0

WIK Relevant Markets Conference, Brussels, 18 November 2014

All-IP and the implications

for voice regulation

J. Scott Marcus

1

WIK Relevant Markets Conference, Brussels, 18 November 2014

PSTN and IP Interconnection and

Two-sided Markets

• Traditional PSTN/PLMN interconnection

• IP-based data interconnection

• IP-based voice interconnection

• Implications of IP-based voice interconnection for

market analysis

• Observations

2

WIK Relevant Markets Conference, Brussels, 18 November 2014

Interconnection in an evolving world

• Switched fixed and mobile networks

- Termination fees in the absence of regulation will tend to

be very high, for both large and small operators.

• Internet

- Peering: two providers exchange traffic only for their

respective customers, often (but not always) with no

explicit charges.

- In most countries, no regulation of peering.

• What happens “when worlds collide”?

3

WIK Relevant Markets Conference, Brussels, 18 November 2014

Traditional interconnection vs IP

interconnection

4

WIK Relevant Markets Conference, Brussels, 18 November 2014

• Calling Party's Network Pays (CPNP) wholesale arrangements

• An alternative (United States) is to have negotiated arrangements under

obligations of reciprocity, often resulting in no wholesale charges (Bill and

Keep). Variants have been used in Canada, Hong Kong, Singapore, ....

Economic background:

Traditional Fixed and Mobile Interconnection Models

Originating

Network

Terminating

Network

Call placed Call received

Retail

CPP

Payment

Wholesale CPNP PaymentWholesale CPNP Payment

5

WIK Relevant Markets Conference, Brussels, 18 November 2014

Economic background: Wholesale and retail

• In an unregulated CPNP system, carriers will tend to establish

very high termination charge levels (the termination monopoly).

- Smaller operators will be motivated to set termination fees even

higher than large operators.

- The problem is addressed in the EU by regulating all rates.

• Several factors contribute to the termination monopoly.

- Since the charges are ultimately borne by another operator’s

customers, normal market forces do not adequately constrain them.

- Customers have no visibility into termination fees.

• Termination charges at the wholesale level interact with retail

pricing arrangements.

- The termination fee generally sets a floor on the retail price.

- Where termination fees are high, they generally limit the

applicability of flat rate or “buckets of minutes” plans.

