1

Mr. S.V.Narasimhan Director(Finance)

Indian Oil Corporation Ltd

Refining Outlookand

Risk Management

2

Presentation Covers….

Refining OutlookFeatures of oil refining Refining capacity utilizationCapacity addition vs demand

Risk ManagementNeed for Risk ManagementHedging tools and marketsPractical considerations

3

Oil Refining – Defining features

Capital and Technology intensive Long gestation period Large investment needs:

To meet rising demand for oil Spec changes for modern engines &

environment issues Transport fuel the drivers – need for

upgrading bottom of the barrel Low margin – occasional cycles of

boom

Investment - a risky proposition

4

Singapore: Gross Refining Margin (Dubai)

- 2

0

2

4

6

8

1 0

J a n - 9 5 A p r - 9 6 J u l - 9 7 O c t - 9 8 J a n - 0 0 A p r - 0 1 J u l - 0 2 O c t - 0 3 J a n - 0 5 A p r - 0 6 J u l - 0 7

$/b

bl

D u b a i ( H y d r o c r a c k i n g S i n g a p o r e )

• Prolonged periods of low, even negative margins• Considerable volatility in the margins from month to month• Occasional boom serves to tide over long periods of poor margins • Domestic pricing policies restrict oil companies much needed

margins to fund future expansions,quality upgradation projects, etc

Source- IEA

Occasional boom

5

Global refinery utilization rate

6 5 0 0 0

7 0 0 0 0

7 5 0 0 0

8 0 0 0 0

8 5 0 0 0

9 0 0 0 0

KB

D

7 9

8 0

8 1

8 2

8 3

8 4

8 5

8 6

8 7

% u

tiliz

ati

on

R e f i n i n g C a p a c i t y % r a t e Source:BP

• In last 5 years, despite refining capacity additions, utilization rates soared to new highs.

• Effective utilization rates exceeded 95% at times considering planned and unplanned shutdowns.

6

Planned refinery additions(mid 2008-end 2009)

Company Location Additional capacity (kbd)

Expected completion

Sinopec Qingdao, China

201 Jun’08(commissioned)

PetroChina Dushanzi, China

104 Q3’08

PetroChina Dalian, China 150 Q4’08

CNOOC Huizhou, China

240 Q4’08

Others Global 389 2008

2008 Total 1084

Reliance Petroleum

Jamnagar, India

580 Q109

Sinopec Fujian, China 161 Q109

Dung Quat Refinery

Vietnam 130 Q209

Sinopec Tianjin, China

150 Q409

Others Global 409 2009

2009 total 1430

Grand Total (2008-09) 2514

Source: Goldman Sachs

7

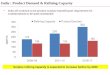

Refining additions Vs. Demand- 2001-12

0

0 . 5

1

1 . 5

2

2 . 5

3

2 0 0 1 2 0 0 3 2 0 0 5 2 0 0 7 2 0 0 9 2 0 1 1C a p a c it y a d d it io n I n c r e m e n t a l d e m a n d

Source: BP,Goldman Sachs and PEL

• During 2002-07, Refinery capacity additions lagged demand, leading to high margins/prices.

• Refining capacity additions to exceed incremental demand over 2008-2012, pointing towards softening margins

(million barrels per day)

Trend reversal •Substantial refining capacity additions - 2008 onwards

8

Refineries’ Dilemma : To build or not?

Build capacity Risk of unsustainable margins

Delay capacity additionsLoss of opportunity

Risks to Refining investments:• Demand growth uncertainty, particularly transport fuels• Light/Heavy differentials and sweet/sour differentials• NOC structure of Asia– not geared purely to economics – can

lead to overcapacity

Derivatives available to mitigate risk of poor economics.

9

Indian Refiners:Need for Risk Management

Existing refineries Extreme volatility in

refining margins Under-recoveries from

domestic products sale Customers seeking

fixed prices Fluctuation in

inventory valuation

New Refinery Projects Over capacity- weak

margins High investment –

poor returns Competition in

international market for export oriented refineries

RBI regulations:

• Permits hedging of risks to existing refineries like margins, inventory, domestic product sales, etc.

