2015.3

Annual Results 2014

Disclaimer

The information contained in this presentation is intended solely for your own

reference only. In addition, information contained in this presentation includes

projections and forward-looking statements that reflect the Company’s current

views with respect to future events and financial performance. These views are

based on assumptions subject to various risks. No assurance can be given that

future events will occur, that projections will be achieved, or that the Company’s

assumptions are correct. Actual results may differ materially from those projected.

Past track record cannot be used as guidance for future performances.

2

2. Segments Review

3. Company Prospects

1. Results Overview

Volatile crude oil price

Barrel of oil costs rose

Regional demands varied

Subsequent increase in supply of large scale equipment

2014:Early Ready for Change

Increase flexibility and Be well-planned

Change in strategy from “building, acquiring, leasing and managing” to “leasing of higher priority”

Optimize financial structure, maintain sufficient cash

Disposal of non-core assets

Enhance competitiveness and efficiency with lower cost

Raise service standards

Enhance operational efficiency

Optimize technology processing

Broaden service fields

Unique advantages

Focus on competitive business and quality development, controlling the operating size.

4

Financial Performance1

RMB 2014 2013 ChangeRevenue (mn) 32,993.2 27,363.8 20.6%

Operating profit (mn) 8,425.9 7,648.3 10.2%

Operating margin 25.5% 28.0% 2.5pp

Net profit (mn) 7,520.2 6,726.4 11.8%

1. The above financial data are adapted from the Company’s audited financial reports prepared in accordance with HKFRS. 2. Impairment on fixed asset of RMB374 million is included in net income calculation.3. Cash available for use represents the sum of monetary funds as well as available-for-sale financial assets.

Very positive cash available3: RMB11.6 billion

Gearing ratio declines further: Debt to capital ratio 42.2%; net debt to equity ratio 43.0%

Rate of return increases: Return to capital employed: 12.2%

5

RMB 2014 2013 ChangeTotal asset (mn) 86,874.3 79,262.3 9.6%

Total debt (mn) 39,552.2 42,002.5 5.8%

Equity(mn) 47,322.1 37,259.8 27.0%

2014 Operating Results

6

2

3

1

Technology Outperformed Equipment

Revenue

9.8

2.7

6.954 7,062

20,889

23,460

2013 2014

47%

12%

Operating Profit

2%

9.8

694 1,364

9,533

2013

97%

20142013 2014 2013

6,475

20142013 2014

4044

Patents Increased

2012 2013 2014

Semi-subJack-up

27

8

30

10

33

11

Expand High-end

463

621

763

69%

31%

Domestic International2013 2014

24%

18,466

22,901

Domestic Revenue International Revenue

2013 2014

13%

8,89810,092

(in RMB million) (in RMB million)

(No. of drilling rigs)

(Equ

ipm

ent s

ecto

r)

(Tec

hnol

ogy

sect

or)

(in RMB million)

(Cum

ulat

ive

no. o

f pat

ents

)

2014 Operating Results

7

Numbers of rigs: received recognitions from

clients, including “Rig of the Month”

HYSY981: completed the deepwater operation in

South China sea 33 days ahead of schedule

Excellent equipment management: Downtime at

1.28 hours/rig/month, equipment integrity rate:

99.41%

Drilling:completed operations in advance with

high efficiency, saved 839 operation days for

clients

Marine support:total voyage increased by

13,000 sea miles which increased job difficulties.

Fuel consumption down by 4600 tons

(4.26%) y-o-y through a variety of optimizations

Well services:new technologies saved 5600

operation hours for clients

Efficiency & competitiveness further increased

Enhance efficiency with lower costs, offer value-added services

Further improve the four regional international businesses, built logistic bases in Singapore and Mexico;

Named the worldwide recognized supplier by Total S.A and Shell;

Steady growth in the Mexican market: New added COSLHunter and COSL7 commenced operation, received

recognition from customers because of excellent services.

