Agriculture and Agrifinance - An Overview

Outline•Agriculture - Overview

• Issues and Concerns

•Agricultural Lending – Concepts, Methods

•Agricultural Lending – Trends & Overview

•Policy Initiatives: Doubling Farmers’ Income

•New and Emerging Agriculture and Agrifinance

•Agrifinance: Challenges and Way forward

Understanding Agriculture

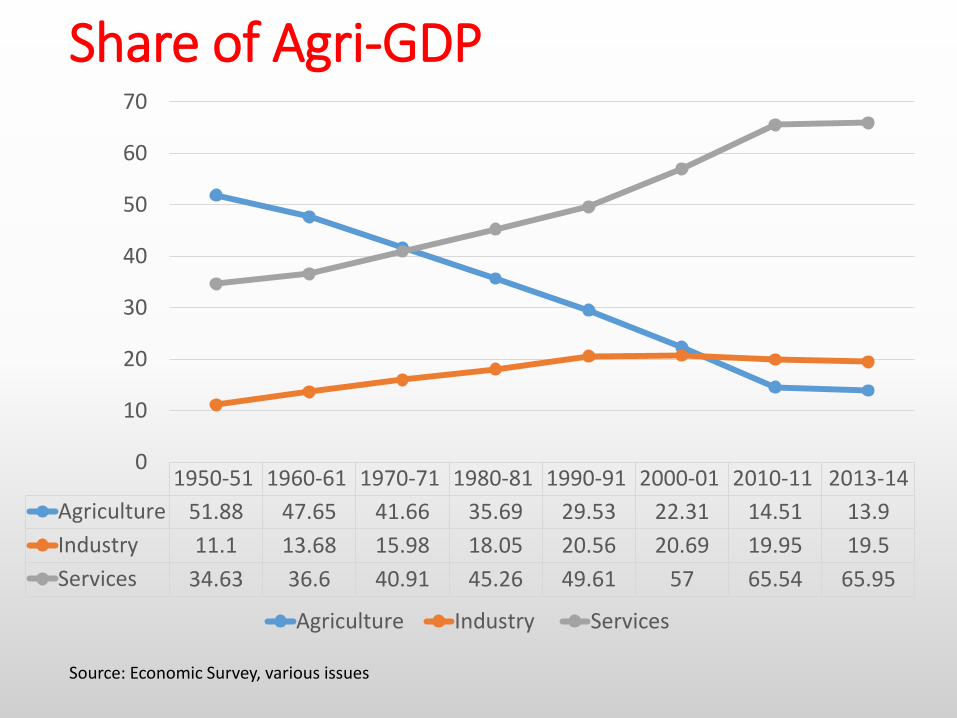

Share of Agri-GDP

1950-51 1960-61 1970-71 1980-81 1990-91 2000-01 2010-11 2013-14

Agriculture 51.88 47.65 41.66 35.69 29.53 22.31 14.51 13.9

Industry 11.1 13.68 15.98 18.05 20.56 20.69 19.95 19.5

Services 34.63 36.6 40.91 45.26 49.61 57 65.54 65.95

0

10

20

30

40

50

60

70

Agriculture Industry Services

Source: Economic Survey, various issues

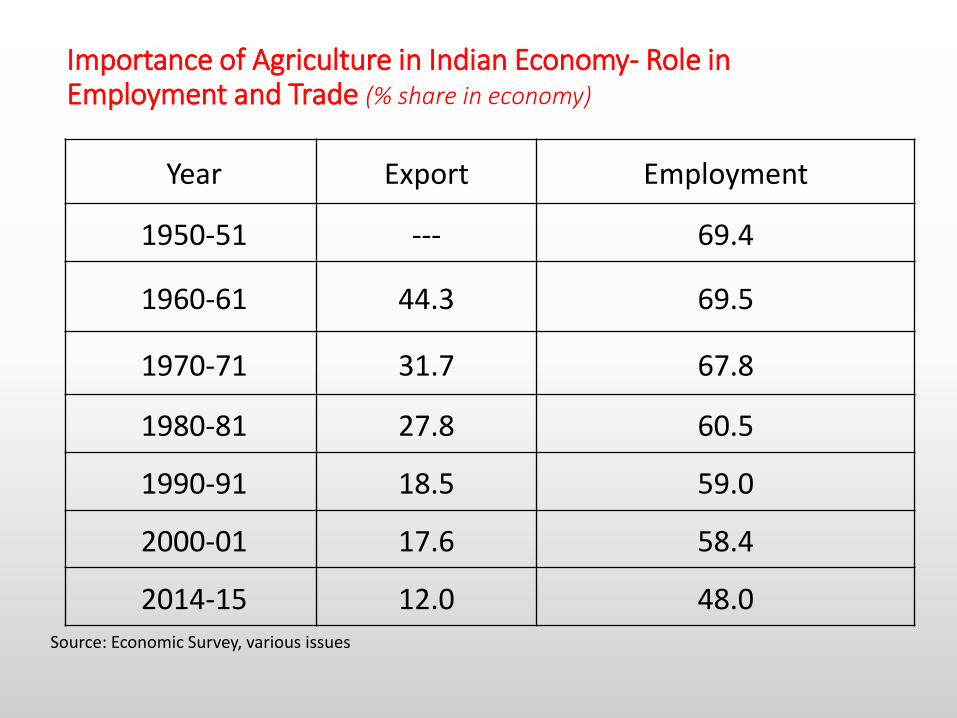

Importance of Agriculture in Indian Economy- Role in Employment and Trade (% share in economy)

Year Export Employment

1950-51 --- 69.4

1960-61 44.3 69.5

1970-71 31.7 67.8

1980-81 27.8 60.5

1990-91 18.5 59.0

2000-01 17.6 58.4

2014-15 12.0 48.0Source: Economic Survey, various issues

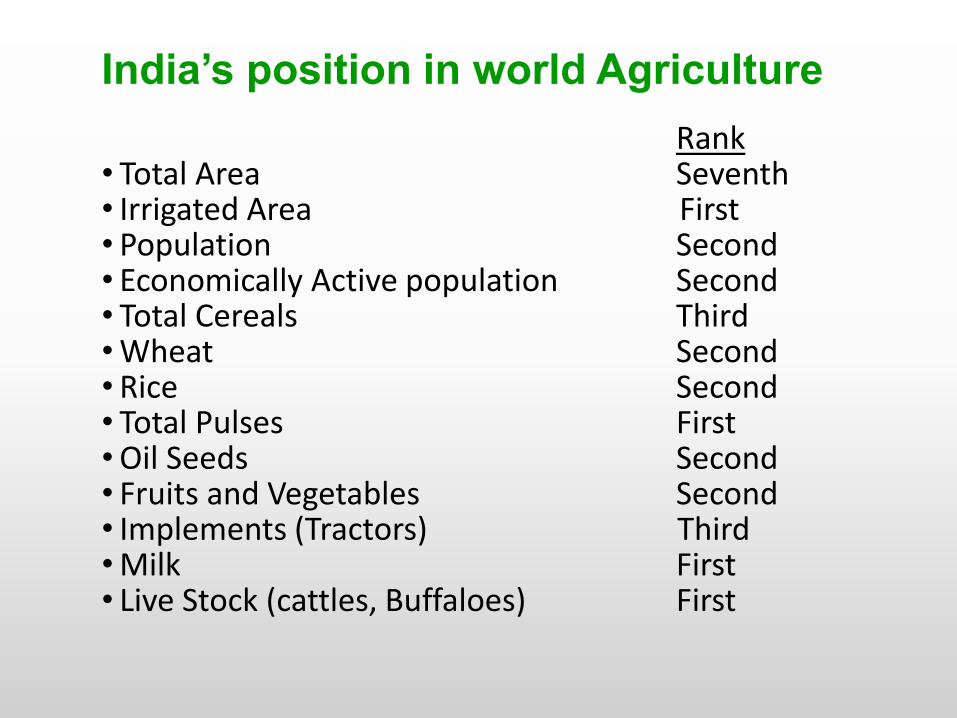

India’s position in world Agriculture

Rank• Total Area Seventh• Irrigated Area First• Population Second• Economically Active population Second• Total Cereals Third•Wheat Second• Rice Second• Total Pulses First•Oil Seeds Second• Fruits and Vegetables Second• Implements (Tractors) Third •Milk First• Live Stock (cattles, Buffaloes) First

Mile Stones in Agricultural Development

•Green Revolution (1968)

•Blue Revolution (water, fish)

•White Revolution (Milk)

•Yellow Revolution (flower, edible)

•Ever-Green Revolution (2004)

•Bio-Technology Revolution

• ICT Revolution

Issues and Concerns & Unleashing Opportunities

Agriculture Sector - Issues

• Declining operational holding

• Declining farm income & profitability.