• Hedging of new refinery projects not permitted

10

Smoothens/reduces revenue volatility for existing refiners

Facilitates remaining within budget

Enables judicious deployment of funds, thereby ensuring timely project implementation

Protect against price spikes

Flexibility to hedge limited volumes allowing to tap market opportunities for remaining volume

Exit possible under unfavourable circumstances

Risk Management - Advantages

11

Markets for hedging

MARKETS

PETROLEUM EXCHANGES1. NYMEX, NEW YORK2. IPE,LONDON3. TOCOM, TOKYO4. DME,DUBAI5. MCX/NCDEX, INDIA

OTC MARKETS1. SINGAPORE2. LONDON3. NEW YORK

12

7 0

8 0

9 0

1 0 0

1 1 0

1 2 0

1 3 0

1 4 0

1 0 - J a n - 0 8 1 1 - F e b - 0 8 1 0 - M a r - 0 8 1 0 - A p r - 0 8 1 3 - M a y - 0 8 1 2 - J u n - 0 8

$ / b b l

A c t u a l p r i c e Q 3 0 8 f o r w a r d p r i c e

Dubai Forward price volatility:Q308

Final settlement price for

Q308:$113.48/bbl

Source: Morgan Stanley, Platt’s

13

1 0

1 5

2 0

2 5

3 0

3 5

4 0

4 5

5 0

1 0 - J a n - 0 8 1 1 - F e b - 0 8 1 0 - M a r - 0 8 1 0 - A p r - 0 8 1 3 - M a y - 0 8 1 2 - J u n - 0 8

$ / b b l

A c t u a l P r i c e F o r w a r d P r i c e

GO vs Dubai Forward price volatility:Q308

Final settlement price for

Q308:$25.7/bbl

Source: Morgan Stanley, Platt’s

14

Hedging tools available for Refiners

Refining margins hedging Options and swaps

Individual Crack spreads

Composite refining margins

Inventory hedgingOptions and swaps

Crude oil

Products

15

Refiners hedging (illustration)

Hedging assures fixed margin

Mechanism of hedging margin:Margins go up: Higher revenue on physical sales offsets outgo on derivative contract.

Margins go down: Lower revenues on physical sales offset by inflow on derivative contracts

Domestic price controls: Higher margins not realised on physical sales but cash outgo on derivatives occurs. This poses additional risk. Hence, need for a consistent and transparent policy.

Naphtha: 15%(Sell 150 bbls)

Kerosene: 15%( Sell 150 bbls)

HSFO 20%(Sell 200 bbls)

Crude 100%

Buy

1000 bbls

Refinery Margin hedging- IllustrationCrack ratio is based on product pattern of the refineries

Gasoil: 50%

(Sell 500 bbls)

16

1 5

2 0

2 5

3 0

3 5

1 5 2 0 2 5 3 0 3 5A c t u a l p r i c e

U S D /b b l

R e a li s e d M a r g i n w i t h h e d g i n g R e a li s e d M a r g i n w i t h o u t h e d g i n g

Swap: Gasoil-Dubai Crack (illustration)

Swap transaction

Swap level - $25/bbl

17

1 5

2 0

2 5

3 0

3 5

1 5 2 0 2 5 3 0 3 5A c t u a l p r ic e

U S D /b b l

R e a li s e d m a r g i n w i t h h e d g i n g R e a li s e d m a r g i n w i t h o u t h e d g i n g

Put Option- Gasoil vs Dubai (illustration)

Premium-$3/bbl

Strike Price: $25/bbl, Premium : $3/bbl

Strike-$25/bbl

18

Hedging practice – Oil companiesS.No

Company Practice (As per trading sources)

1 Shell 20%(appx)

2 Nippon Oil(Japan)

Only export volumes are hedged

3 Suncor(Canada)

40% hedged. (Opportunity loss - USD 100 million, decided not to renew hedges)

4 Valero Not significant volumes

5 Kerr Mcgee Oil production: 80% Hedged

6 Cosmo Oil 50% max (Actual volumes hedged are lower)

7 Idemitsu 50% max (Actual volumes hedged are lower)

8 Amerada Hess Oil production: 70% Hedged (Reported opportunity loss of USD 1.05 billion in 2004)

9 BP Not significant volumes

10 Exxon Exxon does not hedge. Oil companies follow diverse hedging strategies, but volume is typically limited unlike end users who hedge large volumes.

