2016 BenefitsENROLLMENT GUIDE

What’s InsideBenefits Enrollment 2016

Your Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Benefits Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

How to Enroll . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Change In Your Coverage Mid-Year . . . . . . . . . . . . . . . . . . . 4

Health Benefits

Medical Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

- Plan 1: HSA Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

- Plan 2: POS Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

- Medical Plan Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

- Medical Plan Comparison Quick Guide . . . . . . . . . . . . . . 11

- Wellness Incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Flexible Spending Accounts . . . . . . . . . . . . . . . . . . . . . . . . . 13

Dental Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Vision Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Additional Benefits

Short-Term & Long-Term Disability . . . . . . . . . . . . . . . . . . . 16

Life and Accident Insurance . . . . . . . . . . . . . . . . . . . . . . . . . 17

Long-Term Care, Home & Auto, Aflac and Prepaid Legal . . . . . . . . . . . . . . . . . . . . . . . . . . 18

403(b) Retirement Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Comprehensive Leave/Paid Time Off (PTO) . . . . . . . . . . . . 24

Extended Illness Leave . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Employee Education Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Additional Resources

More Medical Plan Information . . . . . . . . . . . . . . . . . . . . . . 27

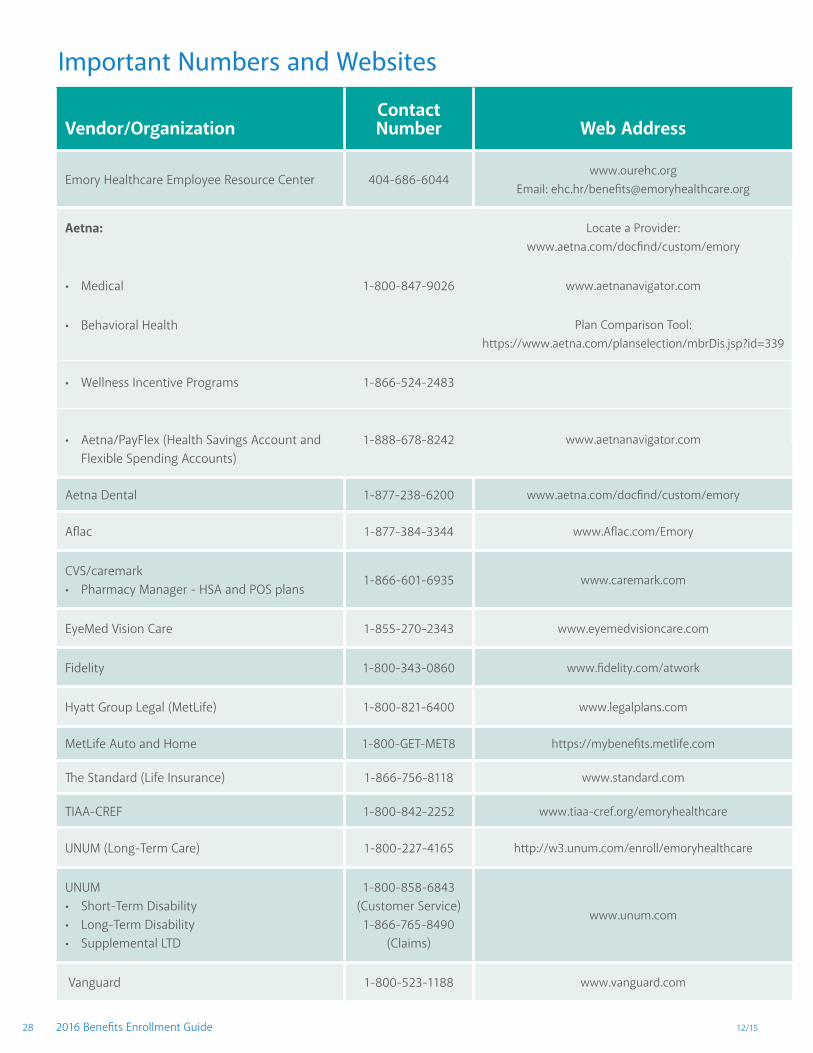

Important Numbers and Websites . . . . . . . . . . . . . . . . . . . . 28

ChoicesEmory Healthcare is proud to be a vital part of the

Atlanta community. One of the reasons we are an

employer of choice is the rich benefits package that

we offer our employees. As a part of Emory

Healthcare, you have numerous benefits available to

you. You have a choice of two medical plans for 2016,

each with unique plan design features. In addition,

there are plans that provide coverage for dental,

vision, disability, retirement, long-term care, legal

services and more. We encourage you to take a close

look at all of the benefits information provided in this

guide. Our benefit plans are just one of the many

ways Emory Healthcare helps you take care of

yourself and your family.

This guide is meant to provide basic benefit plan information. For additional details and specific information, please contact the vendor or review the

Summary Plan Description (SPD) for each plan. SPDs are available on the Your Benefits website (go to www.ourehc.org and select Employee Resources)

or by contacting the Employee Resource Center at 404-686-6044 or EHC.HR/[email protected] for a printed version.

DISCLAIMER: Emory Healthcare reserves the right to terminate or amend its plans and leave policies in whole or in part at any time, including the right to

terminate or modify coverage, and the cost of coverage, for any group of employees, whether active, on leave or retired, and/or dependents at any time,

even during a leave or after retirement. The welfare plans do not provide vested benefits.

The Summary of Benefits and Coverage

(SBC) for each health plan and the

individual health insurance marketplace

exchange notice can be accessed at

www.ourehc.org. Click on Employee

Resources and then Your Benefits.

12/15 2016 Benefits Enrollment Guide 1

What’s InsideBenefits Enrollment 2016

Your Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Benefits Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

How to Enroll . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Change In Your Coverage Mid-Year . . . . . . . . . . . . . . . . . . . 4

Health Benefits

Medical Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

- Plan 1: HSA Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

- Plan 2: POS Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

- Medical Plan Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

- Medical Plan Comparison Quick Guide . . . . . . . . . . . . . . 11

- Wellness Incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Flexible Spending Accounts . . . . . . . . . . . . . . . . . . . . . . . . . 13

Dental Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Vision Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Additional Benefits

Short-Term & Long-Term Disability . . . . . . . . . . . . . . . . . . . 16

Life and Accident Insurance . . . . . . . . . . . . . . . . . . . . . . . . . 17

Long-Term Care, Home & Auto, Aflac and Prepaid Legal . . . . . . . . . . . . . . . . . . . . . . . . . . 18

403(b) Retirement Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Comprehensive Leave/Paid Time Off (PTO) . . . . . . . . . . . . 24

Extended Illness Leave . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Employee Education Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Additional Resources

More Medical Plan Information . . . . . . . . . . . . . . . . . . . . . . 27

Important Numbers and Websites . . . . . . . . . . . . . . . . . . . . 28

Your BenefitsAs an Emory Healthcare employee, you are fortunate to have a wide range of benefit programs available to you.

Benefit programs give you important financial protection when you need it most. Enrolling in your benefits is

quick and easy. Spend a few minutes and review the benefit programs that Emory Healthcare offers to make the

choices that are right for you and your family.

Some benefits Emory Healthcare offers are employer provided, and coverage is automatic if you are eligible. Other benefits give you choices and require you to enroll.

Employer-Provided BenefitsAs an eligible employee, Emory Healthcare automatically provides you with several benefits. Emory Healthcare pays the full cost for basic life insurance and long-term disability coverage and provides a basic employer contribution to the 403(b) retirement plan for eligible employees. For more information on retirement plan options, view the Discover Your Retirement Options Guide located on the Employee Resources site on www.ourehc.org.

Optional BenefitsIn addition to employer-provided benefits, eligible employees may enroll in optional benefits, including medical, dental, vision, supplemental life insurance, accidental death and dismemberment, disability, flexible spending accounts, 403(b) retirement plans and other voluntary plans. You contribute toward the cost of the optional benefits that you elect.

When Coverage BeginsFor most benefits, coverage begins on an employee’s date of hire.

New Hires: If you are benefits-eligible, you must enroll during your first 31 days of employment with Emory Healthcare.

For optional benefits other than the 403(b) and supplemental long-term disability, if you do not enroll during your first 31 days of employment, you will not receive coverage. Your next opportunity to enroll in optional benefits will be during the annual benefits enrollment period, typically held in the fall of each year for the upcoming year, or if you experience a qualified family status change (see page 4 for more information). Life and long-term care benefits require Evidence of Insurability (EOI) for late enrollees.

Current Employees: If you are a current, benefits-eligible Emory Healthcare employee, each year you have an opportunity to review your benefit elections during the annual benefits enrollment period and make changes for the upcoming plan year.

When Coverage EndsFor most benefits, coverage will end on the last day of the month in which:

• Your regular work schedule is reduced to fewer than 20 hours per week;

• Your employment with Emory Healthcare ends due to resignation, termination or death; or

• You stop paying your share of the coverage.

Your dependent(s) coverage ends:

• When your coverage ends, or

• The last day of the month the dependent is no longer eligible:

– For Dependent Child(ren) (up to age 26): End of the month in which they turn 26.

2016 Benefits Enrollment Guide 12/152

Who Can Enroll (Benefits Eligibility)You are eligible for benefits if you are a regular full-time or part-time employee scheduled to work 20 hours or more per week.

If you elect coverage, your dependents are also eligible for medical, dental, vision and life insurance coverage. Eligible dependents include:

• Your legal spouse.

• Same-Sex Domestic Partner (SSDP): Another adult of the same sex who is engaged with you in a spouse-like relationship characterized by mutual dependency.

– Have residence in the same household.

– Financially responsible for each other’s well-being and debts to third parties. This means that you have entered into a contractual commitment for that financial responsibility or have joint ownership of significant assets (such as home, car, bank accounts) and joint liability for debts (such as mortgages and major credit cards).

– Neither partner is married to anyone else nor has another domestic partner receiving benefits.

– Partners are not related by blood closer than would bar marriage in the state of their residence.

– If you choose to cover a same-sex domestic partner, you will pay the same cost and receive the same coverage as you would for a spouse.

– Covering an SSDP will result in additional tax liability (imputed income). If your relationship ends, you will need to notify the Employee Resource Center.

• Your legal child(ren): Includes your natural, adopted or foster child(ren), stepchild(ren), your SSDP’s child(ren) or any child for whom you have legal custody. They are eligible:

– Up to age 26.

– Regardless of age, if fully disabled and unmarried, provided he/she became fully disabled prior to age 19 or between the ages of 19 and 26, if the child was covered by the plan when the disability occurred.

Dependent Verification of EligibilityWhen you first enroll, or if you change coverage mid-year due to a qualified IRS family status change, you are required to provide documentation substantiating the

eligibility of your dependent(s) within 31 days of the change or enrollment.

If documentation is not received within 31 days, a letter will be mailed to you requesting the documentation within a given deadline. Events that require documentation to support the change include:

• Spouse with a last name different than yours

– Document(s): Marriage certificate OR joint tax return (current or previous year only).

• Child with a last name different than yours

– Document(s): Birth certificate or a court document awarding custody or requiring coverage.

• Dependent child over age 26

– Document(s): Birth certificate AND a Social Security Disability Award or letter from a physician AND the parent’s tax return claiming the child (current or previous year only).

• Same-Sex Domestic Partner (SSDP)

– Document(s): Affidavit of Domestic Partnership and a document validating the partnership, such as a joint bank account statement, utility bill or mortgage/lease/rental agreement.

• Employee with five dependents who adds a sixth or more dependents

– Document(s): Birth certificate AND either a court document or the tax return from the parent claiming the child must be submitted (current or previous year only).

• Employee with a 50+ age difference with dependent(s)

– Document(s): Birth certificate AND either a court document or the tax return from the parent claiming the child must be submitted (current or previous year only).

REMINDER: You must provide the documents listed above to the Employee Resource Center within 31 days from your initial election or mid-year family status change if one of the above situations applies to you and your family. If documentation is not received in a timely manner, the election/change requested will not be processed and the affected dependents will not be covered under Emory Healthcare’s plans. Legible copies of required documents are acceptable.

12/15 2016 Benefits Enrollment Guide 3

How to EnrollEnroll Online Enrolling is easy and available 24 hours a day through e-Vantage on www.ourehc.org and Self Service. You can enroll online at any public access computer that has Internet connectivity. To access e-Vantage, you will need your network ID and password. If you do not know your network ID or password, call 8-HELP at 404-778-4357.

