Sepura Plc

Analyst Lunch

8 July 2014

2

1. The PMR market

2. Sepura’s position in the market

3. The opportunity

4. Financials

5. Conclusion

6. Q&A

2

3

1. The PMR market

2. Sepura’s position in the market

3. The opportunity

4. Financials

5. Conclusion

6. Q&A

3

4

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

STANDARDS

TETRA DMR Analogue P25 Other

Digital

VA

LU

E C

HA

IN

Network

operation

Network

infrastructure

Voice

Data

Accessories

Software

Services

Niche

products

Commercial

Consumer

Public safety

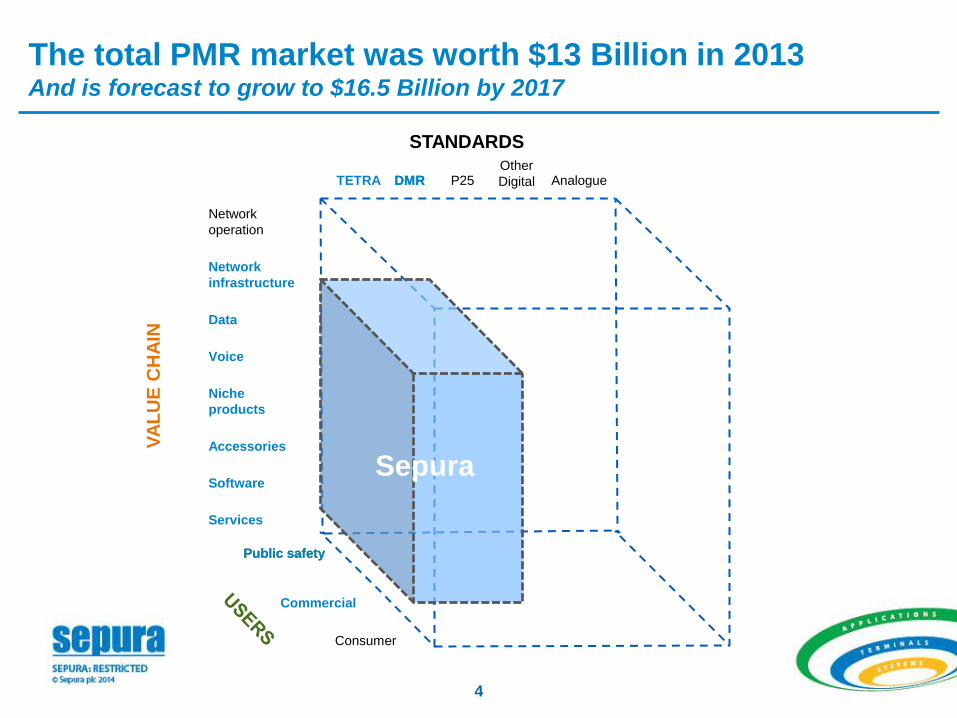

The total PMR market was worth $13 Billion in 2013 And is forecast to grow to $16.5 Billion by 2017

STANDARDS

TETRA DMR Analogue P25 Other

Digital

VA

LU

E C

HA

IN

Network

operation

Network

infrastructure

Voice

Data

Accessories

Software

Services

Niche

products

Commercial

Consumer

Public safety

Sepura

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

5

Analogue

Digital

6,000

5,000

4,000

3,000

2,000

1,000

0 09 10 11 12 13 14 15 16 17

Source: IHS

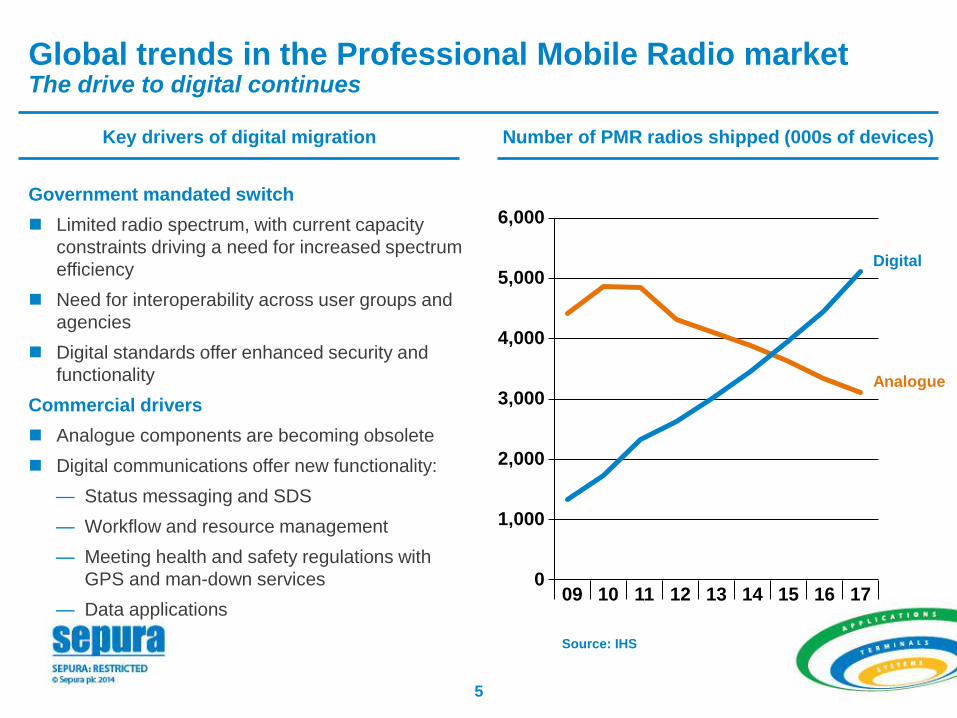

Global trends in the Professional Mobile Radio market The drive to digital continues

Key drivers of digital migration Number of PMR radios shipped (000s of devices)

Government mandated switch

Limited radio spectrum, with current capacity

constraints driving a need for increased spectrum

efficiency

Need for interoperability across user groups and

agencies

Digital standards offer enhanced security and

functionality

Commercial drivers

Analogue components are becoming obsolete

Digital communications offer new functionality:

— Status messaging and SDS

— Workflow and resource management

— Meeting health and safety regulations with

GPS and man-down services

— Data applications

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

6

Analogue

60,000

50,000

40,000

30,000

20,000

10,000

0 09 10 11 12 13 14 15 16 17

Source: IHS

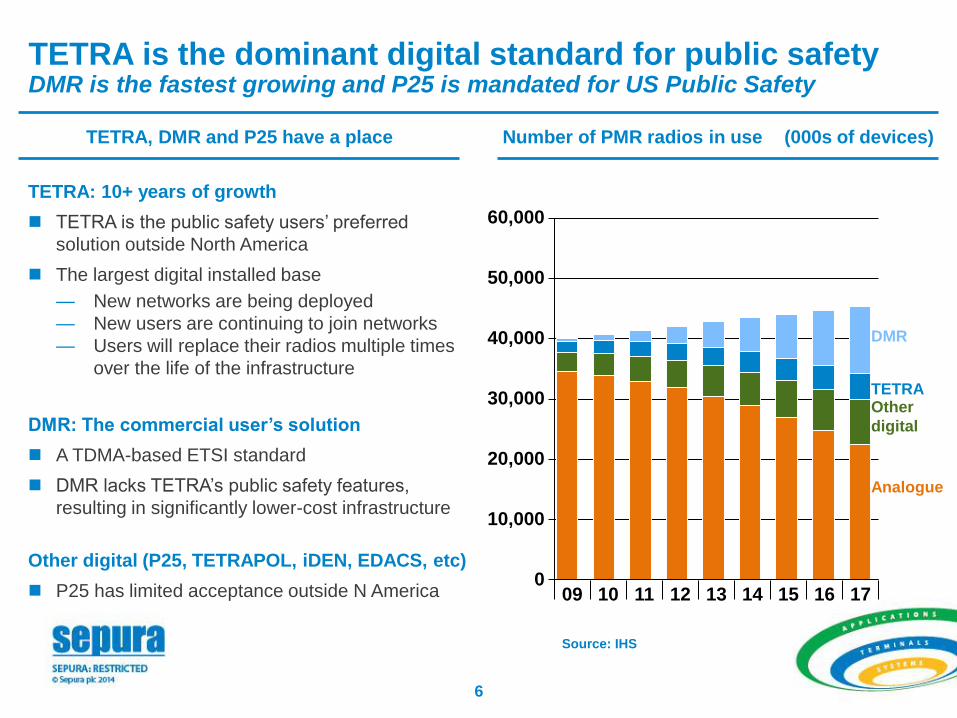

TETRA, DMR and P25 have a place

TETRA is the dominant digital standard for public safety DMR is the fastest growing and P25 is mandated for US Public Safety

