1

October 26th, 2011

Appraisal 101

The Art and Science of Property Valuation

2

WHY DO WE NEED APPRAISALS?

2

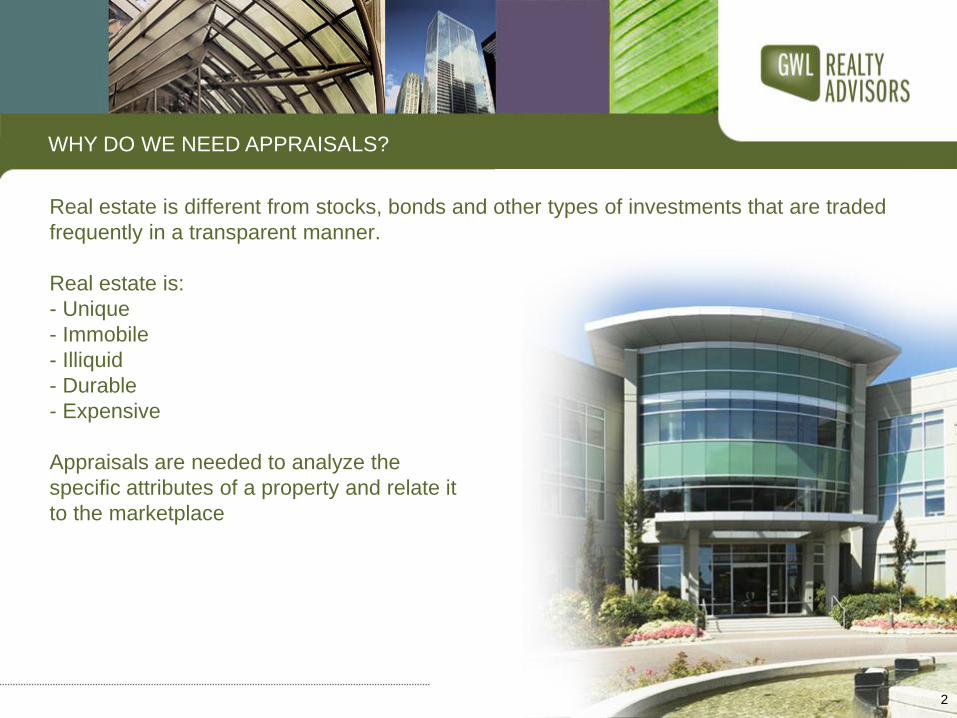

Real estate is different from stocks, bonds and other types of investments that are traded

frequently in a transparent manner.

Real estate is:

- Unique

- Immobile

- Illiquid

- Durable

- Expensive

Appraisals are needed to analyze the

specific attributes of a property and relate it

to the marketplace

3

Owners (Financial Institutions, Pension Funds, Public Companies, REITS, Private

Investors):

- Assets marked-to-market on a monthly, quarterly, annual basis

- Accounting (IFRS) requirements

- Litigation

Real Estate Advisors:

- Acquisition and disposition analysis/ due diligence

Developers:

- Highest and best use analysis

- Feasibility analysis

- Construction financing requirements

Lenders:

- Mortgage financing

WHO USES APPRAISALS?

3

4

Government:

- Land expropriations

- Property assessment appeals

Tenants:

- Rental arbitrations

WHO USES APPRAISALS? (CONT)

4

5

WHO DOES APPRAISALS?

5

An appraiser is a real estate professional who provides an opinion of value of various types of

properties, and is typically accredited with the Appraisal Institute of Canada:

- AACI for commercial properties

- CRA for residential properties

May be a Fee or Non-Fee Appraiser

- Charges a fee based on the type or complexity of the property and purpose of the appraisal

assignment

- Non-Fee Appraisers may also undertake valuation work while working for insurance

companies, assessment authorities, banks, etc.

Requirements for AACI accreditation:

- University Degree or UBC Post Grad Certificate in Real Property Valuation

- Practical work experience

- Is insured through AIC

- Not in breach of the AIC appraisal standards (CUSPAP) and Code of Ethics

6

WHAT IS AN APPRAISAL?

