2018 YE – Earnings ReleaseFebruary 20, 2019

Disclaimer

Confidential

The information and opinions contained in this documenthave been compiled by KORDSA Teknik Tekstil AnonimŞirketi (the “Company”) from sources believed to be reliableand in good faith, but no representation or warranty,expressed or implied, is made as to their accuracy,completeness or correctness. No undue reliance may beplaced for any purposes whatsoever on the informationcontained in this presentation or on its completeness,accuracy or fairness. This document may contain forward-looking statements by using such words as "may", "will","expect", "believe", "plan" and other similar terminologythat reflect the Company management’s current views,expectations, assumptions and forecasts with respect tocertain future events. As the actual performance of thecompanies may be affected by risks and uncertainties, allopinions, information and estimates contained in thisdocument constitute the Company’s current judgment andare subject to change, update, amend, supplement orotherwise alter without notice. Although it is believed thatthe information and analysis are correct and expectationsreflected in this document are reasonable, they may beaffected by a variety of variables and changes in underlyingassumptions that could cause actual results to differmaterially.

The Company does not undertake any obligation, anddisclaims any duty to update or revise any forwardlooking statements, whether as a result of newinformation or future events. Neither this document northe information contained within can construe anyinvestment advice, invitation or an offer to buy or sell theCompany and/or Its group companies’ shares. TheCompany cannot guarantee that the securities describedin this document constitute a suitable investment for allinvestors and nothing shall be taken as an inducement toany person to invest in or otherwise deal with any sharesof the Company and its group companies. Theinformation contained in this document is published forthe assistance of recipients, but is not to be relied uponas authoritative or taken in substitution for the exerciseof judgment by any recipient. You must not distribute theinformation in this document to, or cause it to be usedby, any person or entity in a place where its distributionor use would be unlawful. Neither the Company, its boardof directors, directors, managers, nor any of Itsemployees shall have any liability whatsoever for anydirect or consequential loss arising from any use of thisdocument or its contents.

Agenda

Confidential

1

1

Global Footprint1

2018 YE Highlight2

Market Dynamics3

RM Price Drivers4

Segment Reporting5

New Products6

Update on 2018 YE Results7

Dividend Distribution8

Operating Bridge9

Guidance10

Global Footprint

4 continents11 facilities

~4,500 employees

2 R&DCenters

729 patent application179 patents

181 inventions

W E R E I N F O R C E L I F E

Confidential

Confidential

YE 2018 Highlights

YE 2018Highlights

Tire cord fabrics (“TCF”) Composite

• Strong market position,

• Sustainable growth rate on profitable products,

• Benefits from TL and other EM currency depreciation in the first three quarter of 2018.

• Negative impact of strong TL on financials in the last quarter of 2018.

• Two nylon production lines in Turkey and America shutdowns in the last quarter of 2018.

• Cost improvements in North America operations after the acquisition of Invista and starting flake production

• Finalized the acquisition process of FDI & TPI & AHT which provide advanced composite materials to the commercial aviation industry,

• After the acquisition of FDI & TPI, becoming the sole supplier for Toray which is the main supplier of Boeing,

• Higher actual figures compared to DD figures in these companies

• Potential M&A targets are always under consideration,

Construction

• Completed Kratos Polypropylene production line in Izmit,

• Kratos Macro & Micro Synthetic Fibers are approved and applied in over 50 significant superstructure, industrial and infrastructure reference projects.

EBITDA* = Gross Profit – OPEX + Depreciation/Amortization

TL Financials (MTL) USD Financials (MUSD)

YE 2017 YE 2018 D YE 2017 YE 2018 D

Sales 2,485 3,947 58.8% 681 820 20.3%

EBITDA* 339 621 83.1% 93 129 38.8%

EBITDA* Margin (%) 13.7% 15.7% + 2.1 bp 13.7% 15.7% + 2.1 bp

Global T ire Market

Global Automotive Market

Market Dynamics

Confidential

2017 2018E 2019E 2020E 2021E 2022E 2023E

Ap. Exc. China China EMEA NA SA

2017-2023E CAGR: 2,1%Global LV Assembly – M Units / Year

Source: PWC Autofacts

95 96 98 100 103 106

Global LV Tire Production– M Units / Year

Source: LMC Tyre Forecast

• AP Exc. China: +3.4% Highest growing region because of slowing other regions

• China: +2.2% Effected by tariff wars• EMEA: +1.1%• NA: 0.0% Crossover segment demand is strong• SA: +0.0% Expected market recovery was not

utilized in 2018 as a result of economic developments, slow trend to continue in 2019