Steps to Enrolling Online 1. Once logged in to e-Vantage, click on Self Service,

then Benefits and then Benefits Enrollment.

2. Choose Select to view your current elections and the new election options.

3. Complete the certifications for the Spouse/SSDP medical charge and the tobacco surcharge.

4. After selecting your elections and covered dependents, if any, your payroll deductions will be displayed.

5. You will be prompted at the bottom of the page to Continue to finalize your elections.

6. Click Submit after reading the Authorize Elections Statement. Note: You have not enrolled until you click Submit.

7. Click View/Print to bring up a printable pdf confirmation page. Make sure to save a copy of your confirmation page and carefully review it for accuracy.

• Emory University Hospital - Learning Resource Center

(2nd Floor, Room E214)

- Human Resources (2nd Floor, Room D201)

Don’t have access to a computer? No need to worry! The locations listed below have computers available Monday through Friday. For times, go to www.ourehc.org, Employee Resources and select Contact HR under Need Help.

• Emory University Orthopaedics & Spine Hospital - Human Resources

• Emory Johns Creek Hospital - Human Resources

• Emory Saint Joseph’s Hospital

- Human Resources

• Emory Wesley Woods Center- Houston Building Main Lobby

• Emory University Hospital Midtown

- Learning Resource Center (Glenn Bldg, 2nd Floor, Room 4709)

- Human Resources (W.W. Orr Bldg, 5th Floor)

2016 Benefits Enrollment Guide 12/154

Change in Your Coverage Mid-Year The IRS provides strict regulations about changes to pretax elections during the plan year. If you experience a qualified IRS family status change mid-year, you are permitted to make a change within 31 days of the event.

If the change request is not completed within 31 days of the event, you will not be able to change your elections until the following year’s annual benefits enrollment period, which means the change will not be effective until January 1 of the following year. Below is a list of some of the more commonly known qualified family status changes:

• Marriage, divorce or annulment, or permanent separation from a same-sex domestic partner

• Birth of a child

• Placement of a foster child or child for adoption with you, or assumption of legal guardianship of a child

• Change in your spouse’s/SSDP’s or dependent’s employment status that affects benefits eligibility, including termination or commencement of employment or change in worksite

• You or your spouse/SSDP returns from unpaid leave of absence

• You or your dependent becomes eligible or loses eligibility for Medicare or Medicaid

• The death of your spouse/SSDP or dependent

• Court ordered coverage of your child by you or your spouse/SSDP, allowing you to add or drop the child’s coverage

• Change in your employment that affects benefits eligibility (working at least 20 hours per week)

• Loss of eligibility for a dependent

• Change in dependent care provider or cost for Dependent Day Care Flexible Spending Account

The change you request must be consistent with the qualifying event. To make a family status change, go to www.ourehc.org, log in to e-Vantage and go to Self Service. In most cases, when you enter your family status change through Self Service and make your elections, the process is complete. However, some mid-year changes also require documentation to be submitted within 31 days of the event. Please refer to the below section for a list of events that require documentation.

Please contact the Employee Resource Center at 404-686-6044 for more details.

Dependent loss of the state’s CHIP plan

Judgment, Decree or Court Order to add coverage for a dependent child

Legally married couples with different last names

Dependent child with a last name different than yours

Beginning Same-Sex Domestic Partner Relationship

Ending Same-Sex Domestic Partner Relationship

Change of residence that is inside or outside of the plan area

Family Status Change Event Documentation to Submit

A copy of the Certificate of Creditable Coverage or a termination letter that lists the date your coverage ended

A copy of the court order awarding custody or requiring coverage

Proof of marriage such as marriage certificate or jointly filed tax return

A copy of the birth certificate or a court document awarding custody or requiring coverage

Statement of Same-Sex Domestic Partnership or a civil union certificate from a state or governmental agency that recognizes civil unions

Complete the Same-Sex Domestic Partnership Termination form

A copy of your visa and/or passport that shows the date of entry or exit from the plan area

12/15 2016 Benefits Enrollment Guide 5

Medical Plans

You have a choice of two medical plans:

• Plan 1 — HSA Plan

• Plan 2 — POS Plan

Both plans use the same provider networks; however, there are key differences in how each plan works, including deductibles, co-pays and co-insurance.

Network OptionsBoth plans have three Network options:

• Emory Healthcare Network (EHN): Providers and facilities that are owned by and affiliated with Emory Healthcare give you the maximum benefit available under the plans, with lower co-pays, co-insurance and deductibles. For a list of EHN providers, go to page 27.

• Aetna National (In-Network): Providers and facilities are part of both medical plans through Aetna. Co-pays, co-insurance and deductibles are higher than with the EHN.

• Out-of-Core-Network: Providers and facilities that are not participating with Aetna are considered Out-of-Core-Network. Costs are the highest.

To locate an EHN or Aetna National (In-Network) physician or facility, go to www.aetna.com/docfind/custom/emory or call 1-800-847-9026.

Preventive CareRoutine preventive care is covered at 100% under both medical plans. Preventive care can help you identify potential health risks before they become real health problems. These services include annual physicals, well-child visits, immunizations, health screenings and more. (See www.ourehc.org and click on Employee Resources and Your Benefits for a list of services.)

Tier ZeroBoth plans offer Tier Zero for prescription drugs. With Tier Zero, generic forms of birth control and prescription medications used to prevent and treat chronic health conditions, such as congestive heart failure (CHF), diabetes, high blood pressure, high cholesterol, tobacco addiction and more, are covered at 100%. For Tier Zero medications, you pay $0 for a 30- or 90-day supply.

For a complete list of Tier Zero medications, go to www .ourehc.org and click on Employee Resources and Your Benefits. Please note that, from time to time, this list will change as medications will be moved off patent protection (brand) and placed in a generic status. It is also possible for generic medications to fall off the list as they become available over-the-counter. For the most up-to-date information or to request an updated listing, please contact CVS/caremark at 1-866-601-6935.

Everyone’s health care needs are different. That’s why it’s important to carefully decide which medical plan will work

best for you. In this section, you will find information on the two medical plans that Emory Healthcare offers.

What Is the Same in Both Medical Plans? • Same broad network of physicians in Georgia and nationally

(EHN and Aetna National [In-Network]).

• Routine preventive care is $0 when service is received within the EHN or Aetna National (In-Network).

• Tier Zero (you pay $0 for certain generic prescription drugs).

• Neither plan requires you to select a primary care physician or get a referral to see a specialist.

• Unlimited lifetime maximum applied across both plans and networks.

• The opportunity to earn incentives for wellness activities (see page 12 for more details).

Premium Assistance Under Medicaid and the Children’s Health Insurance Program (CHIP)If you or your children are eligible for Medicaid or CHIP and you are eligible for health coverage from your employer, your state may have a premium assistance program that can help pay for coverage.These states use funds from their Medicaid or CHIP programs to help people who are eligible for these programs, but also have access to health insurance through their employer. For additional information, go to www.ourehc.org, Employee Resources and Your Benefits. Information can be found under the heading “Notices, Summaries, Reports & Resources.”

2016 Benefits Enrollment Guide 12/156

Medical Plans HSA Plan

DeductibleAll eligible expenses incurred by you or your covered dependents throughout the plan year apply toward meeting the annual deductible: $1,350 (Employee Only) or $2,700 (Employee + Spouse/SSDP, Employee + Children or Family) within the EHN or $1,500 (Employee Only) or $3,000 (Employee + Spouse/SSDP, Employee + Children or Family) for In-Network. As expenses are incurred, including ER visits and prescription drugs, you can use funds that have accumulated in your HSA to cover these costs. Once your HSA balance is exhausted, any remaining portion of your deductible that needs to be met for the year will be an out-of-pocket expense and your financial responsibility. The annual deductible must be satisfied before any plan expenses are paid by co-insurance, with the exception of preventive care and Tier Zero prescriptions, which are covered at 100%. If you enroll and elect employee and dependent coverage, any covered expenses incurred will apply toward meeting the family deductible of $2,700 (EHN) or $3,000 (In-Network) before any expenses are covered under co-insurance.

Co-Insurance Once the annual deductible is satisfied, the HSA Plan works like a traditional plan by paying the majority of expenses through co-insurance. EHN care is covered at 90% (you pay 10%); In-Network care is covered at 80% (you pay 20%) and Out-of-Core-Network care is covered at 60% (you pay 40%).

Out-of-Pocket Maximum Like a traditional plan, there is a maximum amount that you are financially responsible for under the plan each year. Once your out-of-pocket eligible expenses reach the annual maximum of $3,200 (Employee Only) or $6,400 (Employee + Spouse/SSDP, Employee + Children or Family) within the EHN or In-Network, the plan pays 100% of eligible expenses for you and your covered dependents for the remainder of the plan year. The individual out-of-pocket maximum of $3,200 within the EHN and In-Network will be applied to a covered family member who incurs medical expenses after the Family deductible of $2,700 within the EHN or $3,000 within the In-Network is completed. This eliminates the need for the full Family out-of-pocket maximum to be satisfied if only one family member needs medical care. However, the combined medical charges incurred by additional family members will satisfy the full Family out-of-pocket maximum. When the Family out-of-pocket maximum is satisfied, eligible expenses for all family members will be covered at 100% for the remainder of the plan year.

It is important to note that, other than preventive care, you have to pay 100% of your eligible medical expenses, including prescription drugs, until your annual deductible is met.* Once met, the plan provides coverage through co-insurance. You need to carefully consider the balance in your HSA and your ability to meet these financial obligations in the event of an illness, injury or accident. * If you elect Employee+Spouse, Employee+Children or Family level coverage, you must meet the family deductible before the plan pays.

Plan 1 – HSA PlanThe HSA Plan, a consumer-driven medical plan with a Health Savings Account, puts you in charge of how your health care dollars are spent. Features of this plan include:

• The same covered services and network of providers as the POS Plan with a different way to pay and save for health care expenses.

• A Health Savings Account (HSA) with tax advantages, funded in part by Emory Healthcare. The HSA gives you the flexibility to choose how to spend your health care dollars.

• 100% coverage for all preventive care when services are in the Emory Healthcare Network (EHN) or Aetna National Network (In-Network).

Like the POS Plan, the HSA Plan has deductibles, co-insurance and an out-of-pocket maximum to protect you in the event you have significant medical expenses during the year.

Learn more about this plan by viewing the HSA Plan Quick Guide posted on the intranet. Go to www.ourehc.org and click on Employee Resources and Your Benefits.

12/15 2016 Benefits Enrollment Guide 7

Medical Plans HSA Plan Continued

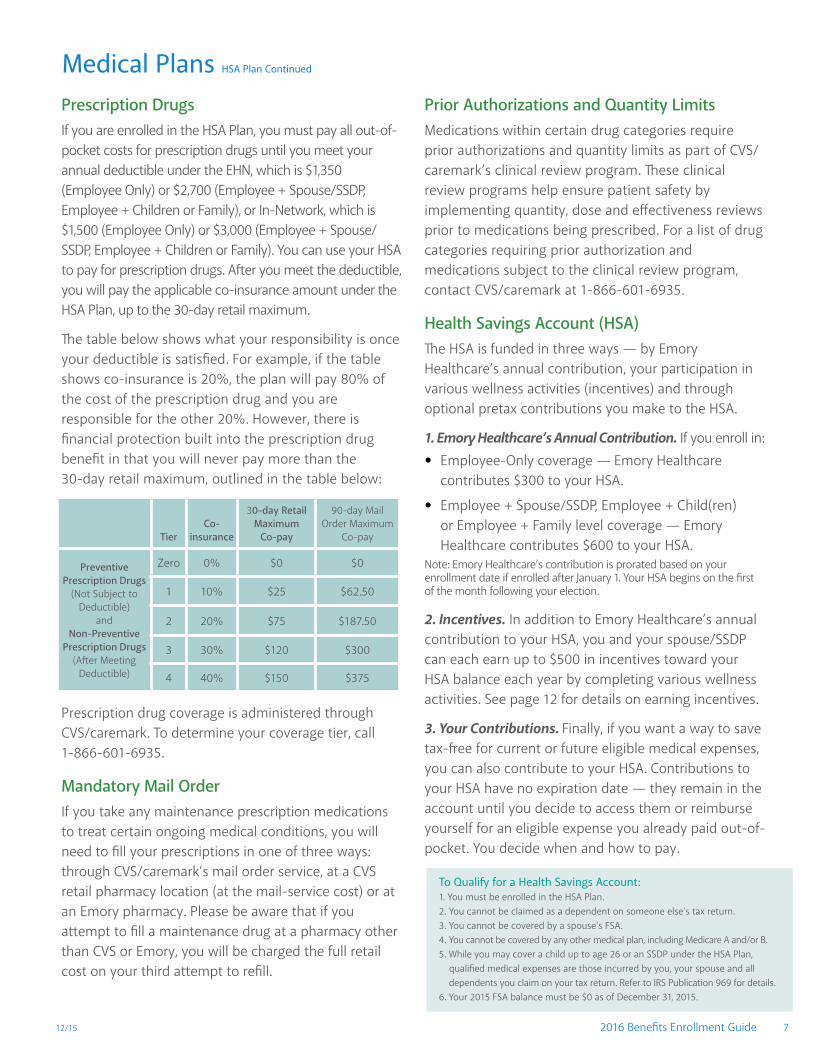

Prescription DrugsIf you are enrolled in the HSA Plan, you must pay all out-of-pocket costs for prescription drugs until you meet your annual deductible under the EHN, which is $1,350 (Employee Only) or $2,700 (Employee + Spouse/SSDP, Employee + Children or Family), or In-Network, which is $1,500 (Employee Only) or $3,000 (Employee + Spouse/SSDP, Employee + Children or Family). You can use your HSA to pay for prescription drugs. After you meet the deductible, you will pay the applicable co-insurance amount under the HSA Plan, up to the 30-day retail maximum.