6

Supportable or defensible estimate or opinion of value

An impartial, expert and reasoned conclusion based

on an analysis of all relevant evidence in the market and

presented in the report

It represents the appraiser’s perception of the most

likely and most probable dollar value of the appraised

interest(s), subject to the qualifying conditions imposed

7

KEY ELEMENTS OF AN APPRAISAL:

7

An appraisal must:

- Identify the client and other intended users, by name

- Identify the intended use of the report (Purpose)

- Identify the subject property by address and legal description

- Provide a definition of market value

- Identify the type of report: current, retrospective, prospective or update

- Provide a date of valuation

- Identify all assumptions and limiting conditions, and hypothetical conditions (if any)

Examples:

- the existing use is a legally conforming use

- legal title is free and clear of financial encumbrances

- building areas and site areas are correct

- soil conditions and building improvements are structurally sound

- no environmental contamination

8

KEY ELEMENTS OF AN APPRAISAL:

8

An appraisal must (cont):

- Identify the nature of the interest being appraised; Leased Fee, Fee Simple or Leasehold

- Provide a physical description of the subject property and surrounding neighbourhood. Note

the date of inspection

- Provide an analysis of Highest and Best Use

9 9

DEFINITION OF MARKET VALUE:

The most probably price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby: 1. The buyer and seller are typically motivated; 2. Both parties are well informed or well advised, and acting in what they consider their best interests; 3. A reasonable time is allowed for exposure in the open market; 4. Payment is made in terms of cash in Canadian dollars or in terms of financial arrangements comparable thereto; and 5. The price represents the normal consideration for the property sold, unaffected by special or creative financing or sales concessions granted by anyone associated with the sale.

10 10

The foundation for all valuations, the definition of

Highest and Best Use is:

“The reasonably probable and legal use of vacant land

or an improved property, which is physically possible,

appropriately supported, financially feasible, and that

results in the highest value”

Appraisers need to determine the Highest and Best Use

“HABU” of the property as “improved” as well “as if

vacant”. The reason for this is that the existing use

may not represent HABU.

HIGHEST AND BEST USE (“HABU”):

11

HIGHEST AND BEST USE (“HABU”) (CONT):

11

Legal Permissibility

- Land is subject to Provincial regulations, Municipal planning and zoning constraints

- Encumbrances on Title: restrictive covenants, rights of way, environmental covenants,

leases, easements, heritage designation

Physical Possibility

- Land is constrained by its physical attributes: size and shape, accessibility, topography,

soil conditions, available services, environmental considerations

Financial Feasibility

- The HABU must be economically feasible within the context of the existing marketplace

(unless there is a hypothetical condition identified in the report)

Maximum Profitability

- More than one option can be economically feasible. An appraiser should determine

which is the most profitable.

12

HIGHEST AND BEST USE (“HABU”) (CONT):

12

Issues/ Examples:

Zoning may allow for development of an office building but the project may not be

financially feasible at this time. HABU may be as a holding property.

Multi-family development versus office development

in downtown Vancouver

13

THE THREE APPROACHES TO VALUE:

13

1. Income Approach

2. Direct Comparison Approach

3. Cost Approach

The approach used is dictated by the market, not

by the appraiser

Usually required to undertake at lease two of

the three approaches

14

INCOME APPROACH TO VALUE:

14

Based on the assumption that a purchaser of income-producing real estate uses the

current and future income generating potential as a measure of value

The value of a property is related to the present worth of the

future income stream that it is capable of producing

Two methods under the Income Approach:

1. Direct Capitalization Approach

2. Discounted Cash Flow Approach

Investors typically will use both approaches,

applying a different weight to each method

based on the particular characteristics of the

investment

15

DIRECT CAPITALIZATION APPROACH TO VALUE:

15

Direct Capitalization Approach takes a single year of income and converts that income

into a value expectation

Typically used on properties that are stabilized (i.e. essentially fully leased and at market

rents)