Int’l Development

Regional and clients diversification

Regional distribution

美洲12%

41%Europe

18%

Middle East 19%S.E. Asia

14%The Americas

8%Others

Singapore base

8

R&DManufacturing

HRTraining

LogisticsSupply

0%

10%

20%

30%

0

2

4

6

8

10

12

2013 2014

Deepwater Capability

First time of joint operation in the South

Sea between HYSY720 and Shell

12-streamer Geophysical Service Fleet

HYSY721 was delivered and launched

GeophysicalSurveying

Deepwater AHTS vessels operated

steadily

Purchased 3 deepwater PSV and

commenced operation

Marine SupportDrilling

High efficient operated 3 Semis in the North Sea HYSY981 operated in Lingshui 17-

2, efficiency reached 98% Achieved breakthrough: IPM operations

in the South Sea

Well Services

Self-developed ELIS logging units

and high end logging units

equipment, deepwater drilling fluids

and cement slurries in terms of deep

water fields

9

Deepwater Revenue up 35%

Contribution up to 20%

18%

20%

RevenueRMB Billion

Proportion(%)

Note: Deepwater businesses above included: drilling rigs operating at water depths over 500 meters, 12-streamer survey vessels and deepwater surveying vessels, deepwater AHTS vessels and PSV, and deep water well services business.

Safety & Environmental Friendly

Excellent safety mgmt ensured operation quality and efficiency

No major incidents during the period, effectively controlled significant risks

Further improve safety mgmt system, strengthening the safety management foundation

Emphasis on energy saving, exceededenergy-saving targets for the year

Achieved energy saving of 23,910 tons of standard coal, representing a significant increase of 74% on a yearly basis

Ice breaking operations

Participate in oilfield joint drills

10

0.45

0.220.270.290.32

0.250.260.23 0.2 0.190.24

0.18

0.08

0

0.1

0.2

0.3

0.4

0.5

02 03 04 05 06 07 08 09 10 11 12 13 14

OSHA Index*

*According to OSHA, coefficient 1 is equivalent to one accident per 200,00 man-hours

First company in China and the

fourth in the world with these

two technologies

Completed land drills, sea drills

and the offshore joint

operations for the first time

ELIS® image logging unit

Completed in tackling key technical problems such as 3D sound waves, 2D nuclear magnetic resonance, laterlogarray and oil-base mud drilling imaging

Overall standard up to international advanced level

Research & Development

11

Application of the R&D results above demonstrated COSL has the ability to meet customer demands for high value-added technologies and provide know-how solutions.

Deepwater drilling fluids and cementing technology

Breakthroughs in on-site

application with operational

experience depth to 1,500m

Able to offer 2,500m depth of

deepwater drilling fluids and

cementing technology

Welleader ® and Drilog ®

Recognitions from Capital Markets

The project of H share private placement awarded“Best Annual Issuance Award” in Asia

“Top 100 China Main Board Listed Company by Value” of the year 2013

“No. 1 China Listed Company on Appraisal Value” and “No. 1 Advanced Company in Mining Industry”

Asia’s Most Honored CompanyBest Investor Relations Company in the Oil & Gas Sector

12

Included in the Hang Seng (China A) Corporate Sustainability Benchmark Index in 2013

2. Segments Review

3. Company Prospects

1. Results Overview

Performances of the Four Segments1

5,765

6,576

694

1,364

464 320726

166

14.1%

96.6%

31.1% 77.1%

2013

201414,655

17,389

6,475

9,533

3,2513,469

2,9732,602

18.6%

47.2%

6.7%12.5%

2013

2014

14

Geo& Surveying

7 seismic vessels

6 integrated

surveying vessels

2 OBC teams

Drilling

33 Jack-ups

11 Semis

2 accom rigs

5 module rigs

Marine Support

72 self-owned

vessels

Managing 49

vessels

Well Services

Logging, drilling fluids, directional drilling, cementing, completion, workover, output boost, etc.

1. As of 31 December 2014 2. Operating profit from marine support includes the impairment loss of RMB151 million

Revenue Operating Profit

RMB million RMB million

Drilling Well Services Marine Support

Geophysical &Surveying

Drilling Well Services Marine Support2

Geophysical &Surveying

2013 2014

17.018.0

91.8%

95.6%

2013

92.1%

3Q14 2014

Drilling & Well Services

Expanded fleet; More high-spec rigs; Higher daily income; More days spent on repairing and oil price drop lead to decreased utilization rate

NH9 and COSLPromoter made full year contribution in 2014

COSLGift and COSLHunter, the high-end jack-ups, were purchased in 2013 and launched in January and April respectively

Efficient leased HYSY932, Gulf Driller I and Kaixuanyihao commenced operation in April, May and July respectively

in USD ’0000/day

Calendar-day Utilization Rate

Average Daily Income

Driven by the drilling synergistic effects Various rigs such as NH9, HYSY932, Gulf Driller I and Kaixuanyihao newly operated in

domestic offshore, driving operation growth of logging, directional drilling, cementing and drilling fluids.

