© K.Cuthbertson and D.Nitzsche

LECTURE

RISK GRADES™ : J.P Morgan

Version 1/9/2001

FINANCIAL ENGINEERING:DERIVATIVES AND RISK MANAGEMENT(J. Wiley, 2001)

K. Cuthbertson and D. Nitzsche

© K.Cuthbertson and D.Nitzsche

Data on Returns and Volatility

RiskGrades™ (J.P. Morgan)

Risk Grades for Various Portfolios

Topics

© K.Cuthbertson and D.Nitzsche

Data on Returns and Volatility

© K.Cuthbertson and D.Nitzsche

HOW RISKY ARE STOCKS?

US - STOCK RETURNS: LONG TERM (1929-54)

June 22nd, 1929 $10,000

Sept 3rd, 1929 $12,417 (+25%)

Oct 29th, 1929 $ 7,495

July 1932 $ 1,342 (-86%)

1954 $10,000

© K.Cuthbertson and D.Nitzsche

Jan 1973 $10,000

Dec 1974 $ 6,600 (-34%)

1983 $10,000

US - STOCK RETURNS: LONG TERM (1973-83)

© K.Cuthbertson and D.Nitzsche

Jan 1988 $10,000

Dec 1989 $18,342

July 1992 $ 6,708 (-33%)

Jan 2000 <$10,000

JAPAN - STOCK RETURNS: (1988-2000)

© K.Cuthbertson and D.Nitzsche

Mean S.D.

Large US stocks 1.029 5.7%

(per month) (per month)

Normality

Only 1% of the time should monthly stock return fall below

1.029 - 2.33(5.7%) = -12.25%

1929-97 = 828 months

How many returns more negative than -12.25%?

Normality = 8.3 Actual = 16 !

Never, trust the ‘normal’ !

US STOCKS: SHORT TERM (Monthly 1926-97)

© K.Cuthbertson and D.Nitzsche

RiskGrades™ (J.P. Morgan)

© K.Cuthbertson and D.Nitzsche

A ‘simplified’ method of calculating the changing risk (usually daily) of a portfolio of assets, for use by individual investors and ‘small’ financial institutions.

Measures change in risk in a transparent and simple way

The returns on the portfolio are ignored (in large part)

Concepts based on elementary portfolio theory

RiskGrades measures volatility ( ) as the S.D. of a portfolio of assets. is usually measured as an EWMA of past squared (daily) returns ( rt = ln(Pt/Pt-1) ) - using = 0.97 and about 150 days/values for r t

RiskGrades™ : What is it ?

© K.Cuthbertson and D.Nitzsche

1) “Portfolio Risk Grade” Risk of portfolio (relative to 20% risk of a ‘world’ benchmark)

2) Undiversified Risk Grade ~ worse case outcome

3) Diversification Benefit = (2) - (1)

4) Marginal Risk Impact = increase in risk as you add (or subtract) one or more assets from your portfolio

Statistics Used

© K.Cuthbertson and D.Nitzsche

i is the DAILY standard deviationbase is fixed at 20% per annum(=av. for international stocks)

Hence RG is just a “scaled” standard deviation

e.g. If RG = 100% then asset has 20% p.a. ‘absolute’ risk

e.g. If RG1 = 100 and RG2 = 400 then asset-2 currently has 4 times the risk of asset-1

10020.0252

100252

xixbasei

iRG

RiskGrades™ (single asset)