Adjustments can be made for lease-up and over/ under market rent but determining

stabilized NOI can be somewhat subjective

The more adjustments required, the less reliable

the results

Direct Capitalization is also typically used for

smaller, non-institutional grade properties

16 16

OCR Approach to Value

Year 1

Year 1 Fully Leased Base Rental Revenue $3,617,568

Plus: Year 1 Retail Sales Percent Revenue $10,508

Plus: Year 1 Recovery Revenue $1,847,271

Total Rent & Recovery Revenue $5,475,347

Plus: Other Income $0

Total Potential Gross Revenue (as if fully leased) $5,475,347

Less: General Vacancy & Credit Allowance 3.25% $177,949

Effective Gross Revenue (EGR) $5,297,398

Less: Total Operating Expenses including Property Taxes $1,860,363

Net Operating Income (as if fully leased) $3,437,035

OCR 7.00%

Estimate of Value (as if fully leased) $49,100,503

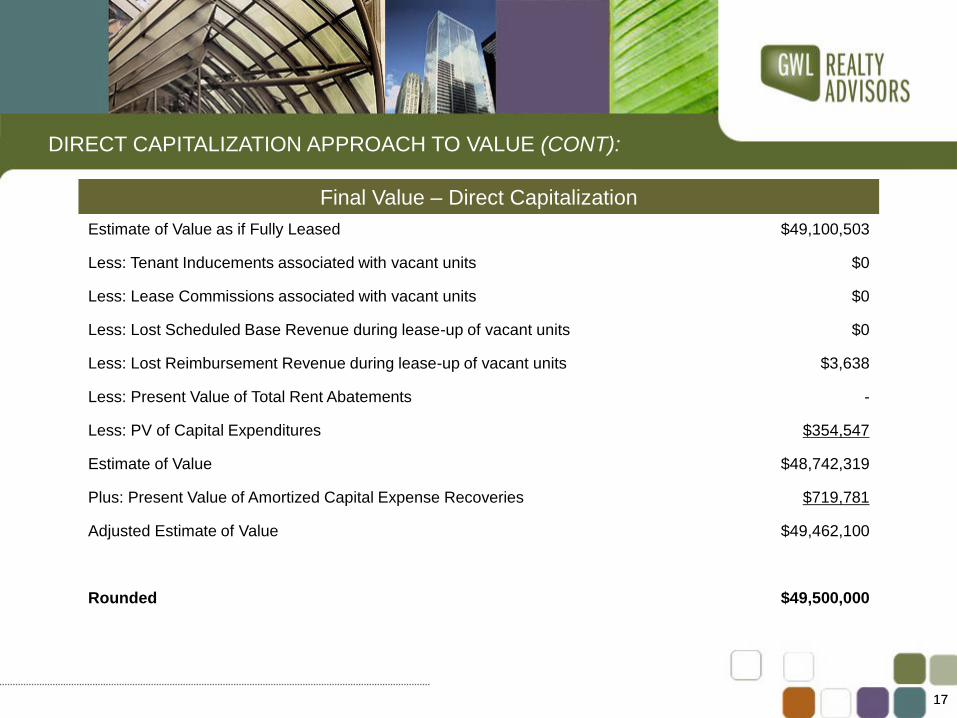

DIRECT CAPITALIZATION APPROACH TO VALUE (CONT):

17 17

Final Value – Direct Capitalization

Estimate of Value as if Fully Leased $49,100,503

Less: Tenant Inducements associated with vacant units $0

Less: Lease Commissions associated with vacant units $0

Less: Lost Scheduled Base Revenue during lease-up of vacant units $0

Less: Lost Reimbursement Revenue during lease-up of vacant units $3,638

Less: Present Value of Total Rent Abatements -

Less: PV of Capital Expenditures $354,547

Estimate of Value $48,742,319

Plus: Present Value of Amortized Capital Expense Recoveries $719,781

Adjusted Estimate of Value $49,462,100

Rounded $49,500,000

DIRECT CAPITALIZATION APPROACH TO VALUE (CONT):

18

DISCOUNTED CASH FLOW APPROACH TO VALUE:

18

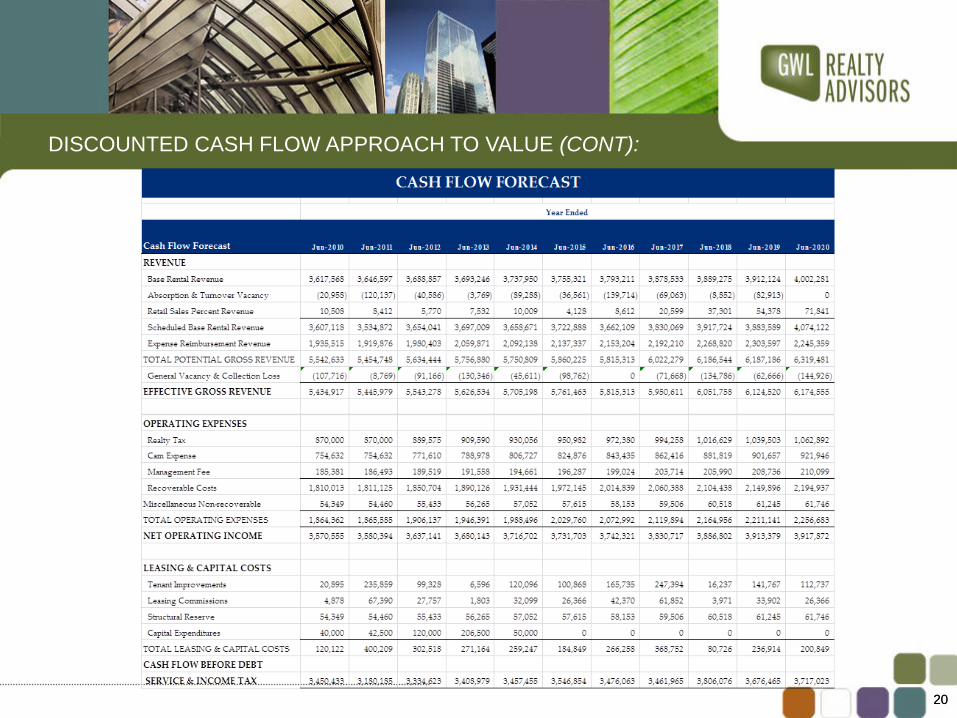

Converts a series of cash flows into a current-day expression of value The income to be generated is typically forecasted over a ten-year period, or the time span which allows the majority of leases in place to expire or “roll-over” at market Income is typically generated from two basic sources: 1. The cash flow received over the holding period; and 2. The future sale price (reversionary value) at the end of the holding period A discount rate (or internal rate of return – “IRR”) is applied to these earnings to find their present worth The reversionary value is established by capitalizing the estimated NOI at the end of the holding period by the Terminal Capitalization Rate (“TCR”) The Terminal Value is also discounted to present date utilizing the established Discount Rate Discounted Cash Flow is typically used on larger, more complex assets where the buyer profile is more sophisticated

19

DISCOUNTED CASH FLOW APPROACH TO VALUE (CONT):