• Dominance of dry land agriculture.

• Degradation of soil & biodiversity.

• Regional disparity & uneven growth.

• Declining land, water & capital investment.

• Huge price spread – market imperfections

• Threat of climate change - temperature, weatherunpredictability, drought & flood.

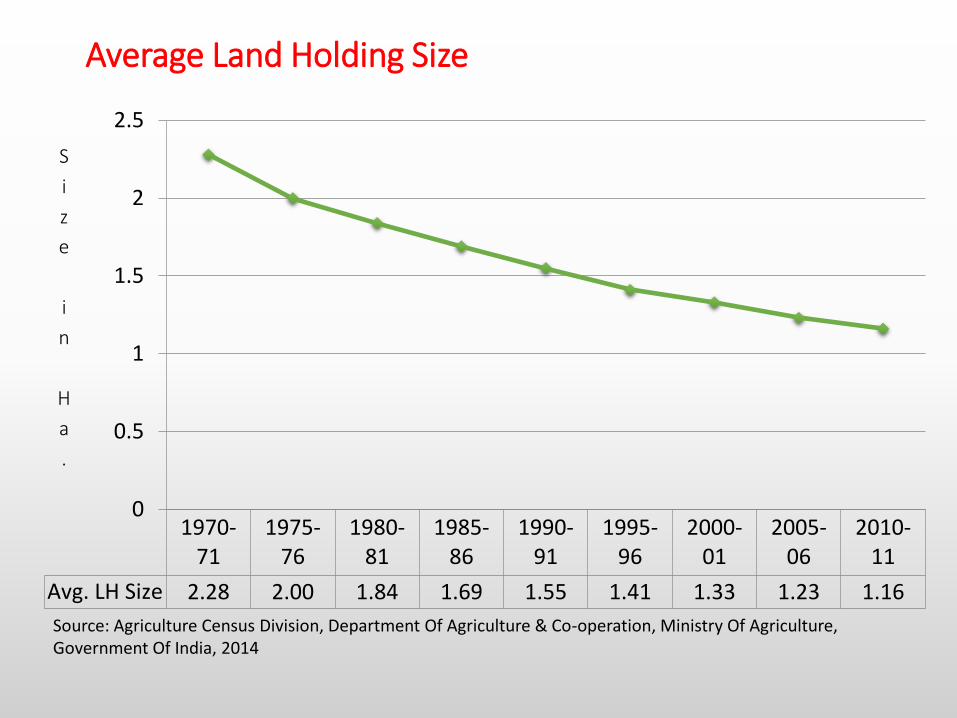

Average Land Holding Size

1970-71

1975-76

1980-81

1985-86

1990-91

1995-96

2000-01

2005-06

2010-11

Avg. LH Size 2.28 2.00 1.84 1.69 1.55 1.41 1.33 1.23 1.16

0

0.5

1

1.5

2

2.5

S

i

z

e

i

n

H

a

.

Source: Agriculture Census Division, Department Of Agriculture & Co-operation, Ministry Of Agriculture, Government Of India, 2014

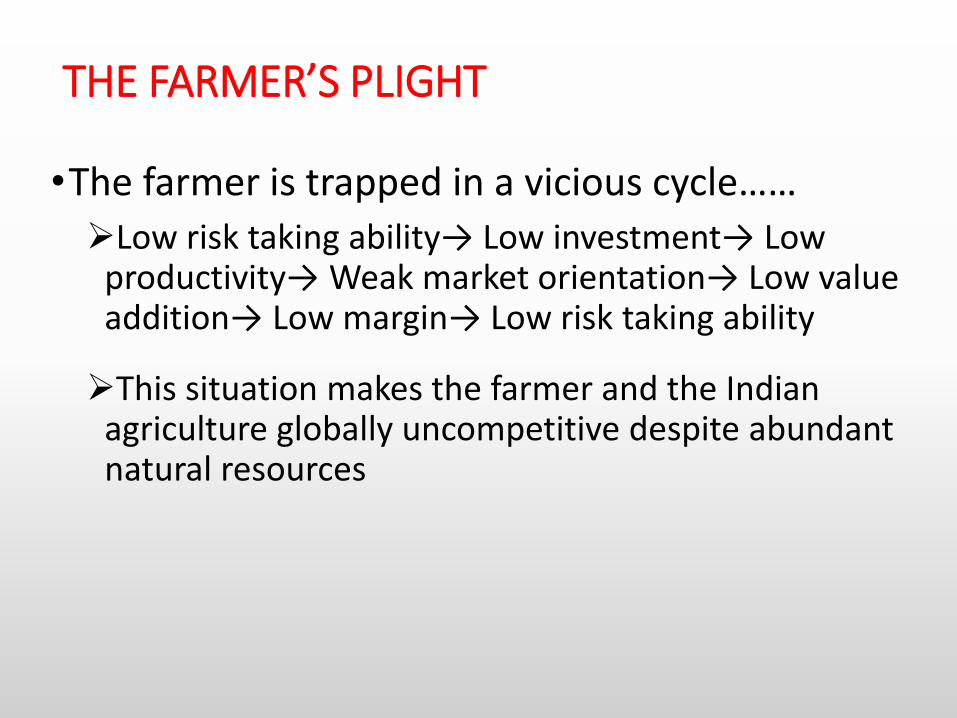

THE FARMER’S PLIGHT

•The farmer is trapped in a vicious cycle……

Low risk taking ability→ Low investment→ Low productivity→ Weak market orientation→ Low value addition→ Low margin→ Low risk taking ability

This situation makes the farmer and the Indian agriculture globally uncompetitive despite abundant natural resources