The table below shows what your responsibility is once your deductible is satisfied. For example, if the table shows co-insurance is 20%, the plan will pay 80% of the cost of the prescription drug and you are responsible for the other 20%. However, there is financial protection built into the prescription drug benefit in that you will never pay more than the 30-day retail maximum, outlined in the table below:

Prescription drug coverage is administered through CVS/caremark. To determine your coverage tier, call 1-866-601-6935.

Mandatory Mail OrderIf you take any maintenance prescription medications to treat certain ongoing medical conditions, you will need to fill your prescriptions in one of three ways: through CVS/caremark’s mail order service, at a CVS retail pharmacy location (at the mail-service cost) or at an Emory pharmacy. Please be aware that if you attempt to fill a maintenance drug at a pharmacy other than CVS or Emory, you will be charged the full retail cost on your third attempt to refill.

Prior Authorizations and Quantity LimitsMedications within certain drug categories require prior authorizations and quantity limits as part of CVS/caremark’s clinical review program. These clinical review programs help ensure patient safety by implementing quantity, dose and effectiveness reviews prior to medications being prescribed. For a list of drug categories requiring prior authorization and medications subject to the clinical review program, contact CVS/caremark at 1-866-601-6935.

Health Savings Account (HSA) The HSA is funded in three ways — by Emory Healthcare’s annual contribution, your participation in various wellness activities (incentives) and through optional pretax contributions you make to the HSA.

1. Emory Healthcare’s Annual Contribution. If you enroll in: • Employee-Only coverage — Emory Healthcare

contributes $300 to your HSA.

• Employee + Spouse/SSDP, Employee + Child(ren) or Employee + Family level coverage — Emory Healthcare contributes $600 to your HSA.

Note: Emory Healthcare’s contribution is prorated based on your enrollment date if enrolled after January 1. Your HSA begins on the first of the month following your election.

2. Incentives. In addition to Emory Healthcare’s annual contribution to your HSA, you and your spouse/SSDP can each earn up to $500 in incentives toward your HSA balance each year by completing various wellness activities. See page 12 for details on earning incentives.

3. Your Contributions. Finally, if you want a way to save tax-free for current or future eligible medical expenses, you can also contribute to your HSA. Contributions to your HSA have no expiration date — they remain in the account until you decide to access them or reimburse yourself for an eligible expense you already paid out-of-pocket. You decide when and how to pay.

To Qualify for a Health Savings Account: 1. You must be enrolled in the HSA Plan.2. You cannot be claimed as a dependent on someone else’s tax return.3. You cannot be covered by a spouse’s FSA.4. You cannot be covered by any other medical plan, including Medicare A and/or B.5. While you may cover a child up to age 26 or an SSDP under the HSA Plan, qualified medical expenses are those incurred by you, your spouse and all dependents you claim on your tax return. Refer to IRS Publication 969 for details.6. Your 2015 FSA balance must be $0 as of December 31, 2015.

TierCo-

insurance

30-day RetailMaximum

Co-pay

90-day Mail Order Maximum

Co-pay

PreventivePrescription Drugs

(Not Subject to Deductible)

andNon-Preventive

Prescription Drugs (After Meeting

Deductible)

Zero 0% $0 $0

1 10% $25 $62.50

2 20% $75 $187.50

3 30% $120 $300

4 40% $150 $375

2016 Benefits Enrollment Guide 12/158

Medical Plans HSA Plan Continued

WHAT’S DIFFERENT ABOUT A HEALTH SAVINGS ACCOUNT?

1. The Health Savings Account (HSA) is only available if you participate in the HSA Plan. The money is yours, is held in an investment account and is portable — it goes with you to be used for qualified medical expenses if you leave Emory Healthcare or when you retire.

2. If you are enrolled in the HSA Plan, you may not participate in a general Healthcare Flexible Spending Account (FSA). However, you can participate in the Limited Aetna Healthcare FSA for dental and vision, and then for medical expenses once you have met your deductible.

3. If you are enrolled in the HSA Plan, you may still participate in the Dependent Day Care Flexible Spending Account (FSA).

Additional HSA Features• Once your HSA account is open, you will receive a

welcome kit from Aetna/PayFlex. The kit will include an Aetna/PayFlex MasterCard debit card to pay eligible expenses.

• Withdrawals from HSAs for qualified medical expenses are tax-free. If you withdraw money for any reason other than qualified medical expenses, you must pay income tax and a 20% IRS tax penalty.

• You must have a balance in your account to make a withdrawal.

• Money in the HSA will be invested in a money market fund.

• The maximum you can contribute to an HSA in one year is set by the IRS (in 2016, $3,350 for single coverage and $6,750 for family coverage). If you are age 55 or older, you can contribute additional catch-up contributions. It is your responsibility to make sure your HSA contributions, including any employer or incentive contributions, do not go over the IRS maximum. The minimum you can contribute is $200.

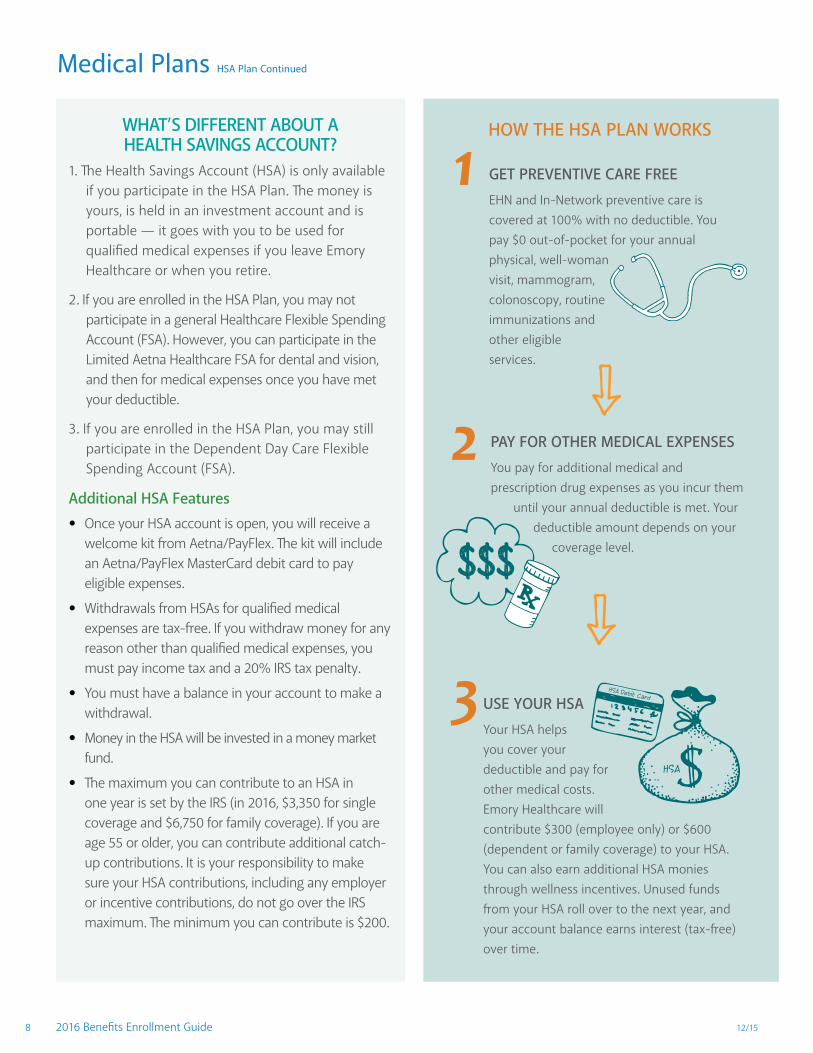

HOW THE HSA PLAN WORKS

GET PREVENTIVE CARE FREE EHN and In-Network preventive care is covered at 100% with no deductible. You pay $0 out-of-pocket for your annual physical, well-woman visit, mammogram, colonoscopy, routine immunizations and other eligible services.

1

PAY FOR OTHER MEDICAL EXPENSESYou pay for additional medical and prescription drug expenses as you incur them

until your annual deductible is met. Your deductible amount depends on your

coverage level.

2

USE YOUR HSAYour HSA helps you cover your deductible and pay for other medical costs. Emory Healthcare will contribute $300 (employee only) or $600 (dependent or family coverage) to your HSA. You can also earn additional HSA monies through wellness incentives. Unused funds from your HSA roll over to the next year, and your account balance earns interest (tax-free) over time.

3 HSA Debit Card

HSA

12/15 2016 Benefits Enrollment Guide 9

Medical Plans POS Plan

The POS Plan allows members to receive services from a national network of providers and facilities. It is an open access plan that:

• Provides the flexibility to choose any provider

• Does not require that a Primary Care Physician (PCP) be identified or selected

• Does not require a PCP referral to see a specialist

With the POS Plan, your biweekly contribution is higher than with the HSA Plan, but your annual deductible is lower. You cannot open a Health Savings Account (HSA) or receive HSA contributions from Emory Healthcare. You do have the option of enrolling in a Healthcare Flexible Spending Account (FSA) which allows you to set aside up to $2,550 pretax dollars to help pay for medical expenses. See page 13 for more information about the FSA.

EHN and In-Network preventive care is covered at 100% and is not subject to the deductible. For all other medical services, the plan pays a portion of your covered expenses - 90% for Emory Healthcare Network (EHN), 80% In-Network (Aetna National) and 60% (Out-of-Core-Network) - after you pay the annual deductible. Office visits are covered with a co-payment. Prescription drugs are covered through co-insurance.

The POS Plan also has an out-of-pocket maximum to protect you in the event you have significant medical expenses during the year. Co-payments, deductibles and co-insurance count toward the out-of-pocket maximum.

