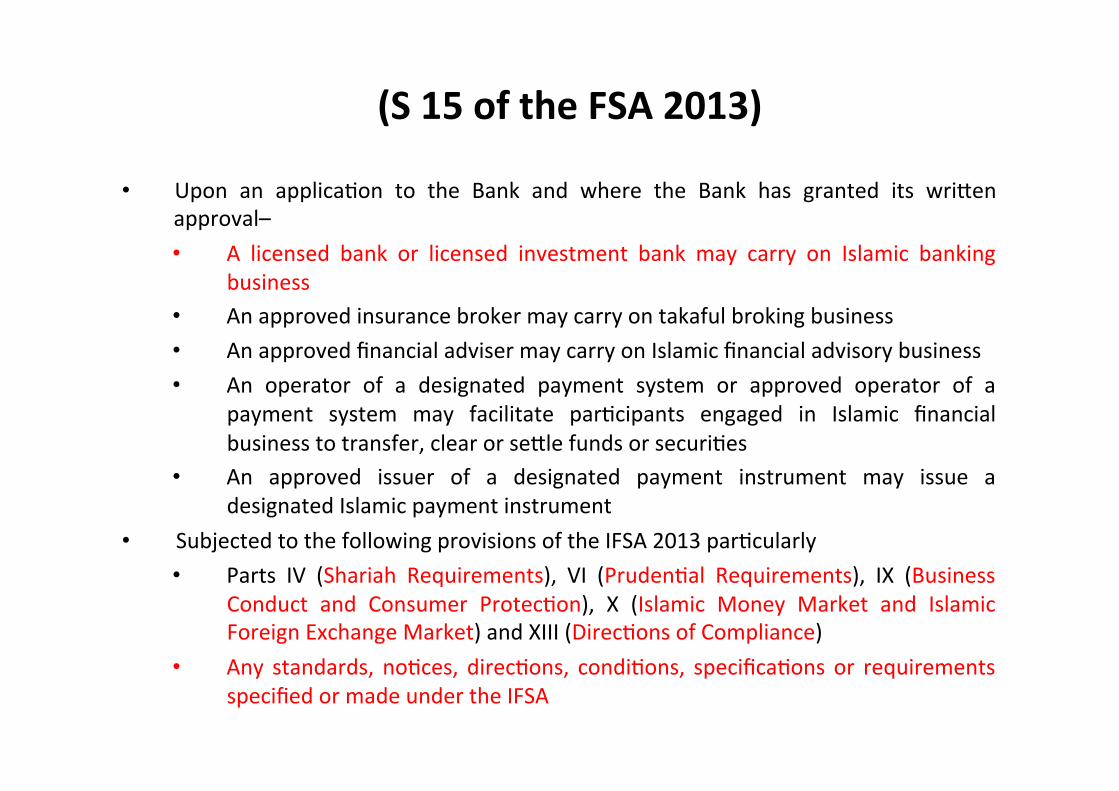

(S15oftheFSA2013)

• Upon an applicaMon to the Bank and where the Bank has granted its wriYenapproval–• A licensed bank or licensed investment bank may carry on Islamic banking

business• Anapprovedinsurancebrokermaycarryontakafulbrokingbusiness• AnapprovedfinancialadvisermaycarryonIslamicfinancialadvisorybusiness• An operator of a designated payment system or approved operator of a

payment system may facilitate parMcipants engaged in Islamic financialbusinesstotransfer,clearorseYlefundsorsecuriMes

• An approved issuer of a designated payment instrument may issue adesignatedIslamicpaymentinstrument

• SubjectedtothefollowingprovisionsoftheIFSA2013parMcularly• Parts IV (Shariah Requirements), VI (PrudenMal Requirements), IX (Business

Conduct and Consumer ProtecMon), X (Islamic Money Market and IslamicForeignExchangeMarket)andXIII(DirecMonsofCompliance)

• Any standards, noMces, direcMons, condiMons, specificaMonsor requirementsspecifiedormadeundertheIFSA

©ZICOlaw.AllRightsReserved.

19

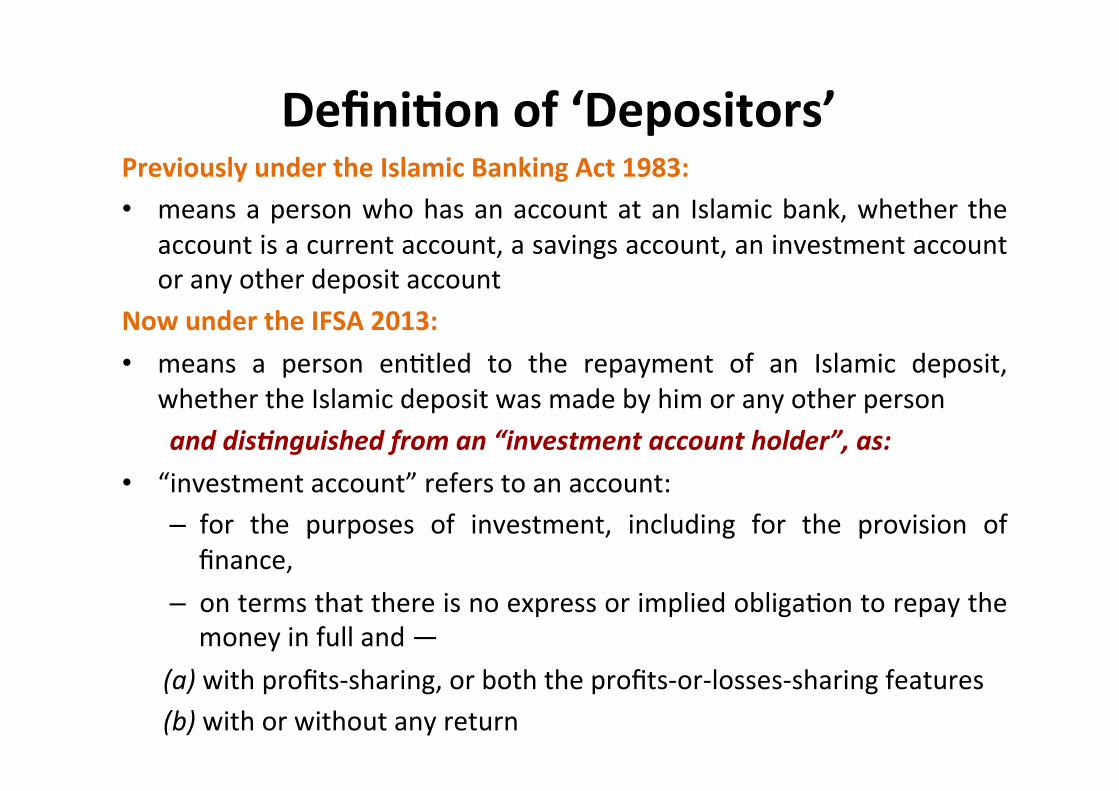

DefiniOonof‘Depositors’PreviouslyundertheIslamicBankingAct1983:• meansapersonwhohasanaccountatan Islamicbank,whether the

accountisacurrentaccount,asavingsaccount,aninvestmentaccountoranyotherdepositaccount

NowundertheIFSA2013:• means a person enMtled to the repayment of an Islamic deposit,

whethertheIslamicdepositwasmadebyhimoranyotherpersonanddis;nguishedfroman“investmentaccountholder”,as:

• “investmentaccount”referstoanaccount:– for the purposes of investment, including for the provision offinance,

– ontermsthatthereisnoexpressorimpliedobligaMontorepaythemoneyinfulland—

(a)withprofits-sharing,orboththeprofits-or-losses-sharingfeatures(b)withorwithoutanyreturn

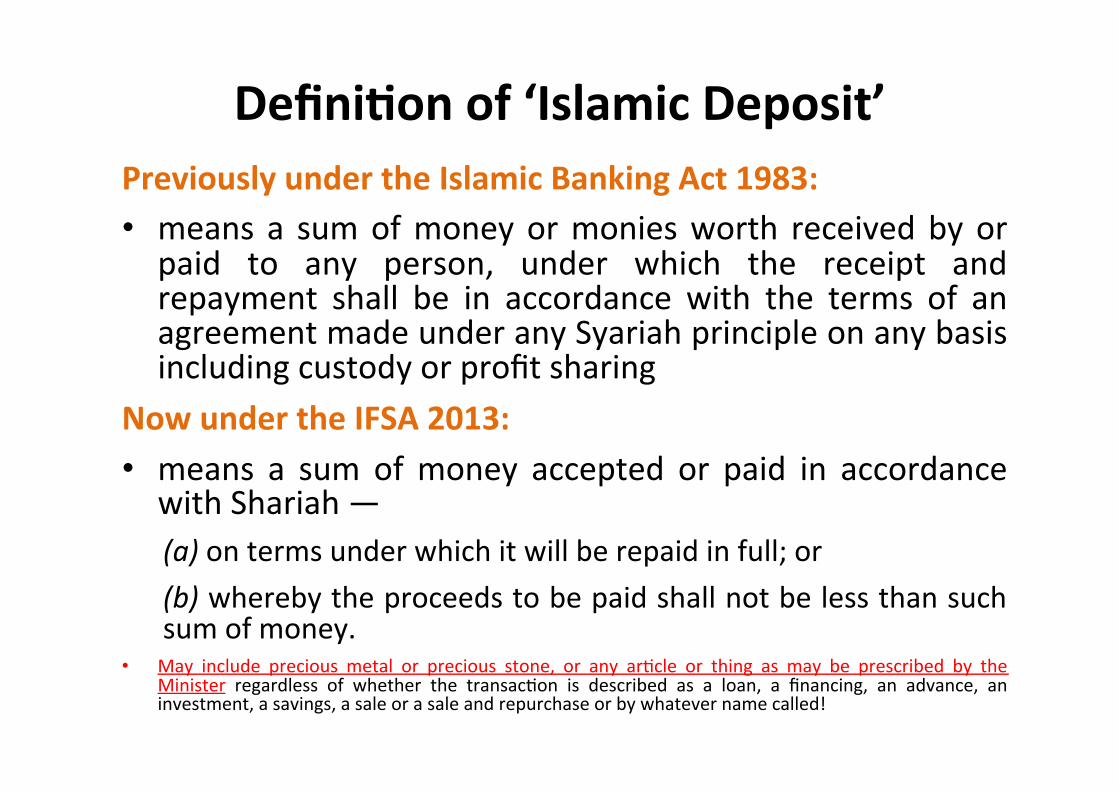

DefiniOonof‘IslamicDeposit’PreviouslyundertheIslamicBankingAct1983:• means a sumofmoneyormoniesworth receivedbyorpaid to any person, under which the receipt andrepayment shall be in accordance with the terms of anagreementmadeunderanySyariahprincipleonanybasisincludingcustodyorprofitsharing

NowundertheIFSA2013:• means a sum ofmoney accepted or paid in accordancewithShariah—(a)ontermsunderwhichitwillberepaidinfull;or(b)wherebytheproceedstobepaidshallnotbelessthansuchsumofmoney.

• May include precious metal or precious stone, or any arMcle or thing as may be prescribed by theMinister regardless of whether the transacMon is described as a loan, a financing, an advance, aninvestment,asavings,asaleorasaleandrepurchaseorbywhatevernamecalled!

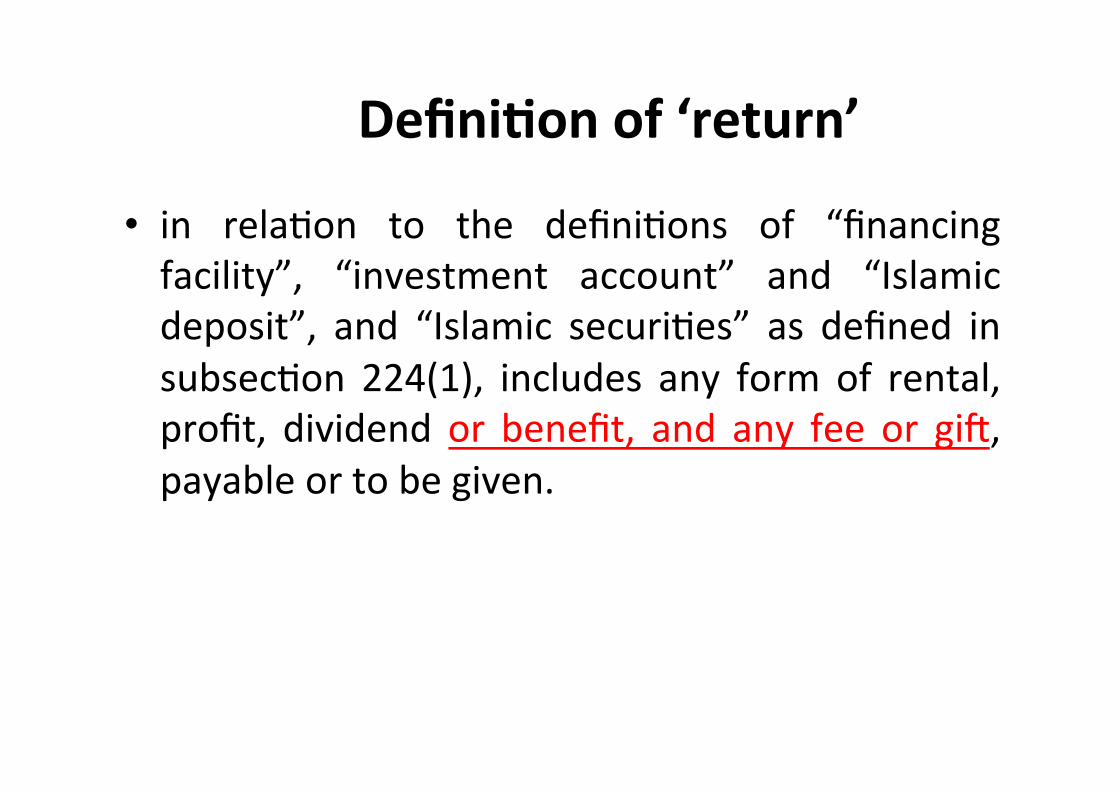

DefiniOonof‘return’

• in relaMon to the definiMons of “financingfacility”, “investment account” and “Islamicdeposit”, and “Islamic securiMes” as defined insubsecMon 224(1), includes any form of rental,profit, dividend or benefit, and any fee or gio,payableortobegiven.

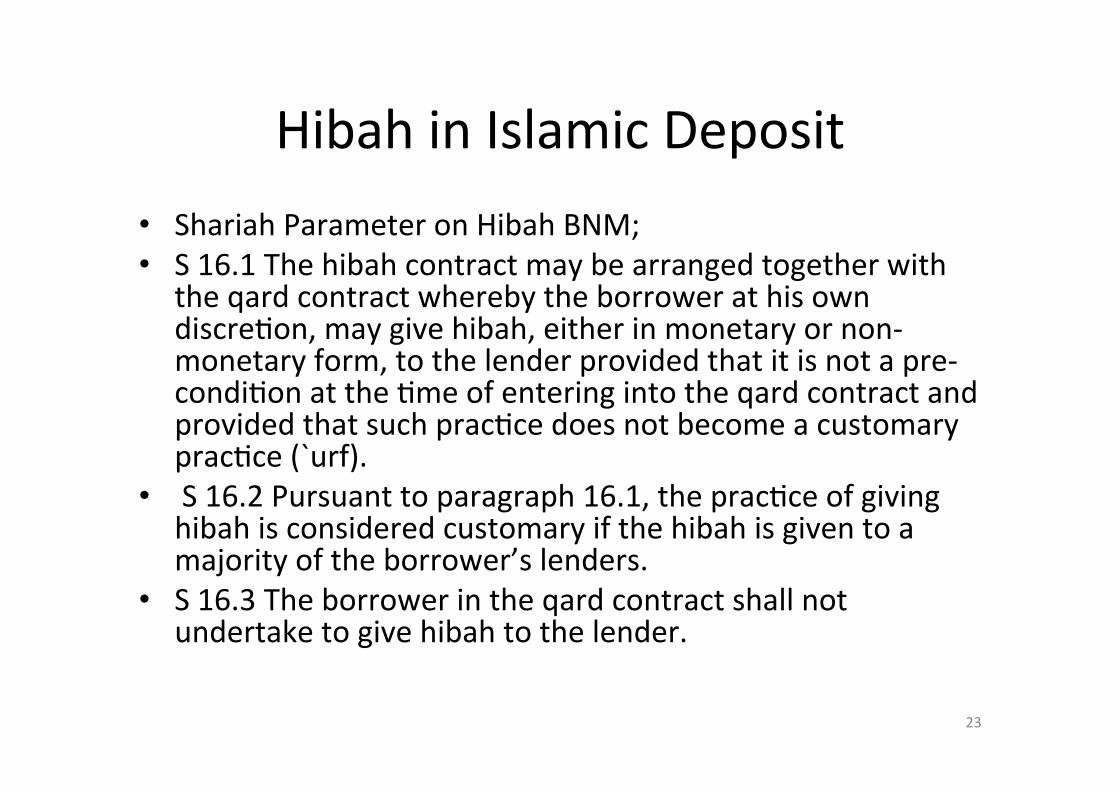

HibahinIslamicDeposit• ShariahParameteronHibahBNM;• S16.1Thehibahcontractmaybearrangedtogetherwith

theqardcontractwherebytheborrowerathisowndiscreMon,maygivehibah,eitherinmonetaryornon-monetaryform,tothelenderprovidedthatitisnotapre-condiMonattheMmeofenteringintotheqardcontractandprovidedthatsuchpracMcedoesnotbecomeacustomarypracMce(`urf).