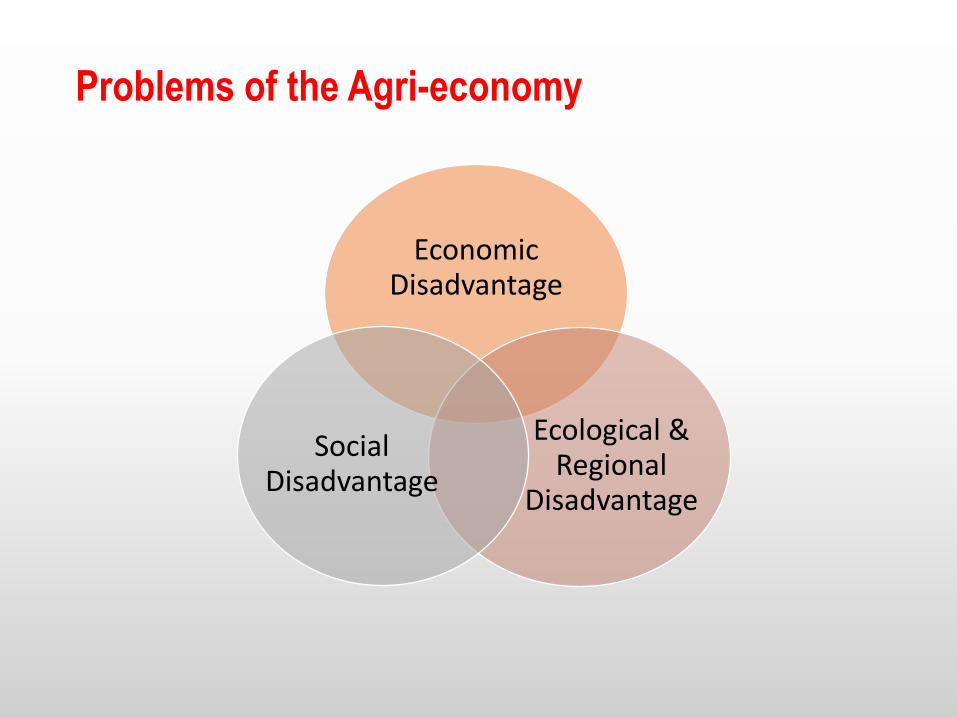

Problems of the Agri-economy

Economic Disadvantage

Ecological & Regional

Disadvantage

Social Disadvantage

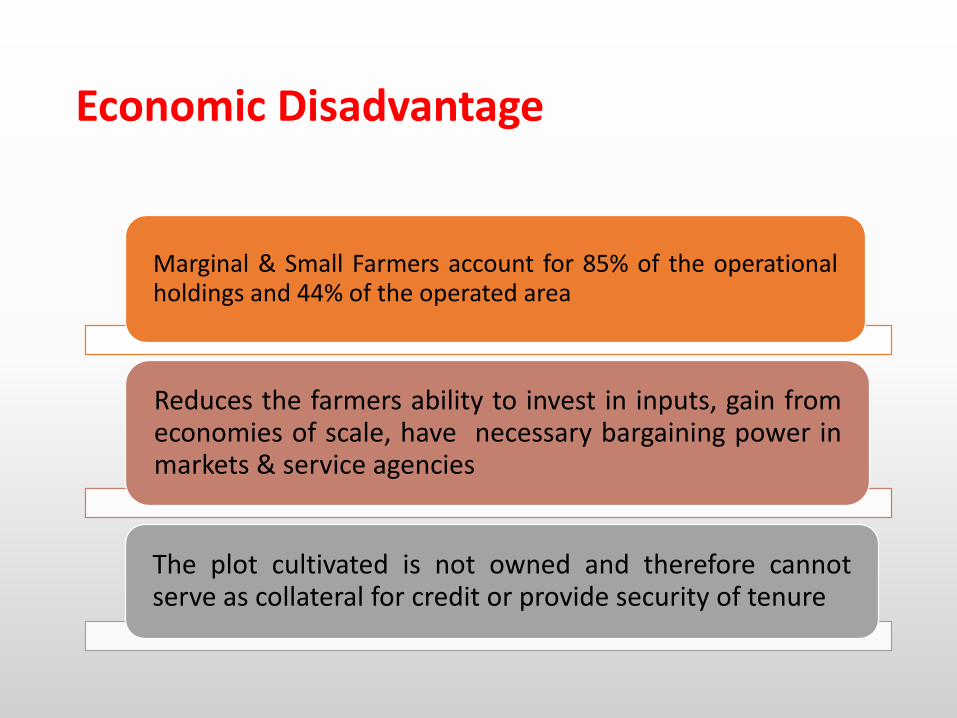

Economic Disadvantage

Marginal & Small Farmers account for 85% of the operationalholdings and 44% of the operated area

Reduces the farmers ability to invest in inputs, gain fromeconomies of scale, have necessary bargaining power inmarkets & service agencies

The plot cultivated is not owned and therefore cannotserve as collateral for credit or provide security of tenure

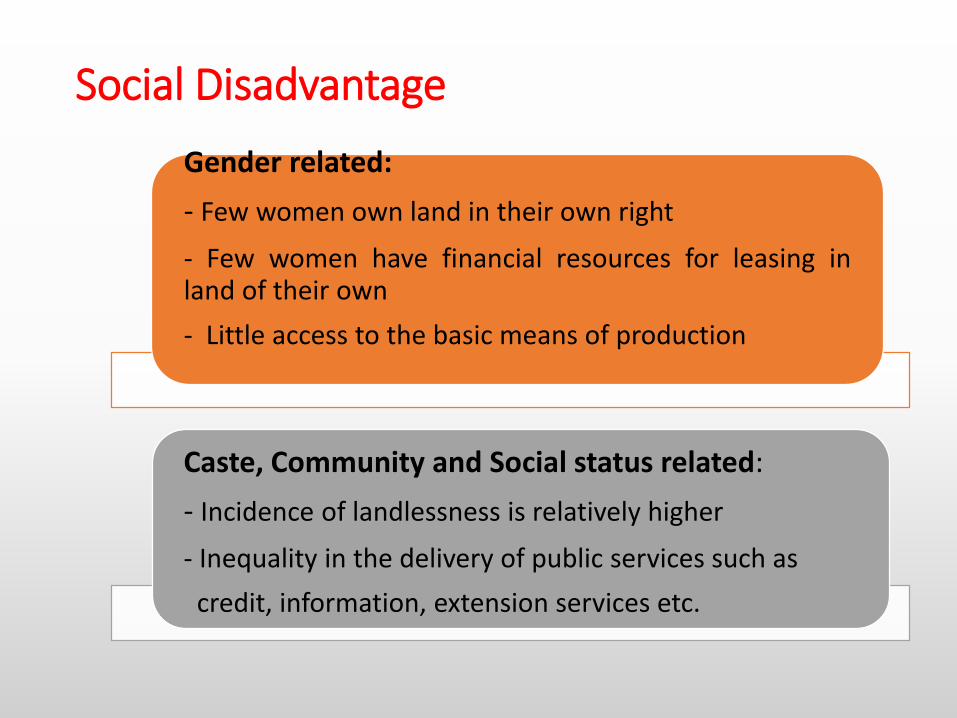

Social Disadvantage

Gender related:

- Few women own land in their own right

- Few women have financial resources for leasing inland of their own

- Little access to the basic means of production

Caste, Community and Social status related:

- Incidence of landlessness is relatively higher

- Inequality in the delivery of public services such as

credit, information, extension services etc.

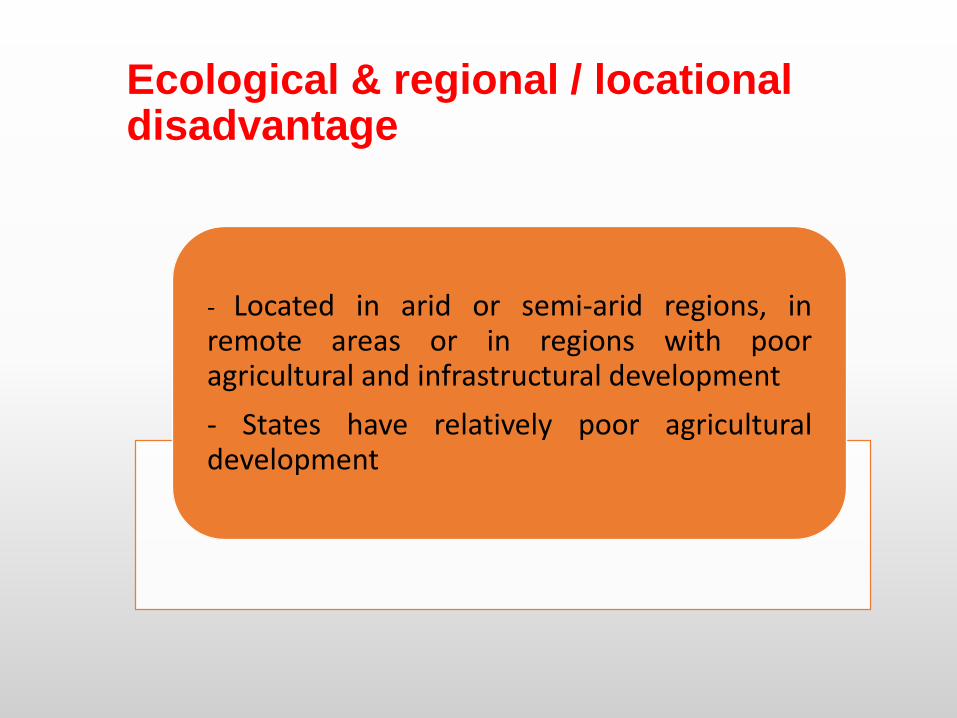

Ecological & regional / locational disadvantage

- Located in arid or semi-arid regions, inremote areas or in regions with pooragricultural and infrastructural development

