Accounting: Fraud Interview

ProcessLoyola University Maryland

Graduate Accounting Certificate ProgramGB767 Professional Communications

Five Types of Interview Questions:

Introductory

Informational

Closing

Assessment

Admission-seeking

Question StylesOpen Questions Avoid “yes” or “no” answers

Encourage monologue

Examples: “Why?”, “How?”, “Would you know?”

Closed Questions Usually answered with “yes” or “no”

Typically factual questions –specific amounts, dates, & times

Leading Questions• Answer is part of the question

• Usually used to confirm facts already known

Introductory Questions

Purpose: Provide introduction Establish rapport Establish theme of interview

Observe subject’s reaction

Create comfortable climate through small talk

Avoid sensitive questions

Take note of respondent’s reactions - Nonverbal clues very important

Informational Questions

Non-confrontational and Non-threatening

Gather factual information

Ask to develop facts in order of occurrence or some other systematic order

Ask only one question at a time. Frame so only one answer

Give respondent ample time to answer. Do not rush.

How to Close an Interview

1) Reconfirm Facts• Go over key facts to understand correctly• Use leading questions so subject can confirm or deny interpretation

2) Gather Additional Facts• Ask if subject knows other documents or witnesses that would help• Gives impression that you’re interested in all information –no matter what side it favors

3) Concluding the Interview• Ask subject if he/she believes he/she has been treated fairly• Ask permission to contact subject with additional questions

Assessment Questions

• These questions ask the subject to agree with matters that go against the principles of most honest people

• Used only when previous statements by respondent are inconsistent & indicate possible deception

• Used to assess verbal & nonverbal responses to establish credibility

• Should proceed from least to most sensitive

Begin in a non-threatening way. Do not indicate that these questions are for a different purpose than seeking information

Example: “I have a few additional questions.”

