Advisory

Total RetailFrom offline to online, the transition accelerates

5 July 2015

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Agenda

•Present key outcomes of the PwC Total Retail Survey, 2015

•How customer expectations affect supply chains?

•What are the strategic supply chain options to be considered?

3Total Retail • Retailers and the Age of Disruption

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

We conducted a global survey to study consumer shopping behaviours and their changes

4Total Retail • Retailers and the Age of Disruption

Russia

US

Canada

Brazil

Chile

South Africa

Australia

JapanChina/HK

IndiaMiddle

East

UK

France

ItalySwitzerlan

d

Turkey

Denmark

Belgium

Germany

Survey now covers more than 19,000 respondents on six continentsOver 1.000 respondents

in Russia

83

80

92

111

135

30

103

65

Russia

Northwestern FD*

305

1,004

Far-Eastern FD*

Moscow

Central FD*

Southern and NorthCaucasian FD*

Urals FD

Saint-Petersburg

Siberian FD*

Privolzhsky FD*

*FD – Federal District

3rd

time

in

Russia

http://www.pwc.ru/ru/retail-consumer/publications/totalretail2015.jhtml

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

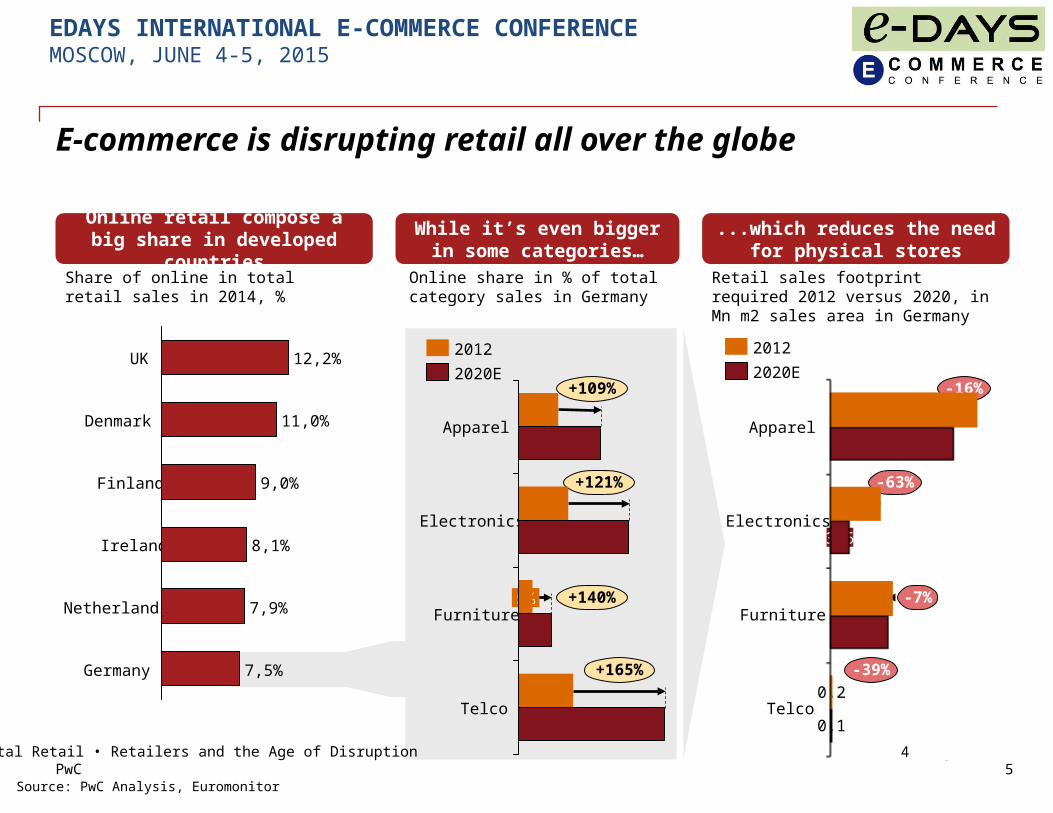

E-commerce is disrupting retail all over the globe

5Total Retail • Retailers and the Age of Disruption

Online retail compose a big share in developed countries

While it’s even bigger in some categories…

...which reduces the need for physical stores

Share of online in total retail sales in 2014, %

Denmark 11,0%

UK 12,2%

Netherlands 7,9%

Ireland 8,1%

Finland 9,0%

Germany 7,5%

Online share in % of total category sales in Germany

18%

Apparel30%

14%

20%

Furniture12%

5%

Electronics40%

+109%

+121%

+140%

+165%

Telco53%

2012

2020E

9,6

24,0

28,5Apparel

11,3

12,1

Electronics3,6

Furniture

-16%

-63%

-39%

-7%

0,1

0,2Telco

2020E

2012

Retail sales footprint required 2012 versus 2020, in Mn m2 sales area in Germany

Source: PwC Analysis, Euromonitor

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Online retail share in Russia has been growing steadily

6Total Retail • Retailers and the Age of Disruption

Online retail is steadily increasing its share in total retail

2014

597

3,3%

2013

474

2,8%

2012

365

2,4%

2011

268

2,0%

2010

202

1,5%

1,7%

158

2009

Share of online, %