• AP Exc. China: +2.4%• China: +0.8% (tariff war effect)• EMEA: +2.4% Miles driven decreased in EU

with high oil prices• NA: +4.2% (mainly replacement effect)• SA: +2.1%

108

2017 2018E 2019E 2020E 2021E 2022E 2023E

Ap. Exc. China China EMEA NA SA

1,9111,721 1,758 1,805

1,858

1,677

1,957

2017-2023E CAGR: 2,6%

Tire Reinforcement Market (PET)

Tire Reinforcement Market (NY6.6)

Market Dynamics

Confidential

2017-2023 CAGR: +2.5%

Source: Company Estimates

2017-2022 CAGR: +3.5%

Source: Company Estimates

• High capacity utilisation rates• Increasing demand for another market,

Enginering Plastics• Switching to NY6

Nylon 6.6

PET HMLS

• Consolidation by Indorama (acquiring PF Kaiping, Glanzstoff, Durafiber)

• Increasing PET usage in Tire

446481 479 492 508 525 530

357,00 366,00 375,00 384,00 394,00 404,00 414,00

2017 2018E 2019E 2020E 2021E 2022E 2023E

kto

n

Supply Demand

797 792828 836 843 851 858

621,00 643,00 665,00 689,00 713,00 738,00 763,00

2017 2018E 2019E 2020E 2021E 2022E 2023E

kto

n

Supply Demand

RM Price Drivers

Confidential

NY Raw Material Trend ( Indexed)

0

20

40

60

80

100

120

140

160

20

13

-01

20

13

-04

20

13

-07

20

13

-10

20

14

-01

20

14

-04

20

14

-07

20

14

-10

20

15

-01

20

15

-04

20

15

-07

20

15

-10

20

16

-01

20

16

-04

20

16

-07

20

16

-10

20

17

-01

20

17

-04

20

17

-07

20

17

-10

20

18

-01

20

18

-04

20

18

-07

20

18

-10

20

19

-01

20

19

-04

20

19

-07

20

19

-10

20

20

-01

20

20

-04

20

20

-07

20

20

-10

Benzene NA Contract Propylene NA Chem Grade Contract-Benchmark Stream Value Butadiene NA ContractSource: IHS Markit

Forecast

PET Feedstock West Europe

PET Feedstock Asia

RM Price Drivers

Confidential

• Crude oil WTI (based on IHS) price is the major driver for PET price,

• MEG prices decrease in 2019 due to new capacity becoming online,

• 2020 and onwards still not clear from crude oil side due to IMO regulations, OPEC supplies, USA sanctions, etc,

• PTE & MEG are expected to remain tight in 2018.

• Crude oil price is the major driver for PET price, • Europe PET chip feedstock prices tend to follow Asian

market prices,• PTA in Europe has also been affected by BP Geel & PK

Orlen’s recent FMs in 2018

10

30

50

70

90

110

2013

-01

2013

-04

2013

-07

2013

-10

2014

-01

2014

-04

2014

-07

2014

-10

2015

-01

2015

-04

2015

-07

2015

-10

2016

-01

2016

-04

2016

-07

2016

-10

2017

-01

2017

-04

2017

-07

2017

-10

2018

-01

2018

-04

2018

-07

2018

-10

2019

-01

2019

-04

2019

-07

2019

-10

2020

-01

2020

-04

2020

-07

2020

-10

MEG Asia Contract ($/mt) Crude Oil Dubai US$ per Barrel

Px Asia Contract ($/mt) PTA Asia Contract ($/mt)

Source: IHS Markit

10

30

50

70

90

110

130

150

2013

-01

2013

-04

2013

-07

2013

-10

2014

-01

2014

-04

2014

-07

2014

-10

2015

-01

2015

-04

2015

-07

2015

-10

2016

-01

2016

-04

2016

-07

2016

-10

2017

-01

2017

-04

2017

-07

2017

-10

2018

-01

2018

-04

2018

-07

2018

-10

2019

-01

2019

-04

2019

-07

2019

-10

2020

-01

2020

-04

2020

-07

2020

-10

Px Europe Contract (€/mt) Crude Oil Dubai US$ per BarrelMEG Europe Contract (€/mt) PTA Europe Contract (€/mt)