Number of PMR radios shipped (000s of devices) in use

DMR

Other

digital

TETRA

TETRA: 10+ years of growth

TETRA is the public safety users’ preferred

solution outside North America

The largest digital installed base

— New networks are being deployed

— New users are continuing to join networks

— Users will replace their radios multiple times

over the life of the infrastructure

DMR: The commercial user’s solution

A TDMA-based ETSI standard

DMR lacks TETRA’s public safety features,

resulting in significantly lower-cost infrastructure

Other digital (P25, TETRAPOL, iDEN, EDACS, etc)

P25 has limited acceptance outside N America

7

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

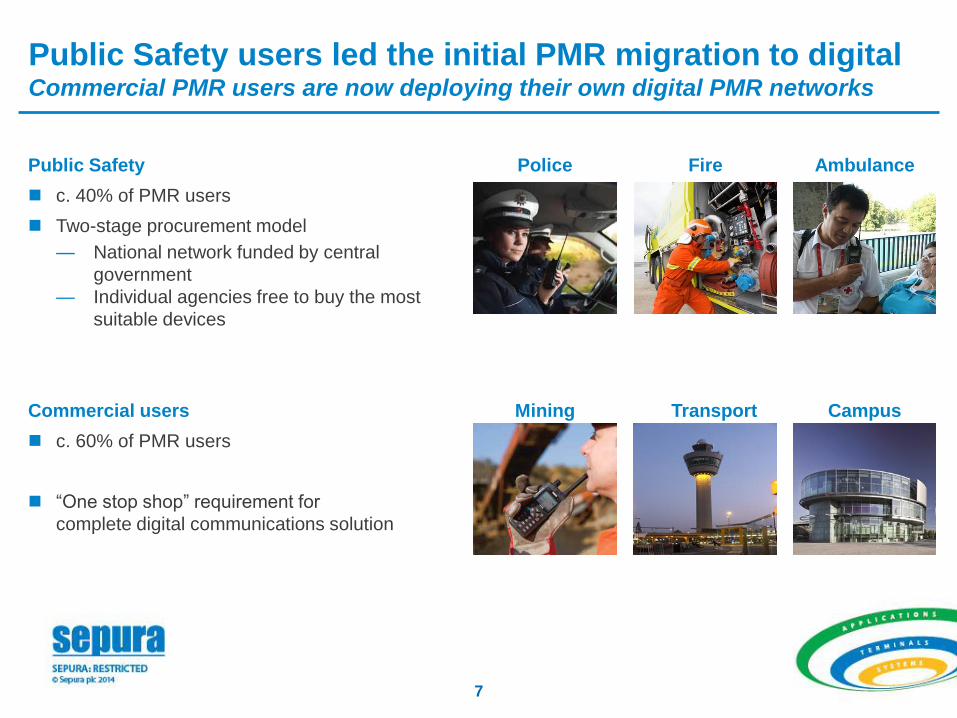

Public Safety users led the initial PMR migration to digital Commercial PMR users are now deploying their own digital PMR networks

Public Safety

c. 40% of PMR users

Two-stage procurement model

— National network funded by central

government

— Individual agencies free to buy the most

suitable devices

Police Fire Ambulance

Mining Commercial users

c. 60% of PMR users

“One stop shop” requirement for

complete digital communications solution

Campus Transport

8

1. The PMR market

2. Sepura’s position in the market

3. The opportunity

4. Financials

5. Conclusion

6. Q&A

8

9

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

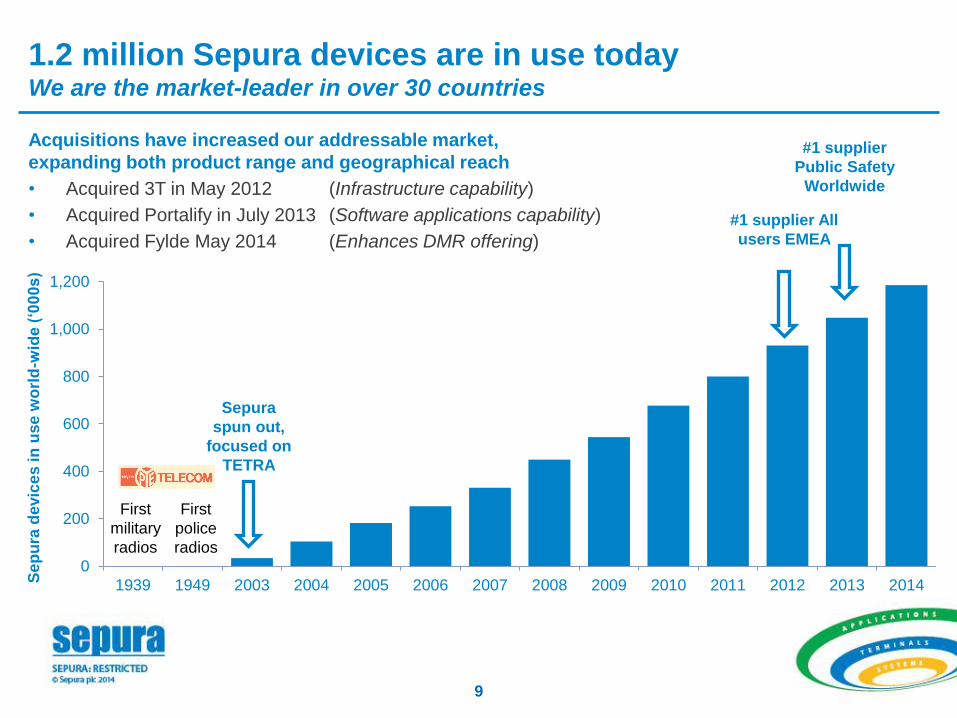

1.2 million Sepura devices are in use today We are the market-leader in over 30 countries

0

200

400

600

800

1,000

1,200

1939 1949 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

First

military

radios

First

police

radios

Se

pu

ra d

evic

es

in

use

wo

rld

-wid

e (

‘00

0s

)

Sepura

spun out,

focused on

TETRA

#1 supplier

Public Safety

Worldwide

#1 supplier All

users EMEA

Acquisitions have increased our addressable market,

expanding both product range and geographical reach

• Acquired 3T in May 2012 (Infrastructure capability)

• Acquired Portalify in July 2013 (Software applications capability)

• Acquired Fylde May 2014 (Enhances DMR offering)