• S16.2Pursuanttoparagraph16.1,thepracMceofgivinghibahisconsideredcustomaryifthehibahisgiventoamajorityoftheborrower’slenders.

• S16.3Theborrowerintheqardcontractshallnotundertaketogivehibahtothelender.

23

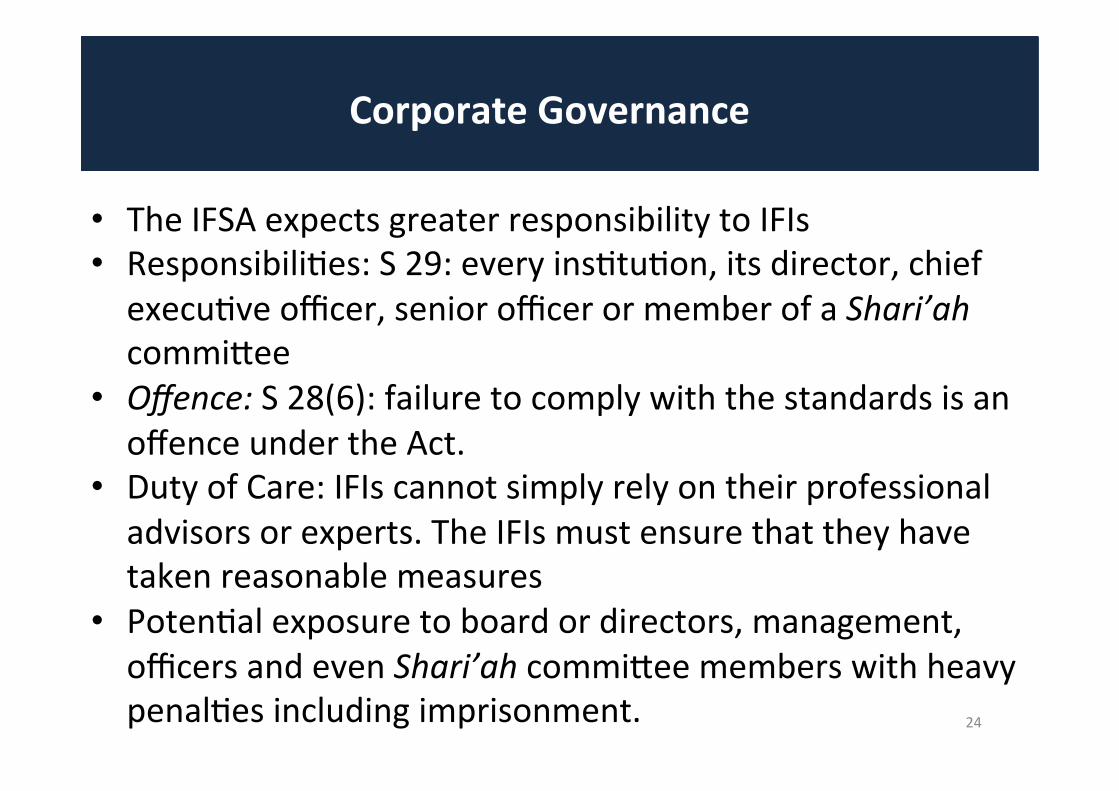

CorporateGovernance

24

• TheIFSAexpectsgreaterresponsibilitytoIFIs• ResponsibiliMes:S29:everyinsMtuMon,itsdirector,chiefexecuMveofficer,seniorofficerormemberofaShari’ahcommiYee

• Offence:S28(6):failuretocomplywiththestandardsisanoffenceundertheAct.

• DutyofCare:IFIscannotsimplyrelyontheirprofessionaladvisorsorexperts.TheIFIsmustensurethattheyhavetakenreasonablemeasures

• PotenMalexposuretoboardordirectors,management,officersandevenShari’ahcommiYeememberswithheavypenalMesincludingimprisonment.

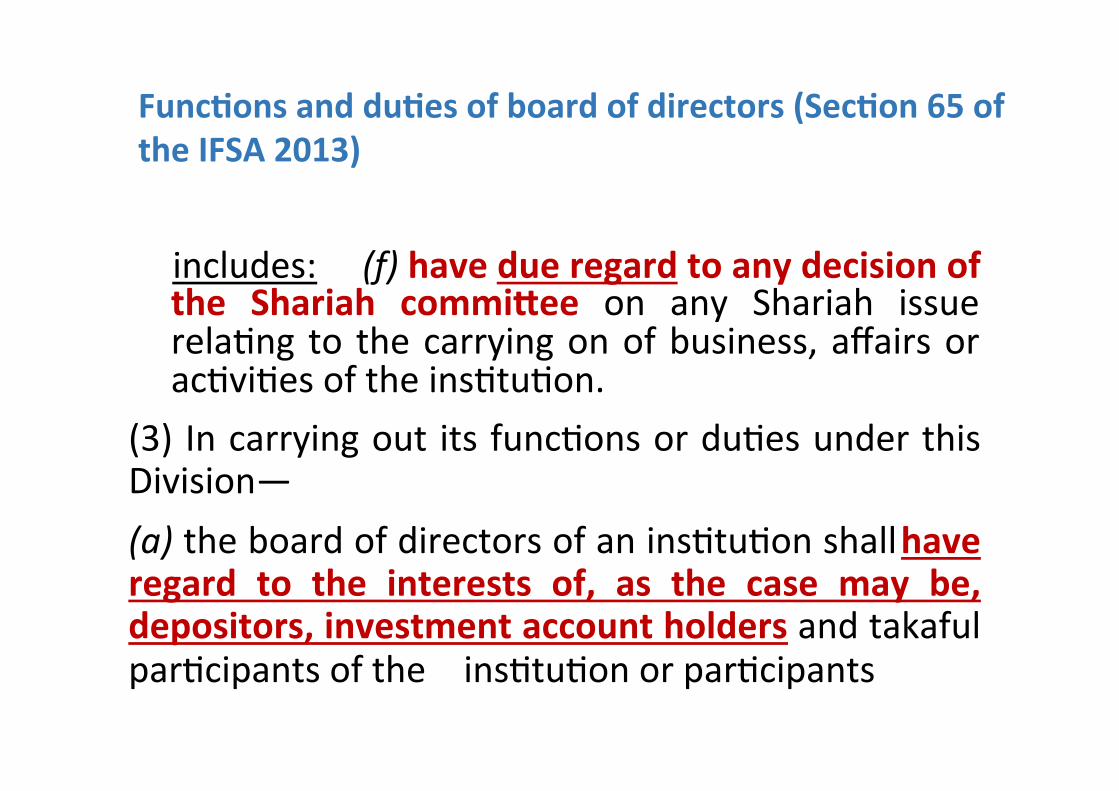

includes: (f)havedueregardtoanydecisionofthe Shariah commi^ee on any Shariah issuerelaMng to thecarryingonofbusiness,affairsoracMviMesoftheinsMtuMon.

(3) Incarryingout itsfuncMonsorduMesunderthisDivision—(a)theboardofdirectorsofaninsMtuMonshallhaveregard to the interests of, as the case may be,depositors,investmentaccountholdersandtakafulparMcipantsofthe insMtuMonorparMcipants

FuncOonsandduOesofboardofdirectors(SecOon65oftheIFSA2013)

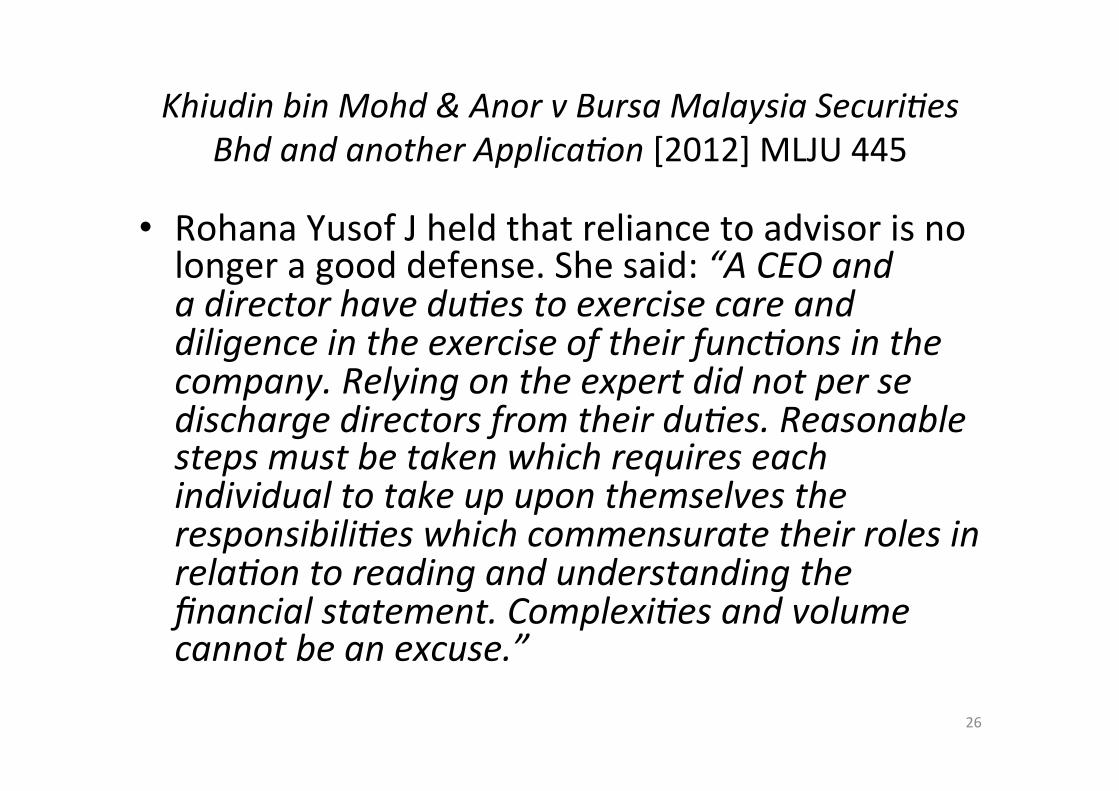

KhiudinbinMohd&AnorvBursaMalaysiaSecuri,esBhdandanotherApplica,on[2012]MLJU445

• RohanaYusofJheldthatreliancetoadvisorisnolongeragooddefense.Shesaid:“ACEOandadirectorhavedu,estoexercisecareanddiligenceintheexerciseoftheirfunc,onsinthecompany.Relyingontheexpertdidnotpersedischargedirectorsfromtheirdu,es.Reasonablestepsmustbetakenwhichrequireseachindividualtotakeupuponthemselvestheresponsibili,eswhichcommensuratetheirrolesinrela,ontoreadingandunderstandingthefinancialstatement.Complexi,esandvolumecannotbeanexcuse.”

26

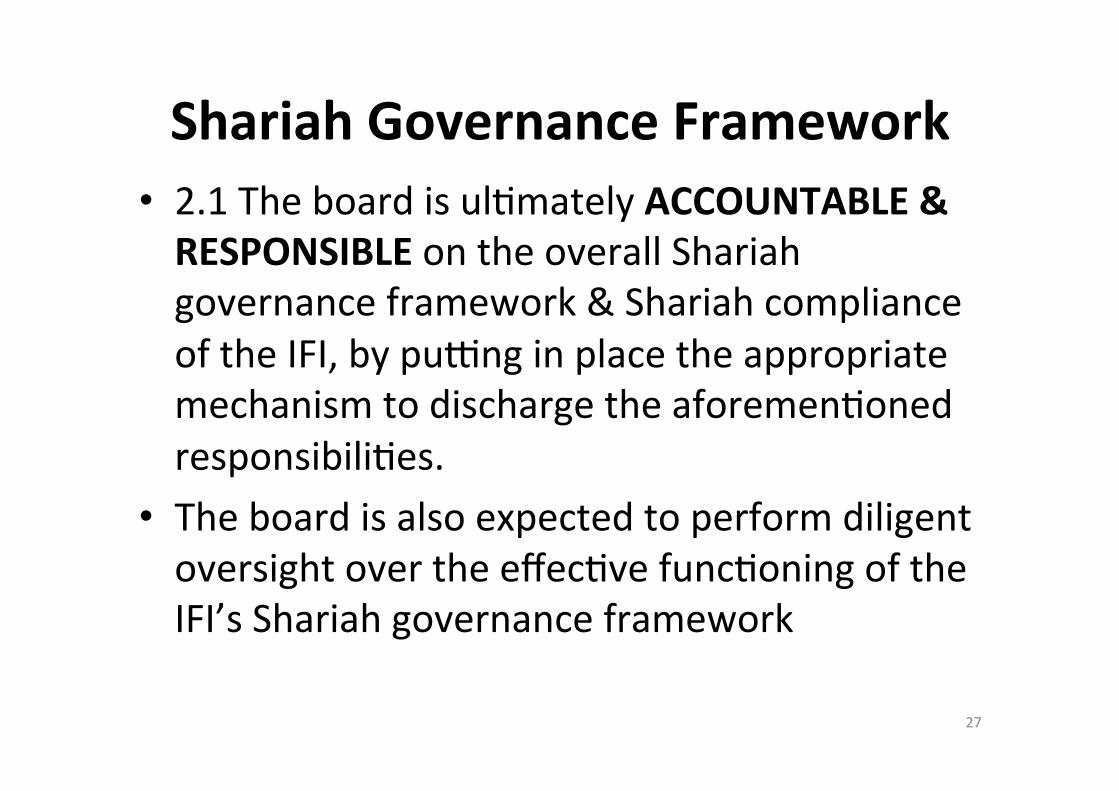

ShariahGovernanceFramework• 2.1TheboardisulMmatelyACCOUNTABLE&RESPONSIBLEontheoverallShariahgovernanceframework&ShariahcomplianceoftheIFI,bypuvnginplacetheappropriatemechanismtodischargetheaforemenMonedresponsibiliMes.