Source: IHS Markit

Capitalize on Global Footprint and EntrenchedSupplier Status with All Key Tire Manufacturers -Segmental Progress

Confidential

57% 60%66% 65% 64%

8%9%

9% 9% 8%4%4%

4% 5% 5%

32%27%

21% 22% 23%

2014 2015 2016 2017 2018

Global Players Regional Players Emerging Players Others

Global Footprint

Confidential

Regionalfootprint

versus keycompetitors

Kordsa market position

• #1 NY TCF producer

• #1 PET TCF producer

• #1 NY TCF producer in the US

• 3 composite manufacturing plants

• #2 NY TCF producer

• #2 PET TCF producer

• The only PET yarn, TCF and SEC producer in LATAM

THAILANDThai Indo Kordsa Co. Ltd. Ayutthaya, Thailan

Tire (TCF)

INDONESIAPt Indo Kordsa Tbk. Jakarta, Indonesia

Tire (NY6.6, PET TCF)

TURKEYHeadquarters Istanbul, Factory Izmit, Technology Center Izmit

Tire (NY6.6, PET, SEC, TCF), Composite, Construction

BRAZILKordsa Brazil Salvador De Bahia, Brazil

Tire (PET, SEC, TCF)

USAKordsaInc. Laurel Hill N.C. Chattanoogo, TN. USAFabric Development Inc., PA; Textile Products Inc., CAAdvanced Honeycomb Technologies; CA

Tire (NY6.6, TCF), Composite

36%

22%

14%

28%

39%

17%14%

30%

36%

18%15%

31%

37%

17%14%

32%35%

24%

12%

29%

EMEA NA SA APAC

2014 2015 2016 2017 2018

YE 2018 Revenue Split Progress by Products

Confidential

71% 74% 76% 76%71%

23% 18%19% 20%

17%

6% 8% 4% 4%12%

2014 2015 2016 2017 2018

TCF NY Yarn Other*

* North America Composite segment effect is around 6.5%.

Technology Leadership at The Cutting Edge of Reinforcement

Confidential

• Kordsa will launch on the free licensing process of enviromentally friendly formula, striving to make it the new standard instead of the 80-year old formula.

Strong focus on R&D Cutt ing edge new products

Sale

s fr

om

ne

w p

rod

uct

s

(US$

m)

Selected col laborations(a) Leadership in Innovation and Technology”

Rolling resistance improvements through higher modulus for high performance tires

Protection layer for truck & bus tires; reduces tire weight

7% higher tenacity and better fatigue performance for aircraft tires (bias)

10% higher dimensional stability for better tire performance (improved labeling)

T802

4G PET

• According to the patent research database, Kordsa is among the top 10 companies in the world with the number of patents issued in industrial textiles as of 2018.

• Kordsa’s 2016 Sustainability Report received Platinium Award in 2018 Inspire Awards by LACP and ranked 21st among top 100 companies

• Listed in BIST Sustainability Index for the third consecutive year

1

Top 10

Rf-Free

(a) includes both, universities as well as individual academics from the names institutions

4152

42 45

64

2014 2015 2016 2017 2018

Key Financials

Confidential

Update on YE 2018 Results

* EBITDA Calculation: Gross Margin-OPEX+Dept & Amort

Kord sa c on t inues to p e rform we l l b ase d on i t s va lu e strate gy

TL Financials (MTL) USD Financials (MUSD)

YE 2017 YE 2018 D YE 2017 YE 2018 D

Sales 2,485 3,947 58.8% 681 820 20.3%

Gross Profit 449 794 76.6% 123 165 33.8%

Gross Margin (%) 18.1% 20.1% 2 pts' 18.1% 20.1% 2 pts'

OPEX (%) 8.6% 7.9% -1 pts' 8.6% 7.9% -1 pts'

Operating Profit 278 525 89.2% 76 109 43.4%

Operating Profit Margin (%) 11.2% 13.3% 2 pts' 11.2% 13.3% 2 pts'

EBITDA* 339 621 83.1% 93 129 38.8%

EBITDA* Margin (%) 13.7% 15.7% 2 pts' 13.7% 15.7% 2 pts'

Net Income 212 339 59.5% 58 70 20.9%

Effective Tax Rate (%) 14.7% 17.8% 3 pts' 14.7% 17.8% 3 pts'

Net Income (%) 8.5% 8.6% 0 pts' 8.5% 8.6% 0 pts'