19

Hedging activity – Refiners in SE Asia

S.No

Country Refinery Risk Management activity

1 Korea SK Corp, KNOC, Hyundai Oil

Active

2 Thailand PTT (NOC) Active

3 Malaysia Petronas (NOC) Not so active.

4 Indonesia Pertamina (NOC) Not so active.

5 Taiwan CPC (NOC), Formosa Active

6 Japan Idemitsu, Nippon Oil, Cosmo

Active

7 China Sinochem Active

As per trading sources

20

Practical considerations- Steep backwardation

G a s o i l v s D u b a i

3 7 .5

3 9 .3 3

4 2 .6 7

4 0 .2 3

3 7 .4 5

3 6 .4 6 5

3 9 .8

3 7 .0 3

3 5 .7 6 3 6 .0 7

3 4 .7 4

3 3 .8 1

3 5 .2 5

3 6 .8 4

3 3 .2 43 3 .4 7 3 3 .1 5

3 2 .7 9

3 5 .1 3

3 2 .2 2

3 4 .9 5

3 3 .3 5

3 2 .23 2 .2 8

3 0

3 4

3 8

4 2

2 - J u n - 0 8 1 0 - J u n - 0 8 1 8 - J u n - 0 8 2 6 - J u n - 0 8 4 - J u l - 0 8

$/b

bl

S p o t Q 4 0 8 Q 1 0 9

• When Gasoil/Dubai spot cracks were at record high of $42.67, Q-4-08 and Q-1-09 were available at $6.6/bbl and $7.7/bbl respectively higher than the spot level.

• Such Backwardation present a serious dilemma for the hedgers!

Source: Platt's, Morgan Stanley

21

Practical considerations -Steep contango

B r e n t c r u d e o i l

8 0

8 5

9 0

9 5

1 0 0

1 0 5

1 1 0

1 1 5

1 2 0

1 2 5

0 1 - S e p - 0 8 0 8 - S e p - 0 8 1 5 - S e p - 0 8 2 2 - S e p - 0 8 2 9 - S e p - 0 8

Do

lla

r/B

ar

re

l

B r e n t D a te d Q 1 0 9

B r e n t D a te d Q 2 0 9

B r e n t D a te d S p o t

• When Brent spot price was at $86.69/bbl on 16th Sep 08, Q-1-09 and Q-2-09 were at $94.81/bbl and $96.26/bbl respectively viz. almost $8.1/bbl and $9.6/bbl higher than spot price.

• Such sharp contango present a serious dilemma for the hedgers!

Source: Platt's, Morgan Stanley

22

Practical considerations: When to hedge

Source:Morgan Stanley

G O v s D u b a i : F o r w a r d C u r v e - E n t r y T i m i n g

2 2

2 7

3 2

3 7

Q 4 0 8 Q 1 0 9 Q 2 0 9

$/b

bl

31/7/08

15/9/08

15/7/08

15/8/08

• Forward prices changed dramatically in a span of few days .

• Timing of entry is crucial – Yet no scientific way to time the market

23

Practical Consideration: Options premium

Premium Level for WTI call options (as of 3rd Oct 08)

Strike ($/bbl) Premium ($/bbl)

Dec’0893.0 7.37

95.0 6.39

98.0 5.22

Jun’0994.0 13.65

96.0 12.81

99.0 11.63

Dec’0996.0 16.13

98.0 15.32

101.0 14.17

• Buying Call Options ‘At the Money(ATM)’ or ‘Out of the Money’(OTM) involve significant premium payout.

Source: NYMEX

24

Risk Management Policy – Key issues

Volume limits Corporates should have clearly defined volume limits, based on the risk appetite.

Tools Swaps: To ensure a pre-determined price.

Options: Call: Caps maximum price(Buyer of crude/products)

Put:Ensures minimum price(Producer/Refiner for margin)

Collar:Combination of call & put to limit premium

Tenor Based on the risk appetite. Prompt positions prone to significant volatility. Hence, positions at back end of curve preferable.

Hedging/ Speculation

Short term entry and exit are speculative in nature.