• TheboardisalsoexpectedtoperformdiligentoversightovertheeffecMvefuncMoningoftheIFI’sShariahgovernanceframework

27

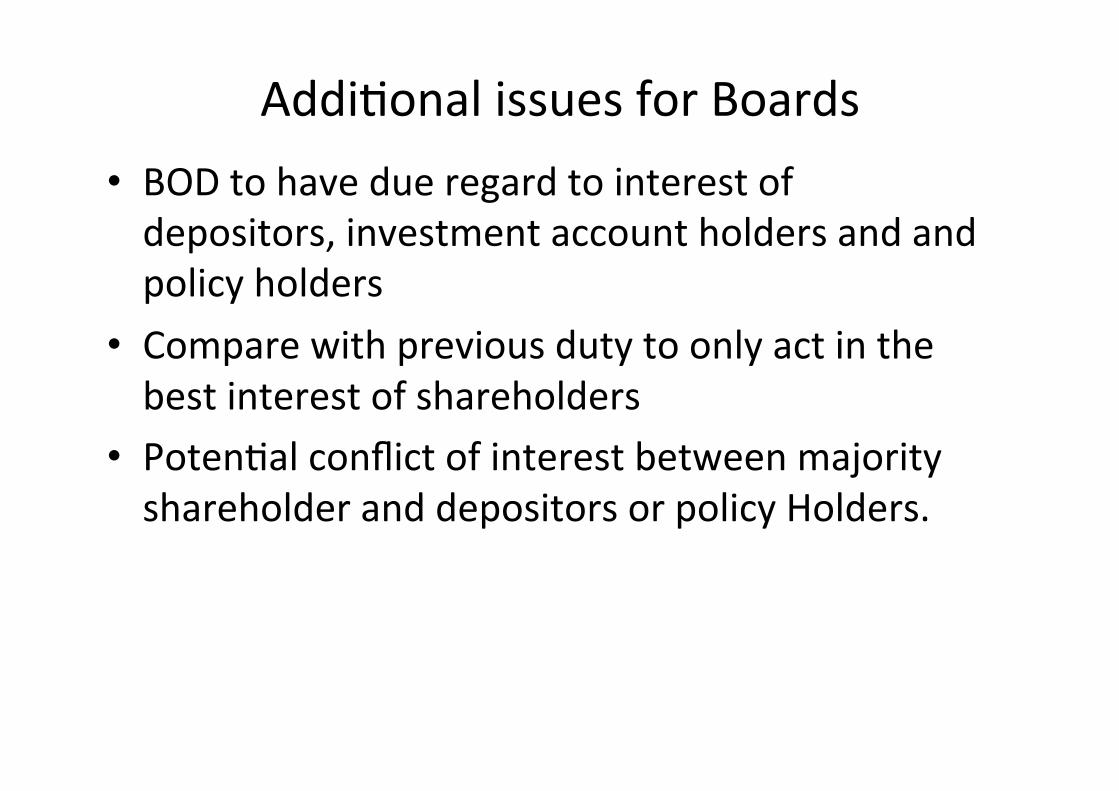

AddiMonalissuesforBoards• BODtohavedueregardtointerestofdepositors,investmentaccountholdersandandpolicyholders

• Comparewithpreviousdutytoonlyactinthebestinterestofshareholders

• PotenMalconflictofinterestbetweenmajorityshareholderanddepositorsorpolicyHolders.

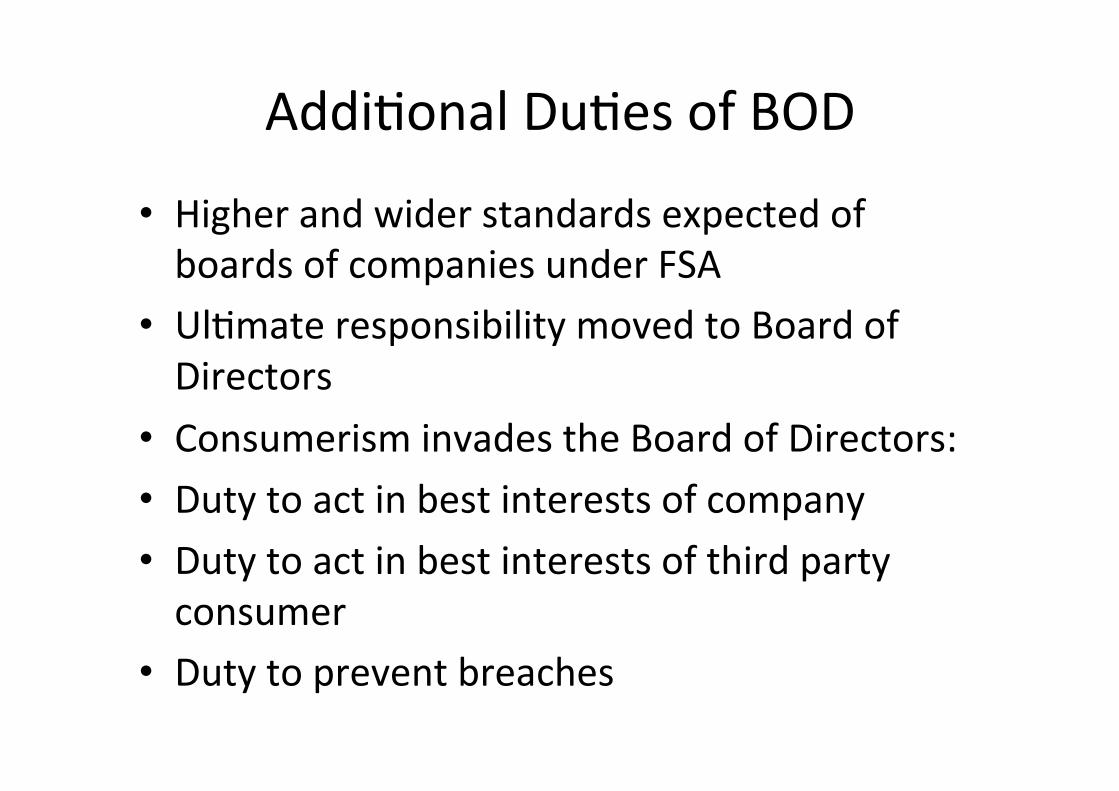

AddiMonalDuMesofBOD

• HigherandwiderstandardsexpectedofboardsofcompaniesunderFSA

• UlMmateresponsibilitymovedtoBoardofDirectors

• ConsumerisminvadestheBoardofDirectors:• Dutytoactinbestinterestsofcompany• Dutytoactinbestinterestsofthirdpartyconsumer

• Dutytopreventbreaches

Consumerism

30

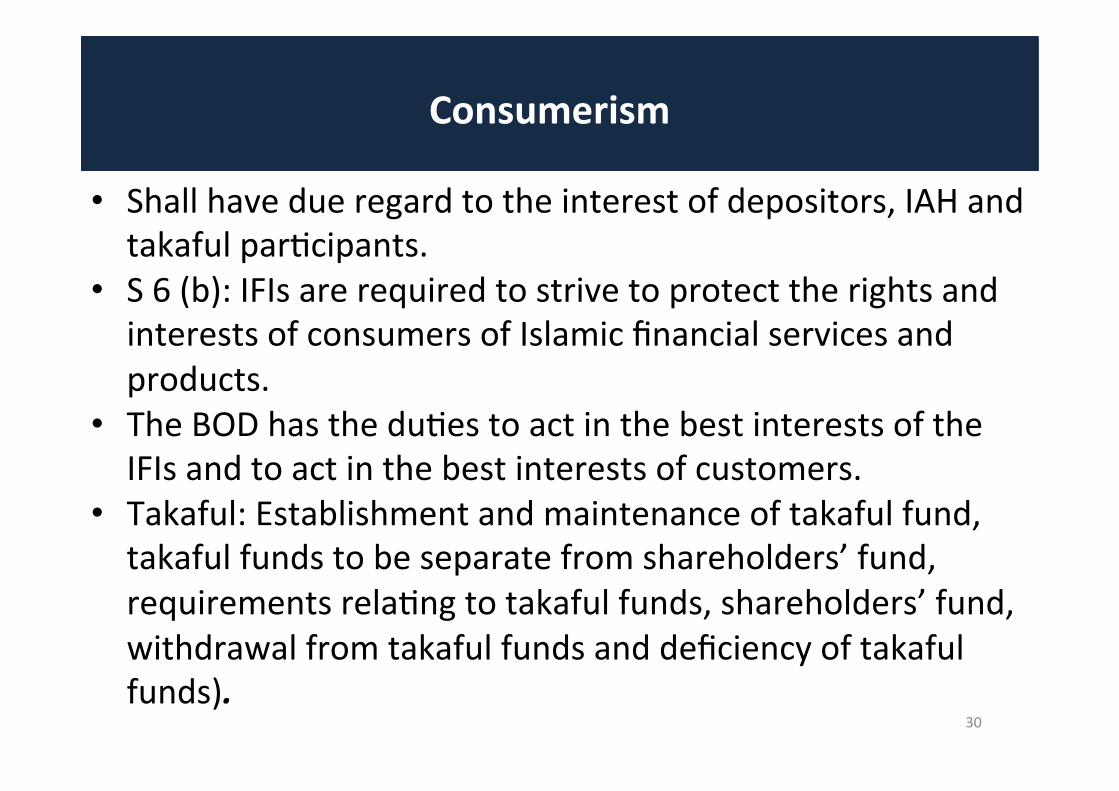

• Shallhavedueregardtotheinterestofdepositors,IAHandtakafulparMcipants.

• S6(b):IFIsarerequiredtostrivetoprotecttherightsandinterestsofconsumersofIslamicfinancialservicesandproducts.

• TheBODhastheduMestoactinthebestinterestsoftheIFIsandtoactinthebestinterestsofcustomers.

• Takaful:Establishmentandmaintenanceoftakafulfund,takafulfundstobeseparatefromshareholders’fund,requirementsrelaMngtotakafulfunds,shareholders’fund,withdrawalfromtakafulfundsanddeficiencyoftakafulfunds).

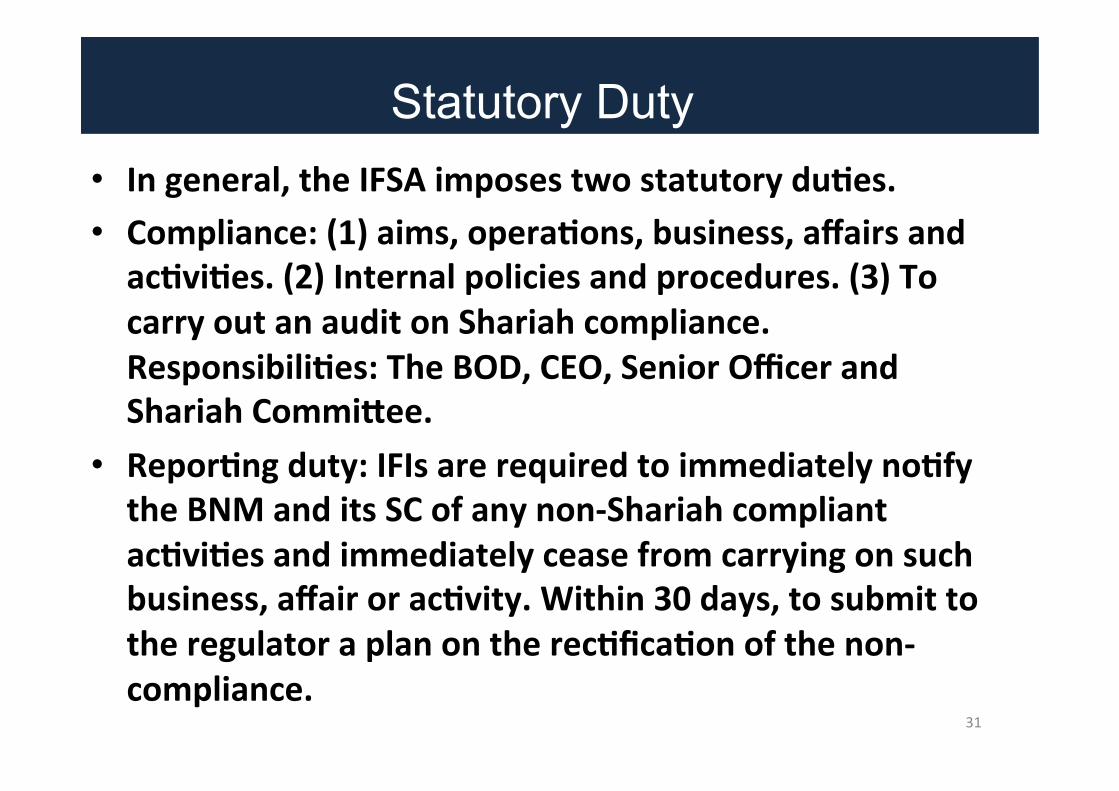

• Ingeneral,theIFSAimposestwostatutoryduOes.• Compliance:(1)aims,operaOons,business,affairsandacOviOes.(2)Internalpoliciesandprocedures.(3)TocarryoutanauditonShariahcompliance.ResponsibiliOes:TheBOD,CEO,SeniorOfficerandShariahCommi^ee.

• ReporOngduty:IFIsarerequiredtoimmediatelynoOfytheBNManditsSCofanynon-ShariahcompliantacOviOesandimmediatelyceasefromcarryingonsuchbusiness,affairoracOvity.Within30days,tosubmittotheregulatoraplanontherecOficaOonofthenon-compliance.

31

Statutory Duty

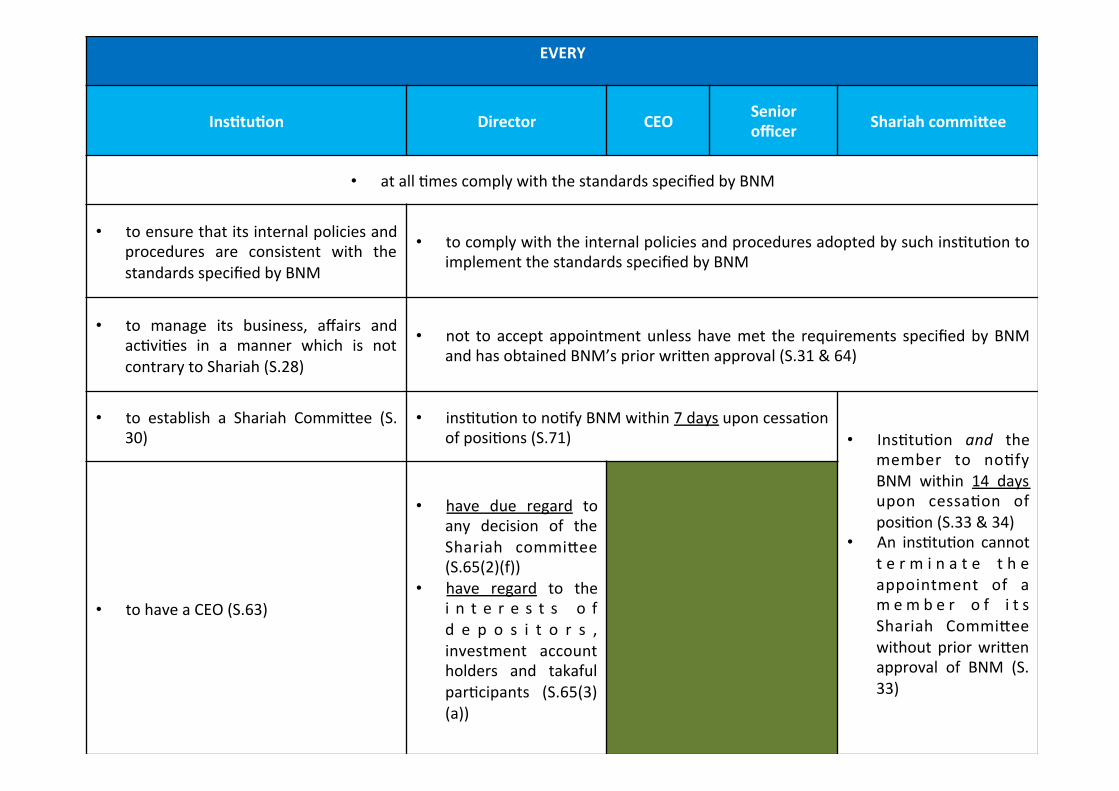

EVERY

InsOtuOon Director CEO Seniorofficer Shariahcommi^ee

• atallMmescomplywiththestandardsspecifiedbyBNM

• toensurethatitsinternalpoliciesandprocedures are consistent with thestandardsspecifiedbyBNM

• tocomplywiththeinternalpoliciesandproceduresadoptedbysuchinsMtuMontoimplementthestandardsspecifiedbyBNM

• to manage its business, affairs andacMviMes in a manner which is notcontrarytoShariah(S.28)

• not to accept appointmentunless havemet the requirements specifiedbyBNMandhasobtainedBNM’spriorwriYenapproval(S.31&64)

• to establish a Shariah CommiYee (S.30)

• insMtuMontonoMfyBNMwithin7daysuponcessaMonofposiMons(S.71) • InsMtuMon and the

member to noMfyBNM within 14 daysupon cessaMon ofposiMon(S.33&34)

• An insMtuMon cannott e r m i n a t e t h eappointment of am e m b e r o f i t sShariah CommiYeewithout priorwriYenapproval of BNM (S.33)

• tohaveaCEO(S.63)

• have due regard toany decision of theShariah commiYee(S.65(2)(f))

• have regard to thei n t e r e s t s o fd e p o s i t o r s ,investment accountholders and takafulparMcipants (S.65(3)(a))

StatutoryDuty:Compliance• S28(1)requiresIFIstoensureatallMmesthattheiraims,operaMons,business,affairsandacMviMesareincompliancewithShariah.