© K.Cuthbertson and D.Nitzsche

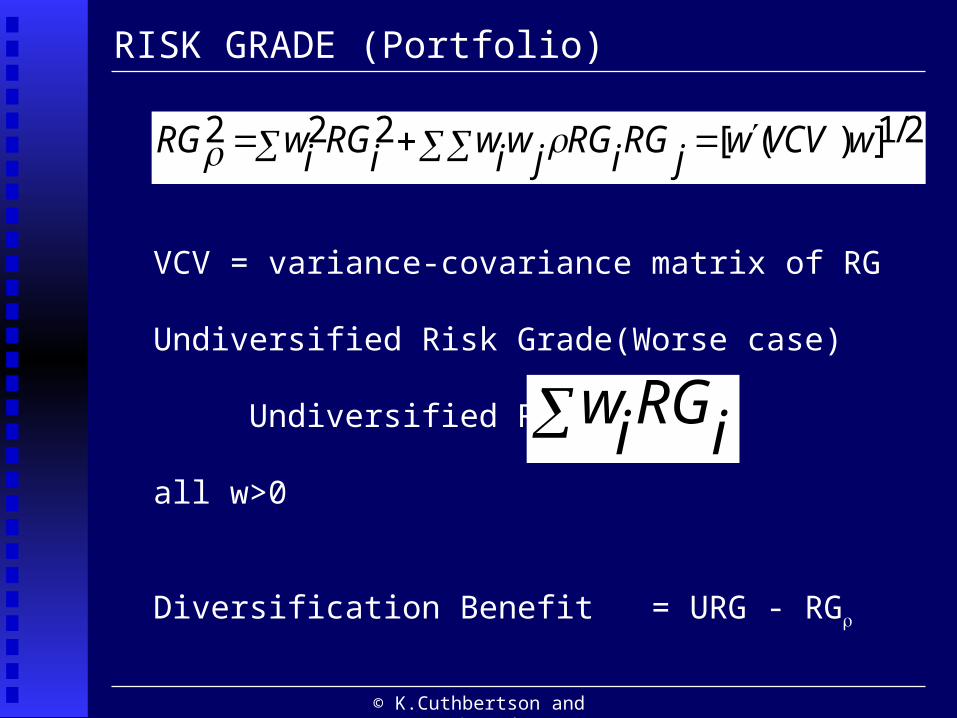

VCV = variance-covariance matrix of RG

Undiversified Risk Grade(Worse case)

Undiversified RG =

all w>0

Diversification Benefit = URG - RG

iRGiw

2/1])([222 wVCVwjRGiRGjwiwiRGiwRG

RISK GRADE (Portfolio)

© K.Cuthbertson and D.Nitzsche

$RI = RGp(n) - RGp

(n-j)

= risk grade whole portfolio – risk grade excluding one (or more) assets

Funds released are held in cash (zero risk/correlation)

%Percent Risk Impact of omitted asset – j

% RI =

Can RI ever increase as you ‘drop’ an asset ?

100)(

$ xnpRG

RI 100$ xportfoliowholeofRiskGrade

jassetofimpactRisk

$ RISK IMPACT of omitted asset (= j)

© K.Cuthbertson and D.Nitzsche

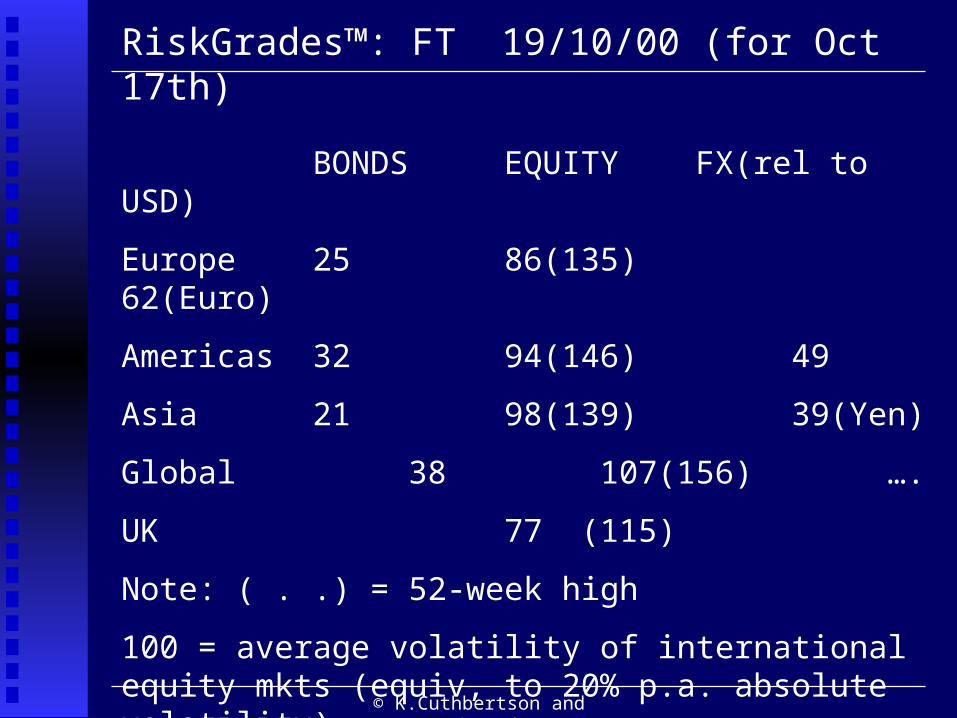

RiskGrades™: FT 19/10/00 (for Oct 17th)

BONDS EQUITY FX(rel to USD)

Europe 25 86(135) 62(Euro)

Americas 32 94(146) 49

Asia 21 98(139) 39(Yen)

Global 38 107(156) ….