19

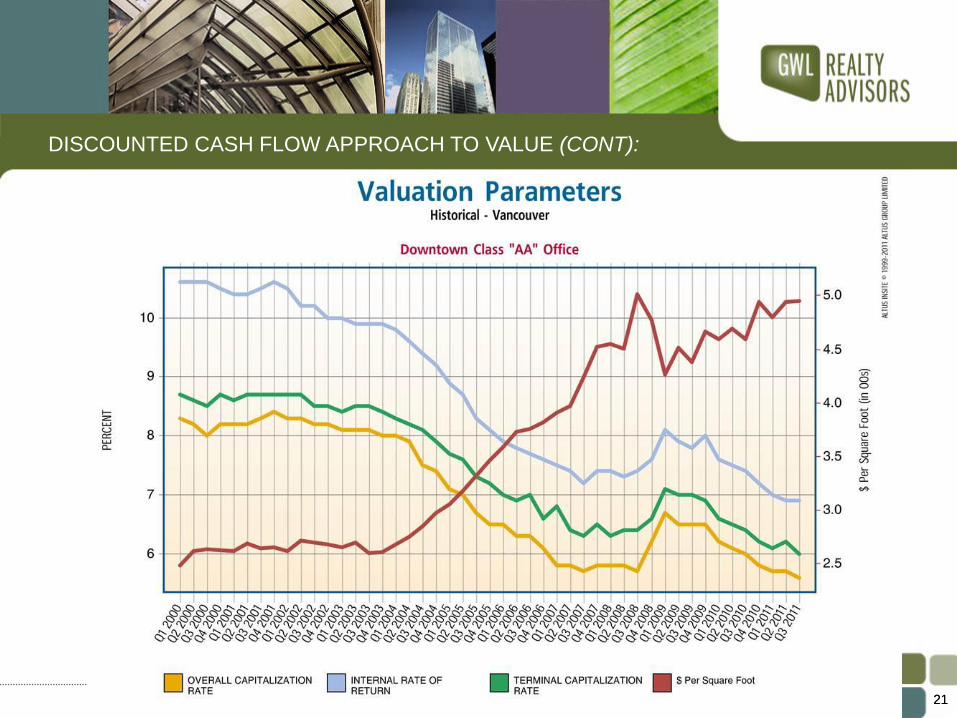

The following is a list of key variables used in a typical Argus model, sorted by three categories: 1. Those variables which one would expect to vary considerably from market to market (i.e. Vancouver vs. Montreal): Direct Cap Rate and TCR Discount Rate (i.e. IRR) Market face rents 2. Variables which one would expect only minor variations from market to market: Inflation rates Lag vacancy (i.e. down time) during investment horizon General vacancy during investment horizon Tenant Improvement Allowances Leasing commissions 3. Variables which one would “usually” expect to remain fixed from market to market. Credit loss Structural allowance Renewal term (number of years) Retention ratio Investment horizon

20

DISCOUNTED CASH FLOW APPROACH TO VALUE (CONT):

20

21

DISCOUNTED CASH FLOW APPROACH TO VALUE (CONT):

21

22

DISCOUNTED CASH FLOW APPROACH TO VALUE (CONT):

22

23

DISCOUNTED CASH FLOW APPROACH TO VALUE (CONT):

23

24

DISCOUNTED CASH FLOW APPROACH TO VALUE (CONT):

24

25

DIRECT COMPARISON APPROACH TO VALUE:

25

The Direct Comparison Approach is based on the principal of substitution that maintains that a willing and prudent purchaser will not pay more for a property than the cost to acquire an equally desirable substitute property Probably the most relevant approach for land and vacant properties which are most likely to be acquired by a user “User” value often higher than “investor” value – investor has to assume the risks and costs of lease-up and maintaining occupancy For an income property, the Direct Comparison Approach is mostly used as a secondary approach or reasonability check (the “price per pound”) Sales adjustments process under the Direct Comparison Approach is subjective. Some factors to adjust for: - Time/ date of sale/ market conditions - Age and condition – physical characteristics - Size and class - Location - Tenant profile - NOI per sq. ft. - Financing (above or below market mortgage)

26

COST APPROACH TO VALUE:

26

The cost method of appraisal is based upon the principal of substitution: No purchaser would be willing to pay more for a property than the cost of a new replica property This proposition leads to a second conclusion which declares that the replacement cost of a new property sets the upper limit of market value The general formula is: MV = L+B-D Where: MV = the market value of the property L = the market value of the site, as if vacant, as of the date of valuation B = the cost (new) of the structural improvements at the date of valuation D = the accumulated depreciation for the improvements on the site The Cost Approach is considered to be the least reliable approach to establish market value This approach is most applicable for: - A new building with no depreciation - A unique property (church, mosque, legislative or historic building) - A subject property where there is no other comparable sales evidence

27

VALUE RECONCILIATION AND CONCLUSION:

27

An appraiser may use more than one approach

to estimate Market Value

If the conditions from each approach are different,

then the values must be reconciled

The appraiser will utilize their judgment and

experience to determine their final estimate of

Market Value

28

HOT TOPICS IN REAL ESTATE APPRAISAL:

28

Estimating value in a volatile market: economic uncertainty around the world has had

positive and negative impacts on Vancouver real estate

The low interest rate environment: will it continue? What happens to value if interest

rates rise?

Estimating value when there are no sale comparables (as in 2009)

Green Buildings: additional value?

Impact of new developments on existing

office building values

Recommended