• toensurethatitsinternalpoliciesandproceduresareconsistentwiththestandardsspecifiedbyBNM,tomanageitsbusiness,affairsandacMviMesinamannerwhichisnotcontrarytoShariahandtoestablishaShariahCommiYee

• IFIstocarryoutanauditonShariahcompliance.TheBOD,CEO,SeniorOfficerandShariahCommiYeeshallberesponsibletoensurethatIFIsareatallMmestocomplywiththestandardsspecifiedbyBNM.

Shari’ahCompliance

34

• TheIFSAcomplementsandstrengthenstheShari’ahGovernanceFramework.

• PotenMalexposureofShari’ahscholarstojailterms(Firstofitskind).

• StrictcondiMonandvigorousShari’ahcomplianceprocessandrequirements.

• S28(3)toimmediatelynoMfyanyincidentsofShari’ahNon-Compliance,immediatelyceasefromcarryingonsuchbusiness,andwithin30dayssubmitaplantotheBNMontherecMficaMonofthenon-compliance.

• BNMCircularonShariahNon-ComplianceReporMngissuedon15March2013andcameintoeffecton1May2013.

Shari’ahAudit

35

• S37and38:ExternalShari’ahAudit• BNMmayrequireanIFItoappointanypersonto

carryoutShariahaudit.• BNM may appoint for an IFI any person to

conductaShariahaudit• TheIFIwillbearremuneraMon&expensesof

theShariahauditor/s.

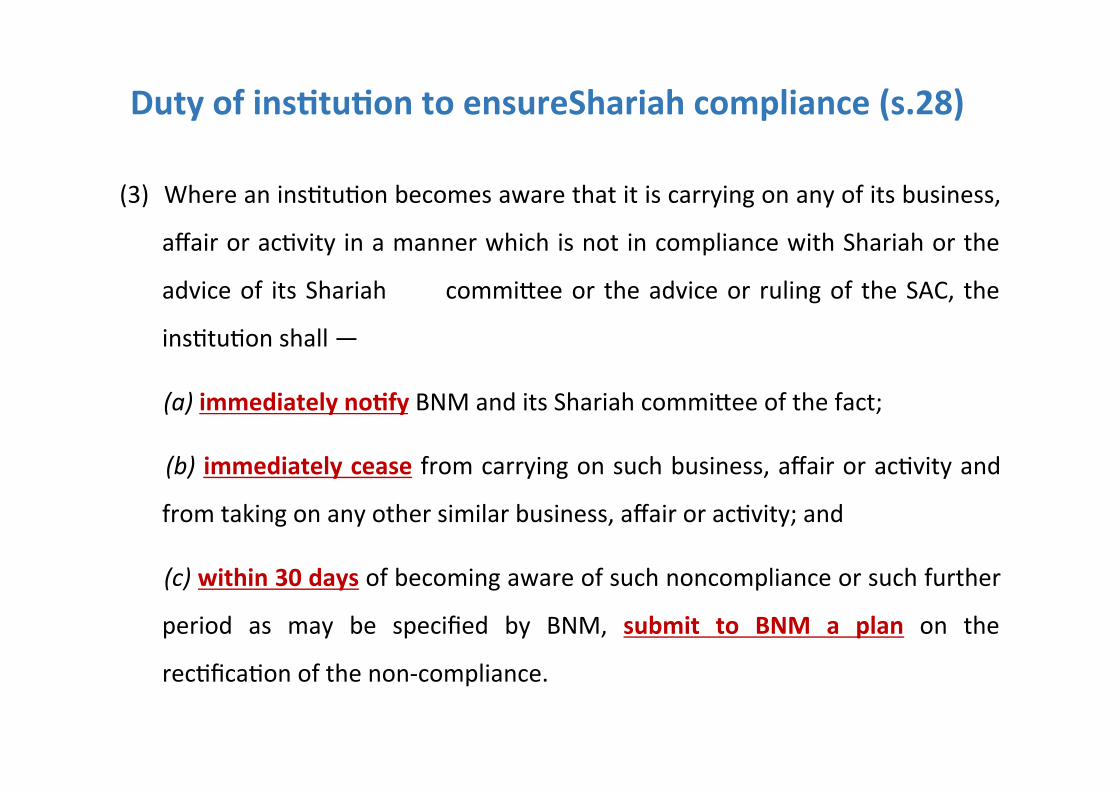

(3) WhereaninsMtuMonbecomesawarethatitiscarryingonanyofitsbusiness,

affairoracMvityinamannerwhichisnotincompliancewithShariahorthe

adviceof itsShariah commiYeeor theadviceor rulingof theSAC, the

insMtuMonshall—

(a)immediatelynoOfyBNManditsShariahcommiYeeofthefact;

(b) immediatelyceasefromcarryingonsuchbusiness,affairoracMvityand

fromtakingonanyothersimilarbusiness,affairoracMvity;and

(c)within30daysofbecomingawareofsuchnoncomplianceorsuchfurther

period as may be specified by BNM, submit to BNM a plan on the

recMficaMonofthenon-compliance.

DutyofinsOtuOontoensureShariahcompliance(s.28)

StatutoryDuty:ReporMng

• IFIsarerequiredtoimmediatelynoMfytheBNManditsShariahcommiYeeofanynon-ShariahcompliantacMviMesandimmediatelyceasefromcarryingonsuchbusiness,affairoracMvity.TheIFIsarerequired,within30days,tosubmittotheregulatoraplanontherecMficaMonofthenon-complianceasprovidedinsecMon28(3)(c).

• SecMon37requiresIFIstosubmitShariahauditcompliancereport.

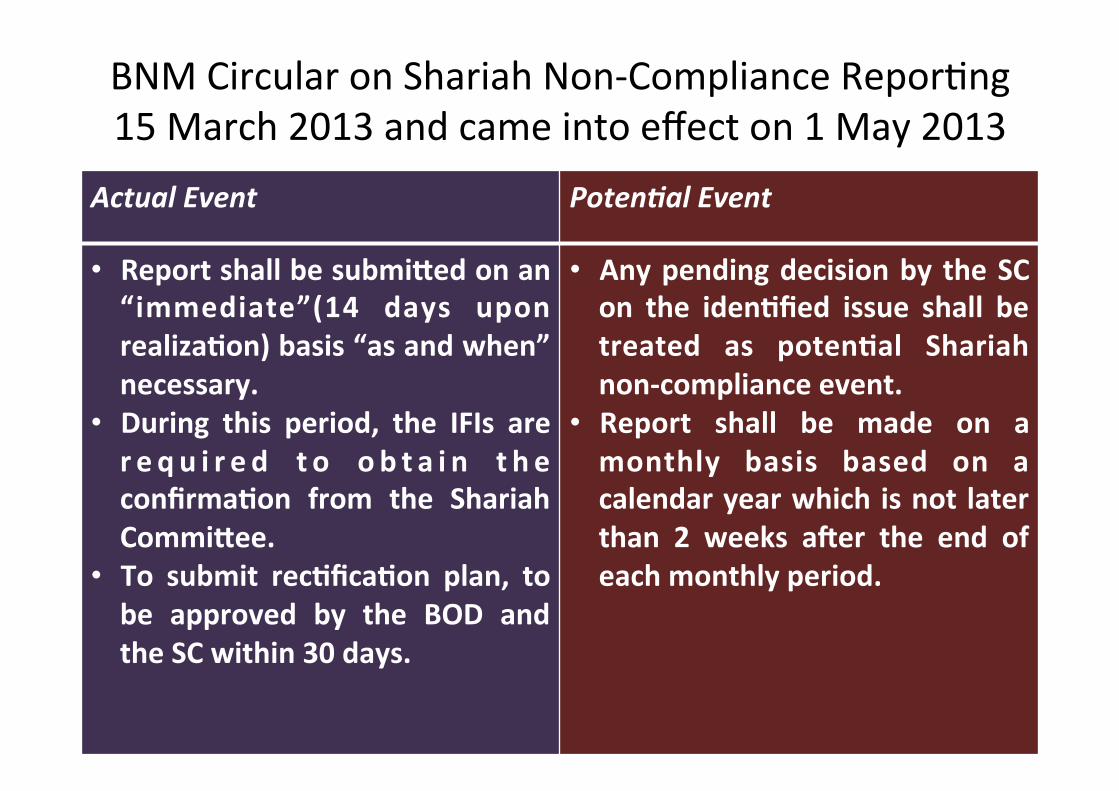

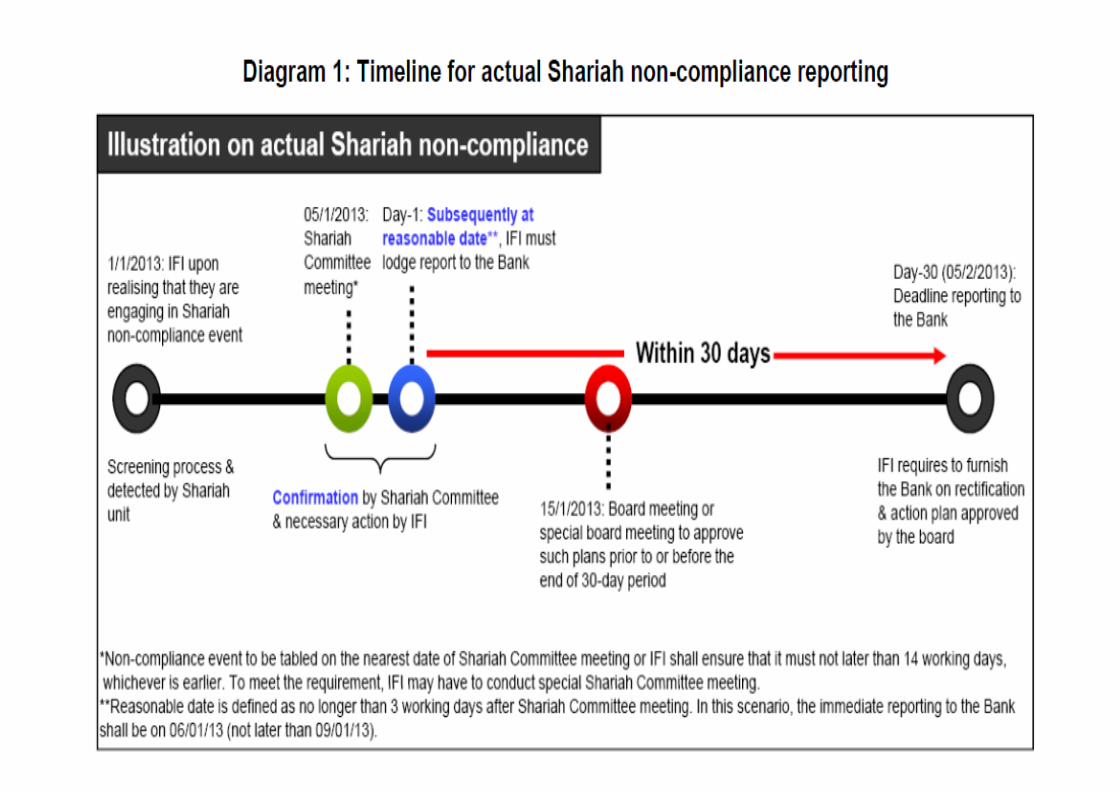

BNMCircularonShariahNon-ComplianceReporMng15March2013andcameintoeffecton1May2013

38

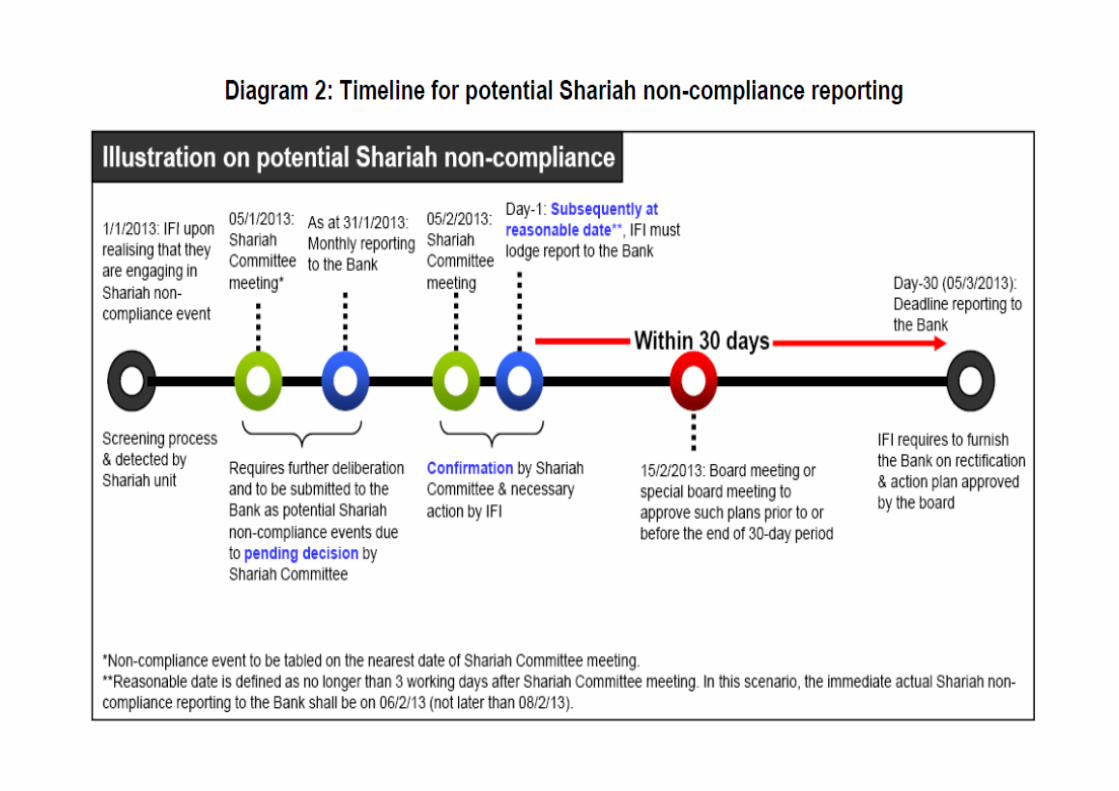

ActualEvent Poten;alEvent

• Reportshallbesubmi^edonan“immediate”(14 days uponrealizaOon)basis“asandwhen”necessary.

• During this period, the IFIs arer e q u i r e d t o o b t a i n t h econfirmaOon from the ShariahCommi^ee.

• To submit recOficaOon plan, tobe approved by the BOD andtheSCwithin30days.

• Anypendingdecisionby theSCon the idenOfied issue shall betreated as potenOal Shariahnon-complianceevent.

• Report shall be made on amonthly basis based on acalendaryearwhich isnot laterthan 2 weeks aier the end ofeachmonthlyperiod.

BNMCircular:ShariahNon-ComplianceReporOng

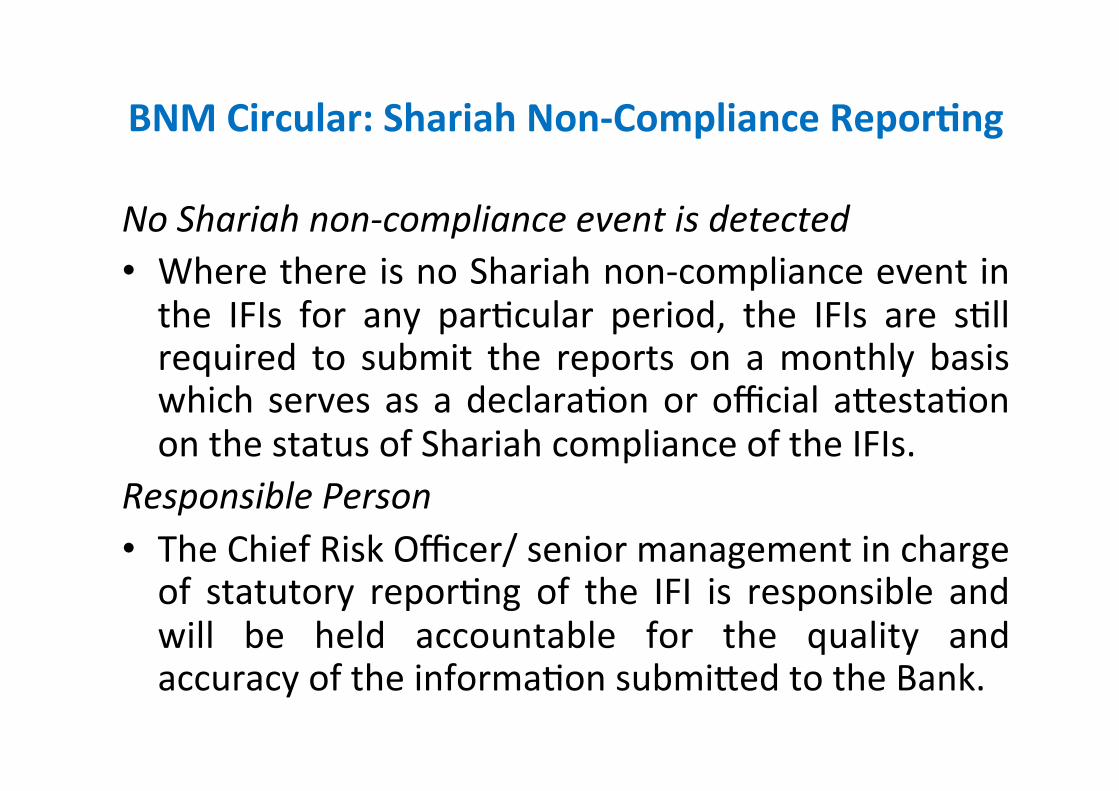

NoShariahnon-complianceeventisdetected• WherethereisnoShariahnon-complianceeventinthe IFIs for any parMcular period, the IFIs are sMllrequired to submit the reports on amonthly basiswhich servesas adeclaraMonorofficial aYestaMononthestatusofShariahcomplianceoftheIFIs.