6

WIK Relevant Markets Conference, Brussels, 18 November 2014

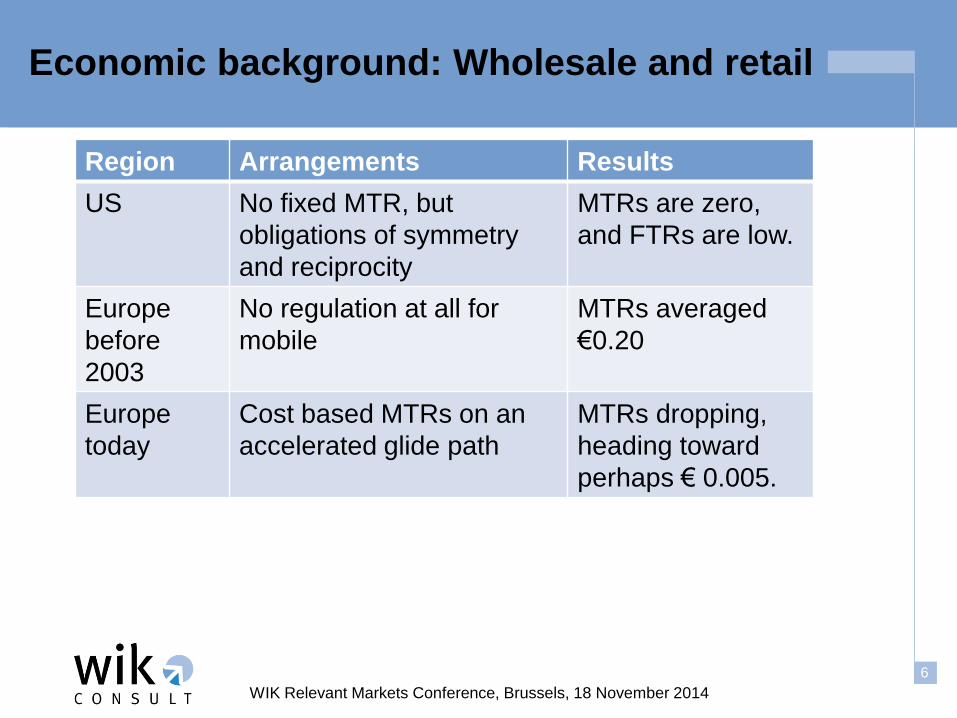

Economic background: Wholesale and retail

Region Arrangements Results

US No fixed MTR, but

obligations of symmetry

and reciprocity

MTRs are zero,

and FTRs are low.

Europe

before

2003

No regulation at all for

mobile

MTRs averaged

€0.20

Europe

today

Cost based MTRs on an

accelerated glide path

MTRs dropping,

heading toward

perhaps € 0.005.

7

WIK Relevant Markets Conference, Brussels, 18 November 2014

Two-Sided Markets

• A relatively new branch of economics deals with two-sided

markets.

• In a two-sided market, a platform provider somehow benefits

by bringing the sides of the market together.

• Payment could come from either side of the market; thus,

relationships between price and cost that would be irrational

in a conventional market might be reasonable in a two-sided

market.

• Examples include broadcast television, and singles bars.

• Rochet, Jean-Charles/ Tirole, Jean (2004): Two Sided

Markets : An Overview, March 2004

8

WIK Relevant Markets Conference, Brussels, 18 November 2014

Two-sided markets … with apologies to John Tenniel and Charles Lutwidge Dodgson.

9

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice call termination as a two-sided market

• Some have argued based on two-sided market theory that a

decline in TRs should lead to an increase in retail price.

• This is plausible, but other factors appear to dominate.

• Wholesale revenues represent only 15% of total mobile

revenues (BoAML), so the direct impact is relatively small.

This limits the magnitude of any two-sided market effects.

• For Mobile-to-Mobile (M2M) calls, the termination rate is a

cost. Lowering the cost of calls in a competitive market tends

to reduce the price, not to increase it. The fraction of calls

that are M2M is increasing.

• Lowering MTRs limits the ability of large MNOs to prevent

small ones from competing on price through on-net off-net

price discrimination, thus enhancing competition.

10

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice call termination and retail revenues

Service-Based Revenue per MoU vs MTRs in Europe

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

2004 2005 2006 2007 2008

$ (

US

)

SBR/MOU

MTR (PPP corrected)