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

10

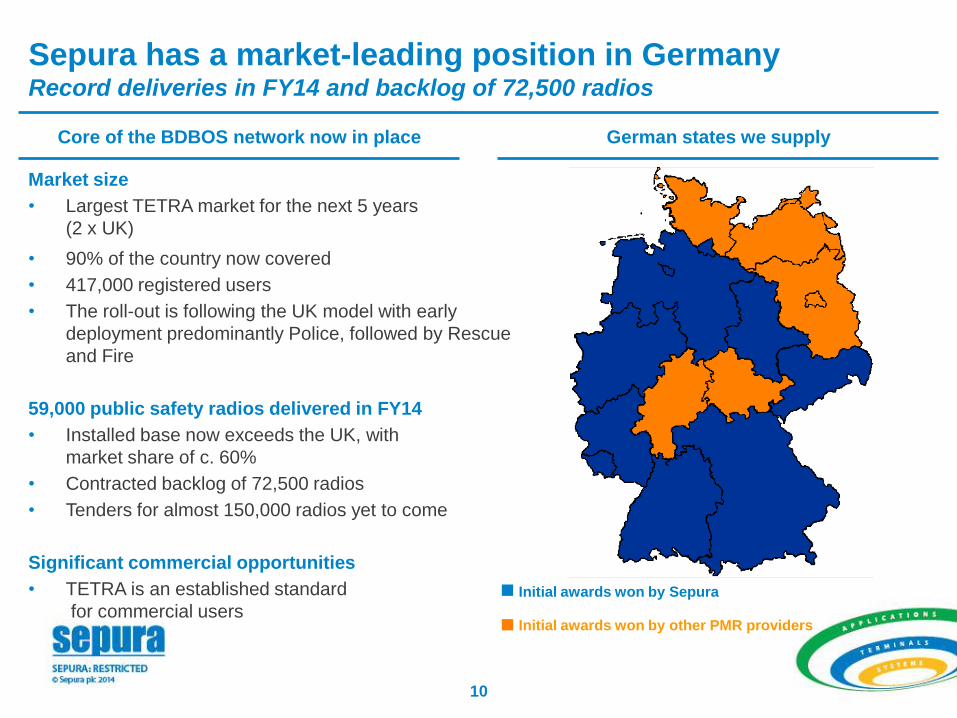

Sepura has a market-leading position in Germany Record deliveries in FY14 and backlog of 72,500 radios

Core of the BDBOS network now in place

German states we supply

Initial awards won by Sepura

Initial awards won by other PMR providers

Market size

• Largest TETRA market for the next 5 years

(2 x UK)

• 90% of the country now covered

• 417,000 registered users

• The roll-out is following the UK model with early

deployment predominantly Police, followed by Rescue

and Fire

59,000 public safety radios delivered in FY14

• Installed base now exceeds the UK, with

market share of c. 60%

• Contracted backlog of 72,500 radios

• Tenders for almost 150,000 radios yet to come

Significant commercial opportunities

• TETRA is an established standard

for commercial users

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

11

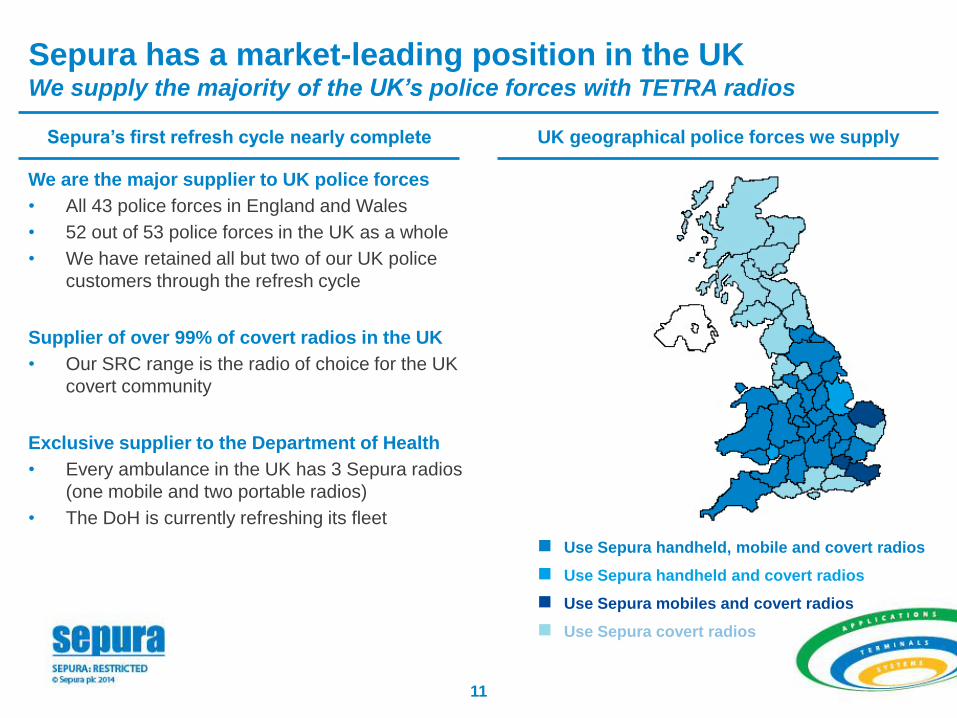

Sepura has a market-leading position in the UK We supply the majority of the UK’s police forces with TETRA radios

Sepura’s first refresh cycle nearly complete UK geographical police forces we supply

We are the major supplier to UK police forces

• All 43 police forces in England and Wales

• 52 out of 53 police forces in the UK as a whole

• We have retained all but two of our UK police

customers through the refresh cycle

Supplier of over 99% of covert radios in the UK

• Our SRC range is the radio of choice for the UK

covert community

Exclusive supplier to the Department of Health

• Every ambulance in the UK has 3 Sepura radios

(one mobile and two portable radios)

• The DoH is currently refreshing its fleet

Use Sepura handheld, mobile and covert radios

Use Sepura mobiles and covert radios

Use Sepura covert radios

Use Sepura handheld and covert radios

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

12

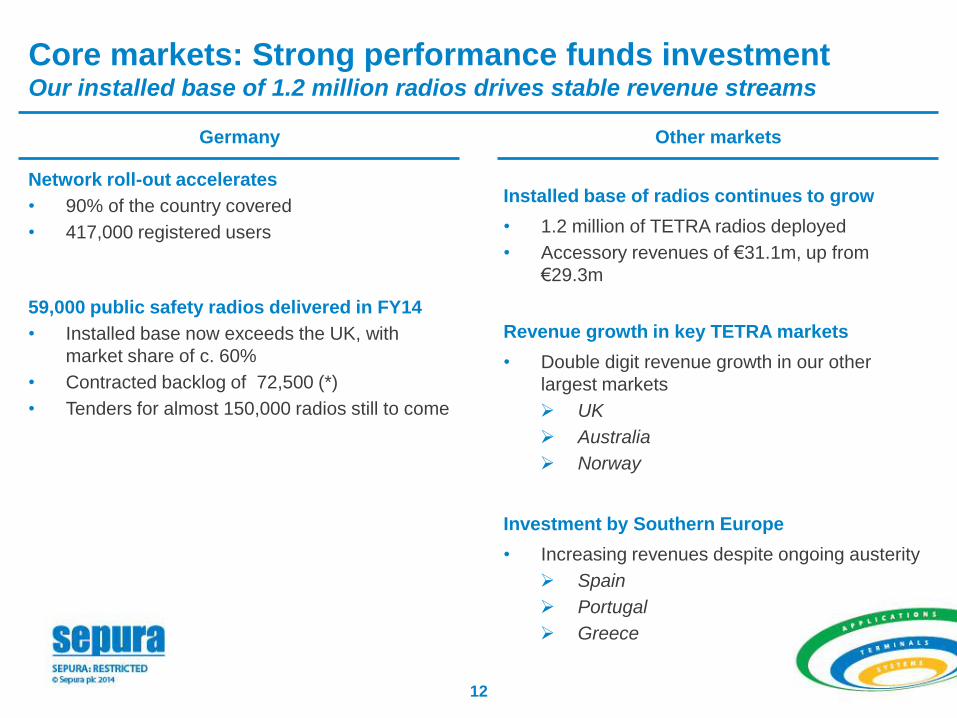

Core markets: Strong performance funds investment Our installed base of 1.2 million radios drives stable revenue streams