ResponsiblePerson• TheChiefRiskOfficer/seniormanagementinchargeof statutory reporMng of the IFI is responsible andwill be held accountable for the quality andaccuracyoftheinformaMonsubmiYedtotheBank.

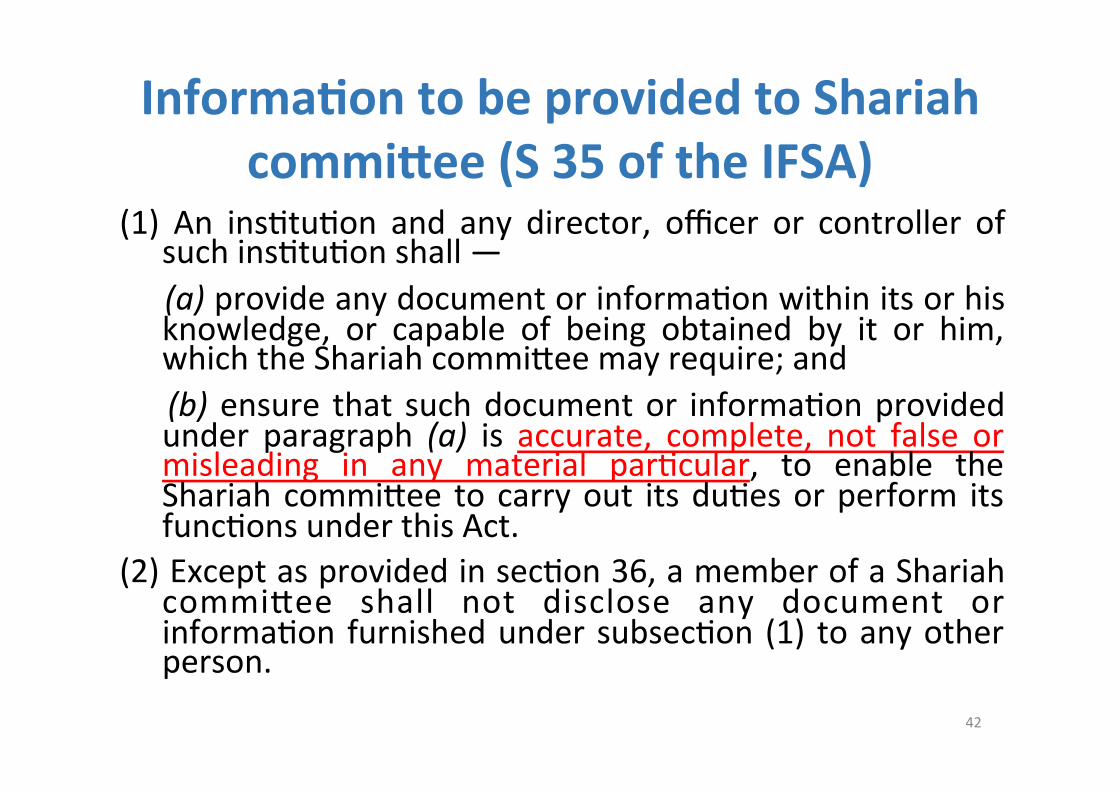

InformaOontobeprovidedtoShariahcommi^ee(S35oftheIFSA)

(1) An insMtuMon and any director, officer or controller ofsuchinsMtuMonshall—(a)provideanydocumentorinformaMonwithinitsorhisknowledge, or capable of being obtained by it or him,whichtheShariahcommiYeemayrequire;and (b)ensure that suchdocumentor informaMonprovidedunder paragraph (a) is accurate, complete, not false ormisleading in any material parMcular, to enable theShariahcommiYee to carryout itsduMesorperform itsfuncMonsunderthisAct.

(2)ExceptasprovidedinsecMon36,amemberofaShariahcommiYee shall not disclose any document orinformaMonfurnishedundersubsecMon (1) toanyotherperson.

42

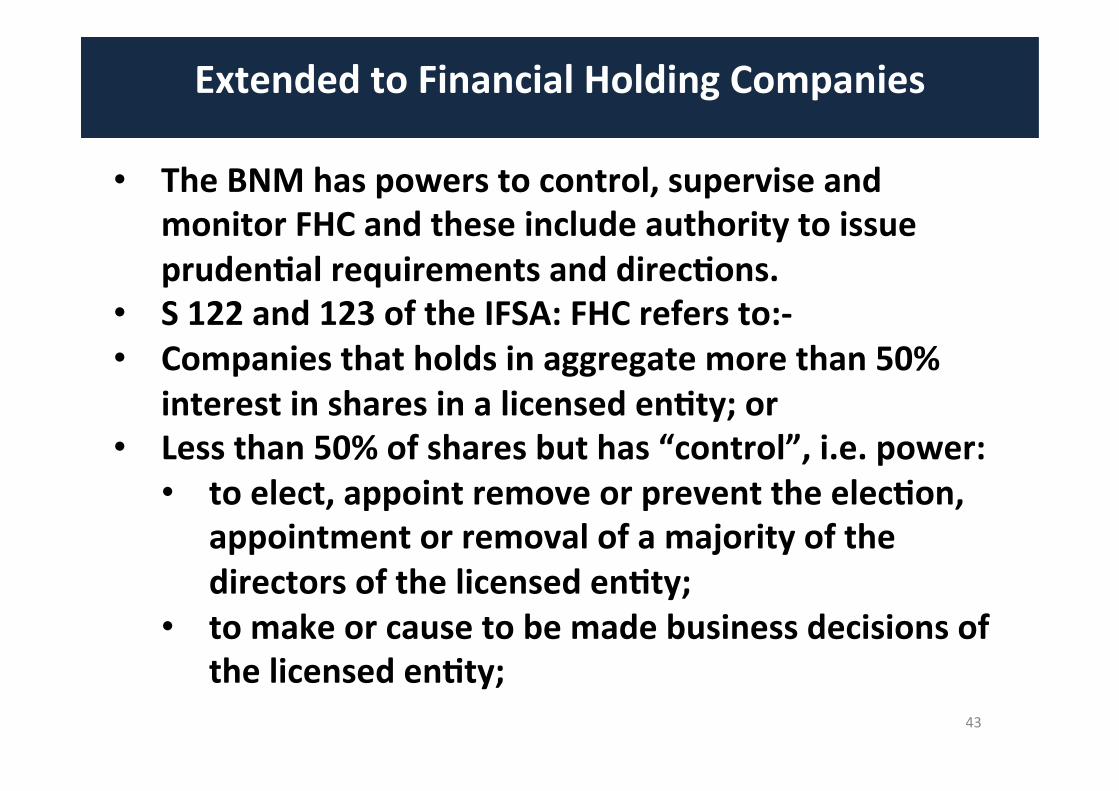

ExtendedtoFinancialHoldingCompanies

43

• TheBNMhaspowerstocontrol,superviseandmonitorFHCandtheseincludeauthoritytoissueprudenOalrequirementsanddirecOons.

• S122and123oftheIFSA:FHCrefersto:-• Companiesthatholdsinaggregatemorethan50%

interestinsharesinalicensedenOty;or• Lessthan50%ofsharesbuthas“control”,i.e.power:

• toelect,appointremoveorpreventtheelecOon,appointmentorremovalofamajorityofthedirectorsofthelicensedenOty;

• tomakeorcausetobemadebusinessdecisionsofthelicensedenOty;

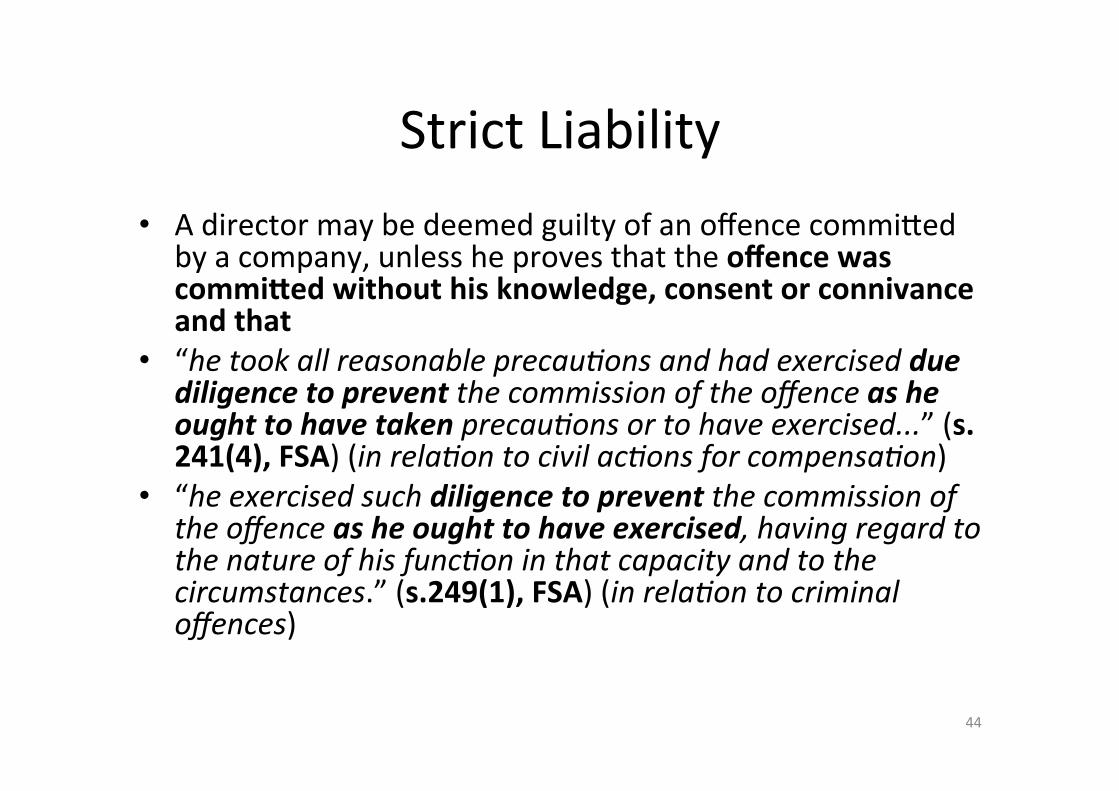

StrictLiability• AdirectormaybedeemedguiltyofanoffencecommiYed

byacompany,unlessheprovesthattheoffencewascommi^edwithouthisknowledge,consentorconnivanceandthat

• “hetookallreasonableprecau,onsandhadexercisedduediligencetopreventthecommissionoftheoffenceasheoughttohavetakenprecau,onsortohaveexercised...”(s.241(4),FSA)(inrela,ontocivilac,onsforcompensa,on)

• “heexercisedsuchdiligencetopreventthecommissionoftheoffenceasheoughttohaveexercised,havingregardtothenatureofhisfunc,oninthatcapacityandtothecircumstances.”(s.249(1),FSA)(inrela,ontocriminaloffences)

44

StrictLiabilityandDefense

45

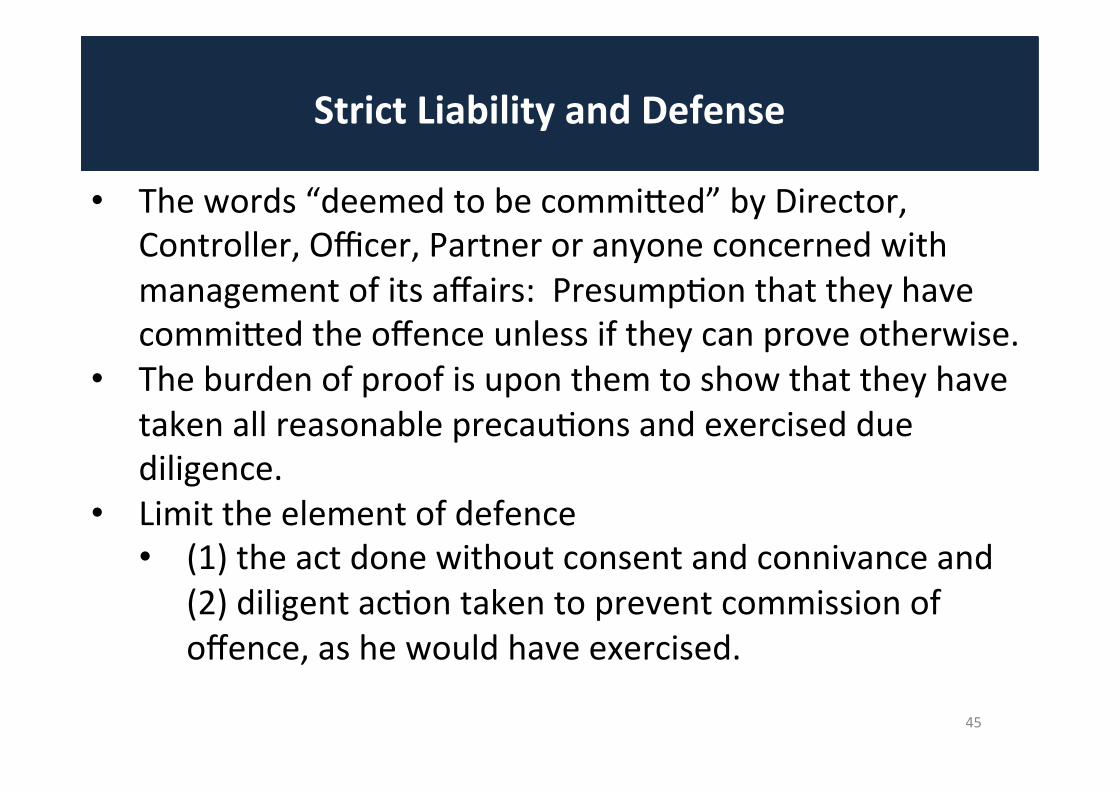

• Thewords“deemedtobecommiYed”byDirector,Controller,Officer,Partneroranyoneconcernedwithmanagementofitsaffairs:PresumpMonthattheyhavecommiYedtheoffenceunlessiftheycanproveotherwise.

• TheburdenofproofisuponthemtoshowthattheyhavetakenallreasonableprecauMonsandexercisedduediligence.

• Limittheelementofdefence• (1)theactdonewithoutconsentandconnivanceand

(2)diligentacMontakentopreventcommissionofoffence,ashewouldhaveexercised.

