1

Quagmire from the Supreme Court Decision SEBC Fall Fly-inAtlanta, October 2, 2012

Robert DavisDirectorDeloitte Consulting LLP

Presented by

Mark HollowaySenior Vice PresidentLockton Companies, LLC

Wayne SoudExecutive Vice PresidentLockton Companies, LLC

Health Insurance Exchanges

3

What Is a Health Insurance Exchange?

A transparent, regulated, competitive marketplace for individuals to purchase health insurance coverage for themselves and their families Established and operated by states Each Exchange must offer a basic level of comprehensive benefits

called “essential health benefits,” as defined by HHS based on “typical” employer plan Bronze (60% actuarial value) Silver (70% actuarial value) Gold (80% actuarial value) Platinum (90% actuarial value)

Only private insurance products will be available Customer assistance tools with information about prices, quality,

and physician and hospital networks, et al., will be available

Small employers (100 or fewer employees) may leverage Exchanges to provide coverage to their employees

States may extend this option to larger employers beginning in 2017

4

Why Do Employers Care About Exchanges?

Decision to continue health benefits for employees (and/or retirees) Employee perceptions of Exchanges as alternative to employer-sponsored

coverage Cost of Exchange coverage relative to employer-based coverage Option to offer coverage through Exchange?

Exposure to shared responsibility payments Employers offering coverage to full-time employees (30+ hours per week)

will need to design plan and premium subsidy to avoid $3,000 penalty for each full-time employee who purchases coverage in an Exchange instead

Employers not offering coverage to full-time employees will pay $2,000 per full-time employee penalty if any full-time employee purchases coverage in an Exchange and qualifies for a premium tax credit or cost-sharing reduction

Administrative burdens Employers must notify employees about Exchanges Employers must file annual report about health benefits with IRS and

communicate with Exchanges to help determine if shared responsibility payments are required

5

State Progress on Health Exchanges

Source: Kaiser Family Foundation, August 2012

6

Why Exchange-based Coverage Is Expected to Be More Costly

Self-funded Employer: Administrative fees typically less than 5% of overall costs. No profit,

risk charges, or state taxes. Tax-deductible expense for company and pre-tax contributions for

employees. Available to actively-at-work employees and their families who are

healthier than the general population. Employee contributions based on salary, not age.

Health Insurance Exchanges: Insured premiums includes profit, risk charges, and state taxes. Pool includes adverse selection because healthy lives purchase only

as needed. Premiums after-tax and age-based with a maximum spread of 3 to

1. Insurers subject to billions in additional taxes and charges.

7

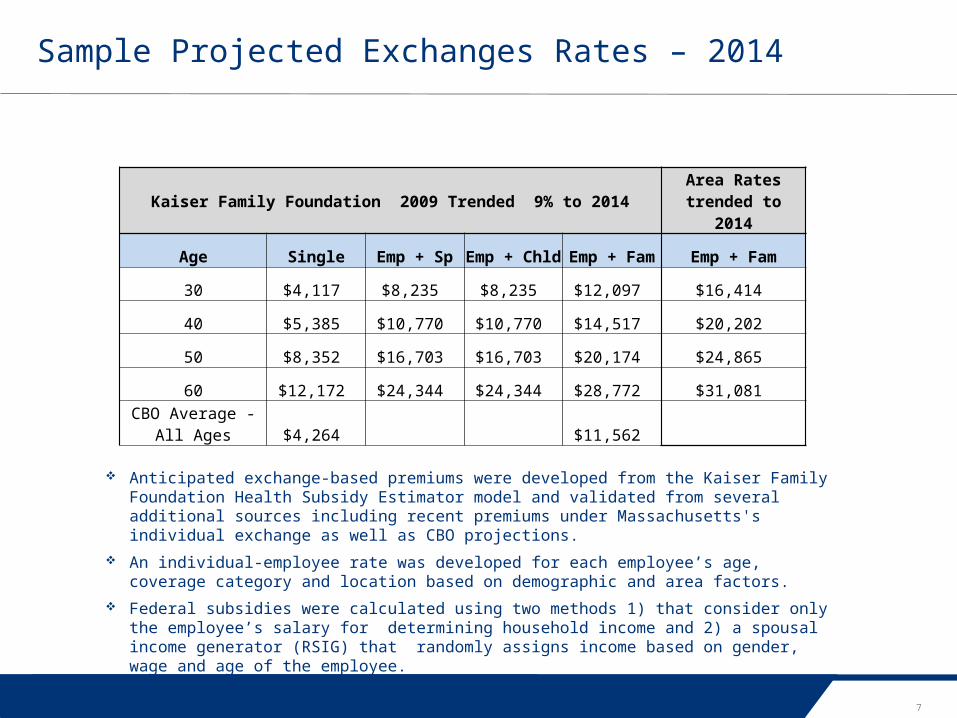

Sample Projected Exchanges Rates – 2014

Anticipated exchange-based premiums were developed from the Kaiser Family Foundation Health Subsidy Estimator model and validated from several additional sources including recent premiums under Massachusetts's individual exchange as well as CBO projections.