- States have relatively poor agriculturaldevelopment

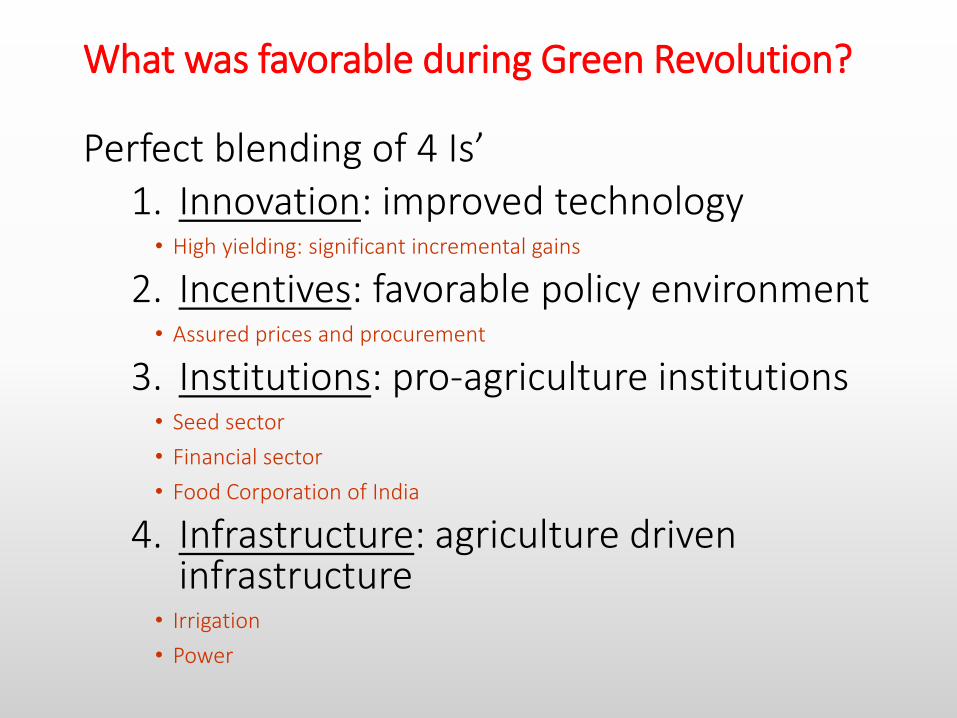

What was favorable during Green Revolution?

Perfect blending of 4 Is’1. Innovation: improved technology• High yielding: significant incremental gains

2. Incentives: favorable policy environment• Assured prices and procurement

3. Institutions: pro-agriculture institutions• Seed sector

• Financial sector

• Food Corporation of India

4. Infrastructure: agriculture driven infrastructure

• Irrigation

• Power

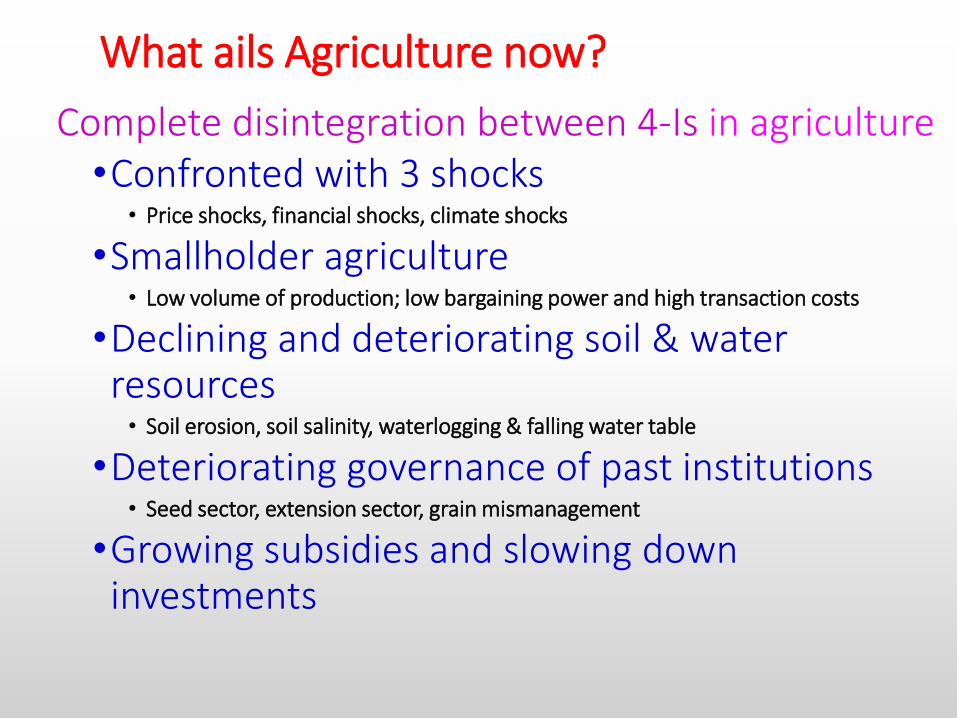

What ails Agriculture now?

Complete disintegration between 4-Is in agriculture•Confronted with 3 shocks

• Price shocks, financial shocks, climate shocks

•Smallholder agriculture• Low volume of production; low bargaining power and high transaction costs

•Declining and deteriorating soil & water resources• Soil erosion, soil salinity, waterlogging & falling water table

•Deteriorating governance of past institutions• Seed sector, extension sector, grain mismanagement

•Growing subsidies and slowing down investments

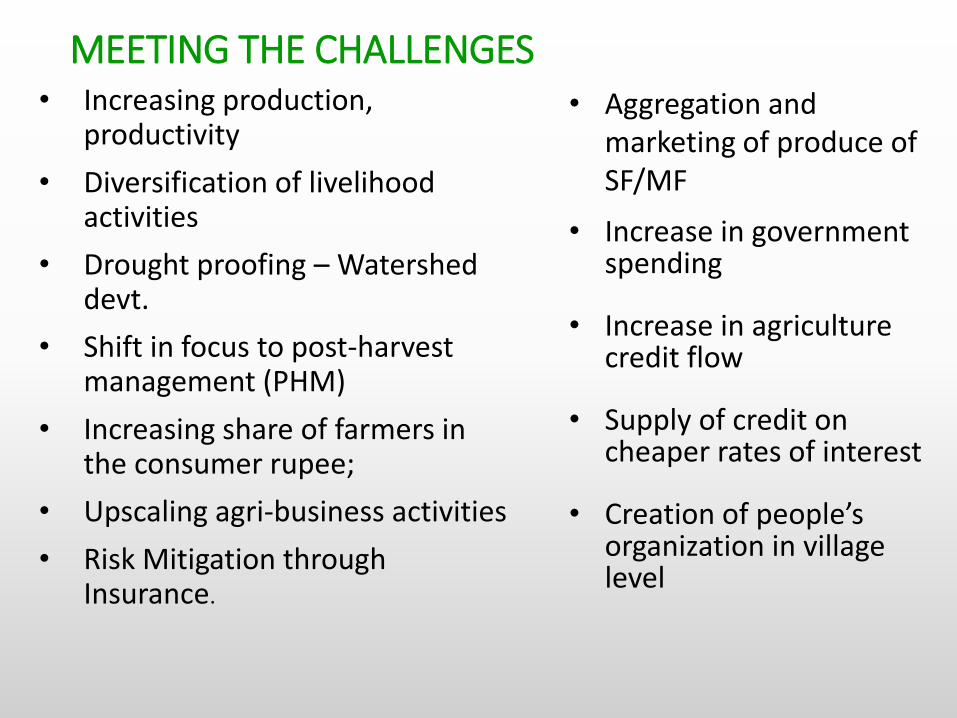

MEETING THE CHALLENGES• Increasing production,

productivity

• Diversification of livelihood activities

• Drought proofing – Watershed devt.