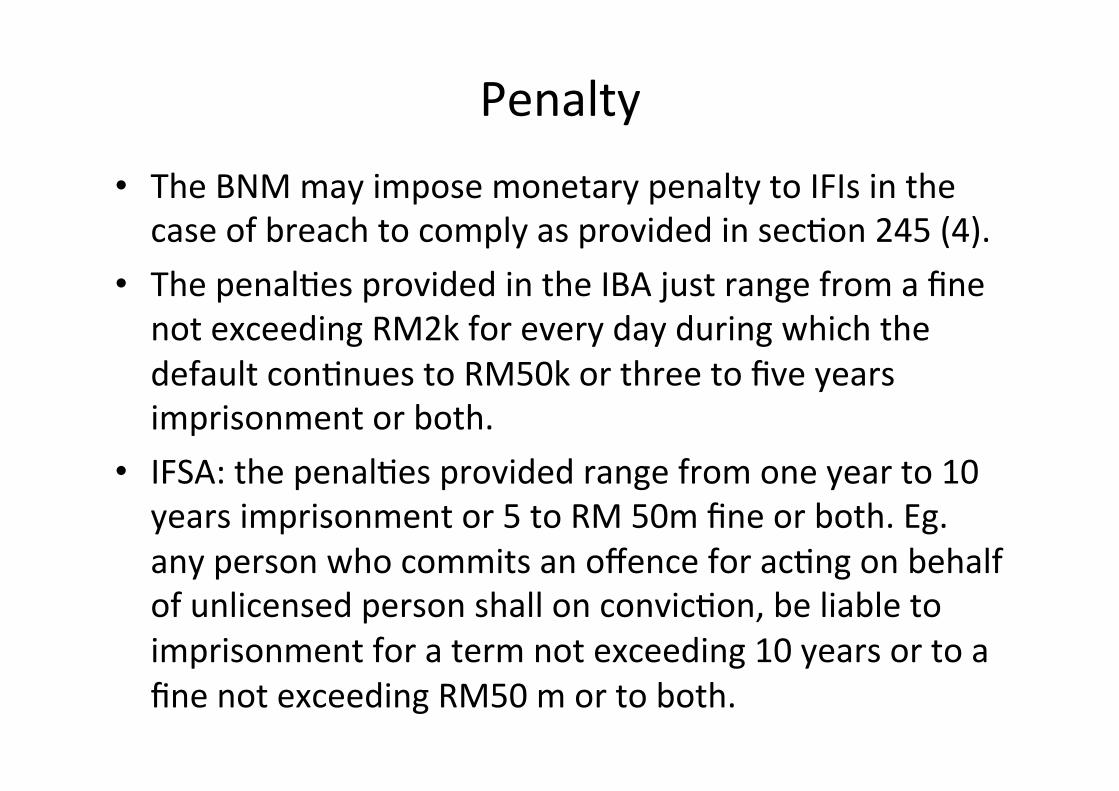

Penalty• TheBNMmayimposemonetarypenaltytoIFIsinthecaseofbreachtocomplyasprovidedinsecMon245(4).

• ThepenalMesprovidedintheIBAjustrangefromafinenotexceedingRM2kforeverydayduringwhichthedefaultconMnuestoRM50korthreetofiveyearsimprisonmentorboth.

• IFSA:thepenalMesprovidedrangefromoneyearto10yearsimprisonmentor5toRM50mfineorboth.Eg.anypersonwhocommitsanoffenceforacMngonbehalfofunlicensedpersonshallonconvicMon,beliabletoimprisonmentforatermnotexceeding10yearsortoafinenotexceedingRM50mortoboth.

PenalMes

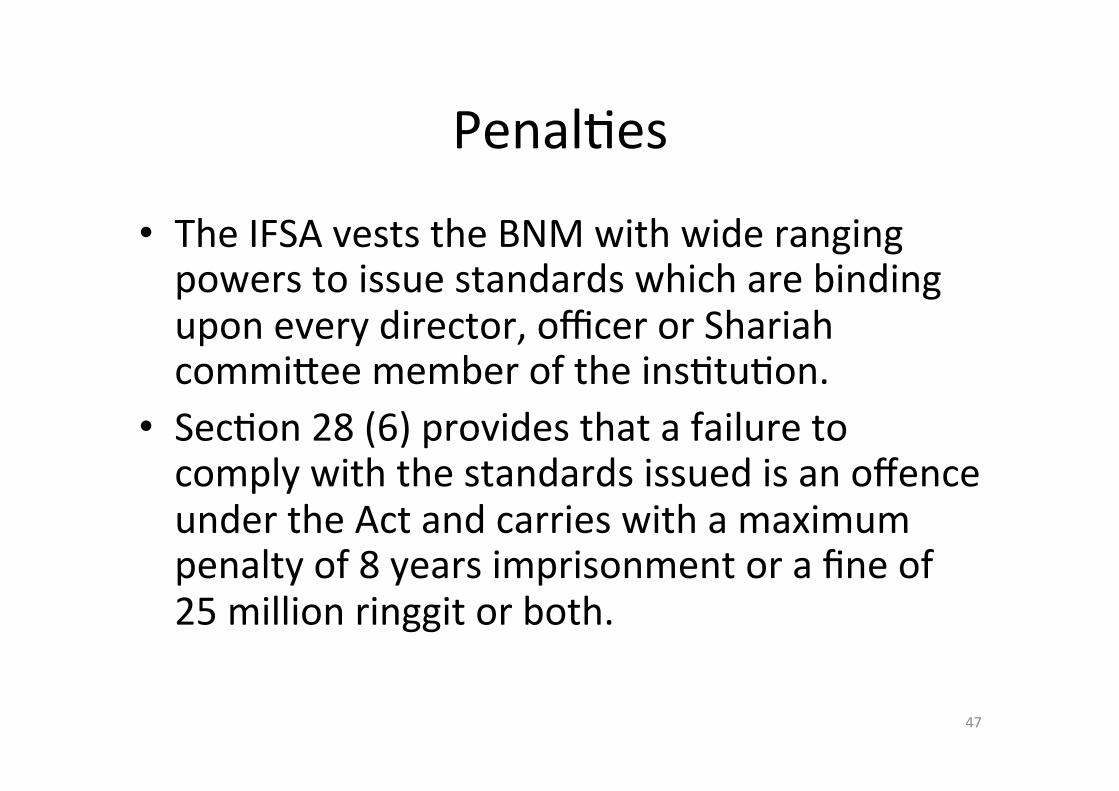

• TheIFSAveststheBNMwithwiderangingpowerstoissuestandardswhicharebindinguponeverydirector,officerorShariahcommiYeememberoftheinsMtuMon.

• SecMon28(6)providesthatafailuretocomplywiththestandardsissuedisanoffenceundertheActandcarrieswithamaximumpenaltyof8yearsimprisonmentorafineof25millionringgitorboth.

47

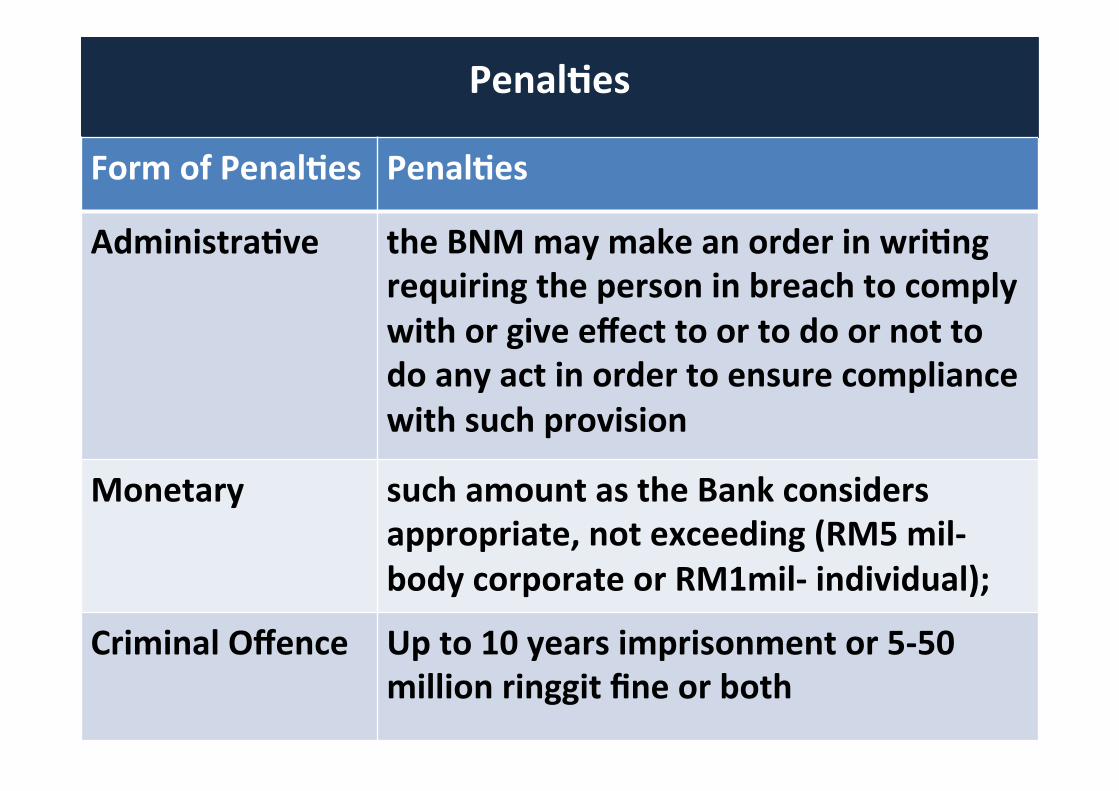

PenalOes

48

FormofPenalOes PenalOes

AdministraOve theBNMmaymakeanorderinwriOngrequiringthepersoninbreachtocomplywithorgiveeffecttoortodoornottodoanyactinordertoensurecompliancewithsuchprovision

Monetary suchamountastheBankconsidersappropriate,notexceeding(RM5mil-bodycorporateorRM1mil-individual);

CriminalOffence

Upto10yearsimprisonmentor5-50millionringgitfineorboth

49

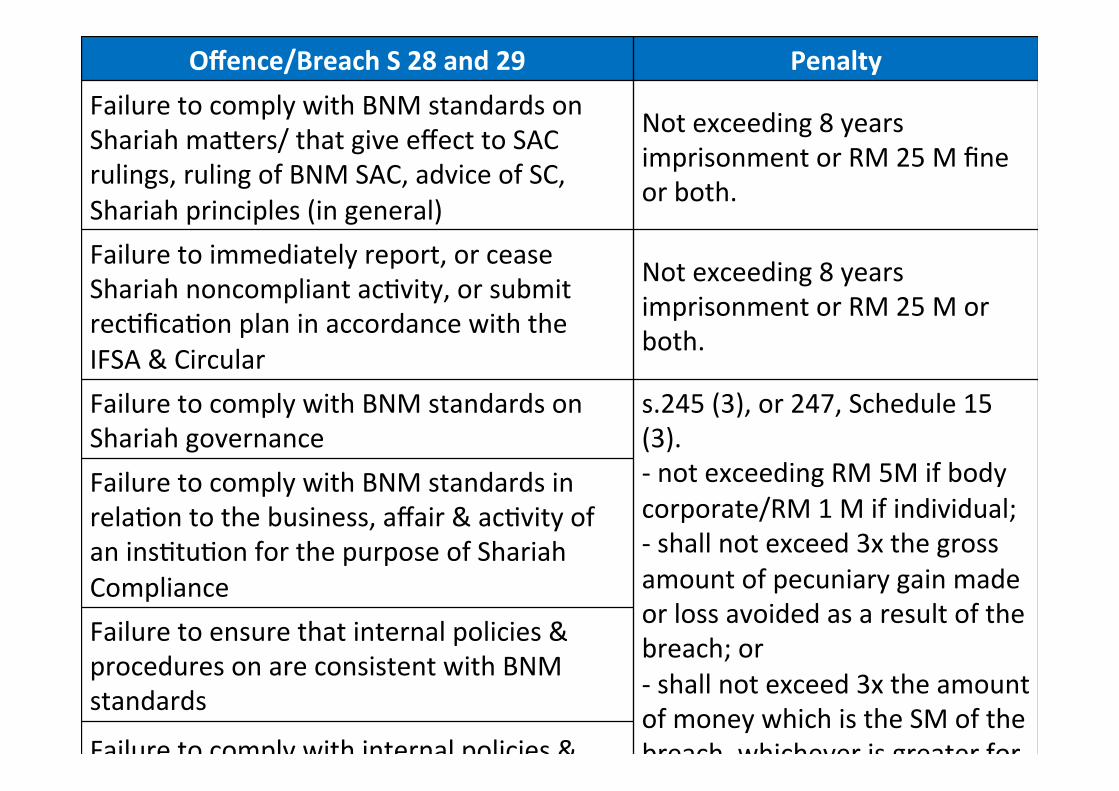

Offence/BreachS28and29 PenaltyFailuretocomplywithBNMstandardsonShariahmaYers/thatgiveeffecttoSACrulings,rulingofBNMSAC,adviceofSC,Shariahprinciples(ingeneral)

Notexceeding8yearsimprisonmentorRM25Mfineorboth.

Failuretoimmediatelyreport,orceaseShariahnoncompliantacMvity,orsubmitrecMficaMonplaninaccordancewiththeIFSA&Circular

Notexceeding8yearsimprisonmentorRM25Morboth.

FailuretocomplywithBNMstandardsonShariahgovernance

s.245(3),or247,Schedule15(3).-notexceedingRM5Mifbodycorporate/RM1Mifindividual;-shallnotexceed3xthegrossamountofpecuniarygainmadeorlossavoidedasaresultofthebreach;or-shallnotexceed3xtheamountofmoneywhichistheSMofthebreach,whicheverisgreaterforeachbreachorfailuretocomply.

FailuretocomplywithBNMstandardsinrelaMontothebusiness,affair&acMvityofaninsMtuMonforthepurposeofShariahComplianceFailuretoensurethatinternalpolicies&proceduresonareconsistentwithBNMstandards

Failuretocomplywithinternalpolicies&proceduresadoptedtoimplementBNMstandards

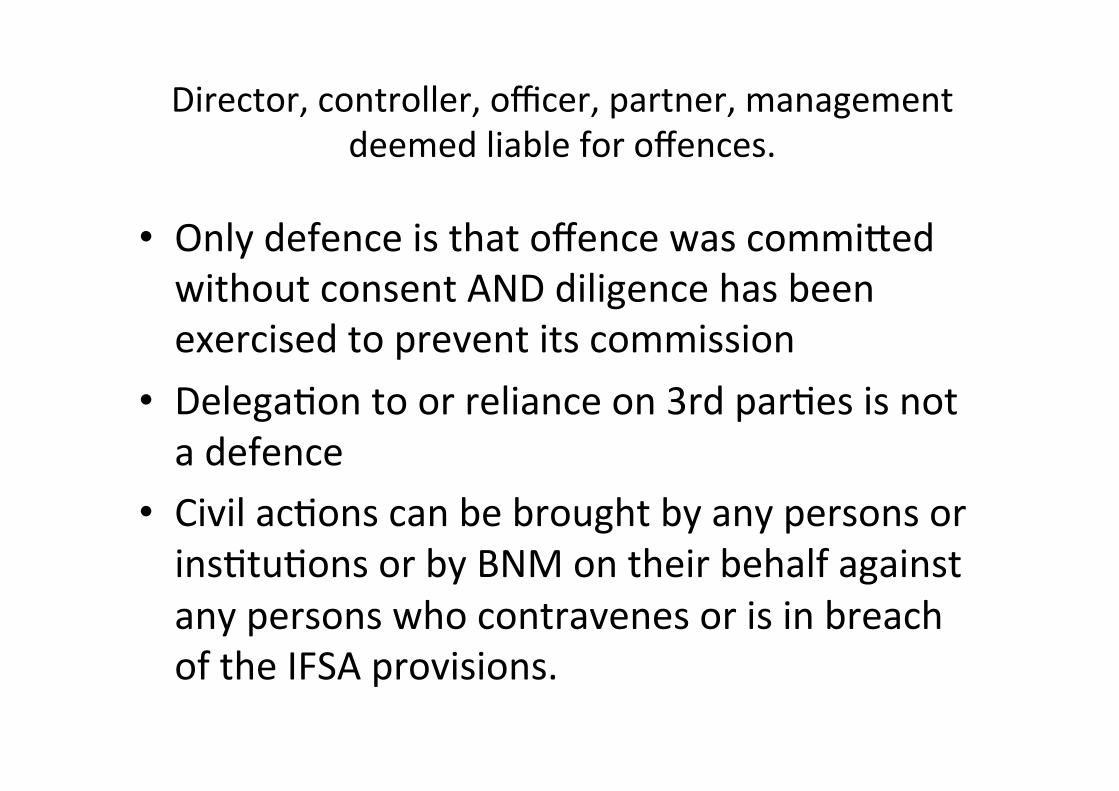

Director,controller,officer,partner,managementdeemedliableforoffences.

• OnlydefenceisthatoffencewascommiYedwithoutconsentANDdiligencehasbeenexercisedtopreventitscommission

• DelegaMontoorrelianceon3rdparMesisnotadefence

• CivilacMonscanbebroughtbyanypersonsorinsMtuMonsorbyBNMontheirbehalfagainstanypersonswhocontravenesorisinbreachoftheIFSAprovisions.