Germany

Other markets

Network roll-out accelerates

• 90% of the country covered

• 417,000 registered users

59,000 public safety radios delivered in FY14

• Installed base now exceeds the UK, with

market share of c. 60%

• Contracted backlog of 72,500 (*)

• Tenders for almost 150,000 radios still to come

Installed base of radios continues to grow

• 1.2 million of TETRA radios deployed

• Accessory revenues of €31.1m, up from

€29.3m

Revenue growth in key TETRA markets

• Double digit revenue growth in our other

largest markets

UK

Australia

Norway

Investment by Southern Europe

• Increasing revenues despite ongoing austerity

Spain

Portugal

Greece

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

13

STANDARDS

TETRA DMR Analogue P25 Other

Digital

VA

LU

E C

HA

IN

Network

operation

Network

infrastructure

Voice

Data

Accessories

Software

Services

Niche

products

Commercial

Consumer

Public safety

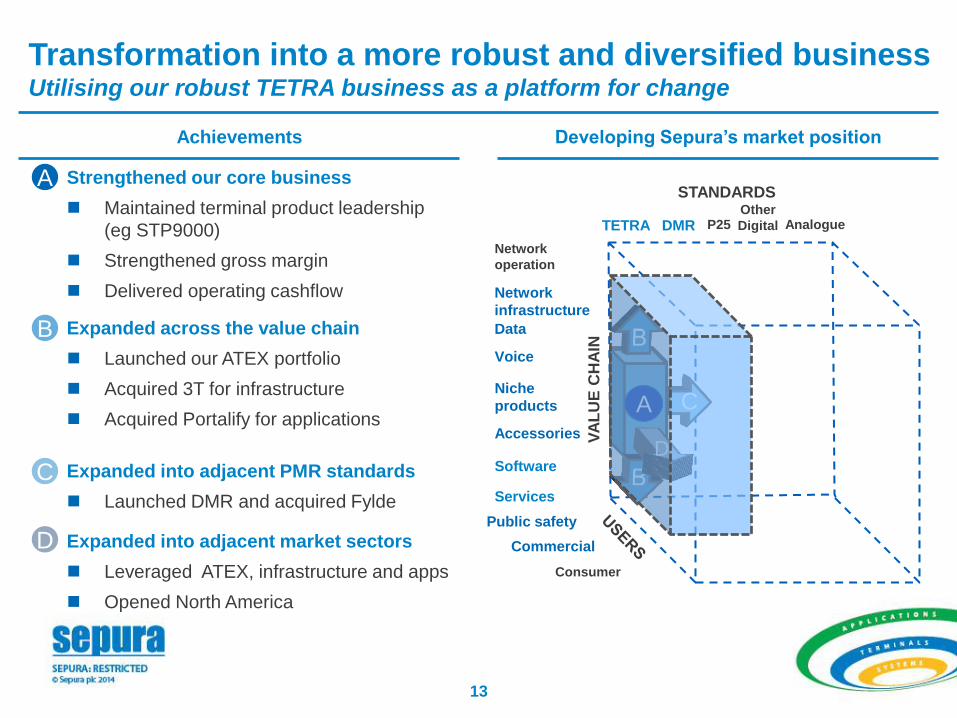

Achievements Developing Sepura’s market position

Transformation into a more robust and diversified business Utilising our robust TETRA business as a platform for change

Strengthened our core business

Maintained terminal product leadership

(eg STP9000)

Strengthened gross margin

Delivered operating cashflow

A

A

Expanded into adjacent PMR standards

Launched DMR and acquired Fylde

C

DMR

A C

Expanded across the value chain

Launched our ATEX portfolio

Acquired 3T for infrastructure

Acquired Portalify for applications

B

Software

Services

A

Data

Network

infrastructure

D Expanded into adjacent market sectors

Leveraged ATEX, infrastructure and apps

Opened North America

D

Commercial

14

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

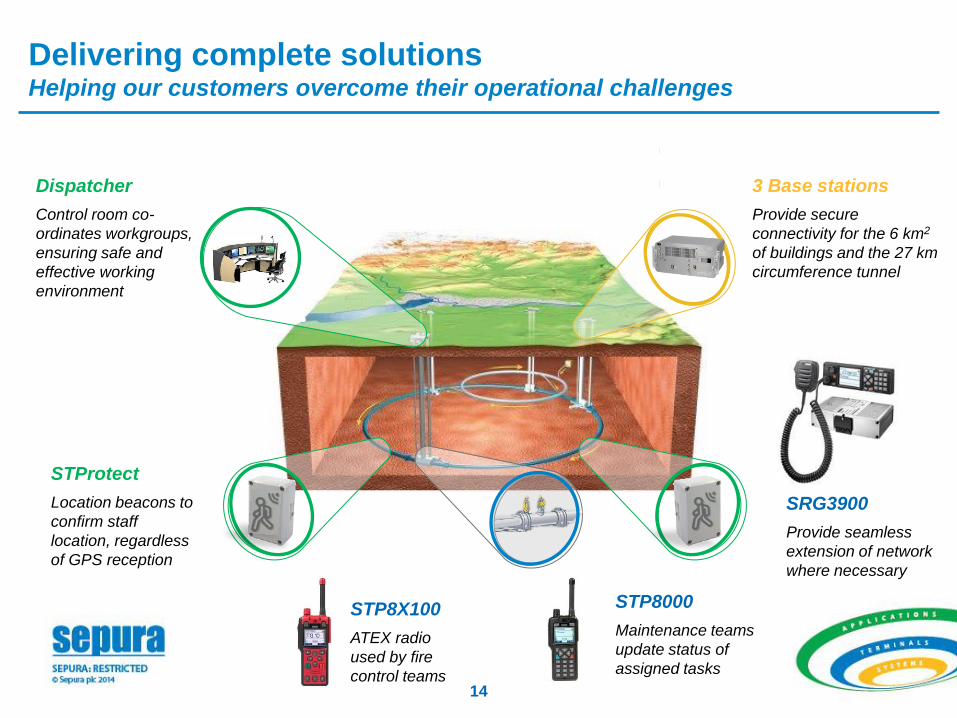

6 km2 of buildings

27 km circumference

tunnel,

50 - 175m below ground

Complex magnetic

environment

Delivering complete solutions Helping our customers overcome their operational challenges