Enhanced technology competitiveness, highly difficult wells, complicated wells and deep-water wells increased

Overall breakthroughs were made with self-developed ELIS logging units and high end logging units equipment, applications of new materials and technologies including deep-water drilling fluids and cement slurries in terms of deep water fields

Oilfield technology equipment and staff operated at full capacity

15

Marine Support & Geo Surveying

Purchased 3 vessels; 2 vessels commenced operations in 2H13 Calendar-day utilization rate maintained stable at 93.6% Chartered vessels achieved 17,183 operating days, up 2,887 days y-o-y with revenue

aggregated RMB1.36 billion Disposal chemical carriers (non-core) business

Reasonable allocation of resources, enhance competitiveness and leading position

16

2D

2014

2013

1H Workload 2H Workload

14,854

12,215

11,122

8,976

Oil price drops led to a decrease in workload and price, sector performance was directly affected. Tried to improve efficiency and reduce production costs

Safety and quality service, stable market demand

2013 14,011 9,645

12,9334,0342014

Data Collection (km) Data Processing (km)

3D

2014

2013 12,899

17,085

11,776

7,121

2013 16,965

6,4712014 11,305

7,432

Data Collection (km2) Data Processing (km2)

1H Workload 2H Workload

2. Segments Review

3. Company Prospects

1. Results Overview

Current Industry Circumstances

Stepping into 2015, international oil price volatiles at USD50/barrel, investment and demand of oil companies significantly reduced.

Further intensified competition in global oilfield service market, prices and utilization rates of various kinds of services have dropped in different extents.

1

2

3

5

18

COSL also faces challenges of the industry; Relying on good fundamentals, COSL will actively seize the industry integration

opportunity and strive to obtain new development.

Global utilization rate of jack-ups fell to 80%, semis fell to 84% 1;

Global utilization rate of seismic vessels was low;

Price cuts, layoffs, discontinuation of business units occurred in the industry.

1. Source: IHS Petrodata, as of February 2015

In medium to long term, oil and gas remains an important component in overall energy consumption structure.

3

Leverage Comparative Advantages

19

Flexibly adjust the business model

Continue to work closely with long term strategic partners

15%

20%

25%

30%

2011 2012 2013 2014 2015P

Continuous optimization of rig fleet structure

Growing contribution fromthe well service segment

34%

50%

16%

Over 25 yrsNo depreciation

(JUs+Semis)

Other semis(high spec /newly

built)

Other Jack-ups(high spec /newly

built)

Enhance flexibility with equipment and technology

EquipmentSegment

TechnologySegment

Continuous optimization ofequipment structure

Exceptional equipment operationefficiency

Unparalleled equipmentmanagement capability

Maintained industry-leading utilization rates

Self-developed Welleader®and Drilog® systems completed joint marine operation

ELIS achieved major technological breakthrough

CoreClients

Integration

Synergies

&

Cost

Advantage

Healthy financial structure provides higher flexibility

COSL's liquidity is very strong… The company also has abundant undrawn credit facilities from domestic and overseas banks and good access tothe debt and equity capital markets.

20

“……low cash cost and and goodliquidity help Asian oil companies tomanage themselves against low oilprices ……”

1. Cash available for use represents the sum of money market funds as well as available-for-sale financial assets. Financial data as of end of 2014

Leverage Comparative Advantages

Very positive cash available for use1:RMB11.6 billion

Further improved gearing: debt-to-assets ratio: 42.2%

Net debt-to-equity ratio: 43.0%

Debt cost: 2.1%, much lower than industry average

Source: Bloomberg, as of 23 Mar 2015

Moody’s S&P Fitch

Schlumberger Aa3 (stable) AA- (stable) -

Halliburton A2 (stable) A (under negativewatch list) -

Baker Hughes A2 (stable) A (under negativewatch list) -

COSL A3 (stable) A- (stable) A (stable)