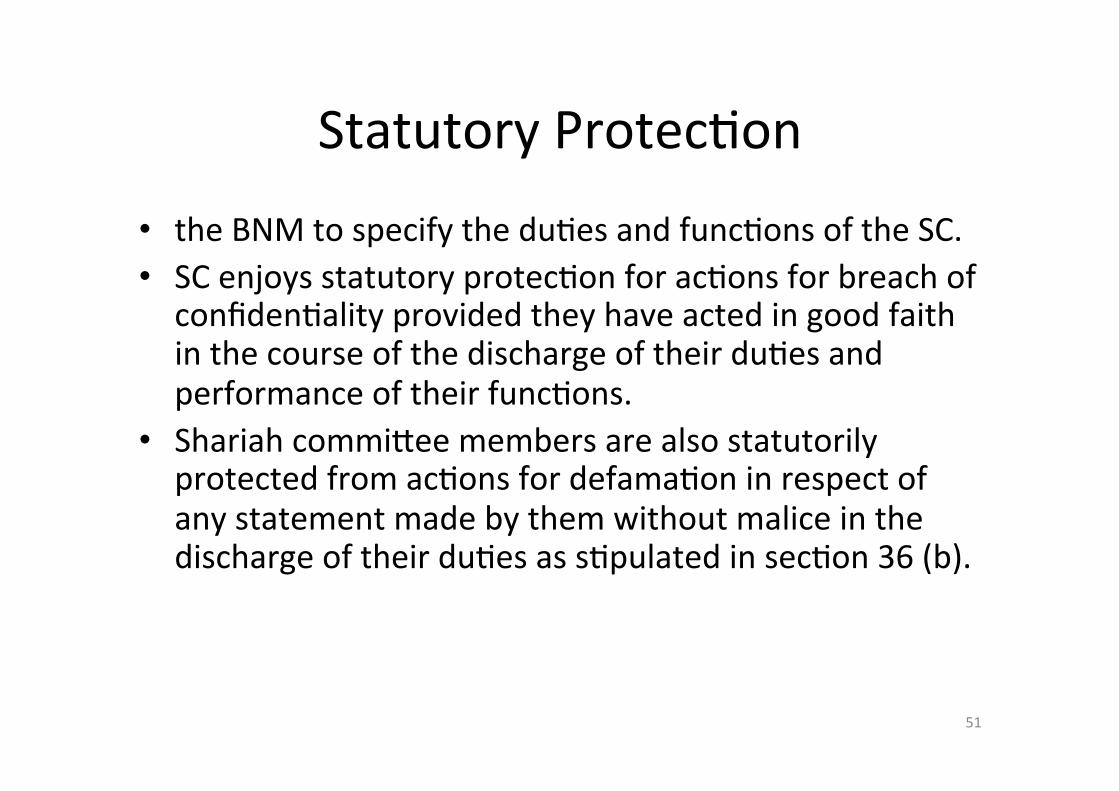

StatutoryProtecMon

• theBNMtospecifytheduMesandfuncMonsoftheSC.• SCenjoysstatutoryprotecMonforacMonsforbreachofconfidenMalityprovidedtheyhaveactedingoodfaithinthecourseofthedischargeoftheirduMesandperformanceoftheirfuncMons.

• ShariahcommiYeemembersarealsostatutorilyprotectedfromacMonsfordefamaMoninrespectofanystatementmadebythemwithoutmaliceinthedischargeoftheirduMesassMpulatedinsecMon36(b).

51

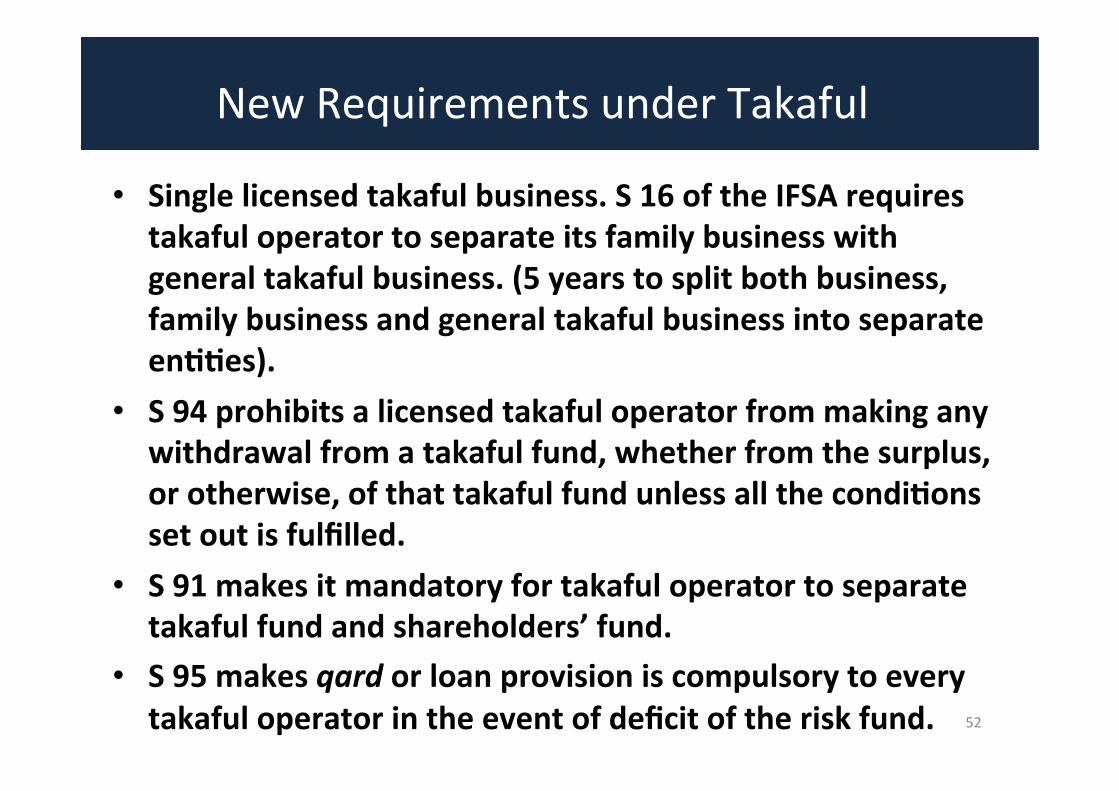

• Singlelicensedtakafulbusiness.S16oftheIFSArequirestakafuloperatortoseparateitsfamilybusinesswithgeneraltakafulbusiness.(5yearstosplitbothbusiness,familybusinessandgeneraltakafulbusinessintoseparateenOOes).

• S94prohibitsalicensedtakafuloperatorfrommakinganywithdrawalfromatakafulfund,whetherfromthesurplus,orotherwise,ofthattakafulfundunlessallthecondiOonssetoutisfulfilled.

• S91makesitmandatoryfortakafuloperatortoseparatetakafulfundandshareholders’fund.

• S95makesqardorloanprovisioniscompulsorytoeverytakafuloperatorintheeventofdeficitoftheriskfund. 52

NewRequirementsunderTakaful

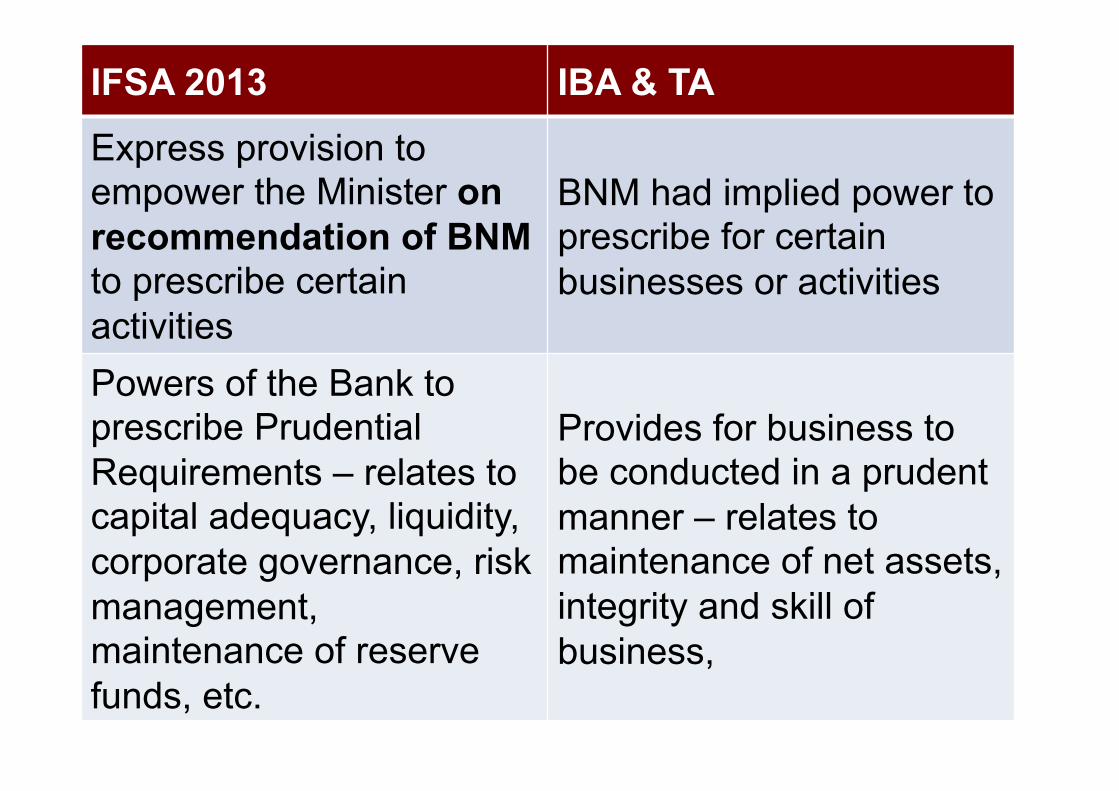

IFSA 2013 IBA & TA

Express provision to empower the Minister on recommendation of BNM to prescribe certain activities

BNM had implied power to prescribe for certain businesses or activities

Powers of the Bank to prescribe Prudential Requirements – relates to capital adequacy, liquidity, corporate governance, risk management, maintenance of reserve funds, etc.

Provides for business to be conducted in a prudent manner – relates to maintenance of net assets, integrity and skill of business,

IFSA 2013 IBA & TA

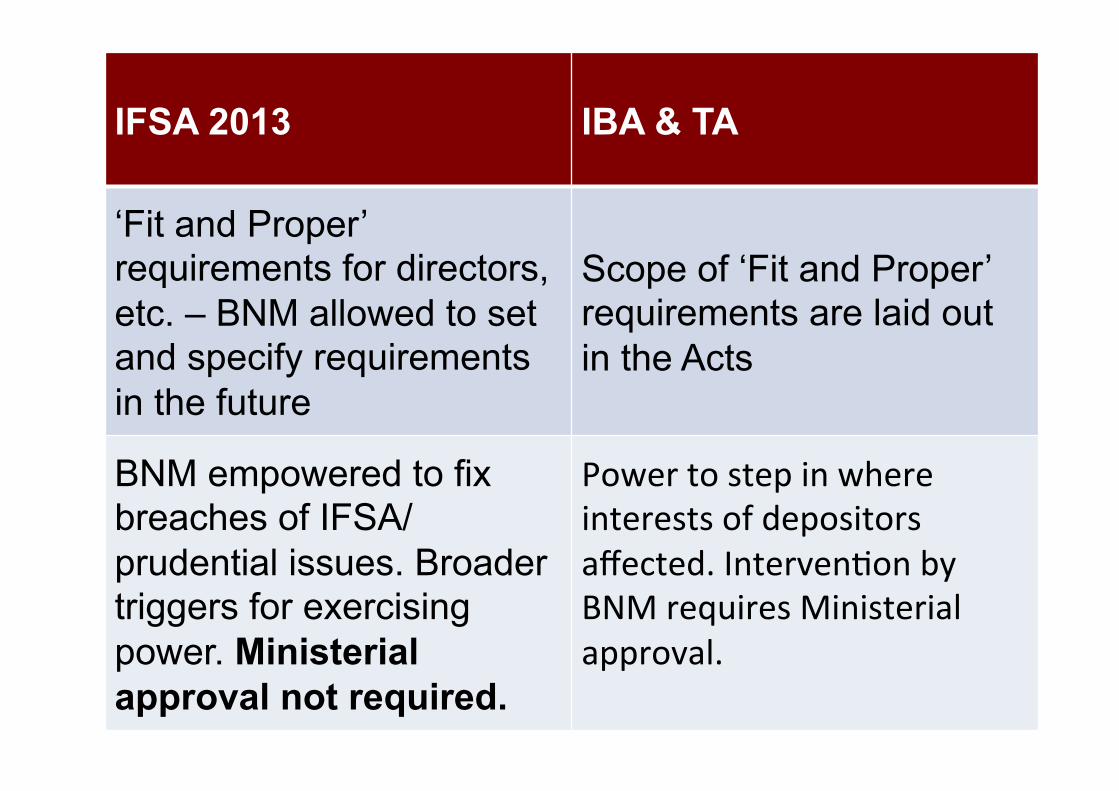

‘Fit and Proper’ requirements for directors, etc. – BNM allowed to set and specify requirements in the future

Scope of ‘Fit and Proper’ requirements are laid out in the Acts

BNM empowered to fix breaches of IFSA/ prudential issues. Broader triggers for exercising power. Ministerial approval not required.

Powertostepinwhereinterestsofdepositorsaffected.IntervenMonbyBNMrequiresMinisterialapproval.

IFSA 2013 IBA & TA

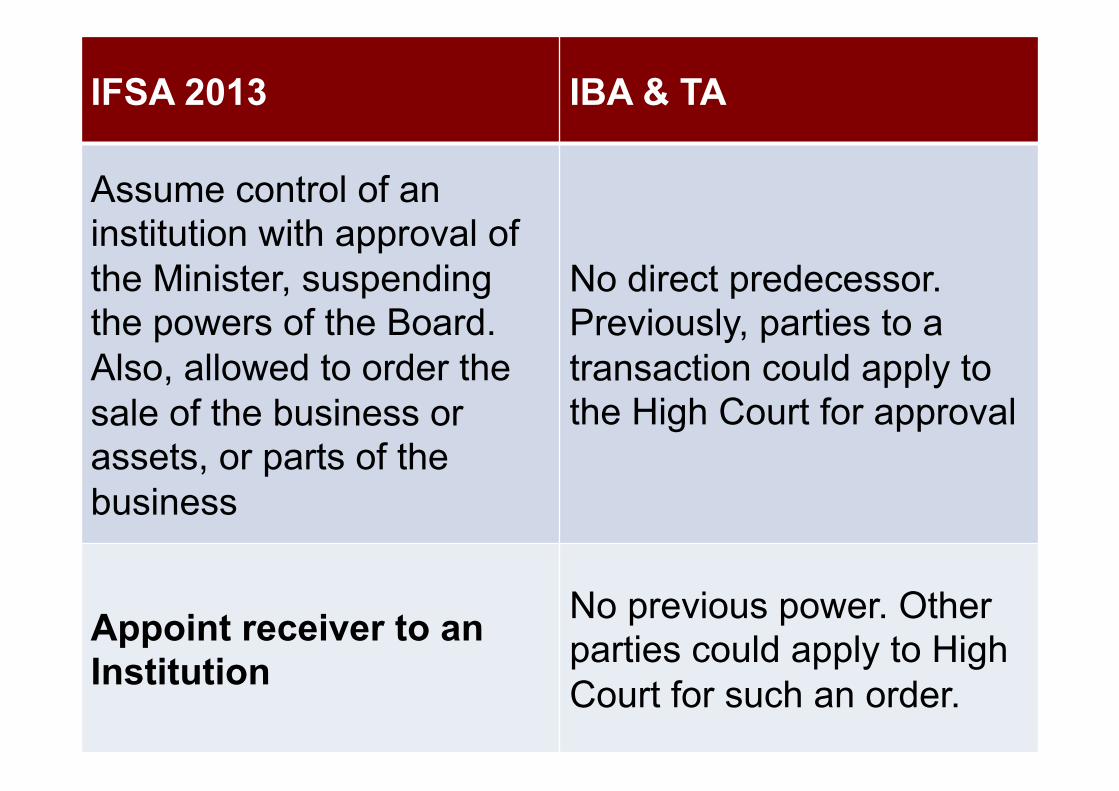

Assume control of an institution with approval of the Minister, suspending the powers of the Board. Also, allowed to order the sale of the business or assets, or parts of the business

No direct predecessor. Previously, parties to a transaction could apply to the High Court for approval

Appoint receiver to an Institution

No previous power. Other parties could apply to High Court for such an order.