STP8000

Maintenance teams

update status of

assigned tasks

SRG3900

Provide seamless

extension of network

where necessary

STP8X100

ATEX radio

used by fire

control teams

3 Base stations

Provide secure

connectivity for the 6 km2

of buildings and the 27 km

circumference tunnel

Dispatcher

Control room co-

ordinates workgroups,

ensuring safe and

effective working

environment

STProtect

Location beacons to

confirm staff

location, regardless

of GPS reception

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

15

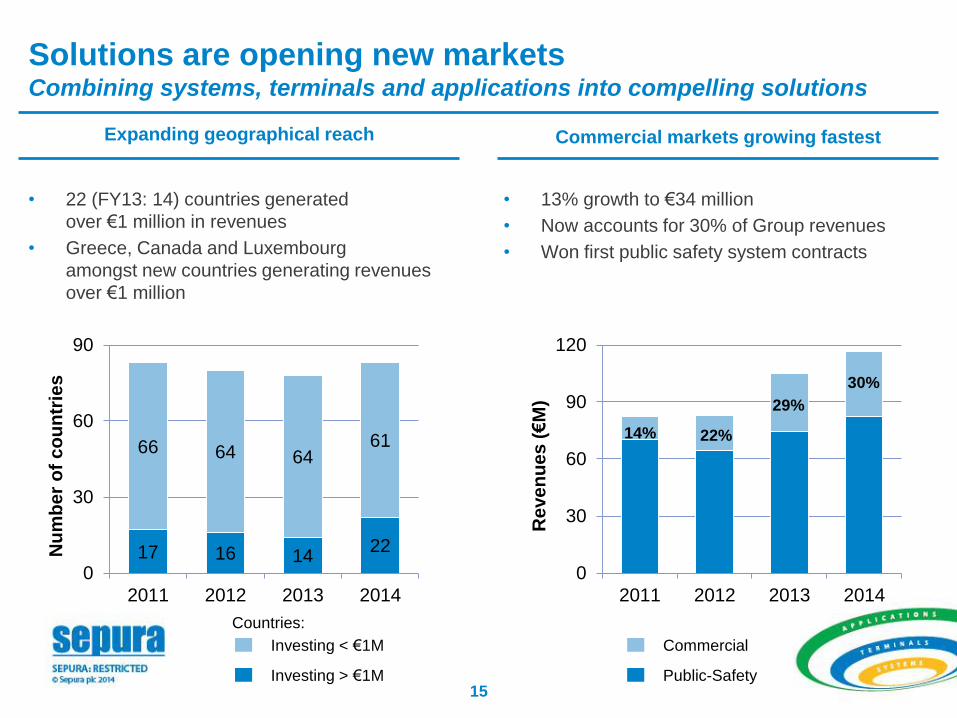

Commercial markets growing fastest

• 22 (FY13: 14) countries generated

over €1 million in revenues

• Greece, Canada and Luxembourg

amongst new countries generating revenues

over €1 million

Expanding geographical reach

• 13% growth to €34 million

• Now accounts for 30% of Group revenues

• Won first public safety system contracts

Investing < €1M

Investing > €1M

Commercial

Public-Safety

Re

ve

nu

es

(€M

)

0

30

60

90

120

2011 2012 2013 2014

29%

30%

22%

17 16 14 22

66 64 64 61

0

30

60

90

2011 2012 2013 2014

Nu

mb

er

of

co

un

trie

s

Solutions are opening new markets Combining systems, terminals and applications into compelling solutions

Countries:

14%

16

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

STProtect

STP8X000 STP9000 STP8X100

Radio Manager 2 SRG3900

Maintaining product leadership through innovation Our continuous process to enhance existing products and deliver new ones

DMR

17

1. The PMR market

2. Sepura’s position in the market

3. The opportunity

4. Financials

5. Conclusion

6. Q&A

17

18

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

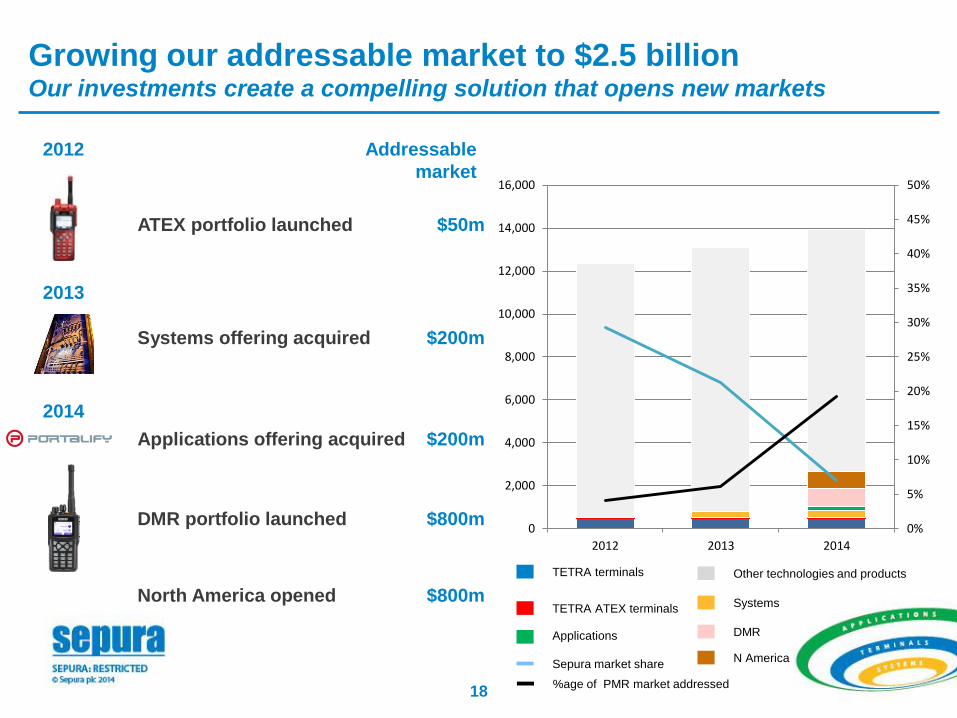

ATEX portfolio launched $50m

2012 Addressable

market

Systems offering acquired $200m

2013

Applications offering acquired $200m

2014

DMR portfolio launched $800m

North America opened $800m

Growing our addressable market to $2.5 billion Our investments create a compelling solution that opens new markets

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2012 2013 2014

DMR

TETRA terminals Other technologies and products

Applications

Sepura market share

Systems TETRA ATEX terminals

%age of PMR market addressed

N America

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

19

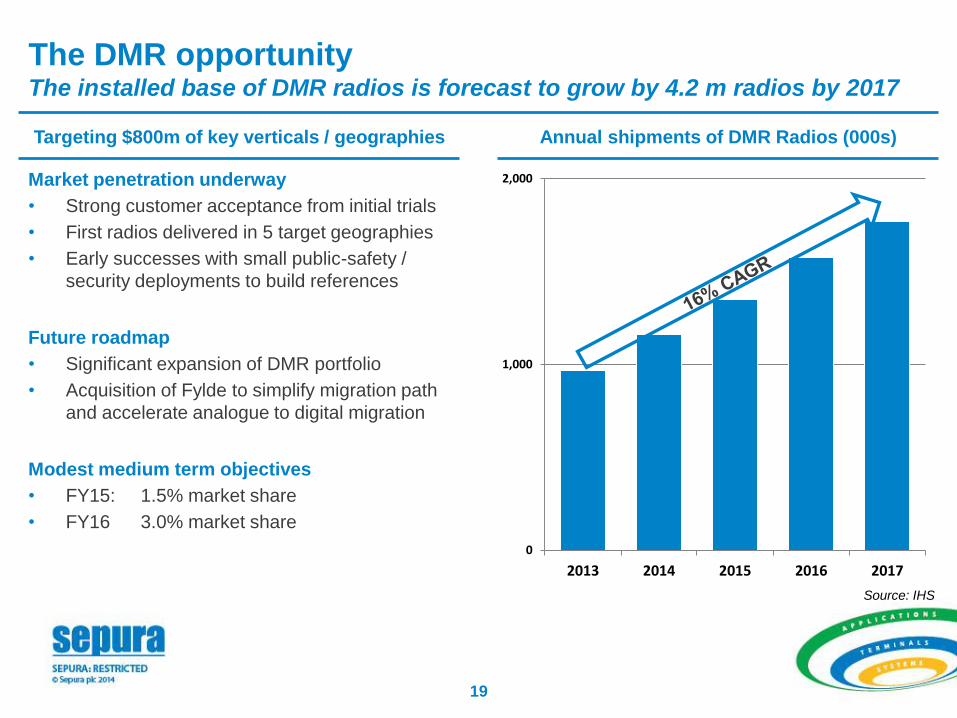

The DMR opportunity The installed base of DMR radios is forecast to grow by 4.2 m radios by 2017