11

WIK Relevant Markets Conference, Brussels, 18 November 2014

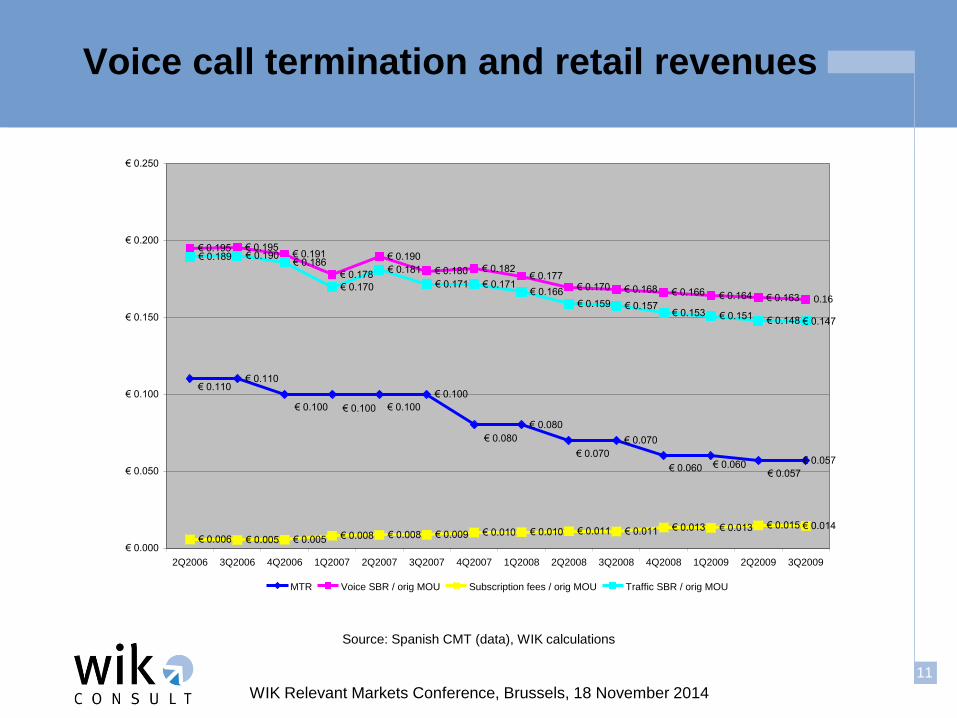

Voice call termination and retail revenues

€ 0.110

€ 0.100

€ 0.080

€ 0.070

€ 0.057

€ 0.195 € 0.195€ 0.191

€ 0.178

€ 0.190

€ 0.180 € 0.182€ 0.177

€ 0.170 € 0.168 € 0.166 € 0.164 € 0.163 0.16

€ 0.006 € 0.005 € 0.005 € 0.008 € 0.008 € 0.009 € 0.010 € 0.010 € 0.011 € 0.011 € 0.013 € 0.013 € 0.015 € 0.014

€ 0.189 € 0.190€ 0.186

€ 0.170

€ 0.181

€ 0.171 € 0.171€ 0.166

€ 0.159 € 0.157€ 0.153 € 0.151

€ 0.148 € 0.147

€ 0.110

€ 0.100€ 0.100€ 0.100

€ 0.057€ 0.060€ 0.060

€ 0.070

€ 0.080

€ 0.000

€ 0.050

€ 0.100

€ 0.150

€ 0.200

€ 0.250

2Q2006 3Q2006 4Q2006 1Q2007 2Q2007 3Q2007 4Q2007 1Q2008 2Q2008 3Q2008 4Q2008 1Q2009 2Q2009 3Q2009

MTR Voice SBR / orig MOU Subscription fees / orig MOU Traffic SBR / orig MOU

Source: Spanish CMT (data), WIK calculations

12

WIK Relevant Markets Conference, Brussels, 18 November 2014

Peering, transit, and Internet access

• Transit

- The customer pays the transit provider to provide

connectivity to substantially all of the Internet.

- Essentially the same service is provided to consumers,

enterprises, ISPs, content provider or application service

providers.

• Peering

- Two ISPs exchange traffic of their customers (and

customers of their customers).

- Often, but not always, done without charge.

• Variants of both exist.

13

WIK Relevant Markets Conference, Brussels, 18 November 2014

Peering, transit, and Internet access

ISP A ISP B ISP 3ISP C

ISP C2

ISP C1

ISP B1

ISP C1a

ISP A2

ISP A1bISP A2

ISP A1

ISP A1a ISP C1b

Peering PeeringISP A ISP B ISP 3ISP C

ISP C2

ISP C1

ISP B1

ISP C1a

ISP A2

ISP A1bISP A2

ISP A1

ISP A1a ISP C1b

Peering Peering

Possibly becoming less hierarchical over time

14

WIK Relevant Markets Conference, Brussels, 18 November 2014

Observations

• Migration of networks to IP is a global trend.

• IP interconnection for Internet traffic is well understood.

• As traditional voice services migrate to IP, there are good

technical reasons to implement interconnection using IP.

• There is movement in this direction, and it is accelerating,

but even in the most developed countries it is not as

advanced as one might expect.

15

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice interconnection via IP

• Different levels of IP-based voice interconnection are visible in

different countries.

• Little or no implementation, little discussion: most of the world.

• Active discussion, implementation only among competitors

and/or cable operators: US (but possibly about to accelerate),

Canada, Spain, New Zealand, many more.