Diamond A3 (stable) A- (neg) -

Ensco Baa1 (stable) BBB+ (stable) -

Oceaneering Intl Baa2 (stable) BBB (stable)

Noble - BBB (stable) Not rated

Weatherford Baa3 (stable) - -

Rowan Rating withdrawn BBB- (stable)

Atwood Oceanics Ba2 (stable) BB (stable)

CGG SA Rating withdrawn B (neg)

Hercules Offshore Caa2 (neg) CCC (neg)

Rig Operation Status in 2015

Location Drilling Rig2015

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Domestic

20 Jack-ups1

(contract terms until end-2015)2 Semi-submersibles

(contract terms until end-2015)

COSLProspector*

HYSY941*

COSLGift*

NH8*/NH9*

NH5*

NH7*

International

6 Jack-ups2

(contract terms until end-2015)3 Semi-submersibles3

(contract terms until end-2015)COSLPower

HYSY937 卡塔尔

COSLSeeker

COSLSuperior*/COSLBoss*

NH6*

21

Note: Data above as of 30 March 2015 and may subject to change; rigs under maintenance are not shown;Jack-ups are marked in blue and semis are marked in green. * Changes of rig contracts occurred during the period of early February till now.1.It is planned to surrender the rental of KT2 after the completion of the short-term operations contract.2.COSLHunter is serving a contract while a subsequent contract is pending confirmation.3.COSLPioneer has suspended its operation and it is expected to resume operation in August.

Australia Under Maintenancein China

Maintenance.