0

1,000

2,000

2013 2014 2015 2016 2017

Annual shipments of DMR Radios (000s)

Market penetration underway

• Strong customer acceptance from initial trials

• First radios delivered in 5 target geographies

• Early successes with small public-safety /

security deployments to build references

Future roadmap

• Significant expansion of DMR portfolio

• Acquisition of Fylde to simplify migration path

and accelerate analogue to digital migration

Modest medium term objectives

• FY15: 1.5% market share

• FY16 3.0% market share

Targeting $800m of key verticals / geographies

Source: IHS

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

20

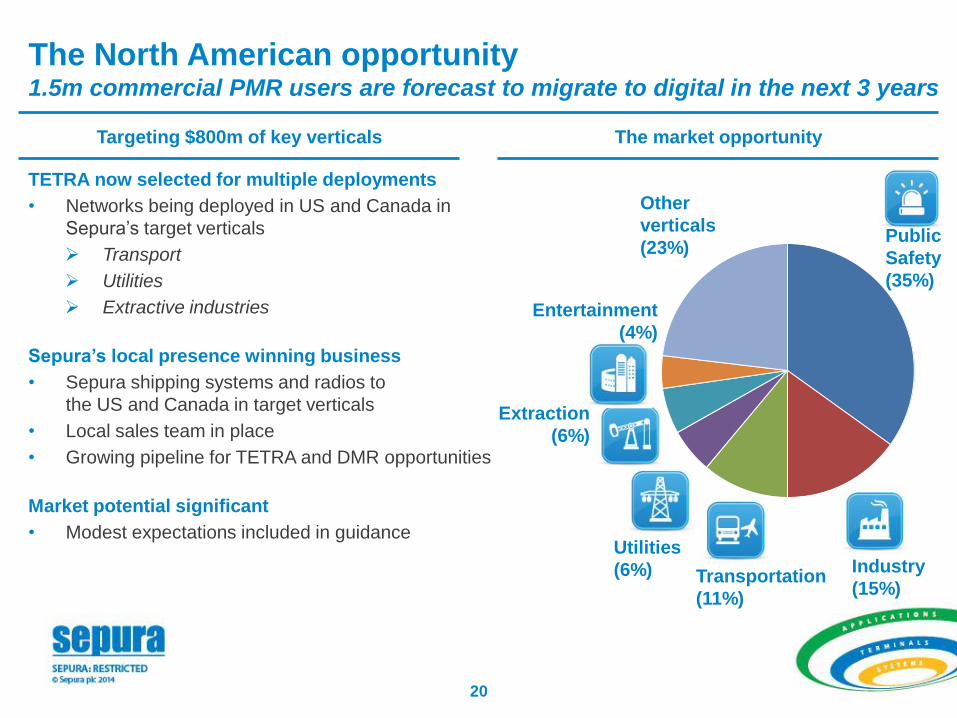

The North American opportunity 1.5m commercial PMR users are forecast to migrate to digital in the next 3 years

The market opportunity Targeting $800m of key verticals

Extraction

(6%)

Utilities

(6%) Transportation

(11%)

Public

Safety

(35%)

Industry

(15%)

Entertainment

(4%)

Other

verticals

(23%)

TETRA now selected for multiple deployments

• Networks being deployed in US and Canada in

Sepura’s target verticals

Transport

Utilities

Extractive industries

Sepura’s local presence winning business

• Sepura shipping systems and radios to

the US and Canada in target verticals

• Local sales team in place

• Growing pipeline for TETRA and DMR opportunities

Market potential significant

• Modest expectations included in guidance

21

1. The PMR market

2. Sepura’s position in the market

3. The opportunity

4. Financials

5. Conclusion

6. Q&A

21

22

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

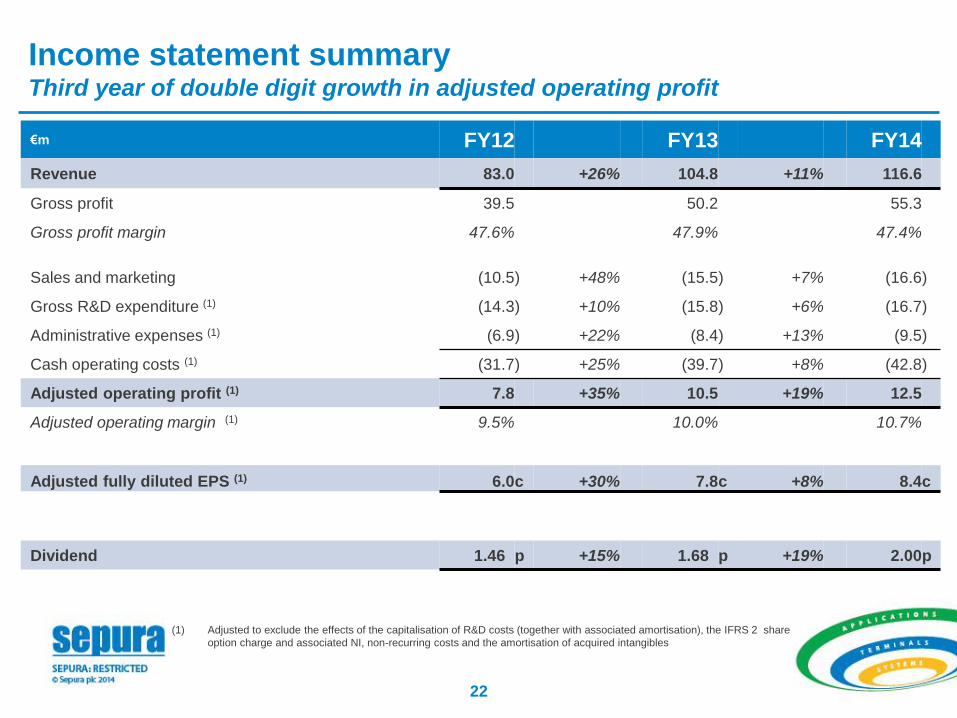

€m FY12 FY13 FY14

Revenue 83.0 +26% 104.8 +11% 116.6

Gross profit 39.5 50.2 55.3

Gross profit margin 47.6% 47.9% 47.4%

Sales and marketing (10.5 ) +48% (15.5 ) +7% (16.6 )

Gross R&D expenditure (1) (14.3 ) +10% (15.8 ) +6% (16.7 )

Administrative expenses (1) (6.9 ) +22% (8.4 ) +13% (9.5 )

Cash operating costs (1) (31.7 ) +25% (39.7 ) +8% (42.8 )

Adjusted operating profit (1) 7.8 +35% 10.5 +19% 12.5

Adjusted operating margin (1) 9.5% 10.0% 10.7%

Adjusted fully diluted EPS (1) 6.0 c +30% 7.8 c +8% 8.4 c

Dividend 1.46 p +15% 1.68 p +19% 2.00 p

(1) Adjusted to exclude the effects of the capitalisation of R&D costs (together with associated amortisation), the IFRS 2 share

option charge and associated NI, non-recurring costs and the amortisation of acquired intangibles

Income statement summary Third year of double digit growth in adjusted operating profit