EPS (TL/1,000 shares) 8.49 15.03 77.0% 2.33 3.12 34.2%

Key Balance Sheet I tems

Confidential

Update on YE 2018 Results

TL Financials (MTL) USD Financials (MUSD)

YE 2017 YE 2018 D YE 2017 YE 2018 D

Cash and Cash Equivalents 16 131 115 4 25 21

Account Receivables 483 830 346 128 158 30

Inventories 585 1,048 462 155 199 44

Other Current Assets 113 140 28 30 27 -3

PPE & Intangibles 1,464 2,233 769 388 424 36

Investment Property 47 115 68 12 22 9

Goodwill 46 172 126 12 33 21

Other Non-Current Assets 113 162 49 30 31 1

Account Payables 314 572 258 83 109 25

Total Debt 632 1,519 887 168 289 121

Short Term Debt 531 994 464 141 189 48

Long Term Debt 101 525 423 27 100 73

Other Liabilities 272 400 128 72 76 4

Net Debt (Cash&Cash Equ. Excluded) 617 1,388 772 164 264 100

WCAP Turnover 3.27 3.35 3.27 3.35

Net Debt / EBITDA* 1.82 2.23 1.76 2.04

Free Cash F low

Confidential

Update on YE 2018 Results

(in TL million, unless otherwise stated) YE 2017 YE 2018 D

Cash Used in Operating Activities 183 341 158

EBIT * (1-t) 252 442 191

Depreciation & Amortization 103 140 36

Change in Working Capital (199) (510) (312)

Other Adjustments 27 269 242

Cash Used in Investing Activities (180) (703) (522)

Maintenance CAPEX (180) (214) (34)

M&A Investments 0 (488) (488)

Free Cash Flow* 3 (362) (365)

* FCF: EBIT(1-Tax Rate) + Depreciation & Amortization - Change in Net Working Capital - Capital Expenditure. It can also be calculated by taking operating cash flow and subtracting capital expenditures. -FCF ( operational cash flow- capex)

Dividend Distribution (MTL)

Confidential

Source: IHS Markit

Distribution of all the distributable profits

• which is lower of Kordsa Turkey solo tax books (VUK) or Kordsa consolidated TFRS (IFRS) net income,

• in the form of cash and/or bonus shares subject to General Assembly approval.

The distribution decision is agreed taking into consideration the sizeable fixed asset purchases, acquisitions, covenants of current liabilities and the Company’s mid and long term strategies, national and global economic conditions.

Kordsa does not apply payment of advance dividends

6861 58

67

2013(paid in 2014)

2014(paid in 2015)

2015(paid in 2016)

2016(paid in 2017)

2017(paid in 2018)

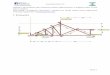

Operating Profit Bridge - MTL

Confidential

278

525-190

-15

245

34 1027 10

127

2017YE Sales Price(Inc. FX)

FeedstockPrices

ConversionCost

(Inc. FX)

Volume Mix OPEX(inc. FPDE)

Other FX on COP 2018YE

MMTL

Appendix

2014 – 2018 Financial Trend (MTL)

Confidential

1.569 1.735 1.908

2.485

3.947

182240

300 339

621

77,16 99,25 143,08 165,10

292,46

2014 2015 2016 2017 2018

Revenue

EBITDA

Net Income (parent)

YE 2018 Highlights (FX Rates)

Confidential

3,78 3,78 3,95 4,054,48 4,56

4,89

6,415,99

5,525,16 5,26

4,68 4,66 4,87 4,905,21 5,31

5,70

7,476,95

6,275,87 6,03

Jan'18 Feb'18 Mar'18 Apr'18 May'18 Jun'18 Jul'18 Aug'18 Sep'18 Oct'18 Nov'18 Dec'18

USDTRY (end rate) EURTRY (end rate)

100,00102,61

105,10

110,08

118,17

121,93118,74

130,76

126,61

117,56

122,16 122,53

100,00100,28 99,54 100,39

102,07105,71 106,16

104,38 103,28106,04 104,91

103,42100,00

102,19 102,56

103,46 104,01

107,39 107,46109,68

111,30113,52 106,90

107,96

90

95

100

105

110

115

120

125

130

135

140

Jan'18 Feb'18 Mar'18 Apr'18 May'18 Jun'18 Jul'18 Aug'18 Sep'18 Oct'18 Nov'18 Dec'18

IndexedUSDBRL (end rate) IndexedUSDTHB (end rate) IndexedUSDIDR (end rate)

Recommended