Online sales, bn RUB

Online sales volume and share of online, current prices

In some categories online has high growth rates, while offline is nearly stagnating

+2,6%+22,9%

+34,7%

2010-2014 CAGRs

Electronics offlineElectronics online

+4,4%

Apparel offlineApparel online

Constant prices

Source: PwC Analysis, Euromonitor

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Based on analysis of consumer behaviour we see that offline and online retail should go hand in hand together

7Total Retail • Retailers and the Age of Disruption

Respondents research for products in-store and then buy online to buy at lower price…

...and do the opposite, research online and buy in-store, to see and touch the product

Buyonline

Researchin-store

80% of respondents have store-to-web experience

Buyin-store

Research online

70% of respondents have web-to-store experience

22%

I wanted to see/touch/try

The item was not in stock in store

1%

39%

36%

To seek advice from store staff

To have delivery

Other

62%

Better prices online 88%

Q: What factors influenced your decision to intentionally browse for products in-store and then purchase those products online?

To avoid paying for delivery

20%

63%

33%

1%

28%

The item was not in stock online

To compare prices of competitors

Better prices in-store

Other

54%

21%

To get the product immediately

To read reviews online

63%I wanted to see/touch/try

Q: What factors influenced your decision to intentionally browse for products online and then purchase those products in-store?

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Key challenges

•Profitable omni-channel

•Responding to changing customer expectations

•Managing complexity

8Total Retail • Retailers and the Age of Disruption

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Omni-channel will increase revenues but require an efficient and flexible SC to maintain margins as well as clear strategy to deal with complexity

8Total Retail • Retailers and the Age of Disruption

Consumer Expectations

• Operating cost impacts

• Inventory cost impacts

• Transportation cost impacts

• Current fulfilment / inventory strategy

• Network constraints / capabilities

• Distribution network strategy

• Omni-channel impact to network • Touch point and channel cost to serve

Itera

tive

Supply Chain Design

Revenues

Cost to serve

Margin ????