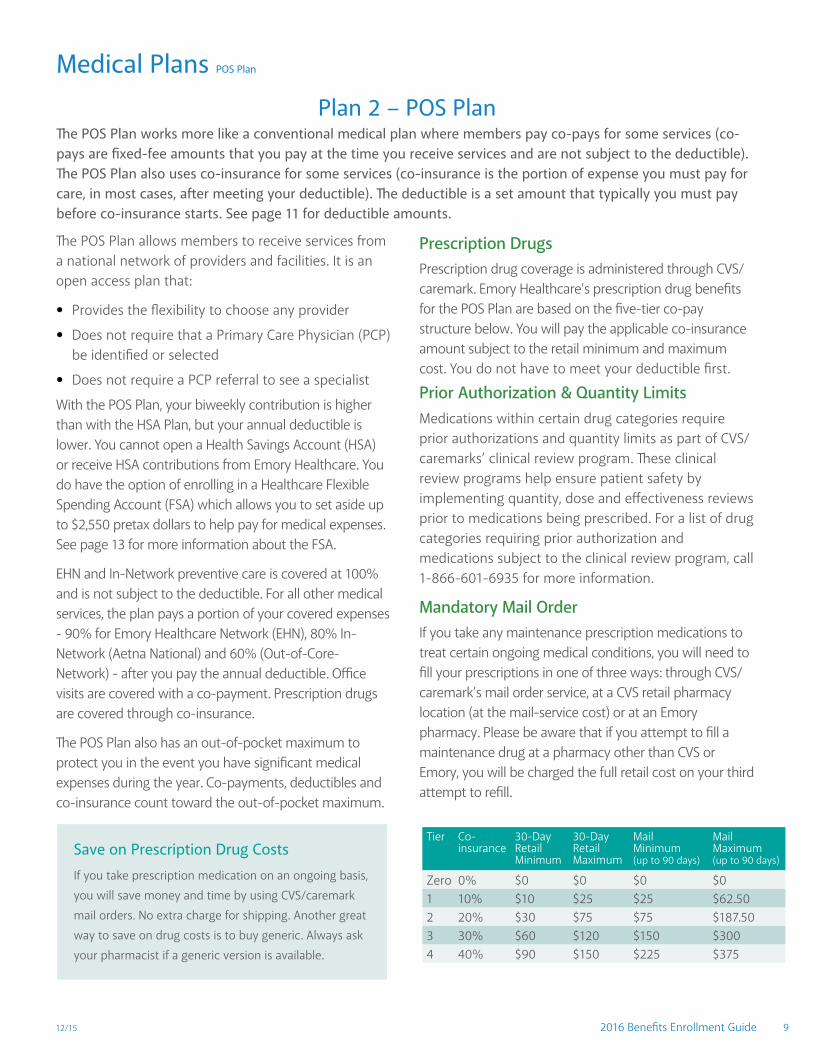

Prescription Drugs Prescription drug coverage is administered through CVS/caremark. Emory Healthcare’s prescription drug benefits for the POS Plan are based on the five-tier co-pay structure below. You will pay the applicable co-insurance amount subject to the retail minimum and maximum cost. You do not have to meet your deductible first.

Prior Authorization & Quantity Limits Medications within certain drug categories require prior authorizations and quantity limits as part of CVS/caremarks’ clinical review program. These clinical review programs help ensure patient safety by implementing quantity, dose and effectiveness reviews prior to medications being prescribed. For a list of drug categories requiring prior authorization and medications subject to the clinical review program, call 1-866-601-6935 for more information.

Mandatory Mail OrderIf you take any maintenance prescription medications to treat certain ongoing medical conditions, you will need to fill your prescriptions in one of three ways: through CVS/caremark’s mail order service, at a CVS retail pharmacy location (at the mail-service cost) or at an Emory pharmacy. Please be aware that if you attempt to fill a maintenance drug at a pharmacy other than CVS or Emory, you will be charged the full retail cost on your third attempt to refill.

Save on Prescription Drug Costs

If you take prescription medication on an ongoing basis,

you will save money and time by using CVS/caremark

mail orders. No extra charge for shipping. Another great

way to save on drug costs is to buy generic. Always ask

your pharmacist if a generic version is available.

Plan 2 – POS PlanThe POS Plan works more like a conventional medical plan where members pay co-pays for some services (co-pays are fixed-fee amounts that you pay at the time you receive services and are not subject to the deductible). The POS Plan also uses co-insurance for some services (co-insurance is the portion of expense you must pay for care, in most cases, after meeting your deductible). The deductible is a set amount that typically you must pay before co-insurance starts. See page 11 for deductible amounts.

Tier Co-insurance

30-Day Retail Minimum

30-Day Retail Maximum

Mail Minimum (up to 90 days)

Mail Maximum (up to 90 days)

Zero 0% $0 $0 $0 $01 10% $10 $25 $25 $62.502 20% $30 $75 $75 $187.503 30% $60 $120 $150 $3004 40% $90 $150 $225 $375

2016 Benefits Enrollment Guide 12/1510

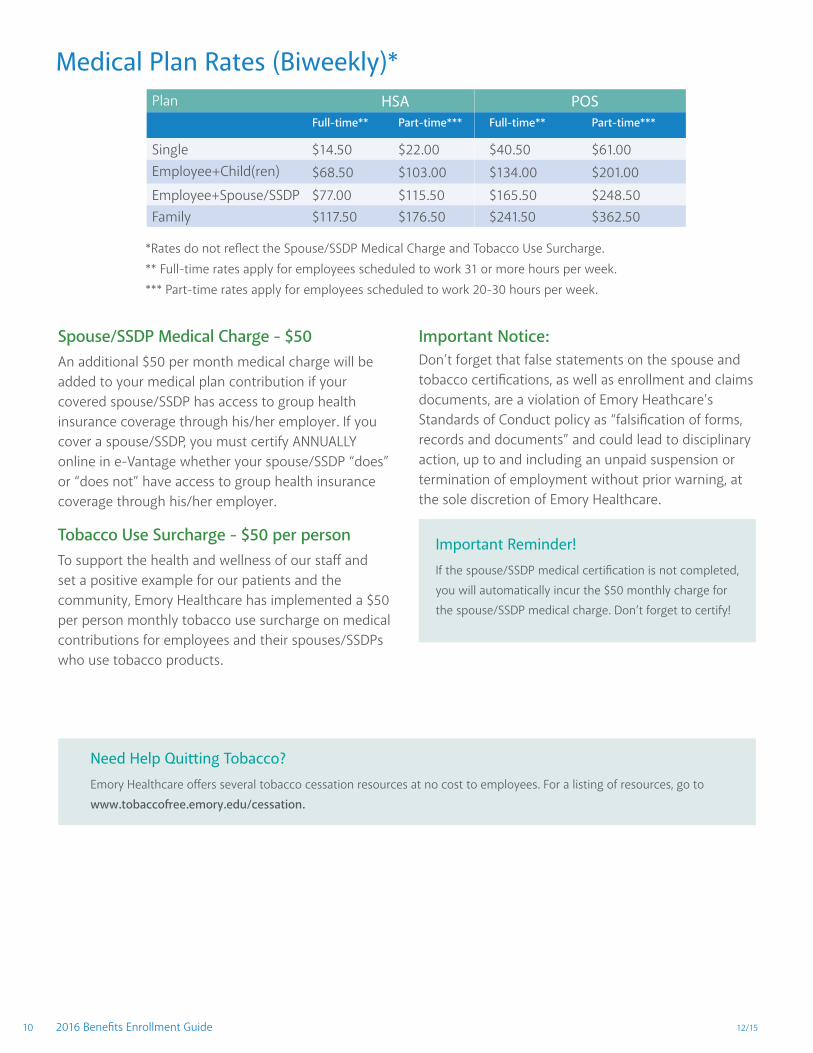

Medical Plan Rates (Biweekly)*

Spouse/SSDP Medical Charge - $50 An additional $50 per month medical charge will be added to your medical plan contribution if your covered spouse/SSDP has access to group health insurance coverage through his/her employer. If you cover a spouse/SSDP, you must certify ANNUALLY online in e-Vantage whether your spouse/SSDP “does” or “does not” have access to group health insurance coverage through his/her employer.

Tobacco Use Surcharge - $50 per person To support the health and wellness of our staff and set a positive example for our patients and the community, Emory Healthcare has implemented a $50 per person monthly tobacco use surcharge on medical contributions for employees and their spouses/SSDPs who use tobacco products.

Need Help Quitting Tobacco?

Emory Healthcare offers several tobacco cessation resources at no cost to employees. For a listing of resources, go to

www.tobaccofree.emory.edu/cessation.

Important Reminder!

If the spouse/SSDP medical certification is not completed,

you will automatically incur the $50 monthly charge for

the spouse/SSDP medical charge. Don’t forget to certify!

*Rates do not reflect the Spouse/SSDP Medical Charge and Tobacco Use Surcharge.** Full-time rates apply for employees scheduled to work 31 or more hours per week.*** Part-time rates apply for employees scheduled to work 20-30 hours per week.

Plan HSA POSFull-time** Part-time*** Full-time** Part-time***

Single $14.50 $22.00 $40.50 $61.00Employee+Child(ren) $68.50 $103.00 $134.00 $201.00

Employee+Spouse/SSDP $77.00 $115.50 $165.50 $248.50Family $117.50 $176.50 $241.50 $362.50

Important Notice:Don’t forget that false statements on the spouse and tobacco certifications, as well as enrollment and claims documents, are a violation of Emory Heathcare’s Standards of Conduct policy as “falsification of forms, records and documents” and could lead to disciplinary action, up to and including an unpaid suspension or termination of employment without prior warning, at the sole discretion of Emory Healthcare.

12/15 2016 Benefits Enrollment Guide 11

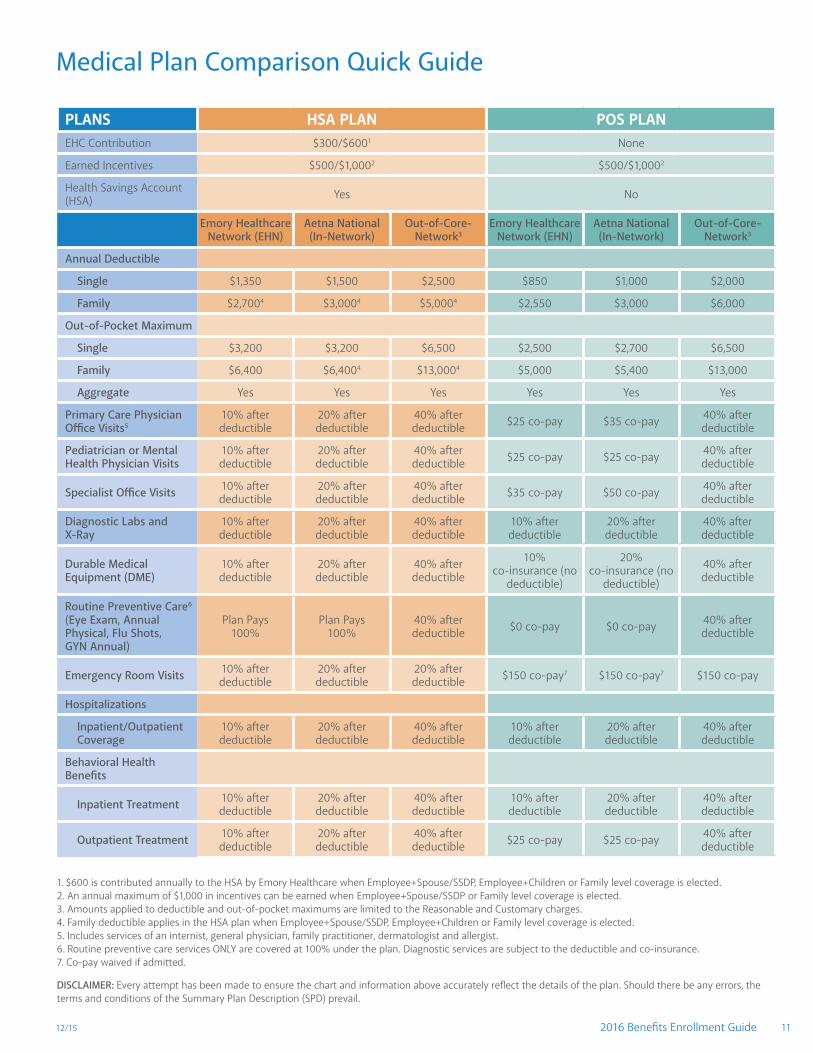

Medical Plan Comparison Quick Guide

1. $600 is contributed annually to the HSA by Emory Healthcare when Employee+Spouse/SSDP, Employee+Children or Family level coverage is elected. 2. An annual maximum of $1,000 in incentives can be earned when Employee+Spouse/SSDP or Family level coverage is elected. 3. Amounts applied to deductible and out-of-pocket maximums are limited to the Reasonable and Customary charges. 4. Family deductible applies in the HSA plan when Employee+Spouse/SSDP, Employee+Children or Family level coverage is elected. 5. Includes services of an internist, general physician, family practitioner, dermatologist and allergist.6. Routine preventive care services ONLY are covered at 100% under the plan. Diagnostic services are subject to the deductible and co-insurance. 7. Co-pay waived if admitted.

DISCLAIMER: Every attempt has been made to ensure the chart and information above accurately reflect the details of the plan. Should there be any errors, the terms and conditions of the Summary Plan Description (SPD) prevail.