• Active incumbent implementation plans: Germany, Norway.

• Implemented by the incumbent: Denmark, Italy.

• Implementations in South Africa, ongoing work in Namibia!?

• This is not as far advanced overall as you might think!

16

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice interconnection: Denmark

• TDC currently offers both TDM and IP interconnection to alternative

operators.

• Alternative operators that have a PSTN gateway can connect to TDC

either using IP or with traditional interconnection.

TDC network structure

Source: TDC, SIP Connect, Bilag 1b. Tekniske

Specifikationer;

Legend: MGW = Media Gateway;

PGW = PSTN Gateway; PSTN = Public Switched

Telephone Network; RTP = Real Time Transport

Protocol; SS7 = Signaling System No. 7;

SIP = Session Initiation Protocol.

17

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice interconnection: Denmark

• NITA decision (2011)*

- Obligation for TDC to offer IP-IC (from January 1, 2012)

- Later obligation also for Colt, Hi3G, Telenor and Telia (from January 21, 2013)

• DBA (2013)** market 3 decision

- Obligation to terminate voice calls to PSTN-, ISDN- and VoIP

subscribers (SS7- and IP-based) imposed on TDC and 36 other SMP

operators

- Specification of 6 PoIs for IP-termination on TDC‘s network

- No obligation regarding TDM-IP conversion, rather subject to

negotiations of market participants; costs of conversion are not part of

the regulated prices

• DBA cost models rest solely on IP technology

• IT- & Telestyrelsen (2011): Markedsafgørelse over for TDC A/S på engrosmar-kedet for fastnetterminering

(marked 3); in particular section 7.5; 20. januar 2011.

• * DBA (2013): Engrosmarkedet for fastnetterminering (marked 3) - Markedsafgørelse over for TDC samt

markedsafgrænsning og -analyse; 18 december; available at:

http://erhvervsstyrelsen.dk/file/436699/endelig-afgorelse.pdf

18

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice interconnection: Italy

• AGCOM has put regulations in place (already in 2011).

• Ministry Economic Dev has developed technical standards (2012).

• Telecom Italia has published:

- Reference Offer 2013 for IP interconnection on October 31, 2012

- A manual of procedures for IP interconnection

- AGCOM has put revised 2013 Reference Offer for public consultation;

final adoption likely end of 2014.

• TI plan based on 16 VoIP Gateway Areas each of which is

characterized by two PoIs (geographical redundancy).

• Price regulation: Glide path until 2015 (prices for TDM-IC only regulated until mid of 2015)

• Currently IP-IC related tests underway between TI and other network

operators; limited implementation to date (mostly Fastweb);

significant increase to be expected in 2015 and beyond.

19

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice interconnection: Norway

• Telenor published plans to offer IP interconnection for voice into their

service portfolio in 2012

- All connect on SIP interface

- Termination (POTS, VoIP, Mobil)

- Transit (SIP-SIP, SIP-SS7)

- PSTN Gateway (translation between SIP and SS7).

• Implementation of the project has been postponed several times: up

until today no SIP-Interconnect offer in the market, rather, market

launch likely mid of 2015 at the earliest.

• Price regulation: NPT‘s cost model assumes full migration from

PSTN/ISDN to NGN between 2011-2015; however, in practice

network operators are only obliged to interconnect on the basis of

TDM as long as IP-IC obligation is introduced.

20

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice interconnection: Germany

• Technologically conformant interconnection

• Technologically non-conformant interconnection

21

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice interconnection: Germany

• No real deployment to date, but DTAG plans announced.

• Phase 1 Introduction (end 2011- mid 2013):

- Introduction of NGN-IC

- Test with every interconnection partner (ongoing!)

- Parallel operation of PSTN-IC and NGN-IC

- Market driven migration

- PSTN continues to be in full operation

• Phase 2 Migration (mid 2013 – beginning 2015):

- Tests with all interconnection partners must be completed before launch

- Parallel operation of PSTN-IC and NGN-IC

- Market-driven migration

- Initiation of dismantling of PSTN

• Phase 3 Finalisation (beginning 2015 – end 2016).