23

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

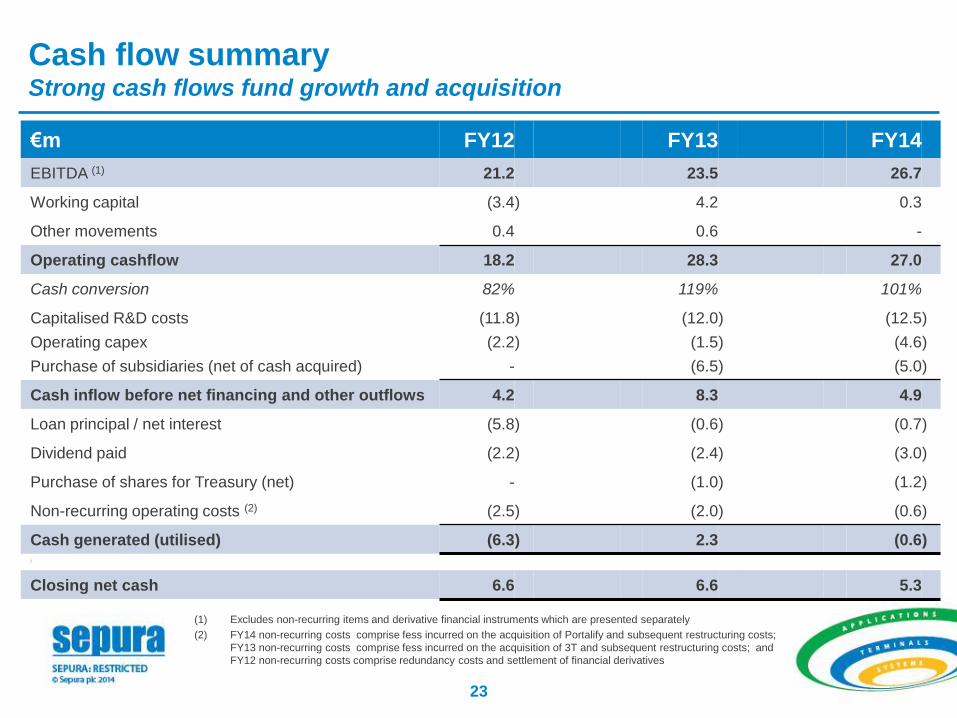

€m FY12 FY13 FY14

EBITDA (1) 21.2 23.5 26.7

Working capital (3.4 ) 4.2 0.3

Other movements 0.4 0.6 -

Operating cashflow 18.2 28.3 27.0

Cash conversion 82% 119% 101%

Capitalised R&D costs (11.8 ) (12.0 ) (12.5 )

Operating capex (2.2 ) (1.5 ) (4.6 )

Purchase of subsidiaries (net of cash acquired) - (6.5 ) (5.0 )

Cash inflow before net financing and other outflows 4.2 8.3 4.9

Loan principal / net interest (5.8 ) (0.6 ) (0.7 )

Dividend paid (2.2 ) (2.4 ) (3.0 )

Purchase of shares for Treasury (net) - (1.0 ) (1.2 )

Non-recurring operating costs (2) (2.5 ) (2.0 ) (0.6 )

Cash generated (utilised) (6.3 ) 2.3 (0.6 ) )

Closing net cash 6.6 6.6 5.3

(1) Excludes non-recurring items and derivative financial instruments which are presented separately

(2) FY14 non-recurring costs comprise fess incurred on the acquisition of Portalify and subsequent restructuring costs;

FY13 non-recurring costs comprise fess incurred on the acquisition of 3T and subsequent restructuring costs; and

FY12 non-recurring costs comprise redundancy costs and settlement of financial derivatives