IND

IND

New Delivered

Qatar/S.E. Asia

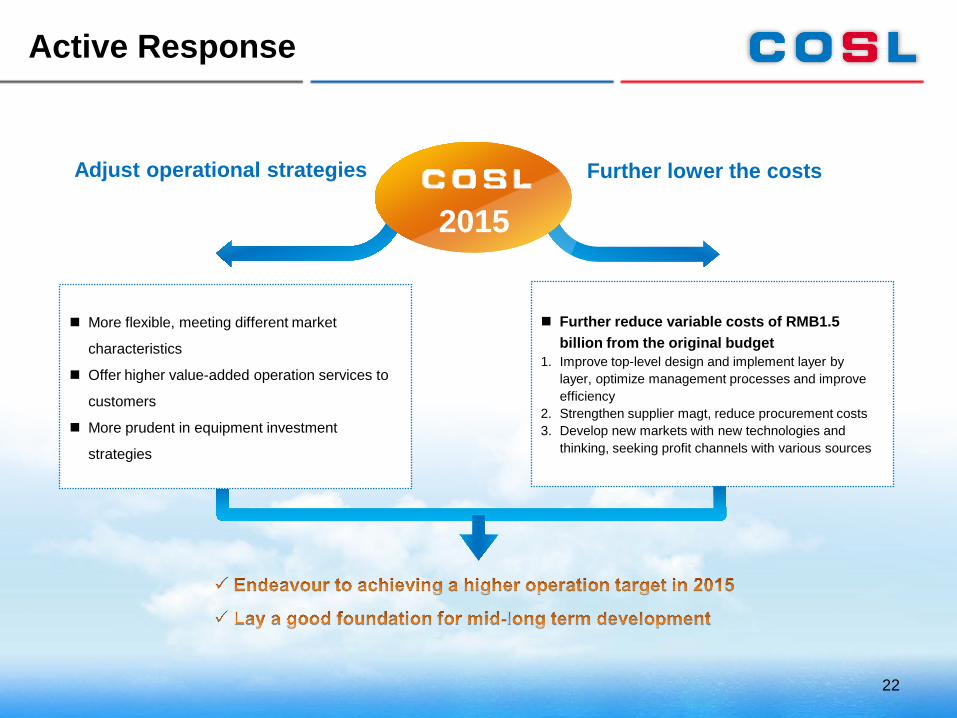

Active Response

2015Adjust operational strategies

More flexible, meeting different market

characteristics

Offer higher value-added operation services to

customers

More prudent in equipment investment

strategies

Further reduce variable costs of RMB1.5 billion from the original budget

1. Improve top-level design and implement layer by layer, optimize management processes and improve efficiency

2. Strengthen supplier magt, reduce procurement costs3. Develop new markets with new technologies and

thinking, seeking profit channels with various sources

Further lower the costs

22

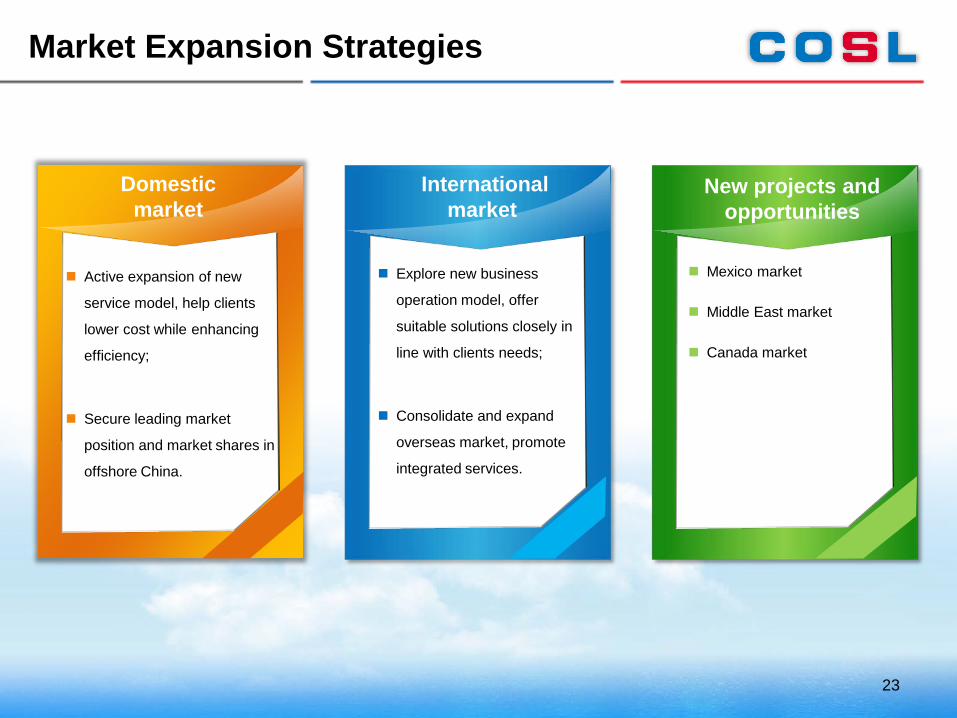

Market Expansion Strategies

Domesticmarket

Active expansion of new

service model, help clients

lower cost while enhancing

efficiency;

Secure leading market

position and market shares in

offshore China.

International market

Explore new business

operation model, offer

suitable solutions closely in

line with clients needs;

Consolidate and expand

overseas market, promote

integrated services.

New projects and opportunities

Mexico market

Middle East market

Canada market

23

CAPEX Plan

24

Drilling(~45%) Well service(~15%)

Marine support(~20%) Geophysical(~20%)

Prudent Capex principle; Continue to implement the projects under construction, selectively upgrade or retire equipment; Increase investment in self-developed high-end technology to enhance competitiveness; Lay a good foundation for mid-long term development.