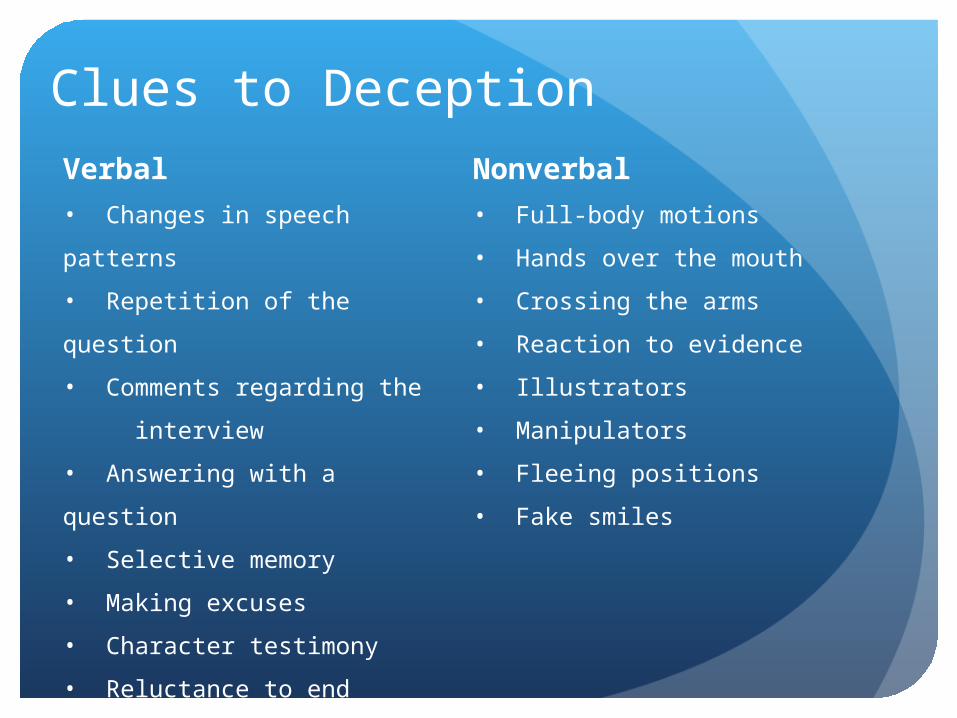

Clues to DeceptionVerbal

• Changes in speech patterns

• Repetition of the question

• Comments regarding the

interview

• Answering with a question

• Selective memory

• Making excuses

• Character testimony

• Reluctance to end interview

Nonverbal

• Full-body motions

• Hands over the mouth

• Crossing the arms

• Reaction to evidence

• Illustrators

• Manipulators

• Fleeing positions

• Fake smiles

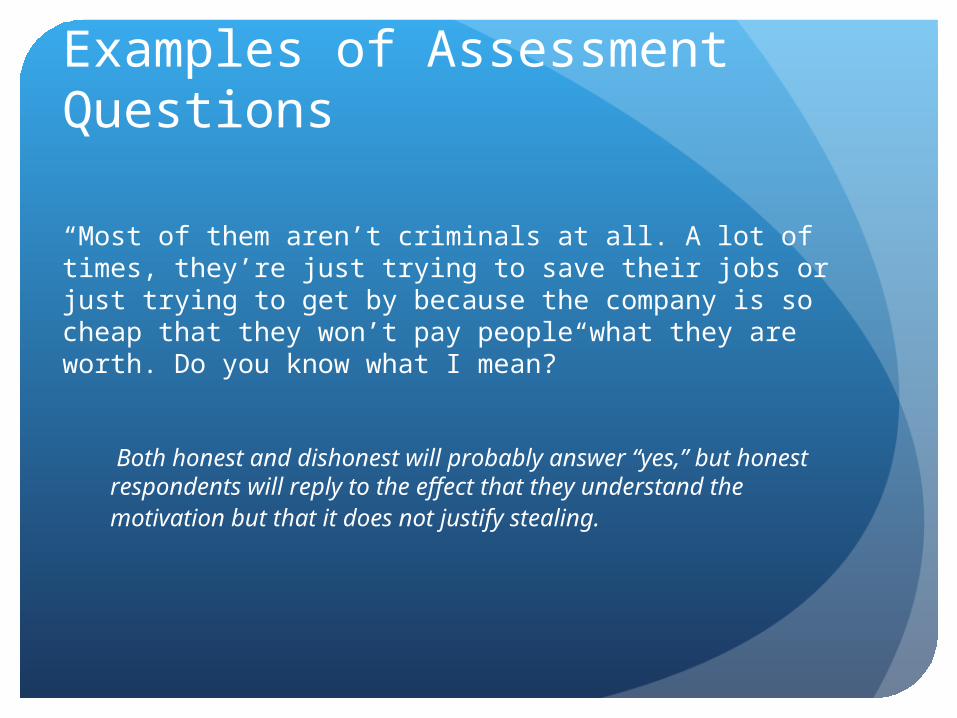

Examples of Assessment Questions

“Most of them aren’t criminals at all. A lot of times, they’re just trying to save their jobs or just trying to get by because the company is so cheap that they won’t pay people what they are worth. Do you know what I mean?”

Both honest and dishonest will probably answer “yes,” but honest respondents will reply to the effect that they understand the motivation but that it does not justify stealing.

