2012 Ambulatory EHR & PM Study

September 2012

Disclaimer: This report and its contents are provided under copyright by CapSite™ and are intended solely for your organization. Any other organization, consultant, investment company or vendor gaining unauthorized access to this report will be liable to compensate CapSite™ for the full price of the report.

© 2012 CapSite

Table of Contents I. Study Participant Profile by

i. Geographic Location ii. Number of Physicians Employed iii. Hospital Owned vs. Free-Standing

I. By Number of Physicians Employed II. Year Organization Was Purchased III. Expected Organization Purchase Date

II. Ambulatory EHR Market Adoption

i. Current Ambulatory EHR Solution ii. Trending Analysis

i. Hospital Owned vs. Free-Standing ii. Year of EHR Purchase

III. Ambulatory EHR Vendor Market Share

i. Current Ambulatory EHR Vendor II. By Number of Physicians Employed III. Hospital Owned vs. Free-Standing

IV. Ambulatory EHR Market Opportunity i. Plans to Purchase or Upgrade Ambulatory EHR

I. Timeframe for Purchase II. Considered Vendors

i. By Number of Physicians Employed ii. Hospital Owned vs. Free-Standing

V. Voice of Customer (VOC)

i. Primary Driver for Purchasing EHR Solution I. By Number of Physicians Employed II. Hospital Owned vs. Free-Standing

ii. Reasons for Not Purchasing EHR I. Trending Analysis

VI. Practice Management Solutions

i. Primary PM Solution Vendor I. By Number of Physicians Employed II. Hospital Owned vs. Free-Standing

VII. Practice Management Solutions Market Opportunity

i. Year of Current PM Solution Purchase

VIII.Practice Management Solutions Market Opportunity continued

i. Plans to Purchase or Upgrade Current PM Solutions I. By Number of Physicians Employed II. Planned Purchase or Upgrade Timeframe

IX. Practice Management Solutions Vendor Mind Share

i. Considered Vendors I. By Number of Physicians Employed II. Hospital Owned vs. Free-Standing III. Would You Consider Replacing Current PM Solution with EHR/PM Integrated Solution? IV. Reasons to Replace Current Integrated EHR/PM Solution

X. Meaningful Use

i. Stage 1 Meaningful Use Compliance Status ii. Have You Received Government Incentive Funds for Stage 1 MU Compliance? iii. How Confident are You that Your Current PM/EHR Solution Will Meet Stage 2

Meaningful Use Criteria? iv. Do You Have Plans to Join a Health Information Exchange (HIE)?

XI. Appendix

Study Participant Profile by Geographic Location (n = 957)

6

Study Participant Profile by Market Segment

0

50

100

150

200

250

300

350

1-2 Physicians 3-10 Physicians 11-25 Physicians 26-100 Physicians 101+ Physicians