• Shift in focus to post-harvest management (PHM)

• Increasing share of farmers in the consumer rupee;

• Upscaling agri-business activities

• Risk Mitigation through Insurance.

• Aggregation and marketing of produce of SF/MF

• Increase in government spending

• Increase in agriculture credit flow

• Supply of credit on cheaper rates of interest

• Creation of people’s organization in village level

Unleashing Opportunities in Agriculture

4 pronged strategy1. Innovations

2. Institutions

3. Incentives

4. Infrastructure

•Harness untapped yield reservoir

• Leverage power of improved technologies

•Utilize fallow lands

•Promote agricultural diversification• High-value & remunerative commodities

• Labor absorbing & water efficient commodities

• Produce for the market

Agricultural Lending – Concepts, Classifications

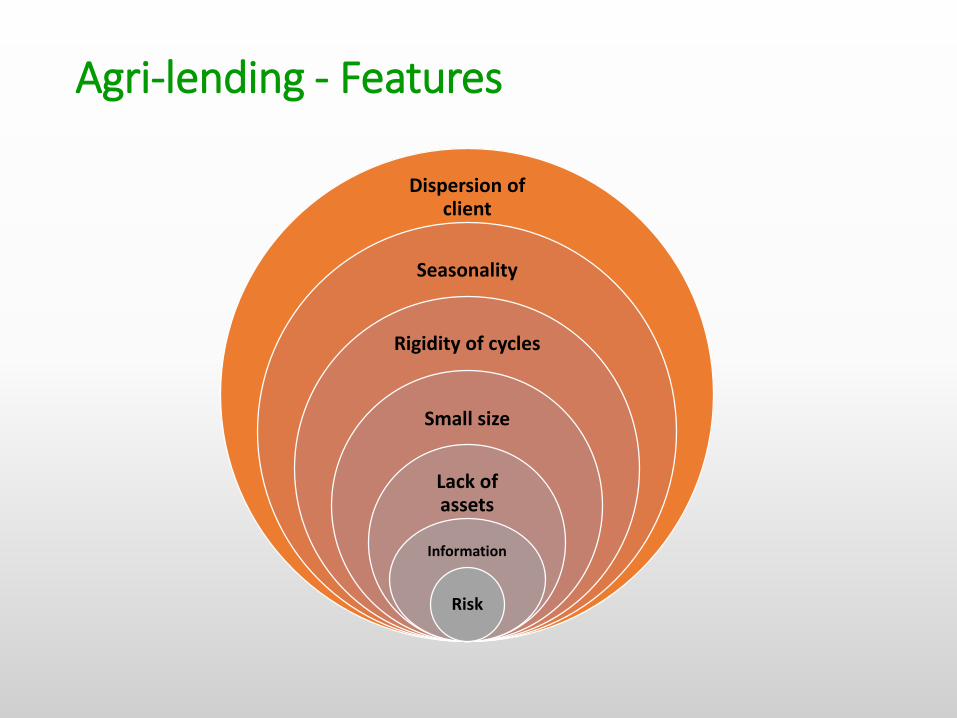

Agri-lending - Features

Dispersion of client

Seasonality

Rigidity of cycles

Small size

Lack of assets

Information

Risk

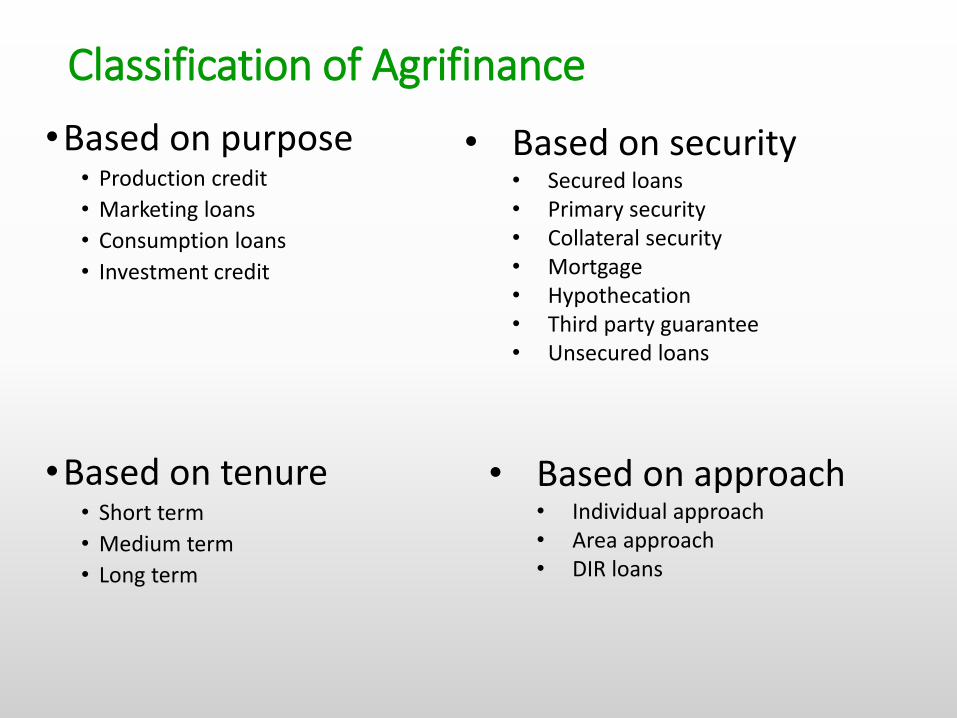

Classification of Agrifinance

•Based on purpose• Production credit

• Marketing loans

• Consumption loans

• Investment credit

•Based on tenure• Short term

• Medium term

• Long term

• Based on security• Secured loans• Primary security• Collateral security• Mortgage• Hypothecation• Third party guarantee• Unsecured loans

• Based on approach• Individual approach• Area approach• DIR loans

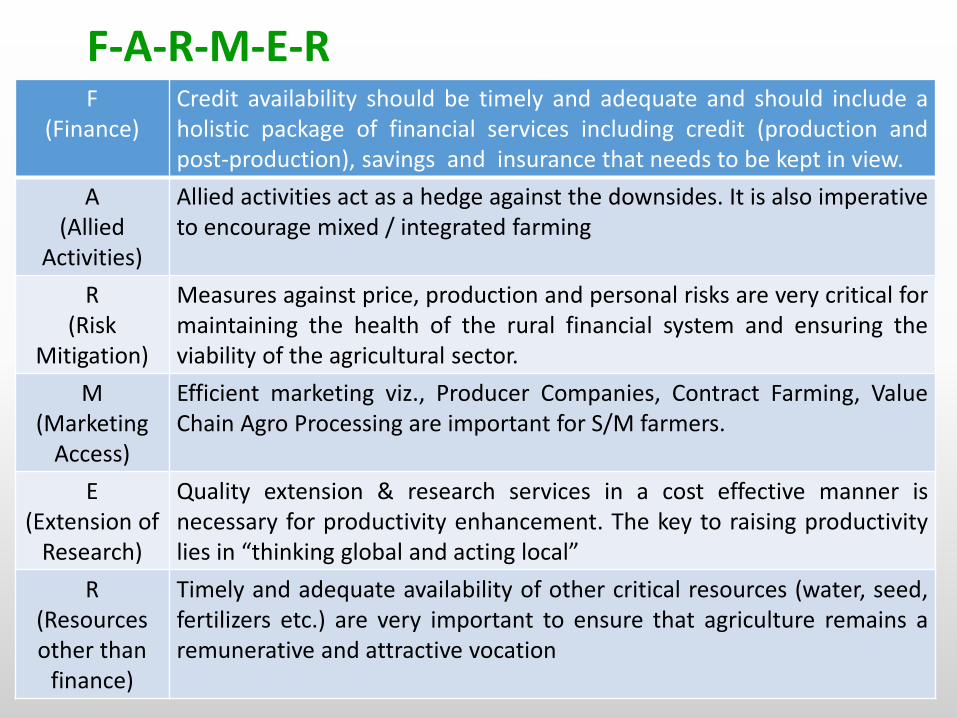

F(Finance)

Credit availability should be timely and adequate and should include aholistic package of financial services including credit (production andpost-production), savings and insurance that needs to be kept in view.