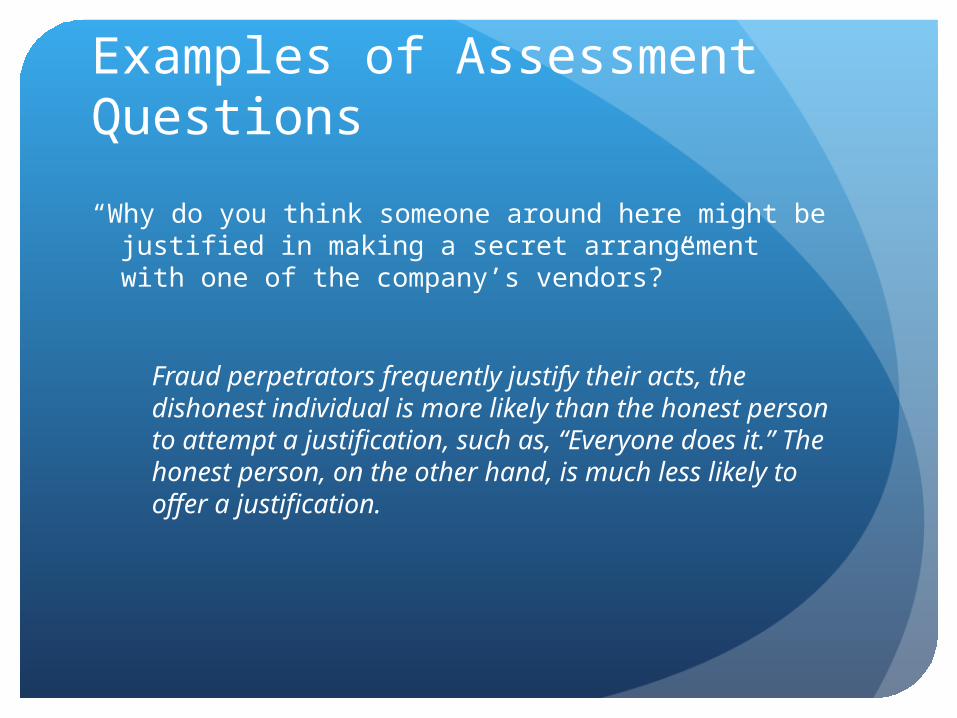

Examples of Assessment Questions

“Why do you think someone around here might be justified in making a secret arrangement with one of the company’s vendors?”

Fraud perpetrators frequently justify their acts, the dishonest individual is more likely than the honest person to attempt a justification, such as, “Everyone does it.” The honest person, on the other hand, is much less likely to offer a justification.

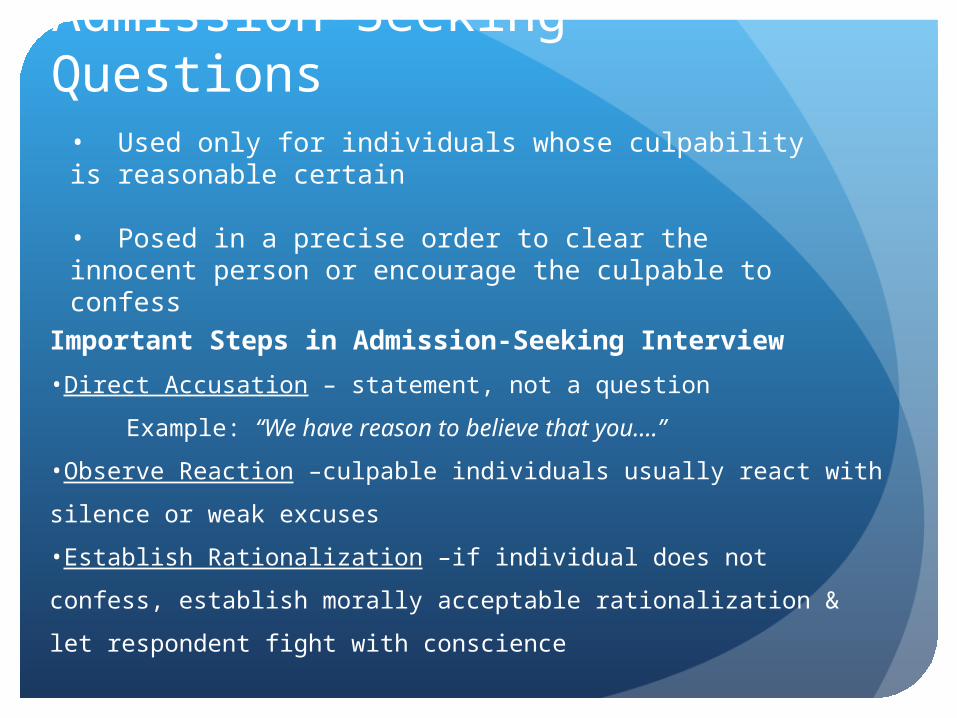

Admission-Seeking Questions• Used only for individuals whose culpability is reasonable certain

• Posed in a precise order to clear the innocent person or encourage the culpable to confess

Important Steps in Admission-Seeking Interview

•Direct Accusation – statement, not a question

Example: “We have reason to believe that you….”

•Observe Reaction –culpable individuals usually react with silence or

weak excuses

•Establish Rationalization –if individual does not confess, establish

morally acceptable rationalization & let respondent fight with

conscience

Things to Remember

Research & set goals before the interview

Take your time constructing questions

Establish an open environment from the beginning

Observe verbal and especially nonverbal reactions

Take notes

Remain calm and confident throughout

* Much of this information is adapted from May and May’s Effective Writing: A Handbook for Accountants 8th Edition

Recommended