An individual-employee rate was developed for each employee’s age, coverage category and location based on demographic and area factors.

Federal subsidies were calculated using two methods 1) that consider only the employee’s salary for determining household income and 2) a spousal income generator (RSIG) that randomly assigns income based on gender, wage and age of the employee.

Kaiser Family Foundation 2009 Trended 9% to 2014Area Rates trended to

2014

Age Single Emp + SpEmp + Chld

Emp + Fam Emp + Fam

30 $4,117 $8,235 $8,235 $12,097 $16,414

40 $5,385 $10,770 $10,770 $14,517 $20,202

50 $8,352 $16,703 $16,703 $20,174 $24,865

60 $12,172 $24,344 $24,344 $28,772 $31,081 CBO Average -All

Ages $4,264 $11,562

8

Impact of Pay Option on Employees By Salary Range

9

Strategies to Mitigate Costs

Restructure work force Could raise eyebrows with DOL Can it be done in your business? Cost increase to job share

Offer all FTEs current plans plus a 60% plan that is affordable Eliminates worry over penalties Still a cost increase (may be more expensive

than the Pay option depending on the # who enroll and the PEPY net cost)

Keeps lower paid “winners” from getting subsidized coverage in Exchange so is it the right thing to do?

10

Strategies to Mitigate Costs (cont.)

Offer all FTEs current plans plus a “minimum essential plan” that costs less than the Exchange subsidized premium Plan will have to be very “skinny” Could still be cost increase to plan but less than penalty How many Ees will buy this coverage? How many Ees will still go to

Exchange?

Offer coverage to all or substantially all FTEs, but do not worry about making it affordable Some employees for whom it is unaffordable

will not seek subsidized coverage in an exchange For those that do, it might be cheaper for the employer

to pay the penalty than to subsidize the coverage

Summary of Benefits and Coverage (SBCs)

12

Summaries of Benefits and Coverage (SBC)

Two parts of new disclosure requirement for Group Health Plans SBC Uniform Glossary

Supplements, but does not replace, the SPD requirement for ERISA plans SBC requirement also applies to non-ERISA plans

Must be provided at specified times, including at open enrollment and upon request

Notice of material mid-year changes not reflected in most recent SBC must be given 60 days before such changes take effect

Effective on the first day of the first open enrollment period beginning on or after September 23, 2012

13

Summaries of Benefits and Coverage (SBCs)

Take advantage of new rule that allows electronic distribution for current enrollees if plan uses on-line enrollment More generous than standard DOL

rules for electronic distribution

Be mindful of accelerated notice if contemplating midyear plan changes

Headache: EAPs that provide counseling benefits

What if the required information cannot fit within the required format? E.g., hospital with different plan design

for use of domestic facilities, in-network and OON benefits

14

Construction and Review of SBCs: Keys to Watch For

Providing SBCs in a “Culturally and Linguistically Appropriate” Manner Enrollees residing in a county where according to

2010 census at least 10% of population is fluent in the same, non-English language, and speak English less than “very well”

Notice in that language, offering translation assistance (must be prominent) Insurer or TPA should have residence, for mailing of

EOBs Feds have supplied model one-sentence notices, in

multiple languages If individual requests translation assistance…

Offer oral translation assistance (i.e. translation services telephone hotline), and (upon request) supply the SBC in the relevant foreign language

Feds have supplied templates and sample completed SBCs, in multiple foreign languages: Spanish, Chinese, Navajo and Tagalog

Recommendation: use the one-sentence notice for everyone (or at least all those in the same state)

15

Summaries of Benefits and Coverage (SBC)

Counties with > 10% individuals fluent only in non-English language

Alaska (2) - Spanish/Tagalog Illinois (1) - Spanish New York (3) – Spanish

Arkansas (1) - Spanish Iowa (2) - Spanish North Carolina (1) – Spanish

Arizona (3) – Spanish, Navajo Kansas (8) - Spanish Oklahoma (1) - Spanish

California (24) – Spanish, Chinese Minnesota (1) - Spanish Oregon (3) – Spanish

Colorado (7) - Spanish Nebraska (3) - Spanish Texas (72) – Spanish

Florida (8) - Spanish New Mexico (7) – Spanish, Navajo Utah (1) – Navajo

Georgia (4) – Spanish[Atkinson, Echols, Hall, Whitfield]