PLANS HSA PLAN POS PLANEHC Contribution $300/$6001 None

Earned Incentives $500/$1,0002 $500/$1,0002

Health Savings Account (HSA) Yes No

Emory Healthcare Network (EHN)

Aetna National (In-Network)

Out-of-Core-Network3

Emory Healthcare Network (EHN)

Aetna National (In-Network)

Out-of-Core-Network3

Annual Deductible

Single $1,350 $1,500 $2,500 $850 $1,000 $2,000

Family $2,7004 $3,0004 $5,0004 $2,550 $3,000 $6,000

Out-of-Pocket Maximum

Single $3,200 $3,200 $6,500 $2,500 $2,700 $6,500

Family $6,400 $6,4004 $13,0004 $5,000 $5,400 $13,000

Aggregate Yes Yes Yes Yes Yes Yes

Primary Care Physician Office Visits5

10% after deductible

20% after deductible

40% after deductible $25 co-pay $35 co-pay 40% after

deductible

Pediatrician or Mental Health Physician Visits

10% after deductible

20% after deductible

40% after deductible $25 co-pay $25 co-pay 40% after

deductible

Specialist Office Visits 10% after deductible

20% after deductible

40% after deductible $35 co-pay $50 co-pay 40% after

deductible

Diagnostic Labs and X-Ray

10% after deductible

20% after deductible

40% after deductible

10% after deductible

20% after deductible

40% after deductible

Durable Medical Equipment (DME)

10% after deductible

20% after deductible

40% after deductible

10%co-insurance (no

deductible)

20%co-insurance (no

deductible)

40% after deductible

Routine Preventive Care6 (Eye Exam, Annual Physical, Flu Shots, GYN Annual)

Plan Pays 100%

Plan Pays 100%

40% after deductible $0 co-pay $0 co-pay 40% after

deductible

Emergency Room Visits 10% after deductible

20% after deductible

20% after deductible $150 co-pay7 $150 co-pay7 $150 co-pay

Hospitalizations

Inpatient/Outpatient Coverage

10% after deductible

20% after deductible

40% after deductible

10% after deductible

20% after deductible

40% after deductible

Behavioral Health Benefits

Inpatient Treatment 10% after deductible

20% after deductible

40% after deductible

10% after deductible

20% after deductible

40% after deductible

Outpatient Treatment 10% after deductible

20% after deductible

40% after deductible $25 co-pay $25 co-pay 40% after

deductible

2016 Benefits Enrollment Guide 12/1512

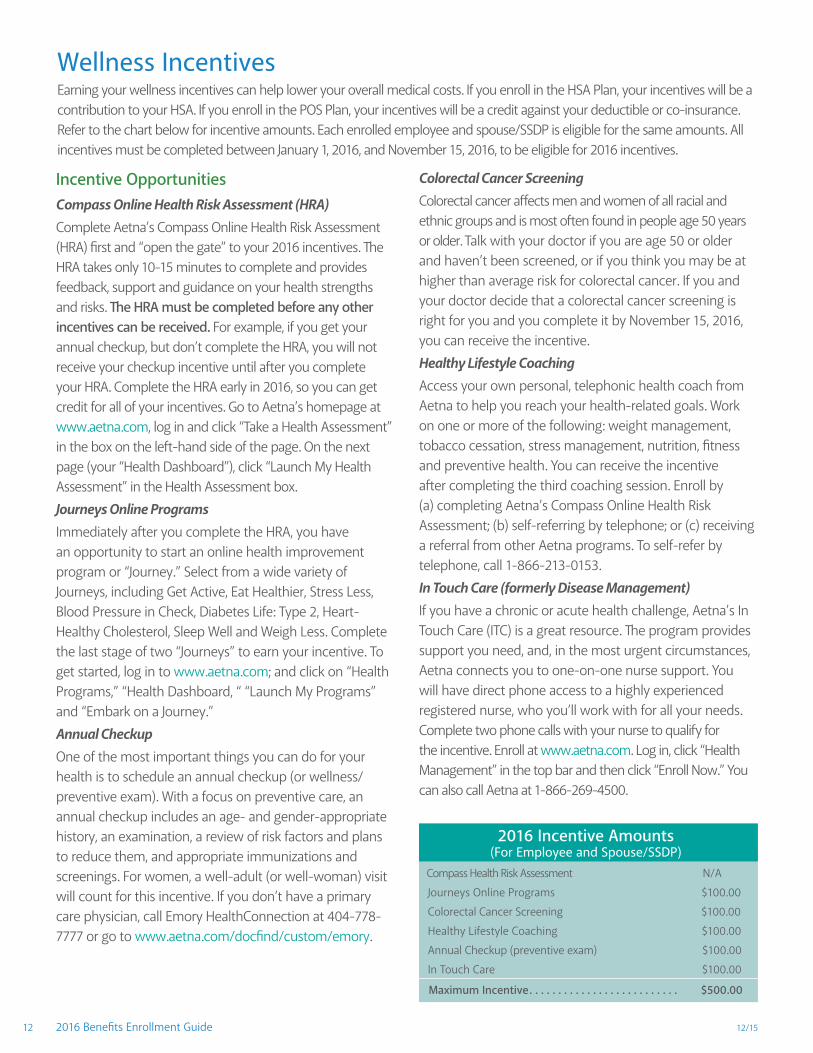

Wellness Incentives

Incentive Opportunities Compass Online Health Risk Assessment (HRA)Complete Aetna’s Compass Online Health Risk Assessment (HRA) first and “open the gate” to your 2016 incentives. The HRA takes only 10-15 minutes to complete and provides feedback, support and guidance on your health strengths and risks. The HRA must be completed before any other incentives can be received. For example, if you get your annual checkup, but don’t complete the HRA, you will not receive your checkup incentive until after you complete your HRA. Complete the HRA early in 2016, so you can get credit for all of your incentives. Go to Aetna’s homepage at www.aetna.com, log in and click “Take a Health Assessment” in the box on the left-hand side of the page. On the next page (your “Health Dashboard”), click “Launch My Health Assessment” in the Health Assessment box.Journeys Online ProgramsImmediately after you complete the HRA, you have an opportunity to start an online health improvement program or “Journey.” Select from a wide variety of Journeys, including Get Active, Eat Healthier, Stress Less, Blood Pressure in Check, Diabetes Life: Type 2, Heart-Healthy Cholesterol, Sleep Well and Weigh Less. Complete the last stage of two “Journeys” to earn your incentive. To get started, log in to www.aetna.com; and click on “Health Programs,” “Health Dashboard, “ “Launch My Programs” and “Embark on a Journey.”Annual Checkup One of the most important things you can do for your health is to schedule an annual checkup (or wellness/preventive exam). With a focus on preventive care, an annual checkup includes an age- and gender-appropriate history, an examination, a review of risk factors and plans to reduce them, and appropriate immunizations and screenings. For women, a well-adult (or well-woman) visit will count for this incentive. If you don’t have a primary care physician, call Emory HealthConnection at 404-778-7777 or go to www.aetna.com/docfind/custom/emory .

Colorectal Cancer ScreeningColorectal cancer affects men and women of all racial and ethnic groups and is most often found in people age 50 years or older. Talk with your doctor if you are age 50 or older and haven’t been screened, or if you think you may be at higher than average risk for colorectal cancer. If you and your doctor decide that a colorectal cancer screening is right for you and you complete it by November 15, 2016, you can receive the incentive.Healthy Lifestyle Coaching Access your own personal, telephonic health coach from Aetna to help you reach your health-related goals. Work on one or more of the following: weight management, tobacco cessation, stress management, nutrition, fitness and preventive health. You can receive the incentive after completing the third coaching session. Enroll by (a) completing Aetna’s Compass Online Health Risk Assessment; (b) self-referring by telephone; or (c) receiving a referral from other Aetna programs. To self-refer by telephone, call 1-866-213-0153. In Touch Care (formerly Disease Management) If you have a chronic or acute health challenge, Aetna’s In Touch Care (ITC) is a great resource. The program provides support you need, and, in the most urgent circumstances, Aetna connects you to one-on-one nurse support. You will have direct phone access to a highly experienced registered nurse, who you’ll work with for all your needs. Complete two phone calls with your nurse to qualify for the incentive. Enroll at www.aetna.com. Log in, click “Health Management” in the top bar and then click “Enroll Now.” You can also call Aetna at 1-866-269-4500.

2016 Incentive Amounts(For Employee and Spouse/SSDP)

Compass Health Risk Assessment N/A

Journeys Online Programs $100.00

Colorectal Cancer Screening $100.00

Healthy Lifestyle Coaching $100.00

Annual Checkup (preventive exam) $100.00

In Touch Care $100.00

Maximum Incentive . . . . . . . . . . . . . . . . . . . . . . . . . . $500.00

Earning your wellness incentives can help lower your overall medical costs. If you enroll in the HSA Plan, your incentives will be a contribution to your HSA. If you enroll in the POS Plan, your incentives will be a credit against your deductible or co-insurance. Refer to the chart below for incentive amounts. Each enrolled employee and spouse/SSDP is eligible for the same amounts. All incentives must be completed between January 1, 2016, and November 15, 2016, to be eligible for 2016 incentives.

12/15 2016 Benefits Enrollment Guide 13

Flexible Spending Accounts (FSAs)

Healthcare FSA for POS PlanYou can contribute between $200 and $2,550 pretax annually into the Healthcare FSA. All money you elect to contribute is accessible immediately. The money you contribute can be used to cover out-of-pocket costs, such as:

• Medical expenses: co-pays, deductibles, co-insurance

• Dental expenses: deductibles and co-insurance • Vision expenses: prescription glasses, contact lenses,

co-pays • Prescription drug costs

• Over-the-counter drugs with a prescription

Limited Healthcare FSA for HSA Plan HSA Plan members are not eligible for the Healthcare FSA but do have access to a special Limited Healthcare FSA administered through Aetna/PayFlex. You may use the Limited FSA to pay for dental and vision expenses and then for medical expenses once your deductible has been met.

Dependent Day Care FSA Money you contribute into a Dependent Day Care FSA can be used toward care for a child under age 13, a physically or mentally disabled parent or child, or elder care for tax-qualified dependents. If you’re single or married and filing a joint tax return, you can contribute up to $5,000 into this FSA. If you’re married and file separately, you can contribute up to $2,500. If you are a highly compensated employee under the IRS definition, you are restricted to an annual contribution of no more than $2,400. Unlike the Healthcare FSA, you can only access the money that is currently in your account. To qualify for reimbursement, these expenses must be incurred so that you (and/or your spouse/SSDP) can work or go to school. HSA Plan members can also participate in the Dependent Day Care FSA.

A Flexible Spending Account (FSA) is funded with money you contribute on a pretax basis. You can use FSA funds to pay for qualified out-of-pocket health care costs for yourself and eligible dependents or dependent day care charges. According to IRS regulations, each year you must enroll during your annual benefits enrollment period if you want to participate in either a Healthcare FSA or a Dependent Day Care FSA. Aetna/PayFlex is Emory Healthcare’s Flexible Spending Account Administrator. Check your FSA balance online and locate more information at aetnanavigator.com.

Aetna/PayFlex CardNew FSA participants will automatically receive an Aetna/

PayFlex Card in the mail for 2016. Please activate the card

when you receive it. The use of the Aetna/PayFlex Card

is for convenience only. IRS guidelines still require you

to retain receipts for any eligible expense for which you

receive reimbursement. On occasion, Aetna/PayFlex may

request verification of expenses and you will need to submit

appropriate documentation for the expense. If not received,

the card will be deactivated until the expense can be

substantiated as eligible under IRS definitions. Check with

Aetna/PayFlex to determine what supporting documentation

is required.

Use It — Don’t Lose It The risk of forfeiting money from your Healthcare FSA has been

reduced by a grace period (extra time in the following year to

use your FSA money). You will be able to use any remaining

balance in your Healthcare FSA at the end of 2016 to pay for

expenses incurred through March 15, 2017. Any 2016 Healthcare

FSA funds not used by March 15, 2017, will be forfeited.

To avoid forfeiture, purchase items such as prescriptions,

eyeglasses, contact lenses and other approved Healthcare FSA

expenditures. Reimbursement requests using your previous

year’s remaining Healthcare FSA balance must be filed by

May 15, 2017. Please remember to keep all of your receipts,

as they are required for verification of expenses. If you have a

Dependent Day Care FSA, you do NOT have a grace period in

which to use remaining previous year balances. All expenses

must occur before December 31, 2016, and claims for the 2016

Dependent Day Care FSA must be filed no later than May 15,

2017, to receive reimbursement.