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

While service level is a relevant decision criterion for e-shoppers in Russia, it is not the first priority yet

9Total Retail • Retailers and the Age of Disruption

Comments

• According to the recently conducted consumer survey in Russia by PwC, price is by far the most important factor affecting decision making for online customers

• However, there are several supply chain related factors which are considered crucial (5 factors from 16 were chosen by respondents):

– 26% of respondents are seeking for assortment availability

– 21% of respondents consider reliable delivery as one of the main factors for choosing a retailer

• Therefore, optimizing supply chain is an opportunity for e-commerce players to increase market share

Fast and reliable delivery

Loyalty programme

Inspiring online content

Availability of a product

Decision-making factors for online purchasesRussian consumer survey, 2014

Price

Assortment

Trust to the brand

Location and staff

Good returns policy

Superior online customer reviews

21%

18%

18%

20%

26%

57%

22%

28%

26%

27%

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Although younger customers are willing to pay for faster delivery, indicating potential for eTailers to differentiate

10Total Retail • Retailers and the Age of Disruption

Younger users are ready to pay extra for the same day delivery

There is no significant difference between the districts

As this population becomes more relevant in terms of household spend, eTailers can differentiate themselves and at the same time benefit from additional revenue by offering faster delivery compared to peers

However, to leverage this opportunity supply chain network needs to support this

Wiliness to pay for the same day deliveryRussian consumer survey, 2014

51.1%

18 - 24 years

35.7%

61.2%

45 - 54 years

25 - 34 years

33.3%

55.1%

55 - 64 years

52.9%

35 - 44 years

65+ years

Comments

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

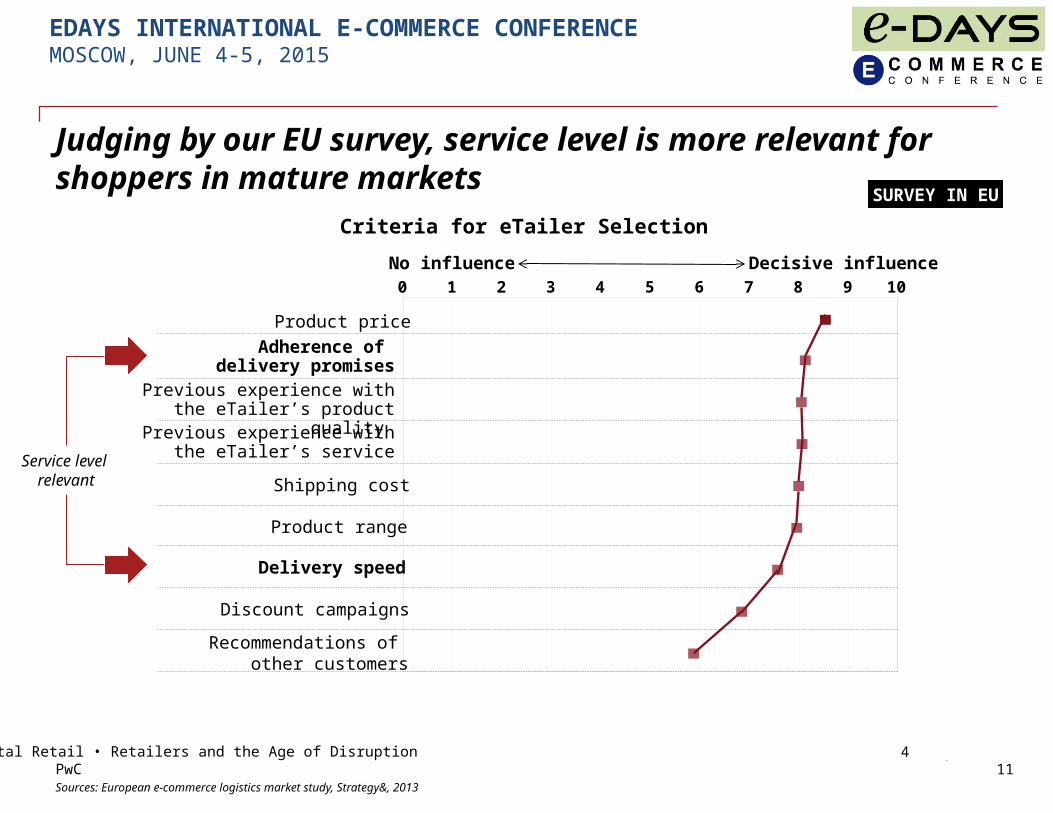

Judging by our EU survey, service level is more relevant for shoppers in mature markets