Cash flow summary Strong cash flows fund growth and acquisition

24

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

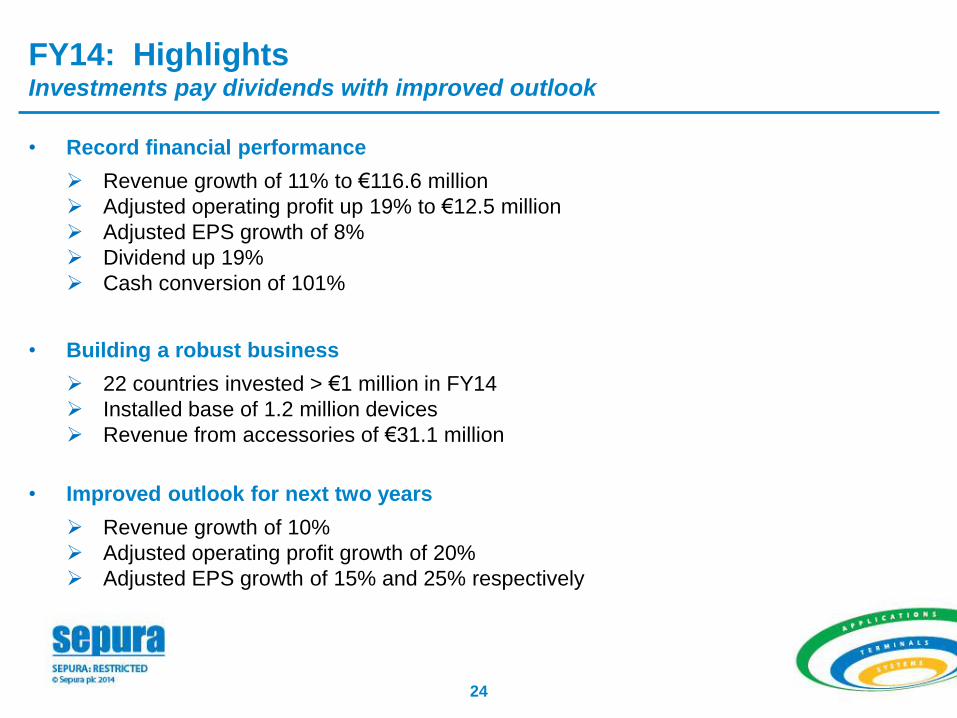

• Record financial performance

Revenue growth of 11% to €116.6 million

Adjusted operating profit up 19% to €12.5 million

Adjusted EPS growth of 8%

Dividend up 19%

Cash conversion of 101%

• Building a robust business

22 countries invested > €1 million in FY14

Installed base of 1.2 million devices

Revenue from accessories of €31.1 million

• Improved outlook for next two years

Revenue growth of 10%

Adjusted operating profit growth of 20%

Adjusted EPS growth of 15% and 25% respectively

FY14: Highlights Investments pay dividends with improved outlook

25

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

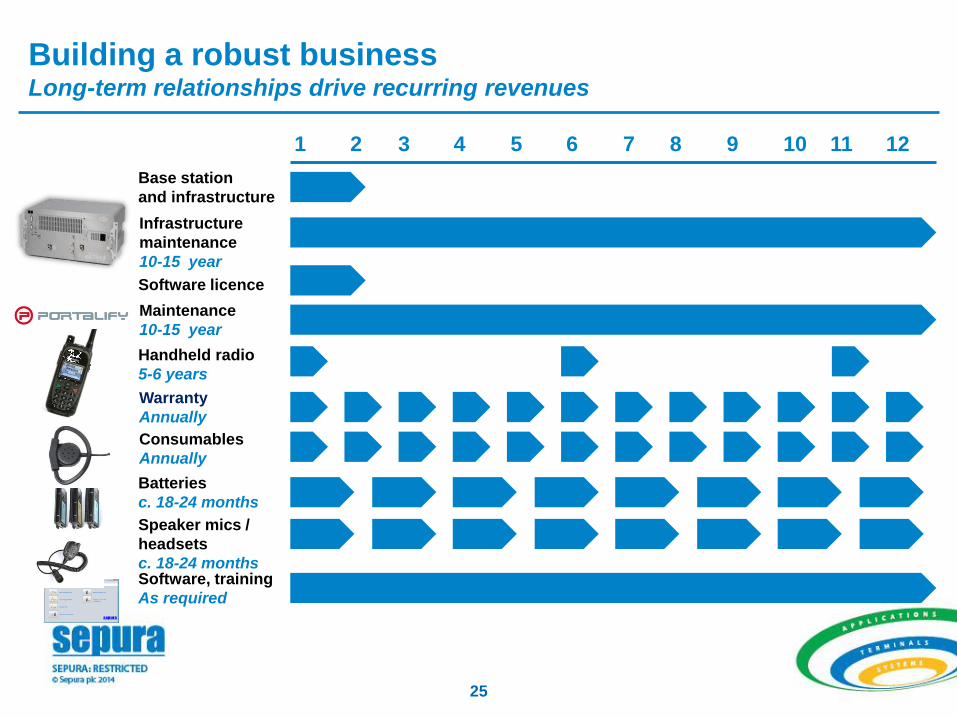

Building a robust business Long-term relationships drive recurring revenues

1 2 3 4 5 6 7 8 9 10 11 12

Base station

and infrastructure

Infrastructure

maintenance

10-15 year

Software, training

As required

Warranty

Annually

Batteries

c. 18-24 months

Speaker mics /

headsets

c. 18-24 months

Handheld radio

5-6 years

Consumables

Annually

Maintenance

10-15 year

Software licence

26

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

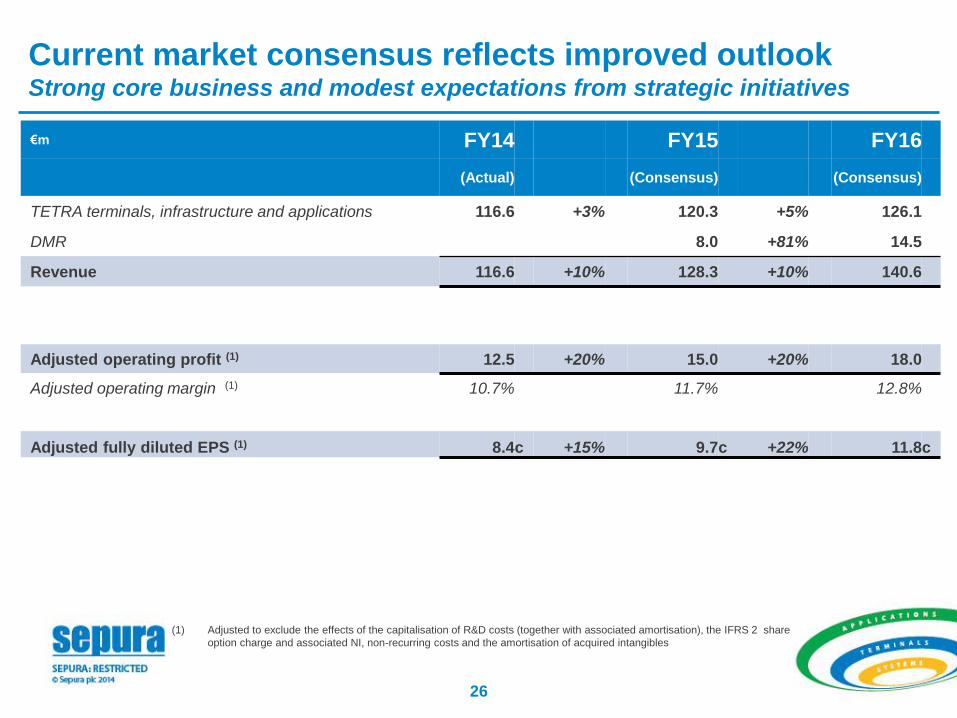

€m FY14 FY15 FY16

(Actual) (Consensus) (Consensus)

TETRA terminals, infrastructure and applications 116.6 +3% 120.3 +5% 126.1

DMR 8.0 +81% 14.5

Revenue 116.6 +10% 128.3 +10% 140.6

Adjusted operating profit (1) 12.5 +20% 15.0 +20% 18.0

Adjusted operating margin (1) 10.7% 11.7% 12.8%

Adjusted fully diluted EPS (1) 8.4 c +15% 9.7 c +22% 11.8 c

(1) Adjusted to exclude the effects of the capitalisation of R&D costs (together with associated amortisation), the IFRS 2 share

option charge and associated NI, non-recurring costs and the amortisation of acquired intangibles

Current market consensus reflects improved outlook Strong core business and modest expectations from strategic initiatives

27

1. The PMR market

2. Sepura’s position in the market

3. The opportunity

4. Financials

5. Conclusion

6. Q&A

27

0

104

180

63

144

198

142

193

227

151

169

191

190

220

239

190

220

239

192

192

192

237

186

30

0

71

156

0

178

89

0

130

200

253

187

48

Apps

Terminals

Systems

28

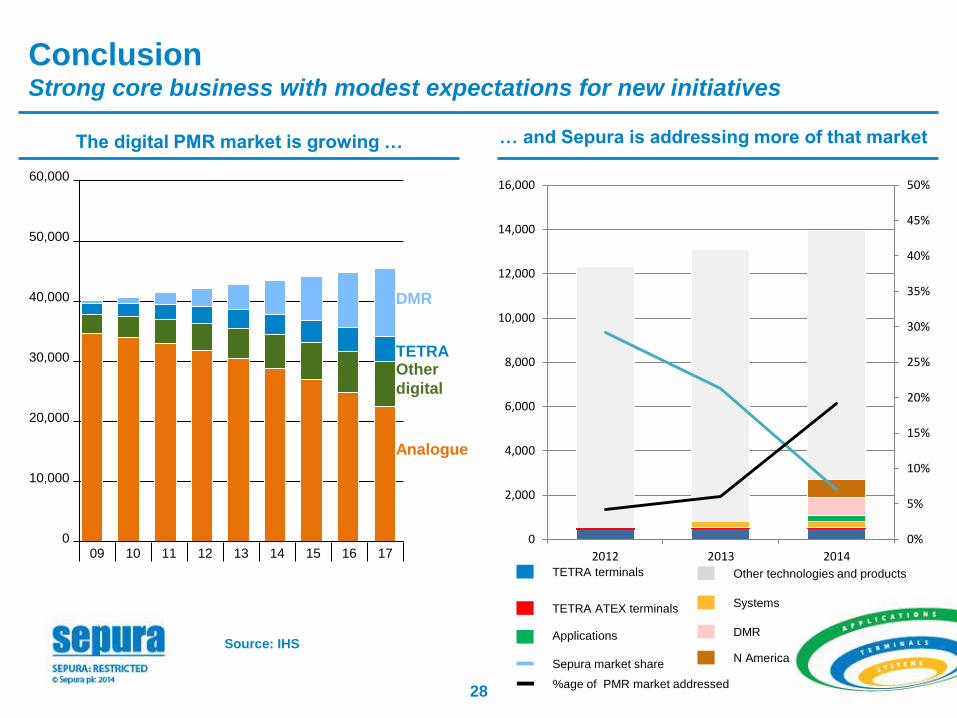

The digital PMR market is growing …

Conclusion Strong core business with modest expectations for new initiatives

… and Sepura is addressing more of that market

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2012 2013 2014

DMR

TETRA terminals Other technologies and products

Applications

Sepura market share

Systems TETRA ATEX terminals

%age of PMR market addressed

N America

Analogue

60,000

50,000

40,000

30,000

20,000

10,000

0 09 10 11 12 13 14 15 16 17

Source: IHS

DMR

Other

digital

TETRA

29

1. The PMR market

2. Sepura’s position in the market

3. The opportunity

4. Financials

5. Conclusion

6. Q&A

29

Recommended

![Presentation made to Analyst / Investor Meeting [Company Update]](https://img.pdfslide.net/doc/110x75/577c7c291a28abe054998a1b/presentation-made-to-analyst-investor-meeting-company-update.jpg)

![Analyst / Investor Meeting / Interaction - Presentation [Company Update]](https://img.pdfslide.net/doc/110x75/577c7a9d1a28abe05495a56e/analyst-investor-meeting-interaction-presentation-company-update.jpg)