Nevada (1) - Spanish Virginia (2) – Spanish

Idaho (4) - Spanish New Jersey (4) - Spanish Washington (5) – Spanish

Puerto Rico (78) - Spanish

Determining Full-Time Employee Status

17

Significance of “Full-Time Employee” Status Under PPACA

Employer Shared Responsibility rules apply only to “Applicable Large Employers” Employed an average of at least 50 “Full-Time Employees” for more

than 120 days during the preceding calendar year “Full-Time Equivalent” employees counted for this purpose only Special rule for seasonal employees

Employer Shared Responsibility penalties apply only with respect to “Full-Time Employees” Potential $2,000 penalty per FTE if coverage not offered to FTEs

and their dependents Potential $3,000 penalty for each FTE who opts out of the

employer’s coverage if it isn’t “affordable” or doesn’t meet a “minimum value” threshold Note: Penalties are “potential” because they are imposed only if a FTE

obtains coverage in a State Health Insurance Exchange and qualifies for a Premium Tax Credit or Cost-Sharing Subsidy

18

Definition of “Full-Time Employee”

The Employer Shared Responsibility rules only apply with respect to “Full-Time Employees” “The term ‘full-time employee’ means, with respect to any month,

an employee who is employed on average at least 30 hours of service per week.” IRC § 4980H(c)(4)(A).

“The Secretary, in consultation with the Secretary of Labor, shall prescribe such regulations, rules, and guidance as may be necessary to determine the hours of service of an employee, including rules for the application of this paragraph to employees who are not compensated on an hourly basis.” IRC § 4980H(c)(4)(B).

Because of the potential penalties associated with not offering coverage to “Full-Time Employees”, this definition raises many concerns Can part-time employees become full-time employees from time to

time, just because they work too many hours in a given month? What about new employees, if the employer isn’t sure how much

they will work? Are there any special rules for temporary and seasonal employees?

19

IRS Notice 2012-58

Describes safe harbors employers will be allowed to use to determine which employees are “full-time employees”

Different safe harbors will be available for different categories of employees New employees New variable hour or seasonal employees Ongoing employees

Employers will be able to rely on the guidance provided in Notice 2012-58 at least through the end of 2014

Unanswered questions persist

20

Determining Full-time Employees

Remember: PPACA contains no mandate to offer coverage to employees averaging 30+ hours per week If you don’t, you are at-risk for penalties if the employee

purchases Exchange coverage

You really don’t have to track hours, if all you have are regular, full-time employees and you’ll concede their “full-time” status under health reform For other employees, where full-time status might be in doubt,

start in 2013… Your obligation to offer FTEs health insurance—or risk penalties—begins

January 1, 2014 (unless authorities will defer this…)

Even if it’s clear the employee is part-time, you’ll need to show the hours to prove it, if you’re not offering qualifying and affordable coverage to him or her

21

Determining Full-time Employees

Loose ends: What hours, precisely, do we count? What if we re-hire a seasonal employee? Do we get to treat him or

her as a new hire? Any special rules for staffing companies? What about employees covered under a Taft-Hartley plan? What measurement and stability periods do we use in the wake of

a merger or acquisition? Managing hours < 30?

2012 Elections

23

Decision 2012 – The Future of Health Reform

How Does the Election Shake Out? White House: President enjoys narrow lead in the polls, and is a

gifted campaigner House: GOP likely to retain majority Senate: Too close to call, but Dems probably deny GOP a majority

Today: 51-47 Democrats lead, plus 2 independents who caucus/vote with Democrats

33 seats up for grabs GOP has 47 continuing, solid or leaning GOP seats Dems have 47 continuing, solid or leaning Democrat seats

24

Decision 2012 – The Future of Health Reform

Possibilities…and Effect on Health Reform President wins re-election

Status quo, no matter who wins Senate Romney wins, Dems hold the Senate

Status quo Romney wins, GOP wins Senate and

holds House GOP lacks votes for cloture, but… Can strip budget-related items from the

law, and… Romney can imperil implementation

25

Any Questions?

Robert DavisDirectorDeloitte Consulting [email protected]

Mark Holloway Senior Vice PresidentLockton Companies, [email protected]

Wayne SoudExecutive Vice PresidentLockton Companies, [email protected]

Recommended