2016 Benefits Enrollment Guide 12/1514

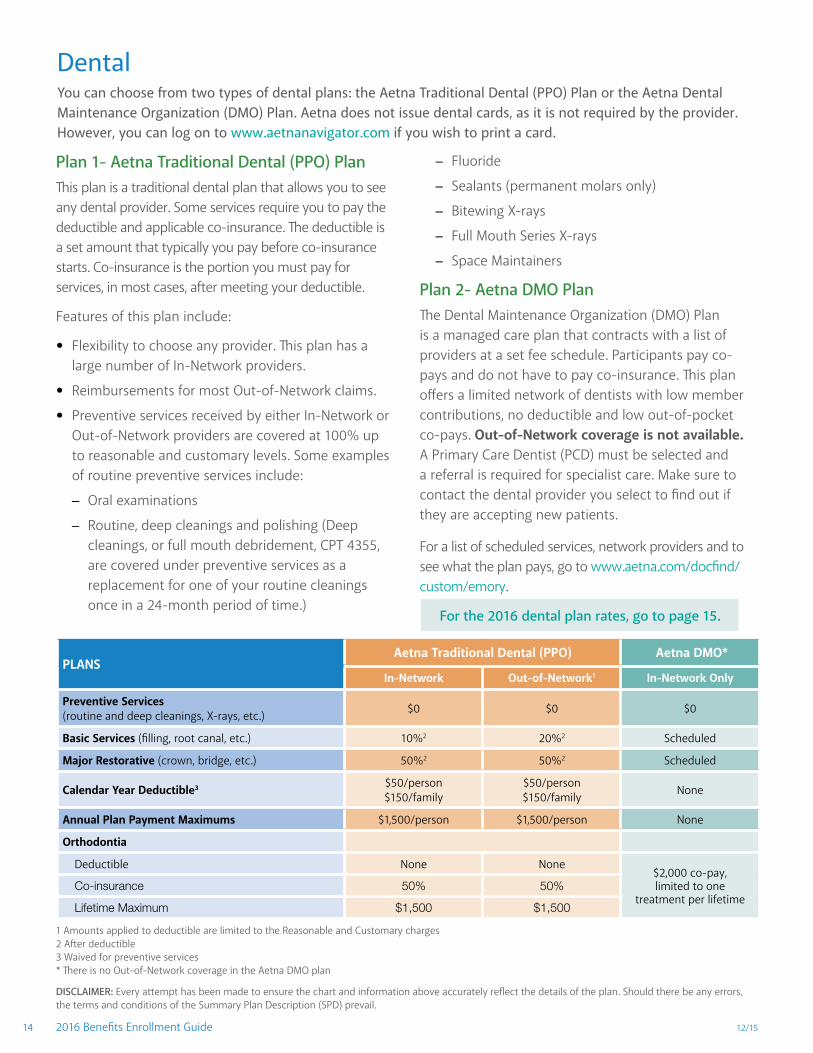

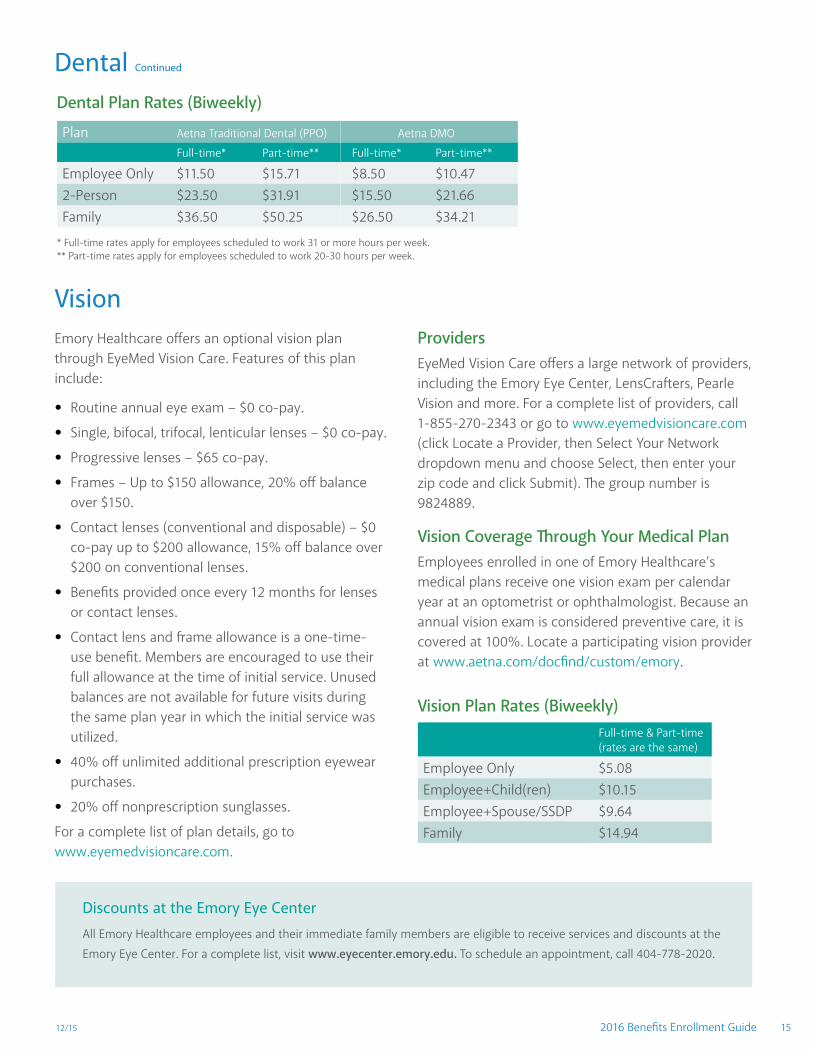

Dental

Plan 1- Aetna Traditional Dental (PPO) Plan This plan is a traditional dental plan that allows you to see any dental provider. Some services require you to pay the deductible and applicable co-insurance. The deductible is a set amount that typically you pay before co-insurance starts. Co-insurance is the portion you must pay for services, in most cases, after meeting your deductible.

Features of this plan include:

• Flexibility to choose any provider. This plan has a large number of In-Network providers.

• Reimbursements for most Out-of-Network claims.

• Preventive services received by either In-Network or Out-of-Network providers are covered at 100% up to reasonable and customary levels. Some examples of routine preventive services include:

– Oral examinations

– Routine, deep cleanings and polishing (Deep cleanings, or full mouth debridement, CPT 4355, are covered under preventive services as a replacement for one of your routine cleanings once in a 24-month period of time.)

– Fluoride

– Sealants (permanent molars only)

– Bitewing X-rays

– Full Mouth Series X-rays

– Space Maintainers

Plan 2- Aetna DMO Plan The Dental Maintenance Organization (DMO) Plan is a managed care plan that contracts with a list of providers at a set fee schedule. Participants pay co-pays and do not have to pay co-insurance. This plan offers a limited network of dentists with low member contributions, no deductible and low out-of-pocket co-pays. Out-of-Network coverage is not available. A Primary Care Dentist (PCD) must be selected and a referral is required for specialist care. Make sure to contact the dental provider you select to find out if they are accepting new patients.

For a list of scheduled services, network providers and to see what the plan pays, go to www.aetna.com/docfind/custom/emory .

PLANSAetna Traditional Dental (PPO) Aetna DMO*

In-Network Out-of-Network1 In-Network Only

Preventive Services (routine and deep cleanings, X-rays, etc.) $0 $0 $0

Basic Services (filling, root canal, etc.) 10%2 20%2 Scheduled

Major Restorative (crown, bridge, etc.) 50%2 50%2 Scheduled

Calendar Year Deductible3 $50/person$150/family

$50/person$150/family None

Annual Plan Payment Maximums $1,500/person $1,500/person None

Orthodontia

Deductible None None$2,000 co-pay, limited to one

treatment per lifetime Co-insurance 50% 50%

Lifetime Maximum $1,500 $1,500

1 Amounts applied to deductible are limited to the Reasonable and Customary charges 2 After deductible 3 Waived for preventive services * There is no Out-of-Network coverage in the Aetna DMO plan

DISCLAIMER: Every attempt has been made to ensure the chart and information above accurately reflect the details of the plan. Should there be any errors, the terms and conditions of the Summary Plan Description (SPD) prevail.

For the 2016 dental plan rates, go to page 15.

You can choose from two types of dental plans: the Aetna Traditional Dental (PPO) Plan or the Aetna Dental Maintenance Organization (DMO) Plan. Aetna does not issue dental cards, as it is not required by the provider.However, you can log on to www.aetnanavigator.com if you wish to print a card.

12/15 2016 Benefits Enrollment Guide 15

Dental Continued

VisionEmory Healthcare offers an optional vision plan through EyeMed Vision Care. Features of this plan include:

• Routine annual eye exam – $0 co-pay.

• Single, bifocal, trifocal, lenticular lenses – $0 co-pay.

• Progressive lenses – $65 co-pay.

• Frames – Up to $150 allowance, 20% off balance over $150.

• Contact lenses (conventional and disposable) – $0 co-pay up to $200 allowance, 15% off balance over $200 on conventional lenses.

• Benefits provided once every 12 months for lenses or contact lenses.

• Contact lens and frame allowance is a one-time- use benefit. Members are encouraged to use their full allowance at the time of initial service. Unused balances are not available for future visits during the same plan year in which the initial service was utilized.

• 40% off unlimited additional prescription eyewear purchases.

• 20% off nonprescription sunglasses.

For a complete list of plan details, go to www.eyemedvisioncare.com.

Providers EyeMed Vision Care offers a large network of providers, including the Emory Eye Center, LensCrafters, Pearle Vision and more. For a complete list of providers, call 1-855-270-2343 or go to www.eyemedvisioncare.com (click Locate a Provider, then Select Your Network dropdown menu and choose Select, then enter your zip code and click Submit). The group number is 9824889 .

Vision Coverage Through Your Medical Plan Employees enrolled in one of Emory Healthcare’s medical plans receive one vision exam per calendar year at an optometrist or ophthalmologist. Because an annual vision exam is considered preventive care, it is covered at 100%. Locate a participating vision provider at www.aetna.com/docfind/custom/emory .

Discounts at the Emory Eye Center

All Emory Healthcare employees and their immediate family members are eligible to receive services and discounts at the

Emory Eye Center. For a complete list, visit www.eyecenter.emory.edu. To schedule an appointment, call 404-778-2020.

Plan Aetna Traditional Dental (PPO) Aetna DMO

Full-time* Part-time** Full-time* Part-time**

Employee Only $11.50 $15.71 $8.50 $10.472-Person $23.50 $31.91 $15.50 $21.66Family $36.50 $50.25 $26.50 $34.21

Full-time & Part-time (rates are the same)

Employee Only $5.08Employee+Child(ren) $10.15Employee+Spouse/SSDP $9.64Family $14.94

Dental Plan Rates (Biweekly)

* Full-time rates apply for employees scheduled to work 31 or more hours per week.** Part-time rates apply for employees scheduled to work 20-30 hours per week.