Num

ber o

f Res

pond

ents

Number of Physicians Employed

7

Physician Groups # of Physicians

1-2 Physicians 107,476

3-10 Physicians 248,887

11-25 Physicians 92,542

26-100 Physicians 48,835

101+ Physicians 11,540

Total 509,280 Source: SK&A

Study Profile by Hospital-Owned vs. Free-Standing Organizations

Hospital-Owned

39%

Free-Standing 61%

8

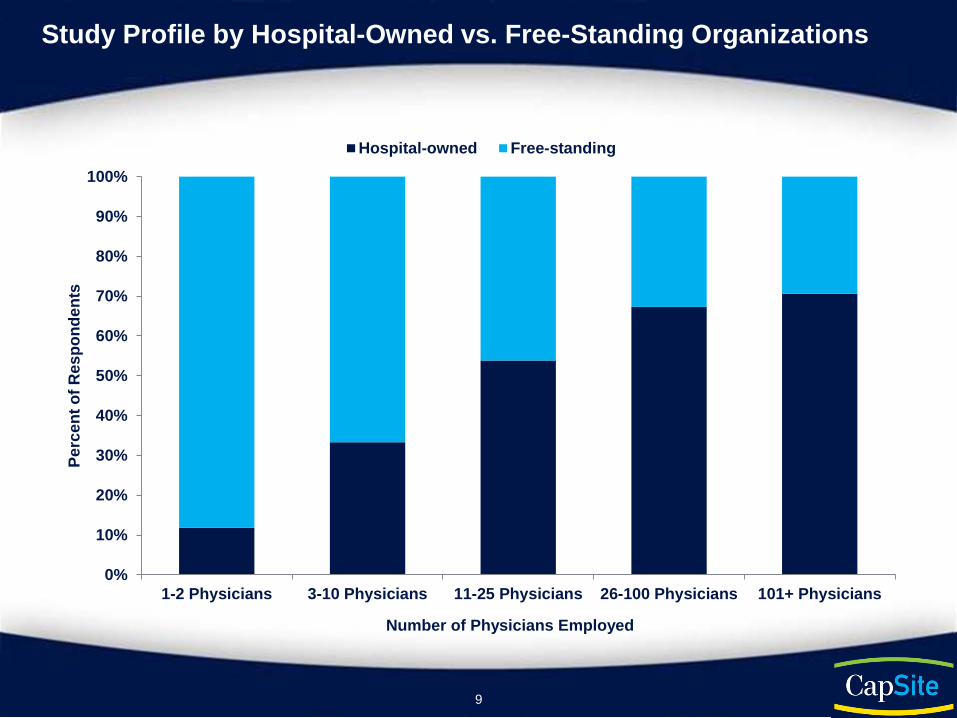

Study Profile by Hospital-Owned vs. Free-Standing Organizations

9

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1-2 Physicians 3-10 Physicians 11-25 Physicians 26-100 Physicians 101+ Physicians

Perc

ent o

f Res

pond

ents

Number of Physicians Employed

Hospital-owned Free-standing

10

APPENDIX

About Us

CapSite is a healthcare technology research and advisory firm.

Our mission is to help our healthcare vendor and provider clients make more informed strategic decisions that enable

them to accelerate the growth of their business.

11

CapSite Database

Optimize your pricing to maximize your revenue and profit

Strategic Industry Reports

Competitive Landscape Market Size

Market Opportunity

Voice of Customer

(VOC)

Align your messaging with your customers perception of value

Diagnostic Benchmarking

Win / Loss

Proven framework to improve your

win rate

Research and Advisory Solutions

12

Database

The CapSite Database is the trusted, easy-to-use online database, providing critical knowledge and evidence-

based information on healthcare technology purchases.

CapSite provides detailed transparency on healthcare technology pricing, packaging and positioning.

When it comes to healthcare technology research, it helps to see all the details. Those details are now available with

13

Database

Positioning

Packaging Pricing

• EHR • Revenue Cycle • HIE • Professional

Services

Health IT

• CT • MR • DR / CR • Mammography • Ultrasound

Imaging Equipment

• Patient Monitors • Smart Pumps

Medical Devices

14

Strategic Industry Reports

2012 Reports Medical Device Integration (MDI) Revenue Cycle Management (RCM) Laboratory IS Beds & Stretchers Smart Infusion Pump

2011 Reports Ambulatory EHR & PM Emergency Department Information

Systems (EDIS) Health Information Exchange PACS Replacement Patient Access Professional Services Radiology Information Systems Teleradiology Transcription Services

2010 Reports Ambulatory EHR and PM Ambulatory EHR Certification Ambulatory EHR Cardiology IT Claims Management Health Information Management Imaging IT Remote Radiology Revenue Cycle Management (RCM) Vendor Neutral Archive (VNA)

* CapSite also creates customized strategic industry reports based on the individual needs of its clients

Published Reports 2010-2012*

15

For more information about our services, or to order a report, please call, email, or click:

802.383.0675 [email protected]

www.CapSite.com

Recommended