11Total Retail • Retailers and the Age of Disruption

No influence Decisive influence0 1 2 3 4 5 6 7 8 9 10

Product price

Adherence of delivery promises

Previous experience with the eTailer’s product quality

Previous experience with the eTailer’s service

Shipping cost

Product range

Delivery speed

Discount campaigns

Recommendations of other customers

Criteria for eTailer Selection

Service level relevant

SURVEY IN EU

Sources: European e-commerce logistics market study, Strategy&, 2013

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

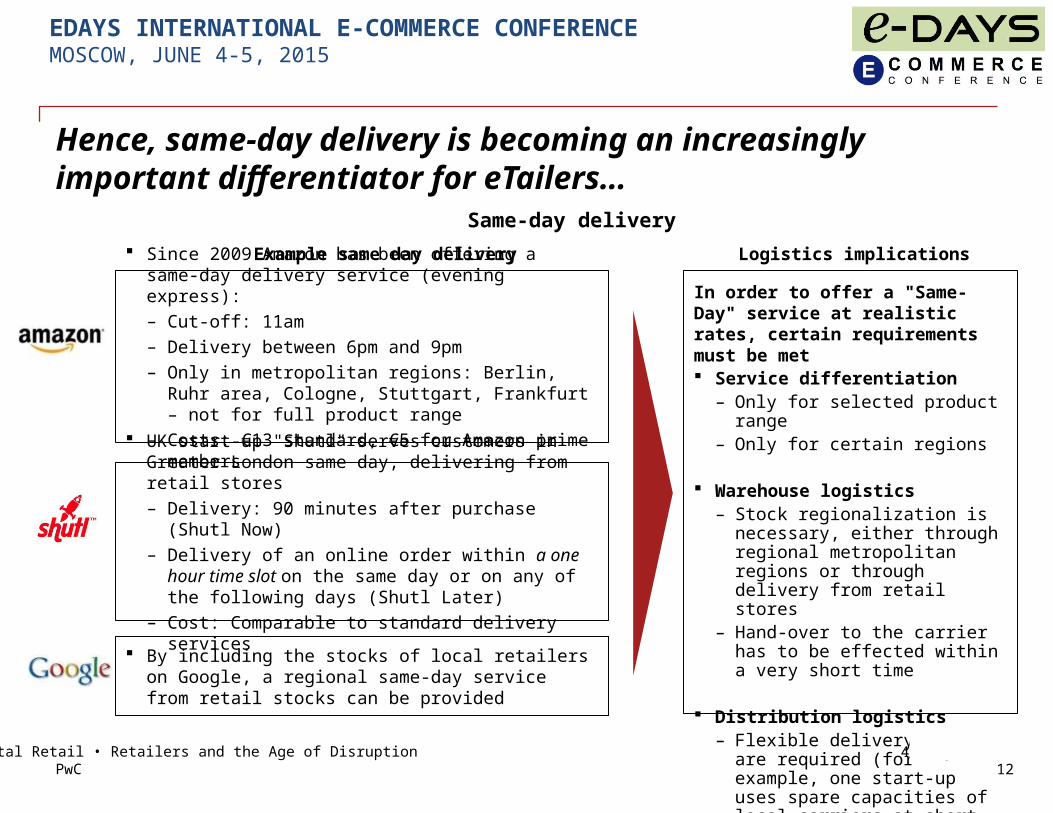

Hence, same-day delivery is becoming an increasingly important differentiator for eTailers…

12Total Retail • Retailers and the Age of Disruption

Same-day delivery

Since 2009 Amazon has been offering a same-day delivery service (evening express):– Cut-off: 11am– Delivery between 6pm and 9pm– Only in metropolitan regions: Berlin, Ruhr area,