A(Allied

Activities)

Allied activities act as a hedge against the downsides. It is also imperativeto encourage mixed / integrated farming

R(Risk

Mitigation)

Measures against price, production and personal risks are very critical formaintaining the health of the rural financial system and ensuring theviability of the agricultural sector.

M(Marketing

Access)

Efficient marketing viz., Producer Companies, Contract Farming, ValueChain Agro Processing are important for S/M farmers.

E(Extension of

Research)

Quality extension & research services in a cost effective manner isnecessary for productivity enhancement. The key to raising productivitylies in “thinking global and acting local”

R(Resourcesother than

finance)

Timely and adequate availability of other critical resources (water, seed,fertilizers etc.) are very important to ensure that agriculture remains aremunerative and attractive vocation

F-A-R-M-E-R

Agricultural Lending

Agri-finance

Every 1% increase in real agricultural creditresults in an increase in agricultural GDP by0.22% with a one-year lag

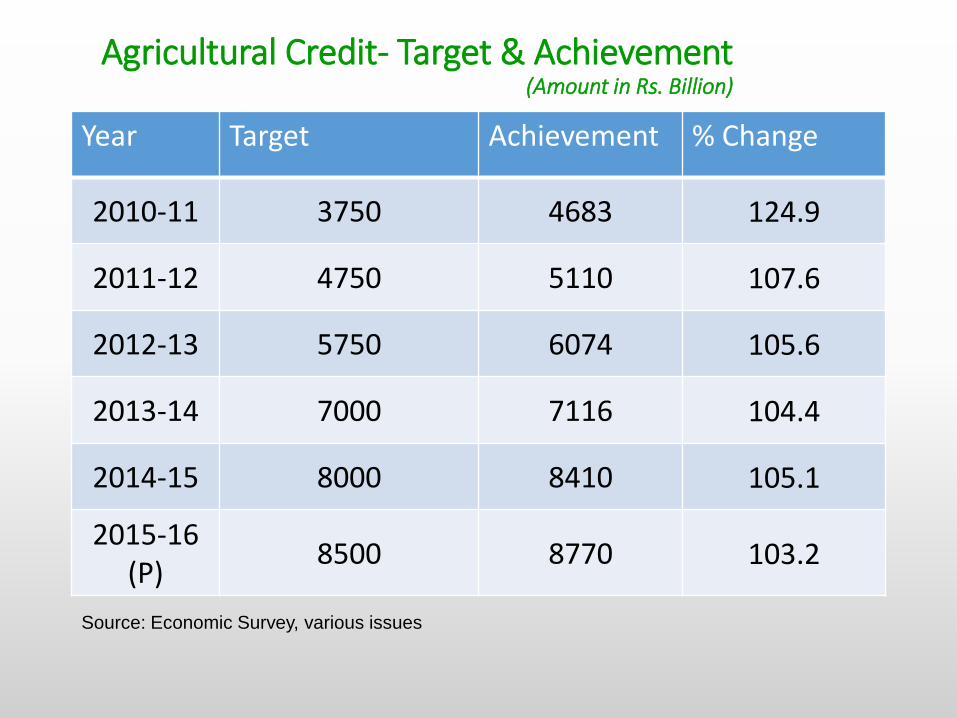

Agricultural Credit- Target & Achievement(Amount in Rs. Billion)

Year Target Achievement % Change

2010-11 3750 4683 124.9

2011-12 4750 5110 107.6

2012-13 5750 6074 105.6

2013-14 7000 7116 104.4

2014-15 8000 8410 105.1

2015-16 (P)

8500 8770 103.2

Source: Economic Survey, various issues

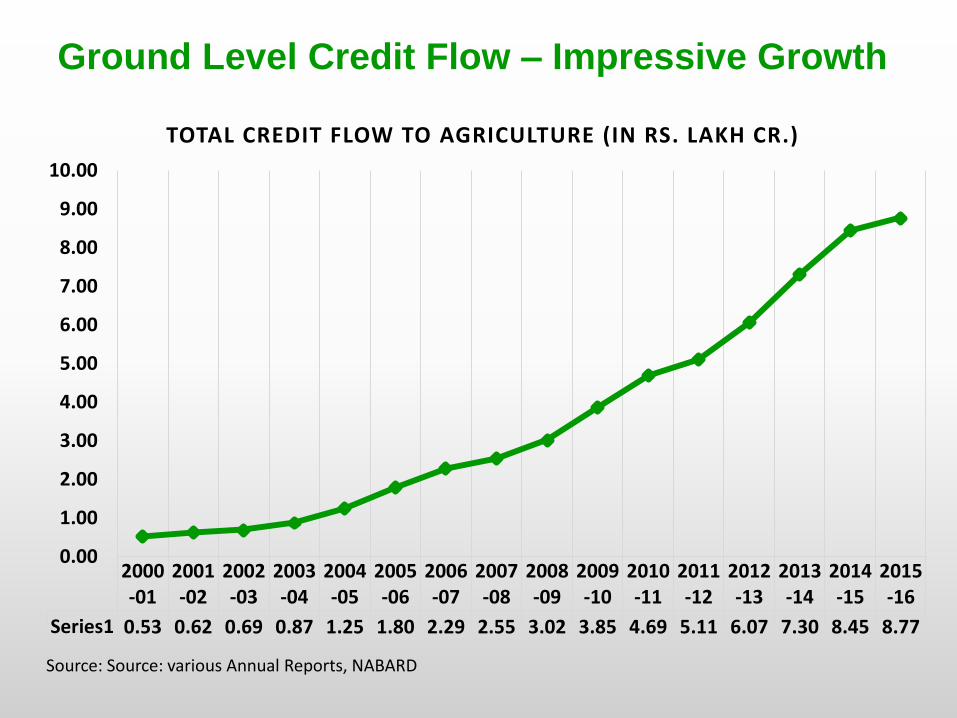

Ground Level Credit Flow – Impressive Growth

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

Series1 0.53 0.62 0.69 0.87 1.25 1.80 2.29 2.55 3.02 3.85 4.69 5.11 6.07 7.30 8.45 8.77

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

TOTAL CREDIT FLOW TO AGRICULTURE (IN RS. LAKH CR.)

Source: Source: various Annual Reports, NABARD

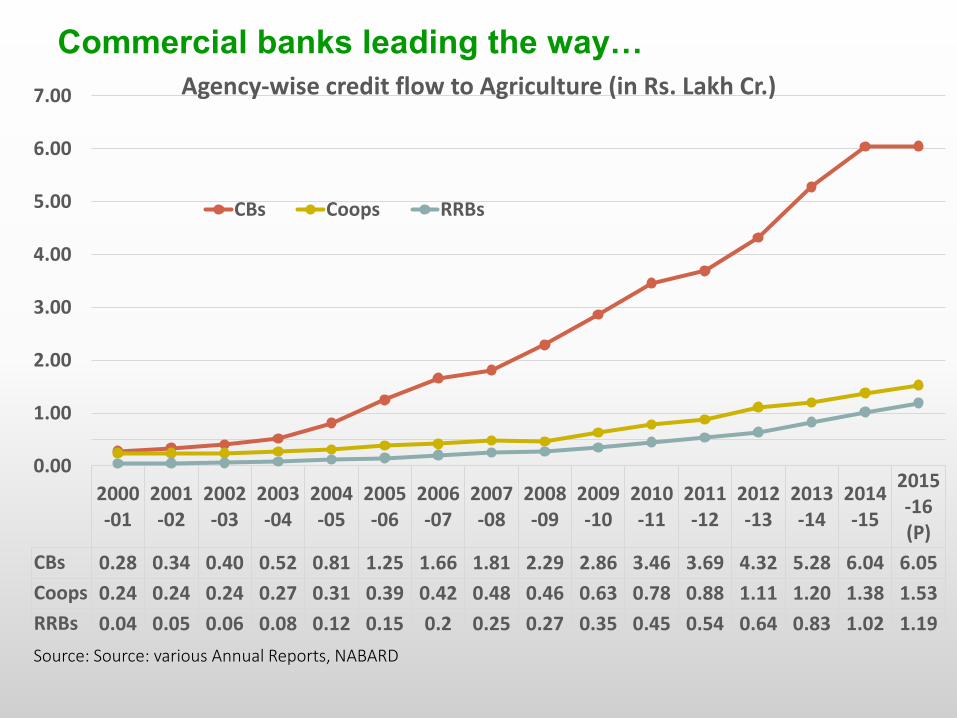

Commercial banks leading the way…

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16(P)