- Parallel operation of PSTN-IC and NGN-IC

- PSTN products no longer marketed by Telekom Deutschland

- PSTN Interconnection Points removed

22

WIK Relevant Markets Conference, Brussels, 18 November 2014

Voice interconnection: United States

• An ongoing discussion for many years.

• Cable companies routinely exchange voice traffic via IP.

• Trials between larger telecommunications firms have been a hot

topic for years.

• In the U.S., where regulation is not technologically neutral, migration

to IP might enable incumbents to achieve even greater deregulation.

- Regulatory discussion of IP interconnection issue intertwined with

discussion of phasing-out the PSTN.

- Links as well to the telephone numbering database, and to VoIP caller

ID “spoofing”.

• AT&T and Verizon just announced that they will enable direct Voice

over LTE (VoLTE) to VoLTE connections in 2015.

23

WIK Relevant Markets Conference, Brussels, 18 November 2014

IP migration and the termination monopoly

• In WIK (2008), “The Future of IP Interconnection”, we

considered claims that the migration to IP would open up

connectivity and end the termination monopoly forever.

• We concluded that the termination monopoly stemmed from

the fact that only a single network operator could complete a

call to a single telephone number, and existed independent

of whether PSTN versus IP was used to complete the call.

• Evolving technology still does not seem to have provided

alternatives at wholesale level.

• The Commission has however observed that there may be

an effective retail constraint for “termination of calls to non-

geographic numbers for the provision of value added

services”. (Explanatory Memorandum (2014))

24

WIK Relevant Markets Conference, Brussels, 18 November 2014

Termination services are

“the least replicable input for

retail voice services”! - Commission, Explanatory Memorandum

25

WIK Relevant Markets Conference, Brussels, 18 November 2014

Observations

• Among conventional PSTN/PLMN networks:

- TRs would be very high absent regulation.

- Regulated TRs should approximate long run incremental costs.

• Among Internet networks:

- Transit prices are generally set by the competitive market.

- Peering charges, if any, are set by commercial negotiations.

- Probably the best way to do it (but not everyone agrees).

• As voice moves to IP:

- The termination monopoly is still relevant, at least for now.

- TRs would be very high absent regulation.

- Basing the TR on the IP-based cost seems to make sense.

• The termination monopoly will be with us for a while!

26

WIK Relevant Markets Conference, Brussels, 18 November 2014

References

Marcus, Dieter Elixmann, et al., The Future of IP Interconnection: Technical,

Economic, and Public Policy Aspects, a study prepared for the European

Commission, available at:

http://ec.europa.eu/information_society/policy/ecomm/doc/library/ext_studie

s/future_ip_intercon/ip_intercon_study_final.pdf.

European Commission (2014), Explanatory note accompanying the document

‘Commission Recommendation on relevant product and service markets

within the electronic communications sector susceptible to ex ante

regulation …’

Rochet, Jean-Charles/ Tirole, Jean (2004): Two Sided Markets : An Overview,

March 2004, at: http://faculty.haas.berkeley.edu/hermalin/rochet_tirole.pdf

Laffont, Marcus, Rey and Tirole (2003), “Internet Interconnection and the off-

net Cost Pricing Principle”, RAND Journal of Economics.

wik-Consult GmbH

Postfach 2000

53588 Bad Honnef

Tel 02224-9225-0

Fax 02224-9225-68

eMail [email protected]

www.wik-consult.com

Recommended

![IP (IO $'' (109,8..-f-(-OtOliol..-Otd)Q2 - AIVC11' fW/(mKll langenbezogener Warme· bruckenverlustkoeffizient x (WIK] punktfcirmiger Warme bruckenveriustkoef fizient Wenngleich fUr](https://img.pdfslide.net/doc/110x75/614916689241b00fbd675515/ip-io-1098-f-otoliol-otdq2-aivc-11-fwmkll-langenbezogener-warme.jpg)