Cologne, Stuttgart, Frankfurt – not for full product range

– Costs: €13 standard, €5 for Amazon prime members

UK start-up "Shutl" serves customers in Greater London same day, delivering from retail stores– Delivery: 90 minutes after purchase (Shutl Now)– Delivery of an online order within a one hour time slot

on the same day or on any of the following days (Shutl Later)

– Cost: Comparable to standard delivery services

Example same day delivery

In order to offer a "Same-Day" service at realistic rates, certain requirements must be met Service differentiation

– Only for selected product range– Only for certain regions

Warehouse logistics– Stock regionalization is necessary,

either through regional metropolitan regions or through delivery from retail stores

– Hand-over to the carrier has to be effected within a very short time

Distribution logistics– Flexible delivery systems are

required (for example, one start-up uses spare capacities of local carriers at short term )

Logistics implications

By including the stocks of local retailers on Google, a regional same-day service from retail stocks can be provided

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

We expect service level to become a differentiator in Russia as well, which is a key consideration for the network design

13Total Retail • Retailers and the Age of Disruption

Density of distribution network impacts service level Implications for network design

• Service level is highly depended on number of warehouses that are located near the customers

• Hence, to increase the service level eTailers should consider covering areas of high demand (mostly in central part of Russia) by warehouses more densely

• However at the same time price of delivery, willingness of shoppers to pay for it and existence of alternatives should be considered

• In addition, impact of increased service level on revenues needs to be understood before taking decisions regarding the network

ILLUSTRATIVE

Higher number of warehouses increases service level

Warehouse

Radius of one-day delivery

Major cities

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

So, how are retailers responding to challenges?

14Total Retail • Retailers and the Age of Disruption

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Supply chain optimisation – Dixons have addressed key issue of inventory transparency

www.dixons.com

16Total Retail • Retailers and the Age of Disruption

Dixons have integrated their store inventory into their digital channels so that consumers can decide to collect their products from any location that has availability

• Stock data (location, quantity) in real time

• Sharing data between supply chain partners

• Sharing data between stores, channels

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Supply chain optimisation – M&S completed a massive re-organisation recently

Single integrated supply chain across the globe – 4 hubs (Turkey, Sri Lanka, Malaysia, China), 26

Regional distribution centres

Reduced sea shipping time from 9 weeks to 1.5 weeks.