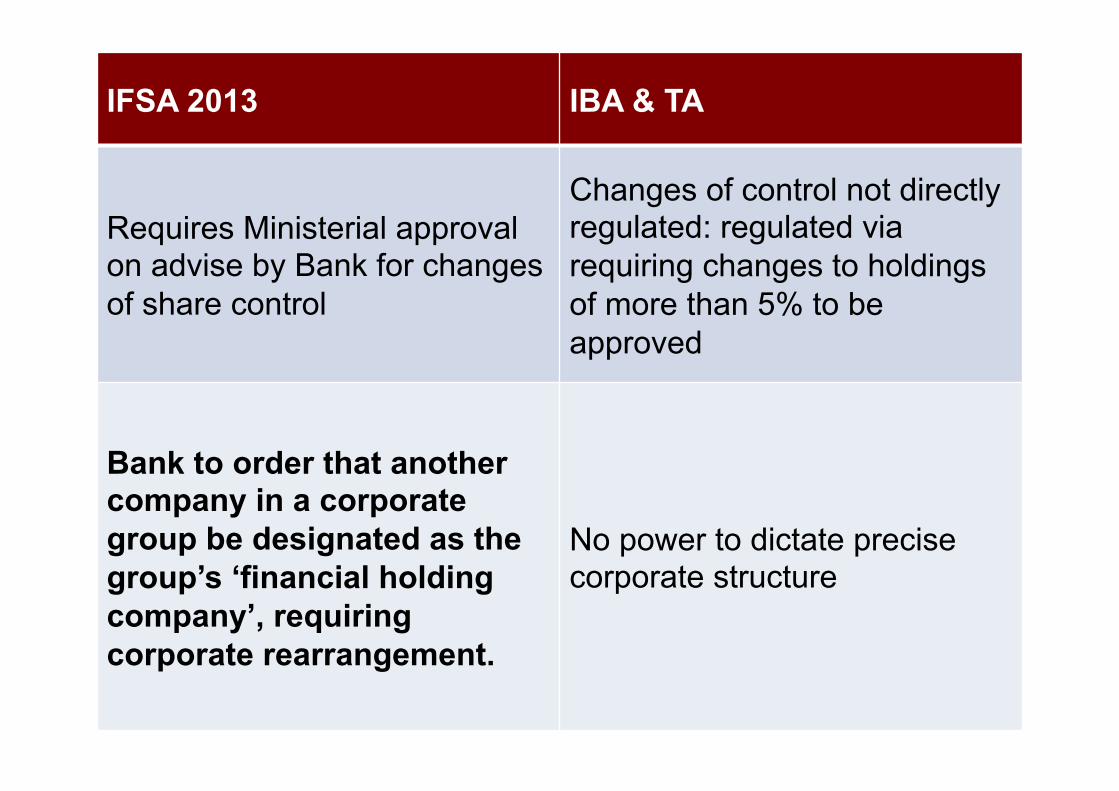

IFSA 2013 IBA & TA

Requires Ministerial approval on advise by Bank for changes of share control

Changes of control not directly regulated: regulated via requiring changes to holdings of more than 5% to be approved

Bank to order that another company in a corporate group be designated as the group’s ‘financial holding company’, requiring corporate rearrangement.

No power to dictate precise corporate structure

IMPLICATIONS,ISSUESANDCHALLENGES

57

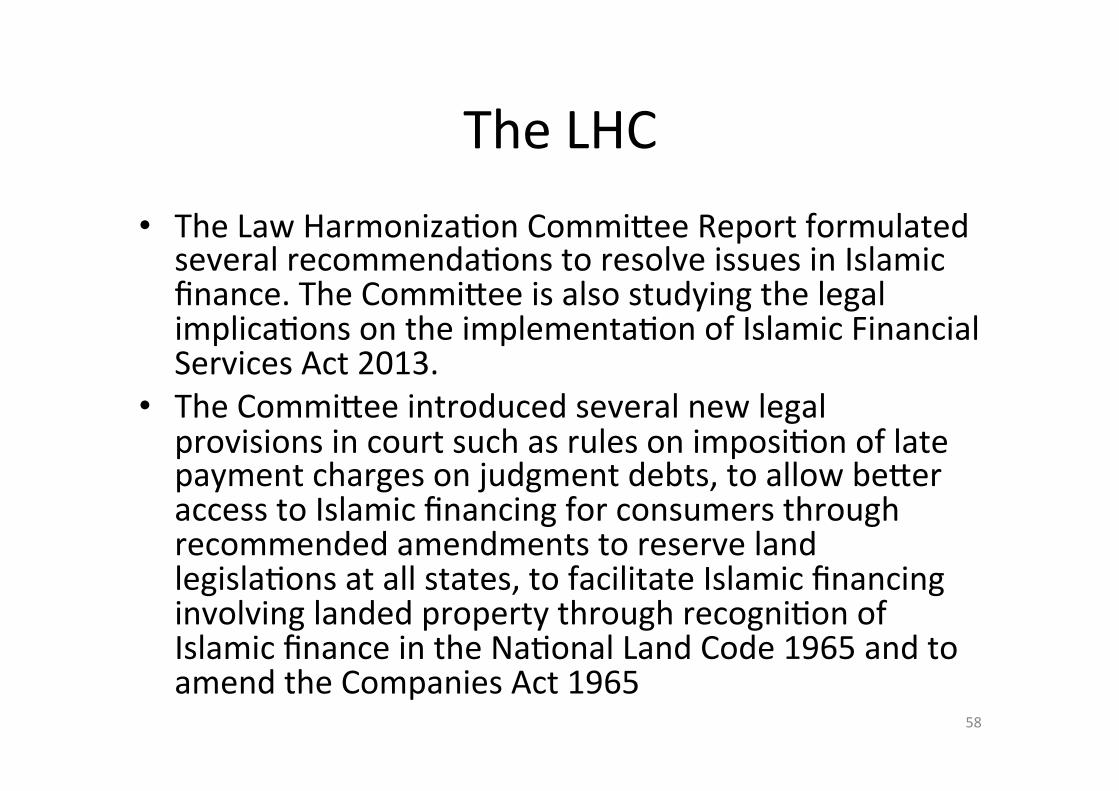

TheLHC• TheLawHarmonizaMonCommiYeeReportformulatedseveralrecommendaMonstoresolveissuesinIslamicfinance.TheCommiYeeisalsostudyingthelegalimplicaMonsontheimplementaMonofIslamicFinancialServicesAct2013.

• TheCommiYeeintroducedseveralnewlegalprovisionsincourtsuchasrulesonimposiMonoflatepaymentchargesonjudgmentdebts,toallowbeYeraccesstoIslamicfinancingforconsumersthroughrecommendedamendmentstoreservelandlegislaMonsatallstates,tofacilitateIslamicfinancinginvolvinglandedpropertythroughrecogniMonofIslamicfinanceintheNaMonalLandCode1965andtoamendtheCompaniesAct1965

58

ShariahNon-ComplianceFramework

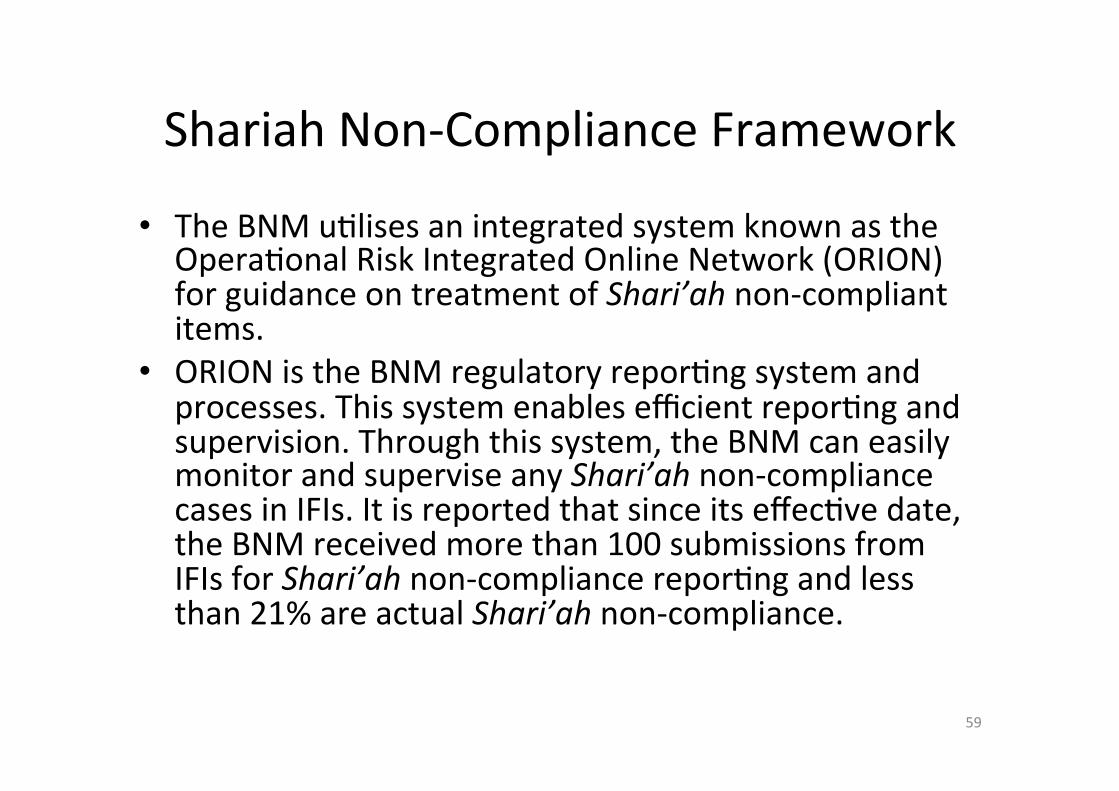

• TheBNMuMlisesanintegratedsystemknownastheOperaMonalRiskIntegratedOnlineNetwork(ORION)forguidanceontreatmentofShari’ahnon-compliantitems.

• ORIONistheBNMregulatoryreporMngsystemandprocesses.ThissystemenablesefficientreporMngandsupervision.Throughthissystem,theBNMcaneasilymonitorandsuperviseanyShari’ahnon-compliancecasesinIFIs.ItisreportedthatsinceitseffecMvedate,theBNMreceivedmorethan100submissionsfromIFIsforShari’ahnon-compliancereporMngandlessthan21%areactualShari’ahnon-compliance.

59

ProfessionalIndemnityInsurance

• theIFSAmakesShari’ahscholarslegallyaccountableandliablefortheirduMesasanyShari’ahcommiYeemembersmaybejailedforuptoeightyearsorfineduptoRM25millionwhichisequivalentofapproximatelyUSD7.6millioniftheyfailtocomplywiththeIFSA.

• ThisseriouslegalimplicaMontriggerstheneedofhavingprofessionalindemnityIslamicinsuranceforShari’ahscholarsasinthecaseofadvocateandsolicitorormedicalpracMMoners.

60

ReclassificaMonofDeposit• 30thJune2015wasthedeadlineforIFIstoclearlyseparatebetweenthedepositsaccountandinvestmentaccount.

• IFIsmustintroduceanewstructureofmudharabahinvestmentaccount,whichreflecttheactualcharacterisMcsofinvestment.

• Islamicdepositasprincipalguaranteedandinvestmentasnon-principalguaranteed.Thedepositinsuranceortakafulalsowillbenolongerrelevantforinvestment-typeofaccounts.

• ThereclassificaMonofdepositsisnotfavourabletoIFIs.ThereclassificaMonofdepositsimposesagreatchallengetoIFIstoaccumulatedeposits,whicharebasedonmudharabahprinciple.

61

InvestmentAccountPlaxorm• TheIFSArequirementontheseparaMonofIslamicdepositandinvestmentaccountisactuallytoallowthebankstocustomisetheirproductsaccordingtothecustomers'profileandriskappeMte.

• IFIsarenowcanofferhigherreturnstoanyinvestorsfortheirinvestmentaccount.

• TofacilitatethistransiMonperiod,theMalaysiangovernmentbackedtheIAPwithaniniMalstart-upfundforRM150millionandtaxexempMonfor3consecuMveyears.LembagaTabungHajialsoallocatedRM200millionfortheestablishmentoftheShari’ahcompliantRestrictedInvestmentAccount.

• TherearefourIFIshaveparMcipatedintheIAPnamelyBIMB,MaybankIslamic,AffinIslamicandBMMB.

62

• TheBNMhasmorepowertodictate-IFIsandanditsholdingcompanyandtheseincludeitsCapitalRequirements,CorporateGovernance,ConsumerProtecMon,Shareholding,IntervenMonandevenShari’ahcompliance.

• PowernotonlytoadvisebutalsotorecommendthedecisionmadebytheMinister.

• TheremustbecertainlegalmechanismtolimitandrestrictsuchauthoriMesandtofindthebestavenuetoreviewandoverseetheBNM’sacMon.

63

JudicialOversightovertheBNM

• TheBODofaninsMtuMonshallhaveregardtotheinterestsofdepositors,IAHandtakafulparMcipants.

• TheIFSAseemstopromotestakeholdersvaluebasedapproachinIslamicfinancialinsMtuMonsratherthantheshareholdersvaluemodel.

• PotenMalconflictofinterestbetweenshareholdersandotherstakeholders.

64

PotenOalConflictofInterestBetweenShareholdersandOtherStakeholders

• TheelementofstrictliabilityintheIFSAwillexposeIFIswithfurthercostandexpenses.

• VigorousShari’ahcompliancerequirementswillalsoincreasethecostofbusinessandfinallywillaffectthelevelofefficiency.

• SinceprecauMonsandduediligencehavetobeexercisedtopreventthecommissionoftheoffence,anymeasurestomiMgatethislegalriskwillcostaddiMonalexpenses.Eg.ProfessionalIndemnityInsurance.

65

Cost and Efficiency

• Heavyregulatedbusinessenvironment-maynegateinnovaMon/lackofinnovaMon/influencethemarketbehaviorandtheplayerswilloptforproductsoflesserconstrains.

• Eg.AllcontractsunderwakalahandmudharabaharedeemedasinvestmentproductsandhencerequireaddiMonaltreatment:DocumentaMon,operaMon,systemandetc.

• Effect:ConcentraMngondebt-basedproductsandconsistentlyneglecMngtheequity-basedproductsbothfromassetandliabiliMessides. 66

InnovaOonofProductandServices

CONCLUSION

67

• Exerciseextracare&vigilanceonShariahcompliancema^ersthrougheffecOveinternalShariahcompliancefuncOons:FullinformaOononproducts&transacOons;pre-and-postapprovalmonitoring,supervisingconductofShariahreview&Shariahauditreports;monitoringrecOficaOonmeasures.

• Examineinternalgapstoa^ain“end-to-end”Shariahcompliance;

• ExamineShariahreview&auditreports&implementrecOficaOonplans;

• Assessandadhereinternalpolicies&proceduresandalsoBNMstandards;

68

Recommendations

• TheIFSAprovidesaframeworktofacilitatethecreaOonandopOmizeahealthyandviableenvironmentforIslamicfinancesysteminMalaysia.

• DespiteposiOvefeaturesoftheIFSA,thereareloopholes,issuesandshortcomingsthatmaynegateitsobjecOves.

• ThesefactorsfinallymayleadtolackofappeOteforproductinnovaOononthepartofIFIs.

• Consideringthesegreatchallenges,itisrecommendedfortheBNMandtheindustrystakeholderstoreviewanddiscussseriouslytheimplicaOonsandconsequencesoftheIFSA.

• YearsaheadwillbearealtestfortruepotenOalofIslamicfinanceinMalaysia. 69

Concluding Remarks

THANK YOU

![[XLS]xa.yimg.comxa.yimg.com/kq/groups/24779538/2009471176/name/SKUSES... · Web viewNOR SHAHIRAH BINTI ZULKIFLI 990605146244 ZULKIFLI BIN HASAN BASRI 0142256692 YASMAINI BINTI SYUIB](https://img.pdfslide.net/doc/110x75/5ae41dce7f8b9a0d7d8e9008/xlsxayimgcomxayimgcomkqgroups247795382009471176nameskusesweb-viewnor.jpg)