CBs 0.28 0.34 0.40 0.52 0.81 1.25 1.66 1.81 2.29 2.86 3.46 3.69 4.32 5.28 6.04 6.05

Coops 0.24 0.24 0.24 0.27 0.31 0.39 0.42 0.48 0.46 0.63 0.78 0.88 1.11 1.20 1.38 1.53

RRBs 0.04 0.05 0.06 0.08 0.12 0.15 0.2 0.25 0.27 0.35 0.45 0.54 0.64 0.83 1.02 1.19

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00 Agency-wise credit flow to Agriculture (in Rs. Lakh Cr.)

CBs Coops RRBs

Source: Source: various Annual Reports, NABARD

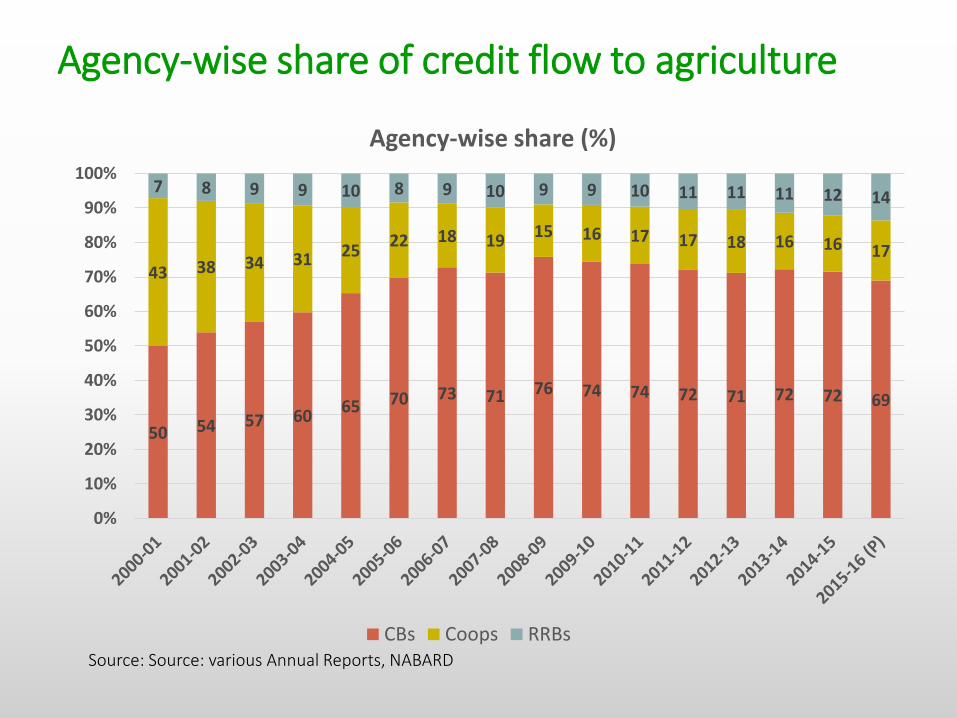

Agency-wise share of credit flow to agriculture

50 54 57 6065 70 73 71 76 74 74 72 71 72 72 69

43 38 34 31 2522 18 19

15 16 17 17 18 16 16 17

7 8 9 9 10 8 9 10 9 9 10 11 11 11 12 14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Agency-wise share (%)