2015 total6.5-7.5 bn

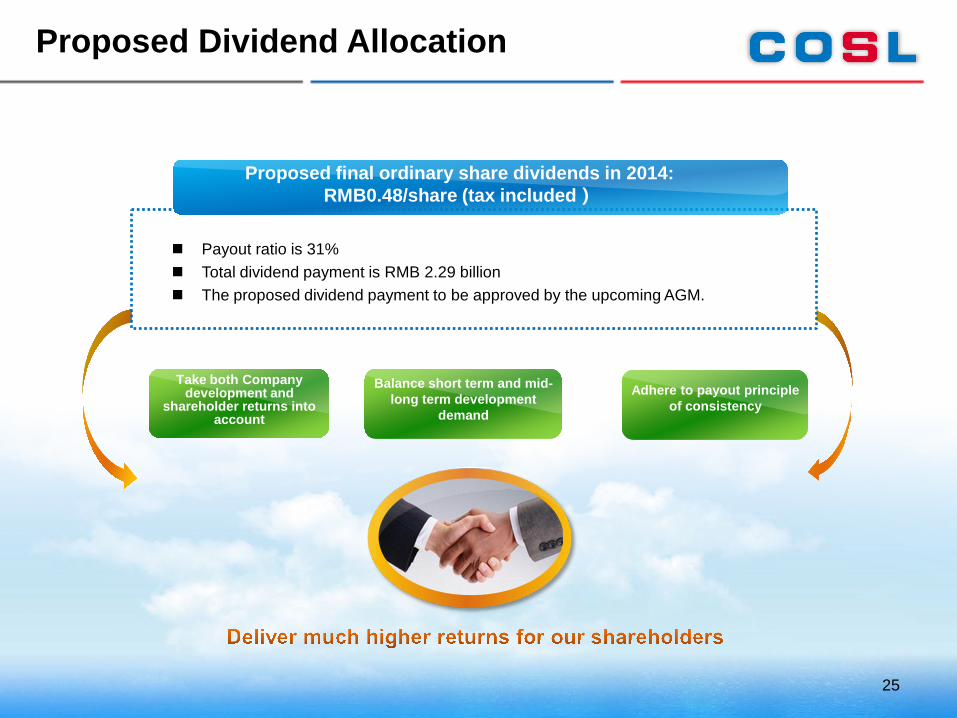

Proposed Dividend Allocation

Adhere to payout principle of consistency

Payout ratio is 31% Total dividend payment is RMB 2.29 billion The proposed dividend payment to be approved by the upcoming AGM.

Proposed final ordinary share dividends in 2014:RMB0.48/share (tax included)

25

Take both Company development and

shareholder returns into account

Balance short term and mid-long term development

demand

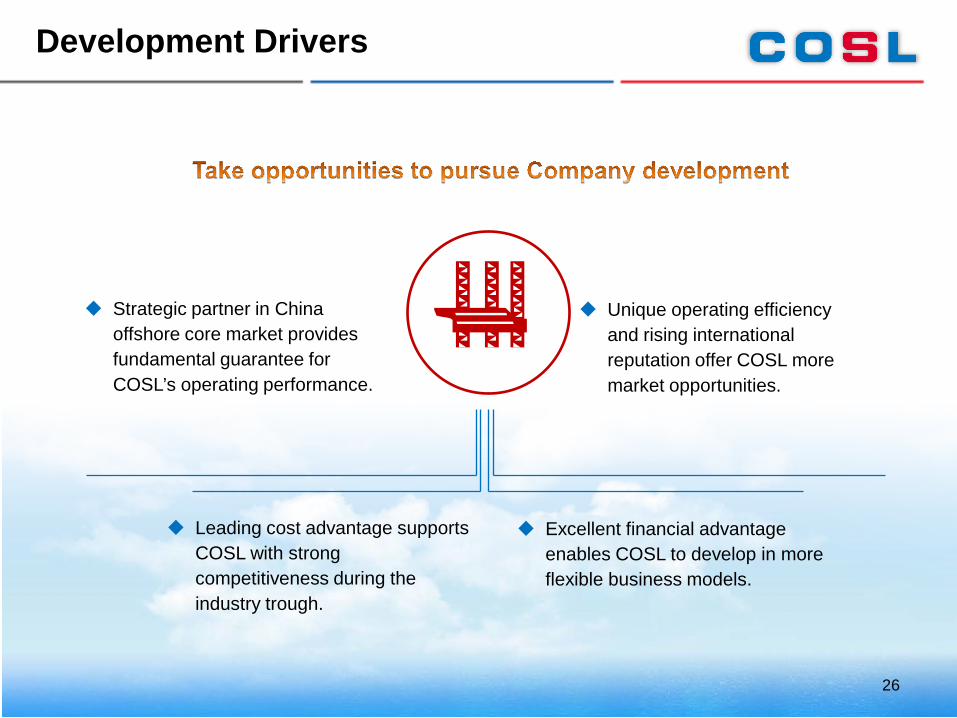

Development Drivers

Strategic partner in China offshore core market provides fundamental guarantee for COSL’s operating performance.

Unique operating efficiency and rising international reputation offer COSL more market opportunities.

Leading cost advantage supports COSL with strong competitiveness during the industry trough.

Excellent financial advantage enables COSL to develop in more flexible business models.

26

Recommended