Vision Plan Rates (Biweekly)

2016 Benefits Enrollment Guide 12/1516

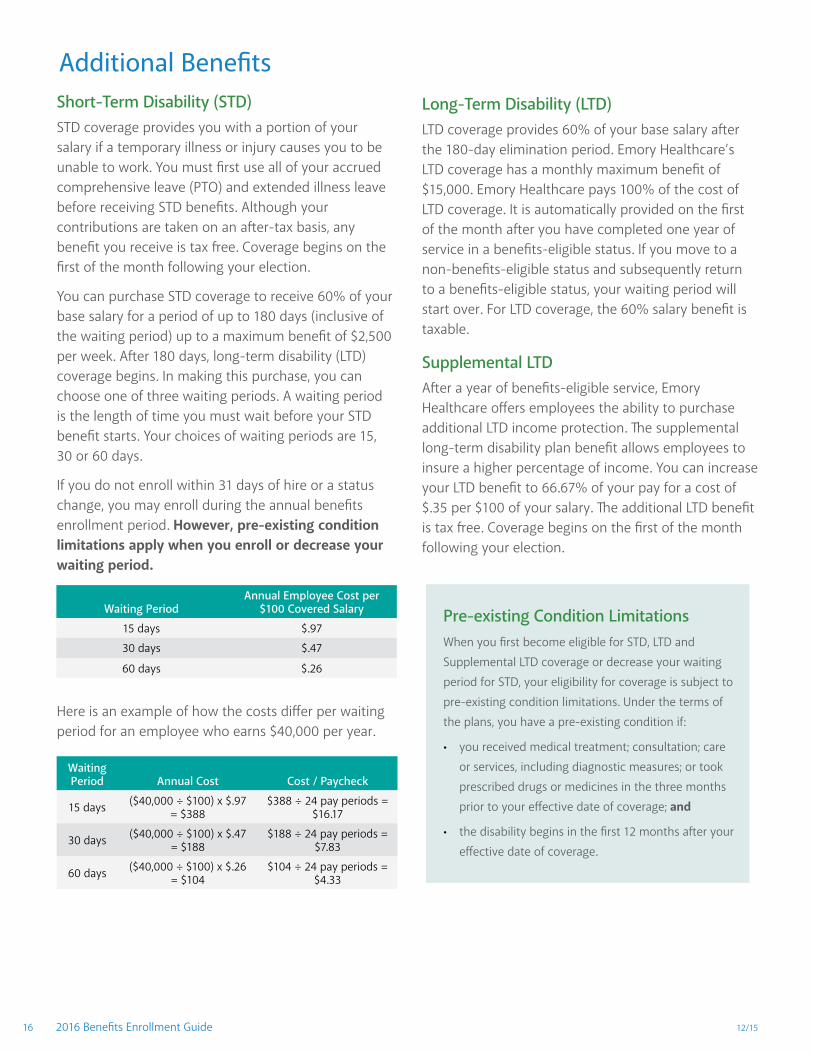

Additional BenefitsShort-Term Disability (STD) STD coverage provides you with a portion of your salary if a temporary illness or injury causes you to be unable to work. You must first use all of your accrued comprehensive leave (PTO) and extended illness leave before receiving STD benefits. Although your contributions are taken on an after-tax basis, any benefit you receive is tax free. Coverage begins on the first of the month following your election.

You can purchase STD coverage to receive 60% of your base salary for a period of up to 180 days (inclusive of the waiting period) up to a maximum benefit of $2,500 per week. After 180 days, long-term disability (LTD) coverage begins. In making this purchase, you can choose one of three waiting periods. A waiting period is the length of time you must wait before your STD benefit starts. Your choices of waiting periods are 15, 30 or 60 days.

If you do not enroll within 31 days of hire or a status change, you may enroll during the annual benefits enrollment period. However, pre-existing condition limitations apply when you enroll or decrease your waiting period.

Here is an example of how the costs differ per waiting period for an employee who earns $40,000 per year.

Long-Term Disability (LTD)LTD coverage provides 60% of your base salary after the 180-day elimination period. Emory Healthcare’s LTD coverage has a monthly maximum benefit of $15,000. Emory Healthcare pays 100% of the cost of LTD coverage. It is automatically provided on the first of the month after you have completed one year of service in a benefits-eligible status. If you move to a non-benefits-eligible status and subsequently return to a benefits-eligible status, your waiting period will start over. For LTD coverage, the 60% salary benefit is taxable.

Supplemental LTDAfter a year of benefits-eligible service, Emory Healthcare offers employees the ability to purchase additional LTD income protection. The supplemental long-term disability plan benefit allows employees to insure a higher percentage of income. You can increase your LTD benefit to 66.67% of your pay for a cost of $.35 per $100 of your salary. The additional LTD benefit is tax free. Coverage begins on the first of the month following your election.

Waiting PeriodAnnual Employee Cost per

$100 Covered Salary

15 days $.97

30 days $.47

60 days $.26

Waiting Period Annual Cost Cost / Paycheck

15 days ($40,000 ÷ $100) x $.97 = $388

$388 ÷ 24 pay periods = $16.17

30 days ($40,000 ÷ $100) x $.47 = $188

$188 ÷ 24 pay periods = $7.83

60 days ($40,000 ÷ $100) x $.26 = $104

$104 ÷ 24 pay periods = $4.33

Pre-existing Condition LimitationsWhen you first become eligible for STD, LTD and

Supplemental LTD coverage or decrease your waiting

period for STD, your eligibility for coverage is subject to

pre-existing condition limitations. Under the terms of

the plans, you have a pre-existing condition if:

• you received medical treatment; consultation; care

or services, including diagnostic measures; or took

prescribed drugs or medicines in the three months

prior to your effective date of coverage; and

• the disability begins in the first 12 months after your

effective date of coverage.

12/15 2016 Benefits Enrollment Guide 17

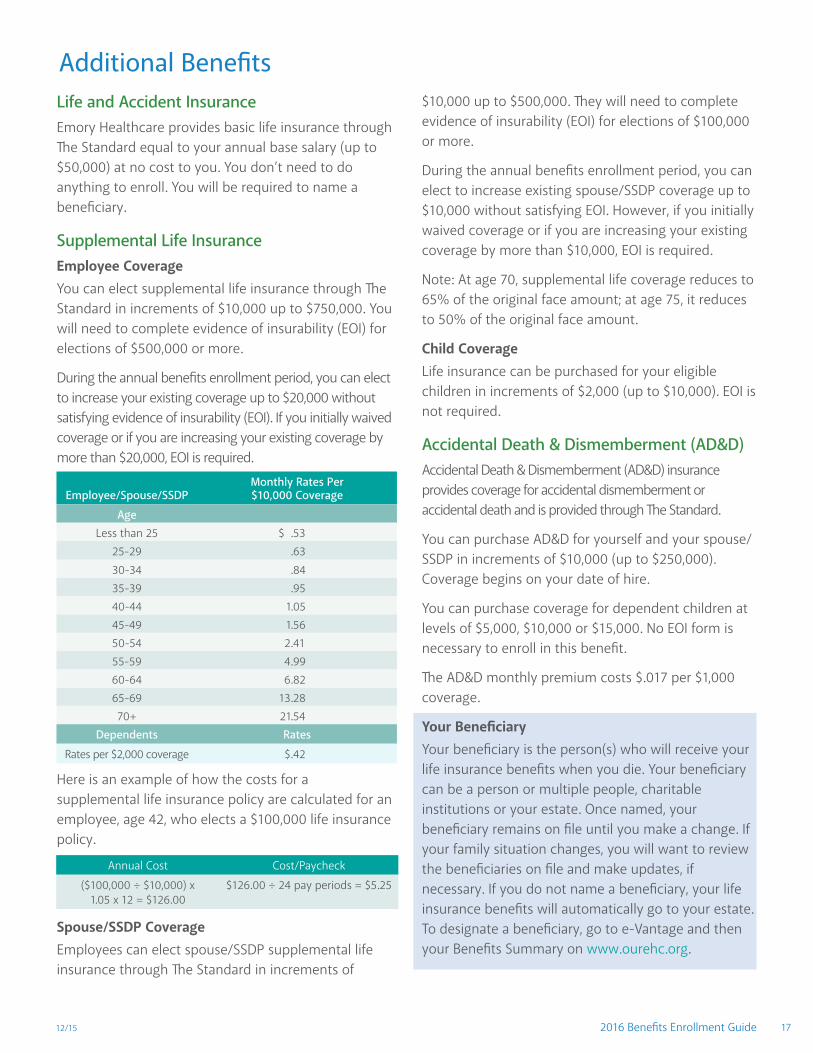

Additional BenefitsLife and Accident InsuranceEmory Healthcare provides basic life insurance through The Standard equal to your annual base salary (up to $50,000) at no cost to you. You don’t need to do anything to enroll. You will be required to name a beneficiary.

Supplemental Life InsuranceEmployee CoverageYou can elect supplemental life insurance through The Standard in increments of $10,000 up to $750,000. You will need to complete evidence of insurability (EOI) for elections of $500,000 or more.

During the annual benefits enrollment period, you can elect to increase your existing coverage up to $20,000 without satisfying evidence of insurability (EOI). If you initially waived coverage or if you are increasing your existing coverage by more than $20,000, EOI is required.

Here is an example of how the costs for a supplemental life insurance policy are calculated for an employee, age 42, who elects a $100,000 life insurance policy.

Spouse/SSDP CoverageEmployees can elect spouse/SSDP supplemental life insurance through The Standard in increments of

$10,000 up to $500,000. They will need to complete evidence of insurability (EOI) for elections of $100,000 or more.

During the annual benefits enrollment period, you can elect to increase existing spouse/SSDP coverage up to $10,000 without satisfying EOI. However, if you initially waived coverage or if you are increasing your existing coverage by more than $10,000, EOI is required.

Note: At age 70, supplemental life coverage reduces to 65% of the original face amount; at age 75, it reduces to 50% of the original face amount.

Child CoverageLife insurance can be purchased for your eligible children in increments of $2,000 (up to $10,000). EOI is not required.

Accidental Death & Dismemberment (AD&D)Accidental Death & Dismemberment (AD&D) insurance provides coverage for accidental dismemberment or accidental death and is provided through The Standard.

You can purchase AD&D for yourself and your spouse/SSDP in increments of $10,000 (up to $250,000). Coverage begins on your date of hire.

You can purchase coverage for dependent children at levels of $5,000, $10,000 or $15,000. No EOI form is necessary to enroll in this benefit.

The AD&D monthly premium costs $.017 per $1,000 coverage.

Your BeneficiaryYour beneficiary is the person(s) who will receive your life insurance benefits when you die. Your beneficiary can be a person or multiple people, charitable institutions or your estate. Once named, your beneficiary remains on file until you make a change. If your family situation changes, you will want to review the beneficiaries on file and make updates, if necessary. If you do not name a beneficiary, your life insurance benefits will automatically go to your estate. To designate a beneficiary, go to e-Vantage and then your Benefits Summary on www.ourehc.org .

Employee/Spouse/SSDPMonthly Rates Per $10,000 Coverage

AgeLess than 25 $ .53

25-29 .63

30-34 .8435-39 .9540-44 1 .0545-49 1 .5650-54 2 .4155-59 4 .9960-64 6 .8265-69 13 .2870+ 21 .54

Dependents Rates

Rates per $2,000 coverage $.42

Annual Cost Cost/Paycheck

($100,000 ÷ $10,000) x 1.05 x 12 = $126.00

$126.00 ÷ 24 pay periods = $5.25

2016 Benefits Enrollment Guide 12/1518

Additional Benefits

Long-Term Care CoverageEmory Healthcare offers optional coverage for long-term care through UNUM. If you do not enroll within 31 days of hire, you may enroll during the annual benefits enrollment period and must complete an EOI form and be approved by UNUM. Guaranteed issue is only available during the new hire period. Long-term care is designed for people who need assistance with daily living activities due to an accident, illness or advancing age. Enrollment kits for you and/or your spouse/SSDP are available online at http://w3.unum.com/enroll/emoryhealthcare or in our Employee Resource Center. For additional information, contact UNUM at 1-800-227-4165.

Group Home and Auto InsuranceEmory Healthcare provides access to this voluntary coverage through MetLife for home and auto insurance. This coverage is available at group rates that are lower than those typically available to individual policyholders. You have access to a wide range of personal property and casualty insurance products through MetLife. You may get coverage for your automobile, boat, motor home or recreational vehicle. For more information or to receive a personal quote, call MetLife at 1-800-GET-MET8 (1-800-438-6388).

AflacEmory Healthcare provides a voluntary coverage through Aflac for hospital, cancer and accident insurance. These policies are available at group rates that are lower than those typically available to individual policyholders. You have access to a wide range of policy and rider insurance products through Aflac. For more information and to enroll, log on to www.Aflac.com/Emory or call Aflac at 1-877-384-3344.

For more information on other additional benefits, discounts and perks available to you, go to the Your Benefits site under the Employee Resources tab on www.ourehc.org.

Emory Healthcare offers a variety of additional benefits for employees and their families. A brief summary is available below. For more detailed information, access the Emory Healthcare Benefits website on www.ourehc.org, Employee Resources and Your Benefits.

Prepaid Legal Plan Whether you have planned legal expenses or just want to be prepared for the unexpected, MetLife’s Group Legal Plan through Hyatt Legal Services is available to meet your needs. Through the plan, you have access to more than 4,000 law firms and 9,000 attorneys nationwide. Attorneys are available for both telephone and office consultations. For more information, call MetLife/Hyatt Legal Services at 1-800-821-6400. You can enroll online in the enrollment tool on e-Vantage. If you do not enroll within 31 days of hire, you may enroll during the annual benefits enrollment period. You can only cancel this benefit during the annual benefits enrollment period.