Need for clear policies on holding position till maturity.

25

Risk Management Policy – Key issuesCounter-Parties

Criteria: Sound financial standing, experience, trade/bank references, credit rating, etc.

Market OTC: Based on exposure of crude oil/productsSingapore market relevant for Asian crude oil/products

Overseas Exchanges: Brent and WTI crude oil Products like Gasoline, Heating Oil, Gasoil, etc.

Approving Authority

Need for clearly defined authority for approving deals

Trading procedure

Competitive basis through bid/offers from 3-5 parties or more is desired.

Controls Daily Mark to Market report, segregation of duties between Trading and Settlement functions, audit, etc essential

26

Risk Management - Adequate Controls Prudent Risk Management strategy is essential.

Systematic reconciliation of internal transaction/positions Periodic reporting to Board, Management and regulatory

agencies

Euro 5 billion(approx) loss. Failure of internal controls and faulty reporting systems.

Societe Generale (2008)

$81 million loss. Inappropriate trading and reporting

Mitsui (2006)

$ 550 million loss. Resulted from selling Options & faulty M2M reports

$ 6 billion loss. One of the biggest collapses in Hedge fund history

China Aviation Oil (2004)

Amaranth (2006)

Derivative Disasters

27

Thank You

28

US Gulf Coast(USGC)-Gross Refining Margin

(Brent crude)

- 6

- 1

4

9

1 4

1 9

J a n - 9 5 J u l - 9 6 J a n - 9 8 J u l - 9 9 J a n - 0 1 J u l - 0 2 J a n - 0 4 J u l - 0 5 J a n - 0 7 J u l - 0 8

$/b

bl

Source- IEA

• Prolonged periods of low, even negative margins• Considerable volatility in the margins from month to month• Occasional boom time serve to tide over long periods of poor margins

Source- IEA

29

North West Europe - Gross Refining Margin (Brent crude)

- 2

0

2

4

6

8

1 0

1 2

J a n - 9 5 J u l - 9 6 J a n - 9 8 J u l - 9 9 J a n - 0 1 J u l - 0 2 J a n - 0 4 J u l - 0 5 J a n - 0 7 J u l - 0 8

$/b

bl

B r e n t ( C r a c k i n g N W E )

Source- IEA

• Considerable volatility in the margins from month to month• Occasional boom time serve to tide over long periods of poor margins

Source- IEA

30

High volatility in prices: WTI (2007-2008)

5 0

6 0

7 0

8 0

9 0

1 0 0

1 1 0

1 2 0

1 3 0

1 4 0

1 5 0Year Daily Change

($/bbl)

Avg Max

2006 0.9 4.4

2007 1.1 4.4

2008 2.3 16.4

Source: Platt's

31

Dubai Forward price volatility:Q408

9 0

1 0 0

1 1 0

1 2 0

1 3 0

1 4 0

1 5 0

4 /1 /0 8 5 /1 /0 8 5 /3 1 /0 8 6 /3 0 /0 8 7 /3 0 /0 8 8 /2 9 /0 8 9 /2 8 /0 8

Q 4 0 8 Source: Morgan Stanley

$/bbl

32

Trading on Exchanges – Some issues

NYMEX and ICE are the major energy international exchanges. Use of exchanges involves huge basis risk During the period Jan’07 to Sep’08,

• Brent dated and ICE Brent showed a strong positive correlation of 0.93.

- 2

- 1

0

1

2

3

J a n - 0 7 M a y - 0 7 S e p - 0 7 J a n - 0 8 M a y - 0 8 S e p - 0 8

$/b

bl

Actual ICE Brent vs Brent (Dated) differential showed substantial variation viz high basis risk

Source: Platt’s

33

Risk Management – To summarise

India Specific Exposure of Indian companies essentially to Asian oil and petro-

products NYMEX and IPE are major petroleum exchanges but do not have liquid

Asia specific commodity contracts. No AG related derivative contracts – Singapore market used as proxy.

Universal•Does not ensure best margin – Only predetermined margin can be hedged.

•Options hedging involves substantial costs•Backwardated markets – can lock into lower margins than currently prevailing

•Timing of entry – crucial in margin that can be locked into

Recommended