UK 77 (115)

Note: ( . .) = 52-week high

100 = average volatility of international equity mkts (equiv, to 20% p.a. absolute volatility).

© K.Cuthbertson and D.Nitzsche

An Example ($10,000 in each of 2 assets)

Weights Risk Grade %R.I.

Coca-Cola ½ 188 28

Cisco ½ 179 25

Portfolio 125

Diversification 58.5

The Risk Grade for various stock indices are now published daily in the Financial Times.

Risk Measures

© K.Cuthbertson and D.Nitzsche

1) Cola’s RG is ‘9’ more than Cisco’s RG - what does this mean?

2) What is the ‘Undiversified RG’ and the ‘Diversification (RG) effect ?

Class Exercise: Interpretation of the Figures

© K.Cuthbertson and D.Nitzsche

3)How do we get the figure of 28% for the Percentage Risk Impact of Cola and what does this 28% mean?

Hint: Note that when you remove Cola, then these funds are held in cash(with zero risk) and you continue to hold only Cisco.

Class Exercise: ‘Risk Impact and %R.I.’

© K.Cuthbertson and D.Nitzsche

Pt = DPV (yt C, M, n)

Use historic(daily) yt to calculate ‘simulated’ Pt .(n, C and M are ‘fixed’ by the bond you hold)

Capital gain = ln(Pt/Pt-1)

“Return” = CG + yt/252

Calculate S.D. of ‘Return’(I.e EWMA using 150 days past data)

Illustrative RG for Government Bonds (different maturities)

RG (¼, ½, 1, 10, 30yr) = 1, 2, 3, 26, 43 respectivelyWhat does RG=43 for 30 year bond mean? What is it so much larger than RG=3 for 1-yr bond?

RiskGrades for Bonds

© K.Cuthbertson and D.Nitzsche

Black-Scholes Formula

Ct = BS(St, rt, , T, Div)

Use historic values of 1st , 2 variables. Construct artificial data series for Ct (with , T, Div fixed):

“Return” = ln(Ct/Ct+1)

Calculate S.D. of Return

Are there any dangers in this method ?Can it be applied to all options ?

Risk Grade for Bonds

© K.Cuthbertson and D.Nitzsche

Risk Grades for Various Portfolios

© K.Cuthbertson and D.Nitzsche

Price/Value R. Grade R. Impact %

Cisco 107.125 179 71

Call 18.125 665 29

Div.Ben 22

Portfolio 125.25 227

What is the ‘undiversified RG’ and why is the ‘Div Benefit’ rather low at ‘22’?Intuitively, why is the RG of the call relatively high at ‘665’?(Hint: assume it’s ‘delta’ is say 0.5) - tricky!