Discounts and Perks As an Emory Healthy employee, you have access to a wide variety of discounts and perks, including:

• The Express Care Clinic, through Occupational Injury Management, which provides some clinical services to employees

• Discounts at several day care centers around the Atlanta area

• Discounted access to certain fitness facilities on the Emory campus and around the Atlanta area

• Sparkfly, a discount program that can help you save on things like travel, entertainment, electronics, apparel, car services and more

• Access to Emory’s Faculty Staff Assistance Program, which provides health, wellness and counseling services to Emory employees

• Assistance with selecting adult and child care assistance through E4 Health

12/15 2016 Benefits Enrollment Guide 19

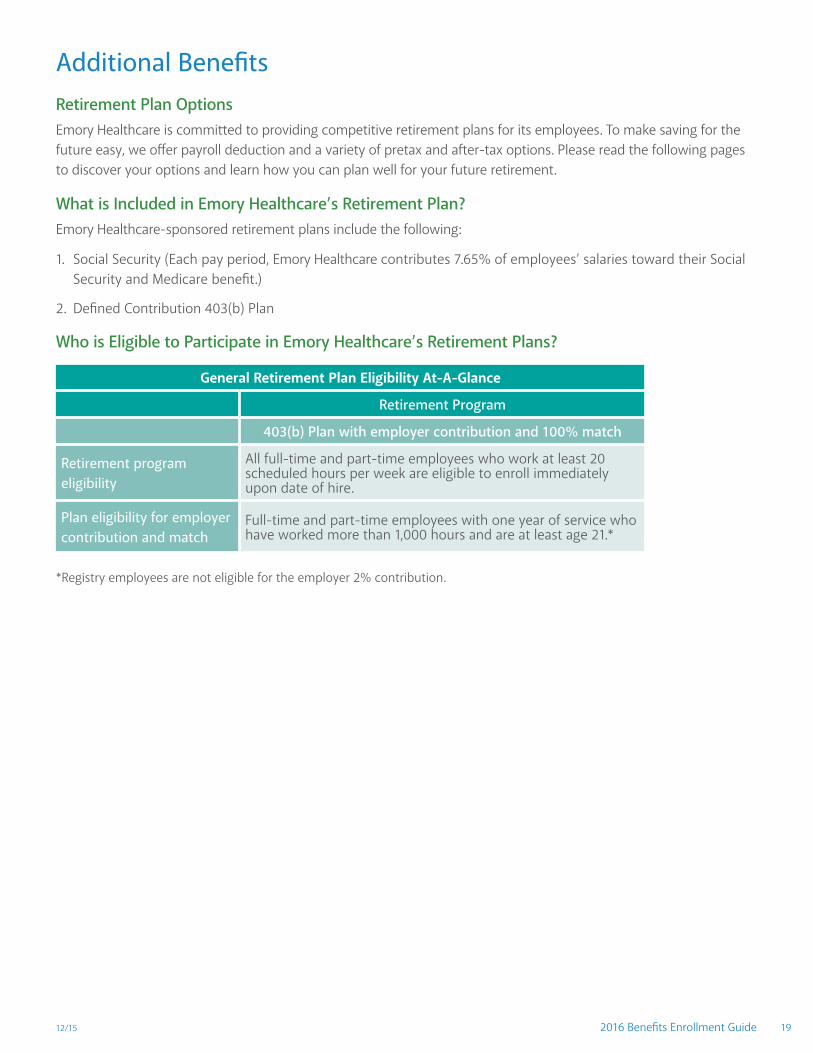

Additional BenefitsRetirement Plan OptionsEmory Healthcare is committed to providing competitive retirement plans for its employees. To make saving for the future easy, we offer payroll deduction and a variety of pretax and after-tax options. Please read the following pages to discover your options and learn how you can plan well for your future retirement.

What is Included in Emory Healthcare’s Retirement Plan?Emory Healthcare-sponsored retirement plans include the following:

1. Social Security (Each pay period, Emory Healthcare contributes 7.65% of employees’ salaries toward their Social Security and Medicare benefit.)

2. Defined Contribution 403(b) Plan

Who is Eligible to Participate in Emory Healthcare’s Retirement Plans?

General Retirement Plan Eligibility At-A-Glance

Retirement Program

403(b) Plan with employer contribution and 100% match

Retirement program eligibility

All full-time and part-time employees who work at least 20 scheduled hours per week are eligible to enroll immediately upon date of hire.

Plan eligibility for employer contribution and match

Full-time and part-time employees with one year of service who have worked more than 1,000 hours and are at least age 21.*

*Registry employees are not eligible for the employer 2% contribution.

2016 Benefits Enrollment Guide 12/1520

Additional BenefitsRetirement Plan Options Continued

403(b) with Employer Contribution and 100% MatchA Defined Contribution 403(b) is a tax-deferred plan available to employees of certain nonprofit organizations. Contributions and investment earnings grow tax-deferred until withdrawal, at which time they are taxed as ordinary income.

Eligible employees can begin contributing to the 403(b) upon hire. Employees will be eligible for the employer contribution and employer match upon satisfying the one-year waiting period (assuming the employee worked 1,000 hours during that year) and reaching age 21.

How the Retirement Program 403(b) Works• Employee contributions – Eligible employees can

contribute to the plan, up to the annual maximum set by the IRS ($18,000). Employees age 50 or older can contribute an additional amount over the IRS maximum amount ($6,000).

• Emory Healthcare’s contributions – Eligible employees receive Emory Healthcare’s contributions as follows:

1. All eligible employees receive an automatic 2% Emory Healthcare contribution even if they are not actively contributing to the 403(b) plan*

2. Additionally, if they are actively contributing to the plan, the employees receive an added match based on years of service:

– 100% match on the first 4% if they have less than 10 years of service

– 100% match on the first 5% if they have 10 or more years of service

Emory Healthcare’s contributions are effective the first of the month after an employee meets the eligibility requirements. If an employee enrolls after meeting these requirements, matching contributions will be effective on the date enrollment elections are submitted.

The total annual EHC contribution opportunity is 7% of eligible pay upon attaining 10 years of service.

• Ownership – Eligible participants are always 100% vested in their contributions and in the money their contributions earn. After three years of service, they are also 100% vested in Emory Healthcare’s contributions (the automatic 2% and any additional matching contributions) and the earnings on those contributions.

• Investment variety – The plan offers a diverse mix of investment options. Keep reading to learn more.

Making Contributions to the PlanEmployees have the option of directing 403(b) contributions as pretax contributions or as Roth after-tax contributions, or some combination of the two that does not exceed that year’s contribution limits.

• When employees make pretax contributions, they put off paying federal and, in most cases, state and local income taxes on the money earned on their contributions. They pay taxes only when they take a distribution or withdrawal from their account. Early withdrawals may be subject to penalties in addition to taxes you pay. By deferring the taxes on their pretax contributions, they lower their taxable income and increase their take-home pay. Employees must pay taxes when they withdraw their money.

• The Roth after-tax contribution allows employees to save for retirement by contributing after-tax dollars to an account that grows tax deferred. At the time of distribution in retirement, the withdrawal of these contributions are tax free; however, the earnings on any contributions are taxed unless the employee’s account has been open at least five years and they have reached age 591/2 .

*Registry employees are not eligible for the employer 2% contribution.

12/15 2016 Benefits Enrollment Guide 21

Additional BenefitsRetirement Plan Options Continued

Four Ways to Invest Your 403(b) Plan ContributionsEmory Healthcare’s 403(b) plan offers you Four Ways to Invest .

Lifecycle InvestmentsLifecycle investments offer you the convenience of investing your contributions into a fund that is managed for you by providing “ready-mixed” investments.

Lifecycle investments are allocated and invested based on your projected retirement timeline, starting out with a higher allocation to stocks when you are younger, and then reallocating gradually toward more conservative assets as you get closer to retirement. Each of the funds assumes a retirement age of 65, so try to select the appropriate fund based on when you plan to retire. All of Emory Healthcare’s Retirement Savings and Matching Plan vendors offer Lifecycle investments – Fidelity (Freedom Funds), TIAA-CREF (Lifecycle Funds) and Vanguard (Target Retirement Funds). These funds are monitored by Emory Healthcare and managed by the vendors; contact your vendor(s) of choice for more information.

Core InvestmentsCore investments streamline your fund choices across major asset classes, enabling you to make easier investment decisions. Selecting funds in the Core investment category enables you to select and combine investments to create a diversified retirement portfolio. These funds are monitored by Emory Investment Management. Contact your vendor(s) of choice for more information.

Expanded InvestmentsExpanded investments provide greater choice and options across all major asset classes. Selecting funds in the Expanded investment category enables you to create a portfolio that is tailored to your individual retirement goals. These funds are monitored by Emory Investment Management. Contact your vendor(s) of choice for more information.

The Mutual Fund Brokerage WindowThe Mutual Fund Brokerage Window gives you access to the world of mutual fund investments. The window provides the flexibility of a brokerage account, with the advantage of investing your retirement savings plan money through the Emory Healthcare 403(b) plan. This option provides more opportunities to create a retirement portfolio that matches your goals, time frame and risk tolerance. You also can monitor your portfolio and adjust it as your needs change.

Funds available through the Mutual Fund Brokerage Window are not selected or monitored by Emory Healthcare or Emory Investment Management in any way, and investments are made at your own risk. Contact your vendor(s) of choice to discuss which funds are available to you.

Accessing Your 403(b) Plan Account While EmployedIf you need to take a distribution from your 403(b) plan account while you are an Emory Healthcare employee, there are several options for you.

Plan LoanA plan loan enables you to borrow funds from your employee contributions and vested employer match money only. Plan loans are repayable through direct debit of your checking or savings account over the time frame of the loan and do not require you to cease participating in the plan during the term of the loan. No penalties are incurred by participants accessing their money. Once all forms are completed/submitted to the appropriate retirement plan vendor, this process typically takes 10 business days.

Hardship WithdrawalA hardship withdrawal enables you to withdraw funds from your contributions to cover certain medical, educational, home purchase or repair items. Hardship withdrawals cannot be repaid, are subject to IRS penalties for early withdrawal, are taxable to the participant and require that you cease participation in the plan for six months. Once all forms are completed/submitted to the appropriate retirement plan vendor, this process typically takes seven business days.

2016 Benefits Enrollment Guide 12/1522

Additional BenefitsRetirement Plan Options Continued

In-Service WithdrawalAn in-service withdrawal from your contributions is available to employees who have reached 591/2 years of age. Withdrawal requests do not have to meet certain reason requirements, are not subject to IRS penalties for early withdrawal and do not require you to cease participation in the plan. Withdrawals are taxable to the participant at the time they are received. Once all forms are completed/submitted to the appropriate retirement plan vendor, this process typically takes seven business days.

Contact your 403(b) plan vendor to learn about options for accessing funds in your retirement plan while employed at Emory Healthcare.

Retirement Plan CounselingFidelity Investments, TIAA-CREF and Vanguard all offer individual counseling sessions at Emory Healthcare throughout the year. Representatives can provide information on investing for retirement, the differences between the retirement benefits available to you and how to diversify your portfolio. To view the retirement counseling schedule, go to the Benefits page on www .ourehc.org and Employee Resources.

You may also schedule an individual session by contacting a vendor at the number below.

Vendor Contacts for All Retirement Plans

Company Phone Online

Fidelity Investments

1-800-343-0860www.fidelity.com/atwork

TIAA-CREF Financial Services

1-800-842-2252www.tiaa-cref.org/emoryhealthcare

Vanguard 1-800-523-1188 www.vanguard.com

Enrolling and Making Changes in the 403(b) PlanYou can enroll or make a change in your 403(b) plan any time using e-Vantage. Just follow these steps:

1. Step 1: Go to the Emory Healthcare intranet home page (www.ourehc.org) and select e-Vantage from the menu on the right.

2. Step 2: Log in using your Emory Healthcare username and password.

3. Step 3: Click Self Service on the left.

4. Step 4: On the Self Service page, click Benefits, then click 403(b) Savings Plan Election.

5. Step 5: From here, click the “Click here to enroll, change, or stop 403(b) elections” button to:

a. Make your contribution elections. You can calculate your maximum allowed contributions by clicking the “Click here to model 403(b) maximum contributions” button.

Basic Contributions