CBs Coops RRBsSource: Source: various Annual Reports, NABARD

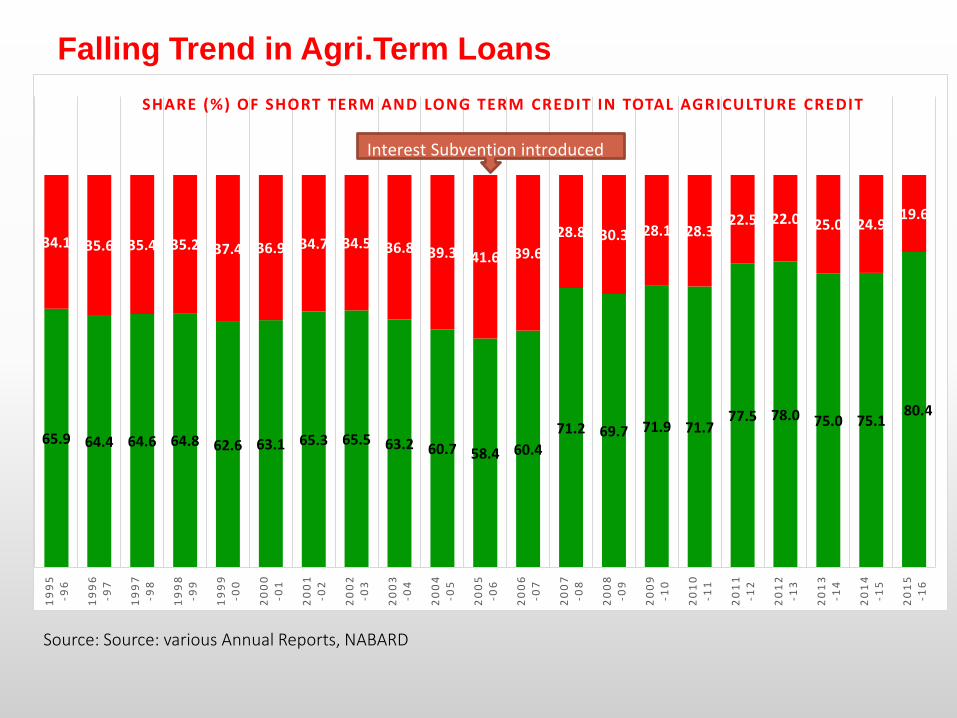

65.9 64.4 64.6 64.8 62.6 63.1 65.3 65.5 63.2 60.7 58.4 60.4

71.2 69.7 71.9 71.777.5 78.0 75.0 75.1

80.4

34.1 35.6 35.4 35.2 37.4 36.9 34.7 34.5 36.8 39.3 41.6 39.6

28.8 30.3 28.1 28.322.5 22.0 25.0 24.9

19.6

19

95

-96

19

96

-97

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

11

-12

20

12

-13

20

13

-14

20

14

-15

20

15

-16

SHARE (%) OF SHORT TERM AND LONG TERM CREDIT IN TOTAL AGRICULTURE CREDIT

Interest Subvention introduced

Falling Trend in Agri.Term Loans

Source: Source: various Annual Reports, NABARD

Policy Initiatives

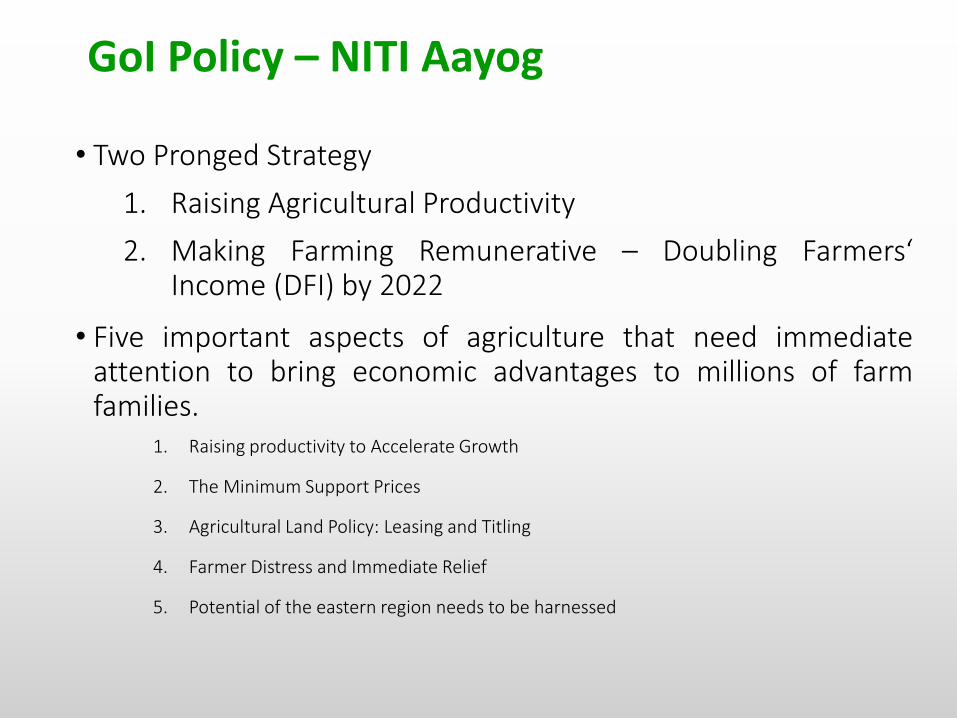

GoI Policy – NITI Aayog

• Two Pronged Strategy

1. Raising Agricultural Productivity

2. Making Farming Remunerative – Doubling Farmers‘Income (DFI) by 2022

• Five important aspects of agriculture that need immediateattention to bring economic advantages to millions of farmfamilies.

1. Raising productivity to Accelerate Growth

2. The Minimum Support Prices

3. Agricultural Land Policy: Leasing and Titling

4. Farmer Distress and Immediate Relief

5. Potential of the eastern region needs to be harnessed

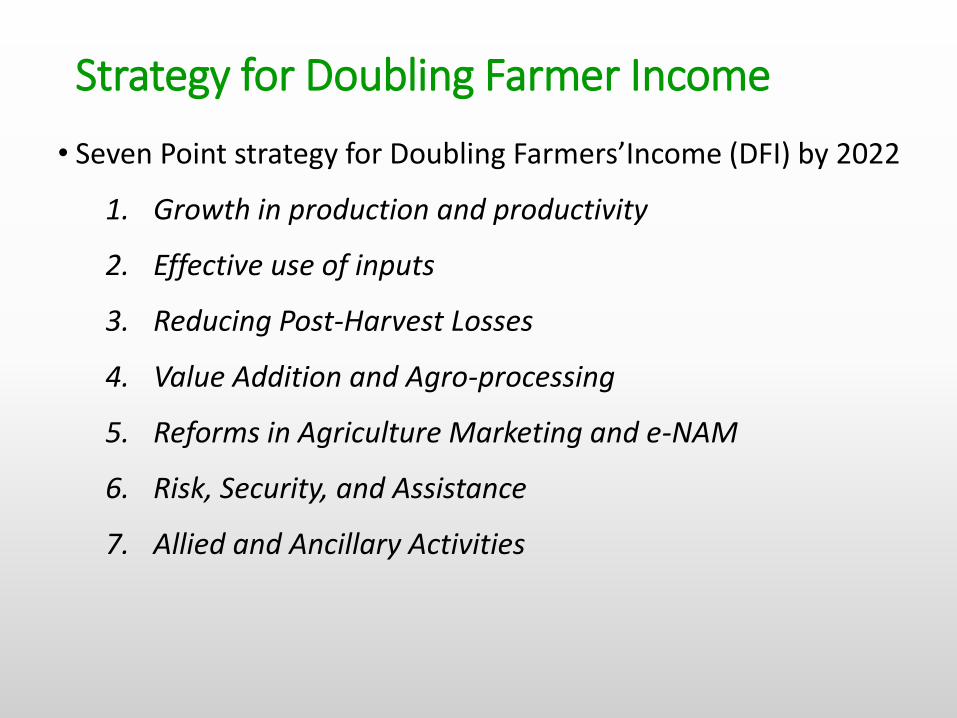

Strategy for Doubling Farmer Income

• Seven Point strategy for Doubling Farmers’Income (DFI) by 2022

1. Growth in production and productivity

2. Effective use of inputs

3. Reducing Post-Harvest Losses

4. Value Addition and Agro-processing

5. Reforms in Agriculture Marketing and e-NAM

6. Risk, Security, and Assistance

7. Allied and Ancillary Activities

Budget Announcements - 2017-18

• Target of Rs.10.0 lakh crore agri credit in FY 2017-18

• Rural, agri and allied – Rs.1.57,223 cr 24% higher than last year

• Committed to double incomes of farmers in five years

• Fasal Bima Yojana allocation is raised to Rs 13,240 crore next fiscal, from Rs 5,500 crore now. Coverage to be 40% (vs.30% last year)

• Rs 5,000 crore Micro-Irrigation Fund to be set up by NABARD

• Long Term Irrigation Fund (LTIF) – corpus to Rs.40000 cr

• New minilabs in 648 KVKs for soil testing

34

• Continued thrust

on doubling

incomes

• Measures

covering water

saving, allied

sectors, market

reform, risk cover

towards that goal

• RA/DF product

for Minilabs by

NB?

Budget Announcements - 2017-18

• Dairy Processing Infra Fund - corpus Rs.2000 cr to grow to Rs 8,000 crore in 3 years

• Agri credit target: Rs 10 lakh cr (2016-17: 9 lakh cr)

• Model law on Contract farming

• Market Reforms

• Coverage of eNAM to expand from 250 to 585

APMCs - Assistance of upto Rs 75 lakh for cleaning

and packaging of farmer produce

• Market reforms will be undertaken, states will be

asked to de-notify perishables from Essential

Commodities Act

• eNAM to integrate with commodity exchanges35

• Increase in

credit target is

a necessary

condition. FI is

sufficient

condition as

40% of farmers

are out of insttl

network

• Persistent in

targeting agri

market reforms

• Growth in volumes impressive - physical outreach is a concern(40% farm households do not have access to Institutionalcredit)

• Only 2% of the food produced is processed while farmcommodities worth Rs.92,000 crores are wasted every year

• Inadequate post harvest infrastructure- as against requirementof 61 mln tonnes of cold storage capacity, only 32 mln tonnesset up so far. Deficit of 29 million tonnes

• Credit (input) intensity increasing rapidly, production response not commensurate.

• Flagging marginal productivity of credit – Issues in real sector –role of public investment.

• Credit focused on production (inputs) - income side of farmers – value addition & marketing - remains a concern.

Challenges and way forward

Emerging Agriculture and Agrifinance

• Financing High value agriculture:

Horticulture – growing fruits & vegetables, a wise & best option …

The new Green Revolution termed as ‘Organic Green Revolution’

High-tech agricultural projects – green house, floriculture, etc.

Livestock & Dairy – exploring livelihood Options

Plantations, agroforestry, wasteland development etc.

• Financing Urban and peri-urban agriculture:

scope for production of Organic Crops

Vertical farming Hydroponics/Aeroponics

• Agriculture to agri-business: Agriculture as an enterprise

• Financing the entire value chain – supply / value chain financing

Compiled by

Dr. Kanhu Charan BadatyaGM & Member of Faculty

College of Agricultural Banking (CAB), Reserve Bank of India (RBI), Pune

Recommended