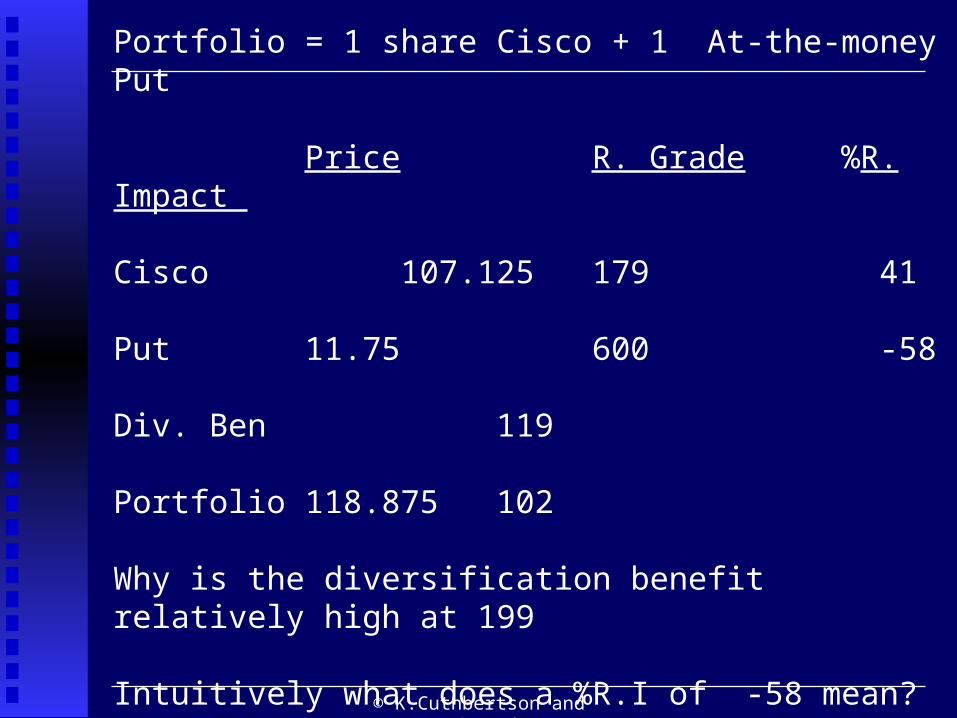

Portfolio = 1 share Cisco +1 At-the-money call on Cisco

© K.Cuthbertson and D.Nitzsche

Price R. Grade %R. Impact

Cisco 107.125 179 41

Put 11.75 600 -58

Div. Ben 119

Portfolio 118.875 102

Why is the diversification benefit relatively high at 199

Intuitively what does a %R.I of -58 mean?

Portfolio = 1 share Cisco + 1 At-the-money Put

© K.Cuthbertson and D.Nitzsche

a) $10,000 in Cola - all own fundsb) $10,000 in Cola, $5000 borrowed funds(ignore interest cost)

a) $’s Risk Grade %R.I.Cola 10,000 188 100Cash 0 0 :Div. Benefit 0 : :‘Portfolio’ 10,000 188 :

b) $’s Risk Grade %R.I.Cola 10,000 188 100Cash -5,000 0 0Div. Benefit : 0 :‘Portfolio’ 5,000 376 :

Intuitively, why has RG of ‘portfolio’ increased to 376. Is there an obvious formula in this simple case?

RiskGrades with purchases ‘on margin’(=Leverage)

© K.Cuthbertson and D.Nitzsche

Intuitively, why is RG=376 relatively high?

Intuitively, why is there a ‘R.I.’ for ‘cash’ whereas there wasno such effect for purchases ‘on margin’ ?

RiskGrades with purchases financed from ‘short sales’

© K.Cuthbertson and D.Nitzsche

a) $10,000 in Cola - all own fundsb) $10,000 in Cola using $5000 funds obtained from short selling Cisco (ignore any ‘haircuts’)

a) $’s Risk Grade %R.I.Cola 10,000 188 100Cash 0 : :Div. Benefit 0 : :‘Portfolio’ 10,000 188 :

b) $’s Risk Grade %R.I.Cola 10,000 188 58Cash -5,000 179 12Div. Benefit : 127 :‘Portfolio’ 5,000 376 :

RiskGrades: purchases financed from ‘short sales’

© K.Cuthbertson and D.Nitzsche

END OF LECTURE

© K.Cuthbertson and D.Nitzsche

1) RG (Cola) – RG(Cisco) = 188-179 = 9 [i.e. Cola is 1.8%p.a. (= 9 x 20%/100) more volatile than Cisco in absolute terms].

2) Undiversified RG = (½)(188)+(½)179 = 183.5

Hence: Diversification effect = 183.5-125 = 58.5

3)Risk Impact of Cola(extreme case of only 2 assets)

%RI(Cola)=

Note that ‘179’ is Cisco’s risk grade.Note (½) in Cisco and ½ is held in cash (with zero risk).

%28)100(125

5.35100125

)2/02/179(125 x

Interpretation of Figures (see above slides)

© K.Cuthbertson and D.Nitzsche

Removing Cola from the portfolio would reduce RG by 35.5 which is equivalent to 7% of the annual S.D. (= 35.5 x 0.20)

Removing Cola from the portfolio would reduce the risk grade in percentage terms by 28% (I.e. compared with the RG of the initial 2-asset portfolio)

This 28% reduction in risk is primarily due to the fact that in the initial 2-asset portfolio you hold 2 x $10,000 in risky assets

while after removing Cola

you only hold $10,000 in risky assets (The other $10,000 is held in cash).

Interpretation of ‘Risk Impact’

© K.Cuthbertson and D.Nitzsche

END OF SLIDES

Recommended