Over 80% stock delivered directly

UK from 110 warehouses to 3

Spent over £150m on website integration with new supply chain

Single view of inventory

17Total Retail • Retailers and the Age of Disruption

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

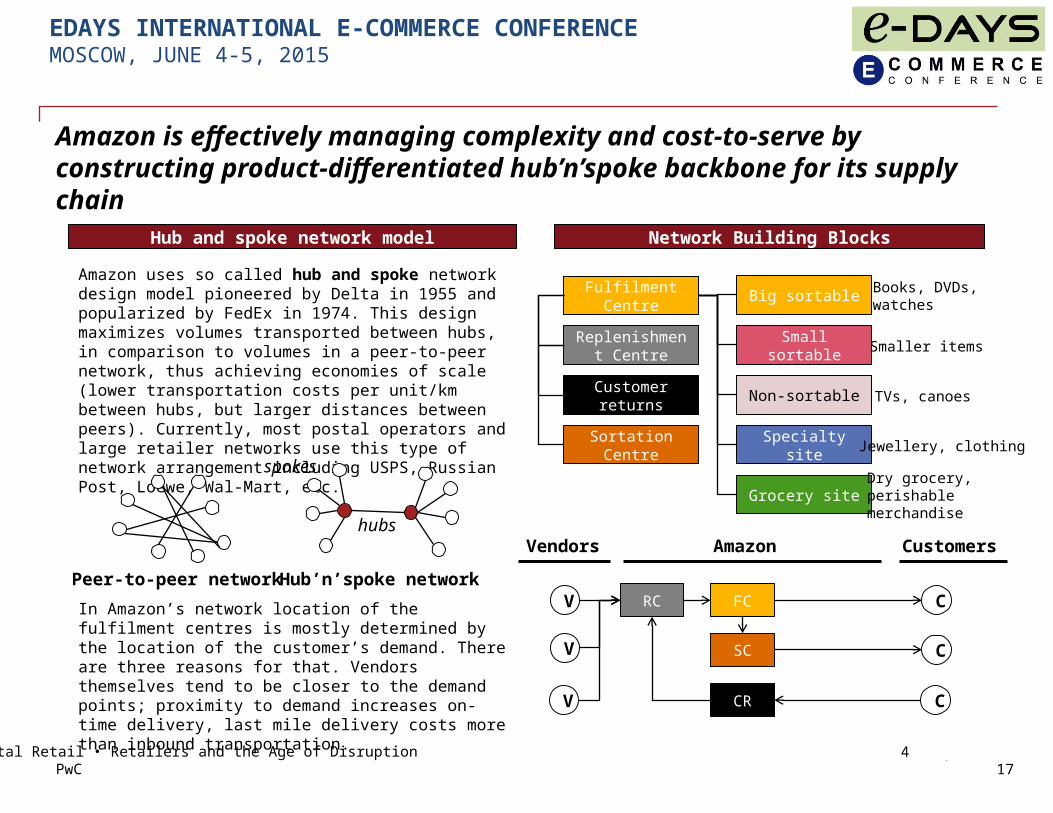

Amazon is effectively managing complexity and cost-to-serve by constructing product-differentiated hub’n’spoke backbone for its supply chain

17Total Retail • Retailers and the Age of Disruption

Hub and spoke network model Network Building Blocks

Amazon uses so called hub and spoke network design model pioneered by Delta in 1955 and popularized by FedEx in 1974. This design maximizes volumes transported between hubs, in comparison to volumes in a peer-to-peer network, thus achieving economies of scale (lower transportation costs per unit/km between hubs, but larger distances between peers). Currently, most postal operators and large retailer networks use this type of network arrangement including USPS, Russian Post, Loewe, Wal-Mart, etc.

In Amazon’s network location of the fulfilment centres is mostly determined by the location of the customer’s demand. There are three reasons for that. Vendors themselves tend to be closer to the demand points; proximity to demand increases on-time delivery, last mile delivery costs more than inbound transportation.

hubs

spokes

Peer-to-peer network Hub’n’spoke network

Big sortable

Small sortable

Non-sortable

Fulfilment Centre

Customer returns

Replenishment Centre

Specialty site

Grocery site

SortationCentre

Books, DVDs, watches

Smaller items

TVs, canoes

Jewellery, clothing

Dry grocery, perishable merchandise

Vendors Amazon Customers

FC

SC

CR

RC

C

C

C

V

V

V

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

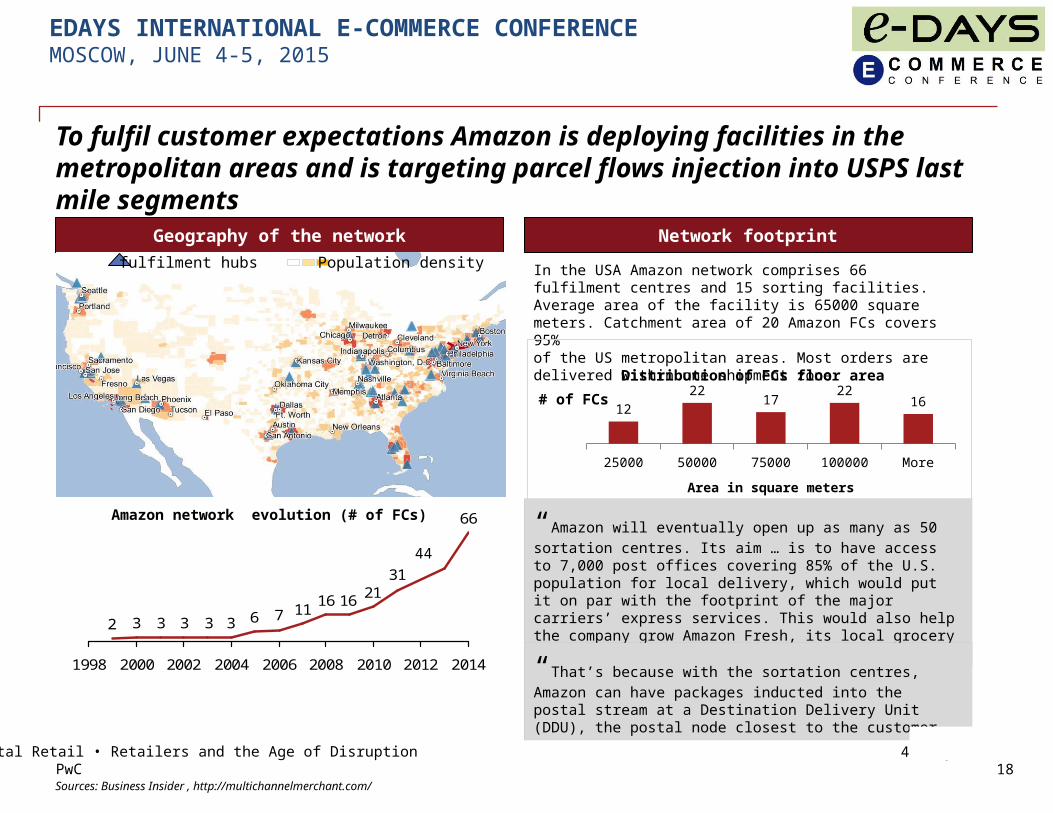

To fulfil customer expectations Amazon is deploying facilities in the metropolitan areas and is targeting parcel flows injection into USPS last mile segments

18Total Retail • Retailers and the Age of Disruption

In the USA Amazon network comprises 66 fulfilment centres and 15 sorting facilities. Average area of the facility is 65000 square meters. Catchment area of 20 Amazon FCs covers 95% of the US metropolitan areas. Most orders are delivered within one shipment zone

Geography of the network Network footprint

25000 50000 75000 100000 More

12

2217

2216

Area in square meters

Sources: Business Insider , http://multichannelmerchant.com/

Distribution of FCs floor area

“Amazon will eventually open up as many as 50 sortation

centres. Its aim … is to have access to 7,000 post offices covering 85% of the U.S. population for local delivery, which would put it on par with the footprint of the major carriers’ express services. This would also help the company grow Amazon Fresh, its local grocery delivery service

“That’s because with the sortation centres, Amazon can have

packages inducted into the postal stream at a Destination Delivery Unit (DDU), the postal node closest to the customer.

# of FCs

66

31211616

1176333332

1998 2000 2002 2004 2006 2008 2010 2012 2014

44

Amazon network evolution (# of FCs)

fulfilment hubs Population density

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

Key strategic options to think through

19Total Retail • Retailers and the Age of Disruption

Centralised

Decentralised

Owned network and key assets

Integrated with 3rd party logistics or postal operator

Ground-based

Aviation/rail included

Uniform

Regional

Assortment mix

Modality

Partnership

Automated

Semi-automated

WH configuration

Sorting automation

Network linkage

Multi-echelon

Hub’n’spokes

Integrated supply chain

One size fits all

Separated supply chains

Service level

Uniform

Differentiated

PwC4 July 2015

EDAYS INTERNATIONAL E-COMMERCE CONFERENCE MOSCOW, JUNE 4-5, 2015

19Total Retail • Retailers and the Age of Disruption

Let’s keep in touch!

Ilya Malyarenko

PwC | Senior Manager, Strategy & OperationsOffice: +7 (495) 232-5405Mobile: +7 (965) 104-7968 Email: [email protected]

Recommended